Embed Size (px)

Citation preview

www.asb.unsw.edu.au

Last updated: 25/07/14 CRICOS Code: 00098G

School of Accounting Seminar Series Semester 2, 2014

Are Auditor Opinions on Internal Control

Effectiveness Influenced by Corporate

Social Responsibility?

Encarna Guillamón‐Saorín Universidad Carlos III de Madrid

Date: Friday 1st August 2014

Time: 3.00pm – 4.30pm

Venue: ASB 220

Australian School of Business

Accounting

Are Auditor Opinions on Internal Control Effectiveness Influenced by

Corporate Social Responsibility?

Andrés Guiral*

Yonsei University

Encarna Guillamón-Saorín

Universidad Carlos III de Madrid

Belen Blanco

The University of Melbourne

*Corresponding author: Andrés Guiral, Yonsei University School of Business, 50 Yonsei-ro, Seodaemun-gu,

Seoul 120-749, Tel.: +(82)2-2123-5452, Email: [email protected] We acknowledge useful comments from Aldonio Ferreira, Carlos Larrinaga, Doocheol Moon, Karla

Johnstone, Maria Jose Montes, Emiliano Ruiz, Greg Shailer, Jordi Surroca, Mark Wilson, and seminar

participants at Australian National University, Monash University, Grenoble Ecole de Management,

Wroclaw University of Economics and Universidad de Burgos.

Andrés Guiral acknowledges financial contribution from the National Research Foundation of Korea Grant

funded by the Korean Government (NRF-2012-S1A3A2-2012S1A3A2033412) and the Spanish Ministry of

Innovation and Science (research projects SEJ2004-00791ECON, SEJ2007-62215/ECON/FEDER, SEJ

2006-14021, ECO2010-17463 ECON-FEDER). Encarna Guillamón-Saorín acknowledges financial

contribution from the Spanish Ministry of Science and Innovation (SEJ2007-67582-C02-02/ECON,

ECO2010-19314) and Comunidad Autonoma de Madrid (SEJ2008-00059-003). Belen Blanco acknowledges

financial assistance from the Spanish Ministry of Innovation and Science (ECO2010-19314, ECO2008-

06238- C02-01/ECON, SEJ2007-67582-C02-02/ECON, ECO2009-10796 and Consolider Grant

#2006/04046/002).

1

Are Auditor Opinions on Internal Control Effectiveness Influenced by Corporate Social

Responsibility?

Abstract

We investigate the relation between corporate social responsibility and auditors’ perception of internal

control quality under the Sarbanes Oxley Act, 404 Section. Previous studies find that the management or the

quality of the board of directors is associated with the strength of internal controls. We contribute to the

existing literature by identifying that the mechanisms used by managers to improve the perception of internal

control effectiveness are related to internally-oriented social responsible engagement and, in particular, to the

enhancement of employee issues. We observe that corporate social responsibility strengths lead to an

improvement of the auditors’ perception of internal control effectiveness while corporate social concerns do

not seem to diminish effectiveness’ perception. We also examine the nature of the weaknesses which leads to

adverse auditor opinions and note that while the presence of company-level weaknesses is negatively

associated with corporate social responsibility, the presence of account-level weaknesses is not. Moreover,

we find that both the quality of information reported and corporate governance affect the relation between

corporate social responsibility and internal control effectiveness’ perception. Our results hold for alternative

proxies of internal controls and after controlling for potential endogeneity issues.

Keywords: Internal control, material weaknesses, CSR, earnings quality

1. Introduction

This study examines the relation between Corporate Social Responsibility (CSR) and the auditor’s

opinion on internal control (IC) effectiveness. Specifically, we question whether firms that exhibit

stronger CSR as established by KLD (KLD 2006) are perceived as having better quality IC and

therefore are less likely to receive an adverse auditor opinion on IC effectiveness made under

Section 404 of the Sarbanes-Oxley Act of 2002 (SOX 2002). We assess this association using data

on IC effectiveness from the provision of the Sarbanes-Oxley Act Section 404 which requires

registrants to document and test IC and their external auditors to independently assess those

controls and offer a separate opinion on IC effectiveness.

The recent collapse of large financial institutions leading to the financial crisis has made

the need of an improvement of information transparency evident (IFAC 2012). Various financial

crises in recent years have demonstrated that in many companies IC practices were deficient or

ineffective mainly because business leaders did not fully understand the risks to which they were

exposed (IFAC 2012)1.

One of the numerous criticisms related to Enron scandals and its accounting and reporting

practices was the responsibility for a weak IC2 (Verschoor 2002). The SOX (2002) introduced in

the U.S. important regulations to improve corporate governance, auditor independence and

financial reporting quality to restore investor’s confidence in reported information.

1 Revealed by the IFAC´s Global Survey on Risk Management and IC (2011) carried out on more than 60

respondents from around the globe and on all types of organizations. 2 Monitoring IC is the result of actions by, and interactions between management, the internal auditor (if

present), the external auditor, and the audit committee.

2

IC effectiveness represents the policies, processes, and procedures intended to ensure

financial statements reliability (Skaifer, Veenman, and Wangerinn 2013). This broad view of IC

effectiveness makes it difficult to observe or assess and the intention of the SOX regulation was to

resolve this through the reporting requirement. Managers reports and auditors opinion in relation to

corporate IC effectiveness should reduce uncertainty and benefit the company (McMullen,

Raghumandan, and Rama 1996; Hammersley, Myers, and Shakespeare 2008). There are two

sections 302 and 404 of the SOX related to IC and which intention has been to enhance investors

understanding of the quality of the firm’s financial reporting3.

We focus on Section 404 passed by the SEC in 2004 which requires that management

publicly state their responsibility for establishing and maintaining adequate controls over financial

reporting as well as an assessment of their effectiveness at the end of the most recent fiscal year.

External auditors, as required by Auditing Standard Number 2 (AS2) issued by the U.S. PCAOB

(2004)4, must perform detailed work that will enable them to provide audit opinions on the

financial statements of the company, management’s assessment of the company’s IC over financial

reporting and the auditor’s own opinion on the company’s IC over financial reporting. SOX 302 IC

disclosures were subject to less scrutiny by both managers and auditors and regulation was less

specific allowing more discretion than SOX 404 (Ashbaugh-Skaife, Collins, and Kinney 2007).

Moreover, one of the main differences between these two provisions is that Section 302 testing was

not compulsory (Hoitash, Hoitash, and Bedard 2009). We focus on the external auditor opinion

under Section 404 because auditors add credibility to financial reporting (DeFond 1992; O’Reilly,

Leitch, and Tuttle 2006) and their assessment on IC quality is considered more reliable than

managers assessment (Hoitash, Hoitash, and Bedard 2008). For example, Skaifer et al. (2013)

investigate the role of auditors in identifying companies where managers use inside information to

get greater rent extraction. The work shows that auditors’ adverse internal control opinions related

to weak “tone at the tone”, which implies lack of integrity and unethical behavior by managers, is

associated with higher insider selling profitability.

Along with the acceleration of corporate governance and IC issues, one of the most

significant trends in the last decade is the growth of CSR. CSR is indeed seen as an extension of

firms’ efforts to implement effective corporate governance methods which would enhance sound

business practices that ensures accountability and transparency (Prior, Surroca, and Tribo 2008;

3 SOX’s Section 302 referring to the SEC-required disclosures was issued first and the main requirement

involved that two senior executives of the company (primarily the CEO and the CFO) regularly reported

publicly on their evaluation of the disclosure controls and procedures ensuring that the information required

under the Securities and Exchange Act (1934) was recorded, processed, summarized and reported accurately

and on a timely basis. 4 The Act created the Public Company Accounting Oversight Board - PCAOB (2004) which, under the SEC

supervision, oversees the audit of public companies and provides guidance to auditors for IC audits with the

aim of protecting investors and the general public by improving the audit report accuracy.

3

Kim, Park, and Wier 2012). Moreover, CSR disclosure demonstrates a company’s confidence in its

CSR activity which constitutes an informative signal (Lys, Naughton, and Wang 2013; Carroll and

Einwiller 2014). Accordingly, more socially responsible companies are likely to be perceived as

having more effective IC systems. According to ethical theories related social responsibility,

companies benefit from being honest and ethical (Jones 1995). Although CSR actions and reporting

are increasing in importance for current business, the issue of its credibility is still at play

(Hemingway and Maclagan 2004; Wang and Tuttle 2014). Prior research also suggests that the

goal of companies engaging in CSR is often window dressing or business image enhancement,

rather than a desire to be accountable to stakeholders or presenting a broader range of information

(Dowling and Pfeffer 1975; Deegan and Gordon 1996; Neu, Warsame, and Pedwell 1998).

