Embed Size (px)

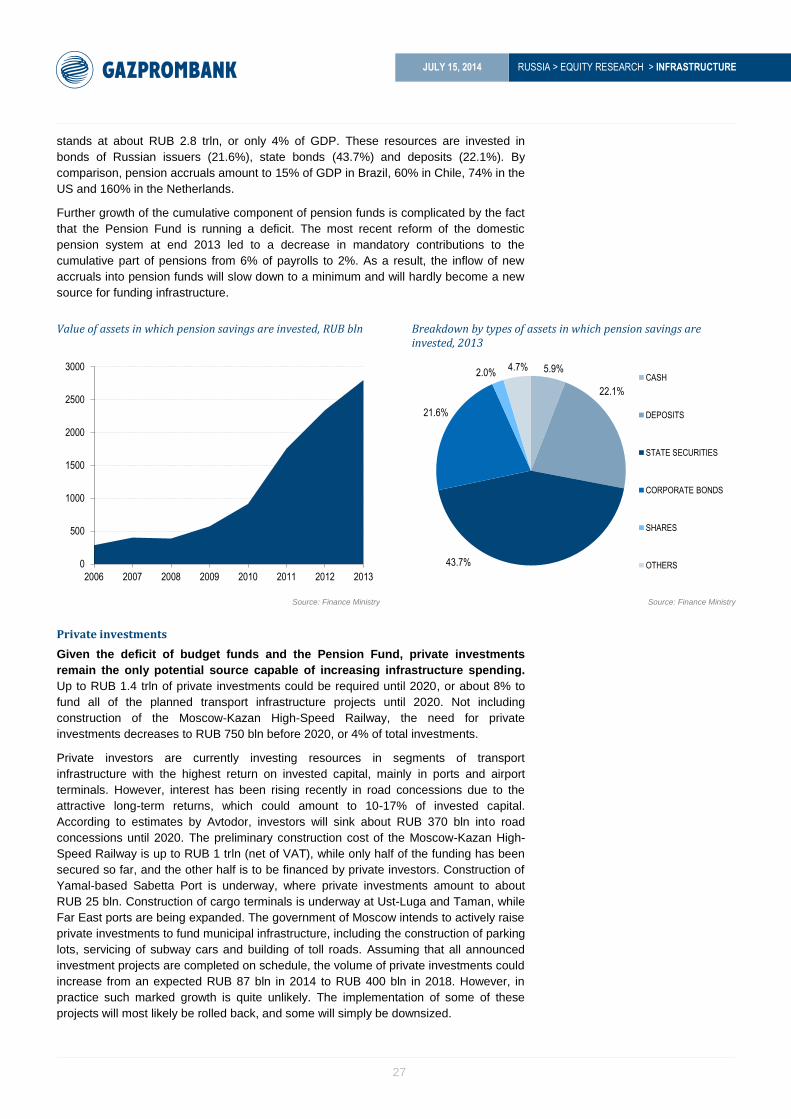

Citation preview

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

1

Copyright © 2003-2014. Gazprombank (Open Joint-Stock Company)

Research Department

INDUSTRY REPORT Mikhail Ganelin

+7 (495) 983 18 00 (ext. 5 45 83)

Sergey Vasin +7 (495) 983 18 00 (ext. 5 45 08)

Russian infrastructure A big ship sails far

The expansion of infrastructure is an imperative for the long-term

economic growth of any country, but securing sources of funding remains

a complex challenge. In this report, we analyze key global infrastructure

expansion trends as well as ways and means to fund infrastructure rollout

projects in various countries. Our main focus is on Russian

transportation, which accounts for 80% of all infrastructure investment in

the country.

Assuming that the global economy grows at 3.3% per year, GDP will

double by 2035. The main contributors to growth include a rise in the global

population (+20% by 2035) and urbanization (the urban population is expected

to increase by 40%), while rapid growth of household income will lead to

accelerated growth of international trade and tourism. Under this scenario,

global air passenger traffic will double as soon as 2020, air freight will triple, and

container shipments will quadruple. In addition, the throughput capacity of most

existing transport channels between Asia and Europe is capable of raising

cargo turnover on average by another 50%. This increment would clearly be

insufficient in case of faster than expected expansion in the coming decades.

The minimum need for infrastructure investment to support economic

growth is 3.5% of GDP, or $57 trln until 2030 ($3.2 trln per year). However,

there is a 20-40% shortfall in infrastructure funding in most countries. State

investments in infrastructure total about 65%, but their ability to ramp up funding

will be limited going forward due to high debt and budget deficits. The role of

private investors, who contribute 35% of infrastructure investment, is

conspicuously on the rise. The governments of various countries are working

out incentives for investors in an effort to strike a reasonable balance between

risk and rewards from infrastructure projects.

In Russia, the rate of infrastructure investment averages 3.6-4.2% of GDP,

or roughly in line with the global average. By 2020, infrastructure investment

will reach $650 bln ($90 bln per year on average). These funds will suffice for

moderate expansion of infrastructure and gradual improvement of its quality, but

not in the event of accelerated expansion. Large projects, such as construction

of infrastructure for the Sochi Winter Olympic Games, will give way to other no

less massive projects, such as construction of the Power of Siberia and South

Stream pipelines, expansion of the Baikal-Amur Mainline and Trans-Siberian

railways, construction of toll roads under concession terms, and the possibility

of deploying the Moscow-Kazan High-Speed Railway with the participation of

private investors. According to our estimates, $25-40 bln of private investments

will be needed until 2020. The bulk of transport infrastructure investment will be

directed to road construction (45%), while rail transport will take 20% (including

the Moscow-Kazan High-Speed Railway and subway facilities), pipeline

transport should account for 30%, while ports and airports will comprise the

remaining 5%.

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

2

CONTENTS

Expansion of global infrastructure: exponential investment growth on the way ......................... 3

World poised for higher infrastructure demand ............................................................................................................................................ 4

Infrastructure investment needs seen at least 60% higher by 2030 .................................................................................................... 5

Sources of infrastructure funding — will resources suffice? .................................................................................................................... 6

Special infrastructure bourse could be established in Japan .................................................................................................................... 8

Examples of investment tools used in various countries for infrastructure projects .................................................................. 11

Current status of Russia’s infrastructure needs ..................................................................................... 18

Russia’s transport infrastructure: rapid growth or concurrent expansion? .................................................................................... 20

Plan of development for transport infrastructure until 2020 ................................................................................................................ 22

How will Russian infrastructure be funded and where will the resources come from? ............................................................. 25

Moscow — largest investor in transport infrastructure ........................................................................................................................... 25

Russian roads: fighting ‘disaster’ brings noticeable results .................................................................................................................... 28

Avtodor: road concessions promise high yields ........................................................................................................................................... 31

Glavnaya Doroga Consortium: first completed PPP project in the road construction field ...................................................... 34

Key market players: competition tightens after the Olympics ............................................................................................................... 35

Railway infrastructure: removing bottlenecks and building high-speed lines ............................................................................... 35

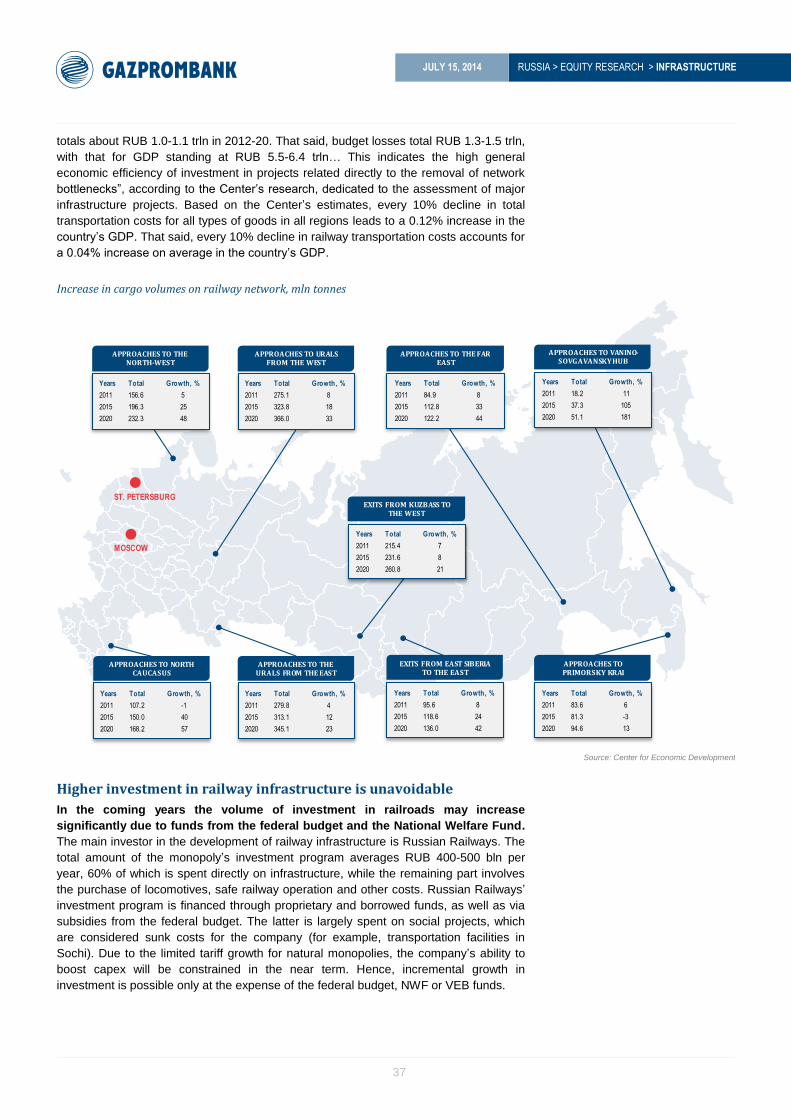

Higher investment in railway infrastructure is unavoidable .................................................................................................................. 37

