Embed Size (px)

Citation preview

Abu Dh Real EstateOverview Q4 2012 Riyadh

Riyadh

Macroeconomic Overview

2

Indicator 2011 2012 (e) 2013 (f)

Saudi Arabia

Population (millions) 28.4 29.3 30.2

Real GDP Growth (Y-o-Y) 8.5% 6.8% 2.7%

Inflation (% Change) 5.0% 4.5% 3.5%

Budget Surplus (USD billions) 78 103 74

Riyadh

Population (millions) 5.4 5.6 5.8

Cost of Living Index (% change) 5.8% 4.0% 3.5%

Sources: Sama, Jadwa, IHS Global Insights January 2013, CDS , 2012 (e) estimate : (f) forecast

Economic Highlights – Q4 2012

3

Real GDP in KSA grew by 6.8% in 2012. Despite adifficult global economic environment, higher oilproduction and expansionary fiscal policy have kept theKingdom’s growth elevated.

Retail sales increased by 24% in 2012. This growth isimproving the profitability of retailers and driving theleasing of new stores.

Bank lending rose consistently during 2012 with netcredit issued reaching SAR 125 billion, the highest levelsince 2008. Bank lending to the building andconstruction sector has increased by 138% whichreflects their participation in infrastructure and housingprojects.

The Labour Ministry has signed an agreement to allowSaudi women to work in lingerie shops. This willincrease the employment of Saudi women in the retailsector.

At 4.5% Y-o-Y, inflation is lower than the 5.0%recorded in 2011. This was almost entirely due to lowerincreases in food prices.

Saudi banks are currently enjoying near record levelsof profitability. Lending to the private sector is up by16% over the previous year. Real estate investmentsby Investment Funds have increased by 4% in 2012.

4

The Kingdom of Saudi Arabia is seeing an increased number of large mixed-use complexes, combining components ofoffice, retail, residential and hospitality use, with several such mega projects now underway in Riyadh, Jeddah andMakkah.

Jones Lang LaSalle are providing advice to clients on a number of these projects including Jabal Omar in Makkah (with37 hotels and 90,000 sq m. of retail floor space ) and the King Abdullah Financial District in Riyadh, the largest urbandevelopment currently under construction anywhere in the world with a project value close to USD 8 billion. The firstphase of the KAFD (comprising four office and four apartment buildings and a conference centre) is currently availablefor lease and will be completed in the summer of 2013.

As the Riyadh market becomes more competitive and occupiers have a greater choice of space, two factors that havepreviously been undervalued in the Saudi market are likely to become more important during 2013: environmentalsustainability; and the quality of property management.

Awareness of the benefits of more sustainable construction and operation of real estate remains at a nascent stage in theSaudi market. An indication of the increasing importance now being attached to this issue is the requirement that allbuildings in the new KAFD project must achieve LEED certification.

Recent green building codes and other initiatives by SEEC (the Saudi Energy Efficiency Centre) and others are alsostarting to raise awareness, but until developers are either mandated to adopt green standards (through stricterlegislation) or the financial benefits of green buildings can be more clearly demonstrated, progress is likely to remainlimited.

Incorporating Sustainability and Property Management into Mixed Use Projects in Saudi Arabia

5

Another trend that we are likely to hear more about is that of effective and pro-active property management as the qualityof property management is often a key influence on an occupier’s final choice of building.

Commercial occupiers are increasingly seeking to understand exactly what they will be getting from their landlord inrespect of the servicing and management of their highly specified new office buildings and whether they are getting valuefor money for the services provided. Driven by the desire of corporate occupiers to manage their total occupancy costsmore effectively, greater transparency of building operating costs will be demanded, especially in respect of the Kingdom’shigher quality developments.

There are three very good reasons why property owners should also address the on going management of their assets.Firstly the recognition that well managed buildings will generally lease up more quickly and maintain a better rental profile.Secondly, well managed properties tend to enjoy a higher retention of tenants over the life of the building. Thirdly, ownersare increasingly aware that ‘you cannot manage what you cannot measure’. Those landlords able to properly analyse thetrue financial performance of their assets and set service charges at a level that equates to operating costs, will reducethe risk of a shortfall between those operating costs and the service charge recovered.

