Embed Size (px)

Citation preview

THE WATCH LIST NEWSLETTER 1

A WEEKLY COLUMN FOCUSING ON DISTRESSED MARKET CONDITIONS, COMMERCIAL REAL ESTATE PROPERTIES, MORTGAGES AND CORPORATIONS PUBLISHED BY COSTAR NEWS

IN THIS WEEK'S ISSUE:

Risky CRE Lending Deadly for Banks ................................................................................................................................................................... 1 Risky or Not, Lenders Slowly Opening Vaults to CRE Lending Again ................................................................................................................. 4 Simon Makes $10 Bil. Offer To Acquire General Growth Properties .................................................................................................................... 7 Multifamily REIT CEOs Upbeat on Apartment Prospects Despite Bleak Fundamentals ....................................................................................... 9 Lennar Acquires $3 Billion Distressed Loan Portfolio ......................................................................................................................................... 12 Walgreens Acquiring Duane Reade for $1.075 Bil............................................................................................................................................... 12 Getting Schooled .................................................................................................................................................................................................. 13 Brookfield Fund Picks Up Nearly 3 Mil-SF Portfolio From JPMorgan ............................................................................................................... 13 Real Money: Capital Raisings, Property Financings ............................................................................................................................................ 14 Loan Maturities .................................................................................................................................................................................................... 15 Specially Serviced Loan Volumes Quadruple ...................................................................................................................................................... 16 Watch List ............................................................................................................................................................................................................ 16

Risky CRE Lending Deadly for Banks FDIC Audits Point to Aggressive Lending, Poor Risk Management;

Congress Warns of Dangers to Banking System By: Mark Heschmeyer The autopsies of 16 bank fatalities completed this year have identified commercial real estate lending as the primary killer in more than half (nine) of the cases, and an accomplice in one other. In the seven cases in which CRE was not specified, the primary culprit for the bank failures was identified as lending for acquisition and construction of development projects. When the FDIC's Deposit Insurance Fund incurs a material loss at an insured depository institution, the FDIC Inspector General is required to make a written report identifying the causes of the loss. A material loss is defined as anything more than $25 million or 2% of an institution's total assets. In reviewing the 16 material loss reports completed this year on banks that all closed last spring and summer, it becomes clear just how much of a toll commercial real estate took on these financial institutions. The closing of those banks has resulted in losses so far for the FDIC of $2.34 billion. The 16 banks audited had total assets of $7.62 billion at the time they were shut down. They were based in states from coast to coast including: Washington, Wyoming, California, Nevada, Utah, Colorado, Texas, Illinois, Georgia and North Carolina. Last year in total, 140 banks failed with total assets of $170 billion. While the total cost to the Deposit Insurance Fund has not been tallied, losses have been averaging about 30% of assets. That would calculate to losses for the fund of about $52 billion for last year. "Federal Reserve examiners are reporting a sharp deterioration in the credit performance of loans in banks' portfolios and loans in commercial mortgage-backed securities (CMBS)," Jon D. Greenlee, associate director, Division of Banking Supervision and Regulation for the Federal Reserve Board, told the Congressional Oversight Panel at a Field Hearing in January. "Of the approximately $3.5 trillion of outstanding debt associated with CRE, including loans for multifamily housing developments, about $1.7 trillion was held on the books of banks and thrifts, and an additional $900 billion represented collateral for CMBS, with other investors holding the remaining balance of $900 billion." "Of note, more than $500 billion of CRE loans will mature each year over the next few years," Greenlee continued in his testimony. "In addition to losses caused by declining property cash flows and deteriorating

