Embed Size (px)

Citation preview

1

Slides by Pamela L. Hall

Western Washington University

Credit Management

Chapter 5

2

Introduction

Many of you have probably received credit card offers (either on campus or through the mail) if you are a college student

About 80% of college students have credit cards

Proper use of a credit card can help establish a solid credit history

Improper use can take years to heal

3

What is Credit?Receiving money, goods and services on the

basis of an agreement that the borrower will repay the lender with a specified time period at a specified rate of interest

Today total consumer credit is over $1.5 trillion (excludes home mortgages and home equity loans)

Americans carry over 1 billion credit cardsOver 1 million Americans file for personal

bankruptcy each year (twice as many as 10 years ago)

4

Figure 5.1: Outstanding Consumer Debt

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

1980 1985 1990 1995 2000

Deb

t O

uts

tan

din

g (

$ b

illio

ns)

Installment loans

Revolving credit

5

Types of Consumer Credit Revolving credit

Consumer can make a number of different purchases, up to a certain credit limit

A minimum payment is due each month and interest is charged on the unpaid balance (average is 14.5%/year)

Installment loans Consumer borrows a fixed amount and repays the principal

plus interest at regular intervals (usually monthly) Lender usually holds title to asset until final payment is made

Mortgage loans and home equity loans Mortgage is an installment loan secured by real estate

Typically have a term of 15 or 30 years

6

Deciding How Much to Borrow

Failure to set debt limits is one reason why people get in trouble with credit cards Guideline: No more than 10 to 20% of

your take-home pay should go toward repayment of installment or revolving credit (exclude mortgage payment) National average is 13.5%

7

The Right Reasons for Borrowing

Purchasing large, important goods or services House Car College education

Dealing with emergencies Loss of job Death of relative (plane tickets on short

notice are expensive)

8

The Right Reasons for Borrowing

Taking advantage of opportunities Good sale on computer (you are saving for one

anyway)

Convenience Easy to pay with a credit card (pay off your

balance every month) when doing day-to-day shopping

Establishing or improving your credit rating Good way for a college student to establish a

credit rating

9

The Wrong Reasons for Borrowing

Living beyond your means Do you have to use your credit card to

pay your basic living expenses (because you can’t afford not to)? Buy groceries Buy clothes Buy gasoline Pay your taxes

10

Sources of Consumer Credit Financial Institutions

Commercial banks, savings banks, credit unions

National Credit Cards University alumni associations, sports franchises, etc. are issuing credit cards with their logo (can be used anywhere a regular bank-issued card is accepted) These organizations receive a fee from the issuing bank

Retailer-specific credit cards (such as Sears and JCPenney) Can only be used at a specific store

11

Sources of Credit

Consumer Finance Companies Company specializing in consumer loans

Ex: Household Finance Make relatively short-term loans Charge high interest rates Generally unsecured Application forms are easier to fill out than a

bank’s Takes a short period of time to receive

approval

12

Sources of Credit

Life-Insurance Companies Policyholders may be able to borrow

against their life insurance policy (up to the amount they have paid in premiums)

Brokerage Account Loans Buying on margin

13

Sources of CreditPersonal loan from family and friends

Always treat these in a businesslike manner Lots of potential for interpersonal conflict

Pawnbrokers Issues loans for a very low percentage of

an item’s face value Item is held as security until the loan is

repaid in full Should be viewed as a lender of last resort

14

Applying for CreditHow creditors evaluate loan applications

Capacity Can you afford to repay the debt Examines current income (and expected future

earning potential) vs. current expenses Are you a good credit risk?

Character Do you live within your means or above it? Do you pay your bills on time? Do you demonstrate stability?

Collateral Property to secure a loan

15

The Role of Credit BureausCredit bureau—a clearinghouse for

consumer credit information What’s in your credit file?

Identifying information Your credit history

Including whether or not you pay your bills on time Information of public record

Bankruptcies, lawsuits, criminal convictions You may request a copy of your credit record at

any time If you’ve recently been denied credit, the credit

reporting service must provide you a copy free of charge

16

What to Do If You Are Denied Credit

The lender must provide you with a written explanation Try negotiating with the lender

