Embed Size (px)

Citation preview

Ohi

o T

ax

Workshop O

Sales Tax on Employment

Services

Thursday, January 27, 2011 3:00 p.m. to 4:00 p.m.

Biographical Information

Anthony L. Ehler, Partner, Vorys, Sater, Seymour and Pease LLP 52 East Gay Street, Columbus, OH 43215 [email protected] 614.464.8282

Mr. Ehler is a partner in the Vorys Columbus office and leads the firm's state and local tax group. He advises clients regarding all aspects of state and local taxation, including compliance issues, planning opportunities, audit preparation and defense, negotiated settlements with tax authorities, and litigation. Within the field of state and local tax, he focuses on sales and use taxes, motor fuel excise tax, real and personal property tax and commercial activity tax. He is also a registered lobbyist and regularly assists clients in achieving desired results through legislative or administrative efforts. Career highlights include: Serving as a speaker at and/or on the organizing committee for the Annual Ohio Tax Conference for each of the previous 20 years Serving as Chairman of the Ohio State Bar Association Taxation Committee Serving as Chairman of the Columbus Bar Association State Tax Committee Appointment by the Speaker of the House to the Committee To Study Motor Fuel Tax Funding of Highways Serving as Member of the Board for Ohio Public Expenditure Council Mr. Ehler is a member of the Ohio State Bar Association and the Institute for Professionals in Taxation. Mr. Ehler has presented a wide variety of state and local tax topics to the Ohio Society of Certified Public Accountants, the Ohio State Bar Association, the American Petroleum Institute, the Ohio Manufacturers Association, the Ohio Petroleum Marketers and Convenience Store Association, the Institute for Professionals in Taxation and the Ohio Chamber of Commerce. Mr. Ehler received his J.D. from Wake Forest University School of Law where he was a member of the Moot Court Board and his B.A. from the University of Notre Dame.

Dara L. Greene, Attorney, Ohio Department of Taxation 30 E. Broad Street, Columbus, OH 43215

[email protected] 614.466.6750

Dara has served as a hearing officer within the Tax Appeals Division since April 2005. Her current duties include conducting administrative hearings within the department and issuing the Tax Commissioner’s final determinations in Sales and Use Tax matters. Her duties also include assisting with legislative analysis and drafting information releases for the department. Dara received her Juris Doctorate degree from The Ohio State University in 1999 and her B.A. in English and Anthropology from the University of Rhode Island in 1994. In addition, she received her L.LM in Taxation from Capital University in 2000.

Sales Tax on EmploymentSales Tax on Employment Services

20th Annual Ohio Tax ConferenceWorkshop Op

Thursday, January 27, 2011

Sales Tax on Employment ServicesSales Tax on Employment Services

“Employment service” is the providing or supplying of personnel, on a temporary or l b i f k dlong-term basis, to perform work under another's supervision or control, when the personnel receive their wages salary orpersonnel receive their wages, salary, or other compensation from the supplier or provider of the employment service or from a thi d t th t id d li d ththird party that provided or supplied the personnel to the provider or supplier.

R C 5739 01(JJ)R.C.5739.01(JJ)

Sales Tax on Employment ServicesSales Tax on Employment Services

“Employment Service” does not include:

(1) Acting as a contractor or subcontractor, where the personnel performing the work are p p gnot under the direct control of the purchaser.

R.C. 57390.1 (JJ)

Sales Tax on Employment ServicesSales Tax on Employment Services

“Employment Service” does not include:

(2) Medical and health care services.

R.C. 57390.1 (JJ)

Sales Tax on Employment ServicesSales Tax on Employment Services

“Employment Service” does not include:

(3) Supplying personnel to a purchaser pursuant to a contract of at least one year between the service provider and thebetween the service provider and the purchaser that specifies that each employee covered under the contract is assigned to the

h t b ipurchaser on a permanent basis.

R C 57390 1 (JJ)R.C. 57390.1 (JJ)

Sales Tax on Employment ServicesSales Tax on Employment Services

“Employment Service” does not include:

(4) Transactions between members of an affiliated group, as defined in division (B)(3)(e) g p ( )( )( )of this section.

R.C. 57390.1 (JJ)

Sales Tax on Employment ServicesSales Tax on Employment Services

“Employment Service” does not include:Employment Service does not include:(5) Transactions where the personnel so provided or supplied by a provider or supplier yto a purchaser of an employment service are then provided or supplied by that purchaser to a third party as an employment service excepta third party as an employment service, except “employment service” does include the transaction between that purchaser and the pthird party. R.C. 57390.1 (JJ)

Sales Tax on Employment ServicesSales Tax on Employment Services

Enactments and Amendments

Am.Sub.H.B. No. 904 – effective January 1, 1993Am.Sub.S.B. 122 – effective June 30, 1993Am.Sub.H.B. 152 – effective July 1, 1993ySub. H.B. 293 – effective January 1, 2007

