Embed Size (px)

Citation preview

Slide15-1

Copyright © 2011 by the McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

Chapter FifteenChapter FifteenLeasesLeases

2

Basic Lease Terms

A lease is an agreement in which A lease is an agreement in which the the lessorlessor conveys the right to conveys the right to

use property, plant, or use property, plant, or equipment, for a stated period of equipment, for a stated period of

time, to the time, to the lesseelessee..Lessor: Lessor:

Owner of Owner of propertyproperty

Lessor: Lessor: Owner of Owner of propertyproperty

Lessee: User of propertyLessee: User of propertyLessee: User of propertyLessee: User of property

3

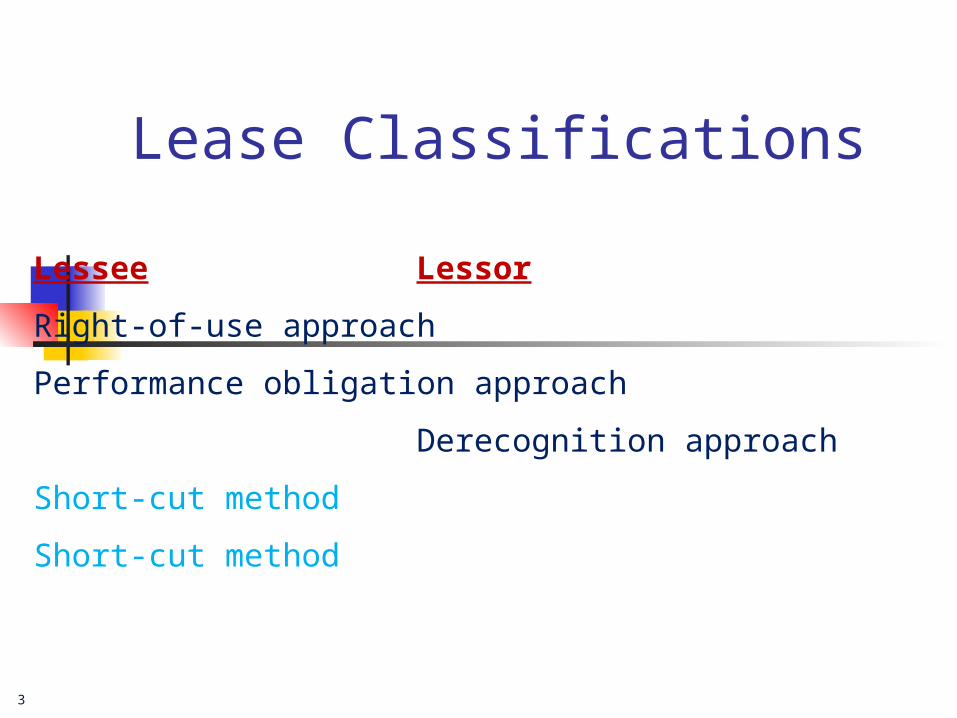

Lease Classifications

Lessee Lessor

Right-of-use approach Performance obligation

approach

Derecognition approach

Short-cut method Short-cut method

4

Illustration

On Jan. 1, 2011, Sans Serif Publishers leased printing equipment from First LeaseCorp who purchased the equipment from CompuDec Corporation for $479,079.

4 annual payments of $100,000 beginning Jan. 1, 2011, and at each Dec. 31 through 2013. Useful life of the equipment is 6 years. Lessor calculated payments using a rate of 10%.

Record the lease.