Ask for a lower loan amount Try another lender

Different lenders have different lending policies

Some are more lenient than others

17

Calculating Total Finance Charges

Lenders are required to clearly state the annual percentage rate (APR) Finance charge: total dollar amount charged

for credit Function of

Amount you borrow APR Term of loan

Annual percentage rate: interest rate paid per dollar per year for credit

Principal: the amount borrowed

18

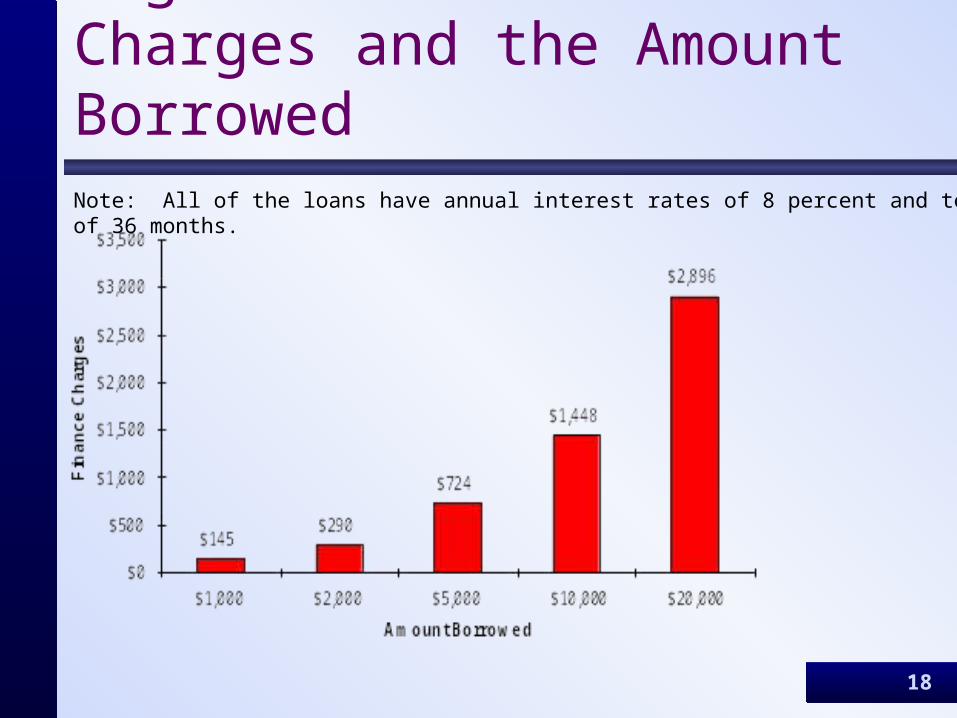

Figure 5.5: Finance Charges and the Amount Borrowed Note: All of the loans have annual interest rates of 8 percent and terms of 36 months.

19

Figure 5.6: Finance Charges and APRs Note: All of the loans are for $10,000 and have terms of 36 months.

20

Figure 5.7: Finance Charges and Repayment Terms Note: All of the above loans are for $10,000 and have APRs of 8 percent.

21

Calculating Periodic Interest

Most consumer debt calculates periodic interest using the simple interest method The outstanding balance on the loan is

multiplied by the periodic interest rate

22

Choosing the Lowest-Cost Credit Card Three main areas to consider

Annual fee Ranges from $0 to $50 annually

Late payment and other fees Annual percentage rate Grace period—how long you have to pay for new

purchases without having to pay interest charges Ranges from 0 days to 30 days

If you pay your bill in full every month, get a card with no annual fee and a grace period of at least 25 days

This way you won’t pay interest charges

23

Choosing the Lowest-Cost Credit Card

Many credit card companies offer a low interest rate for a short time period (to lure you in—called a teaser rate) and then raise the interest rate substantially

Or the company may offer a great rate unless one payment is late and then the rate rises substantially Read the fine print

24

Credit AbuseIf you abuse your credit, it can have

lasting repercussions Repossession—collection of collateral by

the lender May not settle the debt if market value of asset

doesn’t cover amount of loan still outstanding Remaining debt is called deficiency judgment

Wage garnishment—a portion of borrower’s wages is paid directly to lender by the employer Requires a court order

25

Credit AbuseBankruptcy—borrower is relieved of debts, court

divides assets/income among creditors Action of last resort Virtually eliminates chances of securing future credit Over 1 million Americans file for bankruptcy each year

Most are voluntary filings Chapter 7: assets are seized by court and sold, funds are prorated

among creditors (after court costs/legal fees)—70% of bankruptcies Creditors usually receive only small percentage of what’s owed

Chapter 13: individuals establish a 3-year plan of debt repayment Debtor retains possession of property Creditors usually receive 60-70% of what’s owed

26

Credit AbuseBankruptcy doesn’t eliminate all forms of debt

Student loans Back taxes Child support Alimony

Bankruptcy shouldn’t be considered a ‘quick fix’ Remains on your credit record for 10 years Won’t get reasonable credit terms during that time May be difficult to rent an apartment, obtain car

insurance, etc.

27

Credit Counseling and Credit Repair Services

A credit counselor is a trained professional who helps you develop a budget and arrange a program of debt repayment Non-profit Consumer Credit Counseling Service

Funded by lenders and credit card companies (vested interest in repayment)

Credit Repair Doctors often claim they can ‘erase your bad credit’ Can’t deliver on their promises—don’t’ use

them