Sales Tax on Employment ServicesSales Tax on Employment Services

IssuesIssuesSale for resale exemption

Manufacturing exemption

Outsourced Function & Deliverable

Long Term Assignment

Sales Tax on Employment ServicesSales Tax on Employment Services

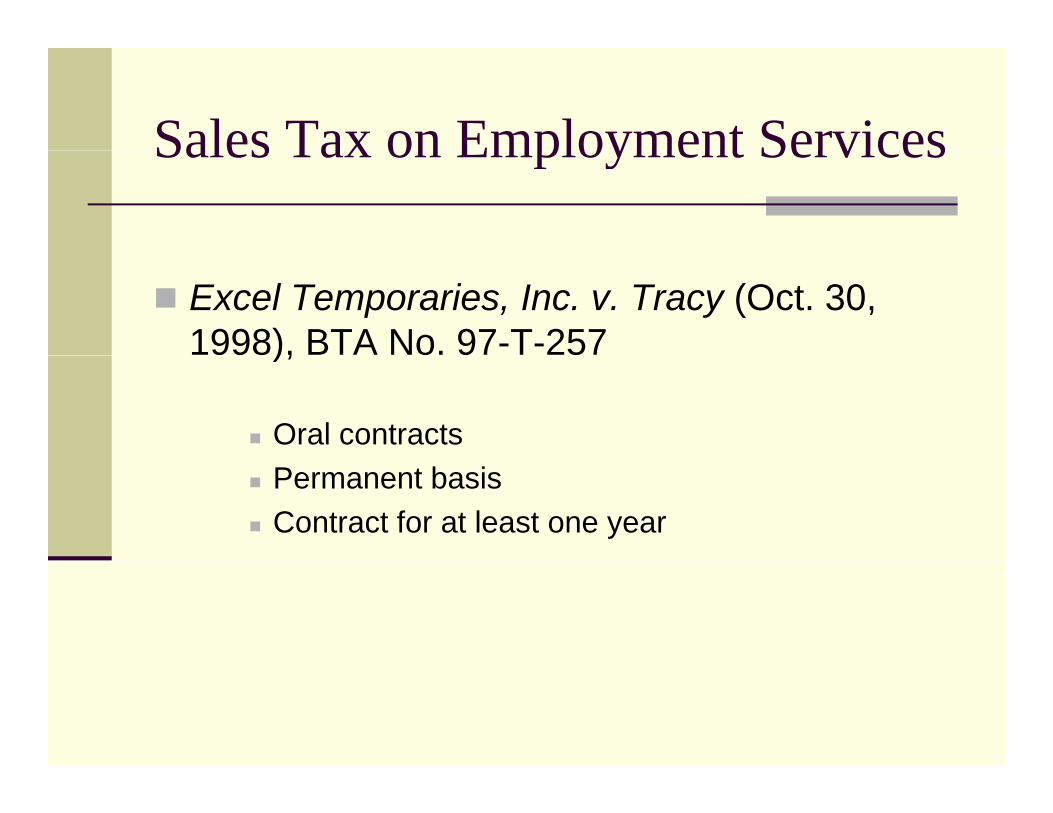

Excel Temporaries, Inc. v. Tracy (Oct. 30, 1998), BTA No. 97-T-257),

Oral contractsPermanent basisContract for at least one year

Sales Tax on Employment ServicesSales Tax on Employment Services

Advantage Services v. Tracy (Oct. 30, 1998), BTA No. 95-T-1391

Oral contractsPermanent basisParol evidence

Sales Tax on Employment ServicesSales Tax on Employment Services

Bellemar Parts Industries, Inc. v. Tracy(2000), 88 Ohio St.3d 351, 725 N.E.2d 1132( ), ,

Sale for resale exemptionpManufacturing exemptionTransfer of the benefit of the service

Sales Tax on Employment ServicesSales Tax on Employment Services

Labor Pool of Cincinnati, Inc. and Employment Service, Inc. v. Tracy (Apr. 14, p y , y ( p ,2000), B.T.A. Nos. 98-A-491 and 98-A-791

Oral contractsContracts for at least one year

Sales Tax on Employment ServicesSales Tax on Employment Services

Success Employment Services, Inc. v. Tracy(Apr. 14, 2000), BTA No. 98-A-489( p , ),

Employees supplied on permanent basisp y pp pSeparation of temporary and permanent employees

Sales Tax on Employment ServicesSales Tax on Employment Services

E.T.S. Inc. v. Tracy (Apr. 14, 2000), BTA No. 97-S-1613

Oral contractsControl and supervision of employees

Sales Tax on Employment ServicesSales Tax on Employment Services

B.J. Alan Company v. Tracy (Mar. 1, 2002), BTA No. 99-N-196

Oral contractsTermination clauses

Sales Tax on Employment ServicesSales Tax on Employment Services

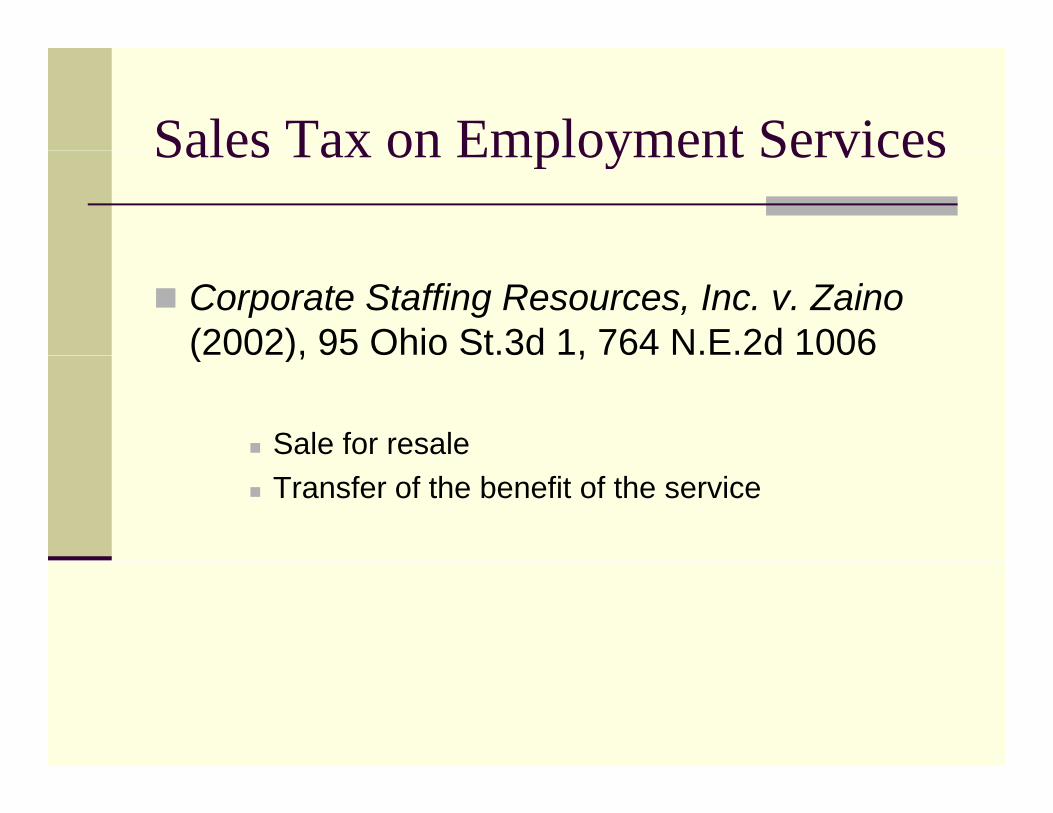

Corporate Staffing Resources, Inc. v. Zaino(2002), 95 Ohio St.3d 1, 764 N.E.2d 1006( ), ,

Sale for resaleTransfer of the benefit of the service

Sales Tax on Employment ServicesSales Tax on Employment Services

Sunbelt Transportation Services, Inc. v. Zaino(Oct. 30, 2002), BTA No. 01-V-997( , ),

Control and supervision of employeesp p yContract of at least one yearEmployees supplied on permanent basis

Sales Tax on Employment ServicesSales Tax on Employment Services

Moore Personnel Services v. Zaino (2003), 98 Ohio St.3d 337, 784 N.E.2d 1178,

Employment service v. payroll personal servicep y p y pSupplying or providing personnel