As a result, we anticipate that best practice property management and carefully structured service charge clauses, willbecome more evident for prime properties across all real estate asset classes in Riyadh over the next few years.

Incorporating Sustainability and Property Management into Mixed Use Projects in Saudi Arabia (continued)

Talking Points – Q4 2012

Kingdom Holding has sold 970,000 sq m of the 16 million sq m of land in the Kingdom Residential City-Riyadh to Subul Development Co for SAR 250 million.

Damac has launched a luxury serviced apartment project, branded as Damac Esclusiva in Riyadh. This project comprises around 100 apartments designed by Fendi.

Fluor has been hired as consultant to oversee work on the 958km Jeddah to Riyadh rail link.

The Real Estate Development Fund (REDF) has approved USD 1.4 billion to finance around 12,500 homes across the Kingdom.

Contract awarded for USD 800m expansion of Riyadh’s King Khalid International Airport (KKIA). NACO, SADECO and HOK will design expansion of Terminals 3 and 4 which are expected to be completed by 2015.

King orders medical cities in Riyadh and Jeddah. Two new complexes to be built providing specialist healthcare for security forces and their families.

6

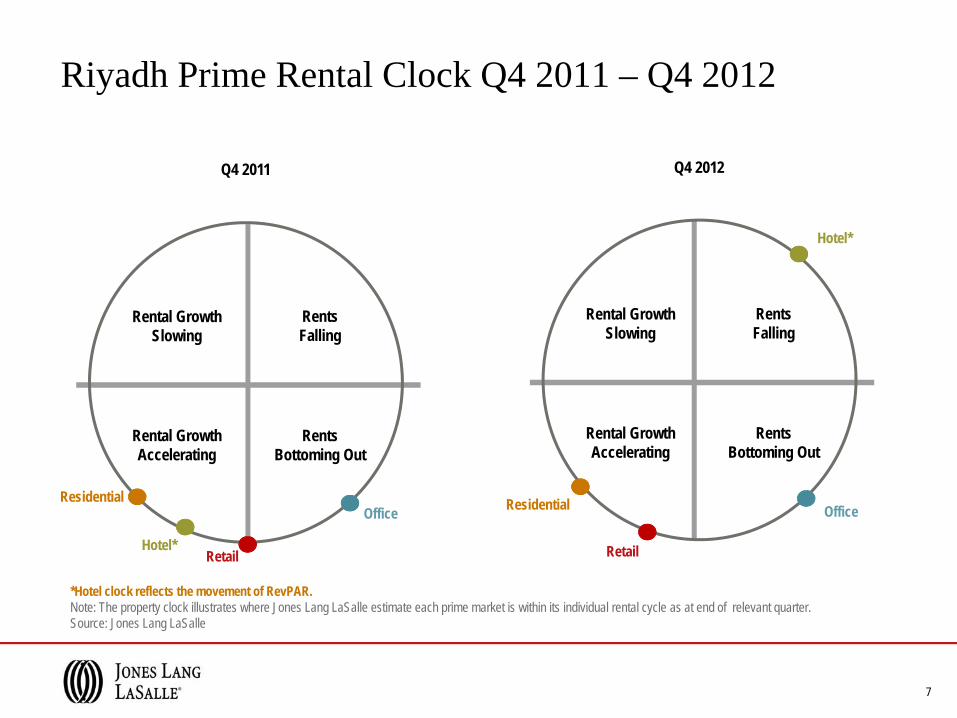

Riyadh Prime Rental Clock Q4 2011 – Q4 2012

*Hotel clock reflects the movement of RevPAR. Note: The property clock illustrates where Jones Lang LaSalle estimate each prime market is within its individual rental cycle as at end of relevant quarter.Source: Jones Lang LaSalle

Q4 2012

7

Q4 2011

Rental GrowthSlowing

RentsFalling

Rental GrowthAccelerating

RentsBottoming Out

Office

Retail

Residential

Hotel*

Rental GrowthSlowing

RentsFalling

Rental GrowthAccelerating

RentsBottoming Out

Office

RetailHotel*

Residential

Riyadh Market Overview

Office

King Abdullah Financial District

Office Supply and Demand

Source: Jones Lang LaSalle, Q4 2012

• Total stock of Grade A and B office space in locations monitoredby Jones Lang LaSalle remains at 1.9 million sq m, with nocompletions recorded in Q4 2012.

