Embed Size (px)

Citation preview

March 17, 2014

Shane Nagle, CFA 416.869.7936 [email protected]

Associate: Greg Doyle 416.869.6538 [email protected]

SILVERCREST MINES INC.

SANTA ELENA MILL CONSTRUCTION SUPPORTS FUTURE LOW-COST GROWTH

INITIATING COVERAGE SVL (TSX): Cdn$2.70 Stock Rating: Outperform Risk Rating: Speculative 12-Month Target: $3.25 12-Month Return: 20% Shares O/S: 117.9 Mln Market Cap: $318 Mln

HIGHLIGHTS Transition of Santa Elena from heap leach to milling operation nearing completion. The

3,000 tpd CCD/Merrill-Crowe circuit will help improve silver recoveries and increase production as the company begins processing higher grade underground ore later this year. We model production growth to 4.8 mln oz/yr AgEq at US$9.00/oz cash costs in 2015 from 2.7 mln oz AgEq at US$7.90/oz in 2013 (NBF Estimate).

Balance sheet sufficient to fund exploration and future expansion opportunities. SilverCrest ended the year with US$19 million in cash (NBF Estimate), and with the recent $23 million equity raise and US$10 million contribution from SSL we estimate a cash low of ~US$35 million in Q2 2014.

Recent acquisition of Ermitano fits company’s strategy of low-risk, step-wise growth. Exploration work will be underway in 2014 and with some success ore could be shipped to an expanded Santa Elena mill (located approximately four kilometres to the southeast) in as little as two to three years.

As a single-asset producer, SilverCrest’s revenue is dependent on the successful transition to milling and underground mining at Santa Elena. Management has exhibited an ability to develop assets in a prudent, cost-efficient manner, while financial risks are largely mitigated by the US$42 million cash balance, no debt and US$40 million of available credit.

We are initiating with a $3.25 target and Outperform rating. SVL is trading at 10.2x EV/2014E CF, in line with peers at 10.4x. We also like the long-term prospects of the company given its expected free cash flow of US$20 million/year (at spot prices) once transition to the mill is complete in H2 2014. EQUITY

RESEARCH

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

TABLE OF CONTENTS

CORPORATE OVERVIEW 2 Stable Financial Position 2 Management Has Displayed Ability to Add Value Throughout Development of Santa Elena 3 Santa Elena Expansion Potential Offers Cost-Effective Growth Prospects 3

INVESTMENT THESIS 4 Fully-Funded Development 4 Room for Organic Growth 4 Expansion Opportunities and Free Cash Flow Make SVL an Attractive Acquisition Target 6 Outperform Rating Supported by Positive Long-Term Outlook Given Strong FCF Growth 6

UPCOMING CATALYSTS / NEWS FLOW 8

RISKS 9

VALUATION, TARGET PRICE & RATING 10 NAV Breakdown 10 Target Price & Rating 11

SANTA ELENA 12 Property Description 12 Historic Work 12 Geology & Mineralization 13 Mining & Processing 14 Potential for Expansion 15

LA JOYA 16 History 16 Geology & Mineralization 16 Results of PEA 17

APPENDIX 1: MANAGEMENT 19

APPENDIX 2: BOARD OF DIRECTORS 20

APPENDIX 3: RESERVES & RESOURCES 21

APPENDIX 4: FINANCIAL STATEMENTS 22

DISCLOSURES 23

The analyst attended a site visit to Santa Elena in November 2013. A portion of the expenses were covered by the issuer.

Industry Rating (Metals & Mining): Market Weight (NBF Economics & Strategy Group)

All dollar amounts in Cdn$ unless otherwise noted. All pricing as at March 14, 2014

All NBF research mentioned in this document is available at www.nbfinancial.com

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 1

FINANCIAL & OPERATING SUMMARY: SILVERCREST MINES INC.

STOCK RATING Outperform TICKER SVL-T

TARGET PRICE (C$) $3.25 CURRENT PRICE (C$) $2.70

RETURN TO TARGET 20% 52-WEEK HIGH (C$) $3.05

RISK RATING Speculative 52-WEEK LOW (C$) $1.19

SECTOR RATING Market Weight SHARES OUTSTANDING (mln) 117.7

FISCAL YEAR-END December 31 MARKET CAPITALIZATION (C$ mln) $317.8

MARKET DATA STOCK CHART

Capital Structure

Shares Outstanding

Options

Warrants

Fully Diluted Shares

Top Ownership

Sprott Asset Management LP

AGF Investments Inc.

Libra Advisors LLC

Global X Management Company LLC

JPMorgan Asset Management UK Ltd.

FINANCIAL DATA

Technical Assumptions 2013E 2014E 2015E 2016E 2017E

Gold (US$/oz) $1,415 $1,250 $1,300 $1,350 $1,400 NAV SUMMARY AND SENSITIVITY

Silver (US$/oz) $23.49 $20.00 $22.00 $22.50 $23.00

Copper (US$/lb) $3.33 $3.25 $3.10 $3.25 $3.50 Santa Elena; After-Tax (5%)

FX Rate (C$/US$) $1.03 $1.08 $1.08 $1.05 $1.05 La Joya; After-Tax (10%)

Additional Exploration Credit (In Situ)

Financial Forecasts 2013E 2014E 2015E 2016E 2017E Project NAV

Balance Sheet (US$ mln) Corporate Adjustments; After-Tax (10%)

Cash & Equivalents $19.0 $41.8 $54.9 $78.9 $102.9 Working Capital

Working Capital $27.0 $54.6 $68.9 $92.7 $116.1 Cash from Dilution

Long-Term Debt $0.0 $0.0 $0.0 $0.0 $0.0 Long-Term Debt

Income Statement (US$ mln) Corporate NAV

Revenue $55.6 $68.7 $97.3 $100.5 $97.6

Operating Costs $19.9 $32.6 $42.9 $49.7 $49.4 Project NAVPS (C$)

G&A Expense $5.5 $6.0 $6.0 $6.0 $6.0 Corporate NAVPS (C$)

EBITDA $29.2 $28.0 $46.2 $42.7 $40.0 Current Price/Corporate NAVPS

DD&A $6.5 $8.9 $12.8 $14.7 $16.2 Target Price/Corporate NAVPS

Net Income $15.4 $11.3 $21.4 $17.8 $15.1

Cash Flow (US$ mln) 2014E CFPS (US$)

Operating CF - Before W/C $25.6 $28.6 $38.5 $34.5 $31.0 2015E CFPS (US$)

Capital Expenditures ($54.1) ($31.3) ($25.1) ($13.1) ($11.0) EV/2014E CFPS

Proceeds from Equity $2.9 $20.2 $0.4 $1.6 $2.5 EV/2015E CFPS

Proceeds from Debt $0.0 $0.0 $0.0 $0.0 $0.0

FCFE ($8.6) $7.7 $13.9 $22.1 $20.9 CONSENSUS ESTIMATE SUMMARY

Adjusted EPS (US$) $0.13 $0.10 $0.18 $0.15 $0.12 Mean High Low Mean High Low

CFPS (US$) $0.24 $0.25 $0.32 $0.29 $0.25 Consensus 2014E $0.15 $0.25 $0.00 $0.23 $0.31 $0.10

Shares Outstanding 108.4 116.8 118.8 119.9 121.7 Consensus 2015E $0.23 $0.43 $0.06 $0.33 $0.56 $0.13

Operating CFPS Sensitivity (US$) 2014E 2015E 2016E 2017E % EPS % CFPS Consensus Target: $2.39

+10% ∆ in Gold $0.02 $0.03 $0.03 $0.02 NBF/Consensus 2014E -36% 6% NBF/Consensus Target: 36%

+10% ∆ in Silver $0.01 $0.02 $0.02 $0.02 NBF/Consensus 2015E -21% 0% Number of Analysts: 10

+10% ∆ in Copper $0.00 $0.00 $0.00 $0.00

+10% ∆ in MXP/US$ ($0.00) ($0.00) ($0.00) ($0.00) COMPARABLE COMPANIES*

Ticker Price

OPERATIONAL DATA ($) 2014E 2015E 2014E 2015E

Consolidated Production Profile 2013E 2014E 2015E 2016E 2017E Endeavour Mining EDV-T $0.97 5.2x 4.6x 5.6x 4.3x

Gold Production (000 oz) 31 39 48 47 41 Fortuna Silver FVI-T $5.23 11.1x 8.9x 7.8x 5.9x

Silver Production (mln oz) 0.8 1.3 1.9 2.0 2.0 First Majestic FR-T $12.78 12.2x 9.2x 9.3x 7.5x

Copper Production (mln lb) 0.0 0.0 0.0 0.0 0.0 Great Panther GPR-T $1.36 10.5x 6.6x 10.1x -

Silver-Equivalent Production (mln oz) 2.7 3.7 4.8 4.8 4.5 Mandalay Resources MND-T $0.98 4.9x 4.3x 3.6x 3.1x

Silver-Equivalent Sales (mln oz) 2.6 3.7 4.8 4.8 4.5 Primero Mining P-T $8.65 13.0x 11.5x 8.7x 7.3x

Total Cash Cost (US$/oz Ag-Eq) $7.90 $8.75 $9.00 $10.32 $10.88 SantaCruz Silver SCZ-V $1.07 16.2x 9.3x 8.6x 4.3x

Average 10.4x 7.8x 7.7x 5.4x

SilverCrest Mines SVL-T $2.70 10.2x 7.7x 10.6x 6.4x

*CF and EBITDA estimates for comparables based on consensus.

REPORTED RESERVES AND RESOURCES*

Tonnes Ag Pb Zn AgEq

(mln) (mln oz) (mln lb) (mln lb) (mln oz)

Proven and Probable Reserve 8.2 19.7 0.0 0.0 39.6

Measured and Indicated Resource 11.5 29.9 0.0 0.0 57.1

Inferred Resource 35.5 72.0 295.2 0.0 129.7

Total Resource 46.9 101.9 295.2 0.0 186.8

*Current as of December 2012. Presented on 100% basis with Resources inclusive of Reserves.

