Embed Size (px)

Citation preview

SHOOT FOR THE STARS? PREDICTING THE RECRUITMENTOF PRESTIGIOUS DIRECTORS AT NEWLY PUBLIC FIRMS

ABHIJITH G. ACHARYASingapore Management University

TIMOTHY G. POLLOCKThe Pennsylvania State University

This study explores how CEOs’ and outside directors’ desires for the benefits ofsignaling and “homophily” intertwine with their concerns over maintaining powerand preserving local status hierarchies to affect the likelihood a firm recruits presti-gious outside directors to its board. Using pooled cross-sectional data on the five yearsfollowing the initial public offerings (IPOs) of 210 firms that went public between 2001and 2004, we found that prestigious CEOs and directors viewed the recruitment ofprestigious new directors differently and that these perceptions were moderated byfactors that increase the salience of risk of potential losses to CEOs and existing boardmembers.

How firms convey their “quality” through pres-tigious affiliations has long captured researchers’interest (e.g., D’Aveni, 1990; Higgins & Gulati,2006; Stuart, Hoang, & Hybels, 1999). The centralpremise of this research stream is that firms inambiguous circumstances, particularly young com-panies that lack established track records or priorperformance histories, seek to reduce others’ uncer-tainties by forging exchange relationships withprestigious or high-status actors, thereby signalingtheir quality through these actors’ willingness toaffiliate with them (Podolny, 1993, 1994; Zimmer-man & Zeitz, 2002). In particular, young firms thatconduct initial public offerings (IPOs) have gar-nered considerable attention from entrepreneur-ship and strategy scholars, who have examined thebenefits of affiliations with top-tier venture capital

firms (Gompers & Lerner, 2004; Lee, Pollock, & Jin,2011; Sanders & Boivie, 2004), prestigious under-writers (Fischer & Pollock, 2004; Gulati & Higgins,2003; Pollock, 2004), and prestigious executives(Higgins & Gulati, 2006; Pollock, Chen, Jackson, &Hambrick, 2010) and directors (Certo, 2003; Chen,Hambrick, & Pollock, 2008; Deutsch & Ross, 2003).

Implicit in all this research is the critical assump-tion that firms prefer prestigious to nonprestigiousaffiliates—an assumption that has not been ex-posed to much systematic scrutiny. Indeed, eventhough recent research has begun to consider thebenefits to prestigious actors of affiliating with non-prestigious actors (Castellucci & Ertug, 2010) andthe negative performance consequences of havingtoo many stars on a team (Groysberg, Polzer, &Elfenbein, 2011), little research has been conductedexploring the extents to which actors recognize andweigh the costs of a prestigious affiliation relativeto its benefits or identified circumstances underwhich perceived costs outweigh benefits in theirinfluence on decision making. To the extent thatthe costs of prestigious affiliations have been con-sidered, the focus has been primarily on financialcosts (e.g., Chen et al., 2008; Hsu, 2004), a concernthat speaks to the means of obtaining prestigiousaffiliates, but not to the desire to do so. Little re-search we are aware of has considered how nonfi-nancial costs can affect the desire to pursue presti-gious affiliations, even when a firm possesses the

Both authors contributed equally to this article. Wewant to thank our action editor and the three anonymousreviewers for all their helpful guidance and suggestions.We also want to thank Laura Field, Scott Graffin, DavidGras, Don Hambrick, Peggy Lee, Vilmos Misangyi, TimQuigley, and the participants in seminars at ArizonaState University, Indiana University, Penn State Univer-sity, the University of California, Irvine, the University ofTexas–Austin and the University of Washington–Seattlefor their helpful comments on drafts of this article. Wealso want to thank Jatinder Jassal for her assistance withthe data collection. We also thank Penn State Universityfor its financial support.

1396

� Academy of Management Journal2013, Vol. 56, No. 5, 1396–1419.http://dx.doi.org/10.5465/amj.2011.0639

Copyright of the Academy of Management, all rights reserved. Contents may not be copied, emailed, posted to a listserv, or otherwise transmitted without the copyright holder’s expresswritten permission. Users may print, download, or email articles for individual use only.

capability to do so via existing stores of prestige(Chen et al., 2008; Pollock et al., 2010).

This issue is important because prior researchhas shown that when it comes to the prestige of afirm’s existing directors, market reactions suggest“more is better” (Pollock et al., 2010). However, wecontend that affiliating with prestigious actors caninvolve considerable internal costs, as adding pres-tigious new actors to a group can disrupt the exist-ing status order and power structure (Bendersky &Hays, 2012; Groysberg et al., 2011; Magee & Galin-sky, 2008). Thus, the perceived desirability of pres-tigious affiliations is likely to vary more than hasbeen assumed. We argue that there are diminishingmarginal benefits and increasing marginal costs toadding more prestigious directors to the board, andthat concerns about the relative costs are height-ened when existing prestigious directors and/or theCEO perceive a threat to their power or standing inthe local status order from adding a prestigious newdirector (Brehm & Brehm, 1981; Cialdini, 2004;Kahneman & Tversky, 1979).

We situate this study in the context of recruitingnew outside directors during the crucial five yearsfollowing a company’s initial public offering (IPO)(Fischer & Pollock, 2004; Kroll, Walters, & Le,2007). Recruiting prestigious directors is a complexsociopolitical process that affects and is affected bya firm’s CEO and incumbent directors (Stern &Westphal, 2010; Westphal & Khanna, 2003). Whileprestigious directors can signal a firm’s unobserv-able quality and provide other benefits associatedwith “homophily,” the desire to associate with oth-ers who share similar values, beliefs, interests, andother characteristics (McPherson & Smith-Lovin,1987; Stryker & Burke, 2000), they can also entailcosts for firms’ upper echelon members, becauseprestigious directors are more likely than nonpres-tigious directors to assert themselves in ways thatdisrupt a current within-group status order andthreaten others’ power and discretion (Bendersky &Hays, 2011; Hambrick & Finkelstein, 1987; Groys-berg et al., 2011). Thus, while prestigious affilia-tions generate many “external” benefits, the per-ceived desirability of prestigious new directors islikely to be contingent on the extent to which theyare also perceived to create internal, or “lo-cal,” costs.

We test our arguments using data from a five-year, pooled cross sectional sample of 210 firmsthat went public between 2001 and 2004. Directorrecruitment at newly public firms is a useful con-text for exploring this issue because prestigious

directors play an important role in a young firm’sdevelopment. IPOs bring about transformationalchanges that “reset the clock” on these firms’ “lia-bilities of newness” (Fischer & Pollock, 2004) andengender substantial uncertainty for external mar-ket evaluators (Jain & Kini, 2000). The ability torecruit and retain prestigious directors significantlyreduces perceived uncertainty during this period(Pollock et al., 2010; Spence, 1973), and a fair bit ofturnover is likely as early investors and othersleave an IPO firm’s board, and/or the board is ex-panded to include new members (Husick & Ar-rington, 1998). In addition, because all directorsreceive the same compensation for their service(Hambrick & Jackson, 2000), this context effectivelycontrols for the association between prestige andcost as an alternative explanation.

Answering the questions why and under whatconditions firms avoid recruiting prestigious direc-tors even when they have the ability to do so con-tributes to several different literatures. Exploringhow the perceived nonfinancial costs of prestigiousaffiliations could affect director recruiting deci-sions contributes to the literatures on corporategovernance and director labor markets (e.g., Coles &Hoi, 2002; Westphal & Zajac, 1995) by providinginsight into director recruiting decisions and iden-tifying some unintended consequences of “goodgovernance” practices. It also contributes to theliterature on status and homophily (e.g., Bendersky& Hays, 2011; McPherson & Smith-Lovin, 1987) byexploring how the social-psychological benefits ofhomophily can be tempered by countervailing con-cerns about the threats to existing actors’ power,and also by increasing understanding of why, andunder what conditions, high-status individualswant to associate with lower-status actors (Castel-lucci & Ertug, 2010; Frank, 1985). Finally, our studycontributes to the literature on signaling (Pollock &Gulati, 2007; Spence, 1973) by developing a morenuanced understanding of the internal factors thatcan influence decisions to engage in activitiesthat have potential signaling benefits, and the ac-curacy of certain governance characteristics assignals.

In the following sections, we first discuss theunderlying logic of signaling and explicate the ben-efits and costs of hiring prestigious directors. Wethen discuss how the prestige and power of a firm’sCEO and incumbent directors can affect their per-ceptions and the likelihood they will recruit newprestigious directors.

2013 1397Acharya and Pollock

THEORY AND HYPOTHESES

Benefits and Costs of Recruiting PrestigiousDirectors

Prestige is defined as an actor’s position in ahierarchical social order that is “tied to the patternof relations and affiliations in which the actor doesand does not choose to engage” (Podolny, 2005:13). Although we primarily use the term “prestige”in this study, “prestige” and “status” are synony-mous in organizational research (e.g., D’Aveni,1990; Podolny, 2005). An actor’s prestige is oftentreated as an indicator of its quality (Podolny,2005), particularly in highly uncertain situations(Higgins & Gulati, 2006; Podolny, 1994; Zimmer-man & Zeitz, 2002). To the extent an actor hasaffiliations with prestigious actors, it is also per-ceived as being of higher quality. In this study wefocus on one prestigious affiliate in particular: out-side directors.

