Embed Size (px)

Citation preview

Page 1 / 36

SIX MiFID II Rule Set Documentation

Version: June 6th, 2018

Page 2 / 36

Revisions

Date Version Details

26.01.2018 0 Initial Version

14.02.2018 1.1 Inclusion of ESMA Regulation for Com-plex/non-complex classifications

6.06.2018 1.2 Inclusion of product release updates from March - May 2018.

Page 3 / 36

Content of the Document

This document is not an implementation specification, rather it proves a general rational and technical support regarding the SIX rule sets for the MiFID II Regulation, based on current knowledge and sta-tus. The information in this document does not claim to be exhaustive. The document is subject to change and the new and modified chapters will be published with a new version number. Only major changes will be listed in the section entitled “Revisions”, minor changes will not be included here. Purpose of the Document

The purpose of this document is to outline the rationale behind the MiFID II SIX rule sets – initially specifically focusing on Complex/non-complex, Reportable Instruments, Leverage Instrument Indica-tor, Autofilling of Target Market Data and Commodity Derivative Indicator. Target Group

This document is aimed at VDF clients who have implemented the SIX MiFID II Data Packages. The key members in the target group for this document are Senior BAs with VDF knowledge, Compliance Officers and MiFID II Project Managers. In order to correctly interpret this document, it is necessary to be familiar with the ESMA MiFID II Regulation as well as VDF, its structure and terminology. Disclaimer

This document is solely for information purposes and is subject to change without notice at any time. SIX does not provide any legal, compliance, financial, investment, tax or other advice. It is the sole responsibility of the client to familiarize itself with any applicable laws, regulations, provisions and de-crees and to assess and implement them accordingly. No express or implied representation, warranty and guarantee is given and all liability is excluded by SIX and its suppliers.

Page 4 / 36

Contents

1. Complex / Non-Complex ............................................................................................................................. 7

Introduction ....................................................................................................................................... 8 1.1

Regulatory Background ..................................................................................................................... 8 1.1.1

SIX classification complex / non-complex ......................................................................................... 8 1.1.2

Cautions approach for the classification ............................................................................................ 8 1.1.2.1.

Country-specific classifications ......................................................................................................... 8 1.1.3

Exceptions ........................................................................................................................................ 8 1.1.4

Classification carried out by the regulator (ESMA) ............................................................................ 8 1.1.4.1.

Classification carried out by the issuer .............................................................................................. 8 1.1.4.2.

Overview of classification based on SIX Security Types (TKT’s) ...................................................... 9 1.2

TKT’s without classification ............................................................................................................... 9 1.2.1

TKT’s always complex ...................................................................................................................... 9 1.2.2

TKT’s always non-complex ............................................................................................................... 9 1.2.3

TKT’s classified with detailed rule set ............................................................................................... 9 1.2.4

Rules per asset class ...................................................................................................................... 10 1.3

Shares (TKT = 1 : unit, particip, cert.) ............................................................................................. 10 1.3.1

TKT = 1 with listing on RM, MTF or recognized market existing ..................................................... 10 1.3.1.1.

TKT = 1 without listing on RM, MTF or recognized market ............................................................. 10 1.3.1.2.

Debt instruments ............................................................................................................................. 10 1.3.2

Listing on RM, MTF or recognized market existing ......................................................................... 10 1.3.2.1.

No listing on RM, MTF or recognized market existing ..................................................................... 10 1.3.2.2.

Funds .............................................................................................................................................. 10 1.3.3

TKT = 7 / Trust Shares .................................................................................................................... 11 1.3.3.1.

TKT = C / Trust cert.unit / fund, invest. Foundation units ................................................................ 11 1.3.3.2.

Remark ETF’s ................................................................................................................................. 11 1.3.3.3.

Money market instruments (TKT = Q) ............................................................................................. 11 1.3.4

Other instruments with cash-flow (TKT = S) .................................................................................... 11 1.3.5

Exchange traded ............................................................................................................................. 11 1.3.6

ESMA requirement .......................................................................................................................... 11 1.3.6.1.

SIX rule set for Exchange traded instruments ................................................................................. 11 1.3.6.2.

Appendix: Excerpts of ESMA articles, including Links .................................................................... 12 1.4

COMMISSION DELEGATED REGULATION (EU) 2017/565 of 25 April 2016 ............................... 12 1.4.1

DIRECTIVE 2014/65/ ...................................................................................................................... 12 1.4.2

Article 4(1)(44)(c) of, Directive 2014/65/EU .................................................................................... 13 1.4.3

SECTION C of ANNEX 1 Directive 2014/65/EU.............................................................................. 13 1.4.4

ESMA Guidelines on aspects of the MiFID suitability requirements ................................................ 13 1.4.5

ESMA MiFID practices for firms selling complex products .............................................................. 14 1.4.6

ESMA QA on non-UCIT-Funds (appropriateness / complex) .......................................................... 14 1.4.7

Guidelines on complex debt instruments and structured deposits .................................................. 14 1.4.8

Page 5 / 36

Final report on complex debt instruments and structured_deposits ................................................ 15 1.4.9

2. Reportable Instrument .................................................................................................................... 16

Introduction ..................................................................................................................................... 17 2.1

Regulatory Background ................................................................................................................... 17 2.1.1

SIX classification ............................................................................................................................. 17 2.1.2

Classification Reportable = Yes ...................................................................................................... 17 2.1.2.1.

Classification Reportable = No ........................................................................................................ 17 2.1.2.2.

No classification .............................................................................................................................. 17 2.1.2.3.

Exceptions ...................................................................................................................................... 17 2.1.3

Classification carried out by the regulator (ESMA) .......................................................................... 18 2.1.3.1.

Instrument existing on ESMA data base ......................................................................................... 18 2.1.3.2.

Classification carried out by the issuer ............................................................................................ 18 2.1.3.3.

Overview of classification based on SIX Security Types (TKT’s) .................................................... 19 2.2

Non fungible / tradable asset classes: classification “non reportable” ............................................. 19 2.2.1

TKT’s classified based on listings only ............................................................................................ 19 2.2.2

TKT’s classified based additionally on listings of the underlying or components ............................ 20 2.2.3

SIX classification rule set / algorithm ............................................................................................... 21 2.3

Instrument existing on ESMA data base ......................................................................................... 21 2.3.1

Classification carried out by the issuer ............................................................................................ 21 2.3.2

SIX classification algorithm ............................................................................................................. 21 2.3.3

Referential (not tradable) instruments ............................................................................................. 21 2.3.3.1.

Instruments with relevant listings .................................................................................................... 21 2.3.3.2.

Instruments without relevant listings without components / underlying ........................................... 21 2.3.3.3.

Instruments without relevant listings with components / underlying ................................................ 21 2.3.3.4.

Components / underlying available in SIX data base ...................................................................... 21 2.3.3.5.

Components / underlying NOT available in SIX data base ............................................................. 22 2.3.3.6.

3. Leveraged Instrument Indicator ...................................................................................................... 23

Introduction ..................................................................................................................................... 24 3.1

Regulatory Background ................................................................................................................... 24 3.1.1

Technical implementation by SIX .................................................................................................... 25 3.2

Example .......................................................................................................................................... 25 3.2.1

Overview by Type of Security.......................................................................................................... 25 3.2.2

Detailed rule set .............................................................................................................................. 26 3.2.3

Bonds (TKT 0) are leveraged if: ...................................................................................................... 26 3.2.3.1.

Shares (TKT 1) are leveraged if: ..................................................................................................... 26 3.2.3.2.

Floating Rate Notes (TKT L) are leveraged if: ................................................................................. 26 3.2.3.3.

Trust Shares (TKT 7) and Trust Certificates / Funds (TKT C) are leveraged if: .............................. 26 3.2.3.4.

Other Instruments with Cashflow (TKT S) are leveraged if: ............................................................ 27 3.2.3.5.

Structured Instruments (TKT 6) are leveraged if: ............................................................................ 27 3.2.3.6.

