Embed Size (px)

Citation preview

ROLE OF THE REINSURER IN ERM (ENTERPRISE RISK MANAGEMENT)

II. Istanbul Insurance Conference, 30 September 2010

Joachim Mathe, Executive Client ManagerJürgen Brucker, Client Manager

Agenda

Overview

Munich Re Risk Management Model

Financial Crisis: How Munich Re weathered the Storm

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Preparation for ERM in Europe: Munich Re’s Support

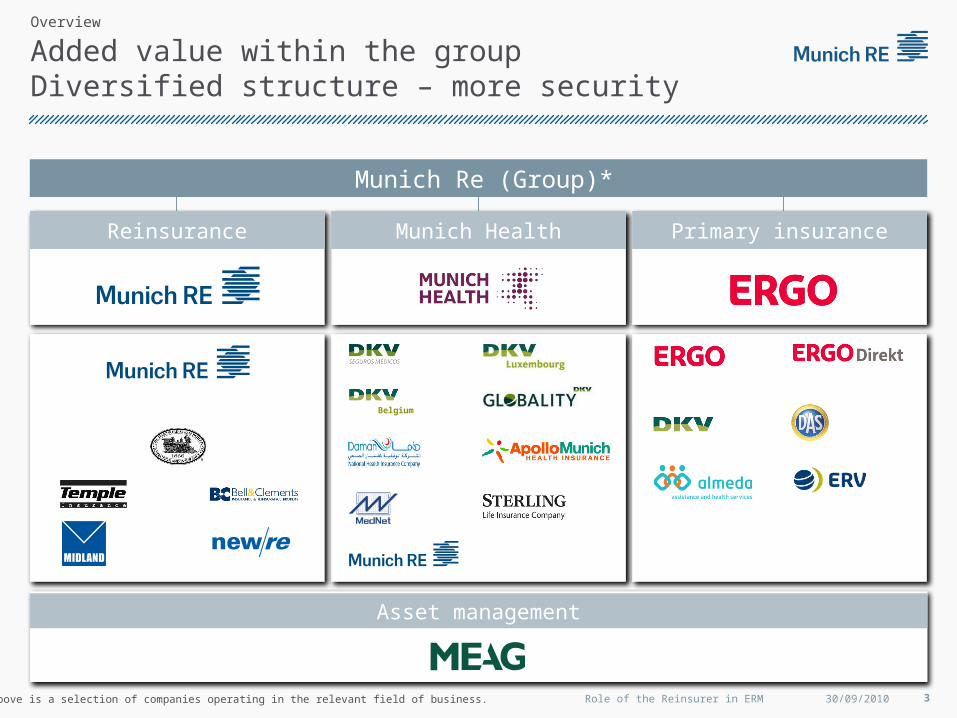

Added value within the groupDiversified structure – more security

Munich Re (Group)*

Asset management

Belgium

*The above is a selection of companies operating in the relevant field of business.

Overview

Reinsurance Primary insuranceMunich Health

30/09/2010 3Role of the Reinsurer in ERM

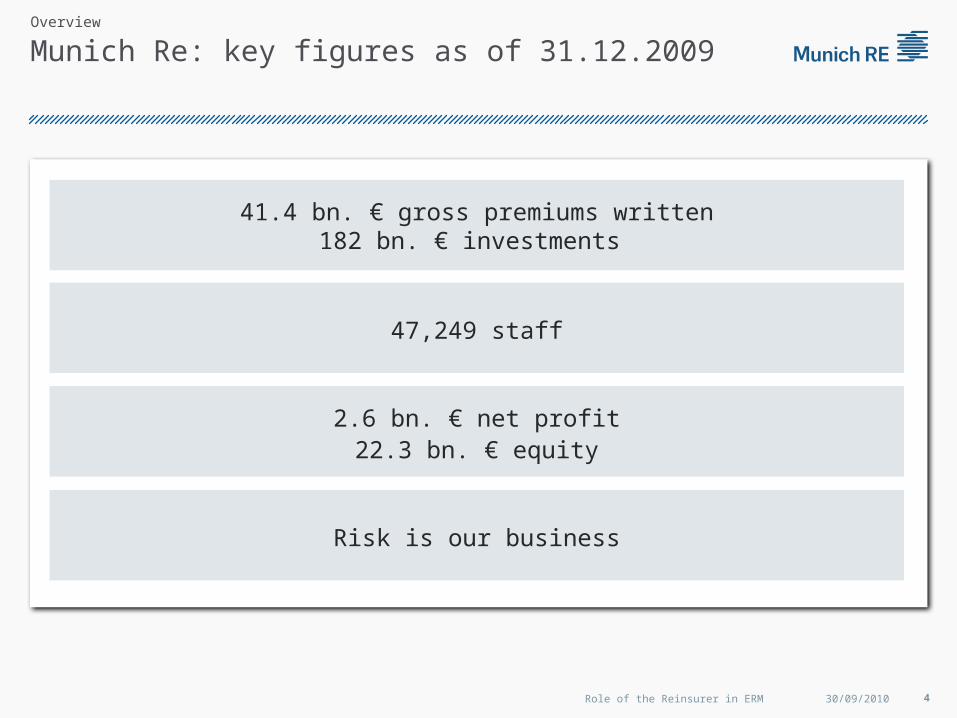

Munich Re: key figures as of 31.12.2009

41.4 bn. € gross premiums written182 bn. € investments

2.6 bn. € net profit22.3 bn. € equity

47,249 staff

Risk is our business

Overview

30/09/2010 4Role of the Reinsurer in ERM

Agenda

Overview

Munich Re Risk Management Model

Financial Crisis: How Munich Re weathered the Storm

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Preparation for ERM in Europe: Munich Re’s Support

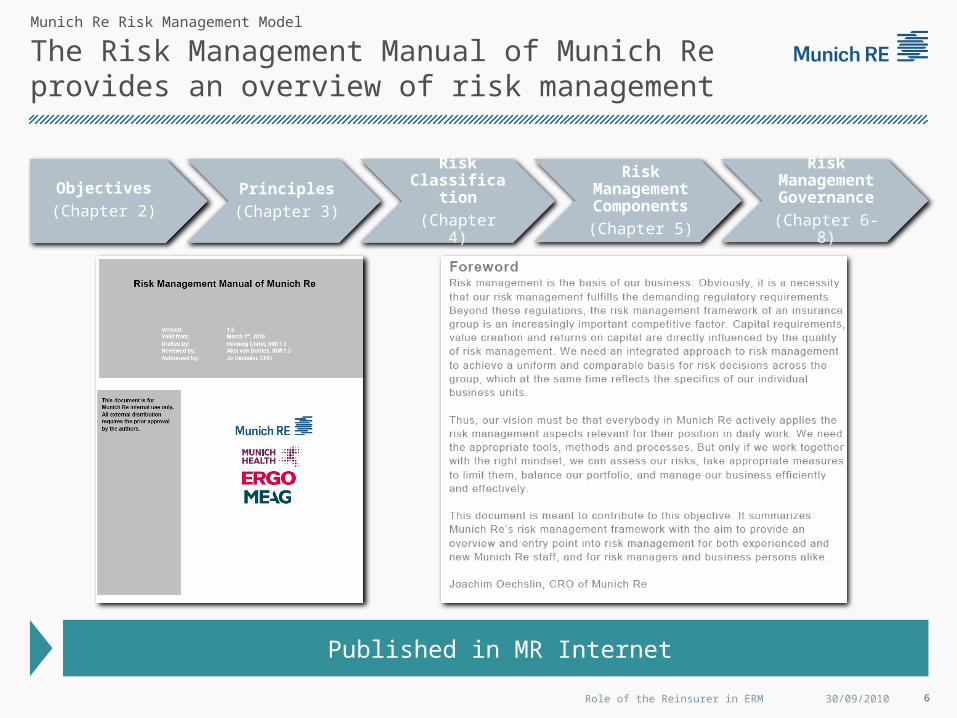

The Risk Management Manual of Munich Re provides an overview of risk management

Objectives

(Chapter 2)Principles

(Chapter 3)

