Embed Size (px)

Citation preview

Senvion SA

Annual Results Presentation 2017 March 15, 2018

1

Disclaimer

This presentation (the “Presentation”) has been prepared by Senvion S.A. (“Senvion” and together with its subsidiaries, “we,” “us” or the “Group”)

solely for informational purposes and has not been independently verified, and no representation or warranty, express or implied, is made or given

by or on behalf of the Group. Senvion reserves the right to amend or replace this Presentation at any time. This Presentation is valid only as of its

date, and Senvion undertakes no obligation to update the information in this Presentation to reflect subsequent events or conditions. This

Presentation may not be redistributed or reproduced in whole or in part without the consent of Senvion. Any copyrights that may derive from this

Presentation shall remain the sole property of Senvion.

This Presentation does not constitute or form part of, and should not be construed as, an offer or invitation or inducement to subscribe for,

underwrite or otherwise acquire, any securities of Senvion, nor should it or any part of it form the basis of, or be relied on in connection with, any

investment decision with respect to securities of Senvion or any other company.

Certain statements in this Presentation are forward-looking statements. By their nature, forward-looking statements involve a number of risks,

uncertainties and assumptions that could cause actual results or events to differ materially from those expressed or implied by the forward-looking

statements. These risks, uncertainties and assumptions could adversely affect the outcome and financial consequences of the plans and events

described herein. Actual results may differ from those set forth in the forward-looking statements as a result of various factors (including, but not

limited to, future global economic conditions, changed market conditions affecting the wind industry, intense competition in the markets in which the

Group operates, costs of compliance with applicable laws, regulations and standards, diverse political, legal, economic and other conditions

affecting the Group’s markets, and other factors beyond the control of the Group). Neither Senvion nor any of its respective directors, officers,

employees, advisors, or any other person is under any obligation to update or revise any forward-looking statements, whether as a result of new

information, future events or otherwise. You should not place undue reliance on forward-looking statements, which speak of the date of this

Presentation. Statements contained in this Presentation regarding past trends or events should not be taken as a representation that such trends or

events will continue in the future. In particular, no statements in this Presentation should be construed as concrete guidance as to the results of

operations, cash-flows, balance sheet data or any non-financial metrics as of or for the financial year ending December 31, 2017 or any subsequent

financial period.

Certain financial data included in the presentation consists of “non-IFRS financial measures”. These non-IFRS financial measures may not be

comparable to similarly titled measures presented by other companies, nor should they be construed as an alternative to financial measures

determined in accordance with IFRS. You are cautioned not to place undue reliance on any non-IFRS financial measures and ratios included herein.

This Presentation does not constitute or contain any investment, legal, accounting, regulatory, taxation or other advice.

Due to rounding, numbers presented through out this and other documents may not add up precisely to the totals provided and percentages may not

precisely reflect the absolute figures.

2

Strategic roadmap and guidance 2018 4

Financials 2017 3

Orders and installations 2

Key achievements 2017 1

Agenda

Key takeaways 5

Key achievements 2017 Building a growth platform for 2019

1

4

2017 – key highlights at a glance Making progress against continuing industry headwinds

CY17 revenues at €1,890mn with adjusted EBITDA of €152mn

Cash on hand improved to € 235mm; net cash generation of €47mn in Q4

Working capital at 2.5% ; likely to become negative by Q2 on commissioning of the Chile project

Financials

1

36% growth yoy in firm orders; 393% growth in new markets

Ranked 4th largest2 in EMEA in 2017; market share gains in key regions Orders

2

3.6M140 EBC rated as one of the top 3MW+ turbines by WPM1

Progressing on moving supply chain footprint to low cost countries Products

3

Opex savings of 19% from efficiency program;

Interest cost lower by c.28% post refinancing; cash interest cost at €30mn/yr Efficiency

4

Service generates 16% of total revenues with double digit growth

10+ years of contract tenors and renewal rate of ~75% Services

5

+393%

2017 2016

Orders from new markets

Int reduction

(28%)

Opex reduction

(19%)

Reductions in 2017

+15%

2017 2016 2015

Revenue development

2

1 Wind Power Monthly, 2. BNEF Feb 2018 for combined market share in onshore and offshore

Building platform for 2019

5

Achieved

Key highlights Performance in line with guidance

Revenues

Guidance 2017 Achieved

Revenue slightly

lower than expected

due to minor project

delays

Financial targets in 2017 achieved

Adj. EBITDA

at 8.0%

Adj. EBITDA

around 8.0-8.5% Margins

Firm order Intake

1

2017

€1.90-1.95bn

2017

€1.89bn

~€2.0bn

2017

~€1.8bn

2017

Two key order

conversions

delayed

350 MW+ orders

already converted

in India & ANZ

6

Senvion in EMEA and globally Senvion gaining market shares in key regions

2

Market share gains in Germany and France – key current markets

Source – BNEF Report Feb 2018 based on commissioned windfarms; 1. Onshore and Offshore combined

EMEA Region – 2017 market share1 Global (Ex China) – 2017 market share1

11.0%

(2016: 9.6%)