MARK HESCHMEYER, EDITOR WWW.COSTAR.COM/ FEBRUARY 18, 2010

THE WATCH LIST NEWSLETTER 2

conditions for construction loans, losses will also be boosted by the depreciating collateral value underlying those maturing loans. These losses will place continued pressure on banks' earnings, especially those of smaller regional and community banks that have high concentrations of CRE loans." The U.S. Congress created the Congressional Oversight Panel in the fall of 2008 to review the current state of financial markets and the regulatory systems overseeing them. The panel was empowered to hold hearings, review official data, and write reports on actions taken by Treasury and financial institutions and their effect on the economy. The Congressional Oversight Panel compiled extensive research and data on the state of commercial real estate and took comments from Greenlee and many others before issuing a 189-page report this past week entitled: Commercial Real Estate Losses and the Risk to Financial Stability. The report is starkly downbeat in its assessment of CRE risks on the banking system. "Over the next few years, a wave of commercial real estate loan failures could threaten America‘s already-weakened financial system. The Congressional Oversight Panel is deeply concerned that commercial loan losses could jeopardize the stability of many banks, particularly the nation‘s mid-size and smaller banks, and that as the damage spreads beyond individual banks that it will contribute to prolonged weakness throughout the economy," the report concluded. Between 2010 and 2014, about $1.4 trillion in commercial real estate loans are expected to reach the end of their terms. By Congressional Oversight Panel estimates nearly $700 billion of that debt is presently 'underwater,' a situation in which the borrower owes more than the current value of the underlying property. "It is difficult to predict either the number of foreclosures to come or who will be most immediately affected," the report concluded. "In the worst case scenario, hundreds more community and mid-sized banks could face insolvency. Because these banks play a critical role in financing the small businesses that could help the American economy create new jobs, their widespread failure could disrupt local communities, undermine the economic recovery, and extend an already painful recession." The problems facing commercial real estate have no single cause, according to the Congressional Oversight Panel. The loans they identified as most likely to fail were made at the height of the real estate bubble when commercial real estate values had been driven above sustainable levels and loans. The panel also noted that many loans were made carelessly in a rush for profit. Other loans were potentially sound when made but the severe recession has translated into fewer retail customers, less frequent vacations, decreased demand for office space, and a weaker apartment market, all factors that increased the likelihood of default on commercial real estate loans. Even borrowers who own profitable properties may be unable to refinance their loans as they face tightened underwriting standards, increased demands for additional investment by borrowers, and restricted credit. The FDIC material loss reports also made it clear that most of the failed banks were either too aggressive in growing their commercial real estate lending portfolios and/or too ill prepared to manage the consequences. Specifically the FDIC auditors questioned the banks' loan underwriting standards on chasing deals either out of their territories or not consistent with their business plans. Those actions, in turn, prompted banks to pursue risky transitory and costly deposits to fund their growth. The following is a summary of the reports examining the 16 banking failures. New Frontier Bank, Greeley, CO; $1.8 bil. in assets. New Frontier failed because its board and management did not implement adequate risk management practices pertaining to rapid growth and significant concentrations of residential acquisition, development and construction (ADC) and agricultural loans. First Bank of Beverly Hills, Calabasas, CA; $1.3 bil. in assets. First Bank failed because its board and management did not adequately manage the risks associated with the institution's heavy concentrations in commercial real estate (CRE) and ADC loans and investments in mortgage backed securities (MBS).

