Embed Size (px)

Citation preview

Select Committee on Labour Select Committee on Labour and Public Enterprises and Public Enterprises

8 March 20058 March 2005

Presentation on thePresentation on theSAFCOL Annual Report 2003/04SAFCOL Annual Report 2003/04

Charles Ntuli Sikkie Kajee

SAFCOL

Kobus Breed Joe Coetzer

Outline Outline

1. Introduction to SAFCOL Operations Map Video

2. Corporate Governance

3. Status of Privatisation Core Assets Non-core Assets Interest in privatised entities

4. Overview of performance against objectives

5. Financial Review 2004

Introduction to SAFCOL OperationsIntroduction to SAFCOL Operations[PMG note: map not included][PMG note: map not included]

Corporate Governance Corporate Governance

Code of Corporate Practices and Conduct

The Directors endorse the Code of Corporate

Practices and Conduct as set out in the King Report.

The Directors confirm the need to conduct the

business with integrity and in accordance with

generally accepted corporate practice.

Public Finance Management Act, 1999 (“PFMA”)

The PFMA became effective on 1 April 2000. As part of the implementation of the PFMA, there is an ongoing process of awareness, education, instruction and advice to the SAFCOL Board and employees.

The Board of Directors are the accounting authority of SAFCOL. The Directors comply with their fiduciary duties as set out in the Act. Since its inception in 1993, SAFCOL followed a policy of good corporate governance and sound accounting principles and internal control and as a result, comprehensive accounting policies, accounting procedures, internal control procedures, conditions of employment and disciplinary procedures, including a code of conduct, were prepared and documented and are well entrenched in the operations of the company.

As a substitute for the corporate plan and

shareholders’ compact, SAFCOL submitted a

privatisation framework, which outlines Government’s

privatisation objectives for SAFCOL. This privatisation

framework does not contain the performance

objectives as stated in the Chief Executive Officer’s

Report, other than the privatisation objective. The other responsibilities have been addressed by

SAFCOL, as far as practically possible, within the

constraints resulting from privatisation.

Except for one item listed below, SAFCOL complies

with the PFMA and Treasury Regulations in all

material respects with regard to the provisions

applicable to public entities.

• Projections of revenue, expenditure and

borrowings for a financial year are included in

the annual budget that is approved by the

Board. This approval does however not take

place at least one month before the

commencement of the financial year, but within

one month of such commencement.

Status of privatisation Status of privatisation

Eastern Cape North (Singisi)

Assets sold on 1/08/2001 to Singisi and obtained 25% shareholding in the company.

KwaZulu-Natal (SiyaQhubeka)

Sold 75% of the shares and shareholder’s loans to the Siyaqhubeka Consortium on 1/10/2001.

Eastern Cape South (AFC)

Negotiations completed in April 2003, awaiting implementation of forest lease agreement.

Southern and Western Cape (MTO)

Negotiations completed on 31/03/2004. Competition Commission approval received on 5/10/2004. Awaiting implementation of forest lease agreement.

Mpumalanga, Limpopo and KwaZulu Natal (KLF)

Negotiations completed on 31/03/2004. The Competition Commission prohibited this transaction. KLF and Bonheur (purchaser) are addressing the issue. The implementation of the forest lease agreement is in process.

No privations transactions were completed during the year under review in respect of the core assets. The status can

be summarised as follows:-

Core Assets In preparation for the eventual privatisation, SAFCOL acquired certain commercial forestry assets and business from DWAF at a nominal value.

Location of sale assets

Approximately planted area (ha)

Employees transferre

d

Effective date

Eastern Cape North

41 500 591 1 August 2001

Eastern Cape South

4 500 31 1 November 2001

Mpumalanga and Limpopo

17 000 357 1 November 2001

Total 63 000 979

The combined sale assets, comprising the major portion of businesses and commercial forestry assets of the company as well as the relevant portions of the commercial forestry assets and businesses acquired from DWAF were transferred to wholly-owned subsidiaries of SAFCOL, as follows :-

Location Company Effective date Includes DWAF

Eastern Cape North

Singisi Forest Products (Pty) Ltd

1 August 2001 Yes

KwaZulu-Natal Siyaqhubeka Forests (Pty) Ltd

1 October 2001 No

Southern and Western Cape

MTO Forestry (Pty) Ltd

1 November 2001

No

Eastern Cape South

Amatola Forestry Company (Pty) Ltd

1 November 2001

Yes

Mpumalanga and Limpopo

Komatiland Forests (Pty) Ltd

1 November 2001

Yes

Sold to Approx. planted area (ha)

Employees transferred

Net assets sold Rm

Net selling price Rm

Profit/(Loss) on disposal Rm

Singisi 60 000 1 129 40.6 17.1 (23.5)

Siyaqhubeka 22 000 91 30.9 100.0 69.1

MTO 85 000 1 119 78.4 78.5 0.1

AFC 15 000 243 7.1 5.4 (1.7)

KLF 129 000 2 148 335.5 384.0 48.5

TOTAL 311 000 4 730 492.5 585.0 92.5

The following table provides an indication of the impact of the said transactions :

Non-Core Assets The portion of the operations in KwaZulu-Natal not transferred to Siyaqhubeka Forests (Pty) Ltd and therefore remaining with SAFCOL, the St Lucia region, comprises of approximately 7 200 ha of commercial forestry plantations. Other assets remaining with SAFCOL are as follows :-Asset Location Effective

date

Avocado project Frankfort December 2004

Lakenvlei Forest Lodge Belfast Part of KLF sale

Lebanon Fruit Farm Trust

Grabouw July 2004

Lourensford properties Somerset West August 2001

Shannon properties Barberton Not sold

Valgrace Investments Pretoria September 2003

Wildflower project Longmore November 2004

Interest in privatised entities Up to 19% of SAFCOL’s interest in the privatised entities has been earmarked for disposal to the following entities :

Entity Portion of interest

A trust established in terms of the National Empowerment Fund Act,

105 of 1998Or

A trust established for the benefit of surrounding local communities

10%

Employee share ownership plan (“ESOP”)

Up to 9%; subject to a maximum of R10000 per employee

Overview of performance Overview of performance against objectives against objectives

POLICY OBJECTIVE RESULTProfitabilityTo achieve and sustain a return on capital in excess of the cost of capital.

Ensure that a commercially acceptable rate of return is achieved subject to constraints placed on the company due to it being a parastatal.

The required returns were not achieved due to various reasons discussed in more detail in the CEO report.

Sustainable Forestry ManagementTo manage the raw material resource of the company in a professional manner so as to ensure sustainability in the long term.

Harvest and market the annual roundwood yield of the Group of approximately 2,7 million m3, in an environmentally responsible manner.

2003/2004 actual log sales volume amounted to 2,58 million m3 which is in line with the target volume.

Internationalisation

To position the company as an international player in the forestry and forestry related industries.

Expand into Southern African countries in a responsible manner.

There are two timber plantation trials at Chimoio in Mozambique. Exceptional growth rates are being recorded.

An investment to purchase 80% shares in IFLOMA, the forestry parastatal in the Manica Province of Mozambique, amounting to US$450,000 has been made. This will benefit both Mozambique and the RSA in the spirit of NEPAD.

