Embed Size (px)

Citation preview

SIRC OF ICAI

SEMINAR ON ENABLING SERVICE TAX.

DEFINITION OF SERVICE, DECLARED SERVICE AND PLACE OF PROVISION RULEAND PLACE OF PROVISION RULE

By

CA V.P.MANAVALAN

Chartered Accountant

I. BASIC EXEMPTION.

II.DEFINITION OF SERVICE.

III.DECLARED SERVICE.

IV.PLACE OF PROVISION OF SERVICES

RULERULE

I. BASIC EXEMPTION. NOTIFICATION NO

33/2012

APPLICABILITY.

For all service provider

THRESHOLD LIMIT

The Central Government, being satisfied that it isIThe Central Government, being satisfied that it is

necessary in the public interest so to do, hereby exempts

taxable services of aggregate value not exceeding ten

lakh rupees in any financial year from the whole of the

service tax

I BASIC EXEMPTION

MEANING OF AGGREGATE VALUE

Aggregate value" means the sum total of value of taxable services

charged in the first consecutive invoices issued during a financial

year but does not include value charged in invoices issued towards

such services which are exempt from whole of service tax leviable

thereon under section 66B of the said Finance Act under any other

notification.

NON-APPLICABILITY OF EXEMPTION

i) Taxable services provided under a brand name or trade name.

(ii) Recipient of service

1.The insurance business

2. Goods Transport Services.2. Goods Transport Services.

3.Sponsorship services to anybody corporate or partnership firm.

4. An arbitral tribunal.

5. Legal services –Individual or Firm Advocates

Continue..

6. Support services to Government

7. Services provided by Directors to the Company

8. Cab Services

9. Supply of Manpower services.9. Supply of Manpower services.

10. Work contract services.

CONDITION FOR CLAIMING EXEMPTION.

1. The Exemption is optional

2. No CENVAT Credit on input, input services and Capital goods

3. Taxable services provided in all the premises shall be taken into

account.account.

4.The aggregate value of taxable services rendered by a provider of

taxable service from one or more premises, does not exceeds ten

lakh rupees in the preceding financial year.

CASE STUDY

1. X is a service providers provides services for Rs 25lakhs during financial year 2011-12 and providesservices of Rs 7.50 lakhs during financial year 2012-13and provides services of Rs 30 lakhs during theFinancial Year 2013-14what is the obligation underFinancial Year 2013-14what is the obligation underService Tax law for the financial Year 2011-12,2012-13and 2013-14.

CASE STUDY

2. A & Co provides original works under works contract service for Rs 23lacs during financial year 2012-13.

Whether A& CO can claim the basic exemption? and what is the taxliability under service tax?

3. X & CO provides construction of commercial complex and provides3. X & CO provides construction of commercial complex and providesservices for Rs 15 lacs during the financial year 2012-13. What is the taxliability under service tax?

There are five Individuals are co-owners of a particular

building and have rented out the premises for Rs 30 lacs to

a persons who issues different cheques to all the above

individuals, as they are co-owners. Whether the aggregate

value of the taxable services rendered by each person can

be considered for the purpose of claiming basic exemption.

II DEFINITION OF SERVICE

WHAT IS SERVICE

• SERVICE MUST BE AN ACTIVITY.

• ACTIVITY FOR ONE PERSON TO ANOTHER PERSON.

• ACITIVITY FOR A CONSIDERATION.• ACITIVITY FOR A CONSIDERATION.

• ACTIVITY MUST BE IN DECLARED SERVICES.

• ACTIVITY SHOULD NOT BE IN NEGATIVE LIST OF SERVICES.

• ACTIVITY SHOULD NOT BE IN EXEMPTED LIST OF SERVICES

WHAT IS AN ACTIVITY

• Activity’ has not been defined in the Act. In termsof the common understanding of the wordactivity would include an act done, a work done,a deed done, an operation carried out, executionof an act, provision of a facility etc. It is a termwith very wide connotation.of an act, provision of a facility etc. It is a termwith very wide connotation.

• Activity could be active or passive and would alsoinclude forbearance to act. Agreeing to anobligation to refrain from an act or to tolerate anact or a situation has been specifically listed as adeclared service under section 66E of the Act.

ONE PERSON TO ANOTHER PERSON

• The phrase ‘provided by one person to

another’ signifies that services provided by a

person to self are outside the ambit of taxable

service. Example of such service would includeservice. Example of such service would include

a service provided by one branch of a

company to another or to its head office or

vice-versa.

MEANING OF THE PERSON

• an individual

• a Hindu undivided family

• a company

• a society

• a limited liability partnership• a limited liability partnership

• a firm

• an association or body of individuals, whether incorporated or not

• Government

• a local authority, or

• every artificial juridical person, not falling within any of the preceding sub-clauses.

