Embed Size (px)

Citation preview

Medium�Term�Strategy2016�to�2020

Ishmael Yamson & Associates

“inspiring and unleashing greater

prospects”

i | P a g e

S t u d e n t s L o a n T r u s t F u n d

1 Contents1 EXECUTIVE SUMMARY ................................................................................................................... iii

1.1 Student Assistance for Ter�ary Educa�on ............................................................................. iii

1.2 Ter�ary Educa�on .................................................................................................................. iii

1.3 The SLTF - Emerging Trends and Aspira�ons ......................................................................... iii

1.4 The Strategic Framework ....................................................................................................... iv

1.5 The Strategic Impera�ves ...................................................................................................... iv

1.6 The Culture ............................................................................................................................. iv

1.7 The Strategic Outcomes .......................................................................................................... v

1.8 Transla�ng the Strategy into Ac�on ....................................................................................... 5

1.9 Monitoring and Evalua�on ..................................................................................................... 5

2 CHAPTER ONE – Developing the Student Loan Trust Fund Strategy .............................................. 1

2.1 Introduc�on ............................................................................................................................ 1

2.2 The Need for a Students Loan Trust Fund .............................................................................. 1

2.3 The Students Loan Trust Fund – the Mandate ....................................................................... 1

2.4 The SLTF Strategy in the Context of Global and Na�onal Development Plans ....................... 2

2.5 Developing the Students Loan Trust Fund Strategy ............................................................... 2

2.5.1 The Brief .......................................................................................................................... 2

2.5.2 The Purpose and Structure of the Strategy Document ................................................... 2

2.6 The Process and the Par�cipants ............................................................................................ 3

2.7 The Key Milestones ................................................................................................................. 4

3 CHAPTER TWO – Ghana’s Ter�ary Educa�on ................................................................................. 5

3.1 The Demand for Ter�ary Educa�on ........................................................................................ 5

3.2 The Structure of Ter�ary Educa�on ....................................................................................... 5

3.3 Funding Ter�ary Educa�on ..................................................................................................... 6

3.4 The Environmental Context of Ghana’s Ter�ary Educa�on ................................................... 7

3.4.1 The Economy ................................................................................................................... 7

3.4.2 The Social Environment .................................................................................................. 8

3.5 Some Emerging Issues and Opportuni�es .............................................................................. 8

3.5.1 Growing Number of Enrolment in Ter�ary Educa�on .................................................... 8

3.5.2 Increasing Sophis�ca�on and Demands from Ter�ary Students.................................... 9

3.5.3 Increasing and Diversified Needs and Expecta�ons. ...................................................... 9

3.5.4 Tougher Compe��on in the Student Loan Industry ....................................................... 9

3.5.5 Increasing demand on Resources and Capacity of Organisa�ons for Relevance ........... 9

3.5.6 Major Technology Changes ............................................................................................. 9

3.5.7 Increasing Risks of Non-recoveries of Loans ................................................................... 9

ii | P a g e

3.5.8 The Increasing Cost of Ter�ary Educa�on ...................................................................... 9

3.6 General Conclusions on Environment in which SLTF operates ............................................. 10

4 CHAPTER THREE – The Opera�ons of the Student Loan Trust Fund ............................................ 11

4.1 The Student Loan Trust Fund ................................................................................................ 11

4.2 The Governance Arrangements ............................................................................................ 11

4.3 Opera�ons and Ac�vi�es of the SLTF ................................................................................... 11

4.3.1 Loan Applica�on and Disbursement ............................................................................. 12

4.3.2 The Students Loan Management So�ware .................................................................. 12

4.3.3 Cost Efficiency and Opera�onal Effec�veness .............................................................. 12

4.4 Situa�onal Analysis (The challenges of the SLTF) ................................................................. 13

4.4.1 Capitalisa�on ................................................................................................................ 13

4.4.2 Collateral ....................................................................................................................... 13

4.4.3 Interest Subsidy ............................................................................................................. 13

4.4.4 Non-repayment ............................................................................................................. 14

4.4.5 Recovery ........................................................................................................................ 14

4.4.6 A�tude of Borrowers from the SLTF ............................................................................ 15

4.4.7 Percep�on of the SLTF .................................................................................................. 15

4.4.8 The Zones ...................................................................................................................... 15

4.5 Some Aspira�ons of the SLTF ................................................................................................ 15

4.6 Some Conclusions on SLTF Internal Scru�ny ........................................................................ 16

5 CHAPTER FOUR – The SLTF Strategic Framework ......................................................................... 17

5.1 Mission .................................................................................................................................. 17

5.2 Vision ..................................................................................................................................... 17

5.3 The Strategic Impera�ves ..................................................................................................... 17

5.4 The Enablers .......................................................................................................................... 18

5.5 The Strategic Outcomes ........................................................................................................ 18

6 CHAPTER FIVE – Transla�ng the Strategy into Ac�on .................................................................. 19

6.1 Transla�ng the Strategy into Ac�on ..................................................................................... 19

6.2 The Corporate Strategic Goals .............................................................................................. 19

6.3 The Key Ac�ons ..................................................................................................................... 20

6.4 Monitoring & Evalua�on ....................................................................................................... 21

iii | P a g e

1 EXECUTIVESUMMARY1.1 StudentAssistanceforTertiaryEducation Countries understand that higher education is a catalyst for economic development and growth. In view of this, Governments develop policies and frameworks within which they either directly provide assistance (including financial assistance) towards the education of their people or provide incentives for the private sector to play that role. In Ghana, many households are poor and in spite of the aspiration of parents and students to obtain tertiary education many are financially handicapped. The need for an intervention, no matter how small is a crucial one and cannot be underestimated. Successive Ghanaian governments have pursued various social interventions designed to support tertiary students financially through their education. The Student Loan Trust Fund (SLTF) is the current non-discriminatory intervention with a mandate to support eligible tertiary students. Its objectives are to: (i) “provide financial resources for the sound management of the Trust for the benefit of students” (ii) “help promote and facilitate the national ideals enshrined in Articles 28 and 38 of the 1992

Constitution” (iii) “administer and manage loans in a manner that ensures that eligible students in accredited institutions

have equal access to tertiary education”. The SLTF has been in operation since the 2006 and is the only fit-to-purpose loans provider for students. However, it is still relatively unknown to many eligible students, especially at the time when they decide on which tertiary institutions to apply for admission into. The SLTF must improve the awareness of potential beneficiaries before and during the application process as the best and most easily accessible financial assistance option for tertiary education. Its presence and operations in all the ten (10) regions needs to be more effective and efficient to increase the proportion of tertiary students covered by SLTF.

1.2 TertiaryEducationThere are over 400,000 students in 140 tertiary institutions in Ghana. Out of those SLTF operations and presence cover 117 institutions with enrolment of about 300,000 students. Less than 10% of these students access SLTF’s loans. The great opportunity is to increase awareness of SLTF and create tailored loan products that are accessible and relatively affordable. As more and more students seek tertiary education and the cost of education keeps going up, the market for student loans will grow. The number of tertiary students who have benefited from the SLTF has increased by almost 50% since 2006 and this is set to increase substantially over the next 5 years. With this increase in applications, the cash requirement to meet the demand will increase.

1.3 TheSLTF -EmergingTrendsandAspirationsA major challenge of the SLTF is that it is unable to provide adequately for the financial needs and requests from eligible tertiary students. The organisation needs to secure and maintain regular and adequate funding from a broad range of benefactors in order to support the widest possible profile of tertiary students on a sustainable basis. This can help maintain competitive interest rates as well. The sustainability of the operations of the SLTF will also depend on its ability to process loan applications, loan disbursements, and loan recoveries for those loans paid out to students. SLTF needs to be internally more effective and efficient in tracking these processes with an appropriate on-line IT system and real-time data. In addition, loan beneficiaries should have more education as part of the application process to change their “non-payment” attitudes and to ensure they understand their obligations in the loans transactions.

S t u d e n t s L o a n T r u s t F u n d

iv | P a g e

The consumers of tertiary education are becoming more sophisticated and demanding, just as their needs are increasingly diverse. This requires a diversification of the loan packages that SLTF offers to students in order to widen its coverage of students, courses of study and institutions and to remain relevant. The SLTF will continue to face competition from the emergence of Microfinance Institutions, Savings and Loans companies and the twenty-five (25) universal banks in Ghana, as alternate loan providers introducing innovative loan products designed specifically for students. The more affordable interest rates from SLTF, its focused operations on student loans and leadership in innovative and tailored services may provide a basis for competitive advantages over other operators. As the SLTF 2016 - 2020 strategy seeks to respond to the emerging consumer and industry trends, it also responds to the organisations’ ambitions to make the SLTF a household name and the first point-of-call for tertiary student financing. It also seeks to create a strong, independent, and sustainable Loan Fund that attracts and retains a large number of Benefactors who associate with the SLTF. The organisation aspires to be driven by a “business mind-set”, ran by a highly trained and developed work force that is empowered and motivated and who are operationally effective and cost efficient.

