Embed Size (px)

Citation preview

South AustralianEnergy PricesJuly 2012 - July 2013

An update report on the South AustralianTariff-Tracking Project

May Mauseth Johnston September 2013

1

Disclaimer*The$energy$offers,$tariffs$and$bill$calculations$presented$in$this$report$and$associated$

workbooks$ should$be$used$as$a$general$guide$only$and$should$not$be$ relied$upon.$

The$ workbooks$ are$ not$ an$ appropriate$ substitute$ for$ obtaining$ an$ offer$ from$ an$

energy$retailer.$ $The$information$presented$in$this$report$and$the$workbooks$is$not$

provided$as$financial$advice.$While$we$have$taken$great$care$to$ensure$accuracy$of$

the$information$provided$in$this$report$and$the$workbooks,$they$are$suitable$for$use$

only$as$a$research$and$advocacy$tool.$We$do$not$accept$any$legal$responsibility$for$

errors$or$inaccuracies.$The$St$Vincent$de$Paul$Society$and$Alviss$Consulting$Pty$Ltd$do$

not$ accept$ liability$ for$ any$ action$ taken$based$on$ the$ information$provided$ in$ this$

report$or$the$associated$workbooks$or$for$any$loss,$economic$or$otherwise,$suffered$

as$ a$ result$ of$ reliance$ on$ the$ information$ presented.$ If$ you$ would$ like$ to$ obtain$

information$about$energy$offers$available$to$you$as$a$customer,$go$to$AER’s$‘Energy$

Made$Easy’$website$or$contact$the$energy$retailers$directly.$

$

$

$

$

$

South$Australian$Energy$Prices$July$2012$–$July$2013$

An$Update$Report$on$the$South$Australian$TariffOTracking$Project$

by$May$Mauseth$Johnston$$$

$

May*Mauseth*Johnston,*September*2013*Alviss*Consulting*Pty*Ltd*ABN$43147408624$

$$

$

$

$

©*St*Vincent*de*Paul*Society*and*Alviss*Consulting*Pty*Ltd**This$work$is$copyright.$Apart$from$any$use$permitted$under$the$Copyright$Act$1968$

(Ctw),$no$parts$may$be$adapted,$reproduced,$copied,$stored,$distributed,$published$

or$put$to$commercial$use$without$prior$written$permission$from$the$St$Vincent$de$

Paul$Society.$$$

$

$

$

$

Contacts:*Gavin*Dufty**Manager$Policy$and$Research,$Victoria$$

Phone:$(03)$98955816$*$

www.vinnies.org.au/energy$$

$$

*

2

Acknowledgements*This$ project$ was$ funded$ by$ a$ research$ grant$ from$ the$ Consumer$ Advocacy$ Panel$

(www.advocacypanel.com.au)$ as$ part$ of$ its$ grants$ process$ for$ consumer$ advocacy$

projects$and$research$projects$for$the$benefit$of$consumers$of$electricity$and$natural$

gas.$

$

The$views$expressed$in$this$document$do$not$necessarily$reflect$the$views$of$the$

Consumer$Advocacy$Panel$or$the$Australian$Energy$Market$Commission.$

$

**************************************

3

Table*of*Contents**Acknowledgements* 2** *The*SA*TariffJTracking*Project:*Purpose*and*outputs* 4** *1.*Energy*price*changes*from*July*2012*to*July*2013* 5** *2.*Regulated*vs.*market*offers*post*July*2013* 8*

2.1$Regulated$electricity$vs.$market$offers$post$July$2013$$ 8$

2.2$Regulated$gas$vs.$market$offers$post$July$2013$ 14$

* $

3.*Supply*charges* 17*3.1$Electricity$supply$charges$ 17$

3.2$Gas$supply$charges$ 18$

* *$

*******************************

4

The*SA*TariffJTracking*Project:*Purpose*and*outputs*$

Under$retail$price$regulation$arrangements,$tariff$tracking$and$tariff$analysis$are$not$

usually$prioritised$activities$amongst$advocates$and$consumer$representatives.$$In$a$

deregulated$environment$however,$ it$becomes$increasingly$evident$that$advocates,$

as$well$as$ consumers$ themselves,$need$ improved$awareness$and$understanding$of$

changing$tariff$offers:$both$in$terms$of$changes$to$price$as$well$as$changes$to$tariff$

shapes.$ $ In$February$2013$the$South$Australian$Government$decided$to$deregulate$

the$energy$retail$market$and$this$decision$ included$a$negotiated$price$reduction$to$

AGL’s$(electricity)$standing$offer,$now$called$standard$retail$contract.$$AGL$agreed$to$

reduce$ the$ electricity$ standing$ contract$ price$ for$ existing$ residential$ consumers$ by$

9.1%$for$the$next$two$years$and$Origin$(gas)$agreed$to$cut$its$gas$standing$contract$

price$by$1%$as$of$February$2013.1$The$development$of$the$SA$TariffOTracking$tool$has$

thus$ been$ well$ timed,$ allowing$ advocates$ to$ undertake$ ‘before$ and$ after’$

comparisons$ and$ monitor$ potential$ impacts$ of$ deregulation$ on$ South$ Australian$

consumers,$as$well$as$energy$affordability$and$market$developments$more$broadly.$