Airports: a tasty morsel for investors ................................................................................................................................................................ 40

Seaports: state and business working in tandem ......................................................................................................................................... 44

Public-private ventures for the expansion of port infrastructure ........................................................................................................ 45

Pipeline infrastructure: Russia’s raw material artery ................................................................................................................................ 46

Other infrastructure segments ..................................................................................................................... 48

Power grid complex ................................................................................................................................................................................................... 48

Telecommunications ................................................................................................................................................................................................. 49

Public utilities ............................................................................................................................................................................................................... 50

Appendix ............................................................................................................................................................... 51

Largest construction companies in Russia: main players and trends ................................................................................................. 51

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

3

EXPANSION OF GLOBAL INFRASTRUCTURE: EXPONENTIAL INVESTMENT GROWTH ON THE WAY

According to OECD forecasts, global GDP is set to grow at an annual pace of

3.3% per year and double by 2035, amounting to $145 trln. China will overtake the

US within the next few years in terms of GDP, calculated as purchasing power parity

(PPP), and become the world’s largest economy, with GDP surging 2.5-fold by 2030

compared to 2013. The GDP of India, the world’s third-largest economy, will triple by

2030 in terms of PPP, while Russia’s GDP will double during this period, moving from

sixth to fifth place among the world’s biggest economies. By comparison, the US

economy is expected to increase by just 40% over this period, while Europe will

expand by 30%. The main factors underpinning growth will be a rise in the population

(+19% by 2030) to 8.3 bln, urbanization (the urban population is set increase by 40%

by 2030; while its proportion will grow from 52% to 58%), faster growth of household

income, as well as further expansion of international trade and tourism.

Given the above pace of growth, the load on infrastructure in most countries is

set to grow exponentially over the next decade, and its timely development will

become the hallmark of steady growth of the global economy. According to

estimates by OECD experts, if global GDP doubles by 2035, the volume of passenger

traffic during the same period will increase by 2.5-fold, air freight will triple, and

container shipments will quadruple. Meanwhile, the throughput capacity of existing

transport channels between Asia and Europe could push up cargo turnover by 50% on

average, while the effect would wear off within 6-8 years. Given that the design,

construction and expansion of large infrastructure facilities will take years, decisions

concerning the ways and means to finance them should be made in the near future.

Size of GDP vs. country’s position in PPP ranking, $ trln Global GDP growth vs. transport sector indicators

Source: PWC, IMF Source: OECD

1

2

3 4 5 6 7

2

1

3

4 7

5 6

0

5

10

15

20

25

30

35

US CHINA INDIA JAPAN GERMANY RUSSIA BRAZIL

2013 2030

0

100

200

300

400

500

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

GLOBAL GDP PASSENGER TURNOVER CARGO TURNOVER CONTAINER CARGO TURNOVER

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

4

Population growth will be accompanied be an increasing share of urban population, bln people

GDP per capita growth

Source: United Nations Source: US Department of Agriculture

Increasing infrastructure investments — a tested and tried way to stimulate

economic growth. Higher infrastructure investments create new jobs in the short term,

stimulate economic growth in the medium term, and lower the transport costs of

companies while improving the standard of living of households in the long term.

According to estimates by McKinsey, an additional 1% of GDP investment in infrastructure

will create 3.4 mln new jobs in India, 1.5 mln in the US and 1.3 mln in Brazil. Given the

similarity of economic indicators between Brazil and Russia, the number of jobs that would

be created in Russia would also match, i.e. 1.7% of the entire economically active

population of the country. According to estimates by the Economy Ministry, aggregate

investment in Russia’s transportation infrastructure yields about 0.3% of GDP growth. In

addition, a 10% decline in aggregate transportation costs for all types of goods would add

0.12% to GDP, according to estimates by the Center for Strategic Research. Furthermore,

high-quality transportation infrastructure raises the mobility of households, who would be

capable of moving with greater ease between areas of cities and regions, for a number of

reasons, including the search for employment. This would improve the structure of the

labor market, lead to overall growth in household income and ultimately stimulate demand,

which is one of the key factors of economic expansion.

World poised for higher infrastructure demand

The biggest passenger plane in the world, the Airbus 380, which is capable of flying

over 800 passengers, executed its maiden voyage in 2007. This was the response of

the European aircraft corporation to conspicuous growth in demand in the field of air

transport and tourism.

In 2012, China commissioned the largest hydroelectric generation facility in the world,

Three Gorges on the Yangtze River with capacity of 22.5 GW, which is 1.5 times

more than the previous world leader, Brazil’s Itaipu hydroelectric power plant. Total

investments exceeded $26 bln. When the facility was under design, the HPP was

expected to provide 10% of China’s power needs. However, during the 20 years it

took to build the plant, power consumption rose at a mind-boggling pace, and the

HPP is currently capable of generating less than 2% of the country’s power.

By 2017, the largest airport in the world, with a six-runway hub, will be built in Istanbul.

The facility will be capable of handling a passenger flow of 150 mln (by comparison, the

biggest airport in the world, currently located in Atlanta, is capable of handling 90 mln

passengers per year). Turkish authorities are convinced that the new airport will become a

major hub connecting East and West, Africa and Europe. The total amount of investments

in the project, to be implemented on concession terms, is about $30 bln.

3.3 3.3 3.3 3.4 3.4 3.4 3.3

3.2 3.6 3.6 3.9 4.3 4.6 5.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

2000 2005 2010 2015 2020 2025 2030

RURAL URBAN

0

50

100

150

200

250

300

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

WORLD US BRAZIL EUROPE

RUSSIA CHINA INDIA TURKEY

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

5

The 684 km Moscow-St. Petersburg Toll Road, with a maximum speed limit of 150 km

per hour, is to be built by 2018. The total cost of the road is $10 bln, to be funded

through concession agreements with private investors. The need for such a highway

has arisen due to a significant increase in freight turnover between the country’s two

largest cities.

The Nicaragua Canal could be built by 2019 between the Caribbean Sea and the

Pacific Ocean, with the facility routed through the territory of Nicaragua. It aims to

provide an alternative to the Panama Canal, the throughput of which has reached

maximum capacity. In 2013, the government of Nicaragua outsourced the

concession project to Hong Kong-based HKND Group for 50 years. Construction of

the canal is expected to get under way around end 2014. The cost of the project is

roughly $40 bln, and aside from the canal, the plan is to build two seaports, an

airport and an oil pipeline.

Infrastructure investment needs seen at least 60% higher by 2030

According to estimates by McKinsey Global Institute, the minimum need for

infrastructure investments stands at $57-67 trln from 2013 through 2030

(averaging $3.4 trln per year). This estimate is based on the historical volume of

investments in infrastructure over the past 18 years at 3.5-3.8% of GDP. However,

these forecasts fail to take into account faster than anticipated growth of household

income and accelerated development of infrastructure in countries where infrastructure

is traditionally underfinanced (for example, in Brazil and Russia). Taking into account

these factors, infrastructure needs could easily exceed 5% of global GDP ($80 trln),

meaning that investment would essentially double compared to the previous period.

In the opinion of McKinsey, the aggregate stock of infrastructure assets should

amount to an average 70% of GDP in order for it to be maintained in proper

condition. The countries where this percentage is lower (e.g. Brazil, Russia, India and

even the US) should ramp up infrastructure investments at a rapid pace, while those

above that baseline (Japan, China and Germany) have the opportunity to reduce the

volume of investments in the coming years.

Estimated value of infrastructure assets in various countries as a % of GDP, 2012

Investments in infrastructure in various countries: % of GDP (1992-2011) and investment need until 2030

Source: McKinsey Source: McKinsey

16%

57%

58%

61%

64%

71%

76%

179%

0% 50% 100% 150% 200%

BRAZIL

UK

INDIA

RUSSIA

US

GERMANY

CHINA

JAPAN

6.9%

6.4%

4.9%

4.0%

3.6%

3.1%

2.6%

4.7%

8.5%

1.5%

3.4%

2.6%

2.6%

5.0%

0% 2% 4% 6% 8% 10%

INDIA

CHINA

BRAZIL

RUSSIA

US

EU

JAPAN

1992-2011 2013-2030

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

6

In Russia, the stock of infrastructure assets relative to GDP (61%), while less than

the recommended GDP threshold, is still roughly in line with the baseline asset-

to-GDP ratio of 70%, but is quite close to such countries as the US (64%) and the

UK (57%). This is due to the fact that all types of infrastructure are to be found in

Russia: highways and railroads, airports, ports, pipelines, power grids (including

nuclear), and water supply. Notably, there are not very many countries in the world

possessing such diversified infrastructure. A case in point is Brazil, which has excellent

highways but hardly any railroads, while many countries have no nuclear power and

only a few have such a developed pipeline system. A number of problems in the US, the

UK and many other developed nations are due to extensive infrastructure depreciation,

as many facilities were built around the middle of the 20th century and therefore are in

need of modernization.

