Embed Size (px)

Citation preview

CES Le ture Series

Regulation of Prot Shifting:

Potential Instruments and Their Optimal Design

Dirk S hindler (Norwegian S hool of E onomi s)

Le ture 2: Debt Shifting, Transfer Pri ing, and the Optimal

Choi e of Thin Capitalization Rules

Dirk S hindler

5 FDI and Thin Capitalization Rules

5.1 Linking FDI, Prot Shifting and Thin Capitalizati-

on Rules

• Two mantras in publi opinion and politi s (partly in e onomi s):

1. FDI is desirable for welfare and should be fostered

→ tax ompetition, investment subsidies...

2. Prot-shifting & tax havens threatening welfare (high-tax oun-

tries)

→ OECD-BEPS: urb prot shifting, ban tax havens

• But: FDI is prerequisite for MNCs doing prot shifting

CES Le ture: Regulation of Prot Shifting 53 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Foreign Dire t Investment (FDI)

⋄ Strong growth of FDI sin e mid-eighties

⋄ MNCs driving for e

⋄ Competition for FDI via tax advantages et .

CES Le ture: Regulation of Prot Shifting 54 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Table 5.1: Top 10 ountries with highest ratio of FDI ows as per entage of GDP (2001-2005)

Rank Country FDI Outow (%) FDI Inow (%) Sum of In- and

Outows (%)

1 Luxembourg 296.6 342.6 639.3

2 Hong Kong (China) 13.5 14.0 27.5

3 Singapore 8.5 13.7 22.2

4 I eland 15.1 5.5 20.6

5 The Netherlands 11.0 5.9 16.9

6 Belgium 6.8 9.8 16.6

7 Ireland 6.6 5.3 12.0

8 Lesotho 0.0 10.9 10.9

9 Switzerland 7.5 2.4 9.9

10 Bulgaria 0.1 9.1 9.3

Sour es: Mintz/Wei henrieder, 2010, based on IMF Statisti s

CES Le ture: Regulation of Prot Shifting 55 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• In publi debate: Thin apitalization rules

⋄ seen as main ounter measure against prot shifting

⋄ an ome as safe harbor or earnings stripping rule

⋄ being ee tive instruments based on empiri al eviden e

⋄ but redu e (inward) FDI and MNCs' a tivity

→ from Le ture 1: Thin apitalization rules might redu e welfare and suer

from tax ompetition

CES Le ture: Regulation of Prot Shifting 56 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Fig. 5.1: Average tax rates and thin- apitalization (safe-harbor) limits in 2004:

Top20 ountries GDP-per apita (left) vs. 34 emerging ountries (right)

CES Le ture: Regulation of Prot Shifting 57 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Table 5.2: Number of ountries with ea h type of thin- apitalization rule in 2013 (sample size = 160)

None or Arm's- Safe Harbor Earnings Stripping Safe Harbor and Safe Harbor or Spe ial

Length Regulation Earnings Stripping Earnings Stripping Rules

100 45 4 2 6 3

CES Le ture: Regulation of Prot Shifting 58 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

