Embed Size (px)

DESCRIPTION

The South African National Roads Agency Limited. Road Infrastructure Roll-Out Presentation to the Portfolio Committee Wednesday 6 November 2002 Cape Town. Contents. Network Strategic Objectives Challenges Non-Toll Roads Proposed 5 Year MTEF SANRAL Contribution to Poverty Relief - PowerPoint PPT Presentation

Citation preview

1Portfolio Committee 6/11/2002

Road Infrastructure Roll-Out

Presentation to the Portfolio Committee

Wednesday 6 November 2002Cape Town

The South AfricanNational Roads Agency Limited

2Portfolio Committee 6/11/2002

Contents

NetworkStrategic ObjectivesChallengesNon-Toll RoadsProposed 5 Year MTEFSANRAL Contribution to Poverty ReliefProgress

Toll RoadsConcession Contracts

3Portfolio Committee 6/11/2002

National Roads (7,200km) National Routes (5,300km) – 12,500km Strategic Network (7,500km) – 20,000km Primary Network (18,000km) – 38,000km

4Portfolio Committee 6/11/2002

STRATEGIC NETWORK

KMS

Existing National Road Network 7,200

Provincial Roads-Transfer Already Agreed:

- Free State 760

- Eastern Cape 850

- Western Cape 600

- Limpopo Province 1,950

Provincial Roads-Transfer to be Finalised 8,640

TOTAL STRATEGIC NETWORK 20,000

5Portfolio Committee 6/11/2002

STRATEGIC OBJECTIVES

To provide and manage a sustainable National Road Network

Minimise the cost of road transport Stimulate economic growth Promote Black economic empowerment and

value for moneys Be sensitive to the environment Meet the needs of our road users and

investors Inspire innovative and effective research and

development

6Portfolio Committee 6/11/2002

CHALLENGES

Capacity of delivery institutions (Private and Public) Use existing capacity within Govt Institutional fragmentation

Network layout and responsibilitiesDevelopment of Human Capital

Within the Agency Within the industry sector

Sources of funding

7Portfolio Committee 6/11/2002

Non-TollMTEF Submission 2003-05 (R Mill)

2003/04 2004/052005/06

Baseline fm 2002/03 1,171 1,241 1,315

Depreciation ZAR 117 124 132

Border posts 62 47 5

Traffic Control 180 220 200

Network Expansion 325 880 1,650

TOTAL 1,855 2,512 3,122

8Portfolio Committee 6/11/2002

PROPOSED 5 YEAR MTEF National and Provincial Roads

7

AdditionalFunding

AdditionalAbsorptionCapacity

Stagnation

Poor CompetitionJob & Skills shortagesPoor QualityJob Creation not SustainablePoor Asset Investment

Competitive IndustrySustainable Job CreationGood QualityBalanced Asset InvestmentBalanced Capacity Expansion

Very competitive – loss of capacityMore Value for MoneyAsset lossEmpowerment Stagnation

•Stable flow of funding is important

Macro Impacts of Funding Levels

9Portfolio Committee 6/11/2002

PROPOSED 5 YEAR MTEF National and Provincial Roads

Ideal situation 5-10% poor to very poor condition Maintain rest between fair and very

good condition

Match to capacity Earmarked allocation for

rural/community roads, +/- R3 bn

10Portfolio Committee 6/11/2002

PROPOSED 5 YEAR MTEF National and Provincial Roads

National and Provincial road condition under this scenario

Good FairVery PoorGood Very

Poor

Con

ditio

n

11Portfolio Committee 6/11/2002

PROPOSED 5 YEAR MTEF National and Provincial Roads

WHAT WE ACHIEVE Growth of backlog halted/slowed Rural (inter/intra village) roads boosted

