Embed Size (px)

Citation preview

PA R T 1SCOPE OF THE BUSINESS

1. SCOPE OF MORTGAGE LOAN BROKERAGE

2. SOURCES OF BUSINESS

Th

om

son

Lea

rnin

gT

M

Th

om

son

Lea

rnin

gT

M

C H A P T E R 1SCOPE OF MORTGAGE LOAN BROKERAGE

PREVIEWA career in real estate mortgage lending can be exciting andprofitable for a person who has energy and is self-motivated.Mortgage loan professionals help potential real estate buyersobtain financing to purchase a property and help property ownersplace a refinance loan on an existing parcel. Along the way,mortgage loan professionals provide a great service by informingborrowers about the costs and terms in the variety of loan pack-ages in the marketplace.

The demand for the services of a well-trained mortgage loan professional is high, but to achieve success takes not only dedication and hard work but also a commitment to continuoustraining and education. As soon as a mortgage loan representativelearns everything about 20 types of loan packages, then 30 totallynew kinds of loan programs hit the marketplace. The ability toadapt to change and the personality to thrive on the opportunityto learn something new every day often make the differencebetween success and failure.

In short, the mortgage brokerage business is fiercely competitivebut offers an individual with a strong work ethic an opportunity tomake a high income. This textbook describes in detail the workingsof the mortgage loan business and gives you the preview you needto help you decide if this business is for you. If you are already in

3

Th

om

son

Lea

rnin

gT

M

the mortgage business, this book will give you ideas to make youmore successful.

At the end of this chapter you will be able to:

1. Understand the structure of the book.

2. Describe the history of real estate lending in the UnitedStates.

3. Explain some current and future trends in real estate lending.

4. Learn about career opportunities in the mortgage loan brokerage field.

5. Differentiate between a mortgage broker and a mortgagebanker.

1.1 Overview of the Book

The book is divided into five parts: scope of the business, loans,processing, the secondary money market, and regulations andoperations. Figure 1.1 gives an overview of the book.

The first part of the book is Chapter 1, which covers the historicbackground that has led to the present-day operations of the mort-gage loan business, and Chapter 2, with information on career oppor-tunities. Originating loans and developing business contacts are alsodiscussed. Developing sources for your loan business means learningtechniques and methods that separate you from your competition andcreating a marketing strategy that complies with all regulations.

Part 2 is three chapters that review real estate loan information.Chapter 3 explains the types and characteristics of the various con-ventional loans, as well as loan features and mortgage insurance.Chapter 4 discusses government and other nonconventional loans. Thebasic details of the Federal Housing Administration (FHA), theDepartment of Veterans Affairs (DVA), and the California Veterans(Cal Vet) loan programs are covered from the point of view of the mort-gage loan broker. Because not all loans in the mortgage loan businessinvolve institutional or government loans, this chapter also discussesjunior liens, refinance and equity loans, Title I loans, and subprimeloans. The last chapter in this section, Chapter 5 discusses loan dis-closures and compliance.

Part 1 Scope of the Business4

Th

om

son

Lea

rnin

gT

M

5Chapter 1 Scope of Mortgage Loan Brokerage

Borrower

Loan OriginationCh 2

Pre-QualCh 6

CreditCh 7

Types of loansChs 3, 4, 5

ProcessingChs 6, 7, 8

UnderwritingCh 9

AppraisalCh 8

FundingCh 10

Escrow titleCh 8

ShippingCh 11

Recording

Investor

ServicingRetained

Ch 12

ServicingAgentCh 12

Chapters 13, 14, 15—Licensing, Finance Mathematics, and Trust Funds

The third part covers the bulk of the loan business, called processing.Once the loan has been originated or obtained, detailed steps arerequired to consummate the transaction. Chapter 6 explains the first stepin processing the loan application, often referred to as prequalification,or prequal. From the application, the mortgage loan broker can run ratiosto begin matching the borrower to the various types of loans that werediscussed in the previous chapters. A prospective borrower usually qual-ifies for more than one type of loan, so the mortgage loan broker dis-cusses the options available with the applicant. The next chapter aboutprocessing, Chapter 7, covers the credit report and compliance with bothcredit laws and fair lending practices. Chapter 8 reviews preparing andhandling verifications. Processing includes the stacking order as requiredby the lender. Chapter 9 is on processing the property. It covers theappraisal, title reports, and escrow, or settlement. Chapter 10 discussesunderwriting and quality control. The last chapter of this part, Chap-ter 11, completes the outline of the loan-processing portion of the mort-gage loan brokerage business with the loan documents, called loan docs,and then goes on to funding and closing the loan.

Figure 1.1 Overview ofthe book.

Th

om

son

Lea

rnin

gT

M

Part 4 is about investment money markets and covers topics aboutthe secondary money market and securities. Chapter 12 explainsshipping and servicing the loan. The loan may be kept in the originat-ing lender’s own portfolio or packaged and sold to other investors. Ineither case, calculating yields, discounting notes, and properly trans-ferring documents used to secure loans on real property are reviewed.

The last section of the text, Part 5, is about the various regulationsand operations of the business. Chapter 13 discusses broker supervi-sion, agency law, and licensing by the California Department of RealEstate (DRE) for Brokers and Salespersons; and loan brokers licensedunder the Corporation Commissioner for brokers handling ConsumerFinance Lender (CFL) loans. Chapter 14 covers the topic that giveslicensees the most trouble with the state licensing agencies—handlingclient trust funds, including threshold reporting, compensation, andsimilar record-keeping elements. Chapter 15 is devoted to real estatefinance mathematics.

1.2 Historic Perspective

In the BeginningMany of the current lending practices are based on the founda-

tions carried forward from the Roman times to the European govern-ments, as shown in Figure 1.2. These standards of practice werebrought to the English colonies by the early settlers and then includedin the laws of the newly formed government of the United States.There were virtually no institutional or government loans available forresidential properties during these early years. Home loans primarilycame from friends or family members.

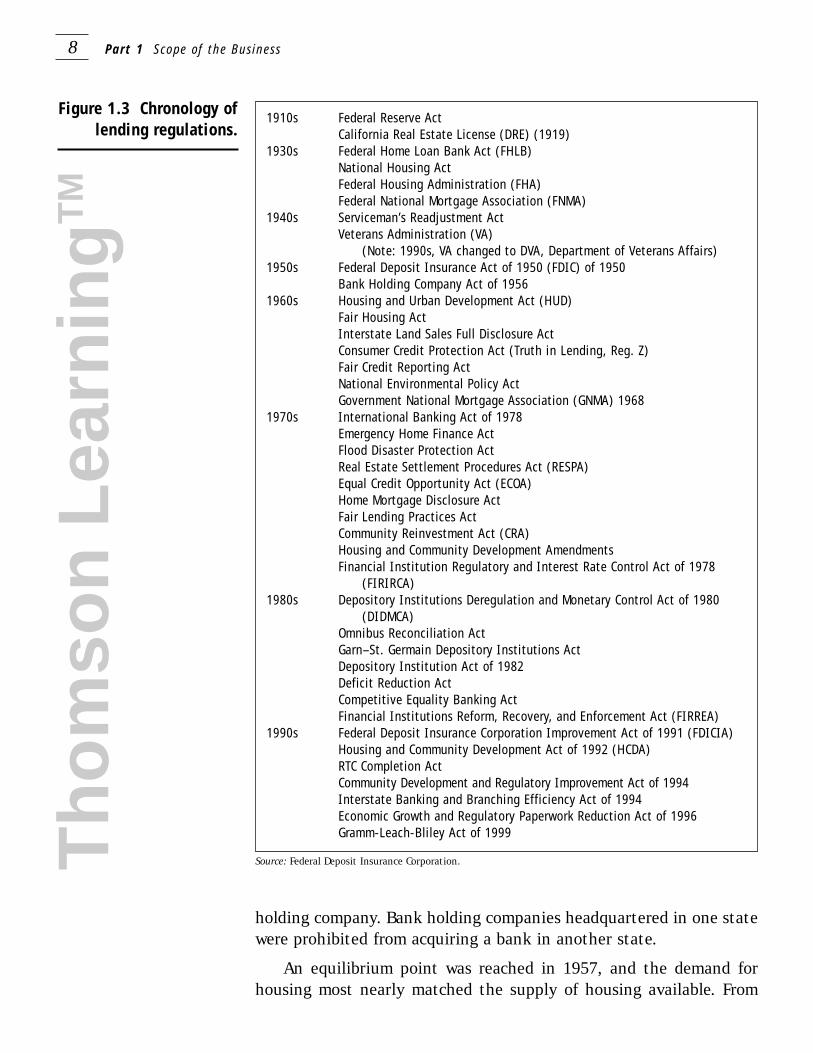

Early ProgressFigure 1.3 shows the progression of major legislation affecting real

estate lending. The Federal Reserve Act became law in 1913. It made realestate loans available through federally chartered commercial banks.California enacted legislation in 1919 to become the first state to licensepeople who practice real estate professions. Other states followed, andtoday nearly all states require most real estate transactions to be per-formed by a licensed real estate agent, including the work of the mort-gage loan broker. Most states exempt owners from transactions directly

Part 1 Scope of the Business6

Th

om

son

Lea

rnin

gT

M

7Chapter 1 Scope of Mortgage Loan Brokerage

Figure 1.2 History of finance.