Others

89%

5.7%

(2016: 4.9%)

Others

94.3%

Selective global approach

Aiming for significant market share gains in targeted new markets by 2019

Large player in all key markets

17

GW

34

GW

4 6

7

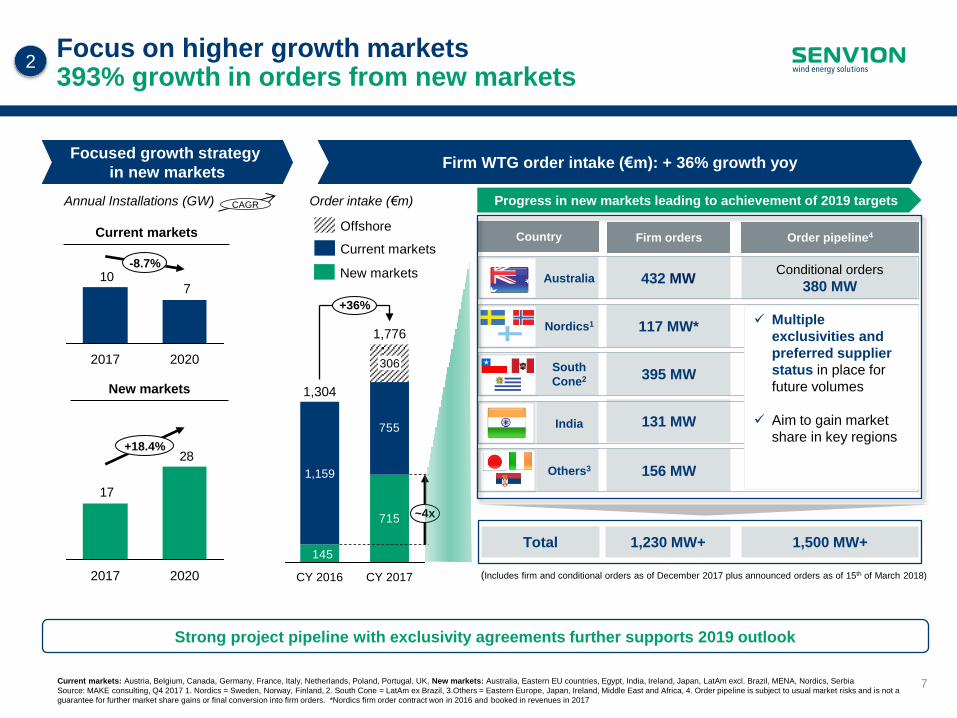

Focus on higher growth markets 393% growth in orders from new markets

Annual Installations (GW)

Current markets Offshore

New markets

Current markets

(Includes firm and conditional orders as of December 2017 plus announced orders as of 15th of March 2018)

Order intake (€m)

New markets

710

2017

-8.7%

2020

28

17

2017

+18.4%

2020

715

145

755

CY 2016

306

1,159

1,304

1,776

~4x

+36%

CY 2017

Current markets: Austria, Belgium, Canada, Germany, France, Italy, Netherlands, Poland, Portugal, UK, New markets: Australia, Eastern EU countries, Egypt, India, Ireland, Japan, LatAm excl. Brazil, MENA, Nordics, Serbia

Source: MAKE consulting, Q4 2017 1. Nordics = Sweden, Norway, Finland, 2. South Cone = LatAm ex Brazil, 3.Others = Eastern Europe, Japan, Ireland, Middle East and Africa, 4. Order pipeline is subject to usual market risks and is not a

guarantee for further market share gains or final conversion into firm orders. *Nordics firm order contract won in 2016 and booked in revenues in 2017

2

CAGR

Strong project pipeline with exclusivity agreements further supports 2019 outlook

Others3 156 MW

India 131 MW

395 MW South

Cone2

Nordics1 117 MW*

Australia Conditional orders

380 MW 432 MW

Total

Progress in new markets leading to achievement of 2019 targets

Country Firm orders Order pipeline4

1,230 MW+ 1,500 MW+

Focused growth strategy

in new markets Firm WTG order intake (€m): + 36% growth yoy

Multiple

exclusivities and

preferred supplier

status in place for

future volumes

Aim to gain market

share in key regions

8

Product philosophy driven by high level of modularity New modular products to drive margin recovery

3MW+ 2.xM

3

Evolution of onshore turbines

2.M 1xx

IEC I

IEC II

IEC

III

2003 - 2014

3MW+ 2.xM

2015 – 2017 (with modular approach)

3MW+ 2.xM

4.M 14x

4.M 14x

2.M 1xx

2018 pipeline

Higher AEP increase with

much lower cost increase

More product variety, with

less component variety

IRR multiplying

effect

Targeting cost

reductions

Competitive offering Project optimized

turbines

Region specific

product fit

4.M 11x

9

MOVE FORWARD Progress card – €52mn fixed cost savings achieved

Consistent and sustainable reduction

in Opex

42363539

5347^

Q4

16

-20%

Q2

16

44^

Q2

17

Q1

16

Q3

17

Q1

17

Q4

17

-18%

-22%

-17%

Q3

16

45^

-28%

56*

2016

40**

2017

^ Adjusted for IPO costs/transaction costs

* Adjusted by shareholder loan interest

** Underlying interest costs without pre payment premium of earlier High yield bond and other related one time expenses of refinancing