• Fifteen new buildings were completed during 2012, adding morethan 200,000 sq m of office GLA. The largest completion wasGOSI’s Granada Business Park (133,000 sq m), the majority ofwhich was pre-let to Government sector occupiers.

• Several new Grade ‘B’ buildings have completed on King FahdRoad and Olaya Street during 2012, but these have not enjoyedthe same pre-letting success. Many occupiers are seeking torelocate away from Olaya / King Fahd CBD as parking andaccess have become more of a challenge.

• During the fourth quarter, take up was led by the financial andengineering sectors that leased around 13,000 sq m of space.

• New supply will increase substantially in 2013, with thecompletion of initial phases of the King Abdullah Financial District(KAFD) and the ‘IT and Communications Complex’ (ITCC).GOSI’s Olaya Towers at the intersection of Tahlia and Olaya willalso add 100,000 sq m of efficient, high quality space in theCBD.

• More than 1 million sq m of new space is scheduled to bedelivered over 2013-14, but some of this space may be delayedas the market becomes oversupplied.

9

1,669 1,883 1,8832,490

3,029

607

539

296

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013 2014 2015

Total

Stoc

k (sq

m G

LA in

000's

)

Riyadh Office Stock (2011 – 2015)

Completed Stock Future Supply

10

Major Existing & Future Offices Projects

1

23

1

2

1 Faisaliyah Center

2 Kingdom Center

3 Tatweer Tower

1 KAFD

2 ITCC

Existing

Future

3 Olaya Towers

3

4

4 Tamkeen Tower

5

5 Granada Business Park

6

6 The Business Gate

4

4 MIG Tower

Office Rental Performance

• The average quoted rents for completed Grade A & B buildingsin Riyadh has declined marginally in Q4 to SAR 1,062 per sq mpa. due to higher vacancy in B grade buildings in the CBD andSouth of Riyadh.

• Quoted prime rents (for the best quality buildings) remainedunchanged at SAR 1,900 per sq m p.a., with the average forGrade A and Grade B buildings at SAR 1,305 and SAR 883respectively.

• Vacancy rates have increased in Q4, with city-wide and CBDvacancies at 16% and 18% respectively. There will be furtherupward pressure on vacancy rates over the next 12 monthsgiven the expected new supply entering the market.

• Given the increased competition to secure tenants, landlords willneed to look carefully at incentives and other terms to remaincompetitive.

• We expect that increased vacancy rates and the greater choiceavailable to tenants will maintain downward pressure on rentallevels during 2013, especially for Grade B properties.

11

SAR

per s

q m p.

a.Source: Jones Lang LaSalle, Q4 2012

Rental Performance (Q4 2011 – Q4 2012)

-

200

400

600

800

1,000

1,200

1,400

1,600

Average Grade A Average Grade B Average (completedGrade A and Grade B

buildings)

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

Indicator Level Comment / Outlook

Current Office Stock 1.9 million sq mIncludes Grade A, B & C space within major precincts (see definitionsfor further details). Total city-wide stock is estimated to be above 3million sq m GLA.

Future Supply (2012 – 2015) 1.44 million sq mThe Riyadh market will face a major supply shock over the next twoyears with the release of space in projects such as ITCC, KAFD andOlaya Towers.

City-wide VacancyCBD Vacancy

16%18%

Average Grade A Rental

Average – Grade B Rental

SAR 1,305 per sq m p.a.

