Embed Size (px)

Citation preview

Separate and Consolidated Annual Report 2013

52nd Financial Year

Shareholders’ Meeting 16 April 2014

DIRECTORS’ REPORT ON OPERATIONS

FINANCIAL AND OPERATING HIGHLIGHTS

GE Capital Interbanca S.p.A. 2013 2012

Balance Sheet and Income Statement – in millions of Euros

Due from banks and loans to customers 2,341 2,942

Equity investments (including other equity interests) 70 75

Equity investments 368 384

Funding 2,518 2,966

Net interest margin 44 49

Net fee and commission income 6 9

Net interest and other banking income 39 54

Net impairment losses (153) (189)

Operating costs (58) (75)

Net income (loss) for the period (128) (169)

Financial ratios - in %

Net interest margin / Net interest and other banking income 114.5 90.9

Net fee and commission income / Net interest and other banking income 14.6 17.0

Operating costs / Net interest and other banking income 150.1 138.9

In millions of Euros

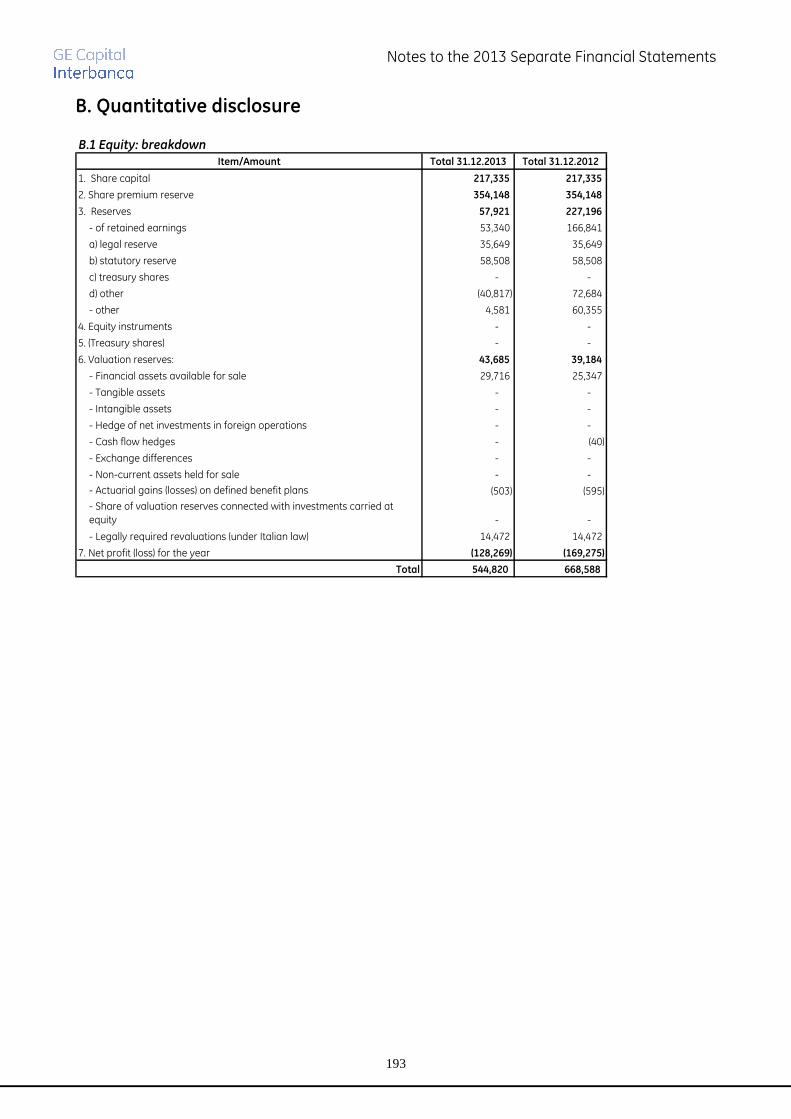

Equity 545 669

Regulatory Tier 1 Capital 498 627

Total regulatory capital 648 814

Capital ratios - in %

Regulatory Tier 1 Capital / Risk-weighted assets (*) 15.4 16.1

Total regulatory capital / Risk-weighted assets (*) 20.0 21.0

Credit risk ratios %

Net impaired loans / Total net loans 23.3 17.6

Net impaired loans / Equity 100.0 77.4

Net non-performing loans / Total net loans 5.6

5.0

In absolute terms

Headcount at year end 256 286

(*) these figures do not include the 25% reduction in regulatory capital requirements for banks belonging to a banking group, as GE

Capital Interbanca S.p.A is also Parent Company of the GE Capital Interbanca Banking Group.

DIRECTORS’ REPORT ON OPERATIONS

1

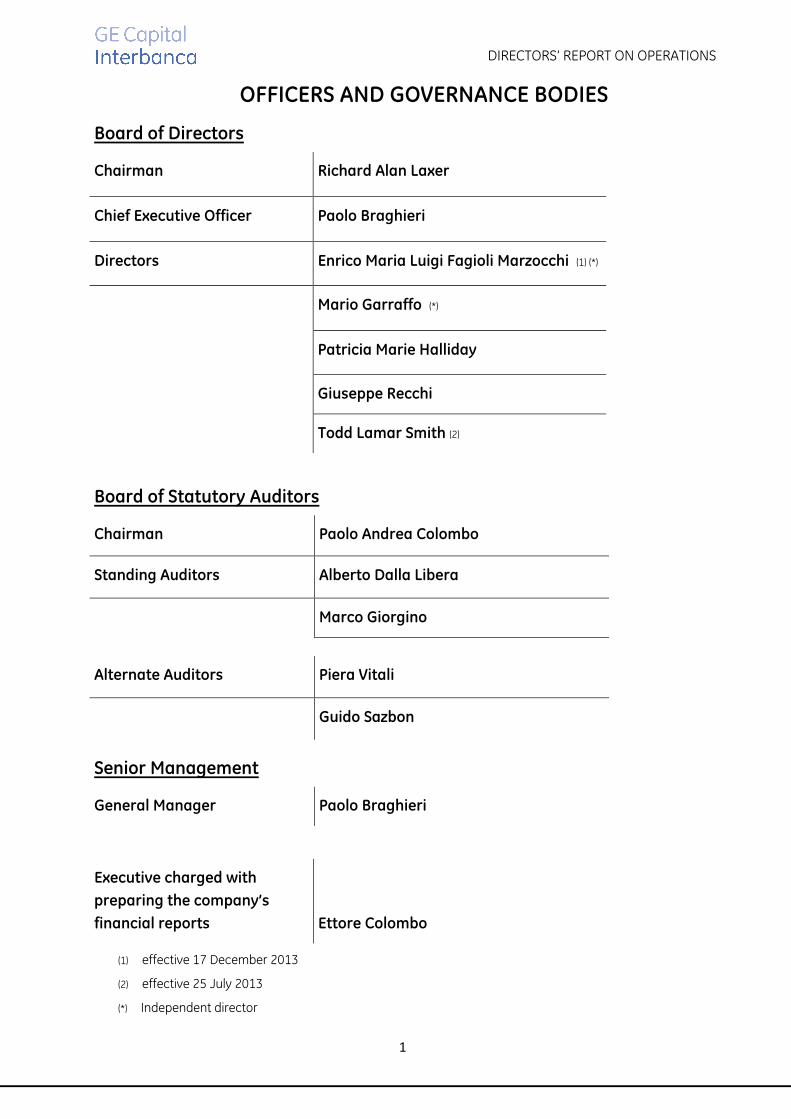

OFFICERS AND GOVERNANCE BODIES

Board of Directors

Chairman Richard Alan Laxer

Chief Executive Officer Paolo Braghieri

Directors Enrico Maria Luigi Fagioli Marzocchi (1) (*)

Mario Garraffo (*)

Patricia Marie Halliday

Giuseppe Recchi

Todd Lamar Smith (2)

Board of Statutory Auditors

Chairman Paolo Andrea Colombo

Standing Auditors Alberto Dalla Libera

Marco Giorgino

Alternate Auditors Piera Vitali

Guido Sazbon

Senior Management

General Manager Paolo Braghieri

Executive charged with

preparing the company’s

financial reports

Ettore Colombo

(1) effective 17 December 2013

(2) effective 25 July 2013

(*) Independent director

DIRECTORS’ REPORT ON OPERATIONS

2

(empty page)

DIRECTORS’ REPORT ON OPERATIONS

3

2013 SEPARATE

ANNUAL REPORT

GE CAPITAL INTERBANCA S.p.A.

52nd Financial Year

DIRECTORS’ REPORT ON OPERATIONS

4

ANNUAL REPORT 2013

� Directors’ Report on Operations 7

� Separate Financial Statements 57

� Notes to the Separate Financial Statements 67

� Report of the Board of Statutory Auditors 213

� Certification of the Financial Statements pursuant to Article 154-bis of Legislative Decree No. 58 of 24 February 1998

219

� Report of the Accounting Audit Firm 221

CONSOLIDATED FINANCIAL STATEMENTS 2013

� Directors’ Report on Consolidated Operations 229

� Consolidated Financial Statements 265

� Notes to the Consolidated Financial Statements 275

� Certification of the Consolidated Financial Statements pursuant to Article

154-bis of Legislative Decree No. 58 of 24 February 1998

425

� Report of the Accounting Audit Firm 427

OFFICES

429

DIRECTORS’ REPORT ON OPERATIONS

5

DIRECTORS’ REPORT ON OPERATIONS 7

SUMMARY OF THE BANK’S ACTIVITIES 11

2013 FINANCIAL RESULTS 28

ADDITIONAL INFORMATION 36

PROPOSED ALLOCATION OF LOSSES 53

OUTLOOK FOR 2014 54

SEPARATE FINANCIAL STATEMENTS 57

NOTES TO THE SEPARATE FINANCIAL STATEMENTS

67

� Part A – Accounting policies 69

� Part B – Information on the Balance Sheet 91

� Part C – Information on the Income Statement 127

� Part D – Statement of Comprehensive Income 147

� Part E – Information on risks and risk management policies 149

� Part F – Information on capital 191

� Part G – Business combinations 199

� Part H – Related-party transactions 201

� Part I – Share-based payments 205

� Part L – Segment reporting 207

ADDITIONAL INFORMATION 209

� Disclosure pursuant to Article 2427-16 bis of the Italian Civil Code 210

� Disclosure pursuant to Article 2497 bis of the Italian Civil Code 211

REPORT OF THE BOARD OF STATUTORY AUDITORS 213

CERTIFICATION OF THE FINANCIAL STATEMENTS PURSUANT TO ARTICLE 154

BIS OF LEGISLATIVE DECREE NO. 58 OF 24 FEBRUARY 1998

219

REPORT OF THE ACCOUNTING AUDIT FIRM 221

DIRECTORS’ REPORT ON OPERATIONS

6

(empty page)

DIRECTORS’ REPORT ON OPERATIONS

7

DIRECTORS’

REPORT

ON OPERATIONS

DIRECTORS’ REPORT ON OPERATIONS

8

(empty page)

DIRECTORS’ REPORT ON OPERATIONS

9

OVERVIEW OF BUSINESS ACTIVITIES

Dear Shareholders,

In 2013, the Italian economy continued to deteriorate and the difficult context was reflected heavily

in businesses’ demand for financing, particularly from SMEs. An important factor in the state of the

crisis for Italian businesses was confirmed by bankruptcy data, which is continually increasing,

posting a 12.1% annual increase over 2013.

The difficult economic and financial situation for businesses had the inevitable result of a decline in

credit quality, with the latest data showing non-performing bank loans and the risk of loans in Italy

growing 24.7% in 2013 (Source: ABI).

Italian GDP was down for the entire year, with an interruption only in the third quarter of 2013,

supported by exports and changes in inventories, although still showing low levels of internal

consumption and investment.

Finally, despite initial signs of stabilisation, the unemployment rate continued to grow, reaching

12.3% in the third quarter of 2013.

As regards the Euro zone, there was a slight and fragile recovery, although the general financial

conditions in the area became more favourable. Industrial production for the Euro zone showed

positive results, starting to recover lost ground in September 2013 and posting an increase in the

trend of 2.8% in November.

This economic context has clearly affected the Bank’s results, operating plans and growth forecasts,

with the latter being reconsidered with a forecast for returns in the medium/long term.

As planned, during 2013 the Bank maintained its prudent risk management, with the shared

objective of rebalancing the portfolio mix through integrated customer service and the expansion of

cross selling among the various businesses.

Profitable organic growth was prioritised, not only for the core product lines - leasing and factoring -

of traditional medium and long-term lending activities and, due to the Bank’s equity solidity

(consolidated Total Capital ratio of 17%), commercial activities continued to grow, posting higher

volumes.

Total disbursements in 2013 were € 336 million, a 7.7% increase from the € 312 million disbursed in

2012.

Along with intensive monitoring and managing of the loan portfolio, considerable progress was

made in containing structural operating costs, by reviewing supply and service contracts.

DIRECTORS’ REPORT ON OPERATIONS

10

In light of continued deterioration in loans to customers, the uncertainty in the overall economic

scenario in which the Bank operates affected the valuation of the non-performing portfolio, which

was reflected in the income statement for € 133 million.

The various factors highlighted above resulted in a net loss for 2013 for the Bank amounting to €

128.3 million.

DIRECTORS’ REPORT ON OPERATIONS

11

SUMMARY OF THE BANK’S ACTIVITIES

LOANS

Total loans to customers and due from banks declined 20% compared to the end of 2012.

In thousands of Euros 31.12.2013 % 31.12.2012 %

Due from banks 226,274 9.7 324,649 11.0

Loans to customers 2,114,951 90.3 2,617,823 89.0

Total 2,341,225 100.0 2,942,472 100.0

LOANS TO CUSTOMERS

Loans to customers declined 19.2% as a result of lower disbursements with respect to loans reaching

maturity and further write-downs.

Total disbursements in 2013 were € 335 million, a 7.7% increase from the € 312 million disbursed in

2012, and counter to the trend for the banking system1 which posted a decline of 5.3% on an annual

basis for loans to non-financial companies.

In particular, new volumes in 2013 consisted of corporate lending activities for € 198 million and

structured finance activities for € 122 million.

The lower weight of the corporate lending component compared to the prior year is mainly due to

the trend in the reference market, which, in an increasingly competitive market, is characterised by

the propensity of potential customers of the Bank to carry out unsecured transactions at conditions

that are not compatible with the Bank’s profitability objectives.

As regards the type of lending activities, the portfolio as at 31 December 2013 is comprised as

follows:

� in the Corporate Finance Sector by:

• Acquisition Finance for € 476 million;

• Real Estate for € 346 million;

• Project Finance for € 295 million;

• Shipping for € 216 million;

� in the Corporate Banking sector by:

• Corporate Lending for € 665 million;

• Corporate Acquisition for € 58 million.

1 Source: Bank of Italy

DIRECTORS’ REPORT ON OPERATIONS

12

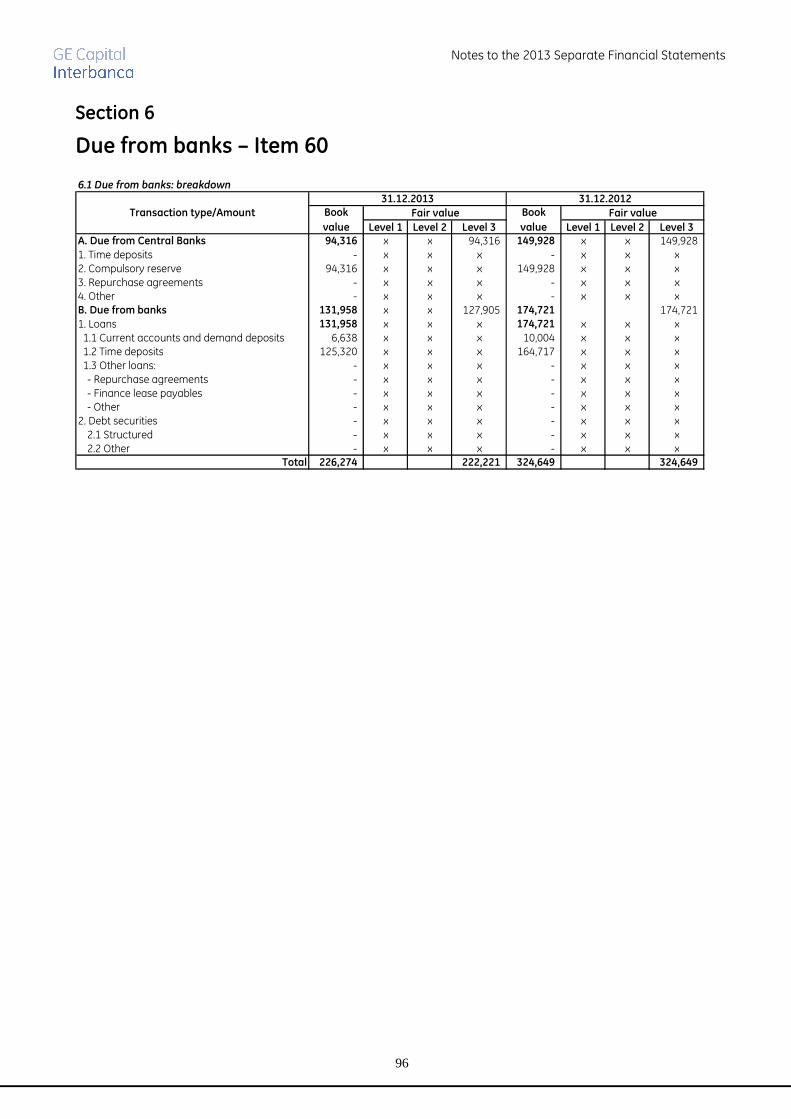

DUE FROM BANKS

Due from banks, equivalent to € 226 million, decreased 30.3% compared to 2012. This item primarily

consists of deposits, mostly those held as collateral for syndicated loans (IBLOR) for € 98 million, bank

demand deposits of € 100 million, and, to a lesser extent, collateral relationships associated with

derivative transactions. The decrease is primarily due to the effect of a temporary liquidity surplus

related to early repayments by customers, which was also seen in 2012.

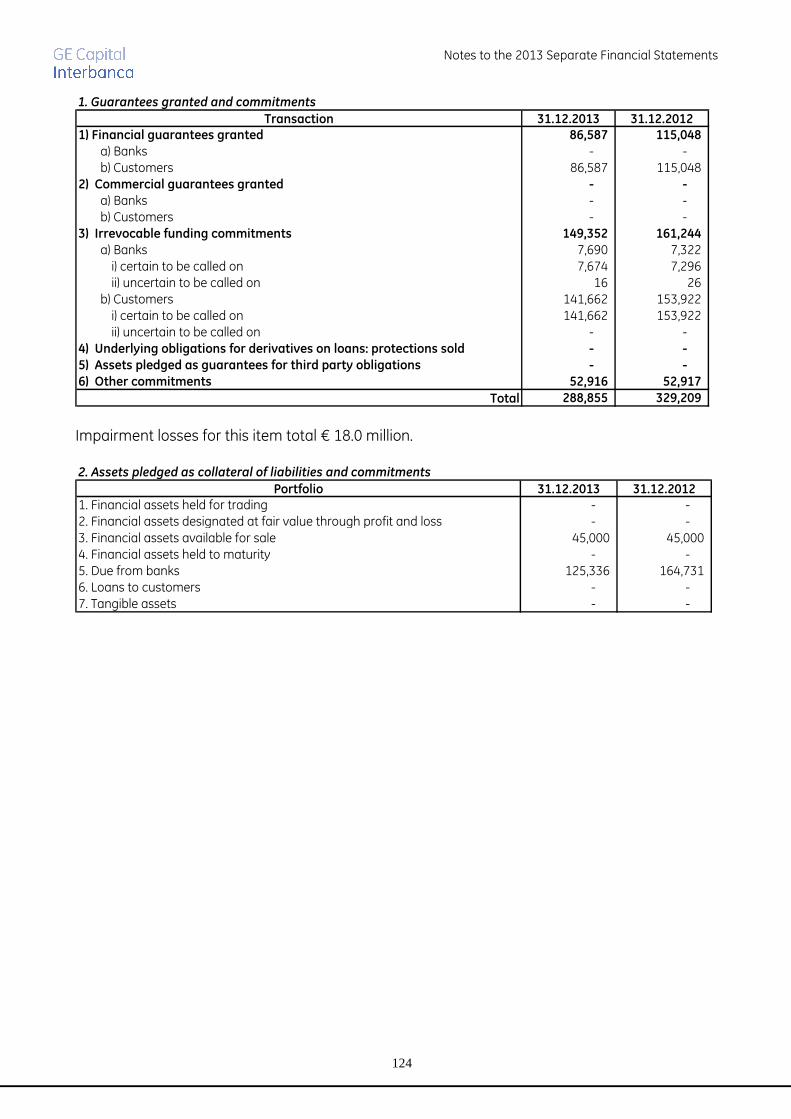

ENDORSEMENTS AND GUARANTEES

Endorsements and guarantees are € 158 million, a decrease of 26.8%, and consist of sureties issued

for € 105 million (of which € 98 million for related IBLOR loan transactions where the collateral

deposit is included under Due from banks) and € 53 million for a pledge on shares in the Bank’s

equity portfolio.

