Embed Size (px)

Citation preview

Size and Compositionof the Central Bank Balance Sheet:

Revisiting Japan’s Experienceof the Quantitative Easing Policy

Shigenori Shiratsuka

This paper reexamines Japan’s experience of the quantitative easingpolicy (QEP) in light of the policy responses against the recent financialand economic crisis. Central banks use various unconventional measuresin the range of financial assets being purchased and in the scale of suchpurchases. As the scope of such unconventional measures expands, it isoften emphasized that the U.S. Federal Reserve policy reactions focusmore on the asset side of its balance sheet, the so-called credit easing.By contrast, the Bank of Japan’s QEP from 2001 to 2006 set a tar-get for the current account balances, on the liability side of its balancesheet. It is crucial to understand that central banks combine the twoelements of their balance sheets, size and composition, to enhance theoverall effects of unconventional policy measures, given constraints onpolicy implementation.

Keywords: Quantitative easing; Credit easing; Unconventional monetarypolicy; Central bank balance sheet

JEL Classification: E44, E52, E58

Institute for Monetary and Economic Studies, Bank of Japan (E-mail: [email protected])

I benefited from the discussions with Shin-ichi Fukuda, Takatoshi Ito, Ken Kuttner, PhilippeMoutot, Kunio Okina, Huw Pill, Kazuo Ueda, Tsutomu Watanabe, the staff of the Bank of Japan(BOJ), and participants at the 2009 WEAI Annual Meeting in Vancouver, seminars at the Bankof England, the Federal Reserve Board, the Peterson Institute for International Economics, andthe workshops at the International Monetary Fund, and the Ministry of Finance of Japan. I alsothank Hiroyuki Ooi and Jouchi Nakajima for their assistance. The views expressed in the paperare my own and do not necessarily reflect those of the BOJ.

MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

DO NOT REPRINT OR REPRODUCE WITHOUT PERMISSION 79

I. Introduction

This paper reexamines Japan’s experience of the quantitative easing policy (QEP) inlight of policy responses to the recent financial and economic crisis in the major econ-omies.1 The paper thereby attempts to provide a roadmap for a more comprehensiveunderstanding of the unconventional monetary policy.

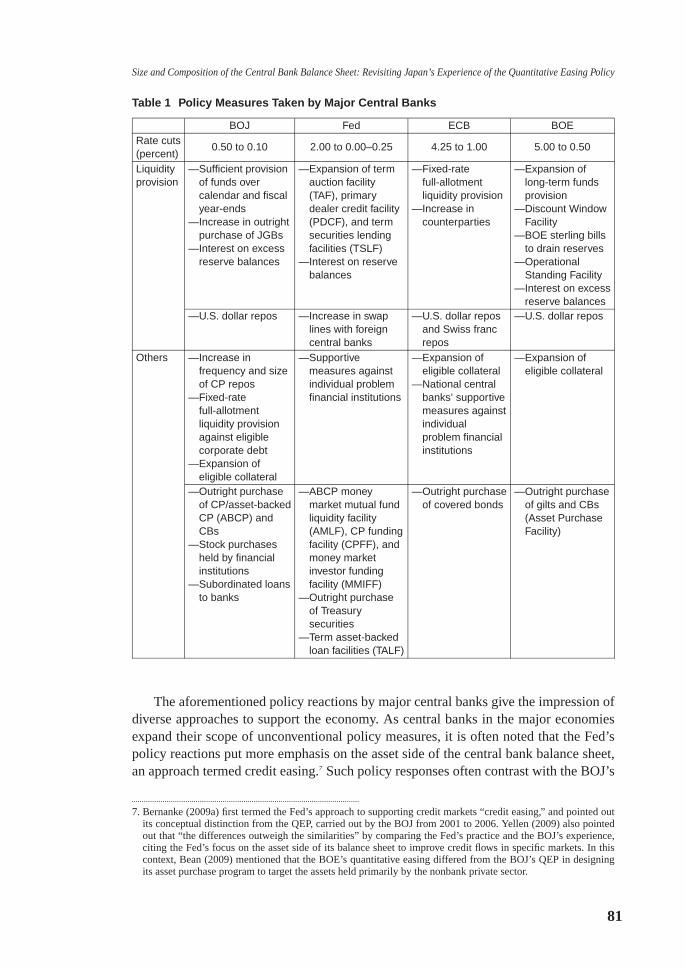

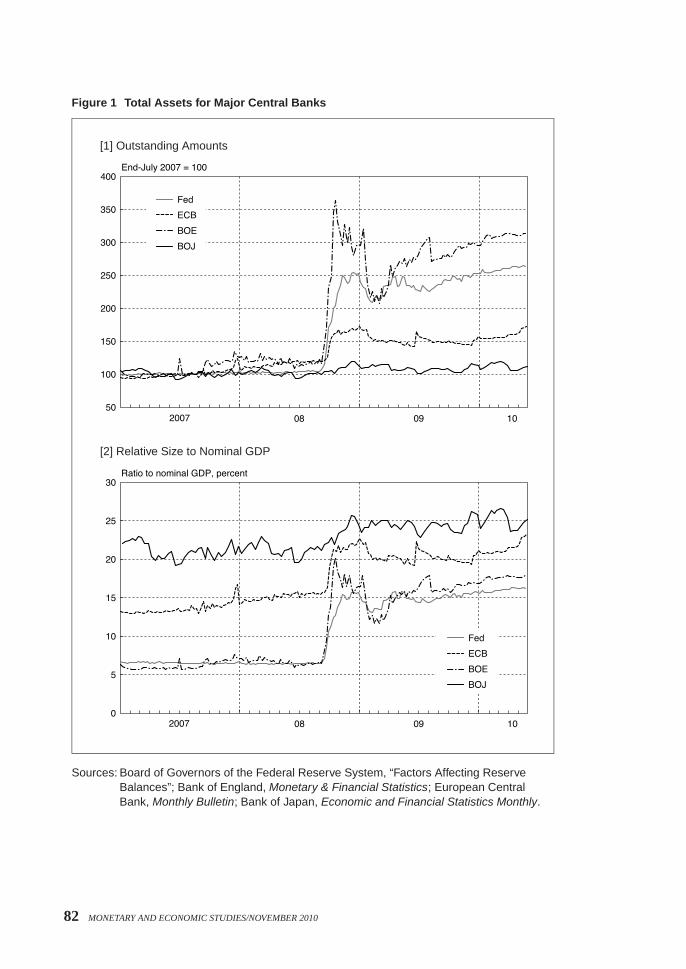

Confronted with the recent financial and economic crisis, central banks have movedswiftly and aggressively to counter the adverse effects of the malfunctioning financialsystem. In that process, they have implemented policy measures mainly in three majorareas: reducing the policy interest rate, securing the stability of financial markets, andfacilitating corporate financing.2 In the second and third areas, central banks in the majoreconomies have introduced various unconventional measures in the range of financialassets being purchased and in the scale of such purchases (Table 1). As a result, centralbanks in major economies have expanded their balance sheets significantly, especiallyafter the collapse of Lehman Brothers in September 2008 (Figure 1).3

The U.S. Federal Reserve has dramatically expanded its balance sheet through“credit easing” measures designed to intervene aggressively in the credit products mar-ket and related markets. The Bank of England (BOE) has established a program foroutright purchase of gilts and corporate bonds (CBs) to boost the supply of moneyand to improve the functioning of corporate credit markets.4 The European Cen-tral Bank (ECB) has extended its regular refinancing operations to “fixed-rate full-allotment” liquidity provisions with a longer maturity up to 12 months. It has alsointroduced a purchasing program for covered bonds.5 The Bank of Japan (BOJ) hasintroduced various measures to ensure stability in the financial markets as well as tofacilitate corporate financing, including fixed-rate full-allotment liquidity provisionsagainst eligible corporate debts. The BOJ has also resumed the purchase of stocksheld by financial institutions and introduced a scheme to provide subordinated loansto financial institutions.6

1. For the lessons from Japan’s experience since the bursting of the bubble in the early 1990s, see also a series ofspeeches by Shirakawa (2009a, c, e, f, 2010).

2. As private financial intermediation restores its normal function, many of the unconventional measures weregradually terminated. However, as the Greek debt crisis worsened, some unconventional measures were intro-duced again, such as foreign currency swap agreements between central banks and the purchases of euro areagovernment bonds by central bank members of the European Central Bank (ECB).

3. Looking at the situation in more detail, the balance sheets of the Bank of England (BOE) and the ECB startedincreasing gradually a bit earlier in the fall of 2007 and around the end of 2007, respectively.

4. The BOE uses the term of “quantitative easing” to describe its unconventional policy measures. For theoutline of its policy framework, see the BOE’s pamphlet, entitled Quantitative Easing Explained (http://www.bankofengland.co.uk/monetarypolicy/pdf/qe-pamphlet.pdf).

5. The ECB termed its unconventional policy measures “enhanced credit support.” See, for example, Trichet(2009a, b).

6. For more detailed information on the BOJ’s policy measures in the recent financial crisis, see the special webpage of the BOJ’s web site (http://www.boj.or.jp/en/type/exp/seisaku_cfc/index.htm). In implementing variousunconventional measures, the BOJ has emphasized the importance of acting as a safety valve for the financialsystem, given that the financial condition of Japanese financial institutions has been relatively stable even afterthe emergence of the U.S. subprime mortgage problem. Regarding the stability of Japan’s financial system, theBank of Japan (2009) concluded that “Japan’s financial system has generally been stable, although the effectsfrom the global financial crisis that began in 2008 still remain.”