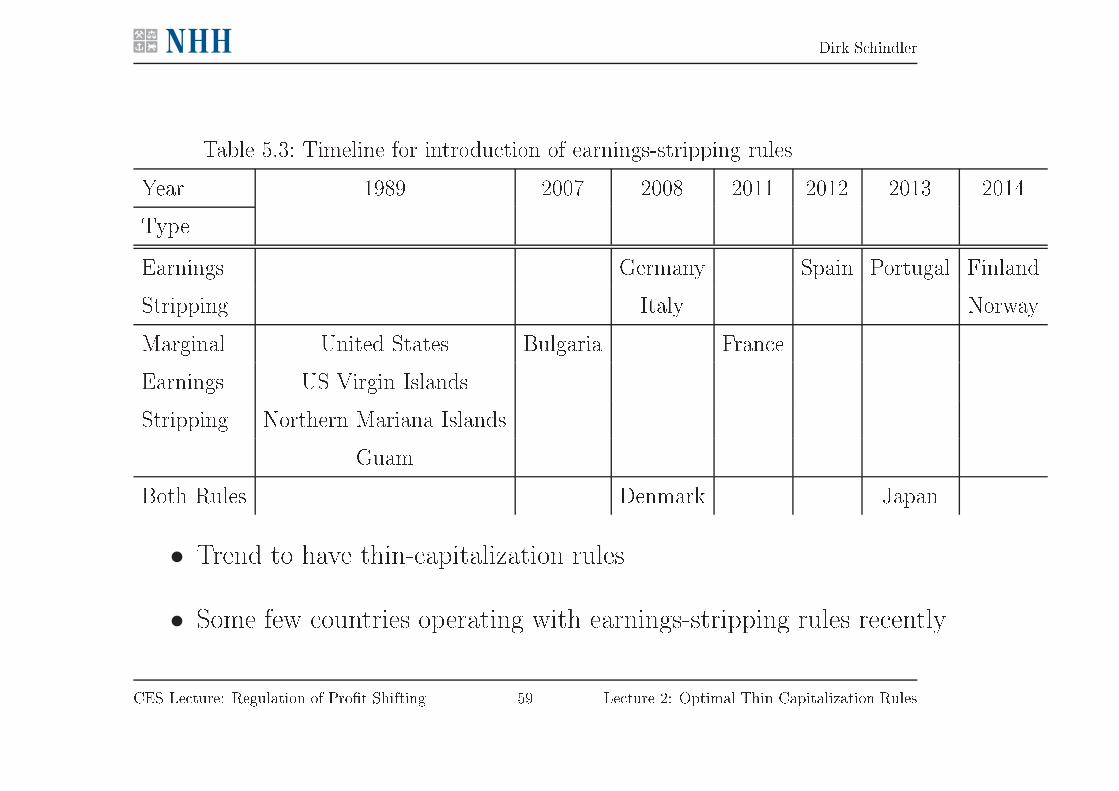

Table 5.3: Timeline for introdu tion of earnings-stripping rules

Year 1989 2007 2008 2011 2012 2013 2014

Type

Earnings Germany Spain Portugal Finland

Stripping Italy Norway

Marginal United States Bulgaria Fran e

Earnings US Virgin Islands

Stripping Northern Mariana Islands

Guam

Both Rules Denmark Japan

• Trend to have thin- apitalization rules

• Some few ountries operating with earnings-stripping rules re ently

CES Le ture: Regulation of Prot Shifting 59 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Questions in this Le ture

• How do FDI and prot shifting intera t and is FDI always good?

• Are tax havens good or bad and does this depend on prot-shifting

hannel?

→ debt shifting vs. transfer pri ing

• How should thin- apitalization regulation look like (if any)?

→ safe-harbor vs. earnings-stripping rules

CES Le ture: Regulation of Prot Shifting 60 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

5.2 Modelling the Relevant Trade-os

• Using Hong/Smart (2010) as point of departure: small open e onomy

• Domesti workfor e inelasti ally supplying one unit of labor L

• Domesti rms

⋄ produ ing with labor only: G(Ld) with Ld as labor demand

⋄ prot fun tion: π = (1− t)[G(Ld)− wLd]

• MNC

⋄ produ ing with labor Lm and apital K

⋄ onstant-returns-to-s ale produ tion fun tion F (Lm,K)

CES Le ture: Regulation of Prot Shifting 61 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Labor-market equilibrium

Ld + Lm = L = 1 ⇒ wage ratew

• Constant e onomi ost of apital r (`integrated world apital market')

• For simpli ity: no external debt (i.e., no orporate bonds)

CES Le ture: Regulation of Prot Shifting 62 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