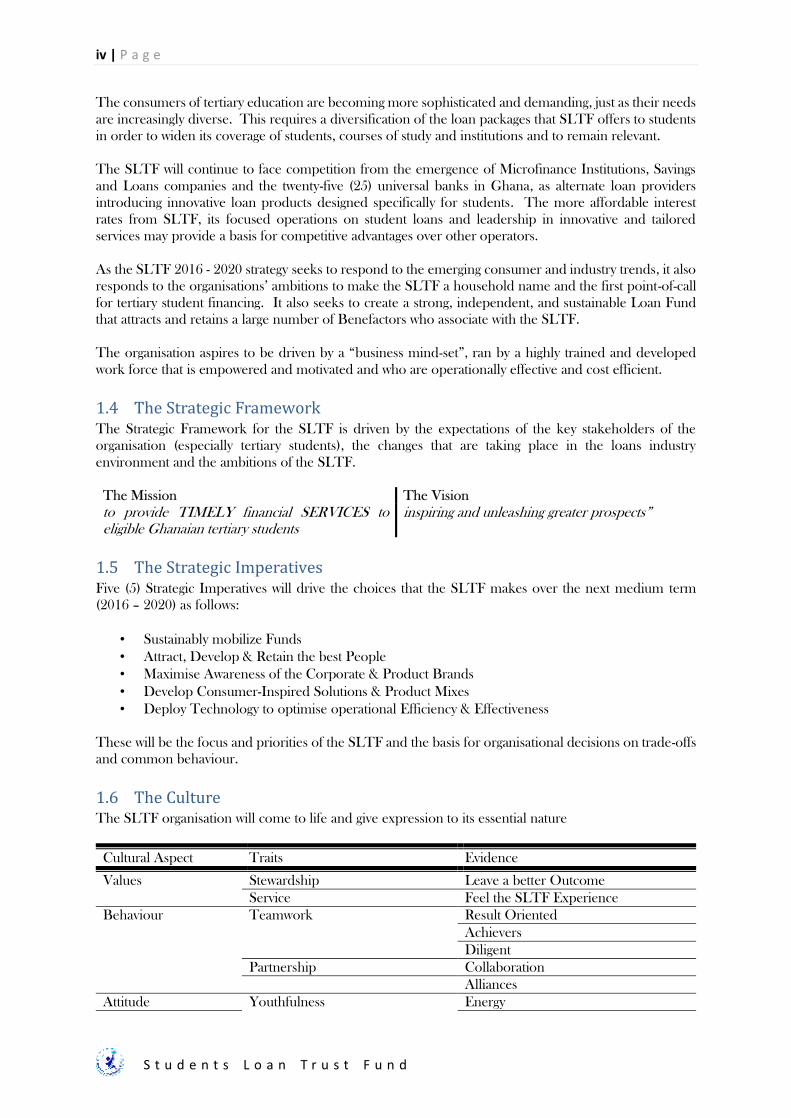

1.4 TheStrategicFrameworkThe Strategic Framework for the SLTF is driven by the expectations of the key stakeholders of the organisation (especially tertiary students), the changes that are taking place in the loans industry environment and the ambitions of the SLTF. The Mission The Vision to provide TIMELY financial SERVICES to eligible Ghanaian tertiary students

inspiring and unleashing greater prospects”

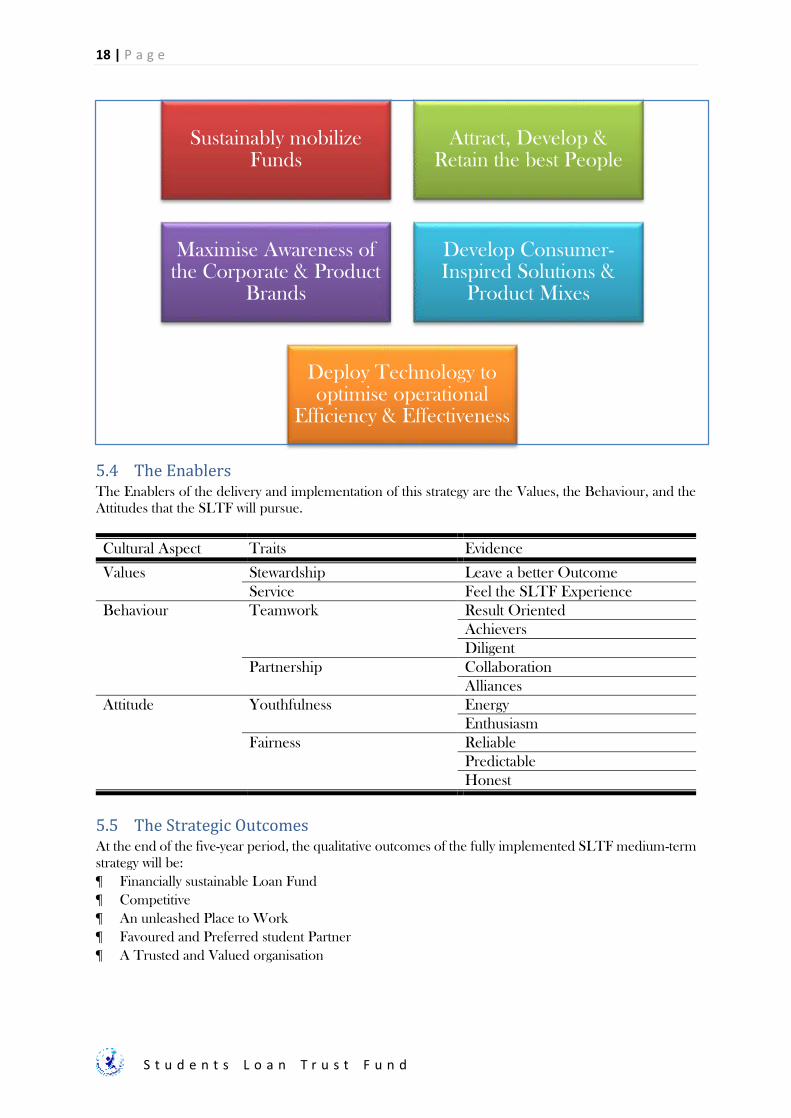

1.5 TheStrategicImperativesFive (5) Strategic Imperatives will drive the choices that the SLTF makes over the next medium term (2016 – 2020) as follows:

• Sustainably mobilize Funds • Attract, Develop & Retain the best People • Maximise Awareness of the Corporate & Product Brands • Develop Consumer-Inspired Solutions & Product Mixes • Deploy Technology to optimise operational Efficiency & Effectiveness

These will be the focus and priorities of the SLTF and the basis for organisational decisions on trade-offs and common behaviour.

1.6 TheCultureThe SLTF organisation will come to life and give expression to its essential nature

Cultural Aspect Traits Evidence

Values Stewardship Leave a better Outcome Service Feel the SLTF Experience

Behaviour Teamwork Result Oriented Achievers Diligent Partnership Collaboration Alliances

Attitude Youthfulness Energy

S t u d e n t s L o a n T r u s t F u n d

v | P a g e

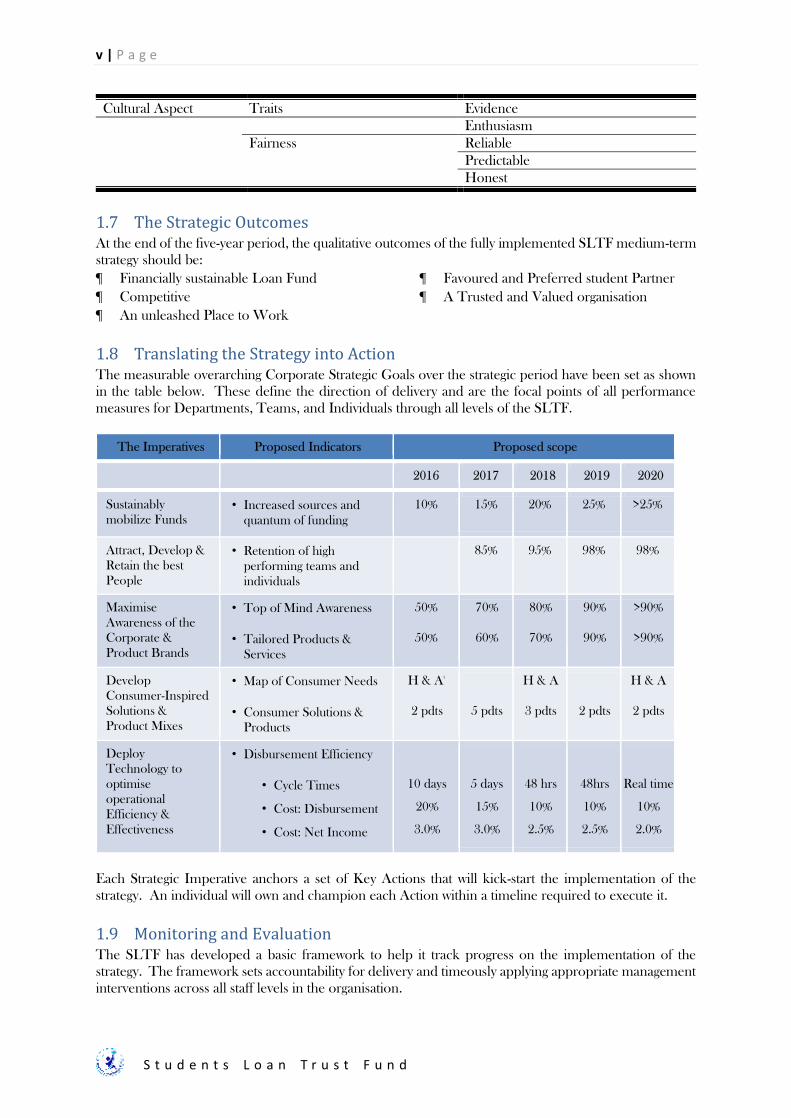

Cultural Aspect Traits Evidence Enthusiasm Fairness Reliable Predictable Honest

1.7 TheStrategicOutcomesAt the end of the five-year period, the qualitative outcomes of the fully implemented SLTF medium-term strategy should be:

· Financially sustainable Loan Fund

· Competitive

· An unleashed Place to Work

· Favoured and Preferred student Partner

· A Trusted and Valued organisation

1.8 TranslatingtheStrategyintoActionThe measurable overarching Corporate Strategic Goals over the strategic period have been set as shown in the table below. These define the direction of delivery and are the focal points of all performance measures for Departments, Teams, and Individuals through all levels of the SLTF.