THE WATCH LIST NEWSLETTER 3

Cooperative Bank, Wilmington, NC; $973.6 mil. in assets. Cooperative Bank failed because its board and management did not adequately manage the risk associated with the institution's aggressive real estate lending, particularly in the area of residential. Strategic Capital Bank, Champaign, IL; $537.1 mil. in assets. Strategic Capital's failure can be attributed to the board and management's speculative and ill-timed growth strategy involving high-risk assets and volatile funding. Strategic Capital's rapid growth strategy was in contravention to long-standing supervisory guidance related to CRE concentrations and securities. Cape Fear Bank, Wilmington, NC; $466.8 mil. in assets. Cape Fear failed because its board and management did not implement effective risk management practices pertaining to rapid growth and significant concentrations of CRE and ADC loans. Mirae Bank, Los Angeles, CA; $410 mil. in assets. Mirae failed because its board and management pursued an aggressive growth strategy centered in CRE lending and failed to ensure sound loan underwriting practices. Southern Community Bank, Fayetteville, GA; $380.6 mil. in assets. Southern Community failed because of a rapid deterioration in asset quality that led to loan and operational losses that quickly eroded the bank's capital. The majority of Southern Community's lending was in CRE, with a particular focus on ADC loans. Westsound Bank, Bremerton, WA; $324.1 mil. in assets. Westsound failed because its board and management did not implement risk management practices commensurate with rapid asset growth and a loan portfolio with significant concentrations in higher-risk ADC loans. America West Bank, Layton, UT; $310 mil. in assets. America West Bank failed because the bank's board and management deviated from the bank's business plan and did not effectively manage the risks associated with rapid growth in CRE and ADC lending. FirstCity Bank, Stockbridge, GA; $291.3 mil. in assets. FirstCity failed because its board and management pursued a strategy of aggressive growth centered in ADC lending. Great Basin Bank, Elko, NV; $228.8 mil. in assets. Great Basin failed because its board did not ensure that bank management identified, measured, monitored, and controlled the risk associated with the institution's lending activities. The institution's loan portfolio included, but was not limited to, out-of-territory purchased participation loans from areas that experienced a significant economic downturn starting in 2007, and a concentration in CRE loans. Bank of Lincolnwood, Lincolnwood, IL; $217.4 mil. in assets. Lincolnwood failed because the bank's board and management did not implement adequate risk management practices pertaining to a significant concentration in ADC loans. Millennium State Bank, Dallas, TX; $121.4 mil. in assets. MSB's failure can be attributed to inadequate management and board oversight, an aggressive growth strategy centered in CRE lending, weak loan underwriting and credit administration, poor earnings, and an inadequate funding strategy. American Southern Bank, Kennesaw, GA; $113.4 mil. in assets. American Southern failed because its board and management materially deviated from its business plan by pursuing a strategy of growth centered in ADC lending. MetroPacific Bank, Irvine, CA; $75.2 mil. in assets. MetroPacific, a de novo bank, failed primarily because it lacked stable and consistent management and oversight as a result of significant turnover in key management positions. The bank's board and management were particularly ineffective in implementing risk management practices pertaining to adherence to the bank's business plan and rapid growth and concentrations in CRE and ADC loans. Bank of Wyoming, Thermopolis, WY; $72.8 mil. in assets. The Bank of Wyoming's failure can be attributed to the board and management's pursuit of loan growth funded significantly with brokered and other non-core

THE WATCH LIST NEWSLETTER 4

deposits. The bank's loan portfolio was concentrated in CRE and ADC loans made to out-of-area borrowers, obtained through loan brokers and participations purchased.

Advertisement

Risky or Not, Lenders Slowly Opening Vaults to CRE Lending Again By: Mark Heschmeyer Even as banking regulators and politicians deal with the fallout from the collapse of commercial real estate values and the subsequent impact on the banking systems, it appears that an increasing number of lenders are more inclined to jump back into the sector. Total renewals of existing commercial real estate accounts increased 57% from November to December of last year, according to numbers released this week by the U.S. Department of Treasury. Treasury completes a monthly tally of lending activity of the nation's 20 largest bank, which control 57% of all U.S. banking assets. While seasonality contributed to the increase -- as year-end is an active time for renewals -- new lending also more doubled in December from the previous month. Total new commercial real estate commitments increased 157%. That was the first increase in four months. Citigroup's new CRE lending increased eightfold in December to $294.4 million. Loan renewals more than doubled to $282.3 million, reflecting an increase in capital‐raising activities by real estate investment trusts,

Citigroup said. Even with new and renewals increasing, the big banks also increased their disposal of CRE assets on their books. Citigroup noted, for example, that its average total CRE loan and lease balances totaled $22.8 billion at

THE WATCH LIST NEWSLETTER 5

the end of December, 3% lower than it was in November. The outstanding balance of CRE loans of all respondents fell 1% in December, and the median change in outstanding balances was a decrease of 1%. Fifth Third Bancorp's average CRE balances decreased by approximately 1.3% in December compared to November. New CRE commitments originated in December 2009 were $196 million, which was up almost 50% from $132 million in November 2009. Renewal levels for existing accounts increased significantly in December 2009 to $1.2 billion versus November 2009 at $471 million due to normal year-end seasonal trends. Even though Fifth Third's combined originations and renewals were higher in December than November, payments and dispositions of troubled CRE outpaced the higher levels of activity causing the overall balances to continue to decline. As commercial vacancy rates continue to rise, Fifth Third said it continues to monitor the CRE portfolios and continues to suspend lending on new non‐owner occupied properties and on new

homebuilder and developer projects in order to manage existing portfolio positions. "We feel this is prudent given that we do not believe added exposure in those sectors is warranted given our expectations for continued elevated loss trends in the performance of those portfolios," Fifth Third reported.