EXCEPTION TO THE SELF SERVICE

• an establishment of a person located in taxableterritory and another establishment of suchperson located in non-taxable territory aretreated as establishments of distinct persons.[Similar provision exists presently in section 66A[Similar provision exists presently in section 66A(2)].

• an unincorporated association or body of personsand members thereof are also treated as distinctpersons. [Also exists presently in part asexplanation to section 65].

CONSIDERATION

• As per Explanation (a) to section 67 of the Act“consideration” includes any amount that is payable forthe taxable services provided or to be provided.

• In simple terms, ‘consideration’ means everythingreceived or recoverable in return for a provision ofreceived or recoverable in return for a provision ofservice which includes monetary payment and anyconsideration of non- monetary nature or deferredconsideration as well as recharges betweenestablishments located in a non-taxable territory onone hand and taxable territory on the other hand.

III.DECLARED SERVICE (SECTION 66E)

Declared service means any activity carried out

by a person for another person for

consideration and declared as such underconsideration and declared as such under

section 66E

1.Renting of immovable propertyMeaning of Rent

allowing,

Permitting

or granting access,

entry,

occupation, use or any such facility, wholly or partly, in an immovable property,

with or without the transfer of possession or control of the said immovable with or without the transfer of possession or control of the said immovable

property

and includes

letting,

leasing,

licensing

or other similar arrangements in respect of immovable property;

EXEMPTION FOR RENTING OF IMMOVABLE

PROPERTY

1.services by way of renting of residential dwelling for use as residence

2.Services by a hotel, inn, guest house, club, campsite or meant for residential

or lodging purposes, having declared tariff of a unit of accommodation below

rupees one thousand per day or equivalent

declared tariff" includes charges for all amenities provided in the unit of

accommodation (given on rent for stay) like furniture, air-conditioner,

refrigerators or any other amenities, but without excluding any discount

offered on the published charges for such unit;

Case Study

• Mr. Arun is an owner of properties gives the following particulars explain taxability.

• (all sums are exclusive tax, if any)– Renting of commercial properties: Rs.21 lakhs (property tax paid

Rs.100000 and interest / fine of Rs. 10000 was also paid)

– Licensing arrangement in respect of immovable properties Rs. 4 – Licensing arrangement in respect of immovable properties Rs. 4 lakhs.

– Rent earned from an inn Rs. 2 lakhs (declared tariff per day Rs.900)

– Rent earned another inn Rs. 2 lakhs (declared tariff per day Rs. 1000 but actual rent was charged @ Rs. 900 per day)

– Renting of residential dwelling for use as residence Rs. 4 lakhs.

– Renting of non – residential building for use as residence Rs. 5 lakhs.

Contd.,

– Renting of residential dwelling for commercial purposes Rs. 6 lakhs.

– Renting of building located at Jammu and Kashmir Rs. 2 lakhs.

– Renting of vacant land for agricultural purpose Rs. 3 lakhs.

– Renting of school building to a higher secondary school Rs. 3 lakhs.lakhs.

– Renting of land for circus Rs. 4 lakhs.

– Permitting placement of vending machines at premises Rs. 1 lakhs.

– Allowing mobile tower to be placed at rooftop Rs. 4 lakhs.

– whether Service Tax is payable on the Pop corns served in Open Food Courts in Centrally Air Conditioned Express Avenue Malls? what if the food courts also provide meals?

2.CONSTRUCTION OF COMPLEX

construction of a complex includes additions, alterations,

replacements, or Remodeling of any existing civil structure

building,

civil structure

or a part thereof,

including a complexincluding a complex

or building intended for sale to a buyer,

wholly or partly, except where the entire consideration is

received after issuance of completion certificate by the

competent authority.