Risk Classification

(Chapter 4)

Risk Management Components

(Chapter 5)

Risk Management Governance

(Chapter 6-8)

Munich Re Risk Management Model

Published in MR Internet

30/09/2010 6Role of the Reinsurer in ERM

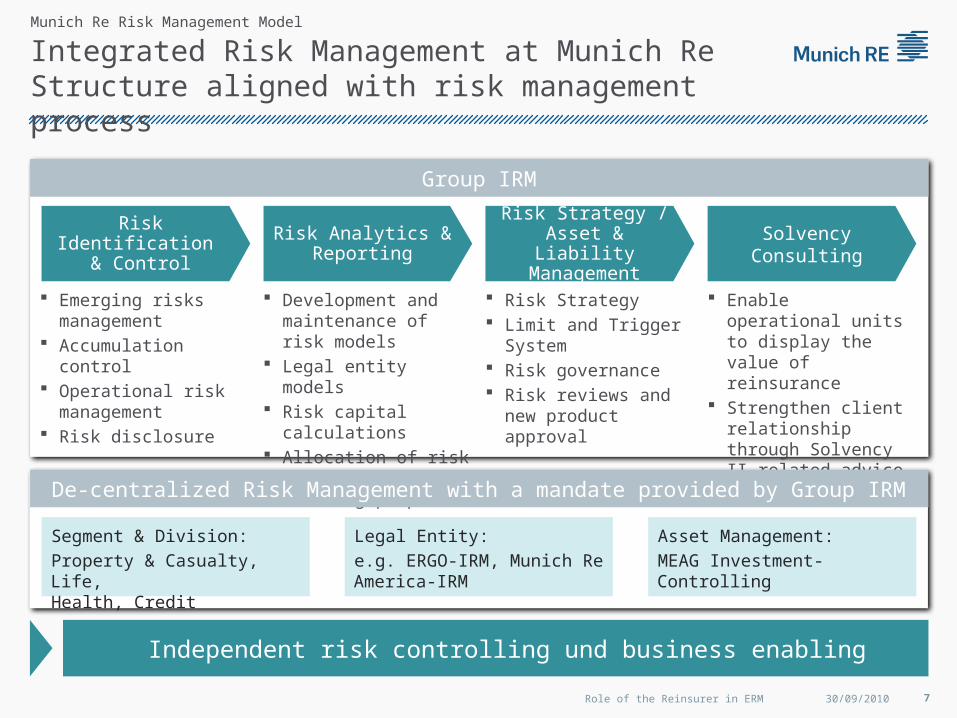

Risk Strategy /Asset & Liability

Management

Risk Analytics & Reporting

Risk Identification & Control

Emerging risks management

Accumulation control Operational risk

management Risk disclosure

Development and maintenance of risk models

Legal entity models Risk capital calculations Allocation of risk capital

for steering purposes

Solvency Consulting

Enable operational units to display the value of reinsurance

Strengthen client relationship through Solvency II-related advice and service

Risk Strategy Limit and Trigger System Risk governance Risk reviews and new

product approval

Integrated Risk Management at Munich ReStructure aligned with risk management process

Group IRM

Segment & Division:

Property & Casualty, Life, Health, Credit

Legal Entity:

e.g. ERGO-IRM, Munich Re America-IRM

Asset Management:

MEAG Investment-Controlling

Munich Re Risk Management Model

Independent risk controlling und business enabling

De-centralized Risk Management with a mandate provided by Group IRM

30/09/2010 7Role of the Reinsurer in ERM

Sets business targets and risk strategy Defines risk limits based on risk-bearing capacity Monitors business and risk profile (e.g. based on risk report)

Independent verification that effective controls are in place and functioning properly

Business planning Identify and evaluate risks Take steps to manage / mitigate all risks associated

with their business Manage and own risks of all transactions regardless

of ultimate approval level Report exposures to independent risk function

Independent risk analysis and monitoring Challenge and provide input for risk strategy Recommend limits and monitor adherence to limits Design and implement risk control processes Act as a risk consultant to Business Units

Board of Management

“Third line of defense” - Internal audit

“Second line of defense” – Independent Risk management functionsFirst “line of defense” - Risk takers

Regulation requires a clear segregation of risk taking responsibilities and controls

Munich Re Risk Management Model

Specific nature of independent oversight may vary by business and risk type

30/09/2010 8Role of the Reinsurer in ERM

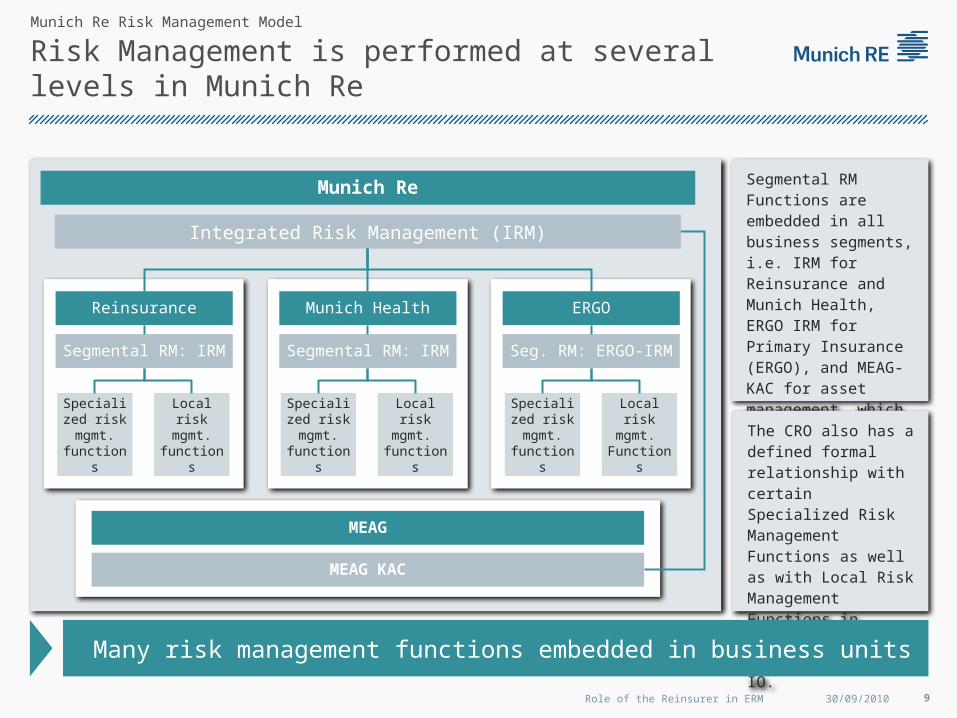

Risk Management is performed at several levels in Munich Re

MEAG

Munich Re

Reinsurance Munich Health ERGO

Segmental RM Functions are embedded in all business segments, i.e. IRM for Reinsurance and Munich Health, ERGO IRM for Primary Insurance (ERGO), and MEAG-KAC for asset management, which have a dotted-line reporting relationship to the CRO.

The CRO also has a defined formal relationship with certain Specialized Risk Management Functions as well as with Local Risk Management Functions in certain legal entities in the IO.

Munich Re Risk Management Model

Many risk management functions embedded in business units

Integrated Risk Management (IRM)

Segmental RM: IRM Segmental RM: IRM Seg. RM: ERGO-IRM

Specialized risk mgmt. functions

Local risk mgmt.

functions

Specialized risk mgmt. functions

Local risk mgmt.

functions

Specialized risk mgmt. functions

Local risk mgmt.