EPS (US$) CFPS (US$)

$0 $0

EV/CF EV/EBITDA

7.7x 7.6x

$0.28

$0.33

9.0x

$0.25

$0.32

10.2x

$0

$357

1.02x

$3.20

0.84x

$3.03

$3.15

0.86x

$2.98

1.03x

$47

$10

$255

$367

$339

$83

$349

$80

($38)

$0

($38)

$47

$10

$269

Base Case (US$ mln)

Average Strike (C$)

$1.69

$0.00

Shares (mln)

117.7

6.3

0.0

124.0

1.4%

Spot (US$ mln)

1.6

% of Outstanding

7.6%

5.9%

5.3%

1.5%

Shares (mln)

9.0

6.9

6.3

1.7

C$/US$: 1.08 Source: NBF Estimates, Thomson, SilverCrest Mines

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

2 SHANE NAGLE

CORPORATE OVERVIEW SilverCrest Mines Inc. (SVL-T) is a Canadian-based silver/gold producer headquartered in Vancouver, Canada. The company produced 2.66 mln oz of AgEq (779,000 oz Ag & 31,000 oz Au) in 2013 from its 100%-owned Santa Elena mine in Sonora State, Mexico. Santa Elena was purchased in 2005 for US$4 million and brought into production as a 3,000 tpd open pit heap leach operation in 2011. The next stage of production is transition to processing underground ore and the reclaimed heap leach pad once ore from the open pit is exhausted in mid-2014 (construction of the 3,000 tpd CCD/Merrill-Crowe plant is currently 95% complete).

We model 3.7 million oz AgEq production in 2014 at US$8.75/oz compared with company guidance of 3.3 – 3.6 million oz of AgEq (based on Au:Ag ratio of 60.5:1) with cash costs in the range of US$8.50/oz to US$9.25/oz.

FIGURE 1: MAP OF ASSETS

Source: SilverCrest Mines

Stable Financial Position As of year-end, SilverCrest had US$19 million in cash (NBF Estimate), no debt and ~US$26 million of initial capital costs remaining to complete the phase II development at Santa Elena. The company also has a fully undrawn US$40 million revolving credit facility.

We estimate the company’s current cash balance to be approximately US$42 million following the $23 million bought deal financing and US$10 million commitment from Sandstorm Gold Ltd. (SSL-T, Outperform, $6.75 target), which were both announced in Q1 2014. The US$10 million commitment from Sandstorm stems from the previous agreement to extend its 20% interest in future gold production from the underground at Santa Elena for US$450/oz (was US$350/oz). As part of this revised agreement, SilverCrest will continue to deliver 20% of gold production to Sandstorm and will receive US$350/oz until a total of 50,000 oz have been delivered (inclusive of the 18,593 oz delivered at the end of 2013), at which point Sandstorm’s payments will increase to US$450/oz.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 3

Management Has Displayed Ability to Add Value Throughout Development of Santa Elena SilverCrest’s management team has exhibited a solid track record throughout the exploration, development, operation and expansion of Santa Elena. The team regularly has “boots on the ground” and takes a hands-on approach to ensure both development and costs track within budget. The team focuses on keeping projects simple and manageable to avoid large capital blowouts and timing delays which have plagued the mining industry throughout recent years. For example, the initial heap leach project at Santa Elena was built on time and below its budget of US$20 million. The Phase II expansion is expected to be completed around the original budget of US$88 million; however, with a revised development plan and increased underground development (driving the ramp to the deeper higher grade areas of the orebody), we model initial capital costs of ~US$90 million (with US$21 million remaining in 2014).

This prudent approach is supported by the significant equity position management has in the company as management and directors own ~8% of the outstanding shares (the three founders, Mr. Drever, Mr. Magnusson and Mr. Fier, own ~5%).

Santa Elena Expansion Potential Offers Cost-Effective Growth Prospects On Jan. 14, 2014, SilverCrest announced an earn-in agreement whereby the company can earn a 100% interest in the Ermitano property by spending US$75,000 up front, US$50,000 annually and completing US$500,000 of exploration expenditures. The project’s previous owners will also retain a 2% net smelter return (NSR) on future production from the property.

Ermitano is located approximately four kilometres to the southeast of Santa Elena and covers an area of 165 sq. km. A similar low-sulphidation epithermal structure to Santa Elena can be traced for approximately 1,400 m along surface at the property. SilverCrest expects to drill approximately 10-20 holes (2,000-4,000m) in a Phase I program at Ermitano beginning in May 2014 and, depending on success, could warrant expansion of the current 3,000 tpd mill.

The company could also secure some value for La Joya, a silver copper-gold skarn deposit located approximately 75 km southeast of Durango. The project hosts an Inferred mineral resource of 126.7 mln tonnes (at a cut-off grade of 15 g/t AgEq) grading 23.5 g/t Ag, 0.19% Cu and 0.17 g/y Au. An October 2013 preliminary economic assessment (PEA) returned a pre-tax NPV (5%) of US$131 million and pre-tax IRR of 30.5% at US$22.00/oz Ag and US$3.00/lb Cu. The PEA was based on US$141 million initial capex for a 1.8 mln tpa milling operation capable of producing 34.8 mln oz/yr of AgEq production over a nine-year mine life. The company is currently looking to option a portion of the project to a mid-tier mining company and/or private equity group. We currently ascribe ~US$50 million of in-situ value for La Joya (based on ~US$0.50/oz AgEq) as under current market conditions our view is that SilverCrest is better off expanding Santa Elena via extension of the current resource and/or sourcing additional ore feed from nearby deposits such as Ermitano.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

4 SHANE NAGLE

INVESTMENT THESIS

Fully-Funded Development We estimate SilverCrest to have ended the year with US$19 million in cash, no debt and a fully undrawn US$40 million revolving credit facility. Following the recent $23 million bought deal financing and US$10 million contribution from Sandstorm Gold, the company’s current cash balance is approximately US$44 million (NBF Estimate). With US$26 million of remaining capital costs at Santa Elena (costs related to mill construction will largely be completed by mid-year), SilverCrest is fully funded to complete construction of the mill and underground development.

We model a cash balance low of ~US$35 million in Q2 2014 (based on US$1,250/oz gold and US$20.00/oz silver). In addition to its fully undrawn US$40 million credit facility, SilverCrest also has some flexibility in capital spending as millfeed is initially going to be sourced from the open pit and reclaimed heap leach pad, allowing for the option to slow down underground development and exploration to conserve cash (if necessary).

FIGURE 2: CASH BLANCE SET TO GROW FROM LOW WATER MARK IN Q2 2014

($20)

($15)

($10)

($5)

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

Q1/13 Q2/13 Q3/14 Q4/13 Q1/14 Q2/14 Q3/14 Q4/14 Q1/15 Q2/15 Q3/15 Q4/15

So

urc

es/U

se

s o

f C

ash

(U

S$

mln

)

($20)

($15)

($10)

($5)

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

$55

$60

En

din

g C

ash

Bal

an

ce (

US

$ m

ln)

Capex Operating CF Proceeds from Equity

Proceeds from Debt Debt Repayment Cash Balance

Source: NBF Estimates

Room for Organic Growth Once the milling circuit is complete (Q2 2014) and underground development sufficient to provide its maximum capacity of 1,500 tpd (Q1 2015), management can focus on expansion of the existing milling circuit to take advantage of excess capacity in both the crushing and Merrill-Crowe circuits. Based on our estimates, mill throughput could be expanded to approximately 4,000 tpd with little capital expenditure required (~US$5 million for additional capacity in the grinding/leach circuits). Further expansion will depend on the completion of a second adit to the underground; capable of increasing throughput to 3,000 tpd (would require capex of ~US$5 million). The net effect on SilverCrest’s NAV would be an increase of 5% with a 20% increase in operating cash flow as soon as H2 2015.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 5

FIGURE 3: IMPACT OF POTENTIAL EXPANSION OF SANTA ELENA

Mill Throughput (2016+) 2500 tpd 3000 tpd 3500 tpd 4000 tpd 5000 tpd 6000 tpd

Average Annual Ag-Eq Production (mln oz) 4.3 5.1 5.7 6.4 6.6 6.8

Average Cash Cost (US$/oz) $10.72 $10.83 $10.75 $10.84 $10.80 $10.73

2016E EBITDA (US$ mln) $36 $43 $53 $60 $70 $83

EV/2016E EBITDA (x) 8.2x 6.9x 5.6x 5.0x 4.2x 3.5x

2016E EPS (US$) $0.12 $0.15 $0.19 $0.21 $0.27 $0.32

2016E P/E (x) 22.0x 18.2x 14.2x 12.9x 10.1x 8.5x

2016E CFPS (US$) $0.25 $0.29 $0.35 $0.39 $0.46 $0.54

EV/2016E CF (x) 10.8x 9.4x 7.8x 7.0x 5.9x 5.0x

Corporiate NAV (Cdn$) $3.06 $3.15 $3.27 $3.23 $3.50 $3.57

P/NAV (x) 0.88x 0.86x 0.83x 0.84x 0.77x 0.76x

Additional Capital Required (US$ mln) $0 $0 $5 $10 $25 $30 Source: NBF Estimates

In addition to expanding the milling circuit for Santa Elena ore, a larger mill expansion could be utilized in order to process ore from nearby satellite deposits (SilverCrest has already optioned the nearby Ermitano property approximately four kilometres to the southeast). Ermitano covers an area of 165 sq. km and displays similar characteristics to Santa Elena, as the property contains what appears to be a low sulphidation epithermal vein covering a strike length of 1,400 m. SilverCrest will begin a detailed exploration program at Ermitano in 2014 and future success could provide a major impact on production growth. Assuming mill throughout could be doubled (to 6,000 tpd) for approximately US$30 million by 2016 and ore is sourced through an open pit with similar grades/strip ratio to Santa Elena (4.0 mln tonnes grading 45 g/t Ag, 1.6 g/t Au and SR of 4:1), the NAV of the project would increase by more than 15% - with 2016 operating cash flow increasing by more than 75%.

