Embed Size (px)

Citation preview

M Imran Centre Director (Riyadh, Jeddah), IE Singapore

Second Secretary (Commercial), Singapore Embassy (Riyadh)

5 February 2015

Saudi Arabia:

An Oasis of Stability, A Country of Prosperity

Agenda

1. Why Saudi Arabia?

2. Where are the opportunities?

• How to tap on them?

• Who to work with?

3. Upcoming key initiatives

4. What other considerations to look out for?

Agenda

1. Why Saudi Arabia?

2. Where are the opportunities?

• How to tap on them?

• Who to work with?

3. Upcoming key initiatives

4. What other considerations to look out for?

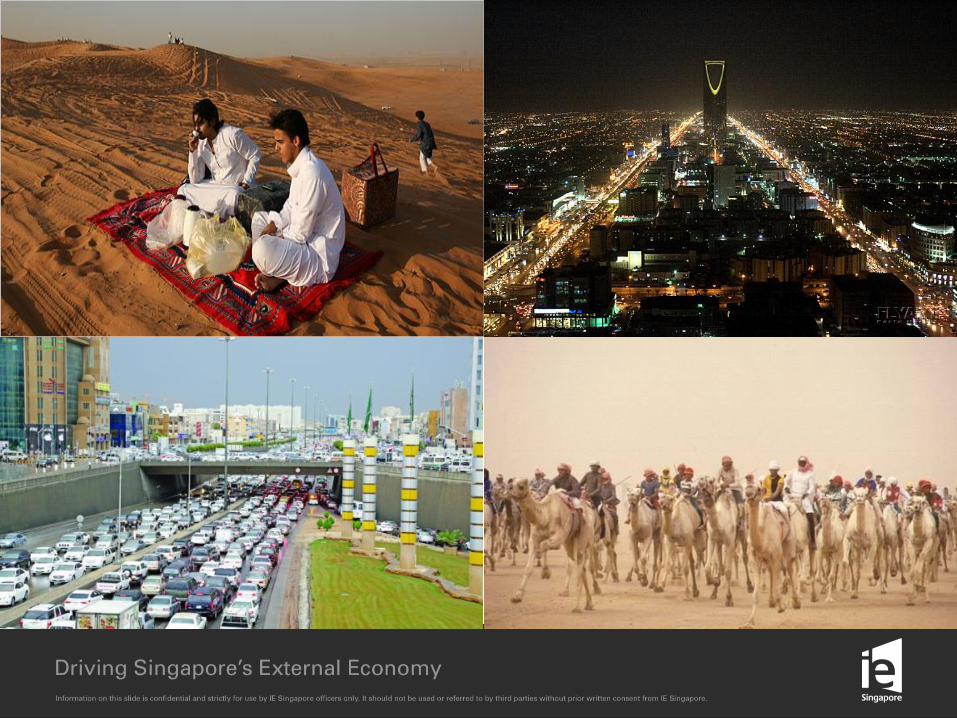

Saudi Arabia in Numbers

13 provinces, 2.15 mn sq km

LARGE INFRA REQ’D

Population - 30,770,375

LARGEST BASE IN ME

GDP- US$ 777.870 billion

THE LARGEST ECONOMY IN ME

GDP per capita- US$25,401

HIGH POTENTIAL FOR CONSUMPTION

Projected GDP growth (2015-2019) – 4.5%

SECOND LARGEST IN GCC

* All figures are 2014 estimates

Saudi-Singapore Economic Figures

Total Trade - S$20.11 billion in 2014

Trade Growth – 5.2% CAGR over the past 5 years

Saudi is Singapore’s 15th largest trading partner &

2nd largest in GCC

Ease of Doing Business (2014) – The World

Bank

Ease of... 2012 Rank

2013 Rank

2014 Rank

Doing Business 49 22 26

Starting a Business 109 78 84

Dealing with Construction Permits 21 32 17

Getting electricity 22 12 15

Registering Property 20 12 14

Getting Credit 71 53 55

Protecting Investors 62 19 22

Paying Taxes 3 3 3

Trading Across Borders 92 36 69

Enforcing Contracts 108 124 127

Resolving insolvency 163 107 106

An Oasis of Stability, A Country of Prosperity

** Saudi Arabia reputation as a pillar of stability was enhanced after it

came out relatively unscathed during the Arab Spring and the smooth

leadership transition given the passing of the late King Abdullah

Singapore companies have successes in the Saudi Arabia

Consumer Retail

Hospitality

Consumer Food

Infra & Utilities

ICT

Transport & Logistics

Oil & Gas

Aviation

Agenda

1. Why the Saudi Arabia?

2. Where are the opportunities?

• How to tap on them?

• Who to work with?