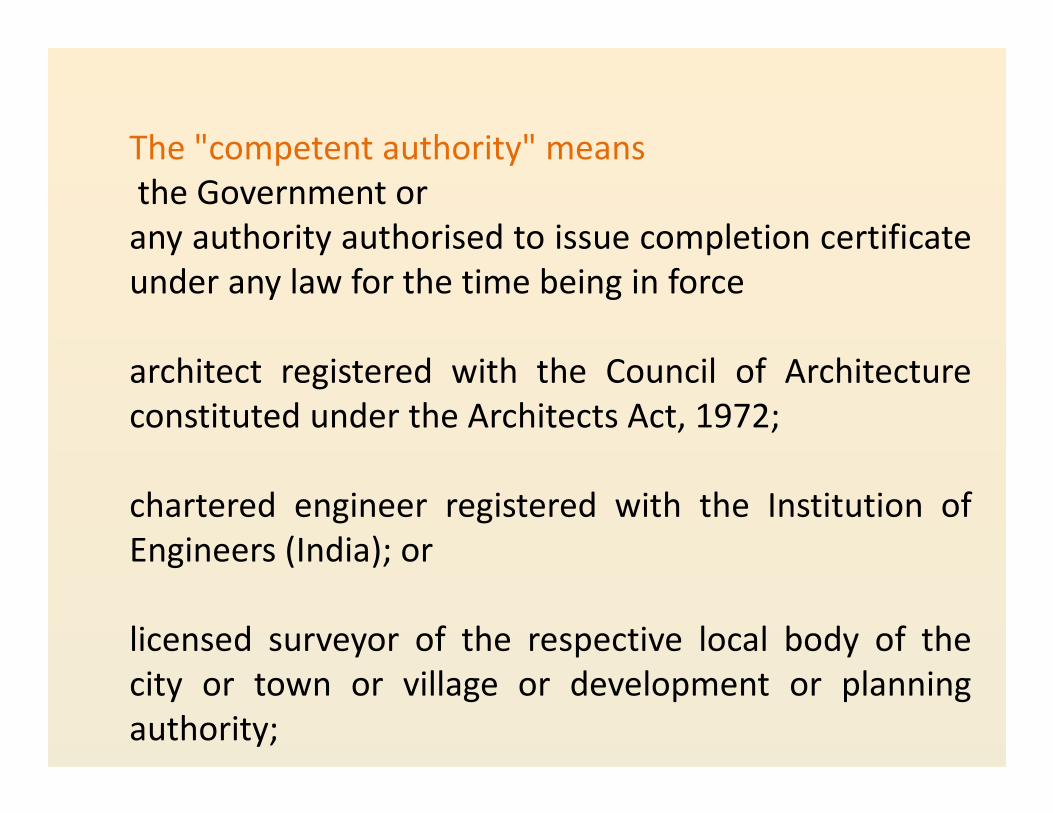

The "competent authority" means

the Government or

any authority authorised to issue completion certificate

under any law for the time being in force

architect registered with the Council of Architecture

constituted under the Architects Act, 1972;constituted under the Architects Act, 1972;

chartered engineer registered with the Institution of

Engineers (India); or

licensed surveyor of the respective local body of the

city or town or village or development or planning

authority;

EXEMPTION UNDER CONSTRUCTION

SERVICES.• A. Services provided to the government, a local authority

or a governmental authority

• Services provided to the Government, a local authority or a governmental authority by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, or alteration of -commissioning, installation, completion, fitting out, repair, maintenance, renovation, or alteration of -

– (a) a civil structure or any other original works meant predominantly for use other than for commerce, industry, or any other business or profession;

– (b) a historical monument, archaeological site or remains of national importance, archaeological excavation, or antiquity specified under the Ancient Monuments and Archaeological Sites and Remains Act, 1958 (24 of 1958);

Contd.,

– (c) a structure meant predominantly for use as (i) an

educational, (ii) a clinical, or (iii) an art or cultural

establishment;

– (d) canal, dam or other irrigation works;

– (e) pipeline, conduit or plant for (i) water supply (ii) water – (e) pipeline, conduit or plant for (i) water supply (ii) water

treatment, or (iii) sewerage treatment or disposal; or

– (f) a residential complex predominantly meant for self-use

or the use of their employees or other persons specified in

the Explanation 1 to clause 44 of section 65B of the said

Act

Contd.,

• Governmental authority ?

It means a board, or an authority or any other body

established with 90% or more participation by way of equity

or control by Government and set up by an Act of the

Parliament or a State Legislature to carry out any function Parliament or a State Legislature to carry out any function

entrusted to a municipality under article 243W of the

Constitution;

Contd.,

B. Services provided by way of construction, erection.Services provided by way of construction, erection, commissioning, installation, completion, fitting out, repair, maintenance, renovation, or alteration of,-

– (a) a road, bridge, tunnel, or terminal for road transportation for use by general public;

– (b) a civil structure or any other original works pertaining to a scheme – (b) a civil structure or any other original works pertaining to a scheme under Jawaharlal Nehru National Urban Renewal Mission or Rajiv AwaasYojana;

– (c) a building owned by an entity registered under section 12AA of the Income tax Act, 1961(43 of 1961) and meant predominantly for religious use by general public;

– (d) a pollution control or effluent treatment plant, except located as a part of a factory; or a structure meant for funeral, burial or cremation of deceased;

Contd.,

• C. Services by way of construction, erection, commissioning,

or installation

of original works pertaining to,-

– (a) an airport, port or railways, including monorail or metro;

– (b) a single residential unit otherwise than as a part of a residential complex

– (c) low-cost houses up to a carpet area of 60 square meters per house in a

housing project approved by competent authority empowered under the

Scheme of Affordable Housing in Partnership’ framed by the Ministry of

Housing and Urban Poverty Alleviation, Government of India;