LCC = Low cost countries

4

Net interest down by 28%

42% reduction in annual interest

costs of high yield bond

Net Interest (€m) Opex (€m)

DONE

2.7 GW capacity; sufficient for growth

Closed three factories in Germany

Increasing sourcing from LCC

(from sub 5% to 30%+)

Increased

proximity

to growth

markets

DONE

Opex run rate Interest costs Supply chain transformation

10

Key results Key attributes

Growing Service business Efficient set-up to drive resilient and profitable growth

5

Service provides a growing, annuity-like cash flow stream to the business

Significant

growth

Consistent, high growth

Increasing relevance of service

offering

High

visibility

High visibility from €2.5bn service

order book

10+ years2 average duration

providing annuity-like revenue

High renewal rate1 (~75% last 3

years)

High

margins and

cash flow

contribution

Stronger contribution margin v/s

turbine business

~16% share of revenues

Higher FCF contribution

Notes:

1.Turbine renewal rate of service contracts since 2016 based on quarterly data

2.Only includes active contracts and tenors weighted by no. of WTGs

+11.6%

Service revenue (€mn)

GW under service

CY17: €308m CY16: €276m

88.8

68.278.872.672.8

65.565.472.6

Dec-17 Sept-17 Jun-17 Mar-17 Dec-16 Sept-16 Jun-16 Mar-16

13.612.712.112.111.911.410.812.8

+12.4%

Dec-17 Sep-17 Jun-17 Mar-17 Dec-16 Sep-16 Jun-16 Mar-16

Orders and installations

2

12

Senvion installations Installation rate in line with revenue plan

Installations (MW)

Decline in installations

in line with revenue

guidance

Q4 installation rate

mainly impacted by

installation shifts from

the 299 MW order in

Chile to 2018

Final commissioning of

Nordergrunde and

Nordsee One offshore

windfarms achieved in

Q4 2017 591

155

485

141

217

185

351

480

185

6

-16.1%

CY 17

1,478

332

CY 16

1,762

112

Annual Installation Q1-Q4 2017 installations

5598

40

68

31

43

79

52

108

183

133

35

55

2642

56

Q4 17

292

29

Q3 17

571

141

Q2 17

372

141

0

Q1 17

243

49 4

12

Offshore Other new markets Other current markets UK France Germany

13

Note: Figures prior Dec 15 relate to Senvion GmbH

Net Firm orders are confirmed orders minus PoC revenues already booked.

Conditional orders are signed contracts where either building permit and/or grid connection and/or financing is missing.

