Embed Size (px)

Citation preview

COUNTY OF SANTA CLARA

Single Audit Reports

Basic Financial Statements with Federal Compliance Section

For the Fiscal Year Ended June 30, 2009

COUNTY OF SANTA CLARA Single Audit Reports

For the Fiscal Year Ended June 30, 2009

Table of Contents

Page(s) FINANCIAL SECTION: Independent Auditors’ Report....................................................................................................................... 1 Management’s Discussion and Analysis (Required Supplementary Information – Unaudited)................... 3 Basic Financial Statements:

Government-wide Financial Statements: Statement of Net Assets ................................................................................................................. 21 Statement of Activities................................................................................................................... 22

Fund Financial Statements: Governmental Funds:

Balance Sheet .......................................................................................................................... 24 Reconciliation of the Governmental Funds Balance Sheet to the Government-

wide Statement of Net Assets – Governmental Activities ................................................... 25 Statement of Revenues, Expenditures, and Changes in Fund Balances .................................. 26 Reconciliation of the Statement of Revenues, Expenditures, and Changes in

Fund Balances of Governmental Funds to the Government-wide Statement of Activities – Governmental Activities .............................................................................. 27

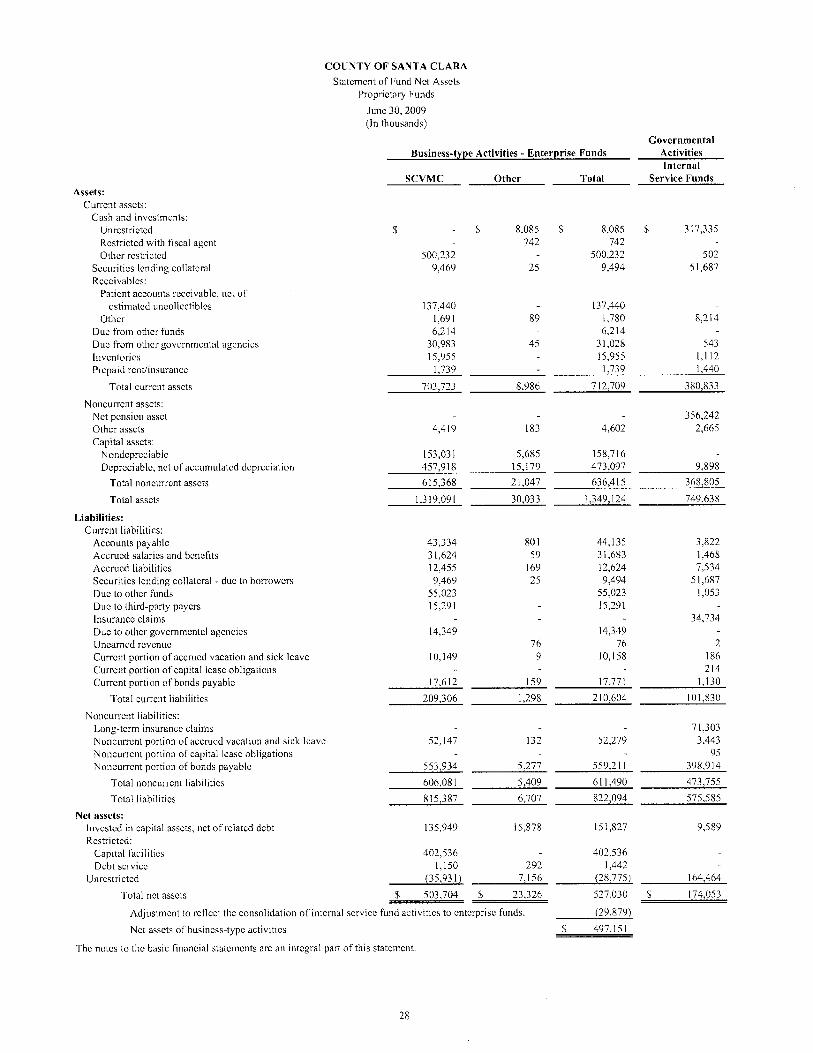

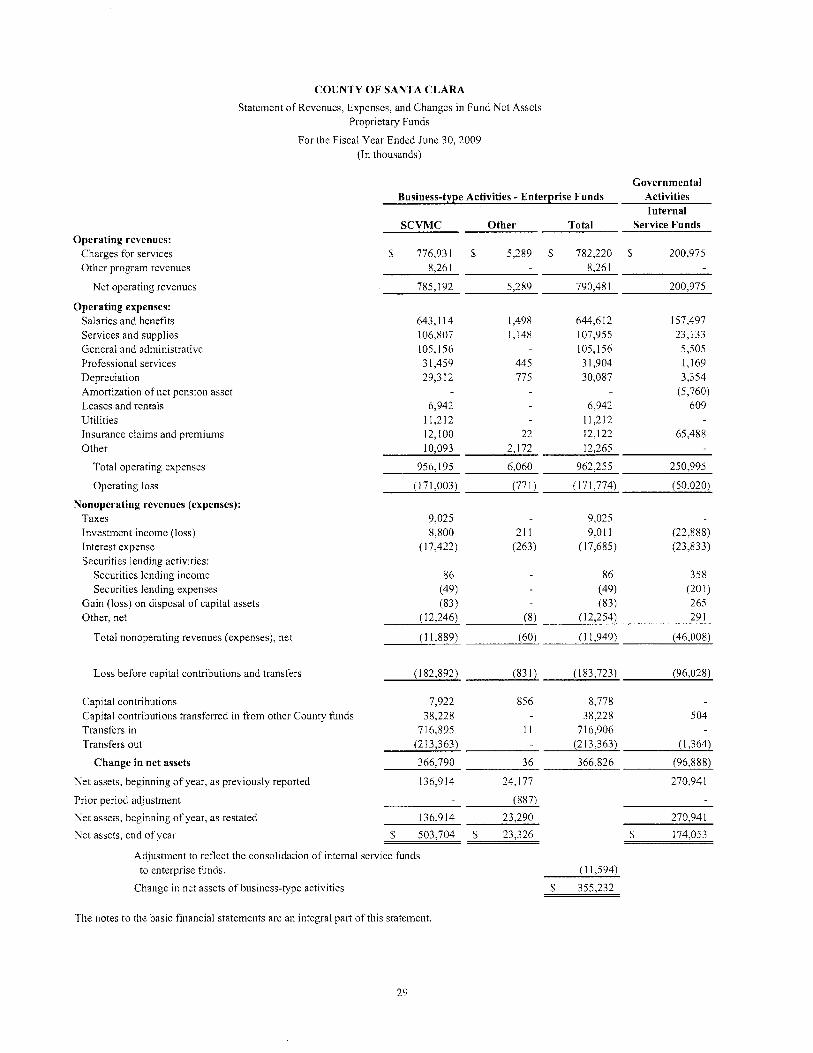

Proprietary Funds: Statement of Fund Net Assets ................................................................................................. 28 Statement of Revenues, Expenses, and Changes in Fund Net Assets ..................................... 29 Statement of Cash Flows......................................................................................................... 30

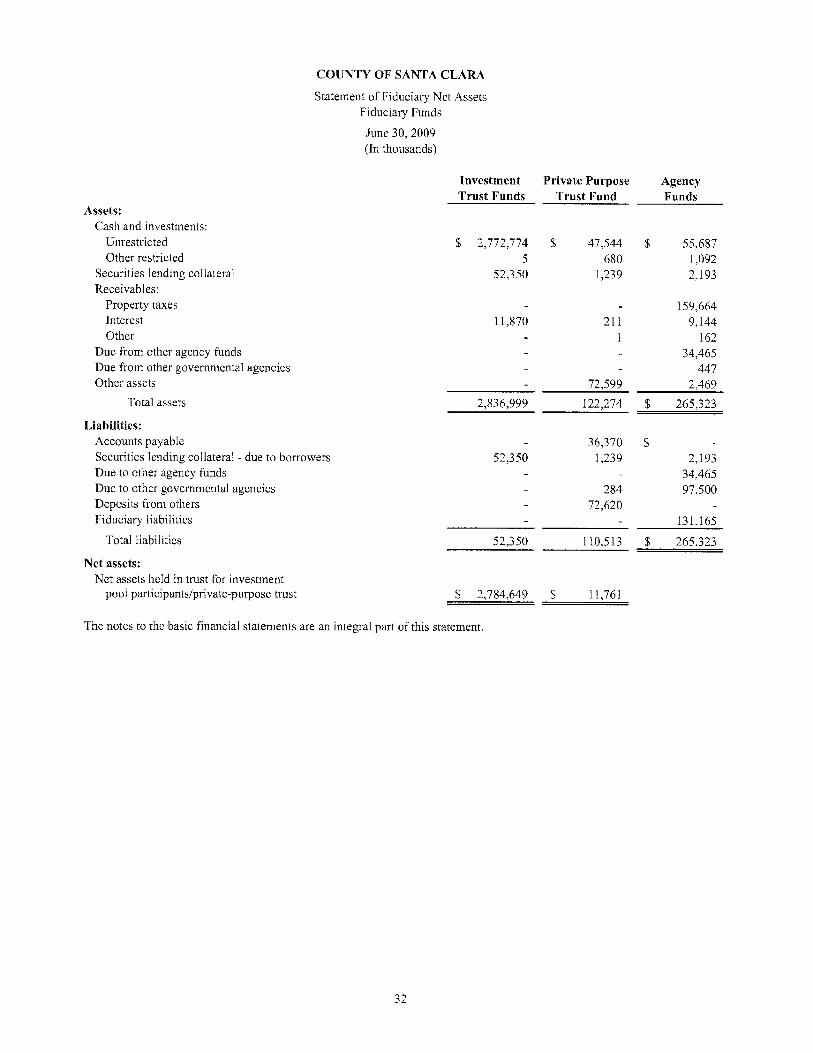

Fiduciary Funds: Statement of Fiduciary Net Assets .......................................................................................... 32 Statement of Changes in Fiduciary Net Assets ....................................................................... 33

Notes to the Basic Financial Statements............................................................................................... 35 Required Supplementary Information (other than MD&A):