5

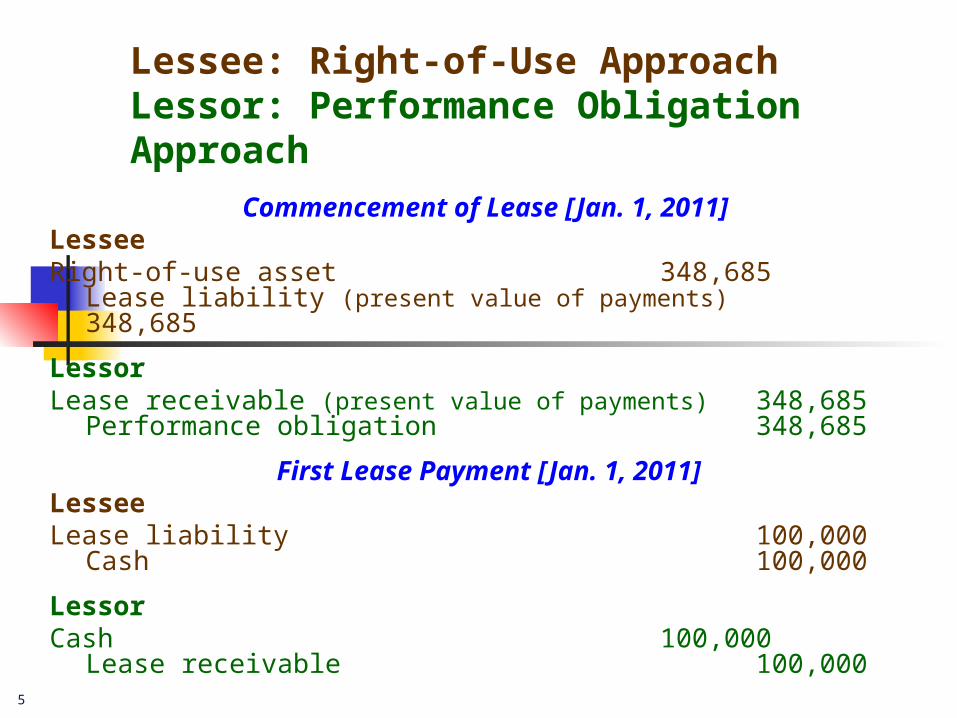

Lessee: Right-of-Use ApproachLessor: Performance Obligation Approach

Commencement of Lease [Jan. 1, 2011] LesseeRight-of-use asset 348,685

Lease liability (present value of payments) 348,685

LessorLease receivable (present value of payments) 348,685

Performance obligation 348,685

First Lease Payment [Jan. 1, 2011]LesseeLease liability 100,000

Cash 100,000

LessorCash 100,000

Lease receivable 100,000

6

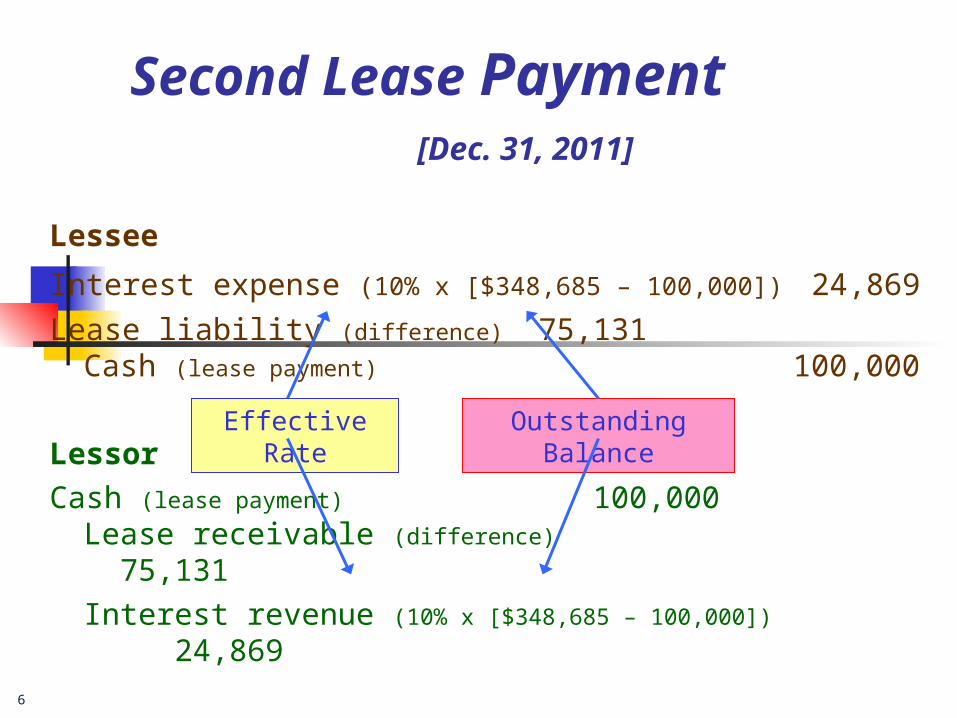

Second Lease Payment [Dec. 31, 2011]

Lessee

Interest expense (10% x [$348,685 – 100,000]) 24,869

Lease liability (difference) 75,131Cash (lease payment) 100,000

LessorCash (lease payment) 100,000

Lease receivable (difference) 75,131Interest revenue (10% x [$348,685 – 100,000])

24,869

Outstanding Balance

Effective Rate

7

LEASE AMORTIZATION SCHEDULE

Effective Decrease Outstanding

Payments Interest in Balance Balance 10% x Outstanding Balance

1/1/11 348,685

1/1/11 100,000 100,000 248,685

12/31/11 100,000 .10 (248,685) = 24,869 75,131 173,554

12/31/12 100,000 .10 (173,554) = 17,355 82,645 90,909

12/31/13 100,000 .10 (90,909) = 9,091 90,909 0 400,000 51,315 348,685

No interest yet; no time has passed.

8

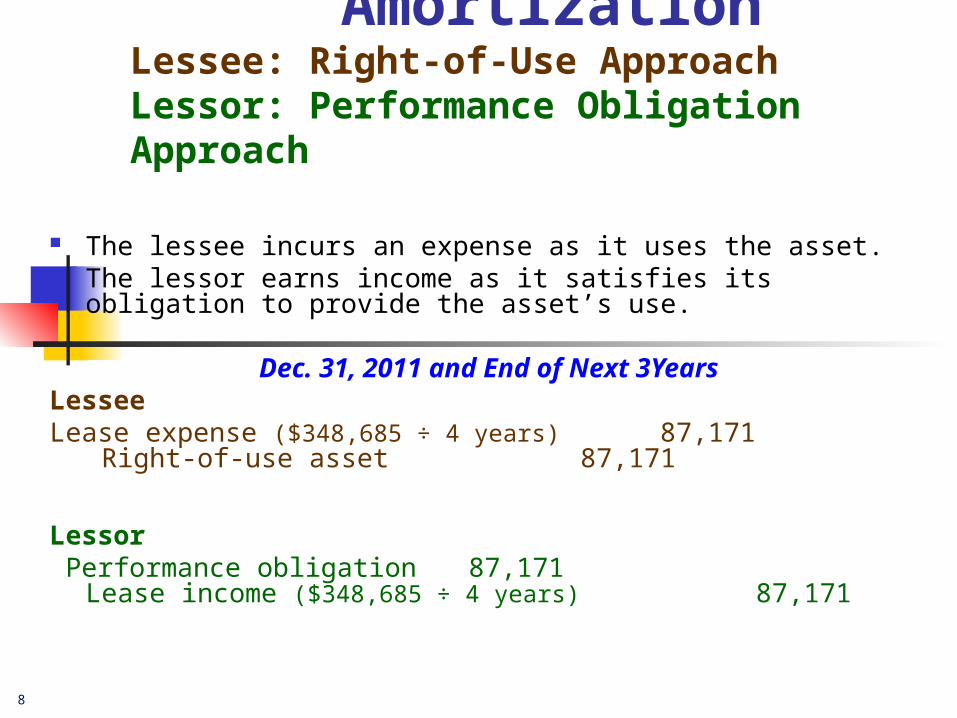

AmortizationLessee: Right-of-Use ApproachLessor: Performance Obligation Approach

The lessee incurs an expense as it uses the asset. The lessor earns income as it satisfies its obligation to provide

the asset’s use.

Dec. 31, 2011 and End of Next 3YearsLesseeLease expense ($348,685 ÷ 4 years) 87,171