Development of Financial InstitutionsPre-1600s 1863

Hidemoney

in homeDeposit into

king’s treasury Deposit withblacksmith,

bullion dealers Moneyholdersinvested funds Checks in

volume America importsEnglishsystem

U.S.Bank Actpassed

on their own property, such as renting or selling their own homes. Alsooften exempt are those working directly for a federal banking operation.

The early 1920s were times when real estate values increased by asmuch as 50% until the collapse of the optimistic real estate market in1927. The stock market crash soon followed the real estate marketcrash. Congress enacted many new laws during the 1930s that weredesigned to prevent a similar future market crash.

The Federal Home Loan Bank (FHLB) Act established a boardand 12 regional banks to provide a central credit clearinghouse forhome finance institutions. The National Housing Act created the Fed-eral Housing Administration (FHA) in 1934. The Federal NationalMortgage Association (FNMA) was authorized to provide a second-ary money market for FHA loans, which provided liquidity for realestate loan investments.

1940 to 1979Toward the end of World War II, in the mid-1940s, the Serviceman’s

Readjustment Act created the Department of Veterans Administration(DVA, formerly referred to as VA), a home loan program. The periodfrom 1945 to 1965 had only a few major real estate or lending lawspertaining to private-sector economic growth. The FDIC Act of 1950revised and consolidated earlier legislation; the Bank Holding Com-pany Act of 1956 required FDIC approval for establishment of a bank

Th

om

son

Lea

rnin

gT

M

Th

om

son

Lea

rnin

gT

MPart 1 Scope of the Business8

Figure 1.3 Chronology oflending regulations.

1910s Federal Reserve ActCalifornia Real Estate License (DRE) (1919)

1930s Federal Home Loan Bank Act (FHLB)National Housing ActFederal Housing Administration (FHA)Federal National Mortgage Association (FNMA)

1940s Serviceman’s Readjustment ActVeterans Administration (VA)

(Note: 1990s, VA changed to DVA, Department of Veterans Affairs)1950s Federal Deposit Insurance Act of 1950 (FDIC) of 1950

Bank Holding Company Act of 19561960s Housing and Urban Development Act (HUD)

Fair Housing ActInterstate Land Sales Full Disclosure ActConsumer Credit Protection Act (Truth in Lending, Reg. Z)Fair Credit Reporting ActNational Environmental Policy ActGovernment National Mortgage Association (GNMA) 1968

1970s International Banking Act of 1978Emergency Home Finance ActFlood Disaster Protection ActReal Estate Settlement Procedures Act (RESPA)Equal Credit Opportunity Act (ECOA)Home Mortgage Disclosure ActFair Lending Practices ActCommunity Reinvestment Act (CRA)Housing and Community Development AmendmentsFinancial Institution Regulatory and Interest Rate Control Act of 1978

(FIRIRCA)1980s Depository Institutions Deregulation and Monetary Control Act of 1980

(DIDMCA)Omnibus Reconciliation ActGarn–St. Germain Depository Institutions ActDepository Institution Act of 1982Deficit Reduction ActCompetitive Equality Banking ActFinancial Institutions Reform, Recovery, and Enforcement Act (FIRREA)

1990s Federal Deposit Insurance Corporation Improvement Act of 1991 (FDICIA)Housing and Community Development Act of 1992 (HCDA)RTC Completion ActCommunity Development and Regulatory Improvement Act of 1994 Interstate Banking and Branching Efficiency Act of 1994 Economic Growth and Regulatory Paperwork Reduction Act of 1996Gramm-Leach-Bliley Act of 1999

holding company. Bank holding companies headquartered in one statewere prohibited from acquiring a bank in another state.

An equilibrium point was reached in 1957, and the demand forhousing most nearly matched the supply of housing available. From

Source: Federal Deposit Insurance Corporation.

the mid-1960s forward, however, many changes occurred. The Housingand Urban Development Act in 1965 created the Housing and UrbanDevelopment (HUD) to consolidate many federal programs. Before1970, the Fair Housing Act, the Interstate Land Sales Full DisclosureAct, the Consumer Credit Protection Act (Truth in Lending [TIL], Reg.Z), the Fair Credit Reporting Act, and the National Environmental Pol-icy Act were all put into place while national interests were directedtoward protecting consumers. During this time, the HUD Act of 1968moved FNMA from government to private authority and created theGovernment National Mortgage Association (GNMA).

In 1978, two important federal acts became law. The InternationalBanking Act brought foreign banks within the federal regulatoryframework and required deposit insurance for branches of foreignbanks engaged in U.S. retail banking. The Financial Institution Regu-latory and Interest Rate Control Act created major statutory provisionsregarding electronic fund transfers and established limits and report-ing requirements for banks.

1980 to 2000Increasing home prices sustained the real estate market for the

next 25 years. Even though prices dipped in the early 1970s, 1980s,and early 1990s, the overall growth rate equated to about 4% per yearuntil 1990. These increasing values created a demand for real estateloans.

The Emergency Home Finance Act provided secondary loan supportfor funding by thrift institutions and enabled FNMA to purchase con-ventional loans, rather than only VA or FHA loans. The Flood DisasterProtection Act required flood insurance for loans in flood hazard areas.The Real Estate Settlement Procedures Act (RESPA), the EqualCredit Opportunity Act (ECOA), the Home Mortgage Disclosure Act,the Fair Lending Practices Act, the Community Reinvestment Act, andthe Housing and Community Development Amendments also receivedCongressional approval.

In 1980, Congress passed the Depository Institutions Deregulationand Monetary Control Act (DIDMCA), which changed many real estatepractices. It extended federal overrides of state usury ceilings, simpli-fied truth in lending, eased geographical lending restrictions, and cre-ated jumbo loans. This act granted new powers to thrift institutionsand raised the deposit insurance ceiling to $100,000.

The Omnibus Reconciliation Act limited housing revenue bondtax exemptions. The Garn–St. Germain Depository Institutions Act

9Chapter 1 Scope of Mortgage Loan Brokerage

Th

om

son

Lea

rnin

gT

M

phased out interest rate differentials and preempted state due-on-salerestrictions by lenders. The Deficit Reduction Act changed loan inter-est reporting procedures and extended the tax exemption for certainloan bonds. The Competitive Equality Banking Act kept savings banklife insurance and gave flexibility to thrifts.

The 1980s ended with a crash in the real estate market thatexceeded the late-1920s disaster. Consequently, most loans above 80%of value require some form of mortgage insurance in the event of loandefault, such as private mortgage insurance (PMI).

The most important new law at that time was the Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA),which created the Office of Thrift Supervision (OTS) under the Trea-sury Department and the Federal Housing Finance Board (FHFB), whileabolishing the Federal Home Loan Bank Board (FHLBB). The act alsoformed the Resolution Trust Corporation (RTC), a temporary agencyto liquidate defaulting assets of member banks. The Savings Associa-tion Insurance Fund (SAIF) was created to replace FSLIC; the BankInsurance Fund (BIF) was created to cover banks.

In 1991, the Federal Deposit Insurance Corporation ImprovementAct (FDICIA) recapitalized BIF and strengthened the FDIC fund by bor-rowing from the Treasury. The act established new capital require-ments for banks and created new truth-in-savings provisions. In thefollowing year, the Housing and Community Development Act waspassed to regulate the structure for government-sponsored enterprises(GSEs) to combat money laundering.

In 1994, the Community Development and Regulatory Improve-ment (CDRI) Act, containing more than 50 provisions to reduce paper-work requirements, was passed. This act established the wholly ownedgovernment corporation that provides financial and technical assis-tance to community development financial institutions. The InterstateBanking and Branching Efficiency Act permitted bank holding compa-nies to acquire banks in other states, thus allowing mergers.

This era ended with the Gramm-Leach-Bliley Act of 1999 thatrepealed the last provisions of the Glass Steagall Act of 1933 andallows affiliation between banks and insurance underwriters. The lawcreates new financial holding company legislation authorizing engage-ment in commercial and merchant banking, investment in and devel-opment of real estate, and other complementary activities. Allfinancial institutions had to provide customers the opportunity to not

Part 1 Scope of the Business10

Th

om

son

Lea

rnin

gT

M

share nonpublic information with unaffiliated third parties as ofJuly 1, 2001.

Unstable MarketThe real estate market often appears to be a bouncing ball. No one

seems to be able to control the height that the ball will bounce, orwhen it will come to a stop. The real estate financial markets are oftencompared with the stock market—uncontrollable, unpredictable, andvolatile. Changes create opportunities and new programs for the mort-gage loan broker.

The transition period from the late 1980s through the 1990sreflected the reaction to the vast regulatory changes. As the variousacts were implemented, the industry kept adjusting its strategies onhow to comply yet stay competitive. Along the way, many loan repre-sentatives and firms ceased operations. Also, new firms emerged withtechnology aids to handle understaffed peak demands and formerlyoverstaffed slower periods. The economic changes can be seen in Fig-ure 1.4, where, in a one-year period from January 1990 to January1991, the difference between the peak of 1.63 million and the valleyof 850,000 is an astounding difference of 780,000 housing starts. Thisdifference represents huge changes in the number of loans generatedand the number of staff positions in the industry.

11Chapter 1 Scope of Mortgage Loan Brokerage

Figure 1.4Housing starts. Annual rate, in millions of dwelling units

1.81.71.61.51.41.31.21.11.00.90.8

Source: U.S. Commerce Department

1989 1990 1991 1992

Th

om

son

Lea

rnin

gT

M

TodayAs the real estate industry progresses into the twenty-first cen-

tury, lenders have become more competitive and specialized as a resultof several factors: the real estate recession of the early 1990s, tech-nology, and the market dominance of minority purchasers. Somelenders specialize in commercial shopping centers, and others seekonly less creditworthy borrowers, referred to as subprime lenders. Asthe government has tried to increase home ownership, new programshave emerged for the first-time homebuyer. These changes have led toloan professionals merging into firms with individuals who specializein a particular type of loan. Firms often employ multilingual loanagents to aid multicultural homebuyers.

Technology has also changed the way business is handled. Theloan agent can now sit at a “for sale” open house with a real estatesales agent and take the loan application on a portable laptop com-puter, calculate the loan qualification ratios, and run a credit report—all without being at “the office.”

The mortgage loan brokerage field now combines many aspects ofthe people-oriented real estate professional with the technical bank-ing aspects to offer many career opportunities. As long as people needto borrow funds, loan arrangers will be in demand.

1.3 Basic Information

Hard Money versus Seller Carry MoneyHard money loans are any institutional or noninstitutional loans for

which the lenders placed their cash funds on the table in a transaction.The lenders’ funds may be from their depositors, from the sale of theirassets, or from funds borrowed against their assets. Private individuals,corporations, and investors may have a mortgage broker place their fundson a hard money, real estate–backed loan. The funds actually changedhands, and upon default, the lenders could lose some or all of their cash,even if the property held as collateral was sold to try to retire the debt.

Because of the higher risk involved for certain types of loans, somehard money lenders rely more heavily on the equity in the propertythan on the borrower, but typical residential loan investors rely on theborrower. To offset the higher risk and illiquidity of real estate loans,hard money investors may demand a higher than normal yield over the

Part 1 Scope of the Business12

Th

om

son

Lea

rnin

gT

M

rate they could receive in a “safe” and secured bank savings account.However, all loans tend to revert back to the normal yield for the spe-cific type of loan, called market yield. This is the amount typicalinvestors would pay in the market for the particular type of loan. Thecourts view these hard money lenders as investors who gave up cashon the good faith expectation that the borrower would repay all funds.

Seller carryback loans (soft money loans) are typically anextension of credit from a seller to a buyer. No funds are taken out ofa bank account, and no assets are sold to raise any capital to makethe loan to the buyer. The loan amount may have been originated onthe note for reasons other than banking or investor criteria. Oftenthese loans are made without the basic requirements that an institu-tional lender would expect, such as a credit application, credit report,or property appraisal.

Some seller carryback loans may be generated to cover costs thatthe seller is initially paying for the buyer, such as an amount to buydown an interest rate, points, or loan fees. These loans often have fea-tures such as more favorable terms. Seller carryback loans may, buttypically do not have loan fees, loan origination points, prepaymentpenalties, and similar provisions. Mortgage insurance on the loan andsimilar items, if handled by a hard money lender, would often result inthe buyers being unable to qualify for or obtain a loan.

After the close of escrow, seller carryback loans may be sold at adiscount to a third party, who becomes the new lender beneficiary. Thepurchaser of the loan is usually a private individual termed the holderin due course. In a foreclosure procedure, should the sale proceedsfall short of covering all the loan amounts owed, the judicial systemusually views hard money and seller carryback lenders differently.

Careers in Mortgage Loan BrokerageThe various persons or entities who are involved in the real estate

lending business at different stages of the loan process can be confus-ing to the novice. Some individuals are licensed, and others are notrequired to have any state regulatory license. Most direct employeesare not licensed and have very specific job duties and assignments,according to a company policies and procedures manual.

A marketing department may have telemarketers, computer-generated form solicitation, advertising personnel, and key network-ing personnel. A loan processor may verify loan application informa-tion according to prescribed steps. This person or a loan assistant may

13Chapter 1 Scope of Mortgage Loan Brokerage

Th

om

son

Lea

rnin

gT

M

prepare computer-generated disclosure forms and credit reports andwork with title company records. The mortgage loan broker file mustcontain certified copies of escrow instructions obtained from theescrow officer. The appraisal report must be ordered. Buyers’ insuranceinformation must be received.

An individual working in this field may be licensed by one or moregovernment-regulated agencies, such as a licensed real estate sales-person working under the supervision of a licensed real estate broker.The individual may, instead, be an employee of a financial institution,such as a loan officer working for a savings and loan. The institutionis regulated by another form of government agency, such as the bankexaminers.

Loan OriginatorsThe loan originators solicit others to obtain applications for loans.

The percentage of market share shown in Figure 1.5 shows the annualdollar volume of residential loan applications by the type of lender.From 1980 to 1995, mortgage bankers and brokers dominated the sin-gle-family conventional market with 35% to nearly 60% of marketshare. Although thrift institutions reached almost 40% in the mid-1980s, their market share declined to only about 15% by the mid-1990s. Commercial banks hold a relative steady market share at about20%, while savings institutions have decreased from about 40% toabout 20% in the 1990s. Independent mortgage companies have grownfrom about 10% to almost 30%, and subsidiary mortgage companieshave grown from less than 20% to about one-third of the market.

Loan originators in California usually hold a Department of RealEstate (DRE) real estate salesperson license. They create a loan in thenormal course of their real estate activity and perform loan duties undera DRE licensed broker. Some employees work in an office under an indi-vidual licensed under the corporation commissioner, as described inChapter 14, and the employee may not need to be licensed.

Loan originations predominantly fall into several groups: (1) themortgage broker, (2) the mortgage banker, and (3) commercial banksor savings and loan institutions (see Figure 1.6).

A mortgage banker acts much like a bank and receives revenuefrom the loan origination. Mortgage bankers may lend their ownfunds. They may also act as local, regional, or national representativesfor an institutional lender. Thus, mortgage bankers may retain a loanin their own portfolio, or they may transfer ownership of the loan to

Part 1 Scope of the Business14

Th

om

son

Lea

rnin

gT

M

15Chapter 1 Scope of Mortgage Loan Brokerage

Figure 1.5 Mortgageorigination activity

by lender type. Savings Commercial Mortgage Co. Independent Credit TotalInstitution Bank Subsidiary Mortgage Co. Union Volume

Market Market Market Market Market ($ Billions)Share Share Share Share Share

1999 21% 21% 29% 26% 3% 9621998 23% 17% 30% 27% 2% 1,1651997 25% 19% 26% 27% 3% 6321996 25% 21% 25% 26% 3% 5581995 25% 22% 25% 26% 2% 4471994 26% 22% 19% 31% 2% 5361993 22% 20% 19% 37% 2% 8341992 40% 24% 19% 25% 2% 6101991 33% 26% 17% 22% 2% 3411990 41% 27% 18% 11% 3% 268

Lender Share of Single-Family Conventional Originations

Market share figures are based on annual dollar volume of residential loan originationreported under the Home Mortgage Disclosure Act (HMDA).

Savings institutions and commercial banks refer to federally regulated, deposit-takinginstitutions, or their service corporations, with assets exceeding an inflation-indexed,minimum threshold, which changes annually. The asset-level cutoff is set by the FederalReserve Board based on changes in the consumer price index (CPI). The threshold was $28 million in 1997, $29 million in 1998 and 1999, $30 million in 2000, and $31 million for 2001.

Credit union refers to a federally regulated, deposit-taking institution that meets theasset and lending threshold tests for covered savings institutions and banks.

Mortgage company subsidiary refers to the mortgage-origination arm of the holding company for an HMDA-covered savings institution or bank when the parent companyowns a minimum 50% interest in the subsidiary.

Independent mortgage company refers to a nondepository lender that (a) had assets,including those of parent corporation, exceeding $10 million (unadjusted for inflation)on the preceding Dec. 31 or (b) originated at least 100 home-purchase or refinancingloans in the preceding calendar year. (Before 1993, a small independent mortgage com-pany with assets of $10 million or less was exempt from reporting to HMDA, even if ithad originated 100 or more loans in the preceding year.)

another entity. They may also sell the loan on the secondary moneymarket to investors or to another lender. If they sell the loan, in suchcase they generate funds to make more loans. The mortgage bankermay retain the servicing on the loan, in which case the borrower oftendoes not notice any difference and the mortgage banker continues toreceive ongoing revenue from loan-servicing fees.

Source: MBA.Th

om

son

Lea

rnin

gT

M

Part 1 Scope of the Business16

Figure 1.6 Originators.

DRE BrokerLOAN

ORIGINATIONLoan

Processing

MORTGAGE BROKER: Third-Party Arranger

Package sent for Lender Approval

and Funding

DRE BrokerLOAN

ORIGINATIONLoan

Processing

MORTGAGE BANKER: Third Party or Primary

LOAN APPROVAl(Their Own Lender,

MI Investor)

Sources of Funds• Bank• Their Own Funds• Investor (FNMA, Corp) SERVICING

InsuringWarehouse

Line

ClosingFunding

Depositors (Interest income)

LOAN ORIGINATION

BANK OR SAVINGS & LOAN: Primary Lender

LoanApproval

SERVICINGDept.

ClosingFundingDept.

BankIncome

Mortgage loan brokers generally do not lend any of their own funds.The mortgage broker connects a lender and a borrower for which a feeis received. Many borrowers do not know that mortgage brokers oftenget wholesale rates that the borrower could not get directly from thesame lender. A discussion of wholesale versus retail loans is found inChapter 13. Many lenders cannot find adequate numbers of borrowers ata particular time and welcome the mortgage broker for placing idlefunds. A mortgage broker does not retain the loan-servicing work.

Th

om

son

Lea

rnin

gT

M

1.4 Licenses and Professional Organizations

Legal and Licensing RequirementsBecause the loan business is involved with large amounts of

money, many regulations intended to protect the general public gov-ern its activities. The California mortgage loan broker is regulated bythe California Department of Real Estate (DRE), which covers both thebroker and the salesperson licenses. The mortgage company and mort-gage banker may be licensed under the Corporation Commissioner as aconsumer finance lender (CFL) or may be an agent for a Californiainstitutional lender and fall under the banking regulations of the par-ent company. Both federal and state institutional lenders are heavilyregulated, and their direct employees may handle loans although theindividual is not required to hold a government agency license. Licenserequirements are covered in greater detail in Chapter 14.

Professional OrganizationsReal estate mortgage loan specialists have formed various local,

state, and national trade associations. These associations go farbeyond the mere social needs of its members to provide service in theareas of community outreach, educational courses, and promotion oflegislative interests affecting the business and political needs of theindustry. These organizations also establish codes of ethics to guidetheir members and protect the public.

For more information on activities in the mortgage loan business,you may wish to contact:

• California Association of Mortgage Brokers1730 “I” Street, Suite 240Sacramento, CA 95814-3017(916) 448-8236, (916) 443-8065http://www.cambweb.org

• National Association of Mortgage Brokers8201 Greensboro Drive, Suite 300McLean, VA 22102Phone: (703) 610-9009; Fax: (703) 610-9005http://www.namb.org

17Chapter 1 Scope of Mortgage Loan Brokerage

Th

om

son

Lea

rnin

gT

M

• National Association of Professional Mortgage WomenP.O. Box 2016Edmonds, WA 98020-9516(800) 827-3034, fax (425) 771-9588http://www.napmw.org

• Mortgage Bankers Association of America1919 Pennsylvania Avenue, NWWashington, DC, 20006(202) 557-2700http://www.mbaa.org

SUMMARY

Lending practices go back as far as Roman times. Early U.S. loanactivity was founded on traditions brought from Europe. The pioneerdays had little activity in home mortgages prior to the 1920s. Today,the loan business is heavily regulated by many different state andfederal laws.

The lending industry views hard money as the primary market. Private lender credit extension activity is viewed as the seller carryback market.

A loan arranger may be an individual agent, a principal, or a financial lending company. The originator is a third party to a realestate transaction who is usually a broker. A common originator isthe mortgage loan broker, who brings together a borrower and alender for a fee. The mortgage loan banker may also be an originator,with its own loan funds or those of another. An originator may beable to locate funds from many sources, thus giving the buyer a better choice of various loan options. A mortgage loan banker maybe able to make a loan on a property that is kept in the bank’s ownportfolio and not sold on the secondary money market, whereas themortgage broker could not make the loan because it would not conform to the requirements of the secondary money market.

IMPORTANT TERMS

Part 1 Scope of the Business18

Th

om

son

Lea

rnin

gT

M

Broker

Department of Real Estate (DRE)

Department of VeteransAffairs (DVA)

Federal Home LoanBank (FHLB)

Federal Housing Administra-tion (FHA)

REVIEWING YOUR UNDERSTANDING

1. Which act made real estate loans available through federallychartered commercial banks?a. Federal Home Loan Bank Actb. National Housing Actc. Federal Reserve Actd. Fair Housing Act

2. Which act limited Housing Revenue Bond Tax Exemptions?a. The Omnibus Reconciliation Actb. Financial Institutions Reform, Recovery, and Enforcement Act

(FIRREA)c. Home Mortgage Disclosure Actd. Community Reinvestment Act

3. Which act created jumbo loans?a. Fair Housing Actb. Interstate Land Sales Full Disclosure Actc. Housing and Urban Development Actd. Depository Institutions Deregulation and Monetary Control Act

4. Which act was passed prior to 1930?a. Federal Reserve Actb. Veterans Administration Act

19Chapter 1 Scope of Mortgage Loan Brokerage

Th

om

son

Lea

rnin

gT

MFederal National Mortgage

Association (FNMA)

Financial InstitutionsReform, Recovery, andEnforcement Act (FIRREA)

Government National Mort-gage Association (GNMA)

Hard money loans

Holder in due course

Home Mortgage Disclosure Act (HMDA)

Housing and Urban Develop-ment (HUD)

Mortgage insurance (MI)

Omnibus Reconciliation Act

Office of Thrift Supervision (OTS)

Originator

Private Mortgage Insurance(PMI)

Real Estate SettlementProcedures Act (RESPA)

Resolution Trust Corporation (RTC)

Savings Association Insur-ance Fund (SAIF)

Seller carryback loans (soft money)

Subprime lenders

c. Fair Credit Reporting Actd. Deficit Reduction Act

5. FIRREA createda. OTS and RTC.b. SAIF.c. both A and B.d. neither A nor B.

6. The mortgage loan brokerage field is regulated bya. a number of government agencies.b. only VA.c. only DRE.d. both FNMA and GNMA.

7. Little legislation affected real estate prior to thea. 1920s.b. 1940s.c. 1960s.d. 1980s.

8. The Serviceman’s Readjustment Act in the 1940s createda. an insurance program. b. an association for retired vets. c. the VA home loan program.d. a loan insurance act.

9. The largest group of single-family conventional originations aremade bya. commercial banks.b. mortgage bankers.c. savings and loan institutions.d. noninstitutional lenders.

10. Loan originators predominantly fall into which two groups?a. mortgage banker or mortgage brokerb. mortgage banker or savings and loanc. mortgage broker or bankd. bank or savings and loan

11. A position in mortgage loan brokerage could bea. escrow officer or loan officer.b. appraiser or review appraiser.c. processor or mortgage loan banker.d. title officer or instrument recorder.

Part 1 Scope of the Business20

Th

om

son

Lea

rnin

gT

M

12. The difference between what the mortgage broker does and whatthe banker does isa. origination.b. servicing.c. appraisal.d. credit.

13. The mortgage loan industry keeps adjusting strategies toa. stay competitive.b. handle understaffed peak demand periods.c. smooth out overstaffed non-peak periods.d. all of the above are true.

14. What brought liquidity to the real estate industry?a. PMI as a disaster protectionb. ECOA as a consumer disclosurec. CRA as a deregulation actd. FNMA as a secondary market source

15. The difference between peak and valley housing starts in theearly 1990s, which would generate new loans, would most nearly be which of the following?a. 250,000b. 500,000c. 750,000d. 1,000,000

16. The single-family conventional market has been dominated bya. banks.b. mortgage brokers.c. seller carryback loans.d. equity loans.

17. FIRREAa. created OTS under the Treasury Department.b. created RTC and SAIF.c. both A and B.d. neither A nor B.

18. An individual may be licensed bya. a financial institution.b. a government agency.c. a beneficiary or mortgagee.d. the holder in due course.

21Chapter 1 Scope of Mortgage Loan Brokerage

Th

om

son

Lea

rnin

gT

M

19. Lenders’ funds could come froma. their own savings.b. the sale of their assets.c. funds borrowed against their assets.d. all of the above are true.

20. The mortgage loan brokera. does not lend any of its own funds.b. lends only FHA or DVA funds.c. lends only savings and loan funds.d. lends only FNMA or GNMA funds.

21. The mortgage broker connects a lender and a borrower anda. is paid by the seller of the propertyb. is paid by the secondary money marketc. a fee is receivedd. receives a kickback from the appraiser

22. The primary reason for affiliation with a professional organization is to aid members ina. fulfilling social needsb. keep common-interest groups togetherc. meet educational, legislative, and political goalsd. make the public aware of the individual’s level of

education

23. What does the lending industry view as the primary market?a. hard moneyb. seller carrybackc. insured loansd. guaranteed loans

24. Real estate loans given as all or part of the purchase price are calleda. purchase money loansb. hard money loansc. servicing agreementsd. secondary money market transactions

25. The extension of credit loan typically does not have which?a. loan feesb. loan origination pointsc. prepayment penaltiesd. all of the above.

Part 1 Scope of the Business22

Th

om

son

Lea

rnin

gT

M

Th

om

son

Lea

rnin

gT

M23

Answers to Reviewing Your Understanding

1. C

2. A

3. D

4. A

5. C

6. A

7. A

8. C

9. B

10. A

11. C

12. B

13. D

14. D

15. C

16. B

17. D

18. B

19. D

20. A

21. C

22. C

23. A

24. B

25. D

Chapter 1 Scope of Mortgage Loan Brokerage

Th

om

son

Lea

rnin

gT

M