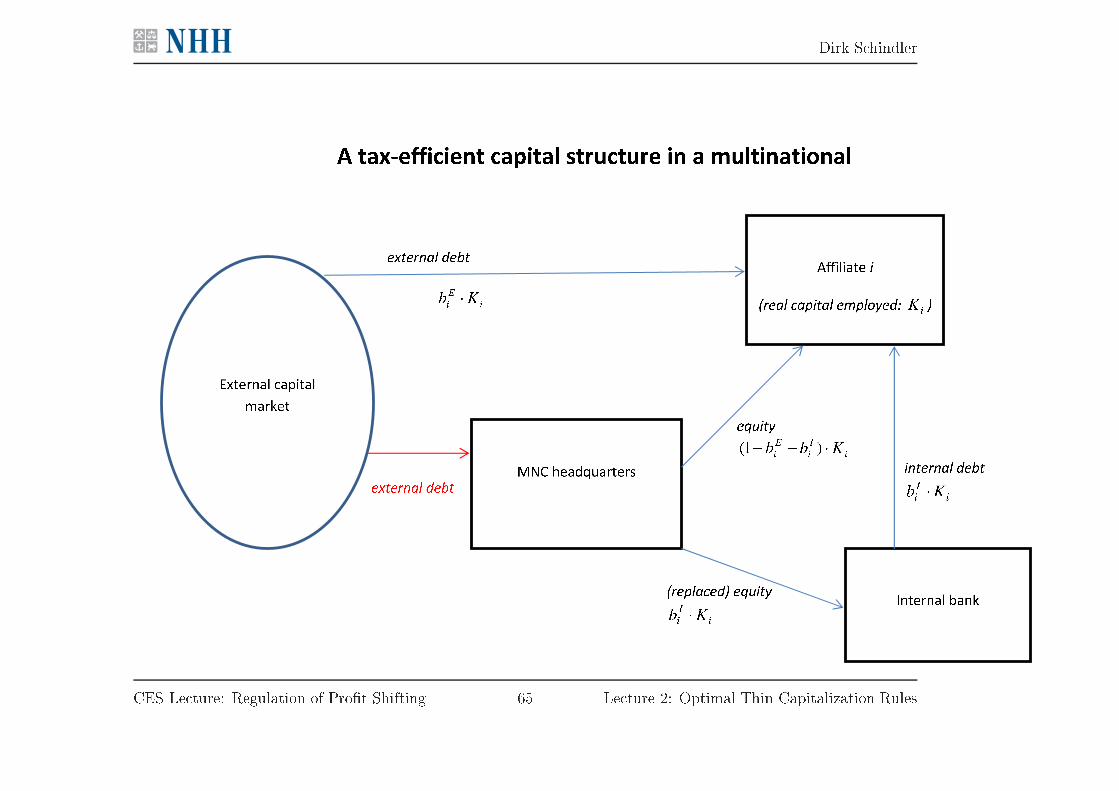

• Finan ing de ision of MNC:

⋄ equity E

⋄ (internal) debt B

→ (internal) leverage ratio b = B/K

• Costs of equity not dedu tible in orporate tax base

• Leveraging until thin- apitalization limit is rea hed (safe-harbor rule)

• Internal debt routed via tax-haven aliate with zero tax rate

CES Le ture: Regulation of Prot Shifting 63 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Possibility to over harge internal interest rate σ > r

→ simplest way to add transfer pri ing to the model (no loss of generality)

• Con ealment osts C(σ − r, B, α) = αc(σ − r)bK

⋄ onvex in interest sur harge, proportional in apital

⋄ α hoi e parameter of government (quality of institutions)

• Output pri e normalized to one: p = 1

• Corporate tax rate t

CES Le ture: Regulation of Prot Shifting 64 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

CES Le ture: Regulation of Prot Shifting 65 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

