Embed Size (px)

Citation preview

27 November 2017

West African Resources (WAF)

26g/t gold resource driving Sanbrado

Recommendation

Buy (Initiation) Price

$0.39 Valuation

$0.62 (Initiation)

Risk

Speculative

Analyst

Duncan Hughes 618 9326 7667

Authorisation

David Coates 612 8224 2887

GICS Sector

Materials

Expected Return

Capital growth 59.0%

Dividend yield 0.0%

Total expected return 59.0%

Company Data & Ratios

Enterprise value $201.3m

Market cap $225.7m

Issued capital 578.7m

Free float 95.9%

Avg. daily val. (52wk) $289,562

12 month price range $0.18-$0.45

Price Performance

BELL POTTER SECURITIES LIMITED ABN 25 006 390 7721 AFSL 243480

DISCLAIMER: THIS REPORT MUST BE READ WITH THE DISCLAIMER ON PAGE 24 THAT FORMS PART OF IT.

Page 1

(1m) (3m) (12m)

Price (A$) 0.41 0.37 0.26

Absolute (%) -3.70 5.41 50.00

Rel market (%) -5.26 1.14 39.36

Speculative See key risks on Page 22.

Speculative securities may not be suitable for retail clients

Sanbrado project transformed through high-grade additions

We feel the DFS completed in February demonstrates the quality of understanding on

the open pit operations but also demonstrated the need for additional exploration

success. We believe the exploration success achieved since February and the recent

resource upgrade to 2.7Moz has transformed the project with high grade underground

ore (575koz @ 22g/t Au) likely to complement bulk tonnage open pit operations. The

blending of high-grade open pit and underground ore creates significant flexibility and

diversification. But, more significantly the M1 South Underground Resource will add

overall grade and production ounces to the first years of mining (and LOM), lower strip

ratios and potentially improve recoveries. An updated DFS is expected in mid – 2018

and we expect this to be vastly improved.

Exploration upside expected to add further value

We believe the favourable geology at Sanbrado positions for project for additional

exploration success. The high grade M1 South Resource remains open at depth and is

currently being drill tested. If mineralisation continues to be defined at 1500ozpvm then

each additional 100m of resource will add 150koz of gold. We expect near term

newsflow from drilling this position and anticipate M1 South additions to a likely

resource upgrade next quarter. In addition, drilling at depth in the southern portion of

the M5 Resource indicates potential for an underground resource here also.

Investment thesis – BUY (Speculative), Valuation $0.62/sh

Our SOTP valuation consists of a discounted (40%) NPV valuation on the Sanbrado

project, cash at face value and a peer reviewed exploration valuation. At Sanbrado we

assume a 10 year 2.5Mtpa CIL project utilising underground and open pit ore to

produce an average of 160kozpa LOM at AISC of circa A$900/oz. We discount this

valuation to reflect technical, exploration, permitting and funding risk. We assume

additional equity funding of A$95m and dilute our valuation accordingly. We believe

WAF is an excellent and undervalued exploration story and initiate with a Spec. Buy.

Absolute Price Earnings Forecast

Year ending 30 June 2018e 2019e 2020e 2021e

Sales (A$m) - - - 521

EBITDA (A$m) (14) (11) (9) 361

NPAT (reported) (A$m) (14) (11) (10) 257

NPAT (adjusted) (A$m) (14) (11) (10) 257

EPS (adjusted) (¢ps) (2) (1) (1) 31

EPS growth (%) n.a n.a n.a n.a

PER (x) (16.1) (31.1) (31.2) 1.3

FCF Yield (%) nm nm nm 81%

EV/EBITDA (x) (14.2) (19.2) (23.7) 0.6

Dividend (¢ps) - - - -

Dividend Yield (%) 0% 0% 0% 0%

Franking (%) 0% 0% 0% 0%

ROE (%) -81% -17% -11% 116%

SOURCE: IRESS SOURCE: BELL POTTER SECURITIES ESTIMATES

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

Nov 15 May 16 Nov 16 May 17 Nov 17

WAF S&P 300 Rebased

Page 2

West African Resources (WAF) 27 November 2017

Contents

Investment case ............................................................................. 3

Valuation ......................................................................................... 6 Peer Analysis ................................................................................. 8 Company overview ........................................................................ 9 Sanbrado Project, Burkina Faso (90%) ...................................... 10 Regional Exploration, Burkina Faso (90%) ................................ 17

Burkina Faso ................................................................................ 18 Board and management .............................................................. 19

West African Resources (WAF) .................................................. 20 Resource sector risks.................................................................. 22

Page 3

West African Resources (WAF) 27 November 2017

Investment case

High grade M1 South resource transforms the project

We feel the DFS completed in February demonstrates the quality of understanding on the

open pit operations but also demonstrated the need for additional exploration success. We

believe the exploration success achieved since February and the recent resource upgrade

(and likely future upgrades) has transformed the project with high-grade underground ore

(575koz @ 22g/t Au) expected to complement bulk tonnage open pit operations. The

blending of high grade open pit and underground ore creates significant flexibility and

diversification. But, more significantly the M1 South Underground Resource will add overall

grade and production ounces to the first years of mining (and LOM), lower strip ratios and

improve recoveries. An updated DFS is expected in mid – 2018 and we expect this to be

vastly improved.

Strong resource base expected to grow and convert

The resource upgrade in October provides a strong resource base of 2.7Moz for the

project. Importantly M1 South (575koz) is at exceptional grades (26g/t Au in Indicated and

16g/t in inferred). Current reserves of 0.9moz are expected to grow from this resource

upgrade where indicated resources currently sit at 2.1moz. We assume reserve life will

grow to support a solid 10 year mine life at ~160kozpa on average over LOM. In addition,

exploration upside is considered excellent with an aggressive 60km drilling program

expected to grow resources further. The favourable geological position of Sanbrado leads

us to believe there is more gold to be found. We see exellent potential to grow high grade

resources down dip of the M1 South and M5 resources.

Depth extensions at M1 South offer near-term upside

The high grade M1 South Resource remains open at depth and is currently being drill

tested. If mineralisation continues to be defined at 1500ozpvm then each additional 100m

of resource will add 150koz of gold (~1 year of underground mine life). The resource is still

relatively shallow and indications are that ground conditions should support mining to

significantly greater depths than the known resource. We expect near term newsflow from

drilling this position and anticipate M1 South additions to a likely resource upgrade next

quarter. In addition, drilling at depth in the southern portion of M5 indicates potential for an

underground resource here also.

However, strike limits on M1 South need careful definition

One consideration at M1 South is the short strike length of mineralisation at <100m. Given

the high-grade of the mineralisation any change from the estimated strike of the ore body

will have a greater than usual impact on the ounces per vertical metre (ozpvm) and the

relative cost of development infrastructure. Based on current strike length estimates the

underground is set to average 1500ozpvm which looks able to support a profitable

underground mine. Resource modelling also looks favourably conservative, however the

risk of unexpectedly shorter strike lengths to this mineralisation and the consequent

dramatic drop-off in ounces should be considered. This should be a major focus in the

updated DFS and ongoing drilling program.

Strike lengths on plunging shoot are short at M1 South

High-grade has transformed the

project

Resources and

reserves to grow

100m = 150koz

Page 4

West African Resources (WAF) 27 November 2017

Processing re-design and blending expected to add value

Metallurgical recoveries in the DFS were 90.7%, however blending more of the higher

grade (higher recovery) M1 South ore as well as an improved SAG and ball mill

comminution circuit is expected to lift recoveries to >93%. Overall gold recovery and costs

will also likely be assisted by the improved gravity recovery (~40% LOM) from coarser M1

South ore and the addition of a Wilfley (shaker) table to the Knelson gravity concentrator

circuit.