DIRECTORS’ REPORT ON OPERATIONS

13

CREDIT REVIEW

Performing loans to customers

During 2013, performing loans were affected by new disbursements of € 335 million and maturing

loans of € 940 million.

The continued worsening in bank credit quality, principally attributable to the economic recession

and weakness in loan demand by businesses, resulted in a reclassification of 33 new defaults to the

category of impaired loans, generating a flow of volumes to the “doubtful” category for € 241 million.

These new positions are lower than the 52 defaults in the previous year and are entirely related to

the loan portfolio prior to the acquisition by GE Capital Corporation Inc.

The 2013 default rate is 4.1%, compared to 4.6% in 2012 and 2.9% in 2011. The LGD rate was 59.2%,

a decline from 60.1% in the previous year, and was influenced by the presence of unsecured

transactions.

Default rate and LGD are parameters used by the calculation model to determine collective

impairment write-downs on the portfolio of performing loans to customers. These parameters,

applied to the categories considered to be at greatest risk, based on statistical results over the last

three years for similar rating groups, resulted in a collective impairment write-down for the portfolio

of 2.81%, against 2.60% for 2012.

In order to calculate the collective impairment write-down, the same criterion adopted by the Parent

Company for performing cash loans is used; the coverage amounts to € 2.3 million, corresponding to

2.83%, compared with 2.65% recorded at the end of 2012.

DIRECTORS’ REPORT ON OPERATIONS

14

Impaired loans

The systematic assessment of “doubtful” loans, through the use of valuation techniques

differentiated based on the type and condition of the position under consideration, results in

collection estimates made on a “case-by-case” basis, with the corresponding proposals for charge-

offs or recoveries. Additionally, impaired loans for which the case-by-case assessment did not

determine any adjustment are written down on a collective basis.

The following table shows gross and net on-balance sheet loans due from banks and customers,

divided by risk class.

Impaired loans 1,192,930 648,101 544,829 23.3 54.3 1,085,015 517,213 5.3

Non-performing 524,035 392,584 131,451 5.6 74.9 526,781 147,994 -11.2

Sub-standard 517,468 204,059 313,409 13.4 39.4 431,014 261,828 19.7

Restructured 103,303 50,301 53,002 2.3 48.7 63,201 44,107 20.2

Past due 48,124 1,157 46,967 2.0 2.4 64,019 63,284 -25.8

Performing loans 1,852,040 55,644 1,796,396 76.7 3.0 2,484,498 2,425,259 -25.9

Total loans 3,044,970 703,745 2,341,225 100.0 23.1 3,569,513 2,942,472 -20.4

In thousands

of Euros

% Coverage

ratio (B/A)

Net exposure

31.12.2012

(D)

% Chg

(C/D)

Gross

exposure

31.12.2013

(A)

Total

impairment

losses

31.12.2013

(B)

Net exposure

31.12.2013

(C)

%

(C)

Gross

exposure

31.12.2012

In valuing the trend in impaired loans during 2013, it was necessary to consider that on 27

December, the Bank sold, without recourse, non-performing loans related to 72 positions for a total

gross value of € 36.4 million, which had been completely written off. This sale took place with the

verified bankruptcy of the customers, all in bankruptcy proceedings, as well as the inclusion of the

loans as unsecured receivables as liabilities in the respective bankruptcy proceedings, for which the

Bank verified the non-recoverability of the receivable based on the results of actions taken and the

status of various procedures.

In terms of overall exposure, the gross impaired loans increased by 9.9% on an annual basis (+13.3%

excluding the effects of the aforementioned sale). This increase is, for the most part, related to the

“Restructured” (+63.5%) and “Sub-standard” (+20.1%) categories, as opposed to the “Non-

performing” category that decreased 0.5% (+6.4% excluding the effects of the sale) and the “Past

due” category, which declined by 24.8%.

2013 figures for the increase in the “Non-performing” category are better than those for the Italian

banking system2 (+24.7%), and specifically in the corporate segment (+29.8%).

New defaults, entirely related to disbursements prior to the acquisition of the controlling interest by

GE Capital Corporation Inc., generated increases of € 242 million, partially offset by reductions,

mainly due to collections of € 65 million, cancellations and sales of € 92 million and transfers to the

performing category of € 17 million.

2 Source: ABI Economic Analysis Department

DIRECTORS’ REPORT ON OPERATIONS

15

Following the trend in gross amounts explained above and the related trends in impairments, net

exposures increased 5.3% over the 2012 year-end figure.

The change in the coverage percentage on total impaired loans, currently at 54.3% compared to

52.3% at the end of the prior year and at 46% in 2011, is related to the growth in exposures at

greater risk.

The Bank’s coverage level in recent years continues to be higher than the system's average. In fact,

for the non-performing category only, the risk data for the Italian banking system showed an

increasing trend, with a coverage percentage was 39.1% in 2009 that reached 48.4% in December

2013, while the Bank’s figures during the same period showed an increasing trend from 60.3% in

2009, reaching 74.9% at the end of 2013.

The following table shows a breakdown of endorsements by risk category.

Impaired exposures 24,312 15,763 8,549 0.4 64.8 53,408 9,069 -5.7

Performing exposures 80,310 2,273 78,037 3.3 2.8 108,864 105,979 -26.4

Total endorsements 104,622 18,036 86,586 3.7 17.2 162,272 115,048 -24.7

Endorsements

In thousands

of Euros

Net exposure

31.12.2012

(D)

% Chg

(C/D)

Gross

exposure

31.12.2013

(A)

Total

impairment

losses

31.12.2013

(B)

Net exposure

31.12.2013

(C)

%

(C)

% Coverage

ratio (B/A)

Gross

exposure

31.12.2012

Gross impaired positions amounted to € 24.3 million and have a coverage percentage of 64.8%.

The total reserve for endorsements amounts to € 18 million and is recognised in the item "Other

liabilities".

DIRECTORS’ REPORT ON OPERATIONS

16

Principal loan ratios

Impaired loans

In % 31.12.2013 31.12.2012

Gross impaired loans / Total gross loans 39.2 30.4

Net impaired loans / Total net loans 23.3 17.6

Net impaired loans / Equity 100.0 77.4

Non-performing

In % 31.12.2013 31.12.2012

Gross non-performing loans / Total gross loans 17.2 14.8

Net non-performing loans / Total net loans 5.6 5.0

Net non-performing loans / Equity 24.1 22.1

Sub-standard

In % 31.12.2013 31.12.2012

Gross sub-standard loans / Total gross loans 17.0 12.1

Net sub-standard loans / Total net loans 13.4 8.9

Net sub-standard loans / Equity 57.5 39.2

Restructured

In % 31.12.2013 31.12.2012

Gross restructured loans / Total gross loans 3.4 1.8

Net restructured loans / Total net loans 2.3 1.5

Net restructured loans / Equity 9.7 6.6

Loans past due by 90 days or more

In % 31.12.2013 31.12.2012

Past due by 90 days or more gross / Total gross loans 1.6 1.8

Past due by 90 days or more net / Total net loans 2.0 2.1

Past due by 90 days or more net / Equity 8.6 9.5

DIRECTORS’ REPORT ON OPERATIONS

17

EQUITY INVESTMENTS

This item includes the following equity interests:

� GE Capital Servizi Finanziari S.p.A.: 100% of share capital;

� GE Capital Finance S.r.l.: 60% of share capital; the remaining 40% indirectly through GE

Capital Servizi Finanziari S.p.A.;

� GE Capital Services S.r.l.: 79% of share capital; the remaining 21% indirectly through GE

Capital Servizi Finanziari S.p.A.;

In addition, the Bank has:

� 100% indirect control of GE SPV S.r.l., a securitisation company, established in accordance

with art. 3 of Italian Law no. 130 of 30 April 1999, through its subsidiary GE Capital Servizi

Finanziari S.p.A.;

� an interest in Renting Italease S.r.l., which represents a joint venture with Italease Gestione

Beni S.p.A., through its subsidiary GE Capital Services S.r.l.

Furthermore, as part of the larger corporate simplification project of the GE Capital Interbanca

Banking Group:

� the direct subsidiaries GE Leasing S.p.A. and Bios Interbanca S.r.l. were merged into GE

Capital Servizi Finanziari S.p.A, effective 1 May 2013;

� the indirect subsidiary GE Commercial Distribution Finance S.r.l. was merged into GE Capital

Finance S.r.l. effective 1 May 2013;

� the indirect subsidiary GE Noleggi S.p.A. was merged into GE Capital Services S.r.l. effective 8

November 2013;

The equity investments in GE Capital Servizi Finanziari S.p.A. and GE Capital Finance S.r.l were

acquired following the authorisation issued by Bank of Italy on 31 December 2010 through a transfer

in kind by the controlling shareholder GE Capital Corporation.

This transfer in kind was recorded directly to a specific net equity reserve with the Bank using the

relevant equity values, totalling € 275 million, representing the fair value at the transfer date.

This figure, attributed to the equity investments at recognition and equivalent to the net equity of the

subsidiaries, was subsequently adjusted for a total of € 38.3 million, corresponding to the losses

incurred by said subsidiaries in recent years, and deemed representative of their impairment.

The equity investment in GE Capital Services S.r.l., a non-financial company that is not included in the

GE Capital Interbanca Banking Group and operates in the market of long-term rentals of vehicles and

operating assets, was acquired on 31 December 2012, again through the transfer in kind by the

controlling shareholder GE Capital Corporation.

This transfer, equivalent to 79% of the share capital of the transferred company, or € 55.8 million,

was made at the fair value calculated based on an appraisal by independent experts, which the Bank

recognised in a specific net equity reserve.

DIRECTORS’ REPORT ON OPERATIONS

18

� Direct subsidiaries belonging to the GE Capital Interbanca Banking Group

GE Capital Servizi Finanziari S.p.A.

The Company, enrolled in the Special Register pursuant to art. 107 of the Consolidated Banking Act,

belongs to the GE Capital Interbanca Banking Group and is subject to the management and

coordination of GE Capital Interbanca S.p.A. The Company is specialised in vehicle leasing and

equipment leasing and operates via a selected network of single-mandate financial asset agents

throughout Italy.

In addition, the Company has:

• 100% of the shares of GE SPV S.r.l.;

• 40% of the shares of GE Capital Finance S.r.l.;

• 21% of the shares of GE Capital Services S.r.l.;

The Shareholders’ Meetings of the companies concerned, held on 5 February 2013, approved the

planned merger by incorporation of GE Leasing Italia S.p.A. and Bios Interbanca S.r.l. into GE Capital

Servizi Finanziari S.p.A. The effective date of the merger is 1 May 2013, with retroactive application

for accounting and tax purposes from 1 January 2013.

Hence, the comments below regarding the balance sheet and income statement results as at 31

December 2013 include the results of the merged companies, while the comparative data as at 31

December 2012 reflects the pre-merger situation.

The key financial data show loans to customers increasing by € 990 million, or 3.7%, compared to the

end of 2012, primarily due to the transfer of the equipment lease portfolio following the merger (€

81.5 million). In the remaining portfolios, there was growth of 1.3% in the core business segment of

auto leasing, and declines in the run-off portfolios related to salary-backed loans (-29.2%), mortgages

to private customers (-8.4%) and auto instalment loans and personal loans (-66.2%).

Disbursement volumes in the core business of auto leasing for the year, equivalent to € 255 million,

were down 18.8% compared to 2012, due to the prolonged crisis in the automotive sector, although

the Company remains the market leader with a share of 14%. For the equipment lease portfolio

resulting from the merger, disbursement volumes amounted to € 42 million compared to € 31 million

in the prior year.

With regard to portfolio quality, the ratio of net non-performing loans to total net loans shows a

decline from the previous year, from 9% to 7.9%, mainly due to the effect of the transfer of the

equipment lease portfolio. The transfer also explains the level of cover on the portfolio, which is

currently 64.3% compared to 58.1% as at 31 December 2012.

Funding from financial institutions primarily consists of variable-rate lines for € 663 million, a fixed-

rate line for € 124 million and funds obtained by securitising the leasing portfolio for € 36 million.

The 2013 income statement shows the net interest margin down € 0.5 million (-1.9%), due to

contrasting factors: on one hand, higher cost of funding on lines renewed at the end of 2012 and, on

DIRECTORS’ REPORT ON OPERATIONS

19

the other, the positive contribution of the transfer of the equipment lease portfolio following the

merger.

Net impairment losses on loans were € 27.6 million, an increase of 27% from the figure at the end of

the previous year.

This increase is chiefly due to the portfolios in run-off, in particular, the mortgage portfolio, to which it

was necessary to apply a Discounted Cash Flow model, as well as the equipment lease portfolio for €

2.1 million.

Operating costs increased by € 3.2 million (+19.6%), principally as a result of increased personnel

expenses, for € 2.3 million, together with the increase in “Other administrative expenses” related to

the aforementioned merger transaction.

Net of the impairment on the value of the equity investment in GE Capital Finance S.r.l. for € 1.4

million, the pre-tax result was a loss of € 20.9 million, an increase from the pre-tax loss of € 11.8

million in the previous year.

The income tax component was positive for € 6.1 million following tax provisions for the option of

converting deferred tax assets for loan write-downs into tax credits, as well as participation in the tax

consolidation with specific agreements among the companies belonging to the Bank’s statutory

scope of consolidation.

Net of income taxes, the result for the year was a loss of € 14.8 million, a deterioration from the € 6.3

million loss suffered in 2012.

GE Capital Finance S.r.l.

The Company, enrolled in the Register pursuant to art. 107 of the Consolidated Banking Act, belongs

to the GE Capital Interbanca Banking Group and is subject to the management and coordination of

GE Capital Interbanca S.p.A. It operates in the factoring sector, offering financing services and

managing business loans. Over the years, the business has gradually begun to focus on the

components of service, creating internal competencies in offering a vast array of products designed

for the Italian market and, specifically, for medium to large businesses that are seeking to optimise

their credit risk profile, administrative management and working capital.

The Shareholders’ Meetings of the companies concerned, held on 26 October 2012, approved the

planned merger by incorporation of GE Commercial Distribution Finance S.r.l. into GE Capital Finance

S.r.l. The effective date of the merger is 1 May 2013, with retroactive application for accounting and

tax purposes from 1 January 2013.

Hence, the comments below regarding the balance sheet and income statement results as at 31

December 2013 include the results of the merged company, while the comparative data as at 31

December 2012 reflects the pre-merger situation.

With regard to operating management, in 2013, the Company’s total turnover increased 111% from

the previous year, from € 557 million in 2012 to € 1,177 million disbursed during the year.

Net loans to customers were € 231 million compared to € 87 million at the end of 2012, an increase

of 165%, thereby allowing the Company to obtain higher market share.

DIRECTORS’ REPORT ON OPERATIONS

20

In terms of portfolio quality, the ratio of net non-performing loans to total net loans showed further

improvement over the previous year, from 2.0% to 0.6%, due to the increase in loan volumes in 2013.

In reference to the key income statement items, note the significant improvement in net banking and

other income, to € 4.6 million, an increase of 51% over 31 December 2012, mainly due to higher

turnover.

Administrative expenses (including personnel expenses) were down 8.7% from 2012, chiefly as a

result of the reduction in cost for services received from GE Capital Group companies.

The valuation components related to loans and other risks and charges generated an impairment of

€ 0.4 million in 2013, compared to the write-back of € 1.8 million in 2012. This change is due to the

collective impairment on the performing portfolio following the increase in volume.

The pre-tax result was a loss of € 3.8 million, an improvement over the pre-tax loss of € 4.4 million in

the previous year.

The income tax component was positive for € 0.4 million following tax provisions for the option of

converting deferred tax assets for loan write-downs into tax credits, as well as participation in the tax

consolidation with specific agreements among the companies belonging to the Bank’s statutory

scope of consolidation.

Net of income taxes, the loss for the year amounts to € 3.4 million, an improvement over the loss of

€ 4.4 million in the previous year.

� Subsidiaries not belonging to the GE Capital Interbanca Banking Group

GE Capital Services S.r.l.

Effective 31 December 2012, the Company is fully owned by the Bank, with 79% direct ownership

and the remaining 21% through GE Capital Servizi Finanziari S.p.A., and is subject to management

and coordination of the Bank.

GE Capital Services S.r.l., classified as a “non-financial company”, operates primarily in the market of

long-term rentals of vehicles and operating assets.

The Shareholders’ Meetings of the companies concerned, held on 11 October 2013, approved the

planned merger by incorporation of GE Noleggi S.p.A. into GE Capital Services S.r.l. The effective date

of the merger is 8 November 2013, with retroactive application for accounting and tax purposes from

1 January 2013.

Hence, the comments below regarding the balance sheet and income statement results as at 31

December 2013 include the results of the merged company, while the comparative data as at 31

December 2012 reflects the pre-merger situation.

The Company has an interest in Renting Italease S.r.l., which represents a joint venture with Italease

Gestione Beni S.p.A.

DIRECTORS’ REPORT ON OPERATIONS

21

The key financial data show loans to customers increasing by € 332 million, or 14.7%, compared to

the end of 2012, primarily due to the transfer of the portfolio following the merger with GE Noleggi

S.p.A.

As regards operating management during 2013, the total volume disbursed by the Company

amounts to € 231 million, a 7.2% decrease from the previous year.

Under operating costs, charges were incurred of € 3.3 million for the collective personnel reduction

procedure, as per Law no. 223/91, for which the agreement was signed on 18 June 2013.

The pre-tax profit is equivalent to € 2.9 million. The income tax component was positive for € 6.4

million, characterised by the effects of participation in the tax consolidation with specific agreements

among the companies belonging to the scope of consolidation, as the taxes on the current IRES

profit, equivalent to € 7.2 million, were completely absorbed by the tax losses of the companies

belonging to the tax consolidation and, as a result, were not recognised in the separate financial

statements, as they were paid to the Parent Company in accordance with the tax consolidation

system in effect.

Net of income taxes, the profit for the year amounts to € 9.3 million, an improvement over the profit

of € 3.2 million in the previous year.

� Indirect subsidiaries belonging to the GE Capital Interbanca Banking Group

GE SPV S.r.l.

The Company, a fully-owned subsidiary of GE Capital Servizi Finanziari S.p.A, was established in March

2008 pursuant to art. 3 of Law no. 130 of 30 April 1999, to carry out a securitisation of performing

loans originated by said Parent Company, for 70% of the auto leasing portfolio volume, or € 400

million, with the objective of diversifying funding sources necessary to finance the growth of business

activities.

The run-off phase of the securitisation transaction began in June 2012, which envisages the

repayment of the Senior Notes consistent with the amortisation of the underlying portfolio, which will

presumably conclude during 2014. The Company closed its financial statements as at 31 December

2013 at breakeven.