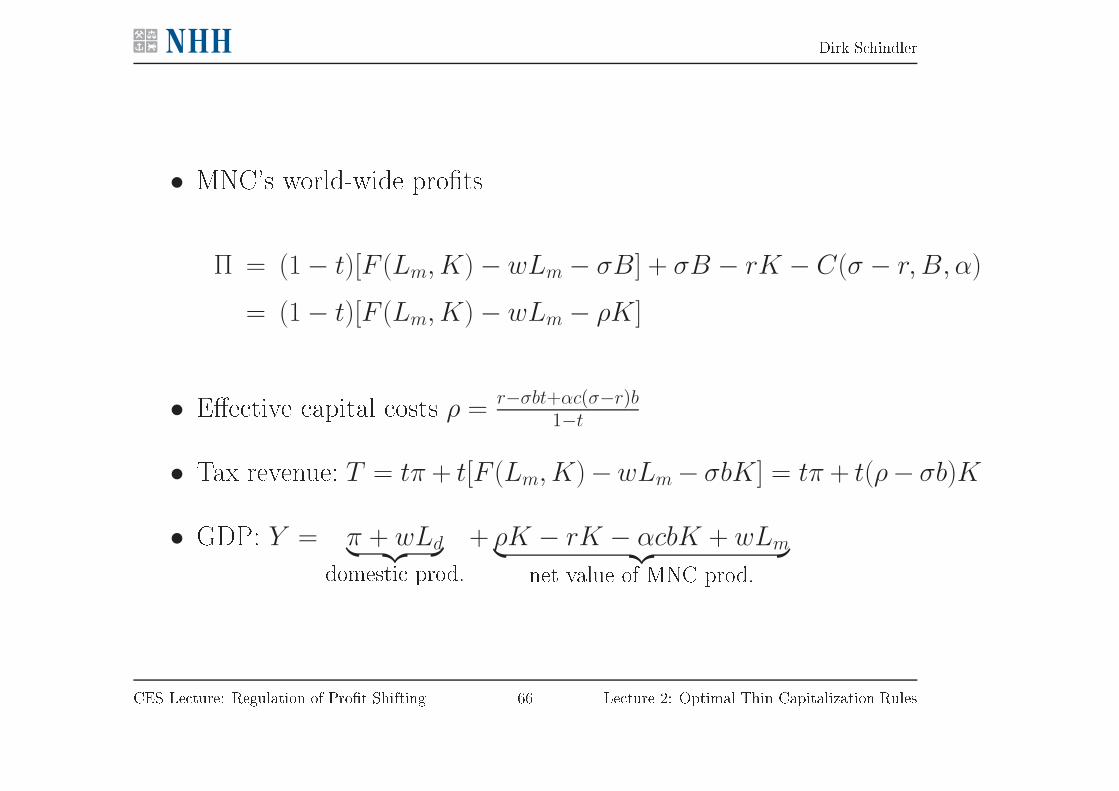

• MNC's world-wide prots

Π = (1− t)[F (Lm, K)− wLm − σB] + σB − rK − C(σ − r, B, α)

= (1− t)[F (Lm, K)− wLm − ρK]

• Ee tive apital osts ρ = r−σbt+αc(σ−r)b1−t

• Tax revenue: T = tπ + t[F (Lm, K)−wLm− σbK] = tπ + t(ρ− σb)K

• GDP: Y = π + wLd︸ ︷︷ ︸

domesti prod.

+ ρK − rK − αcbK + wLm︸ ︷︷ ︸

net value of MNC prod.

CES Le ture: Regulation of Prot Shifting 66 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Welfare fun tion: Ω = CW + βCE

⋄ CW = onsumption of domesti workers

⋄ βCE = weighted onsumption of domesti entrepreneurs

⇒ Equivalent to Ω = Y − (1− β)(1− t)π

CES Le ture: Regulation of Prot Shifting 67 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