The Imperatives Proposed Indicators Proposed scope

2016 2017 2018 2019 2020

Sustainably mobilize Funds

• Increased sources and quantum of funding

10% 15% 20% 25% >25%

Attract, Develop & Retain the best People

• Retention of high performing teams and individuals

85% 95% 98% 98%

Maximise Awareness of the Corporate & Product Brands

• Top of Mind Awareness

• Tailored Products & Services

50%

50%

70%

60%

80%

70%

90%

90%

>90%

>90%

Develop Consumer-Inspired Solutions & Product Mixes

• Map of Consumer Needs

• Consumer Solutions & Products

H & Ai

2 pdts

5 pdts

H & A

3 pdts

2 pdts

H & A

2 pdts

Deploy Technology to optimise operational Efficiency & Effectiveness

• Disbursement Efficiency

• Cycle Times

• Cost: Disbursement

• Cost: Net Income

10 days

20%

3.0%

5 days

15%

3.0%

48 hrs

10%

2.5%

48hrs

10%

2.5%

Real time

10%

2.0%

Each Strategic Imperative anchors a set of Key Actions that will kick-start the implementation of the strategy. An individual will own and champion each Action within a timeline required to execute it.

1.9 MonitoringandEvaluationThe SLTF has developed a basic framework to help it track progress on the implementation of the strategy. The framework sets accountability for delivery and timeously applying appropriate management interventions across all staff levels in the organisation.

S t u d e n t s L o a n T r u s t F u n d

1 | P a g e

2 CHAPTERONE–DevelopingtheStudentLoanTrustFundStrategy

2.1 IntroductionThe effort in Ghana to provide access to financial assistance to students for their tertiary education has evolved over the decades. Starting in the 70’s, students could access loans from commercial banks via a scheme designed to finance books and cover living expenses. That scheme collapsed because the high default rate made it commercially not viable to the participating banks. Subsequently, SSNIT launched a new scheme to provide education loans to tertiary students using funds it was managing on behalf of SSNIT Contributors. Contributors guaranteed these SSNIT student loans using their personal pension lump sum payments as collateral. This too met with challenges. The recovery rate was low and once again, the default level was high. Eventually, SSNIT discontinued its role as a loan provider and administrator to focus on its core mandate of managing pension funds. In August 2000, Government created the Ghana Education Trust Fund (GETFund) to oversee a fit-for-purpose national framework within which Ghanaian students could seek financial assistance for their tertiary education. The GETFund provides;

(i) nation-wide financing of education from basic to tertiary level, (ii) the management of the fund and (iii) makes provision for related matters.

The GETFund receives its funding from pre-agreed proportions of multiple sources of government revenue from taxes. As part of the national framework, Government established the Student Loan Trust Fund to administer and disburse loan requirements to tertiary students who need financial assistance with funds from the GETFund and other sources.

2.2 TheNeedforaStudentsLoanTrustFundMany of the people in Ghana’s large population of poor people require various interventions including the provision of financial assistance when they gain admission into tertiary institutions. The creation of SLTF builds a not-for-profit loans organisation that can continue to be sustainable and relevant for an increasing number of tertiary students who need financial assistance in a manner that is equitable and appropriate as a socially driven mechanism. Though the SLTF is not exclusionary in offering loans students who are eligible, the focus of its mission is on assisting needy and poor students.

2.3 TheStudentsLoanTrustFund–theMandateGovernment established the Students Loan Trust Fund (SLTF) in December 2005, under the Ghana Trustee Incorporation Act 1962, Act 820 to operationalise a social intervention that would help guarantee the fundamental rights of Ghanaians to access education at all levels. The mandates of the SLTF include; (iv) “to provide financial resources for the sound management of the Trust for the benefit of students” (v) “help promote and facilitate the national ideals enshrined in Articles 28 and 38 of the 1992

Constitution” (vi) “to administer and manage loans in a manner that ensures that eligible students in accredited

institutions have equal access to tertiary education”.

Higher education is a catalyst for economic development and growth

S t u d e n t s L o a n T r u s t F u n d

2 | P a g e

The initial source of funding for the SLTF included up to ten percent (10%) of all monies paid into the GETFund and an allocation from the Talk Tax. The SLTF also had the option to secure funding from other sources including but not limited to;

(i) money that may be allocated by Parliament for the Fund (ii) tax-deductible voluntary contributions from private and corporate benefactors, (iii) the mobilization of resources from Ghana’s international partners interested in the

advancement of tertiary education, and (iv) loans from SSNIT.

2.4 TheSLTFStrategyintheContextofGlobalandNationalDevelopmentPlans Ghana adopted the Millennium Development Goals (MDGs) and the successor Sustainable Development Goals (SDGs) as part of its agenda for development. These together with various Development Plans under a broad Vision 2020 agenda implemented since 1995, have helped Ghana define a number of education-specific plans and strategic thrusts for funding education at all levels. The SLTF mandate responds to a matrix of overarching Development Plans and Strategies including the:

· Millennium Development Goals (MDGs) (2000 to 2015) now succeeded by,

· Education Strategic Plans – Ghana (2010 – 2020)

· Ghana Shared Growth & Development Agenda (GSGDA II) (2014 – 2017)

· Sustainable Development Goals (SDGs) (2016 to 2030)

· National Development Planning Commission (NDPC) 40-year Plan (2017 – 2057) The Medium-Term Strategy of the SLTF addresses Goal Four (4) of the SDGs which is to “ensure inclusive and equitable education and promote life-long learning opportunities for all” and two (2) of the seven (7) Thematic Areas under the GSGDA which place emphasis on “Human Development,

Employment & Productivity”, and an “Enhanced Competitive Ghana Private Sector”. The effective, efficient, and sustainable provision of unbiased assistance to tertiary students will provide opportunities to enhance the development of entrepreneurial and employable Human Resource, which is highly productive. This in turn will feed into the development of a Private Sector to drive economic growth.

2.5 DevelopingtheStudentsLoanTrustFundStrategy

2.5.1 TheBrief

The SLTF briefed IY&A to develop a Medium-Term Strategy for the SLTF over a period of 18 weeks “through a participatory process involving staff, Board members and other stakeholders” and to “develop a comprehensive ‘roadmap’ setting the direction and pace of SLTF work over the next 5 years and beyond in a coordinated and focused manner.”

2.5.2 ThePurposeandStructureoftheStrategyDocument

The Medium-Term strategy for the SLTF was to: (i) respond to the key emerging and evolving consumer and industry trends that have

implications on the future sustainability and relevance of the organisation; (ii) articulate the strategic agenda over the next 5 years and the key arrangements required to

translate the strategy into action; and (iii) serve as the reference document for the operations and deliverables of SLTF including an

implementation plan, the set of corporate targets, and a five-year financial plan.

Providing financial assistance for tertiary education will

enhance the delivery of entrepreneurial, highly productive and employable human resource for the

development of private enterprise

S t u d e n t s L o a n T r u s t F u n d

3 | P a g e

One part of this document covers an analysis of the external environment in which the SLTF operates and the evolving consumer and industry trends. Another part scrutinizes the internal operations of the organisation and its performance against the current strategy. Lastly, a third part looks at the strategic framework for the SLTF and the strategic choices made in response to the challenges and opportunities that confront the organisation.