SAR 883 per sq m p.a.

Office Market Summary

12

Riyadh Market Overview

Residential

Al Qasr Project

Residential Supply & Demand

14

Source: Jones Lang LaSalle, Q4 2012

• Approximately 6,000 residential units were completed in Riyadhin Q4. This brings the total residential stock in Riyadh to justunder 910,000 units. The majority of the recent supply has beendelivered in small projects comprising less than 20 units.

• The major new announcement in the fourth quarter was Kinan’sresidential project Masharef Hills located in the north of Riyadhwhich is expected to deliver more than 500 units over the comingfour years.

• An additional 100,000 units are due to enter the market from2013 to 2015, with annual supply of around 34,000 units.

• One of the more active developers is Al-Habib Group, which iscurrently building two residential projects. The first of these,Reem Residences, is expected to deliver 500 units by the end of2013.

• We are seeing an increase in the registration of off-plan salesprogrammes with the Ministry of Commerce.

• The Ministry of Housing is working on new regulations for leasinghousing. This will help standardize leasing contracts and create asystem to register these contracts.

• Approximately 6,000 residential units are expected to bedelivered in expatriate residential compounds over the next fiveyears. This new supply is likely to reduce the current upwardpressure on compound rents.

• Data released by SAMA shows the Real Estate DevelopmentFund disbursed more than SAR 11 billion in loans during thefirst half the 2012. These loans were granted to Saudi citizensto facilitate the building or purchase of new homes.

882909 909

940973

31

33

39

800

850

900

950

1,000

1,050

2011 2012 2013 2014 2015To

tal S

tock (

Numb

er of

units

in 00

0's)

Riyadh Residential Stock (2011 – 2015)

Completed Stock Future Supply

Major Existing & Future Residential Projects

1 Al Qasr Project

2 Balencya Project

3 Al Argan Project

1 Al Rabiah Project

2 Al Shams Arriyadh Project

3 Al Ghroub Project

4 Maskan Arabiah

4 Rafal Tower Project

1

1

2

3

2

34

4

Existing

Future

5 Akaria Village

6 Durrat Al Riyadh

56

• The average sale price of apartments has also increased indistricts to the East, South, and West of Riyadh during Q4 2012.

• The average asking price for new apartments increased 3%during Q4 to SAR 2,810 per sq m (excluding brandedapartments). Average prices will increase further once Al-Arganand Habib Group releases its apartments for sale.

• Al-Reem Residences and Phase 2 of Manazel Al-Qurtaba,currently under construction are expected to deliver around1,300 apartment units. Once complete these projects willprovide quality apartments for end users.

• Currently, most apartments available for sale are located in thelow income areas of Qurtaba, Yarmouk, in the East and Shifa,Badr, and Suwaidi the South.

• Average villa prices have increased across most districts ofRiyadh. The average price has increased by 2% in Q4 to SAR4,200 per sq m due to significant increases in the West andCentral districts.

• However, average prices in the Center of Riyadh have remainedunchanged in Q4 as most sales have been of older / refurbishedprojects due to the lack of new products available for sale.

• Malaqa, Yasmeen, and Sahfa in the North, Al-Hada andKhuzama in the West and Qurtaba and Ishbiliyah in the East areperceived as the most attractive locations for villas.

• The new concept of mixing apartments with villas through aseparate access is becoming more popular in low end districts tothe South and West of Riyadh.

Residential Sale Prices

Source: Jones Lang LaSalle, Q4 2012

16

Source: Jones Lang LaSalle, Q4 2012

SAR

per s

qm

SAR

per s

qm

2,0002,1002,2002,3002,4002,5002,6002,7002,8002,9003,000

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

Apartment - Average Price

3,600

3,700

3,800

3,900

4,000

4,100

4,200

4,300

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

Villa - Average Price

• Villas in residential expatriates compounds have shown a largerincrease in rents, reflecting the long waiting lists for access tothis kind of accommodation.

