Embed Size (px)

Citation preview

ro COPY Board of Governors of the Federal Reserve System

rRV-6 OMB Number 7100-ltgt2Q7 Approval expore1 December 31 2015 Pago 1012

Annual Report of Holding Companies-FR Y-6

Report at the close of business as of the end of fiscal year

This Report is required by law Section 5(c)(1 )(A) of the Bank Holding Company Act (12 USC sect 1844 (c)(1 )(A)) Section 8(a) of the International Banking Act (12 USC sect 3106(a)) Sections 11(a)(1) 25 and 25A of the Feltleral Reserve Act (12 USC sectsect 248(a)(1 602 and 611a) Section 211 13(c) of Regulation K (12 CFR sect 211 13(c)) and Section 2255(b) of Regulation Y (12 CFR sect 2255(b)) and section 10(c)(2)(H) of the Home Owners Loan Act Return to the appropriate Federal Reserve Bank the original and the number of copies specified

NOTEmiddot The Annual Reporl of Holding Companies must be signed by one director of the top-tier holding company This individual should also be a senior official of the top-tier holding company In the event that the top-tier holding company does not have an individual who is a senior official and is also a director the chairshyman of the board must sign the report

I DUANE G DEBS

Name of the Holding Company Director and Official

PRESIDENT

11tle of the Holding Company Director and Ofliclal

attest that the Annual Report of Holding Companies (including the supporting attachments) for this report date has been preshypared in conformance with the instructions issued by the Federal Reserve System and are true and correct to the best of my knowledge and belief

With respect to Information regarding individuals contained in this report the Reporter certrfies that ii has the authority to provide this information to tfle Federal Reserve The Reporter also cerlifies that 1t has the aulhorlty on behalf of each individual to consent or object to public release of information regarding hat individual The Federal Reserve may assume in the absence of a request for confidential treatment submftted in accordance with the Boards bullRules Regarding Availability of Informationbull 12 CFR Pait 261 thal the Reporler anfi individual consent to public release of all details In the report concerning that Individual

Jgt (lt )2 4_ ____ _

SlgnalurlI of Holdlng ComJ)ltlny Director and Official

Oatofttnlo For holding companies m21 registered with lhe SEC-Indicate status of Annual Report to Shareholders 0 ls included with the FR Y-6 report 181 will be sent under separate cover

0 is nol p repared

For Federal Reserve Bank Use Only

RSSDID PiJU CI

This report form Is to be flied by all top-tier bank holding compashynies and top-tier savings and loan holding companies organized under US law and by any foreign banking organization that does not meet the requirements or and is not treated as a qualifyshying foreign banking organization under Section 21123 of Regulation K (12 CFR sect 21123) (See page one of the general Instructions for more detail of who must file ) The Federal Reserve may not conduct or sponsor and an organization (or a person) is not required to respond to an information collection unless it displays a currently valid OMB control number

Dato of Report (top-tier holding companys fiscal year-end)

December 31 2014 Month I Day I Year

NIA

Repor1ers Legal Entity ldontifior (LEI) (20-Character LEI Code)

Reporters Name Street and Mailing Address WEST SUBURBAN BANCORP INC

Legal TitJe of Holding Company

711 SOUTH MEYERS ROAD

(Malling Address of the Holding Company) Street IP O BOll LOMBARD IL 60148 -------Ci1y State Zip Codo

Physical Location If different from mai ling address)

Person to whom questions about this report should be directed DUANE G DEBS PRESIDENT

--Name TiUe

630 652-2801 Vea Code I Phone Number I ExtelISlort

hea Code I FAX Numller d debswestsu burbanba_n_k_c_D_m ___ ______ _

E-mail Aodress wwwwestsuburbanbankcom Address (URL) for lhe Holding Companys web page

Does the reporter request confidontlal troatment for any portion of this submission

0 Yes Please identify lhe report items to which this request applies

No

O In accordance with the mslfuctions on pages GEN-2 and 3 a letter justifying the request is being provided

O The information for which conftdentlal treatment Is sought is being submitted separately labeled Confidential

Pubic reporting burden 10lt lh5 information collecIJon Is esmaled 10 vary from 1 3 lo 101 hours por response with an a11t1rago of 575 hours per response lndudng dma lo galher and mobullnlain dola In tho roqulrod torm and 10 review tnuucuons and complota the mformoon oolleC1 on Sond commcn1s mgonrng this burden osUmato or eny Olhor ospcc1 ol tllgtS conccUon ol Information lnclud ng suggestons for roduc111g thbullbull burden to Sccrc1aty Boord of Govomors of 1hO Federal Reserve System 20th and C Streets NW Washington OC 2055 f and IO lhe Of11co o1 Management and Budget Paperworllt Reoucuon ProJoct (7100-0297) Washington DC 20503

1012014

Profile and Business Review

West Suburban Bancorp Inc (West Suburban ) is the parent bank holding company of West Suburban Bank Lombard I l linois (the Bank and together with West Suburban the Company) The Company had total assets at December 31 2014 of approximately $21 billion and maintained 37 full-service branches seven l imited-service branches and four departments providing insurance financial and other services for the convenience of the customers of the Bank throughout DuPage Kane Kendall and Will Counties in Illinois The Bank is one of the largest independent banks headquartered in DuPage County Illinois and focuses on providing retail and commercial banking products and services in its market area The Company had 490 full-time equivalent employees at December 31 2014

West Suburban Bancorp Inc

Net incon1e Per share data

Earnings per share Book value

Net loans Total assets Total deposits

Financial Highlights

$

Years Ended December 31

(Dollars in thousands except per share data) 2014 2013

13729 $ 7503

3223 1758

44830 39886

1070 109 1028036

2109404 2041212

1902871 1854322

Table of Contents

Profile and Business Review 1 Special Note Concerning forward-Looking Statements I

Letter to Our Shareholders Customers and Friends 2

Financial Statements

Independent Auditors Report 3

Consolidated Financial Statements 4

Notes to Consolidated Financial Statements 9 Selected Financial Data 34

Average Balance Sheets Net Interest Income and Average Rates and Yields on a Tax Equivalent Basis 35

Boards of Directors and Officers 36

Addresses of West Suburban Facilities 39

Map of Facilities 41

Shareholder Information 42

Special Note Concerning Forward-Looking Statements

1his document and future oral and ivritten statements of the (ompany and its tnanagement may contain fonvardshylooking statements with respect to the financial condition results of operations plans objectives future performance and business of the Company Fonvard-looking statements which may be based upon beliejI expectations and assumptions of the Company s management and vn itformation currently available to management are generally identifiable by the use of wordy such as believe expect anticipate plan intend estimate may vi would could should or other similar expressions A number of factors many of which are beyond the ability of the Company to control or predict can cause actual results to differ materially from those in its fonvard-looking statements Additionally all statements in this document including

fiuward-looking statements speak only as of the date they are made and the (ompany undertakes no obligalion to update any statement in light of new information or fature events

To Our Shareholders Customers and Friends

The economic recovery in our 1narkets continues to move in the right direction As an example national unemployment rates have dropped significantly to 56dego as of December 31 2014 from 67oo as of December 31 2013 and in Illinois unemployment rates have decreased to 62dego as of December 31 2014 from 89oo as of December 31 2013

As the economy improves we continue to make significant progress within our organization Our non-performing assets have continued to decrease as other real estate owned decreased to $7 4 million as of December 31 20 I 4 from $205 mill ion as of December 31 2013 and nonaccrual loans decreased $27 million to $224 million as of December 31 2014 from $251 million as of December 31 2013 These reductions allowed us to increase our interest-earning assets while decreasing our expenses associated with problem loans and foreclosed properties

The improving economy has also resulted in the stabilization and improvement in appraisals that we obtain with regard to real estate that serves as collateral for many of our largest loans This has allowed us to record a recovery of provision for loan losses of $50 million based on our comprehensive methodology for estimating the allowance for loan losses The recovery of provision contributed to the significant increase in net income to $13 7 million tOr the year ended Decen1ber 31 2014 from $75 million for the year ended December 31 2013

Although v-re did not declare a dividend during 2014 during 2015 our board of directors will continue to evaluate the adequacy of our capital position and our non-pcrfonning asset levels and make responsible dividend decisions after appropriate consultation with our regulators Please be assured that it is our highest priority to protect your invcstn1cnt by continuing to evaluate refine and improve all areas of our business and to react appropriately to changes in the local and national econo1nic conditions as well as to changes in banking regulations

We would like to express our appreciation and sincere gratitude to everyone for the support that has allowed us to become and reinain one of the largest independent banks headquartered in DuPage County You have enabled us to exceed $2 billion in assets and expand to 37 branches within the four counties that we serve Ve could not have achieved our success without the support of our shareholders customers comn1unities friends and en1ployecs We are mindful that providing high quality responsive service distinguishes us from our competition and we will take great care to ensure that we do not sacrifice this important advantage We look forward to celebrating many new milestones in the years to come and as always we welcome your comments and suggestions

Thank you for your continued support

Sincerely

Kevin J Acker Chairman of the Board and Chief Executive Officer

2

Duane G Debs President and Chief Financial Officer

Crowe Horwath Crowe Horwath LLP independent Member Crowe Horwath lltiternat1onal

Independent Auditors Report

Board of Directors and Shareholders

West Suburban Bancorp Inc Lon1bard Illinois

Report on the Financial Statements

Ve have audited the accornpanying consolidated financial statements of Vest Suburban Bancorp Inc which comprise the consolidated balance sheets as of Dcccnihcr 31 2014 and 2013 and the related consolidated statcn1ents of income co1nprehensive incrnne changes in shareholders equity and cash flows for the years then ended and the related notes to the consolidated financial statements

llanagcmcnts Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance Vith mcounting principles generally accepted in the United States of America this includes the design implcn1cntation and maintenance of inten1al control relevant to the preparation and fair presentation of consolidated financial statcnients that arc free fro1n 1naterial n1isstatemcnt whether due to fraud or error

Auditors Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits Ve conducted our audits in accordance vith auditing standards generally accepted in the United States or An1erica Those standards require that Ve plan and perfom1 the audit to obtain reasonable assurance about whether the consolidated financial statements arc free fro1n material misstatement

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements The procedures selected depend on the auditors judgment including the assess1nent of the risks of material 1nisstatemcnt of the consolidated financial statements vhcthcr due to fraud or error In nlaking those risk asscss1ncnts the auditor considers internal control relevant to the entitys preparation and fair presentation of the consolidated financial statcn1cnts in order to design audit procedures that are appropriate in the circumstances but not for expressing an opinion on the effectiveness of the entitys internal control Accordingly we express no such opinion An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates 1nade by rnanagcment as Veil as evaluating the overall presentation of the consolidated financial statements

Ve believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion

()rinion

In our opinion the consolidated financial statcinents referred to above present fairly in a material respects the financial position of West Suburban Bancorp Inc as of Dece1nber 3 I 2014 and 2013 and the results of its operations and its cash Jlovs

for the years then ended in accordance Vilh accounting principles generally accepted in the United States of America

