Embed Size (px)

Citation preview

Section 13: Asset and Inventory Management13.1 OverviewSchools have substantial investments in stores, equipment, furniture, books and other learning materials. Although most items are covered by insurance administered within the Department, proper asset management procedures must be followed on purchases, custody, loss or disposal of these items to ensure accurate and up-to-date information is maintained.

This policy is aimed to guide schools in accounting for assets in accordance with relevant accounting standards and legislation.

By keeping appropriate records and identifying valuable items of school equipment and furniture, losses can be minimised and the value of the assets can be used to deliver educational services for the school.

It is crucial that schools strictly follow asset management policy and guidelines to ensure accurate reporting and accountability of assets are recorded in CASES21 Finance system.

13.2 Asset acquisition, recognition and recordingAn asset is a resource that, according to the Statement of Accounting Concepts 4 – Definitions and Recognition of the Elements of Financial Statements “represents service potential or future economic benefits controlled by the entity (government department which includes schools) as a result of past transactions or other past events”. This is the minimum dollar value of an item as determined under the Financial Management Act 1994, Part 5 Financial Responsibility.

13.2.1 Mandatory policy (Must do):

13.2.1.1 Purchases must be made in compliance with the Procurement Policy for Victorian Government Schools

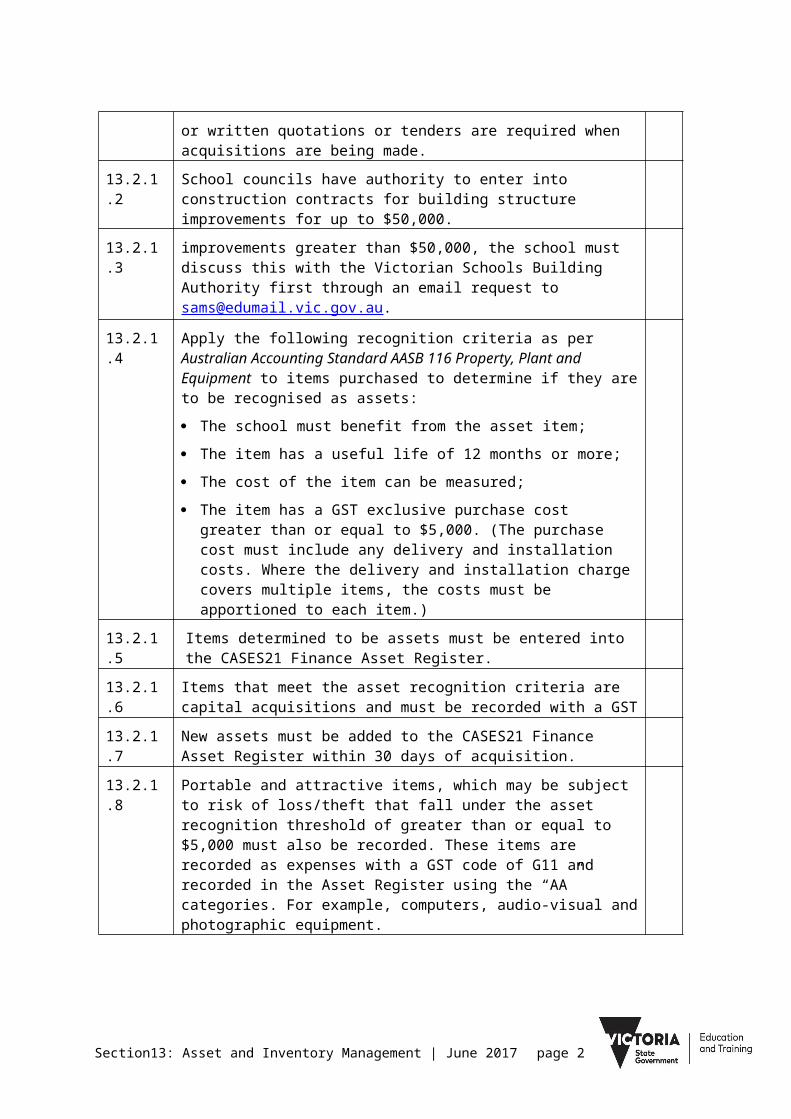

Depending on the value of the goods purchased, oral or written quotations or tenders are required when acquisitions are being made.

13.2.1.2 School councils have authority to enter into construction contracts for building structure improvements for up to $50,000.

13.2.1.3 If a school is considering building structure improvements greater than $50,000, the school must discuss this with the Victorian Schools Building Authority first through an email request to [email protected].

Section13: Asset and Inventory Management | June 2017 page 1

13.2.1.4 Apply the following recognition criteria as per Australian Accounting Standard AASB 116 Property, Plant and Equipment to items purchased to determine if they are to be recognised as assets:

The school must benefit from the asset item;

The item has a useful life of 12 months or more;

The cost of the item can be measured;

The item has a GST exclusive purchase cost greater than or equal to $5,000. (The purchase cost must include any delivery and installation costs. Where the delivery and installation charge covers multiple items, the costs must be apportioned to each item.)

13.2.1.5 Items determined to be assets must be entered into the CASES21 Finance Asset Register.

13.2.1.6 Items that meet the asset recognition criteria are capital acquisitions and must be recorded with a GST code of G10.

13.2.1.7 New assets must be added to the CASES21 Finance Asset Register within 30 days of acquisition.

13.2.1.8 Portable and attractive items, which may be subject to risk of loss/theft that fall under the asset recognition threshold of greater than or equal to $5,000 must also be recorded. These items are recorded as expenses with a GST code of G11 and recorded in the Asset Register using the “AA” categories. For example, computers, audio-visual and photographic equipment.

13.3 Identification of assetsIdentification of an asset or asset tagging is vital for schools. A good asset labelling system with ID numbers enable clear identification of assets, which facilitates the process of asset verification and loss prevention. A standard and consistent approach must be adopted across all schools.