• The availability of new villas for lease is greatest in areas suchas Qurtaba and Monisia in the East , Malaqa, Sahfa and Yasminin the North.

• Villa occupancy in districts between North ring road and PrinceSalman street is increasing rapidly and expected to get moreattention from Saudi families when government offices movetowards the north of Riyadh.

• Villa rents have increased by 6% in Q4 2012 compared to thesame quarter last year. High income villas in the West andCentre have experienced greater increases than other districts.

• Rents in residential areas such as Olaya, Sulemania in thecenter and Hiteen and Nakheel in the west and Shumaisi in thesouth are higher than those in surrounding neighborhoods.

• Due to the preference for apartments in South, villa rents havenot increased much during the last year.

Rental Performance - Villas

Source: Jones Lang LaSalle, Q4 2012

17

SAR

p.a.

0

20,000

40,000

60,000

80,000100,000

120,000

140,000

160,000

180,000

North South East West Center

Villa - Average Annual Rent

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

• Apartment rents have increased at a higher rate than villas overthe past year, growing by 8% in the year to Q4 2012 and nowstand at approximately SAR 31,000 p.a. for an average 2 bed unit.

• Apartment rents in areas such as Wazarat and Malaz in the SouthOlaya in the Center, Diplomatic Quarter in the West and Yarmukand Qurtaba in the East are higher than those in other districts.

• Due to high occupancy rates, and the concentration of privateschools and hospitals, rents in areas such as Warooud, Malaz,Olaya and Sulaimania continue to grow at higher levels.

Rental Performance - Apartments

18

Source: Jones Lang LaSalle, Q4 2012

• Due to lack of labour accommodation within the industrial cities,districts like Batha, Manfoua, Khalediyah and Amal have highconcentration of apartment buildings used as laboraccommodation.

• The Government is planning to move the government officetowards the north while large expat schools are also movingnorth which will impact rents in the North and Centre.

SAR

p.a.

0

5,000

10,000

15,000

20,000

25,000

30,000

35,00040,000

45,000

North South East West Center

Apartment - Average Annual Rent

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

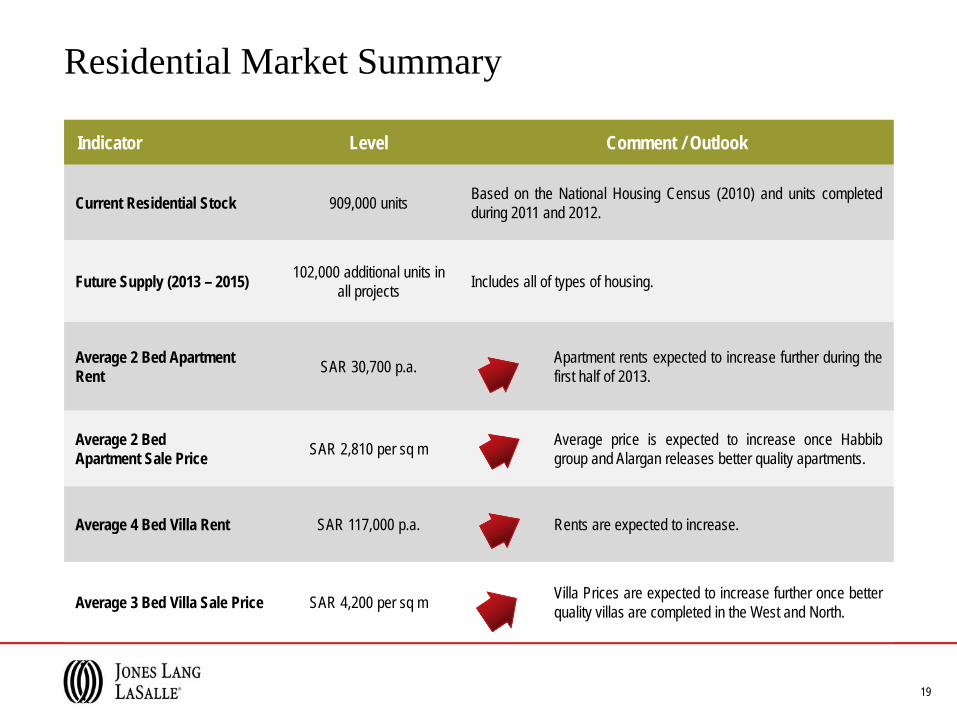

Residential Market Summary

Indicator Level Comment / Outlook

Current Residential Stock 909,000 units Based on the National Housing Census (2010) and units completedduring 2011 and 2012.