Functions

MEAG KAC

30/09/2010 9Role of the Reinsurer in ERM

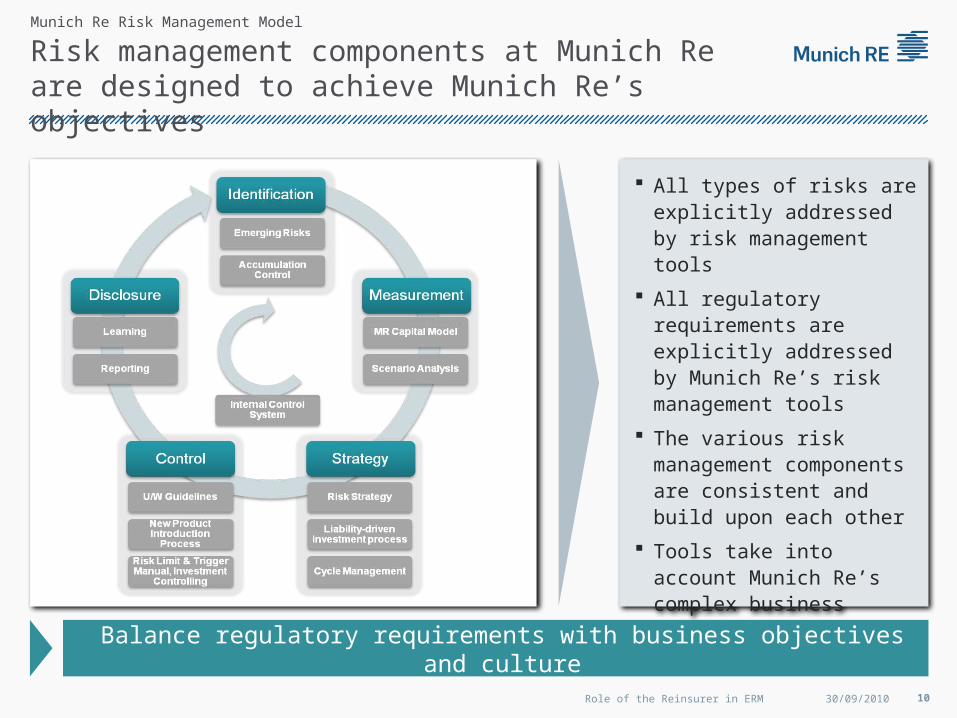

Risk management components at Munich Re are designed to achieve Munich Re’s objectives

All types of risks are explicitly addressed by risk management tools

All regulatory requirements are explicitly addressed by Munich Re’s risk management tools

The various risk management components are consistent and build upon each other

Tools take into account Munich Re’s complex business taking a group perspective

Munich Re Risk Management Model

Balance regulatory requirements with business objectives and culture

30/09/2010 10Role of the Reinsurer in ERM

Agenda

Overview

Munich Re Risk Management Model

Financial Crisis: How Munich Re weathered the Storm

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Preparation for ERM in Europe: Munich Re’s Support

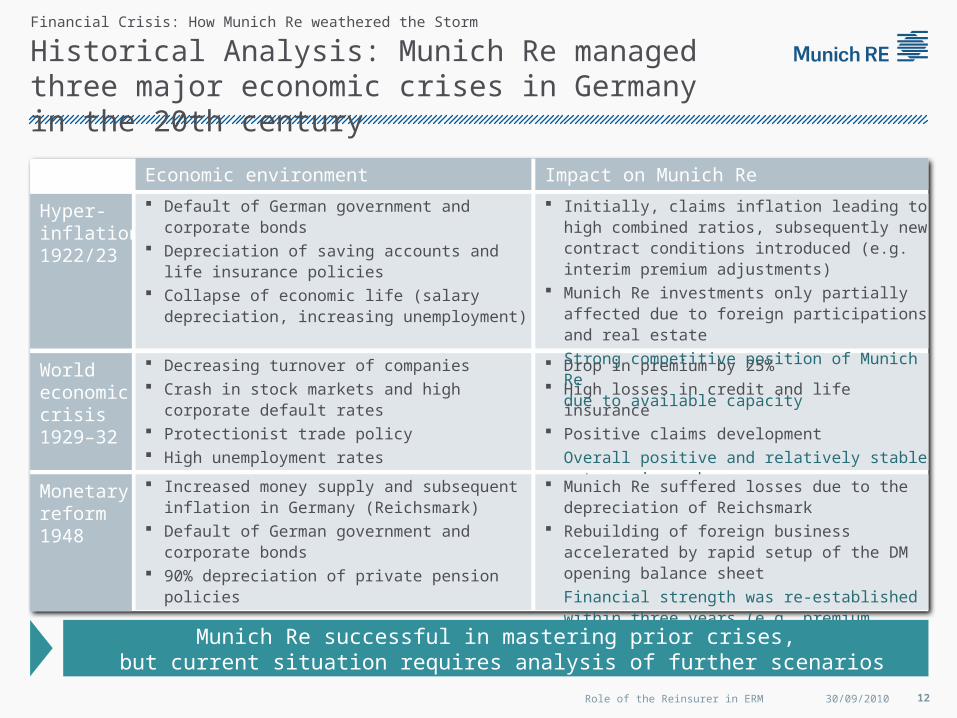

Historical Analysis: Munich Re managed three major economic crises in Germany in the 20th century

Impact on Munich Re

Hyper-inflation1922/23

World economic crisis1929–32

Monetaryreform1948

Drop in premium by 25% High losses in credit and life insurance Positive claims development

Overall positive and relatively stable returns in each year

Economic environment

Decreasing turnover of companies Crash in stock markets and high corporate default

rates Protectionist trade policy High unemployment rates

Munich Re suffered losses due to the depreciation of Reichsmark

Rebuilding of foreign business accelerated by rapid setup of the DM opening balance sheet

Financial strength was re-established within three years (e.g. premium increase by 30%)

Increased money supply and subsequent inflation in Germany (Reichsmark)

Default of German government and corporate bonds

90% depreciation of private pension policies

Initially, claims inflation leading to high combined ratios, subsequently new contract conditions introduced (e.g. interim premium adjustments)

Munich Re investments only partially affected due to foreign participations and real estate

Strong competitive position of Munich Re due to available capacity

Default of German government and corporate bonds

Depreciation of saving accounts and life insurance policies

Collapse of economic life (salary depreciation, increasing unemployment)

Financial Crisis: How Munich Re weathered the Storm

Munich Re successful in mastering prior crises, but current situation requires analysis of further scenarios

30/09/2010 12Role of the Reinsurer in ERM

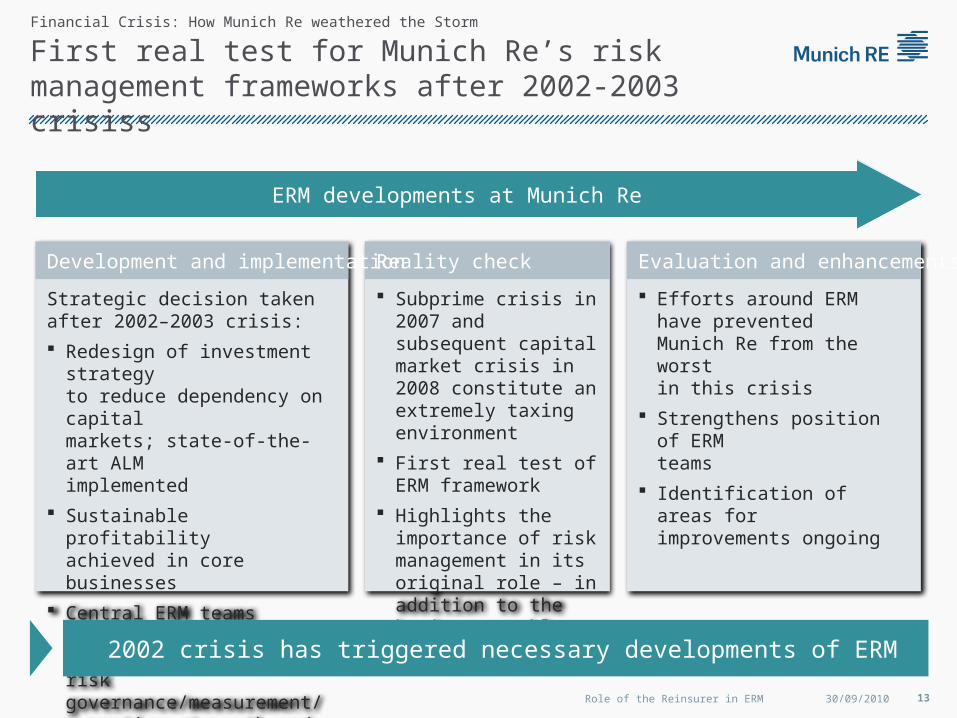

First real test for Munich Re’s risk management frameworks after 2002-2003 crisiss