Global breakdown of investments in infrastructure

Source: World Bank

Sources of infrastructure funding — will resources suffice?

There will not be enough funds for full-fledged infrastructure development in all

countries around the world. According to various estimates, the lack of funding in a

number of countries reaches 20-40% of their needs. Thus, worldwide infrastructure

investment in 2014 should amount to about $2.6 trln (3.6% of global GDP), whereas we

assume that no more than $2.1 trln will actually be invested.

Investments in infrastructure broken down by regions

Source: Gazprombank estimates

29%

8%

1%

4% 21%

20%

17%

MOTORWAYS

RAILROADS

SEAPORTS

AIRPORTS

ENERGY

WATER SUPPLY

TELECOMMUNICATIONS

42%

19%

7%

13%

15%

17%

3%

5%

5%

12%

2% 2%

CHINA

JAPAN

INDIA

NORTH AMERICA

EUROPE

RUSSIA

NEAR EAST

LATIN AMERICA

OTHER ASIA

AFRICA

AUSTRALIA AND OCEANIA

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

7

Breakdown of infrastructure investments by sources of funding

FUNDING SOURCES AMOUNT OF INVESTMENTS IN 2014, $ BLN SHARE

State budgets and funds 1,350 65.4%

Bank loans 160 7.7%

Loans extended by international financial organizations 25 1.2%

Share capital of infrastructure companies 40 1.9%

Own funds of infrastructure companies 125 6.0%

Corporate bonds 365 17.7%

Total 2,060 100%

Source: Gazprombank estimates

The key onus for infrastructure investment falls to the government, which

accounts for over 65%. First of all, this is due to the fact that a significant part of

infrastructure performs a social function and does not involve generation of revenue (for

example, the construction of city roads or water supply systems), and for this reason

such projects are of no interest to private investors. In the second place, many

infrastructure facilities are still unable to generate high enough returns to interest private

investors, so for this reason the state is forced to step in (for example, building airport

runways, port dredging operations, or construction of railroads with low freight-traffic

density). According to our estimates, budget-funded infrastructure will amount to some

$1.4 trln in 2014, and it will be traditionally sourced from tax receipts, excise duties or

sovereign wealth funds. That said, we do not expect to see any substantial increase in

budget spending on infrastructure in the coming years, since debt and budget deficits

are forcing governments to curb spending, including infrastructure outlays.

State debt to GDP ratio, %, 2012

Source: IMF

Private investments as equity and debt financing account for about 35% of all

infrastructure investment. In 2014, the volume of private investment in

infrastructure will amount to about $700 bln, of which 30% ($164 bln) will be raised

from infrastructure company profit and equity placements from these companies

among portfolio investors, while the other 70% comes from bond issues and bank

loans, including those issued by international financial institutions, such as the

World Bank, EBRD, Asian Development Bank, etc.

0 50 100 150 200 250

RUSSIA

CHILE

CHINA

TURKEY

THAILAND

INDIA

BRAZIL

SPAIN

CANADA

FRANCE

UK

US

ITALY

GREECE

JAPAN

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

8

Equity financing. Equity financing accounts for less than 2% of aggregate

infrastructure investment, although investors’ interest in infrastructure projects is

growing from year to year. The number of ad hoc infrastructure funds investing in

the shares of infrastructure companies has risen in recent years from zero to over

700. While in 2004, infrastructure funds took in about $2.4 bln, this figure shot up to

$40 bln by 2013. The return on investment in infrastructure facilities by such funds

falls within the range of 10-16%, according to data from Pregin research agency.

Special infrastructure bourse could be established in Japan

Japan Exchange Group, which runs the Tokyo Stock Exchange, intends to set up a

new stock exchange as part of the Tokyo exchange that would specialize in

infrastructure investment. This bourse should be up and running by 2015. The

securities of infrastructure companies and funds are expected to be listed on this

venue. Infrastructure funds are often closed, raising money mainly from a limited

number of institutional investors. By listing on the new market, they will be able to

raise money from a larger pool of investors, including individuals, who are likely to

treat them as an alternative to real estate investment trusts.

The idea of setting up this bourse is regarded as a major challenge given the

Japanese government’s goal of reducing infrastructure spending. Japanese

airports (Kansai International Airport and Sendai Airport) have already shown

interest in this exchange. Moreover, a large number of projects aimed at deploying

alternative sources of energy are being worked out in Japan. These projects

require private investments and it would be extremely important for them to see this

infrastructure bourse get off the ground. It should also not be ruled out that

companies and funds from neighboring Asian countries would also be interested in

making placements on this bourse.

Breakdown by types of investment funds Volume of funds attracted by infrastructure funds, $ bln

Source: Preqin Source Preqin

Bank loans. According to Infrastructure Journal, bank loans account for nearly

$160 bln per annum. The annual dynamic of loan facilities provision to

infrastructure companies is hard to track, though commercial banks have recently

been reluctant to provide loans for projects with long payback periods. After the

2008 financial crisis, the average cost of borrowing for infrastructure objects,

especially those based in emerging countries, grew 1-2 pps. The requirement

regarding the borrowed to own funds ratio rose to 70:30 vs. a pre-crisis 90:10 in

order to mitigate lending risks. This caused an increase of the weighted-average

cost of capital for an infrastructure project. We do not rule out that the cost of

borrowing will continue to grow further due to an increasing number of riskier

infrastructure startups in emerging countries.

2%

43%

42%

13%

INFRASTRUCTURE FUNDS DIRECT INVESTMENT FUNDS

HEDGE FUNDS REAL ESTATE FUND

2.4 5.2

17.9

34.3

24.7

10.7

32

24.3

29.7

40.7

0

5

10

15

20

25

30

35

40

45

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

9

Corporate bonds. Debt financing via corporate bond issuance accounts for about

18% of total investment in infrastructure. According to Bloomberg, the overall

volume of bonds issued by companies in infrastructure sectors (energy, telecoms,

construction) in 2013 stood at $365 bln, of which 25% occurred in the US,

approximately 25% in Europe and 15% in China. The bulk of placements are

concentrated in the energy (50%) and telecommunications (25%) sectors. The

volume of placements in infrastructure sectors has recently soared, which seems

attributable to a tightening of lending requirements by commercial banks for long-

term infrastructure projects, on the one hand, and the rollout of the QE program in

the US that caused a decrease in the cost of public borrowing. We believe the key

investors in infrastructure bonds are pension and hedge funds as well as

commercial banks.

Volume of corporate bonds issued in infrastructure sectors, $ bln Pension savings as % of GDP, 2012

Source: Bloomberg, Gazprombank Source: OECD

Numerous countries have been recently been striving to arrange public-private

partnerships (PPP) in infrastructure development. As a result, the overall volume of

private investment under the PPP scheme has almost quadrupled over the past 10

years, to $180 bln in 2012. That said, the share of PPP in overall infrastructure

investment stands at a modest 8%. Furthermore, the global financial crisis of 2008

halted this growth due to the aforementioned reasons: a reduction of state spending on

infrastructure and a tightening of lending requirements by commercial banks. At the

same time, the noticeable growth of investment on the part of infrastructure funds

pertains to the most attractive projects that can well do without state support.