– increase economic growth Many opportunities for jobs, SMMEs

and ABEs Stabilise & grow sector Retain skills Develop Human Capital

12Portfolio Committee 6/11/2002

PROPOSED 5 YEAR MTEF National and Provincial Roads

Rural (village) roads; R150-300k/km to upgrade rural roads Labour; 30-40% of construction in community

pockets Every R100m/year on construction;

513 000 – 684 000 person days on directly employed 300-600 km upgraded per year

=>R3bn over 5 years; 11,5 – 15,4 million person days over 5 years Upgrade 7500-15000km of rural roads Leave R670 – R900m in rural economy over 5 years Excludes multiplier effect of 4 - 6

13Portfolio Committee 6/11/2002

PROPOSED 5 YEAR MTEF National and Provincial Roads

Immediate Strategy;

Use MTEF funds to build Govt and industry capacity

Adapt spending to maintain good roads and prevent further deterioration

Ring fence 10-15%/year for rural (inter/intra village) roads for socio-economic improvement

14Portfolio Committee 6/11/2002

SANRAL CONTRIBUTION TO POVERTY RELIEF

107 Projects in rural areas R230 million allocated of R294 million Estimated employment 950 600 person

days R51,6million on labour Skills development Types of project;

Weed eradication Nurseries for indigenous plants Roads safety projects (education, infrastructure) Roads and Bridges

15Portfolio Committee 6/11/2002

SANRAL CONTRIBUTION TO POVERTY RELIEF

SDI’s; Lebombo: Hluhluwe-Kosi Bay (85%)

St Lucia Wetlands Park (98%)

Total Investment R310,2 million 3900 Jobs created

16Portfolio Committee 6/11/2002

PROGRESS-TOLL ROADS

Funding of roads has always been a controversial subject. This is not only true from a fiscal point of view – tax based revenues need to serve a large number of disparate demands – but also from a road user point of view in having to pay tolls.

It is important to note that the Agency manages approximately 80% of its total network as non-toll roads. This places a large financial burden not only on the Agency but also on National Treasury.

It is for this reason that alternative funding instruments be used and developed to address the infrastructural needs of our country while at the same time reducing the stresses

on tax based revenues.

17Portfolio Committee 6/11/2002

PROGRESS-TOLL ROADS

We are mindful that the implementation of toll roads

hinges on many political, economic and social

concerns. They are not simply a matter of capital

augmentation but also depend on such deeply

embedded societal concerns, such as:

Equity

Income transfer

Environmental issues

Attitude towards taxation

Role of Government

18Portfolio Committee 6/11/2002

PROGRESS-TOLL ROADS

In terms of public sentiment towards toll roads there is seldom a distinction drawn between Agency toll roads and toll roads operated by the private sector under concession agreement.