Oak Brook Illinois March 20 2015

3

Crowe Horwath LLP

Assets

Cash and due fron1 banks Federal funds sold

WEST SUBURBAN BANCORP INC CONSOLIDATED BALANCE SHEETS

DECEMBER 31 2014 AND 2013 (Dollars in thousands)

$

Total cash and cash equivalents Securities

Available for sale (amortized cost of $602 7 I 5 in 20 I 4 and $643739 in 20 1 3 )

Held to maturity (fair value o f $2 15 1 98 i n 20 14 and $ 1 89283 in 20 13)

Federal I lame Loan Bank stock Total securities

Loans less allowance for loan losses of$25382 in 2014 and $30552 in 20 1 3

Bank-owned life insurance Pre1nises and equipment net Other real estate owned net A ccrued interest and other assets

2014

83206 25206

1084 1 2

602744

208369 6076

8 1 7 1 89

1 070 1 09 34366 45574

7409 26345

Total assets $ 2 1 09404

Liabilities and shareholders equity

Deposits Dcmand-noninterest-bearing Interest-bearing

Total deposits Prepaid solutions cards Accrued interest and other liabilities

Total liabilities

Shareholders equity Con1mon stock no par value 1 5 000000 shares authorized

426040 shares issued and outstanding at December 3 1 20 I 4 and December 3 1 20 I 3

Surplus Retained earnings Accumulated other comprehensive loss

lotal shareholders equity

Total liabilities and shareholders equity

$ 203373 1 699498 1 90287 1

3 1 86 1 2355

1 9 1 84 1 2

3406 35224

1 52980 (6 1 8)

1 90992 $ 2 1 09404

)ee accompanying notes to consolidated financial statements

4

20 1 3

$ 54382 200

54582

630603

1 8403 1 5 1 3 8

8 1 9772

1 028036 33823 466 1 5 20458 37926

$ 204 1 2 1 2

$ 1 74471 1 67985 1 1 854322

3456 1 3504

1 87 1 282

3406 35224

1 3925 1 (7 95 1 )

1 69930 $ 20412 1 2

WEST SUBURBAN BANCORP INC

CONSOLIDATED STATEMENTS OF INCOME

YEARS ENDED DECEMBER 3I 2014 AND 2013 (Dollars in thousands)

2014 2013 Interest income

Loans including fees $ 47583 $ 46396 Securities

Taxable 14481 12009 Exempt from federal income tax 2047 2318

Federal funds sold Total interest income 64112 60724

Interest expense

[)eposits 5868 7381 Other 11 l

Total interest expense 5879 7382 Net interest income 58233 53342 (Recovery of) provision for loan losses (4994) 4985 Net interest income after provision for loan losses 63227 48357

Nonintcrest income

Service fees on deposit accounts 3392 3677 Debit card fees 2597 2565 Bank-owned life insurance 543 560 Net realized gains on securities transactions 166 1176 Other 3049 3958

Total nonintcrest income 9747 11936

Noninterest expense

Salaries and employee benefits 24893 23940 Occupancy 6114 5247

Furniture and equipment 5295 5078 Other real estate owned expense 2945 4089

FDIC assessments 2780 2762

Loan administration 1 178 1727 Professional fees 1152 977 Advertising and promotion 1133 1005 Other 5721 5042

Total noninterest expense 5121 l 49867

Income before income taxes 21763 10426

Income tax expense 8034 2923 Net income $ 13729 $ 7503

5ee accompanying notes to consolidated financial statements

5

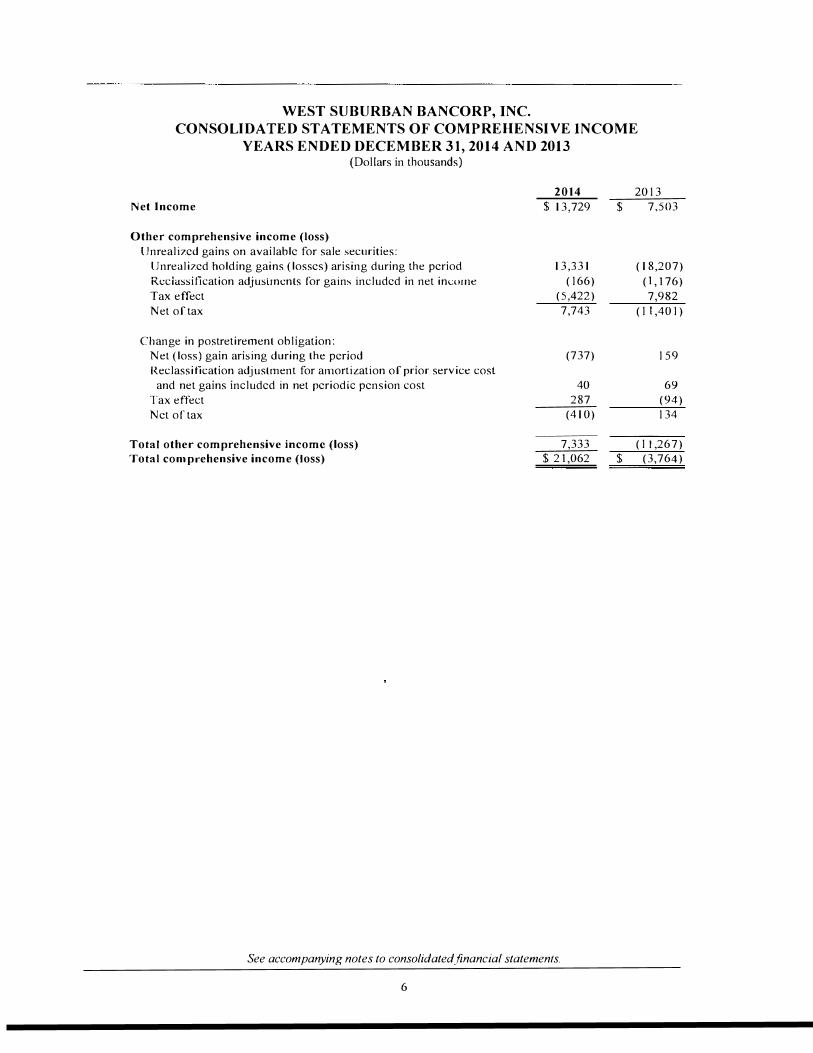

WEST SUBURBAN BANCORP INC

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

YEARS ENDED DECEMBER 31 2014 AND 2013 (Dollars in thousands)

Net Income

Other comprehensive income (loss) Unrealized gains on available for sale securities

Unrealized holding gains (losses) arising during the period

RLciassification adjustrncnts for gains included in net incu111e

Tax effect

Net of tax

Change in postretirement obligation

Net (loss) gain arising during the period

Reclassification adjuslnent for an1ortization of prior service cost

and net gains included in net periodic pension cost

Tax effect

Net of tax

Total other comprehensive income (loss) crotal con1prehensive income (loss)

2014

$ 13729

13331

( 166) (5422)

7743

(737)

40 287

(410)

7333 $ 21062

See accompanying notes to consolidated financial statemenls

6

2013

$ 7503

( 18207)

(1176)

7982

(11401)

159

69 (94) 134

( 11267)

$ (3764)

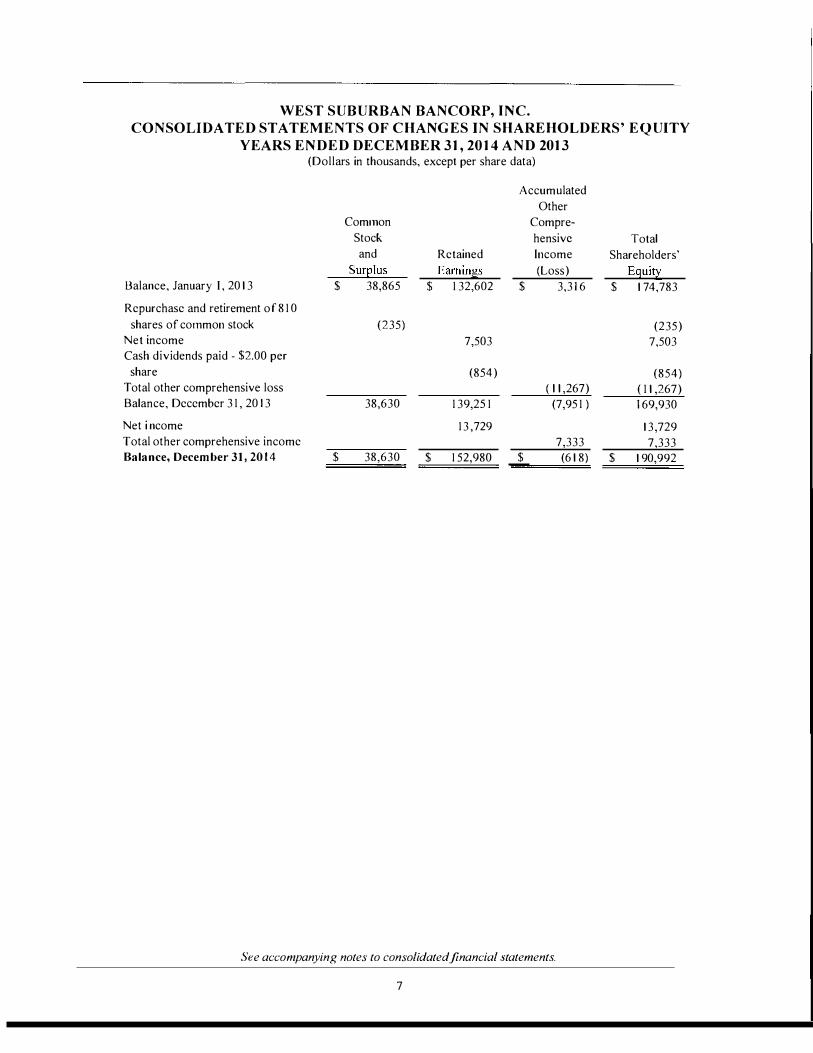

WEST SUBURBAN BANCORP INC CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS EQUITY

YEARS ENDED DECEMBER 31 2014 AND 2013 (Dollars in thousands except per share data)

Accumulated Other

Com1non Com pre-Stock hensivc Total and Retained Income Shareholders

SurElus EarninBs (Loss) Eguit Balance January I 20 1 3 $ 38865 $ 1 32602 $ 33 1 6 $ 1 74783

Repurchase and retirement of 8 1 0 shares of co1nmon stock (235) (235)

Net income 7503 7503 Cash dividends paid - $200 per

share (854) (854) Total other comprehensive loss ( 1 1 267) ( 1 1 267) Balance December 3 1 20 I 3 38630 1 3925 1 (795 1 ) 169930

Net i ncome 1 3 729 1 3729 Total other comprehensive income 7333 7333 Balance December 31 2014 $ 38630 $ 1 52980 $ (6 1 8) $ 1 90992