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 0% 50% 100% 150% 200%

INDIA

CHINA

INDONESIA

RUSSIA

TURKEY

KOREA

THAILAND

GERMANY

NORWAY

PORTUGAL

SWEDEN

BRAZIL

PERU

JAPAN

HONG KONG

DENMARK

CHILE

CANADA

US

AUSTRALIA

UK

SWITZERLAND

NETHERLANDS

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

10

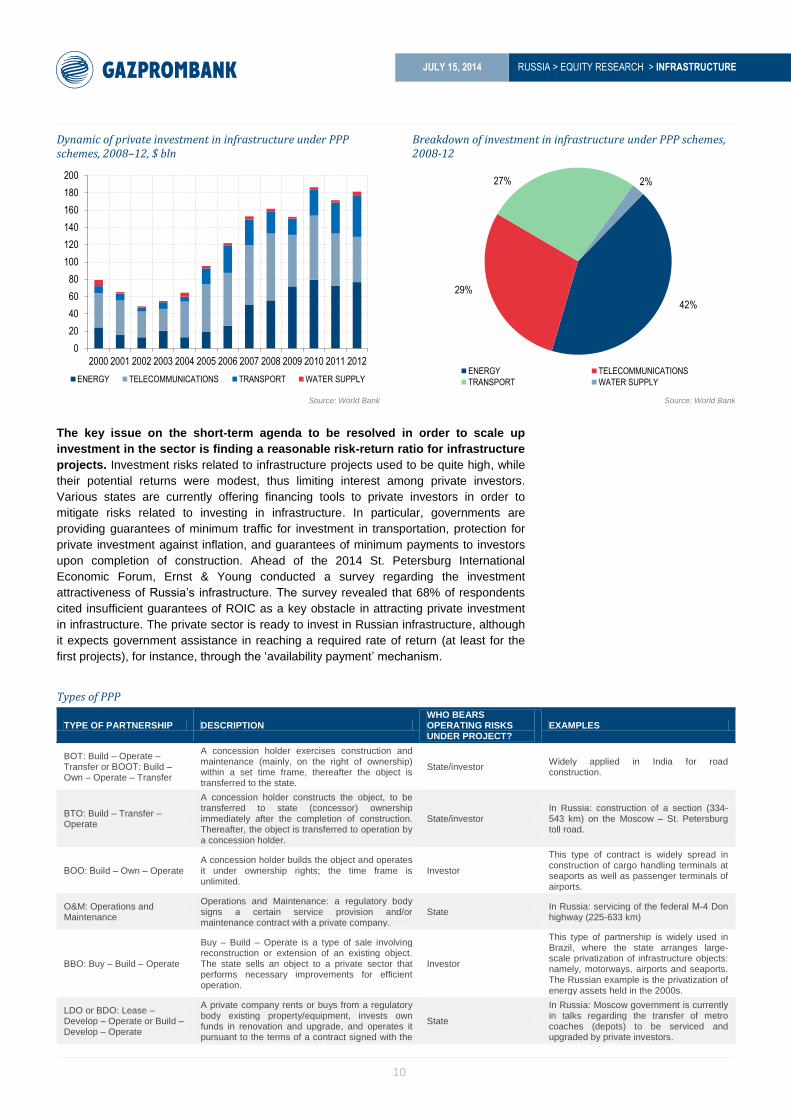

Dynamic of private investment in infrastructure under PPP schemes, 2008–12, $ bln

Breakdown of investment in infrastructure under PPP schemes, 2008-12

Source: World Bank Source: World Bank

The key issue on the short-term agenda to be resolved in order to scale up

investment in the sector is finding a reasonable risk-return ratio for infrastructure

projects. Investment risks related to infrastructure projects used to be quite high, while

their potential returns were modest, thus limiting interest among private investors.

Various states are currently offering financing tools to private investors in order to

mitigate risks related to investing in infrastructure. In particular, governments are

providing guarantees of minimum traffic for investment in transportation, protection for

private investment against inflation, and guarantees of minimum payments to investors

upon completion of construction. Ahead of the 2014 St. Petersburg International

Economic Forum, Ernst & Young conducted a survey regarding the investment

attractiveness of Russia’s infrastructure. The survey revealed that 68% of respondents

cited insufficient guarantees of ROIC as a key obstacle in attracting private investment

in infrastructure. The private sector is ready to invest in Russian infrastructure, although

it expects government assistance in reaching a required rate of return (at least for the

first projects), for instance, through the ‘availability payment’ mechanism.

Types of PPP

TYPE OF PARTNERSHIP DESCRIPTION WHO BEARS OPERATING RISKS UNDER PROJECT?

EXAMPLES

BOT: Build – Operate –Transfer or ВООТ: Build – Own – Operate – Transfer

A concession holder exercises construction and maintenance (mainly, on the right of ownership) within a set time frame, thereafter the object is transferred to the state.

State/investor Widely applied in India for road construction.

BTO: Build – Transfer – Operate

A concession holder constructs the object, to be transferred to state (concessor) ownership immediately after the completion of construction. Thereafter, the object is transferred to operation by a concession holder.

State/investor In Russia: construction of a section (334-543 km) on the Moscow – St. Petersburg toll road.

ВОО: Build – Own – Operate A concession holder builds the object and operates it under ownership rights; the time frame is unlimited.

Investor

This type of contract is widely spread in construction of cargo handling terminals at seaports as well as passenger terminals of airports.

O&M: Operations and Maintenance

Operations and Maintenance: a regulatory body signs a certain service provision and/or maintenance contract with a private company.

State In Russia: servicing of the federal М-4 Don highway (225-633 km)

BBO: Buy – Build – Operate

Buy – Build – Operate is a type of sale involving reconstruction or extension of an existing object. The state sells an object to a private sector that performs necessary improvements for efficient operation.

Investor

This type of partnership is widely used in Brazil, where the state arranges large-scale privatization of infrastructure objects: namely, motorways, airports and seaports. The Russian example is the privatization of energy assets held in the 2000s.

LDO or BDO: Lease –Develop – Operate or Build –Develop – Operate

A private company rents or buys from a regulatory body existing property/equipment, invests own funds in renovation and upgrade, and operates it pursuant to the terms of a contract signed with the

State

In Russia: Moscow government is currently in talks regarding the transfer of metro coaches (depots) to be serviced and upgraded by private investors.

0

20

40

60

80

100

120

140

160

180

200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

ENERGY TELECOMMUNICATIONS TRANSPORT WATER SUPPLY

42%

29%

27% 2%

ENERGY TELECOMMUNICATIONS

TRANSPORT WATER SUPPLY

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

11

TYPE OF PARTNERSHIP DESCRIPTION WHO BEARS OPERATING RISKS UNDER PROJECT?

EXAMPLES

regulatory body.

Turnkey Turnkey construction. State Conventional building contracts.

DB: Design – Build A private company is in charge of design and construction under the project.

DBO: Design – Build – Operate

A single contract is signed for design, construction and operation.

Source: Gazprombank

Examples of investment tools used in various countries for infrastructure projects

China

China is the world’s largest investor in infrastructure, with the volume of investment over

the past 20 years averaging 8.5% of GDP. The bulk of investment is earmarked for motor

and railroad construction, as well as energy development. According to McKinsey, the cost

of Chinese infrastructure assets stands at 76% of GDP, exceeding the lowest

recommended threshold of 70%. It appears that in the coming years there will be a

shrinkage of investment in infrastructure to 6-7% of GDP, although it will remain at the

highest level globally at nearly $400 bln per annum, or 15% of the world total. Chinese

state banks, including China Development Bank, play the key role in financing Chinese

infrastructure, with the latter accounting for around half of local investment in infrastructure.

Top Chinese banks – key investors in the country’s infrastructure

NAME ASSETS, $ BLN DESCRIPTION

China Development Bank

1.220

Established in 1994 to finance China’s infrastructure projects. A 100% stake is owned by the state through the Finance Ministry. Bonds ($800 bln) account for more than 70% of the bank’s liabilities and are considered risk-free, as China’s Finance Ministry provides guarantees. In 2012, the bank placed $200 bln in yuan-denominated bonds (with a coupon rate of 3.85-4.75%), or half of China’s overall investment in infrastructure. The bank’s bonds account for 20% of China’s domestic bond market. Local companies and commercial banks are the major buyers of these bonds.

Industrial and Commercial Bank of China

2.837

China’s largest bank by size of assets. The state is a controlling shareholder, but some of the shares are publicly traded. Approximately 80% of liabilities are in the form of deposits, while the share of debt in the bank’s liabilities stands at below 2% ($40 bln). Around 15% of assets are in the form of infrastructure financing. In 2013, the bank allocated ca. $30 bln to infrastructure companies.

China Construction Bank

2.490 The major source of liabilities is retail deposits (nearly 80% of liabilities), while other types of borrowing account for only 8% ($240 bln). Around 15% of assets ($370 bln) are in the form of infrastructure financing.

Bank of China 2.276 Deposits account for approximately 70% of liabilities, while bonds comprise 15% ($360 bln, of which $280 bln is internal borrowing and $80 bln external).

Source: Gazprombank

High-speed railways — government financing prevails. Over the past 20 years,

China has created an extended railway network with a total length of 15,000 km

and maximum traveling speed of up to 350 km/h. To support and expand railway

infrastructure, state-run China Railways Corporation (the prototype of Russian

Railways), which owns the country’s entire railway infrastructure, uses various

sources of funding. In particular, 40-50% of the total investment needs come from

state banks and are guaranteed by the government (China Development Bank,

Industrial and Commercial Bank of China, and China Construction Bank), about

40% is in the form of CNY-nominated bonds, and the remaining 10-20% is ensured

by provinces through which the railroad will pass. China Railways is the world’s

largest transportation company, with assets exceeding $600 bln. The company’s

liabilities total about $460 bln, of which $170 bln are in the form of bonds. To build

the section of the railroad, a separate company might be created with a controlling

stake belonging to China Railways, while the remaining part will be sold to

investors, namely Chinese insurance and construction companies participating in

construction of this road.