DIRECTORS’ REPORT ON OPERATIONS

22

CORPORATE FINANCE

Equity investments

The subsidiaries confirm the strength of their fundamentals, supported in these dynamics by critical

factors such as geographic diversification of their customer portfolios outside the EU, manageable

levels of indebtedness, historical presence in their respective business sectors and careful control of

costs.

As at 31 December 2013, the equity investments portfolio consisted of 7 active positions, for a total

exposure of € 60.3 million. During the year, the equity investment in Roal Electronics S.p.A. was sold

and the Almeco S.p.A bond was fully repaid.

Other equity interests

At the end of 2013, the “Other equity interests” portfolio amounted to approximately € 9.5 million,

and consisted of 8 positions mainly resulting from restructuring transactions for customers in

temporary financial difficulty, which resulted in part of the debt being converted to capital or similar

equity instruments.

DIRECTORS’ REPORT ON OPERATIONS

23

FUNDING

MAIN FUNDING ITEMS

Total funding (including subordinated loans) decreased by 15.1%, consistent with the decline in loan

volumes over the course of 2013.

In thousands of Euros 31.12.2013 % 31.12.2012 %

Due to banks 11,107 0.5 16,054 0.5

Due to customers 2,287,141 90.8 2,623,863 88.5

Securities in issue 219,705 8.7 325,999 11.0

Total 2,517,953 100.0 2,965,916 100.0

Due to banks

In thousands of Euros 31.12.2013 % 31.12.2012 %

Deposits and loans 11,092 99.9 11,891 74.1

Funding from international organisations 15 0.1 1,663 10.3

Balances in deposits and demand deposits - 0.0 2,500 15.6

Total 11,107 100.0 16,054 100.0

Due to banks is essentially made up of short-term funding on the MID. The Bank did not take

advantage of the sources of financing made available by the ECB.

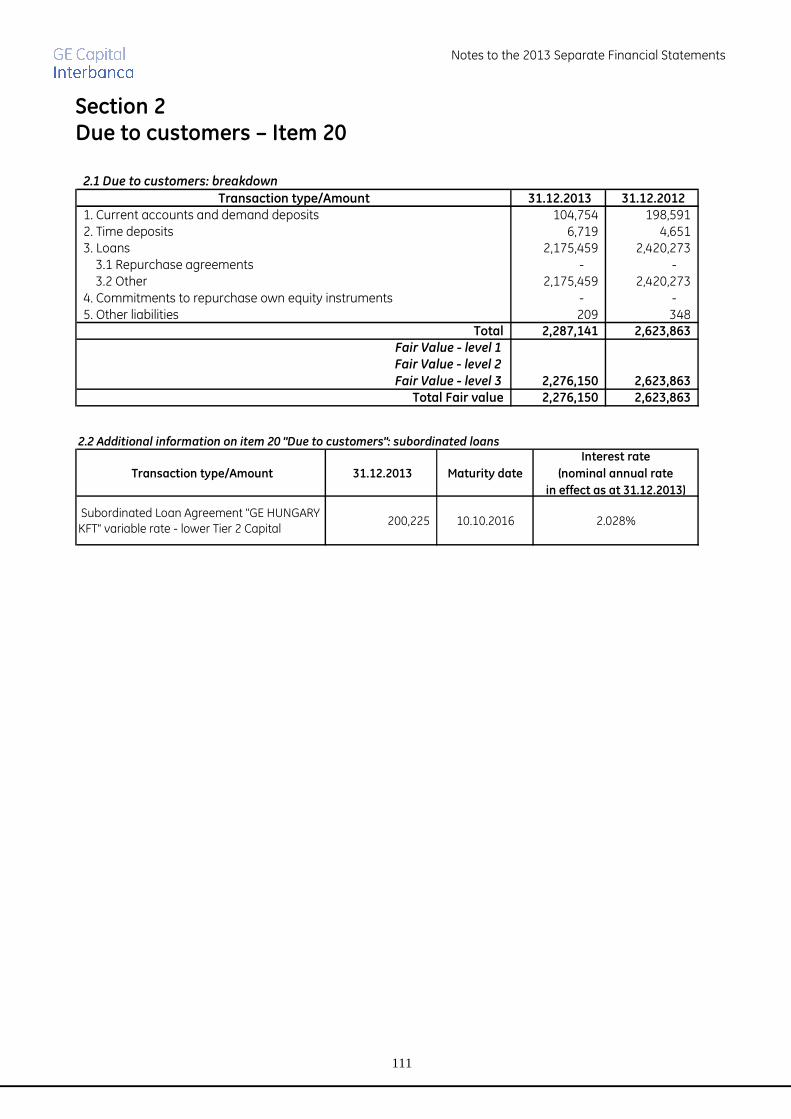

Due to customers

In thousands of Euros 31.12.2013 % 31.12.2012 %

Group loans 2,175,459 95.1 2,420,230 92.2

Deposits and demand deposits - Corporate 110,791 4.9 67,897 2.6

Deposits and demand deposits - Banking Group 681 0.0 135,345 5.2

Other funding 209 0.0 391 0.0

Total 2,287,140 100.0 2,623,863 100.0

Beginning in 2009, financing lines consisted of intercompany funding granted by General Electric

Group companies.

The Bank’s lines are currently guaranteed by the following companies: GE Capital Eireann Funding I

(with headquarters in Ireland), GE Financial Markets Funding I (with headquarters in the United

Kingdom), GE Capital Finance III GmbH & Co KG (with headquarters in Germany) and GE Hungary Kft

(with headquarters in Hungary).

The item “Intercompany deposits and demand deposits” consists of deposits with the Bank’s

subsidiaries. The reduction over the course of 2013 is attributable to higher liquidity needs of

subsidiaries to cover disbursements during the year.

Liquidity generated from corporate customers – a service to support businesses in managing excess

liquidity and optimising yields through time deposits – increased during 2013 with respect to the

previous year, caused by dynamics in liquidity management on the part of said customers.

DIRECTORS’ REPORT ON OPERATIONS

24

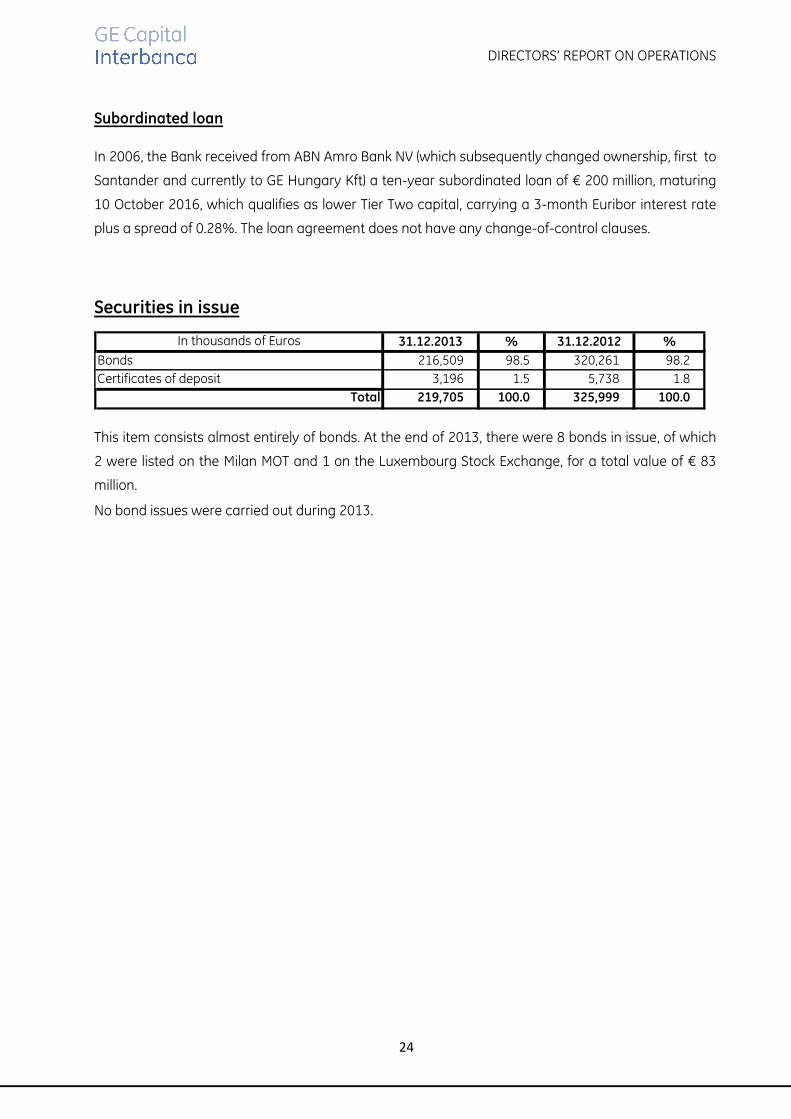

Subordinated loan

In 2006, the Bank received from ABN Amro Bank NV (which subsequently changed ownership, first to

Santander and currently to GE Hungary Kft) a ten-year subordinated loan of € 200 million, maturing

10 October 2016, which qualifies as lower Tier Two capital, carrying a 3-month Euribor interest rate

plus a spread of 0.28%. The loan agreement does not have any change-of-control clauses.

Securities in issue

In thousands of Euros 31.12.2013 % 31.12.2012 %

Bonds 216,509 98.5 320,261 98.2

Certificates of deposit 3,196 1.5 5,738 1.8

Total 219,705 100.0 325,999 100.0

This item consists almost entirely of bonds. At the end of 2013, there were 8 bonds in issue, of which

2 were listed on the Milan MOT and 1 on the Luxembourg Stock Exchange, for a total value of € 83

million.

No bond issues were carried out during 2013.

DIRECTORS’ REPORT ON OPERATIONS

25

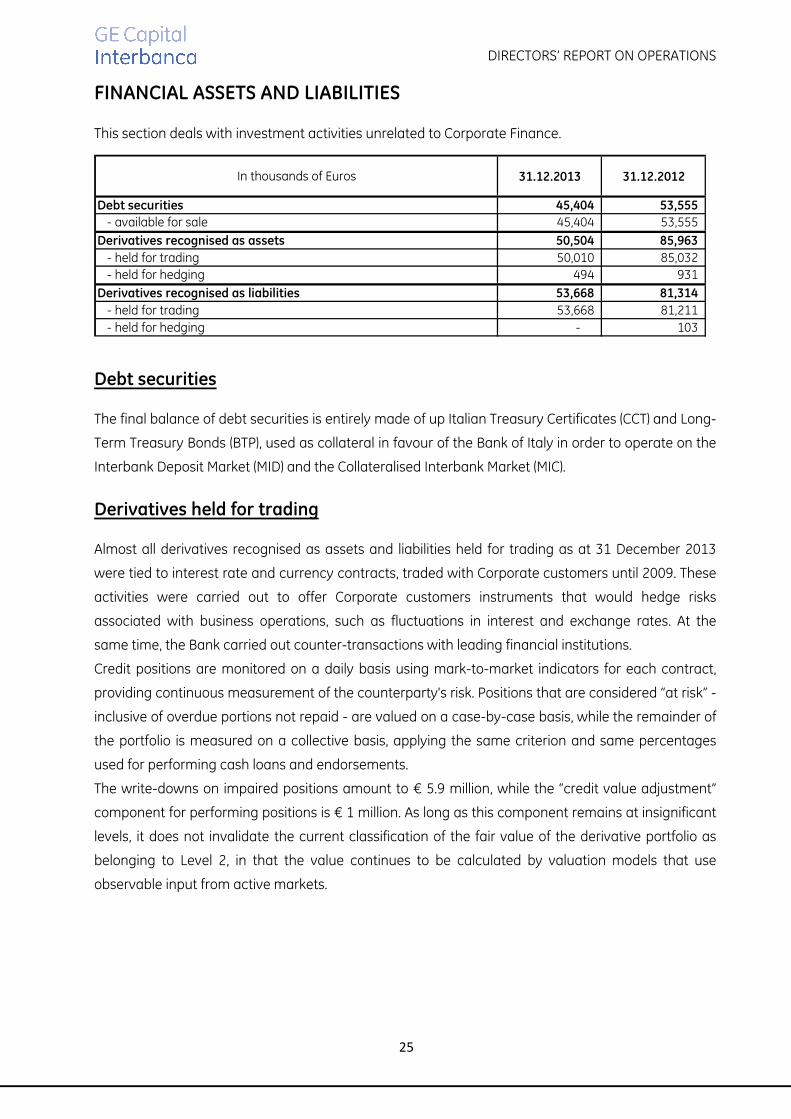

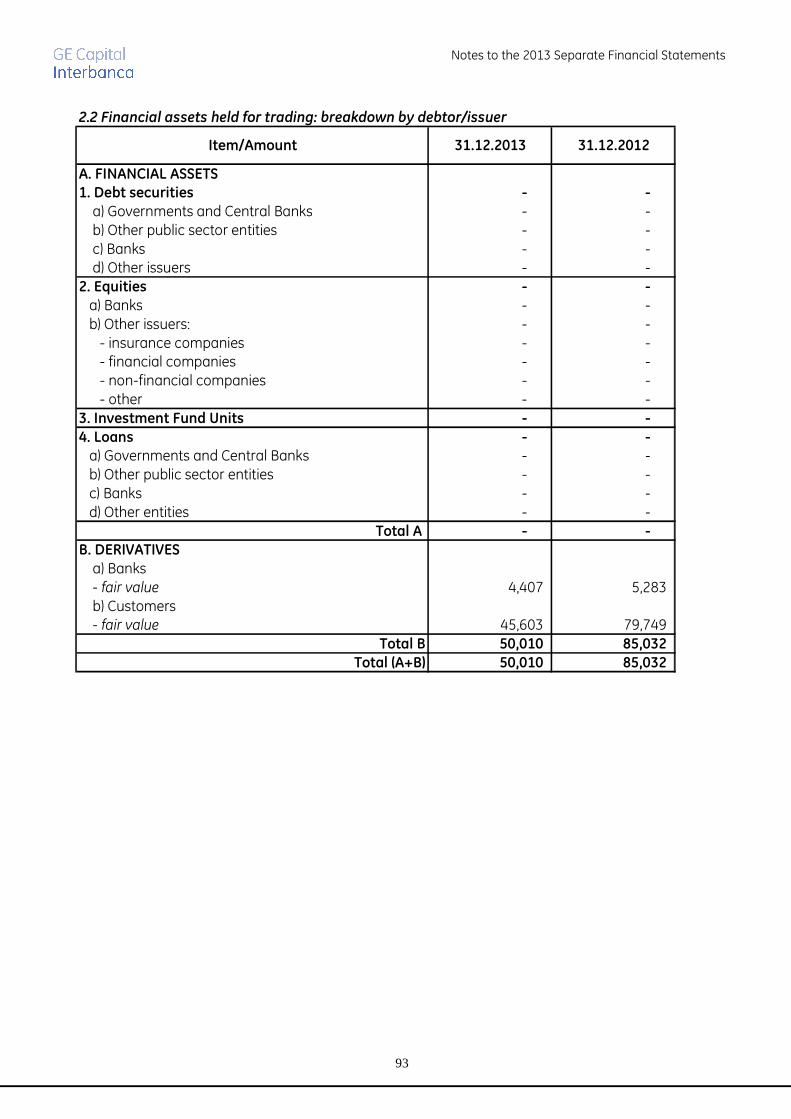

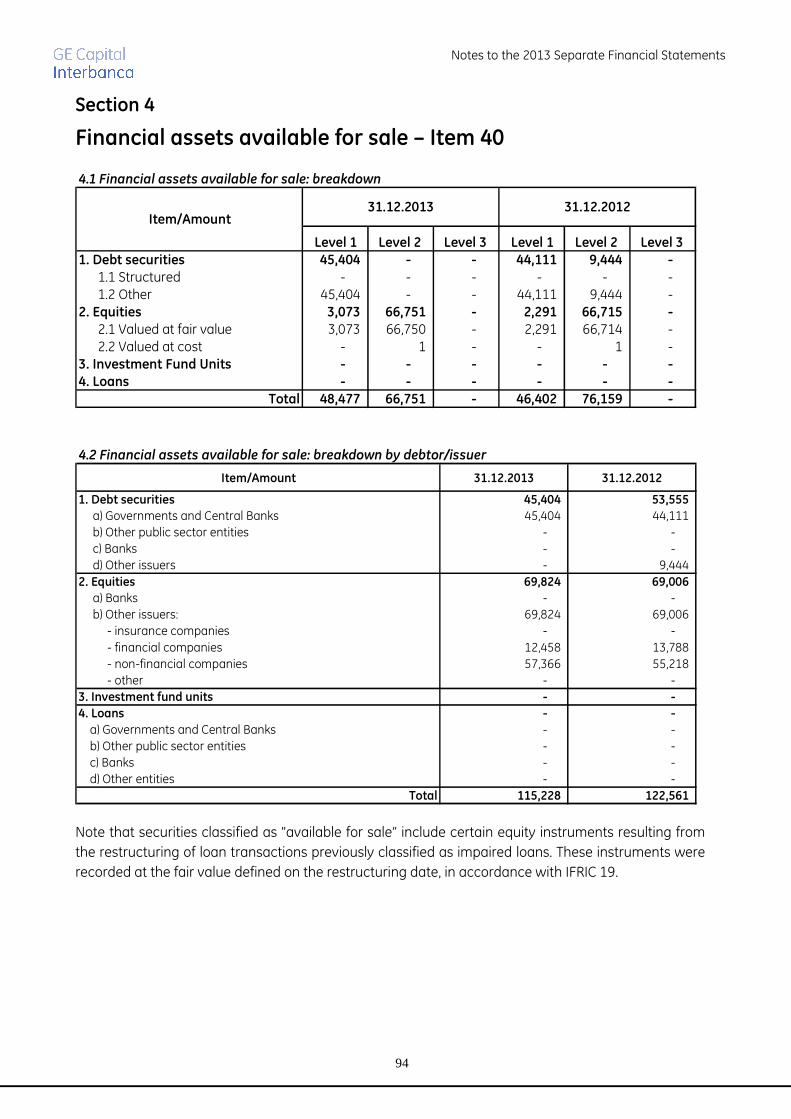

FINANCIAL ASSETS AND LIABILITIES

This section deals with investment activities unrelated to Corporate Finance.