Right-of-use asset 87,171

Lessor Performance obligation 87,171

Lease income ($348,685 ÷ 4 years) 87,171

9

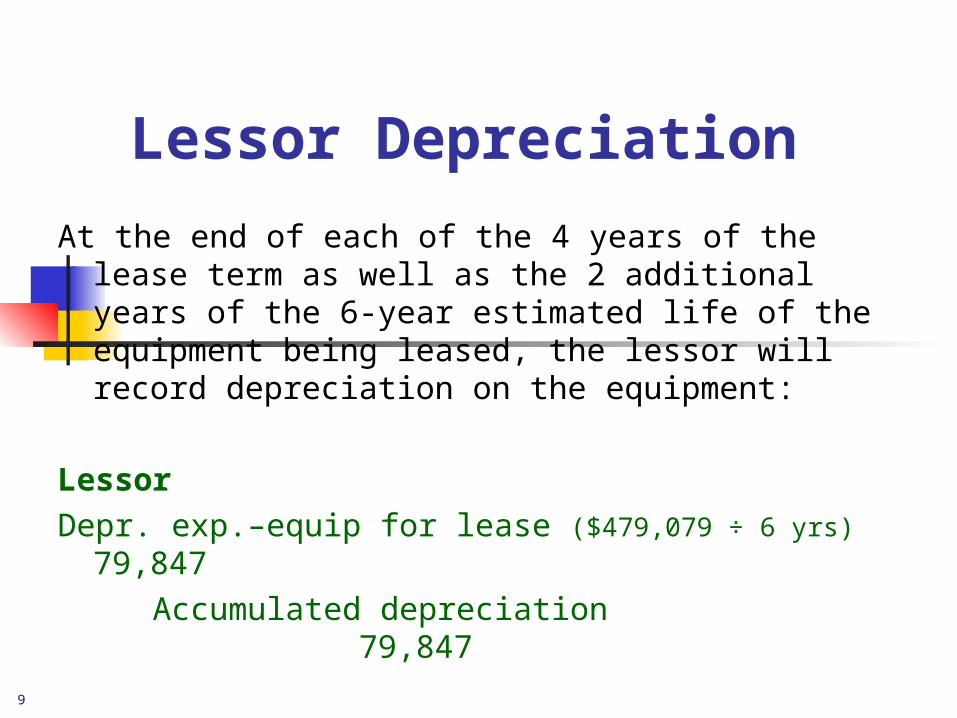

Lessor Depreciation

At the end of each of the 4 years of the lease term as well as the 2 additional years of the 6-year estimated life of the equipment being leased, the lessor will record depreciation on the equipment:

LessorDepr. exp.–equip for lease ($479,079 ÷ 6 yrs) 79,847 Accumulated depreciation

79,847

10

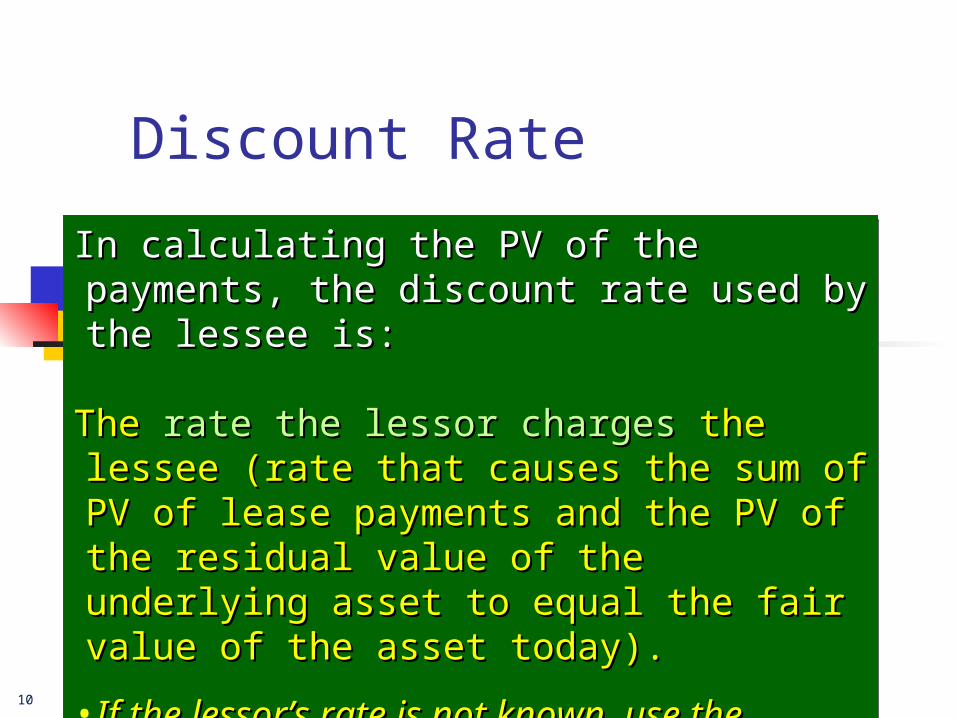

Discount Rate

In calculating the PV of the payments, the discount In calculating the PV of the payments, the discount rate used by the lessee is:rate used by the lessee is:

The The rate the lessor charges rate the lessor charges the lessee (rate that the lessee (rate that causes the sum of PV of lease payments and the PV causes the sum of PV of lease payments and the PV of the residual value of the underlying asset to equal of the residual value of the underlying asset to equal the fair value of the asset today).the fair value of the asset today).

•If the lessor’s rate is not known, use the lessee’s If the lessor’s rate is not known, use the lessee’s incremental borrowing rateincremental borrowing rate..

In calculating the PV of the payments, the discount In calculating the PV of the payments, the discount rate used by the lessee is:rate used by the lessee is:

The The rate the lessor charges rate the lessor charges the lessee (rate that the lessee (rate that causes the sum of PV of lease payments and the PV causes the sum of PV of lease payments and the PV of the residual value of the underlying asset to equal of the residual value of the underlying asset to equal the fair value of the asset today).the fair value of the asset today).

•If the lessor’s rate is not known, use the lessee’s If the lessor’s rate is not known, use the lessee’s incremental borrowing rateincremental borrowing rate..

11

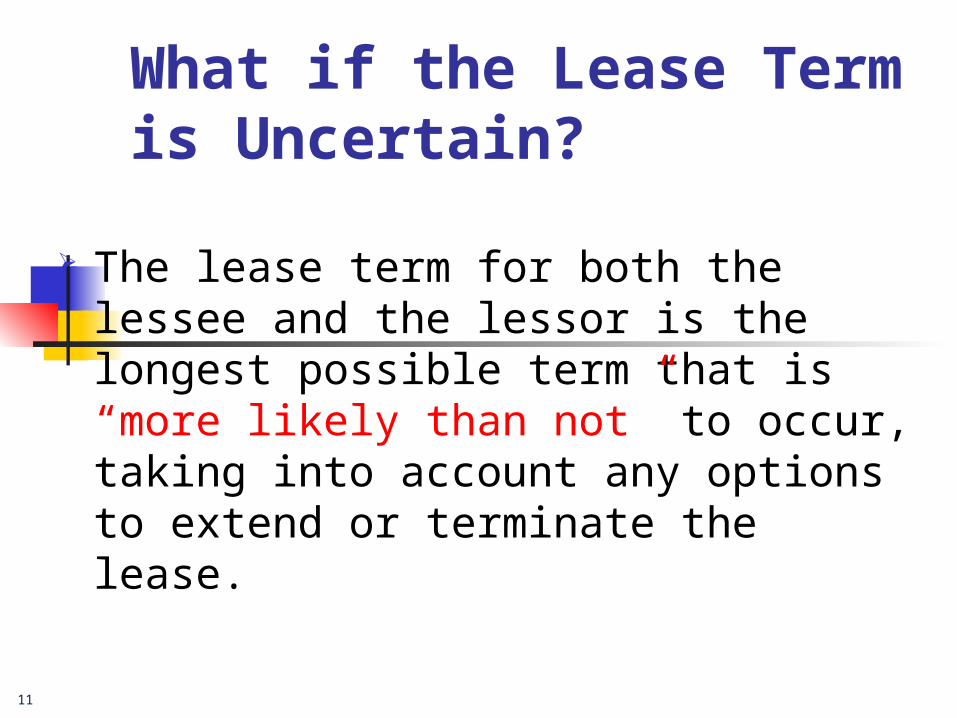

What if the Lease Term is Uncertain?