Permitted for heap leach operation

The project is currently permitted for a heap leach open pit operation. We believe that,

whilst permitting for a CIL processing plant and underground mine is still required, this

initial permit will assist and uncomplicate the pathway to final permitting.

Management experienced and qualified

Management is experienced in the discovery and development of gold assets in West

Africa. Management has experience from a number of successful ventures in West Africa

including the successful takeover of ASX listed Papillon Resources, the merger of ASX

listed Adamus Resources and the operation of Equigold’s Bonikro Gold project. However,

WAF will need to add to its current team should it wish to develop and mine Sanbrado.

Strong balance sheet will take WAF to a production decision

WAF has circa $25m in cash and no debt. WAF is well placed to fund aggressive

exploration and a DFS in 2018. The current shareholder base that includes Sprott,

Dynamic and Macquarie likely leaves WAF better placed than most should it require future

project funding support.

Expect M&A interest

With a strong project and exploration upside we believe WAF will be attracting the interest

of existing producers in West Africa and is potentially at risk of takeover as Sanbrado

progresses towards a funding decision. At current market valuations we see an opportunity

for a larger incumbent producer to acquire Sanbrado and fund from their own balance

sheet. This has the potential for a near term realisation of value for shareholders.

Undervalued on NAV and peer analysis

Our SOTP valuation of $522m indicates considerable upside on the current market

valuation for WAF. Our peer analysis supports our view that the company has a sizeable

resource base to underpin an operation and does not carry the premium valuation we feel

it should when measured against other ASX listed gold explorers.

Table 1 - WAF sum of the parts valuation (A$m)

SOURCE: BELL POTTER SECURITIES ESTIMATES. * FOR FURTHER DETAIL ON THE VALUATION METHODOLOGY PLEASE SEE THE VALUATION SECTION ON PAGE 6

Fair Value Calculation Discount rate NAV (AUD $M) NAV "X" Factor NAV Target (AUD $M) Target SP (AUD

$)

Sanbrado (90%) 10% $582.5 M 0.60 X $349.5 M $0.41

Exploration Upside $50.0 M 1.00 X $50.0 M $0.06

Unpaid capital $95.0 M 1.00 X $95.0 M $0.11

Cash from options $3.2 M 1.00 X $3.2 M $0.00

Cash (est. end qtr) $24.4 M 1.00 X $24.4 M $0.03

Investments $0.0 M 1.00 X $0.0 M $0.00

Total NAV $755.1 M $522.1 M $0.62

Permitting

commenced

Processing recoveries expected to improve

Management has had success in West Africa

WAF a potential M&A target

Funded to a development

decision

Page 5

West African Resources (WAF) 27 November 2017

Figure 1 - SWOT Analysis

SOURCE: BELL POTTER SECURITIES

Upcoming Catalysts

High grade drilling intersections – ongoing;

Metallurgical test work on M1 South and new processing on M5 – 1QCY18;

Resource update – 1QCY18; and

DFS on underground and open pit mine – 1HCY18.

Strengths

Fully focussed on gold

Exceptionally high grade M1 South

Sizeable resource/ reserve with blending of high grade underground and bulk open pit

Good metallurgy with upside

DFS completed on open pits

Healthy balance sheet. $25m cash, no debt

Permitted – but not for CIL

Capable management with track record

Undervalued

Weaknesses

Need to re-house some locals

Study yet to be completed on underground potential

Permitting still to be completed

Government free- carried 10%

Threats

Gold price volatility

Regional security, political risk

Relatively short strike of plunging shoot

Potential takeover target

FX changes

Opportunities

Exploration upside and large budget

Potential Takeover target

Improve metallurgy

Grid power?

Page 6

West African Resources (WAF) 27 November 2017

Valuation

Sanbrado (90%, Burkina Faso 10% free-carry)

We have modelled Sanbrado to commence production in FY21 with a 10 year mine life

supported by production from high grade underground mining for 4 years from FY21 and

lower grade open pit operations over LOM. We assume open pit and underground ore is

blended over the life of the underground operation. Our mine plan assumes 23.3Mt @

2.41g/t Au for 1.9Moz is mined over LOM, compared to current reserves of 0.9Moz. We

assume additional conversion of resources to reserves on the back of the recent high

grade resource upgrade (150% increase) and future upgrades from underground ounces.

We assume production in excess of 200kozpa over the life of the underground (first four

years) and production of circa 120kozpa thereafter.

Table 2 - Sanbrado assumed mine plan (100% of project)

SOURCE: BELL POTTER SECURITIES ESTIMATES.

We have assumed production efficiency and costs based on company announcements and

our own assumptions. Our FX and gold price assumptions are based on Bell Potter

forecasts.

Table 3 - Sanbrado modelling assumptions

SOURCE: BELL POTTER SECURITIES ESTIMATES

We value WAF’s 90% interest in the Sanbrado project on a post-tax basis, calculating an

NPV10% of A$583m. However, given the underground resources are yet to be converted to

reserves or undergo a feasibility study (the open pit reserves were subject to a study prior

to the recent underground resource upgrade) we have decided to risk our valuation by 40%

to reflect technical and funding risk. Our risked 0.6X NPV for WAF’s 90% share in the

project is A$350m or 41c/share (fully diluted) and 60c/share undiluted.

Mine Plan FY21 FY22 FY23 FY24 FY25

Total Plant Feed (Mt) 2.1 2.5 2.5 2.5 2.5

Average Head Grade (g/t Au) 4.6 3.8 3.1 2.8 1.7

Average Plant Recovery (%) 93.0 93.0 93.0 93.0 93.0

Gold produced (koz) 269 284 234 206 124

Assumption Life of Mine

Open Pit Mining Cost (A$/t rock) 3.20

Underground Mining Cost (A$/t ore) 160.00

CIL Processing Cost (A$/t ore) 14.50

M1 South Processing Cost (A$/t ore) 21.33

G&A Cost (A$/t ore) 4.67

Initial Capex (A$m) 200.00

Sustaining Capex (A$m pa) 10.33

Exploration (A$m pa) 5.00

Government Royalty (%) 5.0%

Community Royalty (%) 1.0%

Corporate Tax (% p.a) 27.5%

LOM C1 cost (A$/oz) 558

LOM All in sustaining cost (A$/oz) 847

LOM Average Gold Price (A$/oz) 1933

A$/US$ (Long term) 0. 75

We value Sanbrado at $350m or 41c/sh

Page 7

West African Resources (WAF) 27 November 2017

Exploration tenure

Exploration tenure, a ~1,000km2 package hosting circa 100km of strike of greenstone,

includes the large but relatively low grade Sartenga gold and copper discovery and the

Moktedu exploration trend which was formerly the main focus of the business before

Sanbrado. Exploration tenure also includes additional resources of 800koz at Sanbrado.

We value exploration tenure at A$50m based on peer comparisons.

Cash, corporate costs, unpaid capital and investments

We assume cash at 31 December 2017 of A$24m and value it at face value. Corporate

costs (A$4mpa) and debt funding are factored into our Sanbrado model. WAF has no

significant additional investments.

We assume the A$3.2m in share options are exercised and dilute our valuation by 20m

shares accordingly. We also assume A$95m (45%) of the assumed capital and working

capital expenditure for Sanbrado is funded through the issue of 244m shares at the current

share price. We dilute our valuation to reflect the unpaid capital of 244m shares.

Total valuation

Our total discounted sum-of-the-parts (SOTP) NAV valuation for WAF is A$522m or

A$0.62/share.

Table 4 - WAF: sum-of-the parts valuation

SOURCE: BELL POTTER SECURITIES ESTIMATES.