Subprime crisis in 2007 and subsequent capital market crisis in 2008 constitute an extremely taxing environment

First real test of ERM framework

Highlights the importance of risk management in its original role – in addition to the business enabler

Reality check

Efforts around ERM have preventedMunich Re from the worst in this crisis

Strengthens position of ERM teams

Identification of areas for improvements ongoing

Evaluation and enhancements

Strategic decision taken after 2002–2003 crisis:

Redesign of investment strategyto reduce dependency on capital

markets; state-of-the-art ALMimplemented

Sustainable profitabilityachieved in core businesses

Central ERM teams established under CRO leadership (2004);risk governance/measurement/reporting strengthened

Development and implementation

ERM developments at Munich Re

Financial Crisis: How Munich Re weathered the Storm

2002 crisis has triggered necessary developments of ERM

30/09/2010 13Role of the Reinsurer in ERM

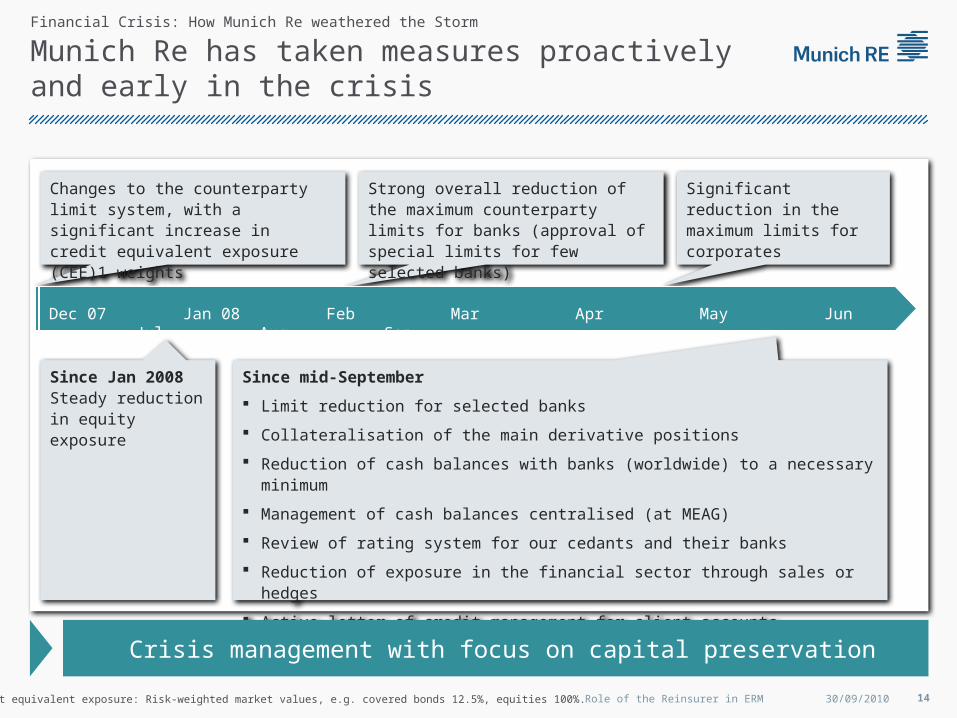

14

Since mid-September

Limit reduction for selected banks

Collateralisation of the main derivative positions

Reduction of cash balances with banks (worldwide) to a necessary minimum

Management of cash balances centralised (at MEAG)

Review of rating system for our cedants and their banks

Reduction of exposure in the financial sector through sales or hedges

Active letter-of-credit management for client accounts

Since Jan 2008 Steady reduction in equity exposure

Strong overall reduction of the maximum counterparty limits for banks (approval of special limits for few selected banks)

Munich Re has taken measures proactivelyand early in the crisis

Changes to the counterparty limit system, with a significant increase in credit equivalent exposure (CEE)1 weights

Significant reduction in the maximum limits for corporates

Dec 07 Jan 08 Feb Mar Apr May Jun Jul Aug Sep

Financial Crisis: How Munich Re weathered the Storm

Crisis management with focus on capital preservation

1 Credit equivalent exposure: Risk-weighted market values, e.g. covered bonds 12.5%, equities 100%. 30/09/2010Role of the Reinsurer in ERM

Forward-looking risk management and de-risking pay off

CDS spreads1 (1.1.2008–31.1.2010)3Beta values1 (1.1.2004–31.1.2010)2

2.2

2.0

1.8

1.6

1.4

1.2

1.0

0.8

0.6

0.4

Source: Bloomberg

2004 2005 2006 2007 2008 2009

J F M A M J J A S O N D J F M A M J J A S O N D J2008 2009

Source: Bloomberg

Munich Re 0.87

0

50

100

150

200

250

300

Munich Re 47 bp

Strong position of Munich Re to deliver solid performance

Confidence in forward-looking risk management

Financial strength reflected inlow CDS spread

1 Peers: Allianz, AXA, Generali, Hannover Re, Swiss Re, Zurich Financial Services.2 Raw beta to DJ Stoxx 600, total return, daily basis, 1-year. 3 5-year credit default swaps (spreads in basis points p.a.).

Financial Crisis: How Munich Re weathered the Storm

30/09/2010 15Role of the Reinsurer in ERM

State of the insurance industry

Industry eventually survived crisis relatively unharmed, with notable exceptions

However, industry threatened by spill-over of regulatory concepts directed to

banks

At times, risk capacity was an issue (sometimes unnoticed)…

…but industry was lucky that Solvency II has not been in place at year end 2008

Uncertainty around Solvency II calibration has recently depressed insurance

sector…

…but finally there are some good news: QIS5 calibration looks more reasonable

than what could be expected

Future earnings potential under pressure due to lower investment income –

insurance companies again in search for yield enhancement

Industry still too dependent on banking industry – government debt an increasing

concern

Financial Crisis: How Munich Re weathered the Storm

30/09/2010 16Role of the Reinsurer in ERM

Agenda

Overview

Munich Re Risk Management Model

Financial Crisis: How Munich Re weathered the Storm

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Preparation for ERM in Europe: Munich Re’s Support

Solvency II is the regulation that comes closest to an enterprise risk management system

Solvency II objectives

Overall goal: Consumer

protection

Creation of a harmonised

supervisory system throughout

Europe based on the actual risk

situation of each insurance

company

Extending the existing

quantitative supervisory system

through development of

companies' own internal risk

models and risk management

processes

Adding a qualitative aspect to

the supervisory system through

internal risk management

system requirements

Solvency II

Planned adaptations of Solvency II in Japan, Israel, Mexico, Chile, Bermuda, etc...

Adjustments of risk-based capital type regulation (USA, Canada, ...)