– (d) Post-harvest storage infrastructure for agricultural produce including a

cold storages for such purposes; or

– (e) Mechanized food grain handling system, machinery or equipment for

units processing agricultural produce as food stuff excluding alcoholic

beverages

Contd.,

• Single residential unit

It means a self-contained residential unit which is designed for use, wholly

or principally, for residential purposes for one family

• Residential complex• Residential complex

It means any complex comprising of a building or buildings, having more

than one s ingle residential unit

• Original works

It means has the meaning assigned to it in Rule 2A of the Service Tax

(Determination of Value) Rules, 2006

Case study

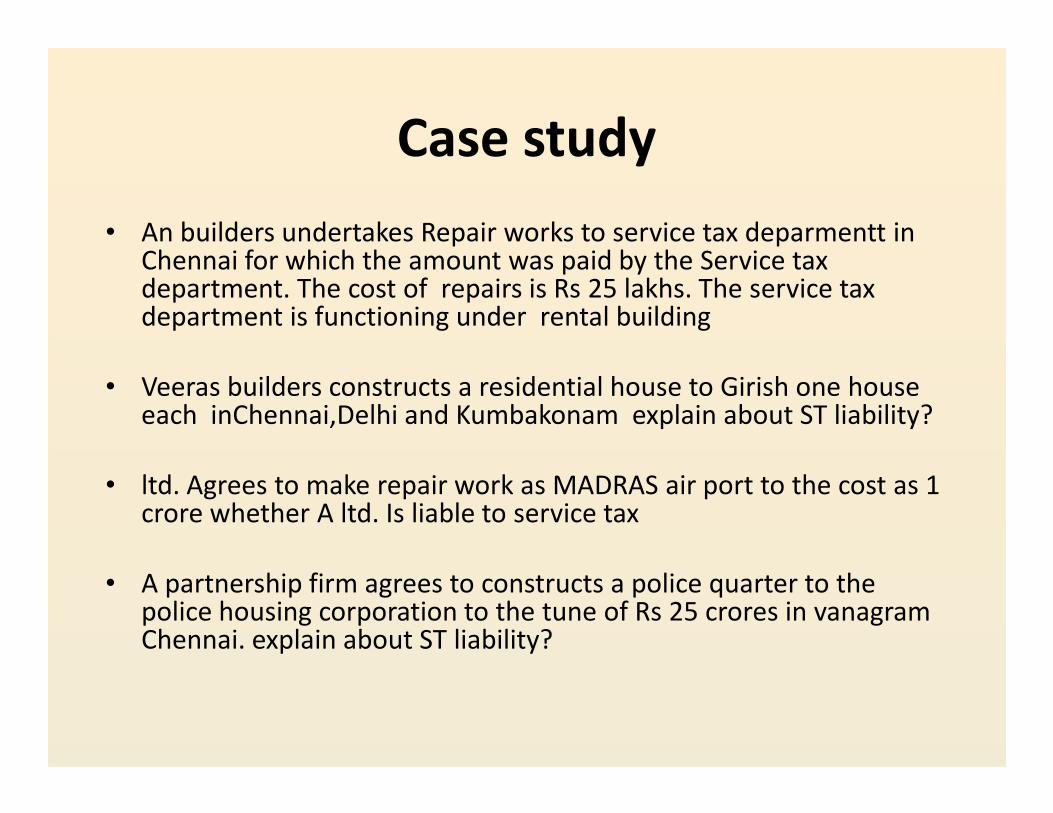

• An builders undertakes Repair works to service tax deparmentt in Chennai for which the amount was paid by the Service tax department. The cost of repairs is Rs 25 lakhs. The service tax department is functioning under rental building

• Veeras builders constructs a residential house to Girish one house each inChennai,Delhi and Kumbakonam explain about ST liability?each inChennai,Delhi and Kumbakonam explain about ST liability?

• ltd. Agrees to make repair work as MADRAS air port to the cost as 1 crore whether A ltd. Is liable to service tax

• A partnership firm agrees to constructs a police quarter to the police housing corporation to the tune of Rs 25 crores in vanagramChennai. explain about ST liability?

Contd.,

• A builders undertakes a repair work for Rs 3 crore to the SBI 7th floor explain about ST liability?

• X ltd. a building developer situated in jammu and Kashmir ask a Anand builders in Tiruchi to constructs a shopping complex in kumbakonam. explain about ST liability to x ltd?

• ABC ltd has entered into a contract for construction of road • ABC ltd has entered into a contract for construction of road meant for general public. ABC ltd sub contracts the aforesaid work to three contractors namely:

• Aruna Ltd , the work of site formation for construction of road

• Anand Builders Ltd , laying the surface of road

• Varun Ltd , other physical activities in respect of such roads.