Q4 15 1.8 0.6 1.2

Q1 16 1.8 0.6 1.2

Q2 16 1.7 0.6 1.1

Q3 16 1.5 0.7 0.8

Q4 16 1.3 0.4 0.9

Q1 17 1.3 0.3 1.0

Q2 17 1.6 0.5 1.1

Q3 17 1.5 0.5 1.0

Q4 17 1.5 0.3 1.2

Order book of €5.0bn Onshore order book improving

Net firm orders at €1.5bn

Order book (€bn) Q4 2017 split by geography

Others

France

UK

Germany

New markets

Offshore

Q4 17

1,471

69

97

186

154

659

306

1.9

2.0

2.1

2.1

2.2

2.3

2.3

2.5

2.5

5.6

5.6

5.4

5.4

5.3

5.5

Figures in €mn

5.5

Onshore

€1.2bn

5.3

1.7

1.9 0.3 1.6

1.8 0.3 1.5

1.6 0.3 1.3

1.4

1.6

1.7

1.3

1.0

Onshore Offshore

5.0

Net Firm Orders Conditional Service Total

14

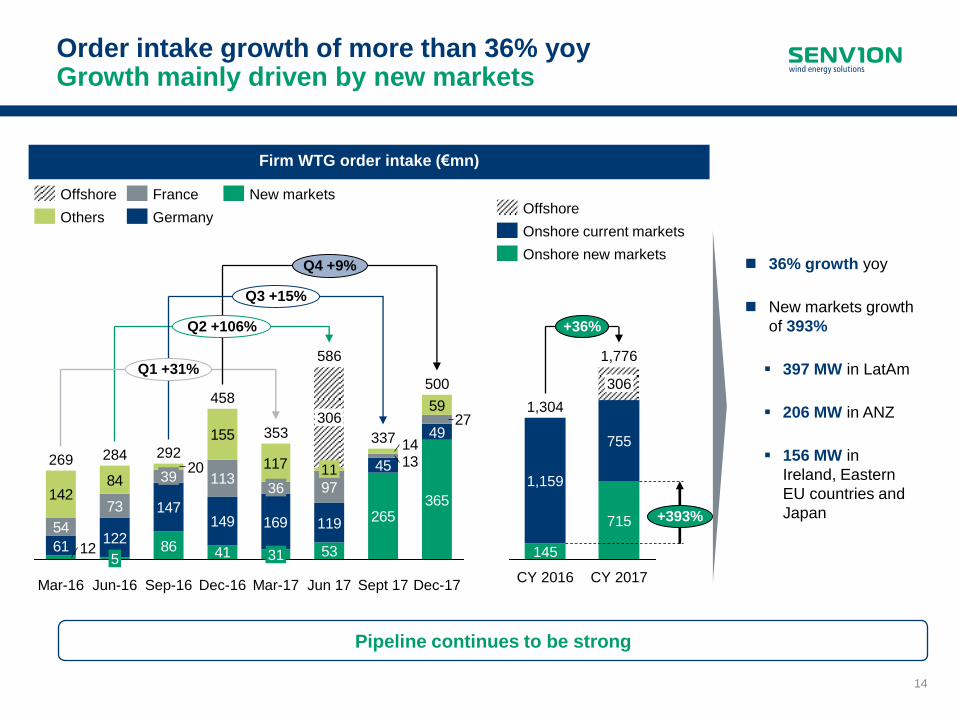

Order intake growth of more than 36% yoy Growth mainly driven by new markets

Firm WTG order intake (€mn)

86

265365

61122

147149 169 119

45

49

54

73

11397142

84

155

117

59

534112

27

1314

20

353

31

36

Dec-16 Mar-17 Sep-16

292

Sept 17

337

458 500

Jun 17

586

11

306

Q4 +9%

Q1 +31%

Q2 +106%

Q3 +15%

Dec-17

39

Jun-16

284

5

Mar-16

269

France

Others

New markets

Germany

Offshore

Pipeline continues to be strong

+393%

+36%

715

755

306

CY 2017

1,776

CY 2016

1,159

1,304

145

36% growth yoy

New markets growth

of 393%

397 MW in LatAm

206 MW in ANZ

156 MW in

Ireland, Eastern

EU countries and

Japan

Onshore new markets

Onshore current markets

Offshore

Financials 2017 Delivering on promises made

3

16

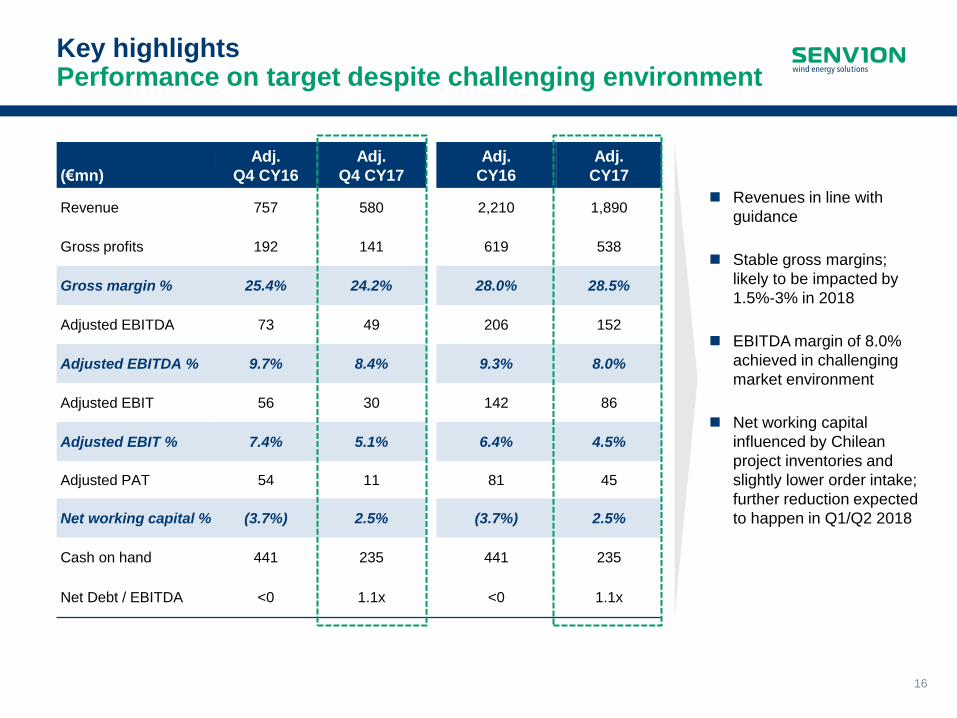

Key highlights Performance on target despite challenging environment

Revenues in line with

guidance

Stable gross margins;

likely to be impacted by

1.5%-3% in 2018

EBITDA margin of 8.0%

achieved in challenging

market environment

Net working capital

influenced by Chilean

project inventories and

slightly lower order intake;

further reduction expected

to happen in Q1/Q2 2018

(€mn)

Adj.

Q4 CY16

Adj.

Q4 CY17

Adj.

CY16

Adj.