The benefits of prestigious directors. In theirquest to reduce uncertainty, firms adopt organiza-tional structures—such as boards composed ofprestigious directors—that can convey the firms’quality (Certo, 2003; Chen et al., 2008; Higgins &Gulati, 2006). Indeed, Pfeffer and Salancik statedthat “prestigious or legitimate persons or organiza-tions represented on the focal organization’s boardprovide confirmation to the rest of the world of thevalue and worth of the organizations” (1978: 145).Recent research (Pollock et al., 2010) showed thatdirector prestige had a positive, linear relationshipwith initial market valuations of IPO firms, suggest-ing that when it comes to prestigious directors,from the market’s perspective more is better.

Prestigious directors also meet Spence’s (1973)two criteria for credible signals: they should be (1)observable and (2) costly to obtain. Membership ona firm’s board of directors is highly visible andeasily observable. Further, prestigious directorsbuild their status over the course of their careers byserving on boards of successful companies andearning elite educational and employment creden-tials (Certo, 2003; Pollock et al., 2010). Given thecostliness of acquiring prestige, prestigious direc-tors are selective in accepting board seats, therebyprotecting their relative standing in the directorlabor market (Fama, 1980; Pozner, 2008) and mak-ing them a valuable and somewhat difficult to ob-tain resource that conveys a firm’s quality to othermarket participants.

In addition, prior research suggests that presti-gious directors can yield more local benefits to a

firm’s executives and directors as a result ofhomophily and by enhancing their own individualstatus via direct affiliation (Chen et al., 2008;Deutsch & Ross, 2003). However, such affiliationscan also impose certain costs on a CEO and otherboard members. In particular, we argue that presti-gious directors are even more likely than nonpres-tigious directors to be actively involved memberswho try to assert their influence on a board (Fink-elstein, Hambrick, & Canella, 2009), which can dis-rupt the board’s prior working relationships andthreaten its current status ordering (Bendersky &Hays, 2011; Gabrielsson, 2007; Groysberg et al.,2011). It is to this issue we now turn our attention.

The costs of prestigious directors. While direc-tors in general represent the corporate elite, presti-gious directors represent this elite group’s innercircle (D’Aveni & Kesner, 1993; Davis, Yoo, &Baker, 2003). As their relative standing in the di-rector labor market is actively built over their ca-reers, prestigious directors carefully guard theirprestige. Arthaud-Day, Certo, Dalton, and Dalton(2006) showed that directors tend to exit firmswhose credibility is under threat to protect theirpersonal prestige. Furthermore, directors may ex-perience a “settling-up” in the director labor mar-ket whereby their past actions affect their statusand subsequent board appointments (Fama, 1980;Srinivasan, 2005).

Extending this line of thought, we argue thatprestigious directors are also likely to guard theirstatus by actively involving themselves in boardactivities. Prior research has shown that “peoplewith higher status have more opportunities to exertsocial influence, try to influence other group mem-bers more often, and are indeed more influentialthan people with lower status” (Levine & More-land, 1990: 600). They also tend to be evaluatedmore positively (Levine & Moreland, 1990). Withrespect to boards specifically, Finkelstein and col-leagues note, “prestigious directors are unlikely toserve solely as ‘rubber stamps’ because (1) they mayvery well have been in a position to select amongmultiple directorship offers and they likelywould not have decided to sit on a board wherethey would have no impact, and (2) prestige may beaccepted as a signal of managerial competence byfirm’s top managers (D’Aveni & Kesner, 1993),opening the door to a wider director role in strategyformulation” (2009: 267).

Further, by affiliating with young, unprovencompanies, prestigious directors face some risk ofstatus leakage (Castellucci & Ertug, 2010; Podolny,

1398 OctoberAcademy of Management Journal

2005). Prestigious individuals are likely to be con-scious of their relative standing in a social order(Frank, 1985; Hambrick & Canella, 1993), so theywill act to establish and/or maintain their presti-gious positions—working hard to increase a firm’ssuccess via increased monitoring (D’Aveni & Kes-ner, 1993; Fama & Jensen, 1983; Finkelstein et al.,2009) and/or offering advice and counsel to topexecutives more frequently (Lynall, Golden, & Hill-man, 2003)—or will exit the situation (Arthaud-Day et al., 2006; Hambrick & Canella, 1993; With-ers, Corley, & Hillman, 2012).

It follows, then, that prestigious directors aremore likely to be active board members who exerttheir power when interacting with executives andother board members, particularly at newly publicfirms, where circumstances are evolving and whereactive directors are likely to have the greatest directinfluence (Daily, McDowall, Covin, & Dalton, 2002;Gabrielsson, 2007). This level and intensity of in-volvement may seem intrusive to incumbent exec-utives and directors, who have their own perspec-tives and who have established work routines andan internal status structure among board members(Bendersky & Hays, 2011; Magee & Galinsky, 2008).Although none of this research has consideredboards of directors explicitly, it nonetheless hassignificant implications for board functioning(Hambrick, 1994). Boards of directors establishnorms and routines of interpersonal interaction(Wagner, Pfeffer, & O’Reilly, 1984) and informalhierarchies (He & Huang, 2011) over repeated inter-actions. New directors may be perceived as disrup-tive and potentially threatening, especially whenthey are powerful (Magee & Galinsky, 2008).

Thus, the addition of prestigious directors to aboard can bring both benefits and costs; whereasprestigious directors provide signaling value, ex-pertise, and valuable network connections, and canenhance the status of a firm and its executives andother directors (Certo, 2003; Graffin, Wade, Porac,& McNamee, 2008), they can also generate costs inthe form of challenges to the power of the CEO andcurrent directors, and disruptions to the internalstatus structure and operations of the board. Below,we develop hypotheses to predict how and whenCEO and board characteristics are likely to influ-ence perceptions of the relative benefits and costsof prestigious directors, and the likelihood that aprestigious director will be recruited to a newlypublic firm’s board. We argue that current directorsand CEOs weigh the benefits and costs of a presti-gious new director differently as a function of their

prestige and of circumstances that decrease the per-ceived costs associated with recruiting a presti-gious new director.

Recruiting Prestigious Directors

Board prestige. Research on board service hasconsidered a variety of nonfinancial motivationsthat lead directors to serve on or exit boards(Boivie, Graffin, & Pollock, 2012; Lorsch & MacIver,1989). This research has suggested that a primarymotivation to accept a board seat is establishingand/or maintaining membership in the corporateelite. As such, prestigious directors are more likelyto be attracted to boards composed of other presti-gious directors (Certo, 2003). This attraction is dueto homophily, or the desire to associate with otherswho share similar values, beliefs, interests, andother characteristics (Stryker & Burke, 2000). Thesesimilarities ease communication and build trust(Lazarsfeld & Merton, 1954; McPherson & Smith-Lovin, 1987) and decrease the duration of dissimi-lar and mismatched associations (Wagner et al.,1984). Further, in the case of status, homophily alsotends to reinforce current status orderings (Pearce,2011; Podolny, 1993).

Newly public firms tend to vary in their stocks ofboard prestige at IPO as a function of their foundingconditions and their early efforts to recruit presti-gious directors (Beckman, Burton, & O’Reilly, 2007;Chen et al., 2008). Recent research has demon-strated that firms with existing stores of prestigehave an easier time recruiting other prestigious ac-tors (e.g., Higgins & Gulati, 2006; Chen et al., 2008)and experience more positive organizational con-sequences as a result (e.g., Pollock et al., 2010;Stuart et al., 1999). Given the signaling and ho-mophily benefits associated with prestigious affili-ations, we expect this process to continue follow-ing an IPO as a board is expanded and/or currentdirectors leave the board.

However, this relationship is unlikely to be lin-ear. Recent research has shown that while addingprestigious individuals can increase group perfor-mance initially, this effect diminishes as the num-ber of prestigious individuals increases. Benderskyand Hays (2011) distinguished among task, rela-tionship, process, and status conflict in groups anddemonstrated that status conflict not only led to adecrease in group performance, but also moderatedthe effects of task conflict (i.e., conflict over what agroup should do) on group performance. Theirfindings are consistent with earlier research sug-

2013 1399Acharya and Pollock

gesting that executives whose relative position inthe corporate status hierarchy diminishes follow-ing an acquisition were more likely to leave a com-pany (Hambrick & Cannella, 1993) and that havingtoo many stars on a team can lead to a decrement ingroup performance (Groysberg et al., 2011).

Thus, we expect that while the prestige of afirm’s current directors can increase the likelihoodthe firm both desires and is able to attract presti-gious new directors (Chen et al., 2008), as theboard’s pre-existing prestige increases, the costs ofrecruiting prestigious new directors become moresalient and the marginal benefits in terms of signal-ing, homophily, and status enhancement diminish.We therefore hypothesize,

Hypothesis 1. When a new outside director isrecruited, a firm’s preexisting board prestigehas a positive but diminishing relationshipwith the likelihood the new director isprestigious.1

CEO prestige. Like prestigious directors, presti-gious CEOs also face competing incentives to re-cruit prestigious new directors. On the one hand,the presence of prestigious directors sends positivesignals that ease resource acquisition, create strate-gic opportunities for a CEO, increase the CEO’sown relative status, and provide the benefits ofhomophily (Hillman et al., 2009; Pfeffer & Salancik,1978). Further, firms headed by prestigious CEOsare likely to be attractive to prestigious outsidedirectors. As noted earlier, directors form an elitegroup, or inner circle, of highly influential corpo-rate leaders (D’Aveni & Kesner, 1993; Davis et al.,2003). Gaining an additional board seat that ex-pands a director’s elite network is another benefitof sitting on a prestigious CEO’s board. Thus, allelse being equal, prestigious CEOs are not onlylikely to enhance their own prestige by affiliatingwith prestigious directors; they will also have aneasier time recruiting prestigious directors becauseof the status affiliation benefits they offer (Graffin etal., 2008; Podolny, 1993, 1994).