$

This$project$has$tracked$electricity$and$gas$tariffs$in$South$Australia$from$July$2009$to$

July$2013,$and$developed$a$spreadsheetObased$tool$that$allows$consumer$advocates$

to$build$on$the$initial$analysis$and$continue$to$track$changes$as$they$occur.$The$first$

report$ for$the$SA$TariffOTracking$project$was$published$ in$August$2012$and$this$upO

date$report$focuses$on$price$changes$that$have$occurred$over$the$last$year.$

$

We$have$developed$four$workbooks$that$allow$the$user$to$enter$consumption$levels$

and$ analyse$ household$ bills$ for$ regulated/standard$ gas$ and$ electricity$ offers$ from$

July$2009$to$July$2013,$as$well$as$current$published$electricity$and$gas$market$offers$

post$the$price$resets$in$July$2012$and$July$2013.2$$$

$

Workbook$1:$Regulated$electricity$offers$July$2009OJuly$2013$

Workbook$2:$Regulated$gas$offers$July$2009OJuly$2013$

Workbook$3:$Electricity$market$offers$post$July$2012$and$July$2013.3$

Workbook$4:$Gas$market$offers$post$July$2012$and$July$2013.$

$$$

The$ four$ workbooks$ and$ the$ reports$ can$ be$ accessed$ at$ the$ St$ Vincent$ de$ Paul$

Society’s$website:$www.vinnies.org.au/energy $

1$Government$of$South$Australia,$Premier$Weatherill$and$Minister$Koutsantonis,$Lower&power&prices&for&South&Australia,$News$release,$18$December$2012$2$All$market$offers$are$published$offers$and$do$not$include$special$offers$that$retailers$market$

through$doorOknocking$campaigns$or$brokers.$We$use$the$AER’s$‘Energy$made$easy’$website$

as$well$as$the$retailers$own$websites$to$collect$market$offer$for$the$TariffOTracking$tool.$The$

TariffOTracking$tool$does$not$include$any$additional$discounts$or$bonuses$but$key$market$

offer$features$are$listed$in$the$spreadsheets.$$This$report$contains$analysis$of$some$of$those$

features.$$$3$This$workbook$also$contains$electricity$market$offers$that$took$effect$upon$the$

deregulation$of$the$retail$market$in$February$2013.!

5

1.*Energy*price*changes*from*July*2012*to*July*2013*$

In$terms$of$general$trends,$the$tariff$analysis$found$that:4$

$

• Annual$ electricity$ costs$ for$ standard$ contract$ customers$ have$ typically$

decreased$by$around$$50$since$July$2012.$See$chart$1$below.$

$

• Households$ that$ signed$ up$ to$ AGL’s$ standing$ offer$ prior$ to$ deregulation$ in$

February$2013$and$are$now$on$AGL’s$ transitional$offer,$are$currently$saving$

approximately$$180$per$annum$(compared$to$the$standard$contract$prices).$$

$

• Significant$gas$price$ increases$mean$that$annual$bills$have$typically$gone$up$

by$$110$(or$12%)$since$July$2012$despite$the$brief$1%$decrease$that$occurred$

as$prices$were$deregulated$in$February.$See$chart$2$below.$

$

• The$majority$ of$ the$ electricity$ retailers$ have$ market$ offer$ rates$ above$ the$

standard$contract$rates$ (prior$ to$discounts)$while$ two$retailers$have$market$

offer$rates$that$are$slightly$below.$

$

• None$of$the$gas$market$offers$have$published$rates$(not$including$discounts)$

that$ are$ lower$ than$ the$ standard$ contract$ rates.$ Two$ retailers$ have$ gas$

market$offer$rates$that$are$higher.$

$

• By$switching$from$the$standard$contract$to$the$best$electricity$market$offers,$

households$ with$ a$ typical$ consumption$ level$ may$ save$ $280$ per$ annum$

(including$discounts$and$pay$on$time$discounts).$Households$currently$on$the$

transitional$offer$may$ save$$110$per$annum$ if$ switching$ to$one$of$ the$best$

market$offers.$

$$

• Customers$that$have$difficulty$paying$their$bills$on$time$should$be$aware$of$

discounts$conditional$upon$prompt$payment.$ $Four$of$the$electricity$market$

offers$produce$annual$bills$above$the$standard$contract$rates$for$late$paying$

customers.$

$

• Gas$ customers$ with$ typical$ consumption$ may$ save$ $75$ per$ annum$ by$

switching$ from$ the$ standard$ contract$ to$ the$ best$ market$ offer$ (including$

discounts$and$pay$on$time$discounts).$$$$

$

****

4$These$calculations$are$based$on$increases$in$the$regulated$offer$for$single$rate$electricity$

customers$using$6,000kWh$per$annum,$increases$in$the$regulated$offer$for$controlled$load$

electricity$customers$(typically$allOelectric$households)$using$7,500kWh$per$annum$(thereof$