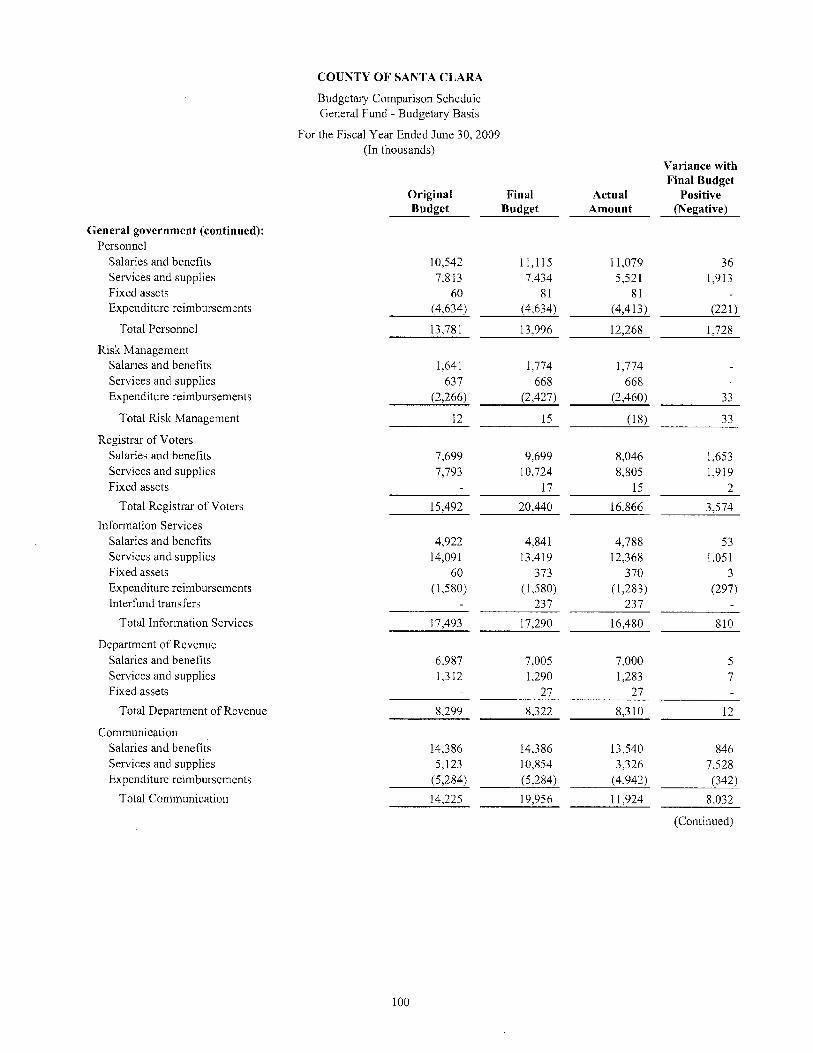

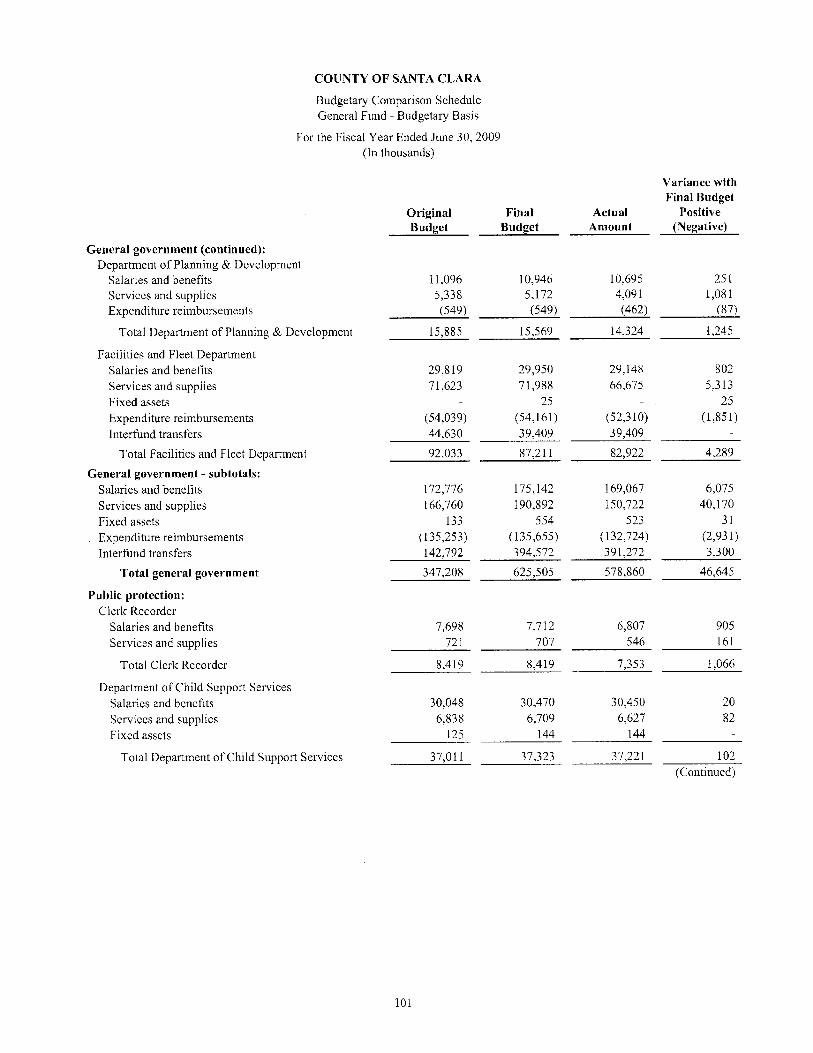

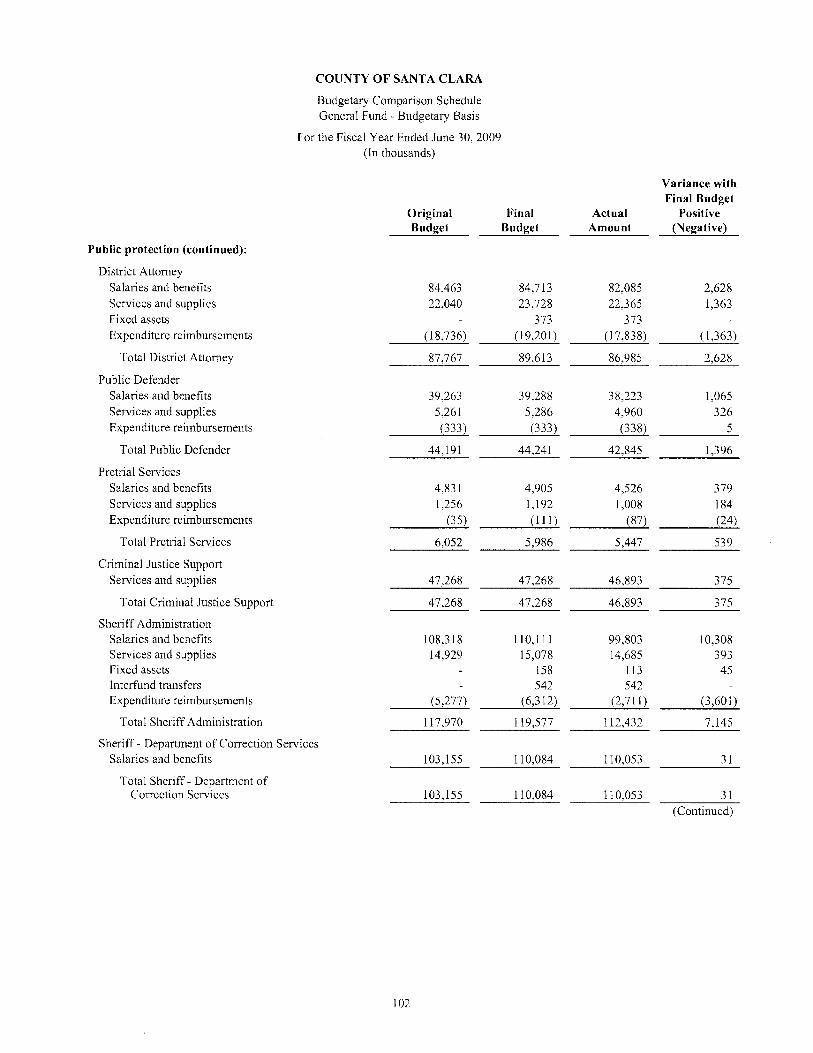

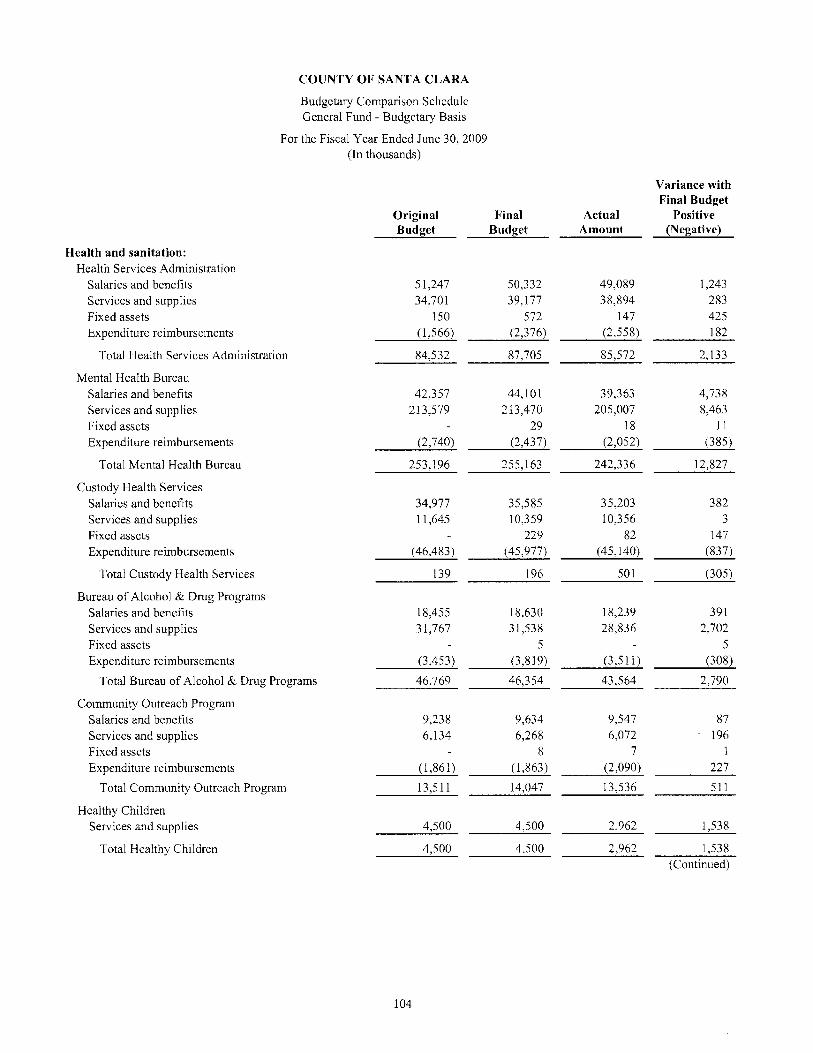

Schedule of Funding Progress .............................................................................................................. 95 Budgetary Comparison Schedule - General Fund - Budgetary Basis................................................... 98 Notes to Required Supplementary Information.................................................................................. 108