Like directors, prestigious CEOs may also per-ceive significant costs associated with recruiting

prestigious outside directors that offset the per-ceived benefits. CEOs tend to be independent, am-bitious individuals (Hambrick, 1994; Hiller & Ham-brick, 2005). Further, the desire to maintain theirindependence and be their own boss is one of themajor factors that drive entrepreneurs to start newbusinesses (Sapienza, Korsgaard, & Forbes, 2003;Shane, 2008). As such, we expect the CEOs ofnewly public firms to resist actions that could re-strict their discretion (Hambrick & Finkelstein,1987) or diminish their power (Westphal, 1998).Thus, they too may be apprehensive about what anew prestigious director may attempt to do if askedto join their board, and how it will affect their ownstanding in the board’s status order.

However, scholars have found that CEOs canpreserve their discretion by engaging in sophis-ticated interpersonal interactions when theirboards’ structural independence is increased(Stern & Westphal, 2010; Westphal, 1998), sug-gesting prestigious CEOs may be less concernedabout adding a prestigious director because theythink they have other means of maintaining theirdiscretion. Thus, all else being equal, we expectthe benefits of signaling and homophily to out-weigh the potential costs and prestigious CEOs tobe more rather than less likely to recruit presti-gious directors. We therefore hypothesize,

Hypothesis 2. When a new outside director isrecruited, the presence of a prestigious CEO ispositively related to the likelihood the new di-rector is prestigious.

Framing Prestigious Director Recruitment as aGain or Loss

Our first two hypotheses are based on conditionsthat “hold all else equal.” However, contextual fac-tors may affect whether the recruitment of a pres-tigious director is framed as a potential gain or lossfor individual directors and/or CEOs and thus in-fluence the weights they assign to the perceivedcosts and benefits of recruiting a prestigious out-side director. Two psychological processes—lossaversion (Kahneman & Tversky, 1979) and psycho-logical reactance (Brehm & Brehm, 1981; Wright,Wadley, Danner, & Phillips, 1992)—suggest thatfactors increasing concerns about the loss of anactor’s status and/or their discretion to act willweaken the positive relationships predicted above.

Loss aversion. A central tenet of prospect theory(Kahneman & Tversky, 1979; see Holmes, Bromi-

1 Although firms can and do recruit more than onedirector in a given year, there were too few instances inwhich more than one new director was prestigious in agiven year to test for the recruitment of multiple presti-gious directors. We therefore phrase our hypotheses interms of recruiting a prestigious director. We address thisissue in our discussion of future research directions.

1400 OctoberAcademy of Management Journal

ley, Devers, Holcomb, and McGuire [2011] for arecent review of the literature) is that individualsweight the potential for gains and losses asymmet-rically and as a function of whether they are cur-rently in a gain or loss position. In general, indi-viduals are more concerned with avoiding lossesthan they are with capturing gains (Holmes et al.,2011; Kahneman & Tversky, 1979). Further, theseassessments are made relative to a reference point,and how a decision is framed can have a significantinfluence on the decision made (Bazerman, 1984;Tversky & Kahneman, 1981). In the context of ourstudy, this suggests that if CEOs and directors feelconfident they can maintain their position in alocal status order and/or discretion, they are morelikely to focus on the gains to be had from recruit-ing prestigious outside directors. However, if theyare less confident in this assessment, then the costswill be weighted more heavily than the benefitsand the likelihood of recruiting a prestigious out-side director will be reduced. Thus, factors thatincrease CEO and/or director confidence that cir-cumstances won’t change if a prestigious new di-rector is recruited should result in a more positiveframing focused on the benefits of adding a presti-gious new director and increase the likelihood aprestigious director is recruited.

Psychological reactance. Psychological reac-tance theory (Brehm & Brehm, 1981; Wright et al.,1992) describes individuals’ reactions to the per-ceived threat of losing control or discretion. It sug-gests that individuals who perceive threats to theirfreedom and control will resist pressure to takeactions that increase these threats. Further, psycho-logical reactance theory suggests that individualsfight harder to avoid losing something they cur-rently possess than they do to acquire somethingthey do not already own or control (Cialdini, 2004).Research in psychology has also shown that suchreactions are more likely in individuals with highself-esteem or internal locus of control, two person-ality traits that typically characterize upper eche-lons members (Brehm & Brehm, 1981; Brockner &Elkind, 1985; Hiller & Hambrick, 2005). Thus, psy-chological reactance theory suggests that directorsand CEOs will fight aggressively to protect theirdiscretion and/or status if they perceive them to bethreatened. In this context, that means they wouldresist recruiting a prestigious new director if theyfelt it threatened the status quo. Below we considertwo contextual factors—one at the board level andthe other at the CEO level—that can influence how

threatening recruiting a prestigious new director islikely to be perceived to be.

Board tenure. Boards are primarily groups ofindividuals (Finkelstein & Mooney, 2003; Ham-brick, 1994), and while the benefits of recruitingprestigious directors are clear, bringing additionalprestigious directors onto a board can also increasestatus and role conflict and decrease overall groupcohesion and performance (Bendersky & Hays,2011; Groysberg et al., 2011). Maintaining effectivegroup processes can be particularly challenging forboards, both because directors meet only episodi-cally (e.g. Forbes & Milliken, 1999) and becausetheir roles are more ambiguous than the CEO roleand thus more apt to be consensually negotiated(Finkelstein & Mooney, 2003; He & Huang, 2011).

Although the addition of any new director can bedisruptive, the addition of a prestigious directorhas greater potential to be disruptive because it ismore likely to affect a current social order. Presti-gious directors tend to be powerful actors who aremore likely to try imprinting their own perspec-tives and ways of functioning on the board (e.g.Westphal & Zajac, 1995) and who will want toestablish their positions at or near the top of thewithin-group status hierarchy (Bendersky & Hays,2012; Hambrick & Cannella, 1993). Thus, they maybe more likely to disrupt group processes and co-hesion and create personal threats to the relativestanding of prestigious directors already on theboard.

However, the extent to which directors haveworked together for longer periods of time can af-fect whether boards perceive themselves to be sus-ceptible to the costs of adding a prestigious newdirector, and thus whether adding a prestigiousdirector will be framed as a potential for gain orloss. He and Huang (2011) found that clarity indirectors’ relative standings on a board increasesboard functioning. Contests over individuals’ rela-tive standings in a social order are more likely tooccur early in a group’s development, when indi-viduals are still getting to know each other andestablishing relationships. Directors who haveserved together for longer periods of time may haveless uncertainty about their place in their localstatus order and may perceive the current order tobe more entrenched and unlikely to change (Han-nan & Freeman, 1984), enhancing their optimismthat they can maintain their positions in the face ofnew competitive threats (Camerer & Lovallo, 1999)and thereby reducing the perceived costs of addinga new prestigious director. Prior research on teams

2013 1401Acharya and Pollock

and working groups has also demonstrated that thetenure of members in any group is an importantfactor influencing team processes such as commu-nication, cohesion, trust, and social integration(e.g., Chatman & Flynn, 2001; Harrison, Price, &Bell, 1998). Furthermore, as communication pat-terns become routinized over time, new directorsare less likely to form communication linkageswith incumbent board members right away, reduc-ing the new directors’ immediate influence (Wag-ner et al., 1984).

Taken together, this suggests that whereas direc-tors who have served together for longer periods oftime are less likely to perceive the addition of aprestigious new outside director as a threat to theirrelative standing, thereby decreasing the likelihoodloss aversion and psychological reactance will betriggered, directors who have worked together forshorter periods may be more susceptible to theseprocesses. We therefore hypothesize:

Hypothesis 3. When a new outside director isrecruited, the positive but diminishing rela-tionship between pre-existing board prestigeand the likelihood the new director is presti-gious is stronger the longer existing directorshave worked together.

Additional sources of CEO power. Like presti-gious directors, prestigious CEOs are also like tovary in their reaction to recruiting a prestigiousnew director depending on whether they perceive agreater potential for gain or loss. Whereas the pri-mary concern for directors is more likely to be withrelative standing in the local status order and groupdynamics, for CEOs the primary concern is likely tobe whether they will be able to maintain their dis-cretion and ability to act as they see fit, which is afunction of a CEO’s sources of power (Finkelstein,1992; Hambrick & Finkelstein, 1987).

While prestige is one source of a CEO’s power(Finkelstein, 1992), Finkelstein identified two ad-ditional sources of executive power: the structuralfeatures of an organization (i.e., structural power)and ownership (i.e., ownership power).2 Greaterlevels of CEO structural and ownership power in-fluence a variety of governance behaviors and stra-tegic corporate initiatives (e.g., Dalton, Daily, Ell-

strand, & Johnson, 1998; Fischer & Pollock, 2004;Nelson, 2003; Pearce & Zahra, 1991; Westphal,1998), and can influence whether prestigious CEOsview a prestigious new director as an opportunityor a threat.

Structural power is derived from the formal or-ganizational structures and hierarchical authoritythat provide a CEO with “the legislative right” (Fin-kelstein, 1992: 509) to exert influence. Serving asboth a firm’s CEO and chairman of the board, in-cluding fewer outside directors on the board, andestablishing governance rules that reduce the threatof hostile takeovers (e.g., Westphal, 1998; Westphal& Zajac, 1995) are examples of structural sources ofCEO power. Ownership power derives from aCEO’s direct ownership of stock (e.g., Boeker &Karichalil, 2002; Pollock, Fund, & Baker, 2009) andfrom being a company’s founder (Nelson, 2003). AsFinkelstein noted, “managers who are founders ofthe firm or related to founders may gain powerthrough their often long-term interaction with theboard, as they translate their unique positions toimplicit control over board members” (1992: 509).Founder status may also confer additional expertpower to the extent the founder is viewed as avisionary leader who has greater knowledge andinsight into the market and/or characteristics of thecompany’s products or technology (e.g., Nel-son, 2003).

Although in general we expect prestigious CEOswill focus more on the benefits than the costs ofrecruiting prestigious new directors, we expect thisrelationship to be stronger the more secure they feelabout their ability to maintain their discretion andinfluence. Possessing multiple sources of powercan enhance this sense of security. Thus, a presti-gious CEO who also possesses structural and/orownership power may be less likely to frame theaddition of a prestigious new director in terms ofloss rather than gain. We therefore hypothesize,

Hypothesis 4. When a new outside director isrecruited, the positive relationship betweenCEO prestige and the likelihood the new direc-tor is prestigious is stronger the greater thestructural and ownership power of the CEO.

DATA AND METHODS

Sample

The data for this study were obtained from theprospectuses filed for all the IPOs conducted be-

2 Although the characteristics we discuss are sourcesof power, and thus antecedent to the actual exercise ofpower, for ease of exposition we hereafter refer to them as“structural power” and “ownership power.”

1402 OctoberAcademy of Management Journal

tween 2001 and 2004 and annual proxy statementsfiled with the Securities and Exchange Commission(SEC) for the five years following the IPOs. Priorresearch has shown that firms are considered“newly public” during the initial five years follow-ing their IPOs and “seasoned” public entities there-after (Fischer & Pollock, 2004; Kroll et al., 2007).Consistently with prior research (e.g. Fischer & Pol-lock, 2004), we excluded closed-end mutual funds,real estate investment trusts (REITS), unit offerings,spin-offs, demutualization of savings banks and in-surance companies, and leveraged buyouts (LBOs)from the analysis. The final sample consisted of232 firms. Missing data reduced this sample to210 firms.

Not all of these firms existed as independententities for all five years of observation. Seventy-seven of the firms were delisted from the stockexchange on which they traded during our periodof study owing to acquisition, bankruptcy, or fail-ure to meet minimum exchange requirements. De-listing data were obtained from the CRSP database.Delisted firms were dropped from the sample afterdelisting occurred, and all other firms were treatedas “right censored,” resulting in 826 firm-yearobservations.

Dependent Variable: Recruitment of a PrestigiousDirector

The dependent variable in this study was therecruitment of a prestigious director in a given year.As in prior research (e.g., D’Aveni, 1990; Chen etal., 2008; Pollock et al., 2010), outside directorswere considered prestigious if they possessed atleast one of the following credentials: a degree froman elite educational institution on Finkelstein’s(1992) list of 20 institutions (educational prestige),experience as an executive at the level of vice pres-ident or above at a Standard & Poor’s (S&P) 500company (employment prestige), or experience asan outside director in an S&P 500 firm (directorialprestige). Although Chen and colleagues focusedon S&P 100 companies, they conducted a single-industry study that included only software compa-nies in three four-digit SIC categories. Because oursample covers 41 industries at the two-digit SIClevel, replicating this level of granularity was notfeasible. When determining the prestige of direc-tors’ prior employment and outside directorships,

we constructed a lagged-year list of S&P 500 firmsfor each year of the study.3

We operationalized director prestige two differ-ent ways. First, since we were interested in whethera prestigious new director was recruited, we con-structed a time-variant dichotomous measurecoded 1 when a firm recruited a director who pos-sessed any of the three prestige credentials in agiven year and 0 otherwise. An average of 33.74percent of firms in any given year reported addingat least one prestigious outside director to theirboards. There was little variation in this averageacross years, which ranged from a low of 29 percentin year 5 to a high of 36 percent in years 1 and 2.

Second, we created a count variable ranging fromzero to three that captured the number of prestigecredentials a new director possessed. This measurereflects how prestigious a new director is. Sixty per-cent of the prestigious new directors in our samplehad one source of prestige, 34 percent had twosources of prestige, and 6 percent had all threesources of prestige.

Independent Variables

Board prestige. This measure was calculated asthe aggregate number of continuing prestigiousdirectors that served on a focal firm’s board in agiven year. We also included the square of thismeasure to test for the hypothesized curvilinearrelationship.

CEO prestige. This measure was operationalizedin the same manner as director prestige. CEO pres-tige was coded 1 if the CEO possessed any one ofthe three prestige credentials (educational, employ-ment, or directorial prestige) and was coded 0otherwise.

Average board tenure. We operationalized theamount of time directors had worked together asthe average tenure of board members (Carpenter,2002; Fischer & Pollock, 2004). This measure wascalculated by summing the number of years eachindividual served as a director on a focal firm’s

3 In analyses not reported here we also exploredwhether there were differences in the effect of each pres-tige indicator on the likelihood a prestigious director wasbe recruited by using each indicator separately in ouranalysis. We did not find any substantive differencesamong the indicators in the construction of the presti-gious director independent variables or dependent vari-able in effects on the likelihood of recruiting prestigiousoutside directors.

2013 1403Acharya and Pollock

board (director tenure) listed in the offering pro-spectus and the annual proxy statements and di-viding the sum by the total number of directors onthe board.4

CEO ownership power. CEO ownership powerwas operationalized using two measures: the per-centage of stock owned by a firm’s CEO, andwhether or not the CEO was a company founder(Finkelstein, 1992). CEO stock ownership equaledthe percentage of shares outstanding at the end ofthe year beneficially held by a firm’s CEO (Fischer& Pollock, 2004). Founder CEO status was coded 1if the CEO was the company founder and 0otherwise.

CEO structural power. CEO structural powerwas operationalized using three measures: CEO du-ality, percentage of outside directors, and use ofstaggered elections of directors. Companies some-times stagger the elections of their directors so thatonly a minority of directors is up for reelection in agiven year to reduce the likelihood of hostile take-overs. CEO duality was coded 1 if a CEO was alsothe chairman of his/her firm’s board in a given yearand 0 otherwise. The outside director ratio equaledthe number of outside directors on a firm’s board,defined as directors lacking any current or pastexecutive positions in the firm and not related toany current employees (e.g., Daily et al., 2002),divided by the total number of directors on theboard. Staggered board was a dummy variablecoded 1 if a firm’s board had staggered electionsand 0 otherwise.

Control Variables

Time-invariant IPO characteristics. Followingprior research (Chen et al., 2008; Pollock, Rindova,& Maggitti, 2008), we controlled for several charac-teristics of an IPO that could create initial condi-tions with long-term consequences for a firm’s de-velopment and ability to attract prestigiousdirectors (e.g., Baron, Hannan, & Burton, 1999;Fischer & Pollock, 2004). Offer size was calculatedas the product of the total number of shares offeredduring an IPO and its offering price. Offer size cansignal the market about a firm’s quality and stabil-

ity (e.g. Fischer & Pollock, 2004; Ibbotson & Ritter,1995). To reduce the effect of extreme values, wetransformed this variable into its natural logarithm.Underpricing was calculated as the percentagechange in a stock’s price ([end price – initial price)/[initial price]) on the first day the stock tradedpublicly on a national exchange (e.g., Loughran &Ritter, 1995). The data used to calculate underpric-ing were drawn from CRSP. Underpricing has beenfound to create buzz and enhance expectations of afirm’s potential, and thus its ability to acquire re-sources during the years following IPO (e.g., Je-gadeesh, Weinstein, & Welch, 1993; Pollock & Gu-lati, 2007). VC backing was a dummy variablecoded 1 if a firm received financial backing fromventure capitalists (VCs) prior to IPO and 0 other-wise. Prior research has shown that VC backingsignificantly affects the prospects of a firm at IPOand beyond (Jain & Kini, 2000). VC prestige was adummy variable coded 1 if any of the venture cap-italists backing a firm were listed as prestigious byPollock and colleagues (2010) and 0 otherwise.5

Prestigious venture capitalists have been shown topositively affect IPO performance and the ability toattract other prestigious actors (Jain & Kini, 2000;Pollock et al., 2010). Underwriter prestige was opera-tionalized using ratings developed by Carter andManaster (1990) and updated by Ritter (http://bear.warrington.ufl.edu/ritter/ipodata.htm). We codedthe lead underwriter in a given IPO as prestigious ifit received the top ranking in the modified Carter-Manaster ranking system for 2001–04 and 0 other-wise. Controlling for underwriter prestige is impor-tant as these are prominent intermediaries thathave been found to attract other prominent actors(Chen et al., 2008; Pollock et al., 2010).6

4 In analyses not reported here we also calculated analternative measure using the average of the pair-wiseoverlap in service among each director (e.g., Barkema &Shvyrkov, 2007). The results were the same as re-ported here.

5 In analyses not included here, we used the counts ofprestigious VCs and underwriters (controlling for thetotal numbers of VCs and underwriters). These measureswere not significant, and our primary analyses remainedsubstantively the same.

6 Another source of prestige that could be relevant forour analysis is top management team (TMT) prestige(e.g., Higgins & Gulati, 2006; Pollock et al., 2010). Whilean offering prospectus provides detailed information ona firm’s entire top management team, we were unable tofind a reliable source of information on full TMT mem-bership or members’ backgrounds for the years followingIPO. In analyses not reported here, we included controlsfor TMT prestige and TMT size at IPO. Neither measurehad a significant relationship with recruiting a presti-gious director. Our other results were unchanged.