Managers may have incentives to engage in CSR to build up their reputation as good social citizens

at the cost of shareholders (Fombrun and Shanley 1990; Linthicum, Reitenga, and Sanchez 2010).

This argument supports the idea of CSR representing management self-serving and strategic

behavior (Hemingway and Maclagan 2004). If this is the case, and if auditors perceive this

behavior, the association between CSR and IC effectiveness perception would be negative.

The response to the pressure exerted by society over companies to engage in social actions

is evident in most companies’ websites where a section for CSR is always present. Evidence of the

link between CSR and strength of IC is clearly observed in many corporate websites as well as in

the content of their CSR reports. We include illustrations of the link between CSR and IC in

Appendix 1. The examples are structured from general (reference to SOX and compliance Panel A)

to specific (reference to corporate governance in Panel B and internal-oriented CSR issues in Panel

C). Corporate strategies through these disclosures reveal that the enhancement of IC mechanisms is

mostly related to internal-oriented social responsible actions such as employee training programs

(related to employee as stakeholders)5 or promoting product quality and safety (often considered a

proxy for consumers as a stakeholder)6. Lys et al. (2013) shows that CSR disclosures are another

channel by which firms convey private information (i.e. future financial prospects) to outsiders.

Further, professional standards (AICPA 2012, AU550.06) require that auditors review other

information such as that related to CSR to verify consistency among different sources of corporate

disclosures (Byus, Deis, and Reed 2013).

Companies may want to explicitly refer to management responsibility for IC in their CSR

reports to state the objectives of the company IC system including describing various components

of that system (e.g. independent audit committee, internal audit function) or to enhance that

management believes that IC is effective7. These arguments and the anecdotal evidence are in line

5 See Appendix 1, Panel C, Examples 12 and 13.

6 See Appendix 1, Panel C, Examples 7, 8 and 9.

7 For example Unitika LTD. includes a section on IC within its CSR section where it states “In April 2007,

we created the Internal Control Promotion Office, and began implementing internal control for financial

4

with the signaling function of CSR disclosure (Lys et al. 2013). Both CSR and IC are broadly

related to management behavior, difficult to observe or assess and considered signaling devices

(Lys et al. 2013). Companies may use CSR to enhance corporate strengths on aspects of the IC

which are difficult to assess for auditors but have a pervasive effect on a company´s financial

reporting (Moody´s Investors Service 2004). In this sense, some users question the ability of

auditors to effectively audit some types of material weaknesses (MWs)8, specifically company-

level weaknesses9 (Moody´s Investors Service 2004; Credit Suisse First Boston 2005). Moody´s

considers these material weaknesses more serious than accounting-specific ones and state that

“Company-level material weaknesses may signify an increased likelihood of financial reporting

problems in the future because the company´s foundation of internal control is weak” (Moody´s

Investors Service 2004). If the lack of observability makes auditors less able to effectively audit

around company-level weaknesses it is likely that they base their adverse opinion, which give rise

to the disclosure of these weaknesses, on additional information provided by the managers and that

signals management control of these important issues. For example, the lack of personnel

resources, competency or training related to IC, if detected by auditors, triggers a qualified opinion

which gives rise to a, what has been denominated in prior literature, company-level weaknesses

(SOX 2002) Section 404. Therefore, companies may want to enhance the existence of employee

training programs in their companies to educate employees on the importance of compliance with

the SOX requirements in relation to IC quality. In line with this argument, Ashland CSR 2008

includes the following statement “Ashland is subject to annual evaluation of IC as required by the

U.S. Sarbanes-Oxley Act of 2002 (SOX). An online learning course through Ashland’s Learning

Management System educates employees on the importance of SOX and the risks of

noncompliance. In 2007, Ashland’s SOX results did not include any reportable deficiencies or

material weaknesses.” (See Appendix 1, Example 12).

Anecdotal evidence, inferred from companies websites and CSR reports, points in the

direction of a strong association between CSR and IC mechanisms but no empirical work has

analyzed the nature of this relationship yet.

Our study also considers the information quality effect. IC problems could affect earnings

quality for example, an inadequate review of the managerial adjustments could derive into earnings

management (Doyle, Ge, and McVay 2007b). Specifically, firms with company-level material

reporting. In July 2008, we established a CSR office by integrating all the sections related to internal

control”. 8 AS2 identifies three levels of IC deficiencies based on the likelihood that a material misstatement of the

financial statements might occur (PCAOB 2004): control deficiency, significant deficiency and material

weakness with the latter being the most sever type of deficiency that results in more than a remote likelihood

that a material misstatement of the financial statement will not be prevented or detected. Only material

weaknesses trigger an adverse audit opinion. 9 Harmmersley et al. (2008) defines “less auditable” weaknesses to refer to company-level weaknesses

(related to pervasive control environment, financial reporting and personnel weaknesses) and “more

auditable” weaknesses related to account-specific weaknesses (related to controls over specific accounts or

transaction-level processes).

5

weaknesses, which are less auditable, rather than those with accounting-specific weaknesses, which

are more auditable, are more highly related with earnings management (Doyle et al. 2007b). Less

auditable weaknesses are more likely to result in erroneous accruals in financial statements.

Moreover, CSR has been associated with good quality of financial information. Transparency in

reporting practices is integrated within the social responsible behavior. Companies that make an

effort to meet their stakeholders expectations following a social responsible track are likely to be

more transparent in reporting leading to a reduction of earnings manipulation (Kim et al. 2012). If

CSR is positively associated with IC quality, companies with less engagement in earnings

management are also less likely to get an adverse SOX 404 IC audit opinion.

After controlling for the potential effects of earnings quality, corporate governance and

other corporate characteristics, our findings suggest that corporate social behavior is likely to

positively influence auditors’ opinion of the quality of the IC monitoring systems. Specifically,

responsible (CSR strengths) rather than irresponsible (CSR concerns) social activities positively

relate to auditors’ IC effectiveness perception. Our main results hold after controlling for

endogeneity issues. Moreover, the evidence emphasizes the relevance of CSR dimensions. In

particular, our results reflect the importance of the effect of activities aimed at internally-oriented

social enhancement such as employee relations and product issues rather than external

enhancement activities such as those involving environmental or community issues (Jo and Harjoto

2011) in forming the auditors´ opinion on IC effectiveness. A possible explanation for these results

is that companies engaging in CSR addressed to employees (i.e. employee training programs)

increase their satisfaction leading to better IC processes (Jo and Harjoto 2011). At the same time,

companies may enhance employees’ relations issues in their CSR to promote IC quality and affect

auditors’ perception10

.

The paper makes several contributions to the extant research. First, we contribute to the

literature on IC effectiveness. Prior research focuses on examining the determinants of IC

disclosure and its effect on cost of capital and stock market responses among others. However,

there is little evidence on the mechanisms used by managers to achieve IC effectiveness. We add to

this literature by showing that IC effectiveness is related to internal-oriented social responsible

engagement and, in particular, to employee relations issues. We show that company-level

weaknesses related to adverse auditor opinions drive this association. Second, we contribute to the

literature on CSR by showing the relevance of separating responsible and irresponsible corporate

social engagement to unmask and better understand its association with the quality of IC. Finally,

our paper provides evidence of the influence of Section 404 in determining auditors’ opinion in

relation to corporate social behavior and controlling for earning quality. To the best of our

knowledge no prior research has investigated this link.

10

See Appendix 1, Panel C, Examples 10 to 20.

6

The rest of the paper is structured as follows. Section 2 reviews the literature on IC quality

and develops the hypotheses that link CSR and IC. Section 3 presents the research methodology

including sample selection, data and variables definition. Section 4 explains the main results.

Section 5 discusses the results and concludes.

2. Literature Review and Hypotheses Development

2.1. The importance of IC quality

Financial scandals have undermined the confidence of capital markets and have placed the

corporate leaders and governance systems of modern corporations under closer scrutiny than ever

(IFAC 2012). As a consequence, investors and regulators are forcing companies to improve

disclosure practices, rethink their relationships with auditors and strengthen corporate boards as

part of a wide reform of corporate governance. In addition, companies are under increasing

pressure from the government, the accounting profession and other key stakeholders to use their

evaluation and compensation systems to encourage responsible behavior at all management levels

(Hoitash, Hoitash, and Johnstone 2012; IFAC 2012).