See accompanying notes to consolidatedfinancial statements

7

WEST SUBURBAN BANCORP INC

CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED DECEMBER 31 2014 AND 2013 (Dollars in thousands)

2014 2013 Cash flows from operating activities

Net income $ 13729 $ 7503 Adjustments to reconcile net inco1ne to net cash provided by

operating activities Depreciation 3543 3391 (Recovery of) provision for loan losses (4994) 4985 Net premium amortization of securities 6417 7550 Net realized gain on securities transactions ( 166) ( I 176) Earnings on bank-owned life insurance (543) (560) Net gain on sales of loans originated for sale (71) (248) Net loss on sales of other real estate owned 369 25 Write down of other real estate owned 2059 1641 Decrease in accrued interest and other assets 6445 747 (Decrease) increase in accrued interest and other liabilities ( 1845) 1177

Net cash provided by operating activities 24943 25035 Cash flows from investing activities

Securities available for sale Sales 83686 62189 Maturities cal Is and redemptions 127665 144759 Purchases ( 176703) (204770)

Securities held to maturity and FHLB stock Maturities calls and redemptions 34050 43893 Purchases (59201) (56773)

Net increase in loans (37888) (69711) Purchases of premises and equipment (2502) (5 114) Sales of other real estate owned 11501 13191

Net cash used in investing activities ( 19392) (72336) Cash flows from financing activities

Net increase in deposits 48549 30823 Repurchase and retirement of common stock (235) Net decrease in prepaid solutions cards (270) (4034) Dividends paid (854)

Net cash provided by financing activities 48279 25700 Net increase (decrease) in cash and cash equivalents 53830 (21601) Beginning cash and cash equivalents 54582 76 183 Ending cash and cash equivalents $ 108412 $ 54582

Supplemental disclosures

Cash paid for interest $ 6095 $ 8566

Cash paid for income taxes 3067 2443

Other real estate acquired through or instead of loan foreclosure 880 12917

Loans originated from the sale of other real estate owned 1658 359

See accompanying notes to consolidated financial statements

8

WEST SUBURBAN BANCORP INC NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in thousands)

Note I - Nature of Business and Summary of Significant Accounting Policies

Vest Suburban Bancorp Inc (West Suburban) through the branch network of its subsidiary West Suburban Bank (the Bank and together with West Suburban the Company) operates 37 full-service branches seven lin1itedshyscrvice branches and four departments providing insurance financial and other services for the convenience of the customers of the Bank throughout DuPage Kane Kendall and Will Counties in Illinois Customers in these areas are the primary consumers of the Companys loan and deposit products and services Although borrower cash flov is expected to be the primary source of repayment the Companys loans arc generally secured by various forms of collateral or security including real estate business assets consumer goods personal guarantees and other iten1s

Principles of Consolidation The consolidated financial statements include the accounts of West Suburban and the Bank Significant intercompany accounts and transactions have been eliminated

Subsequent Events The Company has evaluated subsequent events tOr recognition and disclosure through March 20 2015 which is the date the financial statements were available to be issued

Use of ltttimates To prepare financial statements in conformity with accounting principles generally accepted in the United States of America management makes estin1ates and assun1ptions which are subject to change based on available information These estimates and assumptions affect the an1ounts reported in the financial statements and the disclosures provided and actual results could differ

bull 5ecurities Debt securities are classified into two categories available for sale and held to maturity Available for sale securities are carried at fair value with net unrealized gains and losses (net of deferred tax) reported in accumulated other comprehensive income as a separate component of shareholders equity Held to maturity securities are carried at amortized cost as the Company has both the ability and positive intent to hold them to maturity Interest income includes amortization of purchase premium or discount Premiums and discounts on securities are amortized on the level-yield 1nelhod without anticipating prepayments except for mortgage-backed securities where prepayments are anticipated Gains and losses on sales are recorded on the trade date and determined using the specific identification method The Company does not engage in trading activities

Management evaluates securities for other-than-temporary impairment (OJTI) on at least a quarterly basis and more frequently when economic or market conditions warrant such an evaluation For securities in an unrealized loss position management considers the extent and duration of the unrealized loss and the financial condition and near-term prospects of the issuer Management also assesses whether it intends to sell or it is more likely than not that it will be required to sell a security in an unrealized loss position before recovery of its amortized cost basis If either of the criteria regarding intent or requirement to sell is met the entire difference between amortized cost and fair value is recognized as impairment through earnings For debt securities that do not meet the aforementioned criteria the amount of impairment is split into two cotnponents as follows ( I ) OTTI related to credit loss which must be recognized in the income statement and (2) OTT related to other factors which is recognized in other comprehensive income The credit loss is defined as the difference between the present value of the cash flows expected to be collected and the amortized cost basis

Federal Home Loan Bank (FHLB) Stock The B ank is a member of the Ff-ILB system Members are required to own a certain amount of stock based on the level of borrowings and other factors and may invest in additional amounts Fl-ILB stock is carried at cost classified as a restricted security and periodically evaluated for impainnent based on ultimate recovery of par value Both cash and stock dividends are reported as income

9

Loans Loans that management has the intent and ability to hold for the foreseeable future or until maturity or payoff are reported at the principal balance outstanding net of unearned interest deferred loan fees and costs and an allowance for loan losses Interest income is accrued on the unpaid balance of the Companys loans and includes amortization of net deferred loan fees and costs over the loan tenn Loan origination fees net of certain direct origination costs are deferred and recognized in interest income using the level-yield method without anticipating prepayments

Accrual of interest is generally discontinued on loans 90 days past due or on an earlier date if management believes after considering economic and business conditions and collection efforts that the borrowers financial condition is such that collection of principal or interest is doubtful In some circu1nstances a loan more than 90 days past due may continue to accrue interest if it is fully secured and in the process or collection When a loan is classified as nonaccrual interest previously accrued but not collected is charged back to interest inco1ne Vhen payments are received on nonaccrual loans they are first applied to principal then to interest income and finally to expenses incurred for collection

Allowanceor Loan Losses The allowance ror loan losses is a valuation allowance for probable incurred credit losses in the loan portfolio fhe allowance is increased by a provision for loan losses charged to earnings_ Loan losses are charged against the allowance when management believes the uncollectability of a loan has been established Subsequent recoveries if any are credited to the allowance The allowance consists of specific and general con1ponents The specific component relates to specific loans that are individually classified as impaired The allowance for loan losses is evaluated 1nonthly based on 1nanagen1ents periodic review of loan collectability in light of historical loan loss experience the nature and volume of the loan portfolio inrormation about specific borrower situations and estimated collateral values and prevailing economic conditions Although allocations or the allowance may be made fOr specific loans the entire allowance is available for any loan that in manage1ncnts judgment should be chargedshyoff Manage1nents evaluation of loan collectability is inherently subjective as it requires estimates that arc subject to significant revision as more infOrmation becomes available or as relevant circu1nstances change

The Co1npany evaluates commercial commercial real estate construction and development and residential real estate (mortgage and home equity) loans monthly for impairment A loan is considered impaired when based on current infOrmation and events ruI payn1ent under the loan lerms is not expected Loans for which the tem1s have been modified and for which the borrower is experiencing financial difficulties are considered troubled debt restructurings (TDRs) and classified as impaired Impairn1ent is nieasurcd based on the present value of expected future cash flows discounted at the loans effective interest rate or the poundlir value of the loans collateral if repayment of the loan is collateral dependent A valuation allowance is maintained for the amount of impairment Generally loans 90 days or more past due and loans classified as nonaccrual status are considered for impairment Impairment is considered on an entire category basis fOr smaller-balance loans of si1nilar nature such as residential real estate and consumer loans and on an individual basis for other loans Jn general consumer and credit card loans are charged-off no later than 120 days after a consumer or credit card loan becomes past due

The general component covers pools of other loans not classified as impaired and is based on historical loss experience adjusted for current factors The historical loss experience is determined by portfolio segment and is based on a rolling three year net charge-off history This actual loss experience is supple1nented with other economic factors based on the risks present for each portfolio segment These factors include consideration of the following levels and trends in past dues trends in charge-offs and recoveries trends in volume and teffils of loans effects of collateral deterioration other changes in lending policies procedures and practices experience ability and depth of lending management and other relevant staff national and local economic trends trends in i1npaired loans including impaired loans without specific allowance for loan losses and a factor representing the potential charge-off of specific reserves The following portfolio segments have been identified commercial commercial real estate construction and development residential real estate (mortgage and home equity) and consumer loans

Commercial loans are made based primarily on the identified cash flow of the borrower and secondarily on the underlying collateral provided by the borrower Most often this collateral is accounts receivable inventory equipment or real estate Repayment is prin1arily dependent upon the borrowers ability to service the debt based upon the cash flows generated from the underlying business Secondary support involves liquidation of the pledged collateral and enforcement of a personal guarantee if a guarantee is obtained

10

Commercial real estate lending typically involves higher loan principal a1nounts and the repayment of the loans generally is dependent in large part on sufficient income from the properties securing the loans to cover operating expenses and debt service Economic events or governmental regulations outside of the control of the borrower or the Company may negatively impact the future cash flow and market values of the affected properties

Construction and development lending involves additional risks because funds are advanced based upon values associated with the completed project which are uncertain Because of the uncertainties inherent in evaluating the construction cost estimates that the Company receives from its customers and other third parties as well as the market value of the completed project and the effects of governmental regulation of real property it is relatively difficult to evaluate accurately the total funds required to complete a project and the related loan-to-value ratio As a result construction and development loans often involve the disbursement of substantial funds with repayment dependent i n part on the success of the ultimate project and the ability of the borrower to sell or lease the property rather than the ability of the borrower or guarantor to repay principal and interest

Residential real estate (mortgage and home equity) lending consists primarily of loans secured by first or second mortgages on primary residences The loans are collateralized by owner-occupied properties located in the Companys market area Mortgage title insurance is normally required on first nlortgages and second mortgages $ I 00000 and greater Hazard insurance is normally required on first and second mortgages

The Companys consumer loans are primarily made up of credit card lines and installment loans Credit card lines present inherent risk due to the unsecured nature of the product The installment loans represent a relatively small portion of the Companys loan portfolio and are primarily secured by automobiles

Bank-Owned Lift Insurance (BOLlJ The Company has purchased life insurance policies on certain officers and directors BOLI is recorded at the a1nount that can be realized under the insurance contract at the balance sheet date which is the cash surrender value adjusted for other charges or other a1nounts due that are probable at settlement

Premises and tquipmenl Land is carried at cost Premises and equipment are stated at cost less accumulated depreciation Depreciation i s generally computed o n the straight-line method over the estimated useful lives o f the assets Leasehold iinprovements are amortized over the shorter of the useful life or lease term

Other Real Estate Owned Other real estate owned includes properties acquired in partial or total settlement of problen1 loans Assets acquired through or instead of loan foreclosure are initially recorded at fai r value less anticipated costs to sell when acquired establishing a new basis If fair value declines subsequent to acquisition a valuation allowance is recorded through expense Operating costs after acquisition are expensed as incurred

