Embed Size (px)

Citation preview

Total Cost of Ownershipandand

Price Analysis

1Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Total Cost of Ownership (TCO)Total Cost of Ownership (TCO)

• Is it a correct decision to overemphasize theIs it a correct decision to overemphasize the acquisition cost or purchase price?

• Can it impact other ownership and post• Can it impact other ownership and post ownership costs?TCO• TCO– Acquisition cost– Ownership cost– Post ownership cost

2Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How TCO can be viewed in S i ?Services?

• Apart from other capital intensive costs, theApart from other capital intensive costs, the cost of maintaining the employee base is also an important costp

• Wages as per experience?• RetailRetail

– Can manage inventory related cost by JIT, quality, cost, time

– Equally important is the after sales adjustment, warranty claims, maintaining customer satisfaction f i d fi it i dfor indefinite period

3Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Acquisition costInitial costs short term immediate cash outflowInitial costs, short term, immediate cash outflow

• Price paid for material, freight delivery, capital purchases, installation, testing

Purchase price

• Negotiations, discounts, standardizing specifications, substitute used products

• Developing requirements and specifications, price & cost analysis, supplier

Planning costs

p g q p , p y , ppselection, initial order processing

• E-Procurement

Quality costs

• Prevention costs, Appraisal costs, Failure costs• Selection, certification and monitoring suppliers

Taxes• Customs duties and tariffs, Virtual warehouse, tolls, facility fees• Focus on compliance to avoid penalties, free trade zones

4Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Ownership costs (Quantitative and Qualitative)(Quantitative and Qualitative)

Ongoing use of purchased product• Downtime costs

Troublesome product– Troublesome product– Reduced production volumes, idle resources, lost sales, late deliveries

• Risk costs– Excess inventory Vs stock out, reduced cash flow, lost interest on cash flow,

obsolescence, theft, additional floor space• Cycle time cost

– Strategic alliances with key suppliers,• Conversion costs• Conversion costs

– Wrong material (quality, form or design), material not optimized for production process, machine time, labor requirements, scrap and rework

– Production methods, employee training and working environment, methods of accounting for product costs (overhead costs)accounting for product costs (overhead costs)

• Non value added costs– Poor layout, poor scheduling, maintaining cumbersome operating procedures that

duplicate efoorts, routing taking more time• Others

– Repair and maintenance, Warranty, Training, Contract administration5Arshinder Kaur, Assistant Professor, DoMS,

IIT Madras

Post ownership costsPost ownership costs

• DisposalDisposal• Long term environmental impact

i i d d d li bili i• Unanticipated warranty and product liabilities• Any other risks of customer dissatisfaction

6Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Price AnalysisPrice Analysis

7Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

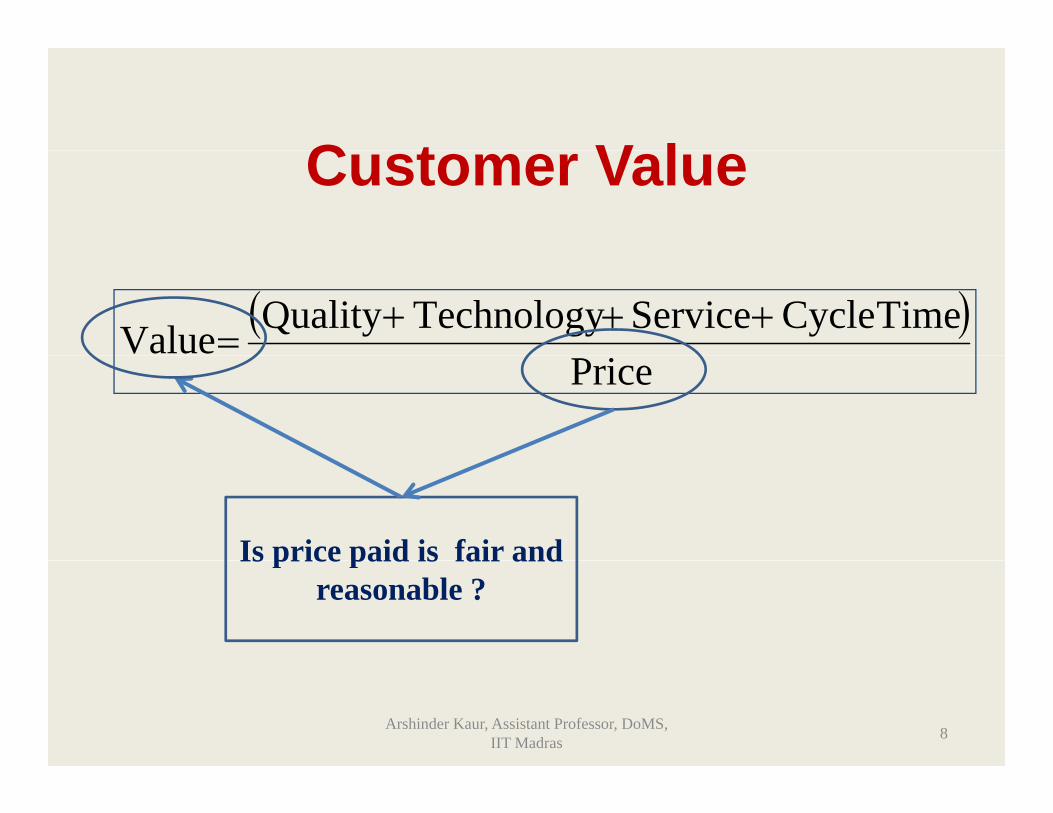

C t V lCustomer Value

( )TimeCycleServiceTechnologyQualityValue +++=

Price

Is price paid is fair andIs price paid is fair and reasonable ?

8Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How to determine fair or reasonable price?

• Evaluation of supplier’s actual cost VsEvaluation of supplier s actual cost Vs Actual purchase price paid

• Control of costs associated with producing f p gthe product Vs Analyzing final price

9Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

PricingPricing

• Is Cost Analysis is as important as PriceIs Cost Analysis is as important as Price Analysis?

• Total cost analysis– Applies the price/cost equation across multiple

processes that span two or more organizations l h iacross supply chain

10Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Cost Fundamentals

• Essential to effective purchasingp g• Recognition of major cost components• Evaluating the process and product capability• Evaluating the process and product capability

of suppliers

11Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Classification of costs• Fixed Costs (Property taxes, rent, depreciation)

– Remains constant or stable and do not vary with volumeRemains constant or stable and do not vary with volume– Change over time– Present even if there is no material output

• Variable Costs– Change proportionally with output

• Semi-variable– Have both fixed and variable cost component– What are the examples?

• Total costS f ll h– Sum of all three costs

12Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Classification of costs (b d i i i h )• Direct costs (material and labor)(based on association with process)

Direct costs (material and labor)– Directly traced and allocated to an item– Direct outcome of an operation or processDirect outcome of an operation or process– Useful for determining item specific cost– Even can be used for make-or-buy analysisy y

• Indirect Costs (burden costs)– Costs not assigned directly to a specific process or g y p p

production item– Energy required for machine, managerial and

administrative expenses13Arshinder Kaur, Assistant Professor, DoMS,

IIT Madras

Implications of cost from the ti f l h iperspectives of supply chain

• Cost reduction throughout the supply chain• Hurdles are “price-based” thinkingp g• Choose different initiatives for different stage of

product life cycleproduct life cycle

14Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Cost reductionCost reduction

• Team based value engineering effortsTeam based value engineering efforts• Supplier development

C i i• Cross-enterprise cost improvement• Joint brainstorming efforts• Supplier suggestion programs• Supply chain redesignSupply chain redesign

15Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Pricing• Price/ Acquisition Cost- Largest component of

total costtotal cost• Right price for one supplier is not necessary

th t th i ht i f th li tthat the right price for another supplier at same or at different points of time

• There are no standard methods available for determining right price

• It is good to understand the constantly changing variables, which influence pricing

16Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How to determine the right i ?price?

• Conditions of competitionV i bl i i i• Variable margin pricing

• Product differentiation• Regulation by competition

17Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How to determine the right i ?price?

• Conditions of competitionV i bl i i i• Variable margin pricing

• Product differentiation• Regulation by competition

18Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Conditions of competitionConditions of competition

Pure Competition MonopolyImperfect

CompetitionCompetition Competition

Monopolistic Oligopoly

Imperfect>>>>>><<<<<<<<<<<<<Competition

19Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Pure CompetitionPure Competition

• Determination of price based on forces of supplyDetermination of price based on forces of supply and demand only

• Producers are price takersp• No control over the price producers receive for

their products• Many buyers and sellers• Many products that are similar in nature hence

substitution can take place• Very few barriers to entry of new companies

20Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Imperfect Competition• Monopolistic

– Many sellers produce many productsM b diff i d d f l– May be differentiated products or not perfectly substitutable products

– Hospitality, Cereal, clothing• Oligopoly

– only a few seller firms, relatively few different products– select group of firms has control over the price– high barriers to entry– oligopolistic firms often produce nearly identical productsoligopolistic firms often produce nearly identical products– companies competing for market share, are interdependent

as a result of market forcesA bil d l– Automobile and steel

21Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Monopolyp y• Only one producer/seller for a product• Entry into such a market is restricted due to high y g

costs or other impediments, which may be economic, social or political

• Prod cers are price makers and seller controls the• Producers are price makers and seller controls the entire supply of a particular commodity

• ExamplesExamples– a government can create a monopoly over an industry

that it wants to control, such as electricityi S di A bi th t h l t l– in Saudi Arabia the government has sole control over the oil industry

– when a company has a copyright or patent that h f i h kprevents others from entering the market

22Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How to determine the right i ?price?

• Conditions of competitionV i bl i i i• Variable margin pricing

• Product differentiation• Regulation by competition

23Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Variable-Margin Pricing

• Firms mostly sell a line of product rather than just a y f p jsingle product

• It is not about getting same profit margin on each product rather to generate satisfactory return on whole line of products

• Permits maximum competition on individual products

• Profits from most efficiently produced “successfully priced” items may offset the losses due to lower margins of inefficiently produced itemsmargins of inefficiently produced items

24Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How supply manager should h dl V i bl i i i ?handle Variable margin situation?

• Identify which products are high margin and which are low margin

• Producers sometimes follow average profit margin over product lineg p

• Analyze full line products using pricing methodsmethods

• In depth analysis of entire product line

25Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How supply manager should handle V i bl i i i ?Variable margin situation? (Contd…..)

• Pricing methods for full line products andPricing methods for full line products and specialty suppliers: should be same?

• Should we focus our price analysis based onShould we focus our price analysis based on just one product at a time?

• In the long run: Price is roughly equal to theIn the long run: Price is roughly equal to the cost of the least efficient producer who is able to remain in business

• In short run : by competition, supply and demand

26Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Example: Variable margin pricingExample: Variable margin pricing

A printed circuit manufacturer incurs overhead forA printed circuit manufacturer incurs overhead for1,88,000 boards consisting of about 4,000 designs.The overhead generated by the production wasapplied by the company to the boards on an equalbasis; however, about 20 percent of the boards drove80 percent of the overhead As expected the 2080 percent of the overhead. As expected, the 20percent were the low volume boards produced insmall lots. Since the company based its prices on thep y pcost estimates, the high volume boards were highlyoverpriced.

27Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How to determine the right i ?price?

• Conditions of competitionV i bl i i i• Variable margin pricing

• Product differentiation• Regulation by competition

28Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Product Differentiation

Di i i h diff i d d i h• Distinguish differentiated products with undifferentiated ones

• Beware of trap- Some sellers successfully make similar products APPEARS different from those of competitors

• It is about determining the quality of products g q y pfrom the analysis of facts and NOT from unsupported claimspp

29Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

How to determine the right i ?price?

• Conditions of competitionV i bl i i i• Variable margin pricing

• Product differentiation• Regulation by competition

30Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Regulation by competition• Sellers quote different prices due to real costs

of production and or competitive position• We may think that it would be just the cost to

company and profit margin which sets the price

Total cost = Cost of material + Cost of labor + cost of overhead

Price = Total cost + Profit (12% of total cost)• But in reality it is the competition which drives

the price –Need for business and price quoted by competitors

31Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Regulation by competitionRegulation by competition• Pricing is one of the most importantPricing is one of the most important

management decisions a firm must make• Lowest Price can be (Cost of material + CostLowest Price can be (Cost of material Cost

of labor)• Highest price can be 12 % in excess of totalHighest price can be 12 % in excess of total

cost• To gain satisfactory volume of business aTo gain satisfactory volume of business a

seller may decide any price between lowest and highest priceg p

32Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Price analysisPrice analysis

• The examination of a seller’s price• The examination of a seller s priceproposal (bid)

• by comparison with reasonable pricebenchmarks,

• without examination and evaluationof the separate elements of the costof the separate elements of the costand profit making up the price.

33Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Tools to conduct price analysisTools to conduct price analysis

• Analysis of competitive price proposalsAnalysis of competitive price proposals• Comparison with regulated, catalog, or market

pricesprices• Use of web based e-procurement• Comparison with historical prices• Use of independent cost estimatesp

34Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Analysis of competitive price lproposals

• The rupee value should be large enough to justifyThe rupee value should be large enough to justify expense

• Clear specifications of item or servicep• Adequate number of suppliers must be there in

market• Technically qualified suppliers• Seller actively want contract• Sufficient time must be given to prepare for

pricing

35Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Analysis of competitive price lproposals

• At least two sources have responded • Proposal are responsive to the buyer’s p p y

requirements• Suppliers competing independently for theSuppliers competing independently for the

award

36Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Regulated, Catalog and Market pricesprices

• Prices set by Law or Regulation• Catalog price• Catalog price

– A price that is included in a catalog, a price list or some other form that is regularly maintained by supplier

– Inspections can be done by customers– Request for recent sales summary

• Market price• Market price– Result from interaction of many buyers and sellers– Willing to trade at a given market priceg g p– Generic product and not unique to the seller– Eggs, vegetables, fruits

D il k t i i bli h d i th– Daily market price is published in the newspaper, independent of the supplier

37Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Internet/ E-Commerce• Price, catalogs through internet• Buying exchanges

i f d ll ff i id i l– List of pre-approved sellers offering identical or similar products

– Prices, discounts from list prices are provided, p p• Reverse auctions

– Potential suppliers are able to see prices submitted by their competitors and revise their bids until the pretheir competitors and revise their bids until the pre-established closing time for the auction

• Tailored global searchesg– Expanded internet search capabilities– Scanning all relevant public and private websites

worldwideworldwide– Procurement-specific portals

38Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Historical pricesHistorical prices

• Comparing proposed bid with historical quotesComparing proposed bid with historical quotes or prices for the same or similar item

Changed conditions– Changed conditions– Is it one-time charges?

Effect of inflation or deflation on the price– Effect of inflation or deflation on the price

39Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Independent cost estimatesIndependent cost estimates

• When other techniques of price analysis cannotWhen other techniques of price analysis cannot be utilized

• Cost analysis can be done to get the fair and• Cost analysis can be done to get the fair and reasonable estimate

40Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Purchasing of Special DesignPurchasing of Special Design

• Who owns the design?Who owns the design?• Who has the right to apply for patent?

h h i l li h li• Who owns the special tooling the supplier must obtain to produce item?

Specify the answers to above questions in p y qpurchase contracts unequivocally to avoid any future uncertainties

41Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Pricing method for design work• Purchaser’s standpoint- Separate the supplier’s

charges into three categoriescharges into three categories– Price for design and development work– Price for special tooling and equipment– Price for manufacturing

• Other desirable or possible contract can bePurchase design work and tooling completely apart– Purchase design work and tooling completely apart from the manufactured components

• There can be a situation when supplier prefer to develop a proprietary product and enjoy monopoly

42Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Documenting Price AnalysisDocumenting Price Analysis• Price Analysis Report- Written Summary ofPrice Analysis Report Written Summary of

the analysis for a given procurement• Basis for the supply manager’s conclusion thatBasis for the supply manager s conclusion that

a price is fair and reasonable• What to be included in reportWhat to be included in report

– Abstract of bids received– Price negotiation memorandum in the findings of ce ego o e o du e d gs o

price analysis– Restate key issues and decisions

43Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

DiscountsDiscounts

• For perceptive supply professional –For perceptive supply professional Technique for reducing prices after all other techniques are failedtechniques are failed

• Trade discountsQ i di• Quantity discounts

• Seasonal discounts• Cash discounts

44Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Trade discounts• Reduction from list price given to various classes

of buyers and distributors to compensate them for performing certain marketing functions for theperforming certain marketing functions for the original seller of the product

• Sequence of individual discounts (25%, 10% and q (5%): Series discounts

• For example The retails price is Rs. 100F ll di d i 25% f R 100 R 75• Full discounted price – 25% of Rs. 100= Rs. 75

• 10% of (Rs. 100- 25) = Rs. 7.50• 5% of (Rs 100 25 10) Rs 3 38• 5% of (Rs. 100-25-10) = Rs. 3.38• The manufacturer’s selling price is = 100-25-7.5-

3.38 = Rs. 64.123.38 Rs. 64.12

45Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Cash discountsCash discounts

• Price reductions for the prompt payment ofPrice reductions for the prompt payment of bills

• Offering discounts as a percentage of the net• Offering discounts as a percentage of the net invoice price

46Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Why seller offers cash discountsWhy seller offers cash discounts

• Attendant costsAttendant costs– Cost of tied-up capital

Cost of operating a credit department– Cost of operating a credit department– Cost of some bad-dept lossesS i hi d b i b t d tSavings achieved by overcoming above costs due to

short term payment may be passed on to the buyer

47Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Why buyer prefers cash discountsWhy buyer prefers cash discounts

• Negotiate highest possible cash discountsNegotiate highest possible cash discounts• For example most commonly used cash

discount isdiscount is A discount of 2% can be takenif the invoice is paid within 10days

2% 10 daysnet 30 days

y

Th f ll h ld bnet 30 days The full amount should beremitted if payment is madebetween 10 and 30 days afterreceipt of the invoicep

48Arshinder Kaur, Assistant Professor, DoMS, IIT Madras

Cash discounts• Is 2% a good amount of saving?• Let’s see it annually

f iy

A bill payment can be done in 30 daysbut discount (of 2%) can be taken upto tenth day

If the buyer is not interested to take the discountto tenth day

The buyer is paying 2%of the total amount ofinvoice to use the cashi l d f 20 d

How many 20 dayperiods in a year(365 days) =365/20 18 25

What is the 2% times 18.25 twenty day periods? involved for 20 days365/20 =18.25periods?

A 2/10 discount translates into an annual discount rate of 36.5 % (2% times 18.25)( % )Getting 36.5 % of annual discount is a good business, Capability to understand the time value of money 49Arshinder Kaur, Assistant Professor, DoMS,

IIT Madras

![Session 4 (a) - Price [Compatibility Mode]](https://img.dokumen.tips/doc/110x75/56d6bfd01a28ab301697c8df/session-4-a-price-compatibility-mode.jpg)