80 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Table 1 Policy Measures Taken by Major Central Banks

BOJ Fed ECB BOERate cuts(percent)

0.50 to 0.10 2.00 to 0.00–0.25 4.25 to 1.00 5.00 to 0.50

Liquidityprovision

—Sufficient provisionof funds overcalendar and fiscalyear-ends

—Increase in outrightpurchase of JGBs

—Interest on excessreserve balances

—Expansion of termauction facility(TAF), primarydealer credit facility(PDCF), and termsecurities lendingfacilities (TSLF)

—Interest on reservebalances

—Fixed-ratefull-allotmentliquidity provision

—Increase incounterparties

—Expansion oflong-term fundsprovision

—Discount WindowFacility

—BOE sterling billsto drain reserves

—OperationalStanding Facility

—Interest on excessreserve balances

—U.S. dollar repos —Increase in swaplines with foreigncentral banks

—U.S. dollar reposand Swiss francrepos

—U.S. dollar repos

Others —Increase infrequency and sizeof CP repos

—Fixed-ratefull-allotmentliquidity provisionagainst eligiblecorporate debt

—Expansion ofeligible collateral

—Supportivemeasures againstindividual problemfinancial institutions

—Expansion ofeligible collateral

—National centralbanks’ supportivemeasures againstindividualproblem financialinstitutions

—Expansion ofeligible collateral

—Outright purchaseof CP/asset-backedCP (ABCP) andCBs

—Stock purchasesheld by financialinstitutions

—Subordinated loansto banks

—ABCP moneymarket mutual fundliquidity facility(AMLF), CP fundingfacility (CPFF), andmoney marketinvestor fundingfacility (MMIFF)

—Outright purchaseof Treasurysecurities

—Term asset-backedloan facilities (TALF)

—Outright purchaseof covered bonds

—Outright purchaseof gilts and CBs(Asset PurchaseFacility)

The aforementioned policy reactions by major central banks give the impression ofdiverse approaches to support the economy. As central banks in the major economiesexpand their scope of unconventional policy measures, it is often noted that the Fed’spolicy reactions put more emphasis on the asset side of the central bank balance sheet,an approach termed credit easing.7 Such policy responses often contrast with the BOJ’s

7. Bernanke (2009a) first termed the Fed’s approach to supporting credit markets “credit easing,” and pointed outits conceptual distinction from the QEP, carried out by the BOJ from 2001 to 2006. Yellen (2009) also pointedout that “the differences outweigh the similarities” by comparing the Fed’s practice and the BOJ’s experience,citing the Fed’s focus on the asset side of its balance sheet to improve credit flows in specific markets. In thiscontext, Bean (2009) mentioned that the BOE’s quantitative easing differed from the BOJ’s QEP in designingits asset purchase program to target the assets held primarily by the nonbank private sector.

81

Figure 1 Total Assets for Major Central Banks

[1] Outstanding Amounts

[2] Relative Size to Nominal GDP

Sources: Board of Governors of the Federal Reserve System, “Factors Affecting ReserveBalances”; Bank of England, Monetary & Financial Statistics; European CentralBank, Monthly Bulletin; Bank of Japan, Economic and Financial Statistics Monthly.

82 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

QEP from 2001 to 2006, setting a target for the current account balances (CABs), theliability side of its balance sheet.

The distinct difference arises not because central banks have different objectives,but because they face different environments and restrictions, such as the types andorigins of the shocks hitting the economy, the structure of the financial system, andinstitutional arrangements of the central bank. Viewed from a broad perspective, theresponses of various central banks demonstrate more similarities than differences.

Looking back at the BOJ’s policy responses after the burst of the bubble, especiallysince the late 1990s, we can find the striking similarities to the policy measures takenby central banks in the major economies.8 The BOJ provided ample excess reservesby using various tools for money market operations, including an increase in the out-right purchase of long-term government bonds. The BOJ also adopted credit-easingmeasures in the current terminology. The assets purchased included asset-backed secu-rities (ABSs) and asset-backed commercial paper (ABCP). In addition, the BOJ tookunprecedented measures to secure the stability of the financial system, including thepurchases of stocks held by financial institutions.

In theory, such unconventional monetary policy can be implemented by combiningthe two elements of the central bank balance sheet, size and composition, as discussedby Bernanke and Reinhart (2004). The size corresponds to expanding the balancesheet, while keeping its composition unchanged (narrowly defined quantitative easing).The composition corresponds to changing the composition of the balance sheet, whilekeeping its size unchanged by replacing conventional assets with unconventional assets(narrowly defined credit easing).

In a financial and economic crisis, both the asset and liability sides of the centralbank balance sheet play an important role in countering the adverse effects stemmingfrom the financial system. The asset side works as a substitute for private financial inter-mediation, for example, through the outright purchase of credit products. The liabilityside, especially expanded excess reserves, functions as a buffer for funding liquidity riskin the money markets. In addition, the two sides interact closely, since malfunctions infinancial intermediation are closely tied to funding liquidity risk at financial institutions,resulting in the increased demand for excess reserves.

In practice, given constraints on policy implementation, central banks have com-bined the two elements of their balance sheet, size, and composition, to enhance theoverall effects of unconventional policy. In this respect, quantitative easing, often usedin a vague manner, better fits as a package of unconventional policy measures makinguse of both the asset and liability sides of the central bank balance sheet, designed toabsorb the shocks hitting the economy (broadly defined quantitative easing). The BOJ’sQEP from 2001 to 2006 can be viewed as broadly defined quantitative easing, as partof the policy responses of central banks to the recent financial and economic crisis.

8. Shirakawa (2009a, c) also points out the striking similarities between the policy measures taken by the BOJsince the late 1990s and those taken by central banks in the major economies. We also find some differences atthe same time, especially in the employment of a policy commitment. The BOJ made a commitment to the QEP“until core CPI inflation becomes stably zero or above.” In the recent crisis, however, quite a few central banks,such as the Bank of Canada and Sveriges Riksbank, have employed policy commitment.

83

Such a way of understanding unconventional policy measures suggests a close con-nection with a policy commitment regarding the duration for maintaining short-terminterest rates at virtually zero, since financial and economic circumstances that requireunconventional policy measures are most likely to accompany an extremely low levelof policy interest rates for a considerable period into the future. In this sense, it isinappropriate to consider that unconventional policy measures and policy commitmentunder zero interest rates are completely separated policy measures.

This paper is organized as follows. Section II summarizes Japan’s experience of theQEP from 2001 to 2006. Section III examines the role of the central bank balance sheetunder unconventional monetary policy, by focusing on the link between the two sides ofthe balance sheet. Section IV addresses some questions regarding the implementationof unconventional monetary policy. Section V provides concluding remarks.

II. The BOJ’s QEP from 2001 to 2006

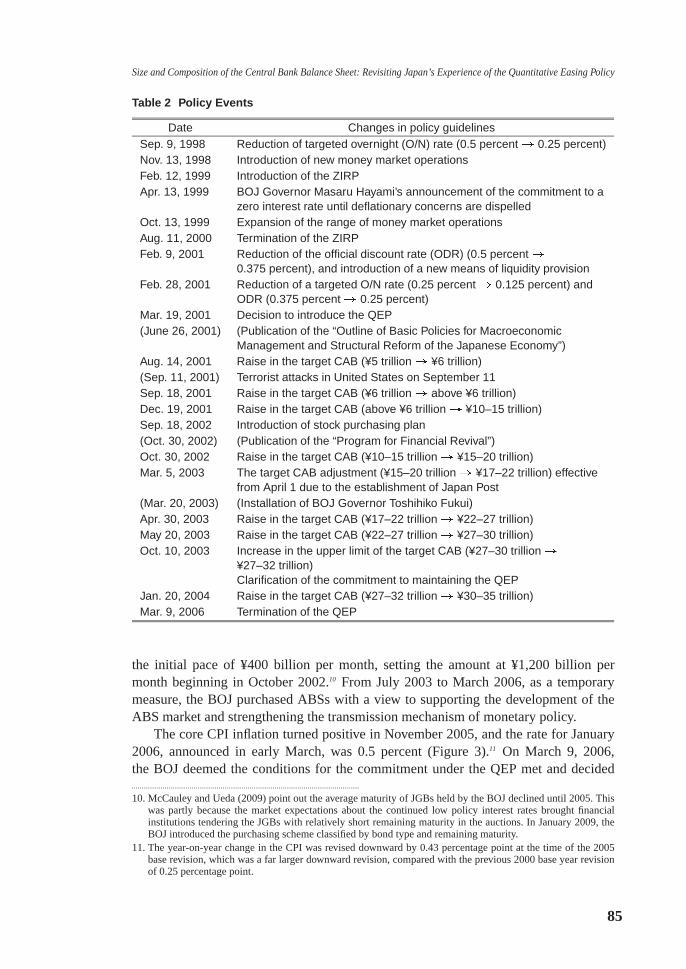

This section reviews Japan’s experience of the QEP and summarizes its effects mainlyon financial markets (see Table 2 for the major policy events under the QEP).

A. Basic Framework of the BOJ’s QEPOn March 19, 2001, the BOJ adopted a new monetary easing framework of the QEP inresponse to an economic downturn triggered by the burst of the global IT bubble. TheQEP consisted of three pillars:

(1) The BOJ changed its main operating target for money market operations fromthe uncollateralized overnight call rate to the outstanding balance of the CABsheld by financial institutions at the BOJ.