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

12

According to an infrastructure report prepared by Ernst & Young, from 1997 to

2007 China conducted a six-stage campaign to increase train travelling speed. As

a result, construction of tunnels and bridges allowed for more declivity, the turning

radius was reduced and continuous welded rails were laid. In 1997, the total length

of high-speed tracks, where trains could pick up speed over 160 km/h, stood at

752 km. By 2007, their length was increased to 14,000 km. Following extended

discussion among experts on which type of high-speed train to choose – traditional

or maglev – in 2006 the PRC’s State Council chose the former (HSR). The next

stage was the development of the high-speed train series CRH (China Railway

High Speed), which ensured a further increase in travelling speed. In 2004, the

Railways Ministry announced a tender to supply 200 high-speed trains that could

conduct transportation services at a speed of over 200 km/h. Applications were

filed by such large companies as Alstom (France), Siemens (Germany),

Bombardier Transportation (Germany), and consortium of Japanese investors

headed by Kawasaki. As a result of the tender, contracts were signed with Alstom,

Bombardier and Kawasaki, while Siemens was not among the winners, as it

refused to lower the price for the trains and technology transfer. The following year,

Siemens reduced the price, which allowed it to win the tender to supply 60 trains to

conduct transportation service at a speed of 300 km/h. Each foreign manufacturer

adapted the supplied high-speed train to China’s unified standards. Train assembly

was performed either jointly or with the assistance of Chinese manufacturers.

Thanks to technological cooperation, Chinese engineers were able to design their

own high-speed trains, based on trains made by foreign manufacturers. Chinese

trains carry passengers from Beijing to Shanghai (1,463 km) in less than six hours,

i.e. twice as fast compared with previous-generation trains. High-speed trains also

allowed an increase in carrying traffic, resulting in higher capacity for the railway

transportation system. As high-speed trains used the same tracks as freight trains,

the only way to further increase the speed and capacity was to build high-speed

lines for passenger trains. Recently, China launched a campaign to build dedicated

high-speed tracks for passenger transportation.

Toll roads — private financing prevails. China embarked on active construction

of toll roads in the early 1990s. The total length of toll roads currently approaches

100,000 km, linking all provinces and major cities in China. Total investment

exceeded $260 bln ($2.6 mln/km). China's State Council and the Transport Ministry

approve projects and construction standards, while their implementation and

financing is performed by the administrations of involved provinces. Originally the

provinces financed up to 90% of road construction from their budgets and through

loans. Once construction is completed, the toll road is incorporated into the capital

of a new company, the shares of which are placed on an equity exchange among

international investors. Administrations spend the received money to build a new

road. Thus, currently about 45% of road construction funds are self-raised, namely

through the sale of shares via IPOs and cash flow from existing toll roads. The

remaining 40% of the investment is still provided by provinces (through loans) and

only 15% comes from the federal budget. Currently more than 15 such companies

with a total market capitalization of $53 bln ($115 bln inclusive of debt) are trading

on the Hong Kong Stock Exchange. Their distinguishing features are high margins

(EBITDA margins of 40-60%) and solid dividends. The average P/E multiple of

these companies for 2014 stands at around 10.0x, which is close to the average of

Hong Kong’s Hang Seng Index.

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

13

China’s publicly-traded companies – owners of toll roads

COMPANY TICKER MCAP, $ MLN. EV, $ MLN FREE FLOAT

CHINA COMMUNICATIONS CONSTRUCTION 1800 HK 10,361 25,246 100.0%

CHINA RAILWAY CONSTRUCTION 1186 HK 9,227 18,826 90.9%

CHINA RAILWAY GROUP 390 HK 9,181 30,711 90.9%

JIANGSU EXPRESS 177 HK 4,698 5,296 100.0%

ZHEJIANG EXPRESSWAY 576 HK 3,941 3,827 100.0%

SHANDONG HI-SPEED 600350 CH 2,277 4,338 12.7%

SHANGHAI TUNNEL ENGINEERING 600820 CH 2,142 4,415 35.5%

SHENZHEN INTL HOLDINGS 152 HK 2,090 4,541 47.4%

HOPEWELL HIGHWAY INFRASTRUCTURE 737 HK 1,474 1,470 29.2%

SICHUAN ROAD&BRIDGE 600039 CH 1,373 3,599 49.3%

SICHUAN EXPRESSWAY 107 HK 1,255 2,419 98.9%

SHENZHEN EXPRESSWAY 600548 CH 1,163 2,710 14.9%

JIANGXI GANYUE EXPRESSWAY 600269 CH 1,045 2,058 46.2%

ANHUI EXPRESSWAY 995 HK 1,037 1,490 95.0%

FUJIAN EXPRESSWAY DEVELOPMENT 600033 CH 932 2,427 44.7%

YUEXIU TRANSPORT INFRASTRUCTURE 1052 HK 850 2,028 100.0%

Total

53,047 115,400

Source: Bloomberg

China’s high-speed railroads financing breakdown China’s toll roads financing breakdown

Source: World Bank Source: World Bank

India

Over the past 20 years, India’s investment in infrastructure has averaged 5% of GDP,

which was insufficient given the country’s average annual GDP growth rate of 7%.

Under the new five-year development plan (2013-17) the Indian government has

decided to double the amount of investment vs. the previous plan to $1 trln, or $200 bln

annually (10% of GDP). The bulk of investment will focus on transportation (35%),

utilities (34%) and telecommunications (17%). This is the most ambitious plan to

stimulate the economy among developing countries, although it is unlikely to be fully

implemented due to a shortage in funding of about $300 bln. The Indian government

plans to provide 53% of the required investment, 25% of which will be covered from the

state budget ($250 bln), 11% will come from extra-budgetary sources, and 17% through

public borrowings. The remaining 47% is comprised of private investment, including

40%

40%

10%

STATE BANKS BONDS REGIONAL BUDGETS

15%

40%

45%

STATE BUDGET BORROWINGS INTERNAL FINANCING (IPO, CASH FLOW)

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

14

15% from investors’ own funds and 35% through borrowing. However, so far the

confirmed size of private investment amounts to ca. $300 bln.

China has offered India financial support and is prepared to invest the $300 bln shortfall

in the country’s infrastructure. China is apparently interested in engaging its construction

companies, equipment and materials. However, the Indian government is in no hurry to

accept the proposal, as a number of infrastructure sectors are considered strategic

(telecommunications, utilities) and do not allow Chinese capital.

Sources of funding implied by the plan (2012-17) Confirmed non-budgetary sources of funding (2012-17)

Source: Deloitte Source: Deloitte

Potential non-budgetary sources of funding for Indian infrastructure under the five-year

development plan until 2017 include the following:

Commercial banks. They could invest about $120 bln over the next five years,

accounting for 12% of the total investment required and 42% of all currently

available private investment.

Non-bank financial institutions ($64 bln; 22%). India has many specialized non-

bank financial corporations, targeting infrastructure investment. They are India

Infrastructure Finance Corporation (IIFCL), National Highways Authority of India,

Rural Electrification of India, Power Finance Corporation (PFC), and Indian Railway

Finance Corporation.

Insurance companies ($1 bln; 3%). Insurance companies that are not involved with

life insurance business are obliged to invest no less than 15% of their assets in

Indian infrastructure.

Key infrastructural financial organizations in India

COMPANY DESCRIPTION CAPITAL STRUCTURE

India Infrastructure Finance Company Limited (IIFCL)

A state-owned corporation established in 2006 to support infrastructure projects. The company participates in infrastructure projects as a co-investor, offering direct financing or providing guarantees to improve the credit quality of infrastructure bonds. The company also takes part in implementation of over 200 projects with a total value of $77 bln.

The company’s assets stand at $5.8 bln. The total value of bond placements amounts to $4.9 bln with a coupon of 8.0-8.9%. In 2013, the company issued loans and guarantees in the amount of $1.9 bln. The company’s bonds are not state-backed, although its ratings are at the sovereign level.

National Highways Authority of India (NHAI)

Government agency for road construction and management.

The state budget is the main source of financing for the agency. At the same time, the regulator has a small number of public loans totaling $2.5 bln carrying 7.4-8.3% coupon rates.

Power Finance Corporation State-run corporation that was specially created in order to attract investments to India’s electric power generation sector.

The Indian government owns 73% of the company’s shares, while free float accounts for the remainder. The company’s MCap stands at $4 bln. The overall number of loans (mainly public) stands at $24 bln with coupon rates ranging from 8.0-9.7%.

Rural Electrification Corporation Limited

State-run corporation specially created to attract investments into India’s power grid assets.

The Indian government holds 65% of the company’s shares with the remainder in free float. The company’s MCap stands at $5.5 bln. Public loans

24.8%

10.6%

16.5%

14.8%

33.3%

STATE BUDGET

NON-BUDGETARY FUNDS

PRIVATE INVESTMENTS

GOVERNMENT BONDS

INVESTORS' OWN FUNDS

42% 22%

8%

3%

25% COMMERCIAL BANKS

NONCOMMERCIAL FINANCIAL INSTITUTIONS

EXTERNAL BORROWINGS

INSURANCE COMPANIES

EQUITY FINANCING

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

15

COMPANY DESCRIPTION CAPITAL STRUCTURE

taken out by the company total $18.7 with coupon rates ranging from 8.0-9.7%.