Contd.,

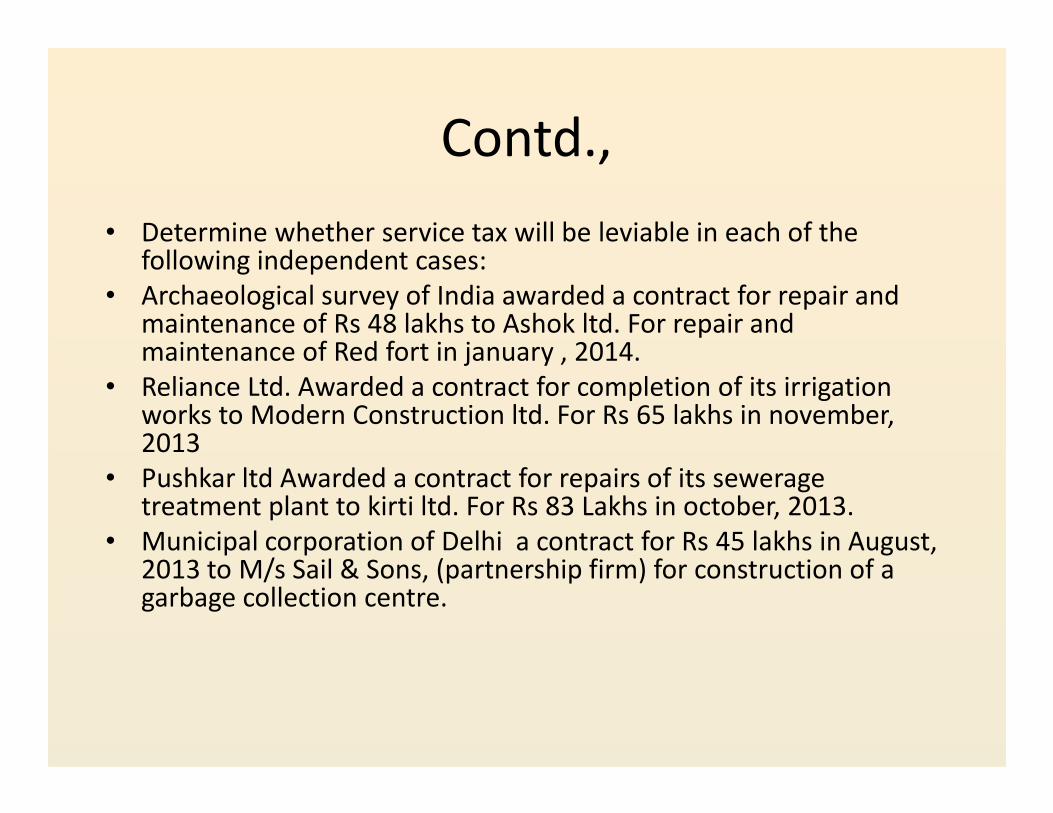

• Determine whether service tax will be leviable in each of the following independent cases:

• Archaeological survey of India awarded a contract for repair and maintenance of Rs 48 lakhs to Ashok ltd. For repair and maintenance of Red fort in january , 2014.

• Reliance Ltd. Awarded a contract for completion of its irrigation works to Modern Construction ltd. For Rs 65 lakhs in november, works to Modern Construction ltd. For Rs 65 lakhs in november, 2013

• Pushkar ltd Awarded a contract for repairs of its sewerage treatment plant to kirti ltd. For Rs 83 Lakhs in october, 2013.

• Municipal corporation of Delhi a contract for Rs 45 lakhs in August, 2013 to M/s Sail & Sons, (partnership firm) for construction of a garbage collection centre.

3.INTELLECTUAL PROPERTY RIGHT

Temporary transfer or permitting the

use or enjoyment of any intellectual

property right;property right;

IPR Includes

Trade Mark.

Copy Right

Patents

Design

EXEMPTION

Temporary transfer or permitting the use or

enjoyment of a copyright covered under

clauses (a) or (b) of sub-section (1) of section

13 of the Indian Copyright Act, 1957 relating to13 of the Indian Copyright Act, 1957 relating to

original literary, dramatic, musical, artistic

works or cinematograph films;

CASE STUDY

1.Sir Company A had entered into a contract with a TV Channel for production

of a TV serial in Tamil. It produces the serial and transfers all the rights in the

serial to the Channel for a fee of Rs.3 lakhs per episode. Company A is free to

sell the dubbed versions to other regional language channels. Company A is

charging service tax on its billing to the TV channel. Is it right for Company A

to charge service tax or Company A should only be collecting VAT from the TV

Channel?