13.3.1 Mandatory policy (Must do):

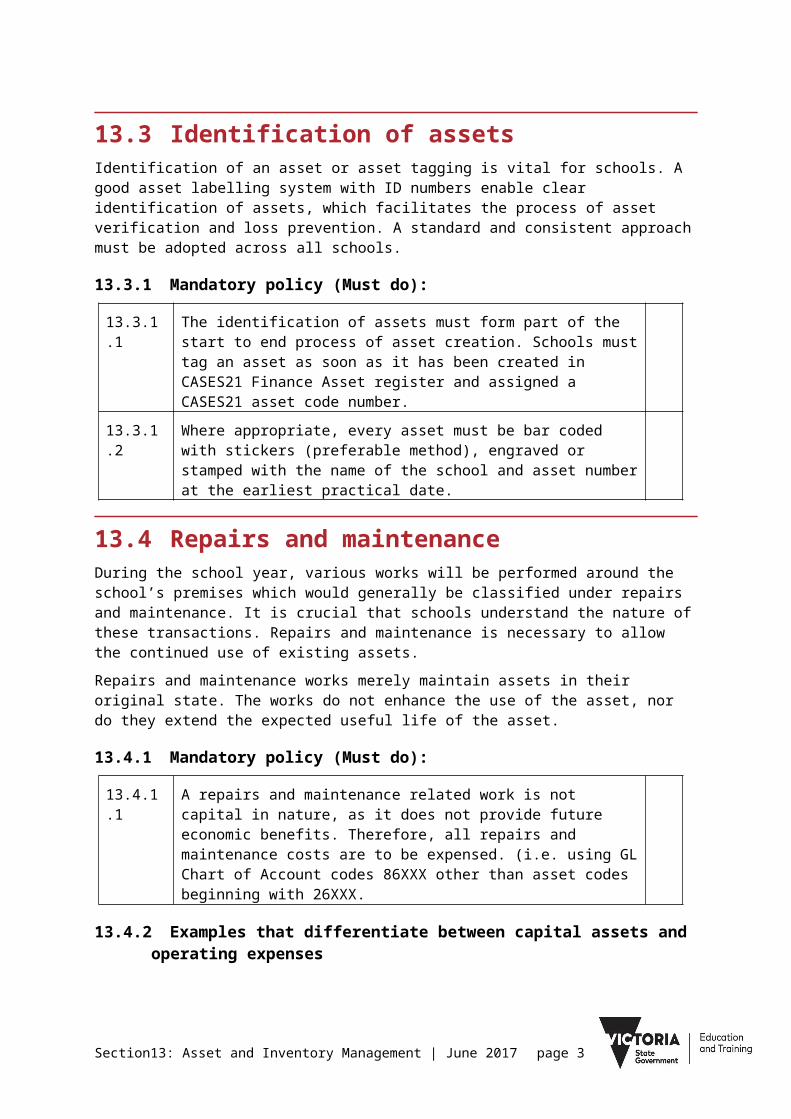

13.3.1.1 The identification of assets must form part of the start to end process of asset creation. Schools must tag an asset as soon as it has been created in CASES21 Finance Asset register and assigned a CASES21 asset code number.

13.3.1.2 Where appropriate, every asset must be bar coded with stickers (preferable method), engraved or stamped with the name of the school and asset number at the earliest practical date.

Section13: Asset and Inventory Management | June 2017 page 2

13.4 Repairs and maintenanceDuring the school year, various works will be performed around the school’s premises which would generally be classified under repairs and maintenance. It is crucial that schools understand the nature of these transactions. Repairs and maintenance is necessary to allow the continued use of existing assets.

Repairs and maintenance works merely maintain assets in their original state. The works do not enhance the use of the asset, nor do they extend the expected useful life of the asset.

13.4.1 Mandatory policy (Must do):

13.4.1.1 A repairs and maintenance related work is not capital in nature, as it does not provide future economic benefits. Therefore, all repairs and maintenance costs are to be expensed. (i.e. using GL Chart of Account codes 86XXX other than asset codes beginning with 26XXX.