Loan Commitments and Related Financial Instruments Financial instruments include off-balance sheet credit instruments such as commitments to nlake loans and commercial letters of credit issued to meet customer financing needs The face amount for these items represents the exposure to loss before considering custon1er collateral or ability to repay Such financial instruments are recorded when they are issued

Income Taxes Income tax expense is the total of the current year income tax due or refundable and the change i n deferred tax assets and l iabilities Deferred tax assets and liabilities are the expected future tax consequences of temporary differences between the carrying amounts and the tax basis of assets and liabilities computed using enacted tax rates A valuation allowance if needed reduces deferred tax assets to the amount expected to be realized

A tax position is recognized as a benefit only if it is more likely than not that the tax position would be sustained in a tax examination with a tax examination being presumed to occur The amount recognized is the largest amount of tax benefit that has a greater than 50oo likelihood of being realized on examination For tax positions not meeting the tnore likely than not test no tax benefit is recorded

1 1

The Company recognizes interest andor penalties related to inco1ne tax matters in income tax expense

40(k) Profit Sharing Plan ESOP and Other Retirement Plans

The Bank maintains the West Suburban Bank 401 (k) Profit Sharing Plan to assist the Company in recruiting and retaining its personnel Participation in the plan is subject to certain age and service requirements Although the Company currently intends to match a percentage of the contributions that each employee voluntarily makes to the plan all contributions by the Company are discretionary and subject to review by the Board of Directors from time to time The plan is also intended to enable long time employees of the Company that also participate in the ESOP to diversify their retirement savings

The Bank also maintains an ESOP which is a noncontributory tax qualified retire1nent plan that covers employees who have satisfied specific service requirements Subject to review by the Board of Directors the Bank may nlake contributions to the ES()P for the benefit of the participants from time to time l)ividends declared on common stock owned by the ESOP are charged against retained earnings Dividends paid on ESOP shares are passed through to participants who have the option to receive cash or reinvest in the plan Earned and allocated ESOP shares are voted by the respective participants

The Company has a postretirement healthcare plan covering certain executives Postretircment benefit costs arc net of service and interest costs and amortization of gains and losses not immediately recognized

The Con1pany has deferred compensation arrangements with certain former and current executive officers and directors Deferred compensation expense allocates the benefits over years of service

Cash Hows

For purposes of reporting cash flows cash and cash equivalents include cash and due from banks and federal funds sold Generally federal funds are sold for one-day periods Net cash flows are reported for customer loan deposit federal funds purchased and prepaid solutions card transactions

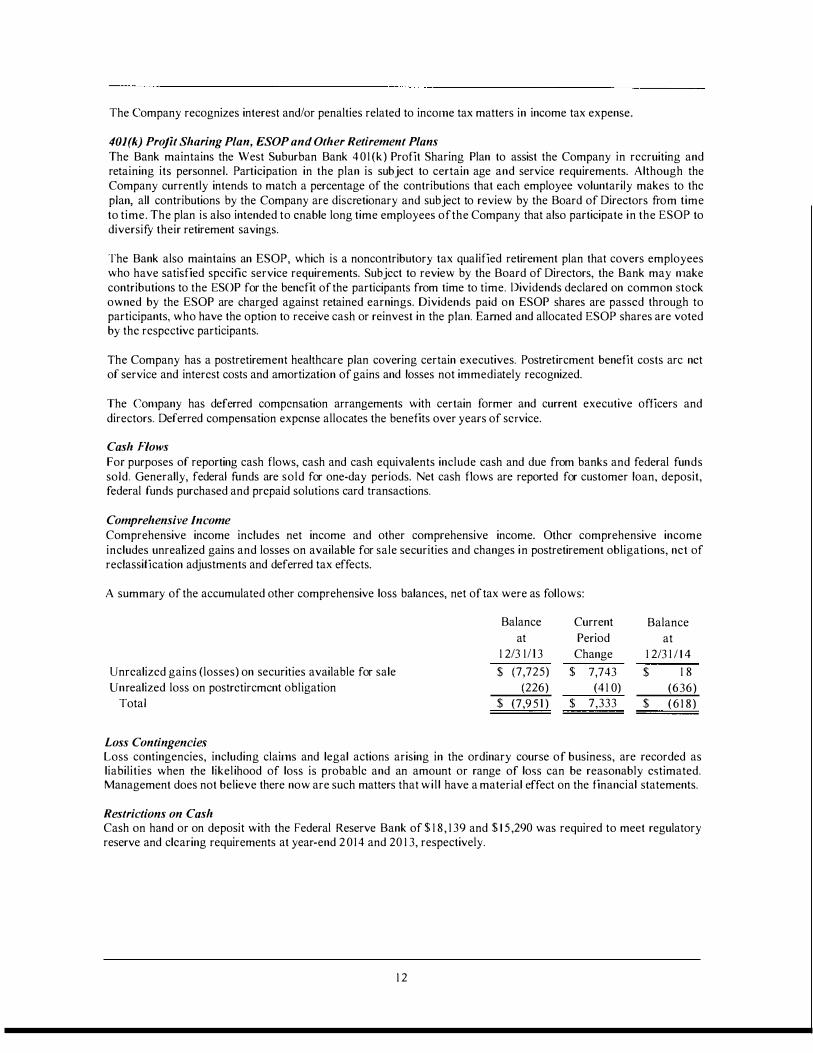

Comprehensive Income Comprehensive income includes net income and other comprehensive income Other comprehensive income includes unrealized gains and losses on available for sale securities and changes in postretirement obligations net of reclassification adjustments and deferred tax effects

A summary of the accumulated other comprehensive loss balances net of tax were as follows

Unrealized gains (losses) on securities available for sale Unrealized loss on postretircmcnt obligation

Total

Loss Contingencies

Balance at

1 213 1 1 13

$ (7725) (226)

$ (79 5 1 )

Current Period

Change

$ 7743 (4 1 0)

$ 7333

Balance at

1 23 1 1 4

$ 1 8 (636)

$ (61 8)

Loss contingencies including clai1ns and legal actions arising in the ordinary course of business are recorded as liabilities when the likelihood of loss is probable and an amount or range of loss can be reasonably estimated Management does not believe there now are such matters that will have a material effect on the financial statements

Restrictions on Cash Cash on hand or on deposit with the Federal Reserve Bank of $ 1 8 1 39 and $ 1 5290 was required to meet regulatory reserve and clearing requirements at year-end 2014 and 20 1 3 respectively

1 2

Dividend Restrictions Banking regulations require maintaining certain capital levels and may li1nit the dividends paid by the Bank to West Suburban or by West Suburban to shareholders (See Note 1 2 in the Consolidated Financial Statements for more specific disclosure)

Fair Value of Financial Instruments Fair value of financial instruments are estimated using relevant market information and other assumptions (Sec Note I 0 in the Consolidated Financial Statements for more specific disclosure) Fair value estimates involve uncertainties and matters of significant judgment regarding interest rates credit risk prepayments and other factors especially i n the absence of broad markets for particular items Changes in assumptions or in market conditions could significantly affect the estimates

Reclassifications Certain reclassifications have been made in prior years financial staten1ents to conforn1 to the current years presentation

Note 2 - Securities

The amortized cost unrealized gains and losses and fai r value of securities available for sale arc as follows at Dece1nber 3 1

US government sponsored enterprises Mortgage-backed residential States and political subdivisions Corporate

Total

US government sponsored enterprises Mortgage-backed residential States and political subdivisions Corporate

Total

Amorti7cd Cost

$ 43 1 5 8 458058

8 1 350 20 149

$ 6027 1 5

An1ortized Cost

$ 70580 424522 1 20303 28334

$ 643739

Gross Unrealized

Gains $ 2

3951 494 400

$ 4847

Gross Unrealized

Gains $ 6 1

2 1 78 167 648

$ 3054

2014 Gross

Unrealized Losses

$ (461) (41 92)

( 1 65)

$ (48 1 8)

20 1 3 Gross

Unrealized losscs

$ (2242) ( 1 2007)

( 194 1 )

$ ( 1 6 1 90)

Fair Value

$ 42699 4578 1 7

8 1 679 20549

$ 602744

Fair Value

$ 68399 4 1 4693 1 1 8529 28982

$ 630603

Mortgage-backed residential securities consist of residential mortgage-backed securities issued by US government sponsored enterprises and agencies pri1narily Fannie Mae Freddie Mac and Ginnie Mae institutions which the govcrntnent has affirmed its commitment to support Corporate securities consist of investinent grade corporate bonds

1 3

The amortized cost unrecognized gains and losses and fair value of securities held to maturity are as follows at December 3 1

2014 Gross Gross

Amortized Unrecognized Unrecognized Fair Cost Gains Losses Value

US Treasuries $ 30039 $ 1 517 $ $ 3 1 556 lJ S government sponsored enterprises 20005 1 08 201 1 3 t1ortgage-backed residential 1 47 167 4679 1 5 1 846 States and political subdivisions 1 1 1 5 8 525 1 1 683

Total $ 208369 $ 6829 $ $ 2 1 5 1 98

20 1 3 Gross Gross

Amortized Unrecognized Unrecognized Fair Cost Gains Losses Value

US Treasuries $ 30027 $ 1 677 $ $ 3 1 704 US government sponsored enterprises 1 5056 432 1 5488 Mortgage-backed residential 1 27065 34 1 8 (553) 1 29930 States and political subdivisions 1 1 883 384 ( I 06) 1 2 1 6 1

Total $ 1 8403 1 $ 59 1 1 $ (659) $ 1 89283

The amortized cost and fair value of debt securities available for sale and held to nlaturity at Decen1ber 3 1 20 1 4 are shown by contractual maturity Expected maturities will differ from contractual maturities because issuers may have the right to call or prepay obligations with or without call or prepayment penalties Approximately $33970 of securities are callable in 2015 Securities not due at a single nlaturity date are shown separately

Available for Sale Held to Maturity Amortized Amortized

Due in I year or less $ Due after 1 year through 5 years Due after 5 years through I 0 years Due after 10 years Mortgage-backed residential

Total $

Sales of securities available for sale were as follows

Proceeds from sales Gross realized gains Gross realized losses

Cost Fair Value 8674 $

74377 6 1 606

458058 6027 1 5 $

2014 $ 83686

555 (389)

8688 $ 74675 6 1 564

4578 1 7 602744 $

2013 $ 62 1 89

1 364 ( 1 88)

Cost Fair Value 206 1 4 $ 2075 1 22494 23 1 3 3 1 8094 19468

147 1 67 1 5 1 846 208369 $ 2 1 5 1 98

Securities with a carrying value of approximately $87741 and $88571 at December 3 1 20 1 4 and 20 1 3 respectively were pledged to secure public deposits fiduciary activities and for other purposes required or permitted by law

At December 3 1 2014 and 20 1 3 the Company did not hold any securities of any single issuer in excess of I Ooo of the Companys shareholders equity except from US government sponsored enterprises

