Embed Size (px)

Citation preview

Slovenia

Market Overview

Bord Bia, Frankfurt

November 27th 2008

Slovenian Market Overview

• Population: Ljubljana

270,000 (Capital), Maribor

111,000, Kranj 53,300,

Koper 50,000, Celje

49,000

• Language: Slovenian

• Currency: Euro

• Joined the EU in May

2004

Market Overview

• The adoption of the Euro in 2007 was expected to fuel growth in GDP.

• Private consumption was also expected to benefit from tax reforms which simplify the personal income tax structure.

• New government elections are taking place in October 2008.

• GDP Growth - real growth rate 4.0% 2008(e) (IGD, 2008)

• Inflation rate: 2.3% (2008(e)) (IGD, 2008)

• Unemployment: 6.6% (2008(e)) (IGD, 2008)

• Consumer spend per capita is increasing; up from €7,435 in 2005 to €8,348 in 2008 (IGD, 2008)

• VAT: 20%

• VAT on Food Preparations: 8.5%

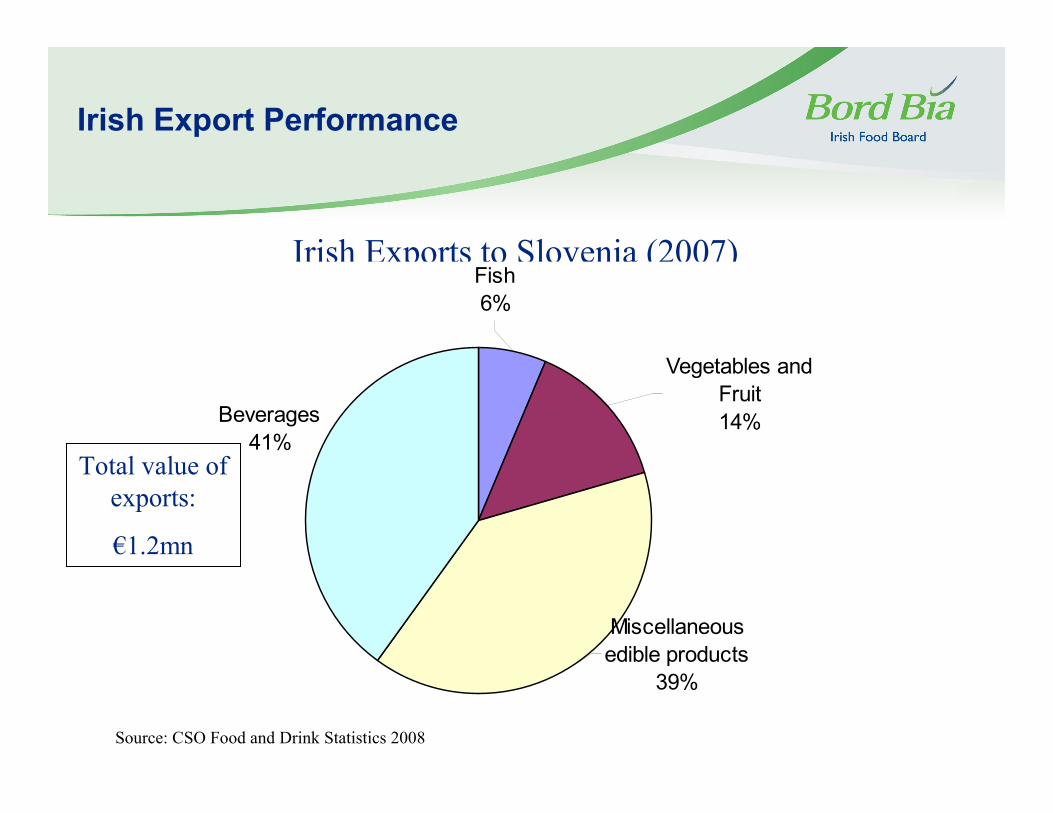

Irish Export Performance

Source: CSO Food and Drink Statistics 2008

Irish Exports to Slovenia (2007)

Miscellaneous

edible products

39%

Vegetables and

Fruit

14%

Fish

6%

Beverages

41%Total value of

exports:

€1.2mn

Key Consumer Trends

in the Market

• The total retail market is growing quite fast with an increase of around €0.5bn for 2007 and 2008

(e). The grocery retail market is growing at a slower speed than that but still growing at around

€0.2bn a year.

• Per capita spending is increasing but is still significantly lower than in Western Europe.

• 52% of retail sales in Slovenia are generated through the food retail sector.

Source: IGD Country Presentations, 2008

2,140

4.25

7.98

2008 (e)

(€)

2,030

4.08

7.50

2007

(€)

1,900Grocery Retail Spend/capita

3.82Grocery Retail Market (billions)

6.97Total Retail Market (billions)

2006

(€)

Retail Grocery Market

• Grocery Retail Value: €4.28 billion 2008(e).