Future Supply (2013 – 2015) 102,000 additional units in all projects Includes all of types of housing.

Average 2 Bed Apartment Rent SAR 30,700 p.a. Apartment rents expected to increase further during the

first half of 2013.

Average 2 Bed Apartment Sale Price SAR 2,810 per sq m Average price is expected to increase once Habbib

group and Alargan releases better quality apartments.

Average 4 Bed Villa Rent SAR 117,000 p.a. Rents are expected to increase.

Average 3 Bed Villa Sale Price SAR 4,200 per sq m Villa Prices are expected to increase further once betterquality villas are completed in the West and North.

19

Riyadh Market Overview

Retail

Al Qasr Mall

Retail Supply & Demand

• There were no significant completions in Q4 2012 and the stockin major retail malls (those over 10,000 sq m in size) acrossRiyadh therefore remains unchanged at approximately 1.2 millionsq m.

• Outside of the mall sector, Othaim hypermarket in Laban areawas the major completion in Q4 2012 (approximately 2,000 sq mof GLA).

• Fawaz Al- Hokair is planning an aggressive expansion inRiyadh. In addition to Nakheel Mall, two other centers havebeen announced, which will add approximately 174,000 sq m ofGLA to their retail portfolio.

• Total mall based retail supply is expected to reach around 1.62million sq m by the end of 2015. This includes around 188,000 sqm of retail space in mixed use projects such as KAFD and ITCC.

• Lulu Hypermarkets are expanding their presence in Riyadh andare currently constructing their 4th store on Khurais road. Thisstore is expected to be completed in 2015.

• Shula community mall (one of oldest retail centers in Riyadh) hasbeen closed after a recent fire. The repositioning of nonperforming retail centers also continues. Part of the second floorof Sadhan Mall in Sulemania has been converted to office space.

21

Source: Jones Lang LaSalle, Q4 2012

1,138 1,214 1,214 1,332 1,498

118 166 123

0200400600800

1,0001,2001,4001,6001,800

2011 2012 2013 2014 2015

Total

Stoc

k ('00

0 sq m

)

Riyadh Retail Stock (2011 – 2015)

Completed Stock Future Supply

Major Existing & Future Retail Malls

1 Riyadh Gallery

2 Sahara Mall

3 Hayat Mall

4 Khurais Plaza

5 Al Otheim MAll2

13

6

4 5

786 Granada Mall

7 Rimal Center

8 Panorama Mall

Existing

Future1 KAFD Retail

1

9

9 Al-Qasr Mall

2

2 Nakheel Mall

Retail Rental Performance• Average retail rents have increased marginally (3%) in super

regional centres, while remaining unchanged in other centretypes during Q4. This has resulted in the average rent across alltypes of centres (super regional, regional and community malls)increasing slightly from SAR 2,520 per sq m in Q3 to SAR 2,562per sq m in Q4.

• Most of the super regional malls have high occupancy rates andrents are expected to continue to increase during 2013.

• However, we anticipate limited increases in average retail rentsin regional and community shopping malls given the availabilityof space and continued downward pressure on rentals in poorerperforming malls.

• There remains demand for retail space outside of organizedmalls. Standalone centers such as Nesto and Othaim haveopened on the Southern Ring Road and in Laban arearespectively. Their new supermarket is Othaim’s 55th store inRiyadh.