COUNTY OF SANTA CLARA Single Audit Reports

For the Fiscal Year Ended June 30, 2009

Table of Contents (Continued)

Page(s) COMPLIANCE SECTION: Independent Auditor’s Report on Internal Control over

Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards ................................................................................ 109

Independent Auditor’s Report on Compliance with

Requirements Applicable to Each Major Program and on Internal Control over Compliance In Accordance with OMB Circular A-133 ............................................................................................................................. 111

Schedule of Expenditures of Federal Awards........................................................................................... 113 Notes to the Schedule of Expenditures of Federal Awards ...................................................................... 117 Schedule of Findings and Questioned Costs ............................................................................................ 123 Summary Schedule of Prior Audit Findings ............................................................................................. 126

1

The Honorable Members of the Board of Supervisors of the County of Santa Clara San Jose, California

Independent Auditor’s Report We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate discretely presented component units and remaining fund information of the County of Santa Clara, California, (the County), as of and for the fiscal year ended June 30, 2009, which collectively comprise the County’s basic financial statements as listed in the table of contents. These financial statements are the responsibility of the County’s management. Our responsibility is to express opinions on these financial statements based on our audit. We did not audit the financial statements of the FIRST 5 Santa Clara County; the County Sanitation District 2 – 3 of Santa Clara County; the Santa Clara County Vector Control District; the Silicon Valley Tobacco Securitization Authority; the Santa Clara County Tobacco Securitization Corporation; and the Santa Clara County Central Fire Protection District, the South Santa Clara County Fire District, and Los Altos Hills County Fire District (collectively, “Fire Districts”), which represent the following percentages of assets, net assets and revenues as of and for the fiscal year ended June 30, 2009:

Those financial statements were audited by other auditors whose reports thereon have been furnished to us, and our opinion, insofar as it relates to the amounts included for those entities, is based on the reports of the other auditors. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the County’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit and the reports of other auditors provide a reasonable basis for our opinions.

Opinion Unit Assets Net Assets RevenuesGovernmental activities 3.2% 4.3% 4.2%Business-type activities 0.7% 1.5% 0.3%Aggregate discretely presented component units and remaining fund information 3.5% 4.1% 1.2%

2

In our opinion, based on our audit and the reports of other auditors, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate discretely presented component units and remaining fund information of the County as of June 30, 2009, and the respective changes in financial position and, where applicable, cash flows thereof for the fiscal year then ended in conformity with accounting principles generally accepted in the United States of America. As discussed in Note 1(o) to the financial statements, the County adopted the provisions of Governmental Accounting Standards Board (GASB) Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations. In accordance with Government Auditing Standards, we have also issued our report dated December 18, 2009, on our consideration of the County’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing the results of our audit. The management’s discussion and analysis, schedules of funding progress and budgetary comparison schedule – General Fund as listed in the table of contents are not a required part of the basic financial statements but are supplementary information required by the accounting principles generally accepted in the United States of America. We have applied certain limited procedures, which consisted principally of inquiries of management regarding the methods of measurement and presentation of the required supplementary information. However, we did not audit the information and express no opinion on it. Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the County’s basic financial statements. The accompanying schedule of expenditures of federal awards (SEFA) is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is not a required part of the basic financial statements. In addition, the SEFA does not include expenditures of federal awards received by the Housing Authority of the County of Santa Clara (Housing Authority). The Housing Authority’s federal expenditures are separately audited in accordance with OMB Circular A-133. The SEFA has been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, is fairly stated, in all material respects, in relation to the basic financial statements taken as a whole. Certified Public Accountants Walnut Creek, California December 18, 2009

109

The Honorable Members of the Board of Supervisors of the County of Santa Clara San Jose, California

Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements

Performed in Accordance with Government Auditing Standards

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate discretely presented component units and remaining fund information of the County of Santa Clara, California, (the County), as of and for the fiscal year ended June 30, 2009, which collectively comprise the County’s basic financial statements, and have issued our report thereon dated December 18, 2009. Our report includes a reference to other auditors. Our report also includes an explanatory paragraph indicating that the County adopted the provisions of Governmental Accounting Standards Board (GASB) Statement No. 49, Accounting and Financial Reporting for Pollution Remediation Obligations. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Other auditors audited the financial statements of the FIRST 5 Santa Clara County; the County Sanitation District 2 – 3 of Santa Clara County; the Santa Clara County Vector Control District; the Silicon Valley Tobacco Securitization Authority; the Santa Clara County Tobacco Securitization Corporation; and the Santa Clara County Central Fire Protection District, the South Santa Clara County Fire District, and Los Altos Hills County Fire District (collectively, “Fire Districts”), as described in our report on the County’s financial statements. This report does not include the results of the other auditors’ testing of internal control over financial reporting or compliance and other matters that are reported on separately by those other auditors. Internal Control Over Financial Reporting In planning and performing our audit, we considered the County’s internal control over financial reporting as a basis for designing our auditing procedures for the purpose of expressing our opinions on the financial statements, but not for the purpose of expressing an opinion on the effectiveness of the County’s internal control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the County’s internal control over financial reporting. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements on a timely basis. A material weakness is a deficiency, or a combination of deficiencies, in internal control such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis.

110

Our consideration of internal control over financial reporting was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over financial reporting that might be deficiencies, significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over financial reporting that we consider to be material weaknesses, as defined above. However, we identified certain deficiencies in internal control over financial reporting, described in the accompanying schedule of findings and questioned costs as items 2009-A and 2009-B that we consider to be significant deficiencies in internal control over financial reporting. A significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness, yet important enough to merit attention by those charged with governance. Compliance and Other Matters As part of obtaining reasonable assurance about whether the County’s financial statements are free of material misstatement, we performed tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, noncompliance with which could have a direct and material effect on the determination of financial statement amounts. However, providing an opinion on compliance with those provisions was not an objective of our audit, and accordingly we do not express such an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are required to be reported under Government Auditing Standards. We noted certain matters that we reported to management of the County in a separate letter dated December 18, 2009. The County’s responses to the findings identified in our audit are described in the accompanying schedule of findings and questioned costs. We did not audit the County’s responses and, accordingly, we express no opinion on them. This report is intended solely for the information and use of the Board of Supervisors, County management, federal awarding agencies and pass-through entities and is not intended to be and should not be used by anyone other than these specified parties. Certified Public Accountants Walnut Creek, California December 18, 2009

111

The Honorable Members of the Board of Supervisors of the County of Santa Clara San Jose, California

Independent Auditor’s Report on Compliance with Requirements Applicable to Each Major Program and on Internal Control over

Compliance in Accordance with OMB Circular A-133 Compliance We have audited the compliance of the County of Santa Clara, California (the County), with the types of compliance requirements described in the U.S. Office of Management and Budget (OMB) Circular A-133 Compliance Supplement that are applicable to each of its major federal programs for the fiscal year ended June 30, 2009. The County’s major federal programs are identified in the summary of auditor’s results section of the accompanying schedule of findings and questioned costs. Compliance with the requirements of laws, regulations, contracts and grants applicable to each of its major federal programs is the responsibility of the County’s management. Our responsibility is to express an opinion on the County’s compliance based on our audit. The County’s basic financial statements include the operations of the Housing Authority of the County of Santa Clara (Housing Authority), which expended $232,236,967 in federal awards, which is not included in the schedule of expenditures of federal awards (SEFA) for the fiscal year ended June 30, 2009. Our audit, described below, did not include the operations of the Housing Authority because we audited and reported on the Housing Authority in accordance with OMB Circular A-133 as a separate engagement. We conducted our audit of compliance in accordance with auditing standards generally accepted in the United States of America; the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States; and OMB Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations. Those standards and OMB Circular A-133 require that we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types of compliance requirements referred to above that could have a direct and material effect on a major federal program occurred. An audit includes examining, on a test basis, evidence about the County’s compliance with those requirements and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. Our audit does not provide a legal determination of the County’s compliance with those requirements. In our opinion, the County complied, in all material respects, with the requirements referred to above that are applicable to each of its major federal programs for the year ended June 30, 2009.