(2) The BOJ committed itself to maintaining the above procedure until the coreconsumer price index (CPI, headline excluding perishables) inflation becamestably zero or above.9

(3) The BOJ would increase the amount at the outright purchase of long-termJapanese government bonds (JGBs), up to a ceiling of the outstanding bal-ance of banknotes issued, if judged necessary to ensure the smooth provisionof liquidity.

The QEP started with a CAB target at ¥5 trillion, a level slightly above the requiredreserve level of ¥4 trillion (Figure 2). The target was then progressively increased inresponse to the decline in economic activity. The target was finally raised to ¥30–35trillion in January 2004, and remained unchanged at that level until the QEP wasterminated in March 2006.

Reflecting the ample liquidity provision under the QEP, the uncollateralized over-night call rate fell to 0.001 percent, a level below the 0.02–0.03 percent in place from1999 to 2000 under the zero interest rate policy (ZIRP). To meet the CAB targetsmoothly, the BOJ gradually increased the outright purchase of long-term JGBs from

9. The BOJ clarified its commitment to maintaining the QEP in October 2003. First, it requires not only that themost recently published core CPI should register zero percent or above, but also that such a tendency should beconfirmed over a few months. Second, the BOJ needs to be convinced that the prospective core CPI will not beexpected to fall below zero.

84 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Table 2 Policy Events

Date Changes in policy guidelinesSep. 9, 1998 Reduction of targeted overnight (O/N) rate (0.5 percent� 0.25 percent)Nov. 13, 1998 Introduction of new money market operationsFeb. 12, 1999 Introduction of the ZIRPApr. 13, 1999 BOJ Governor Masaru Hayami’s announcement of the commitment to a

zero interest rate until deflationary concerns are dispelledOct. 13, 1999 Expansion of the range of money market operationsAug. 11, 2000 Termination of the ZIRPFeb. 9, 2001 Reduction of the official discount rate (ODR) (0.5 percent�

0.375 percent), and introduction of a new means of liquidity provisionFeb. 28, 2001 Reduction of a targeted O/N rate (0.25 percent� 0.125 percent) and

ODR (0.375 percent� 0.25 percent)Mar. 19, 2001 Decision to introduce the QEP(June 26, 2001) (Publication of the “Outline of Basic Policies for Macroeconomic

Management and Structural Reform of the Japanese Economy”)Aug. 14, 2001 Raise in the target CAB (¥5 trillion� ¥6 trillion)(Sep. 11, 2001) Terrorist attacks in United States on September 11Sep. 18, 2001 Raise in the target CAB (¥6 trillion� above ¥6 trillion)Dec. 19, 2001 Raise in the target CAB (above ¥6 trillion� ¥10–15 trillion)Sep. 18, 2002 Introduction of stock purchasing plan(Oct. 30, 2002) (Publication of the “Program for Financial Revival”)Oct. 30, 2002 Raise in the target CAB (¥10–15 trillion� ¥15–20 trillion)Mar. 5, 2003 The target CAB adjustment (¥15–20 trillion� ¥17–22 trillion) effective

from April 1 due to the establishment of Japan Post(Mar. 20, 2003) (Installation of BOJ Governor Toshihiko Fukui)Apr. 30, 2003 Raise in the target CAB (¥17–22 trillion� ¥22–27 trillion)May 20, 2003 Raise in the target CAB (¥22–27 trillion� ¥27–30 trillion)Oct. 10, 2003 Increase in the upper limit of the target CAB (¥27–30 trillion�

¥27–32 trillion)Clarification of the commitment to maintaining the QEP

Jan. 20, 2004 Raise in the target CAB (¥27–32 trillion� ¥30–35 trillion)Mar. 9, 2006 Termination of the QEP

the initial pace of ¥400 billion per month, setting the amount at ¥1,200 billion permonth beginning in October 2002.10 From July 2003 to March 2006, as a temporarymeasure, the BOJ purchased ABSs with a view to supporting the development of theABS market and strengthening the transmission mechanism of monetary policy.

The core CPI inflation turned positive in November 2005, and the rate for January2006, announced in early March, was 0.5 percent (Figure 3).11 On March 9, 2006,the BOJ deemed the conditions for the commitment under the QEP met and decided

10. McCauley and Ueda (2009) point out the average maturity of JGBs held by the BOJ declined until 2005. Thiswas partly because the market expectations about the continued low policy interest rates brought financialinstitutions tendering the JGBs with relatively short remaining maturity in the auctions. In January 2009, theBOJ introduced the purchasing scheme classified by bond type and remaining maturity.

11. The year-on-year change in the CPI was revised downward by 0.43 percentage point at the time of the 2005base revision, which was a far larger downward revision, compared with the previous 2000 base year revisionof 0.25 percentage point.

85

Figure 2 Current Account Balances at the BOJ

Note: Solid line indicates the outstanding amounts of the current account balances at theBOJ, and shaded lines indicate the ceiling and floor of the target range of the currentaccount balances.

Source: Bank of Japan, Economic and Financial Statistics Monthly.

Figure 3 Core Inflation

Note: Core inflation is an indicator that excludes the impacts of perishable food prices from theheadline indicator.

Source: Ministry of Internal Affairs and Communications, Consumer Price Index.

86 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

to terminate the QEP and to return the operating target of money market operationsto the uncollateralized overnight call rate, while maintaining the rate at effectivelyzero percent.

When terminating the QEP, the BOJ announced that the CABs would be reducedover a period of a several months, fully taking into account conditions in the short-termmoney market. The reductions in the CABs proceeded smoothly as scheduled in a fewmonths before the first policy rate increase in July 2006.12 The BOJ’s communicationefforts to convey its policy intention played a key role in several respects. First, theconditions for the commitment to the QEP enhanced the predictability of the timingof the termination of the QEP. Second, in the face of market expectations regardingthe termination of the QEP, the BOJ repeatedly explained that the termination itselfwould entail no sudden policy changes and that the policy rates would be adjusted onlygradually. Third, the BOJ encouraged financial institutions to prepare for a decline inexcess reserves by reestablishing the management system for funding liquidity risk.13

B. Effects of the BOJ’s QEPThis subsection summarizes the effects of the QEP by focusing on financial markets,since empirical evidence suggests that the expansion of the monetary base had limitedeffects on aggregate variables, such as output and inflation. Ugai (2007) concludes in hiscomprehensive survey on empirical studies on the effects of the QEP that the effect ofexpanding the monetary base and altering the composition of the BOJ’s balance sheet,if any, is generally smaller than that stemming from the policy commitment.14

Given the fragile state of the financial markets, the ample provision of reservesunder the QEP, coupled with the policy commitment of maintaining zero interest ratesfor a considerable period into the future, resulted in the strong liquidity effect. Okinaand Shiratsuka (2004a) empirically examined the effects of policy commitment on themarket expectations, implied in the changes in the shape of yield curves, the so-calledpolicy duration effect. They showed that the policy duration effect was highly effectivein stabilizing market expectations regarding the future path of short-term interest rates,thereby bringing longer-term interest rates down to flatten the yield curve.15 They alsoconcluded that the policy duration effect failed to reverse deflationary expectations infinancial markets, since monetary policy alone could not reverse deflation, coupled withlow economic growth.

12. As a basis for the smooth exit from the QEP, the restoration of stability in Japan’s financial system is crucial.In fact, the blanket protection on bank deposits was lifted without confusion in April 2005.

13. In that connection, the maturity of the short-term funds-supplying operation shortened in advance of the termi-nation of the QEP, from the second half of 2005. That was because the BOJ tried to minimize the interventionin the money markets, thereby promoting restoration of their functioning, including smoother formation ofinterest rates on term transactions.

14. In that context, Ito and Mishkin (2006), for example, argued that the BOJ’s policy responses were notsufficiently aggressive to fight deflation and, in addition, that skepticism at the BOJ as to the effectivenessof unconventional policy measures did undermine their effects. By contrast, Ueda (2005) recollected thatmajor misconceptions about the BOJ’s policy measures arose outside of the BOJ, including among academiceconomists, leading to bold arguments for using extreme measures to overcome deflationary economic condi-tions, without recognizing the similarity of the BOJ’s policy measures under the ZIRP and the QEP with policymeasures advocated by academic economists.

15. Oda and Ueda (2007) carried out a counterfactual simulation, based on their estimated macro-finance model,and showed that the policy commitment under the ZIRP and the QEP stabilized market expectations regardingthe future course of short-term interest rates at a low level, thus pushing down the yield curve.

