Embed Size (px)

Citation preview

Intermediate Macroeconomics

Dirk Krueger1 Department of EconomicsUniversity of Pennsylvania

April 2007

1 I would like to thank Charles Jones, Felix Kubler, Beatrix Pall and Tom Sargentfor stimulating discussions about teaching modern macro. All remaining errors aremine.

ii

Contents

1 Introduction 11.1 The Scope of Macroeconomics . . . . . . . . . . . . . . . . . . . . 11.2 US Macroeconomic Data: A Helicopter Tour . . . . . . . . . . . 2

1.2.1 Real GDP . . . . . . . . . . . . . . . . . . . . . . . . . . . 21.2.2 Digression: The Rest of the Course . . . . . . . . . . . . . 31.2.3 Other Macroeconomic Aggregates . . . . . . . . . . . . . 6

2 National Income and Product Accounting (NIPA) 112.1 Gross Domestic Product (GDP) . . . . . . . . . . . . . . . . . . . 11

2.1.1 Computing GDP through Production . . . . . . . . . . . 122.1.2 Computing GDP through Spending . . . . . . . . . . . . 132.1.3 Computing GDP through Income . . . . . . . . . . . . . . 16

2.2 Price Indices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 192.3 From Nominal to Real GDP . . . . . . . . . . . . . . . . . . . . . 202.4 Measuring In�ation . . . . . . . . . . . . . . . . . . . . . . . . . . 212.5 Measuring Unemployment . . . . . . . . . . . . . . . . . . . . . . 222.6 Measuring Transactions with the Rest of the World . . . . . . . . 232.7 Appendix A: More on Growth Rates . . . . . . . . . . . . . . . . 252.8 Appendix B: Chain-Weighted GDP . . . . . . . . . . . . . . . . . 27

3 Economic Growth 333.1 Mathematical Preliminaries . . . . . . . . . . . . . . . . . . . . . 33

3.1.1 Discrete vs. Continuous Time . . . . . . . . . . . . . . . . 333.1.2 Derivatives . . . . . . . . . . . . . . . . . . . . . . . . . . 333.1.3 Some Useful Facts about Logs . . . . . . . . . . . . . . . 343.1.4 Growth Rates (once again) . . . . . . . . . . . . . . . . . 353.1.5 Growth Rates of Functions . . . . . . . . . . . . . . . . . 353.1.6 Simple Di¤erential Equations and Constant Growth Rates 36

3.2 Growth and Development Facts . . . . . . . . . . . . . . . . . . . 373.3 The Solow Model . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

3.3.1 Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 433.3.2 Setup of the Basic Model and Model Assumptions . . . . 433.3.3 Analysis of the Model . . . . . . . . . . . . . . . . . . . . 463.3.4 Introducing Growth . . . . . . . . . . . . . . . . . . . . . 51

iii

iv CONTENTS

3.3.5 Analysis of the Extended Model . . . . . . . . . . . . . . 553.3.6 Evaluation of the Solow Model . . . . . . . . . . . . . . . 64

3.4 The Convergence Discussion . . . . . . . . . . . . . . . . . . . . . 673.5 Growth Accounting and the Productivity Slowdown . . . . . . . 723.6 Ideas as Engine of Growth . . . . . . . . . . . . . . . . . . . . . . 75

3.6.1 Technology . . . . . . . . . . . . . . . . . . . . . . . . . . 753.6.2 Ideas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 763.6.3 Data on Ideas . . . . . . . . . . . . . . . . . . . . . . . . . 79

3.7 Infrastructure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 803.7.1 Cost of Investment . . . . . . . . . . . . . . . . . . . . . . 803.7.2 Bene�ts of Investment . . . . . . . . . . . . . . . . . . . . 81

3.8 Endogenous Growth Models . . . . . . . . . . . . . . . . . . . . . 823.9 Neutrality of Money . . . . . . . . . . . . . . . . . . . . . . . . . 863.10 Summary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 86

4 Business Cycle Fluctuations 894.1 Potential GDP and Aggregate Demand . . . . . . . . . . . . . . 894.2 The IS-LM Framework . . . . . . . . . . . . . . . . . . . . . . . . 92

4.2.1 The Balance of Income and Spending: Keynesian Crossand Multiplier . . . . . . . . . . . . . . . . . . . . . . . . 92

4.2.2 Investment, the Interest Rate and the IS Curve . . . . . . 1054.2.3 The Demand for Money and the LM-Curve . . . . . . . . 1094.2.4 Combination of IS-Curve and LM-Curve: Short-Run Equi-

librium . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1164.2.5 Monetary and Fiscal Policy in the IS-LM Framework . . . 118

4.3 The Aggregate Demand Curve . . . . . . . . . . . . . . . . . . . 1224.4 Unemployment . . . . . . . . . . . . . . . . . . . . . . . . . . . . 123

4.4.1 Concepts and Facts . . . . . . . . . . . . . . . . . . . . . 1244.4.2 Some Theory and the Natural Rate of Unemployment . . 1264.4.3 Unemployment and the Business Cycle . . . . . . . . . . . 129

4.5 The Price Adjustment Process . . . . . . . . . . . . . . . . . . . 1324.5.1 Aggregate Demand, Potential GDP and the Price Adjust-

ment Process . . . . . . . . . . . . . . . . . . . . . . . . . 1364.5.2 Monetary Policy . . . . . . . . . . . . . . . . . . . . . . . 1374.5.3 Fiscal Policy . . . . . . . . . . . . . . . . . . . . . . . . . 138

4.6 Stabilization Policy . . . . . . . . . . . . . . . . . . . . . . . . . . 1404.6.1 Aggregate Demand Shocks and Their Stabilization . . . . 1414.6.2 Price Shocks and Their Stabilization . . . . . . . . . . . . 143

4.7 Real Business Cycle Theory . . . . . . . . . . . . . . . . . . . . . 146

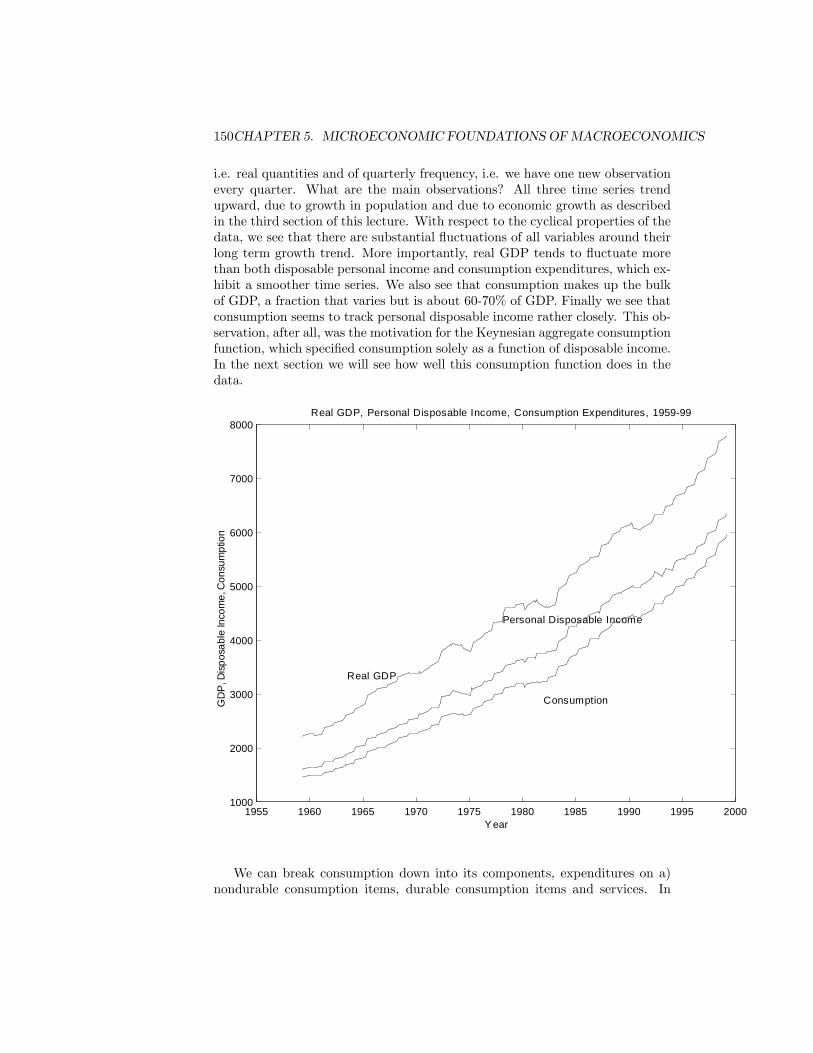

5 Microeconomic Foundations of Macroeconomics 1495.1 Consumption Demand . . . . . . . . . . . . . . . . . . . . . . . . 149

5.1.1 Data on Consumption . . . . . . . . . . . . . . . . . . . . 1495.1.2 The Keynesian Aggregate Consumption Function and the

Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1515.1.3 The Life Cycle/Permanent Income Model of Consumption 153

CONTENTS v

5.2 Investment Demand . . . . . . . . . . . . . . . . . . . . . . . . . 1685.2.1 Facts about Investment . . . . . . . . . . . . . . . . . . . 1685.2.2 The Theory of Investment . . . . . . . . . . . . . . . . . . 171