Sales Tax on Employment ServicesSales Tax on Employment Services

H.R. Options, Inc. v. Zaino (2004), 102 Ohio St.3d 1214, 800 N.E.2d 740,

Supplying or providing personnelpp y g p g pEmployees supplied on a permanent basisFacts and circumstances of employees

i tassignment

Sales Tax on Employment ServicesSales Tax on Employment Services

Reed Elsevier, Inc. v. Zaino (Jun. 30, 2004), BTA No. 2003-J-1083

Control and supervision of employeesp p y

Sales Tax on Employment ServicesSales Tax on Employment Services

Crew 4 You, Inc. v. Wilkins (2005), 105 Ohio St.3d 356, 826 N.E.2d 817,

Sale for resaleTransfer of the benefit of the serviceStatutory definition of “employment service”

Sales Tax on Employment ServicesSales Tax on Employment Services

J.Z.E. Electric, Inc. v. Wilkins (May 19, 2009), BTA No. 2006-A-2218

Employees supplied on a permanent basisp y pp pSeparation of temporary and permanent employees

Sales Tax on Employment ServicesSales Tax on Employment Services

Collective Bargaining Issues

Joint Employer Test

Community of Interests test

Sales Tax on Employment ServicesSales Tax on Employment Services

Benefit Plans

“Regular” employees v. supplied employees

Sales Tax on Employment ServicesSales Tax on Employment Services

Ohio Worker’s Compensation

Exclusive remedy / Statutory immunity

Professional Employer Organization (PEO)Professional Employer Organization (PEO)

PEO Contracts

Host Employee

Sales Tax on Employment ServicesSales Tax on Employment Services

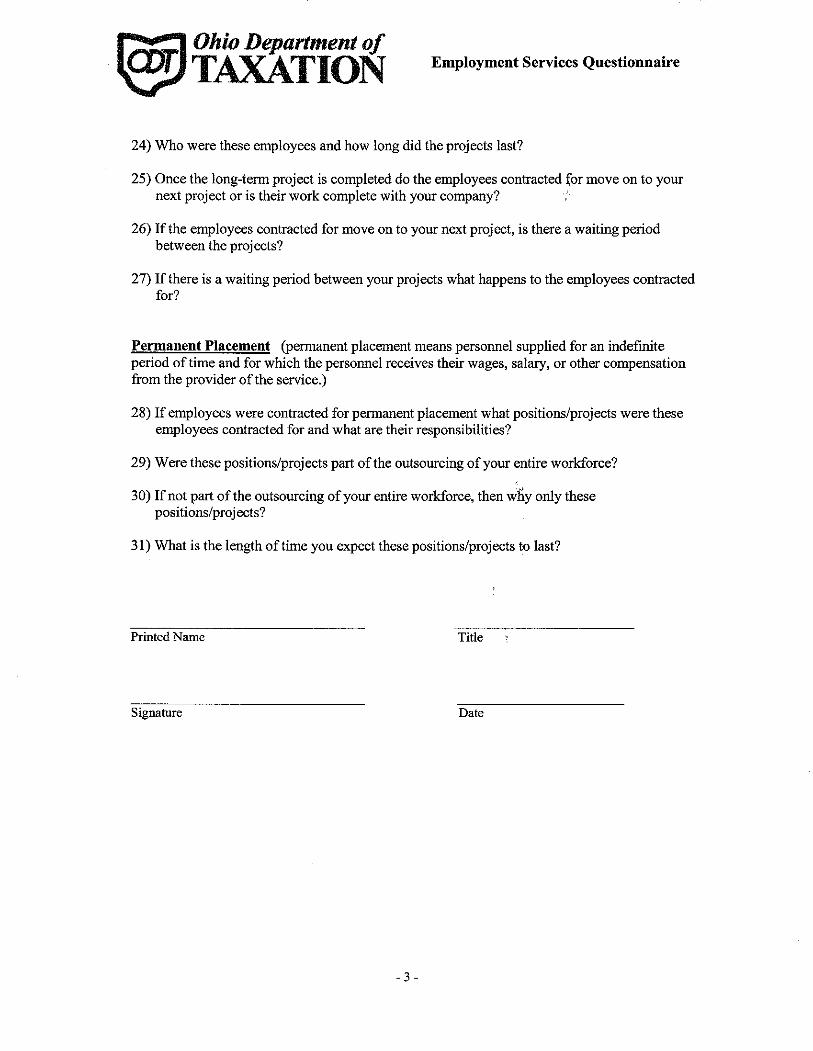

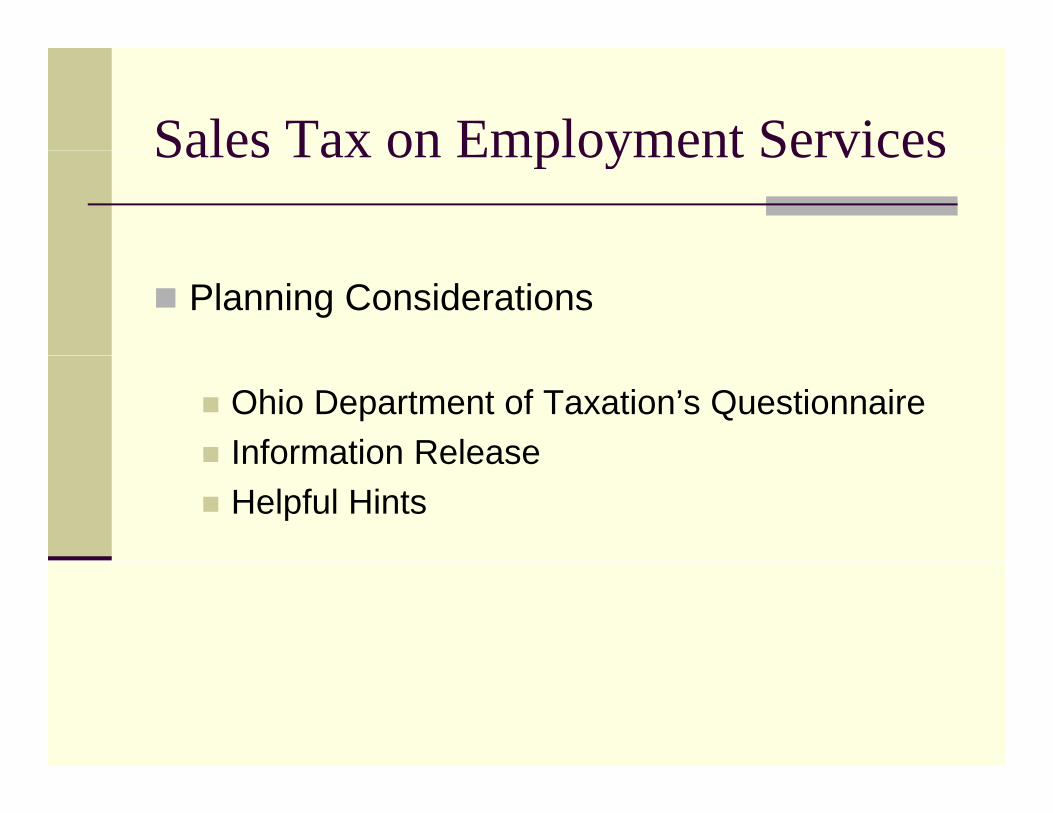

Planning Considerations

Ohio Department of Taxation’s QuestionnaireInformation ReleaseInformation ReleaseHelpful Hints