13.4.2 Examples that differentiate between capital assets and operating expenses

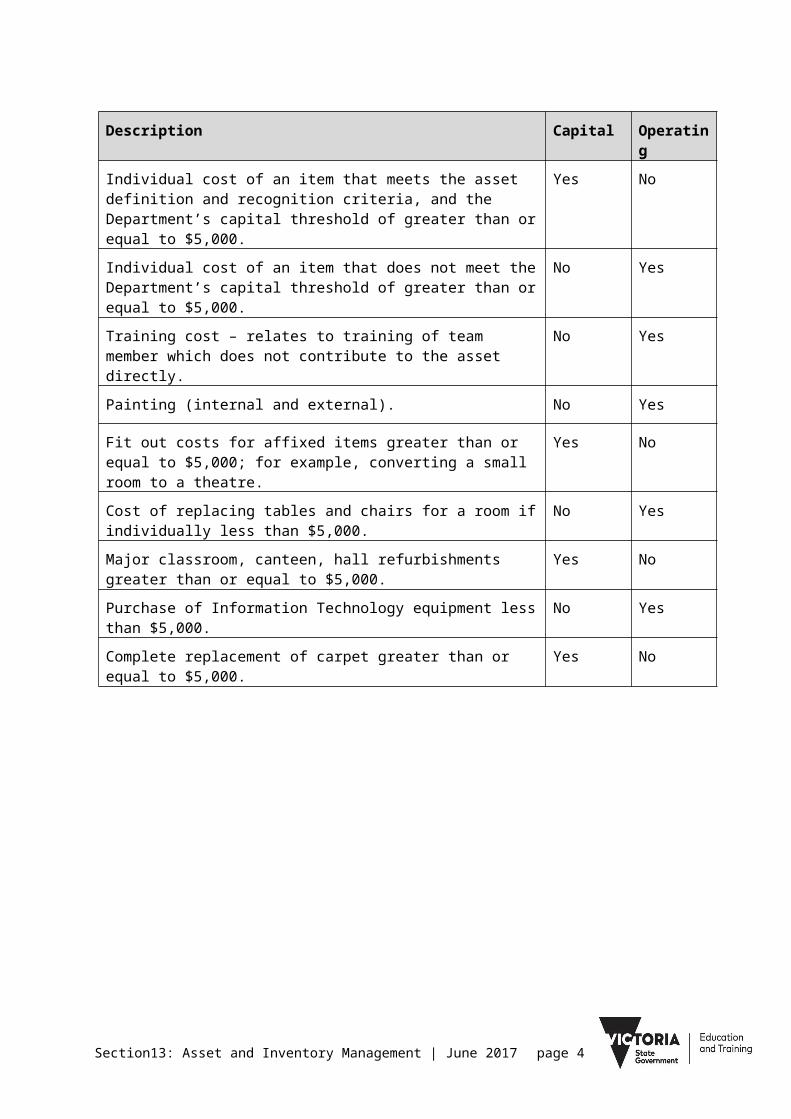

Description Capital Operating

Individual cost of an item that meets the asset definition and recognition criteria, and the Department’s capital threshold of greater than or equal to $5,000.

Yes No

Individual cost of an item that does not meet the Department’s capital threshold of greater than or equal to $5,000.

No Yes

Training cost – relates to training of team member which does not contribute to the asset directly.

No Yes

Painting (internal and external). No Yes

Fit out costs for affixed items greater than or equal to $5,000; for example, converting a small room to a theatre.

Yes No

Cost of replacing tables and chairs for a room if individually less than $5,000.

No Yes

Major classroom, canteen, hall refurbishments greater than or equal to $5,000.

Yes No

Purchase of Information Technology equipment less than $5,000. No Yes

Complete replacement of carpet greater than or equal to $5,000. Yes No

Section13: Asset and Inventory Management | June 2017 page 3

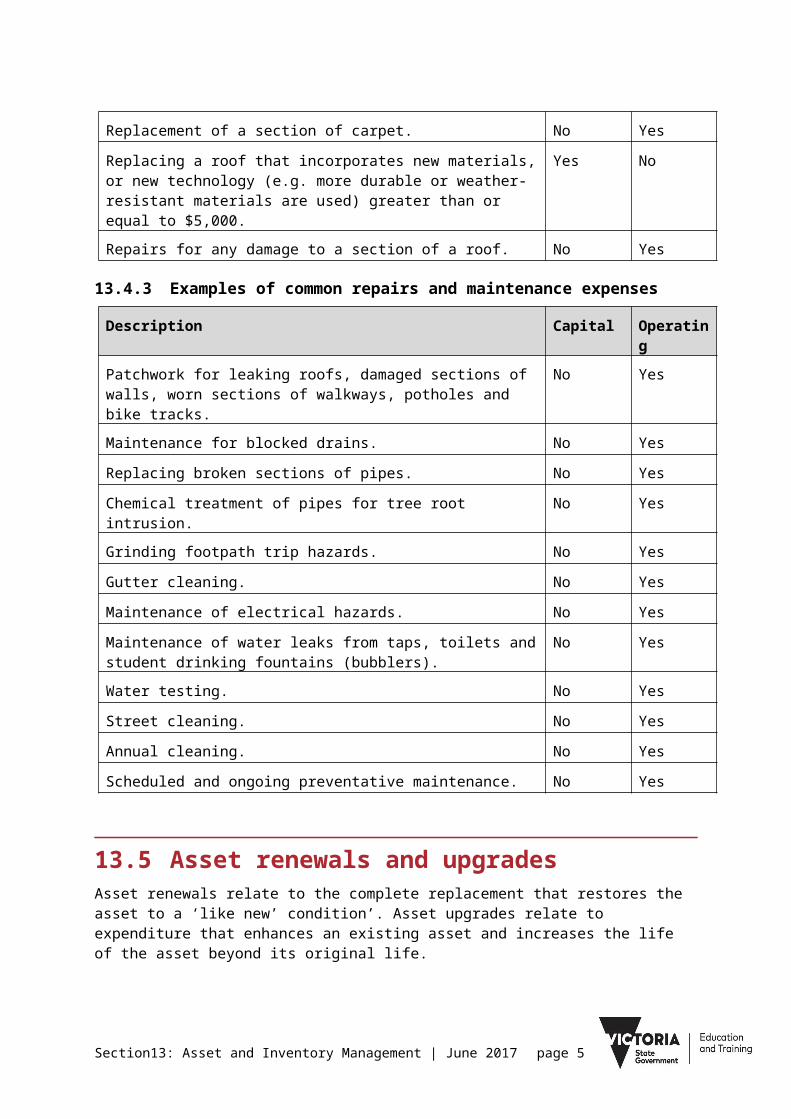

Replacement of a section of carpet. No Yes

Replacing a roof that incorporates new materials, or new technology (e.g. more durable or weather-resistant materials are used) greater than or equal to $5,000.

Yes No

Repairs for any damage to a section of a roof. No Yes

13.4.3 Examples of common repairs and maintenance expenses

Description Capital Operating

Patchwork for leaking roofs, damaged sections of walls, worn sections of walkways, potholes and bike tracks.

No Yes

Maintenance for blocked drains. No Yes

Replacing broken sections of pipes. No Yes

Chemical treatment of pipes for tree root intrusion. No Yes

Grinding footpath trip hazards. No Yes

Gutter cleaning. No Yes

Maintenance of electrical hazards. No Yes

Maintenance of water leaks from taps, toilets and student drinking fountains (bubblers).

No Yes

Water testing. No Yes

Street cleaning. No Yes

Annual cleaning. No Yes

Scheduled and ongoing preventative maintenance. No Yes

13.5 Asset renewals and upgradesAsset renewals relate to the complete replacement that restores the asset to a ‘like new’ condition’. Asset upgrades relate to expenditure that enhances an existing asset and increases the life of the asset beyond its original life.

Asset renewals and upgrades occur after the initial asset acquisition. It must be treated as capital as these activities enhance the use of the asset, its service potential, extend its expected useful life (beyond 12 months) and provide future economic benefits. Asset renewals are distinguished from general repairs relating to reactive/planned maintenance that merely restore the assets through ‘wear and tear’.