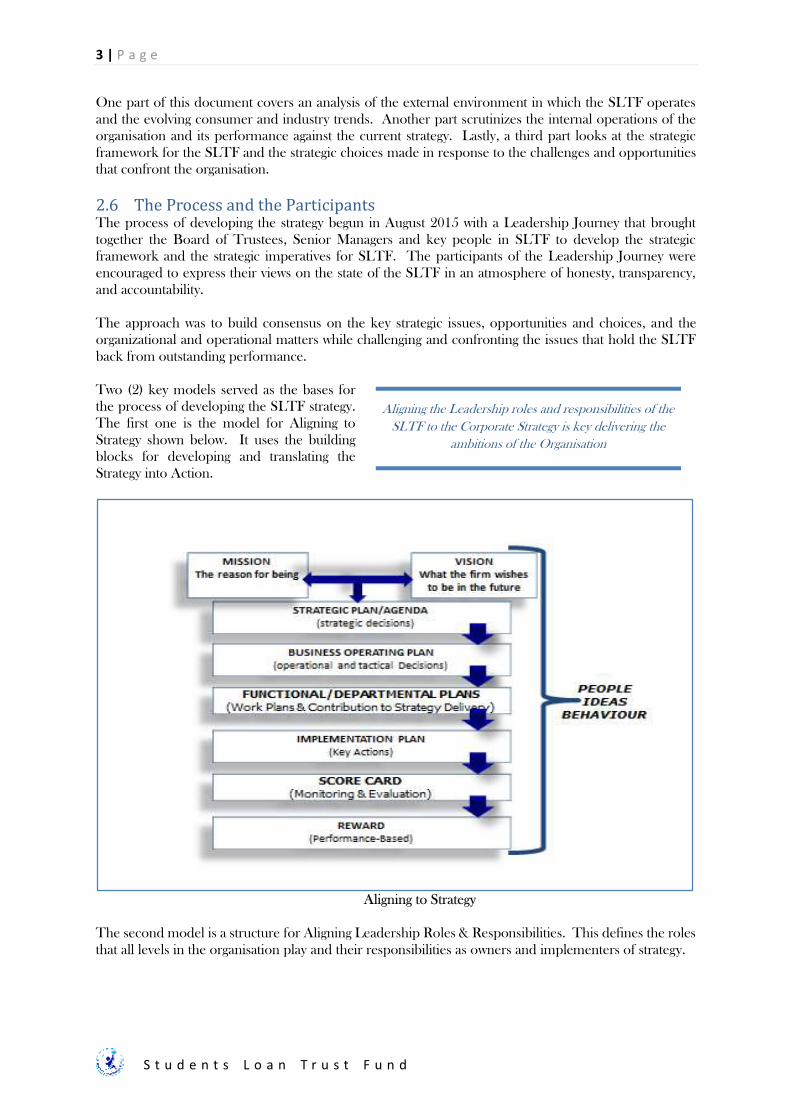

2.6 TheProcessandtheParticipantsThe process of developing the strategy begun in August 2015 with a Leadership Journey that brought together the Board of Trustees, Senior Managers and key people in SLTF to develop the strategic framework and the strategic imperatives for SLTF. The participants of the Leadership Journey were encouraged to express their views on the state of the SLTF in an atmosphere of honesty, transparency, and accountability. The approach was to build consensus on the key strategic issues, opportunities and choices, and the organizational and operational matters while challenging and confronting the issues that hold the SLTF back from outstanding performance. Two (2) key models served as the bases for the process of developing the SLTF strategy. The first one is the model for Aligning to Strategy shown below. It uses the building blocks for developing and translating the Strategy into Action.

Aligning to Strategy

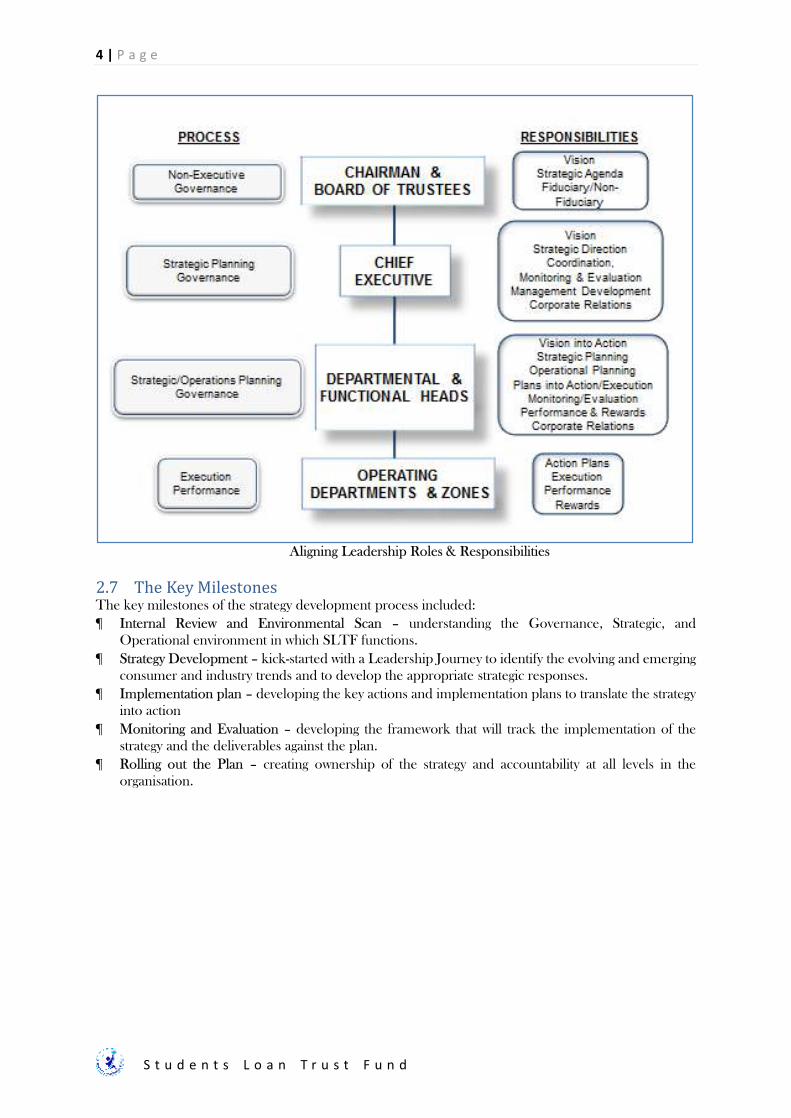

The second model is a structure for Aligning Leadership Roles & Responsibilities. This defines the roles that all levels in the organisation play and their responsibilities as owners and implementers of strategy.

Aligning the Leadership roles and responsibilities of the

SLTF to the Corporate Strategy is key delivering the ambitions of the Organisation

S t u d e n t s L o a n T r u s t F u n d

4 | P a g e

Aligning Leadership Roles & Responsibilities

2.7 TheKeyMilestonesThe key milestones of the strategy development process included: · Internal Review and Environmental Scan – understanding the Governance, Strategic, and

Operational environment in which SLTF functions.

· Strategy Development – kick-started with a Leadership Journey to identify the evolving and emerging consumer and industry trends and to develop the appropriate strategic responses.

· Implementation plan – developing the key actions and implementation plans to translate the strategy into action

· Monitoring and Evaluation – developing the framework that will track the implementation of the strategy and the deliverables against the plan.

· Rolling out the Plan – creating ownership of the strategy and accountability at all levels in the organisation.

S t u d e n t s L o a n T r u s t F u n d

5 | P a g e

3 CHAPTERTWO–Ghana’sTertiaryEducation

3.1 TheDemandforTertiaryEducation In recent years, tertiary education has been in great demand both from individuals and their families because of the employment opportunities higher education offers as well as the greater earnings potential it presumably conveys. Tertiary education is also increasing in importance to governments because of the anticipated public benefits to the social, cultural, political, and economic well-being of countries. Suppliers of tertiary education have responded by expanding opportunities and establishing fit-for-purpose offerings for different needs. Beyond the traditional “full-time” models there are now many tertiary programmes designed for working students who take time out to improve themselves academically. Currently, the influence of the labour market on courses pursued is limited. Many employers say the graduates from the tertiary institutions are not readily employable because of the misalignment between what they study and what the market needs. In addition, the consolidated benefits from improvements in identification, customer data administration, and ICT increasingly reduce the cost of administering loan schemes including that run by the SLTF. There are at least three (3) broad types of tertiary students.

1. The first group includes the normal “continuing students” who go directly through their tertiary education from the Senior High School. This group constitute the vast majority of students who populate the tertiary institutions in Ghana.

2. The second group comprises the matured students who go into employment for a period either because they did not meet the academic entrance requirements at the time or needed to work to build up resources to continue their education. Teachers and nurses who pursue their first degree after teaching and serving for some years fall in this category.

3. The third group consists of those students who pursue other higher degrees sometime after they obtain their first degree. This group tend to be a little more flexible with the design, the length, and the timetables of the programmes.

3.2 TheStructureofTertiary1Education2Ghana is evolving a balanced relationship between the public and private sector providers of tertiary education with close linkages in the award of degrees as the private sector participation expands. The number of students in the chart on the next page are those enrolled in the 117 tertiary institutions currently covered by SLTF. There are in total about 140 tertiary institutions in Ghana.

1 h�p://ghana.usembassy.gov/educa�on-of-ghana.html 2 h�p://www.whystudyinghana.com/es.html

Tertiary education offers employment opportunities and the potential for greater earnings

6 | P a g e

At the same time, individual needs for financial assistance have become more varied and complex. Typically, the financial assistance required for tertiary education should cover the cost of tuition, the cost of learning aids and the cost of boarding and lodging. Though the proportions of these costs differ in quantum between public and private institutions, overall, the private institutions cost much more than the public institutions.