Sales Tax on Employment ServicesSales Tax on Employment Services

Ohio Department of Taxation’s Questionnaire

Used to obtain factual informationWeighed against other informationWeighed against other informationNot an exemption certificateRevisions and updatesRevisions and updates

Sales Tax on Employment ServicesSales Tax on Employment Services

Information Release

Updated in February 2007Examples covering permanent placementExamples covering permanent placement, sale for resale, contract requirements and other issues

Sales Tax on Employment ServicesSales Tax on Employment Services

Helpful HintsOral contractsOral contractsPermanent Assignment“Magic” languageMagic languageOther exemptionsDirect Pay permit customers y pReview contracts and performance

Workshop O

Ohio Sales Tax on Employment Services . . . Taking a Deep Dive into the Tax Businesses Love to Hate

Prepared and Presented by:

Dara Greene, Esq., Attorney Examiner, Ohio Department of Taxation

Tony Ehler, Esq., Partner, Vorys, Sater, Seymour & Pease LLP

January 27, 2011

-2-

I. BACKGROUND

“Employment service” became subject to Ohio sales and use tax on January 1, 1993. Later, on July 1, 1993 changes were made to what constitutes an employment service. More recently, changes were made to accommodate application of the resale exemption to employment services. This document is designed to provide an overview of the law, as well as the way the law has developed from decisions made by both the Board of Tax Appeals and the Ohio Supreme Court.

A. Ohio Statute

The definition of “sale” for the purpose of imposing the sales tax includes all transactions by which employment service is or is to be provided. R.C. 5739.01(B)(3)(k). An employment service is defined in 5739.01(JJ) as:

providing or supplying personnel, on a temporary or long-term basis, to perform work or labor under the supervision or control of another, when the personnel so supplied receive their wages, salary, or other compensation from the provider of the service. Employment service does not include:

(1) Acting as a contractor or subcontractor, where the personnel performing the work are not under the direct control of the purchaser.

(2) Medical and health care services

(3) Supplying personnel to a purchaser pursuant to a contract of at least one year between the service provider and the purchaser that specifies that each employee covered under the contract is assigned to the purchaser on a permanent basis.

(4) Transactions between members of an affiliated group, as defined in division (B)(3)(e) of this section.

(5) Transactions where the personnel so provided or supplied by a

provider or supplier to a purchaser of an employment service are then provided or supplied by that purchaser to a third party as an employment service, except “employment service” does include the transaction between that purchaser and the third party.

B. Enactment and Amendments to Ohio Sales Tax on Employment Services

Am.Sub.H.B. No. 904 introduced in House on December 15, 1992, passed by the House on December 17, 1992; sent to and passed by the Senate on December 17, 1992; Governor signed the Bill into law on December 18, 1992.

-3-

Effective January 1, 1993

Amended by Am.Sub.S.B. 122 to add (JJ)(4), effective 6/30/93, added the affiliated group exception to the definition of employment service.

Amended by Am.Sub.H.B. 152 to add (JJ)(3), effective 7/1/93, added long term employee leasing exception to the definition of employment service.

Amended by Sub. H.B. 293 to add (JJ)(5), effective 1/1/07, shifted who pays the

sales or use tax under circumstances where personnel provided or supplied to perform work or labor to the purchaser of an employment service are then provided or supplied by the purchaser to a third party as an employment service.

II. ISSUES A. Sale for Resale Exemption B. Manufacturing Exemption C. Outsourced Function and Deliverable D. Long-Term Assignment 1. One year term of contract 2. Permanent assignment 3. Performance 4. Proof a. Oral contracts b. Statute of frauds c. Parol evidence rule III. CASE LAW DEVELOPMENT

A. Excel Temporaries, Inc. v. Tracy (Oct. 30, 1998), BTA No. 97-T-257

Excel was engaged in the business of supplying personnel. At issue was Excel’s placement of employees to Webb Truss. The tax commissioner had denied a claim for refund because:

-4-

1. The contract was not in writing 2. Excel failed to prove the oral contract met the requirements of (JJ)(3). In reaching its decision, the BTA noted that generally a determination is made on whether an exemption applies by making the crucial inquiry as to what the seller is providing and what the purchaser is paying for in the agreement. Such a rule is suitable as most exceptions and exemptions are allowed or disallowed based upon the specifics of the transaction itself, not upon the specifics of a contract. However, the General Assembly added a further step in making the (JJ)(3) exception to the definition of employment service. Rather than simply naming the type of transaction that would be excluded from the definition, the General Assembly added a requirement that the circumstances of the transaction be specified in “a contract of at least one year.”

ORAL CONTRACT: The Statute of Frauds does not make an oral contract void; instead it simply makes an oral contract voidable at the will of one of the parties. An oral contract may be considered valid and relied upon but that does not mean that parol evidence will be sufficient in itself to prove that the assignment of personnel is excluded from the definition of employment service. The BTA found that corroborating evidence may be necessary to establish that an oral contract exists and that the parties performance under the contract meets the requirements of the exception to the definition of employment service found in (JJ)(3).

PERMANENT BASIS: The BTA found the employees were permanent. Excel employees were not to be reassigned, nor was there the expectation that any employee would be there for a limited time or until the conclusion of a specific contract. The personnel were hired on an “at will” basis. It is axiomatic that, unless otherwise agreed, either party may terminate the relationship at any time not contrary to law. Termination does not determine whether the employee was engaged on a permanent basis. It is the intent of the parties which is controlling.

CONTRACT FOR AT LEAST A YEAR: The parties indicated that they had an oral contract for the period in question and it was for an “ongoing” period to continue as long as Webb Truss had need for employees and as long as Excel could satisfactorily supply the requested personnel. Excel claimed that its ongoing relationship as well as the fact that the relationship had continued for four years proved that there was a contract for at least a year to satisfy the (JJ)(3) requirement. The BTA found, based upon the testimony of Mr. Delany from Webb Truss, that there was not a contract for at least a year as it was terminable at any time by either party.