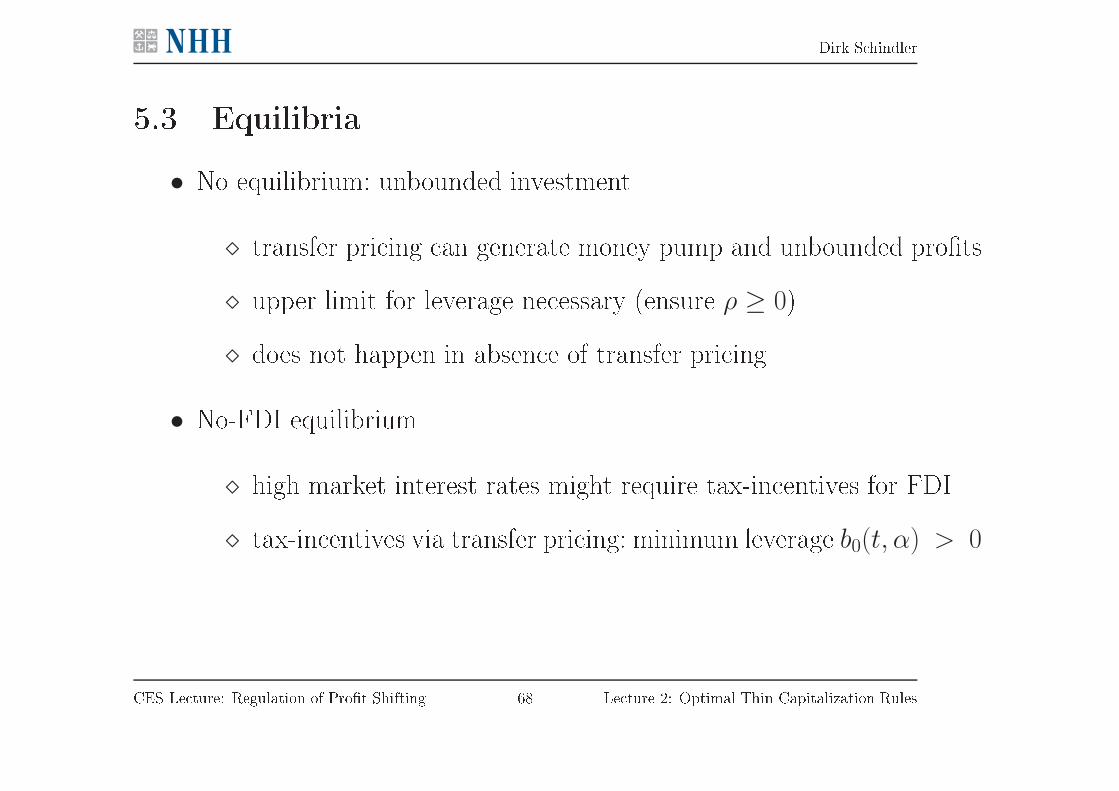

5.3 Equilibria

• No equilibrium: unbounded investment

⋄ transfer pri ing an generate money pump and unbounded prots

⋄ upper limit for leverage ne essary (ensure ρ ≥ 0)⋄ does not happen in absen e of transfer pri ing

• No-FDI equilibrium

⋄ high market interest rates might require tax-in entives for FDI

⋄ tax-in entives via transfer pri ing: minimum leverage b0(t, α) > 0

CES Le ture: Regulation of Prot Shifting 68 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Fig. 5.2: Iso- ost- urves for ee tive apital osts ρ∗

CES Le ture: Regulation of Prot Shifting 69 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

6 FDI, Thin Capitalization Rules and Host

Country Welfare Maximization

• Government maximizing weighted onsumption Ω

• Instruments

⋄ transfer-pri e regulation: ost parameter α

⋄ thin- apitalization limit: safe-harbor rule b

⋄ orporate tax rate t

CES Le ture: Regulation of Prot Shifting 70 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Constraint: labor-market equilibrium

⇒ Obje tive fun tion

maxα,b,t

Ω = Y − (1− β)(1− t)π

s.t. L = 1 = Ld(w) + Lm(w, ρ)

CES Le ture: Regulation of Prot Shifting 71 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

6.1 Case 1: Unrestri ted hoi e

• (Extreme) Assumption: free hoi e of α at no ost

→ interpret α as a ne

• Optimal to set α as high as possible (α→ ∞)

⇒ Shut down transfer pri ing

Result 1: Transfer pri ing is welfare redu ing and should be prevented whenever

this is possible at no administrative/ omplian e osts.

CES Le ture: Regulation of Prot Shifting 72 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Model ollapsing to Hong/Smart (2010)

• We show

⋄ optimal leverage: b∗ = 1

→ full dedu tibility of normal rate of return

⋄ optimal orporate tax rate: t∗ = 1

→ expropriate all supernormal prots

⇒ First-best allo ation (in Hong/Smart, 2010)

CES Le ture: Regulation of Prot Shifting 73 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Intuition: Why no transfer pri ing?

⋄ debt shifting preferable (dire t) instrument to mitigate investment

distortion

⋄ waste of resour es on on ealment osts

⋄ potentially installing a money pump (if negative tax payments

possible)

→ Marks&Spen er ruling by European Court of Justi e

⋄ allowing to shift out supernormal prots / ountries' wealth (re-

sour es)

CES Le ture: Regulation of Prot Shifting 74 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Intuition: Why no thin- apitalization limit?

⋄ small open e onomy: sour e tax on apital shifted fully on to labor

⋄ optimal tax on normal return on mobile apital zero (in standard

model)

⋄ optimal to tax inelasti domesti rms and supernormal prots

⋄ dilemma: only one, uniform orporate tax rate

⋄ but: no use of internal debt in (purely) domesti rms

⇒ all apital as internal debt avoiding tax on MNCs' normal return

⇒ perfe tly dierentiated ee tive tax rates

⇒ orporate tax = non-distortive prot tax

→ Hong/Smart (2010) redoing Gordon (1986)

CES Le ture: Regulation of Prot Shifting 75 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

6.2 Case 2: Restri ted hoi e (upper limit for α)

• Constraint optimization with `exogenous' α, e.g., legal limitation of nes

• Optimal orporate tax rate

∂Ω

∂t=ρ∗ − r − αcb

t(1− t)

∂Ω

∂ρ∗︸ ︷︷ ︸

(−)

−btK

αc′′+ (1− β)π = 0

• Balan ing marginal osts vs. redistributional gains

1. term distorting allo ation and redu ing wages: ()

2. term in reased losses from transfer pri ing: ()