14

Securities with unrealized losses at year-end 20 1 4 and 20 1 3 not recognized in income are presented below by the length of time the securities have been in a continuous unrealized loss position

2014

Less than 1 2 Months 1 2 Months or More Total Fair Unrealized Fair Unrealized Fair Unrealized

Value Loss Value Loss Value Loss US governn1ent sponsored

enterprises $ 9824 $ (84) $ 32601 $ (377) $ 42425 $ ( 46 1 ) Mortgage-backed residential 24735 ( I 1 5 ) 1 73808 (4077) 1 98543 (4 1 92) States and political subdivisions 9458 (32) 1 0454 ( 1 33) 199 1 2 ( 1 65 )

Total temporarily impaired $ 440 1 7 $ (23 1 ) $ 2 1 6863 $ (4587) $ 260880 $ (48 1 8)

20 1 3 Less than 1 2 Months 1 2 Months or More Total

Fair Unrealized Fair Unrealized Fair Unrealized Value Loss Value Loss Value Loss

US governn1enl sponsored enterprises $ 5 1 282 $ ( 1 690) $ 1 4564 $ (552) $ 65846 $ (2242)

Mortgage-backed residential 299264 ( I 0428) 46 1 4 1 (2 1 32) 345405 ( 1 2560) States and political subdivisions 80 1 68 (2045) 1 3 6 1 (2) 8 1 529 (2047)

Total temporarily impaired $ 4307 1 4 $ ( 1 4 1 63) $ 62066 $ (2686) $ 492780 $ ( 1 6849)

The unrealized losses at December 3 1 20 1 4 were in US govern1nent sponsored enterprise securities mortgageshybacked residential and states and political subdivisions Because the decline in fair value on the debt securities is attributable to changes in interest rates and illiquidity and not credit quality and because the Company does not have the intent to sell these securities and management believes it is not 1norc likely than not that the Co1npany will be required to sell the securities before their anticipated recovery the Company docs not consider these securities to be other-than-temporarily impaired at December 3 1 20 1 4

1 5

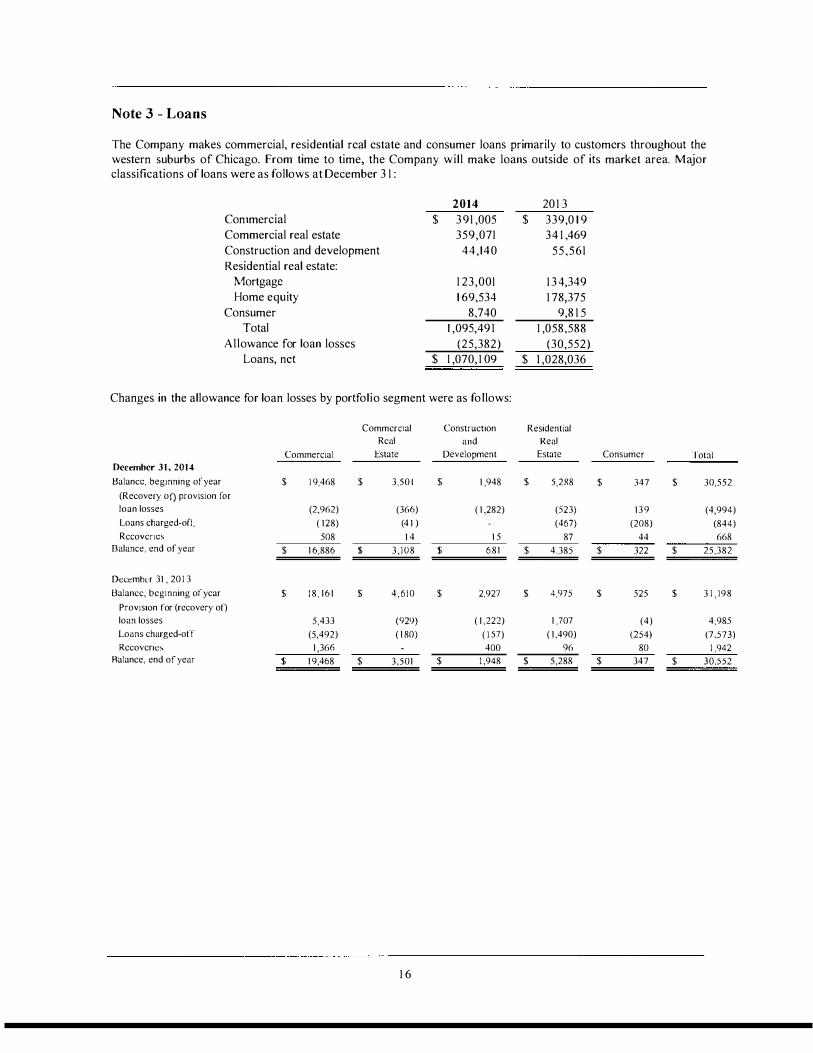

Note 3 - Loans

The Company makes commercial residential real estate and consumer loans primarily to customers throughout the western suburbs of Chicago From time to time the Company will make loans outside of its market area Major classifications of loans were as follows at December 3 1

2014 20 1 3 Con1mercial $ 391 005 $ 3390 1 9 Commercial real estate 359071 34 1 469 Construction and development 44140 55561 Residential real estate

i1ortgagc 1 23001 1 3 4349 Home equity 1 69534 1 78375

Consumer 8740 98 1 5 Total t 09549 1 1 058588

Allowance for loan losses (25382) (30552) Loans net $ 1 070 1 09 $ 1 028036

Changes in the allowance for loan losses by portfolio segment were as follows

Commercial Construction Residential

Real and Real

Commercial Estate Development Estate Consumer Total December 31 2014 Halancc beginning of year $ 1 9468 $ 350 [ $ 1 948 $ 52B8 $ 347 $ 30552

(Recovery of) provision for

loan losses (2962) (366) ( 1 282) (523) 1 3 9 (4994)

Loans charged-off ( 1 28) (4 1 ) (467) (208) (844)

Rccovcncs 508 1 4 1 5 87 44 668 Balance end of year $ 1 6886 $ 3108 $ 6 8 1 $ 4385 $ 322 $ 25382

Decembtr 31 20 1 3

Ualancc beginning of year $ 1 8 1 6 1 $ 4610 $ 2927 $ 4975 $ 525 $ 3 1 198

Prov1s10n for (recovery of)

loan losses 5433 (929) ( 1 222) 1 707 (4) 4985

Loans charged-off (5492) ( 1 80) ( 1 57) ( 1 490) (254) (7573) Recoveries 1 366 400 96 80 1 942

Ralanee end of year $ 1 9468 $ 3501 $ l 948 $ 5288 $ 347 $ 30552

1 6

The balance of the allowance for loan losses and the recorded invest1nent (which does not include accrued interest) in loans by portfolio segment and based on impairment method were as follows

Commcrcwl Construction Residential

Real and Real

Commercial Estate Development Estate Consumer Total December 31 2014 Allowance for loan losses

attnbutabk to loans

Individually evaluated for

1mpamnent $ 5732 $ 259 $ $ 1 242 $ $ 7233

Collectively evaluated

for impairment 1 1 1 54 2849 (8J 3143 322 1 8 149 Total ending allowance

balance $ 1 6886 $ 3 0 8 $ 681 $ 4385 $ 322 $ 25382

Loans

Individually evaluated

for 1mpa1rrnent $ 2 461 $ 17775 $ 2423 $ 1 2882 $ $ 5454 l

Collect1vcy evaluated

for impairment 369544 341 296 4 1 7 1 7 279653 8740 l 040950 Total ending oan balance $ 391 005 $ 359071 $ 44140 $ 292535 $ 8740 $ 1 095491

December 3 1 20 1 3

Allowance for loan losses

attributable to loans

Individually evaluated for

impairment $ 9906 $ 370 $ $ 1 565 $ $ 1 841

Collectively evaluated

for impairment 9562 3 1 3 1 1 948 3723 347 187 l l Total ending allowance

balance $ 19468 $ 3501 $ 1 948 $ 5288 $ 347 $ 30552

Loans

Individually evaluated

ror impa1rmtnt $ 23442 $ 1 8225 $ 4702 $ 14298 $ $ 60667

Collect1vely evaluated

for impairment 3 1 5577 323244 50859 298426 98 1 5 997 92 1 Total endmg loan balance $ 3390 1 9 $ 341 469 $ 55561 $ 3 1 2724 $ 9 81 5 $ 1 058588

1 7

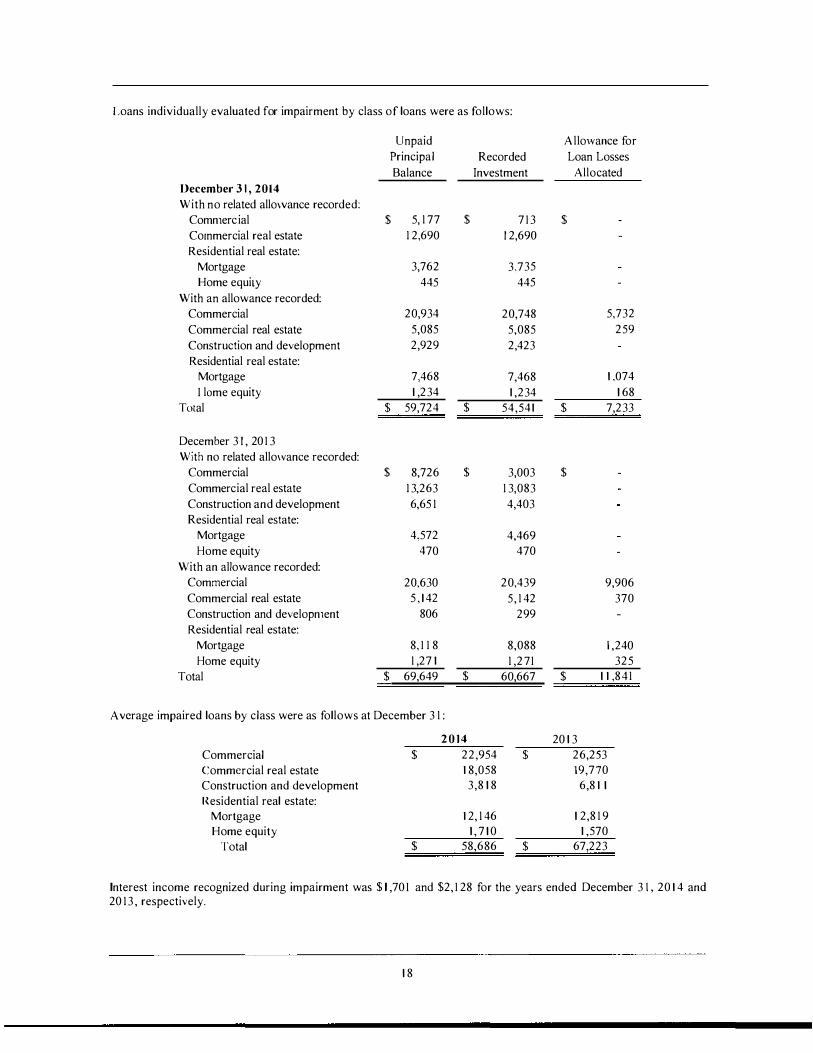

Loans individually evaluated for impairment by class of loans were as follows

Unpaid Allovrance for Principal Recorded Loan Losses Balance Investment Allocated