CY17

Revenue 757 580 2,210 1,890

Gross profits 192 141 619 538

Gross margin % 25.4% 24.2% 28.0% 28.5%

Adjusted EBITDA 73 49 206 152

Adjusted EBITDA % 9.7% 8.4% 9.3% 8.0%

Adjusted EBIT 56 30 142 86

Adjusted EBIT % 7.4% 5.1% 6.4% 4.5%

Adjusted PAT 54 11 81 45

Net working capital % (3.7%) 2.5% (3.7%) 2.5%

Cash on hand 441 235 441 235

Net Debt / EBITDA <0 1.1x <0 1.1x

17

Revenue development New markets starting to grow at a fast clip

Onshore revenue breakup (€mn)

Other revenues at €5m for 2016 and €9m for 2017

-36%

CY17

1.028

516

185 162

166

CY16

1.619

420

192

397

610

2017: Current market

revenues declined led

by UK & Canada

2018: Revenues in

Germany to shrink due

to issues with auction

systems

Revenues from New

markets grew led by

Nordics

Revenues likely to

grow at a fast rate in

2018 led by Chile and

Australia

Revenue split 2017: €1.9bn

Onshore – €1.2bn Offshore – €0.3bn Service – €0.3bn

393 430544

227 263 377359

137263

Q4 17

89 128

Q3 17

68 33

Q2 17

79 94

Q1 17

364

73 91

Q4 16

436

73

Q3 16

478

66 88

Q2 16

577

65 47

Q1 16

73 29

391

754

584 505

Service Offshore Onshore

Revenue split 2016: €2.2bn

Onshore – €1.6bn Offshore – €0.3bn Service – €0.3bn

New Markets Current markets

37

89

+1,704%

CY17

198

21

52

CY16

11

ANZ South Cone Nordics Others

All figures in €mn

Germany France UK Others

18

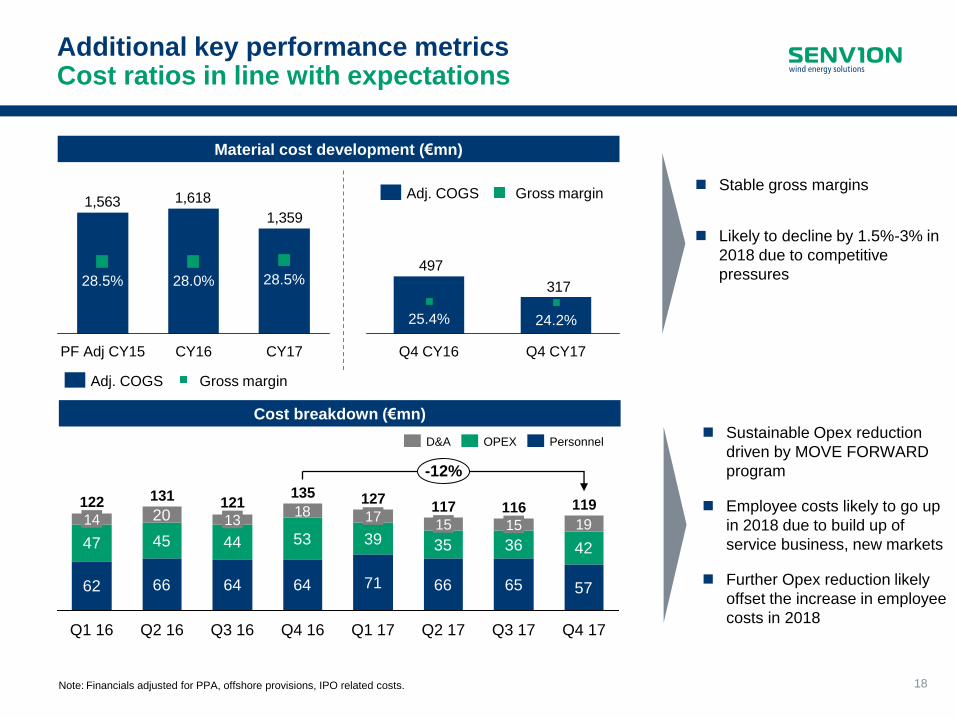

Additional key performance metrics Cost ratios in line with expectations

Material cost development (€mn)

Stable gross margins

Likely to decline by 1.5%-3% in

2018 due to competitive

pressures

1,359

1,6181,563

CY17

28.5%

CY16

28.0%

PF Adj CY15

28.5%

Gross margin Adj. COGS

Cost breakdown (€mn)

62 66 64 64 71 66 65 57

47 45 44 53 39 35 36 42

191820

Q1 16

122

14

-12%

Q4 17

119

Q3 17

116

15

Q2 17

117

15

Q1 17

127

17

Q4 16

135

Q3 16

121

13

Q2 16

131

Personnel OPEX D&A

Note: Financials adjusted for PPA, offshore provisions, IPO related costs.

Sustainable Opex reduction

driven by MOVE FORWARD

program

Employee costs likely to go up

in 2018 due to build up of

service business, new markets

Further Opex reduction likely

offset the increase in employee

costs in 2018

317

497

24.2%

Q4 CY16

25.4%

Q4 CY17

Gross margin Adj. COGS

19

Breakup of total Capex and R&D Achieving more within similar cost budgets

R&D expenditure (€mn)

2.6% 3.1% 3.0% 3.1%

Total intangible and tangible capex1 (€mn)

1.8%

Senvion GmbH Senvion S.A.

