Embed Size (px)

Citation preview

SIM Fund 2014

MBA Presentation - December 5, 2014

James Lyle Noel HillNic KostmanAishwarya Srinivasan

Eugene Lee Jeremy Mortensen Rob Bayless Tyler Blue

2

Agenda Team Intro Objectives Quantitative Strategy

Intro Approach Today’s Portfolio

REITs Intro Today’s Portfolio

3

SIM Fund Objectives

Apply range of course principles to fund management

Utilize resources to maximize learning Manage scope

Portfolio Model 85% - Quantitative Strategy (core) 15% - REITs (diversification)

4

Dividend Premium Strategy

5

Dividend Stock Pricing Anomaly “…Companies have positive

abnormal returns in months when they are predicted to issue a dividend”

(Hartzmark & Solomon 2012)

6

Div-ExDiv Declared

Buy(Div Declared -1)

Sell(Div-Ex)

Dividend Stock Pricing Anomaly

Why does it exist?

Mutual fund demand to pass through dividends (Harris, Hartzmark, and Solomon 2014)

Cash guarantee

7

Constraints

Limited Human Capital Solution: Cap holdings

Trading Rules Solution: Weekly trades on schedule

Uneven distribution of declared dividends Solution: Adjust weights

8

Exclusionary Rules

Traded in the Russell 1000 Index Domiciled in the US Market Cap over $10 billion Exclude the sectors: Insurance, Banks, Utilities, REIT Had Quarterly Dividends over the past year

Universe: 191 securities Team plans to cap holdings with a maximum of 80

9

Div-Ex B

Div Declared A

Buy A, B

Weekly trade schedule

Div Declared B Div Declared C

Div-Ex CDiv-Ex A

Buy CSell A, B

Sell C

10

Strategy comparison

Day trading Weekly trading

Closer to the true dividend model:

Less holding period prior to undeclared

Capture the pure declared-to-ex holding period

Cash drag with scalability As number of holdings increase,

timing differences between stocks cause cash drag

Scheduled activities Timed buy and sell handoff on a

weekly basis; less cash drag Easier to manage scale

Less “efficient” Longer holding period outside of

declaration alpha (up to 6 days), and holding period is only 22 days on average.

Missed ex-date alpha

11

Investment Universe

12

Gantt Chart

Initial Selection – Pure Strategy

13

Initial Selection – Pure + Lead Time

14

Initial Selection – Pure + Lead Time, Weekly

15

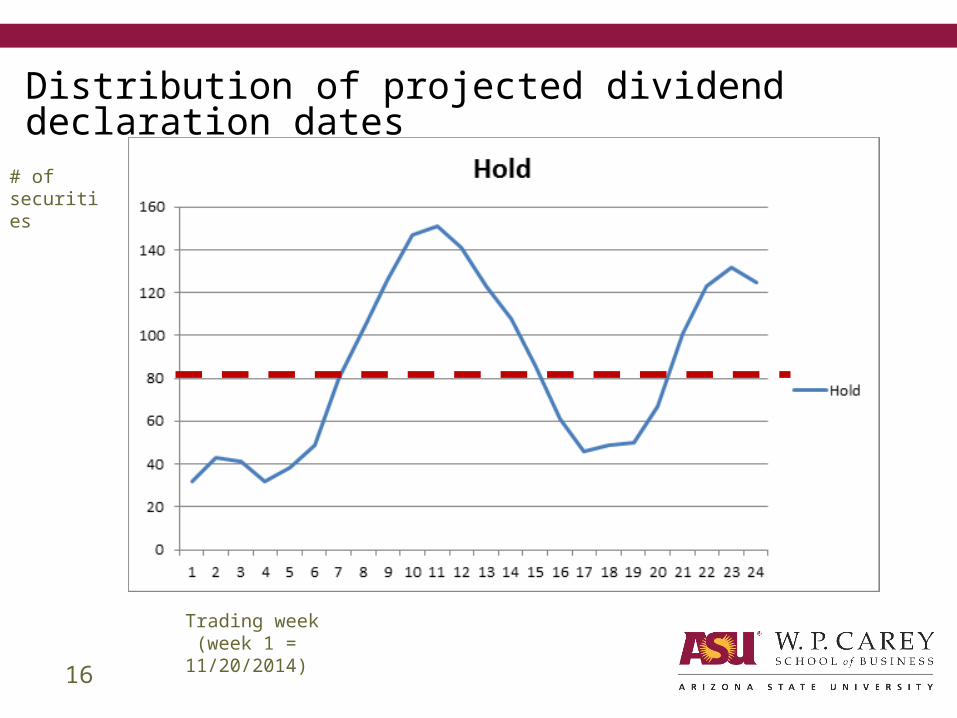

Distribution of projected dividend declaration dates

16

# of securities

Trading week (week 1 = 11/20/2014)

Weighting strategy

17

Issues going forward

Need to maintain diverse holdings (>30) Limited human resources

Cap total holdings to ensure oversight and adequate trade volume

Securities assigned to individual team members for monitoring

Avoid Closet Indexing

18

Portfolio Today – Seeding

Initial seeding on November 20 32 Securities

3 securities eliminated due to deviation from forecast Approximately $18,000 per position

19

Portfolio Today – Industry Mix

20

REITsStrategy

22

REITs – Overall strategy

Approximately 15% of total portfolio Primary purpose (for us) is diversification Focused on ETFs with low expense ratios,

high trading volumes, and high assets under management Also filtered out REIT ETFs from non-reputable

companies

22

REITs – Holdings

23

REITExpense

RatioYTD Ret 3Y Ret 5Y Ret Yield Holdings

Std Dev

AUM (Mil) Vol.

Age (Years)

Vanguard REIT ETF

0.10% 14.11% 16.54% 15.92% 3.51% 139 4.76% 25969.1 5.6 mil

10.19

SPDR Dow Jones REIT ETF

0.25% 14.52% 15.85% 15.50% 3.22% 92 5.47% 2902.9 180k 13.62

Vanguard Global ex-U.S. Real Estate Index Fund

0.27% 4.09% 14.33% n/a 4.28% 632 2.25% 2156.4 293k 4.08

REITs – ETFs: Why we chose them Pros:

Strong performance across most REIT sectors

Highly liquid Diversification Not correlated with rest

of strategy Can hedge against

inflation

Cons: Sensitive to increases

in interest rates Falling occupancy rates

hurt profitability Differentiation

24

Thank you

Questions?

27

Appendix

26

Weighting strategy - traps

27

Anticipated attrition of Week 1 purchase over 14 weeks

28