Shares on issue (m) 578.7

ITM options (m) 20.0

Performance rights (m) -

Unpaid capital (m) 243.6

Diluted (m) 842.3

SOTP* A$m A$/sh

90% Sanbrado (risk discount 40%, NPV10%) 349.5 0.60

Exploration Upside 50.0 0.09

Cash (est. end qtr) 24.4 0.04

Investments - -

Total (undiluted) 423.8 0.73

Cash from options 3.2 0.00

Unpaid capital 95.0 0.11

Total (fully diluted) 522.1 0.62

Discounted valuation of $522m ($0.62/sh)

Page 8

West African Resources (WAF) 27 November 2017

Peer Analysis

Figure 2 below summarises the attributable resource ounces across the ASX listed gold

sector. WAF has a sizeable resource base, the fourth largest for an explorer on the ASX

and the second largest in Africa. As a result we would expect the company to attract

investor attention and a premium valuation.

Figure 3 below summarises the market valuation of each company’s resource ounces. The

chart displays enterprise value per resource ounce and arguably affords a rough

approximation of what the market appears to be valuing each company’s resources at.

There are several notable limitations with an EV per ounce valuation as not all resources

are the same in terms of depth, grade, commerciality and upside potential. In addition, an

EV per ounce valuation does not account for other valuation metrics such as management

quality, country risk, infrastructure or technical evaluation stage.

Across the sector, WAF appears only moderately valued (a slight premium to median

valuations) for its resources against peers. This surprises us given the large resource base

(~2.5moz), strong exploration upside, level of technical studies (DFS on part of project) and

the very attractive combination of 575koz at exceptional grade (22g/t Au) that can be

blended with open pit tonnes. We believe WAF’s resources should be valued at a

substantial premium to peers.

Figure 2 - ASX listed gold explorers - resources Figure 3 – ASX listed gold explorers – EV per resource ounce

SOURCE: COMPANY DATA & BELL POTTER SECURITIES SOURCE: BELL POTTER SECURITIES ESTIMATES

As a consequence, we feel our peer analysis indicates that there is upside in WAF’s

relative valuation against peers owing to the high quality of the Sanbrado resource ounces.

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Mo

z

0

20

40

60

80

100

120

140

160

180

200

EV/o

z (A

$)

WAF’s resources should be valued at a greater premium

WAF’s resources are valued only moderately against peers

Page 9

West African Resources (WAF) 27 November 2017

Company overview

Background

West African Resources (WAF) is a Perth based gold explorer focussed on Burkina Faso

and listed on the ASX and TSXV. WAF listed on the ASX in 2010 with a focus on its Boulsa

project – the northern portion of its current tenement package. Initial results were

encouraging but largely confined to shallow oxide mineralisation at the Moktedu prospect.

In 2012 the company’s focus switched to a large but relatively low grade gold and copper

“porphyry style” deposit called Sartenga.

In 2014 WAF acquired TSXV listed Channel Resources for 30m shares and subsequently

listed on the TSXV in 2014. Channel Resources’ contiguous tenements host the Sanbrado

project (called Tanlouka at the time). Initially WAF looked to develop a low grade heap

leach operation. However, additional high grade intersections and investor appetite led the

company to define a more conventional CIL gold project at Sanbrado and complete a

Definitive Feasibility Study (DFS) on open pit resources in February 2017. The release of a

significant high grade underground resource update in October 2017 looks to have

transformed the economics of the project.

Corporate summary

WAF has 579m shares on issue and 20m options at an average strike price of 16c for a

total potential cash value of $3.24m. The options need to be exercised at various dates

between February 2018 and December 2020 as outlined in the table below. At the current

share price all options are in the money.

Table 5 - WAF options on Issue

SOURCE: WAF, BELL POTTER

There are no performance rights on issue. WAF has net cash estimated at A$24m.

M&A

With a strong project and exploration upside we believe WAF will be attracting the interest

of existing producers in West Africa and is potentially at risk of takeover as Sanbrado

progresses towards a funding decision. At current market valuations we see an opportunity

for a larger incumbent producer to acquire Sanbrado and fund from their own balance

sheet. This has the potential for a near term realisation of value for shareholders.

The Sanbrado Project is located adjacent to TSXV listed Orezone Gold Corporation’s

(ORE) large but very low grade Bombore gold development project (5.7Moz @ 0.64g/t Au).

ORE has a market capitalisation in the order of C$110m. Despite the overall low grade of

Bombore, we see potential synergies with both projects adjacent to each other and looking

to potentially develop their resources.

Expiring Shares (m) ex. Price Value (A$m) ITM (A$m) ITM shares (m)

20/02/2018 5.0 $0.15 $0.73 $0.73 5.0

18/08/2018 0.5 $0.10 $0.05 $0.05 0.5

1/12/2018 2.0 $0.15 $0.29 $0.29 2.0

6/06/2019 5.0 $0.08 $0.42 $0.42 5.0

3/06/2019 1.0 $0.10 $0.10 $0.10 1.0

3/06/2019 1.0 $0.15 $0.15 $0.15 1.0

24/07/2019 1.1 $0.32 $0.35 $0.35 1.1

21/03/2020 0.4 $0.24 $0.10 $0.10 0.4

12/05/2020 0.5 $0.24 $0.12 $0.12 0.5

18/10/2020 0.8 $0.38 $0.28 $0.28 0.8

9/11/2020 2.8 $0.24 $0.66 $0.66 2.8

Total 20.0 $0.16 $3.24 $3.24 20.0

Page 10

West African Resources (WAF) 27 November 2017

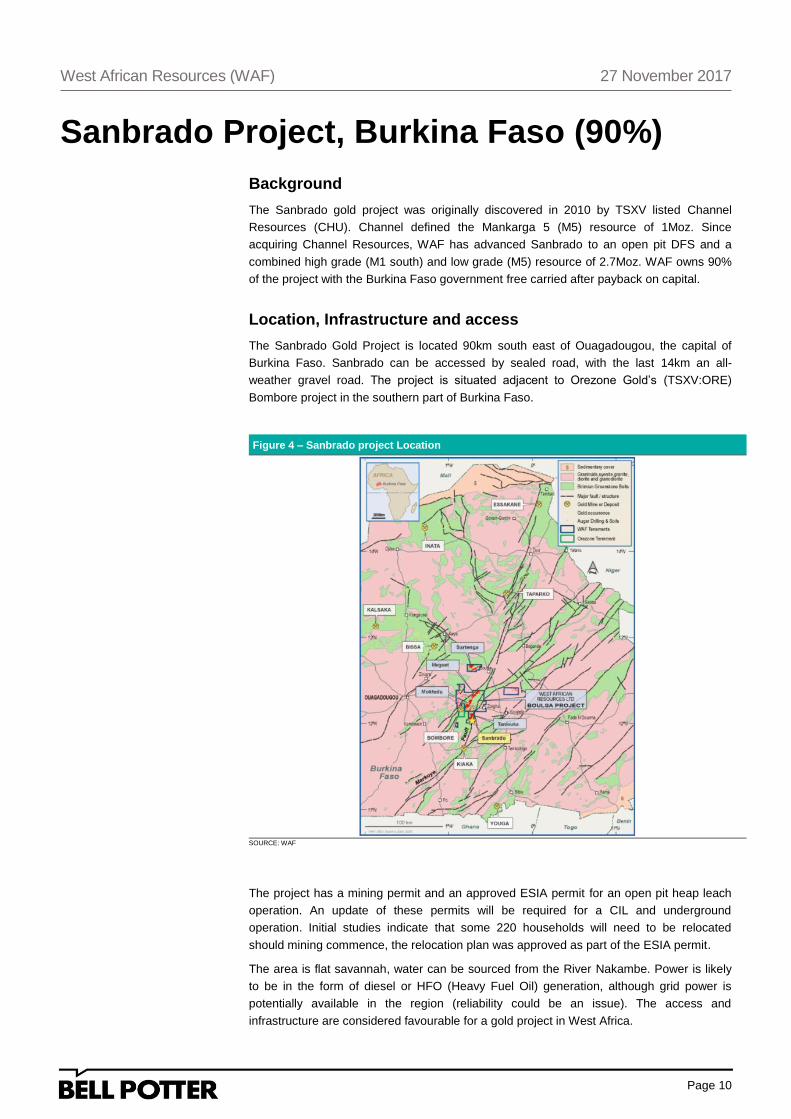

Sanbrado Project, Burkina Faso (90%)