87

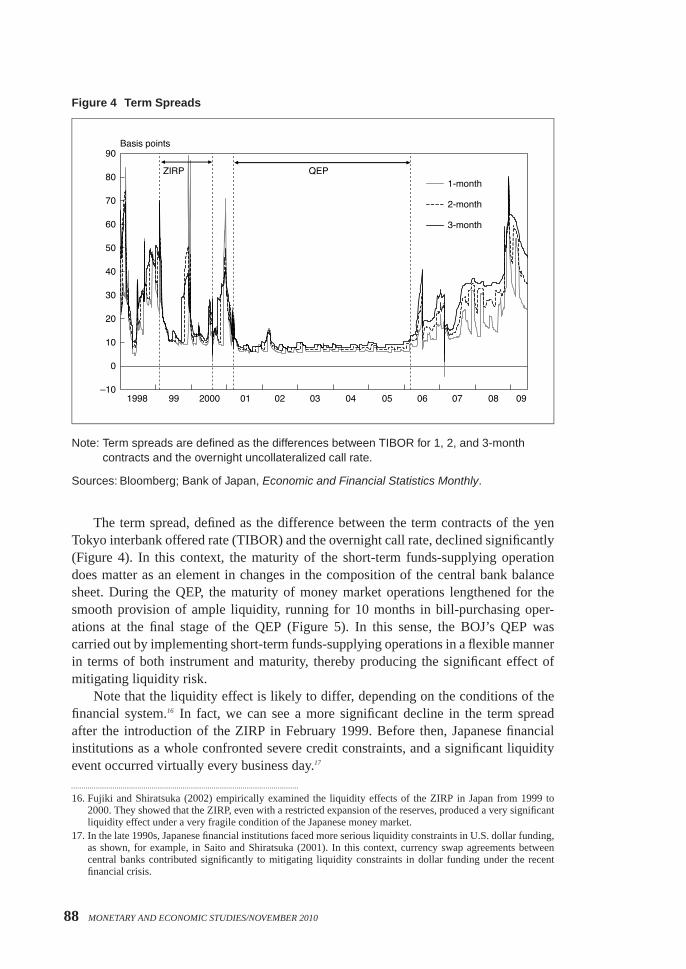

Figure 4 Term Spreads

Note: Term spreads are defined as the differences between TIBOR for 1, 2, and 3-monthcontracts and the overnight uncollateralized call rate.

Sources: Bloomberg; Bank of Japan, Economic and Financial Statistics Monthly.

The term spread, defined as the difference between the term contracts of the yenTokyo interbank offered rate (TIBOR) and the overnight call rate, declined significantly(Figure 4). In this context, the maturity of the short-term funds-supplying operationdoes matter as an element in changes in the composition of the central bank balancesheet. During the QEP, the maturity of money market operations lengthened for thesmooth provision of ample liquidity, running for 10 months in bill-purchasing oper-ations at the final stage of the QEP (Figure 5). In this sense, the BOJ’s QEP wascarried out by implementing short-term funds-supplying operations in a flexible mannerin terms of both instrument and maturity, thereby producing the significant effect ofmitigating liquidity risk.

Note that the liquidity effect is likely to differ, depending on the conditions of thefinancial system.16 In fact, we can see a more significant decline in the term spreadafter the introduction of the ZIRP in February 1999. Before then, Japanese financialinstitutions as a whole confronted severe credit constraints, and a significant liquidityevent occurred virtually every business day.17

16. Fujiki and Shiratsuka (2002) empirically examined the liquidity effects of the ZIRP in Japan from 1999 to2000. They showed that the ZIRP, even with a restricted expansion of the reserves, produced a very significantliquidity effect under a very fragile condition of the Japanese money market.

17. In the late 1990s, Japanese financial institutions faced more serious liquidity constraints in U.S. dollar funding,as shown, for example, in Saito and Shiratsuka (2001). In this context, currency swap agreements betweencentral banks contributed significantly to mitigating liquidity constraints in dollar funding under the recentfinancial crisis.

88 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Figure 5 Maturity of Short-Term Funds-Supplying Operations

Notes: Figures are weighted-average maturities of short-term funds-supplying operationsoffered during each quarter. The amounts of funds supplied are used as the weight.Short-term funds-supplying operations include (1) funds-supplying operations againstpooled collateral (bill-purchasing operations until June 2006), (2) purchase of Japanesegovernment securities with repurchase agreements, and (3) purchases of CP withrepurchase agreements.

Source: Bank of Japan, Economic and Financial Statistics Monthly.

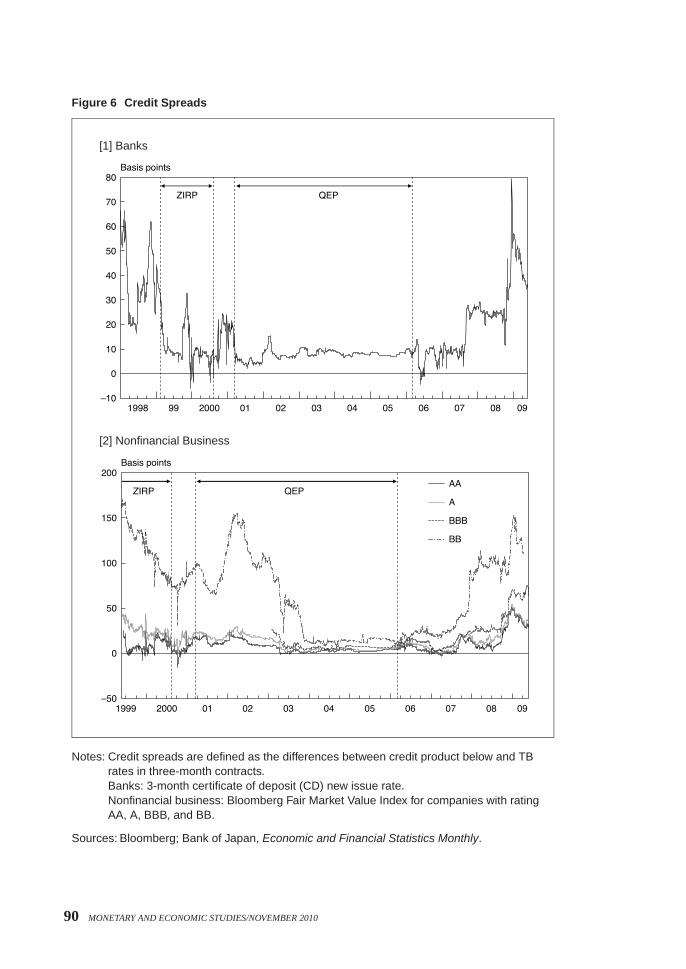

Additionally, the QEP influenced credit spreads significantly (Figure 6).18 Thecredit spread for financial institutions, measured as the difference between the rate oncertificates of deposit and the rate on Treasury bills (TBs) in three-month contracts, ap-pears to have declined sharply soon after the introduction of the QEP. The credit spreadsfor nonfinancial businesses, measured as the differences between the credit product in-dicators across ratings and the TB rate in three-month contracts, also declined, but withcertain time lags after the introduction of the QEP, indicating a significant reductionin the external financing premium for the nonfinancial business sector. It should benoted that such a significant reduction in the external financing premium was realizedby lesser amounts of direct intervention in credit product markets (Figure 7).19

18. See, for example, Baba et al. (2006) for empirical evidence of reduction in credit spreads for Japanese financialinstitutions in money markets.

19. Under the recent financial crisis, the Fed’s large-scale asset purchase program also reduced credit spreadsin mortgage-backed securities significantly, but it is difficult to tell whether such a reduction in spreads wasproduced by the size of asset purchases or their announcement, as with empirical evidence currently available.For example, Gagnon et al. (2010) point out that the purchases result in significant and long-lasting reductionsin premiums in a wide range of securities, including those not directly targeted by the program, while Stroebeland Taylor (2009) indicate that the announcement of the purchase, not the size of the purchases, significantlyreduces premiums.

89

Figure 6 Credit Spreads

[1] Banks

[2] Nonfinancial Business

Notes: Credit spreads are defined as the differences between credit product below and TBrates in three-month contracts.Banks: 3-month certificate of deposit (CD) new issue rate.Nonfinancial business: Bloomberg Fair Market Value Index for companies with ratingAA, A, BBB, and BB.

Sources: Bloomberg; Bank of Japan, Economic and Financial Statistics Monthly.

90 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Figure 7 CP Market

Source: Bank of Japan, Economic and Financial Statistics Monthly.

As examined so far, the QEP played a certain role in bolstering Japan’s economy,in particular by stabilizing the financial system.20 Such stimulative effects failed tobe transmitted outside the financial system, however, suggesting that the transmissionchannel between the financial and nonfinancial sectors had been blocked.21 The QEPthus did not produce the effect of reversing the financial market’s expectations thatdeflation would persist, as discussed in Okina and Shiratsuka (2004a).

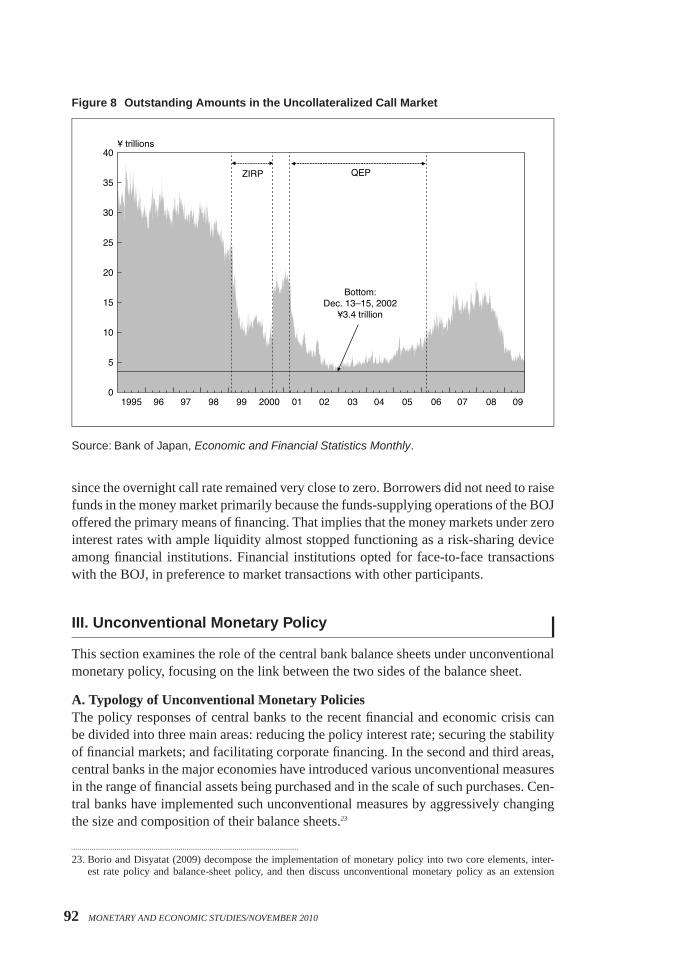

At the same time, the QEP produced certain side effects, particularly stemmingfrom pushing short-term interest rates down to virtually zero, evident as a deteriorationin the functioning of the money markets.22 That is clearly visible in the sharp declinein the outstanding amounts of the uncollateralized call market: from around ¥20 tril-lion in early 2001 to ¥3.4 trillion in December 2002 (Figure 8). Such a decline in theoutstanding amount of the uncollateralized call market was not significantly reversedin 2004–05, even after Japan’s financial system restored its stability as a whole, byresolving the nonperforming-loan problem.