3. term redistributional gains from taxing domesti entrepreneurs: (+)

CES Le ture: Regulation of Prot Shifting 76 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Impli ations

⋄ With FDI, optimal tax rate t∗ < 1

→ distortions and transfer pri ing onstraining tax poli y

⋄ In No-FDI optimum, expropriation of domesti entrepreneurs

⇒ t∗ = 1

CES Le ture: Regulation of Prot Shifting 77 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Optimal thin- apitalization limit

∂Ω

∂b= −

σ∗t− αc

1− t

∂Ω

∂ρ∗− αcK = 0

• Balan ing e ien y gains vs. losses

1. term welfare ee t via fa tor allo ation: (+ / )

2. term losses from transfer pri ing: ()

• Note that

∂Ω∂ρ∗

> 0 possible if too mu h transfer pri ing

• Optimal leverage b∗ < 1 due to osts from transfer pri ing

• Potentially optimal to disallow FDI (i.e., hoose low b∗ < b0)

→ more likely the lower α and the higher apital ost r

CES Le ture: Regulation of Prot Shifting 78 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Intuition: Why an FDI be undesirable?

(+) in reasing produ tion (and potentially labor demand)

(+) in reasing domesti wages

() fa ilitating (via transfer pri ing) to shift out tax revenue and to

expropriate domesti natural resour es

() negative aspe t worse in ountries with weak/lousy institutions

⇒ if FDI taking out more than it brings in, so ial return to FDI

negative

→ imagine 78% tax in petroleum se tor, but unlimited transfer pri-

ing

⋄ matters most for developing ountries

CES Le ture: Regulation of Prot Shifting 79 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

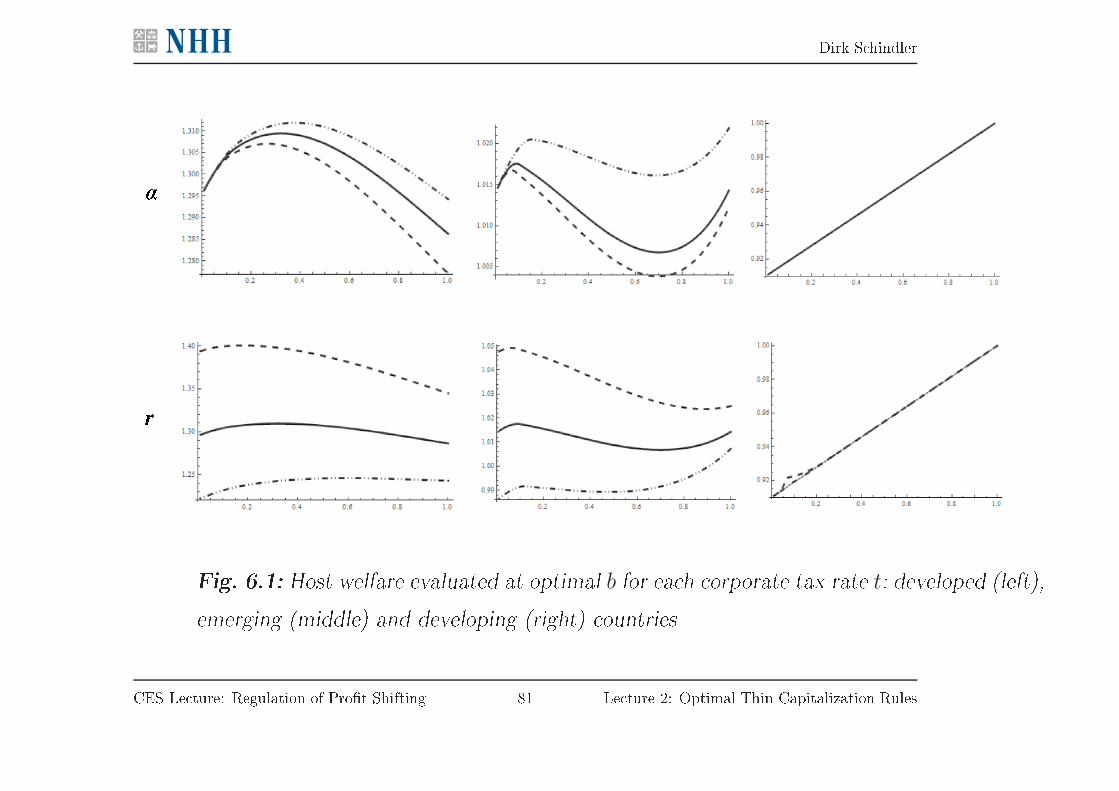

• Heterogeneous ountries

⋄ developed ountries

∗ low apital ost (r = 0.05), relat. high apital share (γ = 0.25)