Section13: Asset and Inventory Management | June 2017 page 4

13.5.1 Mandatory policy (Must do):

13.5.1.1 Asset renewals and upgrades are to be capitalised if the item has a useful life of 12 months or more and has a GST exclusive purchase cost greater than or equal to $5,000. It is also essential that the replaced/renewed asset is derecognised (disposed).

13.5.2 Examples that differentiate between capital assets and operating expenses for asset renewals

Description Capital Operating

Carpet, Tiling and Linoleum replacement for entire area (Complete renewal) greater than or equal to $5,000.

Yes No

Carpet, Tiling and Linoleum replacement for part of area (Part renewal).

No Yes

Landscape development renewals for entire area (Complete renewal) greater than or equal to $5,000, including:

Complete wall replacement;

Re-pavement of entire area;

Re-sewing/re-sodding of entire area;

Asphalt resurfacing of entire area.

Yes No

Landscape maintenance (section/ part of repair):

Section of wall replacement;

Re-pavement of section;

Re-sewing/re-sodding of section;

Asphalt resurfacing of section.

No Yes

Oval/Court and Pitch resurfacing (complete renewal) greater than or equal to $5,000:

Resurfacing for entire oval (renewing old synthetic grass with new synthetic grass);

Resurfacing for entire court/pitch area.

Yes No

Oval/ Court and Pitch maintenance (section/ part of repair)

Resurfacing or part repair of a section of the oval / court / pitch area.

No Yes

Replacement of entire roof greater than or equal to $5,000. Yes No

Maintenance of roof - Replacement of a section of the roof. No Yes

Section13: Asset and Inventory Management | June 2017 page 5

Replacement of performing arts room equipment where individual equipment is greater than or equal to $5,000

Yes No

Resealing for the entire road surface greater than or equal to $5,000.

Yes No

Resealing for part or short section of the road. No Yes

Gravel re-sheeting for entire road length greater than or equal to $5,000.

Yes No

Gravel re-sheeting for part of or short sections of the road length. No Yes

13.5.3 Examples of common asset upgrades

Description Capital Operating

Electrical system upgrade greater than or equal to $5,000. Yes No

Drainage and grounds upgrades greater than or equal to $5,000. Yes No

Building/Structural extensions or enhancements greater than or equal to $5,000 (for example, changing domestic kitchen to a commercial kitchen).

Yes No

Car park extensions greater than or equal to $5,000. Yes No

Oval/Court and Pitch resurfacing greater than or equal to $5,000

Changing from natural grass to synthetic grass;

Changing from asphalt to rubber.

Yes No

Replacing pumps with greater capacity greater than or equal to $5,000.

Yes No

Replacing timber with concrete greater than or equal to $5,000. Yes No

Sprinkler system upgrades greater than or equal to $5,000. Yes No

Widening footpaths greater than or equal to $5,000. Yes No

Pavement upgrade – higher standard greater than or equal to $5,000 (for example, upgrading from gravel surface to concrete).

Yes No

Enlarging a grandstand at a sporting facility greater than or equal to $5,000.

Yes No

Section13: Asset and Inventory Management | June 2017 page 6

13.6 Fit out costsThe purchase price and installation of fit out items (e.g. office partitioning) are capitalised as their own separately identifiable fit out if has a GST exclusive purchase cost greater than or equal to $5,000. Installations are capitalised as they are ‘directly attributable’ in bringing the fit-out items to the condition and location ready for use.

Only items that are ‘affixed’ (for example carpet, blackboard (if fixed to the wall), blinds and curtains) are to form part of the initial fit out. All moveable items (such as tables, chairs, desks, shelves and moveable whiteboards) are capitalised separately if they individually meet the Department’s threshold of greater than or equal to $5,000.

13.6.1 Examples that differentiate between assets that are part of initial fit out cost and separately identifiable plant and equipment

Description Initial Fit Out

Separate asset

Partitions. Yes No

Affixed cabinets. Yes No

Blinds and curtains. Yes No

Affixed projectors. Yes No

Portable projectors greater than or equal to $5,000. No Yes

Affixed digital boards. Yes No

Portable digital boards greater than or equal to $5,000. No Yes

Carpet for entire room. Yes No

Tables and chairs individually greater than or equal to $5,000. No Yes

Moveable shelves individually greater than or equal to $5,000. No Yes

Affixed shelves. Yes No

Section13: Asset and Inventory Management | June 2017 page 7

13.6.2 Case Studies of initial Fit Out of a school classroom

Case Study – Initial Fit Out of a school classroomAs an example, if you had a classroom that has: • 18 tables @ $118.00 each • 24 chairs @ $23.00 each • a desk and chair for the teacher @ $249.00 and $68.00• two sets of book shelves @ $350.00• a blackboard @ $450.00• a whiteboard (mobile) @ $250.00• carpet @ $3750.00• blinds or curtains @ $1534.00.The total dollar value of the furniture and fittings in this room would be $5,734.00, as the only items that are capitalised in the initial fit out are ‘affixed’ items such as the carpet, blackboard (if fixed to the wall), blinds and curtains. All moveable items such as tables, chairs, desks, shelves and the moveable whiteboard are capitalised separately if they individually meet the Department’s threshold of $5,000. If the individual items are <$5,000 then the item must be expensed to the most appropriate CASES21 Chart of account code.

Section13: Asset and Inventory Management | June 2017 page 8

13.7 Asset stocktake guidelinesThe accuracy and completeness of appropriate records is an essential basis for adequate asset verification.

13.7.1 Mandatory policy (Must do):

Stocktake

13.7.1.1 A physical stocktake of all assets must be conducted every two years. Each item must be sighted at least once every two years.

An asset stocktake:

can be performed in stages throughout the year;

must minimise interference to educational programs.

Could be conducted on:

certain asset categories or groups of assets each month or in particular months;

during each term; or

during vacation periods.