Leveraged Products (TKT M), Futures (TKT P), Convertibles (TKT V), Options (TKT Z) are 3.2.3.7.leveraged if: 27

4. Automated Filling of Target Market Data ........................................................................................ 28

Page 6 / 36

Introduction ..................................................................................................................................... 29 4.1

Regulatory Background ................................................................................................................... 29 4.1.1

Technical implementation by SIX .................................................................................................... 30 4.2

Default Values per IBT Code .......................................................................................................... 30 4.2.1

Instruments with EUSIPA Code but no (valid) IBT Code ................................................................. 30 4.2.2

Instruments without EUSIPA and IBT Code .................................................................................... 30 4.2.3

Calculation of Capital Protection ..................................................................................................... 30 4.2.4

No protection ................................................................................................................................... 30 4.2.4.1.

Full or partial protection ................................................................................................................... 30 4.2.4.2.

Calculation of Time Horizon and Recommended Holding Period ................................................... 31 4.2.5

Recommended Holding Period (RHP) ............................................................................................ 31 4.2.5.1.

Time Horizon ................................................................................................................................... 31 4.2.5.2.

5. Commodity Derivative Indicator ..................................................................................................... 32

Introduction ..................................................................................................................................... 33 5.1

Regulatory Background ................................................................................................................... 33 5.1.1

Regulatory Technical Standards ..................................................................................................... 33 5.1.1.1.

Technical implementation by SIX .................................................................................................... 34 5.2

Example .......................................................................................................................................... 34 5.2.1

Overview by Type of Security.......................................................................................................... 34 5.2.2

General rules for all rule sets .......................................................................................................... 34 5.2.3

Country codes ................................................................................................................................. 34 5.2.3.1.

Instrument status ............................................................................................................................. 34 5.2.3.2.

Detailed rule set MiFID II Commodity derivative indicator ............................................................... 35 5.2.4

6. Additional Support and Documentation .......................................................................................... 36

Page 7 / 36

1. Complex / Non-Complex

Page 8 / 36

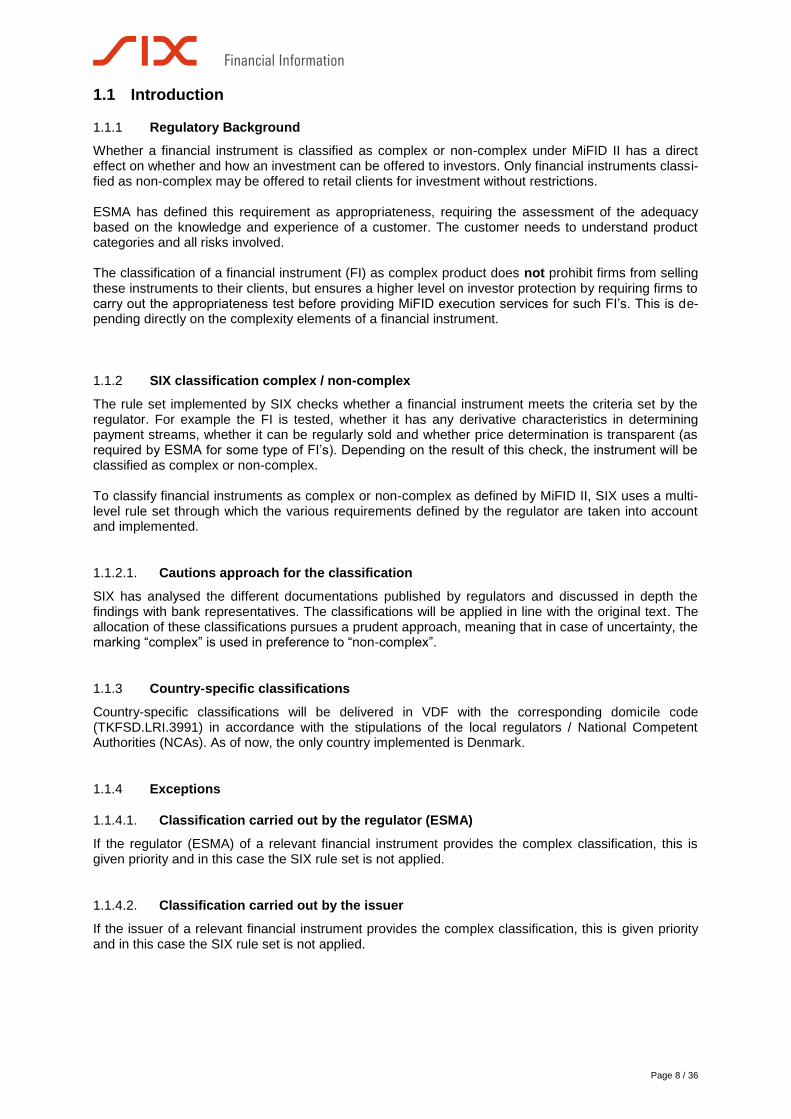

Introduction 1.1

Regulatory Background 1.1.1

Whether a financial instrument is classified as complex or non-complex under MiFID II has a direct effect on whether and how an investment can be offered to investors. Only financial instruments classi-fied as non-complex may be offered to retail clients for investment without restrictions. ESMA has defined this requirement as appropriateness, requiring the assessment of the adequacy based on the knowledge and experience of a customer. The customer needs to understand product categories and all risks involved. The classification of a financial instrument (FI) as complex product does not prohibit firms from selling these instruments to their clients, but ensures a higher level on investor protection by requiring firms to carry out the appropriateness test before providing MiFID execution services for such FI’s. This is de-pending directly on the complexity elements of a financial instrument.

SIX classification complex / non-complex 1.1.2

The rule set implemented by SIX checks whether a financial instrument meets the criteria set by the regulator. For example the FI is tested, whether it has any derivative characteristics in determining payment streams, whether it can be regularly sold and whether price determination is transparent (as required by ESMA for some type of FI’s). Depending on the result of this check, the instrument will be classified as complex or non-complex. To classify financial instruments as complex or non-complex as defined by MiFID II, SIX uses a multi-level rule set through which the various requirements defined by the regulator are taken into account and implemented.

Cautions approach for the classification 1.1.2.1.

SIX has analysed the different documentations published by regulators and discussed in depth the findings with bank representatives. The classifications will be applied in line with the original text. The allocation of these classifications pursues a prudent approach, meaning that in case of uncertainty, the marking “complex” is used in preference to “non-complex”.

Country-specific classifications 1.1.3

Country-specific classifications will be delivered in VDF with the corresponding domicile code (TKFSD.LRI.3991) in accordance with the stipulations of the local regulators / National Competent Authorities (NCAs). As of now, the only country implemented is Denmark.

Exceptions 1.1.4

Classification carried out by the regulator (ESMA) 1.1.4.1.

If the regulator (ESMA) of a relevant financial instrument provides the complex classification, this is given priority and in this case the SIX rule set is not applied.

Classification carried out by the issuer 1.1.4.2.

If the issuer of a relevant financial instrument provides the complex classification, this is given priority and in this case the SIX rule set is not applied.