20%$offOpeak)$and$the$increase$in$the$regulated$offer$for$gas$customers$using$21,000Mj$per$

annum.$$$

6

Chart*1*Differences$to$the$annual$cost$of$standing/standard$contract$electricity$offers$from$

2012$to$2013.$Based$on$annual$consumption$level$of$6,000kWh$for$single$rate$and$7,500kWh$

per$annum$(thereof$20%$controlled$load),$GST$inclusive$

$

**Chart*2*Differences$to$the$annual$cost$of$gas$Standing$offers/Standard$contracts$from$2012$

to$2013,$21,000Mj$per$annum,$GST$inclusive$

$

$$

As$the$South$Australian$Government$negotiated$a$two$year$‘price$freeze’$of$the$retail$

component$of$AGL’s$standard$contract$offer,$customers$that$were$on$AGL’s$

electricity$standard$contract$offer$prior$to$31$January$will$continue$to$receive$bills$

similar$to$that$of$the$February$2013$rates.$$After$just$six$months$since$deregulation$

customers$on$the$standard$offer$prior$to$deregulation$(and$now$on$the$transitional$

offer)$are$saving$approximately$$180$on$their$electricity$bills.$That$said,$the$‘price$

freeze’$is$a$two$year$agreement$and$consumers$currently$benefiting$from$lower$

prices$may$need$to$be$prepared$for$a$price$shock$when$it$ends$in$February$2015.$It$is$

thus$important$to$keep$a$close$eye$on$market$offer$developments$(see$section$2$

below).$$

1,600!1,700!1,800!1,900!2,000!2,100!2,200!2,300!2,400!2,500!2,600!2,700!

Single!rate! Controlled!load!

Annual&bills&($)&

Jul;12!

Feb;13!

Aug;13!

500!

600!

700!

800!

900!

1,000!

1,100!

Adelaide! Port!Pirie! Whyalla! Mt!Gambier!

Riverland!

Annual&bills&($)&

Jul;12!

Feb;13!

Aug;13!

7

In$terms$of$gas,$the$Government$did$not$negotiate$an$ongoing$‘price$freeze’$with$

Origin$Energy$and$prices$have$increased$significantly$since$the$initial$price$drop$of$1%$

in$February$2013.5$$Gas$bills,$as$of$August$2013,$are$12%$higher$than$they$were$in$

July$last$year.$$

$

During$the$three$year$period$from$July$2009$to$July$2012$electricity$prices$increased$

by$ approximately$ 60%$ and$ gas$ prices$ by$ approximately$ 40%.$ $ Since$ July$ 2012$

electricity$prices$have$decreased$slightly$while$gas$prices$have$increased$significantly$

(12%).$ As$ price$ deregulation$ took$ effect$ in$ February$ 2013$ electricity$ prices$ came$

down$ by$ 9%$ and$ gas$ prices$ by$ 1%,$ the$ new$ standard$ offers$ that$ took$ effect$ on$ 1$

August$ 2013,$ however,$means$ that$ the$ overall$ decrease$ (since$ July$ 2012)$ is$much$

lower$ for$ electricity$ and$ has$ resulted$ in$ a$ net$ increase$ for$ gas.$ See$ table$ 1$ and$ 2$

below.$$

**Table*1$Difference$to$annual$bills$for$electricity$by$tariff$type$July$2012$–$July$20136$$

* Single*rate*(6,000kWh)* Two*rate*(7,500kWh,**20%*controlled*load)$

$*Difference* O$45$ O$50$

%*Difference* O2%$ O2%$

$

*Table*2$Difference$to$annual$bills$for$gas$by$area$July$2009$–$July$20127$$

* Adelaide* Port*Pirie* Whyalla* Mt*Gambier* Riverland*$*Difference* $111$ $111$ $111$ $111$ $111$

%*Difference* 12%$ 12%$ 12%$ 12%$ 12%$

$ $ $ $ $ $

$

$

**********

5$See$Origin$Energy,$Media$Release,$18$December$2012$at$

http://www.originenergy.com.au/news/article/asxmediaOreleases/1452$6$Single$rate$calculations$are$based$on$household$consumption$of$6,000kWh$per$annum$at$

the$rate$of$the$regulated$retail$offers.$$The$twoOrate$calculations$are$based$on$household$

consumption$of$7,500kWh$per$annum$(thereof$20%$controlled$offOpeak$load)$at$the$rate$of$

the$regulated$retail$offers.$7$Based$on$the$regulated$gas$rates$for$customers$using$21,000Mj$per$annum.$$