Background

The Sanbrado gold project was originally discovered in 2010 by TSXV listed Channel

Resources (CHU). Channel defined the Mankarga 5 (M5) resource of 1Moz. Since

acquiring Channel Resources, WAF has advanced Sanbrado to an open pit DFS and a

combined high grade (M1 south) and low grade (M5) resource of 2.7Moz. WAF owns 90%

of the project with the Burkina Faso government free carried after payback on capital.

Location, Infrastructure and access

The Sanbrado Gold Project is located 90km south east of Ouagadougou, the capital of

Burkina Faso. Sanbrado can be accessed by sealed road, with the last 14km an all-

weather gravel road. The project is situated adjacent to Orezone Gold’s (TSXV:ORE)

Bombore project in the southern part of Burkina Faso.

Figure 4 – Sanbrado project Location

SOURCE: WAF

The project has a mining permit and an approved ESIA permit for an open pit heap leach

operation. An update of these permits will be required for a CIL and underground

operation. Initial studies indicate that some 220 households will need to be relocated

should mining commence, the relocation plan was approved as part of the ESIA permit.

The area is flat savannah, water can be sourced from the River Nakambe. Power is likely

to be in the form of diesel or HFO (Heavy Fuel Oil) generation, although grid power is

potentially available in the region (reliability could be an issue). The access and

infrastructure are considered favourable for a gold project in West Africa.

Page 11

West African Resources (WAF) 27 November 2017

Geology, resources and reserves

The right structural setting

Sanbrado is hosted within a sequence of structurally deformed Birimian Greenstone rocks,

the Proterozoic aged rocks that host other gold deposits in the region. The sequence of

metamorphosed volcanics and sediments is structurally deformed as part of a regional

deformation event where roughly north-south compression has formed a sequence of

regional transcurrent shear zones that tend northeast as shown in Figure 4. The sequence

of shears and greenstones is intruded by granites and porphyry bodies that often assist in

locating gold mineralisation.

At Sanbrado the M5 structure appears to be a second or third order splay off the regional

Markoye fault zone where it jogs (or deviates) slightly to the north making the area more

favourable for the precipitation of mineralisation fluids in a more extensional/dilational

environment. In addition, the mineralisation appears to be located in the “pressure shadow”

to the south of a competent granodiorite intrusive body. This is a common structural setting

and trap for gold as the large granodiorite affords a ‘de-stress zone’ and dilation which

provides space to trap gold. M1 is likely another structure forced around the granodiorite to

the north. The high grade M1 South shoot likely reflects localized fold hinges or later

faulting that intersects the north trending M1 shear, the likely result from N-S compression.

The Sanbrado gold project is in a geologically favourable location for gold mineralisation

and we see potential for additional gold discoveries here. Interestingly the higher grade

and deeper portions of the M5 trend is located in the south where the M1 trend potentially

intersects, making this a good target for additional high grade gold at depth.

Figure 5 – Sanbrado geology plan

SOURCE: WAF

Gold is found within sheared and boudinaged quartz veining associated with silica,

sulphide (pyrite, arsenopyrite and pyrrhotite), carbonate and calc-silicate alteration. The

high grade plunging shoot at M1 South is associated with particularly intense silicification,

Page 12

West African Resources (WAF) 27 November 2017

this alteration suggests a large amount of fluid flow and potential for a relatively sizeable

gold deposit rather than just a smaller tension gash style of mineralisation.

In long section (Figure 6 below), the high grade plunging shoot at M1 South appears to be

offset slightly to the northwest below 400m vertical depth. We believe this may be a late

structure that could also offset the smaller plunging shoots located at shallow depths to the

northwest in the long section below. In our view, this could open up potential for the offset

continuation of these shallow shoots at depth also. This hypothesised late structure could

also potentially explain why the mineralisation also appears to split at depth on cross

section to the south (Figure 7).

Figure 6 - M1 South long section Figure 7 - M1 South Cross section: ore body splitting at depth

SOURCE: WAF SOURCE: WAF

Resources

Sanbrado hosts four resources, the larger M5 resource, the high-grade M1 South resource

and the smaller M3 and M1 North resources. On 30th October, WAF announced a

substantial (150%) increase in resource ounces at Sanbrado, largely due to the 575koz @

22g/t Au resource from M1 South. M1 South and M5 form the backbone of our assumed

mine plan. M3 will likely provide shallow oxide satellite pits as outlined in the open pit DFS.

Sanbrado hosts a 2.7Moz resource that is JORC 2012 compliant as shown below. The

resource was defined independently with open pit resources defined at a 0.5g/t lower cut

and underground resources at a 3g/t Au lower cut and 250g/t upper cut. Additional

resource upgrades are expected in 2018. The M5 open pit resource and M1 South

underground resource remain open at depth.

Page 13

West African Resources (WAF) 27 November 2017

Table 6 – Sanbrado mineral resources (30 October 2017)

SOURCE: WAF, 100% OF PROJECT

Within the global resource above is an exceptionally high-grade resource at M1 South.

This underground resource is confined to a plunging shoot of mineralisation that has a

relatively short strike length. Given the exceptional grade it is important that mineralisation

is not projected aggressively along strike. Consequently the resource was calculated using

Ordinary Kriging on small parent cell (2.5m x 5m x 5m) block sizes. Modelling allowed

extrapolation no more than 10m along strike at the edge of the resource. Grade distribution

in M1 South shows acceptable variance and a favourably low nugget effect for such a high-

grade ore body with only 4 samples reporting above the 250g/t Au upper cut.

Table 7 – Sanbrado High Grade M1 South mineral resource (30 October 2017)

SOURCE: WAF, 100% OF PROJECT

The high grade resource remains open below 450m.

Open pit reserves were estimated in February 2017 utilizing a 5:1 average strip ratio and

US$1,200/oz gold price. These reserves are expected to grow and the strip ratio fall in an

updated DFS due 1HCY18.

Table 8 - Sanbrado mineral reserves (20 February 2017)

SOURCE: WAF, 100% OF PROJECT

Mining and mine plan

In a potential mining scenario the operation would likely be a combination of open pit

mining and an underground mining operation on M1 South (and possibly at depth on M5

South). The February 2017 DFS assumed an open pit mining operation that would produce

150kozpa over the first 3 years and 93kozpa over the remaining 6 years, at estimated life

of mine (LOM) all in sustaining costs (AISC) of US$759/oz. But with initial capital

expenditure of US$131m the post-tax NPV5 was estimated at ~$100m. This initial DFS was

only based on open pit mining and assumed an extreme 36:1 strip ratio on M1 South.

We believe the recent resource upgrade (and future upgrades) has transformed the

operation with high grade underground ore to complement bulk tonnage open pit

operations. The blending of high grade open pit and underground ore creates significant

flexibility and diversification. But, more significantly the M1 South resource will add overall

grade and production ounces to the first years of mining (and LOM), lower strip ratios and

improve recoveries. We assume contract mining (lower capex slightly higher opex) in our

modelling.