Indian Railway Finance Corporation

Indian Railways’ 100%-owned subsidiary. The company attracts cash from the market to finance the purchases of equipment for subsequent lease to the parent company.

The company’s total assets stand at $12 bln, of which $11 bln are in the form of public offerings.

Infrastructure Development Finance Company

The company was established in 1997 as a government agency for financing various infrastructure sectors. Sometime after that, the company turned into a joint-stock company and offered its shares on the stock exchange.

The company’s total assets amount to $12 bln. The government owns 17% of the company’s shares, while international investors hold the remainder.

Indian Leasing and Financial Services

The company was established in 1987 by the central bank of India and a number of other state bodies. Later, Life Insurance Corporation of India, ORIX Corporation (Japan), and Abu Dhabi Investment Authority also became the company’s shareholders. The company attracts investment in India’s infrastructure facilities. It also builds and manages highways, energy facilities, ports, city infrastructure, and water delivery systems.

Total investments stand at around $25 bln. The major shareholders are Life Insurance Corporation of India (25.34%), ORIX Corporation (23.00%), Abu Dhabi Investment Authority (11.09%), Central Bank of India (8.34%), State Bank of India (6.98%), and ILFS Employees' Welfare Trust (13.65%).

Source: Gazprombank estimates

In addition, the offerings of infrastructure bonds, the incomes from which are not taxed

(tax-free bonds), are widespread in India. The government sets an annual limitation on

such offerings. For example, the government allowed non-banking financial corporations

to issue only $9.2 bln in tax-free bonds in 2014; while private investors were allowed to

issue about $5.0 bln. Moreover, the government sets tax holidays for infrastructure

companies for a period of up to 10 years.

Total ivestments in India, $ bln Investment structure in India

Source: IBEF Source: IBEF

Railways. India has the world’s fourth-longest railway network. Daily passenger

traffic via this network amounts to 30 mln people (vs. about 3 mln passengers

travelling via Russian Railways’ network per day). In 2013, Indian trains carried

about 1.0 bln tonnes of cargoes (vs. 1.2 bln tonnes in Russia). State-run Indian

Railways owns the entire railway infrastructure. The new government development

plan for 2013-17 envisages that investments in railway infrastructure will increase

by 2.5 times to $100 bln. However, investments for 2014 are planned at $12 bln,

which is comparable with Russian Railways’ capex. About 40% of the company’s

investment is financed by the state budget, 30-35% is allocated from company’s

net income and borrowing, and the remaining 25-30% is attracted from additional

sources, including around $1 bln from private investors. Indian Railways includes a

special investment unit called Indian Railway Finance Corporation, which focuses

on attracting private investment. The unit’s assets amount to $12 bln. The

investment company mainly uses the attracted funds to finance the purchases of

locomotives and rail cars, which are subsequently leased out to its parent company

Indian Railways. In early 2014, the company placed several bond tranches

denominated in Indian rupees totaling about $5 bln. The maturity of the bonds was

set at 10-15 years and the coupon rates ranged from 8.2-8.6%. That said, these

0

10

20

30

40

50

60

2009 2010 2011 2012 2013 2014 2015 2016 2017

HIGHWAYS RAILWAYS

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012

PRIVATE PUBLIC % OF GDP

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

16

bonds were not subject to income tax. In addition, the Indian government is

allowing an increasing number of private investors to take part in projects for the

construction of railway infrastructure facilities, i. e. depots, storage facilities, railway

stations, and even special separate rail lines approaching ports in order to speed

up the elimination of existing bottlenecks. Construction of the Western and Eastern

railway corridors with a total length of 3,300 km is now one of the main

infrastructure projects in India. The implementation of this project is to be

completed in 2017, and should increase cargo turnover throughout the country.

Total investments in the project amount to $16.7 bln.

Highways. India has the world’s second-largest highway network (4.7 mln km).

More than 60% of cargoes are carried throughout the country via highways. The

development of a highway network is one of the top priority tasks of the Indian

government. Under the public private partnership, over 50% of private

investments are allocated for highway construction. The bulk of investments are

conducted under the “build-operate-transfer” principle, which envisages a private

investor (or consortium of investors) building a road and using it for 20-30 years,

with the investor eventually returning the road to the government. The Indian

government supports investors by allocating special grants for road construction

(up to 40% of the project value). The Indian government also awards

infrastructure projects with 100% tax holidays over the first five years and 30%

holidays for the following 30 years.

Brazil

The Brazilian experience of attracting private investment to the infrastructure sector is

quite interesting, although it still cannot be recognized as very successful. Since the

mid-1990s, the country’s authorities have demonstrated their commitment to mass

privatization and concession of infrastructure facilities. As a rule, an investor that is

ready either to pay the maximum price for an asset, or to set the minimum tariff for use

of the infrastructure, is selected as the winner in the privatization of roads, airport and

postal terminals. However, Brazil’s infrastructure sector is still poorly developed. The

country was ranked 114th out of 148 countries rated by the Global Competitiveness

Index (GCI), and total investment in Brazilian infrastructure does not exceed 1.5% of

GDP. The main problem involves the high political and economic risks and quite low

returns on investment (ca. 6%). The country suffers from complex and lengthy

bureaucratic procedures, which considerably impede the implementation of

infrastructure projects and decrease returns on private investment.

Projects involving the construction and management of highways and railways offer low

returns on investment. However, investment in airport and seaport infrastructure

remains quite attractive. For example, the Singapore port operator Changi and Brazilian

construction company Odebrecht recently offered $8.2 bln on the tender to get the

airport in Sao Paulo in concession, which is four times the initial price of the tender.

In contrast to China and India, Brazil suffers from a lack of government bodies that

support and attract investment in the infrastructure sector. The Brazilian Development

Bank is the only such organization with assets exceeding $300 bln. However, the

efficiency of the bank’s efforts to develop the country’s infrastructure sector is unclear,

as the bank also supports other branches of the economy, i. e. social, education, and

healthcare sectors, small businesses, environmental projects, etc. Each year, the bank

invests $80-90 bln in the Brazilian economy, of which 35-40% is comprised of

investment in infrastructure projects.

A few years ago, in an effort to attract more private investment to the infrastructure

sector, the Brazilian government set the terms for an offering of special infrastructure

bonds, which must meet the following criteria:

The funds raised via the bond offering must be only used to finance the company’s

investment program;

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

17

The minimum maturity is four years;

The bonds carry a fixed coupons or coupons linked to inflation rates;

The bonds can be redeemed ahead of schedule no earlier than two years after the

bond issuance;

Proceeds from the bonds are not subject to tax (earlier the income tax stood at

6%).

The Brazilian government expects that the bonds will generate up to 10-20% of total

investment in the infrastructure sector. However, Brazilian companies still unwillingly

use infrastructure bond offerings as a low-cost way to attract investment, since such

borrowings remain expensive. Only a few companies have thus far placed infrastructure

bonds with inflation-linked coupons ranging between 9.5-14.0%.

US

According to the American Society of Civil Engineers (ASCE), US demand for

investment in economic infrastructure amounts to about $3 trln for the period through

2020, or more than $400 bln annually. However, because of efforts to reduce the

country’s budget deficit, the planned investment (both public and private) in the

infrastructure sector turned out to be far below the real needs standing at $1.8 trln

through 2020, or around $220 bln annually (less than 2% of GDP). The decrease in

investment in US’ infrastructure is a matter of great concern in that country. Some

experts believe that capital that was earlier withdrawn from the country could become an

additional source of investment in US infrastructure. Lawmakers have suggested

exempting capital returned to the country from taxes, while obliging to invest these funds

in US infrastructure bonds.

The bulk of investment will be shared between two infrastructure segments – highways

(61%) and energy (36%).

Highways. Road construction and reconstruction is financed through the Highway

Trust Fund, mainly replenished with proceeds from fuel excises at a level of 18.3

cents/gallon. The fund’s annual income stands at around $45 bln, but these

proceeds fail to cover its expenses. The major issue is that given the flat level of

inflation, excises have not been raised for the past 20 years, while the growing

number of cars has been accompanied by diminishing fuel consumption, which has

a negative impact on the fund’s financials. Each state is entitled to set its own fuel

levy in order to arrange financing of regional roads. Alaska has the lowest size of

26.4 cents, while New York enjoys the highest rate of 69.6 cents. US fuel levies

average 48.8 cents, or 13.3% of the average retail price of a gallon of gasoline.

Railways. The particularity of the US railway infrastructure is that the segment is

wholly owned by private railway operators, who mainly focus on cargo

transportation (53% of total turnover throughout the country), while passenger

transport accounts for a minimal share.