6 Trade, Exchange Rates & International Financial Markets 1776.1 Terms of Trade, the Nominal and the Real Exchange Rate . . . . 1776.2 E¤ects of the Real Exchange Rate on the Trade Balance . . . . . 1806.3 Determinants of the Real Exchange Rate . . . . . . . . . . . . . . 181

6.3.1 Purchasing Power Parity . . . . . . . . . . . . . . . . . . . 1816.3.2 Real Exchange Rates and Interest Rates . . . . . . . . . . 184

6.4 The International Financial System . . . . . . . . . . . . . . . . . 185

7 Fiscal and Monetary Policy in Practice 1877.1 Fiscal Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 187

7.1.1 Data on Fiscal Policy . . . . . . . . . . . . . . . . . . . . 1877.1.2 A Few Theoretical Remarks . . . . . . . . . . . . . . . . . 195

7.2 Monetary Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . 197

vi CONTENTS

Chapter 1

Introduction

1.1 The Scope of Macroeconomics

Macroeconomics wants to explain the evolution of the main economic aggregatesover time. We are interested in why total production (real GDP) grows over timeon average and why it shows sizeable �uctuations around its long-run growthtrend. We want to understand what causes unemployment and in�ation, howinterest rates behave and what causes a trade de�cit.In contrast to microeconomics, where the object of interest is a single �rm

or household, in macroeconomics we study the whole economy. Our reason-ing, however, will be based on the insights that microeconomic theory provides(therefore the prerequisite requirements for this course).Why should we care about macroeconomics. I could think of three good

reasons

1. It a¤ects us on a day-to-day basis: A rise in the interest rate makes loansfor cars more expensive, raises the interest rate that you pay on a mortgageand (usually) has a negative e¤ect on stock prices. A decline in productionleads to people being laid o¤ -and that could be a member of your family.High in�ation wipes out part of the value of your savings. The list goeson and on....

2. A good understanding of macroeconomics is essential for policy makers.Politicians can change �scal policy (how much the government spendsand how much it taxes you) and central bankers (Alan Greenspan and hisFederal Reserve Board) can change monetary policy (how much currencyto issue and how high to set the Federal Funds Rate -an important interestrate). As we will see later �scal and monetary policy can have good andbad e¤ects on the economy. It is crucial that policy makers and centralbankers understand macroeconomic data and macroeconomic theory tomake an informed decision about when and to what extent to changemonetary and �scal policy.

1

2 CHAPTER 1. INTRODUCTION

3. A good understanding is important for us as good citizens because it helpsus to understand and critic what politicians, central bankers and the presstell us about the economy and what should be done to improve it.

But let�s �rst look at some data to see what it is that we�re talking about,or, to speak with Sherlock Holmes

Data! Data! Data! I can�t make bricks without clay.

1.2 USMacroeconomic Data: AHelicopter Tour

1.2.1 Real GDP

When economists say that the US economy grew 2% last year they usually mean:real Gross Domestic Product (GDP) was 2% higher in 2000 than in 1999. Letus �rst de�ne what nominal GDP is.

De�nition 1 Nominal GDP is the total value of goods and services producedin an economy during a particular time period.

Note that when talking about GDP we have to specify the GDP of whateconomy (e.g. the US) for what time period (e.g. a year, say 2000) we mean.Nominal GDP is measured in dollars. Since prices tend to increase over time(ask your parents how much college tuition cost 30 years ago), so will nominalGDP. To measure the economic activity of a country we are really interestedin how many real goods and services were produced in the economy. This ismeasured by real GDP.

Real GDP =Nominal GDPPrice Level

We will discuss how to compute the �Price Level�in the next section. Finally,a growth rate of a variable is computed as follows. Let Yt denote real GDP inperiod t (i.e. Y2000 is real GDP for the year 2000). Then the growth rate of realGDP from period t� 1 to period t is computed as

gY (t� 1; t) =Yt � Yt�1Yt�1

As an example, suppose real GDP in 1988 equals $ 585 and $ 605 in 1989, thenthe growth rate of real GDP between 1988 and 1989 would equal

gy(1988; 1989) =$605� $585

$585= 0:034 = 3:4%

This is the number that people mean when they say that the economy grew by3:4% in 1989.

1.2. US MACROECONOMIC DATA: A HELICOPTER TOUR 3

Let�s look at some data for real GDP. The solid line in Figure 1 shows theevolution of real GDP for the US economy from 1967 to 2001.1 We have twoprincipal observations

1. Real GDP grows over time. If GDP would have grown at 2.75%, then thegraph of real GDP would have looked like the dotted line. The dotted lineis called �Trend�, because it shows how real GDP evolved on average.

2. Actual real GDP exhibits -occasionally sizeable- deviations from its longterm growth trend. These �uctuations are called business cycles.

Figure 2 shows these �uctuations in more detail. The dotted line at 0 corre-sponds to the trend. When the solid line takes the value -0.061 as in 1983, thismeans that actual real GDP was 6.1% below the trend.

Periods in which real GDP actually declines are called recessions, and, ifthese declines are extremely severe, depressions.2 From 1967 until 2001 the USexperienced 5 recessions.3 Note that, although recessions are recurrent events,the exact timing of a recession is extremely hard to forecast.

1.2.2 Digression: The Rest of the Course

At this stage let�s have a short preview of the course. The two main sections,Sections 3 and 4 deal exactly with the two observations we made about Figure1:In Section 3 we will study why, on average, the economy grows over time.

This area of study is called growth theory and we will discuss the neoclassicalgrowth model. As a sneak preview, the economy grows over time because:

1The data have quarterly frequency, i.e. there one observation for real GDP for each quar-ter. The �rst observation is the GDP for the �rst three months of 1967, the last observationis the GDP for April to June 2001. The data are then converted to yearly numbers (ba-sically by multiplying them by 4). If you are interested in the actual data, on the WWWgo to http://www.economagic.com/em-cgi/data.exe/fedstl/gdp96+1#DataWhat is actuallyplotted is the natural logarithm of real GDP, for the following reason. If GDP grows at aconstant rate g; then the log of GDP is a straight line with slope g: By plotting the log ofGDP we can draw the long-term growth trend as a straight line (rather than an exponentialfunction). This technique is used quite often by economists. Hall and Taylor plot GDP in-stead of log GDP, but use a logarithmic scale on the y-axis on p. 6 (observe that the distancebetween 3500 and 4000 is bigger than between 6000 and 6500 on the y-axis; this is what alog-scale does). Both tricks are equivalent.

2The US economy as well as other economies in the world experienced a depression, theso-called great depression, from 1929 to 1932.

3One de�nition of a recession is �a decline in two subsequent quarters of real GDP�. Ifyou are interested in more detailed information about the timing and length of expansionsand recessions, visit the webpage of the National Bureau of Economic Research (NBER) athttp://www.nber.org/cycles.html. Note that, according to the o¢ cial de�nition of a recession,the U.S. economy is not currently in a recession, as real GDP growth has not been negativein the �rst two quarters of 2001.

4 CHAPTER 1. INTRODUCTION

1970 1975 1980 1985 1990 1995 20008

8.2

8.4

8.6

8.8

9

9.2Real GDP in the United States 19672001

Year

Log

of re

al G

DP

GDP

Trend

1. the population grows. A higher population means that a bigger labor forceis available for the production of goods and services.

2. more capital is accumulated. Over time, more and more machines andother equipment are used in the production process

3. there is technological progress (e.g. the development of faster and fastercomputer chips) makes capital and labor more productive in the produc-tion process.

In Section 4 we will study why there are business cycles, i.e. why the economy�uctuates around its long-term growth trend. In contrast to growth theory,where the level of agreement between economists is fairly high, in business cycletheory there is substantial disagreement about why business cycles exist andwhat the government can do about them. Again a brief sneak preview:

1. in this course we mostly will follow Hall and Taylor (and many others)and assume that in the short run wages and/or prices are �sticky�, i.e. not

1.2. US MACROECONOMIC DATA: A HELICOPTER TOUR 5

1970 1975 1980 1985 1990 1995 20000.08

0.06

0.04

0.02

0

0.02

0.04

0.06

0.08Expansions and Recessions

Year

Perc

enta

ge D

evia

tion

of R

eal G

DP fr

om T

rend

197071recession

197475recession

198082backtoback recessions

199091recession

�exible to adjust immediately to shocks hitting the economy. Potentialshocks could come from the private sector of the economy (a certain dropof households�willingness to buy cars), from world markets (rememberthe oil price shocks in 1973 and 1980) or from changes in monetary and�scal policy. The results are business cycles.