3. Upcoming key initiatives

4. What other considerations to look out for?

Energy

KSA remains a key player in global Oil & Gas

Oil

• 260.2 billion barrels of crude oil reserves (25% of the world's proven recoverable crude oil reserves)

• 3.5 billion barrels of crude oil production (annual)

• 9.5 million barrels of crude oil production (daily average)

Gas

• 284.8 Trillion standard cubic feet of gas reserves (6th in the world)

• 3.9 trillion standard cubic feet of gas production (annual)

• 10.7 billion standard cubic feet of gas production (daily)

Continued heavy spending despite oil price slump

Map of Overall Global Cleantech Innovation Index Scores

Source: Cleantech Group Analysis

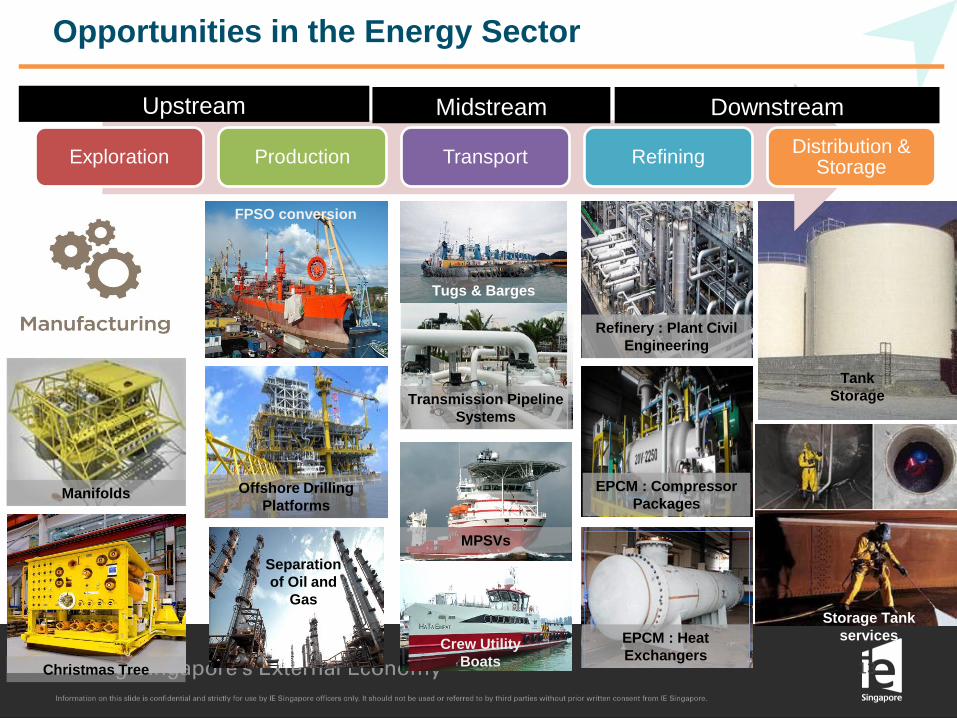

Opportunities in the Energy Sector

13

Exploration Production Transport Refining Distribution &

Storage

Upstream Midstream Downstream

Offshore Drilling

Platforms Manifolds

Christmas Tree

FPSO conversion

MPSVs

Crew Utility

Boats

Tugs & Barges

Transmission Pipeline

Systems

Tank

Storage

EPCM : Compressor

Packages

Refinery : Plant Civil

Engineering

Separation

of Oil and

Gas

EPCM : Heat

Exchangers

Storage Tank

services

Recommendations for Singapore companies engaging the KSA O&G sector

Focus on Supply & Services

Partner with conglomerates/ industry leaders

already qualified with NOCs

1

2

Recommendation 1: Focus on Supply & Services

Supply: Accessing the Global Supply Chain

• Increase supply of niche equipment procured from SG

• Capitalize on GSFTA to enjoy tariff savings

• Establish a local presence in partnership with local leading coy to develop local content

Services

• Lack of maintenance and support services in both marine and O&G sectors such as welding, diving, surveying, facilities maintenance

• Set up a presence in KSA to provide much needed services and over time, engage in technology and skills transfer.

• Conglomerates are important to the Saudi economy, with many owning

companies in energy, telecommunications, property, retail trade and

banking. Source for reliable local coys as distributors, stockist and/or

partners to establish local connections.

Recommendation 2: Partner with conglomerates/ industry leaders already qualified with NOCs

• A large percentage of materials and services are sourced by global

established LSTK (lump sum turn key) contractors worldwide, leverage

on or establish r/p for more palatable sizes.