Page 9 / 36

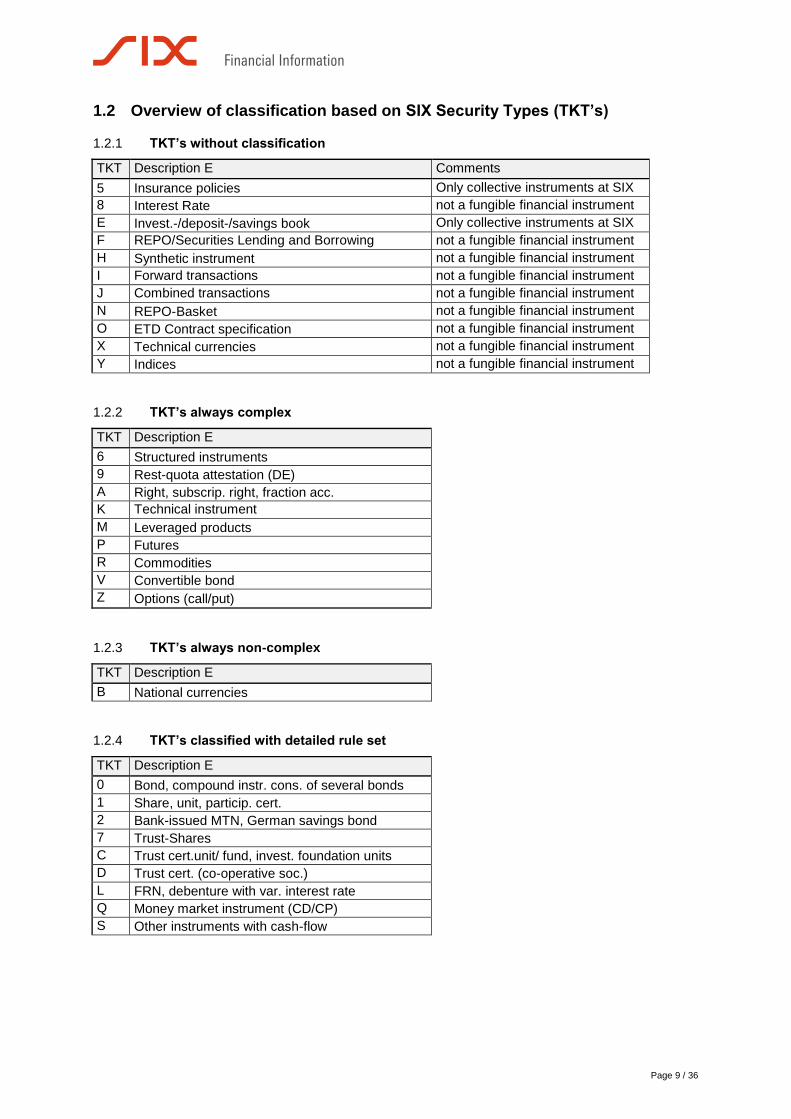

Overview of classification based on SIX Security Types (TKT’s) 1.2

TKT’s without classification 1.2.1

TKT Description E Comments

5 Insurance policies Only collective instruments at SIX

8 Interest Rate not a fungible financial instrument

E Invest.-/deposit-/savings book Only collective instruments at SIX

F REPO/Securities Lending and Borrowing not a fungible financial instrument

H Synthetic instrument not a fungible financial instrument

I Forward transactions not a fungible financial instrument

J Combined transactions not a fungible financial instrument

N REPO-Basket not a fungible financial instrument

O ETD Contract specification not a fungible financial instrument

X Technical currencies not a fungible financial instrument

Y Indices not a fungible financial instrument

TKT’s always complex 1.2.2

TKT Description E

6 Structured instruments

9 Rest-quota attestation (DE)

A Right, subscrip. right, fraction acc.

K Technical instrument

M Leveraged products

P Futures

R Commodities

V Convertible bond

Z Options (call/put)

TKT’s always non-complex 1.2.3

TKT Description E

B National currencies

TKT’s classified with detailed rule set 1.2.4

TKT Description E

0 Bond, compound instr. cons. of several bonds

1 Share, unit, particip. cert.

2 Bank-issued MTN, German savings bond

7 Trust-Shares

C Trust cert.unit/ fund, invest. foundation units

D Trust cert. (co-operative soc.)

L FRN, debenture with var. interest rate

Q Money market instrument (CD/CP)

S Other instruments with cash-flow

Page 10 / 36

Rules per asset class 1.3

Shares (TKT = 1 : unit, particip, cert.) 1.3.1

The following principles are applied:

TKT = 1 with listing on RM, MTF or recognized market existing 1.3.1.1.

a) Only checked for derivative characteristics of FI

TKT = 1 without listing on RM, MTF or recognized market 1.3.1.2.

a) Exchange traded must be given

b) It is checked for derivative characteristics of FI

c) It is also checked for ease of understandability of FI

Debt instruments 1.3.2

Following TKT’s are considered as debt FI’s:

TKT = 0 / Bond, compound instr. cons. of several bonds

TKT = 2 / Bank-issued MTN, German savings bond

TKT = D / Trust cert. (cooperative soc. )

TKT = L / FRN, debenture with var. interest rate The rules applied for debt FI’s are based on the Regulation and the “Guidelines on complex debt in-struments and structured deposits”) Directive Excerpt of article 25 Bonds or other forms of securitized debt

admitted to trading on a regulated market or on an equivalent third country market or on a MTF.

excluding those that embed a derivative or incorporate a structure which makes it difficult for the client to understand the risk involved;

Listing on RM, MTF or recognized market existing 1.3.2.1.

a) Derivative characteristics of FI Examples:

Callable Puttable

Convertible Exchangeable

b) Understandability of FI

Strips

No listing on RM, MTF or recognized market existing 1.3.2.2.

Classification as complex, based on article 25 (see quotation above).

Funds 1.3.3

Following TKT’s are considered Funds:

Page 11 / 36

TKT = 7 / Trust Shares 1.3.3.1.

TKT = C / Trust cert.unit / fund, invest. Foundation units 1.3.3.2.

Only UCIT-funds can be classified as non-complex, when following conditions are met: a) No derivative characteristics b) Not a structured UCIT

Remark ETF’s 1.3.3.3.

ETF’s are non-complex only if a physical full replication exists (see ESMA Report: “Final report on complex debt instruments and structured_deposits” for regulatory details).

Money market instruments (TKT = Q) 1.3.4

a) Either a listing on RM, MTF or recognized market exists OR eligibility for Exchange tradeable exists

Additionally tested on:

b) Derivative characteristics of FI c) Understandability of FI

Other instruments with cash-flow (TKT = S) 1.3.5

a) Either a listing on RM, MTF or recognized market exists OR eligibility for Exchange tradeable exists

Additionally tested on:

b) Derivative characteristics of FI c) Understandability of FI

Exchange traded 1.3.6

ESMA requirement 1.3.6.1.

For some asset classes it is required that “there are frequent opportunities to dispose of, redeem, or otherwise realise that instrument at prices …”. details see Chapter 1.4.1.

SIX rule set for Exchange traded instruments 1.3.6.2.

Step one: Listings are patterned, whether they are relevant, based on

a) Type of listing b) Trading Status c) Listing Status

Step two: In the second step the statistics of all relevant trading places are analyzed. Following details are con-sidered

a) Number of trading places b) Time elapsed since first trading date c) Quantity of days real trades with volume > 1

Page 12 / 36

Appendix: Excerpts of ESMA articles, including Links 1.4

COMMISSION DELEGATED REGULATION (EU) 2017/565 of 25 April 2016 1.4.1

http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32017R0565&from=EN COMMISSION DELEGATED REGULATION (EU) 2017/565 of 25 April 2016 supplementing Directive 2014/65/EU of the European Parliament and of the Council as regards organisational requirements and operating conditions for investment firms and defined terms for the purposes of that Directive Article 57 / Provision of services in non-complex instruments Provision of services in non-complex instruments (Article 25(4) of Directive 2014/65/EU) A financial instrument which is not explicitly specified in Article 25(4)(a) of Directive 2014/65/EU shall be consid-ered as non-complex for the purposes of Article 25(4)(a)(vi) of Directive 2014/65/EU if it satisfies the following criteria:

a) It does not fall within Article 4(1)(44)(c) of, or points (4) to (11) of Section C of Annex I to Di-rective 2014/65/EU;

b) There are frequent opportunities to dispose of, redeem, or otherwise realise that instrument at prices that are publicly available to market participants and that are either market prices or prices made available, or validated, by valuation systems independent of the issuer; leading to our concept of “tradability”, tradability-concept is applied only to - shares (TKT = 1) not traded on RM, MTF or recognized market - TKT = S (other FI’s with cashflow

c) It does not involve any actual or potential liability for the client that exceeds the cost of acquir-ing the instrument;

d) It does not incorporate a clause, condition or trigger that could fundamentally alter the nature or risk of the investment or pay out profile, such as investments that incorporate a right to con-vert the instrument into a different investment;

e) It does not include any explicit or implicit exit charges that have the effect of making the in-vestment illiquid even though there are technically frequent opportunities to dispose of, re-deem or otherwise realise it;

f) Adequately comprehensive information on its characteristics is publicly available and is like-ly to be readily understood so as to enable the average retail client to make an informed judgment as to whether to enter into a transaction in that instrument.