13.7.1.2 For attractive items or shared items (e.g. cameras), it would be prudent to sight these items at least once a term.

13.7.1.3 When carrying out stocktakes or asset verifications, regardless of the method used, the following procedures must be observed:

The principal must nominate the date or period of time for the stocktake to take place.

A stocktaking officer must be appointed by the principal to conduct and supervise the stocktake. This person will be independent and must not have custody of any asset to be counted. Assistant stocktaking officers (i.e. business manager), being persons who have knowledge of the location and identity of the items in particular areas, must also be appointed. An assistant stocktaking officer can be someone who has the responsibility for, or custody of, assets.

Stocktake sheets listing all assets held by the school, by name and location, must be prepared from the asset register.

The stocktake sheets must list the serial numbers or other unique identifying reference against each asset to assist with the asset recognition.

On the appointed date, the areas designated for the stocktake must be systematically checked for assets listed on the appropriate

Section13: Asset and Inventory Management | June 2017 page 9

stocktake sheet by the stocktaking officer and one other person. The quantity of each item must be recorded on the stocktake sheet. The serial numbers or unique identifiers must also be confirmed on the stocktake sheet.

If a third party is engaged to conduct the stocktake, the use of electronic equipment may be used rather than stocktake sheets. The information that is to be provided in the stocktake sheets must be the same as what is entered into the electronic equipment used to conduct the stocktake.

Items encountered that match the definition of an asset that is not on the stocktake sheet/report issued by the third party conducting the stocktake must be recorded for checking on the asset register.

On completion of the physical check of each stocktake sheet/report from the third party in the stocktake, the stocktaking officer must reconcile the count on the stocktake sheet/report from third party engaged to conduct stocktake against the asset register.

Where discrepancies are disclosed the items involved are subject to a recount.

All stocktake sheets or reports produced by the third party must be signed off by the officers who conducted the count and all discrepancies notified in writing to the principal.

13.7.1.4 The stocktake results must accurately reconcile the physical assets to the assets recorded in the CASES21 Finance Asset register.

13.7.1.5 All adjustments identified by the stocktake must be approved by the school council before an adjustment is recorded in CASES21 Asset register.

Discrepancies in Stocktake or Loss of Assets If a stocktake reveals a substantial discrepancy (for example items of equipment/furniture located that are not recorded in the asset register and/ or loss of equipment recorded in the equipment register), the following action must be taken:

13.7.1.6 In the case of items not being recorded in the asset register, the matter must be drawn to the attention of the principal.

13.7.1.7 An investigation must be undertaken to identify how the items were acquired. Only then will it be possible to determine whether the items are owned by the school and is in its custody, the value (cost) of the items and whether they should be treated as school assets.

13.7.1.8 In the case of asset additions because of stocktaking activities, the school must:

Determine the fair value of the asset and advise Schools

Section13: Asset and Inventory Management | June 2017 page 10

Financial Management Support team, if the value of the asset is greater than or equal to $5,000. Email: [email protected]

Schools Financial Management Support team will liaise with Financial Services Division (FSD) to assess the asset and verify the value. If the value of the asset is found to be less than $5,000 then the school must create the asset in CASES21 using ‘PY’ as the asset type and assign a value of zero. If the asset is found to be greater than or equal to $5,000 then the school will be advised of the appropriate asset type by FSD, process an asset additions journal to adjust the quantity and price for the asset, process a subsequent General Ledger journal to reflect the value added in the additions journal and send supporting documentation to [email protected]

13.7.1.9 In the case of loss of equipment, an officer must be appointed by the principal to investigate. The principal must be provided with a written report of discrepancies stating what action has been taken to locate the missing items.

13.7.1.10

The principal must then recommend to the school council the appropriate action/s that must be taken.

Regulations require that all cases of suspected or actual theft, wilful damage, arson, irregularity or fraud in receipt or disposal of money or other property of any kind is to be reported to the regional director and relevant department personnel. Refer to section 3 Risk Management.

13.7.1.11

A police report must be filed if the value of the stolen/lost asset is above the Department’s capitalisation threshold (greater than or equal to $5,000).

13.7.1.12

If the school council is satisfied that any missing item cannot be recovered and appropriate action has been taken as above, the next action is to write off the item and adjust the asset register in CASES21.

13.7.2 Stocktake of Library MaterialsThe increasing importance of library resources in the educational programs of schools and the number, variety and monetary value of these resources make the effectiveness of the library’s stock control methods central to the safeguarding of assets and the efficient operation of the library.

13.7.3 Mandatory policy (Must do):

13.7.3.1 A full stocktake of library books and publications is to be carried out once every two years.

Section13: Asset and Inventory Management | June 2017 page 11

13.7.3.2 While educational evaluations of libraries such as culling, updating the catalogue and reorganising records can be conducted at any time, the stocktake provides a good opportunity to carry out these tasks.

13.7.3.3 Stocktakes are to be conducted in liaison with the library manager at such times as the principal considers best to achieve the aims of effective stock and education management of the library resource. This is to be achieved with a minimum of interference to the school’s educational program.

13.7.3.4 The most desirable method of conducting the stocktake will be to carry out a complete stocktake of all library resources at the one time. The advantage of this is that it provides a comprehensive review of the effectiveness of stock-control methods at a particular time.

13.7.3.5 Other options include:

a half stocktake annually; or

a progressive stocktake of the library covering each area at convenient intervals over two years or a shorter period.

13.7.3.6 Irrespective of the method and frequency of the stocktake, it is recognised that staff involved can normally only effectively perform a stocktake if entry by pupils and other non-involved staff to the stocktaking area is prevented or very strictly controlled. The degree to which access to the library is to be limited or prevented is clearly one which must be clarified by the principal in discussion with the library manager prior to the commencement of the stocktaking exercise.

13.7.3.7 The library manager is responsible for the initiation and maintenance of effective stock-control methods within the library.

13.7.3.8 As a result of a stocktake, the library’s records must accurately show for the area covered:

accession of items available for use;

accession of items missing;

accession of items written off as unsuitable for continued inclusion in the library;

the total net stock at the end of the period covered by the stocktake.