Under the QEP, market participants lost the incentive to engage in transactions in thecall market. Lenders barely covered transaction costs, given very tight interest margins,

20. Kohn (2010) made a similar assessment of the Fed’s large-scale asset purchase program. He pointed out thatthe purchases contributed mostly to stabilizing financial markets, but produced, by and large, uncertain impactson economic activity.

21. Okina and Shiratsuka (2004b) pointed out that the BOJ had to conduct monetary policy under a significant andunforeseen slowdown in potential growth, which differed significantly from a standard stabilization policyaround a stable growth trend. Under such circumstances, it should be stressed that the elimination of thestructural impediments themselves is a more effective policy response than measures taken for a sustainedperiod to offset cyclical factors.

22. There seems to be a general consensus among the central banks that money market rates need to be kept at apositive level to minimize the side effects arising from a zero interest rate environment.

91

Figure 8 Outstanding Amounts in the Uncollateralized Call Market

Source: Bank of Japan, Economic and Financial Statistics Monthly.

since the overnight call rate remained very close to zero. Borrowers did not need to raisefunds in the money market primarily because the funds-supplying operations of the BOJoffered the primary means of financing. That implies that the money markets under zerointerest rates with ample liquidity almost stopped functioning as a risk-sharing deviceamong financial institutions. Financial institutions opted for face-to-face transactionswith the BOJ, in preference to market transactions with other participants.

III. Unconventional Monetary Policy

This section examines the role of the central bank balance sheets under unconventionalmonetary policy, focusing on the link between the two sides of the balance sheet.

A. Typology of Unconventional Monetary PoliciesThe policy responses of central banks to the recent financial and economic crisis canbe divided into three main areas: reducing the policy interest rate; securing the stabilityof financial markets; and facilitating corporate financing. In the second and third areas,central banks in the major economies have introduced various unconventional measuresin the range of financial assets being purchased and in the scale of such purchases. Cen-tral banks have implemented such unconventional measures by aggressively changingthe size and composition of their balance sheets.23

23. Borio and Disyatat (2009) decompose the implementation of monetary policy into two core elements, inter-est rate policy and balance-sheet policy, and then discuss unconventional monetary policy as an extension

92 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Figure 9 Illustration of Unconventional Policy Measures

As central banks in the major economies expand the scope of unconventional pol-icy measures, it is often noted that the Fed’s policy reactions put more emphasis onthe asset side of the central bank balance sheet, in the approach referred to as crediteasing. For example, Bernanke (2009a) first called the Fed’s approach to supportingcredit market “credit easing,” and pointed out the conceptual distinction from the QEPundertaken by the BOJ from 2001 to 2006. He argued that the stimulative effects ofcredit easing depend crucially on the particular mix of lending programs and securitiespurchases tailored to the dysfunctional credit markets in the United States.24

In theory, such unconventional policy can be decomposed into two elements(Figure 9): the first focuses on the size of the central bank balance sheet, while thesecond focuses on the composition. In a hypothetical case, the first element can be

of balance-sheet policy under a crisis. Goodfriend (2010) reviews the Fed’s policy responses to the recentfinancial crisis by classifying central banks’ operations into three: monetary policy, credit policy, and intereston reserves policy.

24. Bernanke (2009a) also mentions that the differences in approach between the Fed and the BOJ do not reflect“any doctrinal disagreement,” but “rather the differences in financial and economic conditions between thetwo episodes.”

93

implemented by increasing the balance sheet size while keeping its composition un-changed by restraining money market operations with standard tools (narrowly definedquantitative easing). The second element can be implemented by changing the compo-sition of the balance sheet while keeping its size unchanged by replacing conventionalassets with unconventional assets (narrowly defined credit easing).

Bernanke and Reinhart (2004) used the above classification of unconventionalmonetary policy and provide an overview of monetary policy strategies when short-term interest rates are very low or even zero.25 They examined the effects of changingthe composition and size of the central bank balance sheet, in addition to altering marketexpectations about the future course of short-term interest rates. They focused primarilyon the portfolio rebalancing effect stemming from the changes in the composition andsize of the central bank balance sheet. By shifting the composition of asset holdingsfrom shorter- to longer-dated government securities, a central bank may influence termpremiums and an overall yield curve, if investors treat them as imperfect substitutes.Similarly, by increasing the monetary base, a central bank may also influence pricesand yields of non-money assets, if the monetary base is an imperfect substitute forother financial assets.

In the policy responses to the recent financial and economic crisis, however, boththe asset and liability sides of the central bank balance sheet play roles different fromthe above portfolio rebalancing effects.26 On the one hand, the asset side works as asubstitute for private financial intermediation, for example, through outright purchasesof credit products. On the other hand, the liability side, especially expanded excessreserves, functions as a buffer for liquidity risk in the money markets. In addition,the two sides interact closely with each other, since malfunctions in financial inter-mediation are closely tied to funding liquidity risk at financial institutions, resulting inthe increased demand for excess reserves.

In practice, central banks attempt to combine the two elements of their balancesheet, size and composition, to enhance the overall effects of unconventional mone-tary policy based on their specific environments and restrictions, such as types andorigins of the shocks hitting the economy, the structure of the financial system, andinstitutional arrangements of the central bank. In this regard, quantitative easing fitsbetter as a package of unconventional policy measures to absorb the shocks hittingthe economy, given the constraints on their policy implementation (broadly definedquantitative easing). The BOJ’s QEP from 2001 to 2006 can be viewed as broadly de-fined quantitative easing, as part of the policy responses of central banks to the recentfinancial and economic crisis.

B. Determinants of Size and CompositionAs described by the typology of unconventional monetary policies, central banks im-plement unconventional monetary policy by changing both the size and composition of

25. Bernanke, Reinhart, and Sack (2004) provide a comprehensive review of empirical evidence of monetary policyalternatives at the zero lower bound of nominal interest rates.

26. One of the important factors in formulating an exit strategy from unconventional policy measures is whetheran expansion of the central bank balance sheet is driven by its asset side or liability side. I will return to thispoint in the next subsection.

94 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Figure 10 Central Bank Balance Sheet

[1] Japan

(continued on next page)

their balance sheets. In that case, the size and composition of the balance sheet dependson the state of the economy, particularly the financial system.

For example, when the increases in balance-sheet size come from increaseddemand for excess reserves due to serious concern over liquidity risk, not the mal-functions in financial intermediation, but the increases in conventional money marketoperations may accommodate an expansion of the balance sheet. In this case, suchconventional operations are implemented by extending their maturity, as seen in theBOJ’s QEP (Figure 5). That can be seen as a kind of credit easing in the variety ofmaturity, rather than product. Conversely, when not excess reserve demand, but the mal-functions in financial intermediation induce an expansion of the central bank balancesheet, increased purchases of unconventional financial assets should be accommodatedby increases in some sort of central bank liability.

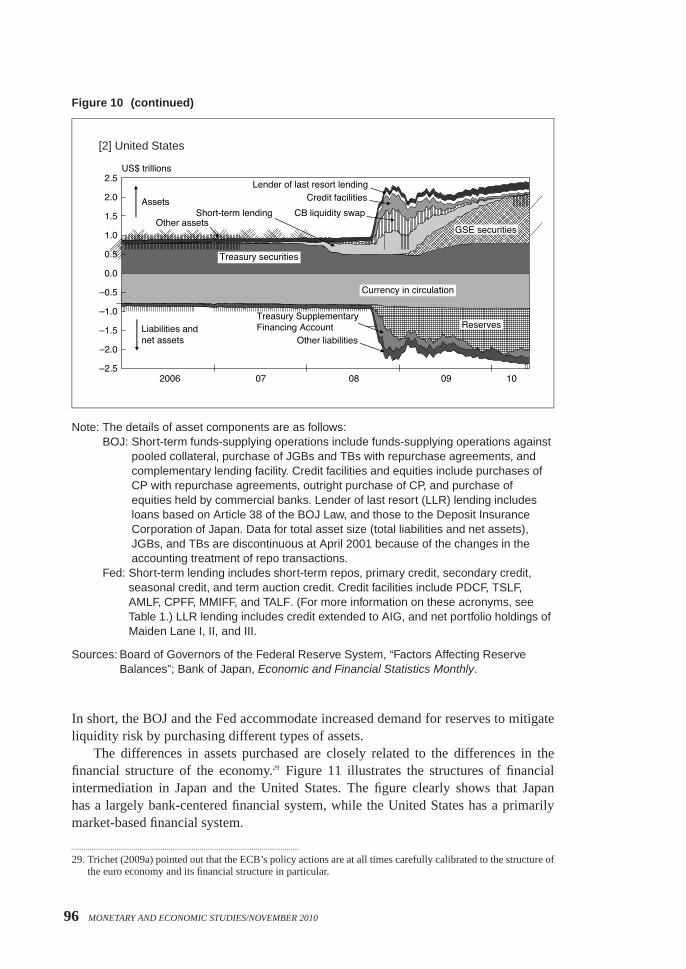

Figure 10 shows the balance sheets for the BOJ and the Fed, respectively.27 Thefigure shows that the increases on the liability side are mostly attributable to the in-creases in reserves, while currency in circulation, a major liability in normal times,remains relatively stable. By contrast, the sources of increases on the asset side sig-nificantly differ between the BOJ and the Fed. The BOJ increases both JGB holdingsand other conventional assets.28 The Fed increases not only short-term lending, but alsocentral bank liquidity swaps, credit facilities, and agency mortgage-backed securities.