Swiss Solvency Test

High

Low

Relative implementation level of enterprise risk management concept

18

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

30/09/2010 18Role of the Reinsurer in ERM

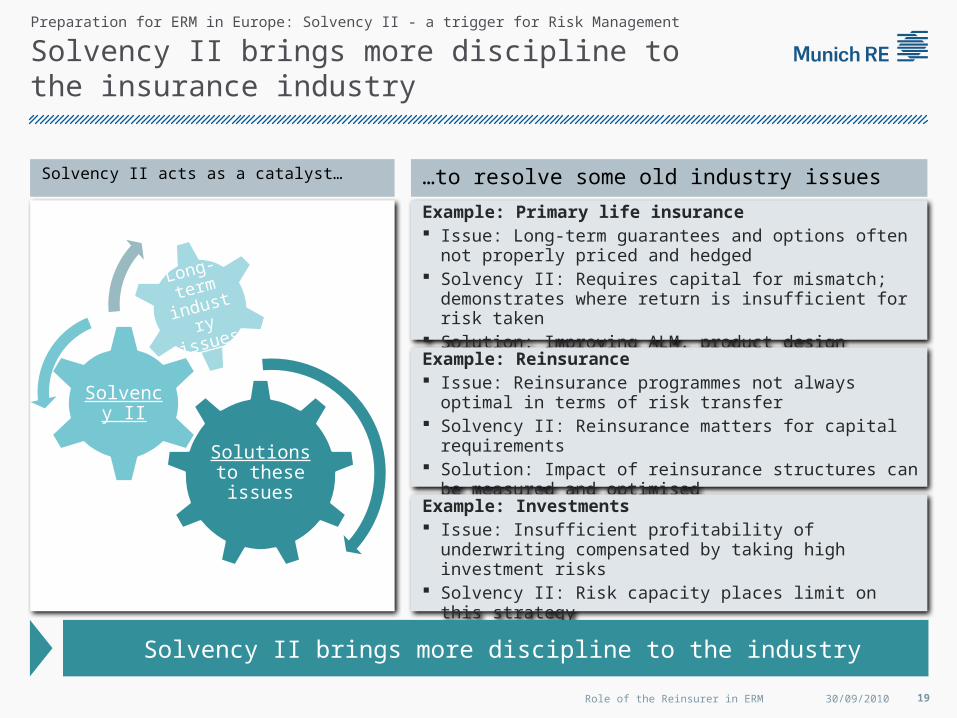

Solvency II brings more discipline to the insurance industry

Solvency II acts as a catalyst… …to resolve some old industry issues

Example: Primary life insurance Issue: Long-term guarantees and options often not properly

priced and hedged Solvency II: Requires capital for mismatch; demonstrates

where return is insufficient for risk taken Solution: Improving ALM, product design

Example: Reinsurance Issue: Reinsurance programmes not always optimal in terms

of risk transfer Solvency II: Reinsurance matters for capital requirements Solution: Impact of reinsurance structures can be measured

and optimised Solutions to these issues

Solvency II

Long-

term

industry

issues

Example: Investments Issue: Insufficient profitability of underwriting compensated by

taking high investment risks Solvency II: Risk capacity places limit on this strategy Solution: Focusing on profitable underwriting

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Solvency II brings more discipline to the industry

30/09/2010 19Role of the Reinsurer in ERM

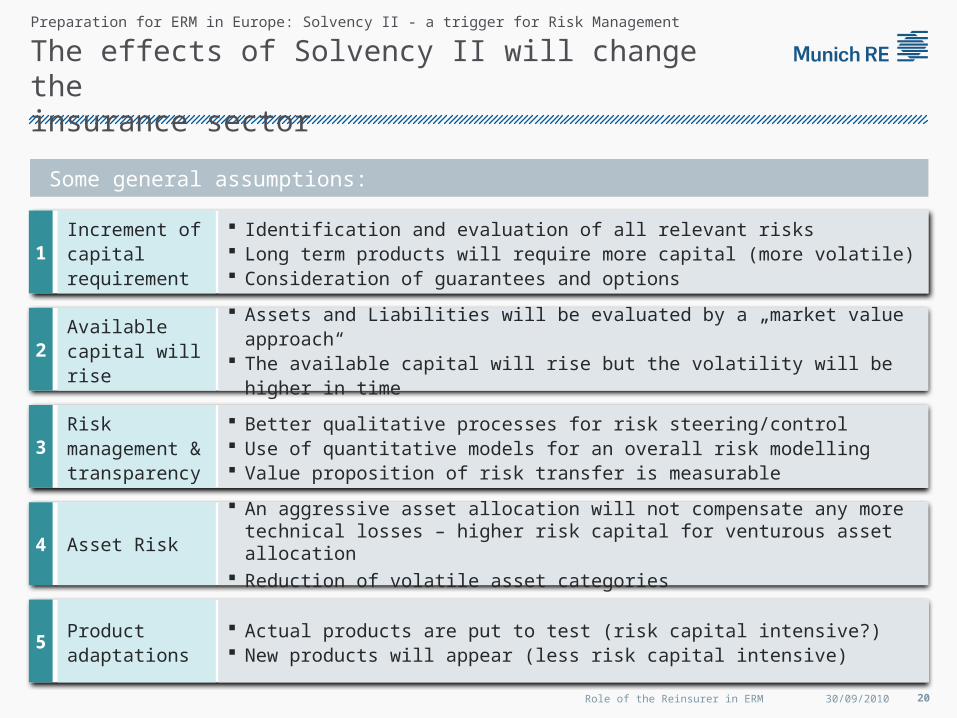

The effects of Solvency II will change the insurance sector

Increment of capital requirement

Identification and evaluation of all relevant risks Long term products will require more capital (more volatile) Consideration of guarantees and options

1

Available capital will rise

Assets and Liabilities will be evaluated by a „market value approach“ The available capital will rise but the volatility will be higher in time

2

Risk management & transparency

Better qualitative processes for risk steering/control Use of quantitative models for an overall risk modelling Value proposition of risk transfer is measurable

3

Asset Risk

An aggressive asset allocation will not compensate any more technical losses – higher risk capital for venturous asset allocation

Reduction of volatile asset categories 4

Product adaptations

Actual products are put to test (risk capital intensive?) New products will appear (less risk capital intensive)

5

Some general assumptions:

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

30/09/2010 20Role of the Reinsurer in ERM

Comparison of Solvency Ratios (European weighted average)

Polan

d

Slova

kia

Germ

any

Denm

ark

Hunga

ry

Austri

a

Franc

eIta

ly

Czech

Rep

ublic

Estoni

a

Roman

ia

Belgi

um

Finla

nd

Sweden

Cypru

s

Lith

uani

a

Greec

e

Luxe

mbo

urg

Spain

Icela

nd

Slove

nia

Portu

gal

Nethe

rland

sM

alta

Unite

d Kin

gdom

Norway

Latvi

a0%

100%

200%

300%

400%

500%

600%

QIS4 Solvency I

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Source: CEIOPS’ QIS4 report 30/09/2010 21Role of the Reinsurer in ERM

Solvency II is a trigger for Enterprise Management and Value based Management

Minimising cost of risk capital

Enterprise Risk Management

Diversification (risk segments, perils, regions, portfolio size)

Operational Excellence (product design, pricing, risk selection, claims,…)

Asset-liability matching

Risk Transfer: Traditional R/I, Securitization, Portfolio Swaps

M&A

Challenges are varied:

Financial conglomerates

Big, international insurance undertakings

Medium-sized to small insurers

Niche insurers

Monoliners

Reinsurers

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

In the past, success was measured by combined ratio and investment income. Return on risk adjusted capital is the new key figure that is also used by MR.

30/09/2010 22Role of the Reinsurer in ERM

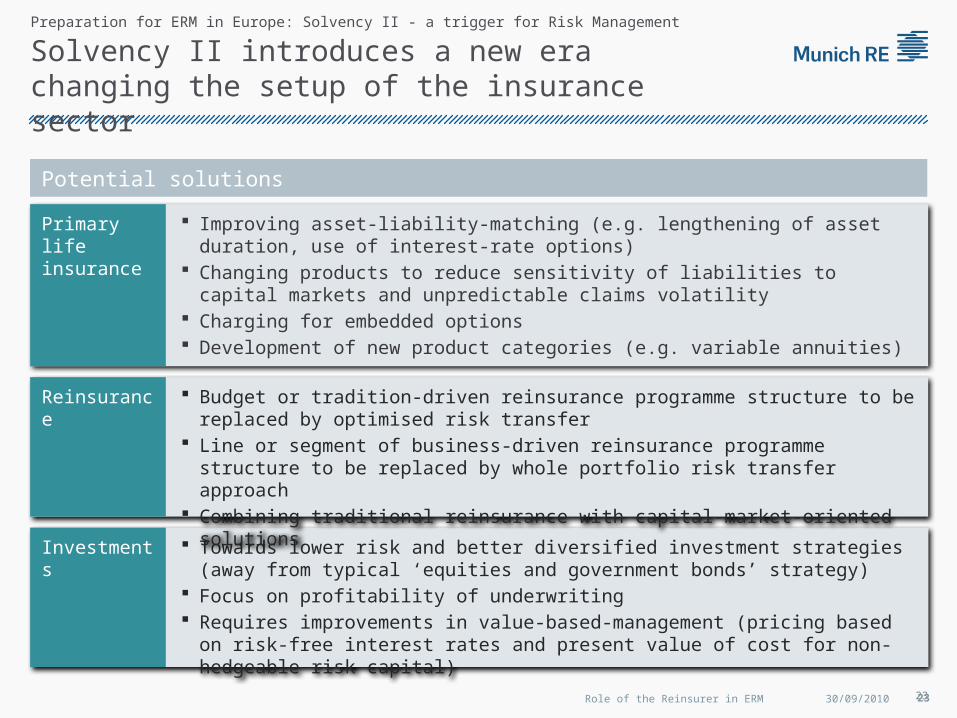

Towards lower risk and better diversified investment strategies (away from typical ‘equities and government bonds’ strategy)