DIRECTIVE 2014/65/ 1.4.2

http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014L0065&from=DE

- DIRECTIVE 2014/65/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 15 May 2014

Article 25

g) Assessment of suitability and appropriateness and reporting to clients - 4. Member States shall allow investment firms when providing investment services that only

consist of execution or reception and transmission of client orders with or without ancillary ser-vices, excluding the granting of credits or loans as specified in Section B.1 of Annex I that do not comprise of existing credit limits of loans, current accounts and overdraft facilities of cli-ents, to provide those investment services to their clients without the need to obtain the infor-mation or make the determination provided for in paragraph 3 where all the following condi-tions are met:

a) the services relate to any of the following financial instruments: i. Shares admitted to trading on a regulated market or on an equivalent third-country

market or on a MTF, where those are shares in companies, and excluding shares in non-UCITS collective investment undertakings and shares that embed a derivative

ii. Bonds or other forms of securitized debt admitted to trading on a regulated market or on an equivalent third country market or on a MTF, excluding those that embed a derivative or incorporate a structure which makes it dif-ficult for the client to understand the risk involved;

Page 13 / 36

iii. Money-market instruments, excluding those that embed a derivative or incorporate a structure which makes it dif-ficult for the client to understand the risk involved;

iv. Shares or units in UCITS, excluding structured UCITS as referred to in the second subparagraph of Article 36(1) of Regulation (EU) No 583/2010;

v. Structured deposits, excluding those that incorporate a structure which makes it difficult for the client to understand the risk of return or the cost of exiting the product before term;

vi. Other non-complex financial instruments for the purpose of this paragraph.

- For the purpose of this point, if the requirements and the procedure laid down under the third and the fourth subparagraphs of Article 4(1) of Directive 2003/71/EC are fulfilled, a third-country market shall be considered to be equivalent to a regulated market.

Article 4(1)(44)(c) of, Directive 2014/65/EU 1.4.3

(c) any other securities giving the right to acquire or sell any such transferable securities or giving rise to a cash settlement determined by reference to transferable securities, currencies, interest rates or yields, commodities or other indices or measures;

SECTION C of ANNEX 1 Directive 2014/65/EU 1.4.4

Financial instruments 1) Transferable securities; 2) Money-market instruments;EN 12.6.2014 Official Journal of the European Union L 173/481 3) Units in collective investment undertakings; 4) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to

securities, currencies, interest rates or yields, emission allowances or other derivatives instru-ments, financial indices or financial measures which may be settled physically or in cash;

5) Options, futures, swaps, forwards and any other derivative contracts relating to commodities that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event;

6) Options, futures, swaps, and any other derivative contract relating to commodities that can be physically settled provided that they are traded on a regulated market, a MTF, or an OTF, ex-cept for wholesale energy products traded on an OTF that must be physically settled;

7) Options, futures, swaps, forwards and any other derivative contracts relating to commodities, that can be physically settled not otherwise mentioned in point 6 of this Section and not being for commercial purposes, which have the characteristics of other derivative financial instru-ments;

8) Derivative instruments for the transfer of credit risk; 9) Financial contracts for differences; 10) Options, futures, swaps, forward rate agreements and any other derivative contracts relating to

climatic variables, freight rates or inflation rates or other official economic statistics that must be settled in cash or may be settled in cash at the option of one of the parties other than by reason of default or other termination event, as well as any other derivative contracts relating to assets, rights, obligations, indices and measures not otherwise mentioned in this Section, which have the characteristics of other derivative financial instruments, having regard to whether, inter alia, they are traded on a regulated market, OTF, or an MTF;

11) Emission allowances consisting of any units recognised for compliance with the requirements of Directive 2003/87/EC (Emissions Trading Scheme).

ESMA Guidelines on aspects of the MiFID suitability requirements 1.4.5

https://www.esma.europa.eu/sites/default/files/library/2015/11/2012-387.pdf 35. In determining the information to be collected, investment firms should also take into account the nature of the service to be provided. Practically, this means that:

Page 14 / 36

(a) when investment advice services are to be provided, firms should collect sufficient information in order to be able to assess the ability of the client to understand the risks and nature of each of the financial instruments that the firm envisages recommending to that client;

ESMA MiFID practices for firms selling complex products 1.4.6

https://www.esma.europa.eu/sites/default/files/library/2015/11/ipisc_complex_products_-_opinion_20140105.pdf 12. The more complex a product, the harder it is to demonstrate that retail clients have sufficient finan-cial knowledge and experience to understand the key features, benefits and risks involved in an in-vestment. 15. As MiFID requires firms to act in the best interests of its clients, NCAs should monitor that trading platforms that give access to complex products only market complex products to those clients for whom they would be potentially suitable, or appropriate (where the client would possess the necessary level of knowledge and experience

ESMA QA on non-UCIT-Funds (appropriateness / complex) 1.4.7

https://www.esma.europa.eu/sites/default/files/library/esma35-43-349_mifid_ii_qas_on_investor_protection_topics.pdf Question 1 [Last update: 6 June 2017] Can shares in non-UCITS collective investment undertakings explicitly excluded under point (i) of Arti-cle 25(4)(a) of MiFID II be nevertheless assessed against the criteria set out in Article 57 of the MiFID II Delegated Regulation and as a consequence potentially be deemed non-complex financial instru-ments for the purposes of the appropriateness test? Answer 1 No. Article 25(4) of MiFID II allows, subject to certain conditions, MiFID firms to provide execution and/or reception and transmission of orders services without having to assess the appropriateness of the product for the client. One condition is that the service to be provided does not relate to a complex product. MiFID II has further clarified which instruments should be deemed complex per se. Shares in non-UCITS explicitly excluded from the universe of non-complex products are complex per se and cannot be reassessed against the criteria set out in Article 57 of the MiFID II Delegated Regula-tion. This approach is confirmed by Recital 80 of MiFID II which clarifies that: “Investment firms are allowed to provide investment services that consist only of execution and/or of the reception and transmission of client orders, without the need to obtain information regarding the knowledge and ex-perience of the client in order to assess the appropriateness of the service or the financial instrument for the client. Since those services entail a relevant reduction of client protection, it is appropriate to improve the conditions for their provision. (…). It is also appropriate to better define the criteria for the selection of the financial instruments to which those services should relate in order to exclude certain financial instruments, including those which embed a derivative or incorporate a structure which makes it difficult for the client to understand the risk involved, shares in undertakings that are not undertakings for collective investment in transferable securities (UCITS) (non-UCITS collective investment undertak-ings) and structured UCITS as referred to in the second subparagraph of Article 36(1) of Commission Regulation (EU) No 583/2010” (our underlining)27. The treatment of shares (or units28) in non-UCITS as complex products does not prohibit firms from selling these instruments but only ensures a higher level on investor protection by requiring MiFID firms to carry out the appropriateness test before providing MiFID execution services in relation to these instruments.

Guidelines on complex debt instruments and structured deposits 1.4.8

https://www.esma.europa.eu/sites/default/files/library/2015-1787_-_guidelines_on_complex_debt_instruments_and_structured_deposits.pdf

Page 15 / 36

Excerpts of ESMA list of examles of complex FI Non exhaustive list of examples of debt instruments that embed a derivative or incorporate a structure which makes it difficult for the client to understand the risk involved and complex structured deposits for the purpose of Article 25(4) (a)(ii), (iii) and (v) of MiFID II

- Convertible and exchangeable bonds - Indexed bonds and turbo certificates - Contingent convertible bonds - Callable or puttable bonds - Credit - linked notes - Warrant - Asset - backed securities and asset - backed commercial papers - Debt instruments the return of which is subordinated to the reimbursement of debt held by

others - Debt instruments lacking a specified redemption or maturity date

Final report on complex debt instruments and structured_deposits 1.4.9

https://www.esma.europa.eu/sites/default/files/library/2015-1783_-_final_report_on_complex_debt_instruments_and_structured_deposits.pdf 53. As already stated at paragraph 13 of the CP, the definition of embedded a derivative proposed in the draft Guidelines for the purpose of the appropriateness test under Article 24(4) of MiFID II is similar to other existing definitions. With reference to the definition provided by Article 10 of UCITS implement-ing directive (Directive 2007/16/EU), ESMA notes that the notion of instruments embedding a deriva-tive concerns the definition of certain eligible assets for investment by UCITS and includes an addi-tional reference to the risk profile of the instrument as a consequence of the embedded derivative. Differently from the UCITS context, the concept of “embedded derivative” provided under Article 25(4) of MiFID II aims at identifying instruments which are complex in the perspective of investors (irrespec-tive of any reference to the risk profile of the instrument).

treated as FI with „embedded derivative“.