Source: Jones Lang LaSalle, Q4 2012

23

-

500

1,000

1,500

2,000

2,500

3,000

Super Regional Regional Community

SAR

/ sqm

Average Retail Rentals (Q4 2011 – Q4 2012)

Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012

Retail Sector Summary

Indicator Level Comment / Outlook

Current Retail Space* (GLA) 1.2 million sq m Existing stock within organised retail malls over 10,000 sq m GLA. Nonew completion in Q4 2012 in Riyadh.

Future Supply (2013 – 2015) 407,000 sq m KAFD and Nakheel Mall are the next major quality retail projectsexpected to be delivered in 2013 and 2014 respectively.

Average Estimated Rental Value SAR 2,562 per sq m p.a.

Average rentals for line stores in major malls have increased by 2% in Q4 2012.

Average Regional Mall Vacancy 10%Vacancies remained largely unchanged over Q4, ranging from 0-30% in major malls.

24

* Retail Supply comprises space within major malls over 10,000 sq m GLA

Riyadh Market Overview

Hotel

Ritz Carlton Hotel

Hotel Supply

• The total room supply in Riyadh as at end of 2012 was around8,400 hotel rooms.

• The fourth quarter of 2012 witnessed the opening of the IbisOlaya, which added 176 rooms to the city’s hospitality marketand introduced a major player in the branded midscale segment.

• Other hotels scheduled to open in end of 2012 such as HiltonGarden Inn and Holiday Inn projects have now been shifted into2013.

• Other announced projects scheduled for completion in 2013include the Movenpick, Fairmont, Hyatt Regency and CrownePlaza amongst others.

• The iconic Kempinski Burj Rafal is expected to open in mid2014. Upon completion this will be one of the highest towers inRiyadh and a landmark in the city.

• Recently announced projects include Sofitel and Four Points bySheraton. The existing Mena Plaza property has been rebrandedas a Suite Novotel from February 2013.

26

Source: Jones Lang LaSalle, Q4 2012

Riyadh Hotel Stock (2012 – 2015)

8,457 8,45711,057

13,557

2,600

2,500

2,300

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2013 2014 2015

No. o

f Roo

ms

Current Stock Future Additions

Hotel Performance

• The Riyadh hotel market has witnessed a continued softening inperformance over the fourth quarter of 2012 as arrival figureshave failed to keep pace with the significant increase in supplyrecorded in 2011.

• Occupancy levels declined to 57% during 2012, down from the62% achieved in 2011.

• Average Daily Rates (ADR) also declined by 4% (down to USD260) in 2012, reversing the increase witnessed during 2011.

• Falling occupancies and room rates resulted in RevPARdeclining (12%) from USD 169 in 2011 to USD 148 during 2012.

27

Source: STR Global

Riyadh Hotel Performance

249 267 253 270 260

71% 62%

60%

62%57%

0%

15%

30%

45%

60%

75%

200

220

240

260

280

2008 2009 2010 2011 2012

Occu

panc

y

ADR

(USD

)ADR Occupancy

Hotel Market Summary

28

Indicator Level Comment / Outlook

Current Hotel Supply 8,450 rooms After the addition of about 1,200 rooms in 2011, the only internationallybranded hotel to enter the market in 2012 was Ibis Olaya.

Future Supply (2013 – 2015) 7,400 rooms Some of the new supply scheduled to enter the market in 2012 has nowbeen shifted into 2013.

2012 (YT Dec) Occupancy 57% Decline in YTD levels of occupancy, reversing thepositive trend in 2011.

2012 (YT Dec) ADR USD 260The increase in supply in 2011 has placed downwardpressure on average rates. RevPAR also contracted (by12%) in 2012 compared to 2011.