Category Tonnes (Mt) Grade (g/t Au) Contained Gold (Koz)

Measured 0.0 0.0 0

Indicated 38.0 1.7 2,080

Inferred 13.3 1.5 655

Total 51.3 1.66 2,735

Category Tonnes (Mt) Grade (g/t Au) Contained Gold (Koz)

Indicated 0.5 26.4 395

Inferred 0.4 16.1 180

Total 0.8 21.8 575

Category Tonnes (Mt) Grade (g/t Au) Contained Gold (Koz)

Probable 16.8 1.70 918

Total 16.8 1.70 918

Page 14

West African Resources (WAF) 27 November 2017

In the recent resource upgrade the company’s Whittle Pit Optimisation assumed relatively

shallow slope angles of 50⁰ for fresh ore, we believe steeper slope angles are possible and

this would likely lower strip ratios and improve the economics of these pits. The Whittle Pit

design assumes an open pit to 120m at M1 South. An underground operation is currently

expected to commence beneath this pit, accessed by a separate box-cut to enable

underground mining at the same time as open pit mining. M1 South underground mining is

likely to be conventional long-hole open stoping. The dip and widths of mineralisation look

to be supportive of this technique with average widths of 45m and a steep dip and plunge.

More geotechnical work will be done as part of the updated DFS in order to more

confidently determine ground support conditions.

One consideration at M1 South is the short strike length of mineralisation at <100m. Given

the high-grade of the mineralisation any change from the estimated strike of the ore body

will have a greater than usual impact on the ounces per vertical metre (ozpvm) and the

relative cost of development infrastructure. Based on current strike length estimates the

underground is set to average 1500ozpvm which looks set to support a profitable

underground mine. Resource modelling also looks favourably conservative, however the

risk of unexpectedly shorter strike lengths to this mineralisation and the consequent

dramatic drop-off in ounces should be considered and be a major focus in the updated

DFS and ongoing drilling program. Drilling to date shows a consistent ore body that is

relatively predictable at M1 South.

Figure 8 - Planned site layout showing open pit, underground access and plant locations

SOURCE: WAF

Processing

Processing is expected to utilize a conventional 2.5mtpa gravity-CIL processing plant.

Metallurgical recoveries in the DFS were 90.7%, however blending more of the higher

grade (higher recovery) M1 South ore as well as an improved SAG and ball mill

comminution circuit is expected to lift recoveries to >93%. Overall gold recovery and costs

Page 15

West African Resources (WAF) 27 November 2017

will also likely be assisted by the improved gravity recovery (~40% LOM) from coarser M1

South ore and the addition of a Wilfley (shaker) table to the Knelson gravity concentrator

circuit. The company will need to consider the risk of gold theft associated with an open

Wilfley table.

Ore is hard and the M1 South ore recovery benefits from finer grind to 75 microns

compared to M5 at 90 microns – hence the introduction of a SAG- Ball mill combination.

This will add to capex and opex but should be offset by the greater recoveries (assumed in

our modelling). Cyanide consumption is low at 300mg/l to achieve relatively rapid leach

times of circa 24 hours which is favourable.

Given the hardness of the ore and the requirement for a relatively fine grind, power costs

will be relatively high. The company is exploring options on possible grid power, Heavy

Fuel Oil or diesel.

Exploration

Exploration upside potential is considerable at Sanbrado. WAF will have 6 drilling rigs on

site and will complete a geophysical (IP) program to aid exploration targeting at Sanbrado

shortly.

M1 South

The highest priority target is clearly down dip of the M1 South resource. The company is

currently drill testing this area. If mineralisation continues to be defined at 1500ozpvm then

each additional 100m of resource will add 150koz of gold (~1 year of underground mine

life). The resource is still relatively shallow and indications are that ground conditions

should support mining to significantly greater depths than the known resource. We expect

near term newsflow from drilling this position and anticipate M1 South additions to a likely

resource upgrade next quarter.

At M1 South we believe a potential faulted offset of shallow shoots to the south could open

up potential for a continuation of these shallow shoots at depth (as outlined in the geology

section on pages 11 & 12).

M1 South remains open to the south. Reconnaissance drilling of this trend is likely oriented

incorrectly given the shear appears to trend more east-west and drilling traverses are

oriented east west and could potentially miss the ore zone.

M5

Another compelling target is at depth beneath the southern part of the M5 pit design. As

outlined in the geology section on page 11, this higher grade portion of M5 is coincident

with a possible intersection with the M1 trend and makes a compelling geological target

that is complemented by favourable drilling results to date. Gold is often focussed and at

higher grades where two gold bearing structures insect.

Drilling at depth at M5 south has returned some very encouraging widths and grades that

could potentially support an underground operation. Better intersections include 27m @

12.3g/t Au and 8m @ 17.5g/t Au.

The M5 trend extends 1.5km along strike to the northeast of the M5 resource. We expect

drilling to test this trend 2018. The size of the Sanbrado tenement limits the strike extent of

these mineralised trends on company ground, although (in our opinion) WAF’s tenement

covers the geologically most prospective ground within the pressure shadow of the

Sanbrado Granodiorite.

Page 16

West African Resources (WAF) 27 November 2017

Figure 9 – M5 Drilling and pit outline and intersections to south Figure 10 – X-section showing depth potential at M5 South

SOURCE: WAF SOURCE: WAF

The bulk of the FY18 field season’s planned 60,000m of RC and Diamond drilling will likely

focus on Sanbrado.

Page 17

West African Resources (WAF) 27 November 2017

Regional Exploration, Burkina Faso (90%)

Sartenga

The Sartenga copper-gold-molybdenum project is a large tonnage porphyry system which

is unique in the Biriman rocks of West Africa. The Inferred Mineral Resources contain

174,000t copper, 651,000oz gold (70 million tonnes at 0.2% copper, 0.3g/t gold, 166g/t

molybdenum and 1.1g/t silver using a 0.45% copper equivalent cut-off). The dominant

sulphide is bornite and therefore mineralisation has the potential to create a high-grade

copper-gold concentrate. The project is located close to potential infrastructure including

rail to port less than 40 km from the project.

Preliminary metallurgical test work has been carried out on a composite sample of

Sartenga primary ore with a head grade of 0.23% Cu and 0.43g/t Au, at a relatively coarse

primary grind size of 106 microns. Flotation rougher recovery of 97.9% was returned for

gold, while a recovery of 96.1% was recorded for copper. These very high rougher

recoveries indicate that final copper and gold recovery levels into a commercial grade

concentrate will also be quite high, potentially in excess of 90%.

Sartenga was the company’s flagship asset prior to accessing the Sanbrado Project.

Moktedu

The Moktedu prospect is located in the southwestern part of the Boulsa Project. The

prospect covers some 10km of strike and is confined within a northeast trending regional

shear. The prospect is also located some 2km northeast of Orezone Gold Corporation’s

(TSXV: ORE) Bomboré gold deposit. Favourable shallow oxide mineralisation was

intersected including 4m @ 8.4g/t Au and 5m @ 10g/t Au. Mineralisation does not appear

to continue at depth into fresh rock.

Other

The Meguet and Fatmatenga prospects are located near the town of Meguet, some 24km

northwest of Zorgho, and are centrally situated within the Boulsa Project. Best drilling

results include 10m at 7.67g/t Au and 10m at 2.77 g/t Au.

Page 18

West African Resources (WAF) 27 November 2017

Burkina Faso

Burkina Faso is a West African nation located between Ghana and Mali. Burkina Faso has

a strong track record of gold mining and exploration success. Burkina hosts nine gold

mines owned and operated by largely North American and European mining companies

including Roxgold (Yaramoko mine), Avocet (Inata mine), Semafo (Mana mine and

Natougou development), IamGold (Essakane Mine), Nordgold (Bissa Hill and Taparko

mines), MNG Gold (Youga mine) and Endeavour Mining (Karma and Hounde mines).

RoxGold’s Yaramoko gold mine is a high grade and profitable underground gold mine and

likely the best analogy for a potential operation at M1 South.

Burkina Faso is currently ranked 8th in Africa and 48th globally in the Fraser Institute

attractiveness for mining investment survey. The country has a transparent mining code,

the corporate tax rate is 27.5% and government gold royalty is 5%. The government

acquires a 10% free carry in mining projects (after capital payback).

In recent years Burkina Faso’s capital has been on the receiving end of a number of

terrorist attacks. The northern part of the country near the border with Mali is deemed

challenging from a security perspective. WAF’s project is located in the southern portion of

the country that is considered relatively safe to operate in by comparison.

Page 19

West African Resources (WAF) 27 November 2017

Board and management

Management has strong and relevant experience in West Africa. However, the executive

team is small and geared towards exploration and would need complementing should the

company look to develop the project to a producing asset (assuming the asset is not

bought by an incumbent producer).

Non-Executive Chairman – Mark Connelly has more than 27 years of experience in the

mining industry, and has held senior executive positions with Newmont Mining Corporation

and Inmet Mining Corporation. He is the former Managing Director and Chief Executive

Officer of Papillon Resources Limited, a Mali-based gold developer which merged with

B2Gold Corp in a US$570 million deal.

He was Chief Operating Officer of Endeavour Mining Corporation following its merger with

Adamus Resources, where he was Managing Director and CEO. Mark has extensive

experience in financing, development, construction and operation of mining projects in a

variety of commodities including gold, base metals and other resources in West Africa,

Australia, North America and Europe.

Managing Director – Richard Hyde is a geologist with 20 years’ experience in the

minerals industry and more than 15 years of experience in West Africa. Richard has

managed large exploration and development projects in a range of different geological

environments in Australia, Africa and Eastern Europe. He has consulted extensively to the

mining industry as a senior consultant with RSG Global and Coffey Mining based in West

Africa and Australia. Richard is a founding director and shareholder of West African

Resources. He is Member of the Australian Institute of Mining and Metallurgy.

Non-Executive Director – Simon Storm is a chartered accountant with more than 25

years of Australian and international experience in the accounting profession and

commerce. He commenced his career with Deloitte Haskins & Sells in Africa and then

transferred to London before joining Price Waterhouse in Perth. He has held various

senior finance and company secretarial roles with listed and unlisted entities in the

banking, resources, construction, telecommunications, property development and funds

management industries. In the past 10 years, he has provided consulting services

involving accounting, financial and company secretarial matters to various companies in

these sectors.

Chief Operating Officer – Lyndon Hopkins has more than 20 years of experience in gold

exploration, development and production. He is the former COO of Equigold NL’s Ivory

Coast operations and Mine Manager for the construction of Regis Resources Ltd’s

Rosemont Gold Mine.

Page 20

West African Resources (WAF) 27 November 2017

West African Resources (WAF)

Company description

WAF is a Perth-based company focused on gold exploration at its 90% owned Sanbrado

project in Burkina Faso. WAF is listed on the ASX and TSX-V.

Sanbrado hosts >2.5moz of gold resources and is undergoing an aggressive 60,000m per

annum exploration program and Definitive Feasibility Study on a potential gold mining

operation. The project hosts the extremely high grade underground resource at M1 South

(575koz @ 22g/t Au) that will likely supplement bulk open pit mining from M5. The

Feasibility Study is due for completion in mid-2018.

Investment thesis – BUY (speculative), Valuation $0.62/sh

Our SOTP valuation consists of a discounted (40%) NPV valuation on the Sanbrado

project, cash at face value and a peer reviewed exploration valuation. At Sanbrado we

assume a 10 year 2.5mtpa CIL project utilizing underground and open pit ore to produce

an average of 160kozpa LOM at AISC of circa A$900/oz. We discount this valuation to

reflect technical, exploration, permitting and funding risk. We assume additional equity

funding of A$95m and dilute our valuation accordingly. We believe WAF is an excellent

and undervalued exploration story and initiate with a Spec. Buy.

Valuation – risk discounted SOTP with DCF on Sanbrado

We have modelled Sanbrado to commence production in FY21 with a 10 year mine life

supported by production from high grade underground mining for 4 years from FY21 and

lower grade open pit operations over LOM. We assume open pit and underground ore is

blended over the life of the underground operation. Our mine plan assumes 23.3Mt @

2.41g/t Au for 1.9Moz compared to reserves of 0.9Moz. We assume additional conversion

of resources to reserves on the back of the recent high grade resource upgrade (150%

increase) and future upgrades from underground ounces.

We value WAF’s 90% interest in the Sanbrado project on a post-tax basis, calculating an

NPV10% of A$583m. However, given the underground resources are yet to be converted

to reserves or undergo a feasibility study (the open pit reserves were subject to a study

prior to the recent underground resource upgrade) we have decided to risk our valuation by

40% to reflect technical and funding risk. Our risked 0.6X NPV for WAF’s 90% share in the

project is A$350m or 40c/share (fully diluted).

Exploration tenure includes the large but relatively low grade Sartenga gold and copper

discovery and the Moktedu exploration trend which was formerly the main focus of the

business before Sanbrado. Exploration tenure also includes additional resources of 800koz

at Sanbrado. We value exploration tenure at A$50m based on peer comparisons.

We assume cash at 31 December 2017 of A$24m and value it at face value. Corporate

costs and debt funding are factored into our Sanbrado model. WAF has no significant

additional investments.

We assume the A$3.2m in share options are exercised and dilute our valuation by 20m

shares accordingly. We also assume the A$95m (45%) of the assumed capital and working

capital expenditure for Sanbrado is funded through the issue of 275m shares at the current

share price. We dilute our valuation to reflect the unpaid capital of 275m shares.

Our total discounted sum-of-the-parts (SOTP) NAV valuation for WAF is A$522m or

A$0.62/share.

Discounted valuation of $522m ($0.62/sh)

Page 21

West African Resources (WAF) 27 November 2017

Figure 11 - WAF: sum-of-the-parts valuation

SOURCE: BELL POTTER SECURITIES ESTIMATES

Shares on issue (m) 578.7

ITM options (m) 20.0

Performance rights (m) -

Unpaid capital (m) 243.6

Diluted (m) 842.3

SOTP* A$m A$/sh

90% Sanbrado (risk discount 40%, NPV10%) 349.5 0.60

Exploration Upside 50.0 0.09

Cash (est. end qtr) 24.4 0.04

Investments - -

Total (undiluted) 423.8 0.73

Cash from options 3.2 0.00

Unpaid capital 95.0 0.11

Total (fully diluted) 522.1 0.62

Page 22

West African Resources (WAF) 27 November 2017

Resource sector risks

Risks to WAF include, but are not limited to:

Operating and capital cost fluctuations. Markets for exploration, development and

mining inputs can fluctuate widely and cause significant differences between planned and

actual operating and capital costs. Key operating costs are linked to energy and labour

costs as well as access to, and availability of, technical skills, operating equipment and

consumables. West Africa is a relatively expensive place to operate.

Lack of exploration success: Our modelling assumes additional exploration success

and the company’s ability to convert resources to reserves. Exploration is by its very nature

risky and there is no certainty, despite our view on its prospectivity. The M1 South ore body

is particularly exposed to risk in fluctuations in its geometry where an unexpected shrink in

strike length could significantly impact economics of mining.

Lack of funding: Exploration/development companies generally do not have a source of

revenue and so they require access to funding to enable them to carry out adequate

exploration and related development activities in order to continue to develop their

operations. WAF will need to acquire funding for the project which we assume to be in the

order of $200m. WAF is well funded for near term requirements with net cash of ~$25m.

Metallurgical issues: Detailed metallurgical test work has been completed on the open pit

options but is yet to be completed on the underground resource in detail. Initial indications

suggest that improvements can be expected, but this is pending additional test work.

Regulatory and social licence approvals: WAF has a mining permit and ESIA approved

for a Heap Leach operation. It is yet to update this process for a CIL processing plant and

underground operation. The granting of a heap leach permit suggests, but does not

guarantee these additional permits will be granted.

Technical risks: a Definitive Feasibility study has been completed on an open pit mining

scenario at Sanbrado. A study is yet to be completed on a combined underground and

open pit mining scenario. Greater de-risking of the project is expected as the company

completes a combined Feasibility Study in 2018.

Corporate/M&A risks. Risks associated with M&A activity include differences between the

entities and the market’s perception of value associated with completed transactions, the

actual performance of an acquired asset vs its expected performance as assessed by the

acquirer. We view WAF as a potential takeover target.

Commodity price and exchange rate volatility: Gold price and exchange rates are

exposed to a number of unpredictable economic factors that are hard to predict and could

alter WAFs revenue potential. Revenue and costs are paid in a different currency (USD

and CAF) to WAF’s domestic currency.

Africa: Africa offers considerable upside opportunities due to its relative lack of

development and exploration of its mining potential. However, with this opportunity comes

risk of social unrest, lack of infrastructure and unexpected government changes to mining

codes and nationalisation. Each country will vary in risk profile and Burkina Faso is

considered considerably more favourable than many African countries due to a stable

mining code that supports mining investment. However, Burkina Faso has experienced a

forced change in government in recent years and some social unrest, though this has not

overly impacted mining in the country to date.

Page 23

West African Resources (WAF) 27 November 2017

West African Resources as at 27 November 2017

Recommendation Buy, Speculative

Price $0.39

$0.62

Table 9 - Financial summary

SOURCE: BELL POTTER SECURITIES ESTIMATES

PROFIT AND LOSS FINANCIAL RATIOS

Year ending 30 June Unit 2018e 2019e 2020e 2021e 2022e Year ending 30 June Unit 2018e 2019e 2020e 2021e 2022e

Revenue $m - - - 520.7 549.9 VALUATION

Expense $m (14.2) (10.5) (8.5) (159.4) (175.6) NPAT $m (14) (11) (10) 257 242

EBITDA $m (14.2) (10.5) (8.5) 361.3 374.2 Reported EPS c/sh (2) (1) (1) 31 29

Depreciation $m - - - (35.3) (40.5) EPS growth % n.a n.a n.a n.a -6%

EBIT $m (14.2) (10.5) (8.5) 325.9 333.7 PER x -16.1x -31.1x -31.2x 1.3x 1.4x

Net interest expense $m 0.0 - (2.3) (7.7) (2.4) DPS c/sh - - - - -

PBT $m (14.1) (10.5) (10.5) 318.5 331.3 Franking % 0% 0% 0% 0% 0%

Tax expense $m - - - (61.3) (89.0) Yield % 0% 0% 0% 0% 0%

NPAT $m (14.1) (10.5) (10.5) 257.2 242.3 FCF/share c/sh nm nm nm 32 32

P/FCFPS x nm nm nm 1.2x 1.2x

CASH FLOW EV/EBITDA x -14.2x -19.2x -23.7x 0.6x 0.5x

Year ending 30 June Unit 2018e 2019e 2020e 2021e 2022e EBITDA margin % nm nm nm 69% 68%

OPERATING CASHFLOW EBIT margin % nm nm nm 63% 61%

Receipts $m - - - 520.7 549.9 Return on assets % -72% -14% -6% 80% 46%

Payments $m (2.3) (2.0) (2.0) (154.4) (170.6) Return on equity % -81% -17% -11% 116% 51%

Tax $m - - - (61.3) (89.0) LIQUIDITY & LEVERAGE

Net interest $m 0.0 - (2.3) (7.7) (2.4) Net debt (cash) $m (19) (45) 105 (163) (430)

Other $m - - 0.3 0.3 - ND / E % na na 113% na na

Operating cash flow $m (2.2) (2.0) (4.0) 297.6 287.8 ND / (ND + E) % na na 53% na na

INVESTING CASHFLOW Current ratio x 9.8x 2.3x 0.1x 3.1x 13.3x

Capex & Mine Development $m (0.1) (60.0) (140.0) (25.1) (15.9) EBITDA / Interest x nm nm -3.7x 47.0x 154.5x

Sale of PP&E $m - - - - -

Exploration $m (11.9) (8.5) (6.5) (5.0) (5.0) MINERAL RESOURCES, RESERVES & MINE PLAN ASSUMPTIONS (Attributable)

Investing cash flow $m (12.0) (68.5) (146.5) (30.1) (20.9) Total Mt Au (g/t) Moz Au EV/oz

FINANCING CASHFLOW Reserve 15 1.7 0.8 $244

Share issues/(buy-backs) $m 22.6 96.0 0.6 0.9 - Resource 46 1.7 2.5 $82

Debt proceeds/(repayments) $m - 30.0 90.0 (43.6) (43.6) LOM Production 23 2.2 1.7 $120

Dividends $m - - - - - - *assumed production includes low grade stockpiles but excludes 0.5moz of TB underground reserves

Other $m 0.2 (0.3) - - - PROJECT ASSUMPTIONS - production profile, costs, capex & pricing

Financing cash flow $m 22.7 126.0 90.6 (42.7) (43.6) Year ending 30 June Unit 2018e 2019e 2020e 2021e 2022e

Cash generated/(lost) $m 8.6 55.5 (59.9) 224.8 223.3 Currency US$/A$ 0.77 0.75 0.75 0.75 0.75

Gold price US$/oz 1,313 1,360 1,420 1,450 1,450

BALANCE SHEET Gold price A$/oz 1,706 1,813 1,893 1,933 1,933

Year ending 30 June Unit 2018e 2019e 2020e 2021e 2022e Cash costs (C1) A$/oz - - - 459 489

ASSETS AISC A$/oz - - - 696 709

Cash & short term investments $m 19.1 74.6 14.7 239.5 462.8 CAPEX - growth A$m - (60) (140) (10) -

Other current assets $m 0.4 0.4 0.4 0.4 0.3 CAPEX - sustaining A$m - - - (15) (16)

PPE & Exp. & Dev. $m 0.1 60.1 200.1 189.9 165.3 Ore milled Mt - - - 2.1 2.5

Other non-current assets $m (0.0) (0.0) (0.0) 0.0 0.0 Head grade g/t Au - - - 4.6 3.8

Total assets $m 19.6 135.1 215.2 429.8 628.4 Attributable Gold Production oz Au - - - 269,311 284,410

LIABILITIES Gold sold oz Au - - - 269,311 284,410

Accounts payable $m 2.0 2.0 2.0 2.0 2.0

Borrowings $m - 30.0 120.0 76.4 32.7 VALUATION

Provisions $m - - - - - Shares on issue (m) 578.7

Other $m - - - - - ITM options (m) 20.0

Total liabilities $m 2.0 32.0 122.0 78.3 34.7 Performance rights (m) -

SHAREHOLDER'S EQUITY Unpaid capital (m) 243.6

Share capital $m 88.2 184.2 184.8 185.7 185.7 Diluted (m) 842.3

Reserves $m 6.3 6.3 6.3 6.3 6.3 SOTP* A$m A$/sh

Retained earnings $m (77.0) (87.5) (98.0) 159.2 401.6 90% Sanbrado (risk discount 40%, NPV10%) 349.5 0.60