Investments focused on the expansion

of the blade facility and consolidation of

nacelle facility in Portugal

1.5% 2.2%

Senvion GmbH

2.7% 2.6% 1.4%

Senvion S.A.

39 45 45 4222 21

1922 23 26

2320

Mar-15

58

Mar-14

45

Mar-13

42

CY17 CY16

68

PF adj

CY15

67 68

R&D spending in line with previous year

Key R&D spending focused on

development of 3xM, 2XM platform

Increasing product portfolio within

the same R&D costs thanks to

modularity and cost savings due to

various measures such as insourcing of

project managers, efficient certification

management etc

Note: 1. Excluding capitalised R&D.

[%] Capex over LTM sales

[%] R&D over LTM sales Expensed

5160

304346

35

März-14 März-13 CY17 CY16 PF adj

CY15

März-15

Capitalised

2.7%

2.9%

20

Net working capital and cash flow summary Working capital to improve by H1 2018

Quarterly net working capital1 evolution (€m)

Quarterly cash flow evolution (€m)

NWC1 % of trailing 12 months revenue Net working capital

Sep-17 Jun 17 Mar 17 Dec-16 Sep-16 Jun-16 Mar-16 Dec-15

Q4 impacted due to delayed order conversions

Likely to improve by Q1/Q2 2018 on the back of order intake and commissioning of Chilean project

Positive free cash flow in H2 2017

Consistent cash flow generation excluding exceptional items

Negative free cash flow in H1 2017 mainly driven by inventory for Chilean projects

Note:

1. Net working capital defined as current assets (adjusted for liquid funds and assets of disposal Group classified as held for sale) minus total current liabilities (adjusted for provisions, liabilities of disposal

Group classified as held for sale and short-term loans and current portion of long-term loans).

185 23 (68) 64 14 (109) (173) 44

Free cash flow Operating cash flow Investing cash flow

Dec-17

47

Sep-17 Jun 17 Mar 17 Dec-16 Sep-16 Jun-16 Mar-16 Dec-15 Dec-17

(101) (132)

(57)

(119) (83)

(5)

99

8 47

(4.7%) (6.4%) (2.7%) (5.8%) (3.7%) (0.2%)

4.6%

0.4%

2.5%

Strategic roadmap and financial goals Enhancing efficiency to achieve 2019 targets

4

22

2.442.432.643.46

4.50

2.85

Maha Febr.-

18

Gujarat Okt.-

17

Jan.-

17

FIT

+17%

New

mark

ets

Positive changes supporting 2019 outlook

Source: Bloomberg auction overview & MAKE regional reports, Senvion Market Intelligence

Prices correspond to the latest average auctions results in each country

Auction systems bring larger volumes at lower prices Prices stabilizing with Senvion gaining ground

Markets dominated by auctions Volumes growing and prices now stabilizing

46374357

70

+24%

Feb-18 Nov-17 Aug-17 May-17 FIT

€/MWh

INR/KWh

$/MWh

415359

2017 2016 2016

74 65

-12%

2018e FIT

709 MW with avg bid price going up by 24%

Govt discussing to add 1.4 GW extra auctions

in 2018

Senvion increasing market share

Stable market, auctions volume to flow into

2020

Senvion maintaining 10-20% market share

Indian government plans 10 GW of auctions

between 2018 – 2020

Senvion with 131 MW orders, a healthy

pipeline and increasing market share

Decent auction prices

Senvion gaining market share

100 MW of co-investment project

€/MWh

Cu

rren

t m

ark

ets

Onshore auction volumes (GW)

Wind auctions in 2017

Auctions in previous years, no wind activity in 2017

24

20

2017

+20.0%

2018E

23

High degree of comfort developing on 2019 volumes Closing gap on 2019 revenue targets

2019e Germany

upside

potential

New

markets

upside

Service+

offshore

2018

Guidance

€1.8-1.9bn

~35%

25%

~40%

1 Onshore market share as per BNEF market share file released in Feb 2018 and Feb 2017

Expanding pipeline with market share gains

Service and offshore growth largely covered by

firm orders

Improving order pipeline in new markets

India: Gaining market share, additional upside if

further auctions are conducted on time

Argentina: Large market share likely in RENOVA 2

auction

Australia: c. 600 MW of volume visibility based on

orders in hand for 2019

Chile and North Africa: Exclusivities for large volumes

Germany

Market share growing from 7% to 10% in 20171

Extra volume expected if proposal to expand auction

volumes by 50% go through

Key risks

Market developments delayed in India and Germany

Delays in order conversions/postponements

Key comments

1

2

3

Increasing visibility on 2019 revenues

1

2

3

€2.6-2.7bn

2017

€1.9bn

54%

11%

35%

Current markets

New markets

Service+Offshore

Current markets New markets Service+Offshore

24

LCoE roadmap in place with early stages of cost outs Intensive efforts required in light of pricing pressure