8

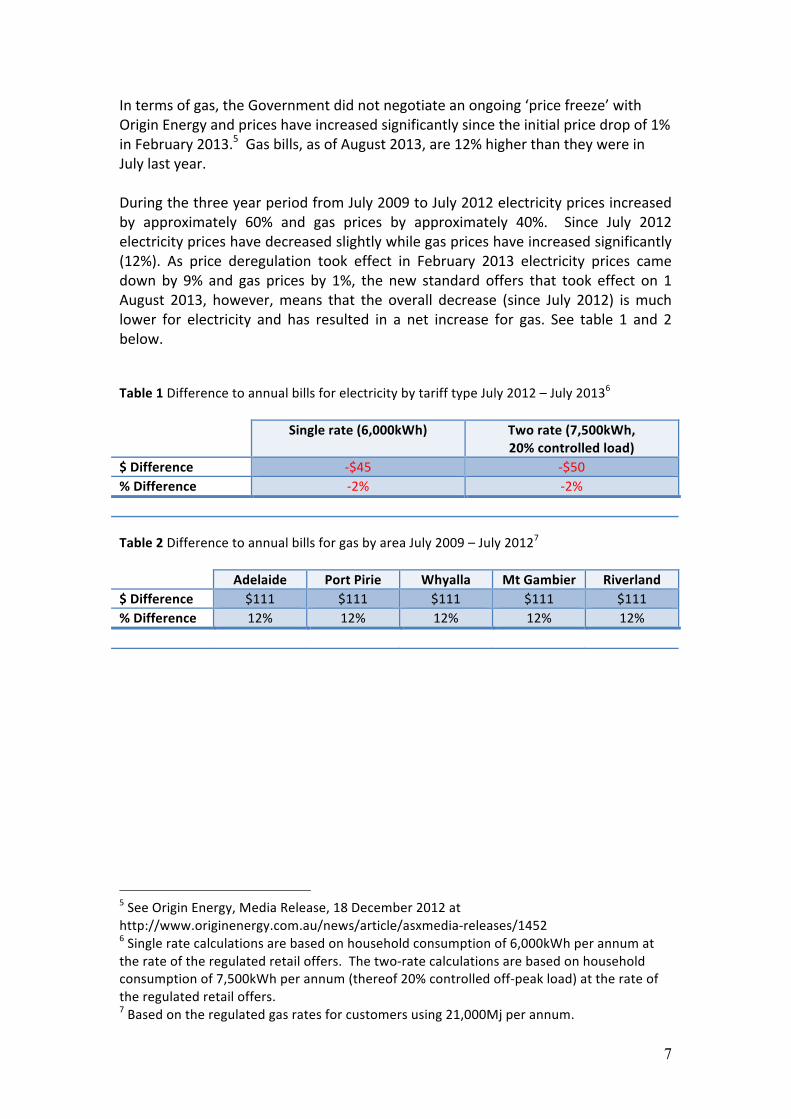

*2.*Regulated*vs.*market*offers*post*July*2013**2.1*Electricity:*Regulated*vs.*market*offers*post*July*20138*$

Chart$3$below$shows$ that$households$using$6,000kWh$per$annum$(single$ rate)$will$

have$ an$ annual$ electricity$ bill$ of$ between$ $2,150$ and$ $2,500,$ and$ that$ the$

transitional$ standing$ offer$ contains$ the$ lowest$ rates.$ $ Furthermore,$ chart$ 3$ shows$

that$while$two$of$the$retailers$(Powerdirect$and$Momentum)$have$market$offer$rates$

below$ the$ standard$ contract$ (when$ calculated$ as$ annual$ bills$ and$ noting$ that$ this$

chart$is$based$on$rates$prior$to$additional$discounts),$six$retailers$have$market$offer$

rates$that$are$higher$than$the$standard$contract.$$In$July$2012,$by$comparison,$only$

one$retailer$had$market$offer$rates$above$the$regulated$rates.**Chart* 3$ Electricity$ offers$ as$ annual$ bills,$ post$ July’13,$ Single$ rate,$ not$ including$ discounts,$6,000kWh$per$annum$(GST$inc)$

$$

$

Chart$4$below$shows$a$similar$trend$for$households$with$controlled$offOpeak$load.$$

$

************

8$Note:$AGL’s$market$offer$took$effect$1$August$2013$

1,600!1,700!1,800!1,900!2,000!2,100!2,200!2,300!2,400!2,500!2,600!

Annual&bill&($)&

9

*Chart* 4$ Electricity$ offers$ as$ annual$ bills,$ post$ July’13,$ Controlled$ load,$ not$ including$discounts,$7,500kWh$per$annum,$thereof$20%$offOpeak$(GST$inc)$

$

$

$

As$stated$above,$the$calculations$for$the$market$offers$in$charts$3$and$4$are$based$on$

rates$only$ (cost$per$kWh$and$ fixed$charges)$and$do$not$ include$other$market$offer$

features$such$as$discounts$on$consumption$ rates,$vouchers,$ signOup$credits,$ loyalty$

bonuses$and$discounts$if$bills$are$paid$on$time.$

$

Consumers$ assessing$ market$ offers$ should$ take$ these$ additional$ features$ into$

account$as$well$as$being$aware$of$contract$conditions$such$as$late$payment$fees,$the$

length$of$the$contract$and$fees$for$exiting$the$contract$early.$$

$

Chart$ 5$ below$ shows$ the$ difference$ in$ annual$ bill$ between$ the$ standard$ and$

transitional$ offer$ and$market$offers$ (both$ including$ and$excluding$discounts).$ They$

show$that$market$offers$(including$discounts$and$pay$on$time$discounts)$can$produce$annual$bills$that$are$around$$280$less$than$the$standard$contract$and$$110$less$than$

the$transitional$standing$offer.$$However,$as$the$transitional$offer$is$subject$to$a$‘rate$

freeze’$ until$ February$ 2015,$ households$ would$ be$ illOadvised$ switching$ from$ the$

transitional$offer$to$a$market$offer$based$on$these$savings.$$$$$

************

1,800!1,900!2,000!2,100!2,200!2,300!2,400!2,500!2,600!2,700!2,800!