112

Internal Control Over Compliance Management of the County is responsible for establishing and maintaining effective internal control over compliance with the requirements of laws, regulations, contracts, and grants applicable to federal programs. In planning and performing our audit, we considered County’s internal control over compliance with the requirements that could have a direct and material effect on a major federal program in order to determine our auditing procedures for the purpose of expressing our opinion on compliance and to test and report on internal control over compliance in accordance with OMB Circular A-133, but not for the purpose of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not express an opinion on the effectiveness of County’s internal control over compliance. A deficiency in internal control over compliance exists when the design or operation of a control over compliance does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, noncompliance with a type of compliance requirement of a federal program on a timely basis. A material weakness in internal control over compliance is a deficiency, or combination of deficiencies, in internal control over compliance, such that there is a reasonable possibility that material noncompliance with a type of compliance requirement of a federal program will not be prevented, or detected and corrected, on a timely basis. Our consideration of internal control over compliance was for the limited purpose described in the first paragraph of this section and was not designed to identify all deficiencies in internal control over compliance that might be deficiencies, significant deficiencies, or material weaknesses. We did not identify any deficiencies in internal control over compliance that we consider to be material weaknesses, as defined above. This report is intended solely for the information and use of the Board of Supervisors, County management, federal awarding agencies and pass-through entities and is not intended to be and should not be used by anyone other than these specified parties. Certified Public Accountants Walnut Creek, California March 23, 2010

Federal Pass Through Federal Grantor/Pass Through Entity/Grant Name CFDA No. Entity Number Expenditures

U.S. Department of Agriculture

Passed Through State Department of Social Services Supplemental Nutrition Assistance Program 10.551 n/a 103,635,071$

State Administrative Matching Grants for the Supplemental Nutrition Assistance Program 10.561 04-35881 308,280State Administrative Matching Grants for the Supplemental Nutrition Assistance Program 10.561 07-65337 212,434State Administrative Matching Grants for the Supplemental Nutrition Assistance Program 10.561 08-85228 64,926State Administrative Matching Grants for the Supplemental Nutrition Assistance Program 10.561 08-85173 660,855State Administrative Matching Grants for the Supplemental Nutrition Assistance Program 10.561 n/a 18,035,996

Subtotal State Administrative Matching Grants for the SupplementalNutrition Assistance Program 19,282,491

Subtotal Pass Through State Department of Social Services 122,917,562

Passed Through State Department of Public HealthSpecial Supplemental Nutrition Program for Women, Infants, and Children 10.557 05-45797 3,293,102

Passed Through State Department of Agriculture Inspection Grading and Standardization 10.162 8415 1,169

Passed Through State Department of Education Child Nutrition Cluster:

School Breakfast Program 10.553 43-10439-6066435-01 231,999National School Lunch Program 10.555 43-10439-6066435-01 359,552

Subtotal of Child Nutrition Cluster 591,551

Subtotal Passed Through State Department of Education 591,551

Total U.S. Department of Agriculture 126,803,384

U.S. Department of Housing and Urban Development Direct Programs

Community Development Block Grants/Entitlement Grants 14.218 n/a 1,629,796HOME Investment Partnerships Program 14.239 n/a 11,104,108

Total U.S. Department of Housing and Urban Development 12,733,904

U.S. Department of Interior Direct Programs

Save America's Treasures 15.929 n/a 38,422

Passed Through State Department of Parks and Recreation Cooperative Endangered Species Conservation Fund 15.615 P0330012 391,928

Total U.S. Department of Interior 430,350

U.S. Department of Justice Direct Programs

Juvenile Accountability Block Grants 16.523 n/a 160,649Community Capacity Development Office 16.595 n/a 150,747State Criminal Alien Assistance Program 16.606 n/a 1,568,071Public Safety Partnership and Community Policing Grants 16.710 n/a 1,262,655Forensic DNA Backlog Reduction Program 16.741 n/a 306,480

Subtotal Direct Programs 3,448,602

Passed Through California Emergency Management AgencyCrime Victim Assistance 16.575 VW 08270430 250,160Edward Byrne Memorial Justice Assistance Grant Program 16.738 DC 08190430 410,181Paul Coverdell Forensic Sciences Improvement Grant Program 16.742 CQ 07050430 13,360Paul Coverdell Forensic Sciences Improvement Grant Program 16.742 CQ 08060430 37,744

Subtotal Paul Coverdell Forensic Sciences Improvement Grant Program 51,104

Subtotal Passed Through California Emergency Management Agency 711,445Total U.S. Department of Justice 4,160,047

COUNTY OF SANTA CLARA Schedule of Expenditures of Federal Awards

For the Fiscal Year Ended June 30, 2009

See accompanying notes to the Schedule of Expenditures of Federal Awards.

113

Federal Pass Through Federal Grantor/Pass Through Entity/Grant Name CFDA No. Entity Number Expenditures

U.S. Department of Transportation Direct Program

Airport Improvement Program 20.106 n/a 856,406

Passed Through State Department of Transportation Highway Planning and Construction 20.205 STPL 5937(108) 1,539,763Highway Planning and Construction 20.205 STPLZ 5937(033) 155,848Highway Planning and Construction 20.205 STPLZ-5937(087) 33,100Highway Planning and Construction 20.205 STPLZ-5937(088) 35,368Highway Planning and Construction 20.205 BHLO 5937(093) 373,271Highway Planning and Construction 20.205 BHLO 5937(096) 7,987Highway Planning and Construction 20.205 BRLS 5937(077) 1,265,705Highway Planning and Construction 20.205 BRLS 5937(107) 73,610Highway Planning and Construction 20.205 BRLS 5937(109) 51,569Highway Planning and Construction 20.205 BRLO 5937(106) 24,558Highway Planning and Construction 20.205 STPLZ 5937(058) 59,944Highway Planning and Construction 20.205 BPMP 5937(105) 21,442Highway Planning and Construction 20.205 STPL 5937(115) 646,302Highway Planning and Construction 20.205 STPL 5937(125) 90,191Highway Planning and Construction 20.205 STPL 5937(126) 81,238Highway Planning and Construction 20.205 TCSPLO8 5937 (128) 108,199Highway Planning and Construction 20.205 HPLUL 5937 (116) 808,031Highway Planning and Construction 20.205 CML 5937 (130) 10,151Highway Planning and Construction 20.205 HSIPL 5937 (117) 45,581Highway Planning and Construction 20.205 BRL-NBIS (508) 88,353

Subtotal Highway Planning and Construction 5,520,211

Subtotal Passed Through State Department of Transportation 5,520,211

Passed Through State Department of Parks and Recreation Recreational Trails Program 20.219 RT-43-006 63,340

Subtotal Passed Through State Department of Parks and Recreation 63,340

Passed Through State Office of Traffic Safety State and Community Highway Safety 20.600 n/a 79,180State and Community Highway Safety 20.600 AL0668 76,630State and Community Highway Safety 20.600 AL0980 33,985State and Community Highway Safety 20.600 n/a 294,665State and Community Highway Safety 20.600 n/a 169,347

Subtotal State and Community Highway Safety 653,807

Subtotal Passed Through State Office of Traffic Safety 653,807

Total U.S. Department of Transportation 7,093,764

U.S. Department of EnergyDirect Programs

Fossil Energy Research and Development 81.089 n/a 822,626

Total U.S. Department of Energy 822,626

U.S. Department of Education Passed Through State Department of Alcohol and Drugs

Safe and Drug-Free Schools and Communities_State Grants 84.186 n/a 8,916

Total U.S. Department of Education 8,916

Schedule of Expenditures of Federal Awards (Continued) For the Fiscal Year Ended June 30, 2009

COUNTY OF SANTA CLARA

See accompanying notes to the Schedule of Expenditures of Federal Awards.

114

Federal Pass Through Federal Grantor/Pass Through Entity/Grant Name CFDA No. Entity Number Expenditures

U.S. Department of Health and Human Services Direct Programs

Consolidated Health Centers (Community Health Center, Migrant Health Centers,Health Care for the Homeless, Public Housing Primary Care, and School BasedHealth Centers) 93.224 n/a 1,241,297

Enhance the Safety of Children Affected By Parental Methamphetamineor Other Substance Abuse 93.087 n/a 1,046,240

Child Support Enforcement Demonstrations and Special Projects 93.601 n/a 67,070ARRA – Health Center Integrated Services Development Initiative 93.703 n/a 15,444

Subtotal Direct Programs 2,370,051

Passed Through Council on Aging Silicon ValleyAging Cluster:

Special Programs for the Aging_Title III, Part C_Nutrition Services 93.045 AP-0708-10 1,332,231Nutrition Services Incentive Program 93.053 AP-0809-10 699,681

Subtotal Aging Cluster 2,031,912

Subtotal Passed Through Council on Aging Silicon Valley 2,031,912

Passed Through State Department of Education Child Care Mandatory and Matching Funds of the Child Care and Development Fund 93.596 43-2243 1,709,417

Subtotal Passed Through State Department of Education 1,709,417

Passed Through State Department of Health Services Public Health and Social Services Emergency Fund 93.003 n/a 1,906,747Project Grants and Cooperative Agreements for Tuberculosis Control Programs 93.116 n/a 527,197Projects for Assistance in Transition from Homelessness (PATH) 93.150 n/a 224,956Immunization Grants 93.268 08-85322 993,302Centers for Disease Control and Prevention _ Investigations

and Technical Assistance 93.283 n/a 1,032,919

Refugee and Entrant Assistance_Discretionary Grants 93.576 n/a 24,909Refugee and Entrant Assistance_Discretionary Grants 93.576 08-43-90841-1 40,000Refugee and Entrant Assistance_Discretionary Grants 93.576 08-43-90840-1 293,000Refugee and Entrant Assistance_Discretionary Grants 93.576 07-43-90840-1 94,347

Subtotal Refugee and Entrant Assistance_Discretionary Grants 452,256

Medical Assistance Program 93.778 n/a 4,673,143National Bioterrorism Hospital Preparedness Program 93.889 PS0423 663,396 HIV Emergency Relief Project Grants 93.914 n/a 2,493,883HIV Care Formula Grants 93.917 n/a 414,006

Grants to Provide Outpatient Early Intervention Services with Respect to HIV Disease 93.918 n/a 763,511

HIV Prevention Activities_Health Department Based 93.940 n/a 1,421,342

Public Health Traineeships 93.964 2008-43 MCH 124,365Public Health Traineeships 93.964 2008-43 BIH 217,499

Public Health Traineeships 93.964 2008-43 AFLP 251,364

Subtotal Public Health Traineeships 593,228

Maternal and Child Health Services Block Grant to the States 93.994 2008-43 BIH 255,327Maternal and Child Health Services Block Grant to the States 93.994 2008-43 AFLP 97,792Maternal and Child Health Services Block Grant to the States 93.994 2008-43 MCH 230,201

Subtotal Maternal and Child Health Services Block Grant to the States 583,320

Subtotal Passed Through State Department of Health Services 16,743,206

Passed Through State Department of Child Support Services Child Support Enforcement 93.563 IV-356 20,690,413ARRA - Child Support Enforcement 93.563 IV-356 3,287,695

Subtotal Child Support Enforcement 23,978,108

Subtotal Passed Through State Department of Child Support Services 23,978,108

For the Fiscal Year Ended June 30, 2009

COUNTY OF SANTA CLARA Schedule of Expenditures of Federal Awards (Continued)

See accompanying notes to the Schedule of Expenditures of Federal Awards.

115

Federal Pass Through Federal Grantor/Pass Through Entity/Grant Name CFDA No. Entity Number Expenditures

U.S. Department of Health and Human Services (Continued) Passed Through State Department of Social Services

Substance Abuse and Mental Health Services_Projects of Regional and National Significance 93.243 n/a 237,279

Promoting Safe and Stable Families 93.556 n/a 1,185,455Temporary Assistance for Needy Families 93.558 n/a 120,985,916Refugee and Entrant Assistance_State Administered Programs 93.566 n/a 1,061,300Refugee and Entrant Assistance_Targeted Assistance Grants 93.584 n/a 361,266 Child Welfare Services_State Grants 93.645 n/a 1,502,095

Foster Care_Title IV-E 93.658 n/a 39,072,584ARRA - Foster Care_Title IV-E 93.658 n/a 872,819

Subtotal Foster Care_Title IV-E 39,945,403

Adoption Assistance 93.659 n/a 11,605,807ARRA - Adoption Assistance 93.659 n/a 977,868

Subtotal Adoption Assistance 12,583,675

Social Services Block Grant 93.667 n/a 9,994,198Chafee Foster Care Independence Program 93.674 n/a 502,473Medical Assistance Program 93.778 n/a 63,142,372

Subtotal Passed Through State Department of Social Services 251,501,432

Passed Through State Department of Mental Health Block Grants for Community Mental Health Services 93.958 n/a 725,929

Passed Through State Department of Alcohol and Drugs Block Grants for Prevention and Treatment of Substance Abuse 93.959 n/a 11,396,013

Total U.S. Department of Health and Human Services 310,456,068

U.S. Department of Homeland Security Passed Through the City and County of San Francisco

Urban Areas Security Initiative 97.008 2007-2008 916,352

Passed Through the California Emergency Management AgencyHomeland Security Grant Program 97.067 2007-8 1,841,766Homeland Security Grant Program 97.067 n/a 137,052

Subtotal Homeland Security Grant Program 1,978,818

Pre-Disaster Mitigation Competitive Grants 97.017 OES # PJ55 73,137 Pre-Disaster Mitigation Competitive Grants 97.017 OES # PJ37 203,938 Pre-Disaster Mitigation Competitive Grants 97.017 OES # PJ45 25,342

Subtotal Pre-Disaster Mitigation Competitive Grants 302,417

Subtotal Passed Through California Emergency Management Agency 2,281,235

Total U.S. Department of Homeland Security 3,197,587

Total Expenditures of Federal Awards 465,706,646$

COUNTY OF SANTA CLARASchedule of Expenditures of Federal Awards (Continued)

For the Fiscal Year Ended June 30, 2009

See accompanying notes to the Schedule of Expenditures of Federal Awards.

116

COUNTY OF SANTA CLARA Notes to the Schedule of Expenditures of Federal Awards

For the Fiscal Year Ended June 30, 2009

117

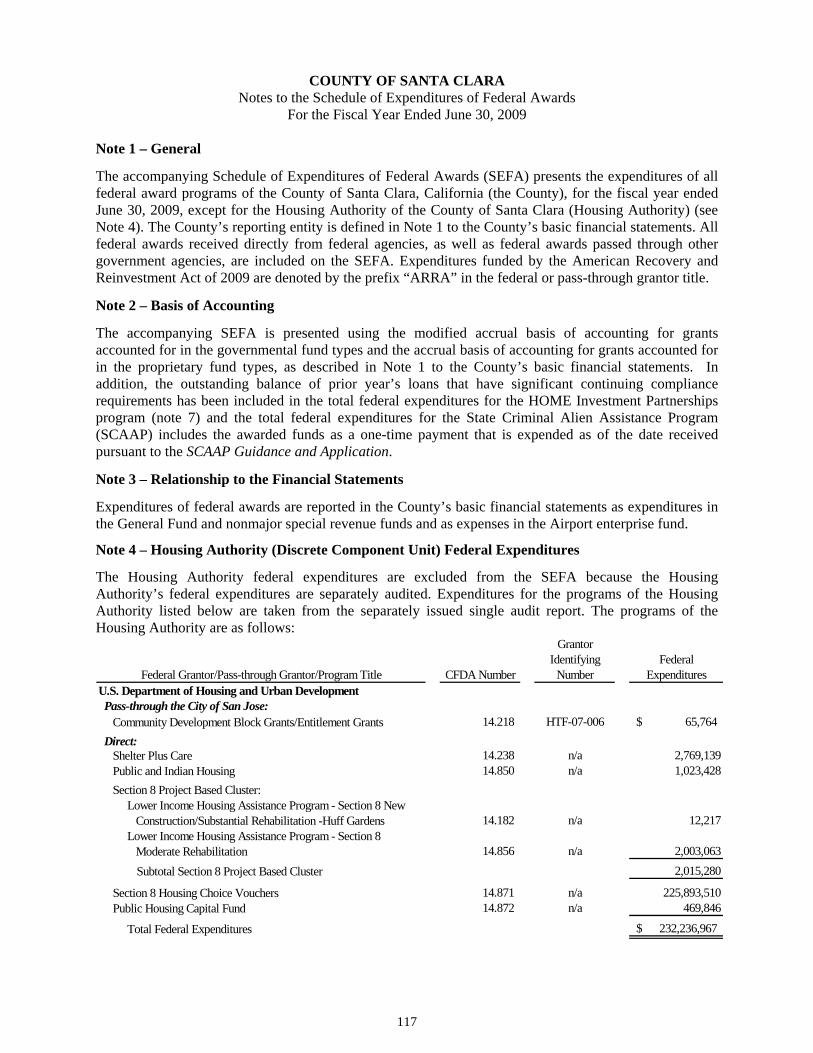

Note 1 – General The accompanying Schedule of Expenditures of Federal Awards (SEFA) presents the expenditures of all federal award programs of the County of Santa Clara, California (the County), for the fiscal year ended June 30, 2009, except for the Housing Authority of the County of Santa Clara (Housing Authority) (see Note 4). The County’s reporting entity is defined in Note 1 to the County’s basic financial statements. All federal awards received directly from federal agencies, as well as federal awards passed through other government agencies, are included on the SEFA. Expenditures funded by the American Recovery and Reinvestment Act of 2009 are denoted by the prefix “ARRA” in the federal or pass-through grantor title. Note 2 – Basis of Accounting The accompanying SEFA is presented using the modified accrual basis of accounting for grants accounted for in the governmental fund types and the accrual basis of accounting for grants accounted for in the proprietary fund types, as described in Note 1 to the County’s basic financial statements. In addition, the outstanding balance of prior year’s loans that have significant continuing compliance requirements has been included in the total federal expenditures for the HOME Investment Partnerships program (note 7) and the total federal expenditures for the State Criminal Alien Assistance Program (SCAAP) includes the awarded funds as a one-time payment that is expended as of the date received pursuant to the SCAAP Guidance and Application. Note 3 – Relationship to the Financial Statements Expenditures of federal awards are reported in the County’s basic financial statements as expenditures in the General Fund and nonmajor special revenue funds and as expenses in the Airport enterprise fund. Note 4 – Housing Authority (Discrete Component Unit) Federal Expenditures The Housing Authority federal expenditures are excluded from the SEFA because the Housing Authority’s federal expenditures are separately audited. Expenditures for the programs of the Housing Authority listed below are taken from the separately issued single audit report. The programs of the Housing Authority are as follows:

GrantorIdentifying Federal

CFDA Number Number ExpendituresU.S. Department of Housing and Urban Development Pass-through the City of San Jose:

Community Development Block Grants/Entitlement Grants 14.218 HTF-07-006 65,764$ Direct:

Shelter Plus Care 14.238 n/a 2,769,139Public and Indian Housing 14.850 n/a 1,023,428Section 8 Project Based Cluster:

Lower Income Housing Assistance Program - Section 8 New Construction/Substantial Rehabilitation -Huff Gardens 14.182 n/a 12,217Lower Income Housing Assistance Program - Section 8 Moderate Rehabilitation 14.856 n/a 2,003,063

Subtotal Section 8 Project Based Cluster 2,015,280

Section 8 Housing Choice Vouchers 14.871 n/a 225,893,510Public Housing Capital Fund 14.872 n/a 469,846

Total Federal Expenditures 232,236,967$

Federal Grantor/Pass-through Grantor/Program Title

COUNTY OF SANTA CLARA Notes to the Schedule of Expenditures of Federal Awards (Continued)

For the Fiscal Year Ended June 30, 2009

118

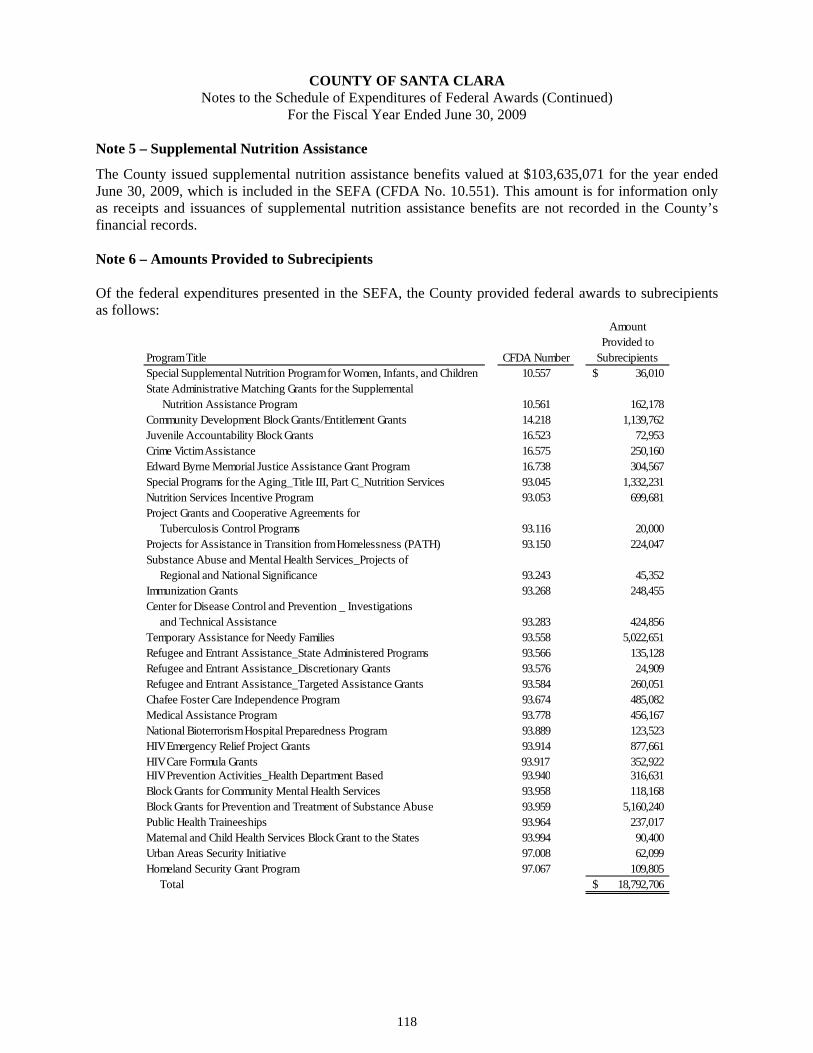

Note 5 – Supplemental Nutrition Assistance

The County issued supplemental nutrition assistance benefits valued at $103,635,071 for the year ended June 30, 2009, which is included in the SEFA (CFDA No. 10.551). This amount is for information only as receipts and issuances of supplemental nutrition assistance benefits are not recorded in the County’s financial records. Note 6 – Amounts Provided to Subrecipients Of the federal expenditures presented in the SEFA, the County provided federal awards to subrecipients as follows:

Amount Provided to

Program Title CFDA Number SubrecipientsSpecial Supplemental Nutrition Program for Women, Infants, and Children 10.557 36,010$ State Administrative Matching Grants for the Supplemental

Nutrition Assistance ProgramCommunity Development Block Grants/Entitlement Grants 14.218 1,139,762 Juvenile Accountability Block Grants 16.523 72,953 Crime Victim Assistance 16.575 250,160 Edward Byrne Memorial Justice Assistance Grant Program 16.738 304,567 Special Programs for the Aging_Title III, Part C_Nutrition Services 93.045 1,332,231 Nutrition Services Incentive Program 93.053 699,681 Project Grants and Cooperative Agreements for

Tuberculosis Control ProgramsProjects for Assistance in Transition from Homelessness (PATH) 93.150 224,047 Substance Abuse and Mental Health Services_Projects of

Regional and National Significance 93.243 45,352 Immunization Grants 93.268 248,455 Center for Disease Control and Prevention _ Investigations

and Technical Assistance 93.283Temporary Assistance for Needy Families 93.558 5,022,651 Refugee and Entrant Assistance_State Administered Programs 93.566 135,128 Refugee and Entrant Assistance_Discretionary Grants 93.576 24,909 Refugee and Entrant Assistance_Targeted Assistance Grants 93.584 260,051 Chafee Foster Care Independence Program 93.674 485,082 Medical Assistance Program 93.778 456,167 National Bioterrorism Hospital Preparedness Program 93.889 123,523 HIV Emergency Relief Project Grants 93.914 877,661 HIV Care Formula Grants 93.917 352,922 HIV Prevention Activities_Health Department Based 93.940 316,631 Block Grants for Community Mental Health Services 93.958 118,168 Block Grants for Prevention and Treatment of Substance Abuse 93.959 5,160,240 Public Health Traineeships 93.964 237,017 Maternal and Child Health Services Block Grant to the States 93.994 90,400 Urban Areas Security Initiative 97.008 62,099 Homeland Security Grant Program 97.067 109,805

Total 18,792,706$

10.561 162,178

93.116 20,000

424,856

COUNTY OF SANTA CLARA Notes to the Schedule of Expenditures of Federal Awards (Continued)

For the Fiscal Year Ended June 30, 2009

119

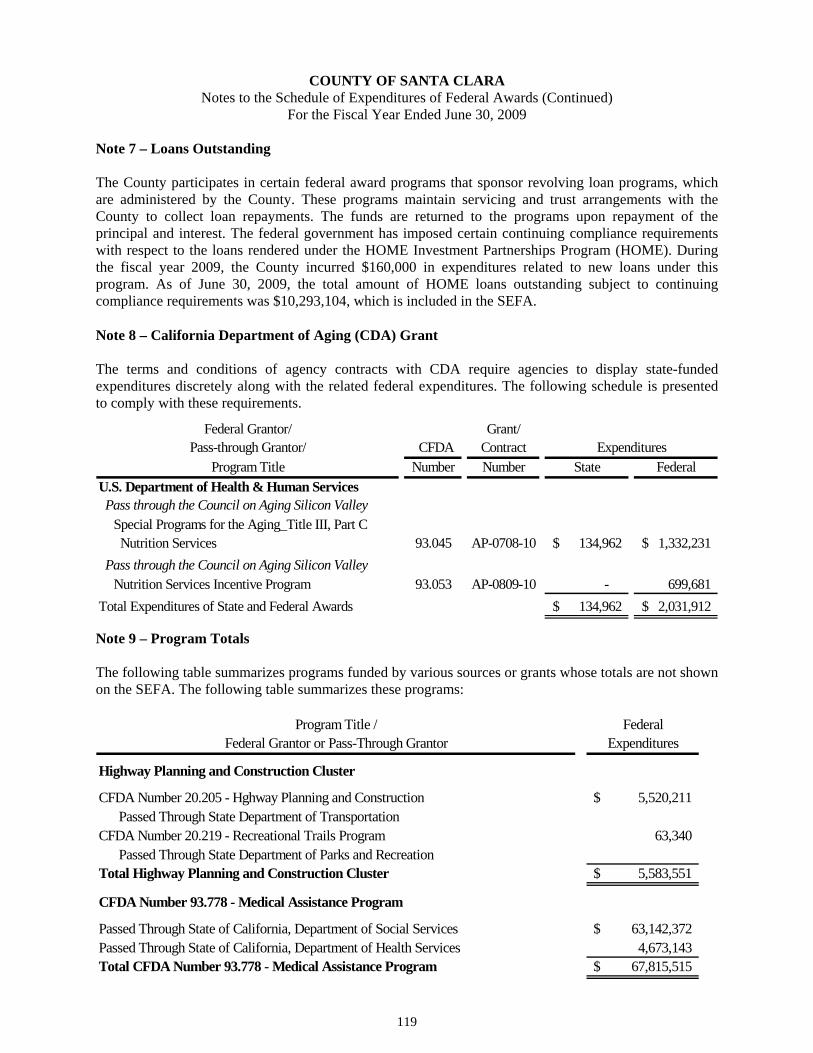

Note 7 – Loans Outstanding The County participates in certain federal award programs that sponsor revolving loan programs, which are administered by the County. These programs maintain servicing and trust arrangements with the County to collect loan repayments. The funds are returned to the programs upon repayment of the principal and interest. The federal government has imposed certain continuing compliance requirements with respect to the loans rendered under the HOME Investment Partnerships Program (HOME). During the fiscal year 2009, the County incurred $160,000 in expenditures related to new loans under this program. As of June 30, 2009, the total amount of HOME loans outstanding subject to continuing compliance requirements was $10,293,104, which is included in the SEFA. Note 8 – California Department of Aging (CDA) Grant The terms and conditions of agency contracts with CDA require agencies to display state-funded expenditures discretely along with the related federal expenditures. The following schedule is presented to comply with these requirements.

Grant/Contract

Number Number State FederalU.S. Department of Health & Human Services Pass through the Council on Aging Silicon Valley

Special Programs for the Aging_Title III, Part C Nutrition Services 93.045 AP-0708-10 134,962$ 1,332,231$

Pass through the Council on Aging Silicon ValleyNutrition Services Incentive Program 93.053 AP-0809-10 - 699,681

Total Expenditures of State and Federal Awards 134,962$ 2,031,912$

ExpendituresFederal Grantor/

Pass-through Grantor/Program Title

CFDA

Note 9 – Program Totals The following table summarizes programs funded by various sources or grants whose totals are not shown on the SEFA. The following table summarizes these programs:

Program Title / FederalFederal Grantor or Pass-Through Grantor Expenditures

Highway Planning and Construction Cluster

CFDA Number 20.205 - Hghway Planning and Construction 5,520,211$ Passed Through State Department of Transportation

CFDA Number 20.219 - Recreational Trails Program 63,340 Passed Through State Department of Parks and Recreation

Total Highway Planning and Construction Cluster 5,583,551$

CFDA Number 93.778 - Medical Assistance Program

Passed Through State of California, Department of Social Services 63,142,372$ Passed Through State of California, Department of Health Services 4,673,143 Total CFDA Number 93.778 - Medical Assistance Program 67,815,515$

COUNTY OF SANTA CLARA Notes to the Schedule of Expenditures of Federal Awards (Continued)

For the Fiscal Year Ended June 30, 2009

120

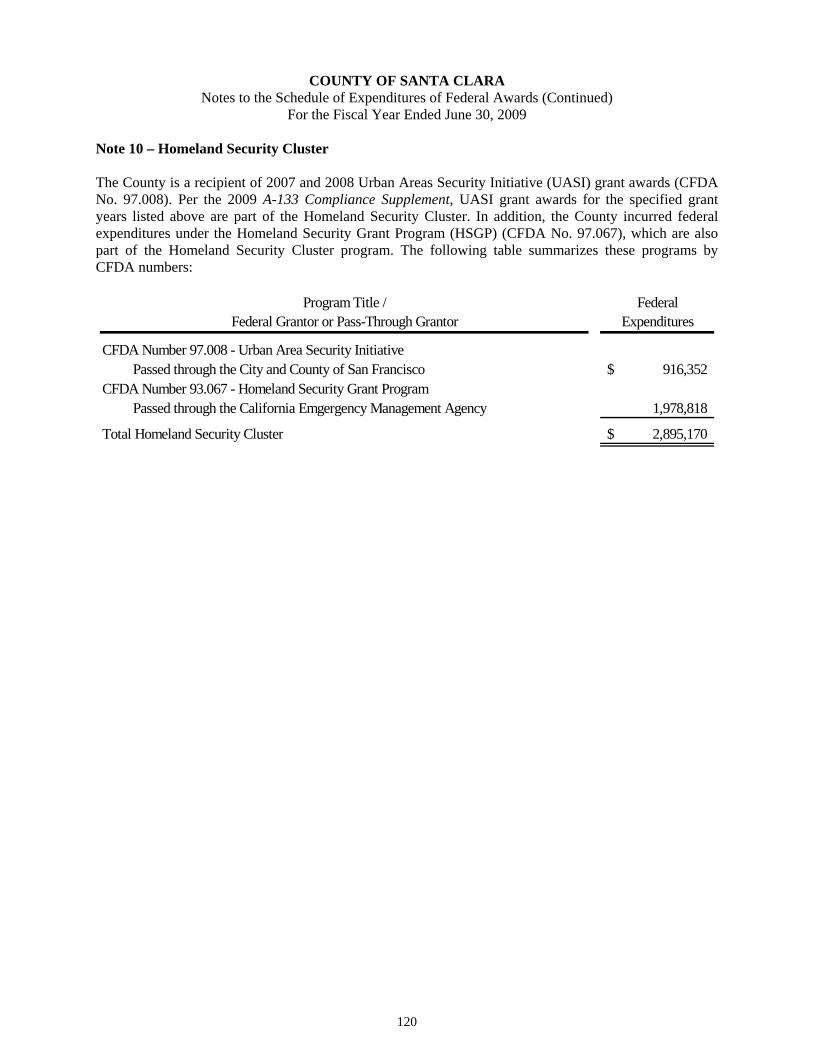

Note 10 – Homeland Security Cluster The County is a recipient of 2007 and 2008 Urban Areas Security Initiative (UASI) grant awards (CFDA No. 97.008). Per the 2009 A-133 Compliance Supplement, UASI grant awards for the specified grant years listed above are part of the Homeland Security Cluster. In addition, the County incurred federal expenditures under the Homeland Security Grant Program (HSGP) (CFDA No. 97.067), which are also part of the Homeland Security Cluster program. The following table summarizes these programs by CFDA numbers:

Program Title / FederalFederal Grantor or Pass-Through Grantor Expenditures

CFDA Number 97.008 - Urban Area Security InitiativePassed through the City and County of San Francisco 916,352$

CFDA Number 93.067 - Homeland Security Grant ProgramPassed through the California Emgergency Management Agency 1,978,818

Total Homeland Security Cluster 2,895,170$

Note 11 - Schedules of the California Emergency Management Agency (Cal EMA) and California Victims Compensation & Government Claims Board

California Emergency Management Agency grant expenditures:The following represents grant expenditures for Department of Justice grants passed through the California Emergency Management Agencyfor the fiscal year ended June 30, 2009.

Grant Award Actual Actual ActualProgram Title and Expenditure Category Number/Period Budget Non-match Match Total Variance

Victim Witness Assistance - Cal EMA VW 08270430Operating Expenses 7/1/08 to 6/30/09 250,160$ 250,160$ -$ 250,160$ -$ Total 250,160$ 250,160$ -$ 250,160$ -$

Anti-Drug Abuse Enforcement Program DC 08190430Personal Services 7/1/08 to 6/30/09 105,614$ 105,614$ -$ 105,614$ -$ Operating Expenses 251,164 251,164 - 251,164 - Equipment 53,403 53,403 - 53,403 - Total 410,181$ 410,181$ -$ 410,181$ -$

Paul Coverdell Forensic Sciences Improvement CQ 07050430Operating Expenses 1/1/08 to 12/31/08 44,746$ 13,360$ -$ 13,360$ 31,386$ Total 44,746$ 13,360$ -$ 13,360$ 31,386$

Paul Coverdell Forensic Sciences Improvement CQ 08060430Operating Expenses 10/1/08 to 8/31/10 101,229$ 37,744$ -$ 37,744$ 63,485$ Equipment 6,121 - - - 6,121 Total 107,350$ 37,744$ -$ 37,744$ 69,606$

(Note: The non-match expenditure of $250,160, $410,181, $13,360 and $37,744 for grants VW 08270430, DC 08190430, CQ 07050430,and CQ 08060430, respectively, are reported as federal expenditures in the SEFA under the following CFDA numbers: 16.575, 16.738, and 16.742.)

COUNTY OF SANTA CLARANotes to the Schedule of Expenditures of Federal Awards (Continued)

For the Fiscal Year Ended June 30, 2009

121

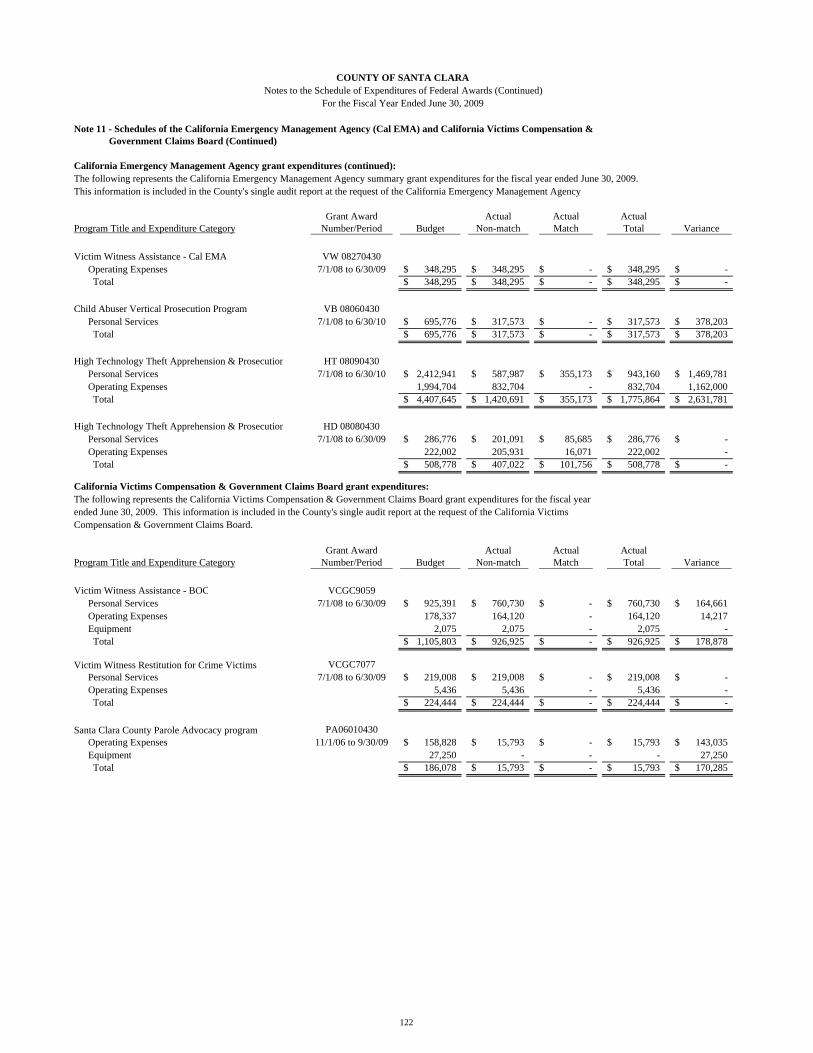

Note 11 - Schedules of the California Emergency Management Agency (Cal EMA) and California Victims Compensation & Government Claims Board (Continued)

California Emergency Management Agency grant expenditures (continued):The following represents the California Emergency Management Agency summary grant expenditures for the fiscal year ended June 30, 2009. This information is included in the County's single audit report at the request of the California Emergency Management Agency

Grant Award Actual Actual ActualProgram Title and Expenditure Category Number/Period Budget Non-match Match Total Variance

Victim Witness Assistance - Cal EMA VW 08270430Operating Expenses 7/1/08 to 6/30/09 348,295$ 348,295$ -$ 348,295$ -$ Total 348,295$ 348,295$ -$ 348,295$ -$

Child Abuser Vertical Prosecution Program VB 08060430Personal Services 7/1/08 to 6/30/10 695,776$ 317,573$ -$ 317,573$ 378,203$ Total 695,776$ 317,573$ -$ 317,573$ 378,203$

High Technology Theft Apprehension & Prosecution HT 08090430Personal Services 7/1/08 to 6/30/10 2,412,941$ 587,987$ 355,173$ 943,160$ 1,469,781$ Operating Expenses 1,994,704 832,704 - 832,704 1,162,000 Total 4,407,645$ 1,420,691$ 355,173$ 1,775,864$ 2,631,781$

High Technology Theft Apprehension & Prosecution HD 08080430Personal Services 7/1/08 to 6/30/09 286,776$ 201,091$ 85,685$ 286,776$ -$ Operating Expenses 222,002 205,931 16,071 222,002 - Total 508,778$ 407,022$ 101,756$ 508,778$ -$

California Victims Compensation & Government Claims Board grant expenditures:The following represents the California Victims Compensation & Government Claims Board grant expenditures for the fiscal year ended June 30, 2009. This information is included in the County's single audit report at the request of the California Victims Compensation & Government Claims Board.

Grant Award Actual Actual ActualProgram Title and Expenditure Category Number/Period Budget Non-match Match Total Variance

Victim Witness Assistance - BOC VCGC9059Personal Services 7/1/08 to 6/30/09 925,391$ 760,730$ -$ 760,730$ 164,661$ Operating Expenses 178,337 164,120 - 164,120 14,217 Equipment 2,075 2,075 - 2,075 - Total 1,105,803$ 926,925$ -$ 926,925$ 178,878$

Victim Witness Restitution for Crime Victims VCGC7077Personal Services 7/1/08 to 6/30/09 219,008$ 219,008$ -$ 219,008$ -$ Operating Expenses 5,436 5,436 - 5,436 - Total 224,444$ 224,444$ -$ 224,444$ -$

Santa Clara County Parole Advocacy program PA06010430Operating Expenses 11/1/06 to 9/30/09 158,828$ 15,793$ -$ 15,793$ 143,035$ Equipment 27,250 - - - 27,250 Total 186,078$ 15,793$ -$ 15,793$ 170,285$

Notes to the Schedule of Expenditures of Federal Awards (Continued)For the Fiscal Year Ended June 30, 2009

COUNTY OF SANTA CLARA

122

COUNTY OF SANTA CLARA Schedule of Findings and Questioned Costs

For the Fiscal Year Ended June 30, 2009

123

Section I – Summary of Auditor’s Results Financial Statements:

Type of auditor’s report issued: Unqualified Internal control over financial reporting: • Material weaknesses identified? No • Significant deficiencies identified that are

not considered to be material weaknesses? Yes Noncompliance material to financial statements noted? No

Federal Awards:

Internal control over major programs: • Material weaknesses identified? No • Significant deficiencies identified that are

not considered to be material weaknesses? None reported Type of auditor’s report issued on compliance for major programs: Unqualified Any audit findings disclosed that are required

to be reported in accordance with section 510(a) of Circular A-133? No

Identification of major programs:

1. CFDA No. 10.557 Special Supplemental Nutrition Program for Women, Infants, and Children (WIC)

2. CFDA No. 14.239 HOME Investment Partnership Program 3. Highway Planning and Construction Cluster CFDA No. 20.205 Highway Program Construction CFDA No. 20.219 Recreational Trails Program 4. CFDA No. 93.558 Temporary Assistance for Needy Families (TANF) 5. CFDA No. 93.563 Child Support Enforcement 6. CFDA No. 93.658 Foster Care – Title IV-E 7. CFDA No. 93.659 Adoption Assistance 8. CFDA No. 93.778 Medical Assistance Program 9. Homeland Security Cluster CFDA No. 97.008 Urban Areas Security Initiative CFDA No. 97.067 Homeland Security Grant Program

Dollar threshold used to distinguish between

Type A and Type B programs: $3,000,000 Auditee qualified as low-risk auditee? No

COUNTY OF SANTA CLARA Schedule of Findings and Questioned Costs (Continued)

For the Fiscal Year Ended June 30, 2009

124

Section II – Financial Statement Findings Significant Deficiency #1 – Item 2009-A Accounting for Securities Lending Transactions Criteria Governmental Accounting Standards Board (GASB) Statement No. 28, Accounting and Financial Reporting for Securities Lending Transactions, established accounting and financial reporting standards for securities lending transactions. Under GASB Statement No. 28, governmental entities should report securities lent (the underlying securities), cash received as collateral, and investment made with the cash received as assets in their statement of net assets/balance sheet and the related collateral due to borrowers should be reported as liabilities. In addition, the cost of securities lending transactions, such as interest costs and agent fees, should be reported as expenditures or expenses, and should not be netted with interest revenues or income from the investment of cash collateral, loan premiums or fees. In December 2006, the County amended its investment policy to include securities lending as a permitted investment. During fiscal year 2009, the County entered into securities lending transactions with its custodian bank, Bank of New York Mellon Corporation (BNY). The County lent investments from its County Commingled and Retiree Health Investment Portfolios to borrowers under securities lending agreements and received cash collateral in return. As of June 30, 2009, the County’s underlying securities loaned from its County Commingled and Retiree Health Investment Portfolios totaled $88.8 million and $48.9 million, respectively. Condition During our audit, we noted that the County did not report the collateral received and collateral due to borrowers on its statement of net assets/balance sheets nor did the County segregate the interest revenues and the cost of the securities lending transactions on its operating statements. As a result, the County’s assets and liabilities were understated by $139.9 million, interest earnings from securities lending transactions were understated by $0.4 million and the cost of securities lending transactions were understated by $0.4 million. The County subsequently recorded an adjustment to correct these misstatements in the June 30, 2009 financial statements. Cause The County’s finance staff was unfamiliar with the application of the securities lending accounting standards. Recommendation As the County enters into non-routine complex transactions, the County staff should obtain additional understanding of the background and nature of the transactions, perform extensive research, and document the County’s accounting treatment on the transactions to ascertain proper accounting and disclosure of these transactions. Management Response County finance staff noted the security lending transactions during the fiscal year and recorded interest income net of expenditures. County staff planned to record the assets, liabilities, and gross interest income and expenditures. County staff subsequently brought this to the attention of the auditors. After discussions with the auditors, these transactions were recorded. Finance staff will ensure that all significant accounting transactions are recorded during the year-end closing process.

COUNTY OF SANTA CLARA Schedule of Findings and Questioned Costs (Continued)

For the Fiscal Year Ended June 30, 2009

125

Section II – Financial Statement Findings (Continued) Significant Deficiency #2 – Item 2009-B Controls over Year-End Capital Projects Payable Accruals Criteria A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct misstatements on a timely basis. Under generally accepted accounting principles, the SCVHHSEF’s capital outlay expenditures are to be recorded when a liability is incurred. As such the SCVHHSEF should record all expenditures related to its capital project programs in the period when a liability is incurred. Condition Throughout the year, the SCVHHSEF utilizes Fund 059 – Capital Projects Subfund to capture its capital project expenditures. During our audit, we noted the SCVHHSEF did not accrue project costs in the amount $12.2 million rendered during the current fiscal year related to the Capital Projects Subfund project. Cause An adequate control over the review of the project payments and contract status with the individual contracts was not effectively performed at year-end to capture all year-end transactions for project costs incurred. Recommendation We recommend the SCVHHSEF perform an expenditure and accrual analysis during its year-end financial reporting process in order to properly record expenditures in the period when a liability is incurred. Management Response SCVHHSEF has always performed an expenditure and accrual analysis during its monthly and year-end financial reporting process in order to properly record expenses in the period when a liability is incurred. At year end the analysis is updated during the various stages of financial statement preparation. The initial analysis is performed in July, with subsequent analyses following in August and September. Fund 59 was not included in the SCVHHSEF follow-up analyses due to SCVHHSEF’s understanding that additional project entries could not be recorded in SAP after the July close. SCVHHSEF Finance will make every effort to submit available capital project accruals before the SAP close in the future. If subsequent analyses provide additional capital project accruals, they will be submitted to the Controller/Treasurer’s Office and the Auditors regardless of the ability to record the entries in SAP. Section III – Federal Award Findings and Questioned Costs No matters were reported.

COUNTY OF SANTA CLARA Summary Schedule of Prior Audit Findings

For the Fiscal Year Ended June 30, 2009

126

Financial Statement Findings

Reference Number: 2008-A – Coordination of the County’s Accounting Standard Implementations

Audit Finding: During our audit we noted that the Santa Clara County Fire Protection District (Central Fire) did not implement Governmental Accounting Standards Board (GASB) Statement No. 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other than Pensions¸ for the fiscal year ended June 30, 2008 along with the rest of the County. As a result, the County under reported its net other postemployment benefit obligation at June 30, 2008 by approximately $12 million. The County should work with Central Fire and all of their other auditors in coordinating the accounting standards to be implemented and presented in their stand alone financial statements at least annually so that these statements meet the County’s comprehensive financial reporting requirements. In addition, the County should review the stand-alone draft financial reports to ascertain whether the information provided for consolidation into the County’s Comprehensive Annual Financial Report is prepared in accordance with the required standards.

Status of Corrective Action: Corrected. Reference Number: 2008-B - Financial Reporting of Net Pension Asset

Audit Finding: In fiscal year 2008, the County issued taxable pension funding bonds in order to refinance its existing obligation and to prepay other amounts arising from enhanced retirement benefits accruing to County employees totaling $386.6 million. The transaction was not properly recorded on the County's financial statements and an audit adjustment was recorded to reduce the County’s obligation in the amount of $42.2 million, reduce the net pension asset in the amount of $29.7 million, and increase net assets by $12.5 million. As the County enters into complex transactions, the Finance Agency staff should continue dialogue between affected parties (e.g., finance and benefits staff) and timely record these transactions in the accounting system.

Status of Corrective Action: Corrected.

COUNTY OF SANTA CLARA Summary Schedule of Prior Audit Findings

For the Fiscal Year Ended June 30, 2009

127

Federal Award Findings

Reference Number: 2008-1

Federal Catalog Number: U.S. Department of Housing and Urban Development 14.239 HOME Investment Partnerships Program

Audit Finding: Program Income - In accordance with the Code of Federal Regulations Title 24 Housing and Urban Development, section 85.25 Program Income, program income shall ordinarily be deducted from total allowable costs to determine the net allowable costs and should be used for current costs unless the federal agency authorizes otherwise. The County received program income in the amount of $44,272 for payments of principal and interest on loans made with HOME grant funds. The County did not factor in the program income received during the fiscal year when it requested for draw down of HOME funds through the HUD’s Integrated Disbursement and Information System (IDIS).

Status of Corrective Action: Corrected based on our current year program requirement tests. Reference Number: 2008-2

Federal Catalog Number: U.S. Department of Health and Human Services Passed through the State of California, Department of Health Services Passed-through the State of California Department of Social Services 93.778 – Medical Assistance Program (Medicaid: Title XIX)

Audit Finding: Eligibility - 2 out of the forty cases tested (out of a population of

145,866), the County did not document the eligibility determination with a MC-13 form in the case file for theses two non U.S. citizen applicants

Status of Corrective Action: Corrected based on our current year program requirement tests.

COUNTY OF SANTA CLARA Summary Schedule of Prior Audit Findings (Continued)

For the Fiscal Year Ended June 30, 2008

128

Reference Number: 2008-3

Federal Catalog Number: U.S. Department of Housing and Urban Development 14.239 HOME Investment Partnerships Program

Audit Finding: Special Tests & Provisions – Housing Quality Standards The Office of Affordable Housing (OAH) did not perform the housing quality inspection performed for 8 projects out of the 9 projects tested (out of a population of 29 projects) within the required timeframe.

Status of Corrective Action: Corrected based on our current year program requirement tests. We noted that the OAH performed and completed housing quality standards inspection on the 8 projects in question subsequent to the required timeframe.

Reference Number: 2008-4

Federal Catalog Number: U.S. Department of Homeland Security Passed through the City and County of San Francisco Passed through the State of California Office of Emergency Services 97.008/97.067 – Homeland Security Cluster

Audit Finding: Subrecipient Monitoring - The Office of Emergency Services (OES) obtained and reviewed the subrecipients’ invoices and supporting schedules before disbursing reimbursement funds to the subrecipients. However, the OES did not require its subrecipients receiving pass-through funding to submit single audit reports. The County did not identify the subrecipients in which single audits are performed, obtain and review the most recent single audit reports to determine if the subrecipients had a completed audit within the required time frame, nor ascertain if these subrecipients had findings or questioned costs related to the grants provided.

Status of Corrective Action: Corrected based on our current year program requirement tests. Reference Number: 2008-5

Federal Catalog Number: U.S. Department of Health and Human Services Passed through the State of California, Department of Social Services 93.558 - Temporary Assistance for Needy Families

Audit Finding: Special Tests & Provisions – Child Support Non Cooperation - 2 out of the forty cases tested (out of a population of 105 fiscal year 2008 cases) that had benefits reduced or terminated did not have a notice of action form in the case file. Special Tests & Provisions – Penalty for Refusal to Work - 1 out of the forty cases tested (out of a population of 12,845 cases) that had benefits reduced did not have a notice of action form in the case file.

Status of Corrective Action: Corrected based on our current year program requirement tests.

![INDEX [dashboard.eidexinsights.com]...statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion We do not express](https://img.dokumen.tips/doc/110x75/5e7c448be82a1d368d480c91/index-statements-and-other-knowledge-we-obtained-during-our-audit-of-the.jpg)