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

18

CURRENT STATUS OF RUSSIA’S INFRASTRUCTURE NEEDS

In 2013, Russia ranked 93rd among 148 countries by the quality of its infrastructure in the

rating of the Global Competitiveness Report 2013-2014, which is calculated by the World

Economic Forum (up eight positions compared to the previous year). Incidentally, this

rating is based on the opinions of entrepreneurs who do not always have a clear picture of

the actual status of the quality of infrastructure in the country. For example, oddly enough

Russia ranks 138th in terms of the Road Quality Index, coming between the Republic of

Chad and Yemen, which seems ridiculous. By the quality of its railroads, Russia ranks

38th, trailing such countries as Finland (6th) and Singapore (10th), countries where a

railroad system barely exists. Moreover, in terms of overall quality of infrastructure, other

CIS countries, including Kazakhstan and Ukraine, rank considerably higher than Russia –

in 64th and 70th position, respectively. Given that this index is overly subjective and does

not reflect the actual status of infrastructure, we believe that the country’s dynamics in the

index over a number of years is of greater relevance, as it is capable of a capturing trends

and conveying changes in the quality of infrastructure.

Russia's position in the rating of countries in terms of the quality of infrastructure

Source: World Competitiveness Index

Changes of Russia’s position in the rating of infrastructure quality

RUSSIA 2008 RUSSIA 2012 RUSSIA 2013 CHINA 2013 BRAZIL 2013 INDIA 2013

Overall quality of infrastructure 81 101 93 74 114 85

Quality of roads 106 136 36 54 120 84

Quality of railroads – 30 31 20 103 19

Quality of seaport infrastructure 72 93 88 59 131 70

Quality of airport infrastructure 79 104 102 65 123 61

Source: World Competitiveness Index

1 2 3 6 10

14 15 19

23 25 28 34

41 45

51

61 64 70

74 82 85

93 98 101

106 114

120

137

0

20

40

60

80

100

120

140

160

SW

ITZ

ER

LAN

D

HO

NG

KO

NG

FIN

LAN

D

FR

AN

CE

GE

RM

AN

Y

JAP

AN

CA

NA

DA

US

A

SO

UT

H K

OR

EA

MA

LAY

SIA

UK

AU

ST

RA

LIA

TU

RK

EY

CH

ILE

ISR

AE

L

TH

AIL

AN

D

KA

ZA

KH

ST

AN

UK

RA

INE

CH

INA

IND

ON

ES

IA

IND

IA

RU

SS

IA

PH

ILIP

PIN

ES

PE

RU

RO

MA

NIA

BR

AZ

IL

AR

GE

NT

INA

VE

NE

ZU

ELA

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

19

Russia’s infrastructure investment needs total at least 4% of GDP. Large-scale

investments are required in virtually all infrastructure segments, including highways and

railroads, power grids, water supply, telecommunications, ports and airports. According

to estimates by McKinsey, Russia spent an average 3.4% of GDP on infrastructure from

1999 through 2011. This figure is broadly in line with our own estimates. By comparison,

global infrastructure investments during this period averaged 3.8% of GDP (3.1% in

developed countries and 5.5% in developing countries). However, going forward the

volume of investments would have to be raised to at least 4% of GDP in order to

maintain domestic infrastructure in good shape and secure its harmonious expansion in

line with GDP growth. Thus, assuming that average annual GDP grows by 2.5% until

2030, the total need for infrastructure investments in Russia during this period would be

RUB 60 trln ($1.7 trln), or about $100 bln per year.

Planned infrastructure spending in Russia will be about 3.6-4.2% of GDP until

2020. In order to assess the magnitude of planned infrastructure investment in Russia,

we analyze a large number of federal target programs spearheaded by the RF

government, Russia’s transport strategy until 2030, federal spending and regional

infrastructure budgets, as well as the investment programs of natural monopolies

(Gazprom, Transneft, Russian Railways), and of companies that invest in infrastructure

(mainly in power engineering and telecommunications). On the basis of these

documents and our calculations, about 3.6-4.2% of GDP will be spent on infrastructure

projects or RUB 3.2-3.6 trln per annum ($90-100 bln), roughly on par with investments

by large developed countries. Infrastructure investments will reach RUB 22.5 trln, or

about 2.2% of global infrastructure investments by 2020. These resources should suffice

for moderate expansion of domestic infrastructure (including highways and railroads), to

raise its quality and efficiency, but would not be enough for accelerated expansion

compared to Russian economic growth. For this reason, many infrastructure restrictions

will remain in place in the country.

A distinguishing feature of investments in the Russian economy is the large proportion

of spending on construction and servicing of pipeline transport. The main investors here

are Gazprom and Transneft, which will sink at least RUB 800 bln per year into

infrastructure by 2020. The structure of Russia’s infrastructure spending, as is the case

in most countries around the world, is dominated by investments in transportation

infrastructure (55%), mostly for the expansion of highways (45%), whereas pipeline

transport investments come second with a proportion of 25%. The other 20% includes

investments in telecommunications, power grids (investments in generating assets are

not classifiable as infrastructural according to our classification) and public utilities

(mainly water supply; housing maintenance and repair are also not regarded as

infrastructure investments).

The RF president and government are aware of the importance of raising

infrastructure investments, since this is one of the key factors stimulating

economic growth in the country. Specifically, the president tasked the government

with expanding infrastructure in a number of areas over the coming decade, as follows:

Double the construction of federal highways from 2013 through 2022 compared

with 2003-12.

Expand the total length of federal highways compliant with statutory requirements

and transport operating standards to 44,000 km (83% of total infrastructure).

Increase the aggregate cargo handling capacity of Russian seaports by 302 mln

tonnes (port capacity currently stands at 800 mln tonnes).

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

20

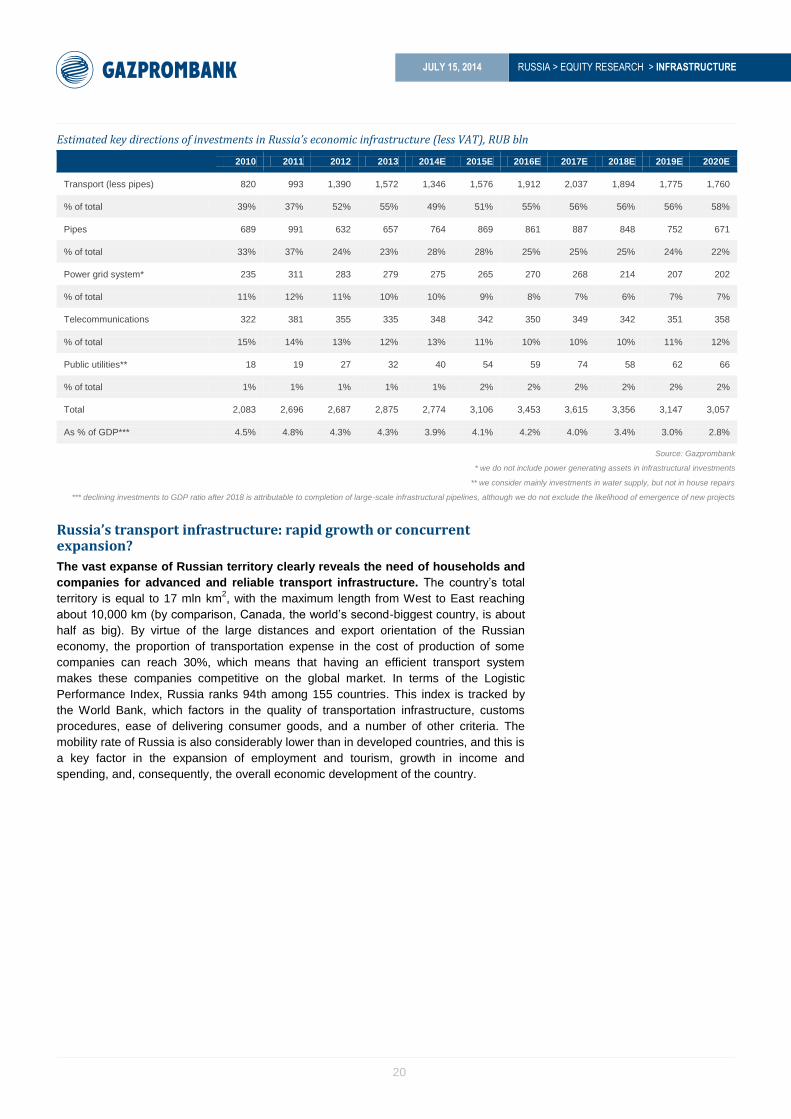

Estimated key directions of investments in Russia’s economic infrastructure (less VAT), RUB bln

2010 2011 2012 2013 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Transport (less pipes) 820 993 1,390 1,572 1,346 1,576 1,912 2,037 1,894 1,775 1,760

% of total 39% 37% 52% 55% 49% 51% 55% 56% 56% 56% 58%

Pipes 689 991 632 657 764 869 861 887 848 752 671

% of total 33% 37% 24% 23% 28% 28% 25% 25% 25% 24% 22%

Power grid system* 235 311 283 279 275 265 270 268 214 207 202

% of total 11% 12% 11% 10% 10% 9% 8% 7% 6% 7% 7%

Telecommunications 322 381 355 335 348 342 350 349 342 351 358

% of total 15% 14% 13% 12% 13% 11% 10% 10% 10% 11% 12%

Public utilities** 18 19 27 32 40 54 59 74 58 62 66

% of total 1% 1% 1% 1% 1% 2% 2% 2% 2% 2% 2%

Total 2,083 2,696 2,687 2,875 2,774 3,106 3,453 3,615 3,356 3,147 3,057

As % of GDP*** 4.5% 4.8% 4.3% 4.3% 3.9% 4.1% 4.2% 4.0% 3.4% 3.0% 2.8%

Source: Gazprombank

* we do not include power generating assets in infrastructural investments

** we consider mainly investments in water supply, but not in house repairs

*** declining investments to GDP ratio after 2018 is attributable to completion of large-scale infrastructural pipelines, although we do not exclude the likelihood of emergence of new projects

Russia’s transport infrastructure: rapid growth or concurrent expansion?