Cost out plans initiated, but execution risks remain

2020 2018 2016 2014

-16%

-12%

LCoE

-4%

LCoE calculation based on reference project for Germany (6.5m/s at 140m, 8WECs), including all project cost from customer perspective

3.xM12x at 139m hub height – 3.xM EBC at 130m/128m/126m hub height

1. LCC – Low Cost Countries

Product LCoE roadmap ready…

3.xM 12X

3.xM 14X EBC

Progress being made on cost outs

Increasing sourcing from LCC1

Agreements in place for generators

and blades from China

Sourcing agreements for towers and

Gearbox from China also in place

Simplifying processes

Lower transport costs

Lower crane and installation costs

Reduction in BoP costs

Reduced time for installation

Key Risks

Delays in new

component sourcing

Competition pressures

on new turbines and

components

Delays in new product

introductions

Risks of quality, testing

period delays cannot

be ruled out

25

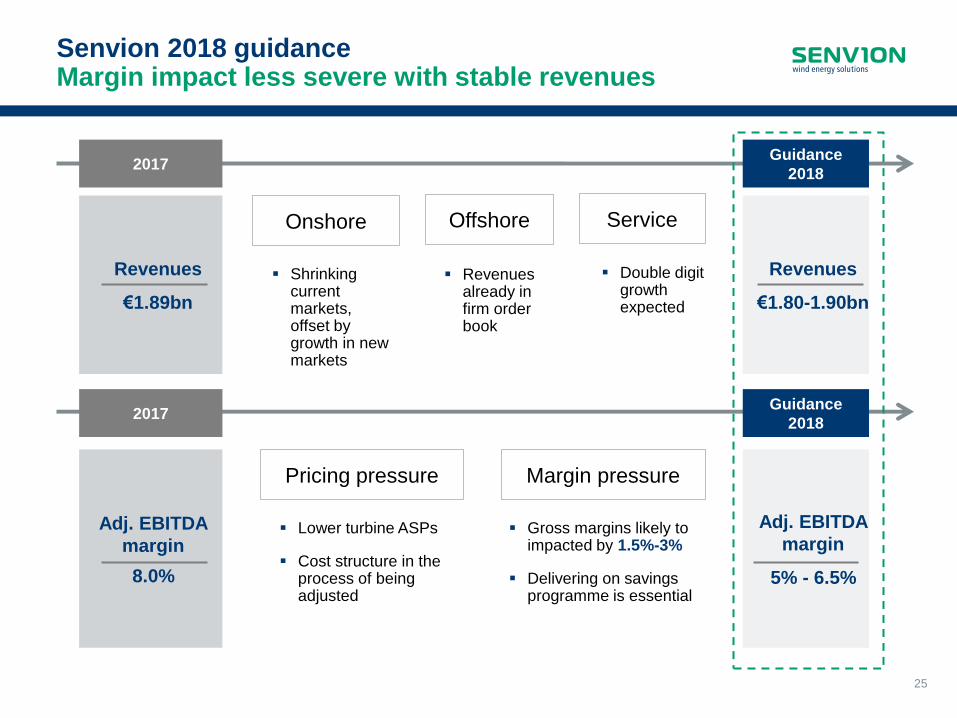

Senvion 2018 guidance Margin impact less severe with stable revenues

Increasing

profitability

Safeguarding

continuous

order intake

Choose the right battles

Minimise sunk costs

Etc.

Revenues

€1.80-1.90bn

Adj. EBITDA

margin

5% - 6.5%

Revenues

€1.89bn

Adj. EBITDA

margin

8.0%

2017 Guidance

2018

Onshore Offshore Service

Shrinking current markets, offset by growth in new markets

Revenues already in firm order book

Double digit growth expected

Pricing pressure

Lower turbine ASPs

Cost structure in the process of being adjusted

Margin pressure

Gross margins likely to impacted by 1.5%-3%

Delivering on savings programme is essential

2017 Guidance

2018

Key takeaways 5

27

Key takeaways

Expanding product portfolio within same R&D budgets and with a

healthy product pipeline

Service business continues to grow

Significant cost cuts achieved under MOVE FORWARD as promised

Market share gains followed by solid order intake from new markets 2

Performance in line with guidance 1

5

3

4

Appendix

MM tubines in France

29

Financial Calendar 2017

Event Date

Annual Results 2017 March 15, 2018

Q1 2018 Results May 15, 2018

Annual General Meeting May 31, 2018

Q2 2018 Results August 14, 2018

Q3 2018 Results November 14, 2018

Financial calendar

Your Investor Relations Team:

Dhaval Vakil

Vice President – Capital Markets and M&A

Phone UK: +44 20 7034 7992

Mobile: +44 7788390185

Email: [email protected]

Anja Siehler

Sr. Manager Capital Markets

Phone Lux: +352 26 00 5285

Mobile: +49 152 21817093

Email: [email protected]

For general queries: [email protected]