Page 16 / 36

2. Reportable Instrument

Page 17 / 36

Introduction 2.1

Regulatory Background 2.1.1

Transactions in financial instruments that are admitted to markets defined as a trading venue by ESMA or for which admission has been applied for (ESMA Regulated Market (RM), Multilateral Trading Facili-ty (MTF) or Organized Trading Facility (OTF)) must be reported to the supervisory authorities. The reporting duty applies irrespective of the country in which the trading venue is located if one of the following conditions applies: a) financial instruments

a. that are admitted to trading on an ESMA defined venue or b. that are traded on an ESMA defined venue or c. for which an application for admission to an ESMA defined venue has been made

b) financial instruments for which the underlying is a financial instrument traded on an ESMA defined venue c) financial instruments for which the underlying includes financial instruments traded on an ESMA defined venue (e.g. in an index or basket).

SIX classification 2.1.2

The SIX-database is used to check for all financial instruments whether they are admitted, traded or registered for admission on a trading venue defined by the regulator. In the case of financial instruments that are based on an underlying or for which the payment streams are dependent on an underlying, a check is also carried out as to whether the underlying is subject to reporting according to the criteria mentioned above. If this is the case, the financial instrument is clas-sified as reportable. In the case of composite financial instruments, financial instruments that are based on composite un-derlying or for which the payment streams are dependent on composite underlying, a check is carried out as to whether one of the instruments included in the composition is reportable according to the criteria mentioned above. If this is the case, the financial instrument is classified as reportable. SIX labels the instruments in question as "MiFID II Reportable Instruments".

Classification Reportable = Yes 2.1.2.1.

Financial instruments which are unambiguously identifiable as "reportable" are classified "reportable instrument =" Yes ".

Classification Reportable = No 2.1.2.2.

Only financial instruments which are unambiguously identifiable as "not reportable" are classified "re-portable instrument =" no ".

No classification 2.1.2.3.

Instruments for which no clear statement is possible due to missing information are not classified at all. (Example: derivative instruments with composed underlying where the components are unknown.)

Exceptions 2.1.3

Certain categories of instruments are exempted from the reporting obligation by the regulator. These exceptions are covered by the rule set and so are not labelled as "MiFID reportable instrument".

Page 18 / 36

Classification carried out by the regulator (ESMA) 2.1.3.1.

If the regulator (ESMA) of a relevant financial instrument provides the reportable classification, this is accorded priority and in this case the SIX rule set is not applied.

Instrument existing on ESMA data base 2.1.3.2.

When a financial Instrument exists on the ESMA data base it is treated like an instrument classified as reportable by ESMA.

Classification carried out by the issuer 2.1.3.3.

If the issuer of a relevant financial instrument provides the reportable classification, this is accorded priority and in this case the SIX rule set is not applied.

Page 19 / 36

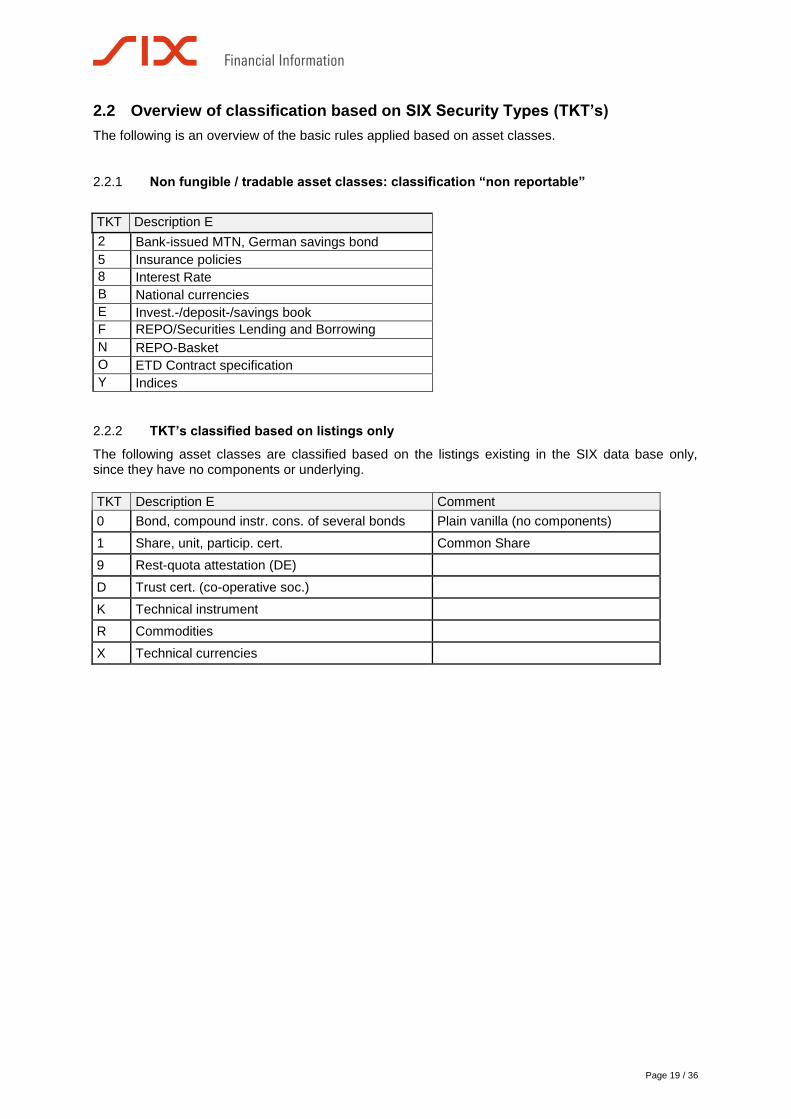

Overview of classification based on SIX Security Types (TKT’s) 2.2

The following is an overview of the basic rules applied based on asset classes.

Non fungible / tradable asset classes: classification “non reportable” 2.2.1

TKT Description E

2 Bank-issued MTN, German savings bond

5 Insurance policies

8 Interest Rate

B National currencies

E Invest.-/deposit-/savings book

F REPO/Securities Lending and Borrowing

N REPO-Basket

O ETD Contract specification

Y Indices

TKT’s classified based on listings only 2.2.2

The following asset classes are classified based on the listings existing in the SIX data base only, since they have no components or underlying.

TKT Description E Comment

0 Bond, compound instr. cons. of several bonds Plain vanilla (no components)

1 Share, unit, particip. cert. Common Share

9 Rest-quota attestation (DE)

D Trust cert. (co-operative soc.)