In thousands of Euros 31.12.2013 31.12.2012

Debt securities 45,404 53,555

- available for sale 45,404 53,555

Derivatives recognised as assets 50,504 85,963

- held for trading 50,010 85,032

- held for hedging 494 931

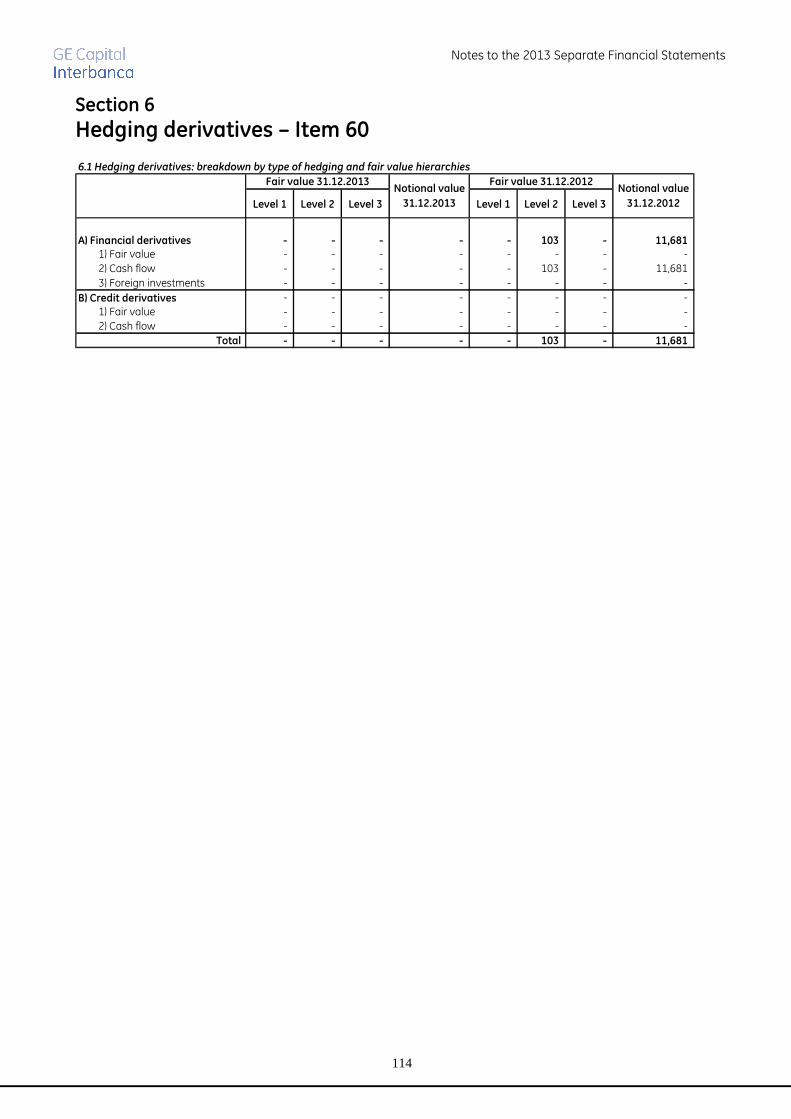

Derivatives recognised as liabilities 53,668 81,314

- held for trading 53,668 81,211

- held for hedging - 103

Debt securities

The final balance of debt securities is entirely made of up Italian Treasury Certificates (CCT) and Long-

Term Treasury Bonds (BTP), used as collateral in favour of the Bank of Italy in order to operate on the

Interbank Deposit Market (MID) and the Collateralised Interbank Market (MIC).

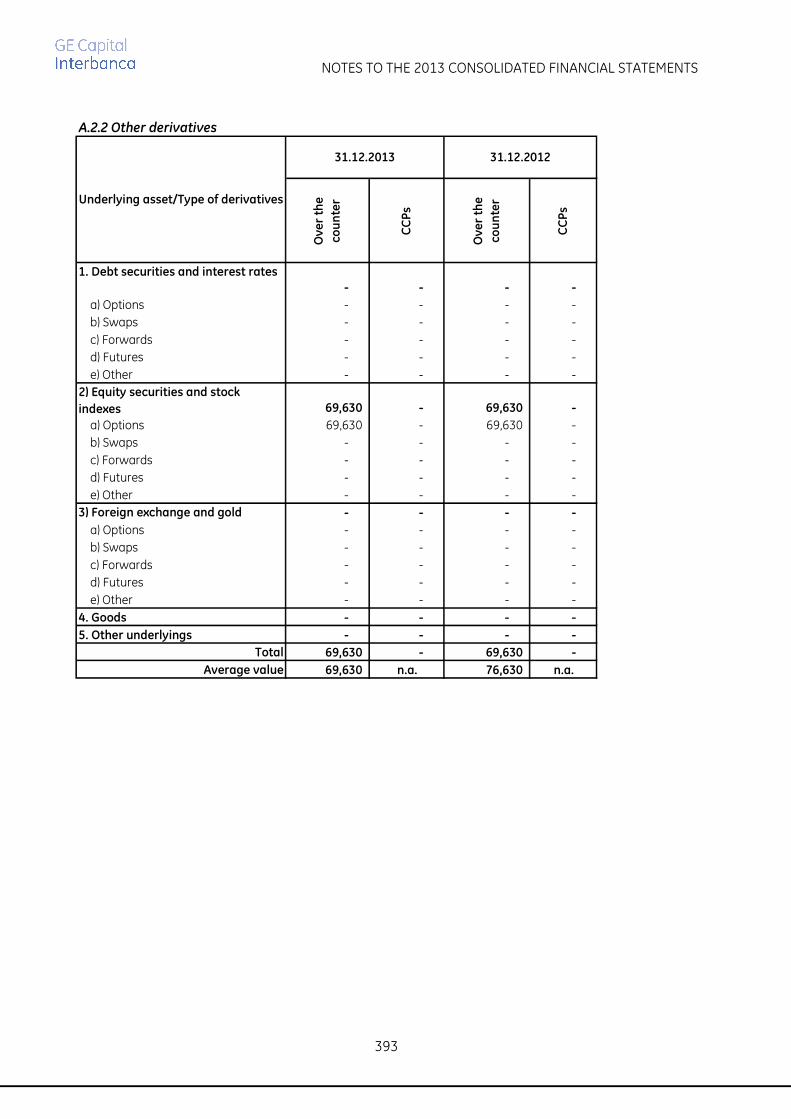

Derivatives held for trading

Almost all derivatives recognised as assets and liabilities held for trading as at 31 December 2013

were tied to interest rate and currency contracts, traded with Corporate customers until 2009. These

activities were carried out to offer Corporate customers instruments that would hedge risks

associated with business operations, such as fluctuations in interest and exchange rates. At the

same time, the Bank carried out counter-transactions with leading financial institutions.

Credit positions are monitored on a daily basis using mark-to-market indicators for each contract,

providing continuous measurement of the counterparty's risk. Positions that are considered “at risk” -

inclusive of overdue portions not repaid - are valued on a case-by-case basis, while the remainder of

the portfolio is measured on a collective basis, applying the same criterion and same percentages

used for performing cash loans and endorsements.

The write-downs on impaired positions amount to € 5.9 million, while the “credit value adjustment”

component for performing positions is € 1 million. As long as this component remains at insignificant

levels, it does not invalidate the current classification of the fair value of the derivative portfolio as

belonging to Level 2, in that the value continues to be calculated by valuation models that use

observable input from active markets.

DIRECTORS’ REPORT ON OPERATIONS

26

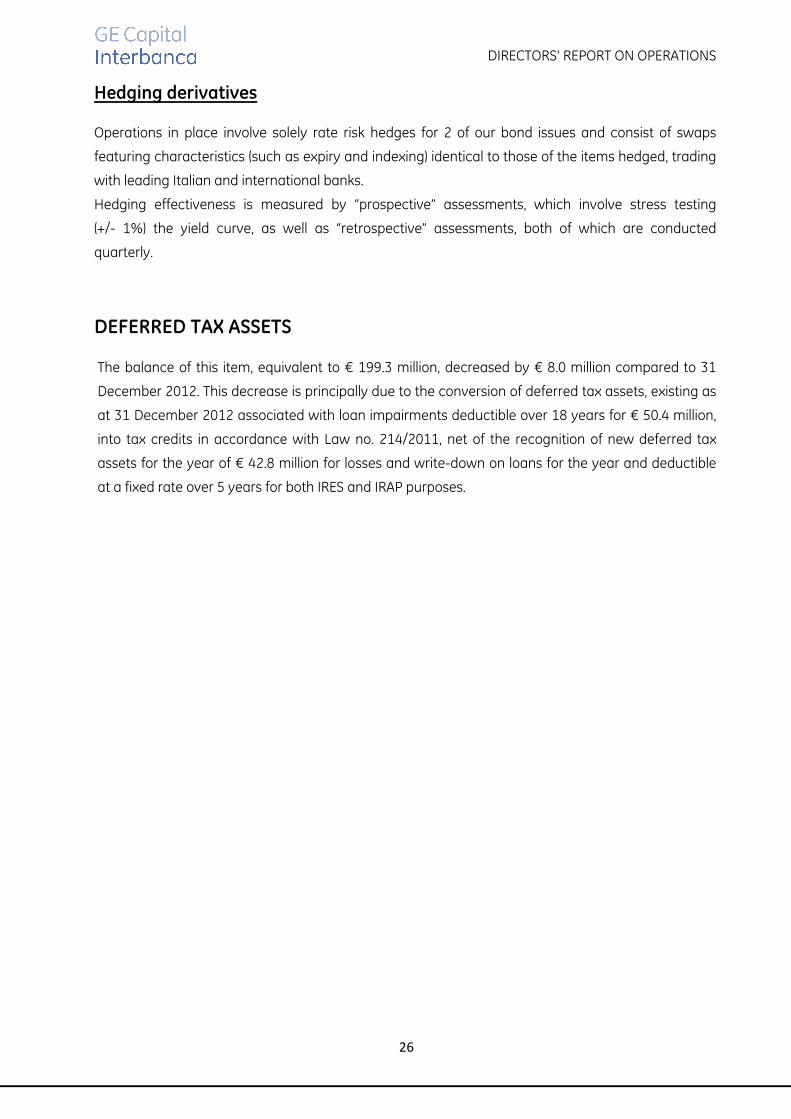

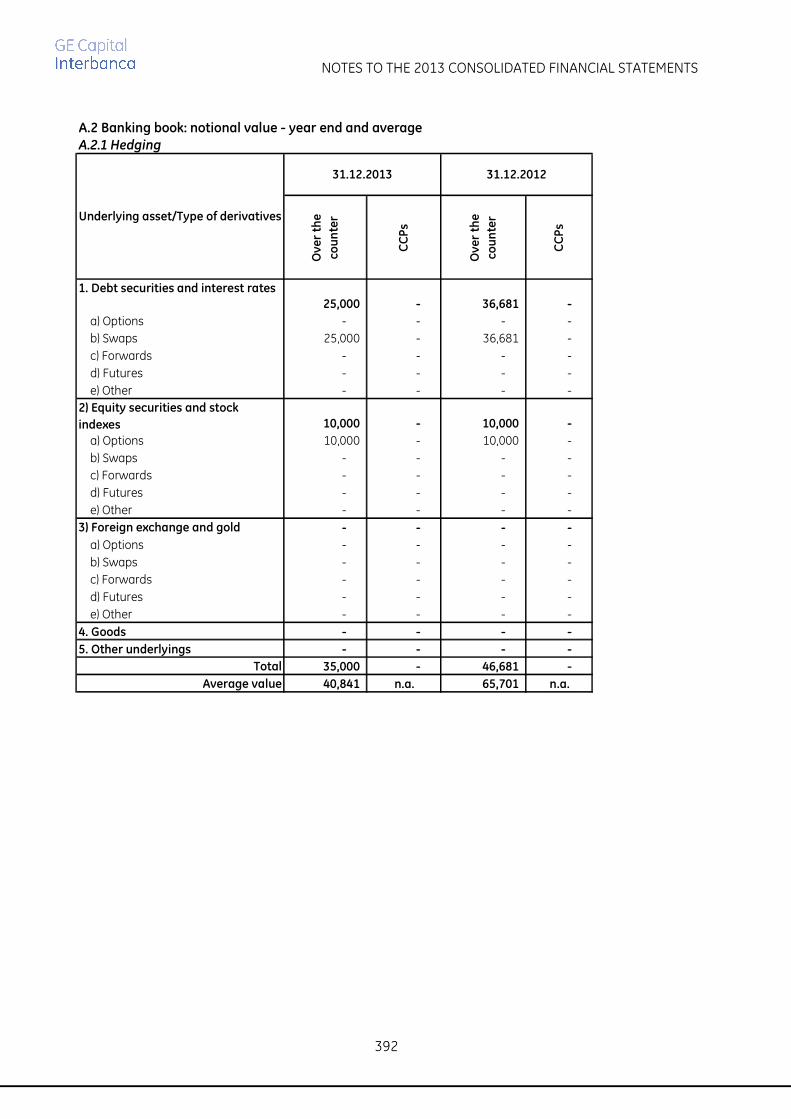

Hedging derivatives

Operations in place involve solely rate risk hedges for 2 of our bond issues and consist of swaps

featuring characteristics (such as expiry and indexing) identical to those of the items hedged, trading

with leading Italian and international banks.

Hedging effectiveness is measured by “prospective” assessments, which involve stress testing

(+/- 1%) the yield curve, as well as “retrospective” assessments, both of which are conducted

quarterly.

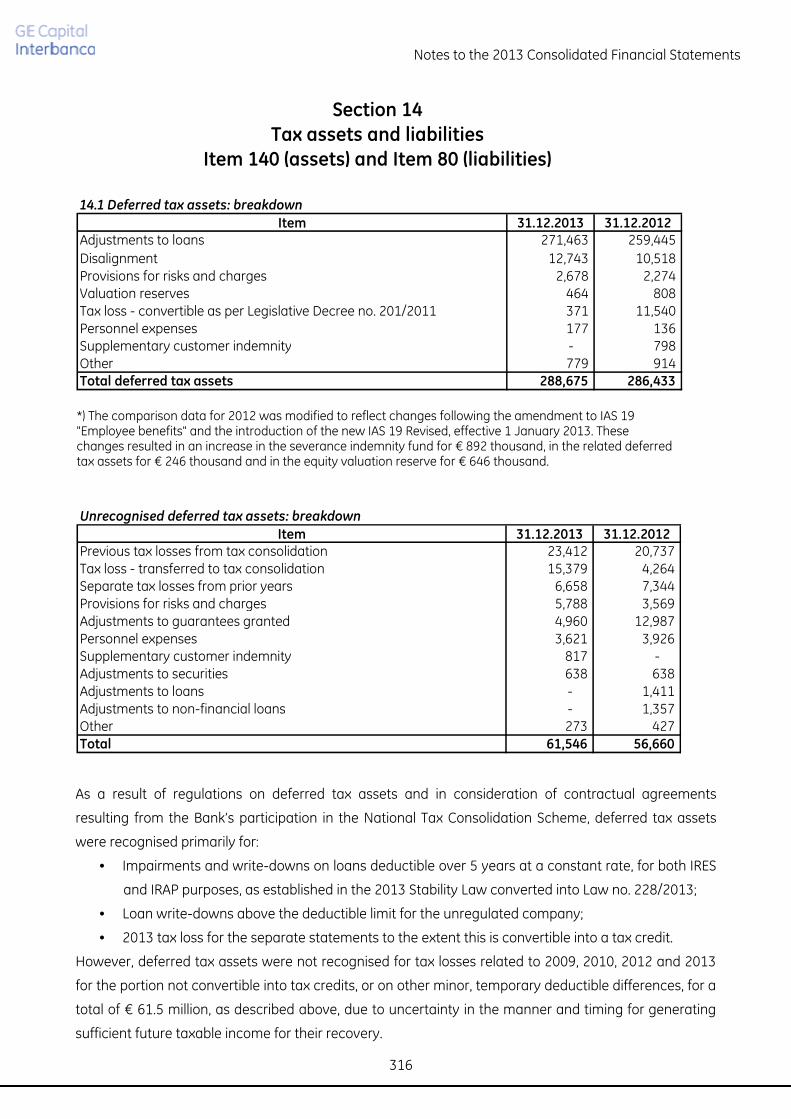

DEFERRED TAX ASSETS

The balance of this item, equivalent to € 199.3 million, decreased by € 8.0 million compared to 31

December 2012. This decrease is principally due to the conversion of deferred tax assets, existing as

at 31 December 2012 associated with loan impairments deductible over 18 years for € 50.4 million,

into tax credits in accordance with Law no. 214/2011, net of the recognition of new deferred tax

assets for the year of € 42.8 million for losses and write-down on loans for the year and deductible

at a fixed rate over 5 years for both IRES and IRAP purposes.

DIRECTORS’ REPORT ON OPERATIONS

27

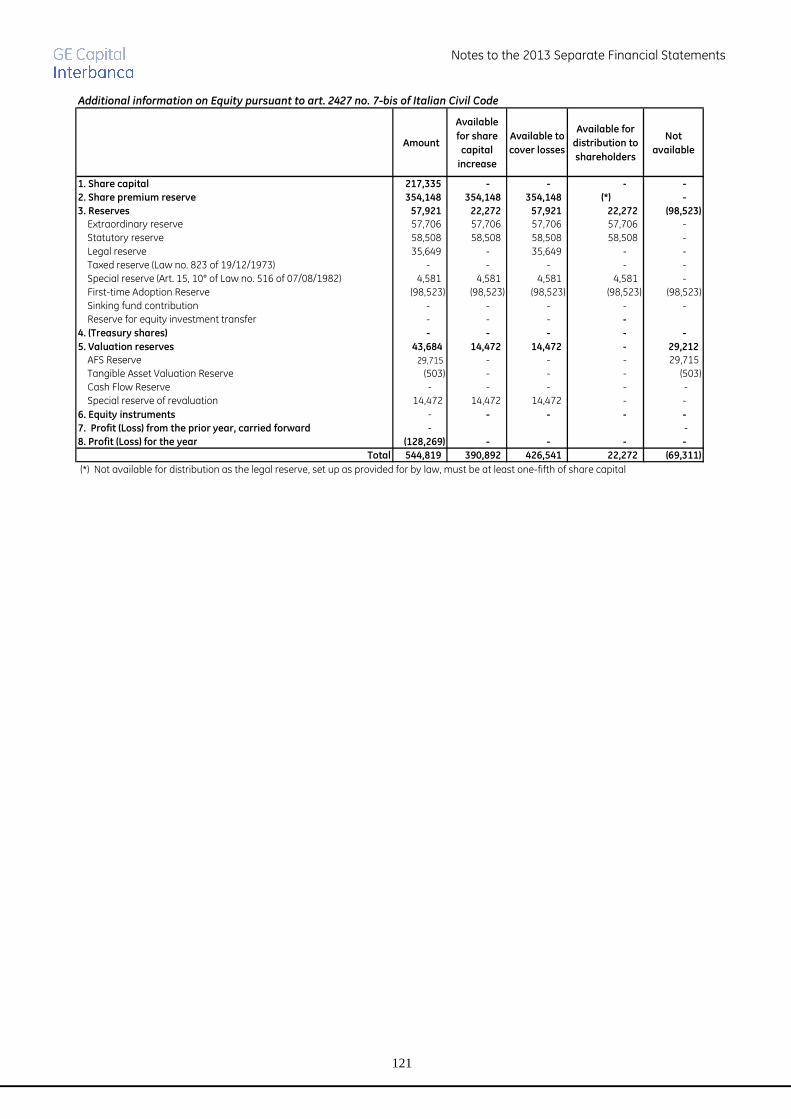

EQUITY

As at 31 December 2013, share capital and reserves – inclusive of the loss for the year – amounted to

€ 544.8 million, down € 123.8 million (-18.5%) with respect to the same figure recorded at the end of

2012.

The principal changes relate to:

• positively, valuation reserves, with a balance of € 4.5 million, in relation to the adjustment of

the fair value on available-for-sale financial instruments and actuarial changes for the

severance indemnity;

• negatively, the loss for the year of € 128.3 million.

Additionally, note that the Shareholders’ Meeting held on 18 April 2013 resolved the following

allocation of the 2012 loss of € 169,275,077.92:

• use of Extraordinary Reserve for € 113,501,077.92;

• use of the reserve that resulted from the transfer in kind of GE Capital Services S.r.l. by GE

Capital Corporation Inc. for € 55,774,000.00.

REGULATORY CAPITAL AND CAPITAL REQUIREMENTS

Tier 1 Capital amounts to € 498.3 million, down 20.5% compared to 31 December 2012, primarily

attributable to the loss for the year of € 128.3 million.

Tier 2 Capital is also lower due to the figurative amortisation of € 40 million from the inclusion of the

subordinated loan for € 200 million expiring in 2016, only partially offset by the positive change in the

valuation reserves for available-for-sale financial instruments of € 1.9 million.

Against these changes, total regulatory capital amounts to € 648.8 million, down 20.5% compared to

the end of 2012.

With regard to capital requirements, note that risk assets decreased, despite the drop in regulatory

capital in all of its components, which helps maintain the consolidated coefficients at higher levels

than those calculated and required by Bank of Italy, following its Supervisory Review and Evaluation

Process (SREP) carried out in 2013, for the Bank as Parent Company, both in terms of the Common

Equity Tier 1 ratio (13.2%) and the Total Capital ratio (17.0%).