2. an alternative view holds that business cycles originate from �technologyshocks� (e.g. in certain years we have bad weather and that makes pro-duction, in particular agricultural production, more di¢ cult). Prices andwages are fully �exible even in the short run. People respond optimallyand work more when the conditions are such that they are productive (inyears of good technology shocks) and less when they are not so productive.Hence in good years workers supply a lot of labor and production (realGDP) is high, in years with bad technology workers supply little laborand real GDP is low. This view has become known as �Real BusinessCycle Theory�(�Real�because the shocks underlying business cycles are

6 CHAPTER 1. INTRODUCTION

technology shocks).4

The dispute between these two schools is not only theoretical. Based ontheory, economists from both camps have di¤erent views about economic pol-icy. In RBC-theory business cycles arise because households react optimallyto technology shocks. Hence there is no role for government policy to improvematters. If business cycles come about because prices and wages can�t adjust inthe short run (as in the �rst view), there may be a role for an active monetaryand �scal policy to reduce the economic �uctuations.Common among both schools is that they both use models -abstract simple

descriptions of the economy, either with equations or graphs- to explain busi-ness cycles and to argue for or against a certain policy. We will follow thismethodological approach.

1.2.3 Other Macroeconomic Aggregates

Why are business cycles bad? Because if real production declines, workers getlaid o¤ and the unemployment rate increases. We should expect that theunemployment rate follows the path of real output rather closely. Let us �rstde�ne the unemployment rate.

De�nition 2 The labor force is the number of people, 16 or older, that areeither employed or unemployed but actively looking for a job. The unemploymentrate is given by

Unemployment Rate =number of unemployed people

labor force

In Figure 3 we plot the unemployment rate for the US from 1967 to 2001.5

We see that in recessions the unemployment rate increases, whereas in expansionit decreases. A variable that shows such a behavior is called �countercyclical�:it is high when real GDP is low (relative to trend) and it is low when real GDPis high. Also note that currently unemployment is at its lowest level since 1970.

Another important macroeconomic variable is the in�ation rate. It mea-sures the growth rate of the price of a particular basket of goods and services.6

Let Pt be the price level in period t: Then the in�ation rate between periodst� 1 and t is given by

�t = gP (t� 1; t) =Pt � Pt�1Pt�1

4The founders of RBC-theory are Finn Kydland from Carnegie Mellon University and EdPrescott from the University of Minnesota -incidentally my Ph.D. thesis advisor.

5The unemployment rate is measured by the Bureau of Labor Statistics (BLS). Go to theirhomepage at http://stats.bls.gov/top20.html if you want to have a look at the original data.

6There are several measures of the in�ation rate. They are distinguished by what goodsand services are included in the basket of goods whose price is measured. The two mostimportant indexes for in�ation are the Consumer Price Index (CPI) and the GDP de�ator.Both will be discussed in the next section.

1.2. US MACROECONOMIC DATA: A HELICOPTER TOUR 7

1970 1975 1980 1985 1990 1995 20002

3

4

5

6

7

8

9

10

11

12Unemployment Rate for the US 19672001

Year

Une

mpl

oym

ent R

ate

197071recession

197475recession

198082backtoback recessions

199091recession

Figure 4 shows the in�ation rate for the US economy from 1967 to 2001.We see that in�ation rates were higher and more volatile in the 70�s and early80�s than in the 90�s. Combining �gure 2 and 4 it is not apparent whether thein�ation rate is procyclical or countercyclical.

Interest Rates are important macroeconomic variables because they de-termine how costly it is to take out a loan to buy a car, a house, stocks, or, for�rms, to �nance new equipment. How are interest rates computed. Suppose inperiod t � 1 you borrow the amount $Bt�1. The loan speci�es that in periodt you have to repay $Bt: In general $Bt will be bigger than Bt�1 (since youhave to repay Bt�1; the so-called principal, and the interest on the loan): Thenominal interest rate on the loan from period t� 1 to period t, it; is computedas

it =Bt �Bt�1Bt�1

8 CHAPTER 1. INTRODUCTION

1970 1975 1980 1985 1990 1995 20000

2

4

6

8

10

12

14

16Inflation Rate for the US 19672001

Year

Infla

tion

Rat

e

This is called a nominal interest rate because it does not take into accountin�ation. The real interest rate rt is de�ned as the di¤erence between thenominal interest rate and the in�ation rate:

rt = it � �t

Note that nominal interest rates historically tend to rise with in�ation: lendersdemand a higher nominal interest rate in times of high in�ation as compensationfor the loss of purchasing power of their money, due to high in�ation.Example: In the year 2000 you borrow $15; 000 to buy a new car and the

bank asks you to repay $16; 500 exactly one year later. Then the yearly nominalinterest rate from 2000 to 2001 is

i2001 =$16; 500� $15; 000

$15; 000= 0:1 = 10%

Now suppose the in�ation rate is 3% in 2001. Then the real interest rate equals10%� 3% = 7%

1.2. US MACROECONOMIC DATA: A HELICOPTER TOUR 9

Note that whenever stating an interest rate, it is crucial to state the lengthof the period with respect to which it applies, i.e. whether it is a yearly, aquarterly, a monthly or a daily interest rate.In Figure 5 the nominal interest rate for the US economy from 1967 to 2001

is plotted.7 Comparing Figure 2 and Figure 5 indicates that interest rates tendto be procyclical: they increase during expansions and fall during recessions.

1970 1975 1980 1985 1990 1995 20000

2

4

6

8

10

12

14

16

18

20Federal Funds Interest Rate 19672001

Year

Nom

inal

Inte

rest

Rat

e in

%

Now we have a rough idea about how the most important macroeconomicvariables evolved over the last 30 years. Now we turn to a discussion how thesevariables are actually measured in the data.

7There are many di¤erent interest rates. The Federal Funds rate is the interestrate that banks charge each other for loans from one evening to the next morning.So this is a daily interest rate. This daily interest rate has been converted into ayearly interest rate by �multiplying� the daily rate by 365. For the original data go tohttp://www.stls.frb.org/fred/data/irates.html.

10 CHAPTER 1. INTRODUCTION

Chapter 2

National Income andProduct Accounting(NIPA)

In this section we look in detail at how the macroeconomic aggregates whosebehavior over the last thirty years we studied in the last section are de�ned andmeasured in the data. We will start with gross domestic product (GDP).

2.1 Gross Domestic Product (GDP)

We de�ned nominal and real GDP in the last section. Now will we discuss howwe measure these entities in the data. Nominal GDP can be measured in threedi¤erent ways which all lead to the same result:1

1. We can measure nominal GDP by adding together the value of productionin all di¤erent industries in the economy.

2. We can measure nominal GDP by adding together the spending on goodsand services of the di¤erent sectors of the economy (households, �rms, thegovernment and foreigners).

3. We can measure nominal GDP by adding together all the income that isgenerated from the production process: wages, salaries and pro�ts.

In fact, the Bureau of Economic Analysis (BEA), the US government agencythat is responsible for measuring GDP, does calculate GDP in these three dif-ferent ways and makes sure that the three numbers they get coincide (as theyshould according to accounting principles).

1The fact that the total value of production always equals the total value of spending andalways equals the total income is called an identity, it is inevitably true as a consequence ofaccounting principles.

11

12CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

2.1.1 Computing GDP through Production

We want to calculate nominal GDP by adding together the value of productionfor all di¤erent industries in the economy, agriculture, mining, construction,manufacturing etc. Can we just add together all those industries�sales? Con-sider the following example: US steel produces a ton of steel and sells it toGM for $1500. GM then uses this steel to build a car that it sells for $10,000.Assume for the moment that a car can be produced only with steel and labor.Should the contribution to GDP be the whole $11,500, the sum of total sales?No, since the steel has been counted double; once when it was sold from US

Steel to GM and once when it, as a part of the car, was sold by GM. But itwas only produced once, so we should only count it once. This is achieved bythe concept of value added. It basically measures how much a �rm, in itsproduction process, added to the value of the intermediate goods it purchasedfrom its suppliers. Roughly, value added of a �rm equals its revenues from salesminus the purchases of intermediate goods -goods that the �rm bought fromother �rms and used to produce its own products.For the example then, the contribution should be only $1500 (from the sale

of steel to GM, the value added of US Steel) plus $8500 (the value added ofGM, equal to the total sale of $10,000 minus the purchase of the intermediategood steel for $1,500).So when we measure nominal GDP through production, we sum up the

value added of all industries in the economy, because the value added (andnot the sales) are the correct contributions of the industries to production. Table1 shows the contribution of di¤erent industries to nominal GDP for 1999. Thenumbers in column 2 are in billions of dollars.2

Table 1Industries Value Added in % of Tot. Nom. GDP

Total Nom. GDP 9,299.2 100.0%Agriculture, Forestry, Fishing 125.4 1.3%Mining 111.8 1.2%Construction 416.4 4.5%Manufacturing 1,500.8 16.1%Transportation, Publ. Utilities 779,6 8.4%Wholesale Trade 643.3 6.9%Retail Trade 856.4 9.2%Finance, Insurance, Real Estate 1,792.1 19.3%Services 1,986.9 21.4%Government 1,158.4 12.5%Statistical Discrepancy -71.9 -0.8%

Note that total nominal GDP in 1999 was $US 9,299.2 billion, or $US9,299,200,000,000. To make this number a little less intimidating, economists

2All data in this section come from the Economic Report of the President (2001).

2.1. GROSS DOMESTIC PRODUCT (GDP) 13

often report GDP per capita. On average in 1999 the population of the US was275,372,000. Hence GDP per capita in 1999 amounted to $33,769.59. In 1999every person in the US, from the newborns to the old, produced on averageabout $34,000 worth of goods and services.

2.1.2 Computing GDP through Spending

Nominal GDP can also be computed by summing up the total spending ongoods and services by the di¤erent sectors of the economy. Formally, let

C = Consumption

I = (Gross) Investment

G = Government Purchases

X = Exports

M = Imports

Y = Nominal GDP

ThenY = C + I +G+ (X �M)

Let us turn to a brief description of the components of GDP:

� Consumption (C) is de�ned as spending of households on all goods, suchas durable goods (cars, TV�s, Furniture), nondurable goods (food, cloth-ing, gasoline) and services (massages, �nancial services, education, healthcare). The only form of household spending that is not included in con-sumption is spending on new houses.3 Spending on new houses is includedin �xed investment, to which we turn next.

� Gross Investment (I) is de�ned as the sum of all spending of �rms on plant,equipment and inventories, and the spending of households on new houses.It is broken down into three categories: residential �xed investment(the spending of households on the construction of new houses), non-residential �xed investment (the spending of �rms on buildings andequipment for business use) and inventory investment (the change ininventories of �rms). To make the concept of investment clearer, we haveto take a little digression about stocks and �ows.

A stock is a quantity measured at a given point in time. A �ow is a quantitymeasured per unit of time. As an example consider �lling a bathtub with water.The amount of water in the tub is a stock -we say that the bathtub contains50 gallon of water. The amount of water �owing out of the faucet is a �ow

3What about purchases of old houses? Note that no production has occured (since thehouse was already built before). Hence this transaction does not enter this years�GDP. Ofcourse, when the then new house was �rst bought by its �rst owner it entered GDP in theparticular year.

14CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

-we say that 2 gallon of water per minute �ow into the tub. Note that wemeasure the stock by gallon, the �ow by gallon per minute. Often stocks and�ows are related. In our example the stock of water in the tub equals theaccumulated �ow of water out of the faucet. The same is true with investmentand the capital stock. The capital stock of an economy is the typical economicexample of a stock, whereas investment, like GDP and its other componentsconsumption, government purchases etc. are �ow variables.4 The capital stockis the total amount of physical capital in the economy, including all buildings andequipment. Part of the capital stock wears out every period in the productionprocess, a process called depreciation (which is again a �ow variable). Wehave the following relationship between the capital stock, gross investment anddepreciation:

Capital Stock at end of this period = Capital Stock at end of last period

+Gross Investment in this period

�Depreciation in this period

We de�ne net investment as

Net Investment = Gross Investment�Depreciation

and therefore

Net Investment = Capital Stock at end of this period

�Capital Stock at end of last period

Note that what enters nominal GDP is gross, not net investment, but that netinvestment in this period equals the change of the capital stock from the end oflast to this period.What residential and nonresidential �xed investment are and why they are

included in nominal GDP is rather obvious. So let�s spend some time to un-derstand inventory investment. Suppose in 1999 Ford produces a car that youpurchase in 1999. Then your spending on the car enters GDP as consumptionunder C: But now suppose Ford produces the car and puts it in its stock forsale in 2000. Since the car is not sold yet, it doesn�t enter GDP as consumptionin 1999. But Ford�s production activity is the same, no matter whether thecar was sold or not in 1999, so the contribution to GDP should be the same.The key is inventory investment: By producing now and putting the car in itsstock, Ford increased its inventory by one car, and the statisticians count thisas investment in inventories. By the same token as before

Inventory Investment = Stock of Inventories at end of this year

�Stock of Inventories at the end of last year

Sometimes the variable �nal sales is reported in the news. (Nominal) �nalsales equal nominal GDP minus inventory investment.

4Remember the de�nition of nominal GDP: it is the total value of goods and servicesproduced in an economy during a particular time period, i.e measured in units per timeperiod.

2.1. GROSS DOMESTIC PRODUCT (GDP) 15

� Government spending (G) is the sum of federal, state and local governmentpurchases of goods and services. Note that government spending does notequal total government outlays: transfer payments to households (suchas welfare, social security or unemployment bene�t payments) or interestpayments on public debt are part of government outlays, but not includedin government spending G:

� As an open economy, the US trades goods and services with the rest ofthe world. Exports (E) are deliveries of US goods and services to the restof the world, imports (M) are deliveries of goods and services from othercountries of the world to the US. Why are imports subtracted from exportswhen computing GDP. Suppose Boeing buys 4 jet engines from the Britishcompany Rolls Royce, puts them into a Boeing 747 and sells the aircraftto the French airline Air France. What has been produced in the US wasthe plane, excluding the engines. So we count the plane as exports outof the US, the engines as import into the US and the net contribution toGDP is (X�M), that is, exports minus imports. The quantity (X�M) isalso referred to as net exports or the trade balance. We say that a country(such as Germany) has a trade surplus if exports exceed imports, i.e. ifX �M > 0. A country has a trade de�cit if X �M < 0; which was thecase for the US in recent years.

In Table 2 you can see the composition of nominal GDP for 1997, brokendown to the di¤erent spending categories discussed above. Again the numbersare in billion US dollars.

Table 2in billion $ in % of Tot. Nom. GDP

Total Nom. GDP 9,299.2 100.0%Consumption 6,268.7 67.4%Durable GoodsNondurable GoodsServices

761.31,845.53,661.9

8.2%19.8%39.3%

Gross Investment 1,650.1 17.7%NonresidentialResidentialChanges in Inventory

1,203.1403.843.3

12.9%4.3%0.5%

Government Purchases 1,634.4 17.6%Federal GovernmentState and Local Government

586.61,065.8

6.3%11.5%

Net Exports -254.0 -2.7%ExportsImports

990.21,244.2

10.6%13.4%

Final Sales 9,255.9 99.5%

16CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

2.1.3 Computing GDP through Income

The production of goods and services generates income, either in the form ofwages and salaries for workers, or in the form of pro�ts for individuals runninga business. This fact provides a third way of computing nominal GDP. Thebroadest measure of the total incomes of all Americans is called national in-come. It is closely related, but not equal to nominal GDP. Remember that USGDP is the value of goods and services produced in the US. Some people inthis country are not Americans, so, although they contribute to US GDP, theirincome is not part of national income. On the other hand there are Americanswho produce goods and services abroad, so they don�t contribute to US GDP,but their income is part of national income. When we add to GDP factorincome from the rest of the world (income of Americans not earned inAmerica) and subtract factor income to the rest of the world (incomeof Non-Americans earned in the US, like my salary) we arrive at Gross Na-tional Product (GNP). GNP is the value of all goods and services producedby Americans, whereas GDP is the value of all goods and services produced inAmerica. There are other parts of GNP that are not part of national income.First we have to subtract depreciation, Since depreciation of capital is a costof producing the output of the economy, subtracting depreciation shows thenet result of economic activity. GNP minus depreciation equals Net NationalProduct (NNP). From NNP we subtract sales and excise taxes to obtainnational income.5 This is due to the fact that NNP is measured in termsof the prices that �rms receive for their products, but only that part of theseprices which does not go to the government becomes income of households. Sothe connection between GDP and national income is given by (in brackets thenumbers for the US in 1999, in billion $US).

Gross Domestic Product (9,299.2)

+Factor Income from abroad (305.9)

�Factor Income to abroad (316.9)= Gross National Product (9,288.2)

�Depreciation (1,161.0)= Net National Product (8,127.1)

�Sales and Excise Taxes (718.1)�Other Adjustments6 (-3.8)

= National Income (7,469.7)

National Income is divided into �ve components, depending on the way theincome is earned:

5Other minor corrections of NNP to obtain national income are the following. To NNPwe add net subsidies of the government to government businesses, and we substract businesstransfers (gifts of businesses) and statistical discrepancy. These adjustments are of minorimportance.

2.1. GROSS DOMESTIC PRODUCT (GDP) 17

1. Compensation of Employees: wages, salaries and fringe bene�ts earned byworkers

2. Proprietors�Income: income of noncorporate business, such as small farmsand law partnerships

3. Rental Income: income that landlords receive from renting, including the�imputed� rent that homeowners pay themselves, less expenses on thehouse, such as depreciation

4. Corporate Pro�ts: income of corporations after payments to their workersand creditors

5. Net interest: interest paid by domestic businesses plus interest earnedfrom foreigners

Commonly the �rst component is called labor income, components 2 to 5together are called capital income.7 The labor share is de�ned as the fractionof national income that goes to labor income, the capital share is de�ned asthe fraction of national income that goes to capital income. Formally

Labor Share =Labor IncomeNational Income

Capital Share =Capital IncomeNational Income

Obviously, since national income equals labor income plus capital income, thelabor share and the capital share sum to 1. In Table 3 you can �nd nationalincome and its component for the US in 1999

Table 3Billion $US % of National Income

National Income 7,469.7 100.0%Compensation of Employees 5,299.8 71.0%Proprietors�Income 663.5 8.9%Rental Income 143.4 1.9%Corporate Pro�ts 856.0 11.5%Net Interest 507.1 6.8%

We see that for 1999 the labor share equals 71% and the capital share equals29%.Finally, let us relate national income to two other, commonly used income

concepts that may coincide more with your common understanding about whatthe income of a household (or in our case the income of all households) is. Aseries of adjustments takes us from national income to personal income, the

7There is some ambiguity about counting proprietors� income as capital income, sincearguably the labor of the farmer is one of the most important inputs to the farms�productionof agricultural products.

18CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

income that households and noncorporate businesses receive. First we have toreduce national income by that fraction of corporate pro�ts that are not paid outin the form of dividends. This entity is called retained earnings. Second wehave to subtract contributions for social insurance (the amount paid to thegovernment for social security and medicare). Third, we want to include interestpayments that households receive, rather than interest payments that businessespay. This is accomplished by reducing national income by net interest paid bybusinesses and adding personal interest income. Finally we add to nationalincome transfers from the government and businesses to households, suchas social security bene�ts and pensions paid by �rms to their retired employees.The relation between national income and personal income is then given by (inbrackets again the numbers for 1999 in billion $US)

National Income (7,469.7)

�Retained Earnings (485.7)�Contributions for Social Insurance (662.1)�Net Interest (507.1)+Personal Interest Income (963.7)

+Government and Business Transfers (1,016.2)

= Personal Income (7,789.6)

Finally, we arrive at Disposable Personal Income (the income that house-holds and noncorporate businesses can spend, after having satis�ed their taxobligations) by subtracting from personal income personal tax and nontaxpayments (such as parking tickets) to the government:

Personal Income (7,789.6)

�Personal Tax and Nontax Payments (1,152.0)= Disposable Personal Income (6,637.6)

This concludes the discussion of how nominal GDP is measured. As you seefrom the numbers for 1999 (and as you will see in the problem sets) all threemethods indeed lead to the same result.One last, but very important fact follows from the equivalence of GDP mea-

sured by spending and measured by income. For simplicity let us consider aneconomy without government and international trade.8 Saving (S) is de�ned asincome minus consumption, or

S = Y � C

But from the spending side of GDP we know that

Y = C + I

8Hall and Taylor show the argument that will follow for the general case with governmentand international trade. The reader is refered to the book for details.

2.2. PRICE INDICES 19

(remember that we assumed that G = X = M = 0). Substituting for Y in the�rst equation we get

S = Y � C= C + I � C= I

Hence saving equals investment. This is again an accounting identity, it is alwaystrue. Note that this identity of saving and investment also holds for the generalcase with government and foreign trade, with saving and investment rede�nedto account for the presence of the government and other countries. It is a crucialidentity that we will use over and over again in growth theory and business cycletheory.

2.2 Price Indices

To compute real GDP we divide nominal GDP by the �Price Level�. To computethe in�ation rate we need price levels in two di¤erent periods. In this sectionwe discuss how we measure the �Price Level�. In general economists measurethe price level by a price index. A price index is a ratio between the price of aparticular basket of goods in period t and the price of the same basket in a baseperiod, say period 0: There are two important questions involved in constructinga price index: a) what period to chose as base period b) what basket of goodsto chose.Let�s consider a very simple economy in which people just produce and

buy two goods, say hamburgers and coke. We denote by ht the amount ofhamburgers consumed (and produced) in period t; and by ct the amount of cokeconsumed in period t: Also let Pht be the price of one hamburger in period t andpct the price of one bottle of coke in period t: Let (h0; c0; ph0; pc0) denote thesame variables at period 0: Now let�s ask ourselves how one would measure theprice level in period t as compared to period 0; which we will take as our baseperiod? One option is to compare how expensive the basket of goods consumedin period 0 are in period t: The result is

Lt =phth0 + pctc0ph0h0 + pc0c0

Such a price index is called a Laspeyres price index. If, on the other hand, wetake as our basket the goods purchased in period t; then we have

Pat =phtht + pctctph0ht + pc0ct

Such a price index is called a Paasche price index. It turns out that all priceindices actually used in practice to compute real GDP or the in�ation rate areeither Laspeyres or Paasche price indices. Before turning to this point, a brief

20CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

comment about these indices. Unfortunately both have their problems.9 Theproblem with the Laspeyres price index is that it tends to overstate in�ationby assuming that households buy the same basket of goods in period t as inperiod 0: But as prices change from period 0 to period t; consumers tend tosubstitute goods that have become relatively more expensive from period 0 toperiod t with goods that have become relatively less expensive. By holdingthe basket of goods �xed at the basket bought in period 0; the Laspeyres priceindex ignores this substitution e¤ect, which tends to lead to an overstatementof in�ation. Now let�s look at the Paasche price index. Consider the followingscenario: suppose a virus is detected in all coke bottles in the country at periodt; so that at period t no coke is produced (and the price of the few bottles in thestores from last year sky-rockets). And suppose that the price for hamburgersstays constant between period 0 and t:What would the Paasche index say aboutthe price level in period as opposed to period 0: Since the Paasche index usesthe basket of goods in period t; and since no coke is produced in period t; theprice change for coke does not have any e¤ect, and the Paasche index wouldbe at Pat = 1 (under the assumption that hamburger prices have remainedconstant). But would we really think that the situation just described is one inwhich prices have remained constant, as the Paasche index indicates. In general,because of this problem the Paasche index tends to understate in�ation. Butnow let�s leave the general theory of price indices and talk about real GDP andin�ation

2.3 From Nominal to Real GDP

Real GDP is the meant to measure the total production of goods and servicesin physical units. But how does one add 10 cars, twelve haircuts and a cruisemissile together to one number? What statisticians do in practice to determinereal GDP is the following: they pick a base year, say 1996. The contributionof computers to real GDP in 2000 is then computed as follows: take the dollaramount spent on computers in 2000 and divide by the price of computers in2000 relative to 1996 (i.e. divide by the price in 2000 and multiply by the pricein 1996). The result the total value of computers sold in 2000 in prices of 1996.Summing up all goods and commodities, evaluated at their 1996 prices, yieldsreal GDP. Note that for the base year nominal and real GDP always coincide.The ratio between nominal and real GDP turns out to be a price index, theso-called GDP-de�ator:

GDP de�ator =Nominal GDPReal GDP

9 In fact, the problem of how to construct an ideal price index is a deep methologicalproblem, know as the index number problem. It has not been, and in fact can�t be fullyresolved. Also it is hard to say which of the two indices discussed is superior.

2.4. MEASURING INFLATION 21

To see why this is, suppose again that our economy produces only hamburgersand coke. Nominal GDP in 2000 would be given by

Nominal GDP = h2000ph2000 + c2000pc2000

Real GDP would be given by (assuming 1996 is the base year)

Real GDP = h2000ph1996 + c2000pc1996

From the previous formula we get

GDP de�ator =h2000ph2000 + c2000pc2000h2000ph1996 + c2000pc1996

This should look familiar to you; in fact the GDP de�ator is a Paasche priceindex; compare this formula to the one for a Paasche price index in the previoussection.

2.4 Measuring In�ation

Remember that the in�ation rate from period t� 1 to period t was de�ned as

�t =Pt � Pt�1Pt�1

where Pt is the price level in period t: One possibility to compute the in�ationrate is to take as the price level the GDP de�ator from the previous section.The basket of goods on which the in�ation rate is then based corresponds tothe current composition of GDP. More often an in�ation rate is reported thatuses a di¤erent basket of goods and services.10

Mostly when the in�ation rate is reported in the news, it is based on theConsumer Price Index (CPI), which the Bureau of Labor Statistics determinesevery month. The news release of this monthly number is followed with wideinterest for the following reasons. The Federal Reserve Bank, who is responsiblefor monetary policy, bases its decision on the development of the in�ation rate,as its major objective is to achieve �price stability�. A higher than expectedin�ation rate causes the FED to increase interest rates, which usually a¤ectthe stock market adversely. Knowing this in advance, the stock market tendsto react negatively to higher than expected in�ation and positively to lowerthan expected in�ation. It is also important because many contracts include so-called COLA�s, cost-of-living adjustments that specify that payments increaseproportionally to the CPI. This is the case for social security bene�ts, for ex-ample. So the CPI is likely the most-watched macroeconomic variable. How isit computed?

10When we are concerned about how the purchasing power of a typical household haschanged over time, a basket of goods that includes cruise missiles, oil platforms and the like(as for the GDP de�ator) may not be very informative.

22CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

Basically, the BLS determines a basket of goods and services that a typicalAmerican household buys in a typical month of the base year. This basketincludes 4 loafs of bread, a case of beer, 1/60 of a car, 4 haircuts and so forth.The BLS then determines how much this basket cost in a typical month of thebase year, and how much it cost in a typical month this year. The CPI for thismonth equals the ratio between the price of the basket in this year and the pricein the base year. Again suppose that the BLS decided that the correct basketwas composed only of hamburgers and coke (and the base year is 1996), thenthe CPI for 2000 is given by

CPI =h1996ph2000 + c1996pc2000h1996ph1996 + c1996pc1996

Again note that this is exactly a Laspeyres price index from the previous section.The in�ation rate is then computed using as price level in period t; Pt the CPIfor period t:

There is a recent political discussion about whether the CPI overstates in-�ation. One problem that we already discussed in the previous section is thatpeople may substitute away from goods that have become relatively more expen-sive. A second problem is the introduction of new goods. Since new goods arenot included in the base year basket, they have no e¤ect on the CPI. Arguably,however, the introduction of new goods makes consumers better o¤. A thirdproblem is unmeasured changes in quality. Suppose a good gets better withoutthis improvement being re�ected in the price (maybe because the improvementis hard to measure), then the CPI remains unchanged although it should havefallen. This problem is not only academic. Because of the COLA�s, governmentoutlays depend signi�cantly on how in�ation is measured. Suppose the CPIoverstates true in�ation by one percentage point (this is the magnitude thatsome economists believe is realistic), then the government in 1997 paid about$10 billion too much for social security bene�ts, quite a signi�cant number.

2.5 Measuring Unemployment

Remember our de�nition of the unemployment rate as the ratio between thenumber of unemployed people and the labor force. In practice about 100,000adults in each month are interviewed and asked about whether they are em-ployed, and, if not, are asked if they are actively looking for a job (i.e. if theyare in the labor force).11 . The number of people that are unemployed and thenumber of people in the labor force are counted and the ratio computed, whichgives the unemployment rate for that month.

11Asking everybody in the US would be quite expensive, and a sample of 100,000 gives aquite accurate description of the entire population.

2.6. MEASURING TRANSACTIONSWITH THE REST OF THEWORLD23

2.6 Measuring Transactions with the Rest of theWorld

We already de�ned what the trade balance is: it is the total value of exportsminus the total value of imports of the US with all its trading partners. Aclosely related concept is the current account balance. The current accountbalance equals the trade balance plus net unilateral transfers

Current Account Balance = Trade Balance+Net Unilateral Transfers

Unilateral transfers that the US pays to countries abroad include aid to poorcountries, interest payments to foreigners for US government debt, and grantsto foreign researchers or institutions. Net unilateral transfers equal transfers ofthe sort just described received by the US, minus transfers paid out by the US.Usually net unilateral transfers are negative for the US, but small in size (theyamounted to about 0.5% of GDP in 1999). So for all practical purposes wecan use the trade balance and the current account balance interchangeably. Wesay that the US has a current account de�cit if the current account balance isnegative and a current account surplus if the current account balance is positive.Note that the current account balance is a �ow (since exports and imports are�ows).The current account balance keeps track of import and export �ows between

countries. The capital account balance keeps track of borrowing and lendingof the US with abroad. It equals to the change of the net wealth positionof the US. The US owes money to foreign countries, in the form of governmentdebt held by foreigners, loans that foreign banks made to US companies and inthe form of shares that foreigners hold in US companies. Foreign countries owemoney to the US for exactly the same reason The net wealth position of theUS is the di¤erence between what the US is owed and what it owes to foreigncountries. Note that the net wealth position is a stock, but that the capitalaccount balance, as the change in the net wealth position, is a �ow:

Capital Account Balance this year = Net wealth position at end of this year

�Net wealth postion at end of last year

Compare this to the relationship between the capital stock and investment fromabove: it is exactly the same principle. Note that a negative capital accountbalance means that the net wealth position of the US has decreased: in netterms, capital has �own out of the US. The reverse is true if the capital accountbalance is positive: capital �ew into the US.The current account and the capital account balance are intimately related:

they are always equal to each other. This is another example of an accountingidentity.

Current Account Balance this year = Capital Account Balance this year

The reason for this is simple: if the US imports more than it exports, it has toborrow from the rest of the world to pay for the imports. But this change in

24CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

the net asset position is exactly what the capital account balance captures. Inthe next �gure we plot the trade balance for the US for the last 30 years.

1970 1975 1980 1985 1990 1995 2000400

350

300

250

200

150

100

50

0

Trade Balance for the US 19672001 (in Constant Prices)

Year

Trad

e Ba

lanc

e

One can see that the trade balance was mostly negative during this period,and has been particularly negative during the expansion of the 90�s. One conse-quence of this �gure and the accounting identity is that the net wealth positionof the US has declined over the years. Since 1989 the US, traditionally a netlender to the world, has become a net borrower: the net wealth position of theUS has become negative in 1989.A last variable that is of strong importance when discussing international

trade are exchange rates. The exchange rate of the dollar with the yen measureshow many yen somebody has to pay to buy one dollar (currently about 119). Theexchange rate of the dollar with the Euro measures how many euro somebodyhas to spend in order to buy 1 dollar (currently about 1.1). The exchangerates are important for the following reasons: suppose the exchange rate of thedollar with the yen increases (i.e. dollar become more expensive to buy forJapanese households). That means it becomes more expensive for Japanese tobuy American products. Reversely if the exchange rate declines. Hence there

2.7. APPENDIX A: MORE ON GROWTH RATES 25

tends to be a close relation between exchange rates and imports and exports (andhence the trade balance). A strong dollar (Euro are cheap, dollars expensive)tends to increase the trade de�cit, a weak dollar tends to decrease it.

2.7 Appendix A: More on Growth Rates

Remember that the growth rate of a variable Y (say nominal GDP) from periodt� 1 to t is given by

gY (t� 1; t) =Yt � Yt�1Yt�1

(2.1)

Similarly the growth rate between period t� 5 and period t is given by

gY (t� 5; t) =Yt � Yt�5Yt�5

Now suppose that GDP equals $1000 in 1992. From 1992 to 1993 it grows at agrowth rate of 2%. From 1993 to 1994 it grows at a rate of 4%, from 1994 to1995 at 7%, from 1995 to 1996 at 1% and from 1996 to 1997 at 3%. How dowe �gure out how big GDP was in 1997? We can use the formula in (2:1): Notethat

gY (t� 1; t) =Yt � Yt�1Yt�1

gY (t� 1; t) � Yt�1 = Yt � Yt�1gY (t� 1; t) � Yt�1 + Yt�1 = Yt

(1 + gY (t� 1; t))Yt�1 = Yt

Hence GDP in period t equals GDP in period t � 1; multiplied by 1 plus thegrowth rate. For the example:

Y1993 = (1 + gY (1992; 1993)) � Y1992= (1 + 0:02) � $1000 = $1020

Y1994 = (1 + 0:04) � $1020 = $1060:80Y1995 = (1 + 0:07) � $1060:80 = $1135:06Y1996 = (1 + 0:01) � $1135:06 = $1146:41Y1997 = (1 + 0:03) � $1146:41 = $1180:80

and the growth rate from 1992 to 1997 is given by

gY (1992; 1997) =$1180:80� $1000

$1000= 18:08%

Particularly interesting is the case where a variable grows at a constant rate,say g, over time. Suppose at period 0 GDP equals some number Y0 and GDPgrows at a constant rate of g% a year. Then in period t GDP equals

Yt = (1 + g)tY0 (2.2)

26CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

For example, if Jesus would have put 1 dollar in the bank at year 0AC and thebank would have paid a constant interest rate of, say, 1.5%, then in 1999 hewould have had a fortune of

Y1999 = (1:015)1999 � $1= $8; 425; 941; 823

which is almost the US GDP for this year. Sometime it is interesting to do thereverse calculation. Suppose you know GDP at time 0 and at time t and wantto know at what constant rate GDP must have grown to reach Yt; starting fromY0 in t years. We can use the formula (2:2) to solve for g

Yt = (1 + g)tY0

(1 + g)t =YtY0

(1 + g) =

�YtY0

� 1t

g =

�YtY0

� 1t

� 1

As an example: Suppose we know that in the year 1900 a country has GDP of$1,000 and in 1999 it has GDP of $15,000. Suppose we assume that the GDPof this country has grown over these years at a constant rate g: How big mustthis growth rate be? If we take 1900 as period 0; then 1999 is period t = 99:We apply the formula to get

g =

�YtY0

� 1t

� 1

=

�$15; 000

$1; 000

� 199

� 1

= 0:028 = 2:8%

Finally, we might be interested in the following question: Suppose we know theGDP of a country in period 0 and its growth rate g and we want to know howmany time periods it takes for GDP in this country to double (to triple and soforth). Again we can use the formula, but this time we solve for t :

Yt = (1 + g)tY0

(1 + g)t =YtY0

(2.3)

Now we need a little mathematical fact about logarithms: if a and b are arbitrarypositive numbers, then

log�ab�= b � log(a)

2.8. APPENDIX B: CHAIN-WEIGHTED GDP 27

Using this fact and taking (natural) logarithms on both sides of equation (2:3)yields

log�(1 + g)t

�= log

�YtY0

�t � log(1 + g) = log

�YtY0

�

t =log�YtY0

�log(1 + g)

Now suppose we want to �nd the number of years it takes for GDP to double,i.e. the t such that Yt = 2 � Y0 or Yt

Y0= 2: We get

t =log(2)

log(1 + g)

So once we know the growth rate of our country, we can answer our question.For example with a growth rate of g = 1% it takes about 70 years, with a growthrate of g = 2% it takes about 35 years, with a growth rate of g = 5% it takesabout 14 years and so forth.

2.8 Appendix B: Chain-Weighted GDP

In this appendix we discuss a recent development in the computation of realGDP and the GDP de�ator. The Bureau of Labor Statistics used to computereal GDP and the GDP de�ator in exactly the fashion described in the maintext. In 1996 it also introduced the Fisher indices to compute real GDP (it stillreports two measures of real GDP, the old and the revised numbers). What isthe problem with the old method?With the old method one would pick a base year, say 1992. The contribution

of computers to real GDP in 1999 is them computed as follows: take the dollaramount spent on computers in 1999 and divide by the price of computers in1999 relative to 1992 (i.e. divide by the price in 1999 and multiply by theprice in 1992). The result the total value of computers sold in 1999 in prices of1992. Summing up all goods and commodities, evaluated at their 1992 prices,yields real GDP. Note that for the base year nominal and real GDP alwayscoincide. The problem is that goods whose prices have fallen a lot betweenthis year and the base year (like computers) receive more and more weight incomputing real GDP. I will use the same example as Hall and Taylor (p. 33),but will deviate once I describe the reforms the BEA has undertaken. Supposea country produces only two goods, computers and hamburgers. The next tabledescribes the spending on both goods as well as their prices

28CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

Table 4Spending in Current $ Prices in Current $

Year Computers (1) Hamburgers (2) Computers (3) Hamburgers (4)

1992 100 106 1.00 1.001994 105 98 0.80 1.051996 103 104 0.60 1.101998 99 100 0.40 1.15

This is how real GDP and the GDP de�ator are computed using the oldmethod. The �rst step is to determine real quantities for the years 1994, 1996and 1998 (again, this is equivalent to valuing 1994, 1996 and 1998 quantities in1992 prices). Note that, since we have chosen 1992 as our base year, in 1992nominal and real quantities coincide (as we have normalized all prices in 1992 to1). This is done by dividing the spending numbers for computers in column (1)by the current prices for computers in column (3), and likewise for hamburgersby dividing the numbers in column (2) by current prices in column (4). Theresults are found in the �rst two columns of the next table.

Table 5Real Quantities Real GDP GDP De�ator

Year Computers (5) Hamburgers (6) (7)=(5) + (6) ((1)+(2))/(7)

1992 100.0 106.0 206.0 1.0001993 131.3 93.3 224.6 0.9041994 171.7 94.5 266.2 0.7781995 247.5 87.0 334.5 0.595

Next we determine real GDP by summing up all real quantities, in this caseonly computers and hamburgers. This is done by summing the �rst two columnsand yields the third column. Finally we compute the GDP de�ator by divingnominal GDP by real GDP in the di¤erent years. Nominal GDP is given by thesum of columns (1) and (2), real GDP is given by the column labeled (7). Ityields the last column of Table 5.The problem with the old method is evident: although in 1998 people spent

more on hamburgers than computers, the weight that computers receive in realGDP is about three times that for hamburgers. Also, the choice of the base yearis quite important, and changes in the base year (which are done about every5 to 7 years) can lead to serious revisions of growth rates of real GDP and theGDP de�ator.The BEA reform addressed both problems. The �rst change was to introduce

chain-weighted indices. Instead of computing variables in comparison to a �xedbase year, variables computed in 1993 are based on 1992, variables in 1994 arebased on 1993 and so forth. Before they were all based on the base year, 1992.Growth rates between 1992 and 1995 are then found by �chaining�the growthrates for single years together (as described in the previous appendix). The

2.8. APPENDIX B: CHAIN-WEIGHTED GDP 29

second change was to allow weights for real GDP to take into account relativeprice changes. I will now describe how the new method computes real GDP andthe de�ator mechanically.12

We �rst have to introduce two quantity indices (which are very similar tothe price indices discussed before). Let

pct = Price of a computer in period t

ct = Number of computers bought in period t

pht = Price of hamburgers in period t

ht = Number of hamburgers bought in period t

Let (pc0; c0; ph0; h0) be the corresponding value for period 0: We de�ne theLaspeyres quantity index as

LQt =htph0 + ctpc0h0ph0 + c0pc0

Note that here we keep prices �xed at period 0 prices and vary the quanti-ties, whereas with the Laspeyres price index we kept quantities �xed at period0 quantities and varied the prices. Similarly we de�ne the Paasche Quantityindex as

PaQt =htpht + ctpcth0pht + c0pct

The new measure for real GDP, in, say 1993, is the real GDP in 1992 times thesquare-root of the product of Laspeyres and Paasche quantity index between1992 and 1993. Formally

real GDP in 1993 = real GDP in 1992 �pLQ1993 � PaQ1993

where period 0 corresponds to 1992.Let us compute real GDP for 1993, using this new method. The only thing

we need are the ingredients for our quantity indices and last periods GDP. Wehave prices already given in columns (3) and (4), and quantities in (5) and (6),as well as 1992 real GDP from summing (1) and (2) for 1992. Nothing more isrequired. The Laspeyres quantity index is

LQ1993 =h1993ph1992 + c1993pc1992h1992ph1992 + c1992pc1992

=93:3 � 1 + 131:3 � 1106 � 1 + 100 � 1

=224:6

206= 1:090

12This discussion is somewhat technical and di¤ers from Hall and Taylor. For furtherreference, the original article from the BEA describing the procedure is by Steven Landefeldand Robert Parker and can by found in the Survey of Current Business, May 1997, pp 58-68.

30CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

The Paasche quantity index is

LQ1993 =h1993ph1993 + c1993pc1993h1992ph1993 + c1992pc1993

=93:3 � 1:05 + 131:3 � 0:8106 � 1:05 + 100 � 0:8

=203

191:3= 1:061

Hence real GDP in 1993 equals

real GDP in 1993 = real GDP in 1992 �pLQ1993 � PaQ1993

= 206 �p1:090 � 1:061

= 221:5

The GDP de�ator is computed as before by dividing nominal by real GDP. Letus do one more year, since it shows the �chain�character of the new method.For 1994 we now take 1993 as period 0: Again we have all the ingredients ready,since we just computed real GDP for 1993. In particular

real GDP in 1994 = real GDP in 1993pLQ1994 � PaQ1994

and we compute the Laspeyres quantity index as

LQ1994 =h1994ph1993 + c1994pc1993h1993ph1993 + c1993pc1993

=94:5 � 1:05 + 171:7 � 0:893:3 � 1:05 + 131:3 � 0:8

=236:6

203= 1:166

and the Paasche quantity index as

LQ1994 =h1994ph1994 + c1994pc1994h1993ph1994 + c1993pc1994

=94:5 � 1:1 + 171:7 � 0:693:3 � 1:1 + 131:3 � 0:6

=207

181:4= 1:141

We get

real GDP in 1994 = real GDP in 1993pLQ1994 � PaQ1994

= 221:5 �p1:166 � 1:141

= 255:5

The �nal results of this exercise are given in Table 6

2.8. APPENDIX B: CHAIN-WEIGHTED GDP 31

Table 6

Year Real GDP GDP De�. Gr.R. GDP In�. R. Gr.R. GDP (old) In�. R. (old)

1992 206.0 1.0001993 221.5 0.916 7.5% -8.4% 9.0% -9.6%1994 255.5 0.810 15.3% -11.6% 18.5% -13.9%1995 294.2 0.676 15.1% -16.5% 25.7% -23.5%

Let us get some feeling for the results. The whole objective of computingreal GDP and the GDP de�ator was to decompose nominal GDP into a pricecomponent and a quantity component since we are interested about how real eco-nomic activity in an economy evolves over time. The old method of computingGDP gives too much weight to commodities whose prices have fallen rapidly, inour example computers. Hence the old method overstates by how much the realcomponent of GDP increased and understates by how much the price componentincreased (in this example it overstates by how much it declined). Comparinggrowth rates of real GDP for both methods and in�ation rates for both methodswe see that the new methods shows lower growth rates of real GDP and higherin�ation rates.13 This is exactly the problem of the old method: it understatesthe importance of the price decline in computers.

Finally, the di¤erence between both methods can be sizeable, not only inour cooked-up example. Growth of real GDP, using these two methods, seemto di¤er by as much as 0.5 to 1% yearly. Given that policies are based on realGDP growth numbers this is not to be underestimated in its importance.

13Note that, as discussed before, the GDP de�ator, computed using the old method, is aPaasche price index, and that, as discussed in the main text, Paasche price indices tend tounderstate in�ation.

32CHAPTER 2. NATIONAL INCOMEAND PRODUCTACCOUNTING (NIPA)

Chapter 3

Economic Growth

3.1 Mathematical Preliminaries

3.1.1 Discrete vs. Continuous Time

So far in this course we have dealt with time as a discrete variable. Time couldtake the values t = 0; t = 1; t = 1995 and so on, but no values in between.For the purposes of growth theory it is often convenient to think of time as acontinuous variable, so that t = 0:3; t = 1995:25 etc are possible. When time iscontinuous, we write our economic variables of interest, like GDP, population,in�ation rate, as functions of time. Let us look at an example.Suppose that the population in a particular country is a function of time:

N(t) gives the population of a particular country at date t; where t can takeany value (not just integer values). So N(1995) is the population of the countryon January 1, 1995, N(1995:5) is the population on July 1, 1995 and so on.

3.1.2 Derivatives

The derivative of a function N; denoted by N 0 or dNdt measures by how much thepopulation changes when the date changes by a very small bit (an instantaneouschange). If the independent variable of a function N is time (as in our example),then it has become customary to denote the derivative of the function N by _N .Hence N 0; dNdt and

_N all denote the same thing, namely the derivative of thefunction N with respect to time. Note that when the population increases overtime, then dN

dt > 0 and when it decreases, thendNdt < 0:

The derivative of a function with respect to time expresses the instantaneouschange of the function. It is closely related to the change of the function over adiscrete time span. Let N(1996) be the population of our country on January1, 1996 and N(1997) be the population on January 1, 1997. Then N(1997) �N(1996) is the change in the population in the time interval between January1, 1996 and January 1, 1997. Here the time interval is one year. If we let thetime interval get shorter and shorter, the change of the variable during that

33

34 CHAPTER 3. ECONOMIC GROWTH

time interval approaches the derivative of the function. Formally, let �t denotethe length of the time interval, then the derivative of N with respect to time tis de�ned as

dN(t)

dt� N 0(t) � _N(t) = lim

�t!0

N(t)�N(t��t)�t

There are a few basic rules to take derivatives:

1. If N(t) = tn with n a positive integer, then

_N(t) = ntn�1

2. If N(t) = ex; then_N(t) = ex

3. If N(t) = log(t); then_N(t) =

1

t

4. If N(t) = g(h(t)); with g; h functions, then

_N(t) = g0(h(t)) � _h(t)

Note that whenever we use the log in this course, we mean the log with basise; or the natural logarithm (Sometime the symbol ln is used for the natural log,but we will always use log to denote the natural logarithm). Examples

If N(t) = t5 then _N(t) = 5t4

If N(t) = log(2x3) then _N(t) =6x2

2x3=3

x

Also note that a very important consequence of the forth rule (the so-calledchain rule) is the following. Suppose we want to �nd the time derivative oflog (N(t)) : Then we use as our function g the log; and as our function h thefunction N to get�

log( _N(t))�� d log(N(t))

dt=

1

N(t)� _N(t) =

_N(t)

N(t)

3.1.3 Some Useful Facts about Logs

Here are some rules for the natural logarithm

log(x � y) = log(x) + log(y)

log

�x

y

�= log(x)� log(y)

log(xa) = a � log(x)log(ex) = x

elog(x) = x

3.1. MATHEMATICAL PRELIMINARIES 35

3.1.4 Growth Rates (once again)

Remember how growth rates were de�ned in the case where time is discrete

gN (t� 1; t) =Nt �Nt�1Nt�1

In continuous time growth rates are de�ned analogously. Noting that, as thetime interval between t�1 and t converges to 0; the di¤erence Nt�Nt�1 (dividedby the time interval) converges to _N(t) and Nt�1 gets closer and closer to Nt:This motivates the fact that in continuous time we de�ne the growth rate of avariable N at time t as

gN (t) =_N(t)

N(t)

Note the important fact that gN (t) =d log(N(t))

dt ; i.e. we can compute the growthrate of a variable by taking the time derivative of the log of this variable. Thisfact turns out to be very useful.

3.1.5 Growth Rates of Functions

The preceding fact, plus the rules for logarithms, can be used to compute growthrates of functions. Suppose we have a variable k(t) that is de�ned to be theratio of two other variables K(t) and L(t); i.e.

k(t) =K(t)

L(t)

In our application we will denote by k(t) as capital per worker, by K(t) theaggregate capital stock and by L(t) the number of workers at time t: Supposewe know the growth rate of K(t) and L(t) and want to �nd the growth rate ofk(t): We do the following. First we take logs on both sides (and use the rulesfor logs)

log(k(t)) = log(K(t))� log(L(t))Now we di¤erentiate both sides with respect to time to get

d log((k(t))

dt=

d log(K(t))

dt� d log(L(t))

dt_k(t)

k(t)=

_K(t)

K(t)�_L(t)

L(t)

gk(t) = gK(t)� gL(t)

Hence the growth rate of the ratio K(t)L(t) equals the di¤erence of the growth rates.

Also, if we want the ratio to remain constant over time (i.e. gk(t) = 0), thisrequires that bothK(t) and L(t) must grow at the same rate, i.e. gK(t) = gL(t):Suppose that total output at period t; Y (t) depends on the total capital

stock K(t) and total number of workers L(t) used in the production process inthe following form

Y (t) = K(t)�L(t)1��

36 CHAPTER 3. ECONOMIC GROWTH

with � a �xed constant between 0 and 1: This particular relationship betweenoutput and capital and labor input is called Cobb-Douglas production functionand we will use it extensively later. Suppose we know the growth rates of capitalK(t) and labor L(t) and we want to �nd the growth rate of output. Again wecan use the trick of �rst taking logs and then di¤erentiate with respect to time.

log(Y (t)) = � � log(K(t)) + (1� �) � log(L(t))d log(Y (t))

dt= � � d log(K(t))

dt+ (1� �) � d log(L(t))

dt_Y (t)

Y (t)= � �

_K(t)

K(t)+ (1� �) �

_L(t)

L(t)

gY (t) = � � gK(t) + (1� �) � gL(t)

Hence the growth rate of output equals the weighted sum of the growth rates ofinputs, with the weight being equal to the (share) parameter � in the productionfunction.

3.1.6 Simple Di¤erential Equations and Constant GrowthRates

Suppose a variable,1 say output Y grows at a constant rate gY (t) from date 0to date T and suppose we know output at period 0; Y (0): What is output atperiod T? In discrete time the answer was

YT = (1 + g)TY0

Now we want to derive a similar formula for continuous time. We start withthe de�nition of a growth rate in continuous time (and use the fact that thisgrowth rate is constant from t = 0 to t = T )

g =_Y (t)

Y (t)

Integrating both sides with respect to time t; from 0 to T; yields2

1This section assumes familiarity with the theory of integration. Readers without thisknowledge may skip to the �nal formulas.

2Keep in mind that the time derivative of log(Y (t)) equals_Y (t)Y (t)

; so the anti-derivative of_Y (t)Y (t)

equals log(Y (t)):

3.2. GROWTH AND DEVELOPMENT FACTS 37

Z T

0

gdt =

Z T

0

_Y (t)

Y (t)dt

gT = log(Y (T ))� log(Y (0))

gT = log

�Y (T )

Y (0)

�egT =

Y (T )

Y (0)

Y (T ) = egT � Y (0) (3.1)

Hence if output at time 0 equals Y (0) and grows at constant rate g; then at timeT output equals egTY (0): Note that with formula (3.1) we can ask exactly thesame questions (and use exactly the same manipulations) in continuous time asin Appendix 1 of Chapter 2 with discrete time.We should note two things: �rst, by taking logs in the formula we get

log(Y (T )) = log(Y (0)) + gT

Hence if output (or any other variable) grows at a constant rate g; then plottingthe log of output gives a straight line with intercept log(Y (0)) and slope g:Therefore economists often plot the log of a variable (rather than the variableitself), because this way it is easy to see whether (and at what rate) the variablegrows over time. See Figures 7 and 8 for the e¤ect.Second, the formulas for discrete and continuous time yield roughly the same

result (you should work out some examples with your pocket calculator). Thetwo formulas would in fact be identical if eg = (1 + g): That this equality isapproximately true can be seen from the Taylor series expansion of eg aroundg = 0

eg = e0 + (g � 0)e0 + (g � 0)2

2e0 +

(g � 0)36

e0 + : : :

= 1 + g +g2

2+g3

6+ : : :

� 1 + g

if g is not too large

3.2 Growth and Development Facts

The economist Niclas Kaldor pointed out the following stylized growth facts(empirical regularities of the growth process) for the US and for most otherindustrialized countries (look back at the �gures in the last section):

1. Output (real GDP) per worker y = YL and capital per worker k =

KL grow

over time at relatively constant and positive rate.

38 CHAPTER 3. ECONOMIC GROWTH

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 50

200

400

600

800

1000

1200

1400

1600Exponentially Growing Variable

Time

Y(t)

2. They grow at similar rates, so that the ratio between capital and output,KY is relatively constant over time

3. The real return to capital r (and the real interest rate r � �) is relativelyconstant over time

4. The capital and labor shares are roughly constant over time. The capitalshare � is the fraction of GDP that is devoted to interest payments oncapital, � = rK

Y : The labor share 1 � � is the fraction of GDP that isdevoted to the payments to labor inputs; i.e. to wages and salaries andother compensations: 1� � = wL

Y : Here w is the real wage.

These stylized facts motivated the development of the neoclassical growthmodel, the so-called Solow model, to be discussed below. The Solow model hasspectacular success in explaining the stylized growth facts by Kaldor. Note thatthe growth facts pertain to data for a single country over a (long) period oftime. Such a data set is called a time series.In addition to the growth facts we will be concerned with how income (per

worker) levels and growth rates vary across countries in di¤erent stages of their

3.2. GROWTH AND DEVELOPMENT FACTS 39

0 0.5 1 1.5 2 2.5 3 3.5 4 4.5 52

3

4

5

6

7

8Exponentially Growing Variable, Log Scale

Time

log(

Y(t)

)

development process. The true test of the Solow model is to what extent it canexplain di¤erences in income levels and growth rates across countries, the socalled development facts. As we will see, the verdict here is mixed.Now we summarize the most important facts from the Summers and Heston�s