Igtecember 3 1 2014 With no related allovance recorded

Comn1ercial $ 5 1 77 $ 7 1 3 $ Co1nmercial real estate 1 2690 1 2690 Residential real estate

Mortgage 3762 3735 Home equity 445 445

With an allowance recorded Commercial 20934 20748 5732 Commercial real estate 5085 5085 259 Construction and development 2929 2423 Residential real estate

Mortgage 7468 7468 1 074 I lame equity 1 234 1 234 1 68

Total $ 59724 $ 54541 $ 7233

December 3 1 20 1 3 With no related allovance recorded

Commercial $ 8726 $ 3003 $ Commercial real estate 1 3263 1 3083 Construction and development 665 1 4403 Residential real estate

Mortgage 4572 4469 Home equity 470 470

With an allowance recorded Commercial 20630 20439 9906 Commercial real estate 5 1 42 5 1 42 370 Construction and developn1ent 806 299 Residential real estate

Mortgage 8 1 1 8 8088 1 240 Home equity 1 27 1 1 271 325

Total $ 69649 $ 60667 $ 1 1 841

A vcrage impaired loans by class were as follows at December 3 1

2014 20 1 3 Commercial $ 22954 $ 26253 commercial real estate 1 8058 19770 Construction and development 38 1 8 68 1 1 Residential real estate

Mortgage 1 2 1 46 1 28 1 9 Home equity 1 7 1 0 1 570

Total $ 58686 $ 67223

Interest income recognized during impairment was $ I 70 I and $2 1 28 for the years ended December 3 I 20 1 4 and 20 13 respectively

1 8

Nonperfonning loans and loans past due 90 days or more still on accrual include both smaller balance homogeneous loans that arc collectively evaluated for impainnent and individually classified impaired loans

The recorded invesunent in nonaccrual and loans past due 90 days or more still on accrual by class of loans was as follows

December 3 1 2014

Commercial Commercial real estate Construction and development Residential real estate

Mortgage Home equity

Consumer Total

December 3 1 20 13 Commercial Commercial real estate Construction and development Residential real estate

Mortgage Home equity

Consumer Total

Nonaccrual

$

$

$

$

1 7094 1 160 2423

1 3 1 4 4 1 3

4 22408

1 86 1 8 451

4702

1 269 98

25 138

Loans Past Due 90 Days or More Still on Accrual

$

$

$

$

4

4

1 1 6 6

26 1 48

Loans past due 90 days or more still on accrual are generally considered to be well-collatcralized and in the process of collection as of December 3 1 2014

1 9

rhe aging of the recorded investment in past due loans were as follows

December 3 1 2014

30 - 59 Days

Past l)uc

Commercial $ 7 1 45 Con1mercial real estate 2265 Construction and

development Residential real estate

i11J1igagc I Ionic equity

Consumer Total

December 3 I 20 1 3

8 1 7 469

$ 1 0696

Commercial $ 43 1 Commercial real estate 2728 Construction and

development Residenlial real estate

Mortgage I tome equity

Consun1er Jolal

1 858 223

2 1 $ 5261

60 - 89 Days

Past J)uc

$ 500

225 339

1 9 $ 1 083

$

948 225

$ 1 1 73

90 Days or More Past f)uc

$ 1 6732 1 1 60

2423

1 3 1 4 4 1 7

4 $ 22050

$ 1 8230 380

4702

1 385 1 04 26

$ 24827

Total Past J)ue

$ 24377 3425

2423

2356 1 225

23 $ 33829

$ 1 8661 3 1 08

4702

4 1 9 1 552

47 $ 3 1 26 1

Loans Not Past l)uc

$ 366628 355646

4 1 7 1 7

1 20645 1 68309

87 1 7 $ 1 06 1 662

$ 320358 338361

50859

1 30 1 58 1 77823

9768 $ 1 027327

lotal

$ 3 9 1 005 359071

44 1 40

1 23001 1 69534

8740 $ 1 095491

$ 3390 1 9 3 4 1 469

5556 1

1 34349 1 78375

98 1 5 $ 1 058588

During the year ended December 3 1 20 1 4 the terms of certain loans were 1nodified as TD Rs The modification of the terms of such loans included one or a combination of the following a reduction of the stated interest rate of the loan an extension of the maturity date al a stated rate of interest lower than the current market rate for new debt with si1nilar risk or a permanent reduction of the recorded investment in the loan

At f)ecember 3 1 20 1 4 the Company had $32593 of loans considered TD Rs which are considered impaired loans compared to $34499 as of December 3 1 20 1 3 As of December 3 1 20 1 4 and 20 1 3 the Company has specifically allocated allowance for loan losses of$2 104 on $ 1 5841 and $2263 on $ 1 6750 respectively of loans considered to be TD Rs The remaining TDRs did not have impaired cash flows or are considered to be collateral dependent and do not have specific allocations of the allowance due to partial charge-offs and the loans being vellshycollatcralized Management has not committed to lend additional amounts to customers with outstanding loans that are classified as TDRs

20

The following table presents loans by class modified as TD Rs during the years ended

Pre-Modification Post-Modification Outstanding Outstanding

Number of Recorded Recorded Loans Investment Investment

December 31 2014

Commercial 2 $ 558 $ 558 Commercial real estate 2 2504 2504 Residential real estate mortgage 2 3 1 3 4 1 4

Total 6 $ 3375 $ 3476

December 3 1 20 1 3 Commercial $ 1 99 $ 1 99 Commercial real estate 582 636 Residential real estate rnortgage 9 1 470 1 489

Total 1 1 $ 225 1 $ 2324

fhe loans modified as TDRs during the year increased the allowance for loan losses by $536 and $325 respectively for the years ended December 3 1 20 1 4 and 20 1 3 During 20 1 4 and 2013 modifications involving a reduction of the stated interest rate of the loan were for interest rates ranging from 30oo to 55oo and periods ranging from 1 2 months to 30 years Modifications involving an extension of the maturity date were for periods ranging from 1 2 to 22 months

The following table presents loans by class modified as TDRs for which there was a payment default following the nlodification during the years ended

Number of Recorded Loans Investment

December 3 1 2014

Commercial $ Commercial real estate

Total $

December 3 1 2013 Commercial $ 1 7 1 Commercial real estate 636

Total 2 $ 807

J loan is considered to be in payment default once it is 90 days past due under the modified contractual terms Loans less than $ 1 00 vill not be evaluated for impairment under TOR accounting guidance

The TDRs that subsequently defaulted described above increased the allowance for loan losses by $0 and $80 respectively for the years ended December 3 1 2 0 1 4 and 20 13 and did not result in any charge-offs

I n order to determine whether a borrower is experiencing financial difficulty an evaluation is performed of the probabil ity that the borrower will be in payment default on any of its debt in the foreseeable future without the modification This evaluation is performed under the Companys internal underwriting policy

2 1

The Company categorizes its non-hotnogeneous loans into risk categories based on relevant information about the ability of borrowers to service their debt such as among other factors current financial information historical payment experience credit documentation public information and current economic trends The Company analyzes loans individually by classifying the loans as to credit risk This analysis includes certain non-homogeneous loans such as commercial commercial real estate and construction and development loans This analysis is done continually on a loan by loan basis The Company uses the following definitions for classified risk ratings

Substandard Loans designated as substandard are inadequately protected by the current net worth and paying capacity of the obligor or of the collaleral pledged i f any Loans have a well-defined weakness or weaknesses that jeopardize the I iquidation of the debt They are characterized by the distinct possibility that the Company will sustain some loss if the deficiencies are not corrected

Doubtful Loans classified as doubtful have all the weaknesses inherent in those classified as substandard with the added characteristic that the weaknesses make collection or liquidation in full on the basis of currently existing facts conditions and values highly questionable and improbable

Loans not 1neeting the criteria above that are analyzed individually as part of the above described process are considered to be pass rated loans The risk categories of loans were as follows

Classified Pass Total December 3 1 20 1 4

Commercial $ 44 1 29 $ 346876 $ 391 005 Commercial real estate 30787 328284 359071 tonstruction and development 2647 4 1 493 44140

Total $ 77563 $ 7 1 6653 $ 794216

December 3 1 201 3 Con1111ercial $ 58382 $ 280637 $ 3390 1 9 Commercial real estate 28664 3 1 2805 341 469 Construction and development 5580 49981 55561

J otal $ 92626 $ 643423 $ 736049

Note 4 - Premises and Equipment

Major classifications of assets comprising premises and equipment are summarized as follows at December 3 1

2014 2013 Land $ 1 5803 $ 1 5803 Premises 57 1 7 1 56 1 74 Furniture and equipment 56646 55394

Total 1 29620 1 27371 Less accumulated depreciation ( 84046) I 80756)

Premises and equipment net $ 45574 $ 466 1 5

22

The Company leases certain branch properties and equipment under operating leases Rent expense was $389 and $554 for 20 14 and 20 1 3 respectively Rent commitments before considering renewal options that generally are present are summarized as follows

20 1 5 20 1 6 20 1 7 20 1 8 2019 Thereafter Total

Note 5 - Other Real Estate Owned

Activity in other real estate owned was as follows at December 3 1

Beginning balance Acquired through or i nstead of loan foreclosure Reductions from sales Write-downs Ending balance

$

$

368 258

74 74 74 43

891

2014

$ 20458 880

( 1 1 870) (2059)

$ 7409

20 1 3 $ 22757

1 291 7 ( 13575)

( 1 64 1 ) $ 20458

Other real estate ovncd is reported net of a valuation allowance of $0 and $477 as of Dcce1nbcr 3 1 20 14 and 20 13 respectively Expenses excluding write-downs relating to other real estate owned for 20 14 and 20 1 3 were $886 and $2448 respectively

Activity in the valuation allowance on other real estate owned was as follows

2014

Beginning balance $ 477 Additions charged to expense Reductions from sales of OREO (477) Ending balance $