3.3 FundingTertiaryEducation In Ghana, the ever-increasing cost of tertiary education frequently makes it difficult and in some cases, impossible for qualified students, particularly those from poor backgrounds, to have access to such education. Though it is obvious that many of these eligible students do, need some form of financial assistance, the assistance required by these different groups differ in size and timing. Some depend on family members, friends, and the churches and associations they belong to for assistance through their tertiary education. There is also evidence that parents or the students themselves obtain loans from individuals (family members, friends), credit unions, micro finance institutions, and banks to fund their education. A few financial institutions offer products described as student loans but how they administer these products is not very different from traditional bank loans including the need for collateral and guarantees. Indeed, some parents and students have applied for one-year loans that they pay off in 12 months and then reapply annually over the period of the education.

The chart on the next page gives a picture of the usual sources of finance for student’s tertiary education, how much they cost and the strictness of the prerequisites needed to access such funding.

307,315 Students 117 Ins�tu�ons

PRIVATE INSTITUTIONS59,172 Stodents Enrolled

University Colleges

Colleges of Educa�on

Schools of Educa�on

Ins�tutes

Tutorial Colleges

4-year Degrees 3-year Diplomas 2-year Diplomas

PUBLIC INSTITUTIONS248,143 Stodents Enrolled

Universi�es

Polytechnics

Colleges of Educa�on

Schools of Educa�on

Ins�tutes

Academy

The increasing cost of

tertiary education sometimes hinders access

The individual needs for financial assistance

have become more varied and complex

S t u d e n t s L o a n T r u s t F u n d

7 | P a g e

3.4 TheEnvironmentalContextofGhana’sTertiaryEducation

3.4.1 TheEconomy

Ghana’s economy underperformed over the past few years and though some of the fiscal and monetary policies required to stimulate a recovery are in place this may be slow over the next two years or so before economic growth accelerates. Some consequences of the depressed performance of the economy are a lack of liquidity, declining household income and high unemployment. The effect of the high base rate – now at 26%, and inflation in excess of 15%, has driven the cost of tertiary education upwards and in many cases pushed the fees beyond the affordability range of many Ghanaians. On top of that, the challenge of tertiary education in these circumstances is creating room for students to access affordable financial assistance with a level of assurance of employment after their education.

Source: World Bank

Family and Personal Funds

Student Loan Trust Fund

Credit Unions

Non-Bank Financial Ins�tu�ons

Tradi�onal Banks

Scholarships

0

1

2

3

4

5

6

7

8

9

10

0 1 2 3 4 5 6 7 8 9 10

Stri

ctn

ess

of

Term

s o

f A

cces

s

Cost of Access

Es�mated Source of Educa�onal Funding

Es�mated Source of Educa�onal Funding

14

9.37.3

4.2 3.55.9

7.8

0

5

10

15

2011 2012 2013 2014 2015 2016 2017

GDP Growth

S t u d e n t s L o a n T r u s t F u n d

8 | P a g e

The Chart above shows the World Bank overview of the performance of Ghana’s economy in the last five (5) years and the forecast for 2016 and 2017. The Government of Ghana’s forecast on GDP growth for 2015 is 4.1% and 5.4% for 2016 (5.2% excluding oil). Over the next three (3) years GoG’s forecast on the average GDP growth is expected to be 8.2% (6.9% excluding oil) and the targeted inflation is 8%.3

3.4.2 TheSocialEnvironment

Ghana’s strategy to reduce poverty has made some gains. However, many Ghanaian households still fall below the poverty line and this is widespread across the country. The Ghana Poverty Mapping Report of May 2015 indicates that the northern half of Ghana has the highest cluster of poor households in the country. This means that many eligible Ghanaian tertiary students cannot make it through their education without some form of financial assistance. In Ghana, it is prestigious to have a tertiary education. The contradiction is that although many students need help financially for their education, they also do not want to carry the social stigma of having borrowed to do so. The resolution to this conflict depends on how loan products are packaged and offered. There is evidence that more and more students are now accepting borrowing to fund higher education as a normal means to an end.

The World Bank has moved from pressuring developing countries and the donor community to prioritise basic education to promoting higher education in the year 2000. This important contextual factor has created more space and means for more households to send their youth into higher education.

The pressure for increasing enrolment in tertiary institutions particularly has been on the back of increasing birth rates over the last decade coupled with rapidly increasing proportions of youth finishing secondary school with legitimate aspirations for some tertiary education.

As indicated earlier there are many avenues, though limited, that students use to fund their tertiary education. There are organisations, associations, and welfare funds that provide “soft” loans for long-standing members to cover financial needs including the funding of education.

3.5 SomeEmergingIssuesandOpportunities

3.5.1 GrowingNumberofEnrolmentinTertiaryEducation

The school list for tertiary institutions in Ghana has risen from 205,027 in 2010 to 307,321 in 2015 representing an increase by 49.9%. This should increase by a comparatively higher rate in the next five years given the country’s good performance on the Millennium Development Goals for enrolment at the basic education level and the fact that more students accessed secondary education in the same period. This stream of pupils will enrol in tertiary education in the years ahead. However, during the same period, the number of students who have benefited from loans from the SLTF has decreased by 33.9% from 35,250 in 2010 to 23,298 in 2015. This represents 7.6% of the total number of enrolled students. Though not all the rest of the 92.4% of enrolled students may require loans for their tertiary education, it represents an opportunity in the market for loans to students that the SLTF must quantify and cover.

3 2016 budget statement by Minister for Finance – November, 2015

Increasing demand from students has created

opportunity for the development of accessible

and affordable tailored loan products

A GDP growth forecast of average 8.2% indicates

room in the economy for the creation of jobs

It is prestigious to have a tertiary education

and there is now space for households to give their youth this kind of education

S t u d e n t s L o a n T r u s t F u n d

9 | P a g e

3.5.2 IncreasingSophisticationandDemandsfromTertiaryStudents

The consumers of tertiary education are becoming more sophisticated and increasingly demanding. These demands are now diverse extending to cover the full support systems required to complete their education. Different loan product propositions and packages are required to satisfy them to enable a widened coverage.

3.5.3 IncreasingandDiversi�iedNeedsandExpectations.

The number of tertiary programmes and tailored offerings are increasing and broadening in response to the growing and diversified needs and expectations of tertiary students. A small but rising number of students now expect the tertiary institutions to align the way they deliver their programmes to the needs of their stage in life. These include the length and timing of programmes. These diverse expectations mean the loans could service any combination of needs including tuition, learning aids or boarding and lodging. Providers of loans must consider different products and offerings designed to meet these needs rather than a one-size-fit-all student’s loan. Some students appreciate the real cost of funding a student loan and are willing, able and ready to pay the right commercial price for such loans.

3.5.4 TougherCompetitionintheStudentLoanIndustry

The competition in the general Loan Industry in Ghana has been increasing rapidly over the last decade owing to the emergence of several Microfinance Institutions as well as Savings and Loans companies in addition to the twenty-five (25) universal banks, which are currently in operation in the country. However, few of these financial institutions have loan packages specifically designed for tertiary level students though they do provide loans for students under their general products. This makes SLTF the single institution that is totally dedicated to financing higher education in the country now.

Ultimately, competition in the industry will heighten, as financial institutions come up with innovative loan products designed for student to compete strongly in the industry for a good share of the Students Loan segment of the loans market.

3.5.5 IncreasingdemandonResourcesandCapacityofOrganisationsforRelevance

Providers of student’s loans, including SLTF, will continue to be relevant to tertiary students only when they continue to offer on time, consumer-led product, and service innovations. This means loan providers must continually develop the internal capacity and capability to lead the market and make the choices on what to focus their resources on for optimum returns.

3.5.6 MajorTechnologyChanges

Technology has become a major backbone for delivering an organisation’s products and services in a consumer-oriented effective and efficient manner. This tool will increasingly provide a competitive advantage in the delivery of the promises for organisations like the SLTF.

3.5.7 IncreasingRisksofNon-recoveriesofLoans

In the context of the current low liquidity in the economy and the lack of expansion in employment, the risk of non-recoveries of loans are getting higher. Some of the traditional collaterals like buildings, insurance and employer guarantees are either no longer readily available or are no longer relevant. The ability to manage risks is very important and organisations need to develop the appropriate responses to the risks.

3.5.8 TheIncreasingCostofTertiaryEducation

The public tertiary institutions have been largely dependent on governments, or taxpayers, for revenues to meet the high and rising per-student cost of education. Government’s ‘near-absolute’ subsidization of tertiary education is consistently dwindling considerably. Accordingly, tertiary institutions are now

The high cost of tertiary education, the high risk

of loan recoveries and technological changes places demands on the resources and

organisational capacities of loan providers

S t u d e n t s L o a n T r u s t F u n d

10 | P a g e

transferring a greater part of the cost of education to students. As this continues, the cost of tertiary education in the public institutions in Ghana will continue to increase. At the same time the privately run institutions will continue to strive for reasonable returns on their investments and therefore will reflect the general cost of running such institutions profitably. In addition, some specialist programmes especially those related to the oil and gas industry place much higher financial demands on students.