27. European Central Bank (2009) also compares the changes in the balance sheets between the BOJ, the ECB,and the Fed. Cross, Fisher, and Weeken (2010) explain the changes in the BOE’s balance sheet under the crisis.

28. In addition, the BOJ introduced the purchases of stocks held by financial institutions, since market riskassociated with stockholdings was the major risk component for Japanese banks, especially major banks.For the details on the cost-benefit analysis of equity holdings of Japanese banks, see Chapter IV of Bankof Japan (2007).

95

Figure 10 (continued)

[2] United States

Note: The details of asset components are as follows:BOJ: Short-term funds-supplying operations include funds-supplying operations against

pooled collateral, purchase of JGBs and TBs with repurchase agreements, andcomplementary lending facility. Credit facilities and equities include purchases ofCP with repurchase agreements, outright purchase of CP, and purchase ofequities held by commercial banks. Lender of last resort (LLR) lending includesloans based on Article 38 of the BOJ Law, and those to the Deposit InsuranceCorporation of Japan. Data for total asset size (total liabilities and net assets),JGBs, and TBs are discontinuous at April 2001 because of the changes in theaccounting treatment of repo transactions.

Fed: Short-term lending includes short-term repos, primary credit, secondary credit,seasonal credit, and term auction credit. Credit facilities include PDCF, TSLF,AMLF, CPFF, MMIFF, and TALF. (For more information on these acronyms, seeTable 1.) LLR lending includes credit extended to AIG, and net portfolio holdings ofMaiden Lane I, II, and III.

Sources: Board of Governors of the Federal Reserve System, “Factors Affecting ReserveBalances”; Bank of Japan, Economic and Financial Statistics Monthly.

In short, the BOJ and the Fed accommodate increased demand for reserves to mitigateliquidity risk by purchasing different types of assets.

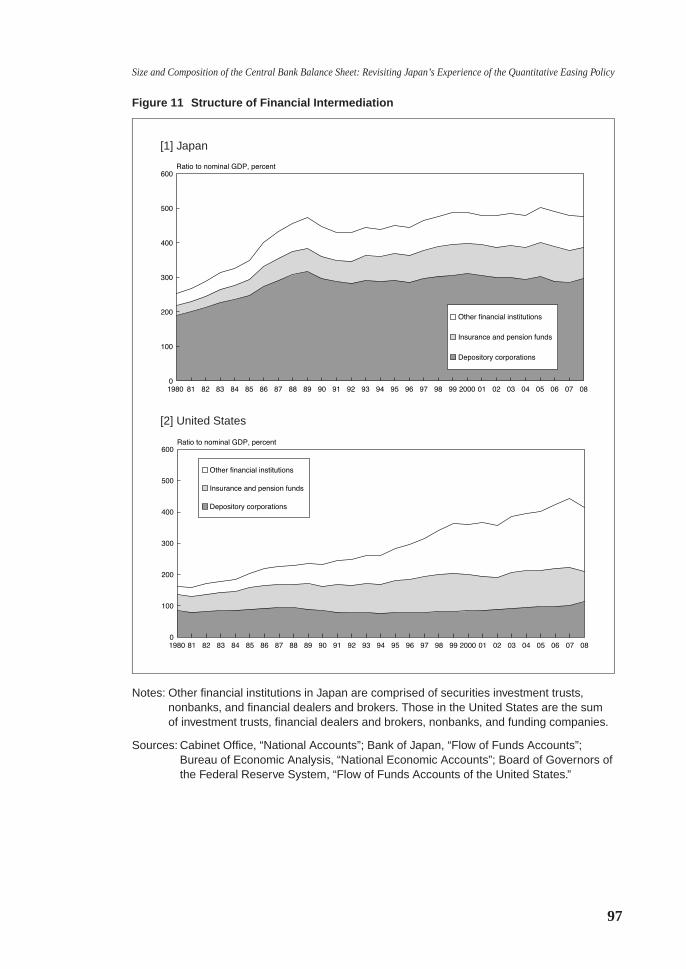

The differences in assets purchased are closely related to the differences in thefinancial structure of the economy.29 Figure 11 illustrates the structures of financialintermediation in Japan and the United States. The figure clearly shows that Japanhas a largely bank-centered financial system, while the United States has a primarilymarket-based financial system.

29. Trichet (2009a) pointed out that the ECB’s policy actions are at all times carefully calibrated to the structure ofthe euro economy and its financial structure in particular.

96 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

Figure 11 Structure of Financial Intermediation

[1] Japan

[2] United States

Notes: Other financial institutions in Japan are comprised of securities investment trusts,nonbanks, and financial dealers and brokers. Those in the United States are the sumof investment trusts, financial dealers and brokers, nonbanks, and funding companies.

Sources: Cabinet Office, “National Accounts”; Bank of Japan, “Flow of Funds Accounts”;Bureau of Economic Analysis, “National Economic Accounts”; Board of Governors ofthe Federal Reserve System, “Flow of Funds Accounts of the United States.”

97

The U.S. financial system, particularly the credit products markets closely linkedto the subprime mortgages, has fallen into serious dislocation. In response, the Fed hasnaturally taken credit-easing measures to intervene aggressively in the credit productsmarkets and related markets, seeking temporarily to serve in place of the malfunctioningprivate financial intermediation using its own balance sheet. In addition, such mal-functions in the credit products markets are closely tied to funding liquidity risk atfinancial institutions, resulting in the accumulation of excess reserves, which appearson the liability side of the Fed’s balance sheet.

C. Balance-Sheet Expansion and Zero Interest RatesAs mentioned above, Bernanke and Reinhart (2004) consider two types of the policyoptions under zero lower bound constraints of nominal interest rates: changing thecomposition and size of the central bank balance sheet as well as altering market expec-tations about the future course of short-term interest rates. In the recent crisis, however,only a limited number of central banks have employed an explicit policy commitment.30

In this case, what do we think of the relationship between unconventional monetarypolicy and policy commitment under zero nominal interest rates?

Focusing on the expectation channel, a central bank can produce further easingeffects by using a policy commitment, even when short-term interest rates decline tovirtually zero.31 A central bank can influence market expectations by making an ex-plicit commitment to the duration for which it will hold short-term interest rates atvirtually zero. If it succeeds in credibly extending its commitment duration, it canreduce longer-term interest rates.32

As mentioned earlier, however, many central banks have employed unconventionalpolicy measures without making a clear commitment to the future path of monetarypolicy in the recent crisis. Unconventional policy measures are implemented by ex-panding the central bank balance sheet, and during that process, policy interest ratesare also reduced. It should be noted that policy interest rates are maintained marginallyabove zero, while policy interest rates were reduced to virtually zero during the ZIRPand the QEP. In the meantime, many central banks have adopted an interest paymentscheme for excess reserves, thus coming to an understanding that it is unnecessary toguide the policy interest rates around virtually zero in maintaining a certain amount ofexcess reserves.33

30. Some central banks have employed some kinds of policy commitment to make clear their policy intentionto stabilize longer-term interest rates. For example, the Bank of Canada committed itself to maintaining itstarget overnight rate at 25 basis points for a full year, based on its inflation projections. In a weaker form ofpolicy commitment, the Fed has been using a type of forward-looking language: “[The committee] continuesto anticipate that economic conditions are likely to warrant an exceptionally low level of the federal funds ratesfor an extended period.”

31. See Reifschneider and Williams (2000), Jung, Teranishi, and Watanabe (2005), and Eggertsson and Woodford(2003) for detailed discussions on the policy commitment effect when a central bank faces the zero boundaryof nominal interest rates.

32. We call this mechanism the “policy duration effect,” after Fujiki, Okina, and Shiratsuka (2001) and Fujiki andShiratsuka (2002).

33. Once private financial intermediation restores normal functions, interest payments on reserves close to policyinterest rates entail a risk of distorting resource allocation through the financial system. Thus, spreads betweenpolicy interest rates and interest rates for reserves are likely to expand gradually, promoting a reduction inexcess reserves. That point is important, especially in relation to the exit strategy I will touch on later.