13.7.3.9 At the conclusion of the stocktake, whether full or progressive, a stocktake statement must be prepared.

Section13: Asset and Inventory Management | June 2017 page 12

13.7.3.10

After the stocktake is completed the library manager:

presents the stocktake statement to the principal and discusses appropriate follow-up action;

with the approval of the principal, writes off items that have been culled from the collection or lost, damaged or missing for more than two years and makes appropriate notations in the accession or card register;

removes the shelf-list cards for written-off items.

13.7.3.11

Where schools suffer loss or damage to library materials as a result of vandalism, theft, fire, flood, rain etc. the library manager must discuss with the principal what action must be taken to assess and quantity the loss or damage and whether a full or partial stocktake is required.

Adjusting for duplicate entries in Asset register

13.7.4 Mandatory policy (Must do):

13.7.4.1 Complete a write-off transaction – Refer to CASES21 Finance Business Process Guide Section 4 – Assets for guidance on disposals.

13.7.4.2 Complete Asset Status Change Request form

Section13: Asset and Inventory Management | June 2017 page 13

13.8 Receipt of Donated Property, Equipment or Materials

13.8.1 Mandatory policy (Must do):

13.8.1.1 The receipt of donated equipment or materials must be reported by the principal at the next school council meeting and minuted.

13.8.1.2 The school must perform the following:

Determine the fair value of the asset and advise the Schools Financial Management Support team. Email: [email protected] if the value of the asset is greater than or equal to $5,000.

The Schools Financial Management Support team will liaise with Financial Services Division (FSD) to assess the asset and verify the value. If the value of the asset is found to be less than $5,000 then the school should create the asset in CASES21 using ‘DO’ as the asset type and assign a value of zero. If the asset is found to be greater than or equal to $5,000 then the school will be advised of the appropriate asset type by FSD, process an asset additions journal to adjust the quantity and price for the asset, process a subsequent General Ledger journal to reflect the value added in the additions journal and send supporting documentation to [email protected]

13.8.1.3 Schools must inform the Department if they have received a donated parcel of land and or a building. Email the Schools Financial Management Support team at [email protected] and the Victorian.

13.8.1.4 Schools are also required to contact the Victorian Schools Building Authority with all the relevant details regarding the donation of land and or a building, as either of these assets must be recorded onto the Department’s asset register at fair value.

Please send an email to the school asset account [email protected] describing the asset. A Victorian Schools Building Authority team member will then be in contact with you.

Section13: Asset and Inventory Management | June 2017 page 14

13.9 Hire/Leasing of Equipment School councils have the necessary authority to enter into hire/lease of equipment agreements provided the conditions stipulated in Part 2.3 Division 3 Section 2.3.6 (3) of the Education and Training Reform Act 2006 and must be strictly adhered to.

13.9.1 Mandatory policy (Must do):

13.9.1.1 A school may enter into an operating lease agreement. For example, a school may lease a photocopier for a period of 3 years.

13.9.1.2 Equipment leased via an operating lease must be included in the CASES21 Asset module (Asset Register) with a purchase cost of $0.00, quantity, lease start and end date and monthly lease cost.

13.9.1.3 Leased assets are not covered under School Equipment Coverage Scheme (SECS) for insurance and schools must obtain their own insurance for leased items.

13.9.2 Prohibited policy (Must not do):

13.9.2.1 School councils do not have the authority to borrow money so therefore are unable to enter into finance leases (as opposed to operating leases).

13.10 Insurance on Stores13.10.1 OverviewThe Department’s School Equipment Coverage Scheme (SECS) applies to school equipment and stores.

13.10.2 Prohibited policy (Must not):

13.10.2.1

Leased assets are not covered under School Equipment Coverage Scheme (SECS) for insurance and schools must obtain their own insurance for leased items.

13.10.3 Additional resources SECS Policy and Guidelines can be viewed from the following link: School Equipment

Coverage Scheme – Policy & Guidelines.

Section13: Asset and Inventory Management | June 2017 page 15

13.11 Library Materials13.11.1 Mandatory policy (Must do):

Identification and Recording Library Materials

13.11.1.1

The library manager is responsible for maintaining methods of stock control that accounts for all library books, textbooks, and other non-accountable items and materials.

13.11.1.2

Where there is no library manager, the direct responsibility is assigned to the principal.

13.11.1.3

All library materials received from any source, except materials having a low value or short life, are to be actioned as soon as practical after receipt. The following are typical examples of items that are entered into the asset register: books, maps, audio materials, projected visual materials, video materials, pictures, charts, microfilms and computer materials.

The accession of Library Materials

13.11.1.4

Alternative methods of the accession of library materials are:

a library asset register/book;

a card register (cards filed in ascending number order) and/or order slip;

a periodical card register (for newspapers, magazines and other periodicals);

electronic tracking e.g. bar coding.

Library Loan Records

13.11.1.5

A record of items on loan must be maintained. School councils may implement a library fine system to encourage the return of borrowed materials.

Section13: Asset and Inventory Management | June 2017 page 16

13.12 Other Assets and TextbooksSchools are required to operate effective stock control over all equipment, textbooks, class sets etc.

13.12.1 Mandatory policy (Must do):

13.12.1.1

A single book with a value of greater than or equal to $5,000 must be capitalised

13.12.1.2

Works of art with a value in excess of $200 must be recorded in the CASES21 Finance asset register.

13.12.1.3

Assets won as prizes, must be added to the CASES21 Finance asset register at their fair value at the time they were acquired.

13.13 Inventory ControlInventory may be divided into two types:

trade (canteen stock, school uniforms, stationery and office equipment such as calculators that are sold to pupils and staff);

consumable items used in the day-to-day running of the school.

They are items that must be monitored and managed for the efficient running of the school and for insurance purposes.

13.13.1 Mandatory policy (Must do):

13.13.1.1

Inventory items must be recorded separately.

13.13.2 Prohibited policy (Must not do):

13.13.2.1

Inventory items must not be recorded on the CASES21 Finance asset register.

13.13.3 Hazardous Substances All chemicals must be considered dangerous. Effective stock control of chemicals is therefore essential.

13.13.4 Mandatory policy (Must do):

13.13.4.1

Schools must base their control of chemical stocks on the use of secure areas for the storage of dangerous or bulk reserve supplies, and stock cards that note receipt and issue of chemicals.

Section13: Asset and Inventory Management | June 2017 page 17

13.13.4.2

Schools must comply with the Dangerous Goods (Storage and Handling) Regulations 2000 and the Occupational Health and Safety (Hazardous Substances) 1999 by maintaining a Chemicals/Hazardous Substances/ Dangerous Goods Register together with Material Safety Data Sheets (MSDs) obtained from the supplier.

13.13.5 Additional ResourcesFor further information, refer to the, Health, Safety and Worker's Compensation website.

13.13.6 Class and Library MaterialsEffective stock control over class and library materials is essential.

13.13.7 Mandatory policy (Must do):

13.13.7.1

When textbooks and similar learning materials are issued on loan to students, a record of the issue must be maintained to facilitate their return.

13.13.7.2

In cases of low-value or short-duration loans, the principal must implement an alternative system of control. Schools must develop systems appropriate to their circumstances.

13.14 Loan of Equipment to Community Groups or Individuals

13.14.1 Mandatory policy (Must do):

13.14.1.1

A principal may make loans of specified items of school equipment to individual students.

13.14.1.2

The officer who is designated this authority is responsible for ensuring that records, including the signature of the student borrowing the article, are maintained to allow for the recovery of the article.

13.14.1.3

When equipment is lent by the school principal, a receipt signed by the borrower must be obtained and a record of the loan must be maintained to facilitate its return.

13.14.1.4

If library materials or textbooks are lent to students, teachers or other school-based staff, a record of the loan must be maintained to facilitate their return.

13.14.1.5

Items borrowed for personal use must be insured by the borrower.

Section13: Asset and Inventory Management | June 2017 page 18

13.15 Transfer of assets between schools 13.15.1 Mandatory policy (Must do):

13.15.1.1

When a school transfers an asset, the receiving school must enter the asset at the same value as the transferring school has written off the asset.

13.15.1.2

The items must be at current Net Book Value (NBV).

13.15.1.3

Schools must ensure that an Asset Status Change Request form is completed and approved by the principal before any physical items are transferred.

For further guidance contact the Schools Financial Management Support team. Email: [email protected]

13.16 Transfer of Materials or EquipmentWhen materials or equipment are transferred between Government schools or to an office of the Department without a change being made to their value, a transfer advice giving full details, must be completed in triplicate by the dispatching schools.

13.16.1 Mandatory policy (Must do):

13.16.1.1

Schools must ensure that an Asset Status Change Request form is completed and approved by the principal before any physical items are transferred out.

Section13: Asset and Inventory Management | June 2017 page 19

13.17 Disposal of Surplus or Unserviceable Assets of Materials

School councils, under Part 2.3, Division 5, Section 2.3.1.8 of the Education and Training Reform Act 2006, can sell assets/equipment, goods or other personal property acquired for use in the school. The main purpose of this section of the Act is to enable school councils to sell obsolete and surplus goods and equipment.

13.17.1 Mandatory Policy (Must do):

General Policy

13.17.1.1

All surplus, obsolete or unserviceable stores or assets must be assessed by a board of survey prior to any decision being made about disposal.

13.17.1.2

A school council can retain the proceeds of the sale of the asset if the amount is less than $10,000. (Less than $10,000 threshold is determined by the Minister).

13.17.1.3

If the proceeds of the sale of an asset exceeds $10,000, the school council must seek approval in writing from their local region al director to retain the proceeds of sale.

13.17.1.4

All money raised by the disposal of goods must be re-used to the benefit of the educational program of the school.

Board of Survey

13.17.1.5 In the normal course of events, three people constitute a board of survey. The board will consist of the principal, a school council representative and a third nominee.

13.17.1.6 The board’s role is to:

identify obsolete or unserviceable equipment;

recommend to school council a course of disposal action, for example, wreck, convert to a training aid or sell;

in the case of asset sales, advertise locally that the asset is available for purchase and request bids from any interested person; and

arrange for any proceeds of sale to be paid to the school or the local regional finance manager, in accordance with the above.

13.17.1.7 Asset Status Change Request form must be completed in a timely manner.

Section13: Asset and Inventory Management | June 2017 page 20

13.18 Delegated authority for disposal of assets (land and/or buildings)

School councils have the delegated authority to dispose of school assets (land and/or building) with a residual value of up to $50,000.

13.18.1 Mandatory Policy (Must do):

13.18.1.1

Schools must seek advice on the value of an asset prior to taking local action.

13.18.1.2

This is required regardless of whether the asset was originally funded by the Department or by the school.

13.18.1.3

Schools are required, regardless of whether the asset was originally funded by the Department or by the school, to provide the following:

Send an email to the school asset account [email protected] describing the demolition work you want to undertake, with a marked-up school plan clearly identifying the asset that is to be removed.

A Victorian Schools Building Authority team member will respond with a current asset value and the guidance for the principal to authorise the demolition.

Once the school has received the asset value, the school will need to provide an email authorising the demolition work with a marked-up (shaded or outlined in red) school plan showing the asset that has been disposed, the date of the disposal and how the asset was disposed (demolition, sale and removal).

A Victorian Schools Building Authority team member will remove the asset from the Department’s asset register.

If the asset value is greater than $50,000, the school must discuss the disposal of the asset with the Victorian Schools Building Authority first through an email request to [email protected].

Section13: Asset and Inventory Management | June 2017 page 21

13.19 Delegated authority for disposal of assets (Plant and Equipment and Intangibles)

13.19.1 Mandatory Policy (Must do):

13.19.1.1 Schools must ensure that the standard form is completed for asset disposals.

13.19.1.2 All Plant and Equipment asset disposals must be completed via the Asset Status Change Request Form in a timely manner.