The BTA affirmed the tax commissioner’s Final Determination.

-5-

B. Advantage Services v. Tracy (Oct. 30, 1998), BTA No. 95-T-1391

Advantage supplied personnel to its customers. At issue was whether the employees provided to two customers were assigned on a permanent basis pursuant to a contract of at least one year.

The BTA revisited some of the same issues discussed above. Citing Excel, the BTA rejected the commissioner’s contention that the contract must be in writing and reiterated that oral contracts may be valid. An oral contract would be valid if evidence establishes that an agreement exists between the service provider and its customer, and that the performance under the contract meets the requirements of (JJ)(3).

In addition to his Statute of Frauds argument, the commissioner also claimed that the wording of the exception, which states that the contract “specifies” that personnel are permanently assigned, requires a written contract. The BTA found this contention to be inconsistent with the definition of a contract.

The BTA found that a written contract is not necessary under (JJ)(3) in every circumstance. However, “[w]here the taxpayer has reduced its agreement to writing, that taxpayer may not rely upon parol evidence to amplify the terms of the written contract . . .” The intentions of the parties that have not been included in the contract are deemed to not exist and may not be shown by parol evidence.

It is important to note that, as in Excel, the BTA was mindful that the contract’s reference to permanent assignment was still subject to the actual performance of the parties. Also, to the extent the BTA’s decision seems critical of taxpayer’s presenting extrinsic evidence regarding the meaning of contract terms, this criticism seems unfounded under Ohio jurisprudence on parol evidence

C. Bellemar Parts Industries, Inc. v. Tracy (2000), 88 Ohio St.3d 351, 725 N.E.2d 1132

Bellemar Parts Industries (BPI) operated a wheel manufacturing and assembly line. To assist with its production, BPI contracted with two companies for temporary employees who would perform the wheel assembly. Tax was paid on the transactions and a refund application filed.

The tax commissioner rejected both of BPI’s claims that the purchases were exempt under the resale exemption in R.C. 5739.01(E) and the manufacturing exception in R.C. 5739.01(E)(9) [as was in effect for the period — now R.C. 5739.02(B)(43)(g)] and 5739.011. The BTA reversed the commissioner’s decision on the basis of the resale exception and did not determine whether the manufacturing exception applied.

The Ohio Supreme Court found that neither exception applied and reversed the decision of the BTA.

-6-

The commissioner argued that the benefit received by BPI was a flexible, less costly and more efficient work force. The court agreed with the commissioner’s characterization of the service stating that:

. . . Construed in that manner, the benefit of the employment services was not sold in an unchanged form to BPI’s customers. Rather, BPI received the benefit of those services and combined it with BPI materials and the labor of permanent employees under BPI direction and control to create the item sold. Therefore, according to the Tax Commissioner, the resale exception does not apply to BPI’s purchase of employment services.

We are convinced that the Tax Commissioner has correctly identified the benefit of the employment services, and we therefore agree with his analysis. The benefit of the services of a temporary work force must include and focus upon its most obvious benefit-that provided by the labor itself. . . .

Note that the Court’s holding did not eliminate the resale exception’s application to services. The exception remains applicable to all services and applies when the necessary statutory conditions are met.

The Court also rejected the contention that the temporary employment service was a “thing” under R.C. 5739.01(E)(9). “Thing” included only transactions in R.C. 5739.01(B)(3)(a), (b) and (e). Employment service is not included and therefore cannot be considered as a “thing transferred.”

This decision was a 4-3 split vote. Two dissenters remain on the bench while none of the justices in the majority still hold office. (See Attachment A, editorial by Justice Pfeifer explaining his dissent.)

D. Labor Pool of Cincinnati, Inc. and Success Employment Service, Inc. v. Tracy (Apr. 14, 2000), BTA Nos. 98-A-491 and 98-A-761

Labor Pool provided low and semi-skilled industrial workers to businesses. It also did business as Success, providing temporary office employees.

Labor Pool and Success claimed that they provided permanent employees to their customers under oral contracts for periods of at least one year. At issue was whether the employees supplied to Panacea/J-Mak and Superior Die under these oral contracts qualified for the exception to the definition of employment service found in (JJ)(3). Panacea/)-Mak had obtained leased employees for ten or eleven years. The agreement was ongoing in nature, and had no specific stated length. Superior’s relationship was also ongoing with no stated term limitation.

Relying on its decision in Excel, the BTA determined that both appellants failed to sufficiently establish that the oral contracts met the statutory requirements of (JJ)(3).

-7-

The BTA further determined that where no other evidence or testimony is offered to support that an oral contract meets the requirement of (JJ)(3), self-serving letters detailing the customers’ relationship with Labor Pool/Success are not sufficient to establish that a contract existed between the parties or what the terms of such contracts were. Bare assertions contained in such writings cannot be relied on.

E. Success Employment Services, Inc. v. Tracy (Apr. 14, 2000), BTA No. 98-A-489

Success (AKA Capitol Temporary Staffing) provided unskilled and semi-skilled workers to customers engaged in manufacturing. In this case, a refund was requested of tax paid on employees provided to Q3, the maker of automobile and dishwasher parts.

At issue was whether or not the employees should be considered exempt under (JJ)(3). The agreements between the parties provided that “(I)t is the intention of Capitol and Q3 Stamped Metal that the Permanent Core Personnel are assigned to Q3 Stamped Metal on a permanent basis. . . .” It was also conceded by the tax commissioner that the contracts contained a one year term. The main issue of the case was whether or not each agreement “specifies that each employee covered under the contract is assigned to the purchaser on a permanent basis ...” The commissioner argued that the contracts did not meet the requirement of specifically stating that each employee covered under the contract is assigned to a customer permanently. The commissioner had suggested that either the name of the employees be provided, or at least a listing of the positions to be filled be included with the contracts to prove the permanency of the arrangement. Further, the commissioner argued that such specificity was needed because both permanent and temporary workers were provided to Q3.

The BTA found that the degree of specificity contemplated by the commissioner is not required by the statute. Section (JJ)(3) requires specification that each employee under the contract be assigned on a permanent basis. It does not require the specific naming, of each employee or -the-positions to which they will be assigned. As to the separation of permanent from temporary workers (e.g. temporary support personnel for a receptionist that would call in sick), the CFO of Q3 testified that the temporary employees were treated separately from the provided permanent employees, that is, they were invoiced separately and could be tracked by way of such invoices. The BTA reversed the denial of the refund and remanded.