∗ strong institutional quality (high ost parameter) α = 6

⋄ emerging ountries

∗ moderate apital ost (r = 0.08), low apital share (γ = 0.2)

∗ moderate institutional quality (low ost parameter) α = 1

⋄ developing ountries

∗ high apital ost (r = 0.15), low apital share (γ = 0.2)

∗ weak institutional quality (very low ost parameter) α = 0.1

CES Le ture: Regulation of Prot Shifting 80 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Fig. 6.1: Host welfare evaluated at optimal b for ea h orporate tax rate t: developed (left),

emerging (middle) and developing (right) ountries

CES Le ture: Regulation of Prot Shifting 81 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Extensions

⋄ results qualitatively robust for

∗ transfer pri ing in third (intermediate) fa tor

∗ de reasing returns to s ale: supernormal prots

⋄ no-loss oset in orporate tax

∗ money-pump gone

∗ under onstant returns to s ale ba k to Hong/Smart

∗ robust results under de reasing returns to s ale (?!)

→ working on extension with heterogenous rms and entry osts

CES Le ture: Regulation of Prot Shifting 82 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Result 2 FDI is not always bene ial. Developing ountries ould be better o

under autarky.

⇒ Tax havens deteriorating welfare

Result 3 It is always optimal to restri t internal leverage in order to mitigate

revenue losses (and waste of resour es) from transfer pri ing if transfer

pri ing annot be prevented at no osts.

⇒ Whi h type of rules better: safe-harbor vs. earnings-stripping rules?

CES Le ture: Regulation of Prot Shifting 83 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

7 Choi e of Safe-harbor vs. Earnings-stripping

Rules

• Use model from previous hapter with some simpli ations

⋄ exogenous orporate tax rate t > 0

⋄ normalize ost parameter for transfer pri ing α = 1

⋄ add some (agen y) ost of leverage D(b)

⋄ equal welfare weights (β = 1): `utilitarism'

• Implement two systems of simultaneous thin- apitalization regulation

⋄ safe-harbor rule bs

⋄ earnings-stripping rule be

CES Le ture: Regulation of Prot Shifting 84 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