Non-controlling interest $m - - - - - Exploration Upside 50.0 0.09

Total equity $m 17.5 103.0 93.1 351.3 593.6 Cash (est. end qtr) 24.4 0.04

Shares on issue at year end m 583.7 836.8 838.8 842.3 842.3 Investments - -

Total (undiluted) 423.8 0.73

CAPITAL STRUCTURE Cash from options 3.2 0.00

Unpaid capital 95.0 0.11

Shares on issue m 578.7 Total (fully diluted) 522.1 0.62

Performance shares / other m 0.0 * corporate costs and debt incorporated in project NPV

Total shares on issue m 578.7

Share price $/sh 0.390 LT* GOLD PRICE (US$/oz) & DISCOUNT RATE VALUATION SENSITIVITY TABLE

Market capitalisation $m 225.7 Discount/Price $1,150 $1,250 $1,300 $1,400 $1,450 $1,500

Net cash (est.end qtr) $m 24.4 15% $0.39 $0.43 $0.46 $0.50 $0.52 $0.54

Enterprise value (undiluted) $m 201.3 12% $0.43 $0.48 $0.50 $0.55 $0.58 $0.60

Options outstanding m 20.0 10% $0.46 $0.51 $0.54 $0.59 $0.62 $0.65

Options (in the money) m 20.0 8% $0.49 $0.55 $0.58 $0.64 $0.67 $0.70

Performance rights m 0.0 5% $0.55 $0.62 $0.66 $0.73 $0.77 $0.80

Issued shares (diluted for options/rights) m 598.7 0% $0.69 $0.79 $0.84 $0.93 $0.98 $1.03Market capitalisation (diluted) m 233.5 * long term = FY21 onwards

Net cash + options $m 27.6 PRODUCTION PROFILE FY17-FY23

Enterprise value (diluted) $m 205.9

MAJOR SHAREHOLDERS DIRECTORS & MANAGEMENT

% m Non Exec. Chair

Dynamic Fund (1832) 7.9% 45.7 Managing Director

Macquarie 7.0% 40.5 Non Exec. Director

Sprott 5.7% 33.0 Chief Ops Officer

Dir. & Mngmt. 4.1% 23.7

- -

Top 4 24.7% 142.9

Mine Life Assumption

Operation Sanbrado

Years 10

VALUATION METRICS

Implied capital return (%)

P/NAV (x)

End Qtr.

Mark Conelly

Richard Hyde

Simon Storm

Lyndon Hopkins

Current

59%

0.63

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

-

50,000

100,000

150,000

200,000

250,000

300,000

FY2021 FY2022 FY2023 FY2024 FY2025 FY2026 FY2027 FY2028 FY2029

Gold Produced Gold Price (A$/oz) AISC (A$/oz)

Page 24

West African Resources (WAF) 27 November 2017

Bell Potter Securities Limited ACN 25 006 390 7721

Level 38, Aurora Place 88 Phillip Street, Sydney 2000

Telephone +61 2 9255 7200 www.bellpotter.com.au

Recommendation structure

Buy: Expect >15% total return on a

12 month view. For stocks regarded

as ‘Speculative’ a return of >30% is

expected.

Hold: Expect total return between -5%

and 15% on a 12 month view

Sell: Expect <-5% total return on a

12 month view

Speculative Investments are either start-up

enterprises with nil or only prospective

operations or recently commenced

operations with only forecast cash flows, or

companies that have commenced

operations or have been in operation for

some time but have only forecast cash

flows and/or a stressed balance sheet.

Such investments may carry an

exceptionally high level of capital risk and

volatility of returns.

Research Team

Staff Member

TS Lim

Industrials

Sam Haddad

Chris Savage

Jonathan Snape

Tim Piper

John Hester

Tanushree Jain

Financials

TS Lim

Lafitani Sotiriou

Resources

Peter Arden

David Coates

Duncan Hughes

Associates

James Filius

Alexander McLean

Title/Sector

Head of Research

Industrials

Industrials

Industrials

Industrials

Healthcare

Healthcare/Biotech

Banks/Regionals

Diversified Financials

Resources

Resources

Resources

Associate Analyst

Associate Analyst

Phone

612 8224 2810

612 8224 2819

612 8224 2835

613 9235 1601

612 8224 2825

612 8224 2871

612 8224 2849

612 8224 2810

613 9235 1668

613 9235 1833

612 8224 2887

618 9326 7667

613 9235 1612

612 8224 2886

@bellpotter.com.au

tslim

shaddad

csavage

jsnape

tpiper

jhester

tnjain

tslim

lsotiriou

parden

dcoates

dhughes

jfilius

amclean

The following may affect your legal rights. Important Disclaimer:

This document is a private communication to clients and is not intended for public circulation or for the use of any third party, without the prior approval of Bell Potter Securities

Limited. In the USA and the UK this research is only for institutional investors. It is not for release, publication or distribution in whole or in part to any persons in the two specified

countries. In Hong Kong this research is being distributed by Bell Potter Securities (HK) Limited which is licensed and regulated by the Securities and Futures Commission,

Hong Kong. This is general investment advice only and does not constitute personal advice to any person. Because this document has been prepared without consideration of

any specific client’s financial situation, particular needs and investment objectives (‘relevant personal circumstances’), a Bell Potter Securities Limited investment adviser (or the

financial services licensee, or the representative of such licensee, who has provided you with this report by arrangement with Bell Potter Securities Limited) should be made

aware of your relevant personal circumstances and consulted before any investment decision is made on the basis of this document.

While this document is based on information from sources which are considered reliable, Bell Potter Securities Limited has not verified independently the information contained

in the document and Bell Potter Securities Limited and its directors, employees and consultants do not represent, warrant or guarantee, expressly or impliedly, that the

information contained in this document is complete or accurate. Nor does Bell Potter Securities Limited accept any responsibility for updating any advice, views opinions, or

recommendations contained in this document or for correcting any error or omission which may become apparent after the document has been issued.

Except insofar as liability under any statute cannot be excluded. Bell Potter Securities Limited and its directors, employees and consultants do not accept any liability (whether

arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage (whether direct, indirect, consequential or

otherwise) suffered by the recipient of this document or any other person.

Disclosure of interest:

Bell Potter Securities Limited, its employees, consultants and its associates within the meaning of Chapter 7 of the Corporations Law may receive commissions, underwriting

and management fees from transactions involving securities referred to in this document (which its representatives may directly share) and may from time to time hold interests

in the securities referred to in this document.

Exploration Risk Warning:

The stocks of resource companies without revenue streams from product sales should always be regarded as speculative in character. Since most exploration companies fit this

description, the speculative designation applies to all exploration stocks. Stocks with ‘Speculative’ designation are prone to high volatility in share price movements. Exploration and

regulatory risks are inherent in exploration stocks. Exploration companies engage in exploration programs that usually have multiple phases to them where positive results at some

stages are not indicative of ultimate exploration success and even after exploration success, there is often insufficient economic justification to warrant development of an extractive

operation and there is still significant risk that even a development project with favourable economic parameters and forecast outcomes may fail to achieve those outcomes.

Investors are advised to be cognisant of these risks before buying such a stock as WAF.

ANALYST CERTIFICATION

Each research analyst primarily responsible for the content of this research report, in whole or in part, certifies that with respect to each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal views about those securities or issuers and were prepared in an independent manner and (2) no part of his or her compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed by that research analyst in the research report.