F. E.T.S. Inc. v. Tracy (Apr. 14, 2000), BTA No. 97-S-1613

ETS was engaged in providing consulting, engineering and design services to businesses. It employed engineers with various fields of expertise. It contacted manufacturers to solicit engineering projects. ETS and the manufacturer determine the scope of the project and ETS would draft a proposal. ETS provided the appropriate engineer to complete the project.

-8-

At issue was R.C. 5739.01(JJ)(1), which sets forth an exception from the definition of employment service for contractors, where the personnel performing the work are not under the direct control of the purchaser.

The BTA found that ETS had established that it provided professional engineering and consulting services as a contractor and, in providing such services, ETS retained control over its employees. The president and owner of ETS testified that over the course of a project he would evaluate the project, draft proposals and purchase orders, and determine the area of expertise needed and select the appropriate engineer. He stated that he exercised control and supervision over the employees at the project site by reviewing written reports. Although there was a contact person at the job sites that the employee reported to for general communications, the contact persons were not authorized to supervise or control the ETS employees.

The BTA found that for all the customers at issue, ETS acted as a contractor and the (JJ)(1) exception applied. However, the burden of proof was on ETS. The BTA stated that “ . . . for ETS to remove its activities from the statutory definition of employment services found in R.C. 5739.01(JJ)(1), ETS must establish that, for each of the projects in issue herein, it acted as a contractor providing professional services whose employees were not under the control of its customers.” From an evidentiary stand point the BTA was consistent with its initial decision in Excel. ETS operated under oral contracts which were occasionally memorialized in purchase orders and additional documentation. Since there were no written contracts setting forth the relationships, the BTA used the testimony and other evidence to determine if the contracts met the requirement of (JJ)(1).

G. B.J. Alan Company v. Tracy (Mar. 1, 2002), BTA No. 99-N-196

Appeal to Ohio Supreme Court dismissed Aug. 20, 2002 Cross Appeal dismissed Oct. 25, 2002

B.J. Alan Company (Alan) is a vendor of fireworks. It contracted with two companies to provide contract labor. The positions were primarily packaging, warehousing, manufacturing and office clerical. Alan had contracted with Callos since 1992. This contract was in writing. The contract with Allied had been in place since “1995 or prior” and was not in writing.

There were two issues. First, whether a termination clause in the written contract with Callos takes it out from under the (JJ)(3) exception. Second, whether the oral contract with Allied meets the requirements of the (JJ)(3) exception.

Using the statute and then its decision in Excel to start its analysis, the BTA found that the termination clause does not negate a written contract with a stated term of at least one year. Callos’ company president and its vice president of sales testified as to its intent to supply employees to Alan for a duration of more than a year. The contract had

-9-

been in place for more than a year. The BTA found that the intent was established by the signature on the contract. The stated intent was that the agreement was to be for a term of a year as the document asserted on its face. As to the second issue, the BTA found that there was a lack of evidence to show that the oral contract met the (JJ)(3) exception. Although Alan’s controller testified that the intent was to obtain permanent employees, he did not begin his employment with Alan until after the contract began and there was no foundation laid for his testimony regarding the Allied contract. Accordingly, the commissioner’s decision was affirmed in part and reversed in part.

H. Corporate Staffing Resources, Inc. v. Zaino (2002), 95 Ohio St. 3d 1, 764 N.E.2d 1006

Corporate Staffing Resources, Inc. (CSR) provided their client Sarcom with maintenance and repair technicians. Sarcom sold computer hardware and software as well as computer maintenance and repair services. Sarcom contracted with CSR to obtain extra technicians to help it keep up with its maintenance and repair obligations to its customers. The technicians would report to Sarcom or to designated client worksites where they would be supervised by a Sarcom employee.

At issue was whether Sarcom’s purchase of employees from CSR to satisfy its maintenance and repair contracts were resold to its customers in the same form as received, thus meeting the resale exception found in R.C. 5739.01(E).

CSR argued that Sarcom qualifies for the exception because its use of the CSR employees to satisfy its service plans constitute the resale of the benefit of the service in the same form in which it was received. It also argued that it logically follows from the fact that the service was provided at customer locations on customer equipment that Sarcom and Sarcom’s customers were joint beneficiaries (unlike Bellemar) as the same benefit was received by both.

The Court disagreed with CSR and found the resale exception was not applicable. The Court found that by utilizing the employees provided by CSR, Sarcom was able to have enough technicians to meet its contractual obligations. The real benefit to Sarcom was not the product of the labor, but a flexible staff of technicians that allowed it to meet its obligations. The Court also decided that CSR’s joint beneficiary reasoning was flawed. CSR’s reasoning was too narrow and failed to take into account that Sarcom and the customers have different, though related, benefits regardless of where the work on the equipment is actually performed.

I. Sunbelt Transportation Services, Inc. v. Zaino (Oct. 30, 2002), BTA No. 01-V-997 Dismissed on appeal Jan. 24, 2003 Franklin Cty. Ct. of Appeals

Sunbelt provided its customers with qualified drivers to make routine deliveries using the customers’ vehicles.

-10-

Sunbelt raised three arguments. First, that the transportation services it provides do not constitute employment services under R.C. 5739.01(JJ) because its employees are not “under the control of another.” Second, that if its service is found to be an employment service, it is subject to the exclusion found in (JJ)(1). Third, Sunbelt argued that its services are excluded under (JJ)(3).

The BTA disagreed with Sunbelt as to its first point. The BTA found that while it was true that Sunbelt had the inherent authority as the employer to recruit, screen, train, promote, assign, evaluate, discipline and fire its employees, Sunbelt’s evidence did not go to the real issue of whether the drivers provided were performing their duties under the supervision of the customer. The evidence indicated that the customers were clearly in control of the drivers as they directed the mode, manner and timing of the driver’s daily schedules.

Likewise the BTA disagreed with Sunbelt’s argument that the (JJ)(1) exception applied. The evidence indicated that the drivers were under the direct control of the customer. The customer dictated the timing, frequency, order and method of its transportation.

Finally, as to the (JJ)(3) exclusion, there was no dispute that the term of the contract was for at least one year. However, the written contracts were silent as to whether the drivers were assigned on a permanent basis. Going back to its decision in Advantage, the BTA used the standard that when there is a written contract, it will not overlook the written contract. Citing from page 10 of the Advantage case, the BTA stated that in such a situation the appellant-taxpayer “. . . may not now come forward with parol evidence in an attempt to add terms not expressed in the writing.” Sunbelt’s argument that the contracts’ provision that only allowed for the customer’s removal of an employee for just cause after the probationary period equates to permanent placement was denied by the BTA.