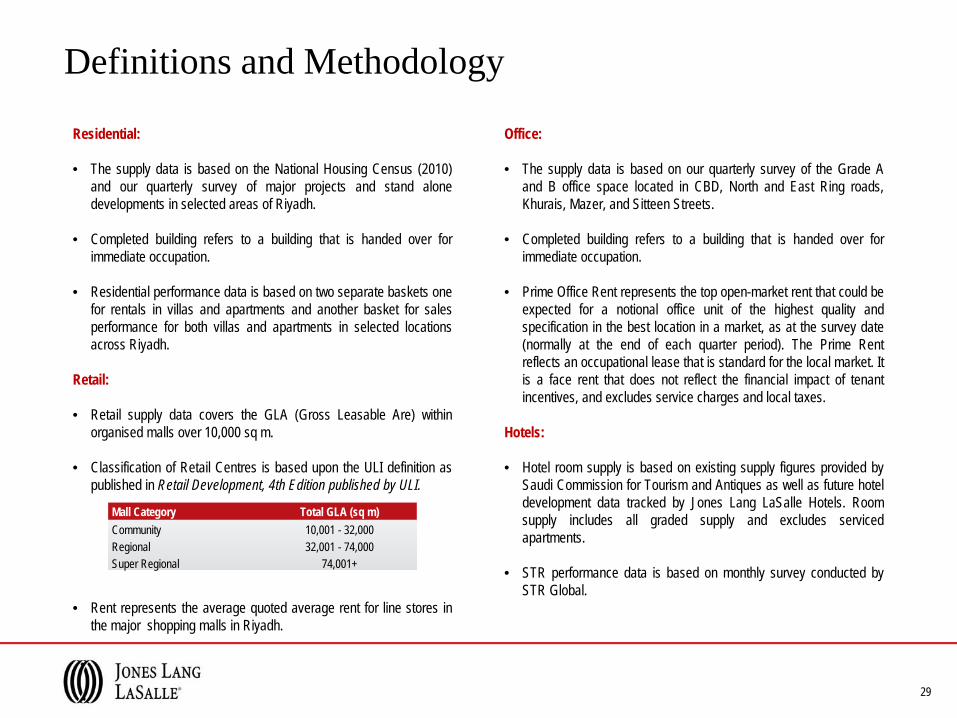

Definitions and Methodology

Residential:

• The supply data is based on the National Housing Census (2010)and our quarterly survey of major projects and stand alonedevelopments in selected areas of Riyadh.

• Completed building refers to a building that is handed over forimmediate occupation.

• Residential performance data is based on two separate baskets onefor rentals in villas and apartments and another basket for salesperformance for both villas and apartments in selected locationsacross Riyadh.

Retail:

• Retail supply data covers the GLA (Gross Leasable Are) withinorganised malls over 10,000 sq m.

• Classification of Retail Centres is based upon the ULI definition aspublished in Retail Development, 4th Edition published by ULI.

• Rent represents the average quoted average rent for line stores inthe major shopping malls in Riyadh.

Office:

• The supply data is based on our quarterly survey of the Grade Aand B office space located in CBD, North and East Ring roads,Khurais, Mazer, and Sitteen Streets.

• Completed building refers to a building that is handed over forimmediate occupation.

• Prime Office Rent represents the top open-market rent that could beexpected for a notional office unit of the highest quality andspecification in the best location in a market, as at the survey date(normally at the end of each quarter period). The Prime Rentreflects an occupational lease that is standard for the local market. Itis a face rent that does not reflect the financial impact of tenantincentives, and excludes service charges and local taxes.

Hotels:

• Hotel room supply is based on existing supply figures provided bySaudi Commission for Tourism and Antiques as well as future hoteldevelopment data tracked by Jones Lang LaSalle Hotels. Roomsupply includes all graded supply and excludes servicedapartments.

• STR performance data is based on monthly survey conducted bySTR Global.

29

Mall Category Total GLA (sq m)Community 10,001 - 32,000Regional 32,001 - 74,000Super Regional 74,001+

www.joneslanglasalle-mena.com

COPYRIGHT © JONES LANG LASALLE IP, INC. 2012This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the priorwritten consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation ismade, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not acceptany liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

John [email protected]

Gabriel MatarDirector, [email protected]

Peter [email protected]

Craig PlumbHead of [email protected]

David MacadamHead of [email protected]

Fayyaz AhmadAssociate Director, AdvisorySaudi Arabia [email protected]

Contacts: