Embed Size (px)

Citation preview

Sally OdlandScarsdale High SchoolTeachers WorkshopNovember 2013

Supply/Price Dynamics of Unconventional Petroleum Production

Oil prices more than tripled in the last decade, yet crude oil supply increased by only 7%

Old Price Norm

New PriceNorm

Unconventional Oil from Texas and N Dakota has offset other US decline

Horizontal Drilling and Hydraulic Fracturing is the only reason that both US oil & gas

production are not in decline

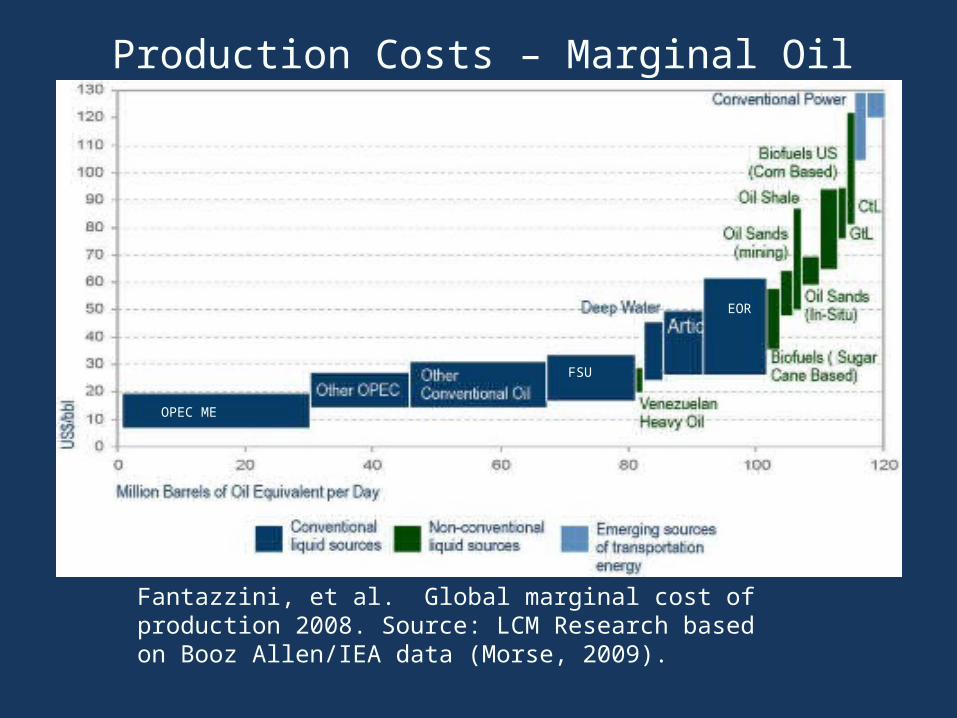

Production Costs – Marginal Oil Supply

Fantazzini, et al. Global marginal cost of production 2008. Source: LCM Research based on Booz Allen/IEA data (Morse, 2009).

OPEC ME

FSU

EOR

Shale and tight reservoir plays are ‘high-hanging fruit’•Disseminated oil and gas, i.e. not concentrated

•Low permeability - the petroleum doesn’t flow

•Rock must be ‘stimulated’ to release the HCs

•Well production rates are much lower than conventional reservoirs

•Ultimate recovery much lower than conventional reservoirs (2-8% v 35-40% of original oil in place)

•Decline rates are much steeper

Total recovery is smaller and decline rate faster in unconventional oil fields

Bakken Oil Well and Field Decline Rates

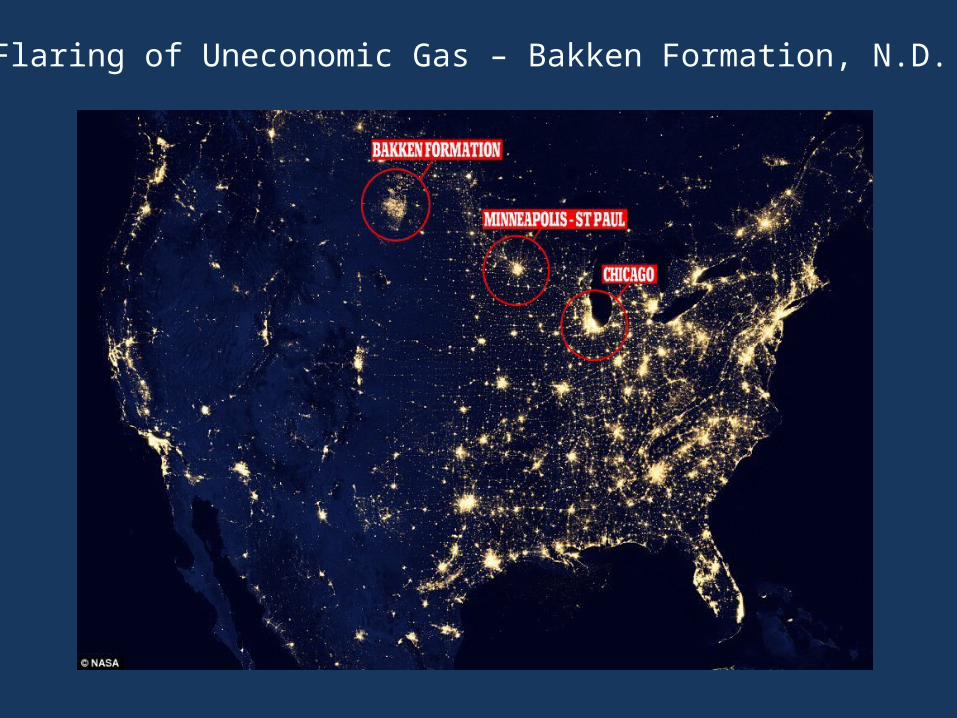

Flaring of Uneconomic Gas – Bakken Formation, N.D.

Market Dynamics

•Dry gas drilling in US largely uneconomic at recent prices of $2 - $4 MMbtu. Glut keeps price down.

•Rigs switching to oil and ‘wet gas’ with NGLs

•Power plants switch from coal to gas around $4

•US nat gas prices (<$4) is less than ½ Europe’s price ($10-$12) and ¼ of Asia’s ($15-18)

•Pressure for LNG export terminals

Supply/Demand Balance is Resolved by Price•Price is set at the margins

•FLOOR: Cost to produce the next barrel or mcf Oil: Deepwater ? Tar Sands ? Shale Oil? Gas: Horizontal drilling, fracking, water, regs

•CEILING: Price the marginal consumer is willing to pay for an additional barrel.

•What price will the Seller/Exporter accept? Can decide to leave in ground for the future

Conclusion:

We are navigating a narrow Supply/Demand ledge