J. Moore Personnel Services v. Zaino (2003), 98 Ohio St.3d 337, 784 N.E.2d 1178

Moore Personnel Services (Moore) provided employees to its customers. Moore indicated that it had “understandings”, but no written contracts, with its customers. The customers would find the individuals that they wanted to work for them and they would send the individuals to Moore who would put the employees on its payroll. Moore paid the employees’ wages and the customers paid Moore a fee for its services. The tax commissioner assessed sales tax against Moore for the services. The BTA reversed the tax commissioner’s finding that Moore’s services were not employment services, as Moore did not provide or supply the employees but instead provided a nontaxable payroll and personal service. The tax commissioner appealed.

The Court found that to satisfy the definition of an employment service three criteria had to be met. First, the provider must supply personnel on a temporary or long- term basis. Second, the personnel supplied must perform the work under the supervision

-11-

or control of another. Third, the personnel must receive their wages, salary or other compensation from the provider of the service. The first requirement was in dispute in this case. Accordingly, the resolution turned on whether Moore was supplying or providing personnel.

Since no definition appears in the statute for “providing” and “supplying,” the Court looked at common and ordinary usage of these terms. Under common usage “provide” means “to supply or furnish for use” [Oxford English Dictionary (1933) cited from Sowers v. Schaeffer (1949), 152 Ohio St. 65] and “supply” means to “to furnish with what is wanted” [Black’s Law Dictionary (5th Ed. 1979) cited from Van Dyne Crotty Co. v. Limbach (1990), 53 Ohio St. 3d 3]. The Court found that the fact that Moore’s customers told it who they wanted on Moore’s payroll was not a factor to be considered in determining whether employment services were being provided. No distinction is made in the definition of employment service as to who makes the initial choice of the personnel. The General Assembly could have made the definition turn on who supplied the personnel if it had so chosen. Accordingly, the services provided by Moore met the definition of employment service as it is set out in the statute.

K. H.R. Options, Inc. v. Zaino (2004), 102 Ohio St. 3d 1214, 800 N.E.2d 740

H.R. Options (HRO) was in the business of providing third-party employment service for its clients. It served as the employer of record, hiring persons whose service its clients wanted to utilize but whom the client did not want to hire as their own employees. HRO did not fill the employment needs of its clients from its own pool of workers.

The original issue was whether or not HRO provided an employment service. The BTA had found that it did not provide an employment service basing its decision on its own determination in Moore. That decision was overturned by the Ohio Supreme Court. Thus, the Court found that HRO did provide an employment service. The contracts met the requirement that they be for at least one year. The issue then became whether the (JJ)(3) exception applied: more specifically, what was meant by “permanent.”

The commissioner agreed that the word “permanent” did not have to appear in the contract. The Court disagreed with the BTA’s determination of permanency based on whether the employees are ever reassigned by the service provider. The Court started with the basic premise that permanent did not mean that an employee must be assigned forever. In the context of (JJ)(3), the Court felt that assigning an employee on a permanent basis meant that the employee was assigned, for an indefinite period--i.e., that the contract did not specify an ending date and the employee was not being provided as a substitute for an employee on leave, as a seasonal worker, or for a short-term workload condition. The Court stated that “[t]hus, both the contract and the facts and circumstances of the employee’s assignment are factors that must be reviewed to determine whether the employee is being assigned on a permanent basis.”

-12-

L. Reed Elsevier, Inc. v. Zaino (Jun. 30, 2004), BTA No. 2003-J-1083

Reed Elsevier, Inc. (Reed) provides computerized services (Lexis-Nexis) to subscribers. It employed regular employees to work on lines of code in developing software. When its regular employees were not of a sufficient number or lacked the specific skills needed, Reed would obtain additional employees from outside companies. The outside vendor’s did not supervise the work of their personnel. Both Reed’s regular employees and the additional personnel were supervised on the job by Reed’s project manager.

At issue was whether the (JJ)(1) exception to the definition of employment service applied.

Reed argued that the commissioner should examine the “true object” of the services provided, which it says was the creation of lines of code. The BTA found that a determination on the “true object” of the transaction isn’t necessary in deciding whether Reed was purchasing employment service. Instead, under the definition of employment service, a resolution of who supervises and controls the employees is the determining factor.

Referring to Bellemar, the BTA found that Reed sought the temporary workers. It received the benefit of a flexible workforce.

Reed also argued that if the service was employment service, then it was not provided under the direct control or supervision by Reed.

The BTA found that the cased cited by Reed, Sunbelt and ETS, were not controlling. Since Reed testified that a project manager supervised the work performed, the BTA found that the temporary employees were not controlled by the service provider and that the (JJ)(1) exception did not apply.

M. Crew 4 You, Inc. v. Wilkins (2005), 105 Ohio St.3d 356, 826 N.E.2d 817 Crew 4 You, Inc. (Crew 4 You) is a company that provides personnel

needed to operate technical equipment during a live television broadcast. A broadcast company rented the technical equipment from a trucking company and in turn the trucking company hired the personnel needed from Crew 4 You. The broadcast company supervised the personnel. The personnel were paid by Crew 4 You.

At issue was whether Crew 4 You sold taxable employment services and if so,

was the sale exempt from the state sales tax under the “sale for resale” exemption. The Court found that Crew 4 You did sell taxable employment services but found that the resale exemption did not apply because the trucking company did not resell the employment services.

-13-

The Court found that Crew 4 You was (1) a business that supplied personnel on a

temporary or long-term basis; (2) that the personnel supplied by Crew 4 You were controlled by a third party, the broadcast company; (3) that Crew 4 You did not act as a contractor because it was not hired to produce the final result – a broadcast; and (4) the personnel received their wages from Crew 4 You. For the reasons above, the Court found that Crew 4 You provided a taxable employment service.

The Court also found that the services that Crew 4 You sold were not resold by

the trucking company to the broadcast company. The BTA had found that the “benefit of Crew 4 You’s personnel services (a flexible, temporary workforce) were passed on through the trucking company to the broadcast company, therefore the services were resold. However, the Court found that the trucking company did not sell “employment services” based upon the strict definition in R.C. 5739.01(JJ). Because the personnel did not receive their wages from the trucking company, the services sold to the broadcast company were not employment services.