Annual&bill&($)&

10

Chart* 5$ Annual$ bills$ excluding$ vs.$ including$ discounts.$ Electricity$ offers$ post$ July$ 2013$ as$annual$bills,$Single$rate,$6,000kWh$(GST$inc).

9*

*$

$

The$discounts$(including$pay$on$time$discounts)$used$to$estimate$the$annual$bills$for$

chart$5$above$are$shown$in$table$3$below.$$Table$3$also$shows$other$contract$terms$

and$ features,$ such$ as$ early$ termination$ fees,$ associated$with$ these$market$ offers.$

Some$ of$ the$ retailers$ have$multiple$market$ offers$ and$may$ offer$ higher$ discounts$

than$those$listed$here.$$However,$if$the$discount$is$higher$the$length$of$the$contract$

term$is$generally$longer,$and$vice$versa.$

*********************

9$Calculations$include$discounts$off$usage$or$bill$as$well$as$pay$on$time$discounts$off$usage$or$

bill.$

1,600!1,700!1,800!1,900!2,000!2,100!2,200!2,300!2,400!2,500!2,600!

Annual&bill&($)&

Discounts!excl!

Discounts!incl!

11

Table* 3* Published$ electricity$ market$ offers$ taking$ effect$ after$ July$ 2013:$ Key$ additional$

features$and$contract$conditions$$

* Discounts* Fixed*term*

Early*Termination*Fee*

Late*Payment*Fee*

Pay*on*time*discounts*

Other**

AGL^$ 5%$off$

usage$

3$years$ Up$to$$75$ $14$ 3%$off$usage$ Yes$

Origin^^$ 12%$off$

usage$

1$year$ $70$ $12$ 2%$off$

consumption$

Yes$

Energy$

Australia$$

4%$off$bill$ 3$years$ Up$to$$90$ No$ 3%$off$bill$ No$

$

Simply$ No$ 2$years$ Up$to$$95$ No$ 15%$off$usage$ No$

Alinta$ No$ No$ No$ No$ 15%$off$usage$ No$

Lumo$ No$ 2$years$ $75$ No*$ 15%$off$bill$

$

No$

Powerdirect**$ 12%$off$

usage$

3$years$ $48$ $14$ No$ No$

Red$Energy$ No$ 2$years$ Up$to$$95$ No*$ 10%$off$bill$

$

No$

Momentum$ No$ 1$year$ No$ No*$ No$ No$

^$AGL’s$offer$includes$a$further$2%$off$consumption$rates$if$bills$are$paid$by$direct$debit$

^^$Origin’s$offer$includes$a$further$1%$off$consumption$rates$if$bills$are$paid$by$direct$debit$and$1%$off$

electricity$consumption$if$customer$signs$up$for$gas.$

*The$Price$and$Product$Information$Statements$do$not$stipulate$whether$late$payment$fees$apply.$

**Powerdirect’s$discount$on$usage$does$not$include$controlled$offOpeak.$

$

Note:$Examples$of$other$features$include$loyalty$bonuses,$credits$to$the$account$upon$commencing$a$

contract$and$shop$vouchers.$

$

$

Pay$ on$ time$ discounts$ are$ becoming$ an$ increasingly$ common$ feature$ of$ energy$

market$offers.$$In$South$Australia,$however,$high$discounts$conditional$upon$prompt$

payment$are$still$a$ feature$more$commonly$offered$by$2nd$tier$retailers.$ $That$said,$

the$difference$ in$ annual$ bills$ between$ those$paid$on$ time$and$ those$paid$ late$has$

increased$since$last$year.10$Pay$on$time$discounts$combined$with$late$payment$fees,$

means$ that$ South$ Australian$ households$ can$ be$ significantly$ penalised$ for$ late$

payment.$Or$conversely,$South$Australian$households$can$be$significantly$rewarded$

for$prompt$payment.$$It$does,$however,$highlight$an$issue$that$negatively$impacts$on$

households$with$cashOflow$problems.$

$

*********

10$See$St$Vincent$de$Paul$Society,$South$Australian$Energy$Prices$2009O2012,$August$2012$at$

www.vinnies.org.au/energy$

12

Table*4:$Difference$($)$in$annual$bill$between$paying$all$bills$on$time$vs.$paying$all$bills$late$

(based$on$6,000kWh$per$annum,$single$rate,$4$bills$per$annum).$Electricity$offers$taking$

affect$after$July$2013.$$

$

* Difference*July*2013$Standard*contract/transitional*offer* $56$AGL* $118$Origin* $92$Energy*Australia* $74$Simply* $325$Alinta* $326$Lumo** $360$Powerdirect* $56$Red*Energy** $239$Momentum** $0$

*$The$Price$and$Product$Information$Statements$do$not$stipulate$whether$late$payment$fees$

apply$and$these$calculations$do$therefore$not$include$a$late$payment.$

$

Table$4$above$shows$that$paying$ late$can$become$very$expensive$on$some$market$

offers.$ $ Households$ with$ Simply,$ Alinta,$ and$ Lumo,$ for$ example,$ can$ be$ between$

$325O$360$worse$off$if$they$pay$late$compared$to$paying$on$time.$$

$

Chart$6$below$shows$the$estimated$annual$electricity$bill$for$customers$that$always$

pay$on$time$and$for$those$who$always$pay$late,$for$published$electricity$offers.$$$

*Chart*6*Estimated$annual$bill$for$customers$that$pay$on$time$vs.$pay$late,$electricity$offers$as$

of$July$2013,$Single$rate,$6,000kWh$(GST$inc)11$$

$

$

$

11$Annual$bill$calculation$includes$discounts,$pay$on$time$discounts$and$late$payment$fees$as$

per$energy$offer.$$

1,500!

1,700!

1,900!

2,100!

2,300!

2,500!

2,700!

Annual&bill&($)&

Paid!on!time!

Paid!late!

13

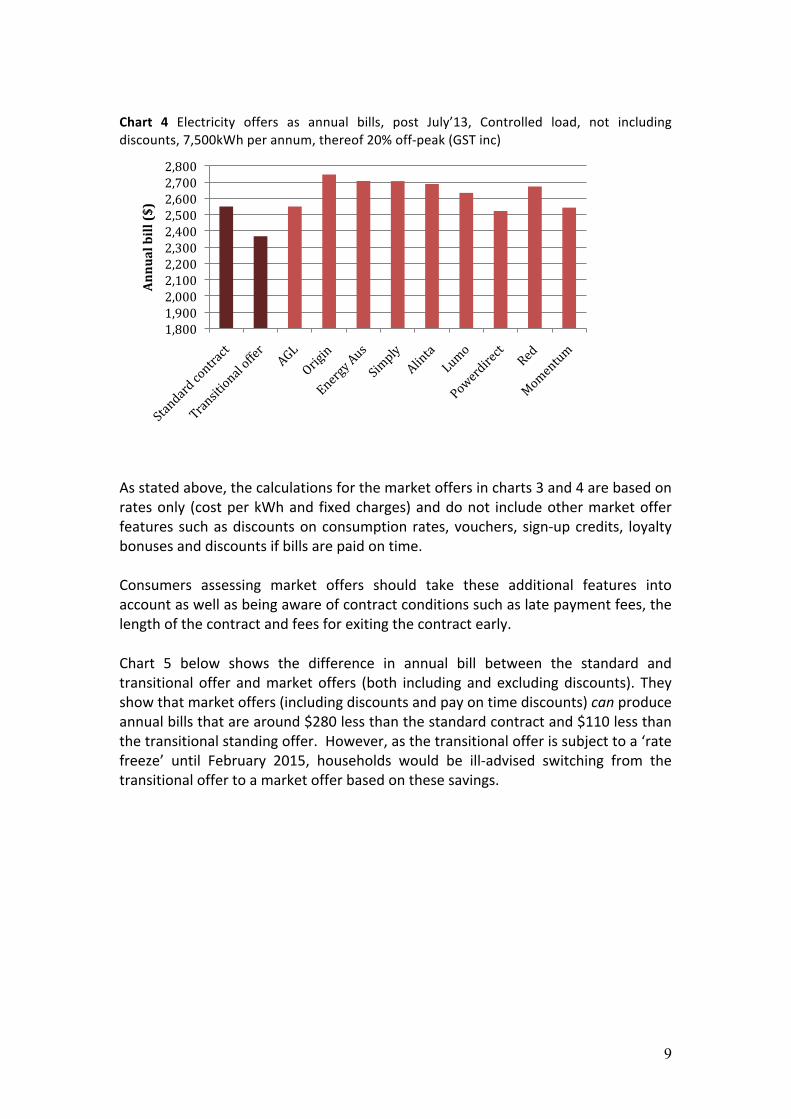

Households$ always$ able$ to$ pay$ their$ electricity$ bills$ by$ the$ due$ date$ can$ save$

significantly$ by$ switching$ from$ the$ standard$ contract$ offer$ to$ a$ market$ offer.$ $ By$

switching$ from$ the$ standard$ contract$ offer$ to$ Powerdirect’s$market$ offer$ a$ typical$

consumption$household$may$save$$280$per$annum.$Lumo$and$Alinta$also$have$offers$

that$could$shave$more$than$$200$off$the$annual$bill$(by$switching$from$the$standard$

contract)$if$always$paid$on$time.$

$

Households$with$cashOflow$problems,$and$thus$late$paying$bills,$are$not$always$able$