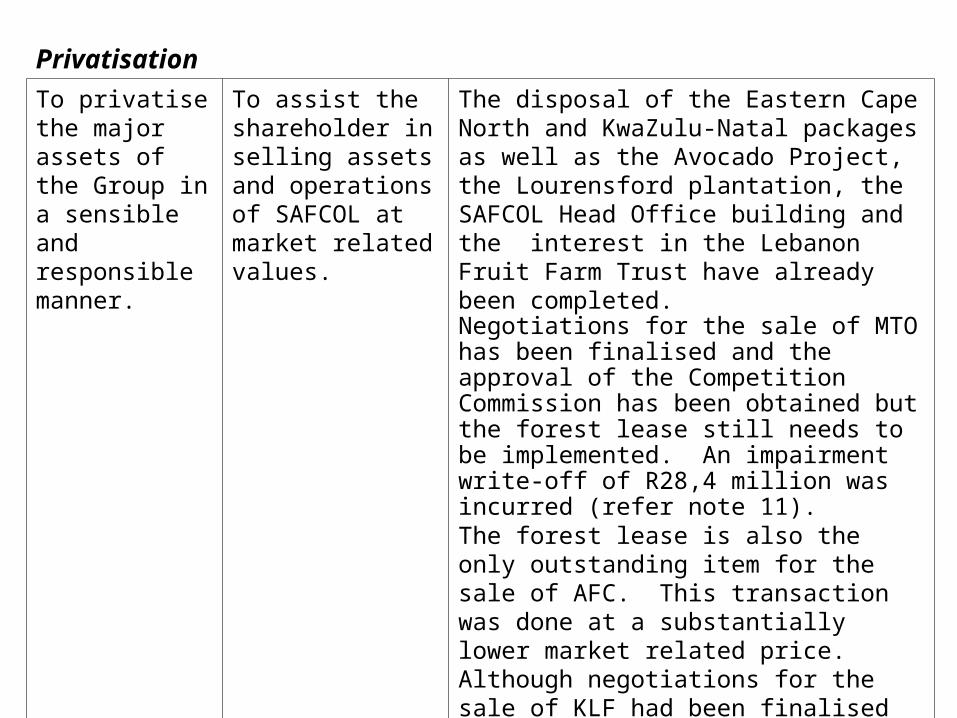

Privatisation

To privatise the major assets of the Group in a sensible and responsible manner.

To assist the shareholder in selling assets and operations of SAFCOL at market related values.

The disposal of the Eastern Cape North and KwaZulu-Natal packages as well as the Avocado Project, the Lourensford plantation, the SAFCOL Head Office building and the interest in the Lebanon Fruit Farm Trust have already been completed.Negotiations for the sale of MTO has been finalised and the approval of the Competition Commission has been obtained but the forest lease still needs to be implemented. An impairment write-off of R28,4 million was incurred (refer note 11).The forest lease is also the only outstanding item for the sale of AFC. This transaction was done at a substantially lower market related price.Although negotiations for the sale of KLF had been finalised some months ago the Competition Commission has now prohibited the transaction. Refer Directors report for further detail.

Enhancement of Sawmilling Technology

To upgrade SAFCOL’s sawmilling technology with a specific view to add value to our raw material.

Upgrade SAFCOL’s sawmills to international technology standards.Maximise the value of the raw material through appropriate recovery techniques and the utilisation of high quality material.

Superior product quality continues to be available to industrial markets.

Additional raw material is being sourced to ensure optimum plant utilisation.

In the short to medium term, SAFCOL’s technology policy is focused on mill specialisation, enhancing of drying facilities and value adding dry mills. However the sawmills, with the exception of the George sawmill, did not operate profitably due to various reasons.

Research & Development

To invest in research and development projects with the objective to enhance the quality and volume of the standing timber stock.

Increase SAFCOL’s mean annual increment by at least 10 % by the year 2020.

Continuous site-species matching, genetic research and improvement of silvicultural practices ensure that the objectives are met.

Seedlings and cuttings planted in SAFCOL originate from the top 10 Pine breeding programme families.

Tissue culture is successfully used to “bulk up” the best Eucalyptus material. As a result, superior genetic material is commercialised faster than through the conventional seed method.

Maintenance of Permanent Sample Plots (PSP) as part of the PSP programme is used for monitoring growing trends and growth modelling.

Employee Development

Development of SAFCOL employees to their optimum capabilities.

This is a continuous process to put as many employees as possible through development programmes, subject to employee and operational requirements.

Separately reported in Human Resources section of the CEO report.

Equality in Employment

SAFCOL is an equal opportunity employer, focusing on and addressing historical employment imbalances.

To have a competent and well-balanced employee profile by 2005 according to the guidelines prescribed in the Employment Equity Act.

Management have committed themselves to the implementation of employment equity and the development of employees. Own initiatives have however been disrupted by the impact of privatisation but targets have been set in the sales agreements entered into with the successful bidders.

Corporate Social Investment

To annually allocate a portion of the net profit of the company to corporate social investment. The amount so allocated is subject to affordability, i.e. actual realised profit.

Invest in the social upliftment of our employees and surrounding communities. Projects are identified and prioritised in consultation with applicable stakeholders.

An amount of R0,7 million has been allocated to Corporate Social Investment (CSI) projects in the financial year under review. In total the CSI expenditure since SAFCOL’s inception amounts to R16,9 million.

Environmental Management Philosophy (EMP)

To be one of the leading forestry companies in terms of environmental and conservation management.

To maintain Forestry Stewardship Council (FSC) certification where possible.Fully integrate health and safety into the Environment Management System.

FSC certification of all business units, other than the exit plantations of MTO and the St Lucia management unit has been maintained. NOSA safety standards are being strived for at all business units.

Financial Review Financial Review For the year ended 30 June 2004

FINANCIAL RESULTS

2004 2003 2002 2001 2000 Growth

R'000 R'000 R'000 R'000 R'000 %

(a) (b) (a-b)/b

REVENUE 681,958

677,257

692,408

645,075

578,114

0.7

OPERATING PROFIT (PBIT) * 64,787

97,542

44,428

41,265

11,044

(33.6)

INCOME FROM INVESTMENTS 13,819

21,616

11,233

4,799

5,326

(36.1)

INCOME FROM ASSOCIATES (4,843)

8,648

6,770

-

-

(156.0)

PROFIT BEFORE TAXATION (PBT) * 71,912

125,680

62,112

45,317

13,823

(42.8)

TAXATION * 34,858

31,889

29,166

13,463

(1,137)

9.3

NET PROFIT / (LOSS) * 37,054

93,791

32,946

31,854

14,959

(60.5)

DIVIDEND PAID 50,000

18,000

66,667

-

-

177.8

RETAINED INCOME / (LOSS) * (12,946)

75,791

(33,721)

31,854

14,959

(117.1)

FINANCIAL POSITION2004 2003 2002 2001 2000

Growt

h R'000 R'000 R'000 R'000 R'000 %

(a) (b) (a-b)/b ASSETS

PROPERTY, PLANT & EQUIP 118,211

116,678

122,205

157,056

160,137

1.3

PLANTATIONS * 681,381

604,823

275,724

344,114

341,007

12.7

AGRICULTURAL ASSETS 3,165

4,309

5,063

5,883

5,984

(26.5)

INVESTMENTS IN ASSOCIATES 46,384

51,639

46,677

-

-

(10.2)

INVESTMENTS AND LOANS 5,486

35,925

30,243

17,615

17,626

(84.7)

CURRENT ASSETS 254,451

273,210

248,520

209,454

165,836

(6.9)

EQUITY AND LIABILITIES

CAPITAL AND RESERVES * 787,639

802,651

488,118

465,734

440,569

(1.9)

DEFERRED TAXATION 115,906

103,822

(12,014)

42,228

31,509

11.6

LONG-TERM PROVISIONS 24,205

23,217

31,864

128,847

117,911

4.3

INTEREST BEARING LOANS 11,089

12,437

6,895

-

-

(10.8)

CURRENT LIABILITIES 170,239

144,456

213,570

97,315

100,601

17.8

Cents Cents Cents Cents Cents %

BASIC EARNINGS PER SHARE 11.7

29.5

10.4

10.0

4.7

(60.3)

(net profit/number of shares)

Financial Review (continued) Financial Review (continued)

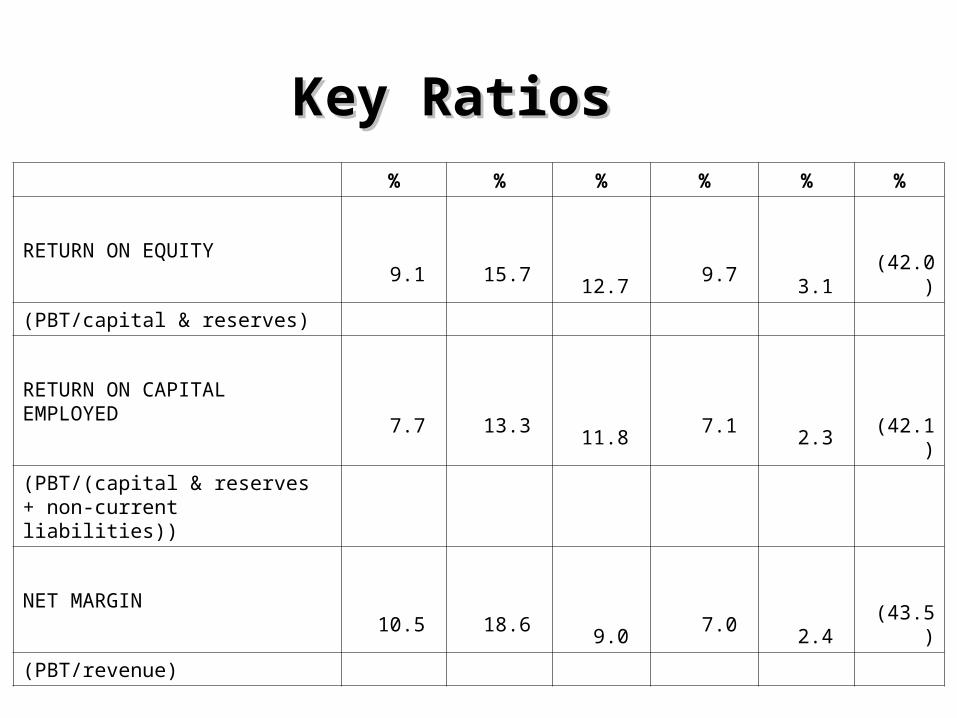

% % % % % %

RETURN ON EQUITY

9.1

15.7

12.7

9.7

3.1 (42.0)

(PBT/capital & reserves)

RETURN ON CAPITAL EMPLOYED

7.7

13.3

11.8

7.1

2.3

(42.1)

(PBT/(capital & reserves + non-current liabilities))

NET MARGIN

10.5

18.6

9.0

7.0

2.4 (43.5)

(PBT/revenue)

* All the above figures include the AC 137 fair value adjustment for 2004 and 2003 of R64,8 million and (R14,5 million) respectively.

Key RatiosKey Ratios

GROUP VALUE ADDED STATEMENTFor the year ended 30 June 2004

The statement below details how the value added is applied to meet certain obligations, reward those responsible for its creation and the portion that is reinvested in the business for the continued operation and expansion of the group.

2004 2003 R'000 % R'000 %

TURNOVER 681,958

677,257

LESS: DIRECT COST (excluding labour cost) 388,061

344,011

VALUE ADDED BY OPERATIONS 293,897

333,246

ADD: INVESTMENT INCOME 13,819

21,616

TOTAL VALUE ADDED 307,716

354,862

DISTRIBUTED AS FOLLOWS: EMPLOYEES (remuneration, benefits, social welfare and training)

206,107

67.0

201,236

56.7

PROVIDERS OF FINANCE 1,851

0.6

2,126

0.6

CORPORATE SOCIAL INVESTMENT 663

0.2

620

0.2

GOVERNMENT FOR TAXATION* 34,858

11.3

31,889

9.0

DIVIDENDS TO THE STATE 50,000

16.2

18,000

5.1

SUB TOTAL 293,479

95.3 253,871

71.6

VALUE REINVESTED 14,237

4.5 100,991

28.4

DEPRECIATION 27,183

8.8

25,200

7.0

RETAINED INCOME / (LOSS) (12,946)

(4.3)

75,791

21.4

TOTAL VALUE DISTRIBUTED 307,716 99.8

354,862 100.0

FINANCIAL HIGHLIGHTS

YEARS ENDED2004 2003 2002 2001 2000

R'000 R'000 R'000 R'000 R'000

Turnover 681,958

677,257

692,408

645,075

578,114

Operating profit - PBIT* 64,787

97,542

44,428

41,265

11,044

Profit before taxation - PBT* 71,912

125,680

62,112

45,317

13,823

Net profit / (loss)* 37,054

93,791

32,946

31,854

14,959

Basic earnings per share (cents)* 11.7

29.5

10.4

10.0

4.7

Capital expenditure 32,891

25,009

31,562

29,467

14,053

* After the AC 137 fair value adjustment of R64,8 million and (R14,5 million) for 2004 and 2003 respectively.