Note 6 - Deposits

The major categories of deposits arc sun1marized as follows at December 3 1

Demand-non interest-bearing NOW Money market checking Savings Time deposits

Less than $250000 $250000 and greater

Total

23

20 1 4 $ 203373

42 1 1 99 546288 457055

2603 1 2 1 4644

$ 1 902871

20 1 3 $ 477

$ 477

20 1 3 $ 1 74471

40 1 1 5 5 534275 433995

293206 1 7220

$ 1 854322

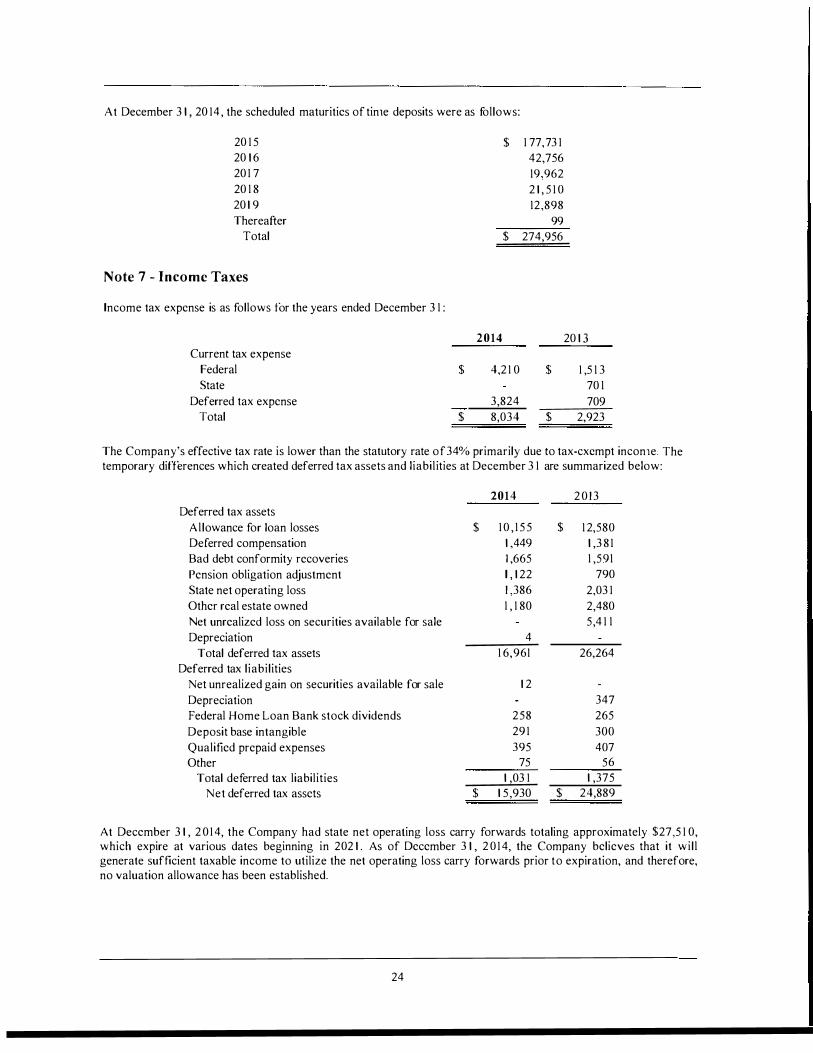

At December 3 1 20 14 the scheduled maturities of tin1e deposits were as follows

20 1 5 $ 1 77 73 1 20 1 6 42756 20 1 7 19962 20 1 8 2 1 5 1 0 20 1 9 12898 Thereafter 99

Total $ 274956

Note 7 - Income Taxes

Income tax expense is as follows tOr the years ended December 3 1

2014 20 1 3 Current tax expense

Federal $ 42 1 0 $ 1 5 1 3 State 70 1

Deferred tax expense 3824 709 Total $ 8034 $ 2923

The Companys effective tax rate is lower than the statutory rate of34oo primarily due to taxcxcmpt incon1e The temporary differences which created deferred tax assets and liabilities at December 3 1 are summarized below

2014 2013 Deferred tax assets

Allowance for loan losses $ 1 0 1 5 5 $ 1 2580 Deferred compensation 1 449 1 3 8 1 Bad debt conformity recoveries 1 665 1 591 Pension obligation adjustment I 1 22 790 State net operating loss 1 386 203 1 Other real estate owned 1 1 80 2480 Net unrealized loss on securities available for sale 54 1 1 Depreciation 4

Total deferred tax assets 1 6961 26264 Deferred tax liabilities

Net unrealized gain on securities available for sale 1 2 Depreciation 347 Federal Home Loan Bank stock dividends 258 265 Deposit base intangible 29 1 300 Qualified prepaid expenses 395 407 Other 75 56

Total deferred tax liabilities 1 03 1 1 375 Net deferred tax assets $ 1 5930 $ 24889

At December 3 1 20 14 the Company had state net operating loss carry forwards totaling approximately $275 1 0 which expire at various dates beginning in 202 1 As of December 3 1 20 14 the Company believes that it will generate sufficient taxable income to utilize the net operating loss carry forwards prior to expiration and therefore no valuation allowance has been established

24

Based on the carry back available and expected future taxable income management believes it is more likely than not that the remaining deferred tax asset as of December 3 1 20 1 4 and 20 1 3 will be realized lhereforc no valuation allowance has been established

There were no unrecognized tax benefits as of December 3 1 2014 and 20 13 The Company does not expect a significant change in the unrecognized tax benefit in the next twelve months During 2014 and 20 1 3 the Company did not record any interest or penalties related to income tax matters in income tax expense The Co1npany and its subsidiaries are subject to US federal income tax as well as income tax of the State of I l l inois The Company is no longer subject to examination by taxing authorities for years before 20 1 1

Note 8 - Benefit Plans

The Bank maintains the West Suburban Bank 401 (k) Profit Sharing Plan (the 40 l (k) Plan) which currently serves as the Companys principal retirement plan The 40 I (k) Plan was established to address the limited availability of West S uburban common stock for acquisition by the ESOP and to offer participants an avenue to diversify their retirement savings The Company recorded expenses totaling $644 and $60 1 during 20 1 4 and 20 1 3 respectively for contributions to the 401 (k) Plan

The Bank also maintains an ESOP which is a noncontributory tax qualified retirement plan that covers en1ployees who have satisfied specific service requirements The ESOP provides incentives to employees by granting participants an interest in West Suburban common stock which represents the ESOPs primary investment

At December 3 1 2014 and 20 1 3 the ESOP held 85253 and 87053 shares of West Suburban common stock respectively that were allocated to ESOP participants Upon termination of their employment participants who elect to receive their benefit distributions in the form of West Suburban common stock may request the Company to purchase when the Company is legally pern1itted to purchase its comn1on stock the common stock distributed at the appraised fair n1arket value during two 60-day periods The first purchase period begins on the date the benefit is distributed and the second purchase period begins on the first anniversary of the distribution date The estimated fair value of the con1mon stock allocated to the ESOP participants was $363 1 8 and $28379 at Decc1nber 3 1 20 1 4 and 20 13 respectively

During 2014 and 2013 the ESOP distributed $437 and $353 respectively in cash representing the interests of participants In addition the ESOP distributed 1 799 shares of West Suburban co1nmon stock in 20 1 4 and 1 1 68 shares i n 20 1 3 The Company recorded expenses totaling $454 and $304 during 20 1 4 and 20 13 respectively tOr contributions to the ESOP Plan

An individual account is established for each participant under the 401 (k) Plan and the ESOP and the benefits payable upon retirement termination disability or death arc based upon service the amount of the en1ployers and for the 40 1 (k) Plan an etnployees contributions and any income expenses gains and losses and forfeitures allocated to the participants account

The Co1npany maintains deferred compensation arrangements with certain fom1er and current executive officers and certain metnbers of the Board of Directors The deferred compensation was $87 and $ I 00 for the years ended December 3 1 20 1 4 and 20 1 3 respectively Executive officers can elect to defer the pay1ncnt of a percentage of their salaries and cash bonuses if any and members of the Board of Directors can elect to defer the payment of their directors fees In addition the Co1npany can elect to make annual contributions for the benefit of current participants in the Companys deferred compensation arrangements The annual contributions tOr certain senior executive officers in 20 1 4 and 20 1 3 were $75 and $ 1 00 respectively or $25 per officer There were no annual contributions for certain other executive officers in 2014 and 20 1 3

The total accumulated liability for all deferred compensation arrangcrncnts was $3621 and $3354 at December 3 1 20 1 4 and 20 1 3 respectively These amounts are included in accrued interest and other liabilities in the consolidated balance sheets

25

The Cornpany maintains a noncontributory postretirement benefit plan covering certain senior executives The plan provides postretirement n1edical dental and long term care coverage for certain executives and their surviving spouses The eligible retirement age under the plan is age 62 The company used a December 3 1 measurement date for its postretirement benefit plan The plan is unfunded

lnfonnation about changes during 20 1 4 and 20 1 3 in obligations of the postretirement benefit plan follows

Change in benefit obligation

lcginning benefit obligation

Service cost

Interest cost

Actuarial loss (gain)

l3enefits paid

Ending benefit obligation

Change in plan assets at fair value

Beginning plan assets

Employer contributions

Benefits paid

Ending plan assets

Unfunded status at December 3 1

$

2014

l 298 1 2 6 1

737 (29)

2079

29 (29)

$ 2079

$

2013

l 4 1 4 1 7 53

( 1 59) (27)

1 298

27 (27)

$ 1298

Amounts recognized in accumulated other comprehensive loss at December 3 1 consist of

2014 2013 Net actuarial loss $ 953 $ 235 Prior service cost 1 27 148

Total $ l 080 $ 383

The accumulated benefit obligation was $2079 and $ 1 298 at December 3 1 20 1 4 and 20 1 3 respectively

26

Net postretirement benefit costs included the following components for the years ended December 3 1

201 4 2013 Service cost $ 1 2 $ 1 7 Interest cost 6 1 5 3 Amortization of unrecognized prior service cost 2 1 2 1 Amortization of net loss 1 9 48

Net periodic postrctirement benefit cost 1 1 3 1 3 9

Net loss (gain) 737 ( 1 59) Prior service cost Amortization of net gain ( 19) ( 48) Amortization of prior service cost (2 1 ) ( 2 1 )

Total recognized i n other comprehensive loss (income) 697 (228) Postretirement benefit cost and other comprehensive loss (income) $ 8 1 0 $ (89)

The esti1nated net loss and the prior service cost for the defined postretirement benefit plan that will be amortized fron1 accumulated other comprehensive incon1c into net periodic benefit cost over the next fiscal year are $ 1 43 and $2 1 respectively

The discount rate used to determine the benefit obligations in 20 1 4 and 20 1 3 was 425oo and 475 respectively The discount rate used to determine the net periodic benefit costs in 20 1 4 and 2013 was 475oo and 375 respectively

For measurement purposes a 65 annual rate of increase in the per capita premium cost of covered healthcare benefits was assun1ed for 2015 with the rate of increase reducing 5 per annum to an ultimate rate of increase of 5 in 2018 Dental benefits were assun1ed to increase 5 for 20 1 5 which rate of increase is assumed to apply to future periods

Assumed healthcare cost trend rates have a significant effect on the amounts reported for the healthcare plans A one-percentage-point change in assumed healthcare cost trend rates would have the following effects

Effect on total service and interest cost Effect on accumulated postretirement benefit obligation

One-Percentage-Point Increase

$ 82 2400

One-Percentage-Point Decrease

$ 63 1 8 1 3

The Company expects to contribute a1nounts i n 20 1 5 to satisfy its postretirement benefit plan obligations The following benefit payn1ents which reflect expected future service are expected for the years indicated

