Embed Size (px)

Citation preview

Semi-annual Report as at 30 June 2003

— 1 —

SEMI-ANNUAL REPORT AS AT 30 JUNE 2003

The semi -annual report as at 30 June 2003 is English translation of Italian Semi-annual report.

Semi-annual Report as at 30 June 2003

— 2 —

Credito Valtellinese Società Cooperativa a r.l.Head Office in Sondrio — Piazza Quadrivio, 8

Tax and Sondrio Company Register no. 00043260140 — Bank Register no. 489Parent company of Gruppo bancario Credito Valtellinese — Bank Register code no. 5216.7

Internet site: http://www.creval.it E-mail: [email protected] as at 30/06/2003: Share capital 163,733,652 euro — Reserve 307,426,340 euro

SEMI-ANNUAL REPORTAS AT 30 JUNE 2003

Semi-annual Report as at 30 June 2003

— 3 —

Semi-annual Report as at 30 June 2003

— 4 —

Corporate bodies of Credito Valtellinese

Board of DirectorsChairman Giovanni De CensiVice Chairman Salvatore VitaliExecutive Director Renato BartesaghiBoard Members Franco Bettini

Michele Colombo Giovanni Continella

Mario CotelliPier Domenico De FilippisFrancesco GuicciardiEmilio RigamontiMarco SantiGiuliano Zuccoli

Members of the executive committee

Board of Statutory AuditorsChairman Angelo PalmaPermanent members Roberto Campidori

Fabiano GarbelliniSubstitute members Aldo Cottica

Alfonso Rapella

Board of ArbitratorsPermanent Arbitrators Emilio Berbenni

Francesco BertiniItalo Vittorio Lambertenghi

Substitute Arbitrators Ettore NegriFedele Pozzoli

General ManagementGeneral Manager Miro FiordiFirst Vice General Manager Giovanni Paolo MontiVice General Manager Franco Sala

Audit Company Reconta Ernst & Young S.p.A.

Semi-annual Report as at 30 June 2003

— 5 —

Semi-annual Report as at 30 June 2003

— 6 —

Contents

FINANCIAL STATEMENTS: CONSOLIDATED SEMI-ANNUAL FINANCIAL STATEMENTS AS AT 30 JUNE 2003................................................................. 8

Consolidated Balance Sheet............................................................................ 9Consolidated Income Statement ...................................................................11

FINANCIAL STATEMENTS: SEMI-ANNUAL FINANCIAL STATEMENTS OF CREDITO VALTELLINESE AS AT 30 JUNE 2003............................................. 12

Credito Valtellinese Balance Sheet .............................................................. 13Credito Valtellinese Income Statement....................................................... 15

REPORT ON OPERATIONS FOR GRUPPO CREDITO VALTELLINESE IN THE FIRST HALF 2003 ............................................................................................. 16

A. Information on operations in the first half 2003.................................. 171. Group operations................................................................................................................. 172. The operating environment.................................................................................................. 193. Group strategic guidelines and business policies ............................................................... 204. Operating performance in the first half 2003...................................................................... 255. Information on the operating performance of the Gruppo Credito Valtellinese companies30

Structure and content of the consolidated semi-annual report................. 40B. Valuation Criteria...................................................................................... 42

Section 1 - Illustration of accounting principles........................................................................ 42Section 2 – Tax adjustments and provisions .............................................................................. 48D) INFORMATION ON THE INCOME STATEMENT ............................................................. 61E) OTHER INFORMATION ...................................................................................................... 65F) SCOPE OF CONSOLIDATION ............................................................................................ 66ATTACHMENTS........................................................................................................................ 67

AUDIT COMPANY’S REPORT........................................................................... 72

Semi-annual Report as at 30 June 2003

— 7 —

Semi-annual Report as at 30 June 2003

— 8 —

Financial statements:Consolidated Semi-Annual Financial

Statementsas at 30 June 2003

Semi-annual Report as at 30 June 2003

— 9 —

Consolidated Balance Sheet

Assets 30/06/2003 31/12/2002 30/06/2002

10. Cash and deposits with central banks and post offices 73.876 110.245 70.913

20. Treasury bills and similar securities eligible for refinancing with central banks 221.445 209.388 456.818

30. Due from banks: 777.068 723.864 319.519

a) repayable on demand 93.571 81.981 60.340

b) other 683.497 641.883 259.179

40. Loans to customers 6.872.316 6.664.462 6.059.244

including:

- loan using public funds administered 57 62 82

50. Bonds and other debt securities: 708.799 603.901 975.210

a) issued by public bodies 519.523 426.567 786.389

b) issued by banks: 162.682 151.054 131.319

including:

- own securities 16.264 18.918 11.988

c) issued by financial institutions 15.485 21.683 44.938

d) other issuers 11.109 4.597 12.564

60. Shares, quotas and other equities 178.203 180.567 186.300

70. Equity investments 62.371 61.506 69.691

a) carried at equity 43.773 43.015 49.382

b) other 18.598 18.491 20.309

80. Investments in Group companies 50 50 -

b) other 50 50 -

90. Goodwill arising on consolidation 110.085 115.684 112.878

100. Goodwill arising on application of the equity method 1.210 680 735

110. Intangible fixed assets 27.508 25.108 28.146

including:

- start-up costs 362 435 601

- goodwill 5.842 2.790 3.190

120. Tangible fixed assets 247.092 244.466 235.381

including:

- assets pending financial leasing 48.700 50.529 40.051

140. Own shares 811 57 5.144

(nominal value Euro 284 thousand)

150. Other assets 341.002 424.384 341.671

160. Accrued income and prepayments: 65.023 66.198 66.890

a) accrued income 56.398 58.347 57.533

b) prepayments 8.625 7.851 9.357

including:

- issue discounts on securities 851 449 867

Total assets 9.686.859 9.430.560 8.928.540

Semi-annual Report as at 30 June 2003

— 10 —

Liabilities and shareholders' equity 30/06/2003 31/12/2002 30/06/2002

10. Due to banks: 151.221 428.678 397.666

a) repayable on demand 41.610 27.497 43.875

b) time deposits or with notice period 109.611 401.181 353.791

20. Due to customers: 5.995.105 5.602.735 5.237.424

a) repayable on demand 5.162.598 4.719.155 4.322.600

b) time deposits or with notice period 832.507 883.580 914.824

30. Securities issued 2.054.820 2.031.187 1.972.105

a) bonds 1.809.096 1.794.005 1.710.003

b) certificates of deposit 184.402 187.592 194.343

c) other securities 61.322 49.590 67.759

40. Public funds administered 57 62 82

50. Other liabilities 422.912 355.703 335.914

60. Accrued expenses and deferred income: 51.387 55.554 57.574

a) accrued expenses 35.135 37.102 35.721

b) deferred income 16.252 18.452 21.853

70. Provisions for termination indemnities 57.367 55.614 55.764

80. Provisions for risks and charges: 76.770 96.424 72.153

a) pensions and similar commitments 29.672 29.669 28.850

b) taxation 24.180 43.819 23.744

c) other 22.918 22.936 19.559

90. Reserve for possible loan losses 718 18 1.568

100. Reserve for general banking risks 34.083 31.773 29.283

110. Subordinated liabilities 299.642 226.121 207.758

120. Negative goodwill on consolidation 10.349 15.524 15.525

130. Negative goodwill on application of the equity method

13.130 11.591 5.752

140. Minority interests 132.847 137.102 151.554

150. Share capital 163.734 154.255 160.255

160. Share premium reserve 179.158 168.031 168.031

170. Reserves: 37.299 45.365 54.187

a) legal reserve 35.263 32.625 32.625

b) reserve for own shares 811 57 5.144

c) statutory reserves 1.225 11.611 16.418

d) other reserves - 1.072 -

200. Net profit (loss) for the period 6.260 14.823 5.945

Total liabilities and shareholders' equity 9.686.859 9.430.560 8.928.540

GUARANTEES AND COMMITMENTS

Items 30/06/2003 31/12/2002 30/06/200210. Guarantees given 736.643 657.686 625.098

including:

- acceptances 10.478 7.438 7.100

- other guarantees 726.165 650.248 617.998 -

20. Commitments 365.698 277.164 235.222

Semi-annual Report as at 30 June 2003

— 11 —

Consolidated Income Statement

Voci 1° Sem 2003 1° Sem 2002 2002

10. Interest income and similar revenues 206.877 220.536 440.216

including from:

- loans to customers 181.560 180.654 372.982

- debt securities 13.663 30.552 48.478

20. Interest expense and similar charges -84.903 -95.941 -192.974

including on:

- deposits from customers -46.070 -49.703 -104.237

- securities issued -34.744 -37.709 -74.423

30. Dividends and other revenues: 1.759 2.593 5.315

a) from shares, quotas and other equities 60 573 624

b) from equity investments 1.699 2.020 4.691

40. Commission income 71.761 62.919 142.112

50. Commission expense -7.124 -5.355 -14.259

60. Profits (losses) on financial transactions 9.311 1.366 12.389

70. Other operating income 21.615 24.070 49.168

80. Administrative expenses: -154.363 -143.125 -299.530

a) payroll and related costs -88.136 -81.890 -167.977

including:

- wages and salaries -56.028 -52.575 -106.117

- social security charges -18.397 -16.141 -34.044

- termination indemnities -5.310 -4.386 -10.070

- pensions and similar commitments -2.456 -2.634 -6.443

b) other administrative expenses -66.227 -61.235 -131.553

90. Value adjustments to tangible and intangible fixed assets -22.706 -21.886 -47.136

100. Provisions for risks and charges -2.490 -2.605 -7.187

110. Other operating expenses -1.561 -4.000 -7.648

120. Value adjustments to loans and provisions for guarantees and commitments

-22.157 -20.740 -41.614

130. Writeback of adjustments to loans and provisions for guarantees and commitments 8.609 9.047 17.132

140. Provisions for possibile loan losses -700 - -

150. Value adjustments to financial fixed assets -38 -505 -948

160. Writeback of adjustments to financial fixed assets - 39 -

170. Income from investments carried at equity 3.150 2.487 8.091

180. Profit (loss) on operating activities 27.040 28.900 63.127

190. Extraordinary income 5.245 6.390 10.127

200. Extraordinary charges -3.544 -6.226 -10.584

210. Extraordinary income, net 1.701 164 -457

230. Change in reserve for general banking risks -2.310 -1.863 -4.353

240. Income taxes for the period -18.734 -19.170 -38.975

250. Profit (loss) for the year pertaining to minority interests

-1.437 -2.086 -4.519

260. Net profit (loss) for the period 6.260 5.945 14.823

Semi-annual Report as at 30 June 2003

— 12 —

Financial statements: Semi-Annual Financial Statements

of Credito Valtellineseas at 30 June 2003

Semi-annual Report as at 30 June 2003

— 13 —

Credito Valtellinese Balance Sheet

Assets30/06/2003 31/12/2002 30/06/2002

10. Cash and deposits with central banks and post offices 28.427.358 39.601.019 22.386.734

20. Treasury bills and similar securities eligible for refinancing with central banks

56.472.954 54.466.135 170.313.938

30. Due from banks: 1.386.516.707 1.732.832.628 1.338.700.430

a) repayable on demand 62.452.148 87.772.889 334.239.582

b) other 1.324.064.559 1.645.059.739 1.004.460.848

40. Loans to customers 2.430.516.706 2.384.017.386 2.147.083.663

including:

- loans using public funds administered 57.240 62.253 81.523

50. Bonds and other debt securities: 592.439.772 535.648.612 652.842.077

a) issued by public bodies 216.007.735 114.001.212 213.131.228

b) issued by banks: 366.075.887 406.957.229 410.660.284

including:

- own securities 6.905.235 7.705.823 2.021.939

c) issued by financial institutions 7.524.799 11.355.664 23.175.429

d) other issuers 2.831.351 3.334.507 5.875.136

60. Shares, quotas and other equities 67.528.235 67.405.808 73.767.959

70. Equity investments 44.977.045 30.423.698 29.271.365

80. Investments in Group Companies 440.039.882 428.235.807 418.763.231

90. Intangible fixed assets 7.859.545 8.480.963 9.157.324

including:

- start-up costs 5.725.243 6.369.961 7.014.678

100. Tangible fixed assets 433.905.973 431.117.624 359.322.115

including:

- leaded assets 310.598.285 306.092.533 245.073.042

- assets pending financial leasing 46.816.887 47.659.057 36.584.478

120. Own shares 810.569 56.523 5.143.799

( nominal value 283.515)

130. Other assets 120.502.230 152.974.191 141.144.142

140. Accrued income and prepayments: 50.147.896 56.381.463 46.820.804

a) accrued income 45.809.225 53.642.574 42.789.940

b) prepayments 4.338.671 2.738.889 4.030.864

including:

- issue discounts on securities 891.475 541.084 738.012

Total assets 5.660.144.872 5.921.641.857 5.414.717.581

Semi-annual Report as at 30 June 2003

— 14 —

Liabilities and shareholders' equity30/06/2003 31/12/2002 30/06/2002

10. Due to banks: 1.682.944.791 2.159.691.562 1.825.547.256

a) repayable on demand 974.267.964 728.573.828 754.897.344

b) time deposits or with notice period 708.676.827 1.431.117.734 1.070.649.912

20. Due to customers: 1.853.247.850 1.794.815.193 1.648.025.018

a) repayable on demand 1.607.108.588 1.517.129.895 1.293.509.288

b) time deposits or with notice period 246.139.262 277.685.298 354.515.730

30. Securities issued 1.128.471.940 1.132.190.794 1.084.301.179

a) bonds 1.048.748.658 1.050.505.217 990.239.181

b) certificates of deposit 62.756.317 65.791.317 67.636.362

c) other securities 16.966.965 15.894.260 26.425.636

40. Public funds administered 57.240 62.253 81.523

50. Other liabilities 156.922.809 124.959.326 146.064.131

60. Accrued expenses and deferred income: 46.698.167 42.837.986 43.869.966

a) accrued expenses 38.141.253 33.972.088 34.091.349

b) deferred income 8.556.914 8.865.898 9.778.617

70. Provisions for termination indemnities 17.087.649 16.805.672 16.610.096

80. Fondi per rischi ed oneri 43.237.876 51.086.337 40.985.374

a) pensions and similar commitments 18.137.634 17.910.134 17.776.923

b) taxation 18.786.650 27.401.295 18.738.069

c) other 6.313.592 5.774.908 4.470.382

90. Reserve for possible loan losses 2.764.863 3.253.750 4.551.329

100. Reserve for general banking risks 44.157.065 44.157.065 44.157.065

110. Subordinated liabilities 231.174.309 124.159.809 124.159.809

120. Share capital 163.733.652 154.254.639 160.254.639

130. Share premium reserve 179.158.446 168.030.909 168.030.909

140. Reserves: 61.797.919 56.674.053 67.451.964

a) legal riserve 35.262.941 32.625.039 32.625.039

b) reserve for own shares 810.569 56.523 5.143.799

c) statutory reserves 14.244.171 12.512.253 18.225.359

d) other reserves 11.480.238 11.480.238 11.457.767

150. Revaluation reserves 22.312.910 22.312.910 22.312.910

170. Net profit (loss) for the period 26.377.386 26.349.599 18.314.413

Total liabilities and shareholders' equity 5.660.144.872 5.921.641.857 5.414.717.581

GUARANTEES AND COMMITMENTS

Items 30/06/2003 31/12/2002 30/06/200210. Guarantees given 478.520.681 475.196.146 377.406.577

including:

- acceptances 5.101.635 2.111.241 2.464.425

- other guarantees 473.419.046 473.084.905

374.942.152

20. Commitments 99.435.833 136.488.743 135.442.737

Semi-annual Report as at 30 June 2003

— 15 —

Credito Valtellinese Income Statement

Items 1° Sem 2003 1° Sem 2002 200210. Interest income and similar revenues 99.152.596 103.815.374 208.997.146

including from:

- loans to customers 65.588.717 63.771.584 133.510.721

- debt securities 9.528.055 16.572.260 28.467.066

20. Interest expense and similar charges -63.687.232 -66.439.657 -137.144.444

including on:

- deposits from customers -14.518.595 -15.819.052 -33.450.176

- securities issued -20.079.201 -21.624.430 -42.292.061

30. Dividends and other revenues: 30.921.551 23.856.749 23.656.334

a) from shares, quotas and other equities 36.343 428.443 446.281

b) from equity investments 8.390.891 3.690.742 3.472.489

c) from investments in Group Companies 22.494.317 19.737.564 19.737.564

40. Commission income 21.708.878 21.842.749 44.418.347

50. Commission expense -5.319.599 -5.795.474 -9.702.549

60. Profits (losses) on financial transactions 4.052.838 -11.966 4.704.593

70. Other operating income 56.894.662 49.804.014 108.383.903

80. Administrative expenses: -54.417.073 -49.163.526 -99.128.644

a) payroll and related costs -27.048.949 -25.107.197 -48.631.952

including:

- wages and salaries -16.031.641 -14.955.983 -29.634.961

- social security charges -5.649.259 -5.389.642 -9.992.408

- termination indemnities -2.123.045 -1.177.615 -2.613.612

- pensions and similar commitments -1.542.045 -1.472.903 -2.867.142

b) other administrative expenses-27.368.124 -24.056.329 -50.496.692

90. Value adjustments to tangible and intangible fixed assets -41.388.324 -36.493.627 -79.406.551

100. Provisions for risks and charges -690.000 -603.700 -1.664.599

110. Other operating expenses -375.766 -668.820 -940.981

120. Value adjustments to loans and provisions for guarantees and commitments -8.124.081 -10.992.507 -18.992.680

130. Writeback of adjustments to loans and provisions for guarantees and commitments

3.024.114 5.938.788 7.896.875

140. Provisions for possibile loan losses - -596.897 -1.139.546

170. Profit (loss) on operating activities 41.752.564 34.491.500 49.937.204

180. Extraordinary income 3.061.096 3.060.823 5.032.370

190. Extraordinary charges -1.320.401 -4.517.506 -5.235.216

200. Extraordinary income, net 1.740.695 -1.456.683 -202.846

220. Income taxes for the period -17.115.873 -14.720.404 -23.384.759

230. Net profit (loss) for the period 26.377.386 18.314.413 26.349.599

Semi-annual Report as at 30 June 2003

— 16 —

Report on operations for Gruppo Credito Valtellinese in the first half 2003

Semi-annual Report as at 30 June 2003

— 17 —

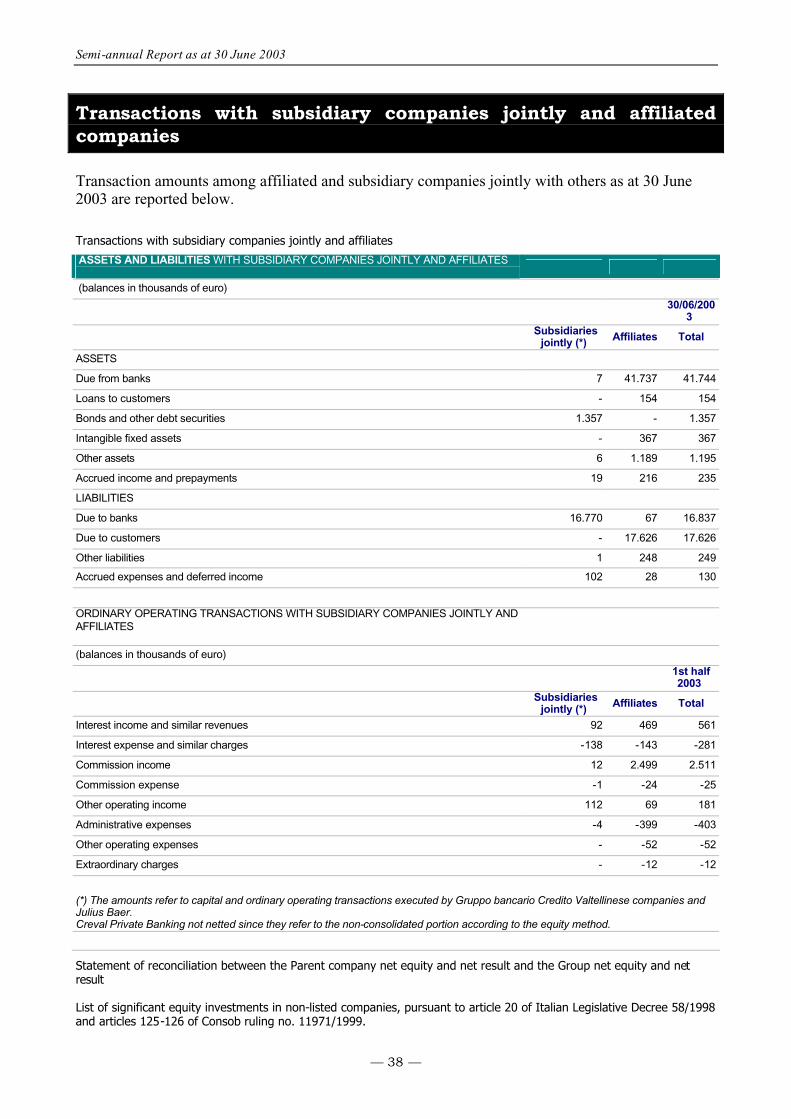

A. Information on operations in the first half 2003

1. Group operations

The Credito Valtellinese banking group operates through four local banks, three specialised financial companies, and three service companies. This report contains the Gruppo Credito Valtellinese consolidated financial statements, highlights of the results reported by the several Group companies, and information on the Group's strategic guidelines and business policies with a view to illustrating its capital standing and financial position.

The "Group Map" diagram below summarises the Group organisation and the percentages held in subsidiaries.

Semi-annual Report as at 30 June 2003

— 18 —

Map of Gruppo bancario Credito Valtellinese

..

The Group structure was modified in the first half 2003 when the Parent company finalised the sale of 51% of its equity investment in Banca Popolare di Rho to the company Julius Baer Holding Ltd.Banca Popolare di Rho then changed company name to Julius Baer Creval Private Banking S.p.A. and a request was made to cancel it from Gruppo bancario Credito Valtellinese.The other major changes to the Group structure during the six months to June included the 1.83% increase in the Credito Valtellinese equity investment in Credito Artigiano, the 5.4% increase in the equity investment in Banca dell’Artigianato e dell’Industria, and the Credito Siciliano acquisition of a further 10% of Bancaperta's share capital.

The company financial statements reported in the tables above have been consolidated into those of the Parent company Credito Valtellinese according to the line-by- line method, except for Aperta Fiduciaria shown at cost since it was not operating as at 30 June 2003. Julius Baer Creval Private Banking S.p.A. is consolidated according to the net equity method sinceit is jointly controlled by Credito Valtellinese and Julius Bear Holding Ltd.

The following have been consolidated according to the net equity method: - The equity investment in Ripoval S.p.A., tax collection service concessionaire for the province

of Sondrio in which Credito Valtellinese has a 50% equity investment for 2,582,300 euro;

BANCADELL’ARTIGIANATOE DELL’INDUSTRIA

CREDITO

ARTIGIANO

BANCAPERTA

65,17%

45,15%

STELLINEDELTASBANKADATI

24,44% 63,44%

20% 20%50%

80% 80%50%

CREDITO VALTELLINESE

39,43%

31,29%

35,79%

37,35%

CREDITO

SICILIANO

11,50%

13,30%

100%

APERTAFIDUCIARIA

31,23%

CASSA SAN GIACOMO

RILENO

100%

BANCADELL’ARTIGIANATOE DELL’INDUSTRIA

CREDITO

ARTIGIANO

BANCAPERTA

65,17%

45,15%

STELLINEDELTASBANKADATI

24,44% 63,44%

20% 20%50%

80% 80%50%

CREDITO VALTELLINESE

39,43%

31,29%

35,79%

37,35%

CREDITO

SICILIANO

11,50%

13,30%

100%

APERTAFIDUCIARIA

31,23%

CASSA SAN GIACOMO

RILENO

100%

Semi-annual Report as at 30 June 2003

— 19 —

- the 40% equity investment in Global Assistance S.p.A., an insurance company with head offices in Milan and share capital amounting to 2,583,000 euro;

- the 40% equity investment, corresponding to 100,000 euro of share capital, held by Bancaperta in Global Assicurazioni S.p.A. with head offices in Milan;

- the equity investment in Crypto S.p.A., head offices in Sondrio and 100,000 euro in share capital, held through Bankadati with a 20% stake and Bancaperta also with a 20% stake;

- the equity investment in Istituto Centrale delle Banche Popolari S.p.A., head offices in Milan and share capital amounting to 33,148,239 euro, in which Credito Valtellinese owns 22.5% of the shares with voting rights at ordinary shareholders' meetings;

- the equity investment in Aperta Gestioni SA, head offices in Lugano (Switzerland) in which Bancaperta has a 49% stake amounting to CHF 600,000.

2. The operating environment

In this section we present a brief general summary of the macroeconomic and lending environment in which the Group has operated.

The general economic scenarioDuring the first half of the year signs of a pick-up in economic activity on a global scale were limited. In the United States, there was a trend reversal in the industrial production index, but this was accompanied by an increase in the unemployment rate in June which may have a negative impact on consumer confidence and spending. In the short-run, the eurozone may experiencedifficulties in generating a significant recovery under conditions of weak domestic demand and the adverse effect of the exchange rate on net exports. The signals from the Japanese economy are not favourable, while the other east Asian countries are showing signs of improvement as the negative impact of the SARS effect fades.

Returning to the eurozone, according to Eurostat data, consumer price growth decelerated in May; in fact inflation slowed from 2.1% in the previous month to 1.9%, mainly reflecting the performance of volatile components such as energy prices. There continues to be a significant gap among the several eurozone countries: the inflation rate in Italy is 2.9%, in France 1.8%, while in Germany the harmonised inflation rate is 1.0% and is exposed to the risk of deflation.

According to Eurostat estimates, second quarter real GDP growth in the eurozone was zero. The data show that economic activity has remained weak since the beginning of the year. According to the estimates, both consumer spending and gross fixed investment contracted sharply after a period of growth in the second half 2002. At the same time the contribution of net exports to GDP growth fell back slightly because of the euro's appreciation against the other currencies.In fact, the euro strengthened further on the foreign exchange markets in June; the average monthly EUR/USD exchange rate increased 0.9% from 1.1570 in May to 1.1670.

Lending1

The rate of increase in total euro-denominated deposits (including savings deposits, current accounts, certificates of deposit, and bonds) held by Italian banks accelerated slightly in the first half 2003. As at 30 June 2003, total bank deposits amounted to 911 billion euro, a 6.76% year-on-year growth rate.

1 Source — Associazione Bancaria Italiana (ABI): monthly breakdown of the total reported by banks with short-term and medium/long-term deposits.