to$ achieve$ the$ same$ savings$ by$ switching$ from$ the$ standard$ contract$ offer$ to$ a$

market$ offer.$ Powerdirect’s$market$ offer$ will$ produce$ the$ greatest$ saving$ for$ late$

paying$customers$ looking$ to$switch,$with$an$estimated$annual$saving$of$$280$ for$a$

typical$ consumption$ household.$ $ AGL$ and$Origin’s$market$ offers$would$ produce$ a$

saving$ of$ approximately$ $100$ for$ the$ same$ household.$ The$ greatest$ risk$ for$ late$

paying$customers$ is,$however,$ that$ they$would$be$worse$off$on$half$of$ the$market$

offers$compared$to$the$standard$contract$offer.$$$

*Table*5*Potential$annual$savings$($)$by$switching$from$standard$contract$offer$to$market$

offer$(based$on$6,000kWh$per$annum,$single$rate,$4$bills$per$annum),$electricity$offers$post$

July$2013$

* Paid*on*time* Paid*late*AGL* $165$ $103$

Origin* $131$ $95$

Energy*Australia* $40$ $22$

Simply* $188$ O$81$

Alinta* $201$ O$70$

Lumo** $280$ O$24$

Powerdirect* $284$ $284$

Red*Energy** $175$ O$7$

Momentum** $30$ $86$

*$The$Price$and$Product$Information$Statements$do$not$stipulate$whether$late$payment$fees$

apply$and$these$calculations$do$therefore$not$include$a$late$payment.$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

$

14

2.2*Gas:*Regulated*vs.*market*offers*post*July*201312*There$ are$ very$ few$ gas$market$ offers$ in$ South$ Australia$ and$ the$ only$ area$where$

there$ is$more$ than$ one$market$ offer$ is$ greater$ Adelaide$ (households$ in$ the$ other$

areas$only$have$access$ to$Origin’s$market$offer).$ $As$ such,$ the$below$analysis$only$

comprises$standard$contracts$vs.$market$offers$in$the$greater$Adelaide$area.$Chart$7$

below$shows$that$market$offer$rates$(excluding$additional$discounts)$are$either$the$

same$or$more$than$the$standard$contract.$$$

*Chart*7$Gas$offers$post$July’13,$as$annual$bills$(21,000Mj$per$annum)*

**However,$the$calculations$for$the$market$offers$include$their$rates$only$(cost$per$MJ$

and$fixed$charges)$and$do$not$include$other$market$offer$features$such$as$discounts$

on$ consumption$ rates,$ vouchers,$ signOup$ credits,$ loyalty$ bonuses$ and$ discounts$ if$

bills$are$paid$on$time.$$As$such,$consumers$assessing$market$offers$should$take$these$

additional$features$ into$account$as$well$as$being$aware$of$contract$conditions$such$

as$ late$ payment$ fees,$ the$ length$ of$ the$ contract$ and$ fees$ for$ exiting$ the$ contract$

early.$

************

12$Note$that$due$to$the$new$price$reOsets$post$deregulation$in$February$2013,$most$of$these$

gas$offers$first$took$effect$in$August$2013.$

400!

500!

600!

700!

800!

900!

1,000!

1,100!

1,200!

Standard!contract!

AGL! Origin! Energy!Aus!

Simply! Alinta!

Annual&bill&($)&

15

Table*6*Published$gas$market$offers$in$the$Adelaide$gas$zone$post$July$2013:$Key$additional$

features$and$contract$conditions$

$

* Discounts* Fixed*term*

Early*Termination*Fee*

Late*Payment*Fee*

Pay*on*time*discounts*

Other**

AGL^$ 5%$off$

usage$

2$years$ Up$to$$75$ $14$ 3%$off$usage$ Yes$

Origin^^$ 8%$off$

usage$

1$year$ $70$ $12$ 2%$off$usage$ Yes$

Energy$

Australia$

4%$off$bill$ 3$years$ Up$to$$90$ No$ 8%$off$bill$ No$

$

Simply*$ No$ 2$years$ Up$to$$95$ No$ 10%$off$usage$

$

Yes$

Alinta*$ No$ No$ No$ No$ 10%$off$usage$

$

No$

^$AGL’s$offer$includes$a$further$2%$off$consumption$rates$if$bills$are$paid$by$direct$debit.$

^^$Origin’s$offer$includes$a$further$1%$off$consumption$rates$if$bills$are$paid$by$direct$debit$and$1%$off$

electricity$consumption$if$customer$signs$up$for$gas.$

*$Gas$offers$only$available$in$conjunction$with$electricity$(dual$fuel$offers).$

*Note:$Examples$of$other$features$include$loyalty$bonuses,$credits$to$the$account$upon$commencing$a$

contract$and$shop$vouchers.$

$

$

Chart$8$below$shows$the$difference$in$annual$bill$between$the$standard$contract$and$

market$offers$(both$including$and$excluding$discounts).$They$show$that$market$offers$

(including$ discounts$ and$ pay$ on$ time$ discounts)$ can$ produce$ annual$ bills$ that$ are$around$$75$less$than$the$standard$contract.$

$

Chart* 8*Annual$ bills$ excluding$ vs.$ including$ discounts.$Gas$ offers$ (Adelaide$ area)$ post$ July$2013$as$annual$bills,$21,000Mj$(GST$inc)$

$

$

$

600!