Focus on profitability of underwriting Requires improvements in value-based-management (pricing based on risk-free

interest rates and present value of cost for non-hedgeable risk capital)

Investments

Budget or tradition-driven reinsurance programme structure to be replaced by optimised risk transfer

Line or segment of business-driven reinsurance programme structure to be replaced by whole portfolio risk transfer approach

Combining traditional reinsurance with capital-market-oriented solutions

Reinsurance

Improving asset-liability-matching (e.g. lengthening of asset duration, use of interest-rate options)

Changing products to reduce sensitivity of liabilities to capital markets and unpredictable claims volatility

Charging for embedded options Development of new product categories (e.g. variable annuities)

Primary life insurance

Potential solutions

Solvency II introduces a new era changing the setup of the insurance sector

23

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

30/09/2010 23Role of the Reinsurer in ERM

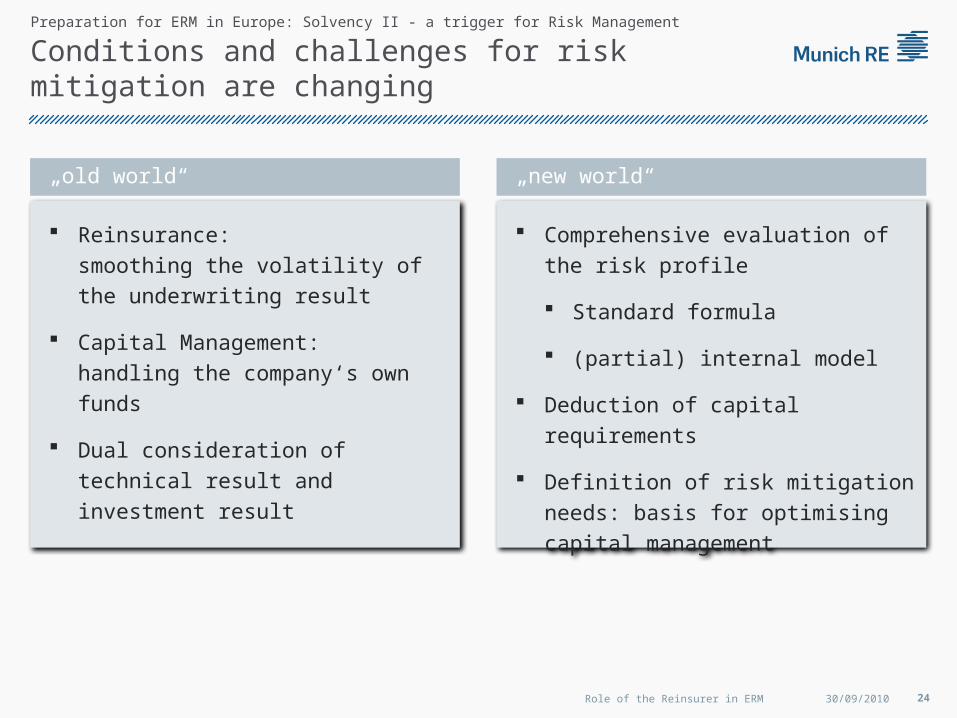

Reinsurance:

smoothing the volatility of the

underwriting result

Capital Management:

handling the company‘s own funds

Dual consideration of technical result

and investment result

Comprehensive evaluation of the risk

profile

Standard formula

(partial) internal model

Deduction of capital requirements

Definition of risk mitigation needs:

basis for optimising capital

management

Conditions and challenges for risk mitigation are changing

„old world“ „new world“

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

30/09/2010 24Role of the Reinsurer in ERM

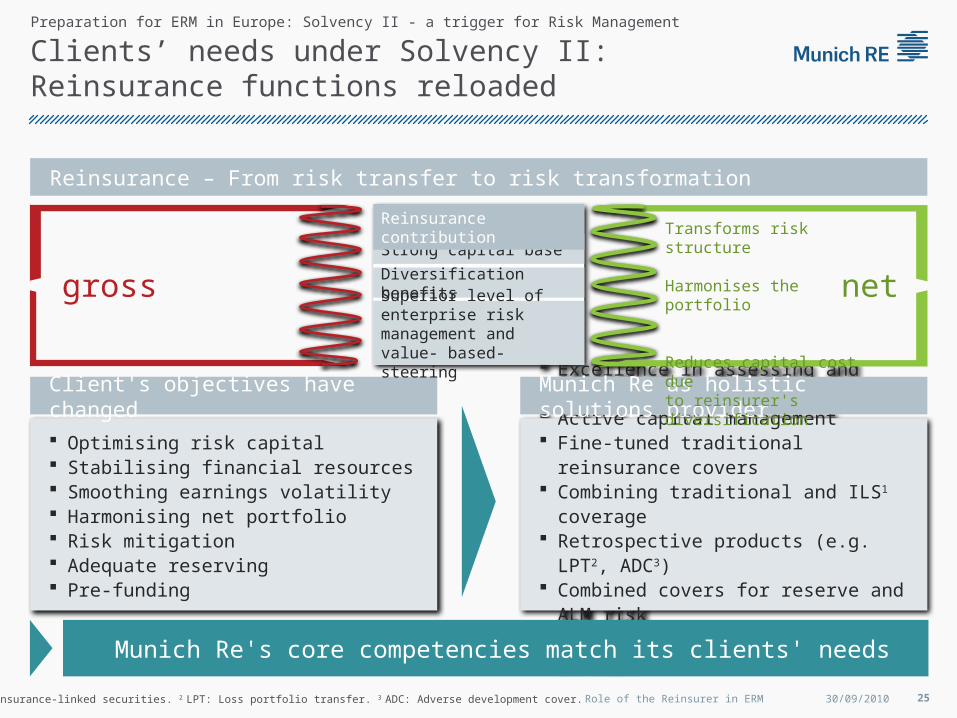

Clients’ needs under Solvency II: Reinsurance functions reloaded

Optimising risk capital Stabilising financial resources Smoothing earnings volatility Harmonising net portfolio Risk mitigation Adequate reserving Pre-funding

Client's objectives have changed

Excellence in assessing and modelling risk Active capital management Fine-tuned traditional reinsurance covers Combining traditional and ILS1 coverage Retrospective products (e.g. LPT2, ADC3) Combined covers for reserve and ALM risk Life: Pre-funding, monetisation of MCEV

Munich Re as holistic solutions provider

Reinsurance – From risk transfer to risk transformation

Transforms risk structure

Harmonises the portfolio

Reduces capital cost dueto reinsurer's diversification

Strong capital base

Diversification benefits

Superior level of enterprise risk management and value- based-steering

gross net

Reinsurance contribution

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Munich Re's core competencies match its clients' needs

1 ILS: Insurance-linked securities. 2 LPT: Loss portfolio transfer. 3 ADC: Adverse development cover. 30/09/2010 25Role of the Reinsurer in ERM