2015 $ 69 20 1 6 84 20 1 7 6 1 201 8 59 20 1 9 69 Fallowing 5 Years 496

27

Note 9 - Off-Balance Sheet Risk Contingent Liabilities and Guarantees

The Company is a party to off-balance sheet financial instruments to meet the financing needs of its customers These financial instruments include com1nitments to extend credit and standby letters of credit These financial instruments involve to varying degrees elements o[ credit and interest rate risks Such financial instruments arc recorded when funded

Commitments to extend credit are agreements to lend to a customer as long as there is no violation of any condition established in the agreement These commitments primarily consist of unused lines of credit undrawn portions of construction and development loans and commitments to make new loans Commit1nents generally have fixed expiration dates or other termination provisions and may require the payn1ent of a fee Since many of the com1nitments are expected to expire without being exercised or drawn upon the total commitment an1ounts do not necessarily represent future cash requirements

The Companys exposure to credit risk in connection with commitments to extend credit and standby letters of credit is the contractual amount of those instruments before considering customer collateral or ability to repay The Company uses the same credit policies in making commitments and conditional obligations as it does tOr onshybalance-sheet instruments The Co1npany generally requires collateral or other security to support financial instrun1ents with credit risk The Company evaluates each customers creditworthiness on a case-by-case basis The amount of collateral obtained i f deemed necessary by the Company is based on 1nanagcments credit evaluation of the customer Collateral held varies and may include accounts receivable i nventory and equipment or comn1crcial or residential properties

A summary of the contractual exposure to off-balance sheet risk as of December 3 1 follows

Co1nmercial loans and lines of credit

Check credit lines of credit

Mortgage loans

l-ome equity lines of credit

Letters of credit

Credit card lines of credit

Total

Note 1 0 - Fair Value of Financial Instruments

$

$

2014

1 32498 786

1 09453 6333

32 1 0 1 28 1 1 7 1

$

$

20 1 3 1 3 1 387

796 3468

1 1 2774 7691

33474 289590

Fair value is the exchange price that would be received for an asset or paid to transfer a liability (exit price) in the principal or most advantageous market for the asset or liabil ity in an orderly transaction between market participants on the measurement date There are three levels of inputs that may be used to measure fair values

Level I middot middot Quoted prices (unadjusted) fOr identical assets or liabilities in active markets that the entity has the ability to access as of the measurement date Level 2 - Significant other observable inputs other than Level I prices such as quoted prices for similar assets or liabilities quoted prices in markets that are not active or other inputs that are observable or can be corroborated by observable market data Level 3 - Significant unobservable inputs that reflect a companys own assumptions about the assumptions that market participants would use in pricing an asset or l iabil ity

1he Company used the following methods and signi ficant assu1nptions to estin1ate the fair value of each type of financial instrument

Securities The fair value of securities is detennined by quoted market prices if available (Level 1 ) For securities where quoted prices are not available fair value is calculated based on market prices of similar securities (Level 2)

28

1or securities where quoted prices or market prices of similar securities are not available fair value is calculated using discounted cash flows or other market indicators (Level 3 )

Impaired Loans The fair value of i1npaired loans secured by real estate with specific allocations of the allowance for loan losses is based on recent real estate appraisals These appraisals may utilize a single valuation approach or a combination of approaches including comparable sales and the income approach Adjustments are routinely made in the appraisal process by the appraisers to adjust fOr ditlerences between the comparable sales and income data available Such adjustments are usually significant and typically result in a Level 3 classification of the inputs for detennining fair value Non-real estate collateral may be valued using an appraisal net book value per the borrowers iinancial statements or aging reports adjusted or discounted based on managements historical knowledge changes in market conditions from the time of the valuation and managements expertise and knowledge of the client and clients business resulting in a Level 3 fair value classification Impaired loans are evaluated on a quarterly basis tOr additional i1npairn1ent and adjusted accordingly

()ther Real Estate Owned Assets acquired through or instead of loan foreclosure arc initially recorded at fair value less costs to sell when acquired establishing a new cost basis These assets are subsequently accounted for at lower of cost or fair value less estimated costs to sell Fair value i s commonly based on recent real estate appraisals which arc generally updated no less frequently than annually These appraisals may utilize a single valuation approach or a combination of approaches including comparable sales and the income approach Adjustments arc routinely made in the appraisal process by the independent appraisers to adjust for differences between the comparable sales and income data available Such adjustments are usually significant and typically result in a Level 3 classification of the inputs for determining fair value Real estate owned properties are evaluated on a quarterly basis for additional impairment and adjusted accordingly

Assets and liabilities nleasured at fair value on a recurring basis are as fOllovs at year-end

Significant Quoted Prices in Other

Active Markets for Observable Carrying Identical Assets Inputs

Value (Level I ) (Level 2)

2 0 1 4 Recurring basis

US government sponsored enterprises $ 42699 $ $ 42699 Mortgage-backed residential 4578 1 7 4578 1 7 State and political subdivisions 8 1 679 8 1 679

corporate 20549 20549 Total securities available for sale $ 602744 $ $ 602744

20 1 3 Recurring basis US government sponsored enterprises $ 68399 $ $ 68399 Mortgage-backed residential 4 1 4693 4 1 4693

State and political subdivisions 1 1 8529 1 1 8529

Corporate 28982 28982 Total securities available for sale $ 630603 $ $ 630603

There were no transfers between Level I and Level 2 during 20 1 4 and 20 13

Significant Unobservable

Inputs (Level 3)

$

$

$

$

During 20 1 4 and 2013 the Company had no securities where the fair value was determined using Level 3 inputs

29

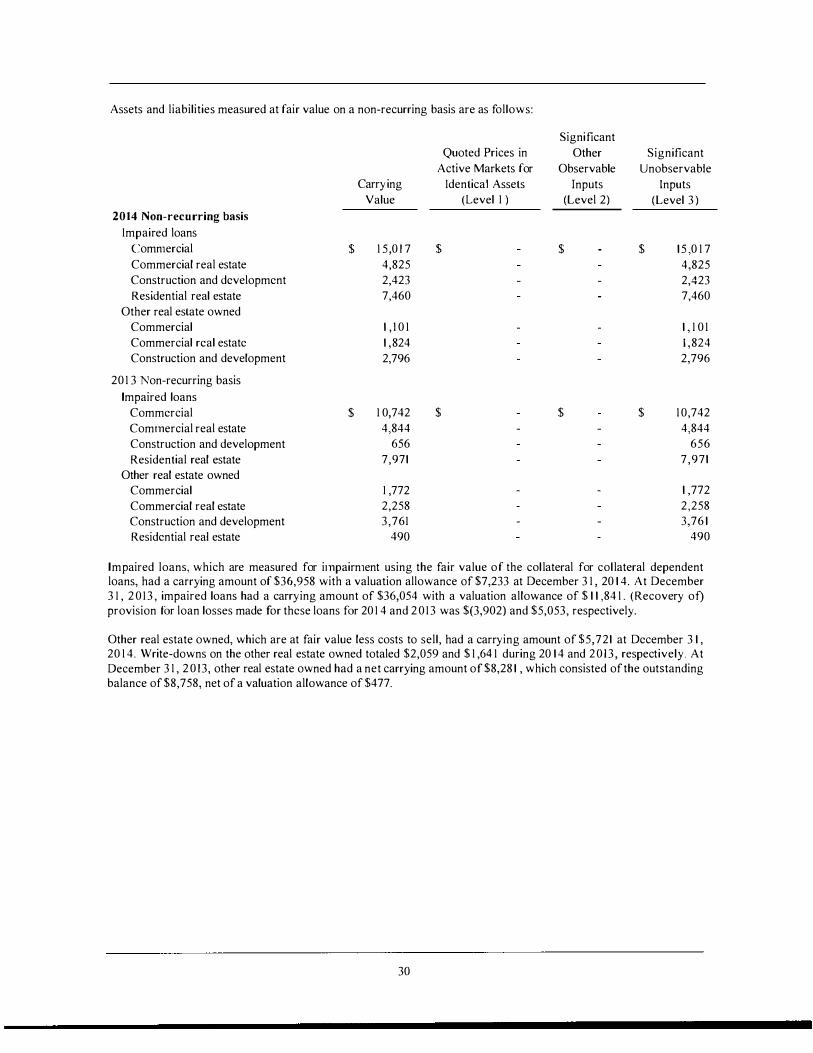

Assets and liabilities measured at fair value on a non-recurring basis are as follows

2014 Non-recurring basis

Impaired loans (omn1ercial Commercial real estate Construction and development Residential real estate

Other real eslate owned Commercial Commercial real estate Construction and development

20 1 3 11on-recurring basis Impaired loans

Commercial Comtnercial real estate Construction and development Residential real estate

Other real estate owned Commercial Commercial real estate Construction and development Residential real estate

$

$

Quoted Prices in Active Markets for

Carrying Identical Assets Value (Level 1 )

1 50 1 7 $ 4825 2423 7460

1 1 0 1 1 824 2796

1 0742 $ 4844

656 7971

1 772 2258 3761

490

Significant Other Significant

Observable Unobservable Inputs Inputs

(Level 2) (Level 3)

$ $ 1 5 0 1 7 4825 2423 7460

1 1 0 1 1 824 2796

$ $ 1 0742 4844

656 7971

1 772 2258 376 1

490

Impaired loans which are measured for i1npairn1ent using the fair value of the collateral for collateral dependent loans had a carrying amount of $36958 with a valuation allowance of $7233 at December 3 1 20 1 4 At December 3 1 20 13 impaired loans had a carrying amount of $36054 with a valuation allowance of $ 1 1 84 1 (Recovery of) provision for loan losses made for these loans for 20 1 4 and 2013 was $(3902) and $5053 respectively

Other real estate owned which are at fair value less costs to sell had a carrying amount of $5721 at December 3 1 20 1 4 Write-downs on the other real estate owned totaled $2059 and $ 1 64 1 during 20 1 4 and 2013 respectively At December 3 1 20 13 other real estate owned had a net carrying amount of $828 1 which consisted of the outstanding balance of $8758 net of a valuation allowance of $477

30

The following table presents quantitative infonnation about Level 3 fai r value measurements for financial instruments measured at fair value on a non-recurring basis

2014 Non-recurring basis

In1paired loans Commercial

Commercial real estate

Construction and development Residential real estate

Other real estate ovvned commcrcial commcrcial real estate Construction and development

2013 Non-recurring basis Impaired loans

Commercial Commercial real estate Construction and development Residential real estate

Other real estate ovvned Commercial

(ommenial real estate Construction and development Residential real estate

$

$

Fair Value

12278

2739

3295

1530

2423

7460

1 101

1824

2796

1 0742

4844

656

7971

1 326

446

2258

3761

490

Valuation Techniques Range

Sales comparison 5oo - 12

Sales and income approach 7

Sales cotnparison 5 - (Yo

Sales and cost approach 7ltyo