DIRECTORS’ REPORT ON OPERATIONS

28

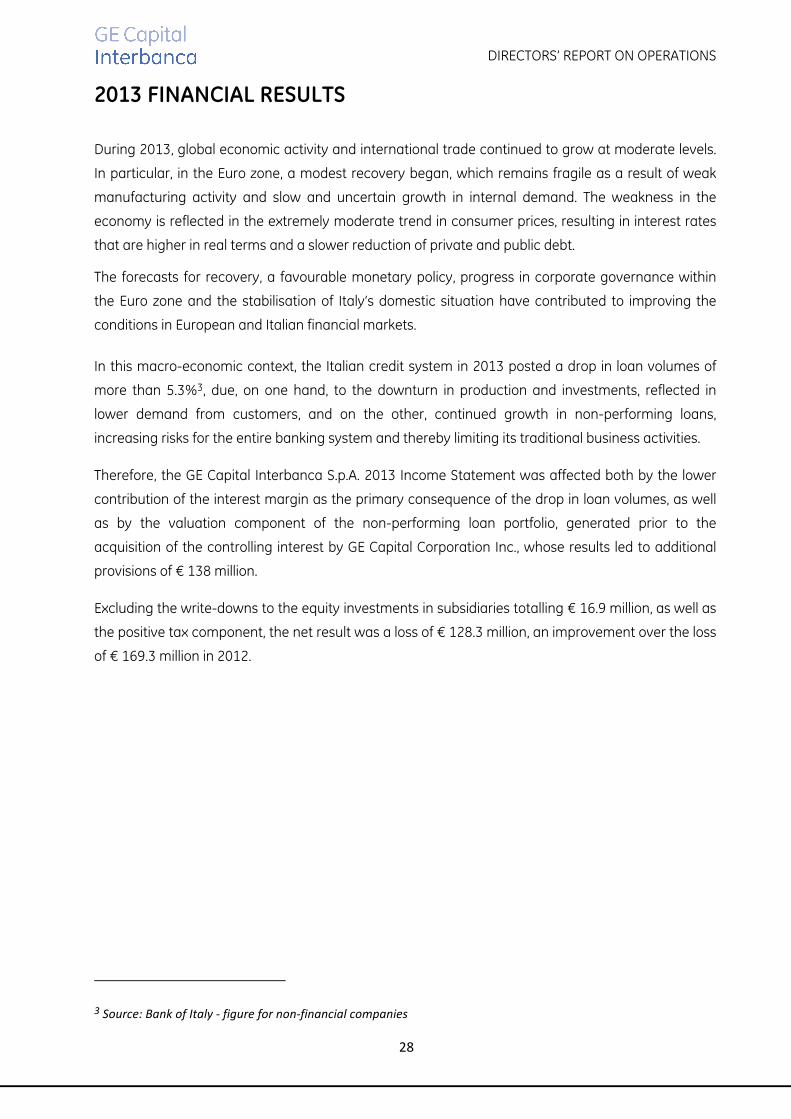

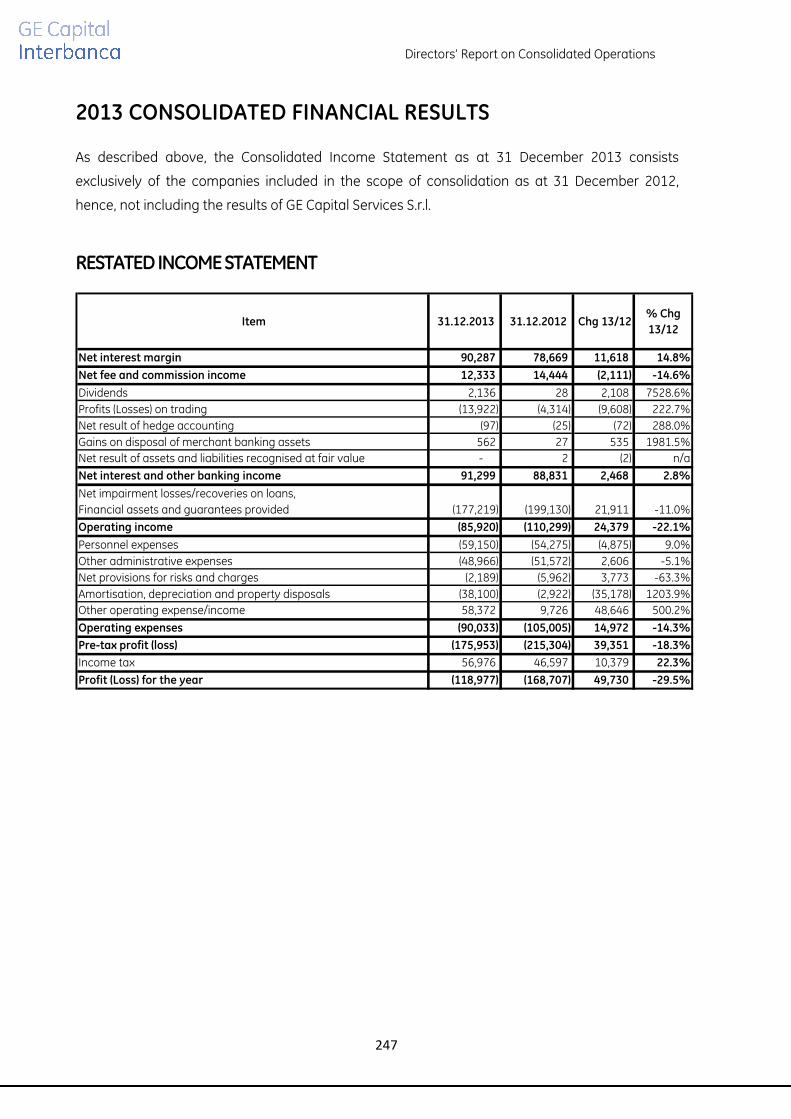

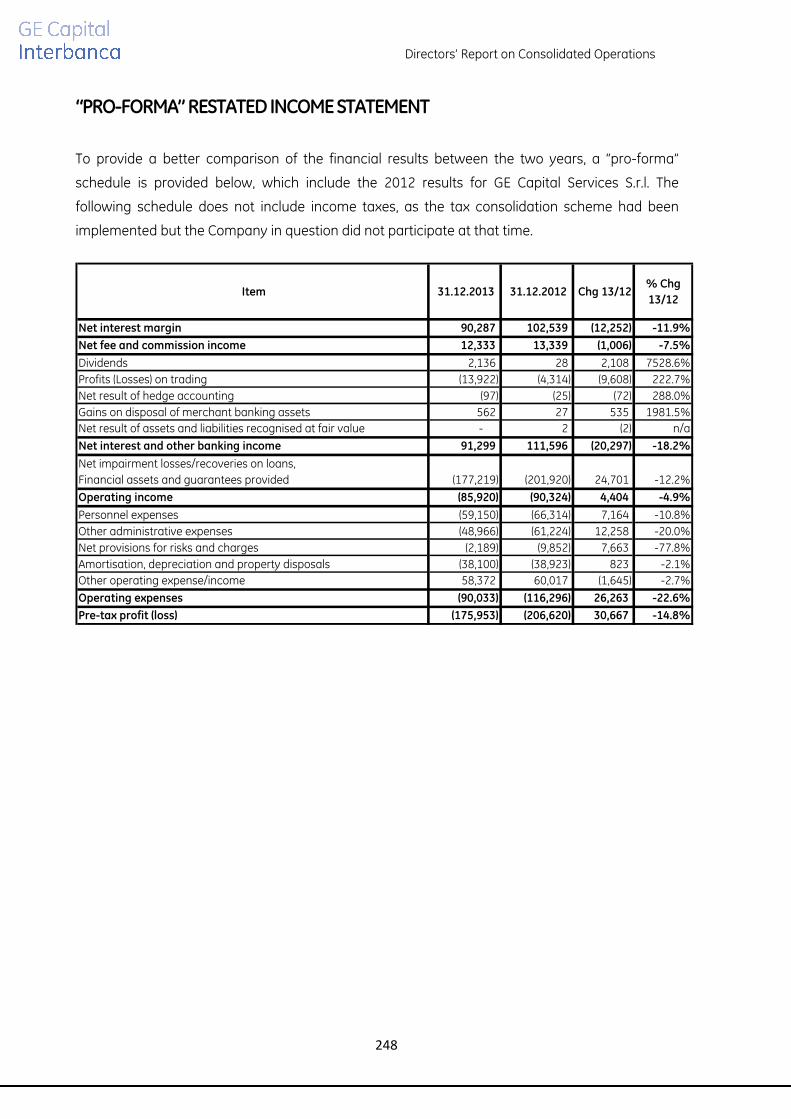

2013 FINANCIAL RESULTS

During 2013, global economic activity and international trade continued to grow at moderate levels.

In particular, in the Euro zone, a modest recovery began, which remains fragile as a result of weak

manufacturing activity and slow and uncertain growth in internal demand. The weakness in the

economy is reflected in the extremely moderate trend in consumer prices, resulting in interest rates

that are higher in real terms and a slower reduction of private and public debt.

The forecasts for recovery, a favourable monetary policy, progress in corporate governance within

the Euro zone and the stabilisation of Italy’s domestic situation have contributed to improving the

conditions in European and Italian financial markets.

In this macro-economic context, the Italian credit system in 2013 posted a drop in loan volumes of

more than 5.3%3, due, on one hand, to the downturn in production and investments, reflected in

lower demand from customers, and on the other, continued growth in non-performing loans,

increasing risks for the entire banking system and thereby limiting its traditional business activities.

Therefore, the GE Capital Interbanca S.p.A. 2013 Income Statement was affected both by the lower

contribution of the interest margin as the primary consequence of the drop in loan volumes, as well

as by the valuation component of the non-performing loan portfolio, generated prior to the

acquisition of the controlling interest by GE Capital Corporation Inc., whose results led to additional

provisions of € 138 million.

Excluding the write-downs to the equity investments in subsidiaries totalling € 16.9 million, as well as

the positive tax component, the net result was a loss of € 128.3 million, an improvement over the loss

of € 169.3 million in 2012.

3 Source: Bank of Italy - figure for non-financial companies

DIRECTORS’ REPORT ON OPERATIONS

29

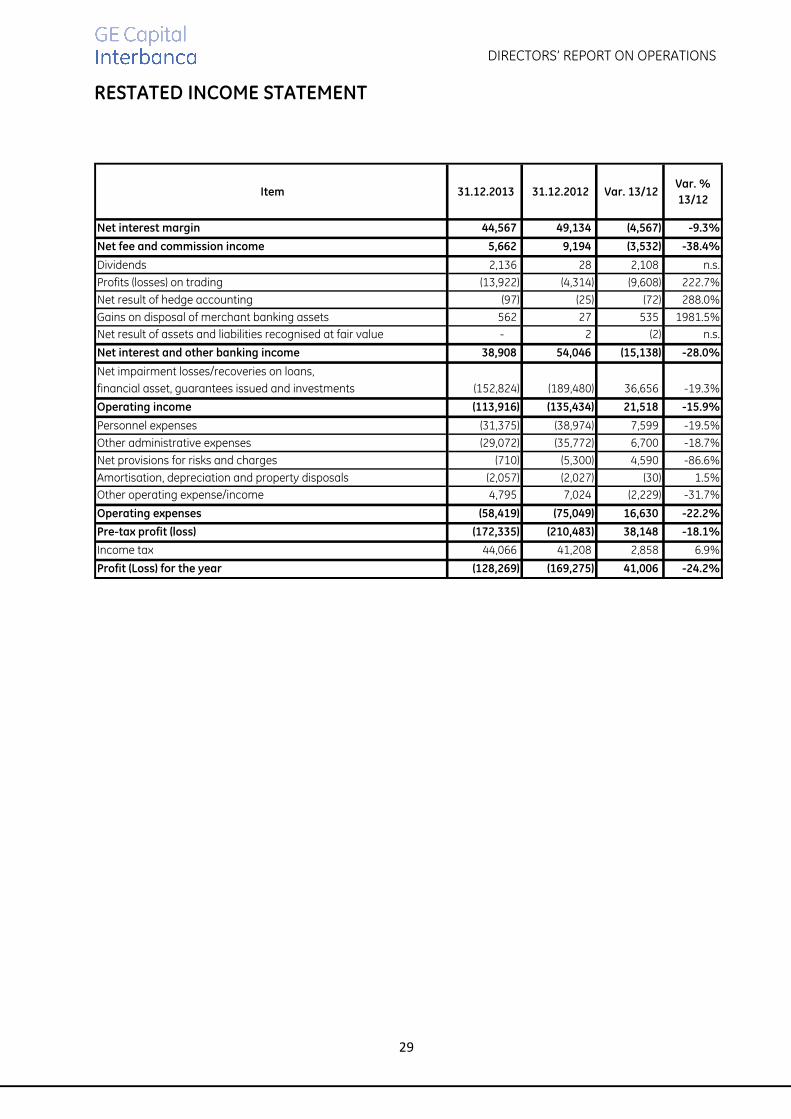

RESTATED INCOME STATEMENT

Item 31.12.2013 31.12.2012 Var. 13/12 Var. %

13/12

Net interest margin 44,567 49,134 (4,567) -9.3%

Net fee and commission income 5,662 9,194 (3,532) -38.4%

Dividends 2,136 28 2,108 n.s.

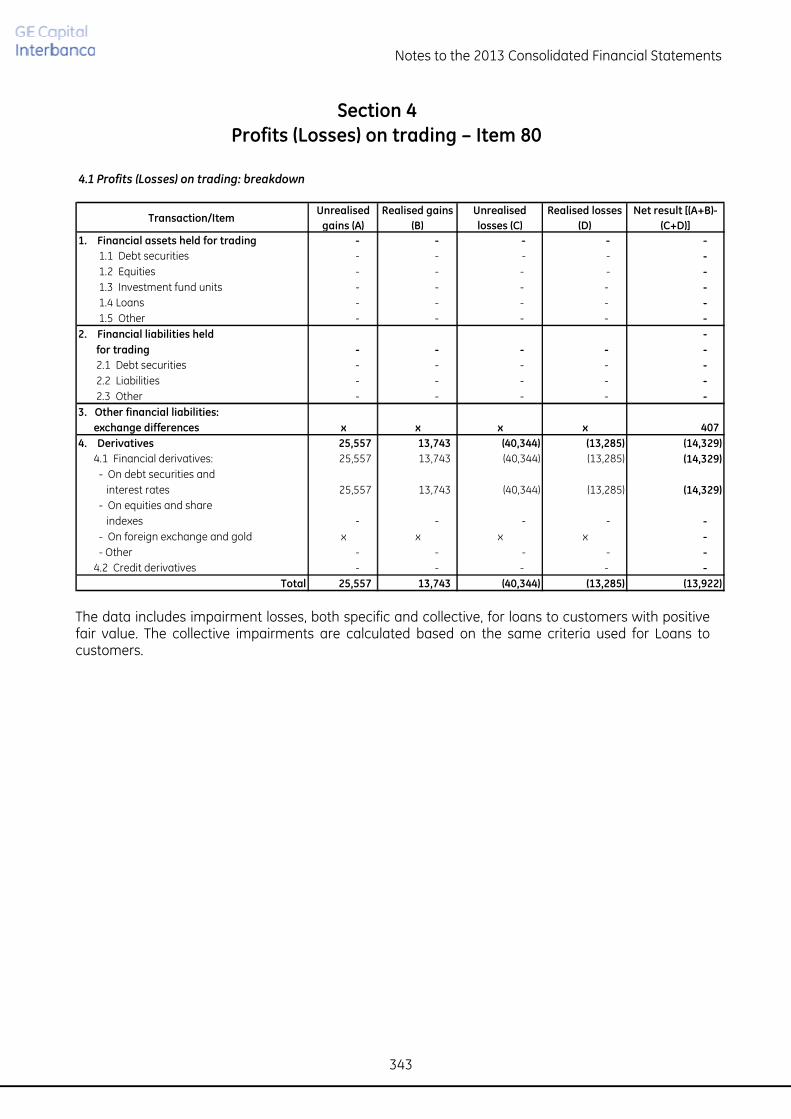

Profits (losses) on trading (13,922) (4,314) (9,608) 222.7%

Net result of hedge accounting (97) (25) (72) 288.0%

Gains on disposal of merchant banking assets 562 27 535 1981.5%

Net result of assets and liabilities recognised at fair value - 2 (2) n.s.

Net interest and other banking income 38,908 54,046 (15,138) -28.0%

Net impairment losses/recoveries on loans,

financial asset, guarantees issued and investments (152,824) (189,480) 36,656 -19.3%

Operating income (113,916) (135,434) 21,518 -15.9%

Personnel expenses (31,375) (38,974) 7,599 -19.5%

Other administrative expenses (29,072) (35,772) 6,700 -18.7%

Net provisions for risks and charges (710) (5,300) 4,590 -86.6%

Amortisation, depreciation and property disposals (2,057) (2,027) (30) 1.5%

Other operating expense/income 4,795 7,024 (2,229) -31.7%

Operating expenses (58,419) (75,049) 16,630 -22.2%

Pre-tax profit (loss) (172,335) (210,483) 38,148 -18.1%

Income tax 44,066 41,208 2,858 6.9%

Profit (Loss) for the year (128,269) (169,275) 41,006 -24.2%

DIRECTORS’ REPORT ON OPERATIONS

30

Net interest margin

The net contribution of the interest margin amounted to € 44.6 million, a 9.3% decrease from the

€ 49.1 million recorded in 2012.

The year-over-year change reflects the continued contraction of the portfolio for € 340 million in

average volumes, partially offset by the higher spread applied to new loans.

Net fee and commission income

The net result deriving from the provision of services amounts to € 5.7 million, compared to € 9.2

million in the prior year. This decrease is primarily due to non-recurring commissions recognised in

2012 for debt restructuring and settlements for € 1.5 million, as well as the lower contribution from

Corporate Finance activities and leader transactions.

The income component amounts to € 6.5 million and mainly refers to lending activities such as

leader transactions and agency fees (€ 1.8 million), debt revisions and settlements (€ 1.5 million),

guarantees issued (€ 1.6 million), and early repayments and settlements (€ 0.5 million).

The fees component of € 0.8 million is represented almost entirely by non-use commissions paid on

financing lines guaranteed by GE Capital Group.

Dividends

Dividends collected during the year of € 2.1 million are essentially attributable to the equity

investment in Dayco LCC.

Profits (losses) on trading

Trading consists of derivative transactions carried out for corporate customers until 2009, in order to

provide them with hedges for business operating risks, while the Bank carried out a counter-

transaction with leading financial institutions.

The period result revealed a negative balance of € 13.9 million, an increase from the figure as at 31

December 2012 and amounting to a loss of € 4.3 million; in particular, this figure was affected by the

analytic write-downs of certain impaired positions.

DIRECTORS’ REPORT ON OPERATIONS

31

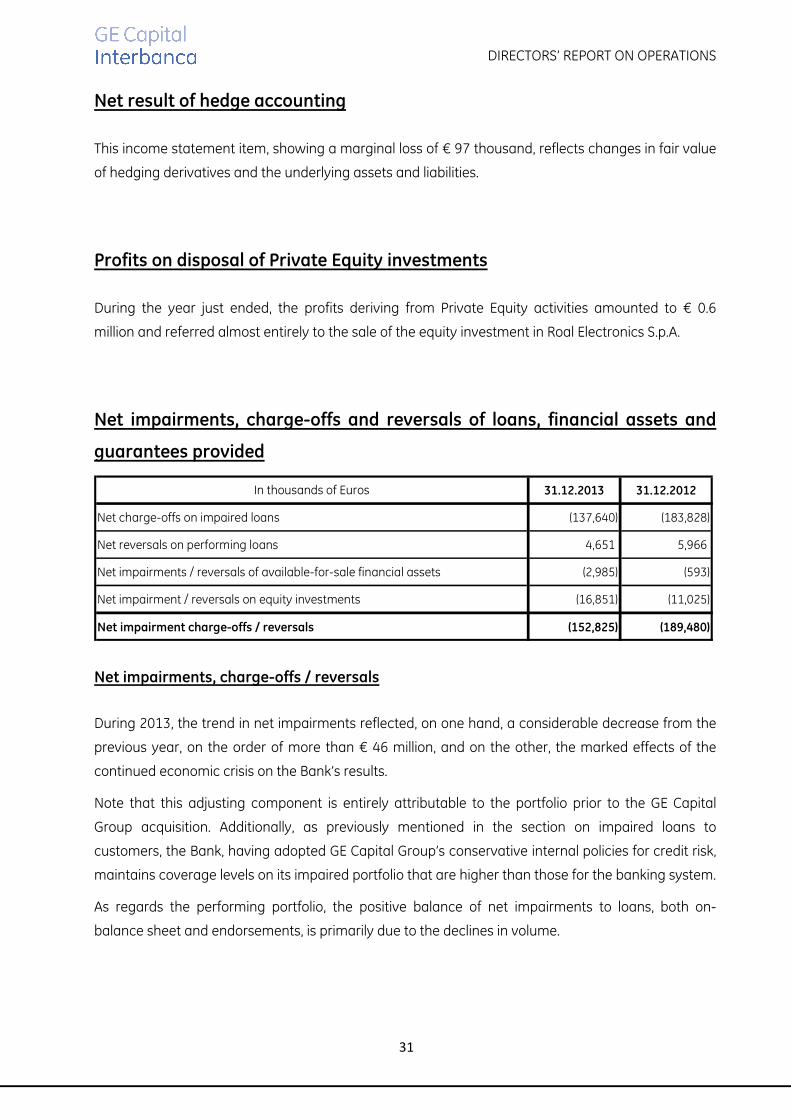

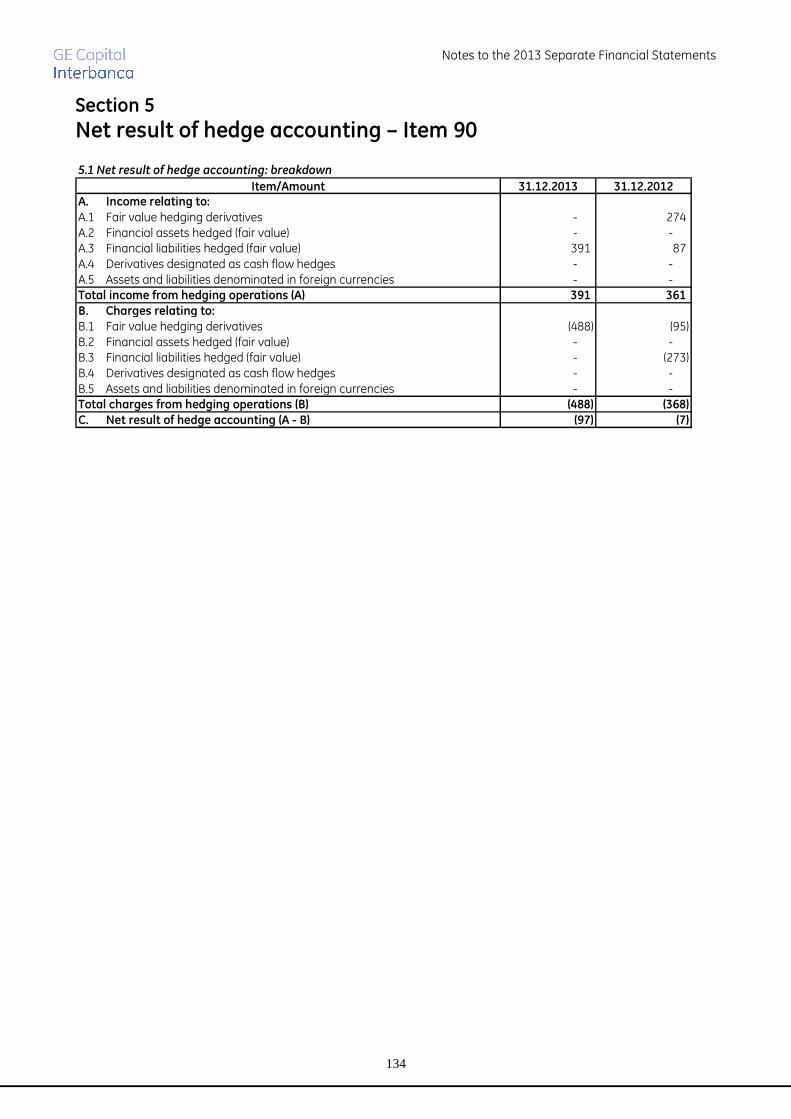

Net result of hedge accounting

This income statement item, showing a marginal loss of € 97 thousand, reflects changes in fair value

of hedging derivatives and the underlying assets and liabilities.

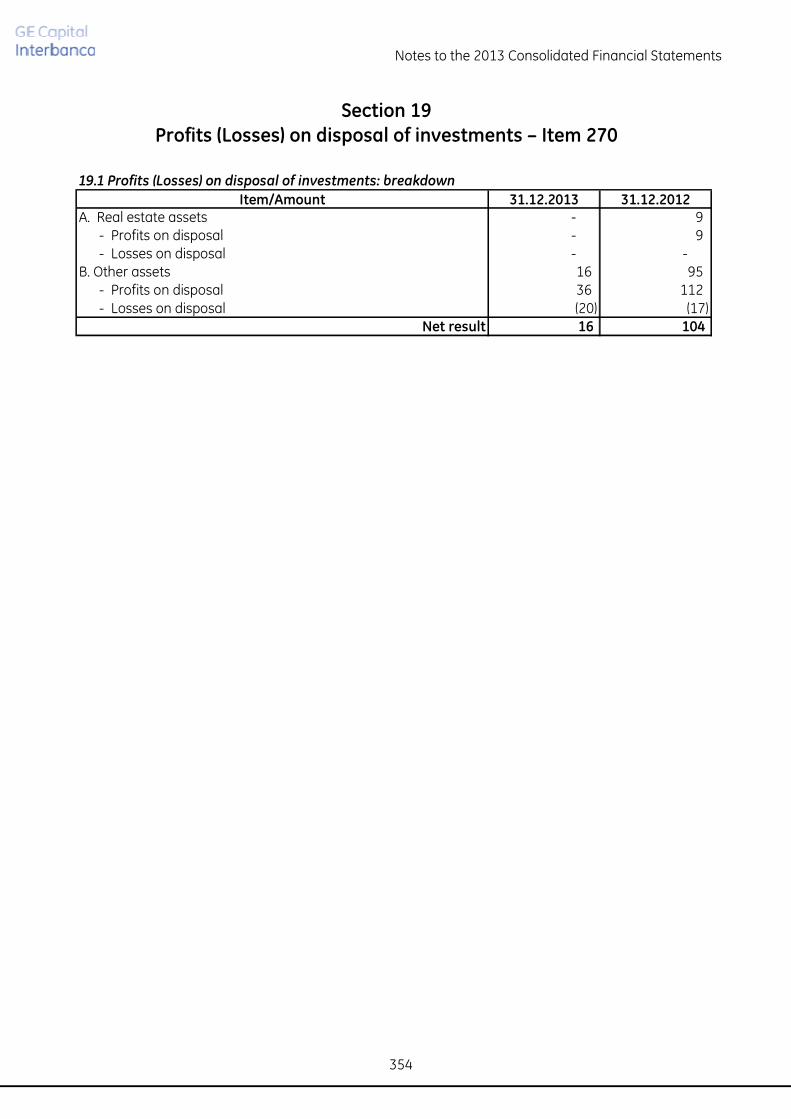

Profits on disposal of Private Equity investments

During the year just ended, the profits deriving from Private Equity activities amounted to € 0.6

million and referred almost entirely to the sale of the equity investment in Roal Electronics S.p.A.

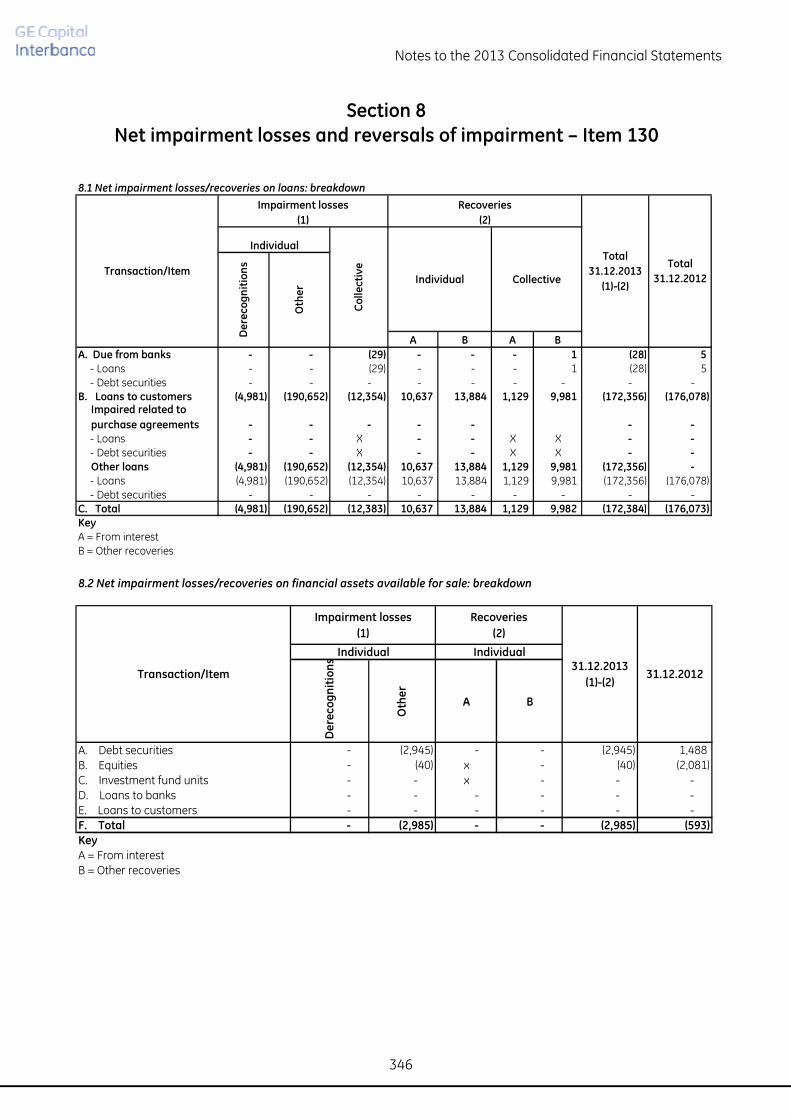

Net impairments, charge-offs and reversals of loans, financial assets and

guarantees provided

In thousands of Euros 31.12.2013 31.12.2012

Net charge-offs on impaired loans (137,640) (183,828)

Net reversals on performing loans 4,651 5,966

Net impairments / reversals of available-for-sale financial assets (2,985) (593)

Net impairment / reversals on equity investments (16,851) (11,025)

Net impairment charge-offs / reversals (152,825) (189,480)

Net impairments, charge-offs / reversals

During 2013, the trend in net impairments reflected, on one hand, a considerable decrease from the

previous year, on the order of more than € 46 million, and on the other, the marked effects of the

continued economic crisis on the Bank’s results.

Note that this adjusting component is entirely attributable to the portfolio prior to the GE Capital

Group acquisition. Additionally, as previously mentioned in the section on impaired loans to

customers, the Bank, having adopted GE Capital Group’s conservative internal policies for credit risk,

maintains coverage levels on its impaired portfolio that are higher than those for the banking system.

As regards the performing portfolio, the positive balance of net impairments to loans, both on-

balance sheet and endorsements, is primarily due to the declines in volume.

DIRECTORS’ REPORT ON OPERATIONS

32

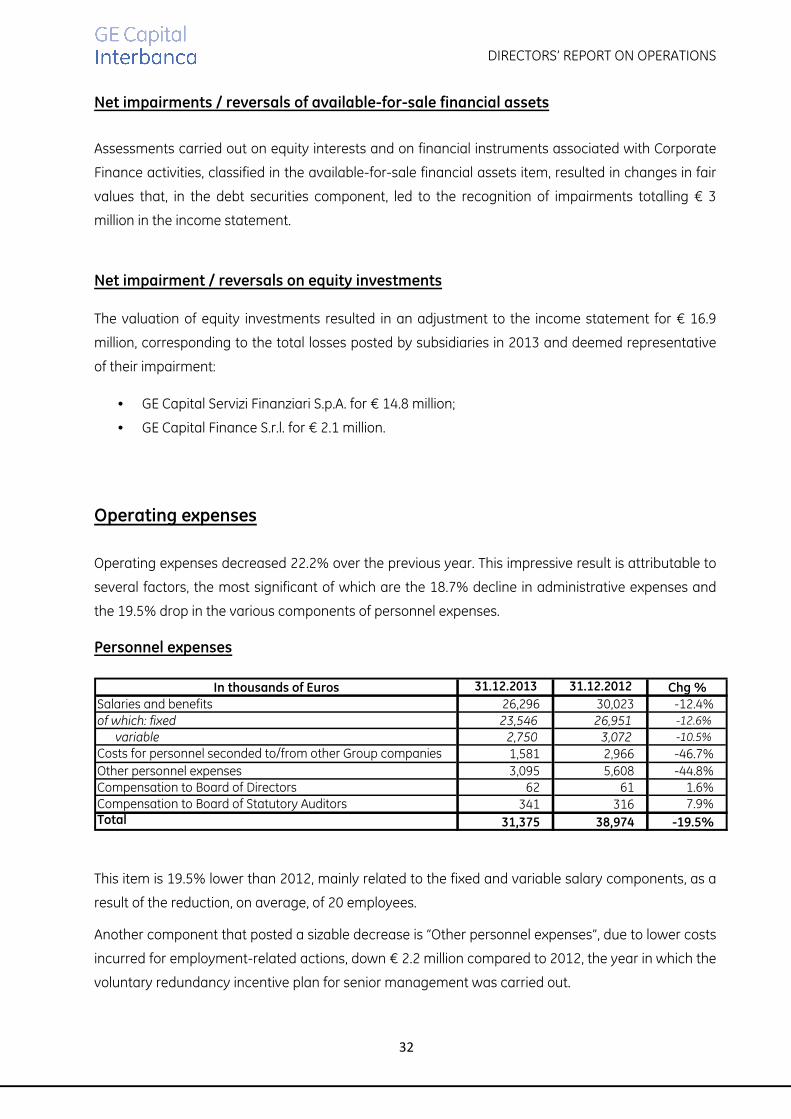

Net impairments / reversals of available-for-sale financial assets

Assessments carried out on equity interests and on financial instruments associated with Corporate

Finance activities, classified in the available-for-sale financial assets item, resulted in changes in fair

values that, in the debt securities component, led to the recognition of impairments totalling € 3

million in the income statement.

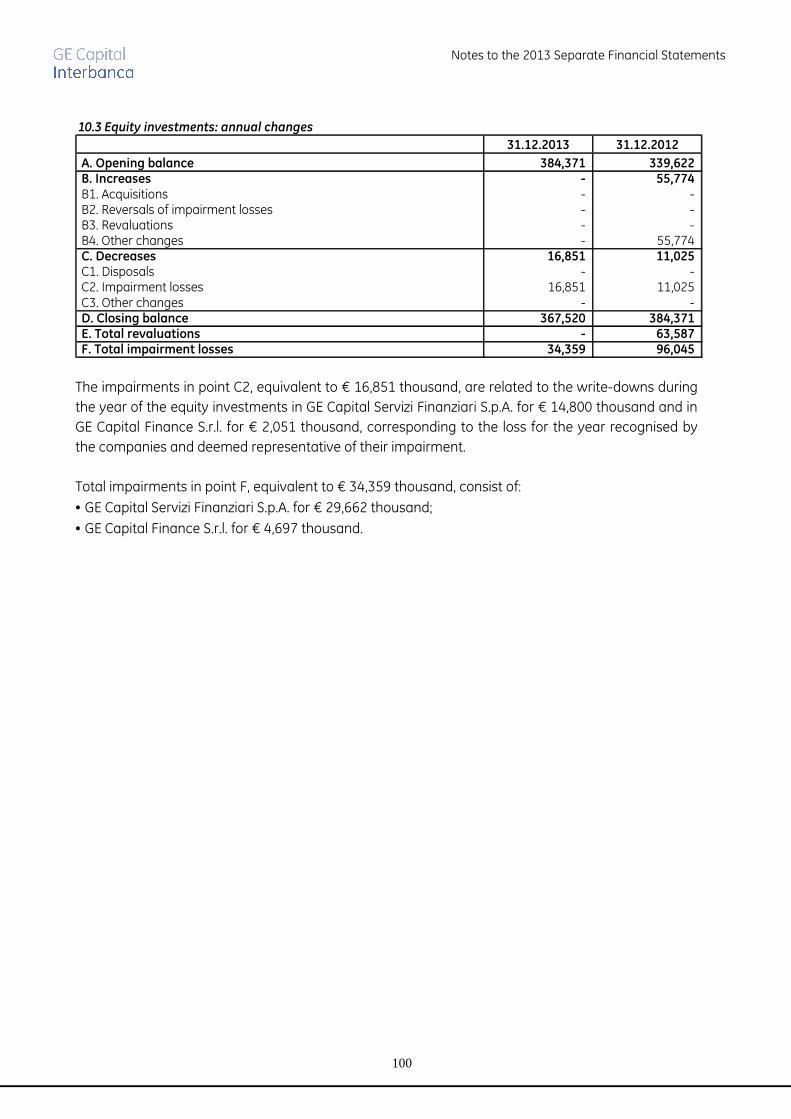

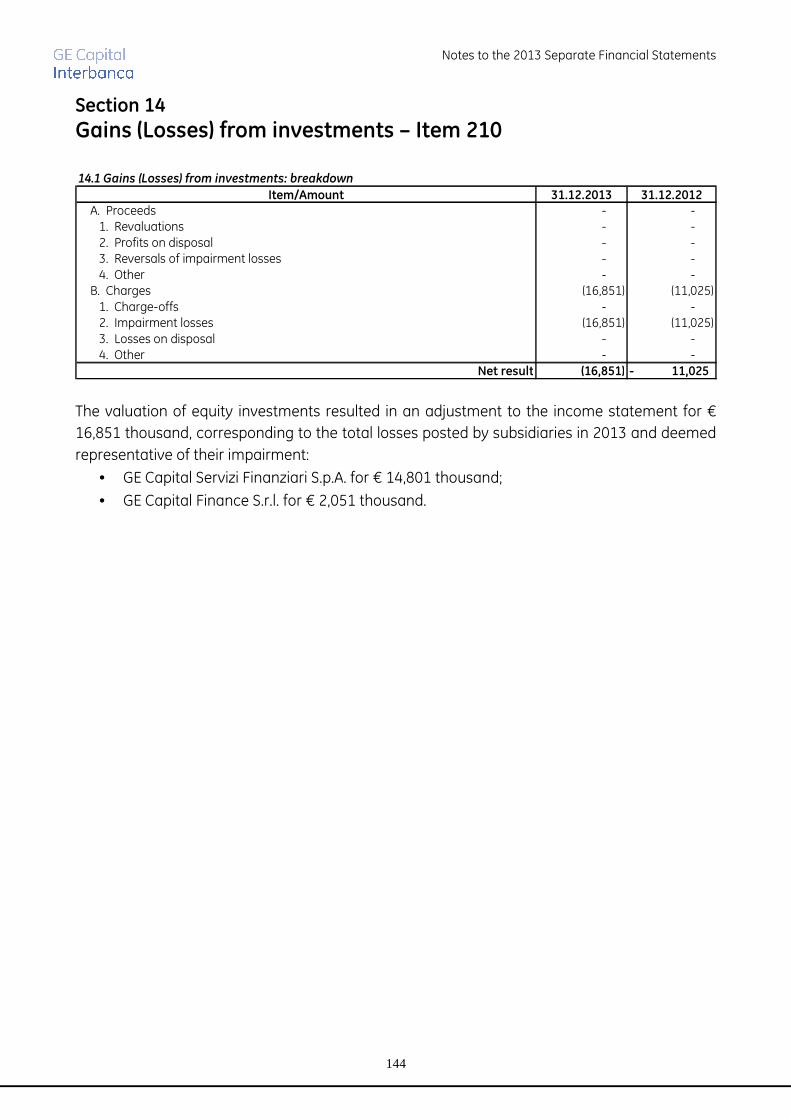

Net impairment / reversals on equity investments

The valuation of equity investments resulted in an adjustment to the income statement for € 16.9

million, corresponding to the total losses posted by subsidiaries in 2013 and deemed representative

of their impairment:

• GE Capital Servizi Finanziari S.p.A. for € 14.8 million;

• GE Capital Finance S.r.l. for € 2.1 million.

Operating expenses

Operating expenses decreased 22.2% over the previous year. This impressive result is attributable to

several factors, the most significant of which are the 18.7% decline in administrative expenses and

the 19.5% drop in the various components of personnel expenses.

Personnel expenses

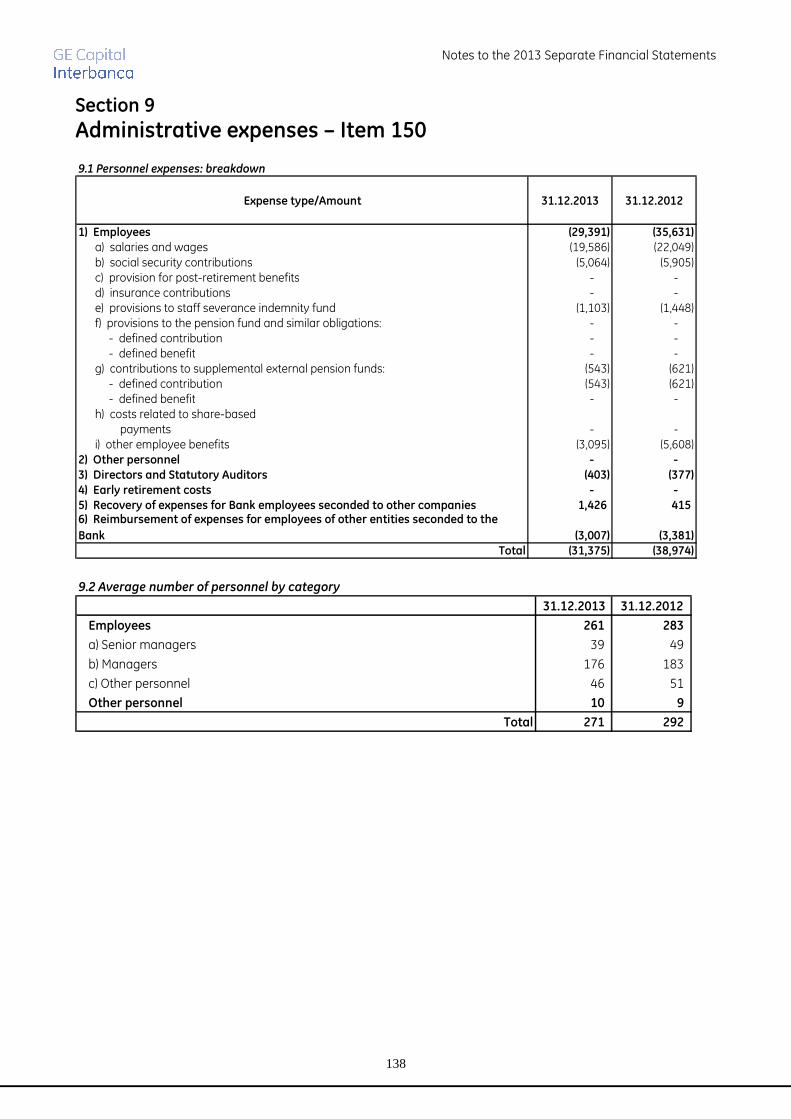

In thousands of Euros 31.12.2013 31.12.2012 Chg %

Salaries and benefits 26,296 30,023 -12.4%of which: fixed 23,546 26,951 -12.6%

variable 2,750 3,072 -10.5%

Costs for personnel seconded to/from other Group companies 1,581 2,966 -46.7%

Other personnel expenses 3,095 5,608 -44.8%Compensation to Board of Directors 62 61 1.6%Compensation to Board of Statutory Auditors 341 316 7.9%Total 31,375 38,974 -19.5%

This item is 19.5% lower than 2012, mainly related to the fixed and variable salary components, as a

result of the reduction, on average, of 20 employees.

Another component that posted a sizable decrease is “Other personnel expenses”, due to lower costs

incurred for employment-related actions, down € 2.2 million compared to 2012, the year in which the

voluntary redundancy incentive plan for senior management was carried out.

DIRECTORS’ REPORT ON OPERATIONS

33

Finally, note that additional charges of € 0.9 million were incurred compared to the prior year for

adjustments to the 2009 redundancy programme, for the extension of the inclusion in the Banking

Sector Solidarity Fund, pursuant to art. 24, para. 14 of Law 214/2011.

Other administrative expenses

In thousands of Euros 31.12.2013 31.12.2012 Chg %

Costs for services from Group companies 9,805 14,391 -31.9%

External consulting and professional services 6,012 7,727 -22.2%

Leasing of equipment and software 4,788 4,024 19.0%

Outsourcing 2,687 2,800 -4.0%

Rental and office expenses 1,373 1,514 -9.3%

Indirect taxes and duties 1,296 1,223 6.0%

Information expenses 981 985 -0.4%

Maintenance expenses 467 1,005 -53.5%

Advertising and other promotional expenses 298 474 -37.1%

Other expenses 1,365 1,629 -16.2%

Total 29,072 35,772 -18.7%

“Other administrative expenses” posted a marked reduction, down 18.7% from 2012.

The expenditure components that had the most influence on the drop in administrative expenses are

those relating to the Master Service Agreement entered into with the General Electric Group and also

includes royalties for use of the GE name and brand, which together decreased € 4.6 million, following

both a redefinition of the contractual base for the royalties, as well as a different division of costs in

the Master Service Agreement on local platforms.

In addition, the decrease in this item is the result of the first year under the costs savings project,

which seeks to reduce costs by renegotiating the existing service contracts and from a general cost

containment policy.

The growth in the item “Leasing of equipment and software” of € 0.8 million is due to the IT Data

Centre Consolidation project, whose objective is to completely reorganise the technology

infrastructure (servers, communication lines, and logistics) within the Group.

DIRECTORS’ REPORT ON OPERATIONS

34

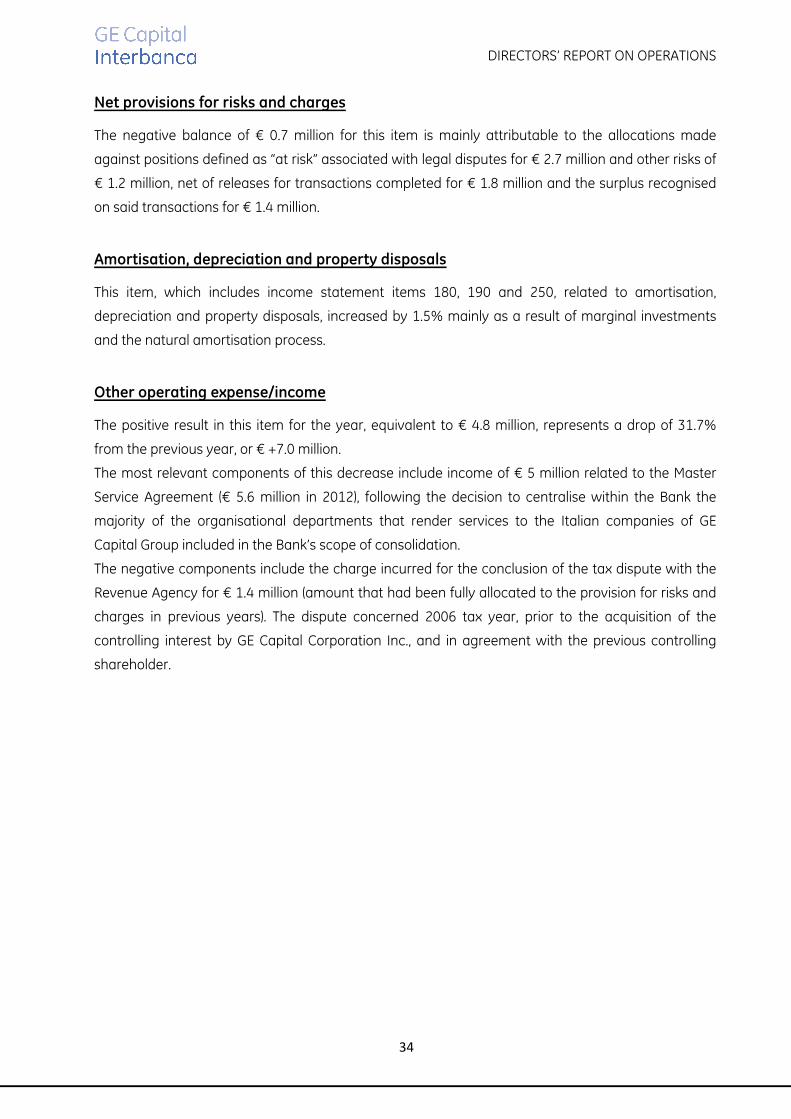

Net provisions for risks and charges

The negative balance of € 0.7 million for this item is mainly attributable to the allocations made

against positions defined as “at risk” associated with legal disputes for € 2.7 million and other risks of

€ 1.2 million, net of releases for transactions completed for € 1.8 million and the surplus recognised

on said transactions for € 1.4 million.

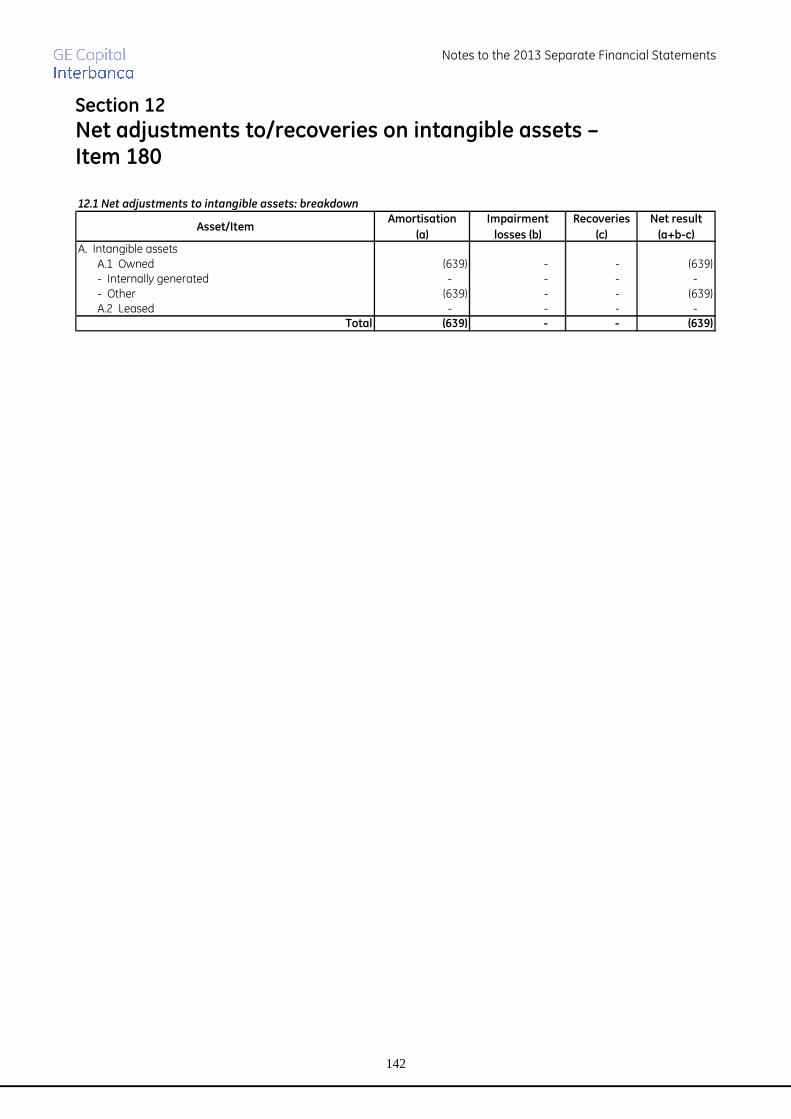

Amortisation, depreciation and property disposals

This item, which includes income statement items 180, 190 and 250, related to amortisation,

depreciation and property disposals, increased by 1.5% mainly as a result of marginal investments

and the natural amortisation process.

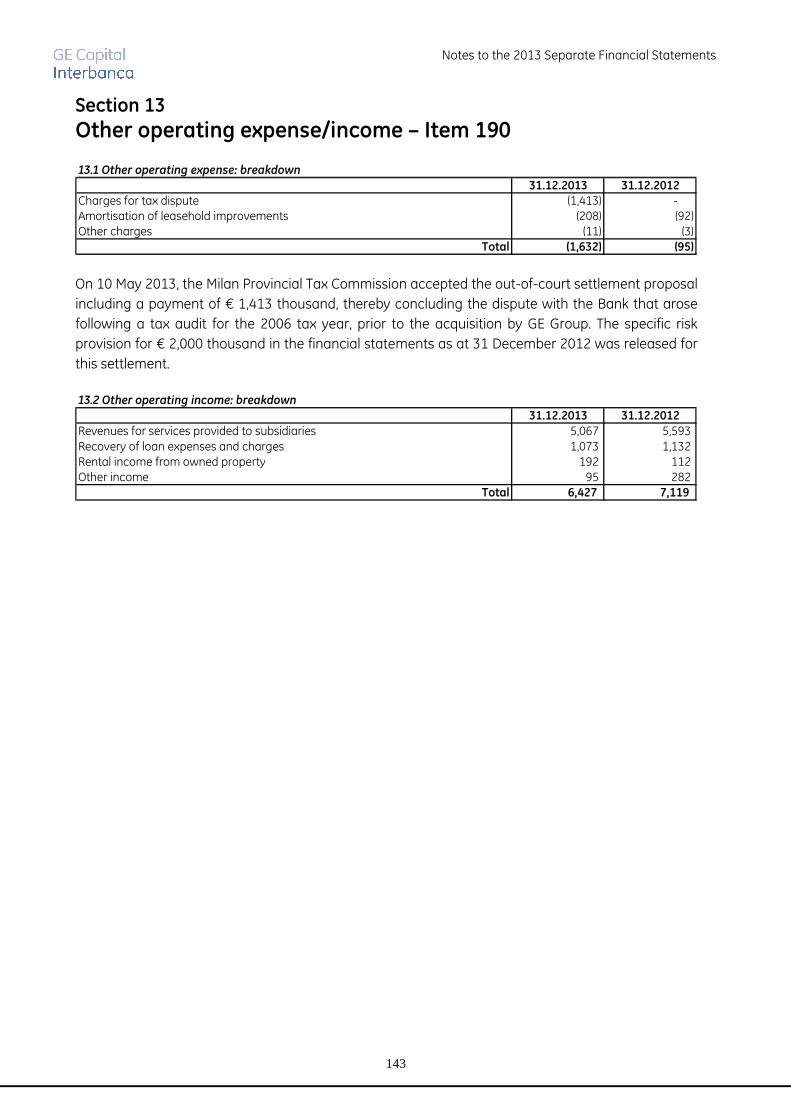

Other operating expense/income

The positive result in this item for the year, equivalent to € 4.8 million, represents a drop of 31.7%

from the previous year, or € +7.0 million.

The most relevant components of this decrease include income of € 5 million related to the Master

Service Agreement (€ 5.6 million in 2012), following the decision to centralise within the Bank the

majority of the organisational departments that render services to the Italian companies of GE

Capital Group included in the Bank’s scope of consolidation.

The negative components include the charge incurred for the conclusion of the tax dispute with the

Revenue Agency for € 1.4 million (amount that had been fully allocated to the provision for risks and

charges in previous years). The dispute concerned 2006 tax year, prior to the acquisition of the

controlling interest by GE Capital Corporation Inc., and in agreement with the previous controlling

shareholder.

DIRECTORS’ REPORT ON OPERATIONS

35

Income tax and net profit (loss) for the period

The pre-tax result was a loss of € 172.3 million, an improvement over the pre-tax loss of € 210.5

million in the previous year.

The income tax component was positive for € 44.1 million following tax provisions for the option of

converting deferred tax assets for loan write-downs into tax credits, as well as participation in the tax

consolidation with specific agreements among the companies belonging to the Bank’s statutory

scope of consolidation.

Specifically, the Bank:

• Recognised the amount of the deferred tax assets associated with write-downs and

impairments on loans deductible over 5 years, net of uses for releases of impairments on loans

deductible over 18 years, allocated in previous years and converted into tax credits, increasing

the balance as at 31 December 2012 from € 195.6 million to € 199.0 million; with the approval

of the 2013 Financial Statements and, at the same time, recognising a statutory loss, it will be

possible to continue with the conversion of deferred tax assets into tax credits for € 40.5

million;

• With the approval of the 2012 Financial Statements, converted into tax credits the deferred tax

assets for loan impairments deductible over 18 years, recognised as at 31 December 2012 for

€ 39.5 million, in relation to the 2012 Italian statutory loss;

• During September 2013, converted into tax credits the deferred tax assets for loan

impairments deductible over 18 years, recognised as at 31 December 2012 for € 10.9 million,

in relation to the 2012 Italian tax loss;

• Did not recognise deferred tax assets on previous losses and on estimated losses for the year,

or on other temporary differences, of a lower amount, for a total of € 50.3 million, as,

consistent with IAS 12, general market conditions give rise to substantial uncertainty on the

timing and amount of future taxable profit that the Group may generate.

Net of income taxes, the result for the year was a loss of € 128.3 million, a 24.2% improvement over

the € 169.3 million loss suffered in 2012.

DIRECTORS’ REPORT ON OPERATIONS

36

ADDITIONAL INFORMATION

RESEARCH AND DEVELOPMENT

The Bank does not perform any research and development activities.

INVESTMENTS

Information Technology

During 2013, information technology investments were focused on completing the modernisation

and simplification of the infrastructure:

• The Data Centre Consolidation project was completed with the closing of 5 Data Centres and

the concentration of production equipment in a single site in Milan, which meets the

conservative security policies of GE Capital Group;

• The Disaster Recovery environment was renewed to ensure operations continuity consistent

with the business requirements;

• The summary systems used for Supervisory and Anti-Money Laundering reporting were

updated for new regulations;

• A system for producing reports required by the Federal Reserve was developed and

consolidated.

Tangible assets

During 2013, projects to restructure office space were completed, improving operating efficiency; in

particular:

• Extraordinary maintenance was performed on the Bank’s premises in Corso Venezia 56 and

Via Borghetto 5 in Milan. The work on the systems mainly involved extraordinary

maintenance on lifts, installing a system to automatically return the lift to the ground floor in

an emergency, heating and air-conditioning systems and emergency lighting systems;

• Rental contracts were cancelled on offices used for hard copy archives and archiving

services were outsourced to an external supplier;

• The Rome branch in Via Principessa Clotilde 7 was relocated to Via F. Cesi 72, bringing about

a reduction in operating costs and a better use of office space.

DIRECTORS’ REPORT ON OPERATIONS

37

HUMAN RESOURCES

Breakdown of Personnel

Of the 256 employees as at 31 December 2013 (286 in 2012), 17 had part-time contracts (18 in 2012).

3 employees are working for other General Electric Group companies, while 14 employees of other

subsidiaries of the Bank are working for the Bank.