K Technical instrument

R Commodities

X Technical currencies

Page 20 / 36

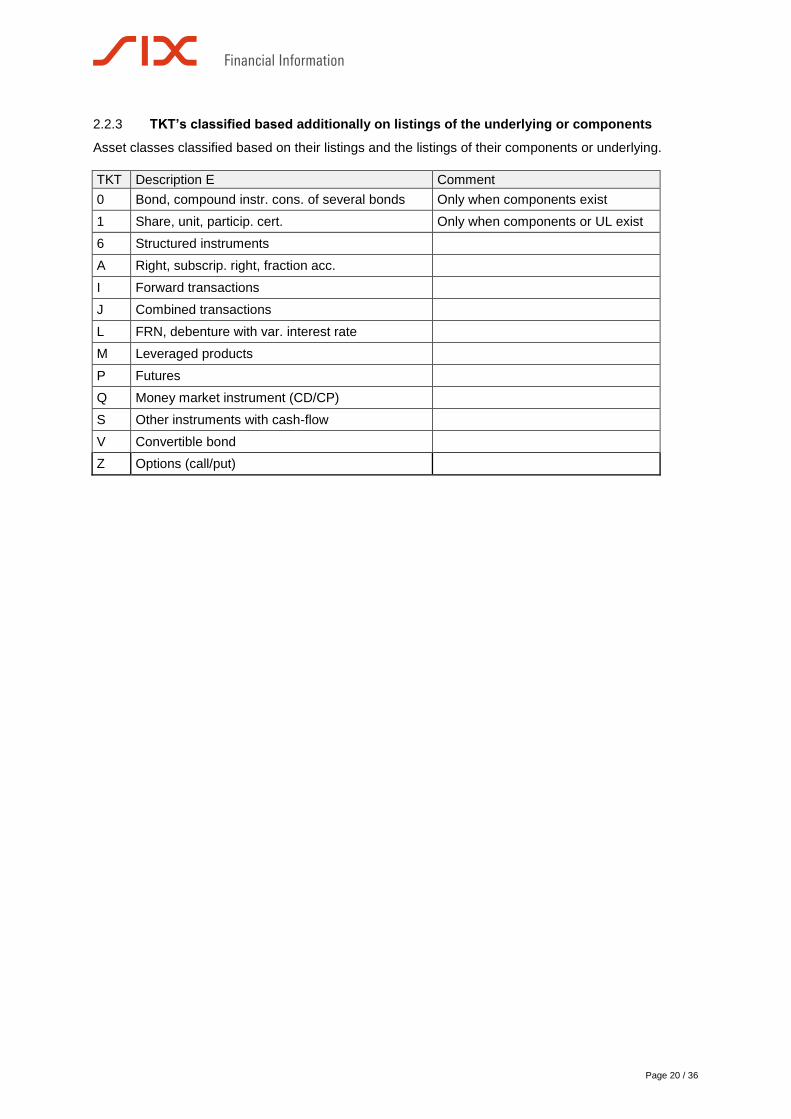

TKT’s classified based additionally on listings of the underlying or components 2.2.3

Asset classes classified based on their listings and the listings of their components or underlying.

TKT Description E Comment

0 Bond, compound instr. cons. of several bonds Only when components exist

1 Share, unit, particip. cert. Only when components or UL exist

6 Structured instruments

A Right, subscrip. right, fraction acc.

I Forward transactions

J Combined transactions

L FRN, debenture with var. interest rate

M Leveraged products

P Futures

Q Money market instrument (CD/CP)

S Other instruments with cash-flow

V Convertible bond

Z Options (call/put)

Page 21 / 36

SIX classification rule set / algorithm 2.3

Instrument existing on ESMA data base 2.3.1

If a financial instrument exists on the ESMA database, it is classified as reportable, with source of the classification = ESMA. The SIX rule set will not be applied.

Classification carried out by the issuer 2.3.2

If the issuer of a financial instrument provides the reportable classification, the classification will be delivered with “issuer” as source The SIX rule set will not be applied.

SIX classification algorithm 2.3.3

Based on the asset class / TKT of a financial instrument, the following rules are applied:

Referential (not tradable) instruments 2.3.3.1.

Non fungible / not tradable instruments are classified as “not reportable” with “SIX” as source of the classification.

Instruments with relevant listings 2.3.3.2.

Financial instruments are classified based on their listings in the SIX database. If a listing was applied for or a listing has been admitted on one of following trading venues

- ESMA Regulated Market (RM) - ESMA Multilateral Trading Facility (MTF) - or an ESMA Organized Trading Facility (OTF))

the instrument will be delivered with the classification “reportable” and “SIX” as source of the classifica-tion.

Instruments without relevant listings without components / underlying 2.3.3.3.

If a financial instrument has no relevant listing and the instrument is defined as not having components and / or underlying the classification “not reportable” and “SIX” as source of the classification will be delivered.

Instruments without relevant listings with components / underlying 2.3.3.4.

If no relevant listing exist for the instrument but the instrument is defined as having components and / or underlying, all components and / or underlying are checked NOTE: The composition funds is not analyzed (see QA on reporting of funds https://www.esma.europa.eu/sites/default/files/library/esma70-1861941480-56_qas_mifir_data_reporting.pdf).

Components / underlying available in SIX data base 2.3.3.5.

If one of the components / underlying has a relevant listing the instrument will be delivered with the classification “ reportable” and “SIX” as source of the classification. If none of the components / underlying has such a listing the classification “not reportable” and “SIX” as source of the classification will be delivered.

Page 22 / 36

Components / underlying NOT available in SIX data base 2.3.3.6.

When components / underlying are not available in the SIX data base no classification will be deliv-ered.

Page 23 / 36

3. Leveraged Instrument Indicator

Page 24 / 36

Introduction 3.1

Regulatory Background 3.1.1

MiFID II requires (Commission Delegated Regulations EU 2017/565, Art. 62, par. 2) that a client is informed as soon as an instrument is classified as "leveraged", i.e. subject to a price change of 10% or a multiple of 10%. Unfortunately, the MIFID II directive does not provide a clear definition of "leveraged". Therefore, SIX has decided to offer its customers a "leveraged" label based on a rule set of its own, based on the ESMA's answer set in ESMA Q&A 2016-1444 on investor protection topics (Question 3, page 45). This label is to be regarded as a recommendation and indicates that the instrument in ques-tion is to be checked for "leveraged" status to fulfil the regulatory requirements. No account is taken either of the change in the leverage effect because of changes in the price of the instrument or the customer's individual purchase price or position. Thus, ultimate responsibility for the classification as a "leveraged instrument" and for monitoring price changes lies with the party that manages the position for the customer. SIX uses the following definition for "leveraged": The return on the instrument (profit or loss) in relation to the return on the underlying or on the capital invested is magnified by the leverage effect.

Page 25 / 36

Technical implementation by SIX 3.2

SIX marks most instruments as "leveraged or "not leveraged" When the rule set cannot be applied, the instrument is not marked at all. For the Leveraged Instrument Indicator classification in accordance with MiFID II, SIX uses a multi-level rule set through which various requirements defined by SIX are covered and implemented. The Leveraged Instrument Indicator can be found in the VDF DOC TKFSD (Tax and Reporting / Regu-lation) as follows: VDF DOC TKFSD Country 816 (European Economic Area, EEA) Classification Level 1 M11 in segment FSL Classification Level 2 M11I01 in segment FSM Classification Level 3 (FSN, not used) Leveraged M11I01, applicability = 16 (yes) Not leveraged M11I01, applicability = 17 (no) No classification M11I01, Level2 doesn't exist