2. A company using designs for making machinery, designs supplied by

principal owner outside India. The Indian Co. made provisions of payment of

royalty on design charges on percentage of sale of machinery. The actual

payment was not made only provisions were there in B/S for 2011-12, 2012-

13. Will the service tax arise on provision of royalty amount ?

3.Sir Prior to 1.4.2013 any transaction w.r.t. temp. trfr. of rights in films were

exempt - be it temp. trfr. by producer to distributor, dist. to sub dist., temp.

trfr. of satellite rights,etc. However, from 1.4.2013 (Notifi. no.3/2013-ST,

dated 1-3-2013), only temp. trfr. of film rights to cinema theatres is exempt

for service tax. Temp. transfer by producer to distributor, sale of satellite

rights for temp. period etc. are subjected to service tax. Is my understanding

correct?

4. If a company creates a mobile application and charges users on per

download basis from portals such as itunes/google play. Whether such

revenue is taxable under "permitting use of IPR". or is is "IT softwarerevenue is taxable under "permitting use of IPR". or is is "IT software

service"? How is the place of provision determined if users from anywhere in

the world can download?

4.INFORMATION TECHNOLOGY

SOFTARE

Taxability.

Software development,

Software design,

Software programming, Software programming,

Software customisation,

Software adaptation,

Software upgradation,

Software enhancement, implementation

MEANING OF IT SOFTWARE

Any representation of instructions, data, sound

or image, including source code and object

code, recorded in a machine readable form,

and capable of being manipulated or providingand capable of being manipulated or providing

interactivity to a user, by means of a computer

or an automatic data processing machine or

any other device or equipment;

CASE STUDY

1.The assessee is providing Website Development & Maintenance and software

Development & maintenance,upgradation services to the clients situated outside

India. He is receiving money in foreign currency. This services are used by the

clients solely outside India. Whether the assessee is liable for service tax on it?

2. My Client is engaged in the business of software development that consist of

both Packaged Software as well as the customized software (as per the

requirement of clients) .Now he want to know following:- 1:- Is Service tax and VATrequirement of clients) .Now he want to know following:- 1:- Is Service tax and VAT

both is applicable on Packaged Software ? if yes then at what rate ? 2:- Is Service

tax and VAT is applicable on customized Software ? if yes then at what rate ?

3. A person make an app. & sell it to google. whether this transaction attrect

service tax? & Can ans get change if he sell app to a indian co.? if yes, give the