AAA AA A BBB BB 0%

10%

20%

30%

40%

50%

60%

1% 3%7%

25%

55%

1% 2%5%

17%

38%

1 reinsurer 2 reinsurers 3 reinsurers 4 reinsurers 5 reinsurers 6 reinsurers

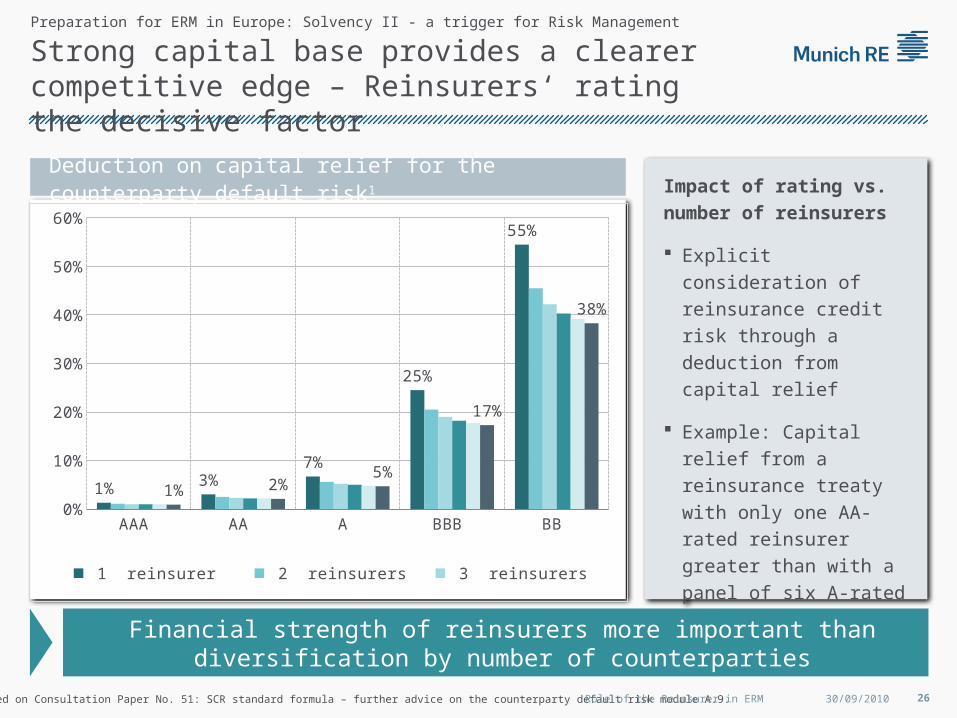

Strong capital base provides a clearer competitive edge – Reinsurers‘ rating the decisive factor

Impact of rating vs. number

of reinsurers

Explicit consideration of

reinsurance credit risk

through a deduction from

capital relief

Example: Capital relief from

a reinsurance treaty with

only one AA-rated reinsurer

greater than with a panel of

six A-rated reinsurers

Deduction on capital relief for the counterparty default risk1

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Financial strength of reinsurers more important thandiversification by number of counterparties

1 Graph based on Consultation Paper No. 51: SCR standard formula – further advice on the counterparty default risk module A.9. 30/09/2010 26Role of the Reinsurer in ERM

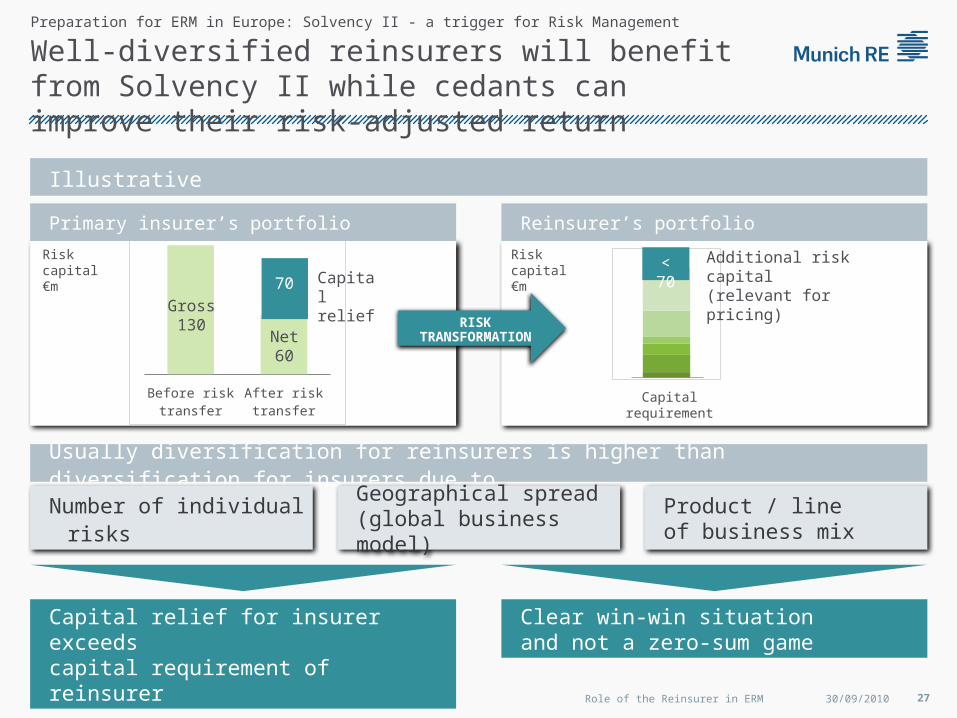

Illustrative

Well-diversified reinsurers will benefit from Solvency II while cedants can improve their risk-adjusted return

Before risk transfer

After risk transfer

Primary insurer’s portfolio Reinsurer’s portfolio

Usually diversification for reinsurers is higher than diversification for insurers due to

Capital relief for insurer exceedscapital requirement of reinsurer

Clear win-win situationand not a zero-sum game

RISK TRANSFORMATION

Number of individual risksGeographical spread (global business model)

Product / lineof business mix

Risk capital€m

Gross 130

Net60

70 Capital relief

< 70

Additional risk capital(relevant for pricing)

Capital requirement

Risk capital€m

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

30/09/2010 27Role of the Reinsurer in ERM

Agenda

Overview

Munich Re Risk Management Model

Financial Crisis: How Munich Re weathered the Storm

Preparation for ERM in Europe: Solvency II - a trigger for Risk Management

Preparation for ERM in Europe: Munich Re’s Support

29

Munich Re offers services using its own expertiseto help clients meet Solvency II requirements

Solvency Consulting

Operational units

IntegratedRisk Management

Preparing Munich Re’s operational units for the ‘new world’ of reinsurance purchasing: Risk modelling, enterprise risk management, IT tools, …

Transparent modelling services: Every calibration step is shared with the client, data and software free of charge available for further use by the client

Expertise from own Solvency II preparation facilitates impact analysis and solution design for clients Service products: Quicker development, client-oriented through ongoing contact with operational units Combined set-up for life and non-life business Profound market and industry expertise from our underwriting database helps compensate for lack of

client data

Solvency Consulting is a subdivision of Munich Re's Integrated Risk Management

Preparation for ERM in Europe: Munich Re’s Support

30/09/2010Role of the Reinsurer in ERM

Business enabling under Solvency II – From quantitative capital relief …

Price CapacitySolvency

Relief

Value of re-

insurance+ + =Traditional GAAP

VBM1 aspects

Supervisory andsolvency aspects

Analysis and calibration of risk and claims

profiles. Specific risk analysis (NatCat, biometric,

industrial, etc.), in-depth product and market

expertise Stochastic modelling of the underwriting risk:

Open source software platform (PillarOne) Analysis of Solvency Capital Requirement

(SCR): Optimisation of portfolio and of

reinsurance structure (PODRA2 service)

Design and provision of tailor-made risk

transfer solutions: Traditional reinsurance in

combination with alternative concepts,

e.g. securitisation and portfolio swaps Beyond risk transfer:

Asset-liability-matching (ALPHA) Life: Stochastic modelling of biometric

risks (BRiSMA)

Quantitative

Preparation for ERM in Europe: Munich Re’s Support

Independent, fully transparent analysis – no black boxMunich Re’s position strengthened by superior risk expertise

1 VBM: Value-based management.2 PODRA: Pillar One Dynamic Reinsurance Analysis. 30/09/2010 30Role of the Reinsurer in ERM