Consumer

Country

Gross Domestic Product (GDP) Household consumption expenditure Consumption Expenditure as % of GDP

2011 2012 2013 2011 2012 2013 2011 2012 2013

Bahrain 29,044,085,407 30,756,332,649 32,897,761,327 11,245,621,872 11,686,269,269 13,266,488,785 38.72 38.00 40.33

Kuwait 154,034,939,461 174,044,699,037 175,831,217,319 37,279,655,594 41,071,595,436 42,529,117,946 24.20 23.60 24.19

Oman 69,521,984,671 77,497,360,083 79,655,916,775 21,041,593,443 22,840,362,336 17,593,499,131 30.27 29.47 22.09

Qatar 169,804,736,002 189,944,505,495 202,450,000,000 21,952,110,454 24,088,516,427 28,194,380,225 12.93 12.68 13.93

Saudi Arabia 669,506,763,733 733,955,613,519 748,449,649,075 181,802,933,333 209,441,066,667 222,209,787,781 27.15 28.54 29.69

Singapore 272,316,082,866 284,298,603,868 295,744,026,213 101,483,421,899 109,936,397,599 113,582,753,936 37.27 38.67 38.41

United Arab Emirates 347,454,050,374 372,313,955,071 402,340,095,303 181,076,923,077 178,972,089,857 200,387,474,472 52.12 48.07 49.81

Saudi’s consumption & GDP expenditure is the highest in GCC

Sources: National Accounts Main Aggregates Database; United Nations Statistics Division; Euromonitor

Highest

in the

GCC

This robust consumption is driven by:

Young and growing

population

Increasing

household wealth

This robust consumption is driven by:

Increasingly smaller family sizes, Increase number of households

Recommendations for Singapore consumer companies

Consumer Services: Collaborate with relevant local

consumer giants

Consumer Products: Work with multi-brand retail

operators

1

2

Consumer Services: Collaborate with relevant local consumer giants

• Local consumer giants are companies who are mall developers/ owners, retailers or

franchisees.

• Collaboration models - Leasing, JV, Consignment, Franchising

• Select local franchising coy which has experience in the target consumer segment and consumer profile.

• Landing point for Asian food retail: Jeddah – One of the 3 largest economic cities in KSA with the highest proportion of expatriates.

• Expansion to Riyadh & Eastern Province as the next 2 most dense regions

Food Services

• Shop location is key to reaching target consumer

• Choice of partner is important as financial and social clout is needed to secure ideal location

Fashion Retail

• Taking a long term view of the market

• Branding – Commitment of resources to create brand awareness

• First target consumer would be the Asian expatriate population

Learning points

Consumer Products: Work with multi-brand retail operators

• Local multi-brand operators could be distributors, master/ area franchisees, or

retailers with their own brands and other acquired brands

• Collaboration Models – JV, Franchise, Distribution

•Commitment to brand awareness initiatives

•Natural affinity for western products; hence coys should target primarily the huge Asian expatriate population that numbers approximately 9million in the whole of the Kingdom.

•Packaging is key, especially for premium products.

Brand awareness

•The general consumer is very price sensitive with very little brand loyalty.

•Associate premium products with Western markets. Price sensitive

•When choosing channel partners/distributors, it is important to choose a partner who is experienced with marketing and distributing Asian products.

Choice of Partner

• Important to partner with a local coy with strong traditional trade channels in order to access the other regions of Saudi that are less urbanised

Strong distribution

Other Non Oil Sector growth

Sizable opportunities in infrastructure, Transport & Logistics, Construction

• Growth is also being driven by projects in the non‐oil sectors such as

transport and infrastructure, power and water as well as

communications and construction

• SR232.3bn ($62bn) worth of non‐oil projects were awarded in 2013 and

SR76.58bn ($20.4bn) expected to be awarded in 2014.

• Around 37 per cent of upcoming projects under execution belong to the

transport sector with 21 per cent in power and 19 per cent in the

education sectors respectively.

• While SG coys are not able to front the projects, there are opportunities

for niche products & services.

Agenda

1. Why Saudi Arabia?

2. Where are the opportunities?

• How to tap on them?

• Who to work with?

3. Upcoming key initiatives

4. What other considerations to look out for?

2015 Key Initiatives

• Supplier Day to Saudi Arabia & Qatar/Abu Dhabi in 2nd quarter 2015. Roundtable prior to speak about opportunities.

• Key upcoming projects: World class maritime yard in Saudi Arabia between Aramco, Sembcorp, Bahri (currently in FS)

Oil & Gas

• King Abdullah Economic City (KAEC) @ Rabigh

• Focus: Port and logistics, Pharmaceuticals, FMCG, light industry

• Size: 168-180 million square metres

• Master developer: Emaar, The Economic City

• Current anchor tenants: Mars, Total, Pfizer and Sanofi

• Jizan Economic City (JEC) @ Jizan

• Focus: Energy and labour-intensive industries

• Investment: $27bn

• Master developer: Saudi Aramco

Economic Cities –

KAEC, JEC

Agenda

1. Why Saudi Arabia?

2. Where are the opportunities?

• How to tap on them?

• Who to work with?

3. Upcoming key initiatives

4. What other considerations to look out for?

Other macro business considerations

1

2

3

Factor time for business processes

Relationship building is key

Be present in the country, engage in

technology and skills transfer

Thank You www.iesingapore.com