N. J.Z.E. Electric, Inc. v. Wilkins (May 19, 2009), BTA No. 2006-A-2218 J.Z.E. Electric, Inc. (J.Z.E.) is an electrical contractor. J.Z.E. purchased

employment services from Tradesmen International, Inc. (Tradesmen), Construction Labor Contractors (CLC) and Clock Electric. The services purchased from Tradesmen and CLC were separated into two categories by J.Z.E. Some of the services were “leased,” meaning that J.Z.E. wanted the services for an indefinite period and some of the services were “temporary,” meaning that J.Z.E. only wanted the services for a limited duration. Both classifications of employment services were covered by the same contract from Tradesmen and CLC. The services purchased from Clock Electric were done as “a favor” to Clock Electric by J.Z.E. because the services were purchased only when Clock Electric did not have enough work to keep its employees busy.

At issue was whether the (JJ)(3) exception applied to the transactions. The BTA

found that for the Tradesman and CLC contracts, a contract for at least a year existed. However, because the contracts covered both “leased” and “temporary” workers and the contracts did not specify the names of the employees, it could not be determined which employees were assigned on a permanent basis. No other records or documentation existed to delineate which employees were permanently assigned, and the BTA refused to rely upon hearsay statements. The BTA found that J.Z.E. failed to meet its burden that the transactions were within the statutory exclusion.

For the transactions with Clock Electric, the BTA could not find any evidence of

a contract of at least a year, nor could J.Z.E. illustrate that the employees were permanently assigned because the employees were placed with J.Z.E. only when Clock Electric could not find enough work for its employees. The transactions were found to be taxable employment services.

-14-

IV. COLLECTIVE BARGAINING ISSUES The issue here is who gets to vote for formation of a union and collective bargaining. Sometimes employers of an employment agency can be in the same bargaining unit as “regular” employers of the host employer. This can be a dynamic exercise depending upon the political party that controls the White House and thus the NLRB. When control is with a Democrat, the Joint Employer Test and the Community of Interests Test must be satisfied, if the employers do not consent to the combination. If consent is provided only the second test (Community of Interests Test) must be satisfied. If Republicans are in control, consent by the employers is a requirement and cannot be overcome by satisfaction of the Joint Employer Test. The Community of Interest Test also must be satisfied. A. Joint Employer Test For a unit to be composed of both temporary and “regular” or “permanent” employees, the temporary agency and the employer must be joint employers of the temporary employees. Under current Board precedent, two entities are joint employers if they share or codetermine matters governing essential terms and conditions of employment. The employers must meaningfully affect matters relating to the employment relationship such as firing, discipline, supervision, and direction. Riverdale Nursing Home, 317 NLRB 881 (1995). B. Community of Interests Test For a unit to be composed of both temporary and “permanent”, the temporary employees must share a “community of interests” with the “permanent” employees. 1. Definition The purpose of the test is to determine whether differing groups of employees should be included in one bargaining unit. Employees must share a community of interests “in wages, hours, and other conditions of employment” sufficient to justify their mutual inclusion in a single bargaining unit. Buy-Rite Lumber Company v. N.L.R.B., 1996 U.S. App. LEXIS 16820 (6th Cir. 1996). 2. Factors The community of interest test examines factors to determine whether a mutuality of interests in wages, hours, and working conditions exists among the employees involved. Kalamazoo Paper Box, 136 NLRB 134 (1962). In the past, the Board has examined the following factors: (1) central control over daily operations and labor relations; (2) skills and functions of employees; (3) general working conditions; (4) bargaining

-15-

history, if any; (5) interchange of employees; and (6) geographic proximity of the facilities. Eastman Interiors, Inc., 273 N.L.R.B. 621 (1984). Under Board precedent, a group of employees working side by side at the same facility, under the same supervision, and under common working conditions is likely to share a sufficient community of interest to constitute an appropriate unit. Kalamazoo, 136 NLRB at 134. V. BENEFITS The host employer may be responsible for extending the same benefits it provides its “regular” employees to employees supplied by an agency. This issue depends upon how the employer benefit plan is described. There should be an express exclusion in the host employer’s benefit plan documents. In addition, the agency agreement ideally would reference that all employees assigned give up any rights to host employer benefits as described in its plan documents unless expressly provided for in the agency agreement. Assigned employees may be asked to confirm this by signing a confirmation or waiver. VI. OHIO WORKER’S COMPENSATION A. Exclusive Remedy/Statutory Immunity precludes employee from pursuing civil cause of action for injury sustained in the course and performance of employment. B. Professional Employer Organization (“PEO”)

C. PEO Contracts

D. Host Employee

E. What Does All This Mean for Sales Tax

VII. PLANNING CONSIDERATIONS

A. Ohio Department of Taxation’s Questionnaire (See Attachment B) 1. The use of the questionnaire is intended solely to obtain factual information in the context of an audit. 2. The responses will be accorded whatever weight the Department deems appropriate in light of any other information in the Department’s possession. Other information could include time sheets, requisitions, purchase orders and letters of negotiation.

-16-

3. The questionnaire may be used by an employment service provider as a means to help determine the taxability of their contracts but by no means will it be treated as an exemption certificate. 4. If the questionnaire is used by the employment service provider at the time the contract is entered into, it should be reviewed from time to time to determine the actual performance of the employees provided. B. Information Release (See Attachment C) The latest Information Release from the Ohio Department of Taxation was issued in February of 2007. Generally, most questions have come regarding the exception to the definition of employment service found in section (JJ)(3). Both the Department and taxpayers have struggled with interpreting this exception. For example, there was disagreement on whether the contract had to be in writing, whether the specific employees or positions covered by the contract had to be enumerated in the agreement and what was meant by the word “permanent.” Subsequently, many of these questions have been addressed by the Ohio Board of Tax Appeals of the Ohio Supreme Court. Their decisions in the individual cases have not always provided guidance. However, as time has gone by, there has been an evolution of sorts in the decisions that have allowed the Department to set its current audit policy. The current Information Release contains thirty examples designed to illustrate the Department’s position regarding the application of R.C. 5739.01 (JJ) to specific fact patterns. C. Helpful Hints 1. Avoid use of oral contract when possible. 2. A contract for a one-year term does not equate to permanent assignment of employees. 3. Review all contracts for compliance with the statutory requirements. Contracts containing the magic language may satisfy an agent at the audit level. Follow-up by reviewing contract performance. 4. Determine if any of the contracts fit within another sales and use tax exception. For example, were services provided on state contracts or to 501(c)(3) organizations? 5. Document any customers that hold a direct pay permit. One taxpayer vendor had nearly $1 million in tax deducted from the audit because a customer had a direct pay permit.

-17-

6. Identify largest customers. Can you rely on these customers to provide letters of usage to the State upon assessment? These letters can be crucial in proving that performance matched intent. 7. Providing personnel and charging hourly likely to be scrutinized more closely regardless of other terms. 8. Obtain competent advice in contract preparation, review periodically and at the first sign of an audit.