98 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

In general, a central bank expands its balance sheet to deal with the worsening ofthe financial intermediation function and the increase in funding liquidity risk, associ-ated with downward pressure on economic activity. Under such circumstances, mon-etary policy is principally directed toward reducing the policy interest rates, therebyeasing monetary conditions. In particular, it is supposed that a central bank attemptsto maintain the policy interest rate at an extremely low level for a considerable periodwhen it expands its balance sheet on a large scale to deal with the tremendous adverseshocks stemming from the financial system. Therefore, financial and economic circum-stances that require unconventional policy measures are most likely to accompany anextremely low level of policy interest rates. In that sense, it is inappropriate to considerthat unconventional policy measures and policy commitment under zero interest ratesare completely separated policy measures.

Note that central banks’ policy responses in the recent crisis are not a natural ex-tension of pure monetary policy under zero interest rates, but an emergency operationto rescue the financial system. In the recent crisis, given the expansion of market-basedfinancial intermediation, many central banks have extended the scope of such rescueoperations beyond the traditional role as the lender of last resort, such as provision offunding liquidity to nonbank financial institutions and restoration of market liquidityin credit products and related markets.34

IV. Discussions

Given the understanding of unconventional monetary policy discussed so far, this sec-tion addresses some questions at stake regarding the implementation of unconventionalmonetary policy.

A. Nature of Balance-Sheet ExpansionSeveral policy implications arise from the above arguments on the determinants of sizeand composition of the central bank balance sheet.

First, quantitative easing is a package of unconventional policy measures makinguse of both the asset and liability sides of the central bank balance sheet designed toabsorb the shocks hitting the economy. A central bank attempts to combine the sizeexpansion and the composition change to enhance the overall effects of unconventionalmonetary policy. That is a common characteristic of the BOJ’s QEP from 2001 to 2006and the policy responses of central banks to the recent financial and economic crisis.

Second, quantitative easing is a temporary policy response.35 The increase in sizeand the change in composition of the central bank balance sheet simply buy time until

34. Kuttner (2008), for example, views the recent Fed’s policy responses as the lender of last resort, and theireffects and costs in detail. In addition, Tucker (2009) discusses three types of last-resort operations in a financialcrisis: lender of last resort, market maker of last resort, and capital of last resort. He points out that the first twooperations are carried out by a central bank, while the third must be done by a government.

35. From a long-term perspective, it is important to explore a comprehensive policy framework for a central bankthat encompasses policy management in normal times and crisis management. Such a framework needs tointegrate monetary policy and prudential policy to achieve macroeconomic stability, comprised of price stabilityand financial system stability, as a basis for sound development of the economy. For further discussions on thispoint, see Shirakawa (2009b, d, e).

99

certain progress can be made in balance-sheet adjustments at financial institutions, suchas disposal of nonperforming assets and recapitalization. The increase in size and thechange in composition of the central bank balance sheet do not directly lead to the earlyrestoration of the financial intermediation function.

Third, quantitative easing is likely to produce side effects, as a consequence ofthe strong policy measures implemented to stabilize the financial system. A massiveexpansion of the central bank balance sheet is the corollary of public intervention inprivate financial transactions, potentially distorting incentives and resource allocationin the private sector. In particular, such side effects become more obvious as the du-ration of quantitative easing is prolonged. In this sense, a cost-benefit comparison ofunconventional monetary policy depends crucially on the length of time for which suchmassive intervention is needed.

B. Permanent Portion as a Price-Level DeterminantWhile balance-sheet expansion is a temporary policy response, the permanent portionof the expansion does matter with regard to the effects on general prices in the longerterm.36 To avoid the adverse effects on general prices, any expansion of the balancesheet must be confined to sustainable levels in the medium to long term, even thoughan extraordinary expansion is allowed temporarily to absorb the shocks hitting theeconomy.37 In that context, it is crucial to stave off public concern that expanding thecentral bank balance sheet will result in money-financing of the government deficit,thereby preventing instability in the government bond market.

In this regard, outright purchases of long-term government bonds play an importantrole. The BOJ has prudently implemented outright purchases of JGBs, as a long-termstable asset for the central bank, based on the need for money market operations tosmoothly provide long-term stable funds according to the banknote demand. Whenintroducing the QEP, the BOJ established a ceiling for outright purchases of long-termJGBs within the outstanding amount of bank note issuance (the so-called “banknoterule”). This rule makes it clear that the BOJ has no intention of providing price supportfor JGBs or money-financing of government deficit, thereby securing the credibility ofthe monetary policy.

C. Balance-Sheet Reduction in an Exit StrategyIn formulating an exit strategy, a central bank needs to consider how to reduce itsbalance sheet as the financial system restores its stability over time.

Once private financial intermediation restores its normal function, a prolonged highlevel of central bank intervention to the financial system entails a risk of distortingresource allocation through the financial system. Thus, central bank intervention in the

36. In this context, Auerbach and Obstfeld (2005) discuss the effects of the central bank balance-sheet expansionthrough the fiscal channel. When the private sector recognizes that the monetary base will permanently increasethrough massive purchases of long-term government bonds by a central bank, the private sector comes to expectgovernment debt interest payments to decline over time, consequently reducing the private sector’s tax burden.In that case, massive inflation is required to achieve high nominal growth after the economy returns to normalwith positive interest rates, while maintaining a permanent increase in the monetary base.

37. It seems a bit surprising that no economist argues that expansion of the central bank balance sheet is crucial incombating deflation in the current situation. Many economists used to advocate that the BOJ should expand itsbalance sheet as much as possible to combat deflation under zero nominal interest rates, because both deflationand inflation are monetary phenomena.

100 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

financial system is no longer necessary, and a central bank is unlikely to face any seriousobstacle in reducing its balance sheet.38 By contrast, a central bank is unlikely to exitfrom unconventional policy in a smooth manner with malfunctions in private financialintermediation. Early economic recovery is hardly possible under such circumstances,given the interaction between the real and financial sectors of the economy.

Suppose that a central bank needs to reduce its balance sheet, since, for example,demand for excess reserves subsides, reflecting the recovery in the financial systemfunctions, while a large amount of unconventional assets remains on the asset sideof the central bank balance sheet. In particular, such a situation is likely to becomeprolonged, if the maturity of unconventional assets is long. In this process, a centralbank is nevertheless able to control the size of its balance sheet by employing debtinstruments to absorb excess liquidity from financial markets, including reverse repos,in addition to interest payments to excess reserves.39

Conversely, suppose that a central bank needs to raise short-term interest rates,while very high demand for excess reserves still exists at financial institutions. Thisimplies that reserves and money markets transactions are still imperfect substitutes foreach other. Money markets have yet to restore their normal function as a risk-sharingdevice among financial institutions. In that case, transactions in money markets remainhighly restricted, and money market rates easily become volatile. Given such fragileconditions in money markets, a central bank is likely to face difficulty in guidingmoney market rates smoothly in a consistent manner to the targeted level of policyinterest rates. In addition, a central bank may need to raise short-term interest rateson a larger scale, since the transmission mechanism linking financial and nonfinancialsectors remain blocked.

The above case is most likely to occur when a central bank is forced to raiseshort-term interest rates in view of the economy’s risk of falling into stagflation. Itis certainly critical for a central bank to maintain the credibility of monetary policyunder such a difficult situation.40 In fact, some argue that a central bank will be able toexit from very low interest rate conditions without reducing its balance sheet size, sincea central bank has effective tools for controlling short-term interest rates, includingpayment of interest on reserves. In that case, a central bank needs to control short-term interest rates by making use of interest payments on reserves, while maintaininga certain size of its balance sheet. It should be noted, however, that a considerabledegree of uncertainty remains regarding the transmission mechanism from short-terminterest rates to medium- to long-term interest rates, asset prices, and general prices andeconomic activity.

38. Nishimura (2009) argues that unconventional policy measures need to possess a self-fading characteristic, bydesigning those measures to unwind themselves as market function improve. Trichet (2009c) also emphasizesthat the ECB’s unconventional policy measures were designed with exit consideration in mind, and that anumber of measures would phase out naturally.

39. Bernanke (2009c) argues that the Fed would be able to reduce its balance sheet in a smooth manner with interestpayments to reserves, combined with the steps to reduce excess reserves, such as large-scale repurchasingagreements, term deposits to financial institutions, and the outright sale of its holdings of long-term securities.See also Dudley (2009) for further discussions on the Fed’s money market operation to reduce its balance sheet.

40. See, for example, Goodfriend (2010), and Bernanke (2009b).

101

V. Concluding Remarks

This paper has attempted to provide a roadmap for a better and more comprehensiveunderstanding of unconventional monetary policy by reexamining Japan’s experienceof the QEP in light of the policy responses to the recent financial and economic crisisin major economies. It is crucial to understand that unconventional monetary policy inreality combines the two sides of the central bank balance sheet, size and composition,to enhance the overall effects of unconventional policy to absorb the shocks hitting theeconomy, given the constraints on policy implementation.

102 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

References

Auerbach, Alan J., and Maurice Obstfeld, “The Case for Open-Market Purchases in a Liquidity Trap,”

American Economic Review, 95 (1), 2005, pp. 110–137.

Baba, Naohiko, Motoharu Nakashima, Yosuke Shigemi, and Kazuo Ueda, “The Bank of Japan’s

Monetary Policy and Bank Risk Premiums in the Money Market,” International Journal of

Central Banking, 2 (1), 2006, pp. 105–135.

Bank of Japan, Financial System Report, September, 2007.

, Financial System Report, September, 2009.

Bean, Charles, “Quantitative Easing: An Interim Report,” speech to the London Society of Chartered

Accountants, October 13, 2009.