The vast expanse of Russian territory clearly reveals the need of households and

companies for advanced and reliable transport infrastructure. The country’s total

territory is equal to 17 mln km2, with the maximum length from West to East reaching

about 10,000 km (by comparison, Canada, the world’s second-biggest country, is about

half as big). By virtue of the large distances and export orientation of the Russian

economy, the proportion of transportation expense in the cost of production of some

companies can reach 30%, which means that having an efficient transport system

makes these companies competitive on the global market. In terms of the Logistic

Performance Index, Russia ranks 94th among 155 countries. This index is tracked by

the World Bank, which factors in the quality of transportation infrastructure, customs

procedures, ease of delivering consumer goods, and a number of other criteria. The

mobility rate of Russia is also considerably lower than in developed countries, and this is

a key factor in the expansion of employment and tourism, growth in income and

spending, and, consequently, the overall economic development of the country.

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

21

Logistics performance index, 2013 Population mobility index

Source: World Bank Source: Gazprombank

Transportation costs of Russian companies are higher than in developed

countries. In the USSR, there was a powerful transport infrastructure, which, until

recently, was more or less capable of meeting the needs of Russia’s rapidly growing

economy. However, traffic handling capacity in the most developed areas has peaked in

recent years and is essentially no longer capable of coping with growing demand. This

situation has given rise to massive traffic jams (average speed on downtown Moscow

roads is 20 kph, compared to 40 kph in large European cities); it has also created

bottlenecks on railroads and reduced the speed of rolling stock (average speed of

freight trains decreased by 12% to 300 km per day in 2013).

Dynamic of Russia's cargo turnover, bln t/km Growth index of infrastructure indicators

Source: State Statistics Service Source: State Statistics Service, Gazprombank estimates

The rate of investments in development of Russia’s transport infrastructure is

already close to that of developed economies, about 3% of GDP. These funds are

sufficient for moderate expansion, but are insufficient for qualitative

improvement. Countries with developed infrastructure spend an average 2.5-3.0% of

GDP per year on maintenance and development, in line with World Bank

recommendations. According to our estimates, Russia also spends about 3% of GDP,

including investments in pipeline transport. Net of that item (only highways and

railroads, airports and ports), the proportion of GDP spending has reached 2.3% in

recent years, although it was less than 1% in the mid-2000s. There is no point in

comparing Russia with China or India, where spending on transport infrastructure is

considerably higher, as these countries frequently create infrastructure from scratch,

whereas Russia went through this phase during industrialization in the 20th century.

1 2 3 4 5 9 10 13 16 24 28

35 42

50 54 65

71

88 90 99

125 135

149

0

20

40

60

80

100

120

140

160

GE

RM

AN

Y

NE

TH

ER

LAN

DS

BE

LGIU

M

UK

SIN

GA

PO

RE

US

A

JAP

AN

FR

AN

CE

AU

ST

RA

LIA

FIN

LAN

D

CH

INA

TH

AIL

AN

D

CH

ILE

ME

XIC

O

IND

IA

BR

AZ

IL

PE

RU

KA

ZA

KH

ST

AN

RU

SS

IA

BE

LAR

US

AZ

ER

BA

IJA

N

MO

NG

OLI

A

KY

RG

YZ

ST

AN

0.5 0.4

2 2.2 2.9

4

0.27

1.4 1.6

0.5 0.4

0.3

0.8

0.32

0

1

2

3

4

5

6

ITA

LY

FR

AN

CE

US

EU

UK

TU

RK

EY

RU

SS

IA

INTERNATIONAL FLIGHTS PER 1 PERSON DOMESTIC FLIGHTS PER 1 PERSON

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1970

1980

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

BY CARS BY INTERNAL WATER TRANSPORT

BY AIR TRANSPORT BY RAILROAD

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

CARGO TURNOVER PRIVATE CARS PER 1,000 PEOPLE FEDERAL ROADS RAILWAYS PIPES

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

22

Investments in transport infrastructure, % of GDP

Source: McKinsey, Gazprombank

* including pipeline transport

** excluding pipeline transport

Plan of development for transport infrastructure until 2020

Russia has a large number of detailed federal and regional special-purpose programs

devoted to the development of transportation infrastructure. These programs provide

detailed overviews of infrastructure projects and deployment costs, but no reference is

made to clear-cut sources of funding. Furthermore, these programs incorporate a

plethora of expenses unrelated to infrastructure issues (for example, passenger air

traffic subsidies, purchase of locomotives, and rolling stock for the railroad industry, as

well as construction of vessels). As a result, programs are often revised and

underfinanced. Nonetheless, they make it possible to analyze the dynamics of industry

development, pinpoint key investment areas, determine their overall trends, and assess

the priorities and status of large projects. The above programs can be summed up as

follows:

Federal Special-Purpose Program Upgrade of the Transport System of Russia 2010-

2020

Transport Strategy until 2030

Federal Budget Spending for 2014 and Subsequent Years

Regional Budgets Spending for 2014 and Subsequent Years, Including Moscow and

St. Petersburg

Investment Programs of Natural Monopolies: Russian Railways, Gazprom, Transneft

and State Company Russian Highways (Avtodor)

In order to assess the size and dynamics of the transport infrastructure market, we

made a number of adjustments to these programs by excluding all expenditures that are

not directly related to infrastructure (for example, subsidization of passenger air travel),

and adjusted them for VAT (18%). We also adjusted some programs downward, since

none of them has been 100% executed. The average implementation rate of federal

programs is 85-90%, while the fulfillment of regional programs is even worse. According

to our estimates, investments in transport infrastructure, not including pipeline transport,

have nearly doubled since 2010 and totaled about RUB 1.5 trln (net of VAT) in 2013.

The table below highlights the main growth factors.

2.3% 2.6% 2.8% 2.9% 3.0% 3.0%

3.3% 3.3% 3.4% 3.7%

6.0%

8.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

RU

SS

IA**

JAP

AN

GE

RM

AN

Y

FR

AN

CE

US

A

RU

SS

IA*

UK

SW

ED

EN

CA

NA

DA

AU

ST

RA

LIA

IND

IA

CH

INA

RUSSIA > EQUITY RESEARCH > INFRASTRUCTURE

JULY 15, 2014

23

Estimated aggregate investments in transport infrastructure, RUB bln

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Federal roads 238 296 375 428 427 495 640 714 664 732 791

Regional roads 308 360 548 620 448 470 493 518 544 571 600

Railroads 198 234 288 274 233 277 277 277 168 168 168

Moscow - Kazan Highspeed Railway 0 0 0 0 0 50 250 300 300 100 0

Metro 38 50 98 134 125 150 141 125 125 126 127

Airports 22 37 59 67 55 47 52 56 57 57 54

Sea ports 15 16 22 51 59 88 59 47 36 20 20

Pipes 689 991 632 657 764 869 861 887 848 752 671

Total 1,508 1,984 2,022 2,229 2,110 2,445 2,774 2,924 2,743 2,527 2,430

% of GDP 3.3% 3.5% 3.2% 3.3% 3.0% 3.2% 3.4% 3.3% 2.8*% 2.4% 2.2%

Less pipes 820 993 1,390 1,572 1,346 1,576 1,912 2,037 1,894 1,775 1,760

% of GDP 1.8% 1.8% 2.2% 2.4% 1.9% 2.1% 2.3% 2.3% 1.9% 1.7% 1.6%

Source: Gazprombank estimates

* declining investments to GDP ratio after 2018 is attributable to completion of large-scale infrastructural pipelines, although we do not exclude the likelihood of emergence of new projects

Other large-scale projects follow the rollout of Olympic facilities in Sochi, but will

there be enough resources? We expect infrastructure investments to decrease by 5%

to RUB 2.1 trln this year compared to 2013 after the completion of the Olympic facilities,

due to sluggish economic growth and a decline in budget spending. The main reason for

the decline is a drop in regional road fund revenues (-24% YoY) due to deterioration of

economic conditions in the regions and higher budget deficits. Investments in transport

infrastructure could once again increase in subsequent years. The fact is that in the

wake of Olympic construction, there are a large number of projects which aim to build

toll highways and expand railroad infrastructure; the Moscow government is pouring

massive funds into expansion of the subway and major thoroughfares, and preparations

are being made to host the World Footfall Championship in 2018. Taking into account all