Embed Size (px)

Citation preview

2

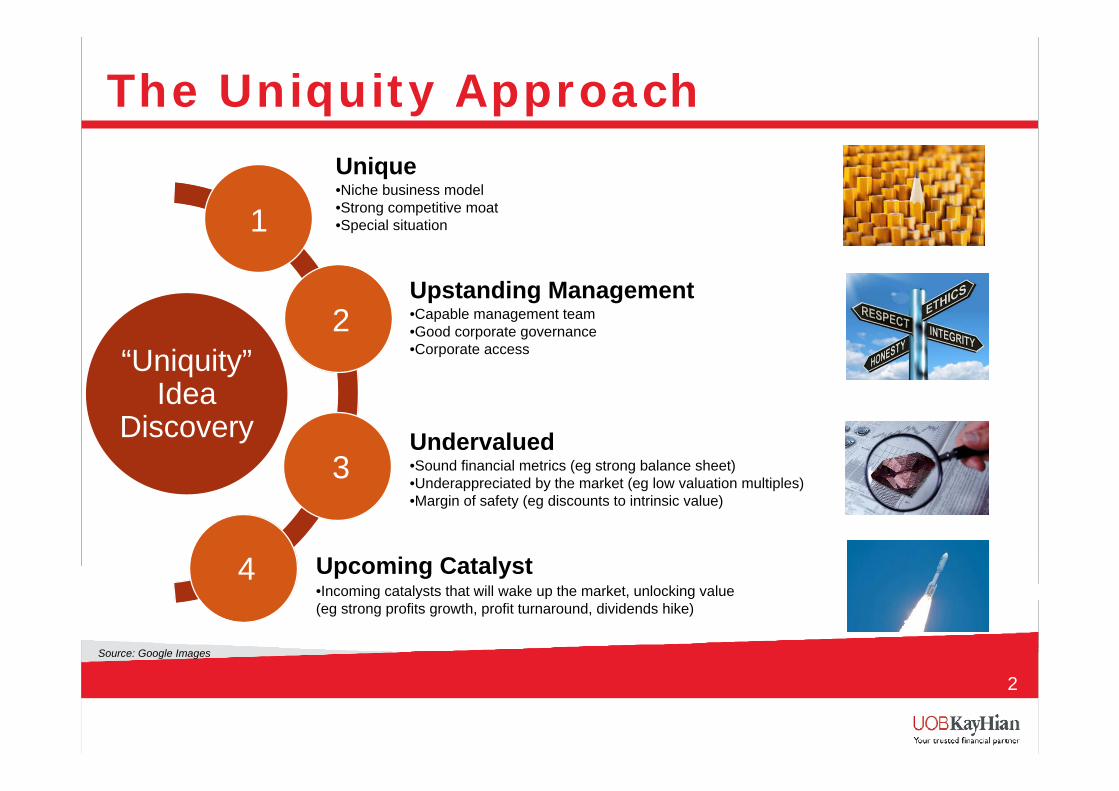

“Uniquity”Idea

Discovery Undervalued•Sound financial metrics (eg strong balance sheet)•Underappreciated by the market (eg low valuation multiples) •Margin of safety (eg discounts to intrinsic value)

Upcoming Catalyst•Incoming catalysts that will wake up the market, unlocking value (eg strong profits growth, profit turnaround, dividends hike)

The Uniquity Approach

1

2

3

4

Upstanding Management•Capable management team•Good corporate governance•Corporate access

Unique•Niche business model •Strong competitive moat •Special situation

Source: Google Images

The Uniquity Approach

• Bottom-up approach and visit as many small & mid cap companies as possible

• Channel checks with competitors, suppliers and customers

0.39BUY0.3174KTG SPKatrina Group4

1.02BUY1.015250CITN SPCityneon3

Ranking Company Name Ticker Market Cap (S$m)

Current Share Price (S$) Rating Target Price

(S$)

1 China Aviation Oil CAO SP 1,300 1.51 BUY 1.85

2 Nera Telecommunications NERT SP 255 0.705 BUY 0.835

Our Stock Picks

Source: Bloomberg, UOB Kay Hian

3

Did you know…?

Only one in twenty-five Chinese citizens have a passport.

China is expected to overtake the United States as the world’s largest passenger market (defined by traffic to, from and within) by 2029.

In 2034 China will account for some 1.19 billion passengers, 758 million more than 2014 with an average annual growth rate of 5.2%.

Source: Bloomberg, Google Images, IATA

Monopolistic Fuel Distribution

Source: CAO, UOB Kay Hian

Exclusive refueller - SPIA

Source: BAFS, CAO

Oil storage facilities

Into-plane refuelling operations at Shanghai Pudong International Airport

China Aviation Oil Singapore Corp(CAO SP/BUY/Target: S$1.85/Market Cap: S$1,300m*)

Proxy To China’s Global Aviation Traffic Boom

Rare monopoly on China’s jet fuel imports is growing source of recurring income (cost-plus business model) (18.3% of profits).

Second solid recurring income is from immensely profitable SPIA refueller (50% of profits).

Catalysts: Shanghai Disneyland, China’s push on general aviation.

Five-year plan to double profits with organic growth and M&As (US$230m net cash war chest).

TP based on 14.4x 2017F PE, a 20% discount to peers’ average of 18x PE

Data as at 20 July 16

6

70

100

130

160

190

220

250

0.50

1.00

1.50

2.00(%)

(lcy)CHINA AVIATION OIL SINGAPORE

China Aviation Oil Singapore/FSSTI Index

0

5

10

Jul 15 Sep 15 Nov 15 Jan 16 Mar 16 May 16

Volume (m)

For Dividend Investors

Source: NeraTel, UOB Kayhian

NeraTel’s Business

S$88m

Expected Gains S$71.5m

Valued at P/E 31.3x

2015 Profit Generated S$2.8m (21% of total)

Estimated Special Dividend 16 SG cents

Estimated Total Dividend for 2016 19 SG cents

Dividend Yield for 2016 27%

Payment Solutions

NeraTel provide end-to-end electronic payment solutions for brick and mortar, internet and mobile commerce to the Banking, Financial Services and Retail industries.

Remaining Business

2015 Profit Generated S$10.6m(79% of total)

Expected Growth 10%

Dividend 4 SG cents a year

Dividend Yield 5.8%

NeraTel provide wireless infrastructure networks, end-to-end solutions and services in the wireless space. NeraTel also provide high-performance IP Network Infrastructure to enable Service Providers to deploy differentiated cost effective services and new revenue streams, it address various market sectors such as Service Providers, ISPs, Broadcasters, Enterprises, Government Organisations.

Source: NeraTel, UOB Kayhian

Nera Telecommunications (NERT SP/BUY/Target: S$0.835/Market Cap: S$261m*)

Get Paid While Waiting

Hefty 2016 dividend of around S$0.19/share likely.

Record-high order backlog for the remaining business.

Growth to continue as CSP capex grows.

S$0.04/share dividends sustainable going forward.

Maintained BUY with S$0.835 TP based on SOTP, valuing remaining business at historical PE of 14.6x.

Data as at 20 July 16

4

60

70

80

90

100

110

120

130

140

150

0.40

0.50

0.60

0.70

0.80

0.90

1.00(%)(lcy)

NERA TELECOMMUNICATIONS LTD

Nera Telecommunications Ltd/FSSTI Index

0

5

10

Jul 15 Sep 15 Nov 15 Jan 16 Mar 16 May 16

Volume (m)

The Marvel Success

Avengers: Age of Ultron (2015)Worldwide Gross: US$1.4b

Transformers: Age of Extinction (2014)Worldwide Gross: US$1.1b

The Avengers (2012)Worldwide Gross: US$1.5b

Transformers: Dark of the Moon (2011)Worldwide Gross: US$1.1b

Source: Google Images, Box Office Mojo

The Disney Success

Source: Yahoo Finance

The Avengers S.T.A.T.I.O.NThe Avengers S.T.A.T.I.O.N. Las Vegas

Different Rooms To Learn More About Avengers Lore

Source: Victory Hill Exhibitions, UOB Kay Hian

The CityNeon Success?

Sets

Customer

Rented outFixed royalty portion: minimum guarantee (MG) upfront fee to use set. Anywhere from S$1-3m.

Customer bears cost of setting up the set at the location

Assembled Set

Variable royalty portion:20% of total ticket sales, merchandise sales net of MG

Sets are insured by customer for US$7m each

Other expenses10% of royalties go to Marvel

Licensing Fee: Depends on length of contract.

Outside of Las Vegas (Low execution risk)

Las Vegas (Full execution risk)

Sets

Assembled Set

Permanent fixtures at Treasure IslandSet up cost borne by Cityneon

Revenue streams:- Ticket sales- Merchandise- Ticket service charge - Naming rights to building

Other expenses-10% of royalties go to Marvel-Rental paid for building-Labor

Source: Cityneon, UOB Kay Hian

Cityneon Holdings (CITN SP/BUY/Target: S$1.02/Market Cap: S$216m*)

Data as at 20 July 16

Immersing In Marvel’s Victory

Explosive EPS 3-yr CAGR growth forecasted at 180%.

Sustainable growth momentum supported by Marvel and Transformers movie sequels all the way to 2020.

Scalable: Potential new Intellectual Property rights with other franchises provide exciting growth opportunities. (e.g. DC Comics, Star Wars)

SOTP-based TP of S$1.02, implying FY17F PE of 14.9x which is a 42% premium to peers’ average (10.5x).

11

0

80

160

240

320

400

480

0.00

0.20

0.40

0.60

0.80

1.00

1.20(%)(lcy)

CITYNEON HOLDINGS LTDCityneon Holdings Ltd/FSSTI Index

0

20

40

Jul 15 Sep 15 Nov 15 Jan 16 Mar 16 May 16

Volume (m)

A Buffet Of Brands – Katrina Group

Source: Katrina Group

Peer Group

Source: Yahoo Finance

31.54.014.217.0-54.40.315SGDKTG SPKatrina Group

17.6 2.7 19.4 22.4 29.4 Average

19.5 2.5 18.3 21.3 25.7 527 97.75THBOISHI TBOishi Group Pcl

10.6 1.6 17.8 22.6 40.9 232 1.105SGDBREAD SPBreadtalk Group Ltd

15.3 3.6 21.7 23.8 25.6 1,368 52.25THBM TBMk Restaurants Group Pcl

14.7 3.3 14.5 15.8 16.2 216 1.94MYROTB MKOldtown Bhd

27.5 2.0 21.3 24.6 38.7 306 0.64SGDJUMBO SPJumbo Group Ltd

18.3 3.1 22.5 26.3 29.1 1,967 26.15HKD341 HKCafe De Coral Holdings Ltd

Peer Comp

20162016201720162015(US$m)1-Aug-16Curr

ROE (%)Yield (%)PE (x)Mkt CapPrice @TradingTickerCompany

Katrina Group (KTG SP/BUY/Target: S$0.39/Market Cap: S$73m*)

Data as at 20 July 16

A Buffet Of Brands

34 restaurants, 9 brands cater to a variety of different palates. Clustering of different brands allow for better terms with landlords.

Halal certification for 4 our of 9 brands allows catering to the growing Muslim population. Halalcertification for restaurants provides a barrier to entry as Muis conducts audits and requires an in-house Halal team

Strong cash flow generation. Free cash flow for FY13-15 was S$2.1m to S$3.9m with minimal debt. Aiming to open 4 outlets per annum.

Online and regional expansion to spur growth.

PE-based target price of S$0.39 based on a 10% discount to peers average PE ratio.

11

70

90

110

130

150

170

190

0.15

0.20

0.25

0.30

0.35

0.40(%)(lcy) KATRINA GROUP LTD Katrina Group Ltd/FSSTI Index

0

20

40

60

Jul 16

Volume (m)