• Slovenian retailers dominate the market but there is a number of

international retailers who have entered the market - Spar International,

E. Leclerc, Aldi (under the Hofer name) and Lidl (IGD, 2007).

• Acquisitions are a favoured strategy in Slovenian retailing with domestic

Mercator favouring a highly acquisitive strategy (IGD, 2007).

• Hypermarkets first entered the market in 2000 and they dominate in

larger cites while smaller towns and villages still favour supermarkets.

(IGD, 2007)

Retail Grocery Market

• The retail sector has had rapid transformation in recent years with a move away from manufacturer power and the focus being placed on larger retail formats and customer satisfaction.

• Mercator are looking to expand their operations and to modernise their current outlets. They aim to become a leading retailer in a number of SE European countries such as Croatia, Serbia and Macedonia.

• SPAR aim to have a 25% market share in the coming years and plan to invest €100 million to achieve this. Their strategy will be a focus on differentiation.

• Lidl entered the market in March 2007 making it the 6th discount chain on the market. They operate 28 stores currently in Slovenia.

Retail Market Share

Source: IGD Analysis Country Presentation Slovenia 2008

Mercator

38%

SPAR

13%

Aldi

2%

Other

34%

E. Leclerc

1%

Engrotus

12%

Retail Market Structure

Top 5 2006

Source: IGD Analysis, Country Presentation, Slovenia, 2007

17,400292.62%-100100Aldi

+7.1%

+16.1%

+12.2%

+2.3%

% Change

Grocery Sales

2006 v 2005

120,70025113.12%526526Engrotus*

103,5566314.48%553553Spar International

8,30011.17%4545E. Leclerc

232,25057134.90%1,3781,619Mercator*

Sales

Area

(sqm)

No. of

Stores

Grocery Retail

Market Share

*(%)

Grocery

Sales

(€m)

Total

Sales

(€m)

Retailer

•Grocery Retail Market Shares exclude cash & carry operations.

Data is for grocery formats only except Total Sales which includes non-grocery if applicable. Total Sales & Grocery Sales are

Net.

Data includes franchised operations where appropriate.

Slovenian Market

Facts

• Slovenia’s accession into the EU led to an increase in foreign investment which is set to continue into the coming years.

• Mercator dominates the retail market and this combined with a small population and a shortage of large cities could hamper retail development for hypermarkets and supermarkets.

• This is a very price sensitive market and as such there are a number of discounters operating in the market.

• Slovenia has an ageing population with the lowest fertility rates in Europe. The average age in Slovenia is 40.6years and by 2050 it is estimated that over 30% of the population will be 65+.

• There are strict restrictions on retail trading hours with Monday – Friday shops closing at 6pm and 1pm on a Saturday. Sunday has three rules - stores with essentials can open up to 10 Sundays a year and small stores with essential items at train stations, borders, petrol stations are allowed open. Everything else is closed.

Foodservice

Establishments

• McDonald’s

– Operate 15 outlets in the country.

– Entered the market in 1993.

– The only major international fast food chain operating there, though

Burger King are set to open in 2009.

Foodservice

Establishments

• A number of operators have entered and subsequently exited the

market in Slovenia. Examples include:

– Subway who closed their single store in Ljubljana last year.

– Dairy Queen - were the first to enter the market and exited in the

late 1990’s.

– Quick also entered and exited the market (IFE Foodapest, 2008).

Reasons for targeting Slovenia

• High concentration of organised trade predominantly Western European

owned relative to other Eastern countries

• Highest level of disposable income per head of population of the Eastern

European accession countries

• Slovenia is traditionally a gateway to the other markets of ex Yugoslavia

• Over 50% of retail sales are in food (€4.25bn)

• Member of Eurozone

• Good opportunity for export of whiskey and spirits

Barriers/challenges in supplying

Slovenia market

• Low level of Irish food exports currently to Slovenia

• Small population (2m)

• Large international foodservice operators have previously withdrawn from

the market with the exception of McDonald’s

Bord Bia services 2009

• Bord Bia market mentor (Mr. Kieran Fahy) available for Eastern Europe market and trade related queries:

• Services include: Itinerary Development, Category Analysis, Media review and translation services, Product Price auditing and tracking, Product retrieval, Buyer networking, Distributor searches

Kieran Fahy Also: Liam MacHale

Sarospatak ut 32 Bord Bia

1125 Budapest Wöhler Str. 3-5

Hungary 60323 Frankfurt, Germany

Tel: +36 706 144871 Tel +49 69 710 423 255

Email: [email protected] Email: [email protected]

![ワークーション・ズィーアールテン 1 piece 19 / 18 …¥46,000 ¥47,000 ¥49,000 17×8.0J 47 [F:36/H:44] 35 [F:48/H:56] ¥48,000 ¥49,000 ¥51,000 17×9.0J 32 [F:28/H:36]](https://img.dokumen.tips/doc/110x75/5f4d32f8f286726c13798ea2/fffffffffff-1-piece-19-18-46000-47000.jpg)