13.19.1.3 All surplus, obsolete or unserviceable stores or assets must be assessed by a board of survey prior to any decision being made about disposal.

13.19.1.4 All money raised by the disposal of goods must be re-used to the benefit of the educational program of the school.

13.19.1.5 In the normal course of events, three people constitute a board of survey. The board must consist of the principal, a school council representative and a third nominee.

13.19.1.6 The board’s role is to:

identify obsolete or unserviceable equipment;

recommend to school council a course of disposal action, for example, wreck, convert to a training aid or sell.

13.19.1.7 Schools councils have the authorisation to dispose of assets with Net Book Value (NBV) up to $50,000 and any asset with a NBV higher than $50,000 must be approved by the Department.

13.19.1.8 Schools must first identify the asset through the asset register to be disposed, and then contact an asset team member by emailing [email protected] to obtain the NBV of the asset. This is to determine if approval is needed for the asset disposal from the Department.

13.19.1.9 The school must get the completed approval for the disposal of the asset before proceeding with the disposal in the CASES21 Asset module system.

13.19.1.10 The physical disposal of the asset must be initiated soon after CASES21 disposal.

13.19.1.11 All disposals must be signed off prior to the disposal of asset.

13.19.1.12 Disposal in CASES21 Asset module system will flow onto the Department’s asset management system.

Section13: Asset and Inventory Management | June 2017 page 22

13.19.1.13 It is critical that schools file all disposal forms and supporting documentation, as this information needs to be available upon request by the Department.

Legislative requirementsLegislationThe advice in this section was based on requirements outlined in the following legislation:

AASB 116 Property, Plant and Equipment, AASB 13 Fair Value Measurement, AASB 138 Intangible Assets.

Asset Management Accountability Framework.

Education and Training Reform Act 2006 – Part 2.3 Government School Councils.

Education and Training Regulations 2017 – Part 4 – Government School Councils and Parents Clubs.

Financial Management Act 1994 – Part 5 Financial Responsibility.

Financial Reporting Direction 103F Non-Financial Physical Assets.

Standing Directions of the Minister for Finance 2016 under the Financial Management Act 1994.

Statement of Accounting Concepts 4 – Definition and Recognition of the Elements of Financial Statements.

Definitions Asset An asset is, according to the Statement of Accounting Concepts 4 –

Definitions and Recognition of the Elements of Financial Statements, a resource that “represents service potential or future economic benefits controlled by the entity (government department) as a result of past transactions or other past events”.

The definition assumes:

the asset will generate a positive contribution for the entity – i.e. the service potential will be realised;

the entity has capacity to control the asset;

the asset possesses a value that can be measured reliably; and

the estimated value is above the minimum amount specified in a recognition threshold (greater than or equal to $5,000 Department’s threshold).

Asset clearing This is a holding account where transactions/amounts are recorded

Section13: Asset and Inventory Management | June 2017 page 23

account temporarily and that are to be transferred to specific asset accounts once the purchase is complete.

Asset disposal This is the act of selling an item (usually a long-term asset) that has been depreciated over its useful life or is no longer required by the school.

Asset recognition threshold (capitalisation threshold)

This is the minimum dollar amount below which expenditure is recorded, even if it associated with an activity that is typically capital in nature. The Department’s capitalisation threshold is greater than or equal to $5,000.

Asset register A comprehensive list of items and equipment that shows what the school owns. An asset register is used to track and manage school assets.

Control of an asset

Asset control is usually evidenced by an school’s:

ability to use the asset to achieve its objectives;

ability to restrict or change access to the asset;

ability to surrender the asset to another entity;

ability to dispose of the asset; and

obligation to bear the risks associated with holding the asset.

Fair value The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

Finance lease This effectively transfers ownership of the leased property from the company to the school at the end of the lease term, usually at a cost to the school (residual).

Characteristics of a finance lease are:

the lease is not able to be cancelled, or cancelled without the imposition of a large penalty;

ownership of the object leased is transferred at the end of the lease;

the lease contains a nominal purchase option;

the lease term is for 76 per cent or more than the useful life of the leased item;

the present value of the minimum lease payments is equal or greater than 90 per cent of the fair value of the leased item.

Importantly, school councils do not have the authority to borrow money so therefore are unable to enter into finance leases (as opposed to operating leases).

Section13: Asset and Inventory Management | June 2017 page 24

Net book value The net value of an asset. Equal to its original cost (its book value) minus depreciation and amortisation.

Non-current physical asset

These assets are items that are tangible – i.e. they have a physical nature and a useful life beyond the current accounting period, typically one year.

Non-current physical assets differ from inventory items as inventory items are ‘consumable’ (used up, expended, have a limited life, are on sold), or under the recognition threshold for the category.

Operating lease This is like a rental agreement where the goods are eventually returned to the lesser (company). For example, a school leases a photocopier for a period of three years. At the end of the three years, the school returns the photocopier to the company without further obligation.

Residual value The estimated amount that a school would currently obtain from disposal of the asset, after deducting the estimated costs of disposal, if the asset were already of the age and in the condition expected at the end of its useful life.

Stocktake Verification of the physical existence, location and condition of assets and inventories on a regular basis.

Useful life Is the period over which an asset is expected to be available for use by the school.

Section13: Asset and Inventory Management | June 2017 page 25

Additional resources CASES21 Finance Business Process Guide Section 4 – Assets

Chart of Accounts for Victorian Government Schools available on the Finance website: http://www.education.vic.gov.au/school/teachers/management/finance/Pages/cases21.aspx

School Policy and Advisory Guide http://www.education.vic.gov.au/school/principals/spag/Pages/spag.aspx

Version and revision control recordDate Version Approver Next Review

30/06/2017 1.0 Chief Finance Officer - Financial Services Division

01/11/2017

Section13: Asset and Inventory Management | June 2017 page 26

Section13: Asset and Inventory Management | June 2017 page 27