3.6 GeneralConclusionsonEnvironmentinwhichSLTFoperates There are some challenges in the general loans environment that have their roots in the general performance the economy, cost of accessing funds and the cost of doing business while remaining viable over the long term. Many Ghanaians households are poor and in spite of the aspiration of parents and students to obtain tertiary education many are financially handicapped. The need for an intervention, no matter how small is a crucial one and cannot be underestimated. As more and more students seek tertiary education and the cost of education keeps going up, the market for student loans will grow. The great opportunity is to create tailored loan products that are accessible and relatively affordable.

S t u d e n t s L o a n T r u s t F u n d

11 | P a g e

4 CHAPTERTHREE–TheOperationsoftheStudentLoanTrustFund

4.1 TheStudentLoanTrustFundTen (10) years after its establishment, the SLTF is carrying out this mandate and growing in importance in the area of funding tertiary education both in terms of the absolute numbers of beneficiaries and in terms of the overall value of loans given by the Fund. This is evident in the increasing number of students who access the Fund’s loans and the increasing level of the amounts made available to these students over the years.

4.2 TheGovernanceArrangementsA Board of Trustees led by a Non-Executive Chairman runs the SLTF. The Board performs it duties through eight (8) sub-committees. A Management Team made up of the Heads of Finance & Administration, Operations Planning, Research & Information Systems, and Internal Audit and led by the Chief Executive Officer supports the Trustees.

4.3 OperationsandActivitiesoftheSLTF The activities and operations of SLTF span from the receipt and/or acquisition of funds, the processing of loan applications, disbursement of loans to eligible students to the recovery of loans upon maturity. The SLTF operates much like a bank receiving deposits from Government of Ghana through GETFund and the CST and then give it out as loans to tertiary students in Ghana.

Receipts and reviews of applications from students are handled through 14 zonal offices with presence on fifty-one (117) campuses across all ten (10) regions of Ghana. SLTF employees staff these offices and operate as the first point-of-call for prospective and existing borrowers in the loan application process.

Board of TrusteesComprising Eleven (11) members,

nine (9) of whom are non-execu�ve

Chief Execu�ve Oficer

Opera�onsPlanning, Research & Informa�on Systems

Finance & Administra�on Internal Audit

Legal/Compliance Commi�ee

Claims Review Commi�ee

MIS & Opera�ons Commi�ee

Finance, Investments, Administra�ve & Fund

Raising Commi�ee

Execu�ve Commi�eeAudit Report

Implementa�on Commi�ee

Communica�ons & Interna�onal Rela�ons

Commi�eeComplians Commi�ee

SLTF

- 14 Zonal Offices - In 10 Regions

- With presence on 117 campuses

S t u d e n t s L o a n T r u s t F u n d

12 | P a g e

4.3.1 LoanApplicationandDisbursement

The SLTF currently runs an online Students Loan Application System (SLAS). Applicants who do not have easy access to internet fill out the application forms manually and submit to the nearest SLTF office (Zone/Campus) of their respective institutions. When the online application is completed, SLTF requires that applicants submit printed copies of the summary of their completed applications to the Fund’s office together with all related documents for verification to complete the application process.

The easy to use online application platform includes a Means Testing Methodology that assesses the financial background of families in determining the financial needs of borrowers and this helps SLTF to allocate support to applicants more equitably. The SLTF loans repayment process gives two (2) years grace period after graduation of the loan beneficiary to

start repayment over three (3) or four (4) years depending on the number of years spent on the education. This means a total of nine (9) to ten (10) years between when SLTF initially disburses a loan and when the beneficiary fully pays back the loan with interest. SLTF approves and disburses loans annually for the period of the student’s study in the tertiary institution as long as they are registered at their institutions as students. One of the limitations of the system that underpins the disbursement and repayment process (the Students Loans Management System) is that if a beneficiary starts repayments before all the annual payments are disbursed the system will suspend subsequent pre-approved disbursements until the beneficiary settles all outstanding balances. For example, a four (4) year student who starts repaying from year one (1) will not get his/her next three (3) disbursements until the year 1 balance is paid.

4.3.2 TheStudentsLoanManagementSoftware

The Students Loan Management System (SLMS) is also in place to ensure proper loan data management. It also helps to reduce the risk of giving loans to wrong applicants.

4.3.3 CostEf�iciencyandOperationalEffectiveness

Across Africa the standard measure of operating efficiency used by student loans organisation is the percentage of operating cost of the net cumulative income. Over the past five (5) years, as shown in the chart below, SLTF operating efficiency of 3% compares well with other student loans operations in Africa. The 2012 and 2013 period for the SLTF was characterised by increasing investments required to consolidate the operations. The second chart on the next page shows the relationship between the average amounts disbursed per beneficiary and the average cost of operations per beneficiary. Another operating efficiency measure shown in that chart is the relationship between operating cost and the loans disbursed. With this measure the efficiency measure SLTF’s rose up to 35% in 2013 and though it dropped to 23% in 2015 it is still higher than the 2010 start-up level of 15%. All efforts must be made to bring this at least to the 2010 level.

A recommended cost to value ratio is between 9% and 11%. This level of cost efficiency that will contribute greatly to the sustainability of the SLTF.

GH¢ m 2010 2011 2012 2013 2014 Net Income 53.0 71.4 88.2 101.3 124.5 Operating Expenses 2.0 2.2 2.3 2.8 3.8 %age cost 4.0% 3.1% 3.0% 3.0% 3.0%

Relationship between Net Income and Operating Cost

The core operating cycle of SLTF is

Receiving Funding, Receiving Loan Applications and Approving Loans, Disbursing the Approved Loans and

Recovering the Loans paid out, all in a cost efficient manner

S t u d e n t s L o a n T r u s t F u n d

13 | P a g e

4.4 SituationalAnalysis(ThechallengesoftheSLTF)

4.4.1 Capitalisation

The greatest risk to the relevance, quality, coverage, and sustainability of all effort including the current manifestation of the Student Loan scheme is securing and maintaining adequate capitalisation. The SLTF needs to receive regular injections of funding from a broad range of benefactors to be able to offer student loans to the widest possible profile of tertiary students on a sustainable basis. However, the SLTF presently, is almost entirely dependent on the GETFund and this is not sustainable in the long term. Consequently, the SLTF should build long lasting relationships that will enable them to attract private entities and motivate them to increase their benevolent giving through the organisation.

4.4.2 Collateral

Whilst Ghana has addressed the fact that financially needy students cannot provide any collateral by allowing them to use SSNIT contributors, religious bodies, etc. as guarantors, many remain unable to borrow because potential guarantors are put off by the risks of associated with non-payment by borrowers, and the fact that an entity can only guarantee one loan at a time. Indeed, the new NPRA law now makes the use of SSNIT Contributors irrelevant. The SLTF needs to develop a more rigorous framework for managing the risks of providing loans to students.

4.4.3 InterestSubsidy

SLTF’s advantage in the Students loan industry partly comes from its ability to mobilize cost free funds, which makes it possible for it to charge comparatively low interest rates on its loans to students. There is moratorium on repayments of loans until two years after a person has completed their programme of study and have started working. This makes the Fund’s loan product comparatively attractive than other student loan packages that demand repayments while the student is in school or soon after a person completes their education with no consideration as to whether they have started receiving income or not. The element of interest payments is a double-edged problem. First, misconceptions about the policy of charging compound interest calculation causes some potential beneficiaries to believe that student loans are not affordable. The socio-economic and political dynamic tends to default towards a zero-interest loan or even ‘free money’ that minimises or removes any obligation for repayment. This is unsustainable.

SLTF needs to attract funding from more sources including private entities and also become a hub

through which increased benevolent giving can be channeled to support tertiary education

GHS 381

GHS 450

GHS 471

GHS 573

GHS 1,043GHS 944

GHS 57 GHS 83 GHS 123GHS 199 GHS 223 GHS 21815%

18%

26%

35%

21% 23%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

GHS -

GHS 200.00

GHS 400.00

GHS 600.00

GHS 800.00

GHS 1,000.00

GHS 1,200.00

35,2492010

26,9552011

18,6052012

13,8332013

17,0952014

23,2982015

Evalua�on of SLTF Disbursement/Cost Efficiency

Average Value of Loan Disbursed Average Cost of Opera�ons

Cost:Value Ra�o Cost of Opera�ons : Disbursements

S t u d e n t s L o a n T r u s t F u n d

14 | P a g e

Second, is the fact that the uneconomic interest rates that are charged represent a massive interest subsidy and a substantial and costly “hidden grant”. This is also unsustainable.

4.4.4 Non-repayment

The SLTF continues to improve its systems for collection of repayments and tracking borrowers in order to minimise losses due to non-repayment. However, the massively weak economy is unable to generate

large numbers of graduate-level jobs. As a borrower expressed, “In the back of my mind I was always thinking, this money is an investment — that later on, when I graduate and get a job, I’ll be able to pay it off, but now I don’t think I’m going to get the return I thought I would”. The SLTF loan recovery systems remain technologically limited by the

weakness of national systems that support the traceability of individuals such as social security numbers, national address systems, and a credible births and deaths registry.