reason for same

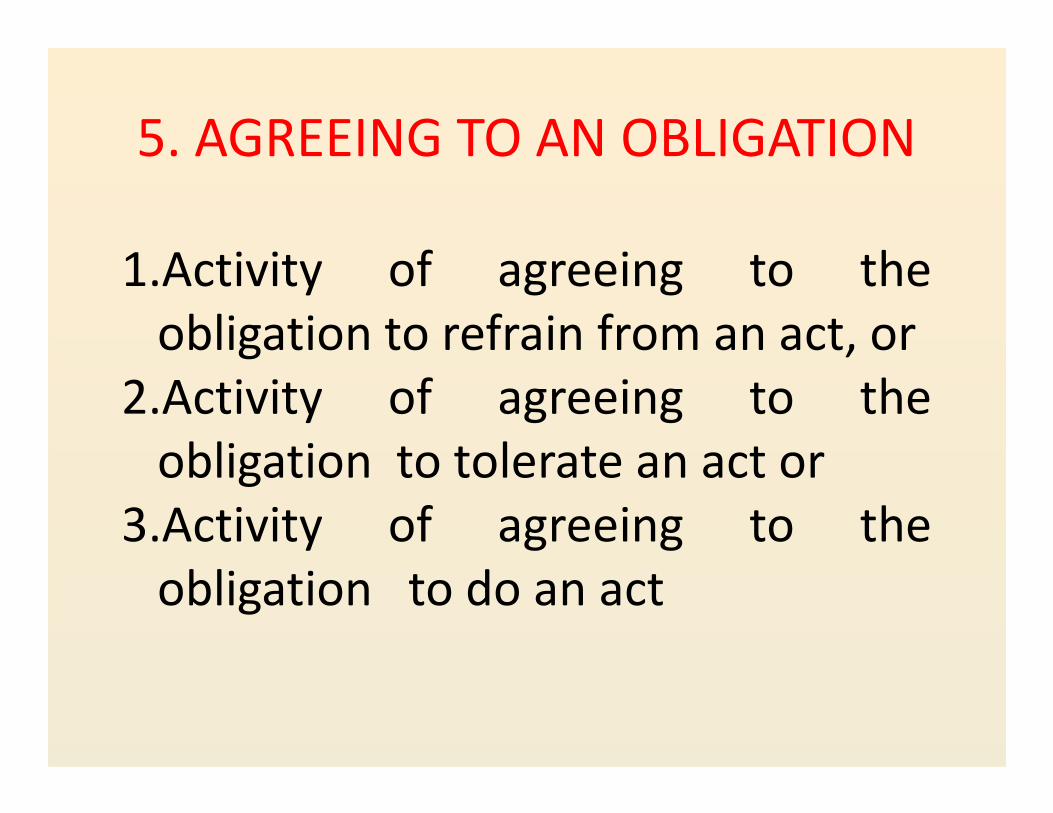

5. AGREEING TO AN OBLIGATION

1.Activity of agreeing to the

obligation to refrain from an act, or

2.Activity of agreeing to the2.Activity of agreeing to the

obligation to tolerate an act or

3.Activity of agreeing to the

obligation to do an act

CASE STUDY

1.ABC Pvt Ltd is a motor car dealer. If the customer cancels the booking of the car, then

ABC Pvt Ltd refunds the booking advance, after retaining a certain sum towards the

expenses incurred on cost of postage and other incidental charges incurred by ABC Pvt

Ltd while booking the car on behalf of the customer.whether such sum retained towards

the expenses, liable for service tax?

2. A Ltd. has entered into an agreement for Purchase of goods (M S Channel) with B Ltd,2. A Ltd. has entered into an agreement for Purchase of goods (M S Channel) with B Ltd,

A Ltd. Cancelled the purchase order, and as per the agreement between the parties A

Ltd. is liable to pay the compensation to B Ltd in case of Cancellation of purchase order.

A Ltd. paid compensation of 60 lakhs to B Ltd. Is service tax is attracted on payment of

such compensation amount?

3. We are company manufacturing and trading in coal (mineral). We do receive

Liquidated damages if buyer does not lift coal in stipulated period and we do charge

penalty from our suppliers of spares as penalty for late delivery. Does both above attract

Service Tax?

6. TRANSFER OF GOODSBY WAY OF

HIRING

Transfer of goods by way of hiring,

leasing, licensing or in any such manner

without transfer of right to use suchwithout transfer of right to use such

goods;

CASE STUDY

1.Our Company has given vessel(Dredging Vessel) on hire to a Co.(including labours

for work) from whom we get monthly hire charges. Hire Charges comprises of

Monthly Vessel hire charges as well includes labour charges. whether Service tax is

liablie as hire of goods if yes then any abatement is there or ST is payable of Full

Hire amount?

2. If the owner of an elephant, giving his elephant on hire to (i) a timber

merchant/mill for lifting/removing the wood articles or (ii) the organisers of a

festival to make that festival more colourful/attractive, then that service of renting

the elephant, without transfering the right to use and effective control of the

elephant, can be brought under any of the taxable category under the Finance Act

?

7.GOODS UNDER HIRE PURCHASE

Activities in relation to delivery of

goods on hire purchase or any

system of payment by instalmentssystem of payment by instalments

8.WORKS CONTRACT

works contract" means a contract wherein transfer of

property in goods involved in the execution of such

contract is leviable to tax as sale of goods and such

contract is for the purpose of carrying out construction,

erection, commissioning, installation, completion, fittingerection, commissioning, installation, completion, fitting

out, repair, maintenance, renovation, alteration of any

movable or immovable property or for carrying out any

other similar activity or a part thereof in relation to such

propety;

CASE STUDY

1.Dear Sir, ABC P Ltd is constructing a new housing society. R ltd has constructed

the brick work and made ready the structure. S Ltd is doing the work of

plastering, Tiling, sanitation & Finishing (with material) (Building is under

construction and new, without use). whether S Ltd will charge service tax @40%

(assuming new construction) OR will charge service tax @70%. (assuming it as

completion & Finishing services as mentioned in Rule 2A(ii)(B)(ii) of the Valuation

rules.rules.

2 A Constructs a villa to B. B transfers 3 AC machines 5 Fan and 50 bags cement to

A . Please explain about service tax liability on such free supply.

9.SUPPLY OF FOODS AND HUMAN

CONSUMPTION

service portion in an activity wherein

goods, being food or any other article of

human consumption or any drinkhuman consumption or any drink

(whether or not intoxicating) is supplied

in any manner as a part of the activity.

IV.PLACE OF PROVISION OF RULE

Determination of location of service provider

/receiver

SL NO LOCATION OF SERVICE PROVIDER/RECEIVER POP

1 Single/Centralised Registration Registered premises

2 Premises is not registered Registered office or2 Premises is not registered Registered office or

Administration office

3 Service provided other than business establishment Fixed Establishment

4 Service provided in more than one establishment Establishment most directly

concerned

5 Cannot be find out location Usual place of residence

General Rule (Rule 3).

• POP= location of the recipient of service.

• If location of the recipient of service is not

available.

• POP= location of the service provider• POP= location of the service provider

POP Under performance based service (Rule 4).

• 1. Physical presence of goods.

• Goods required physically for service provided.