1404 OctoberAcademy of Management Journal

Time-varying firm characteristics. We also con-trolled for a number of firm-level characteristicsthat varied over time. Firm size was measured asthe natural logarithm of annual sales. This measurewas log-transformed to reduce the effects of ex-treme values. As some of the firms did not have anysales in their year of IPO, we added a 1 to the salesof each company before transforming the values.Firm age at IPO was measured as the difference inthe number of years between the year of incorpora-tion and the year of IPO. We again log-transformedthe variable to minimize the effects of extreme val-ues. Firm performance equaled total stockholderreturn (TSR) for a given year. A commonly usedstock market indicator of firm performance (e.g.,Sanders & Hambrick, 2007), TSR was calculated asyear-end stock price minus year-start stock price,plus dividends paid, divided by year-start stockprice. Board size, calculated as the total number ofdirectors on a firm’s board, has been used in priorresearch to signify the extent to which resources areavailable and affect the extent to which firms cansignal quality via prestigious outside directors(Certo, Daily, & Dalton, 2001).7

CEO tenure. CEO tenure is another potentialsource of power and can also affect the workingrelationships that a CEO has established with aboard. This measure was operationalized as thenumber of years a CEO had held his/her position ata given firm.

Multiple hires. All else being equal, firms thatrecruit more than one director in a given year maybe more likely to add a prestigious director. Multi-ple hires was a dummy variable coded 1 if a firmrecruited more than one director in a given yearand 0 otherwise.

Total departures. Recruiting new directors islikely to be a function of director exits; that is, firmsare more likely to recruit new directors when in-cumbent directors leave their boards. This measurewas operationalized as the number of directorsserving in a previous year who did not stand for

reelection and was included in the first-stage mod-els predicting director recruitment.8

Industry dummies. Industry dummies were in-cluded because systematic differences could existbetween companies in different industries for boththe independent and dependent variables. In keep-ing with prior research (Fischer & Pollock, 2004;Pollock, 2004) five industry dummy variables wereincluded in the analysis: business services, chemi-cal and allied products, instruments and relatedproducts, electronic and other electric products,and retail. These categories parsimoniously capturethe variety of industries represented in the IPOmarket in 2001–04. Firms were assigned to thesecategories on the basis of their SIC classifications.

Year of issue and years since IPO. Dummy vari-ables for the year of issue were coded 1 if compa-nies went public in 2002, 2003, or 2004 (2001 wasthe omitted year). We also created dummy vari-ables for each of the years since IPO, coded 1 ifcompanies were in their second, third, fourth, orfifth years following their IPO year (year one wasthe omitted year). We controlled for these variablesbecause a variety of factors associated with when acompany went public and how far beyond its IPO ithas moved may affect the likelihood it will recruita prestigious director.

Method of Analysis

Our hypotheses compare the recruiting of a pres-tigious director to the recruiting of a nonprestigiousdirector. Thus, they are predicated on a recruitingevent occurring. However, every firm did not re-cruit new directors every year. Approximately55 percent of firms recruited new directors in agiven year, with the annual percentages rangingfrom 50.3 percent in year four to 61.5 percent inyear two. To compare the effects of director andCEO prestige and CEO power on the recruitment ofprestigious versus nonprestigious directors, we rantwo-stage models that predicted whether or not afirm was likely to recruit a new director in the firststage and then predicted director prestige in thesecond stage. For the analyses using the dichoto-mous dependent variable, we employed the “heck-prob” command in STATA 11.0, which generates aHeckman correction for probit models in which the

7 Because group size can influence group functioningin a nonlinear fashion (Yetton & Bottger, 1983), in anal-yses not reported here we also included board sizesquared. The squared term was not significant, and ourresults remained unchanged. We also considered salesgrowth and net income as two additional firm-level in-dicators of quality. Neither variable had significant ef-fects, and our other results remained unchanged whenthey were included in the models.

8 In analyses not reported here, we also consideredprestigious departures. The results of our hypothesistests were unchanged.

2013 1405Acharya and Pollock

outcomes in both stages are dichotomous variables.For the analysis using the count measure, we onlyused the observations in which a recruiting eventoccurred and employed negative binomial regres-sions using the “nbreg” command with robust stan-dard errors. STATA does not provide a two-stageselection model for negative binomial regressions;therefore we calculated the inverse of the Millsratio using the code provided by Hamilton andNickerson (2003) in a separate probit regressionand included it as a control in the count models. Inboth analyses, we used the number of directorsleaving a board, board size, VC backing, CEO pres-

tige, the industry dummies, and the post-IPO yeardummies to predict the likelihood of recruiting anoutside director in the first-stage models. The num-ber of departures was excluded from the second-stage models (Bascle, 2008; Hamilton & Nicker-son, 2003).

RESULTS

Table 1 provides the descriptive statistics and acorrelation matrix for all the key variables in thestudy. To save space and make the tables morereadable we do not include the year of IPO, year

TABLE 1Descriptive Statistics and Correlations for Firm-Level Variables

Variable Mean s.d. 1 2 3 4 5 6 7 8 9 10 11 12

1. Prestigious hire 0.34 0.472. Count prestigious hires 0.45 0.69 .90*3. Firm agea 2.69 0.77 .02 �.054. Firm sizea 5.23 1.90 �.03 �.05 .41*5. Offer sizea 18.34 0.82 .01 .02 .29* .45*6. Underpricing 0.13 0.18 .00 .00 �.01 .15* .16*7. Total stockholder

return2.35 0.16 .06 .05 .07* .14* .24* .01

8. Multiple hires 0.23 0.42 .55* .52* .05 .06* .06* �.01 .11*9. Total departures 0.66 0.91 .21* .22* .03 .02 .05 �.02 .06 .31*

10. Board size 7.82 1.75 .22* .21* .09* .21* .23* .04 .05 .31* .0611. CEO tenure 6.20 5.37 �.05 �.09* .11* .07* �.06* �.11* .00 �.03 �.14* �.12*12. VC backing 0.51 0.50 .03 .02 �.14* �.22* �.22* .09* �.04 �.02 .00 �.05 .0013. VC prestige 0.21 0.41 .00 �.01 �.16* �.15* �.16* .06* �.04 �.04 .03 �.06* .04 .51*14. Underwriter prestige 0.68 0.47 .05 .07 .04 .25* .41* .13* .10* .06 .07 .11* �.08* �.0515. CEO duality 0.44 0.50 �.06 �.03 .00 .07* .04 .01 .08* �.02 �.06 �.05 .26* �.20*16. Founder CEO 0.43 0.49 �.07* �.03 �.30* �.16* �.12* �.13* �.06 �.06 �.12* �.15* .39* �.0517. CEO ownership 0.07 0.10 �.12* �.07 �.11* �.11* �.09* �.06* �.04 �.04 �.09* �.15* .29* �.0118. Staggered board 0.69 0.46 �.03 �.05 .12* .11* .06 .05 .00 .02 .02 .06 �.03 .11*19. Outside director ratio 0.79 0.09 .06 .00 .17* .12* .14* .01 .01 .09* .02 .23* �.02 .0320. Average board tenure 4.70 2.21 �.05 �.16* .23* .04 �.15* .01 �.13* �.12* �.12* �.10* .39* .17*21. Board prestige 3.10 2.19 .33* .36* �.17* �.12* .01 .08* �.01 .16* .03 .33* �.07* .16*22. Board prestige squared 14.42 16.57 .29* .33* �.16* �.08* .04 .11* �.02 .16* .01 .36* �.05 .12*23. CEO prestige 0.35 0.48 .07* .08* �.11* �.10* .02 .07* �.01 .00 �.01 .01 �.02 .04

13 14 15 16 17 18 19 20 21 22

13. VC prestige14. Underwriter prestige .0115. CEO duality �.17* �.0316. Founder CEO �.08* �.09* .43*17. CEO ownership �.02 �.25* .34* .50*18. Staggered board �.01 .09* .00 �.10* �.06*19. Outside director ratio .03 .12* �.16* �.24* �.34* .0520. Average board tenure .07* .00 �.03 .05 �.09* �.03 .0121. Board prestige .05 .10* �.04 �.09* �.10* �.05 .09* �.0522. Board prestige squared .06 .12* �.04 �.08* �.06 �.04 .07* �.04 .93*23. CEO prestige �.01 �.06* .09* .00 �.03 �.03 .01 �.05 .43* .38*

a Logarithm.* p � .05

1406 OctoberAcademy of Management Journal

post-IPO and industry dummies in any of the ta-bles, although they were included in all the regres-sion models. For ease of interpretation, means andstandard deviations were calculated using rawdata, and log-transformed values were used for allthe analyses.

To save space, we do not present the first-stagemodels predicting the likelihood of recruiting anew director. In all the selection models, boardsize, number of departures, the dummy variablesfor the electronic and other electrical products in-dustry, and the first two years post-IPO had posi-tive, significant effects on the likelihood of outsidedirector recruitment. CEO prestige had a negative,significant relationship with the likelihood of di-rector recruitment.

Table 2 presents the results of the second-stagemodels testing the hypotheses using the dichoto-mous outcome, and Table 3 presents the resultsusing the count measure. In each table, model 1represents the baseline model and includes onlythe control variables. Model 2 adds the main effectsof preexisting board prestige and CEO prestige topredict the likelihood of recruiting prestigious di-rectors, as stated in Hypotheses 1 and 2. Models3–8 add each of the interactions used to test Hy-potheses 3 and 4, and model 9 presents the fullysaturated model.

Hypothesis 1 predicts that preexisting boardprestige will be positively associated with the like-lihood of recruiting prestigious directors, but at adiminishing rate. Boards had three prestigious di-rectors on average, and the number of prestigiousdirectors ranged from 0 to 11. The average boardsize was approximately 8, so slightly over a third ofthe directors, on average, were prestigious. The co-efficient for preexisting board prestige was positiveand significant in all models, and the squared termwas negative and significant in all models in bothTables 2 and 3, a finding that is consistent with apositive but diminishing curvilinear relationship.

To test the curvilinearity of this relationship, weemployed the method developed by Lind andMehlum (2009) using the “utest_rev” command inSTATA 11.0. This test calculates the inflectionpoint and determines whether each part of thecurve before and after the inflection point, as wellas the overall relationship, is significantly differentfrom either a monotone or U-shaped relationship.The analysis of the coefficients in model 2 of Ta-ble 2 confirmed a positive but diminishing relation-ship. The inflection point was 10, which is withinthe bounds of our data, and while the lower portion

of the curve was significantly different from amonotone relationship, the portion above the in-flection point was not. However, when the resultsfrom model 2 of Table 3 are used, the relationshipis fully curvilinear. The inflection point is 8, andthe tests for both the upper and lower portions ofthe curve, as well as the overall test for curvilinear-ity, are significant at p � .002 or better. Thus,Hypothesis 1 is supported, and our results furthersuggest that when considering how prestigious anew director is likely to be, the relationship actu-ally becomes negative at high levels of boardprestige.

Hypothesis 2 predicts that CEO prestige will bepositively related with the recruitment of presti-gious directors. This hypothesis is not supported inour main effects models; CEO prestige has a nega-tive, nonsignificant relationship with recruiting aprestigious director in Table 2 and with the amountof director prestige in Table 3. This finding heldeven when CEO prestige was excluded from thefirst-stage model. However, the main effect be-comes significant in some models including inter-actions. We consider the implications of these find-ings when we discuss the tests of Hypothesis 4.

Hypothesis 3 argues that the amount of time out-side directors have served together on a board willincrease the positive relationship between directorprestige and the likelihood of recruiting a presti-gious director. We tested this hypothesis with in-teractions between average board tenure and thelinear and squared board prestige measures. Theresults in model 3 of both Tables 2 and 3 show thataverage board tenure has a negative and significantinteraction with the linear term and a positive,significant interaction with the squared term. Fur-ther, the main effect of average board tenure be-comes positive and significant. To fully considerthe nature of this relationship, we graphed the re-sults from model 3 of Table 2 using average boardtenure and board prestige one standard deviationbelow and above their means. Figure 1 illustratesthis interaction and shows that although the rela-tionship remains curvilinear in both instances,firms are more likely to recruit a prestigious direc-tor when average board tenure is high. Further, theinflection point at which the marginal effect ofadding a prestigious director becomes negative andis shifted left, to approximately seven prestigiousdirectors. Curvilinearity tests confirm that this re-lationship is also now fully curvilinear. The resultsbased on the findings in Table 3 are the same, and

2013 1407Acharya and Pollock

TABLE 2Results of Second-Stage Heckman Models Predicting Recruitment of Prestigious Directorsa

Variables Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9

Firm ageb 0.13 0.25* 0.25* 0.25* 0.25* 0.25* 0.25* 0.24* 0.24*(0.10) (0.11) (0.12) (0.11) (0.11) (0.11) (0.11) (0.11) (0.11)

Salesb �0.14** �0.13** �0.14** �0.13* �0.13** �0.11* �0.12* �0.12* �0.11*(0.05) (0.05) (0.05) (0.05) (0.05) (0.05) (0.05) (0.05) (0.05)

Offer sizeb 0.02 0.05 0.07 0.05 0.05 0.08 0.05 0.06 0.12(0.09) (0.11) (0.10) (0.11) (0.11) (0.10) (0.10) (0.10) (0.10)

Underpricing 0.06 �0.27 �0.39 �0.27 �0.27 �0.42 �0.32 �0.27 �0.53(0.40) (0.46) (0.44) (0.47) (0.46) (0.44) (0.46) (0.45) (0.42)

Total stockholder returnsc �0.15 �0.29 �0.29 �0.29 �0.29 �0.27 �0.29 �0.28 �0.26(0.31) (0.36) (0.36) (0.36) (0.36) (0.33) (0.35) (0.36) (0.33)

Multiple hires 0.92*** 1.08*** 1.10*** 1.08*** 1.08*** 1.12*** 1.09*** 1.09*** 1.14***(0.16) (0.15) (0.15) (0.15) (0.15) (0.15) (0.15) (0.15) (0.15)

Board size 0.08† �0.08 �0.06 �0.08 �0.08 �0.07 �0.07 �0.08† �0.06(0.05) (0.05) (0.05) (0.05) (0.05) (0.05) (0.05) (0.05) (0.05)

CEO tenure 0.01 0.01 0.00 0.01 0.01 0.01 0.01 0.01 0.00(0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01)

VC backing 0.33† 0.04 0.09 0.04 0.05 0.06 0.07 0.05 0.11(0.18) (0.19) (0.18) (0.19) (0.18) (0.18) (0.19) (0.19) (0.18)

VC prestige �0.18 �0.11 �0.12 �0.11 �0.11 �0.11 �0.12 �0.13 �0.13(0.18) (0.20) (0.19) (0.20) (0.20) (0.20) (0.20) (0.20) (0.19)

Underwriter prestige 0.03 �0.25 �0.29† �0.25 �0.25 �0.24 �0.25 �0.28† �0.30†

(0.15) (0.17) (0.16) (0.17) (0.17) (0.17) (0.17) (0.17) (0.16)CEO duality 0.09 �0.02 0.03 �0.02 �0.04 �0.04 �0.04 �0.02 �0.01

(0.14) (0.16) (0.16) (0.16) (0.17) (0.16) (0.16) (0.16) (0.17)Founder CEO �0.06 0.03 0.03 0.02 0.02 �0.01 �0.04 0.03 �0.01

(0.16) (0.19) (0.19) (0.19) (0.19) (0.19) (0.21) (0.19) (0.20)CEO ownership �2.25** �1.68* �1.56* �1.69* �1.66* �1.38† �1.68* �1.66* �0.89

(0.88) (0.76) (0.77) (0.80) (0.77) (0.76) (0.76) (0.75) (0.85)Staggered board �0.15 �0.05 �0.10 �0.05 �0.05 �0.08 �0.05 0.03 �0.05

(0.14) (0.15) (0.15) (0.15) (0.15) (0.15) (0.15) (0.17) (0.16)Outside director ratio �1.21† �1.38† �1.50† �1.38† �1.37† �0.10 �1.38† �1.43† �0.20

(0.70) (0.81) (0.80) (0.81) (0.81) (0.97) (0.82) (0.81) (0.98)Average board tenure �0.03 0.02 0.19** 0.02 0.02 0.02 0.02 0.03 0.18**

(0.03) (0.04) (0.07) (0.04) (0.04) (0.04) (0.04) (0.04) (0.07)Board prestige 0.52*** 0.87*** 0.52*** 0.52*** 0.51*** 0.52*** 0.53*** 0.85***

(0.08) (0.16) (0.08) (0.08) (0.08) (0.08) (0.08) (0.16)Board prestige squared �0.03*** �0.05*** �0.03** �0.03*** �0.03*** �0.03*** �0.03*** �0.05**

(0.01) (0.02) (0.01) (0.01) (0.01) (0.01) (0.01) (0.02)CEO prestige �0.18 �0.21 �0.18 �0.20 3.55* �0.25 �0.05 3.85**

(0.15) (0.14) (0.17) (0.20) (1.41) (0.18) (0.28) (1.37)Board prestige � average board

tenure�0.08* �0.08*(0.03) 0.03

Board prestige squared �average board tenure

0.01† 0.01†

(0.00) (0.00)CEO prestige � CEO ownership 0.04 �2.18

(1.85) (1.90)CEO prestige � CEO duality 0.07 0.03

(0.25) (0.29)CEO prestige � outside director

ratio�4.53** �4.75**(1.69) (1.63)

CEO prestige � founder CEO 0.27 0.20(0.29) (0.38)

CEO prestige � staggered board �0.22 �0.22(0.33) (0.32)

Continued

1408 OctoberAcademy of Management Journal

the inflection point drops to six. Hypothesis 3 istherefore supported.

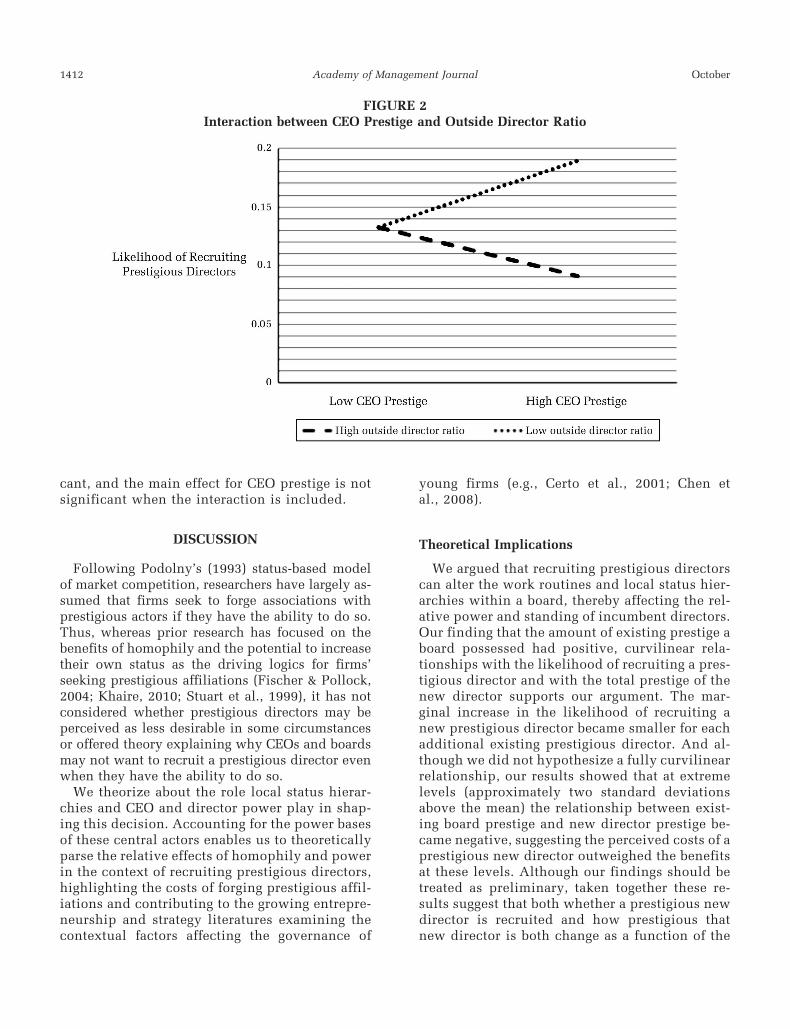

Hypothesis 4 argues that the structural andownership power of a CEO will enhance the ef-fect of CEO prestige on the likelihood that a firmrecruits a prestigious director. The results in Ta-ble 2 provide partial support for Hypothesis 4.When the CEO prestige by outside director ratiointeraction is included in the model, the maineffect of CEO prestige is positive and significant(p � .03), and the interaction is negative andsignificant (p � .02). None of the other interac-tions were significant. Figure 2 graphs this inter-action for values one standard deviation aboveand below the mean for the outside director ratio.When the outside director ratio is low, CEO pres-tige has a positive relationship with recruiting aprestigious director; however, when the outsidedirector ratio is high, the relationship betweenCEO prestige and recruiting a prestigious directoris negative. This finding is consistent with ourargument that a prestigious CEO will weight thebenefits of a prestigious new outside directormore heavily than the costs when she /he feelsmore secure about being able to maintain her/hisdiscretion but will weight the costs more heavilythan the benefits when discretion may be atgreater risk.

The results in Table 3 reveal a different patternof results, although they still provide some sup-port for the positive moderating effect suggestedin Hypothesis 4. CEO prestige remained negativeand became significant (p � .05) when the inter-actions with CEO duality and founder CEO wereincluded in the models. Both interactions werepositive, and the interaction with founder statuswas significant (p � .05), but the interaction withCEO duality was not significant (p � .11). Since

both the CEO prestige and founder CEO measuresare dummy variables, we assessed the interac-tion’s effect by comparing the coefficients. Inkeeping with Hypothesis 4, when a prestigiousCEO is not a firm’s founder, new director prestigeis reduced; however, when the prestigious CEO isalso the founder, the new director is likely to bemore prestigious.

The main effects for some of the structural andownership power measures were also significant inTable 3. The outside director ratio had a negative,significant relationship (p � .001) and founder CEOstatus had a positive, significant relationship (p �.002) with the amount of new director prestige.These findings are consistent with our argumentsthat more powerful CEOs are less threatened by amore prestigious new director.

Thus far we have treated preexisting board pres-tige and CEO prestige categorically: either you areprestigious by virtue of possessing at least one typeof prestigious affiliation, or you are not. This ap-proach is consistent with prior research (e.g., Chenet al., 2008; Higgins & Gulati, 2006; Pollock et al.,2010) and our research question. However, likenewly recruited directors, CEOs and existing direc-tors may have more than one type of prestigiousaffiliation. To explore whether the cumulativeamount of prestige held by a board and a CEO wasconsequential, we calculated cumulative prestigeon the basis of all of the prestigious affiliations of aCEO and a board and reran our models. The resultsof this analysis were the same as reported here forboth dependent variables.

Another assumption we made in our analysiswas that all three types of prestige were equiva-lent. However, it is possible that different pres-tige values are associated with each type of pres-tigious affiliation. We explored this issue by

TABLE 2(Continued)

Variables Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9

Constant 0.28 0.13 �0.89 0.13 0.17 �1.63 0.14 �0.22 �3.01(1.75) (1.94) (1.92) (1.94) (1.94) (2.01) (1.93) (1.90) (1.94)

Log pseudo-likelihood �746.54 �700.79 �697.55 �700.79 �700.76 �697.07 �700.41 �700.46 �693.29

a n � 826.b Logarithm.c Lagged variable.

† p � .10* p � .05

** p � .01*** p � .001

2013 1409Acharya and Pollock

TABLE 3Results of Negative Binomial Regression Models Using the Count Measure of Prestigea

Variables Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9

Firm ageb �0.03 0.15* 0.15* 0.15* 0.16* 0.16* 0.15* 0.16* 0.17*(0.07) (0.07) (0.07) (0.07) (0.07) (0.07) (0.07) (0.07) (0.07)

Salesb �0.02 0.00 0.00 0.00 0.00 0.00 0.02 0.00 0.00(0.03) (0.03) (0.03) (0.03) (0.03) (0.03) (0.03) (0.03) (0.03)

Offer sizeb 0.00 �0.01 0.01 �0.01 �0.02 0.00 �0.02 �0.01 �0.01(0.06) (0.06) (0.06) (0.06) (0.06) (0.06) (0.06) (0.06) (0.06)

Underpricing 0.18 �0.12 �0.18 �0.13 �0.15 �0.13 �0.15 �0.12 �0.23(0.25) (0.23) (0.23) (0.23) (0.23) (0.23) (0.23) (0.23) (0.23)

Total stockholder returnsc �0.20 �0.13 �0.15 �0.14 �0.14 �0.11 �0.13 �0.14 �0.13(0.18) (0.18) (0.18) (0.18) (0.18) (0.19) (0.19) (0.18) (0.19)

Multiple hires 0.99*** 0.61*** 0.61*** 0.62*** 0.62*** 0.62*** 0.61*** 0.61*** 0.62***(0.09) (0.09) (0.08) (0.09) (0.09) (0.09) (0.09) (0.09) (0.09)

Board size 0.06† �0.08** �0.07* �0.07** �0.07* �0.07* �0.07* �0.08** �0.06*(0.03) (0.03) (0.03) (0.03) (0.03) (0.03) (0.03) (0.03) (0.03)

CEO tenure 0.01 0.00 0.00 0.00 0.00 0.00 0.00 0.00 �0.01(0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01) (0.01)

VC backing 0.27** 0.18† 0.20* 0.18† 0.18† 0.18† 0.18† 0.18† 0.19†

(0.11) (0.10) (0.10) (0.10) (0.10) (0.10) (0.10) (0.10) (0.10)VC prestige �0.18 �0.03 �0.03 �0.03 �0.01 �0.04 �0.04 �0.02 �0.03

(0.12) (0.11) (0.11) (0.11) (0.11) (0.11) (0.11) (0.11) (0.11)Underwriter prestige 0.07 �0.12 �0.12 �0.11 �0.11 �0.12 �0.10 �0.11 �0.10

(0.09) (0.10) (0.10) (0.10) (0.10) (0.10) (0.10) (0.10) (0.10)CEO duality 0.04 �0.03 �0.01 �0.03 �0.12 �0.03 �0.07 �0.02 �0.08

(0.11) (0.10) (0.10) (0.10) (0.12) (0.10) (0.10) (0.10) (0.12)Founder CEO 0.13 0.25* 0.26* 0.25* 0.25* 0.26* 0.14* 0.26* 0.18

(0.12) (0.12) (0.12) (0.12) (0.12) (0.12) (0.13) (0.12) (0.14)CEO ownership �1.75* �0.89 �0.75 �1.06 �0.88 �0.80 �0.87 �0.91 �0.39

(0.82) (0.56) (0.56) (0.73) (0.56) (0.56) (0.57) (0.56) (0.73)Staggered board �0.19* �0.06 �0.07 �0.06 �0.05 �0.07 �0.04 �0.10 �0.12

(0.09) (0.08) (0.08) (0.08) (0.08) (0.08) (0.08) (0.12) (0.11)Outside director ratio �1.10* �1.43*** �1.43*** �1.46*** �1.45*** �0.98† �1.48*** �1.41*** �0.98†

(0.44) (0.37) (0.37) (0.39) (0.37) (0.56) (0.37) (0.38) (0.56)Average board tenure �0.03 �0.01 0.13 �0.01 �0.01 �0.01 �0.01 �0.01 0.13

(0.02) (0.03) (0.06) (0.03) (0.03) (0.03) (0.02) (0.03) (0.06)Inverse Mill’s ratio �0.40* 0.05 0.04 0.05 0.08 0.03 0.08 0.06 0.05

(0.19) (0.19) (0.19) (0.19) (0.19) (0.19) (0.19) (0.19) (0.20)Board prestige (H1) 0.53*** 0.87*** 0.52*** 0.52*** 0.53*** 0.52*** 0.53*** 0.86***

(0.06) (0.15) (0.07) (0.06) (0.06) (0.06) (0.06) (0.15)Board prestige squared

(H1)�0.04*** �0.07*** �0.04*** �0.03*** �0.04*** �0.03*** �0.04*** �0.07***(0.01) (0.02) (0.01) (0.01) (0.01) (0.01) (0.01) (0.02)

CEO prestige (H2) �0.09 �0.09 �0.12 �0.19* 0.68 �0.21* �0.14 0.45(0.08) (0.08) (0.09) (0.10) (0.62) (0.10) (0.13) (0.65)

Board prestige � averageboard tenure (H3)

�0.08* �0.08*(0.03) (0.03)

Board prestige squared �average board tenure(H3)

0.01* 0.01*(0.00) (0.00)

CEO prestige � CEOownership (H4)

0.56 �0.89(0.98) (1.10)

CEO prestige � CEOduality (H4)

0.26 0.11(0.16) (0.18)

CEO prestige � outsidedirector ratio (H4)

�0.97 �0.92(0.77) (0.77)

Continued

1410 OctoberAcademy of Management Journal

creating a weighted average value of prestige foreach director (both existing and newly recruited)and CEO. Given that rarity is often associatedwith value, we used the relative frequency ofeach type of prestige to create weighting factors,operationalized as one minus the frequency ofoccurrence in our sample. Approximately 64 per-cent of the directors and executives had educa-tion prestige; 24 percent possessed employmentprestige; and 12 percent possessed directorshipprestige. Thus, education prestige received thelowest weighting, and directorship prestige re-

ceived the highest weighting. The weights werethen multiplied by the sources of prestige foreach individual and divided by the total sum ofthe weights to get the weighted average. We usedthe “heckman” command in STATA to conductthis analysis since the dependent variable is nowa continuous measure. The results for board pres-tige continue to remain robust and are the sameas presented here. As in the event count models,CEO prestige has a negative main effect, but it isnow consistently significant (p � .05). However,the interaction with outsider ratio is not signifi-

TABLE 3(Continued)

Variables Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9

CEO prestige � founderCEO (H4)

0.35* 0.31(0.17) (0.20)

CEO prestige � staggeredboard (H4)

0.08 0.14(0.17) (0.17)

Constant 0.24 0.20 �0.64 0.26 0.39 �0.42 0.45 0.32 �0.81(1.06) (1.18) (1.21) (1.17) (1.17) (1.32) (1.16) (1.20) (1.35)

Log pseudo-likelihood �513.95 �441.94 �440.60 �441.87 �441.35 �441.59 �440.96 �441.89 �439.17

a n � 451.b Logarithm.c Lagged variable.

† p � .10* p � .05

** p � .01*** p � .001

FIGURE 1Interaction between Board Prestige and Average Board Tenure

2013 1411Acharya and Pollock

cant, and the main effect for CEO prestige is notsignificant when the interaction is included.

DISCUSSION

Following Podolny’s (1993) status-based modelof market competition, researchers have largely as-sumed that firms seek to forge associations withprestigious actors if they have the ability to do so.Thus, whereas prior research has focused on thebenefits of homophily and the potential to increasetheir own status as the driving logics for firms’seeking prestigious affiliations (Fischer & Pollock,2004; Khaire, 2010; Stuart et al., 1999), it has notconsidered whether prestigious directors may beperceived as less desirable in some circumstancesor offered theory explaining why CEOs and boardsmay not want to recruit a prestigious director evenwhen they have the ability to do so.

We theorize about the role local status hierar-chies and CEO and director power play in shap-ing this decision. Accounting for the power basesof these central actors enables us to theoreticallyparse the relative effects of homophily and powerin the context of recruiting prestigious directors,highlighting the costs of forging prestigious affil-iations and contributing to the growing entrepre-neurship and strategy literatures examining thecontextual factors affecting the governance of

young firms (e.g., Certo et al., 2001; Chen etal., 2008).

Theoretical Implications

We argued that recruiting prestigious directorscan alter the work routines and local status hier-archies within a board, thereby affecting the rel-ative power and standing of incumbent directors.Our finding that the amount of existing prestige aboard possessed had positive, curvilinear rela-tionships with the likelihood of recruiting a pres-tigious director and with the total prestige of thenew director supports our argument. The mar-ginal increase in the likelihood of recruiting anew prestigious director became smaller for eachadditional existing prestigious director. And al-though we did not hypothesize a fully curvilinearrelationship, our results showed that at extremelevels (approximately two standard deviationsabove the mean) the relationship between exist-ing board prestige and new director prestige be-came negative, suggesting the perceived costs of aprestigious new director outweighed the benefitsat these levels. Although our findings should betreated as preliminary, taken together these re-sults suggest that both whether a prestigious newdirector is recruited and how prestigious thatnew director is both change as a function of the

FIGURE 2Interaction between CEO Prestige and Outside Director Ratio

1412 OctoberAcademy of Management Journal

amount of existing board prestige. Further, thesechanges occur at somewhat different rates, withthe amount of prestige decreasing a little morerapidly. Future research should continue to ex-plore these dynamics.

We also found that the amount of time directorshad worked together influenced these relation-ships. Our results suggest that high average boardtenure increases the likelihood a prestigious direc-tor will be recruited, as well as the total prestige ofthe director recruited. When a board has loweraverage tenure, the local status order may still be influx, and adding a new prestigious director at thisjuncture may be perceived as more threatening be-cause individual directors’ positions in the statusorder may be more precarious and political con-tests more prevalent. Conversely, serving togetherfor longer periods of time could create clarity andstability in the local status order that decrease theperceived threat of adding a prestigious new direc-tor. These findings suggest local status order con-cerns can create boundary conditions on how ho-mophily influences director recruitment decisions,affecting a board’s signaling value (Pollock et al.,2010) and the board capital available (Hillman &Dalziel, 2003).

When a new director was recruited, CEO prestigehad a negative relationship with the likelihood thedirector was prestigious when CEO structuralpower was low. However, when a firm recruited anew director and its CEO possessed more structuralpower—reflected in a low outside director ratio—the relationship between CEO prestige and the like-lihood of recruiting a prestigious new director be-came positive. Although speculative, this findingsuggests that when new directors are recruited andCEOs feel secure in their structural power relativeto their boards, prestigious CEOs focus more on thebenefits of gaining additional prestigious affilia-tions than on the potential loss of discretion, butwhen they are less secure in their structural power,they focus more on the threats associated with pres-tigious new directors.

The results of our analyses predicting theamount of prestige a new director possessed whena new director was recruited yielded a more nu-anced pattern of results. CEO prestige generally hada negative, nonsignificant relationship that becamesignificant when a CEO was also board chairman orcompany founder, although only the latter interac-tion effect was significant. These findings are con-sistent with our previous findings, as well as thegeneral argument that a prestigious CEO is likely to

be less threatened and to focus on the benefitsrather than the costs of a prestigious new directorwhen the CEO has other sources of power.

Our analyses also showed that founder CEOs andCEOs with fewer outsiders on their boards werelikely to recruit more prestigious directors, whileCEOs who own larger percentages of stock werelikely to recruit less prestigious directors. Althoughthey should be treated as preliminary, these find-ings, combined with the positive moderating ef-fects previously discussed, may have significantimplications for governance research and practice.Agency theory (Fama, 1980; Fama & Jensen, 1983)and current governance “best practices,” as re-flected, for example, in the Sarbanes-Oxley Act,prescribe very high levels of outside director rep-resentation on boards as a corrective for executiveself-interest. Further, the received wisdom amongventure capitalists is that it is more often than notbest to replace founder CEOs with “more experi-enced” leadership (Pollock et al., 2009; Wasserman,2003). Our findings suggest that these prescriptionsmay have the unintended consequence of reducingthe likelihood a company recruits the types of direc-tors who may be more active and who bring greaterhuman and social capital to a board (e.g., D’Aveni &Kesner, 1993; Hillman & Dalziel, 2003). Thus, likerecent research on multiple agency (e.g., Arthurs,Hoskisson, Busenitz, & Johnson, 2008; Kroll et al.,2007) and the benefits of founder CEO presence(e.g., Fischer & Pollock, 2004; Nelson, 2003), ourresults suggest that rather than treating these deci-sions in a “one size fits all” manner, future theoriz-ing in corporate governance on the roles of boardstructure and founder CEOs should more fully con-sider both the benefits and costs of the actionstaken and recognize that which predominates maybe contingent on contextual characteristics.

Our findings (1) that CEO prestige can sometimeshave a negative relationship with recruiting a newdirector and the amount of prestige a new directorpossesses and (2) that greater CEO stock ownershipcan also lead to recruiting less prestigious directorshighlight that having a powerful CEO can be adouble-edged sword. Further, it suggests that as-suming different dimensions of CEO power areequivalent in their consequences for firms may beinappropriate. Future research should continue toexplore the ways in which different sources of CEOpower vary and how they may combine in differentways to influence organizational outcomes.

More generally, another contribution of thisstudy is to the literature on the microprocesses

2013 1413Acharya and Pollock

underlying corporate board functioning. Whileboards are comprised of members of the corporateelite (Davis et al., 2003), they are also groups, andthey experience typical group processes such asconflict, teamwork, cohesiveness, and consensus(Finkelstein & Mooney, 2003; Forbes & Milliken,1999). A considerable amount of research has ex-amined the demographic characteristics (e.g., Dal-ton et al., 1998; Dalton, Daily, Johnson, & Ellstrand,1999), social and friendship ties (e.g., Westphal &Zajac, 1995; Zajac & Westphal, 1996), and interlockpatterns (e.g., Davis et al., 2003) of corporateboards, but it has not explicitly considered thenature of directors’ status hierarchies—either theirstanding in the broader director labor market ortheir standing in a board’s local status hierarchy.We begin to consider how local status hierarchiesoperate, as directors seek to balance the need toaffiliate with similar others with the need to pre-serve their standing and power within boards. Byexplicating the nuances of directors’ local statushierarchies, we offer theoretical insights into a veryimportant social characteristic pervasive among theupper echelons of corporate hierarchies.

Future Research Directions