700!

800!

900!

1,000!

1,100!

1,200!

Discounts!excl!

Discounts!incl!

16

However,$all$of$these$gas$market$offers$contain$a$pay$on$time$discount$component$

and$some$offers,$including$the$standard$contract,$contain$late$payment$fees.$$Chart$9$

below$ shows$ the$ estimated$ annual$ gas$ bill$ for$ customers$ that$ always$pay$on$ time$

and$customers$who$do$not$for$published$gas$offers$in$the$Envestra/Adelaide$zone.$$$

*Chart*9$Gas$offers$in$the$Adelaide$area:$Estimated$annual$bill$for$customers$that$pay$on$time$

vs$pay$late,$Based$on$21,000Mj$and$4$bills$per$annum,$GST$incl$

$

$

$

$

Adelaide$ households$ can$ reduce$ their$ gas$ bills$ slightly$ by$ switching$ from$ the$

standard$contract$ to$a$market$offer.$Simply’s$market$offers$will$produce$an$annual$

saving$ of$ approximately$ $75$ for$ customers$ that$ pay$ on$ time,$ while$ late$ paying$

customers$may$save$$60$by$switching$to$Origin.$$

*Table*7*Potential$annual$savings$($)$by$switching$from$regulated$offer$to$market$offer$in$the$

Adelaide$gas$zone$(based$on$21,000Mj,$4$bills$per$annum)$

$

Adelaide*Gas*Zone* Paid*on*time* Paid*late*AGL* $53$ $30$

Origin* $67$ $59$

Energy*Australia* $22$ O$13$

Simply* $74$ $53$

Alinta* $28$ $4$

$

$

*******

600!

700!

800!

900!

1,000!

1,100!

1,200!

$&per&annum&

Paid!on!time!

Paid!late!

17

3.*Supply*charges* **3.1*Electricity*supply*charges*The$supply$charge$is$a$fixed$daily$charge$that$is$paid$in$addition$to$the$consumption$

charges$ for$ electricity$ used.$ $ In$ South$ Australia$ the$ supply$ charge$ for$ regulated$

electricity$offer$ (single$ rate)$ increased$by$60%$ from$July$2009$ to$ July$2012.$Due$ to$

the$‘price$freeze’$agreement$with$AGL,$however,$the$supply$charge$has$not$increased$

for$the$standard$contract$offer$over$the$last$year.$

$

High$ supply$ charges$ result$ in$ low$consumption$households$paying$a$proportionally$

higher$ cost$ per$ unit$ of$ energy$ than$ high$ consumption$ households.$ $ This$ has$

significant$ equity$ implications$ as$ some$ customer$ classes$ characterised$ by$ low$ and$

fixed$income$also$use$less$electricity$than$the$South$Australian$average.$Pensioners$

make$up$one$of$these$lower$consumption$groups.$Consumers$shopping$around$for$a$

better$market$offer$ should$ thus$be$aware$ that$some$retail$offers$have$significantly$

higher$ supply$ charges$ compared$ to$ other$ market$ offers$ as$ well$ as$ the$ standard$

contract.$ $ Chart$ 10$ below$ shows$ the$ daily$ supply$ charges$ (cents$ per$ day)$ for$ the$

various$offers$available$post$July$2013.$Simply’s$supply$charge$at$ just$over$80$cents$

per$ day$ means$ that$ customers$ would$ pay$ almost$ $30$ more$ per$ annum$ in$ fixed$

supply$charge$on$this$offer$compared$to$the$standard$contract.$$$$$

$

$

Chart* 10$ Daily$ supply$ charges$ for$ electricity$ (single$ rate$ and$ controlled$ load),$ standard$contract$and$market$offers$post$July$‘13$

$

*********

50!55!60!65!70!75!80!85!90!

Cents&per&day&

18

3.2*Gas*supply*charges*The$price$discrepancy$between$the$different$retailers’$supply$charges$is$even$greater$

for$ gas.$ Chart$ 11$ shows$ that$ two$ retailers$ have$ a$ daily$ supply$ charge$ of$ 86$ cents$

while$ the$supply$charge$for$ the$standard$contract$offer$ is$71.5$cents$per$day.$ $This$

means$that$customers$on$Energy$Australia$and$Simply$energy’s$market$offers$would$

pay$ over$ $50$ more$ in$ supply$ charges$ per$ annum$ compared$ to$ customers$ on$ the$

standard$contract.$$

*Chart*11*Daily$supply$charges$for$gas,$standard$contract$and$market$offers$post$July$‘13$

*$

$

$

$

$

*******************

50!

55!

60!

65!

70!

75!

80!

85!

90!

Standard!contract!

AGL! Origin! Energy!Aus!

Simply! Alinta!

Cents&per&day&

19

****************$