Semi-annual Report as at 30 June 2003

— 20 —

In the twelve months to June, the stock of deposits increased by around 58 billion euro. In detail, the growth trend in customer deposits accelerated slightly, reaching 6.98%, while the growth in bank- issued bonds consolidated at a 6.40% pace year-on-year.The average interest rate on bank deposits in June was 0.95%, eight basis points below average level the previous month. As compared to the same period in the previous year, average deposit rates decreased by 52 basis points from 1.47% to 0.95%.Growth in bank lending accelerated in the twelve months to June: total loans, denominated in both euro and other currencies, issued by all banks in Italy increased 6.64% year-on-year. In detail, total loans in the Italian banking system reached 1,007 billion euro with a net inflow of 63 million euro in new loans as compared to 30 June 2002. Lending growth has apparently been sustained almost exclusively by the medium/long-endsegment. In fact, medium/long-term bank loans increased 11.81% in the year to 30 June 2003 while short-term loans increased only 1.12%.The average lending rate fell further in June 2003, in line with the ECB's monetary policy stance, reaching 5.08%, 71 basis points lower than the year-before period. As at end-April 2003, non-performing loans net of write-offs amounted to 19,744 million euro, an increase of 381 million euro as compared to March 2003 and of only 29 million euro as compared to April 2003. The net non-performing loans/total loans ratio stood at 1.96% as at end-April 2003, down from 2.08% a year earlier. The fact that lending quality remains high is also shown by the decline in the net non-performing loans/surveillance capital ratio from 11.43% as at 30 April 2002 to 10.80%.

3. Group strategic guidelines and business policies

In this section we illustrate the main events affecting Gruppo bancario Credito Valtellinese in the first half of 2003.

New Strategic PlanDuring the period the Group began the necessary groundwork for drawing up its new strategic plan.The new plan will summarise the objectives, the operating guidelines, and the strategic projects to be pursued with a view to the Group's medium/long-term growth.

Julius Baer Creval Private BankingAfter having received Bank of Italy authorisation, Julius Baer Creval Private Banking beganoperating in May. The bank was formed by the transformation of Banca Popolare di Rho into a specialised bank offering private banking services. As part of the transaction, Credito Artigiano acquired the Banca Popolare di Rho retail business unit, effective as of 1st March 2003, consisting of five branch offices operating in the province of Milan. As a result, Credito Artigiano had gained a foothold in the north Milan province area and it is the only Group bank operating in the province as a whole. In June, Credito Valtellinese S.c. a r.l. finalised the sale of 51% of its equity investment in Julius Baer Creval Private Banking S.p.A. to Julius Baer Holding Ltd. of Zurich for 13.5 million euro.The members of the new company's Board of Directors are Messrs. Giovanni De Censi (Chairman), Thomas Baer (Vice Chairman), Renato Bartesaghi, Raymond Baer, Miro Fiordi, and Filippo La Scala (Board member). In addition, the Board nominated Mr. Maurizio Sella as General Manager.

Semi-annual Report as at 30 June 2003

— 21 —

Aperta Fiduciaria S.r.l.After having received Bank of Italy authorisation, Aperta Fiduciaria S.r.l. became part of Gruppo bancario Credito Valtellinese in June. Bancaperta formed the company in late 2002 for the purpose of expanding the range of services on offer to the Group banks' private customers and of providing new tools to the network, in particular concerning the private banking organisation and corporate finance.

Equity InvestmentsDuring the course of the first half 2003, Credito Valtellinese increased its controlling stake in Credito Artigiano from 63.34% to 65.17%. This increase was achieved through both market transactions and the conversion of the expiring instalment of the "Credito Artigiano TV 1994-2004convertibile subordinato" bond.

During the period, Credito Valtellinese also increased its equity investment in Banca dell’Artigianato e dell’Industria from 7.9% to 13.3% through the conversion of the “B.A.I. TV 2000-2005 convertibile subordinato” bond and the exercise of the attached warrants. As at end-June, the Gruppo Credito Valtellinese controlling stake in Banca dell’Artigianato e dell’Industria amounted to 58.45%, including the 45.15% held by Credito Artigiano.

Among the most important changes occurring during the first six months of the year regarding equity investment was the definition of the ownership structure for Julius Baer Creval Private Banking, the private banking joint-venture started up in partnership with Julius Baer. Credito Valtellinese's stake in Banca Popolare di Rho had grown steadily until it sold the majority of the share capital to its Swiss partner. After the transaction, the Parent company's investment was reduced to 47.9%.

In the first half 2003, Credito Valtellinese also strengthened its position as the main shareholder in Istituto Centrale delle Banche Popolari through the acquisition of 276,235 shares, lifting its investment to 22.5% of share capital, the upper limit obtainable by a single banking Group in accordance with the provision of the Milan-based bank's Articles of Association.

Among transactions affecting other Group companies, we point to Credito Siciliano's acquisition of a 10% stake in Bancaperta held by Julius Baer after having received Bank of Italy authorisation.

The “Banc@perta” Line

During the course of the first half 2003, the Group continued to expand the range of services offered through the Internet. In particular, during the period the Group made available to all its customers the Post@inlinea service, a new method of electronic communication allowing customers to view and save on the web all correspondences in relation to transactions executed with the several Group banks. In addition, subscribers to the banc@aperta service can use the new functions. In particular, in the "Tax" section, the new "Pagamento RAV" function is available, allowing customers to pay RAV pay- in forms directly from home. Customers can view and print a payment receipt for all transactions executed. In addition, the banc@perta line has been enhanced with the "Movimenti Carte di Credito Key Client" function, allowing customers to view payments, according to various selection criteria, made through Key Client credit cards issued by the Gruppo Credito Valtellinese banks.During the course of the half-year period, in pursuit of its objective to satisfy the needs of the owners of "Linea Cart@perta" products (the prepaid card line providing a new and easy-to-usepayment method) the Group made new functions available such as, for example, an increase in the spending limit to 10,000 euro. In addition, with Cart@perta, customers can activate and customise the automatic and periodic recharge and withdraw cash at all ATM-Bancomat stations into Italy under favourable conditions. Finally, customers in possession of Cart@perta can receive transfer

Semi-annual Report as at 30 June 2003

— 22 —

payments on the card and, starting on 1st July 2003, according to plan, all recharges through the banc@perta Internet service will be free of charge. As at 30 June 2003, the banc@perta line had 136,377 customers, a 13.9% increase over 119,710 as at year-end 2002. Among the innovative products offered through the Internet, we point to the @pertacity portal which as at end-June 2003 counted 755 agencies, associations, service and marketing companies as well as craftsmen and businessmen acquiring space in the Group's portal.

Development of the Group marketing organisationIn the first half 2003, Gruppo bancario Credito Valtellinese was committed to consolidating the scope of operations, selling the business unit consisting of the retail operations of Banca Popolare di Rho to Credito Artigiano on 1st March 2003. The sale involved five branch offices operating in the province of Milan. The Group's local network expanded further during the six months to June with the opening of four new branch offices, bringing the total to 305.The Parent company Credito Valtellinese established a presence in Mozzato and opened an agency in Appiano Gentile. Meanwhile, Credito Artigiano started up agency 19 in Milan. Credito Siciliano transferred two agencies, agency 2 of Mascalucia to Taormina (province of Messina) and agency 2 of Syracuse to Catania, and it opened agency 8 in Catania. Finally, Banca dell’Artigianato e dell’Industria opened a branch office in Rovato.

Marketing operations In the bancassurance area, the range on offer was expanded with three new and highly innovative products developed in co-operation with the subsidiary Global Assicurazioni: Global Rewind, Global Cedola, and Global Orizzonti. Global Rewind is a policy linked to the performance of a basket of mutual funds, investing the premiums paid by customers on the markets plus a further amount added by the insurance company.When the seven-year contract expires, the insurance company will pay back the initial capital invested (including the additional component) plus 66% of any increase earned on the investment in the linked basket of mutual funds. Global Cedola is a product targeted to investors with a preference for investing in securities with guaranteed capital and a minimum guaranteed income paid annually in the form of a coupon: two such issues were placed during the six months to June. In detail, these policies are linked to the performance of a special insurance fund investing mainly in bonds. Each year, the fund pays the customer a coupon equal to 100% of the its operating performance which in any case cannot be less than the pre-set minimum guaranteed yield. Global Cedola offers the usual advantages featured in life policies, with a minimum initial investment of 5,000 euro and a five-year contract term. Global Orizzonti is a policy consisting of a bond base (guaranteeing the repayment of capital at expiration and two certain annual coupons of 2.5% and 3.0%, respectively) and an option linked to the performance of a pre-defined basket of shares determining the amount of the remaining four coupons. As a result of this particular option structure, Global Orizzonti allows investors to benefit from both positive and negative fluctuations in the basket of stocks. Global Orizzonti has a minimum initial investment of 2,500 euro and a six-year contract term.During the first half 2003, the Group carried out intensive marketing operations in connection with the repatriation and regularisation of capital held abroad known as the "tax shield". The law was re-proposed with several amendments changing some application methods and extending the tax shield program also to juridical persons. As a result of Bancaperta's experience in the tax area and the major partnerships forged, Gruppo Credito Valtellinese has prepared a package of products and services designed to take advantage of these opportunities. In February, owners of the “Credito Valtellinese 2% 1999-2004” bond were given the option to convert half of the bond instalment payment coming due into Credito Valtellinese shares and to

Semi-annual Report as at 30 June 2003

— 23 —

receive, in case of conversion, a premium generated by the stock market indexes to which the bond issue is linked, equal to 5.52 euro for every 100 euro of the bond payment amount coming due. Finally, there was also a major development in the area of payment settlements for Internet purchases: the introduction of the Bankpass Web service targeted to tradespeople wishing to take advantage of the chance to market their products made available by the recent technologicalinnovations. The main advantage of the service is the expansion of the payments tools usable for Internet transactions through the introduction of ATM cards and pre-paid cards, resulting in a noticeable increase in customer potential for tradespeople taking part in the program. In addition, Bankpass Web lets tradespeople identify the buyer at the act of sale, taking away all risks of dispute in the buy transaction. Moreover, Bankpass Web can be perfectly integrated with company management systems and is particular effective for the management and control of payment operations, permitting users to continuously monitor the status of the orders input through the Web, among other things.

Asset Management at BancapertaFor the second consecutive year in May, Bancaperta was among the top performers in the standings of the category Italy equity funds/Sicavs in several European countries acting as advisor for the Gruppo Credito Valtellinese fund Italy Stock Julius Baer Multicooperation. In detail, in the 2002 standings drawn up by Standard & Poor's Fund Services, Bancaperta earned the number one spot in Germany and Austria out of a total of 23 and 20 funds, respectively. The bank also earned the number two spot in Switzerland, out of a total of 24 funds, and Luxembourg (35 funds). Finally, the Italy Stock Julius Baer Multicooperation fund earned the number four spot in Italy out of a total of as many as 200 funds. The asset management area was also slotted in the Lipper Leaders For Preservation categorystandings, earning a top position. Lipper is a primary information provider for Reuters, specialising in fund research. Bancaperta earned the number two spot in its classification compiled for the second edition of the Lipper Fund Awards – Italy 2003. The certificate awarded to Bancaperta for the results achieved by the Julius Baer Italian Stock Fund reflect its ability to preserve capital over time in its particular asset class.

Euro Medium-Term Notes Issue ProgramAs part of the "Euro Medium Term Notes" (EMTN) program, in April Credito Valtellinese issued a 150 million euro, lower tier II, variable rate 10-year subordinate bond with an option for early repayment in the fifth year. Through the single issues executed by the Group banks, the EMTNprogram gives the Group access to international capital markets with a view to implementing a financing policy based on efficiency and flexibility criteria.

Quality CertificationIn June, Credito Siciliano obtained the renewal and expansion of its UNI EN ISO 9001:2000 certification for its quality control operating system.

Credito Siciliano was the first bank in Sicily to receive a quality certification in 2001. The CISQUERT Certification Committee, an agency of the CISQ Federation, renewed its recognition of the bank's general management services and the services provided to the branch offices of the former Banca Popolare Santa Venera and their extension to the branch offices of the former Banca Regionale Sant'Angelo and Cassa San Giacomo.

New Members of the Parent Company's General Management Team

Meeting after the Shareholders' Meeting held on 26 April, the Credito Valtellinese Board ofDirectors nominated Mr. Giovanni De Censi as Chairman of the Board (formerly the Bank's executive director since 1996). Later, on the new Chairman's proposal, the Board of Directors

Semi-annual Report as at 30 June 2003

— 24 —

nominated Mr. Renato Bartesaghi (formerly the Bank's general manager since 1996) as the new executive director for Credito Valtellinese. The position of General Manager was entrusted to Mr. Miro Fiordi, and Mr. Giovanni Paolo Monti was nominated as First Vice General Manager, assisted by Mr. Franco Sala nominated Vice General Manager. After the new nominations, the Credito Valtellinese Board of Directors consisted of the following: Mr. Giovanni De Censi, Chairman; Mr. Salvatore Vitali (Vice Chairman); Renato Bartesaghi (Executive Director). The Bank's general management team consists of: Mr. Miro Fiordo (General Manager); Mr. Giovanni Paolo Monti (First Vice General Manager); and Franco Sala (Vice General Manager).

Bank of Italy Inspection

The Bank of Italy's surveillance agency carried out an inspection during the half-year period, involving the Parent company Credito Valtellinese, Credito Artigiano, Bancaperta, and Cassa San Giacomo.

Semi-annual Report as at 30 June 2003

— 25 —

4. Operating performance in the first half 2003

Gruppo bancario Credito Valtellinese continued its positive growth into the first half 2003.

RECLASSIFIED CONSOLIDATED FINANCIAL STATEMENTSRECLASSIFIED BALANCE SHEET (in thousands of euro)

ASSETS 30/06/2003 31/12/2002 30/06/2002Change%

(1)Cash and deposits with central banks and post offices 73.876 110.245 70.913 -32,99%

Due from banks 777.068 723.864 319.519 7,35%

Loans to customers 6.872.316 6.664.462 6.059.244 3,12%

Dealing securities 1.059.283 938.724 1.555.146 12,84%

Fixed assets

- securities 49.164 55.132 63.182 -10,82%

- equity investments 62.421 61.556 69.691 1,41%

- tangible and intangible assets 274.600 269.574 263.527 1,86%

Goodwill arising on consolidation and application of the equity method

111.295 116.364 113.613 -4,36%

Other asset items 406.836 490.639 413.705 -17,08%

Total assets 9.686.859 9.430.560 8.928.540 2,72%

(1) Calculated with respect to the previous year.

LIABILITIES AND SHAREHOLDERS’ EQUITY 30/06/2003 31/12/2002 30/06/2002Change%

(1)Due to banks 151.221 428.678 397.666 -64,72%

Direct deposits from customers (2) 8.049.982 7.633.984 7.209.611 5,45%

Other liabilities items 474.299 411.257 393.488 15,33%

Reserve for specific use 134.855 152.056 129.485 -11,31%

Subordinated liabilities 299.642 226.121 207.758 32,51%

Minority interests 132.847 137.102 151.554 -3,10%

Shareholders’ equity 444.013 441.362 438.978 0,60%

Total liabilities and shareholders’ equity 9.686.859 9.430.560 8.928.540 2,72%

(1) Calculated with respect to the previous year.

(2) Includes the items 20 “Due to customers”; 30 “Securities issued”; 40 Public funds administered”.

GUARANTEES AND COMMITMENTS 30/06/2003 31/12/2002 30/06/2002Change%

(1)Guarantees given 736.643 657.686 625.098 12,01%

Commitments 365.698 277.164 235.222 31,94%

(1) Calculated with respect to the previous year.

Semi-annual Report as at 30 June 2003

— 26 —

DepositsAs at 30 June 2003 direct customer deposits2 amounted to 8,349.6 million euro, a 6.2% increase from 7,860.1 million euro at year-end 2002. In particular, the item "due to customers" (including current accounts, savings deposits, and repurchase agreements) increased 6.9% to 5,995.1 million euro, while "securities issued" (including bonds, certificates of deposit, and other securities)increased 1.2% to 2,054.8 million euro. Direct customer deposit also includes subordinate loans, amounting to 299.6 million euro as at 30 June 2003, a 32.5% increase during the six-month period.Consolidated indirect deposits amounted to 9,057.2 million euro, a 6.6% increase as compared to year-end 2002. A breakdown of its components shows the following: assets under management increased 1.9% to 4.486.2 million euro, assets under management rose 10.5% to 3,798.7 million euro, and insured assets climbed 18.76% to 772.3 million euro.

Total Group funding – including both direct and indirect customer deposits – amounted to 17,406.8 million euro, a 6.4% increase from 16,356.6 million euro as at year-end 2002.

LoansAs at 30 June 2003, customer loans issued amounted to 6,872.3 million euro, a 3.1% increase as compared to year-end 2002. During the six-month period the increase in loans issued was guided by a careful selection policy based on counterparty solvency. Net non-performing loans amounted to 253.3 million euro at the end of the period. The ratio of non-performing loans to total customer loans, an indicator of credit quality, was 3.7%, basically unchanged from year-end 2002. The degree of coverage for non-performing loans was 57.5% of the gross value 3.

Securities portfolio The total value of the securities portfolio amounted to 1,108.4 million euro, an 11.5% increase from 993.9 million euro as at year-end 20024. Non-fixed securities amounted to 1,059.3 million euro, while fixed securities, amounting to 49.1 million euro, accounted for 4.4% of the entire portfolio. The portfolio invests in treasury and similar securities (item 20) amounting to 231.4 million euro, in bonds and other debt securities (item 50) amounting to 708.8 million euro (83.9% of the entire portfolio), and in shares and other equity securities amounting to 178.2 million euro, for the most part shares in investment funds (Sicav shares and mutual fund shares) in the bond sector.It is also pointed out that the bond portfolio largely consists of interest-rate indexed instruments.

Net equityGroup consolidated net equity as at 30 June 2002 amounted to 444 million euro, up 0.6% from 441.4 million euro as at year-end 2002. The main events affecting net equity were: - the conversion of the second tranche of the “Credito Valtellinese 2% 1999-2004 index- linked,

convertibile, cum warrant, subordinato” bond, generating the issue of 3,159,671 shares for a total amount of 20.6 million euro, including 9.5 million euro in shares and 11.1 million euro in share premium reserves;

2 Includes the items: “20 – Due to customers”; “30 – Securities issued”; “40 – Third-party funds in custody”; “110 – Subordinate liabilities”.3 The degree of coverage is the ratio of write-downs to gross exposure to non-performing loans. 4 The aggregate "Securities portfolio" includes item 20 – treasury securities and similar admissible for refinancing at central banks"; item 50 – bonds and other debt securities; and item 60 – shares, quotas and other equity securities.

Semi-annual Report as at 30 June 2003

— 27 —

- a 20.5 million euro dividend pay-out;- the 6.3 million euro in consolidated profit for the period.

Gruppo Credito Valtellinese Operating PerformanceRECLASSIFIED INCOME STATEMENT (in thousands of euro)

1st half 2003

1st half 2002 2002

Change%(1)

Interest income and similar revenues 206.877 220.536 440.216 -6,19%

Interest expense and similar charges -84.903 -95.941 -192.974 -11,50%

Interest margin 121.974 124.595 247.242 -2,10%

Profit from companies carried at equity and dividends 4.909 5.080 13.406 -3,37%

Net commission 64.637 57.564 127.853 12,29%

Profits (losses) on financial transactions 9.311 1.366 12.389 581,63%

Other net revenues 20.054 20.070 41.520 -0,08%

Net interest and other banking income 220.885 208.675 442.410 5,85%

Administrative expenses -154.363 -143.125 -299.530 7,85%

a) payroll and related costs -88.136 -81.890 -167.977 7,63%

b) other administrative expenses -66.227 -61.235 -131.553 8,15%

Value adjustments to tangible and intangible fixed assets -22.706 -21.886 -47.136 3,75%

Gross operating result 43.816 43.664 95.744 0,35%

Net value adjustments to loans and provisions -14.248 -11.693 -24.482 21,85%

Provisions for risk and charges -2.490 -2.605 -7.187 -4,41%

Net value adjustments to financial fixed assets -38 -466 -948 -91,85%

Profit from operating activities 27.040 28.900 63.127 -6,44%

Extraordinary income (loss) 1.701 164 -457 937,20%

Gross profit 28.741 29.064 62.670 -1,11%

Income taxes for the period -18.734 -19.170 -38.975 -2,27%

Change in the reserve for general banking risks -2.310 -1.863 -4.353 23,99%

Profit for the period pertaining to minority interests -1.437 -2.086 -4.519 -31,11%

Net profit (loss) for the period 6.260 5.945 14.823 5,30%

(1) Calculated with respect to the same period in the previous year.

Interest income and similar revenues amounted to 122 million euro, a 2.1% decrease as compared to the first half 2002. The decrease was attributable to the decline in market interest rates which outpaced the rise in total customer deposits.Interest and other banking income amounted to 220.9 million euro, a 5.9% increase from 208.7 million euro in the first half 2002. The increase was attributable to the rise in net commissions and profits on financial transactions. In detail, net commissions grew 12.3% from 57.6 million euro in the year-before period to 64.6 million euro in the first half 2003. The volatile performance on the financial markets actually helped generate an increase in profits on financial transactions from 1.4 million euro previously to 9.3 million euro in the first half 2003.

Semi-annual Report as at 30 June 2003

— 28 —

Profits generated from companies consolidated according to the net equity method and dividends from equity investments amounted to 4.9 million euro, a 3.4% decrease as compared to the first half 2002. In detail: - profits from companies consolidated according to the net equity method amounted to 3.1 million

euro, up from 2.5 million euro in the first half 2002; - dividends paid to the Group from minority equity investments not included in the scope of

consolidation amounted to 1.8 million euro.

Payroll costs increased 7.6% from 81.9 million euro in the first half 2002 to 88.1 million euro, while other administrative expenses increased 8.2% to 66.2 million euro. The rise is attributable to the ongoing rationalisation of the Group structure, the development and promotion of new products,and the acquisition of Rileno S.p.A.

Value adjustments to tangible and intangible fixed assets increased 3.7% from 21.9 million euro previously to 22.7 million euro.

As a result of the foregoing items, operating profit amounted to 43.8 million euro, virtuallyunchanged from 43.7 million euro in the second half 2002. Provisions to risks and charges, net value adjustments to financial fixed assets, and provisions to risks and charges contributed 16.8 million euro in expenses to the income statement in the first half 2003. In detail: - 14.2 million euro for net adjustments to loans and provisions for guarantees and commitments; - 2.5 million euro in provisions to risks and charges.

Consolidated ordinary profit for the first half 2003 amounted to 27 million euro, down 6.4% as compared to the year-before period. Net extraordinary income amounted to 1.7 million euro, as compared to virtually zero in the first half 2002.The most important extraordinary item was the 2.3 million euro in capital gains generated from the sale of 51% of the equity investment held in Julius Baer Creval Private Banking. Taxes for the period amounted to 18.7 million euro, while the provision to the reserve for general banking risks amounted to 2.3 million euro, and 1.4 million in profit was attributable to minority interest. As a result, net profit for the period was 6.3 million euro, a 5.3% increase from 5.9 million euro in the first half 2002.

Expansion of the Group networkThe Group continued to expand its local presence during the course of the first half. The expansion included the opening of four new branches, bringing the total number of local branch offices to 305.In addition to this traditional type of outlet, the Group also expanded its alternative channels which now include 344 automatic teller machines, 10,005 points of sale, and 6,689 distance contracts for corporates (including 1,218 banc@pertaCBI contracts). Meanwhile, Internet contracts amounted to 136,377 as at end-June 2003.Group staff at the end of the period counted 2,981 persons, up from 2,951 as at year-end 2002. The growth in staff is a response to effective operating needs, both current and forecast, allowing the degree of efficiency to remain at satisfying levels. Human resources management features an intense program of professional training and skills-updating involving almost the entire staff for a total of 4,713 training days. Of this total, some 1,146 days were attributable to the Group's increasing use of distance training, including 840 daysin self- learning and 306 days in virtual classroom courses.

Semi-annual Report as at 30 June 2003

— 29 —

Performance outlookThe results for the first half 2003 were in line with forecasts, and management expects this type of performance to continue into the second half of the year. In the second half, the Group will continue to focus its attention on the e-business sector with a view to taking advantage of opportunities which may arise in this area. The Group will also continue to develop its business operations and strengthen those areas generating revenues from services which, in view of the rise in total volume, provides the basis for further increases in the Group's profitability in the second half of the year.

After the close of the period and as of the approval date for this report, no significant events occurred which may have had an impact on the operating results presented herein; ordinaryoperations continued according to the lines of development set and approved by the Board of Directors.

Semi-annual Report as at 30 June 2003

— 30 —

5. Information on the operating performance of the GruppoCredito Valtellinese companies

In this section we illustrate the operating performance of each of the Group companies individually.

Parent Company

Credito Valtellinese

In the first half 2003, Credito Valtellinese reported an increase in both net assets and operating profit in line with budget targets. Among the significant events affecting the Parent company's performance for the period was the change in the equity investments in the Group companies, illustrated in detail below. In January, the third tranche of the convertible subordinate bond issued by Credito Artigiano at the time of its stock market listing in July 1999 came due for repayment. As a result of the exercise of the conversion option, in conjunction with market transactions, the Parent company increased its equity investment in Credito Artigiano from 63.34% to 65.17%.In May 2003, Credito Valtellinese exercised its right to convert the third tranche of the subordinate convertible bond issued by Banca dell'Artigianato e dell'Industria, exercising also the attached warrant. As part of these transactions, the Parent company underwrote 385,728 new shares worth 2.4 million euro, lifting it equity investment in Banca dell'Artigianato e dell' Industria from 7.9% to 13.3%.In June, the Parent company Credito Valtellinese sold 51% of its equity investment in Julius Baer Creval Private Banking to Julius Baer Holding, resulting in the new company's exit from the Gruppo Credito Valtellinese scope of consolidation. The details of the transactions are illustrated in the section on the Group's strategy and business policies. Also among the significant events occurring during the half-year period was the conversion in February of the second tranche of the “Credito Valtellinese 2% 1999-2004 index- linked,convertibile, cum warrant, subordinato” bond. The conversion option was exercised almost in its entirety, generating the issue of 3,159,671 new shares effective as of 1st January 2003, increasing share capital by 6.1% from 154.3 million euro to 163.7 million euro. As part of the Euro Medium Term Notes” (EMNT) program, during the six-month period the Parent company Credito Valtellinese issued a 10-year, 150 million euro, lower tier II, variable-ratesubordinate bond. To ease access to capital markets and improve the Bank's visibility internationally, the Parent company submitted to an annual review by the rating agency Moody's Investors Service, assigning it a Baa1 credit rating. Following the opening of two new branches, one in Mozzate and the other in Appiano Gentile, as at 30 June 2003 the Parent company has 85 branch offices. In addition to the local network, for some years now Credito Valtellinese provides its customers with the opportunity to use the Internet channel; the number of customers subscribing to the Internet banking service increased from 36,988 as at year-end 2002 to 41,585. These figures testify to the widespread use of this innovative channel for access to banking services.As at 30 June 2003, Credito Valtellinese counted 777 registered employees, mostly unchanged from year-end 2002.The Bank of Italy carried out inspections at Credito Valtellinese during the course of the half-yearperiod.

Semi-annual Report as at 30 June 2003

— 31 —

Balance Sheet HighlightsTurning now to total funds, at the end of the first half 2003, direct customer deposits amounted to 3,213 million euro, a 5.3% increase from 3,051.2 million euro as at year-end 2002. The different types of direct deposits showed different growth rates. In detail, short-term amounts due to customers amounted to 1,607.1 million euro, a 5.9% increase attributable to the contribution of current accounts, while customer term deposits decreased from 277.7 million euro as at year-end2002 to 246.1 million euro. Customer deposits in the form of securities issued, certificates of deposit, and other securities amounted to 1,128.5 million euro, mostly unchanged as compared to year-end 2002. As for subordinate liabilities, the Bank executed two transactions during the half-year period bringing the item to 231.2 million euro: in February, the expiration of the second tranche of the convertible subordinate bond, reducing subordinate liabilities by 43 million euro; and the issue of the 10-year, 150 million euro, lower tier II, variable-rate subordinate bond with the option of early repayment in the fifth year. Indirect deposits amounted to 3,487.7 million euro, rising 5.7% from 3,299.1 million euro as at year-end 2002. In detail, assets under management amounted to 1,755.3 million euro, a 5% increase in the six months to end-June, while assets under management, including both private assets and mutual funds, increased 5.5% since the beginning of the year to 1,400.4 million euro, accounting for 40-2% of total indirect deposits. Finally, deposits in the form of insurance reached 332 million euro as at end-June, a 10.6% increase as compared to year-end 2002.

The Parent company's total deposits (the sum of direct and indirect deposits) reached 6,700.7 million euro as at end-June 2003, a 5.5% increase as compared to year-end 2002As at 30 June 2003, loans to customers reached 2,430.5 million euro, a 2% increase in the six-month period.Among the Bank's customer receivables, net non-performing loans increased slightly from 45.1 million euro as at year-end 2002. The securities portfolio as at end-June 2003 amounted to 716.4 million euro, a 9% increase as compared six months earlier. The portfolio consists of 53.6 million euro in fixed securities held for stable investment purposes and the remaining 662.8 million euro of non-fixed securities. The Bank's own portfolio consists largely of indexed-rate debt securities, reflecting the conservative approach to the securities portfolio mix. At the end of the period, the value at risk (VaR) of the non-fixed portfolio measured over a 10-day time horizon with a 99% confidence interval amounted to 461,000 euro. During the course of the six-month period, VaR fluctuated between a high of 736,000 euro and a low of 420,000 euro, ending the period at 556,000 euro.Net equity as at 30 June 2003 amounted to 497.5 million euro, an increase of 25.7 million (or 5.5%) from 471.8 million euro as at year-end 2002.

Income statement Now turning to the analysis of the income statement, we note that interest income and similar revenues decreased 5.1% as compared the first half 2002, amounting to 35.5 million euro. The contraction was mostly attributable to the decline in interest rates, reflected in the narrowing of spreads, only partially offset by the increase in business volume.Income from services, including net commissions and other net revenues, increased 11.9% in the six months to June, reaching 72.9 million euro. A breakdown of the individual components shows that net commissions increased 2.1% to 16.4 million euro, while net other operating revenues grew 15% from 49.1 million euro in the first half 2002 to 56.5 million euro, boosted by the 44.6 million euro contribution from leasing fees.Profits on financial operations amounted to 4.1 million euro, including 2.1 million euro in profit on securities trading and 2.0 million euro on currency trading.

Semi-annual Report as at 30 June 2003

— 32 —

As a result of the above components, and including dividends which increased 29.6% as compared to the first half 2002, interest and other banking income rose 13.4% from 126.4 million euro previously to 143.3 million euro. Operating costs, including administrative expenses and value adjustments to tangible and intangible fixed assets, amounted to 95.8 million euro, an 11.8% increase. In detail, payroll and related costs increased 7.7% as compared to the first half 2002, while other administrative expenses rose 13.8% attributable to the increase in fees paid to the auxiliary companies, and value adjustments to tangible and intangible fixed assets reached 41.4 million euro, including 37.8 million euro for thedepreciation of leased assets. Gross operating margin amounted to 47.5 million euro, a 16.7% increase from 40.7 million euro in the first half 2002. Subtracting from gross operating margin the 5.8 million euro in value adjustments to loans and provisions for risks and charges, operating profit amounted to 41.8 million euro, a 21% increase as compared to the first half 2002. Extraordinary income amounted to 1.7 million euro, mainly consisting of the capital gain generated by the sale of 51% of the equity investment in Julius Baer Creval Private Banking S.p.A. to Gruppo Julius Baer, and income taxes for the period amounted to 17.1 million euro. As a result, net profit for the period was 26.4 million euro, a 44% increase as compared to the first half 2002.

Shareholders'equity

of which: net results

Shareholders'equity

of which: Net results

Balances as per Parent Bank financial statements 497.537 26.377 471.780 26.350

Results of equity investments reported in their statutory financial statements- consolidated line-by-line 11.788 11.788 18.025 18.025- carried at equity 3.032 3.032 7.758 7.758

Amortization of positive differences- relating to the current year (9.572) (9.572) (18.779) (18.779)- relating to previous years (102.241) - (84.114) -

Differences with respect to the book values, relating to:- companies consolidated line-by-line 51.548 54.433- companies carried at equity 13.102 11.563

Adjustment for dividends received during the year:- relating to prior year profits - (22.003) - (17.045)- relating to current year profits - - - -

Other consolidation adjustments:- reversal of items exclusively for tax purposes 4.290 (568) 4.854 496- elimination of infraGroup gains and losses (25.471) (2.794) (24.158) (1.982)

Balances as per consolidated financial statements 444.013 6.260 441.362 14.823

RECONCILIATION OF THE SHAREHOLDERS' EQUITY AND NET RESULTS OF THE PARENT BANK ANDTHE CORRESPONDING GROUP BALANCES (in thousands of Euro)

30/06/2003 31/12/2002

Semi-annual Report as at 30 June 2003

— 33 —

Credito Artigiano

During the half-year period Credito Artigiano completed the acquisition of the retail business unit of Banca Popolare di Rho consisting of five branch offices located in the province of Milan in the municipalities of Rho and Canegrate, allowing the bank to strengthen its local presence in the north Milan province area. The transaction was part of a wider corporate restructuring program at the Group level.The balance sheet and income statement data for the first half 2003 show that the growth trend is continuing.Direct deposits, including amounts due to customers, securities issues, and subordinate liabilities, amounted to 3,216.7 million euro as at 30 June 2003, up 10% as compared to year-end 2002. Indirect deposits increased 5.3% from 3,561.3 million euro as at 31 December 2002 to 3,749million euro. The item included a 10% increase in assets under management, reaching 4,468.2 million euro, while insured assets amounted to 1,468.2 million euro, a 10.6% increase. Total deposits, the sum of direct and indirect deposits, amounted to 6,965.7 million euro, a 7.4% increase.Loans to customers continued to grow in the six months to June, reaching 2,607.3 million euro, a 4.2% increase from 2.502.7 million euro as at year-end 2002. The selective credit management policy is reflected in the relatively low 1.8% net non-performingloans to total loans ratio, basically unchanged as compared to six months previously.The change in equity investments during the period was entirely attributable to the underwriting of shares in Banca dell'Artigianato e dell'Industria deriving from the conversion of the third tranche of the convertible subordinate bond issued by the Brescia-based bank. Net equity at end-June amounted to 309.6 million euro, a 6.5% increase from 290.8 million euro six months previously. The rise is explained by the conversion of the third tranche of the Credito Artigiano 1994-2004 bond issued at the time of the stock market listing, generated a capital increase from 112.9 million euro to 122.7 million euro.Turning to the income statement, interest income and other revenues reached 42 million euro, a 2.8% increase as compared to the first half 2002, showing that the growth in business volume offset the further narrowing of spreads. Income from services, the sum of commissions and revenues from customer services, amounted to 31 million euro, a 22.3% increase from 25.4 million euro in the first half 2002, attributable to the start-up of leasing operations. Dividends, deriving almost exclusively from the equity investment in Bancaperta, amounted to 2.9 million euro, up from 1.4 million euro in the first half 2002. As a result of the above items, interest and other banking income increased 15.7% year-on-year to 78.7 million euro. Operating costs, including administrative expenses and value adjustments to tangible and intangible assets, amounted to 58.2 million euro, an 18.1% increase from 49.3 million euro in the first half 2002. In detail, payroll and related costs amounted to 22 million euro, mostly unchanged from the year-before period, while other administrative expenses increased from 23 million euro to 27 million euro and value adjustments to tangible and intangible assets rose from 4.4 million euro to 9.2 million euro. Gross operating margin amounted to 20.4 million euro, a 9.4% increase as compared to the first half 2002.Value adjustments to loans and provisions for risks and charges amounted to 5.9 million euro, up from 5.3 million euro in the year-before period. As a result, profit from ordinary operations amounted to 14.5 million euro, an 8.4% increase from 13.4 million euro in the first half 2002.

Semi-annual Report as at 30 June 2003

— 34 —

After taxes due for the period, net profit amounted to 7.9 million euro, a slight 0.4% increase as compared to the year-before period. As at end-June 2003, the Credito Artigiano network consisted of 85 branch offices.

Credito Siciliano

Credito Siciliano was formed by the merger of Banca Popolare Santa Venera S.p.A. andLeasingroup Sicilia into Banca Regionale Sant'Angelo. As such it completed its first year ofoperations on 30 June 2003. The comparison with the first six months reflects Credito Siciliano's July 2002 acquisition of the branch network of Cassa San Giacomo whose strategic role is now to co-ordinate credit risk on behalf of the entire Group. As at 30 June 2003, direct deposits amounted to 1,856.2 million euro, a 0.8% increase from 1,841.9 million euro six months earlier. Indirect deposits exceeded 1,186 million euro, a 14.9% increase as compared to year-end 2002. In detail, assets under management amounted to 138.8 million euro, rising 57.6% during the six-month period, whole direct investments in mutual funds reached 330.4 million euro, a 24.3% increase. Insured assets also enjoyed strong growth, rising 64.7%,attributable to the placement of innovative bancassurance products. Total deposits as at 30 June 2003 amounted to 3,042.6 million euro, a 5.8% increase as compared to year-end 2002.Loans amounted to 1,152.7 million euro, rising 4.9% in the six months to end-June. The bank's lending operations play a significant role in Sicily's economic development. Turning to the income statement, interest income and similar revenues reached 31.6 million euro, a 6.4% increase as compared to the first half 2002. Commissions from customer services rose 19.3% and profits on financial transactions increased by 900,000 euro, lifting interest and other banking income to 68.3 million euro, an 8.6% increase as compared to the year-before period. Operating costs amounted to 64.5 million euro, a 9.5% increase. The item includes 25.4 million euro in payroll and related costs, 24.1 million euro in other administrative expenses, and 15 millioneuro in value adjustments to tangible and intangible assets.

Gross operating margin amounted to 3.7 million euro, a 3.7% decrease from 3.9 million euro in the first half 2002. Profit from ordinary operations, net of depreciation and amortisation, adjustments and provisions, amounted to 1.3 million euro, a 53.3% increase as compared to the year-before period. Extraordinary income amounted to 1.8 million euro and taxes 2.5 million euro. As a result, net profit amounted to 629,000 euro as compared to the break-even result in the first half 2002. As at 30 June 2003, the Credito Siciliano network consists of 130 branch offices.

Banca dell’Artigianato e dell’Industria

In the first half 2003, Banca dell'Artigianato e dell'Industria reported a continuation of the growth trend in terms of total assets and profit margin on ordinary operations. In detail, direct deposits amounted to 91.9 million euro in the first half 2003, a 57.1% rise as compared to year-end 2002, while indirect deposits amounted to 30.5 million euro. Total customer deposits, the sum of direct and indirect deposits, reached 122.4 million euro, a 29.9% increase.In response to the demand for credit in the local area where the bank operates, loans to customers grew 25% from 88.7 million euro as at year-end 2002 to 110.9 million euro in the six months to June.

Semi-annual Report as at 30 June 2003

— 35 —

Turning to the income statement, interest income and similar revenues increased 39.3% to 2 million euro, and interest and other banking income rose 33.8% to 2.6 million euro.Operating costs amounted to 2.2 million euro, a 15.4% increase from 1.9 million euro in the first half 2002. Gross operating margin amounted to 390,000 euro, a vast improvement from the break-even result in the year-before period. After adjustments to loans and provisions to taxes, the net result for the period was a 607,000 euro loss.As at end-June 2003, Banca dell’Artigianato e dell’Industria operates through 5 branch offices plus the agency in Iseo added in July.

Bancaperta

Bancaperta is not only the Group's web bank, it is also the sole manager for the Group's financial operations with a particular focus on asset management, private banking, corporate finance, and bancassurance. The results for the first half 2003 show that Bancaperta continues to put in a solid performance.

Direct customer deposits, consisting of amounts due to customers and securities issued, amounted to 351.8 million euro as at 30 June 2003, a 6.6% increase from 330.2 million euro six months earlier. Indirect deposits grew 5.4% from 4.076.1 million euro as at year-end 2002 to 4,294.3 million euro. In detail, assets under management increased 15.3% to 48.1 million euro, assets under management rose 4.2% to 3,812.1 million euro, and insured deposits reached 195 million euro, upsignificantly in the six months to end-June.Turning to the income statement, interest income and similar revenues reached 79,000 euro, showing an increase over the first half 2002. Interest and other banking income amounted to 29.2 million euro, down 17.8% from the year-before period due to the 35.6% reduction in net revenues from leasing operations which are steadily winding down. Operating costs decreased 17.7% as compared to the first half 2002 as result of lower depreciation costs on leased assets.As a result of the above components, profit on ordinary operations amounted to 6.1 million euro, down 16.8% from 7.3 million euro in the first half 2002 as a result of the decrease in extraordinary income.Net profit for the period amounted to 3.7 million euro, down 17.1% from 4.5 million euro in the first half 2002. The banc@perta line of online services continued to grow during the first half, surpassing 136,000 customers as at 30 June 2003.

Cassa San Giacomo

On 30 June 2003, Cassa San Giacomo completed its first year of operations as the Group's management centre for credit risk and non-performing loans as well as legal advisory and complete servicing for leasing operations. In commenting on the change in total assets and the income statement highlights, the influence of the extraordinary events in connection with the redefinition of the business model should be borne

Semi-annual Report as at 30 June 2003

— 36 —

in mind: in the first half 2002, the bank was involved exclusively in traditional retail operations, while in the first half 2003 Cassa San Giacomo was fully involved in operating in the new areas assigned to it. As a consequence, data comparisons between the first half 2003 and the year-before period are not significant.Total deposits decreased a slight 1.6% from 165.5 million euro as at year-end 2002 to 162.9 million six months later. Loans amounted to 140 million euro at the end of the period, down 5% from year-end 2002. This amount consists entirely of non-performing loans attributable to Cassa SanGiacomo itself and those acquired from Credito Siciliano.Turning to the income statement, interest income and similar revenues amounted to 481,000 euro, while interest and other banking income amounted to 7.4 million euro in the first half 2003. The latter item included 6.9 million euro in other net revenues, including fees received for contracted services rendered to the Group banks. Operating costs amounted to 5.3 million euro, including a rather low level of payroll and related costs attributable to direct staff, while other administrative expenses reached 5.2 million euro, almost entirely attributable staff seconded from Group companies. Gross operating margin amounted to 2 million euro in the first half 2003. As part of its careful monitoring of non-performing loans, the bank appropriately set aside 2.7 million euro in provisions to value adjustments for loans. Net extraordinary income amounted to 1.2 million euro and taxes for the period 479,000 euro. As a result, net profit for the period was 27,000 euro.

Rileno

Rileno's operations in the first half were strongly influenced by legislation concerning a tax amnesty leading to, on the one hand, a slowdown in typical tax collection operations and, on the other, an increase in commission income. As for organisation, the action plan to fully integrate the company into the Group structure was successfully implemented. Also satisfactory was the launch ofbusiness plan for local taxation as well as the start-up of the action plan leading to the ISO 9001 quality certification by the end of this year. Net profit for the period amounted to 288,000 euro. Settlement of outstanding receivablesamounted to 604,000 euro, while interest expense totalled 677,000 euro, directly attributable to taxes due collected at the beginning of the year.

Deltas

During the first half 2003, Deltas' operations focused on supporting the formulation and control of the Group's unified strategic planning, the centralised management and provision of assistance and advisory services, and operations and research support for all the Group companies. Net profit for the period amounted to 63,000 euro, mostly in line with the budget target.

Stelline Servizi Immobiliari

In the first half 2003, the company provided property services on behalf of the Group banks. In detail, operations focus on research in real estate and urban planning, the development of building projects, and the construction of branch offices. Of particular importance was the adaptation and the completion of the Acireale complex.

Semi-annual Report as at 30 June 2003

— 37 —

During the half-year period, the company continued to develop its credit issue technical support evaluation operations as well as supervision of already-existing credit terms. Among its other operations, the company virtually completed the construction of the Centro di Interscambio in Bollate (province of Milan), as well as the preliminary urban planning procedure for the rehabilitation of the Carini-Marzotto area in Sondrio. Meanwhile, Stelline is continuing with the rehabilitation project for the abandoned industrial areas also in Sondrio, a major project for Gruppo Credito Valtellinese also in terms of financing.At the end of the period, Stelline's balance sheet showed 14.4 million euro in assets and the income statement 50,000 in net profit.

Bankadati Sistemi Informatici