IC has been highlighted as a determinant corporate governance mechanism to reduce

agency problems and information asymmetry by most of the codes of best practice around the

World such as COSO (2004) in the US and Turnbull Guidance and Combined Code (2005) in the

UK. IC can provide assurance regarding the reliability of financial reporting and hence effective IC

contributes to agency problems mitigation (Hoitash et al. 2009). This is also reflected on the

emphasis put by the SOX regulation on IC quality (SOX sections 302 and 404 on the effectiveness

of IC and related disclosures). The SOX regulation has strongly influenced the literature on IC and

has motivated prior work in this area.

Prior to SOX, researchers were interested in examining the nature and economic incentives

of voluntary IC reporting. For example, Bronson et al. (2006) conducted empirical research on IC

reporting in the U.S. under the voluntary settings pre-SOX and Deumes and Knechel (2008)

investigated managers’ economic incentives for voluntarily reporting on risk management and IC

using a sample of publicly traded firms in the Netherlands in the late 1990s. Subsequent research

investigates the determinants of IC weaknesses and its disclosure (Ge and McVay 2005; Krishnan

2005; Bronson et al. 2006; Ashbaugh-Skaife et al. 2007; Doyle et al. 2007b; Goh 2009; Naiker and

Sharma 2009; Munsif, Raghunandan, and Rama 2012), the positive effect of IC effectiveness on

disclosure as well as the negative association of IC weaknesses with accrual quality (Ashbaugh-

Skaife et al. 2007; Doyle et al. 2007b; Feng and McVay 2009). Evidence of the negative effect of

MWs on cost of capital or stock market responses has been shown in the literature (Ashbaugh-

Skaife et al. 2007; Ogneva, Raghunandan, and Subramanyam 2007; Beneish, Billings, and Hodder

2008; Ittonen 2010). Prior research also considers the association between IC quality and the

auditor’s involvement, for example, investigating the relationship between IC weaknesses and audit

7

delay, audit fees or auditor change (Ettredge, Sun, and Li 2006; Raghunandan and Rama 2006;

Ettredge, Li, and Scholz 2007; Hogan and Wilkins 2008; Elder, Yan, Jian, and Nan 2009; Hoitash

et al. 2009; Ettredge, Heintz, Li, and Scholz 2011; Munsif et al. 2012).

Among the purposes of SOX regulation is to provide information about corporate IC

systems to improve investors understanding of the quality of the firm’s financial reporting and

increase its credibility which is supported by the evidence in prior literature.

2.2 The link between CSR and IC

Ethical theories suggest that social responsible behavior should be integrated as part of the goal of

any company jointly with the profit-making objective (Carroll 1979). Jones (1995) contends that

CSR firms achieve higher benefits by being honest, and ethical. The moral and ethical dimension

of CSR leads to enhancing management incentives to do “the right thing”. Moreover, recent

research also emphasizes the role of CSR in improving the financial disclosure credibility (Wang

and Tuttle 2014). The arguments of CSR engagement based on ethical behavior implies that

companies investing in CSR should have higher reporting transparency and earnings quality (Kim

et al. 2012). Prior studies’ findings demonstrate that CSR improves information available to

investors by reducing analyst forecast errors (Dhaliwal, Radhakrishnan, Tsang, and Yang 2012),

decreasing cost of capital (Dhaliwal, Li, Tsang, and Yang 2011) and reducing the likelihood of

management engagement in earnings manipulation (Kim et al. 2012). This is consistent with the

idea that companies that exhibit CSR also behave responsibly by constraining earnings

management and delivering more reliable information to investors.

Research and anecdotal evidence suggests that CSR may be not only considered an

extension of firm efforts to implement effective internal governance mechanisms which would lead

to an improvement of business practices in relation to accountability and transparency but also

reducing idiosyncratic risk (Lee and Faff 2009). Companies engaging in CSR are likely to be

perceived as having better IC systems because their aim is to improve transparency and to build a

trustworthy relationship with stakeholders. This argument points to CSR engagement signaling

corporate high quality (Lys et al. 2013) and influencing auditors’ opinion of IC effectiveness. If the

link between CSR and IC effectiveness is positive and CSR is associated with decreases in earnings

management, it is also logical that companies that engage less in earnings management enjoy

stronger IC systems.

The competing explanation suggests that companies use CSR strategically to manage

impression of users of information or to compensate poor quality of financial information (Dowling

and Pfeffer 1975; Deegan and Gordon 1996; Neu et al. 1998; Prior et al. 2008). This argument

supports the idea of CSR representing management self-serving and strategic behavior

(Hemingway and Maclagan 2004; Byus et al. 2013). If auditors are somehow suspect of this

behavior, the association influence of CSR on IC effectiveness would be zero or even negative.

8

Despite these two alternative proposed directions, we expect that the signaling hypothesis will

dominate because of the cost for managers of following the second approach.

Although we do not formally propose a hypothesis related to the effect of information

quality on the relation between CSR and IC effectiveness, we include proxies for earnings quality

in our models to explicitly account for its potential effect.

Given these arguments we propose the following hypothesis to test the influence of CSR on

IC effectiveness.

H1: After controlling for earnings management and corporate governance, companies

engaging in CSR are likely to be perceived by auditors as having better IC systems

We further investigate the nature of the effect of CSR engagement on the auditors’

perception of IC effectiveness by investigating the type of weaknesses which give rise to an

adverse auditor opinion. We focus on MWs which reflect the likelihood that material misstatements

in the financial statements will not be detected or prevented. Prior literature finds that reporting of

these MWs is associated with negative market reactions and that specific characteristics of the

MWs convey information to market participants (e.g. Hammersley et al. 2008). MWs are

sometimes issued under situations of significant uncertainty which requires auditor’s judgment

(Earley, Hoffman, and Joe 2008; Hoitash et al. 2008; Bedard and Graham 2011). Therefore,

managers have incentives to influence auditors using additional cues such as information about

CSR enhancing specific relevant issues that auditors are likely to consider to form their opinions on

IC effectiveness. These weaknesses can be classified attending to their auditability level (Moody´s

Investors Service 2004; Public Company Accounting Oversight Board (PCAOB) 2007). Company-

level MWs are considered less auditable and refer to fundamental problems such as control

environment, personnel related issues or the overall financial reporting process while accounting-

specific weaknesses concern transactions and account balances and are regarded as more auditable.

According to Moody’s, company-level weaknesses are less auditable because of the pervasive

nature of the underlying IC issues. The difficulty to audit around these weaknesses does not depend

on the amount of tests or effort the auditors dedicate to assess it but it rather depends on the ability

to determine where this substantive testing should occur (Doyle et al. 2007b). Company-level

weaknesses reflect not only management’s uncertain ability to prepare accurate financial reports

but also question its ability to control the business (Doss and Jonas 2004).

The implications of the difficulty to audit around company-level weaknesses have been

evidenced in relation to audit fees, market reactions and earnings quality. Prior literature

documents that auditors’ increases in audit fees are strongly associated with the presence of

company-level weaknesses. Market participants also consider company-level MWs more serious

9

than accounting-level ones and react negatively to the presence of the former (Hammersley et al.

2008). IC problems derived from the lack of proper checks and balances might result in procedural

errors and the inadequate review of managerial adjustments might facilitate earnings management

(Doyle et al. 2007b). Doyle et al. (2007b) find that the relation between weak IC and lower accruals

quality is driven by weaknesses disclosures that relate to company-level controls. This implies that

more auditable, accounting-level problems are detected and corrected by auditors before the

issuance of the financial statements (Doyle et al. 2007b).

Based on these arguments, we expect that engagement in CSR will not be associated with

the occurrence of accounting-level MWs. These weaknesses refer to accounting specific issues

which fall within the expertise of auditors. Auditors’ opinion in relation to accounting-level

weaknesses is based on their own assessment of IC quality and is not affected by the signal sent by

the CSR engagement. On the contrary, we expect that company-level weaknesses to be negatively

associated with CSR engagement indicating that, given their complex nature implying higher

difficulty to audit around, auditors are likely to base their opinion in relation to these weaknesses

on the signal sent by CSR engagement.