FIGURE 4: OPPORTUNITIES FOR PRODUCTION GROWTH AT SANTA ELENA

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

2013 2014 2015 2016 2017 2018 2019 2020

Ag

-Eq

Pro

du

ctio

n (

mln

oz)

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

Cas

h C

ost

(U

S$

/oz)

Ag-Eq Production (Base Case) Ag-Eq Production (Small Expansion)

Ag-Eq Production (Includes Ermitaño) Cash Cost (Base Case)

Cash Cost (Small Expansion) Cash Cost (Includes Ermitaño)

Source: NBF Estimates

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

6 SHANE NAGLE

Expansion Opportunities and Free Cash Flow Make SVL an Attractive Acquisition Target The short mine life of the original heap leach operation (approximately three years of operation) would have been a deterrent for most acquirers in recent years, and the current transition to an underground mine and milling operation may cause some concerns on operating costs to potential acquirers at the present time. However, with the successful completion of construction, ramp-up of the underground and demonstrating potential for additional low-cost expansion opportunities, SilverCrest could become an acquisition target for several mid-tier precious metal producers in the years to come.

If we base potential takeout metrics on recent acquisitions in the junior gold producer space (averaging US$400/oz Au of reserves for producing assets) or all-in acquisition costs of 85% of spot (based on reserves). Implied takeout metrics support our $3.25 target price, and the scarcity of high-quality single asset precious metal producers makes SilverCrest an attractive target in the current market.

FIGURE 5: IMPLIED ALL-IN COSTS & TAKEOUT METRICS FOR SVL

Assumed Takeout Price, C$/sh $2.75 $3.00 $3.25 $3.50 $3.75

Implied EV (US$ mln) $255 $282 $310 $337 $365

LOM Capex (US$ mln) $83 $83 $83 $83 $83

LOM Opex (Excl. By-Products) (US$ mln) $519 $519 $519 $519 $519

All-in Cost/oz Ag-Eq - Santa Elena; M&I (US$/oz) $15.67 $16.17 $16.68 $17.18 $17.68

% of Spot (%) 72% 74% 76% 79% 81%

All-in Cost/oz Ag-Eq - Santa Elena; Total (US$/oz) $12.88 $13.30 $13.71 $14.12 $14.53

% of Spot (%) 59% 61% 63% 65% 67%

EV/oz Ag-Eq - All Properties; M&I (US$/oz) $4.47 $4.95 $5.43 $5.91 $6.39

EV/oz Ag-Eq - All Properties; Total (US$/oz) $1.36 $1.51 $1.66 $1.81 $1.95

P/NAV (x) 0.87x 0.95x 1.03x 1.11x 1.19x

EV/2015E CF (x) 6.6x 7.3x 8.0x 8.8x 9.5x

EV/2016E CF (x) 7.4x 8.2x 9.0x 9.8x 10.6x

Source: NBF Estimates, SilverCrest Mines

Outperform Rating Supported by Positive Long-Term Outlook Given Strong FCF Growth Based on our estimates, SilverCrest is currently trading at 0.86x NAV and 10.2x EV/2014E CF compared with NBF peers at 1.2x NAV and junior silver producers at 10.4x EV/2014E CF. The company’s H1 2014 results are expected to be messy as Santa Elena transitions from heap leach to milling operation in Q2 and mining moves from the open pit to underground later in the year; however, once this transition is complete we anticipate stable free cash flow and a strong potential for future growth through the development of nearby satellite deposits and mill expansion.

If we focus on SilverCrest’s relative financial position to other junior precious metal companies within our coverage universe, we see the company fares relatively well given the transition to free cash flow in H2 2014.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 7

FIGURE 6: NBF AVAILABLE LIQUIDITY COMPARISON

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SS

L-T

RG

LD

-O

SL

W-T

FN

V-T

SM

F-T

DG

C-T

AE

M-T

K-T

SV

L-T

TM

M-T

YR

I-T

IMG

-T

AS

R-T

LG

C-T

LS

G-T

NG

D-T

OS

K-T

GS

C-T

Cash 2-Year CFO Undrawn Credit 2 year capex 2 year capex & debt repayment

Source: NBF Estimates / Company Reports

Comparing free cash flow yields across our coverage universe, we see that SilverCrest screens among the most favourable and is one of the higher quality single-asset producers.

FIGURE 7: 2014-2016 FREE CASH FLOW YIELDS (NBF COVERAGE UNIVERSE)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

SS

L-T

LSG

-T

K-T

SM

F-T

RG

LD-O

YR

I-T

SV

L-T

DG

C-T

LGC

-T

SLW

-T

FN

V-T

AE

M-T

OS

K-T

IMG

-T

AS

R-T

NG

D-T

GS

C-T

Source: NBF Estimates

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

8 SHANE NAGLE

UPCOMING CATALYSTS / NEWS FLOW 2014 - Completion of mill construction – Q2 2014 - Initial production from underground – Q3 2014

o ~47,000 tonne test stope planned from 525 m level in July - Initial drill results from recently acquired Ermitano project

o 2,000 – 4,000 m program set to get underway by May (pending permits)

2015 - Potential for further expansion of the mill with additional adit to underground workings

Other - Potential sale of JV interest at La Joya - Additional near-mine acquisitions - Potential Index inclusion

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 9

RISKS SilverCrest is exposed to risks that affect all precious metal companies, mainly technical, commodity prices, exchanges rates, input costs and political risks.

Development/Commissioning – As construction of the Santa Elena mill nears completion, most construction risks associated with the project have been mitigated. SilverCrest appears to have successfully completed construction within the initial budget of US$88 million (after having built the heap leach operation in 2010/2011 under budget as well: US$19 million spent vs. initial estimate of US$20 million). The remaining technical risks will be commissioning of the 3,000 tpd mill and completing underground development – approximately 35,000 tonnes of underground ore have been mined throughout development and placed on the pad or stockpiled to date and we also await data from a test stope (15m x 25m x 50m) in July to confirm underground gold/silver grades and mining method.

Financing – With approximately US$42.5 million in cash presently (NBF Estimate), inclusive of the recent closed $23 million equity financing and US$10 million payment from Sandstorm Gold as well as a US$40 million fully-undrawn credit facility, SVL remains in a strong position financially to complete mill development and fund additional exploration. We estimate that SVL could complete construction and operate cash flow positively at silver prices as low as US$12.50/oz (the company could operate at even lower silver prices sub-US$10.00/oz by milling just heap leach material for a period of up to three years). Additional financing risk may arise should the company choose to develop La Joya (September 2013 PEA initial capital of US$141 million including US$17 million of contingencies) or expand the existing Santa Elena mill (~US$20 – US$30 million to double plant capacity).

Commodity/Currency – SilverCrest’s valuation is primarily leveraged to long-term silver/gold prices (following mill construction, revenue will be split ~50/50 between gold/silver). A 10% change in our commodity price assumptions impacts our corporate NAV by approximately 6.7% and our 2014E/2015E CFPS by 5.8% and 7.0%, respectively. Additionally, SilverCrest’s operations reside in Mexico and its corporate headquarters are in Canada. With revenue generated by commodity prices (U.S. dollars) and costs partially in Mexican pesos, Canadian dollars and U.S. dollars, the company will be exposed to exchange rate risks at the operation – a 10% move in the Mexican peso impacts our NAV by ~1%.

Political – Last year the decision was made by the Mexican government to increase corporate tax rates within Mexico to 30% as well as adding a 7.5% tax on EBITDA for all mining operations (plus an additional 0.5% tax on precious metal production). There can be no assurances that future governments will not impose additional royalties/taxes which would adversely impact SilverCrest’s financial projections.

Estimates – We model 3.7 mln oz of AgEq production in 2014 at cash costs of US$8.75/oz – compared with SVL guidance of 3.3 -3.6 mln oz AgEq at cash costs in the range of US$8.50 - US$9.25/oz. We base our estimates on production from the heap leach ceasing in Q2 2014 and production from the mill ramping up to the nameplate 3,000 tpd by the end of Q3 2014. Any delay in initial production from the mil and/or issues with commissioning could impact our 2014 production estimates and near-term cash flow projections.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

10 SHANE NAGLE

VALUATION, TARGET PRICE & RATING

NAV Breakdown Our NAV of $3.15 per fully diluted share is based on a DCF valuation for Santa Elena including production from the mill beginning in late April (fed with both open pit and reclaimed heap leach pad until the end of Q3 2014 with a combination of underground ore and reclaimed heap leach pad thereafter). We use a 5% discount rate (similar to other precious metal producers within our coverage universe) for the project as well as long-term gold/silver prices of US$1,400/oz and US$23.00/oz, respectively.

Our NAV also includes a resource credit for SilverCrest’s La Joya and Cruz de Mayo projects at US$0.50/oz of AgEq (equal to ~US$30/oz of AuEq which compares with other early stage Latin American exploration assets). We currently ascribe no value to the recently acquired Ermitano property as we await results from initial drilling later this year.

The current share price implies a 0.86x multiple to our NAV, with our $3.25 target representing a multiple of 1.03x.

FIGURE 8: SILVERCREST NAV BREAKDOWN

Spot

US$ mln Cdn$ Cdn$

Santa Elena $269 $2.29 $2.28

La Joya $0 $0.00 $0.00

Additional Exploration Credit (In Situ) $80 $0.70 $0.74

Project NAV $349 $2.98 $3.03

Corporate Adjustments ($38) ($0.33) ($0.34)

Working Capital $47 $0.41 $0.42

Cash from Dilution $10 $0.09 $0.09

Long-Term Debt $0 $0.00 $0.00

Corporate NAV $367 $3.15 $3.20

P/NAV 0.86x 0.84x

Fully Financed Shares

Base Case

124.0 Source: NBF Estimates

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 11

Target Price & Rating Our $3.25 target price is derived from a multiple of 8.0x EV/2015E CF (30%) + 1.2x NAV (70%). Our EV/2015E CF multiple is in line with the current peer group average and looks beyond the transition year of 2014 at Santa Elena, while our NAV multiple is in line with metrics used for other junior golf producers within our coverage universe. Our weighted multiple ascribes value to long-term free cash flow growth form Santa Elena by basing a higher portion of our target on the company’s NAV, while allocating a portion of the target on near-term cash flow to reflect the market’s short-term view on late-stage development projects given the potential for cost overruns, commissioning issues and/or potential liquidity constraints.

FIGURE 9: BREAKDOWN OF VALUATION METRIC

Multiple Weight Target

Project NAV $2.98 1.2x -

Coporate Adjustments $0.17 1.0x -

Overall NAV/share $3.15 1.2x 70% $2.60

2015E CFPS $0.32 8.0x EV/CF 30% $0.65

$3.25

Metric

Source: NBF Estimates

We rate the shares as Outperform given the fully-funded status of the phase II expansion and low all-in cash costs of US$13.25/oz AgEq (including sustaining capital costs, corporate G&A, taxes and impact of the Sandstorm Gold stream). We note that once the Santa Elena mill construction is complete and underground access enables more consistent millfeed, Santa Elena could be expanded in order to take advantage of excess capacity in both the crushing and Merrill Crowe circuits. Delineating significant resources at nearby targets (including the recently optioned Ermitano property) could lead to a more significant mill expansion.

FIGURE 10: POTENTIAL GROWTH IN TARGET

$0.10$0.15

$0.10

$0.65

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

Current Target NAV 2015+ Small Expansion (4,000 tpd)

Incl. Ermitaño (6,000 tpd)

+10% ∆ in Gold andSilver Price

Imp

lied

Tar

ge

t P

ric

e (C

dn

$)

Source: NBF Estimates

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

12 SHANE NAGLE

SANTA ELENA

Property Description SilverCrest’s flagship Santa Elena property (100%) covers an area of 3,160 hectares and is located approximately 150 km northeast of Hermosillo in Sonora State, Mexico.

FIGURE 11: LOCATION OF SANTA ELENA

Source: SilverCrest Mines

Historic Work Earliest records of work on the property are from the late 19th to early 20th century when Consolidated Fields operated a mining operation at Santa Elena until the onset of the Mexican Revolution in 1910. During the early 1980s, Tungsteno de Baviacora (Tungsteno) mined 45,000 tonnes grading 3.5 g/t gold and 60 g/t silver from an open cut at Santa Elena. After 2003, Tungsteno periodically surface mined high silica/low fluorine material from Santa Elena and shipped it to the Grupo Mexico smelter in El Tajo, approximately 60 km to the northeast.

An extensive surface/underground mapping and sampling program was carried out in 2004 with a total of 145 channel samples (89 underground and 56 surface) collected and analyzed. On Dec. 8, 2005, SilverCrest entered into an option agreement with Tungsteno to acquire a 100% interest in the Santa Elena property through staged option payments totaling US$5 million over five years. SilverCrest completed payments as per the terms of the agreement in August 2009. The mine and heap leach operation was brought into production in 2011 after spending US$19 million of capital.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 13

Geology & Mineralization Santa Elena is located in the Basin and Range Province (part of the Sonora Desert subprovince) near the Proterozoic rifted continental margin of the North American plate. Subduction of the Farallon Plate beneath the North American Plate during Jurassic time resulted in continental volcanism. In late Jurassic time, a northwest-trending rift basin formed which was the site of sedimentation and felsic and intermediate volcanism.

Locally, the primary rock types are early Tertiary andesite and rhyolite flows which exhibit propylitic to silicic alteration. The main mineralized zone is a cross-cutting structure trending approximately east-west and dipping about 40 -60° to the south. Alteration is widespread and pervasive with significant silicification, kaolinization and chloritization. Gangue minerals consist of quartz, calcite, chlorite and fluorite.

The Santa Elena deposit is considered to be high calcium, low-sulfidation type with replacements, stockworks and hydrothermal breccias similar to other high level low-sulfidation deposits found throughout North and South America. The Santa Elena vein has been drill tested in some spots to a depth of 600 m.

The Santa Elena mine has good potential for additional resources with the deposit open in most directions. The El Cholugo zone is a NW-SE trending offset from the middle of the current pit and the Tortuga zone is a similar offset from the western edge of the current pit. Both of these offsets warrant further exploration as well as extension of the deposit at depth below the current open pit (highlighted in Figures 12 & 13below).

FIGURE 12: SANTA ELENA MINERALIZATION

Source: SilverCrest Mines

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

14 SHANE NAGLE

FIGURE 13: SANTA ELENA LONG SECTION

Source: SilverCrest Mines *Looking North – Ultimate pit and U/G development: Est. Reserves in pink and Est. Resources in grey. Drill holes: red dots 2005-2011, blue 2012-13, green stars Newly Reported

Mining & Processing In 2014, Santa Elena will undergo a transformation from open pit heap leach operation to underground mining and milling via a staged transition that also involves re-treating the current heap leach pad (containing ~4 million tonnes of leached ore grading 67 g/t of silver and 1.5 g/t of gold.

Construction of the conventional 3,000 tpd CCD/Merrill Crowe processing plant is approximately 95% complete with majority of the remaining work consisting of piping and electrical work for the mill components. The mill is scheduled to be in operation by the end of April (an approximate delay of one month form the company’s original guidance due to a delay in the delivery of the ball mill). We model an average of 2.2 million oz/yr of silver and 47,500 oz/yr of gold over a 10.5 year mine life.

We model initial processing of the open pit (approximately 3-5 months of mine life remaining) with reclaimed leach pad ore, then progressive ramp up of underground production as well as reclaimed leach pad ore for the remainder of the mine life beginning in Q3 2014.

Total underground development progressed to 2,265 metres: lateral development of 805 metres and main decline ramp to 1,460 metres in length as of December 31, 2013. A 1,500 metre underground drill program was completed to assist with detailed design of initial production stopes. Mining of these stopes is anticipated in the second half of 2014, with a 15m x 25m x 50m test stope (~47,000 tonnes) planned for July, 2014.

There is sufficient tailings capacity for the current mine plan (dry stack tailings); however, a location has been identified on site for deposition of traditional tailings. Once permitted deposition of tailings at this location will provides sufficient capacity for future expansion and will help reduce operating costs.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 15

Potential for Expansion In 2014, SilverCrest will continue to focus its exploration efforts through organic growth on: (1) surface and underground drilling at Santa Elena for potential resource expansion and further reserve definition, (2) the 30/60 kilometre program surrounding the Santa Elena mine to identify additional resources including the recently optioned Ermitano property (30/60 relates to targets being within 30 km of the mine as top priority and within 60 km from the mine as a secondary priority).

Additionally, SilverCrest has the Cruz de Mayo project, with 16 million oz of AgEq located approximately 35 km from Santa Elena. With the distance to Santa Elena and more complex metallurgy, we don’t incorporate any future production from this asset in our formal valuation. As we noted previously we are more optimistic on the prospects of the nearby Ermitano deposit illustrated in Figure 14 below. Initial drilling at this property is set to get underway in April and future success could lead to expansion of the Santa Elena mill.

FIGURE 14: ERMITANO OFFERS SANTA ELENA LOOK-ALIKE WITHIN FOUR KILOMETRES

Source: SilverCrest Mines

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

16 SHANE NAGLE

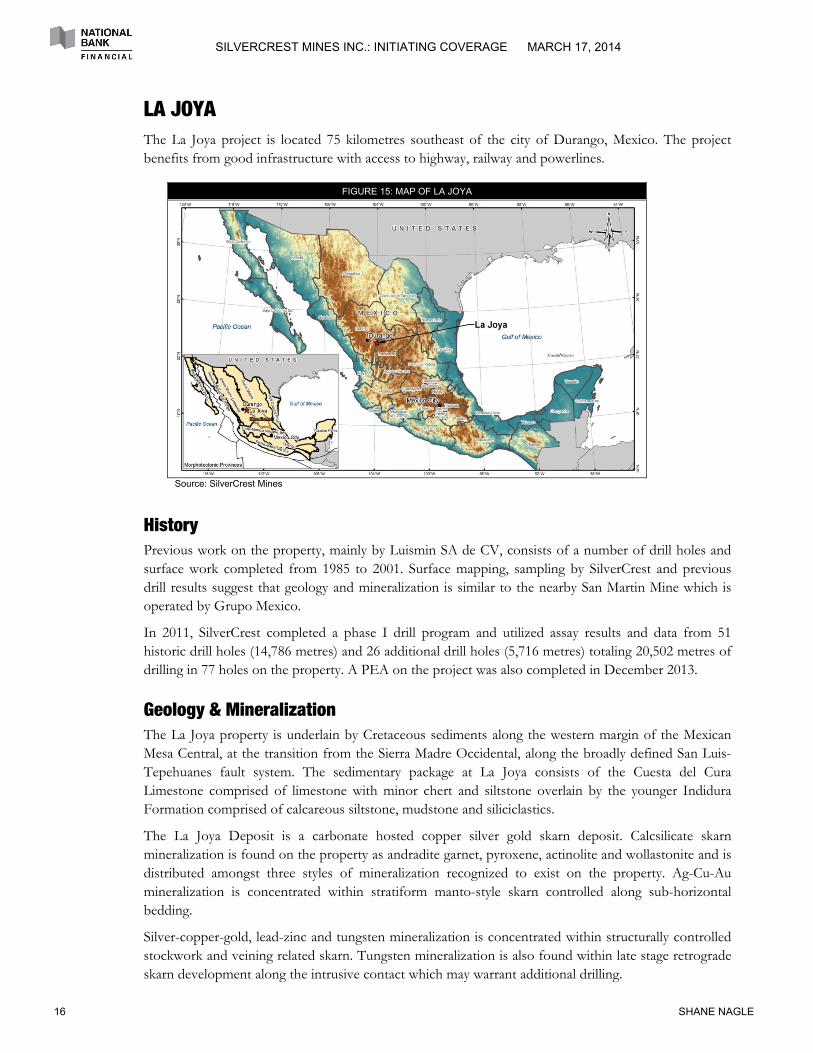

LA JOYA The La Joya project is located 75 kilometres southeast of the city of Durango, Mexico. The project benefits from good infrastructure with access to highway, railway and powerlines.

FIGURE 15: MAP OF LA JOYA

Source: SilverCrest Mines

History Previous work on the property, mainly by Luismin SA de CV, consists of a number of drill holes and surface work completed from 1985 to 2001. Surface mapping, sampling by SilverCrest and previous drill results suggest that geology and mineralization is similar to the nearby San Martin Mine which is operated by Grupo Mexico.

In 2011, SilverCrest completed a phase I drill program and utilized assay results and data from 51 historic drill holes (14,786 metres) and 26 additional drill holes (5,716 metres) totaling 20,502 metres of drilling in 77 holes on the property. A PEA on the project was also completed in December 2013.

Geology & Mineralization The La Joya property is underlain by Cretaceous sediments along the western margin of the Mexican Mesa Central, at the transition from the Sierra Madre Occidental, along the broadly defined San Luis-Tepehuanes fault system. The sedimentary package at La Joya consists of the Cuesta del Cura Limestone comprised of limestone with minor chert and siltstone overlain by the younger Indidura Formation comprised of calcareous siltstone, mudstone and siliciclastics.

The La Joya Deposit is a carbonate hosted copper silver gold skarn deposit. Calcsilicate skarn mineralization is found on the property as andradite garnet, pyroxene, actinolite and wollastonite and is distributed amongst three styles of mineralization recognized to exist on the property. Ag-Cu-Au mineralization is concentrated within stratiform manto-style skarn controlled along sub-horizontal bedding.

Silver-copper-gold, lead-zinc and tungsten mineralization is concentrated within structurally controlled stockwork and veining related skarn. Tungsten mineralization is also found within late stage retrograde skarn development along the intrusive contact which may warrant additional drilling.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 17

FIGURE 16: IMAGE OF LA JOYA HIGHLIGHTING AREAS OF MINERALIZATION

Source: SilverCrest Mines

The updated Inferred mineral resource for La Joya includes 126.7 million tonnes (at a cut-off grade of 15.0 g/t AgEq) grading 23.5 g/t silver, 0.19% copper and 0.17 g/t gold (containing: 198.6 million oz of silver, 533 million lbs of copper and 95,900 oz of gold).

Results of PEA In December 2013, SilverCrest published results from a PEA on La Joya which returned an after-tax NPV(5%) of US$93 million and an IRR of 22% (at US$22.00/oz silver, US$3.00/lb copper and US$1,200/oz gold).

Initial capital cost for the project is estimated to be US$141 million (including US$17 million of contingencies) and production was estimated to be 34.8 million oz AgEq over a nine-year mine life.

Cash operating costs for the first three years averaged US$10.00/oz AgEq (US$13.00/oz AgEq LOM).

FIGURE 17: SUMMARY OF LA JOYA PEA

La Joya PEATonnes of Ore (mln) 127Silver Grade (g/t) 23.50Gold Grade (g/t) 0.17Copper Grade (%) 0.19%

Strip Ratio (Waste:Ore) 2.9:1

Average Annual Ag-Eq Production (mln oz) 34.8Mine Life (years) 9.0

LOM Average Cash Cost (US$/oz) $13

Initial Capex (US$ mln) $141LOM Sustaining Capex (Incl. Closure) (US$ mln) $14

Pre-tax NAV (5%), US$Mln (US$ mln) $133IRR (%) 31%

*PEA based on US$22.00/oz Ag, US$1,200/oz Au, US$3.00/lb Cu Source: SilverCrest Mines / NBF

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

18 SHANE NAGLE

Several opportunities are identified that could significantly enhance the economic return outlined in the PEA, including:

- additional exploration to upgrade/expand the current Inferred resources o Mineralization at La Joya is open in most directions with excellent potential to further increased resource.

- detailed metallurgical test work is required to optimize the flow sheet and identify possibilities to further improve recoveries

- optimization of the mining schedule could potentially provide opportunities for reduction in waste and haulage costs

- an economic analysis for additional products not included in the PEA (including tungsten, molybdenum, lead, zinc and tin) could be carried out

In addition to improving the economics of the current La Joya project, several other targets have been identified on the 10,000 hectare concession that could be evaluated and upgraded for potential exploration drilling.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 19

APPENDIX 1: MANAGEMENT J. Scott Drever: CEO – has 45 years of geological expertise. He has dealt extensively with strategic planning, mergers & acquisitions and operations for international mining corporations. Mr. Drever has served as an Executive Officer and Director of a number of public companies listed on the TSX and the TSX Venture Exchange, including Placer Dome Ltd., Blackdome Mining Corp. and Goldsource Mines Inc.

N. Eric Fier, CPG, P.Eng: President & COO - has over 25 years of international experience in a senior capacity including exploration, acquisition, development and production of numerous mining projects in Chile, Brazil, Honduras, Mexico and Peru. His background includes project evaluation and management, reserve estimation and economic analysis, as well as operations management. Mr. Fier previously served as Chief Geologist with Pegasus Gold Corp., Senior Engineer and Manager with Newmont Mining Corp. and Project Manager with Eldorado Gold Corp.

Barney Magnusson, CA: CFO - has spent more than 30 years in corporate finance and public company management. He has actively been a part of management teams responsible for structuring and building rapidly expanding companies. Mr. Magnusson is a former Senior Officer and Director of six mining companies that developed, constructed or operated eight precious metal mines in North and South America: Dayton Mines Inc. (Chile), High River Gold Mines Ltd. (Manitoba, Canada) and Brohm Resources Inc. (South Dakota, USA).

Brent McFarlane, VP Operations - has over 25 years of diverse experience, including over 10 years in senior management positions in Latin America. He has managed all phases of open pit and underground mining projects and has been instrumental in leading projects through feasibility, construction and into production. Mr. McFarlane previously worked as a project engineer with Pegasus Gold Corp, General Manager with Knight Piesold at Yanacocha and Country Manager for Minefinders Corp. Ltd. in Mexico.

Marcio Fonseca, P.Geo., MSc: VP Corporate Development - has over 20 years experience. He served as Division Director at Macquarie Metals & Energy Capital with focus on equity and debt financing for the mining sector over the last nine years. Prior to that, he held corporate positions in business development, project development, operations and exploration with Vale and Phelps Dodge in Latin America. Mr. Fonseca holds a MSc in Mining Project Appraisal from Imperial College, London in a joint programme between Imperial College Department of Earth Science and Engineering and Imperial College Business School program.

Salvador Aguayo Salinas, Ph.D.: VP Development (Mexico) – holds a Ph. D. in Hydrometallurgy from the Imperial College of Science and Technology (United Kingdom). He previously worked as a professor at the Universidad de Sonora, actively engaged in research in the areas of base metals chemical extraction, recovery and effluent treatments. He has more than 25 years of experience in the areas of leaching and recovery of precious metals. He has been a consultant for several mining companies including Hecla Mining, El Dorado and Grupo Mexico.

Bernard Poznanski, B.Sc., LLB, LLM: Corporate Secretary - has a broad legal background in corporate finance, mergers & acquisitions and securities law. He has acted for a wide variety of companies listed on the Toronto Stock Exchange, the TSX Venture Exchange, the American Stock Exchange and NASDAQ. Mr. Poznanski is one of the founding partners of Koffman, Kalef and currently heads the firm's securities group.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

20 SHANE NAGLE

APPENDIX 2: BOARD OF DIRECTORS SilverCrest has a six-member Board, of which three members are independent. Scott Drever, the current CEO is the Chairman, with other members of management on the board including: Eric Fier, President & COO and Barney Magnusson, CFO. The Board also includes:

George W. Sanders - has a background spanning almost 30 years in mining and exploration finance. He previously worked as a mining analyst, a stockbroker specializing in resource issues and in managing a wide range of exploration finance activities. Mr. Sanders has held positions with Canaccord Capital Corp., Richmont Mines Inc., Consolidated Cinola Mines Ltd. and Shore Gold Inc. He is currently President and Director of Goldcliff Resource Corporation, a gold explorer focused on new discoveries in historic mining districts.

Graham C. Thody, CA - has spent more than 30 years in corporate finance and public company management. His focus has included audits of reporting companies, IPOs, corporate mergers & acquisitions, as well as domestic and international tax matters. Mr. Thody is a former partner of Nemeth Thody Anderson, Chartered Accountants. He is currently a director of several reporting corporations which are involved in mining exploration and development throughout North, Central and South America.

Ross Glanville, P.Eng., MBA, CGA - has over 40 years of resource-related experience in numerous countries, and has been involved in the exploration, financing, development and operation of a number of mines. Mr. Glanville has specialized in valuations, fairness opinions and litigation support, often as expert witness, related to the mining and exploration industry. He has prepared hundreds of valuations and fairness opinions for mining and exploration companies in North America, Africa, Australia, South America, Asia and Europe. Mr. Glanville has formed public companies listed on the Toronto Stock Exchange, the Australian Stock Exchange, NASDAQ and the TSX Venture Exchange, and has served on the Boards of Directors of four companies with producing mines.

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 21

APPENDIX 3: RESERVES & RESOURCES RESERVES & RESOURCES

SANTA ELENA - OPEN PIT

CategoryTonnes(000 t)

Au Grade (g/t)

Ag Grade(g/t)

Cu Grade(%)

Au(000 oz)

Ag(000 oz)

Cu(000 lb)

Ag-Eq(000 oz)

P&P 1,427 1.5 67 0.0% 70 3,064 0 7,308

M&I (Exclusive) 0 0.0 0 0.0% 0 0 0 0

M&I (Inclusive) 1,427 1.5 67 0.0% 70 3,064 0 7,308

Inferred 0 0.0 0 0.0% 0 0 0 0

TOTAL 1,427 1.5 67 0.0% 70 3,064 0 7,308

SANTA ELENA - UNDERGROUND

CategoryTonnes(000 t)

Au Grade (g/t)

Ag Grade(g/t)

Cu Grade(%)

Au(000 oz)

Ag(000 oz)

Cu(000 lb)

Ag-Eq(000 oz)

P&P 3,921 1.6 108 0.0% 198 13,626 0 25,671

M&I (Exclusive) 2,143 1.7 115 0.0% 116 7,916 0 15,003

M&I (Inclusive) 6,063 1.6 111 0.0% 314 21,542 0 40,674

Inferred 1,490 1.5 156 0.0% 72 7,453 0 11,826

TOTAL 7,553 1.6 119 0.0% 386 28,994 0 52,500

SANTA ELENA - LEACH PAD

CategoryTonnes(000 t)

Au Grade (g/t)

Ag Grade(g/t)

Cu Grade(%)

Au(000 oz)

Ag(000 oz)

Cu(000 lb)

Ag-Eq(000 oz)

P&P 2,845 0.7 33 0.0% 59 3,045 0 6,664

M&I (Exclusive) 0 0.0 0 0.0% 0 0 0 0

M&I (Inclusive) 2,845 0.7 33 0.0% 59 3,045 0 6,664

Inferred 0 0.0 0 0.0% 0 0 0 0

TOTAL 2,845 0.7 33 0.0% 59 3,045 0 6,664

CRUZ DE MAYO

CategoryTonnes(000 t)

Au Grade (g/t)

Ag Grade(g/t)

Cu Grade(%)

Au(000 oz)

Ag(000 oz)

Cu(000 lb)

Ag-Eq(000 oz)

P&P 0 0.0 0 0.0% 0 0 0 0

M&I (Exclusive) 1,141 0.1 62 0.0% 2 2,289 0 2,423

M&I (Inclusive) 1,141 0.1 62 0.0% 2 2,289 0 2,423

Inferred 6,065 0.1 67 0.0% 14 12,967 0 13,798

TOTAL 7,206 0.1 66 0.0% 16 15,256 0 16,221

LA JOYA

CategoryTonnes(000 t)

Au Grade (g/t)

Ag Grade(g/t)

Cu Grade(%)

Au(000 oz)

Ag(000 oz)

Cu(000 lb)

Ag-Eq(000 oz)

P&P 0 0.0 0 0.0% 0 0 0 0

M&I (Exclusive) 0 0.0 0 0.0% 0 0 0 0

M&I (Inclusive) 0 0.0 0 0.0% 0 0 0 0

Inferred 27,900 0.3 58 0.5% 251 51,578 295,243 104,092

TOTAL 27,900 0.3 58 0.5% 251 51,578 295,243 104,092

Source: SilverCrest Mines / NBF

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

22 SHANE NAGLE

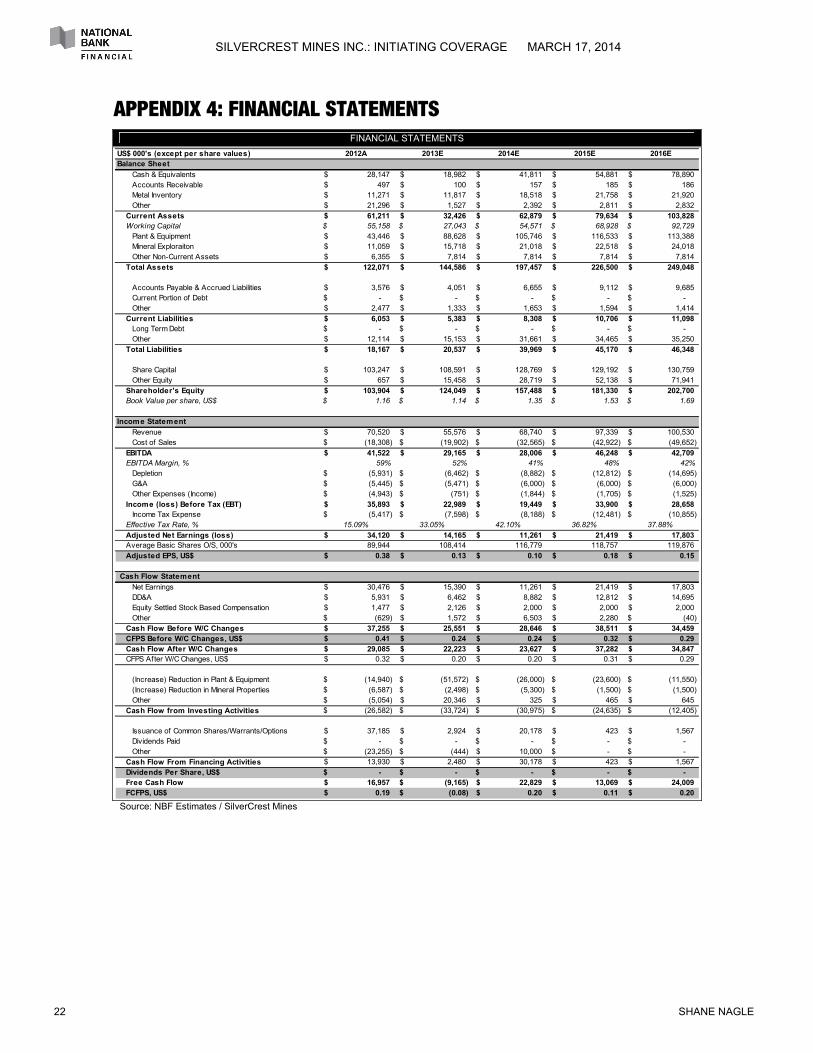

APPENDIX 4: FINANCIAL STATEMENTS FINANCIAL STATEMENTS

US$ 000's (except per share values) 2012A 2013E 2014E 2015E 2016EBalance Sheet

Cash & Equivalents 28,147$ 18,982$ 41,811$ 54,881$ 78,890$ Accounts Receivable 497$ 100$ 157$ 185$ 186$ Metal Inventory 11,271$ 11,817$ 18,518$ 21,758$ 21,920$ Other 21,296$ 1,527$ 2,392$ 2,811$ 2,832$

Current Assets 61,211$ 32,426$ 62,879$ 79,634$ 103,828$ Working Capital 55,158$ 27,043$ 54,571$ 68,928$ 92,729$

Plant & Equipment 43,446$ 88,628$ 105,746$ 116,533$ 113,388$ Mineral Exploraiton 11,059$ 15,718$ 21,018$ 22,518$ 24,018$ Other Non-Current Assets 6,355$ 7,814$ 7,814$ 7,814$ 7,814$

Total Assets 122,071$ 144,586$ 197,457$ 226,500$ 249,048$

Accounts Payable & Accrued Liabilities 3,576$ 4,051$ 6,655$ 9,112$ 9,685$ Current Portion of Debt -$ -$ -$ -$ -$ Other 2,477$ 1,333$ 1,653$ 1,594$ 1,414$

Current Liabilities 6,053$ 5,383$ 8,308$ 10,706$ 11,098$ Long Term Debt -$ -$ -$ -$ -$ Other 12,114$ 15,153$ 31,661$ 34,465$ 35,250$

Total Liabilities 18,167$ 20,537$ 39,969$ 45,170$ 46,348$

Share Capital 103,247$ 108,591$ 128,769$ 129,192$ 130,759$ Other Equity 657$ 15,458$ 28,719$ 52,138$ 71,941$

Shareholder's Equity 103,904$ 124,049$ 157,488$ 181,330$ 202,700$ Book Value per share, US$ 1.16$ 1.14$ 1.35$ 1.53$ 1.69$

Income Statement

Revenue 70,520$ 55,576$ 68,740$ 97,339$ 100,530$ Cost of Sales (18,308)$ (19,902)$ (32,565)$ (42,922)$ (49,652)$

EBITDA 41,522$ 29,165$ 28,006$ 46,248$ 42,709$ EBITDA Margin, % 59% 52% 41% 48% 42%

Depletion (5,931)$ (6,462)$ (8,882)$ (12,812)$ (14,695)$ G&A (5,445)$ (5,471)$ (6,000)$ (6,000)$ (6,000)$ Other Expenses (Income) (4,943)$ (751)$ (1,844)$ (1,705)$ (1,525)$

Income (loss) Before Tax (EBT) 35,893$ 22,989$ 19,449$ 33,900$ 28,658$ Income Tax Expense (5,417)$ (7,598)$ (8,188)$ (12,481)$ (10,855)$

Effective Tax Rate, % 15.09% 33.05% 42.10% 36.82% 37.88%

Adjusted Net Earnings (loss) 34,120$ 14,165$ 11,261$ 21,419$ 17,803$ Average Basic Shares O/S, 000's 89,944 108,414 116,779 118,757 119,876

Adjusted EPS, US$ 0.38$ 0.13$ 0.10$ 0.18$ 0.15$

Cash Flow Statement

Net Earnings 30,476$ 15,390$ 11,261$ 21,419$ 17,803$ DD&A 5,931$ 6,462$ 8,882$ 12,812$ 14,695$ Equity Settled Stock Based Compensation 1,477$ 2,126$ 2,000$ 2,000$ 2,000$ Other (629)$ 1,572$ 6,503$ 2,280$ (40)$

Cash Flow Before W/C Changes 37,255$ 25,551$ 28,646$ 38,511$ 34,459$ CFPS Before W/C Changes, US$ 0.41$ 0.24$ 0.24$ 0.32$ 0.29$ Cash Flow After W/C Changes 29,085$ 22,223$ 23,627$ 37,282$ 34,847$ CFPS After W/C Changes, US$ 0.32$ 0.20$ 0.20$ 0.31$ 0.29$

(Increase) Reduction in Plant & Equipment (14,940)$ (51,572)$ (26,000)$ (23,600)$ (11,550)$ (Increase) Reduction in Mineral Properties (6,587)$ (2,498)$ (5,300)$ (1,500)$ (1,500)$ Other (5,054)$ 20,346$ 325$ 465$ 645$

Cash Flow from Investing Activities (26,582)$ (33,724)$ (30,975)$ (24,635)$ (12,405)$

Issuance of Common Shares/Warrants/Options 37,185$ 2,924$ 20,178$ 423$ 1,567$ Dividends Paid -$ -$ -$ -$ -$ Other (23,255)$ (444)$ 10,000$ -$ -$

Cash Flow From Financing Activities 13,930$ 2,480$ 30,178$ 423$ 1,567$

Dividends Per Share, US$ -$ -$ -$ -$ -$ Free Cash Flow 16,957$ (9,165)$ 22,829$ 13,069$ 24,009$ FCFPS, US$ 0.19$ (0.08)$ 0.20$ 0.11$ 0.20$

Source: NBF Estimates / SilverCrest Mines

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

SHANE NAGLE 23

DISCLOSURES NBF Disclosures, please visit URL: http://www.nbcn.ca/contactus/disclosures.html

For a paper copy of the disclosures, please send a written request (indicating the name and date of the product) to:

National Bank Financial (Research Department) c/o Research Publications 130 King Street West 4th Floor Podium Toronto, Ontario, Canada M5X 1J9

SILVERCREST MINES INC.: INITIATING COVERAGE MARCH 17, 2014

24 SHANE NAGLE

NOTES

�����������

����������������� ������ �

����������� �� ��� ���������������������������� �� ��� ������������������������ �� ��� ���

�� �����

������������� �� ��� ����������������� ����!��� �� ��� ��"����������#����������!� �� ��� ��$

���������������������������%�������&������� $� ��� '$�����������(�����# �� �� ��� �$��

�� ��� ��������&��������� �� ��� �'�

���������� �����������)���%���*� � �� ��� ��"����������&���� �+����� �� ��� ��'����������,��-�.���- �� ��� ��'

�������� ��������)������/������� $� ��� ''"���������#�-� ���������� $� ��� �$�

� ����� �������������+�1*��������� $� ��� "���� ������������������������

)�� 2#�!�1�)�������� � $� ��� "��$��������������������������

��0�)��������� � $� ��� '$�����������������

�����������-����� $� ��� "�����������������

��������#������� $� ��� $�����������

������ ������������������� ��

#!���+���� $� ��� '"�'���������)�����+����� $� ��� '$������������3��������������� �� ��� �$�$

�����

�������������� 4��-�%� ��� �� ��� ���$���������+����5������ �� ��� ���"���������#�!��6���0� �� �� ��� �$��

!"��#������$��%�&�'$����(�'�&��' &���)���� �" '�� $����������# ���&�7�� �" �2��$'���������8�����,�-��� �" '��2$$����������������%��� �" �2��'�

�����6���� �� �" '�� $�'$���������# ���&�7�� �" �2��$'���������8�����,�-��� �" '��2$$����������������%��� �" �2��'�

����#��'�&���$��%�&�'$����(&������ ��)������ �" '�� $��'����������#���%���- �" '�� $�'������������0�%��9�� �" � ��$$

�������� ��� ����� ��� ���� ����� �� �� ������ � ������ ����� ���������� �� �������� ��� �� ���������� ����� ����� �������� ���������� �������� ���� ���� ����� ��� ������� �������� ��� ��� ��� ��������� �� �� ������ �� �� �������� ��� �������� �!���������� ����� ���� ��� �������� ��� �������������� �� ����� ����� ����� ��� ��� ��� �� �� �������� �� � ���� ������� �� ����� �� ��� �� ���� ��� �� ���������������� ���������� ������� � � �� ����� ��� �������" ��� �� � ��� �� ����������� ��� ������ �� ��� ����������������� ������ ������ �� ���� � ������������ ��� ��� ����� ��� ������� ���#�� ��� ���� ���" ���� ����" ���������������" ���� �����"��� ���� � �������� �� ��� �� ���������������� ������ ���������� ��� ����� ���#�� ����� ������� �� ������� ���� ���� �� ���� �� ��� ���������� �� ������������ $�%� ���������& �� %� ������� �$%'� �����" �� ��������� �� ��� ����" � ���� �������������� ��� ��� ������� �� ���� ������" ���(� � �� ��� ����� ��� ��� ������'��$�%� ������������ �� ���� � ������ ����� �� ��� �� ����� ��� ����� ������ ������ �� �� ���� ����� ���%� ������� �$%'� ��������� ��������� ��� �� ������� �� ������� �� �� ����" �� ������� ����������� �� ��������� �� �������� �� �� ������������������� ������ ��� �����������" �������� �� �� ������� �������� �� �� �� �������� ��������� �� �� � ��� ��� ����� �!����� ������ �� �������� ��� ����� ����

��)�(��� ���$�(�$�� ������������*�' $�"�$"��)����0������� �" '�� $$�����������0��� ��-���� �" '�� $�

����� ������+� ��

�'�,�������� "�'���)��������� �!-� �� ��� �'���������)������/��� �� ��� �$�$

����� �*��&����'���'( +��9������� �� ��� �'$������������0����%����- �� ��� ��'

��� ������������ ������������� ��

����� �+����!��� �� ��� ��"���������������,� �� ��� ����

��������������

+�������- � �� ��� ��"����������4��-�&�� � �� ��� �$"�

+��3��)������ �� ��� �������������%��� ���,�9 ��0 �� ��� ��

�����������:���� �� $�� ���$

����������

���������0� �� $�� ������������&�6����%���- �� $�� ���'

���3���������� �� ��� �$�����������;�!���,��� �� ��� ������������%�����������<=��� �� ��� �$��

��� ����������������3���������� �� ��� �$��������������-���0%����0� �� $�� �������������;�!���,��� �� ��� ������������%�����������<=��� �� ��� �$��

,����#-��>����� $� ��� '$����������/��!���0�����9 �� $� �' ��'�

�-#���'��(�", �� ��� �$''����������������

'�#(���� !",� �� ��� ��"���������������������

�'��'��#"�-'�& �� ��� ��"��������� ����! ��

�'����.#%'� �� �" '�"��������"������ �������

���������� ������������������ ��������� ����������� ��������������

���������� ��������� ��� ������ ���������

����������� ��� �� �������� �� ���� ���E��������! �. 1-� G ���) �� ��� )�# ���-�� �.F �9�#��-���������#�G������G��)-��)-����������- :���� 5�A*��>�5*�����"��!���9�����!9����37 1���H ��������'���1���H��E�F�����'��(���

��� �� J B� �#����� 7�����# �##�) �� �� �: ����!�J ����! �� B� �#��� 2����)� �� G��!J ��)�� � �# B� �#��� 2����)� �� ���;���� ��

J 0 �� ;�� �����! � �# 9?)-����J ��)�� � �# B�!�#��. �##�) �� ��J�5$

J �������� 9?)-����J 1������ ���)> 9?)-����

����������������������������� ����

���� ����9�#��-����������-G����5�A*��>�5*�����1���H ����������

Baie-Comeau • 337, boulevard Lasalle, Baie-Comeau QC, G4Z 2Z1 • 418.296.8838

Barrie•126 Collier St., Barrie QC, L4M 1H4 • 418.296.8838

Beauce•11505, 1re Ave. est, Bureau 100 St-Georges, Beauce QC, G5Y 7X3 • 418.227.0121

Berthierville•779, rue Notre-Dame, Berthierville QC, J0K 1A0 • 450.836.2727

Bin-Scarth • 24 Binscarth Rd ,Toronto ON, M4W 1Y1 • 450.836.2727

Brampton • 10520 Binscarth Rd, Brampton ON, L6R 2S3 • 905.456.1515

Brandon • 633-C, 18th Street, Brandon, MB, R7A 5B3 • 204.571.3200

Burnaby • 218-4211 Kingway St., Burnaby BC, V5H 1Z9 • 604.541.8500

Calgary • Suite 2800, 450-1 St SW, Calgary AB, T2P 5H1 • 403.531-8401

Calgary • Suite 1100, 10655 Southport Rd., Southland Tower, Calgary AB, T2W 4Y1 • 403.301-4859

Charlottetown • 310-119 Kent St., BDC Tower, Campbellville PEI, C1A 1N3 • 905.569.8813

Chatham • 380 St. Clair St., Chatham ON, N7L 3K2 • 519.351.7645

Chicoutimi • 1180, boulevard, Talbot Suite 201, Chicoutimi QC, G7H 4B6 • 418.549.8888

DIX30 • 9160 boulevard Leduc, 7ième étage, Brossard, QC, J4Y 0E3 • 450.462.2552

Drumheller • 356 Centre St., Drumheller AB, T0J 0Y0 • 403.823.6857

Drummondville • 150, rue Marchand, Bureau 401, Drummondville QC, J2C 4N1 • 819.477.5024

Duncan • 206-2763, Beverly St., Duncan BC, V9L 6X2 • 250.715.3050

Edmonton • Manulife Place, 10180-101st St., Suite 3500, Edmonton AB, T5J 3S4 • 780.412.6600

Edmonton • TD Tower, 10088-102 Ave., Suite 903, Edmonton AB, T5J 2Z1 • 780.412.4455

Fredericton • 551 King St., Suite B, Fredericton NB, E3B 1E7 • 506.453.9040

Gatineau • 920, St-Joseph, Bureau 100, Gatineau QC, J8Z 1S9 • 819.770.5337

Granby • 150, rue St-Jacques Bureau 202, Granby QC, J2G 8V6 • 450.378.0442

Grand-Mère • 602, 6e Ave., Grand-Mère QC, G9T 2H5 • 819.538.8628

Halifax • Purdy’s Wharf Tower II, 1969 Upper Water St., Suite 1601, Halifax NS, B3J 3R7 • 902.496.7700

Halifax • 5670 Spring Garden Rd., Suite 901, Halifax NS, B3J 1H6 • 902.425.1283

Halifax • 1741 Brunswick St., Suite 120B, Halifax NS, B3J 3X8 • 902.425.2318

Joliette • 40, rue Gauthier sud, Bureau 3500, Joliette QC, J6E 4J4 • 450.760.9595

Kelowna • 1632 Dickson Ave., Suite 500, Kelowna BC, V1Y 7T2 • 250.717.5510

Kentville • 402 Main St., Kentville NS, B4N 3X7 • 902.679.0077

La Pocatière • 608 C, 4e Ave., La Pocatière QC, G0R 1Z0 • 418.856.4566

Lac Mégantic • 4947 Boulevard des Vétérans, Lac Mégantic, QC, G6B 2G4 • 819.583.6035

L’Assomption • 821, L’Ange Gardien Nord, Bureau 107A, L’Assomption QC, J5W 1P5 • 450.589.1138

Laval • 2500, boulevard Daniel-Johnson, Bureau 610, Laval QC, H7T 2P6 • 450.686.5700

Lethbridge • 404-6th St. South, Lethbridge AB, T1J 2C9 • 403.388.1900

London • City Centre 802-380 Wellington Ave., London ON, N6B 5B5 • 519.646.5711

London • 333 Dufferin Ave., London ON, N6B 1Z3 • 519.439.6228

Mississauga • 350 Burnhamthorpe Rd. W., Suite 603 Mississauga ON, L5B 3J1 • 905.272.2799

Mississauga • 295 Eglinton Ave. E., Delaware Sq., Mississauga ON, L4Z 3K6 • 905.507-4883

Moncton • 735 Main St., Suite 300, Moncton NB, E1C 1E5 • 506.857.9926

Montréal • 1, Place Ville-Marie, Bureau 1805, Montréal QC, H3B 4A9 • 514.879.5200 514.871.9000

Montréal • 1, Place Ville-Marie, Bureau 2201, Montréal QC, H3B 3M4 • 514.879.2509

Montréal • Édifice Sun Life, 1155, rue Metcalfe, Montréal QC, H3B 4S9 • 514.879.2222

Montréal • Acadie 9001, boul. de l’Acadie, Bureau 801, Montréal QC, H4N 3H5 • 514.389.5506

Montréal • 600 de la Gauchetière Ouest, Niveau A, Montréal QC, H3B 4L2 • 514.871.5021

Mont Laurier • 906, Albiny-Paquette, Mont Laurier QC, J9L 1L4 • 819.623.6002

Mont-St-Hilaire • 436, boul. Sir Wilfrid-Laurier, bureau 100, Mont-St-Hilaire QC, J3H 3N9 • 450.467.4770

Nanaimo • 75 Commercial Street, Nanaïmo, BC, V9R 5G3 • 250.751.1111

North Bay • 680 Cassells St., Suite 101, North Bay ON, P1B 4A2 • 705.476.6360

Oakville • 105 Robinson St., Oakville ON, L6J 1G1 • 905.842.1925

Ottawa • MetLife Centre, 50 O’Connor St., Suite 1602, Ottawa ON, K1P 6L2 • 613.236.0103

Outremont • 1160, Laurier Ouest #1, Outremont QC, H2V 2L5 • 514.276.3532

Penticton • 305-399 Main St., City Center Building, Penticton BC, V2A 5B7 • 250.487.2600

Plessisville • 1719 rue St Calixte, Plessisville, QC, G6L 1R2 • 819.362.6000

Pointe-Claire • 1, rue Holiday, Tour est Bureau 145, Pointe-Claire QC, H9R 5N3 • 514.426.2522

Québec • 900, boul. René Lévesque est, Bureau 640, Québec QC, G1R 2B5 • 418.649.2525

Québec • 3 Edifice Delta 3 2875, boul. Laurier, Bureau 700, Québec QC, G1V 2M2 • 418.651.0680

Red Deer • 200-4719 48th Ave., Red Deer AB, T4N 3T1 • 403.348.2600

Regina • 1770-1881 Scarth St., 17th Floor, Regina SK, S4P 4K9 • 306.781.0500

Repentigny • 534, rue Notre-Dame, Bureau 201, Repentigny QC, J6A 2T8 • 450.582.7001

Richmond • 135-8010 Saba Rd., Richmond BC, V6Y 4B2 • 604.658.8050

Richmond Hill • 500 Highway 7 East, Gr. Floor, Richmond Hill ON, L4B 1J1 • 905.477.2002

Rimouski • 121, boul René-Lepage Est, Bureau 100, Rimouski QC, G5L 1P1 • 418.721.6767

Rivière-du-Loup • 10, rue Beaubien, Rivière-du-Loup QC, G5R 1H7 • 418.867.7900

Rosemère • 218, boul. Curé-Labelle, Rosemère QC, J7A 2H4 • 450.437.3456

Rouyn-Noranda • 74, Ave. Principale, Rouyn-Noranda QC, J9X 4P2 • 819.762.4347

Saint John • 72 Prince William St., Saint John NB, E2L 2B1 • 506.642.1740

Sainte-Marie-de-Beauce • 100-249, Du Collège, Ste-Marie-de-Beauce QC, E2L 2B1 • 418.387.8155

Saint-Félicien • 1120, boul. Sacré-Coeur, St-Félicien QC, G8K 1P7 • 418.679.2684

Saint-Jérôme • 100-265, rue St-George, St-Jérôme QC, J7Z 5A1 • 450.569.8383

Saint-Nicolas • 425, rue des Chutes, Bureau 100, St-Nicolas QC, G7A 1E7 • 450.261.5268

Saskatoon • 1220-8th St. East, Saskatoon SK, S7H 0S6 • 306.657.3465

Saskatoon • 410-22nd St. East, Suite 1360, Saskatoon SK, S7K 5T6 • 306.657.4400

Sept-Iles • 1005, boul Laure, Suite 305, Sept-Iles QC, G4R 4S6 • 418.962.9154

Sherbrooke • 1802, rue King Ouest, Suite 200, Sherbrooke QC J1J 0A2 • 819.566.7212

Sidney • 2537 Beacon Ave., Suite 205, Sidney BC, V8L 1Y3 • 250.657.2200

Sorel • 26, Pl. Charles-de-Montmagny, Sorel-Tracy QC, J3P 7E3 • 450.743.8474

St. Catharines • 40 King St., St. Catharines ON, L2R 3H4 • 905.641.1221

St-Jean-sur-Richelieu • 383, Boul du Séminaire N., Bu.224, St Jean sur Richelieu QC, J3B 8C5 • 450.349.7777

St-Hyacinthe • 1355, rue Johnson Ouest, Suite 4100, St-Hyacinthe QC, J2S 8W7 • 450.774.5354

Steinbach • 102-344 Main St., Steinbach MB, R5G 1Z1 • 204.320.9536

Sudbury • 10 Elm St., 5th Floor, Sudbury ON, P3C 1S8 • 705.671.1160

Swift Current • 202-406 Cheadle St. W, Swift Current SK, S9H 0B6 • 306.778.4770

Thedford-Mines • 222 boul. Frontenac Ouest, Thedford-Mines QC, G6G 6N7 • 418.338.6183

Thunder Bay • Hydro Blg 34 Cumberland St. N., 7th FI, Thunder Bay, ON P7A 4L3 • 807.683.1777

Toronto • 130 King St. W., 4th Floor Podium, Toronto ON, M5X 1J9 • 416.869.3707

Toronto • 130 King St. W., Suite 3200, Toronto ON, M5X 1J9 • 416.869.3707

Trois-Rivières • 7200, rue Marion, Trois-Rivières QC, G9A 0A5 • 819.379.0000

Valleyfield • 1356, boul. Monseigneur-Langlois, Valleyfield, QC, J6S 1E3 • 450.370.4656

Val d’Or • 840, 3e Ave., Val d’Or QC, J9P 1T1 • 819.824.3687

Vancouver • Park Place, 666 Burrard St., Suite 3300, Vancouver BC, V6C 2X8 • 604.623.6777

Vancouver • 550 Burrard St., Suite 1028, Vancouver BC, V6C 2B5 • 604.686.6371

Vancouver • 1333 W. Broadway Ave., Suite 1488, Vancouver BC, V6H 4C1 • 604.738.5655

Vernon • 3100-30th Ave., Suite 101, Vernon BC, V1T 2C2 • 250.260.4580

Victoria • 700-737 Yates St., Victoria BC, V8W 1L6 • 250.953.8400

Victoria Fort • 1480 Fort St., Victoria BC, V8S 1Z5 • 250.953.8400

Victoriaville • 650, rue Jutras Est, Bureau 150, Victoriaville QC, G6S 1E1 • 819.758.3191

Waterloo • Allen Square 180 King St. S., Suite 340, Waterloo, ON, N2J 1P8 • 519.742.9991

West Vancouver • 202-545, Clyde Ave., West Vancouver BC, V7T 1C5 • 604.925.5640

White Rock • 2121 160th St., Surrey BC, V3S 9N6 • 604.541.4925

Willowdale • 3640 Victoria Park Ave., 3rd Floor, Willowdale ON, M2H 3B2 • 416.756.4016

Windsor • 1 Riverside Drive W., Suite 600, Windsor ON, N9A 5K3 • 519.258.5810

Winnipeg • 400-200 Waterfront Drive, Winnipeg MB, R3B 3P1 • 204.925.2250

Yorkton • 89 Broadway St. W., Yorkton SK, S3N 0L9 • 306.782.6450

![OneCNC Solid Design AA Mill Express Mill …OneCNC Solid Design AA Mill Express Mill Advantage Design 280,000B (ü%l]) 280,000B 480,000B 28 Milling & Multi Axis Mill 800,000B Mill](https://img.dokumen.tips/doc/110x75/5f867f1cac5a475cf73aa2f7/onecnc-solid-design-aa-mill-express-mill-onecnc-solid-design-aa-mill-express-mill.jpg)