• POP= location where the services are actually performed.

• 2. Physical presence of Person.

• physical presence of the service receiver or the person acting onbehalf of the service receiver.behalf of the service receiver.

• POP= location where the services are actually performed.

• 3. Services provided from a remote location through E- mode.

• POP= where goods are situated at the time of provision of service.

• 4.Temporarily imported into India for repairs and export after repair, this clause does not apply

POP relating to immovable property (Rule 5)

• For the following services POP= where immovableproperty is located or intended to be located.

• 1.Services provided in this regard by experts and estateagents

• 2.provision of hotel accommodation by a hotel, inn,• 2.provision of hotel accommodation by a hotel, inn,guesthouse, club or campsite, by whatever, namecalled.

• 3.Grant of rights to use immovable property.

• 4.Services for carrying out or co-ordination ofconstruction work, including architects or interiordecorators.

POP relating to events (Rule 6)

• For the following services POP= where the eventis actually held.

• Services provided by way of admission to, ororganization of

• Cultural, artistic• Cultural, artistic

• Sporting, scientific, educational

• Entertainment event.

• Celebration, conference, fair, exhibition, or similarevents, an

• Services ancillary to such admission.

POP of services provided at more than one

location (Rule 7).

• Where any service referred to in rules 4, 5, or

6 is provided at more than one location,

including a location in the taxable territory, its

place of provision shall be the location in theplace of provision shall be the location in the

taxable territory where the greatest

proportion of the service is provided.

POP provider and recipient are located in

taxable territory (Rule 8).

• POP= location of the recipient of service.

POP of specified services (Rule 9)

• For the following services POP= location of the serviceprovider.

• (a) Services provided by a banking company, or afinancial institution, or a non-banking financialcompany, to account holders;

• (b) Online information and database access or• (b) Online information and database access orretrieval services.

• Meaning.

• online information and database access or retrievalservices” means providing data or information,retrievable or otherwise, to any person, in electronicform through a computer network

© Intermediary services.

intermediary” means a broker, an agent or any

other person, by whatever name called, who

arranges or facilitates a provision of a service

(hereinafter called the ‘main’ service) or supply(hereinafter called the ‘main’ service) or supply

of goodsbetween two or more persons, but does

not include a person who provides the main

service or supply of goods on his account;

(d)Service consisting of hiring of means of

transport, upto a period of one month.

POP of goods transportation services (Rule 10)

• Transportation of goods, other than by way of

mail or courier

• POP= destination of the goods:

• For GTA POP= location of the person liable to

pay tax

POP of passenger transportation service (Rule 11).

• Where the passenger embarks on the conveyancefor a continuous journey.

• Continuous journey” means a journey for whicha single or more than one ticket or invoice isa single or more than one ticket or invoice isissued at the same time, either by one serviceprovider or through one agent acting on behalf ofmore than one service provider, and whichinvolves no stopover between any of the legs ofthe journey for which one or more separatetickets or invoices are issued

POP of services provided on board a conveyance.(

Rule 12).

• Services provided on board a conveyance

during the course of a passenger transport

operation.

• POP= The first scheduled point of departure of• POP= The first scheduled point of departure of

that conveyance for the journey.

Order of application of rules (Rule 14).

• Where the provision of a service is, prima

facie, determinable in terms of more than one

rule, it shall be determined in accordance with

the rule that occurs later among the rules thatthe rule that occurs later among the rules that

merit equal consideration.

CASE STUDY

1.XYZ(India) is providing the service of Engineering Documentation and Tendering

Documentation to PQR(U.K.) through email. These services are used by PQR in relation

to manufacture and sale of their product either outside India or to India. Is XYZ liable

to pay service tax on it? Please Explain about ST applicability.

2. Employees of ABC(India) are visiting the different client in India and outside India to

find and explore the business opportunities and prospective customers. All expensesfind and explore the business opportunities and prospective customers. All expenses

incurred for this purpose including employee cost (salary) are billed to XYZ,

U.K.(Parent Company) with mark-up in foreign currency. Is ABC liable to pay service tax

on it?

3. XYZ having establishment in India paid the amount charged by the advocate in

foreign for the case pleaded in foreign court. Whether under reverse charge

mechanism the tax is payable by XYZ or not on the basis of the service provided by the

advocate outside India? Please help.

4.SP is Indian Company acting as commission agent. It raised

commission invoice to its foreign company for supply of

goods by said foreign company to its customer based in

India. Commission is received in Foreign Exchange. what is

ST incidence on said commission considering recent

amendment in definition of "intermediary"

THANK YOU THANK YOU THANK YOU THANK YOU

CA. V.P.MANAVALAN B.COM.,FCA.,ACMA.,

MANAVALAN & Co.,

Chartered Accountants

Phone: 9500154000

Email: [email protected]