H2: After controlling for earnings management and corporate governance, the effect of

CSR on the auditor’s perception of IC effectiveness depends on the type of MWs

H2a: CSR is not associated with accounting-level IC MWs

H2b: CSR is negatively associated with company-level IC MWs

3. Research Design

3.1. Sample Selection and Data

We match companies covered by the Kinder, Lyndenberg and Domini (KLD) database (KLD

2006) with non-financial and non-regulated US firms from the Compustat annual files for the

period 2004 to 2010. We start with 31,306 company-year observations from Audit Analytics with

available Section 404 IC opinions. From this sample we remove 9,207 observations from firms in

the financial sector (SIC 60-67), 1,787 observations that are not contained in the Compustat

database, and an additional 1,608 observations that are missing other required Compustat data. This

process yields a total sample size of 18,704. Next, we match the sample from Audit Analytics and

Compustat with the KLD database. Our final sample comprises 8,396 firm-year observations with

data on all variables to run all of our tests.

3.2. Measurement of Variables

Measuring IC Effectiveness

Our dependent variable IC effectiveness (Effective_IC) is an indicator variable which takes the

value of 1 if the auditor issues a qualified IC report (auditor finds the registrant’s IC over financial

10

reporting effective), and 0 otherwise (taken from audit analytics)11

(Doyle et al. 2007b; Hoitash et

al. 2009; Gordon and Wilford 2012; Munsif et al. 2012).

We also consider different types of weaknesses by splitting them into accounting-specific

(Accounting_MW) and company-level (Company_MW) as in prior research (Moody´s Investors

Service 2004; Doyle, Ge, and McVay 2007a; Doyle et al. 2007b; Hammersley et al. 2008; Munsif

et al. 2012). Further, we identify specific weaknesses related to personnel issues (Personnel_MW)

(Ge and McVay 2005; Hammersley et al. 2008). Personnel issues (such as segregation of duties,

lack of training programs or competency) are common reasons for MWs for U.S. firms. Prior

research shows that higher level of investment in IC personnel is negatively related to the

likelihood of reporting MWs (Choi, Choi, Hogan, and Lee 2013). Information on IC personnel

investment is not available in the U.S. and therefore, our measure of the relevance attributed by the

company to personnel issues is proxied by the “Employee relations” dimension included in KLD.

We expect that companies enhance the strength of personnel issues to signal concern about these

aspects of the IC quality to affect auditor perceptions of the IC effectiveness positively. Specific

measures of IC effectiveness and MWs are detailed in Appendix 2.

Measuring CSR

KLD’s Stats includes over 3,000 companies containing various CSR characteristics. KLD uses a

combination of surveys, financial statements, articles in journal (popular and academic) and

government reports to assess companies’ social performance. In particular, KLD’s social rating

criteria contains strength and concern ratings for seven qualitative issue areas including

community, corporate governance, human rights, diversity, employee relations, environment and

product12

. By aggregating a wide range of aspects relating to CSR and environmental management,

KLD covers activities that benefit society directly or indirectly13

. Following prior research

(Waddock and Graves 1997; Chatterji et al. 2009), we construct a CSR score measured as total

strengths minus total concerns in KLD’s six basic dimensions representing different stakeholders

11

Audit analytics includes companies that are required to file reports with the SEC. Section 302 of SOX

became effective for fiscal year ending after August 29, 2002 for all companies. Section 404 of the SOX

requires accelerated filers to file both a management report and an auditor's attestation on IC over financial

reporting starting with annual reports filed after November 15, 2004. Accelerated filers include companies

that have an aggregate market value of at least $75 million as of the end of their most recently completed

second quarter. The dataset covers all SEC registrants who have disclosed their assessments of IC over

financial reporting in electronic filings since 2004. Non-accelerated filers are firms with market capitalization

less than $75 million and which are not required to comply with Section 404 reporting provisions until fiscal

year ending on or after July 15, 2007. 12

Besides, KLD includes five exclusionary screen categories dimensions such as alcohol, gambling, military

contracting, nuclear power, and tobacco. 13

KLD data is considered the most comprehensive data on CSR research in a varied number of areas (for

example, accounting, economics, finance, management, and marketing). However, some limitations have

been pointed out in prior research. KLD data has an unbalanced panel structure and certain construct-validity

issues have to be considered (Chatterji, Levine, and Toffel 2009). The data is based on a snapshot over a

number of companies’ social ratings by KLD analysts in binary responses for each strength or concern (rating

1 indicates the presence and 0 absence of strength) and therefore, affected by sample selection bias.

11

(community relations, diversity, employee relations, environment, human rights and product). As in

prior literature, corporate governance is excluded and tested as a separate variable14

. However,

prior work stated that strengths and concerns are not opposing effects but distinct type of social

action that may show different effects (Mattingly and Berman 2006). Therefore, we also

decompose CSR scores into total strengths (i.e., responsible CSR) and total concerns (i.e.,

irresponsible CSR) and analyze them separately.

Given its nature KLD data can also help to understand firm-level differences with respect

to social responsibility and can be classified and conceptualized to represent not only social

performance outcomes but also as indicators of firms’ social actions towards stakeholders

(Mattingly and Berman 2006). This later formulation and classification allows identifying

important aspects related to social responsiveness towards the stakeholders represented by each one

of the groups that KLD rates. To this end, we define a dummy variable to test the CSR activities

representing internally-oriented social engagement (i.e. employee and product quality) and external

social engagement (community, human rights, diversity and environment)15

in relation to CSR

activities addressed to the stakeholders represented by these groups (Jo and Harjoto 2011).

Moreover, we create variables related to each one of the individual stakeholders KLD data.

Main Control Variables: Earnings Quality and Corporate Governance

Discretionary accruals (DA) and real activities manipulations (RAM) are included in our models as

proxies for earnings quality. We use the absolute value of discretionary accruals (ABS_DA) as a

proxy for earnings management following prior work (Jones 1991; DeFond and Subramanyam

1998; Kothari, Leone, and Wasley 2005). If we consider that companies engaging in CSR show

better earnings quality and will also be perceived as having a better quality IC system, we expect

the coefficient of earnings management (ABS_DA) to be negative. The expected sign should be

positive when considering the management opportunistic view of CSR investment which would be

associated, if detected, with auditors´ perception of less IC effectiveness.

We also test the effect of RAM on the IC quality. The proxies are defined following prior

literature (Roychowdhury 2006; Cohen, Dey, and Lys 2008; Cohen and Zarowin 2010; Zang

14

Corporate governance is perceived as a distinct contract from CSR and its impact on corporate reporting

and disclosure practices has been widely investigated in the literature (Klein 2002; Garcia Osma and

Guillamon-Saorin 2011). Therefore, we construct a CSR score based on the five remaining dimensions,

excluding corporate governance. We control for corporate governance in our regressions by including a net

score of KLD´s corporate governance ratings (Kim et al. 2012) as well as other proxies of corporate

governance quality. 15

Diversity and Human rights dimensions are treated differently in prior works. Prior literature finds the

diversity dimension either significantly adding value to company as one of the dimensions that internally

enhances CSR (Jo and Harjoto 2011) or not considered as one of the CSR dimensions that significantly

improves the company value (Godfrey, Merrill, and Hansen 2009). We include and exclude diversity from

our CSR_Internal and the results are similar. Similarly, Human rights is not clearly considered as an external

CSR dimension in prior literature and therefore, we include it and exclude it from our tests which produce

similar results.

12

2012). RAM occurs when managers carry out actions that change the timing or structuring of an

operation, investment or financing transaction attempting to influence the output of the accounting

process. Our measures of real activities manipulation are: (1) abnormal levels of operating cash

flows (AB_CFO), (2) abnormal production costs (AB_PROD), (3) abnormal discretionary

expenses (AB_EXP), and (4) a combined measure of real activities manipulation (COMB_RAM)

(Cohen et al. 2008; Kim et al. 2012). We measure abnormal levels of the first three real activities

manipulation measures as the residual from the relevant models estimated by year and the two-digit

SIC industry code.

Considering the expected directions of the first three variables, we calculate COMB_RAM

as AB_CFO - AB_PROD + AB_EXP. Higher levels of abnormal operating cash flows (AB_CFO),

abnormal expenses (AB_EXP) and overall real activities manipulation indicate more conservative

operating decisions. We expect auditors´ perception of IC effectiveness to be positively associated

with AB_CFO, AB_EXP and COMB_RAM and negatively related to AB_PROD.

We also consider corporate governance in our models. IC is an important aspect of an

organization’s governance system (IFAC 2012). The quality of an entity’s IC is affected by its

control environment (including board of directors and audit committee) and by other non-

governance related controls (Krishnan 2005). The strength of corporate governance plays a key role

in enhancing disclosure credibility. Appendix 1, Panel B includes examples which illustrate the

role played by corporate governance strength in the link between CSR and IC effectiveness

perception. The statements included in the CSRs of companies included in our sample imply that

corporate governance strength ensures stringent IC and good business practices. Prior literature has

reported a positive association between the level of IC quality and corporate governance (Krishnan

2005; Zhang, Zhou, and Zhou 2007; Goh 2009; Hoitash et al. 2009). The nature of MW also varies

with the strength of corporate governance and in particular with the level of expertise of the

personnel involved in the governance activities (Hoitash et al. 2009). Moreover, a recent work

finds a positive association between the disclosure of IC MWs and changes in corporate

governance (Johnstone, Li, and Rupley 2011b). We control for corporate governance (CorpGov) in

our models by including the net score of KLD ratings in the governance category (Kim et al. 2012).

This is measured by subtracting the number of concerns from the number of strengths in the KLD

database. As for the rest of dimensions included in KLD we also identify and tests separately

strengths and concerns for CopGov (CorpGov_strengths and CorpGov_concerns).

Other Control Variables

Since the establishment of the SOX requirement on the quality of IC over financial reporting there

has been a debate arguing that its approach is too narrow because only takes into account financial

reporting without considering operational, compliance risk and financial risk. Literature

investigating corporate IC documents that firms’ operating characteristics, such as firm size,

13

financial health, growth and litigation risk among others, are significantly associated with the

quality of the IC system, (Krishnan 2005; Bronson et al. 2006; Ashbaugh-Skaife et al. 2007; Doyle

et al. 2007b; Deumes and Knechel 2008; Munsif et al. 2012). These characteristics are referred to

as the inherent risk factors within the business, which in turn will influence a firm’s decision on IC

disclosure. When internal risks are high, a firm will have more incentives to make outsiders aware

that their IC system operates effectively through a more credible IC monitoring system. On the one

hand, investors care more about IC, and benefit more from monitoring IC, when there is a high

level of inherent risk within an organization.

We include the following control variables: (1) return on assets (ROA), (2) firm size

(SIZE), measured with log of total assets at the year-end. IC is costly and smaller companies have

less resources to invest in increasing IC quality (Krishnan 2005; Bronson et al. 2006; Munsif et al.

2012); (3) market to book ratio (MB) is a proxy for corporate growth and it is computed as market

value of equity scaled by book value (Kim et al. 2012); (4) auditor type (Big4), an indicator

variable that is equal to 1 if the external auditor is a Big4 and 0 otherwise (Hoitash et al. 2009); (5)

financial health (LOSS), a dummy variable equals to 1 if there was a net loss at the year end and 0

otherwise. Companies with poor performance are likely to have more IC problems given the

restriction for investing on IC (Krishnan 2005; Ashbaugh-Skaife et al. 2007; Hoitash et al. 2009;

Gordon and Wilford 2012); (6) Litigation risk (LIT), managers of firms facing greater risk of

lawsuits have greater incentives to disclose the adverse news of an IC problem to minimize

potential share price declines that can trigger shareholder litigation (Ashbaugh-Skaife et al. 2007).

LIT is coded one if a firm was in a litigious industry—SIC codes 2833–2836; 3570–3577; 3600–

3674; 5200–5961; and 7370-7374, and zero otherwise (Ashbaugh-Skaife et al. 2007; Hoitash et al.

2009; Munsif et al. 2012); (7) Leverage (LEV) is the ratio of assets to equity; we also assess the

firm liquidity by including the ratio of operating cash flows to sales (Kim et al. 2012). Companies

with higher liquidity are more likely to have a stronger IC system. (8) Cash-ratio is cash to total

assets; (9) the Zmijewski’s (1984) score is a proxy for financial health or firm probability of

bankruptcy. A high Zmijewski score indicates high financial stress (Krishnan 2005).

3.3 Model Specifications

To test our hypotheses, we use a logistic regression model. Specifically, to test H1 we regress

Effective_IC dummy on (1) CSR, (2) earnings quality, (3) internal and external governance

mechanisms and (4) other control variables measuring firm characteristics (Appendix 2 presents the

definitions and measurements of all variables). To test H2a we regress Accounting_MW as the

dependent variable and Company_MW is used to test H2b. Additionally we define Personnel_MW

which represents specific cases of company level weaknesses related to personnel issues (e.g.

segregation of duties, ethical problems, issues with senior management, and insufficient training

and resources) (Hammersley et al. 2008; Hoitash et al. 2009). Observations with missing data from

14

any of the variables included in the model are eliminated. Models are estimated using industry and

year fixed effects. Standards errors are clustered by firm (Petersen 2009). The models are:

Effective IC j,t /Accounting_MWj,t / Company_MWj,t / Personnel_MWj,t = α + β1 CSRj,t +β2 ABS_DAj,t +

β3 RAMj,t + β4 CorpGovj,t +β5 ROAj,t + β6 SIZEj,t + β7 MB j,t + + β8 Big4j,t + β9 LOSSj,t + β10

LITj,t + β11 LEVj,t + β12 Cash-ratioj,t + β13 Zmijewskij,t + Σ k βk Control industry k,j,t + Σ h βh Control year h,j,t +εj,t (1)

Consistent with prior research, we expect a positive/negative/negative/negative coefficient on β1, β3,

β4, and a negative/positive/positive/positive coefficient on β2 for the model using Effective_IC,

Accounting_MW, Company_MW and Personnel_MW as dependent variables. No prediction is

offered for the rest of the coefficients.

Firms can engage in both accruals and real earnings management jointly or separately

depending on the costs (Zang 2012). Following prior literature (Cohen et al. 2008; Kim et al.

2012), we control for the substitutive nature of accrual-based and real activities manipulation. To

this end, we include proxies for both accrual-based earnings management and real activities

manipulation in our regressions. We include control variables as explained in previous section.

4. Results

4.1 Illustrating the link between CSR and IC

We illustrate the link between CSR and IC effectiveness by reviewing a random sample of CSR

reports of companies included in our study and searching for the term “internal control”. We

classify the statements in the CSR that refer to IC by nature (see Appendix 1). Particularly, we

define three main categories. Panel A, “General reference to SOX compliance”, illustrates cases

where companies explicitly refer to the importance of complying with SOX regulation in their

CSR. Panel B, “Reference to corporate governance issues”, includes examples where companies

refer to the role of corporate governance to improve IC in their CSR. Panel C, “Reference to

internal-oriented issues (products and personnel)”, includes examples related to products and

personnel issues mentioned in the CSR. References to personnel issues in relation to IC seem to be

the most pervasive. The reasons for MWs on personnel, according to SOX Section 404, are also

included in Panel C. These are the reason description for IC MWs following audits analytics

taxonomy. The examples clearly demonstrate the link between CSR and IC weaknesses. Even more

interesting, the issues included in CRS enhance the strength of companies on aspects of IC

referring to personnel that otherwise may have derived into a MW. For instance, consider Example

10 where P&G company CSR report enhances the strength of the company on segregation of duties

and development of employees. On the right hand side column we include the definition of IC MW

42 (taken from Audits Analytics MWs taxonomy file). This emphasis made by the company on the

15

quality of their policies and procedures related to employees is likely to positively influence

auditor´s opinion on IC effectiveness and reduce the likelihood of getting an adverse opinion.

The evidence shown using the qualitative analysis of CSR reports is anecdotal rather than

systematic and is included to help us to support the empirical evidence presented in the following

section16

.

4.2. Descriptive Statistics

Table 1 reports the descriptive statistics for the sample. To test H1 we use a sample of 7,968

Effective _IC firms (94.8 percent) and 436 non-effective IC firms (5.1 percent) for a total of 8,396

firms meeting all selection criteria.17

For H2a we employ a total sample of 7,813 company-year

observations, where 164 (2.1%) non-effective IC firms had an accounting-level MWs. To H2b we

use two samples of 8,089 and 8,025 firm-year observations, where 323 (4.0%) and 256 non-

effective IC firms were classified as having a company level and a personnel MW, respectively.

Our main variable of interest, CSR, has a mean (median) value of -0.330 (-1.000). The

negative mean value of CSR is reflected by a relatively lower mean of CSR_strengths, 1.390,

compared to the mean value of CSR_concerns, 1.721, indicating that firms are more involved in

irresponsible than responsible CSR activities. Further, while the mean value of internal dimensions

of CSR (i.e., employee relations and product quality) is negative, -0.398, the mean value of

external dimensions of CSR (i.e., community, human rights, diversity and environment) is positive,

0.067. This preliminary evidence suggests that while firms have, on average, irresponsible

involvement in internal-oriented CSR activities, they show social responsiveness toward external

oriented CSR activities.

The mean (median) value of discretionary accruals (DA) is -0.018 (-0.005). The mean

(median) values of real activities manipulations variables, i.e., abnormal cash flows (AB_CFO),

abnormal production expenditures (AB_PROD), and abnormal discretionary expenses (AB_EXP)

are 0.168 (0.101), -0.113 (-0.046), and -0.082 (-0.092), respectively. The mean (median) value

measure of combined real activities manipulations (COMB_RAM) is 0.199 (0.063). The mean

(median) value of corporate governance (CorpGov) is -0.223 (0.000). This negative value of

CorpGov is illustrated by relatively lower mean of CorpGov_strengths, 0.204, compared to the

mean value of CorpGov_concerns, 0.428.

16

While we focus on disclosures made in CSR reports to provide this anecdotal evidence, the empirical study

is based on a diverse number of sources of CSR reporting (such as surveys, financial statements, articles in

journals and government reports) used to produce the KLD database (KLD Research & Analytics Inc. 2003;

KLD 2006). 17

These percentages of effective vs. non effective IC firms are similar to those shown in prior literature

(Dhaliwal, Hogan, Trezevant, and Wilkins 2011; Gordon and Wilford 2012).

16

For the control variables, the mean (median) values of auditor type (Big4) is 0.898 (1.000).

ROA, MB, LEV and Cash ratios have a mean value of 7.6 percent, 168.6 percent, 36.7 percent, and

57.0 percent, respectively. The mean value of equity (SIZE) is 7,004 (i.e., $1,101 million). About

twenty two percent of all observations (i.e., 22.1 percent) show losses. The Zmijewski score has a

mean (median) value of -2.237 (1.808). Finally, more than forty-six percent of all observations (i.e.,

45.7 %) belong to a litigious industry.

(Insert Table 1 about here)

In Panel B of Table 1 we compare descriptive statistics of variables between effective IC

firms and non-effective IC firms. The mean value of the CSR score is higher for the Effective IC

firms (-0.317) in comparison to that of the non-effective IC firms (-0.571). The difference is

statically significant at the 5 percent level, indicating that effective IC firms are more socially

responsible than non-effective IC firms. Specifically, effective IC firms present significantly higher

CSR_strengths (1.419 vs. 0.854, p = 0.00) but also higher CSR_concerns (1.737 vs. 1.425, p = 0.00)

than those of non-effective IC firms. Further, CSR_internal is significantly lower for effective IC

firms than for non- effective IC firms (-0.393 vs. -0.495, p = 0.07). CSR_external is lower for

effective IC firms than for non- effective IC firms but non-significant (0.075 vs. -0.076). Therefore,

effective IC firms not only show higher (lower) commitment toward responsible (irresponsible)

CSR activities, but also lower (higher) involvement in irresponsible (responsible) internal (external)

CSR dimensions.

Both effective and non-effective IC firms exhibit positive values of discretionary accruals

being larger for the non-effective IC sample (mean values of 0.016 and 0.054, respectively; p=

0.00), indicating that CSR firms are less likely than non-CSR firms to use discretionary accruals to

manage earnings. Regarding real activities manipulations, Effective IC firms show higher mean

values of AB_CFO (0.172 vs. 0.113, p = 0.00) and COMB_RAM (0.201 vs. 0.801, p = 0.00) than

non-effective IC firms. Mean values of AB_PROD and AB_EXP for the Effective IC firms are

significantly lower than those for non-effective IC firms at the 1 percent level. These results

suggest that effective IC firms are less likely to engage in real activities manipulation than non-

effective IC firms. There are no significant differences between effective and non-effective IC

firms in terms of corporate governance. Furthermore, effective IC firms are larger, financially

healthier, face lower litigation risk, and rely more on Big4 auditors than non-effective IC firms. We

did not find significant differences in either corporate governance mechanisms or ROA between the

two groups.

The data presented in Panel C of Table 1 reveals that the most heavily represented industry

is Chemicals and Allied Products (SIC code 28), followed by Business Services (SIC code 73),

17

Electronic & Other Electric Equipment (SIC code 36), Industrial Machinery and Computer

Equipment (SIC code 35), and Instruments and Related Products (SIC code 38).

Table 2 presents the Pearson correlation matrix of main variables. CSR is significantly and

positively related to Effective_IC (0.02). CSR_strengths, CSR_concerns, and CSR_internal are also

positively correlated with Effective_IC. Accounting_MW, Company_MW, and Personnel_MW are

significantly and negatively correlated with CSR_strengths and CSR_internal. This provides

preliminary evidence consistent with a positive relation between IC quality and CSR activities.

While DA is negatively correlated with Effective_IC (-0.03), COMB_RAM is positively related to

Effective _IC (0.06). CSR is also positively correlated with DA (0.03) and COMB_RAM (0.13).

CorpGov is positively related to DA (0.07). Overall, most explanatory variables are not highly

correlated to each other and, therefore, multicollinearity does not seem to be a problem.18

(Insert Table 2 about here)

4.2 Main Tests

Table 3 presents the results of the probit regression analyses regarding the impact of CSR on

Effective_IC after controlling for accrual-based and real activities earnings management as well as

for the role played by corporate governance19

. Columns 1, 2, 3 and 4 of Table 3 report the results

controlling for different proxies of real activities manipulations, i.e., AB_CFO, AB_PROD,

AB_EXP, and COMB_RAM, respectively. Our main interest is in the sign and magnitude of the

coefficients on CSR. The coefficients on CSR are positive and significant for the regressions of

AB_CFO (0.022, p < 0.10, column 1), AB_PROD (0.028, p <0.05, column 2), AB_EXP (0.027, p

<0.05, column 3), and COMB_RAM (0.028, p <0.05, column 4).

Further, columns 1 to 4 show that the coefficients on ABS_DA are negative and significant

at the 5 percent level, indicating that firms involved in absolute discretionary accruals are

associated with less IC quality. As for real activities manipulation, while the coefficients of

AB_CFO (0.053, p < 0.10, column 1), AB_EXP (0.055, p <0.01, column 3), and COMB_RAM

(0.041, p <0.01, column 4) on Effective_IC are positive and significant, the coefficient of

AB_PROD (-0.060, p <0.01, column 2) is negative and significant, indicating that, in general, firms

that engage in real activities manipulation are associated with poor IC effectiveness. Regarding the

role played by corporate governance mechanisms, the coefficients on CorpGov are positive and

18

CSR, CSR_strengths, CSR_concerns CSR_internal, CSR_external are highly correlated with each other.

Similarly, COMBINED_RAM is highly correlated with AB_CFO, AB_PROD and AB_EXP. However, this is

not a problem since we test these variables in separate models. 19

Prior research (Graham, Harvey, and Rajgopal 2005; Cohen et al. 2008; Kim et al. 2012; Zang 2012) has

demonstrated the positive association between accruals and real activities earnings management. Therefore,

we simultaneously control for discretionary accruals and earnings management activities in our regressions

because of the potential trade-off between the two.

18

significant at the 1 percent level for all the regressions.

(Insert Table 3 about here)

Turning to control variables in Table 3, the coefficients on the Big4 variable is positive and

significant at the 1 percent level, indicating that, in general, firms audited by large audit firms are

more likely to have more effective IC systems. The coefficients on ROA, SIZE, MB, Cash-ratio and

Zmijewski variables are positive and significant, suggesting that more profitable, larger, higher

market-valued, more liquid, and less financially distressed firms are associated with more effective

IC. In contrast, the coefficients on LOSS and LEV are negative and significant, indicating that firms

with qualified audit report, losses and higher leverage are more prone to have non-effective IC

systems. The coefficient on LIT is insignificant for all the regressions.

In summary, Table 3 shows that, after controlling for the role played by corporate

governance, accrual-based and real activities earnings management, firms engaging in CSR

activities are less likely to get an adverse SOX 404 IC audit opinion (H1).

In Table 4, columns 1 to 3, we report the results of the probit regression analyses replacing

the dependent variable Effective_IC with Accounting_MW, Company_MW and Personnel_MW,

which are indicator variables that equal 1 if the firm has a MW pertaining to accounting-specific,

company-level and personnel-related material weaknesses, respectively, and 0 otherwise. For

brevity, we only report coefficients for the variables of interest.

(Insert Table 4 about here)

We find that the coefficients on CSR are negative and significant for the regressions of

Company_MW (-0.031, p < 0.05, column 2) and Personnel_MW (-0.038, p <0.05, column 3).

However, the coefficient on CSR is negative but non-significant for the Effective_IC (-0.032, p >

0.10, column 1). When CSR is separated into strengths and concerns (CSR_strengths and

CSR_concerns), we observe that the effect is driven by the strengths and that concerns is not

significant. These results are consistent across all models and provide some evidence that the

observed effect is based on perceptions of the quality of IC rather than on CSR activities. If the

effect was driven by CSR activities we would expect to see a decrease in IC effectiveness for

companies showing CSR concerns. Columns 1, 2 and 3 of Table 4 also show that the coefficients

on ABS_DA (COM_RAM) are positive (negative) and significant, indicating that firms involved in

absolute discretionary accruals (real activities manipulation) are associated with fewer accounting-

specific, company-level and personnel-related MWs, respectively. Further, the coefficients on

CorpGov are negative and significant for all the regressions, indicating that firms with stronger

corporate governance mechanisms are associated with fewer accounting-specific, company-level

and personnel-related MWs.

Taken together, this evidence suggests that after controlling for earnings management and

19

corporate governance, CSR activities are not associated with the detection of account-specific MW

(H2a). On the contrary, firms engaging in CSR activities are negatively associated with company-

level and personnel-related MWs (H2b).

4.3 Additional tests

Responsible vs. Irresponsible CSR Activities

Mattingly and Berman (2006) classify corporate social action patterns and argue that responsible

(CSR strengths) and irresponsible (CSR concerns) social actions are distinct constructs and should

be investigated separately20

. They run an additional test separating CSR strengths and CSR

concerns for all KLD dimensions to make sure that the aggregation is not hiding important

effects21

. Following prior literature (Waddock and Graves 1997; Mattingly and Berman 2006;

Chatterji et al. 2009; Kim et al. 2012; Cho et al. 2013), we split the CSR score into strengths and

concerns and run our main test on the effect of CSR on IC quality.

Table 4, columns 4 to 7 summarize the results for the impact of CSR strengths and

concerns on effective IC, accounting-specific, company-level and personnel-related MWs,

respectively. We find that the coefficient on CSR_strengths is positive and significant (0.046, p <

0.05, column 4) for the regression of Effective_IC. Further, the coefficients on CSR_strengths are

negative and significant for the regressions of Company_MW (-0.133, p < 0.10, column 6) and

Personnel_MW (-0.204, p <0.01, column 7) but not significant for the Accounting_MW (-.118, p >

0.10, column 5).

The coefficient on CSR_concerns is negative and non-significant for the regression of

Effective_IC (column 4) and positive and non-significant for the MWs regressions (columns 5 to 7).

Results for the role played by earnings management and corporate governance are qualitative

similar to our main findings in Table 3. These results seem to support that IC quality, in terms of

the presence of an adverse SOX 404 IC audit opinion and the absence of company-level and

personnel MWs, is improved through a responsible involvement in CSR activities (i.e., CSR

strengths) and that involvement in irresponsible CSR activities (i.e., CSR concerns) is not

associated with IC effectiveness and company-level and personnel-related MWs.

Dimensions of CSR

Prior work suggests that corporate social engagement responds to internal or external stakeholders

based on manager’s perceptions of their relative importance (Mattingly and Berman 2006). To this

20

The classification of social action patterns involves considering KLD data as indicators of corporate social

actions rather than consequences or outcomes of action (Mattingly and Berman 2006). 21

For example, a recent research of Cho, Leeb, and Pfeiffer (2013) finds that irresponsible CSR is much

stronger than responsible CSR in reducing information asymmetry.

20

end, prior research investigates the effect of the disaggregated dimensions of CSR included in

KLD, which represent different stakeholders, as well as groups of dimensions representing internal

or external-oriented social actions (Turban and Greening 1997; Mattingly and Berman 2006; Jo and

Harjoto 2011; Kim et al. 2012) 22

. We draw on prior research and adapt the methodology to our

particular setting. Prior work finds that investment in personnel related to IC is associated with IC

systems quality and, in particular, to be negatively associated with the disclosure of IC weaknesses

(Choi et al. 2013). Therefore, enhancing the significance of employees training programs to make

them aware of the importance of IC quality is likely to send a strong signal to auditors and

influence their perception of IC effectiveness. Accordingly, we build a measure for each CSR

dimension and combine them to test the effect of firm internal enhancement CSR activities

(employee and product quality) and external oriented CSR activities (community, human rights,

diversity and environment) on IC quality (Jo and Harjoto 2011)23

.

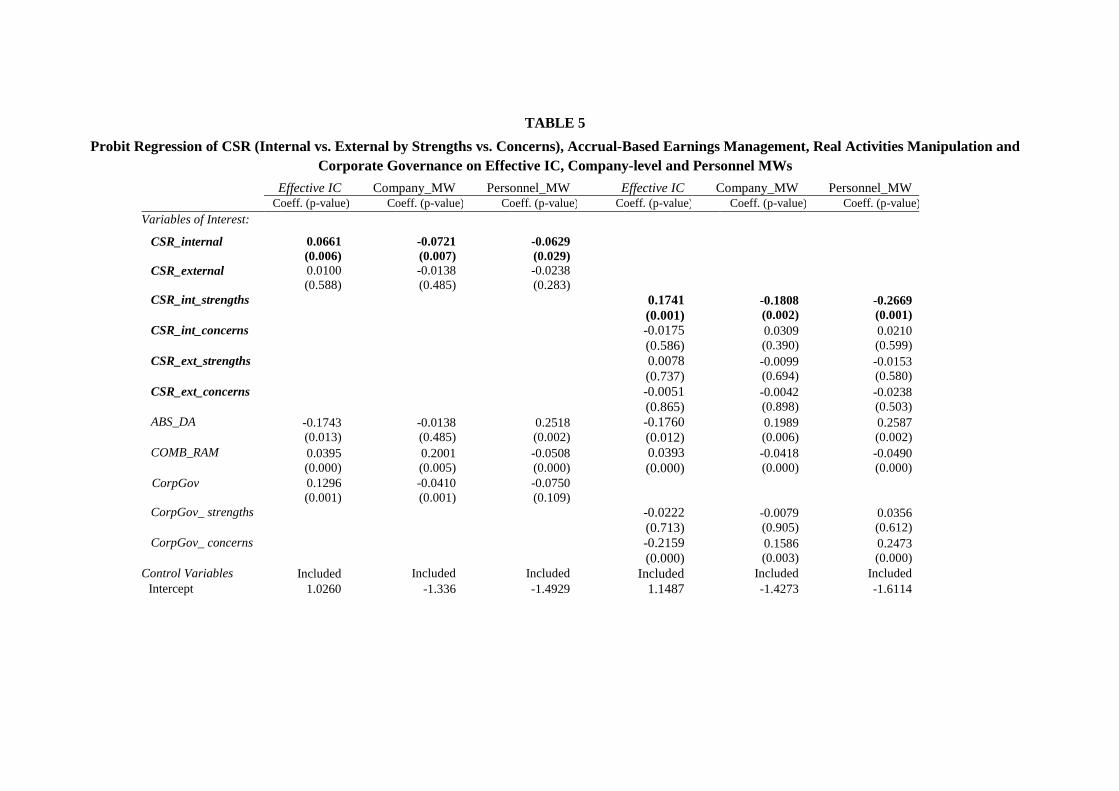

(Insert Table 5 about here)

Summarized results in Table 5 show that while the coefficient of CSR_internal on

Effective_IC is positive and significant (0.066, p < 0.01, column 1), the coefficient of

CSR_external is also positive but not significant. We find similar results for the regressions of

Company_MW and Personnel_MW, where the coefficients on CSR_internal are negative and

significant (-0.072, p < 0.01; -0.063, p < 0.05; columns 2 and 3, respectively). Further, columns 4

to 6 of Table 5 also present the results of internal and external CSR dimensions separated by

strengths and concerns. Results show that only the coefficient of CSR_int_strengths has a positive

and significant effect on Effective_IC (0.174, p < 0.01) and a negative and significant effect on

Company_MW (-0.181, p < 0.01, column 5) and Personnel_MW (-0.267, p < 0.01, column 6).24

(Insert Table 6 about here)

We run additional analyses based on individual KLD Ratings Categories. Columns 1 to 3

of Table 6 present a model using disaggregated subscores of CSR for each of the six qualitative

screening categories of community (CSR_Com), diversity (CSR_Div), employee relations

(CSR_Emp), environment (CSR_Env), human rights (CSR_Hum) and product (CSR_Prod).

Results show that only the coefficient on CSR_Emp is positive and significant for the regression of

22

Employee relations dimension refers to policies such as employees’ cash profit-sharing program,

employees’ involvement in management decision-making, stock ownership, and retirement benefits program.

Product dimension refers to quality or investment in R&D. Community refers to activities related with

charitable giving, support for education, support for housing, volunteer programs. Environment dimension

refers to pollution prevention policies, recycling programs, clean energy. The diversity dimension refers to

promotion of women and minorities, programs addressing work/life concerns, human research programs for

the disabled, progressive programs towards gay and lesbian employees.

24

Nontabulated results show that consistent with the results of Table 4, neither CSR_internal nor

CSR_external had a significant effect on accounting-specific MW.

21

Effective_IC (0.102, p <0.01, column 1) and negative and significant for the regressions of

Company_MW (-0.099, p < 0.01, column 2) and Personnel_MW (-0.107, p < 0.01, column 3). In

columns 4 to 6, by splitting the six aforementioned dimensions into strengths and concerns, we find

a significant and positive coefficient on CSR_Emp_strengths for the regression of Effective_IC

(0.227, p <0.01, column 4) and negative and significant for the regressions of Company_MW (-

0.304, p < 0.01, column 5) and Personnel_MW (-0.320, p < 0.01, column 6). This evidence

suggests that only a responsible commitment toward employee relations CSR activities is

associated with more effective IC and, particularly, with the absence of company-level and

personnel-related MWs.25

Responsible involvement in philanthropy (community related activities),

diversity, environmental, human rights or product quality CSR activities does not lead to IC

effectiveness. These results empirically confirm the evidence derived from the qualitative content

analysis carried out on CSR of companies and illustrated in Appendix 1. The results support the

idea that the observed effect of CSR on IC effectiveness is explained by the signaling purpose of

CSR management strategies (Lys et al. 2013). Employee CSR dimension is one of the main reasons

for the occurrence of MWs. By focusing on the most positive aspects of CSR related to personnel

issues (measured as CSR_Emp_strengths in our work) managers enhance the visibility of those

aspects which will contribute to form a positive impression of users of this information. This is also

consistent with prior literature investigating the role of CSR in enhancing the credibility of

financial disclosure (Wang and Tuttle 2014).

Number of IC weaknesses

We rerun our analyses using the number of weaknesses as an alternative measure of IC quality

(Jonhstone, Li, and Rupley 2011; Lu, Richardson, and Salterio 2011; Gordon and Wilford 2012).

Effectiveness of IC and disclosure of MWs may capture different aspects of IC but we expect that

both measures are significantly associated with CSR.26

When using number of IC weaknesses as the dependent variable, the sign is expected to be

the opposite to those found for IC effectiveness where companies with more engagement in CSR

are associated with less number of weaknesses. Untabulated results show that the coefficients on

CSR are negative and significant in the regressions on the number of weaknesses, after controlling

25

Again, nontabulated results show that neither CSR dimension nor its direction had a significant impact on

accounting-specific MW. 26

There is no explicit requirement that firms disclose material weaknesses to the public under Section 302.

However, Item 307 of Regulation S-K (“Disclosure controls and Procedures”) implicitly requires the

disclosure of any identified material weakness. Item 307 requires companies to disclose on the effectiveness

of IC systems and logically companies will only conclude that their IC is ineffective if they discover a

material weakness. As in prior literature, we assume that all material weaknesses are discovered and

disclosed (Doyle et al. 2007b; Leone 2007). This assumption can be considered one of the limitations of the

paper (Leone 2007).

22

for earnings management and corporate governance. Furthermore, results confirm that firms

showing a commitment toward employee relations CSR activities are associated with lower number

of IC weaknesses. Further, the signs of the coefficients on discretionary accruals earnings

management, real activities manipulation and CorpGov variables are significant and opposite to

those in the main tests, suggesting that firms engaging in earnings management or with less robust

corporate governance mechanisms are associated with higher number of material IC weaknesses.

CSR and non-effective IC firms

We further investigate whether involvement in CSR activities helps reduce the severity of IC MWs.

To this end, we limit our sample to those firms which IC continue to be non-effective in year t+1

(N = 432 observations). As dependent variable, we use total number of IC weaknesses. Untabulated

results show that the reduction of the number of IC weaknesses is marginally associated with firms’

CSR involvement. In terms of strengths and concerns, the number of IC weaknesses is significantly

reduced through a responsible involvement in CSR activities. Finally, as for specific KLD

dimensions, we observe that involvement in CSR activities related with community is the only

CSR dimension that contributes to reduce the number of IC weaknesses for non-effective IC

firms27

.

Controlling for endogeneity

Since better quality firms tend to choose CSR engagement, the contribution of CSR to IC quality

will be overstated if we do not correct for endogeneity problems (Greene 2003). Our main tests do

not account for the possibility that our dependent variables (i.e., Effective_IC, Accounting_MW,

Company_MW, and Personnel_MW) and CSR are endogenously related. One problem with

standard OLS estimations in Equation (1) is that it is assumed that error term (εj,t) is uncorrelated

with the observed covariates, CSR and our dependent variables. Our basic hypothesis is that

companies that choose to engage in CSR are not a random sample of firms. Using IV allows us to

estimate the effect of CSR on our dependent variables indirectly, without the need to use directly

our original endogenous measure of CSR. The main difficulty with IV estimation is the

identification of valid instrument variables because most of observable company characteristics are

already included in the equation. Characteristics of a good instrument variable are such that it is not

correlated with the error term in the equation but that it is correlated with the endogenous variable

of interest, CSR.

27

Prior literature refers to philanthropic activities as discretionary responsibilities (Carroll 1979; Maignan

and Ferrell 2009) linked to social or cultural projects. These activities are likely to create goodwill and offer

insurance-like protection to companies in the presence of a negative effect (Godfrey et al. 2009). Investment

in philanthropic activities, therefore, can be seen as an alternative for companies with non-effective IC but

which try to reduce IC ineffectiveness.

23

To do so, we adopt a two-stage instrumental variable approach (Rusticus and Larcker 2010)

to reexamine our main findings reported in Table 3 and columns 1 to 3 of Table 4. Specifically, we

model CSR in the first stage and then, in the second stage, we regress our dependent variables on

the probability of being a CSR company obtained from the first stage regression (CSR_IV).

Specifically, we estimate the following instrumental variable equation (2):

CSR_IVj,t = α + β1 CSRj,t-1 +β2 ABS_DAj,t-1 + β3 RAMj,t-1 + β4 CorpGovj,t-1 + β5 ROAj,t-1 + β6 MBj,t-1

+ β7 SIZEj,t-1 +β8 Marketing intensityj,t-1 + β9 R&D intensityj,t-1 + Σ k βk Control industry k,j,t

+Σ h βh Control year h,j,t +εj,t (2)

In the first stage (untabulated), we include the lagged value of CSR due to the control time

series of CSR as an instrumental variable (Ittner and Larcker 1998). Equation (2) also contents

lagged values of ABS_DA, RAM and CorpGov since firms showing that engaged in earnings

management or firms with poor corporate governance are less likely to become good corporate

citizens (Prior et al. 2008). CSR can be also affected by various factors like previous financial

performance and firm size (Orlitzky 2001; Surroca, Tribo, and Waddock 2010). To control for

these effects, we use lagged values of ROA, MB and SIZE. We also include lagged R&D intensity

and lagged Marketing intensity in Equation (2) since previous innovation and advertising intensity

can be positively associated with CSR (McWilliams and Siegel 2000; Prior et al. 2008; Surroca et

al. 2010). Finally, we also control for industry and year effects.

Table 7, columns 1 to 4, presents the results for the second stage estimation of the impact

of CSR_IV on Effective_IC, Accounting_MW, Company_MW, and Personnel_MW, respectively.