4.4.5 Recovery

Personal commitment to repay is weak and the institutional commitment to assure repayment is weak. SLTF must review its system for tracking beneficiaries who are due for repayment. Under the current system, Zonal officers must manually trace 1000+ long lists of names of beneficiaries in their territory and remind them of their obligations. This makes the model highly ineffective and stretches the resources required to carry out these activities. SLTF has loan repayment partnerships with banks such as the GCB, ECOBANK, NIB, and GN Bank. Borrowers are able to make repayments wherever they are through the Fund’s account in any of these banks. SLTF has introduced the Students Loan Protection Scheme to help reduce the financial burden on guarantors and families in the event of death or total or permanent incapacitation of borrowers. The table below shows SLTF’s recovery trends data over the past five years.

2010 2011 2012 2013 2014

Total Outstanding 53,688,764.57 72,102,458.84 88,393,514.57 102,042,105.20 126,213,201.79

Total Principal 43,871,745.60 55,916,202.40 63,850,442.31 69,660,219.49 85,030,415.63

Total Interest 9,817,018.97 16,186,256.44 24,543,072.26 32,381,885.71 41,182,786.16

Total Due 157,118.69 5,669,753.79 21,308,853.66 23,978,614.02 24,978,203.73

Total Recovered 149,364.55 498,003.72 1,983,890.82 6,038,428.74 8,150,013.73

Total Overdue 25,111.54 436,880.79 2,228,654.40 6,047,423.07 12,520,259.30

0.00

20,000,000.00

40,000,000.00

60,000,000.00

80,000,000.00

100,000,000.00

120,000,000.00

140,000,000.00

Ce

dis

PerformanceofRecoveries

SLTF must ensure sustainability by being “business-

like” and by continuously striving for full loans recovery at interest rates that are viable.

S t u d e n t s L o a n T r u s t F u n d

15 | P a g e

The current Students Loan Management System (SLMS) is not able to automatically generate all the relevant reports and to keep track of the full recovery of loans. These gaps points to the need for a Process and Systems review that will further streamline and align the operations SLTF in a way that the reports from the Students Loan Management System (SLMS) are easy to understand and drive the management decisions on loans recovery. A new in-house Student Loan Information System is being developed to address this. It is important that the design of this new system responds to all the information requirements needed to run the Fund. The new system should also enable SLTF project the future funding requirements and inflows of receivables more robustly so that targets and plans to drive pre-payments, manage the risks from delayed payments and non-payments are more actionable.

4.4.6 AttitudeofBorrowersfromtheSLTF

Ghana now has an evolving students loan programme designed to become eventually self-financing through repayment of student loans. However, non-payment and failure to index tightly, repayment to inflation have effectively converted the loans into grants. The focus groups4 discussion done across the various institutions as part of this strategy development process shows that students view student loans as a burden, have a negative attitude towards the loan repayment, and some beneficiaries hold back on their repayments because they:

· Claim that not enough education is received about their responsibilities to the fund;

· Believe that the systems to credit loan repayments properly to their accounts are weak;

· Assume that there is no database available to aid the SLTF track them when they default

· Know employers do not take steps to deduct loan repayment from the salaries even after they are informed that an employee is a beneficiary of student loans; and

· Do not trust/know formulas for calculating the compounded interest over time. Yet together these factors undermine the commonly repeated claims that more beneficiaries will repay their loans once the SLTF reduces the interest rates on the loans and increases the repayment period.

4.4.7 PerceptionoftheSLTF

The relationship between SLTF and students is largely one of apprehension mainly because students hear many untruths from colleagues and other self-acclaimed false ambassadors of SLTF who have made it their job to talk people out of accessing SLTF loans. Majority of students do not know of SLTF until they are in the middle of their education programmes and critically in need of funding.

4.4.8 TheZones

The SLTF should consider a common strategy with tracking mechanisms to increase the ability of the zones to conduct track outreach, recruit beneficiaries, and track them post-graduation to facilitate repayments.

4.5 SomeAspirationsoftheSLTF The Board of Trustees and the Management of the SLTF believe that the organisation can be inspired to create a future that will anchor it as the favoured hub of student loans and related services in tertiary education in Ghana. The following are some of the aspirations that expressed by the leadership team of the SLTF:

1) SLTF to become a household name & educational bank which is true to its Mandate, and Positioned to be the first point-of-call for tertiary student financing.

4 Cape Coast, Sunyani, Gbaawa, Accra, 5 groups of average 12 people

As SLTF aspires to become a

household name it must dispel the misconceptions about its services and

liberate its Zonal operations

S t u d e n t s L o a n T r u s t F u n d

16 | P a g e

2) An Organisation that is able to Attract & Retain a large number of Benefactors who associate with the Aspirations of SLTF.

3) A Strong, Independent, and Sustainable Students Loan Fund with wide-ranging sources of funding.

4) A highly Driven & Coherent Leadership Team that has stability of tenure. 5) An Organisation that has entrenched Values & Behaviour 6) Managed with a Transparent and objective Succession Plan. 7) A highly Trained & Developed Work Force that is motivated by a Performance-Based

Rewards System. 8) Diversified & Targeted Loan Products aligned to the specific needs of students. 9) Decentralised & Empowered Zonal/Regional Operations to serve Clients. 10) An Operationally Effective & Cost Efficient loans Fund. 11) Strong and Better relations and collaborations with key Stakeholders.

4.6 SomeConclusionsonSLTFInternalScrutiny The table on the next page shows the outcomes from the discussions from the Leadership Journey on the internal dynamics of SLTF. The discussion looked at Governance, Strategy, and Performance in SLTF. The internal scrutiny revolved around the Operations of SLTF and the People, Finances in the context of the loans industry. It also looked at the perceptions of Stakeholders and Clients of the SLTF. Strength Weakness

· A specialist Students Loan provider

· Cost free funding

· Low interest rate

· Repayment moratorium

· Low consumer awareness

· Low consumer education

· Inadequate funding

· Insufficient loans disbursements

· Inflexible Loans System Opportunities Threats · Demand for Loans

· Increased market coverage

· Development of product and service mixes

· Diversified needs

· A strong financially independent organisation

· Decentralised organisation

· Increase Competition from Banks

· Sustainable sources of funding

· Low loan repayment rate

· Non-recovery of loans

S t u d e n t s L o a n T r u s t F u n d

17 | P a g e

5 CHAPTERFOUR–TheSLTFStrategicFramework

The Strategic Framework for the SLTF responds to the evolving trends in the loans environment and the aspirations of the SLTF. The Framework defines the pillars that will drive the organisational decisions, resource allocations, and common objectives. The design of the framework elements emphasises interdependent targets and operating systems.

5.1 MissionThe Mission of the SLTF and the reason for being is “to provide TIMELY financial SERVICES to eligible Ghanaian tertiary students”. 5

5.2 VisionThe Vision of the SLTF and the future aspiration of the organisation is “inspiring and unleashing greater prospects”.6

5.3 TheStrategicImperativesFive (5) Strategic Imperatives will drive the choices that the SLTF makes over the next medium term (2016 – 2020). These imperatives reflect a total perspective of delivering value to its stakeholders and the challenges and opportunities they present to the organization. They are the most important objectives that the SLTF will focus on and succeed in achieving. They will have sustained impact on performance and will be the basis for common behaviour and common organizational decisions on trade-offs, resource allocation and prioritisation.

5 The mission places emphasis on �meliness of SLTF disbursements of loans and the �meliness of the repayments of loans. It also places emphasis on the all-round services that the SLTF provides to its clients beyond just loan disbursement 6 Greater prospects for all stakeholders including the students, their employers, their contribu�on to Ghana’s economy, the ter�ary ins�tu�ons and the SLTF itself

S t u d e n t s L o a n T r u s t F u n d

18 | P a g e

5.4 TheEnablersThe Enablers of the delivery and implementation of this strategy are the Values, the Behaviour, and the Attitudes that the SLTF will pursue.

Cultural Aspect Traits Evidence

Values Stewardship Leave a better Outcome Service Feel the SLTF Experience

Behaviour Teamwork Result Oriented Achievers Diligent Partnership Collaboration Alliances

Attitude Youthfulness Energy Enthusiasm Fairness Reliable Predictable Honest

5.5 TheStrategicOutcomesAt the end of the five-year period, the qualitative outcomes of the fully implemented SLTF medium-term strategy will be:

· Financially sustainable Loan Fund

· Competitive

· An unleashed Place to Work

· Favoured and Preferred student Partner

· A Trusted and Valued organisation

Sustainably mobilize Funds

Attract, Develop & Retain the best People

Maximise Awareness of the Corporate & Product

Brands

Develop Consumer-Inspired Solutions &

Product Mixes

Deploy Technology to optimise operational

Efficiency & Effectiveness

S t u d e n t s L o a n T r u s t F u n d

19 | P a g e

6 CHAPTERFIVE–TranslatingtheStrategyintoAction

6.1 TranslatingtheStrategyintoActionThis chapter focuses on the targets and the actions required to deliver the strategy over the period 2016 to 2020. The measurable overarching Corporate Strategic Goals over the strategic period have been set as shown in the table below. These define the direction of delivery and is the focal point of all performance measures for Departments, Teams, and Individuals through all levels of the SLTF.

6.2 TheCorporateStrategicGoals

The Imperatives Proposed Indicators Proposed scope

2016 2017 2018 2019 2020

Sustainably

mobilize Funds

• Increased sources and

quantum of funding

10% 15% 20% 25% >25%

Attract, Develop &

Retain the best

People

• Retention of high

performing teams and

individuals

85% 95% 98% 98%

Maximise

Awareness of the

Corporate &

Product Brands

• Top of Mind Awareness

• Tailored Products &

Services

50%

50%

70%

60%

80%

70%

90%

90%

>90%

>90%

Develop

Consumer-Inspired

Solutions &

Product Mixes

• Map of Consumer Needs

• Consumer Solutions &

Products

H & A7

2 pdts

5 pdts

H & A

3 pdts

2 pdts

H & A

2 pdts

Deploy

Technology to

optimise

operational

Efficiency &

Effectiveness

• Disbursement Efficiency

• Cycle Times

• Cost: Value Disbursed

• Cost: Net Income

10 days

20%

3.0%

5 days

15%

3.0%

48 hrs

10%

2.5%

48hrs

10%

2.5%

Real time

10%

2.0%

7 Habits and A�tudes Study

All actions to deliver the strategic goals will

be based on common organisational decisions on priorities, trade-offs and

resource allocations

S t u d e n t s L o a n T r u s t F u n d

20 | P a g e

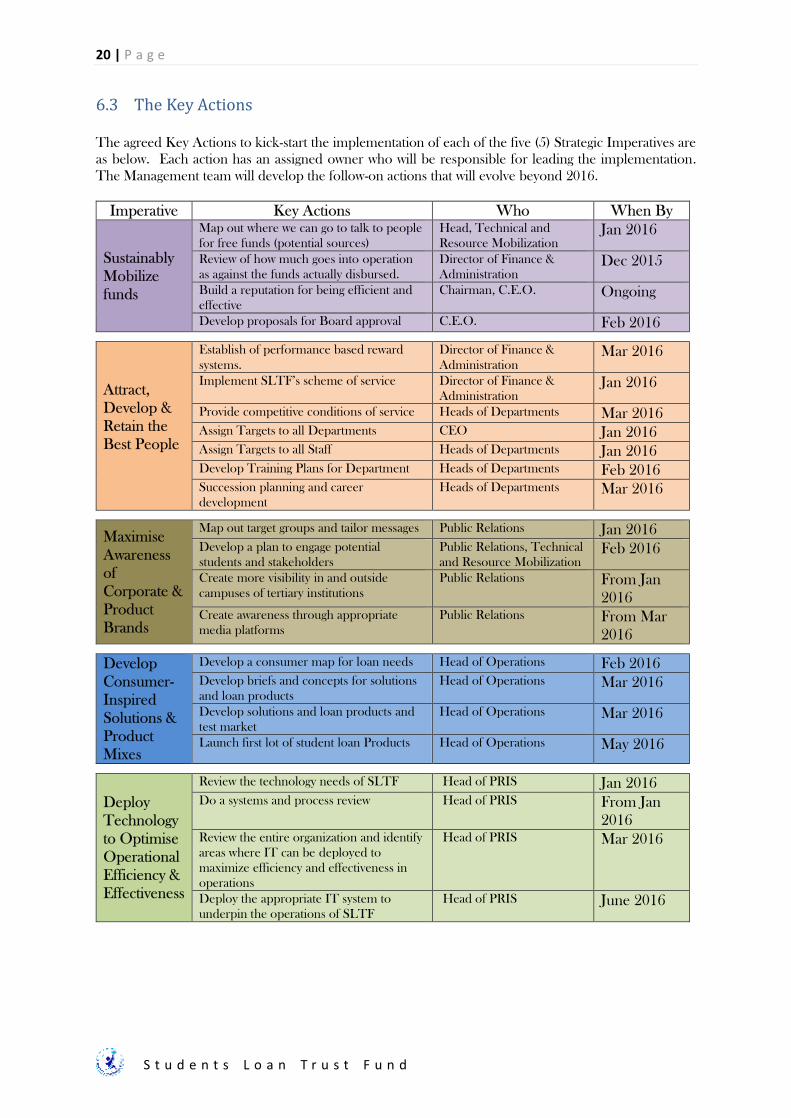

6.3 TheKeyActions The agreed Key Actions to kick-start the implementation of each of the five (5) Strategic Imperatives are as below. Each action has an assigned owner who will be responsible for leading the implementation. The Management team will develop the follow-on actions that will evolve beyond 2016.

Imperative Key Actions Who When By

Sustainably Mobilize funds

Map out where we can go to talk to people for free funds (potential sources)

Head, Technical and Resource Mobilization

Jan 2016

Review of how much goes into operation as against the funds actually disbursed.

Director of Finance & Administration

Dec 2015

Build a reputation for being efficient and effective

Chairman, C.E.O. Ongoing

Develop proposals for Board approval C.E.O. Feb 2016

Attract, Develop & Retain the Best People

Establish of performance based reward systems.

Director of Finance & Administration

Mar 2016

Implement SLTF’s scheme of service Director of Finance & Administration

Jan 2016

Provide competitive conditions of service Heads of Departments Mar 2016 Assign Targets to all Departments CEO Jan 2016 Assign Targets to all Staff Heads of Departments Jan 2016 Develop Training Plans for Department Heads of Departments Feb 2016 Succession planning and career development

Heads of Departments Mar 2016

Maximise Awareness of Corporate & Product Brands

Map out target groups and tailor messages Public Relations Jan 2016 Develop a plan to engage potential students and stakeholders

Public Relations, Technical and Resource Mobilization

Feb 2016

Create more visibility in and outside campuses of tertiary institutions

Public Relations

From Jan 2016

Create awareness through appropriate media platforms

Public Relations

From Mar 2016

Develop Consumer-Inspired Solutions & Product Mixes

Develop a consumer map for loan needs Head of Operations Feb 2016 Develop briefs and concepts for solutions and loan products

Head of Operations Mar 2016

Develop solutions and loan products and test market

Head of Operations

Mar 2016

Launch first lot of student loan Products Head of Operations May 2016

Deploy Technology to Optimise Operational Efficiency & Effectiveness

Review the technology needs of SLTF Head of PRIS Jan 2016 Do a systems and process review Head of PRIS From Jan

2016 Review the entire organization and identify areas where IT can be deployed to maximize efficiency and effectiveness in operations

Head of PRIS Mar 2016

Deploy the appropriate IT system to underpin the operations of SLTF

Head of PRIS June 2016

S t u d e n t s L o a n T r u s t F u n d

21 | P a g e

6.4 Monitoring&EvaluationIt is important that the Board and Management of SLTF own the delivery of the Strategic Goals and drive the implementation of the Key Actions. The Monitoring & Evaluation Model begins with the setting of the Corporate Targets with milestone that is broken down for Departments/Functions, Teams, Zones and individuals. Each of these targets should contribute to the full delivery of the Corporate Targets. The Monitoring & Evaluation Model assumes the following:

1. The agreed Corporate Goals have been phased with milestones over the strategy period 2. All Departmental, Functional, Team and Individual targets have been approved and signed 3. Cycles of Senior Management, Departmental, Functional, Team and Zonal meetings are in place 4. SLTF has an Appraisal System in place 5. A manager will be assigned to co-ordinate and report on Corporate performance against targets

Monitoring & Evaluation will be by series of meetings across five (5) levels as follows:

1. Individual - this will be a daily on-the-job review and weekly evaluation of performance of individuals against their personal targets. This will be led by the line managers of the individuals and should be part of the normal appraisal process of SLTF.

2. Team/Zone – weekly and monthly evaluation of the performance of Teams/Zones against the set targets for the Team/Zone. The evaluation of the Teams will be self-assessing and led by the Team/Zone Leader.

3. Departmental/Functional – weekly and monthly evaluation of the Department/Function against the Departmental/Functional targets. The Departmental/Functional evaluations will also be self-assessing led by the head of department/function.

4. Corporate – quarterly evaluation led by the CEO with Departmental/Functional evaluation reports presented by the Heads of Departments. The outcomes from these evaluations should reflect the overall performance of the SLTF against the Corporate Goals

5. Board Reviews – bi-annual Board Evaluations focusing on the performance against the Corporate Targets and Milestones.

The Monitoring & Evaluation Framework

Board ReviewBi-Annual Evaluation Evaluation Reports presented

by CEOLed by Chairperson

Corporate EvaluationQuarterly Evaluation Evaluation Reports presented

by Heads of DepartmentsLed by CEO

Departmental/Functional EvaluationMonthly Meetings Quarterly Evaluations Self-Assessing

Led by Head of Department

Team EvaluationWeekly Meetings Monthly Evaluation Self-Assessing Led by Team Leader

Individual EvaluationOngoing/Daily on-the-

jobWeekly Meetings STLF Appraisal Cycle Led by Line Manager

S t u d e n t s L o a n T r u s t F u n d