30

Income statement 2017 Bridge between reported and adjusted earnings

€mn Q4 17 Adj. Adj Q4 17 CY17 Adj. Adj CY17

Revenue 580 580 1,890 1,890

Total performance 458 458 1,893 1,893

Material expenses (317) (317) (1,355) (1,355)

Gross profit 141 141 538 538

Gross margin % 24.2% 24.2% 28.5% 28.5%

Other operating income 10 10 30 30

Personnel expenses (57) (57) (260) (260)

Opex (42) (42) (153) (153)

FX gain/loss (3) (3) (4) (4)

EBITDA 49 49 152 152

EBITDA % 8.4% 8.4% 8.0% 8.0%

D&A (34) 15 (19) (158) 92 (66)

EBIT 14 29 (6) 86

EBIT% 2.4% 5.0% (0.3%) 4.5%

Extraordinary Expenses 1 (1) (0) (54) 54 0

Net interest (10) (10) (61) 20 (41)

Taxes (3) (6) (8) 28 (28) (0)

Net profit (Con. Ops) 2 11 (93) 45

PAT % 0.3% 1.8% (4.9%) 2.4%

Key adjustments

1

Includes € 0.6mn restructuring

provision reversed

Includes PPA impact

of € 15.2mn

2

1

2

4

7

5

Includes € 54.1mn of

restructuring measures

Includes PPA impact

of € 92.1mn

Includes € 20.4mn of bond

refinancing costs

4

6

5

Q4 2017

CY 2017

3

Includes positive PPA

impact of € 5.5mn 3

6 Includes positive PPA

impact of € 28.3mn 7

31

Assets (€mn) Dec 17 Sep 17 Dec 16

Liquid Funds 235 190 441

Current Assets (excluding liquid funds) 774 804 814

Receivables 206 153 257

Inventories 490 560 430

Others 78 91 127

Property, plant & equipment 224 234 222

Other intangible assets 527 541 604

Other non current assets* 35 40 19

Deferred tax assets 13 0 0

Total 1,808 1,808 2,101

Liabilities (€mn) Dec 17 Sep 17 Dec 16

Loans (short term, long term and High Yield Bond) 400 401 407

Current liabilities (excluding provisions and short term loans) 728 796 897

Advance payments received 119 159 189

Trade payables 340 381 431

Gross amount due to customers for contract work as a liability 139 119 122

Others 131 137 155

Provisions 300 247 289

Deferred tax liability 150 140 173

Total equity capital 230 225 334

Total 1,808 1,808 2,101

Senvion S.A. Balance sheet

* - Includes assets held for sale

32

Senvion S.A. Cash flow summary

Senvion

S.A.

Senvion

S.A.

Senvion

S.A.

Senvion

S.A.

(€mn) Q4 CY16 Q4 CY17 CY16 CY17

Result before income taxes (38) 5 (89) (121)

Adjustments for Depreciation on property, plant and equipment, amortization of intangible assets and write-offs on

financial assets 43 35 167 158

Interest income (0) (2) (1) (4)

Interest expenses 14 13 64 65

Increase/decrease in provisions 76 53 71 10

Change in working capital (35) (27) (23) (100)

Interest received 0 3 1 4

Interest paid (14) (18) (40) (68)

Income tax paid/received (0) (3) (12) (36)

Cash flow from operating activities 46 57 138 (91)

Cash receipts from the sale of property, plant and equipment, intangible and other long-term assets 1 (0) 3 3

Cash payments for the purchase of intangible assets (13) (8) (50) (42)

Cash payments from purchase of property, plant and equipment and other long-term assets (20) (2) (58) (59)

Cash payments from loans granted to related parties 0 0 0 0

Acquisition of subsidiary: Net of cash acquired (0) (1) (0) (1)

Cash flow from investing activities (32) (11) (105) (99)

Acquisition of treasury shares (4) 0 (7) (8)

Net Cash repayments of amounts borrowed / repayments (1) (0) (5) (4)

Cash flow from financing activities (5) (0) (12) (12)

Increase/decrease in cash and cash equivalents 9 46 20 (203)

Cash and cash equivalents at the beginning of the period 425 184 413 434

Cash and cash equivalents at the end of the period 434 231 434 231

Liquid funds 441 235 441 235

Short-term bank liabilities (8) (5) (8) (5)

Cash and cash equivalents at the end of the period 434 231 434 231

33

Overview of PPA Adjustments

Expected yearly P&L effects1 (€mn)

Notes:

1. Including deferred tax impacts and is not the complete schedule; assumed group tax rate of 29.935% for calculations.

Source: Company information; Deloitte analysis.

27

28

28

64

Dec-20e

Dec-19e

Dec-18e

Dez.-17

Net PPA booked in CY17 (€mn)

18

18

18

10

64

Q4 17

Q3 17

Q2 17

Q1 17

CY 2017

© Senvion S.A.

All rights reserved. No part of this document may be

reproduced or transmitted in any form or by any means,

electronic or mechanical, including photography,

recording, or any information storage and retrieval

system, without permission from Senvion S.A.

Thank you for your participation