Example 3.2.1

FSL Report Reg Classification Example

7908 Classification level 1 M11 = MiFID-II - Indicators

FSM Second-Level Classification Example

7909 Classification level 2 M11I01 = Leveraged Instrument

7863 Applicability 16 = yes

2811 Valid from 02.01.2018

2812 Valid to -

7850 Allocation type 4 = by SIX

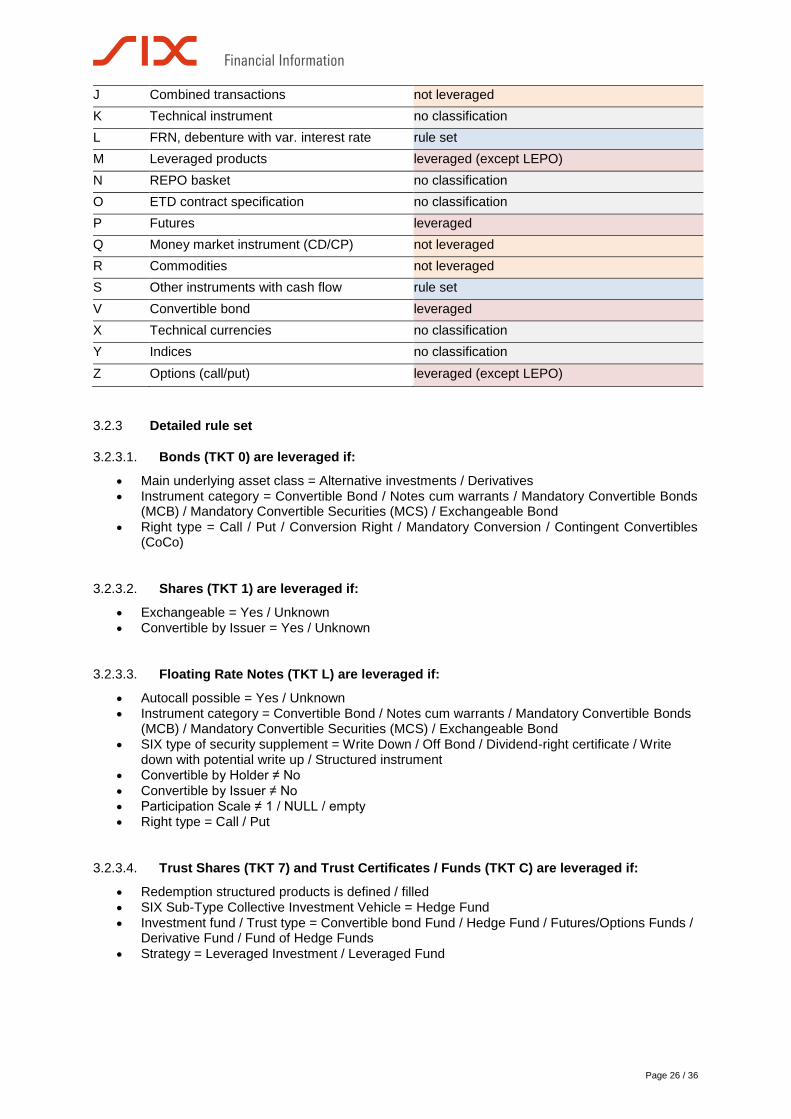

Overview by Type of Security 3.2.2

TKT Description MiFID-II Leveraged

0 Bond, compound instr. cons. of several bonds

rule set

1 Share, Unit, PS rule set

2 Bank-issued MTN, German savings bond not leveraged

5 Insurance policies no classification

6 Structured instruments rule set

7 Trust shares rule set

8 Interest rate no classification

9 Rest-quota attestation (DE) not leveraged

A Right, subscript. right, fraction acc. not leveraged

B National currencies not leveraged

C Trust cert. unit/fund, invest. foundation units rule set

D Trust cert./co-partner share not leveraged

E Invest.-/deposit-/savings book not leveraged

F REPO/securities lending and borrowing not leveraged

H Synthetic instrument no classification

I Forward transactions not leveraged

Page 26 / 36

J Combined transactions not leveraged

K Technical instrument no classification

L FRN, debenture with var. interest rate rule set

M Leveraged products leveraged (except LEPO)

N REPO basket no classification

O ETD contract specification no classification

P Futures leveraged

Q Money market instrument (CD/CP) not leveraged

R Commodities not leveraged

S Other instruments with cash flow rule set

V Convertible bond leveraged

X Technical currencies no classification

Y Indices no classification

Z Options (call/put) leveraged (except LEPO)

Detailed rule set 3.2.3

Bonds (TKT 0) are leveraged if: 3.2.3.1.

Main underlying asset class = Alternative investments / Derivatives Instrument category = Convertible Bond / Notes cum warrants / Mandatory Convertible Bonds

(MCB) / Mandatory Convertible Securities (MCS) / Exchangeable Bond

Right type = Call / Put / Conversion Right / Mandatory Conversion / Contingent Convertibles (CoCo)

Shares (TKT 1) are leveraged if: 3.2.3.2.

Exchangeable = Yes / Unknown Convertible by Issuer = Yes / Unknown

Floating Rate Notes (TKT L) are leveraged if: 3.2.3.3.

Autocall possible = Yes / Unknown Instrument category = Convertible Bond / Notes cum warrants / Mandatory Convertible Bonds

(MCB) / Mandatory Convertible Securities (MCS) / Exchangeable Bond SIX type of security supplement = Write Down / Off Bond / Dividend-right certificate / Write

down with potential write up / Structured instrument Convertible by Holder ≠ No

Convertible by Issuer ≠ No Participation Scale ≠ 1 / NULL / empty Right type = Call / Put

Trust Shares (TKT 7) and Trust Certificates / Funds (TKT C) are leveraged if: 3.2.3.4.

Redemption structured products is defined / filled SIX Sub-Type Collective Investment Vehicle = Hedge Fund

Investment fund / Trust type = Convertible bond Fund / Hedge Fund / Futures/Options Funds / Derivative Fund / Fund of Hedge Funds

Strategy = Leveraged Investment / Leveraged Fund

Page 27 / 36

Other Instruments with Cashflow (TKT S) are leveraged if: 3.2.3.5.

Instrument category = Convertible Bond / Notes cum warrants / Mandatory Convertible Bonds (MCB) / Mandatory Convertible Securities (MCS) / Exchangeable Bond

Right type = Call / Put / Conversion Right / Mandatory Conversion / Contingent Convertibles (CoCo)

Structured Instruments (TKT 6) are leveraged if: 3.2.3.6.

Participation Scale ≠ 1 / NULL / empty

Leveraged Products (TKT M), Futures (TKT P), Convertibles (TKT V), Options (TKT Z) 3.2.3.7.are leveraged if:

Always

Only LEPOs are not leveraged

Bank-issued MTN, German savings bond (TKT 2), Rest-quota attestation (DE) (TKT 9), Right, subscrip. right, fraction acc. (TKT A), National currencies (TKT B), Trust cert/Co-partner share (TKT D), Invest.-/deposit-/savings book (TKT E), REPO/Securities Lending and Borrowing (TKT F), Forward transactions (TKT I), Combined transactions (TKT J), Money market instru-ment (CD/CP) (TKT Q), Commodities (TKT R) are always NOT leveraged

Insurance policies (TKT 5), Interest Rate (TKT 8), Synthetic instrument (TKT H), Technical in-strument (TKT K), REPO-Basket (TKT N), ETD Contract specification (TKT O), Technical cur-rencies (TKT X), Indices (TKT Y) are not covered by the rule set and therefore not marked at all

Page 28 / 36

4. Automated Filling of Target Market Data

Page 29 / 36

Introduction 4.1

Regulatory Background 4.1.1

From a regulatory perspective, guidelines for manufacturers and distributors to identify the target mar-ket for their products as required in the ESMA Final Report "Guidelines on MiFID II product govern-ance requirements" from June 2017 ESMA, sets five criteria that manufacturers and distributors should use as a basis for defining the target market for their products:

1. Type of clients to whom the product is targeted 2. Knowledge and experience 3. Financial situation with a focus on their ability to bear losses 4. Risk tolerance and compatibility of the product's risk/reward profile with the target market 5. Clients' objectives and needs

Additionally, manufacturers should specify the appropriate distribution channel. Although ESMA's sets guidance on defining the target market, it does not provide exact details. This leads to different interpretations and presents challenges for efficient implementation. Different meth-odologies are currently being developed by industry associations or national authorities which, alt-hough aligned in general, differ in terms of the detail. SIX is part of the various discussions to provide a more harmonized template for target market assessment information. Currently the European MiFID II Template EMT V1.0 is used as reference.

Page 30 / 36

Technical implementation by SIX 4.2

The allocation type for automatically filled target market data is "by SIX". As soon as an issuer or an intermediary provides target market data, the automatic filling is stopped and all target market data with allocation type "by SIX" will be removed.

Default Values per IBT Code 4.2.1

For each IBT code, there is a set of default values defined, which is used to set all target market data (M21 to M27, M28 and M29 are reserve). The exception is for the ones described in chapters 4.2.4 and 4.2.5 which will be calculated.

Instruments with EUSIPA Code but no (valid) IBT Code 4.2.2

Each EUSIPA code can be connected with many IBT codes (one-to-many relationship). For instruments with an EUSIPA code but without IBT code, there has been built a special one-to-one relationship, matching an EUSIPA code with the first connected IBT code. This one-to-one relationship can be used to apply the default values of the selected IBT code to the instrument with EUSIPA code.