… to enterprise risk management support

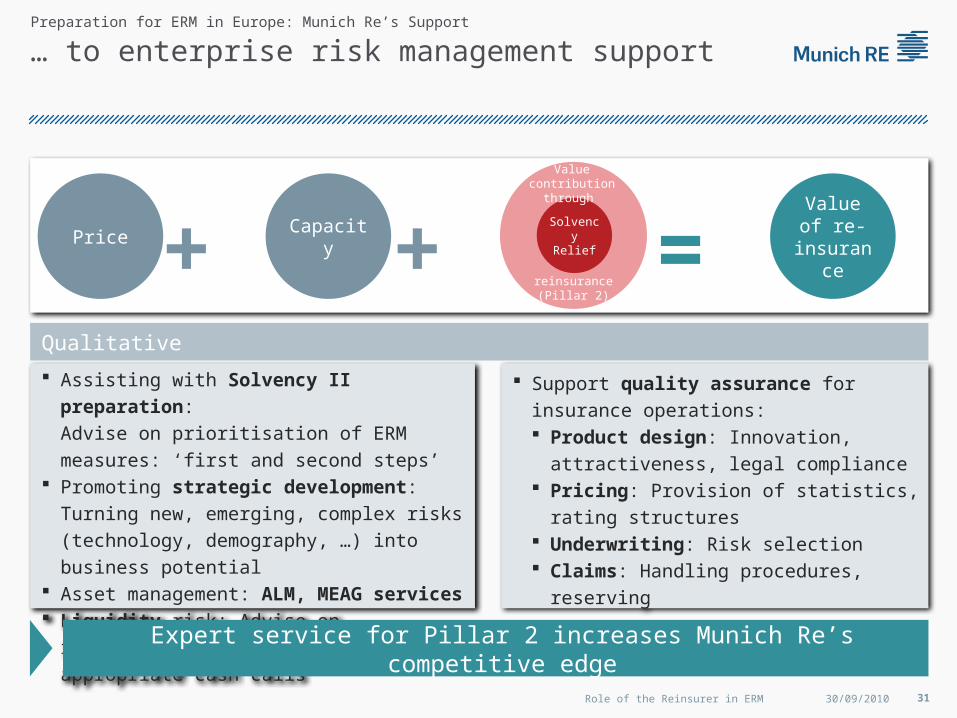

=Solvency Relief

Valuecontribution through

reinsurance(Pillar 2)

Assisting with Solvency II preparation:

Advise on prioritisation of ERM measures: ‘first

and second steps’ Promoting strategic development: Turning new,

emerging, complex risks (technology,

demography, …) into business potential Asset management: ALM, MEAG services Liquidity risk: Advise on retentions, NatCat

covers, appropriate cash calls

Support quality assurance for insurance

operations: Product design: Innovation, attractiveness,

legal compliance Pricing: Provision of statistics, rating

structures Underwriting: Risk selection Claims: Handling procedures, reserving

Qualitative

Value of re-

insurancePrice Capacity ++

Preparation for ERM in Europe: Munich Re’s Support

Expert service for Pillar 2 increases Munich Re’s competitive edge

30/09/2010 31Role of the Reinsurer in ERM

The qualitative impact of reinsurance

Reinsurance can be used as a risk-mitigation tool, for example in respect of

liquidity risk.

Besides, reinsurance can improve qualitative risk management in terms of

process support (i.e. underwriting, claims management), second opinion,

consultancies, and support of process excellence. No extra fee will be charged

because these additional services are normally covered by the reinsurance

contract.

Compared to third-party consulting services, which have to be paid additionally

by the insurer, the quality of reinsurance advice differs fundamentally: The

reinsurer shares the risk with its cedant, by participating in the underwriting result

of the reinsurance contract (“follow-the-fortunes” principle).

Preparation for ERM in Europe: Munich Re’s Support

Best services means best protection for both parties.

30/09/2010 32Role of the Reinsurer in ERM

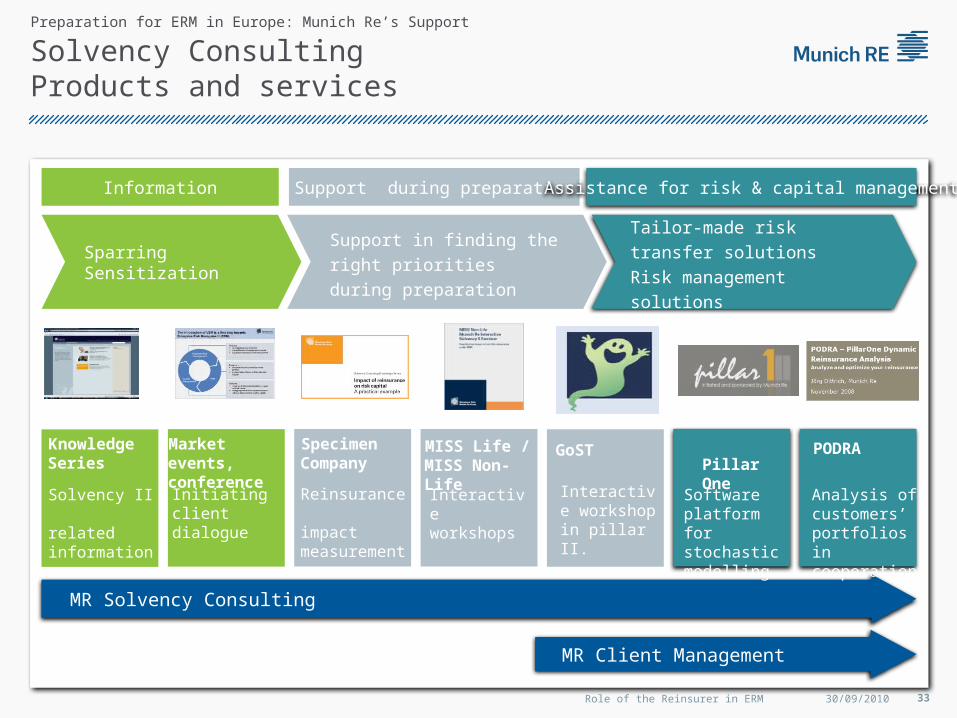

Solvency ConsultingProducts and services

Sparring SensitizationSupport in finding the right

priorities during preparation

Support during preparationInformation

Tailor-made risk transfer

solutions

Risk management solutions

Assistance for risk & capital management

Solvency II related information

Knowledge Series

Market events, conference

MISS Life / MISS Non-Life

Interactive workshops

Initiating client dialogue

SpecimenCompany

Reinsurance impact measurement

Analysis of customers’ portfolios in cooperation

PillarOne PODRA

Software platform for stochastic modelling

MR Solvency Consulting

MR Client Management

GoST

Interactive workshop in pillar II.

Preparation for ERM in Europe: Munich Re’s Support

30/09/2010 33Role of the Reinsurer in ERM

Our strengths = your added value: ALPHAClients benefit from MR Asset Liability Management Know-how

30/09/2010Role of the Reinsurer in ERM 34

Optimum-return asset allocation in

accordance with client’s risk appetite

Optimisation potential: Indication of ways to

increase return (usually up to 90 BP, i.e.

often above € 1m for a small/mid-sized

insurance company) or reduce the risk/risk

capital

Tried-and-tested analysis techniques and

understanding of requirements thanks to

several years of successful implementation

at Munich Re (proved worth during financial

crisis)

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%

Current allocation

Efficient frontier

Less Risk

Efficient frontier of Benchmark Portfolios

Replicating portfolio

More Return

Illustrative Figures

99.5% VaR (based on asset volume)

Exc

ess-

Ret

urn

ALPHA process and added value

Benchmarkportfolio(BMP)

Asset Management

Economicvaluation

CashflowsLoss data

Client

ClaimsPremiums

loss data;asset data where possible

OptionalAnalysis and support

Trad.RI

Internal MR process chain

ReplicatingPortfolio

(RP)

Preparation for ERM in Europe: Munich Re’s Support

Customer benefits

THANK YOU VERY MUCH FOR YOUR ATTENTION

Joachim Mathe Jürgen Brucker

© 2

01

0 M

ünc

hen

er R

ückv

ersi

che

run

gs-G

ese

llsch

aft

© 2

010

Mu

nich

Rei

nsu

ran

ce C

omp

any