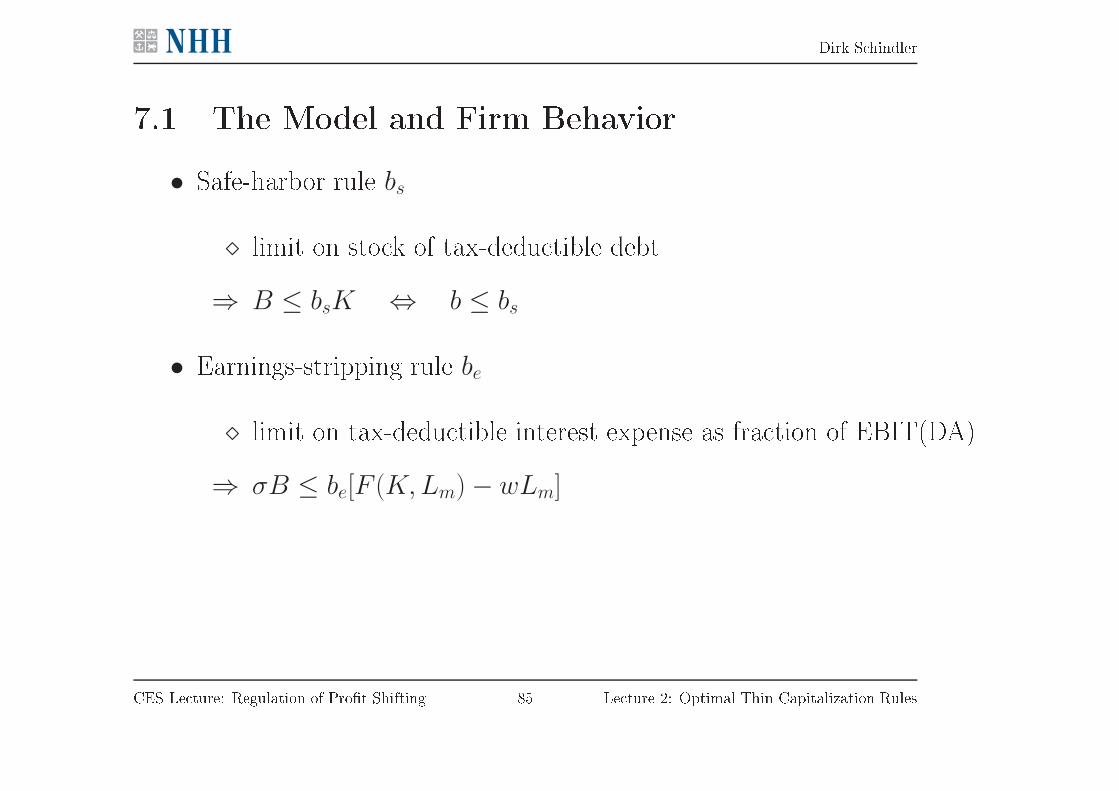

7.1 The Model and Firm Behavior

• Safe-harbor rule bs

⋄ limit on sto k of tax-dedu tible debt

⇒ B ≤ bsK ⇔ b ≤ bs

• Earnings-stripping rule be

⋄ limit on tax-dedu tible interest expense as fra tion of EBIT(DA)

⇒ σB ≤ be[F (K,Lm)− wLm]

CES Le ture: Regulation of Prot Shifting 85 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Firms' prot maximization

⋄ optimal un onstraint amount of debt 0 < B(σ, r) < K

⋄ earnings-stripping rule redu ing transfer pri ing

→ substitution ee t towards debt shifting

CES Le ture: Regulation of Prot Shifting 86 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Fig. 7.1: Prot-maximizing transfer pri es and debt levels (given K and L)

CES Le ture: Regulation of Prot Shifting 87 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

7.2 Host Country Welfare

• Relaxation of safe-harbor rule bs

⋄ in rease in FDI ∂K/∂bs > 0; in reasing also wages and produ tion

⋄ no ee t on transfer pri e (∂σ∗/∂bs = 0)

Result 4 Never optimal to have both binding safe-harbor and binding earnings-

stripping rule.

• Intuition

⋄ relaxing safe-harbor rule in reasing FDI and wages

⋄ earnings-stripping rule preventing loss in tax revenue

⇒ Ine ient regulation in Denmark and Japan

CES Le ture: Regulation of Prot Shifting 88 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Fig. 7.2: Binding equilibrium thin apitalization rules

CES Le ture: Regulation of Prot Shifting 89 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Result 5 If there is a thin- apitalization restri tion, the optimal hoi e is imple-

menting an earnings-stripping rule without a safe-harbor limit.

• Intuition

⋄ safe-harbor limits redu ing investment,

but no dire t ee t on transfer pri ing

⋄ earnings-stripping rules redu ing transfer pri ing,

less negative ee ts on investment

⇒ earnings-stripping rules partly sheltering normal rate of return

while urbing welfare-deteriorating transfer pri ing

CES Le ture: Regulation of Prot Shifting 90 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

Main Take-away from Le ture 2

• Prot shifting by debt shifting bene ial to shelter normal rate of return

→ allowing to dis riminate between immobile rms and mobile apital

• Transfer pri ing is always deteriorating welfare

• FDI an be undesirable in ase of ex essive transfer pri ing

• FDI an be harmful for national welfare if too mu h transfer pri ing

→ parti ularly problemati for developing ountries with weak institutions

CES Le ture: Regulation of Prot Shifting 91 Le ture 2: Optimal Thin Capitalization Rules

Dirk S hindler

• Tax havens are `bad' as along as transfer pri ing out of ontrol

• Tax havens potentially bene ial if transfer pri ing pre luded

• Thin- apitalization restri tion via earnings-stripping rule dominant

→ impli itly restri ting transfer pri ing without urbing FDI too mu h

CES Le ture: Regulation of Prot Shifting 92 Le ture 2: Optimal Thin Capitalization Rules

![[XLS] · Web viewBridge Room & Board Social Workers MH Coun-Phd MH Coun-Msw MH Coun-Inst MH Inst-Non-Coun Phys-Visits Phys-Surgery Language Interpreter/Translation Service Phys-Lab](https://img.dokumen.tips/doc/110x75/5afe6f9f7f8b9a434e8f130e/xls-viewbridge-room-board-social-workers-mh-coun-phd-mh-coun-msw-mh-coun-inst.jpg)