Solidarity Fund

Following the recognition by INPS of the Bank’s compliance with requirements for accessing the

safeguard measures referred to in art. 24, para. 14 of Law no. 214/2011, during 2013, 16 employees

terminated their employment relationship with the Bank to have access to the extraordinary benefits

of the Solidarity Fund, as they were already participating in the Agreement of 14 January 2010 and

indicated as participants in the Agreement of 22 December 2011.

The financial impact of access to the Solidarity Fund for these 16 employees had already been

allocated in previous years; the cost difference of € 0.9 million was allocated during the year, to

extend participation in the Solidarity Fund for eligible employees until they reach 62 years of age.

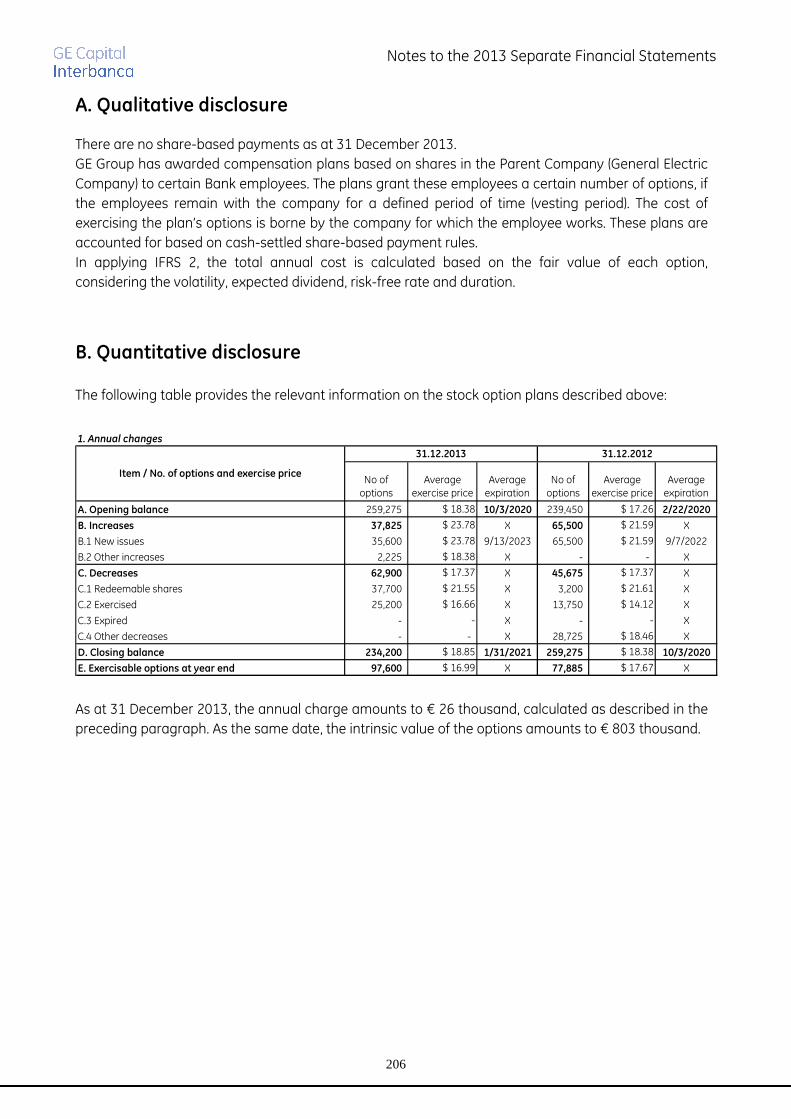

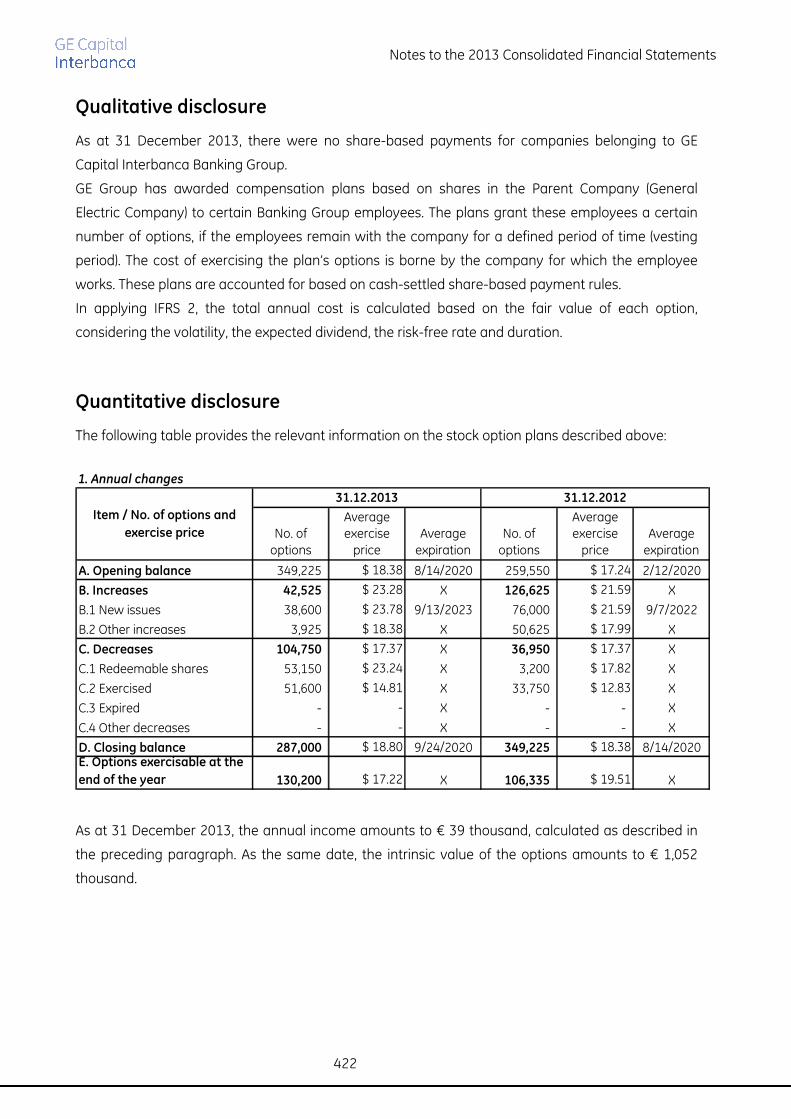

Stock options

General Electric Company granted options for its stock to certain Bank employees. In the Notes to the

Financial Statements - Part A Accounting Policies - the accounting standards adopted in applying

IFRS 2 are explained. Under the section “Share-based payments”, the quantitative and qualitative

features of the plans are detailed.

“HealthAhead” Programme

HealthAhead is a General Electric Group global initiative with the objective of helping employees and

their families develop healthy lifestyles and is part of the broader General Electric Group programme,

"Healthymagination", which reflects the Group’s commitment to develop a culture that promotes

health through internal initiatives and investments.

The programme includes the creation of the internal Wellness Committee that organises activities

with health education content and makes tools and structures available to assist in realising these

activities. The Italian HealthAhead team organised activities in 2013 around the following topics:

• Physical activities - fitness classes at the office sites and outdoor running groups were

organised throughout the year; in addition, agreements were made with gyms near the

offices;

• Nutrition - meetings on a healthy diet and cooking classes for children were organised to

promote healthy eating habits;

DIRECTORS’ REPORT ON OPERATIONS

38

• Tobacco – the smoking prohibition has been confirmed in all buildings and external areas;

Professional psychological support was offer for smokers who have initiated a cessation

programme and reflexology sessions were offered to treat nicotine addition;

• Education and prevention - various sessions on prevention and body composition analysis

were offered:

• Stress management - a programme on stress management techniques was organised.

GENERAL REGULATION

The Bank has developed a General Regulation.

During 2013, the Board of Directors of GE Capital Interbanca S.p.A. resolved actions to simplify the

organisational structure, primarily through:

• Reorganisation of the Commercial Department activities, specifically:

- The separation of the Partnership and Commercial Excellence activities, which was

assigned to the primary Strategic Marketing Department;

- The separation of Insurance activities, which will be managed directly by the individual

Group platforms.

• Rationalisation of the activities of the Communications and Business Development

Departments, centralised under the responsibility of the Strategic Marketing Department.

Moreover, it was resolved to extend the participation of the Manager of Compliance and Anti-money

Laundering Department (a control department reporting to the Board of Directors) to meetings of the

Management Committee.

PRIVACY CODE

In accordance with Legislative Decree 196/2003 on personal data protection, the Bank upgraded its

Security Planning Document on 31 March 2013, for the technical regulations in Attachment B of

Legislative Decree no. 196 of 30 June 2003, “Privacy Code”, although rescinded by Conversion Law

no. 35 of 4 April 2012 governing “Urgent regulations for simplification and growth”.

DIRECTORS’ REPORT ON OPERATIONS

39

CORPORATE GOVERNANCE

The Bank’s overall corporate governance framework, intended as the system of rules and procedures

to which corporate bodies refer to guide their behaviour and fulfil their responsibilities, was defined in

consideration of governing legislation as well as regulations prescribed by Bank of Italy.

The Bank and all of the companies in the Banking Group use the “traditional” model that, in applying

the principle of organisational independence and proportionality, the Bank deems the most suitable

model to ensure management independence, operating efficiency and effectiveness of controls to

achieve sound and prudent management, allowing a clear distinction of roles and responsibilities, an

appropriate division of powers and balanced composition of bodies.

Corporate bodies

Corporate functions are delegated, according to their respective competencies, to the following

bodies: (i) Shareholders’ Meeting, (ii) Board of Directors, (iii) Chairman, (iv) Chief Executive Officer, (v)

General Manager and (vi) Board of Statutory Auditors.

The Shareholders’ Meeting may be held either in ordinary or extraordinary session, and must be

convened in ordinary session at least once per year to resolve on issues reserved to its competence

by law and in extraordinary session to resolve on issues reserved to its competence by law.

Participation and representation at Shareholders’ Meeting are governed by law; for the valid

constitution of the Shareholders’ Meeting, both in ordinary and extraordinary session, the quorum

requirements envisaged by governing regulation are applied. The Shareholders’ Meeting, both in

ordinary and extraordinary session, resolves with the voting quorum determined by governing

regulation. Participation and representation at Shareholders’ Meeting are governed by law.

The Board of Directors has the exclusive responsibility, which cannot be delegated, for the strategic

supervision and management of the Bank, which it exercises through the Chief Executive Officer. As

at 31 December 2013, the Bank’s Board of Directors consists of 7 Directors. The mandate of the

current Board of Directors will expire on the date of the Shareholders’ Meeting convened to approve

the 2014 Financial Statements.

The members of the Board of Directors must meet the requirements established by governing

legislation and regulations. Specifically, the Independent Directors must meet the independence

requirements set forth in art. 2399 of the Italian Civil Code.

The Board of Directors elects a Chairman from its members. Its meetings are normally held once per

month and any time the Chairman deems it necessary or if there is a reasoned request, indicating

the issues to be discussed, presented by the Chief Executive Officer or at least one third of the

members of the Board of Directors. For the Board of Directors’ meeting to be considered valid, a

majority of members in office must be present. The Board’s resolutions are made through an

absolute majority of the participants. The Board of Directors may establish an internal audit

committee, an investments committee and a compensation committee.

DIRECTORS’ REPORT ON OPERATIONS

40

The Chairman oversees the Bank’s performance and the effective functioning of the corporate

governance systems, ensuring balance of powers with respect to the Chief Executive Officer and

other Directors. In addition, the Chairman is the legal representative of the Company before third

parties and judicial authorities.

The Chief Executive Officer oversees the business management as part of the powers attributed to

him/her and according to the general guidelines established by the Board of Directors.

The General Manager implements the Board of Directors’ resolutions.

In the Bank, the roles of Chief Executive Officer and General Manager are performed by the same

individual.

The Board of Statutory Auditors consists of 3 Standing Auditors and 2 Alternate Auditors with the

powers assigned by law.

The Auditors must meet the requirements established by governing legislation and regulations. They

remain in office for 3 years and their term expires on the date of the Shareholders’ Meeting convened

to approve the financial statements for the third year of office. The Auditors are eligible for re-

election. The Board of Statutory Auditors meets as necessary, and normally, at least every 90 days.

Resolutions are taken with the presence and favourable vote of the majority of members.

The accounting audit is performed by an Accounting Audit Firm that meets the requirements and is

appointed according to law. As at 31 December 2013, Accounting Audit Firm assigned the

accounting audit is KPMG S.p.A.

***

On 19 December 2013, the Bank’s Board of Directors resolved to approve the establishment of the

Compensation Committee, setting the number of members at 3.

The Committee was assigned the task of making proposals, consulting, and monitoring issues related

to compensation and internal policies. The same Board of Directors has approved the relative

regulation for its functioning and appointed as Committee members: (i) Richard Laxer, Chairman of

the Board of Directors, who was also appointed Chairman of the Committee (ii) Mario Garraffo and (iii)

Enrico Fagioli Marzocchi, both Independent Directors of the Bank.

DIRECTORS’ REPORT ON OPERATIONS

41

Corporate governance, qualitative/quantitative composition of the Board of

Directors and the interlocking prohibition

With the favourable opinion of the Board of Statutory Auditors and the Board of Directors resolution

of 25 June 2009, GE Capital Interbanca S.p.A. adopted the Corporate Governance Project containing

the organisational and corporate governance solutions most appropriate for its structure in

compliance with the "oversight provisions for the organisation and corporate governance of banks”,

pursuant to Bank of Italy Communications no. 264010 of 4 March 2008 and no. 213623 of 27

February 2009.

As such, and in consideration of:

• Effective 31 December 2010, the “GE Capital Interbanca Banking Group” was established,

enrolled in the Banking Group register pursuant to art. 64 of Legislative Decree no. 385/1993;

• On 11 January 2012, Bank of Italy issued a measure governing “the application of supervisory

regulations regarding corporate governance and organisation of banks", which amended the

Bank of Italy Communications no. 264010 of 4 March 2008 and no. 213623 of 27 February

2009;

• On 31 January 2012, the Bank’s Shareholders’ Meeting approved the new Articles of

Association that include the new name of the Bank "GE Capital Interbanca S.p.A” replacing

“GE Capital S.p.A.” and the description of the circumstances under which the Bank is “subject

to management and coordination as defined by art. 2497 bis of the Italian Civil Code, of GE

Capital Corporation, with registered office in the United States of America”,

it was deemed appropriate to update the Corporate Governance Project.

For this purpose, on 22 March 2012, the Bank’s Board of Directors resolved to approve the changes

to the Project. The changes include the introduction of set criteria inherent in the

qualitative/quantitative composition of the Board of Directors that is considered appropriate and

suitable to ensure the best structure for the Bank’s Board of Directors given its complexities and

strategies, as well as those of the Banking Group.

In applying said criteria, the Board of Directors, in its meeting of 22 March 2012, also resolved the

correlation between the qualitative/quantitative composition of the Board of Directors established as

part of the Project, as modified and supplemented, and the composition of the Board of Directors as

at said date.

In December 2013, Bank of Italy issued a consultation document containing “Oversight provisions for

the organisation and corporate governance of banks”. In this document, certain amendments to the

aforementioned oversight provisions issued by Bank of Italy in 2008 were made available for public

consultation. The objective of these amendments was to implement changes introduced by Directive

2013/36/EU (so-called “CRD IV”), whose implementation deadline was set for 31 December 2013, and

to update the regulation in light of application experience. As part of the imminent effective date of

DIRECTORS’ REPORT ON OPERATIONS

42

the aforementioned new “Oversight provisions for the organisation and corporate governance of

banks”, the Corporate Governance Project was subjected to an appropriate revision.

On 23 May 2012, the Bank’s Shareholders’ Meeting, having acknowledged the expiry of the term in

office of members of the Board of Directors and the Board of Statutory Auditors pursuant to art. 2383

of the Italian Civil Code, resolved to appoint for 2012, 2013 and 2014, with expiry on the date of the

approval of the financial statements as at 31 December 2014, (i) a Board of Directors made up of six

members: Richard Alan Laxer (Chairman), Giuseppe Recchi, Paolo Braghieri, Patricia Marie Halliday,

Robert Charles Green and Mario Garraffo (Independent Director) and (ii) a Board of Statutory Auditors

consisting of: Paolo Andrea Colombo (Chairman), Marco Giorgino, Alberto Dalla Libera and as

Alternate Auditors, Piera Vitali and Guido Sazbon.

Following this appointment, on 24 May 2012 the Board of Directors of GE Capital Interbanca S.p.A.

resolved the correlation between the qualitative/quantitative composition as defined in the Project

and the composition of the Board of Directors resulting from the appointment process.

In its meeting of 24 May 2012, the Board verified that the individual members met the requirements

of reputation, professionalism, and independence by completing the necessary valuations, upon first

application, pursuant to art. 36 of Legislative Decree no. 201/2011 converted into Law no. 214/2011

regarding “protecting the intersection of competition and personal participation in credit and

financial markets”.

In its meeting of 25 July 2013, following the appointment by co-optation of Director Todd Lamar

Smith, the Bank’s Board of Directors verified the consistency between the qualitative/quantitative

composition requirements of the Project and the composition resulting from the appointment

process. Furthermore, the Board verified that the new Director (i) met the reputation and

professionalism requirements and (ii) did not have any situations that would be in contrast with the

provisions referred to in the aforementioned art. 36 of Legislative Decree no. 201/201 converted into

Law no. 214/2011.

The Bank’s Board of Directors resolved in its meeting of 17 December 2013 to: (i) increase the number

of Board members from 6 to 7, (ii) confirm Director Todd Lamar Smith in office and (iii) appoint Enrico

Maria Luigi Fagioli Marzocchi as Independent Director.

The verification that requirements were met (including independence requirements) were performed

by the Board of Directors on 19 December 2013, following the appointment of Enrico Maria Luigi

Fagioli Marzocchi as Independent Director.

That said, as at 31 December 2013, the Bank’s Board of Directors consists of the following 7

Directors: Richard Alan Laxer (Chairman), Giuseppe Recchi, Paolo Braghieri (Chief Executive Officer

and General Manager), Patricia Marie Halliday, Todd Lamar Smith, Mario Garraffo (Independent

Director) and Enrico Maria Luigi Fagioli Marzocchi (Independent Director).

DIRECTORS’ REPORT ON OPERATIONS

43

Related parties

On 28 June 2012, the Board of Directors resolved the approval of the Regulation governing

transactions with related parties and associated parties of individual companies belonging to the

Banking Group and the Banking Group itself, having received the positive opinions of the

Independent Director Mario Garraffo and the Board of Statutory Auditors and in compliance with

applicable regulations, particularly Bank of Italy Circular no. 263/2006.

In its meeting of 20 December 2012, the Board of Directors resolved (i) the approval of an updated

version of the aforementioned Regulation and (ii) the approval of the Regulation on controls related

to policies on risk assets and conflicts of interest in regards to related parties. These documents were

subsequently implemented by the individual companies, other than the Bank, that belong to the

Banking Group.

As required by Bank of Italy, the Bank’s Shareholders’ Meeting held 21 December 2012 was informed

regarding the Board approval of the document containing the internal control policies on related

parties.

Establishment of the Banking Group

GE Capital Interbanca S.p.A. is the Parent Company of the GE Capital Interbanca Banking Group,

enrolled in the Banking Group Register according to art. 64 of the Consolidated Banking Act.

The most significant steps in the evolution that resulted in the establishment of the Banking Group

are described below.

On 31 December 2010, GE Capital Interbanca S.p.A. acquired the equity investments in GE Capital

Finance S.r.l., GE Capital Servizi Finanziari S.p.A. and GE Leasing Italia S.p.A.

During 2011, the procedures to enrol the new Banking Group in the Banking Group Register were

completed, as well as the related amendments to the Articles of Association.