The lease term for both the lessee and the lessor is the longest possible term that is “more likely than not” to occur, taking into account any options to extend or terminate the lease.

12

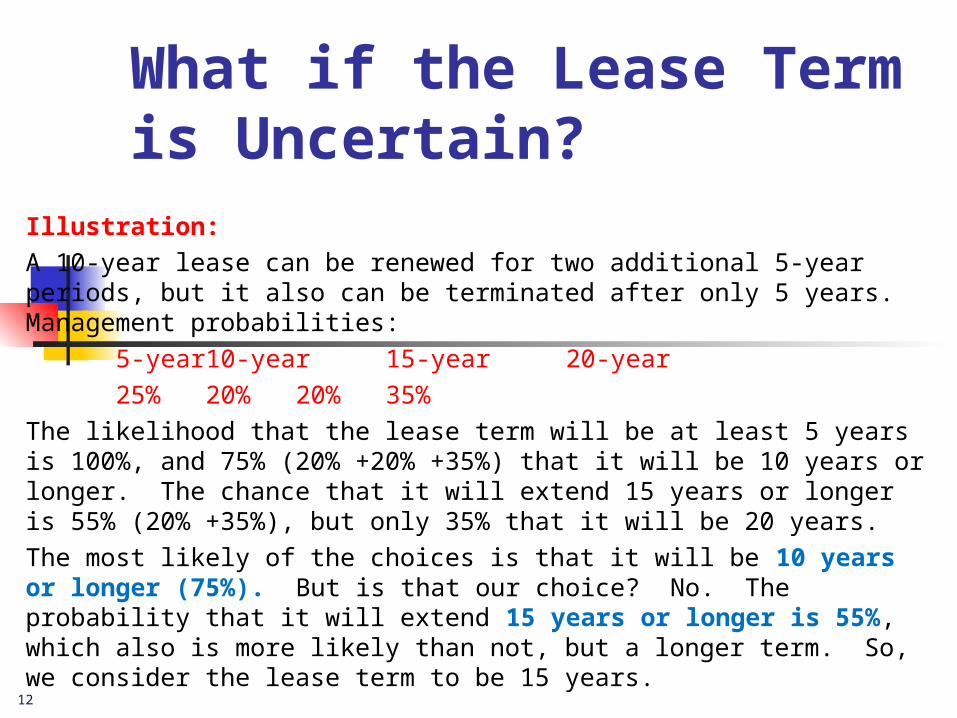

What if the Lease Term is Uncertain?

Illustration:A 10-year lease can be renewed for two additional 5-year periods, but it also can be terminated after only 5 years. Management probabilities:

5-year 10-year 15-year 20-year 25% 20% 20% 35%

The likelihood that the lease term will be at least 5 years is 100%, and 75% (20% +20% +35%) that it will be 10 years or longer. The chance that it will extend 15 years or longer is 55% (20% +35%), but only 35% that it will be 20 years. The most likely of the choices is that it will be 10 years or longer (75%). But is that our choice? No. The probability that it will extend 15 years or longer is 55%, which also is more likely than not, but a longer term. So, we consider the lease term to be 15 years.

13

What if the Lease Payments are Uncertain?

If the amounts of future lease payments are

uncertain due to contingencies or otherwise, we estimate the expected outcome of those payments.

The expected outcome is the PV of the probability-weighted average of the cash flows for a reasonable number of possible outcomes.

14

What if the Lease Payments are Uncertain?

Suppose the lease payments are

$100,000 each for four years, but that if the lessee’s net income exceeds a prespecified amount in the second year (40% likelihood), the payments the last two years will be $120,000 each.

15

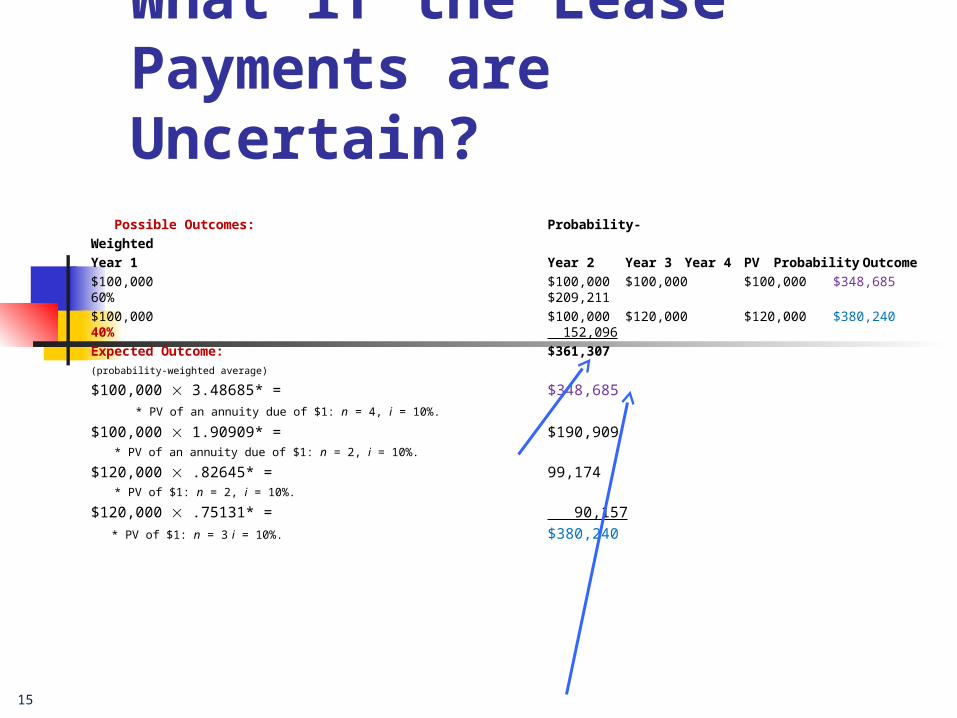

What if the Lease Payments are Uncertain?

Possible Outcomes: Probability-Weighted

Year 1 Year 2 Year 3 Year 4 PV ProbabilityOutcome$100,000 $100,000 $100,000 $100,000 $348,685

60% $209,211 $100,000 $100,000 $120,000 $120,000 $380,240

40% 152,096Expected Outcome: $361,307

(probability-weighted average)

$100,000 3.48685* = $348,685 * PV of an annuity due of $1: n = 4, i = 10%.

$100,000 1.90909* = $190,909 * PV of an annuity due of $1: n = 2, i = 10%.

$120,000 .82645* = 99,174 * PV of $1: n = 2, i = 10%.

$120,000 .75131* = 90,157 * PV of $1: n = 3 i = 10%. $380,240

16

Reassessing the Lease Term and the Expected Lease Payments

If circumstances later indicate that a significant change has occurred in the amounts measured for the lessee’s liability to make lease payments or the lessor’s right to receive lease payments, we should

Reevaluate the lease term and the expected amount of lease payments and

Make necessary adjustments.

17

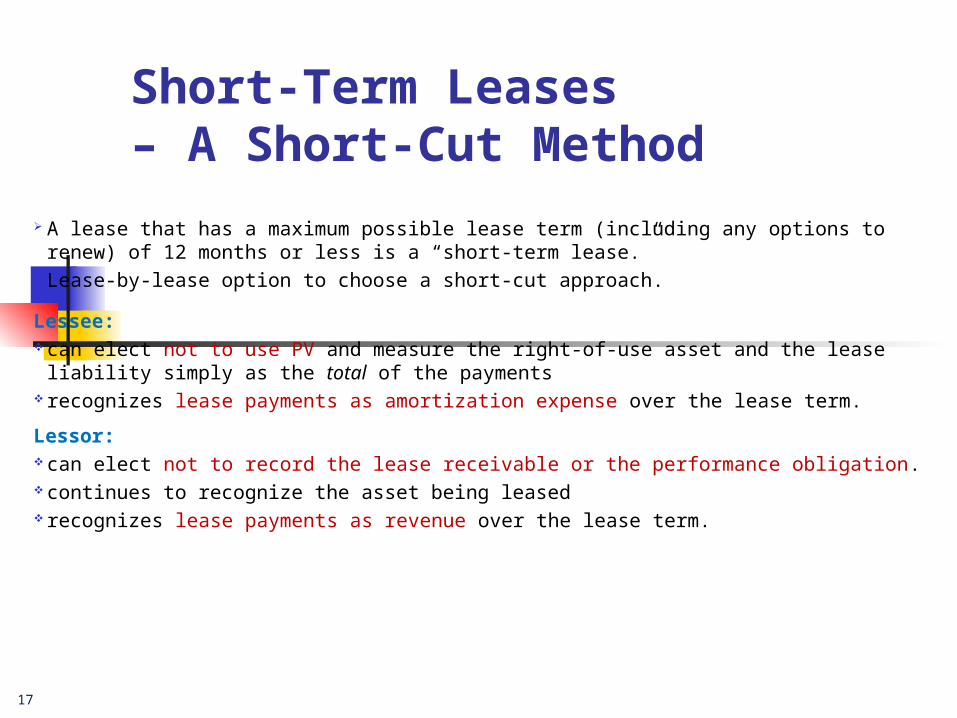

Short-Term Leases – A Short-Cut Method

A lease that has a maximum possible lease term (including any options to renew) of 12 months or less is a “short-term lease.”

Lease-by-lease option to choose a short-cut approach.

Lessee: can elect not to use PV and measure the right-of-use asset and the lease liability

simply as the total of the payments recognizes lease payments as amortization expense over the lease term.

Lessor: can elect not to record the lease receivable or the performance obligation. continues to recognize the asset being leased recognizes lease payments as revenue over the lease term.

18

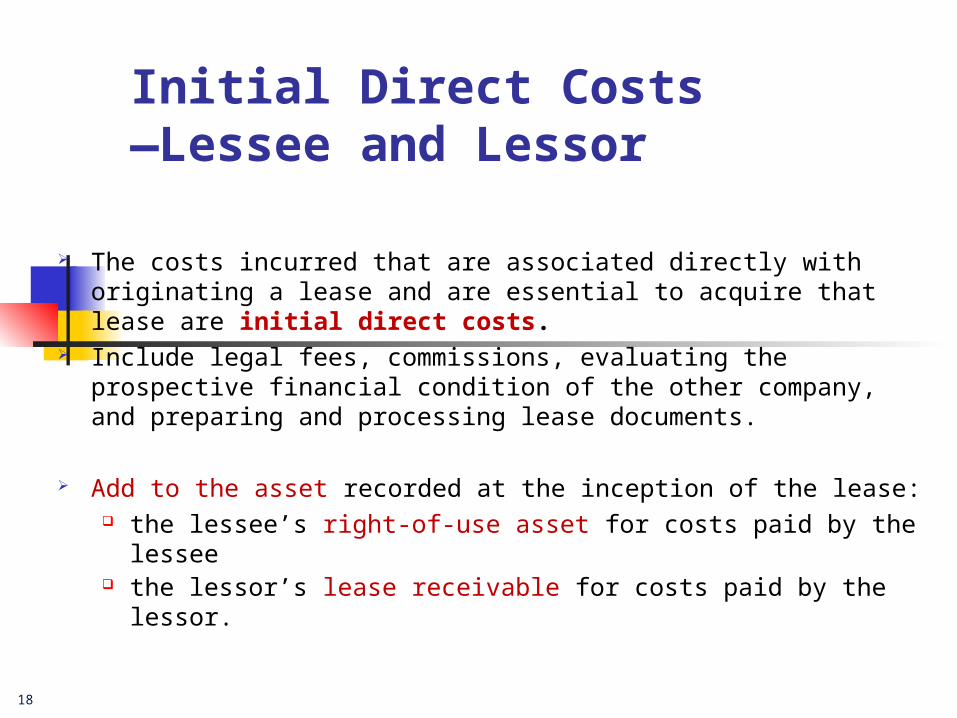

Initial Direct Costs—Lessee and Lessor

The costs incurred that are associated directly with

originating a lease and are essential to acquire that lease are initial direct costs.

Include legal fees, commissions, evaluating the prospective financial condition of the other company, and preparing and processing lease documents.

Add to the asset recorded at the inception of the lease: the lessee’s right-of-use asset for costs paid by the lessee the lessor’s lease receivable for costs paid by the lessor.

19

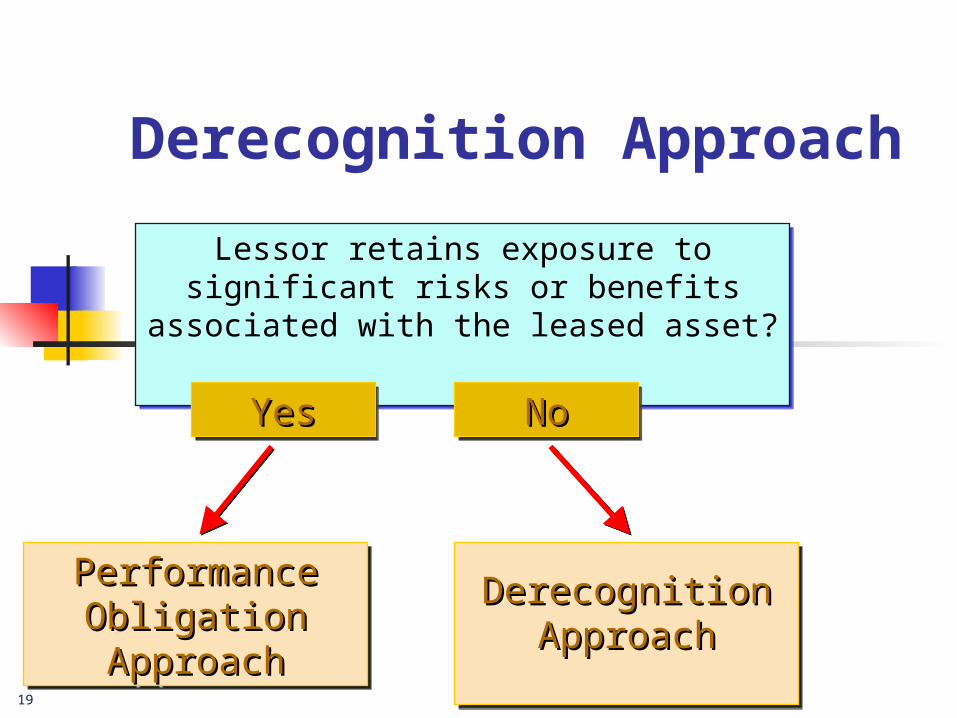

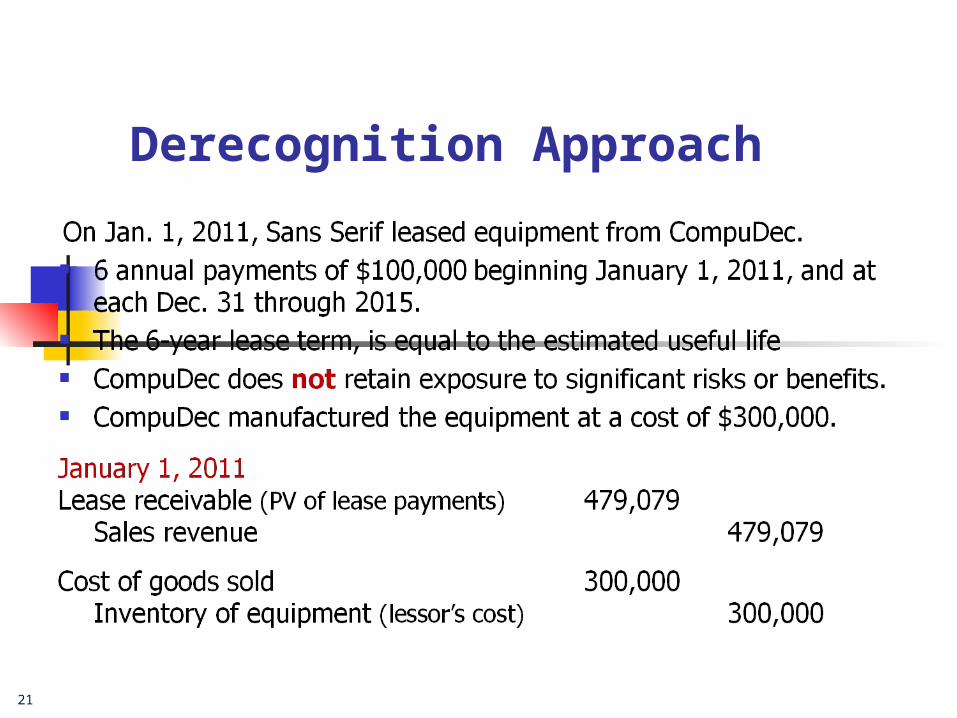

Derecognition Approach

Lessor retains exposure to significant risks or benefits associated with the

leased asset?

Lessor retains exposure to significant risks or benefits associated with the

leased asset?

Performance Performance Obligation Obligation ApproachApproach

Performance Performance Obligation Obligation ApproachApproach

DerecognitionDerecognitionApproachApproach

DerecognitionDerecognitionApproachApproach

YesYesYesYes NoNoNoNo

20

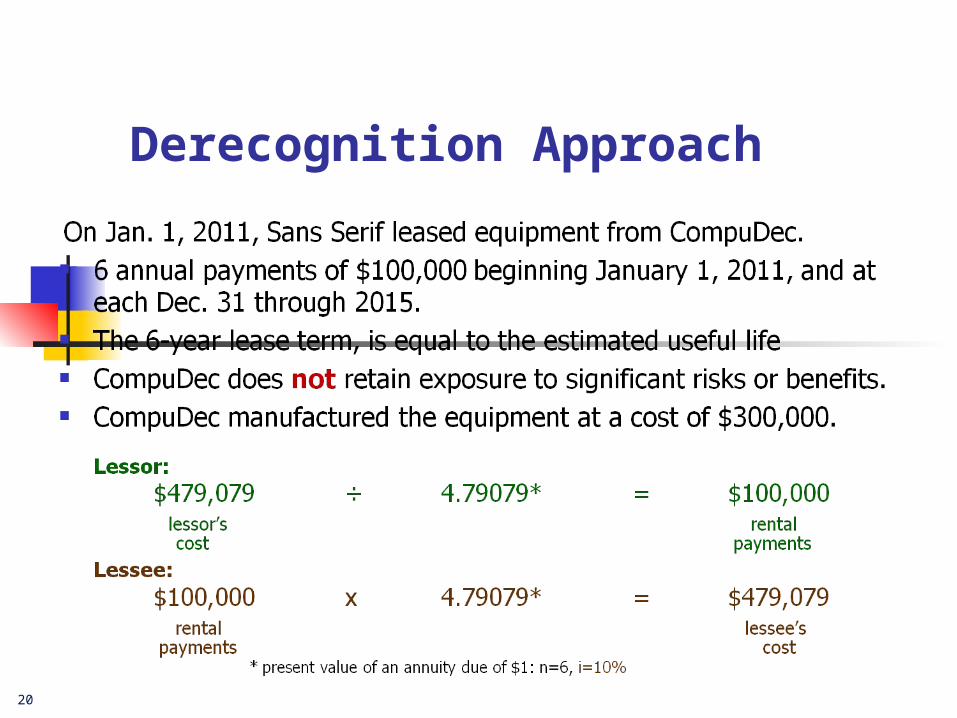

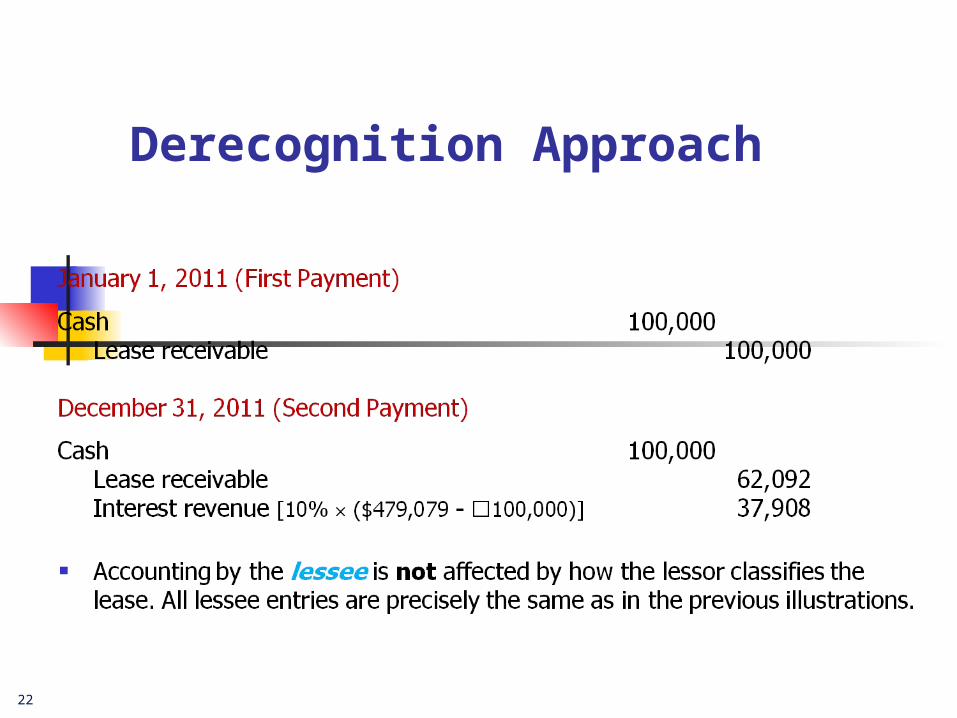

Derecognition Approach

21

Derecognition Approach

22

Derecognition Approach

23

If PV of Payments is Less than Asset's Fair Value

24

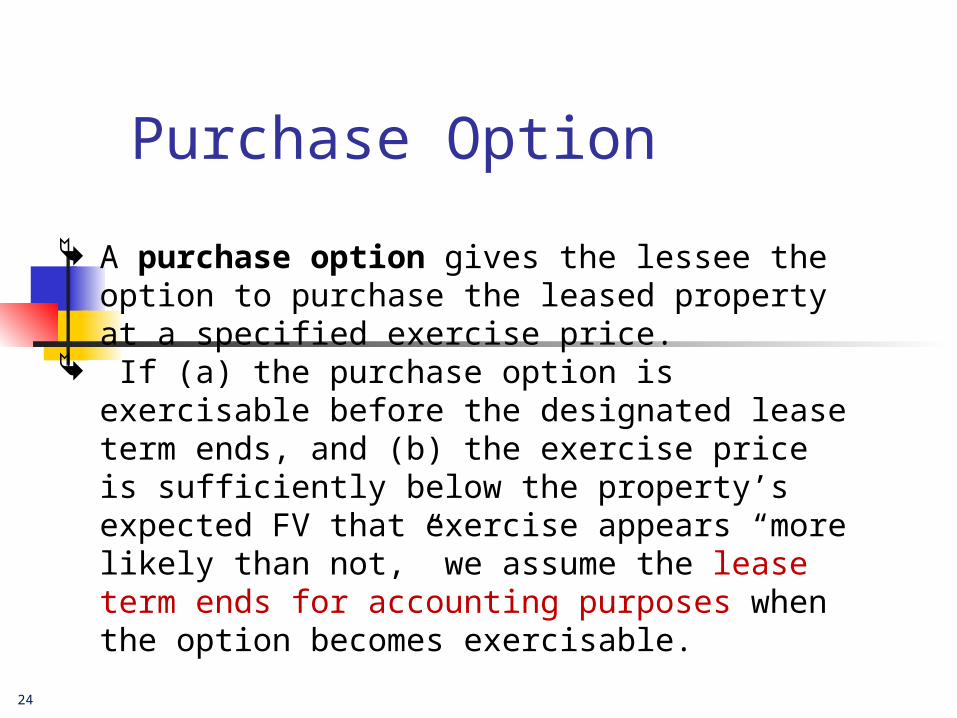

Purchase Option

A purchase option gives the lessee the option to purchase the leased property at a specified exercise price.

If (a) the purchase option is exercisable before the designated lease term ends, and (b) the exercise price is sufficiently below the property’s expected FV that exercise appears “more likely than not,” we assume the lease term ends for accounting purposes when the option becomes exercisable.

25

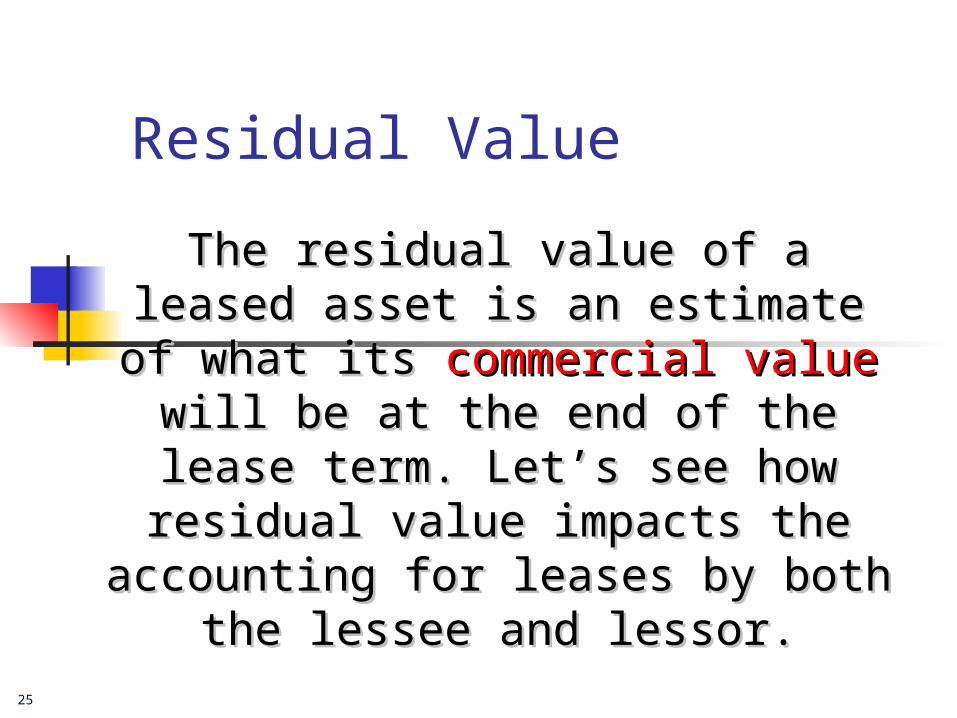

Residual Value

The residual value of a leased asset is an The residual value of a leased asset is an estimate of what its estimate of what its commercial valuecommercial value will will be at the end of the lease term. Let’s see be at the end of the lease term. Let’s see

how residual value impacts the accounting how residual value impacts the accounting for leases by both the lessee and lessor.for leases by both the lessee and lessor.

26

RESIDUAL VALUE At the end of the 4-year lease term the copier is

expected to be worth $191,000. Lessee guarantees a residual value of $241,000.

The excess guaranteed residual value ($50,000) is viewed as an additional cash flow and its PV is included:

PV of periodic payments ($100,000 3.48685*)$348,685

Plus: PV of the estimated payment under residual value guarantee ([$241,000 – 191,000] .68301†)

34,151PV of expected lease payments $382,836

† present value of $1: n=6, i=10%* present value of an annuity due of $1: n=6, i=10%

27

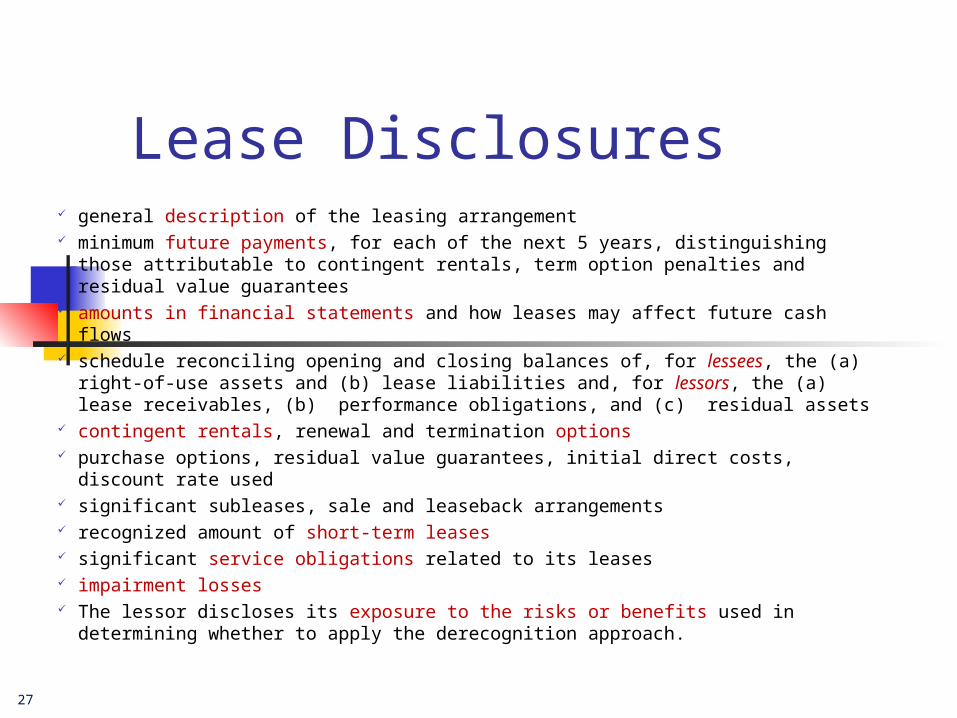

Lease Disclosures general description of the leasing arrangement minimum future payments, for each of the next 5 years, distinguishing those

attributable to contingent rentals, term option penalties and residual value guarantees

amounts in financial statements and how leases may affect future cash flows schedule reconciling opening and closing balances of, for lessees, the (a)

right-of-use assets and (b) lease liabilities and, for lessors, the (a) lease receivables, (b) performance obligations, and (c) residual assets

contingent rentals, renewal and termination options purchase options, residual value guarantees, initial direct costs, discount rate

used significant subleases, sale and leaseback arrangements recognized amount of short-term leases significant service obligations related to its leases impairment losses The lessor discloses its exposure to the risks or benefits used in determining

whether to apply the derecognition approach.

28

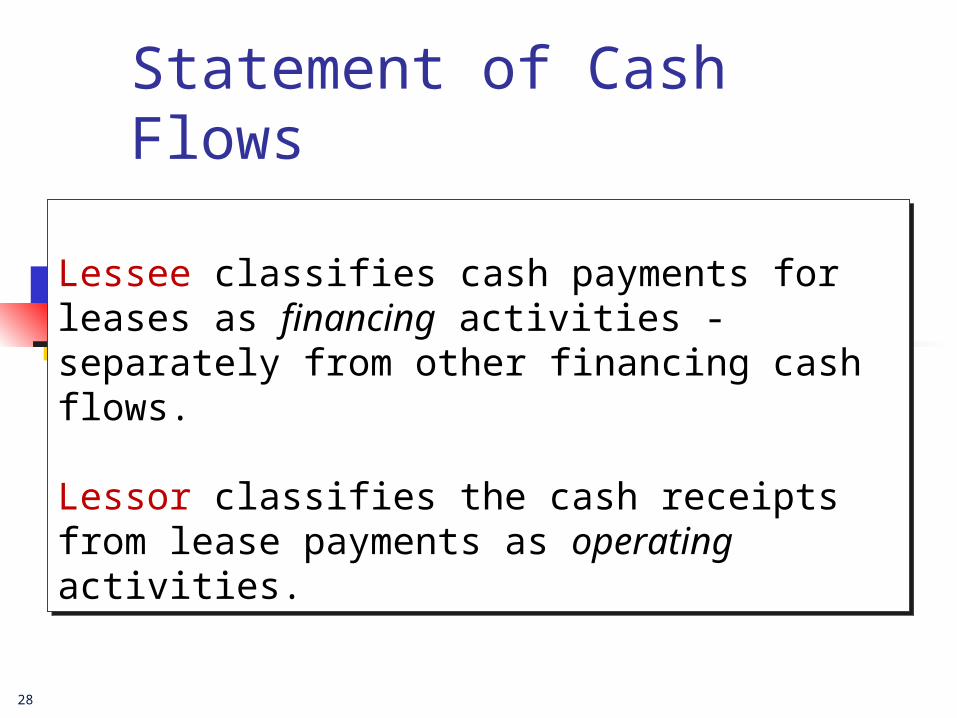

Statement of Cash Flows

Lessee classifies cash payments for leases as financing activities - separately from other financing cash flows.

Lessor classifies the cash receipts from lease payments as operating activities.

Lessee classifies cash payments for leases as financing activities - separately from other financing cash flows.

Lessor classifies the cash receipts from lease payments as operating activities.