Instruments without EUSIPA and IBT Code 4.2.3

Extra default values have been defined for instruments without EUSIPA and IBT codes. These instru-ments are divided into the following groups which are identified by virtual IBT codes (0000xx):

000010: Futures (TKT P)

000011: Options (TKT Z)

000020: Equities non-complex (TKT 1 with M10C02 "non-complex instrument" = Liable/ appli-cable (1)

000021: Equities complex (TKT 1 with M10C01 "complex instrument" = Liable/ applicable (1)

000030: Bonds non-complex (TKT 0/L/V with M10C01 "complex instrument" = does not exist (NULL)

000031: Bonds complex with guarantee or seniority (TKT 0/L/V with M10C01 "complex instru-ment" = Liable/ applicable (1) and guarantee code = joint guarantee total / state guarantee / collateral / covered bond / covered bond under specific law or ranking = senior / super senior

000032: Bonds complex without guarantee and without seniority (TKT 0/L/V with M10C01 "complex instrument" = Liable / applicable (1) and guarantee code ≠ joint guarantee total / state guarantee / collateral / covered bond / covered bond under specific law and ranking ≠ senior / super senior

Calculation of Capital Protection 4.2.4

The handling of the four fields for "Ability to bear Losses" is divided into two separate rules:

No protection 4.2.4.1.

M23T03 "not protected capital" and M23T04 "loss of more than capital" are set according to the default values in the IBT TM table

Full or partial protection 4.2.4.2.

M23T01 "fully protected capital "and M23T02 "partially protected capital " as well as the value in M23T02V1 "percentage loss definition" are calculated as follows:

If protection level in % >= 100%, then for M23T01 "Fully protected capital" and M23T02 "Par-tially protected capital" the Classification Object is set to 41 "Yes" (both = positive target mar-ket)

If protection level in % < 100% and > 0%, then for M23T01 "Fully protected capital" the Classi-fication Object is set to 42 "No" (= negative target market) and for M23T02 "Partially protected capital" the Classification Object is set to 41 "Yes" (= positive target market)

Page 31 / 36

If protection level in % <= 0%, then for M23T01 "Fully protected capital" and M23T02 "Partially protected capital" the Classification Object is set to 42 "No" (both = negative target market)

The value for the protection level in % is stored in Classification Level 3: M23T02V1: Percentage loss definition

Calculation of Time Horizon and Recommended Holding Period 4.2.5

Recommended Holding Period (RHP) 4.2.5.1.

If not provided by the issuer, the RHP is calculated daily as difference between Maturity / Expiry Date and the current date and expressed in whole years (rounded down) in classification level 3 (M25T05V1). Example: 14 months 1 year or 9 months 0 years If an instrument has no maturity / expiry date, the RHP will be set by default to 1 day for derivatives (options, futures, leveraged products and warrants) and 5 years for all other instruments. Matured or expired instruments have nor RHP (M25T05V1 does not exist). Additionally to the common Time Unit (2902) and Number of Time Units (6921) the RHP will be stored according to the European Mifid Template (EMT) as a decimal number in years in element 6911.

Time Horizon 4.2.5.2.

The automatic filling of the time horizon (M25T01 – M25T04) is derived from the RHP (M25T05V1) either provided by issuer or calculated by SIX according to the following rule:

M25T04: very short term = RHP in whole years rounded down >= 0 and < 1

M25T01: short term = RHP in whole years rounded down >= 1 and < 3

M25T02: medium term = RHP in whole years rounded down >= 3 and < 5

M25T03: long term = RHP in whole years rounded down >= 5 The horizon period matching the RHP will be marked as positive target market (classification object = 41 "yes"), all other periods will be marked as negative target market (classification object = 42 "no"). As the instrument ages the time horizon will be altered in time.

Page 32 / 36

5. Commodity Derivative Indicator

Page 33 / 36

Introduction 5.1

Regulatory Background 5.1.1

Indication as to whether the financial instrument falls within the definition of commodities derivative is under Article 2(1)(30) of Regulation (EU) No 600/2014. The definition of "commodity derivative" under Article 4(1)(50) of MiFID II cross references the defini-tion of commodity derivative under Article 2(1)(30) of MiFIR which states 'commodity derivative' means those financial instruments defined in Article 4(1)(44)(c) of MiFID II; which relate to a commodity or an underlying referred to in Section C(10) of Annex I [of MiFID II]; or in points (5), (6), (7) and (10) of Sec-tion C of Annex I thereto. Other source: http://www.emissions-euets.com/internal-electricity-market-glossary/677-commodity-derivatives.

Regulatory Technical Standards 5.1.1.1.

RTS 23, regulatory technical standards on supply of financial instruments reference data under Article 27 of MiFIR, Annex, Table-3, Field-4. Exception Exchange Traded Commodities ETCs Exchange traded commodities (ETCs) are debt instruments which are within the scope of Article 4(1)(44)(b) of MiFID II and are classified as such in RTS 2. Therefore, they are outside the definition of commodity derivatives in Article 2(1)(30) of MiFIR and the position limits regime does not apply to them. (ETCs_esma70-872942901-28_cdtf_qas)

Page 34 / 36

Technical implementation by SIX 5.2

There will be different schemas for the Classification Level 1, e.g.: ESMA II Indicators, and the corre-sponding Classification Level 2 for determining the Commodity derivative indicator (Yes/No). To classify the Commodity Derivative Indicator in the sense of MiFID-II, SIX uses a multi-level set of rules, in which various requirements defined by SIX are taken into account and implemented. In a first step, the following classification is made on the basis of the title category or where financial instrument has an index as underying and this is a commodity. The Leveraged Instrument Indicator can be found in the VDF DOC TKFSD (Tax and Reporting / Regu-lation) as follows: VDF DOC TKFSD Country 816 (European Economic Area, EEA) Classification Level 1 M11 in segment FSL Classification Level 2 M11I03 in segment FSM Classification Level 3 (FSN, not used) Commodity derivative indicator M11I03, applicability = 16 (yes) Commodity derivative indicator M11I03, applicability = 17 (no) doesn't exist No classification M11I03, Level2 doesn't exist

Example 5.2.1

FSL Report Reg Classification Example

7908 Classification level 1 M11 = MiFID-II - Indicators

FSM Second-Level Classification Example

7909 Classification level 2 M11I03 = Commodity derivative indicator

7863 Applicability 16 = yes

2811 Valid from 02.01.2018

2812 Valid to -

7850 Allocation type 4 = by SIX

Overview by Type of Security 5.2.2

TKT Description MiFID II - Commodity derivative indicator

6 Structured instruments rule set

M Options (certificates), warrants rule set

P Futures rule set

Z Options (Call/Put) rule set

6,M The underlying is an index (= commodity) rule set

All other title category no mentioned in this table

no classification

General rules for all rule sets 5.2.3

Country codes 5.2.3.1.

All classifications in the specified rule sets are for MIFID II in general and must be stored under country code = 816 (EEA).

Instrument status 5.2.3.2.

Only active instruments will be processed in the rule sets and therefore the following rule applies.

Page 35 / 36

Detailed rule set MiFID II Commodity derivative indicator 5.2.4

When an instrument is opened or mutated into one of the corresponding security types, the " Com-modity derivative indicator" mark must be set. Leveraged and structured Products (TKT M) and (TM 6) The check must be carried out upon opening or mutation from / to the corresponding security type.

Certificate type is not an ETC ( Exchange Traded Commodity) Underlying key is a commodity

Commodity exists and is not: Emission Reduction Units (ERU), Emission Reduction Units (ERU), European Union Allowances (EUA) or European Union Aviation Allowances (EUAA)

Futures (TKT P) and Options (TKT Z)

Underlying key is a commodity Commodity exists and is not: Emission Reduction Units (ERU), Emission Reduction Units

(ERU), European Union Allowances (EUA) or European Union Aviation Allowances (EUAA)

Page 36 / 36

6. Additional Support and Documentation

For additional support, information and updates to this and other related documents, please go to the following websites: SIX MiFID II Website https://www.six-financial-information.com/en/site/mifid-ii.html SIX MiFID II User Group http://marketing.six-financial-information.com/mifid-ii-working-group-log-in SIX Financial Information Website https://www.six-financial-information.com/en/home.html#country=xx