Bernanke, Ben S., “The Crisis and the Policy Response,” speech at the Stamp Lecture, London School

of Economics, January 13, 2009a (available at http://www.federalreserve.gov/newsevents/

speech/berake20090113a.htm).

, “The Fed’s Exit Strategy,” Wall Street Journal, July 21, 2009b.

, “The Federal Reserve’s Balance Sheet: An Update,” speech at the Federal Reserve Board

Conference on Key Developments in Monetary Policy, October 8, 2009c (available at

http://www.federalreserve.gov/newsevents/speech/berake20091008a.htm).

, and Vincent R. Reinhart, “Conducting Monetary Policy at Very Low Short-Term Interest

Rates,” American Economic Review, 94 (2), 2004, pp. 85–90.

, , and Brian P. Sack, “Monetary Policy Alternatives at the Zero Bound: An Empirical

Assessment,” Brookings Papers on Economic Activity, 2, 2004, pp. 1–78.

Borio, Claudio, and Piti Disyatat, “Unconventional Monetary Policies: An Appraisal,” BIS Working

Paper No. 292, Bank for International Settlements, 2009.

Cross, Michael, Paul Fisher, and Olaf Weeken, “The Bank’s Balance Sheet during the Crisis,” Bank of

England Quarterly Bulletin, 1st Quarter, Bank of England, 2010, pp. 34–42.

Dudley, William C., “The Economic Outlook and the Fed’s Balance Sheet: The Issue of ‘How’ versus

‘When,’” remarks at the Association for a Better New York Breakfast Meeting, July 29, 2009

(available at http://www.ny.frb.org/newsevents/speeches/2009/dud090729.html).

Eggertsson, Gauti B., and Michael Woodford, “The Zero Bound on Interest Rates and Optimal

Monetary Policy,” Brookings Papers on Economic Activity, 1, 2003, pp. 139–211.

European Central Bank, “Recent Developments in the Balance Sheets of the Eurosystem, the Federal

Reserve System and the Bank of Japan,” European Central Bank Monthly Bulletin, European

Central Bank, October, 2009, pp. 81–94.

Fujiki, Hiroshi, Kunio Okina, and Shigenori Shiratsuka, “Monetary Policy under Zero Interest Rate:

Viewpoints of Central Bank Economists,” Monetary and Economic Studies, 19 (1), Institute

for Monetary and Economic Studies, Bank of Japan, 2001, pp. 89–130.

, and Shigenori Shiratsuka, “Policy Duration Effect under the Zero Interest Rate Policy in

1999–2000: Evidence from Japan’s Money Market Data,” Monetary and Economic Studies,

20 (1), Institute for Monetary and Economic Studies, Bank of Japan, 2002, pp. 1–31.

Gagnon Joseph, Matthew Raskin, Julie Remache, and Brian Sack, “Large-Scale Asset Purchases by

the Federal Reserve: Did They Work?” Staff Report No. 441, Federal Reserve Bank of New

York, 2010.

Goodfriend, Marvin, “Central Banking in the Credit Turmoil: An Assessment of Federal Reserve

Practice,” paper presented at Carnegie-Rochester Conference on April 16–17, 2010.

103

Ito, Takatoshi, and Fredric S. Mishkin, “Two Decades of Japanese Monetary Policy and the Deflation

Problem,” in Takatoshi Ito and Andrew Rose, eds. Monetary Policy with Very Low Inflation in

the Pacific Rim, Chicago: The University of Chicago Press, 2006, pp. 131–193.

Jung, Taehun, Yuki Teranishi, and Tsutomu Watanabe, “Optimal Monetary Policy at the Zero-Interest-

Rate Bound,” Journal of Money, Credit and Banking, 37 (5), 2005, pp. 813–835.

Kohn, Donald, “The Federal Reserve’s Policy Actions during the Financial Crisis and Lessons for the

Future,” remarks at Carleton University, May 13, 2010.

Kuttner, Kenneth N., “The Federal Reserve as Lender of Last Resort during the Panic of 2008,” mimeo,

2008.

McCauley, Robert N., and Kazuo Ueda, “Government Debt Management at Low Interest Rates,” BIS

Quarterly Review, Bank for International Settlements, June, 2009, pp. 35–51.

Nishimura, Kiyohiko G., “Unconventional Policies of Central Banks: Restoring Market Function and

Confidence,” remarks at the Money and Banking Conference sponsored by the Central Bank

of Argentina, September 1, 2009.

Oda, Nobuyuki, and Kazuo Ueda, “The Effects of the Bank of Japan’s Zero Interest Rate Commitment

and Quantitative Monetary Easing on the Yield Curve: A Macro-Finance Approach,” Japanese

Economic Review, 58 (3), 2007, pp. 303–328.

Okina, Kunio, and Shigenori Shiratsuka, “Policy Commitment and Expectation Formation: Japan’s

Experience under Zero Interest Rates,” North American Journal of Economics and Finance,

15 (1), 2004a, pp. 75–100.

, and , “Asset Price Fluctuations, Structural Adjustments, and Sustained Economic

Growth: Lessons from Japan’s Experience since the Late 1980s,” Monetary and Economic

Studies, 22 (S-1), Institute for Monetary and Economic Studies, Bank of Japan, 2004b,

pp. 143–167.

Reifschneider, David, and John C. Williams, “Three Lessons for Monetary Policy in a Low-Inflation

Era,” Journal of Money, Credit and Banking, 32 (4), 2000, pp. 936–966.

Saito, Makoto, and Shigenori Shiratsuka, “Financial Crises as the Failure of Arbitrage: Implications

for Monetary Policy,” Monetary and Economic Studies, 19 (S-1), Institute for Monetary and

Economic Studies, Bank of Japan, 2001, pp. 239–276.

Shirakawa, Masaaki, “Way Out of Economic and Financial Crisis: Lessons and Policy Actions,”

speech at the Japan Society in New York, April 23, 2009a (available at http://www.boj.or.jp/

en/type/press/koen07/ko0904c.htm).

, “Preventing the Next Crisis: The Nexus between Financial Markets, Financial Institutions

and Central Banks,” speech at the London Stock Exchange, May 13, 2009b (available at

http://www.boj.or.jp/en/type/press/koen07/ko0905b.htm).

, “Financial System and Monetary Policy Implementation: Long and Winding Evolution in

the Way of Thinking,” opening speech at the 2009 International Conference hosted by the

Institute for Monetary and Economic Studies, Bank of Japan, in Tokyo on May 27–28, 2009c

(available at http://www.boj.or.jp/en/type/press/koen07/ko0905e.htm).

, “The Role of Central Banks in the New Financial Environment,” remarks at the International

Monetary Conference in Kyoto on June 9, 2009d (available at http://www.boj.or.jp/en/type/

press/koen07/ko0906b.htm).

, “Some Thoughts on Incentives at Micro- and Macro-Level for Crisis Prevention,” remarks at

the Eighth Bank for International Settlements Annual Conference in Basel, Switzerland, June

26, 2009e (available at http://www.boj.or.jp/en/type/press/koen07/ko0906e.htm).

104 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010

Size and Composition of the Central Bank Balance Sheet: Revisiting Japan’s Experience of the Quantitative Easing Policy

, “Unconventional Monetary Policy—Central Banks: Facing the Challenges and Learning the

Lessons,” remarks at the conference co-hosted by the People’s Bank of China and the Bank for

International Settlements in Shanghai, August 8, 2009f (available at http://www.boj.or.jp/en/

type/press/koen07/ko0908a.htm).

, “Revisiting the Philosophy behind Central Bank Policy,” speech at the Economic

Club of New York, April 22, 2010 (available at http://www.boj.or.jp/en/type/press/koen07/

ko1004e.htm).

Stroebel, Johannes C., and John B. Taylor, “Estimated Impact of the Fed’s Mortgage-Backed Secu-

rities Purchase Program,” NBER Working Paper No. 15626, National Bureau of Economic

Research, 2009.

Trichet, Jean-Claude, “Supporting the Financial System and the Economy: Key ECB Policy Actions

in the Crisis,” speech at a conference organized by the Nueva Economía Fórum and the Wall

Street Journal Europe in Madrid, June 22, 2009a.

, “The ECB’s Enhanced Credit Support,” keynote address at the University of Munich, July

13, 2009b.

, “The ECB’s Exit Strategy,” speech at the ECB Watchers Conference, Frankfurt, September

4, 2009c.

Tucker, Paul, “The Repertoire of Official Sector Interventions in the Financial System: Last Re-

sort Lending, Market-Making, and Capital,” remarks at the 2009 International Conference

hosted by the Institute for Monetary and Economic Studies, Bank of Japan, in Tokyo on

May 27–28, 2009.

Ueda, Kazuo, “The Bank of Japan’s Struggle with the Zero Lower Bound on Nominal Interest Rates:

Exercises in Expectations Management,” International Finance, 8 (2), 2005, pp. 329–350.

Ugai, Hiroshi, “Effects of the Quantitative Easing Policy: A Survey of Empirical Analyses,” Monetary

and Economic Studies, 25 (1), Institute for Monetary and Economic Studies, 2007, Bank of

Japan, pp. 1–47.

Yellen, Janet L., “U.S. Monetary Policy Objectives in the Short and Long Run,” presentation to the

Andrew Brimmer Policy Forum IBEFA/ASSA Meeting, San Francisco, January 4, 2009.

105

106 MONETARY AND ECONOMIC STUDIES/NOVEMBER 2010