19Portfolio Committee 6/11/2002

PROGRESS-TOLL ROADS

Extension to existing toll routesRoute Kms Status

N1 Great North 108 - Construction underway,

completion due early 2003

N2 Tsitsikamma 54 - Final environmental approval awaited

N3 Mariannhill 86 - Process anticipated to commence mid 2003

N4 Pretoria 71 - Construction commenced,

completion expected mid 2004

N17 Springs-Ermelo 170 - Pending proclamation of national roads

20Portfolio Committee 6/11/2002

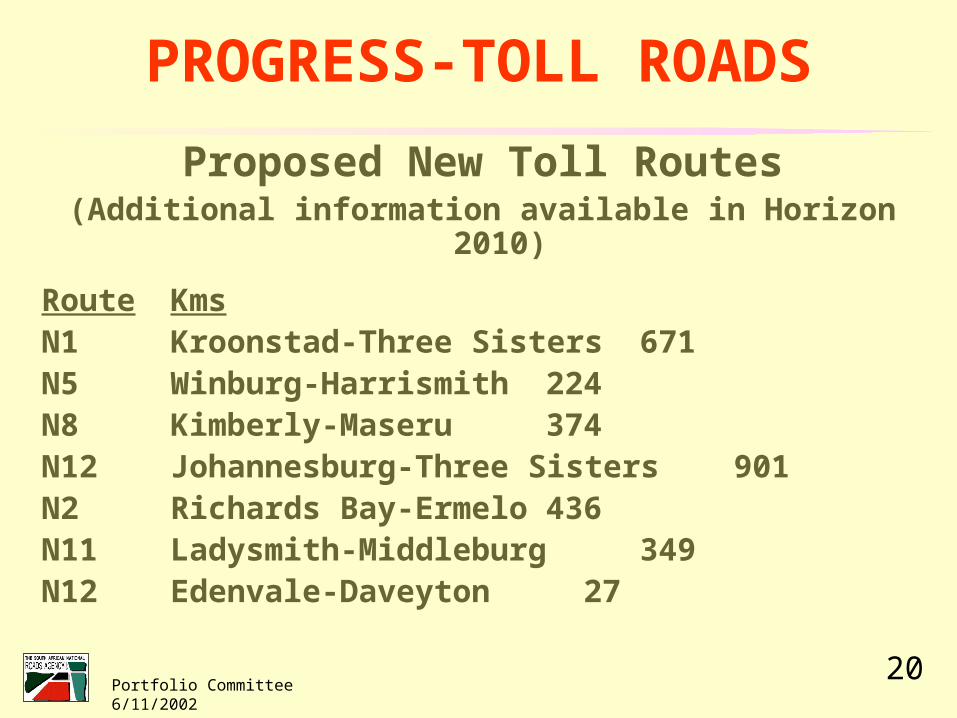

PROGRESS-TOLL ROADS

Proposed New Toll Routes(Additional information available in Horizon 2010)

Route KmsN1 Kroonstad-Three Sisters 671N5 Winburg-Harrismith 224N8 Kimberly-Maseru 374N12 Johannesburg-Three Sisters 901N2 Richards Bay-Ermelo 436N11 Ladysmith-Middleburg 349N12 Edenvale-Daveyton 27

21Portfolio Committee 6/11/2002

PROGRESS-TOLL ROADS

Proposed New Toll Routes

The feasibility studies are underway and the Public Participation Process is

currently being designed.

Please refer to “Horizon 2010” for further details

22Portfolio Committee 6/11/2002

PROGRESS-CONCESSIONS

Existing Concession ContractsMaputo Development Corridor (100%)N3 Jhb to Cedara (95%)Platinum (60%)

Total Investment R9.7bn Direct foreign investment R 1bn Jobs created - 10200

23Portfolio Committee 6/11/2002

PROGRESS-CONCESSIONS

Works in the near future;Wild Coast Development Corridor–

commences 2003N1/N2 Development Corridor in

Western Cape – commences 2003/2004

Estimated Investment R3,8bn Estimate of Jobs 8000

24Portfolio Committee 6/11/2002

Proposal for sustaining expanded non-toll network

Proposed total network

TOTAL

20 000 km

NON-TOLL

13 200 km

TOLL

4 000 km

CONCESSION

2 800 km

(1) Current MTEF funding 2002 (5 300kms) 1 061 1 061

(2) Annual expenditure requirement, current toll & concession network

725 370 355

(3) Annual expenditure requirement toll & concession expansion

2 500 2 100 400

(4) TOTAL NATIONAL ROAD NETWORK

ANNUAL EXPENDITURE (1+2+3) 4 286 1 061 2 470 755

(5) Total private sector contribution to annual expenditure requirement (public sector saving) (2+3)

3 225 2 470 755

(6) Reallocation of 65% of public sector saving (5x65%)

0 2 100 -1 600 -500

(7) REVISED PUBLIC SECTOR FUNDING (1+6) 3 161 3 161

(8) Available for other uses (5-6) 1 125

Of the total “saving” to the fiscus, it is proposed that 65% be consolidated into the treasury funding of non-toll roads in order to susin the expansion in the non-toll network and the remaining 35% put to other uses.