OTHER BANKS FOLLOW LEAD

What is happening among the majors also seems to be the route other banks say they will be more willing to take this year. According to findings from Jones Lang LaSalle's annual 2010 Lenders' Production Expectations Survey, bankers are predicting that loan production will increase this year. The number of respondents that said they expect their loan production to range from $2 billion to $4 billion in 2010 doubled from last year to 43%. Showing even more future optimism, nearly 70% of respondents said their loan production will ramp up to $2 billion to 4 billion in 2011. In another encouraging metric, the number of lenders that expect to lend more than $4 billion jumped up 6% from 9.3% in 2009 to 15.2% in 2010. "Lenders we spoke with say they'll be giving borrowers 24+ month extensions in order to avoid foreclosure on high quality, well-located assets," said Bart Steinfeld, Jones Lang LaSalle's managing director of the real estate investment banking practice. "With more than $1 trillion worth of commercial real estate loans expected to mature between now and 2013, it's no surprise that a majority of borrowers are placing significant importance on restructuring those loans. However, many financial institutions don't want to hold on to assets and now are coming to terms with the fact that they can no longer 'extend and pretend.' They're now realizing it makes good sense to move these assets off their balance sheets to create greater ability to originate loans this year." The number of lenders willing to lend greater sums toward single-asset acquisitions is also shifting. In 2009, the majority of respondents indicated they would lend only $10 to 25 million on a single asset acquisition. In 2010, the greatest percentage of respondents was split evenly at 28% each among those willing to lend $50 million to $100 million and $100+ million (hence 56% will lend $50 million and more for single-asset purchases). In 2011, the number of lenders willing to lend $50 to $100+ million rises by 8% to 64% of respondents. "A few life companies and investment banks we spoke with indicated that they're willing to lend $150 [million] to $500 million on large, single-asset acquisitions in 2010," said David Hendrickson, managing director of Jones Lang LaSalle's real estate investment banking practice. Approaching maturities will continue to share the stage in 2010, with more than 67% of life company respondents acknowledging 40% to 60% of their portfolios will be allocated to the refinancing of maturing loans. While liquidity within the capital markets is expected to turn from a trickle to a slow-but-steady flow in 2010, borrowers can expect the same tightened underwriting standards they experienced from life company lenders in 2009. Loan to value ratios in 2010 will fall predominantly in the 50% to 70% range, according to more than 74% of life company respondents, and that number is expected to remain steady in 2011. As for new conventional commercial real estate loans in 2010, 59% say most loan terms will range five years or greater, with an additional 28% indicating a preference for three to five year terms.

THE WATCH LIST NEWSLETTER 6

As for the sectors that lenders would most prefer to lend, a majority of respondents (27%) said they would single out multifamily for their loan dollars, while another 21% said they would focus on the office sector in 2010. The hotel sector stood out as the sector to which lenders are least likely to lend. There was a significant increase in the number of lenders who said they are selling performing and non-performing loans. In addition, these lenders said they are prepared to accept significant discounts in 2010 to create liquidity and to rid themselves of these non-core or problem assets. For performing loans, 29% of respondents indicated they are selling performing notes at 90 cents on the dollar and another 24% are selling performing loans between 70 cents and 80 cents on the dollar. "There is also increased interest in selling sub-performing, or "scratch and dent" loans," said Noble Carpenter, managing director of Jones Lang LaSalle's real estate investment banking practice. "Depending on the remaining term, interest rate, property type and market, over 45% of survey respondents indicated a willingness to sell these loans below 0.60 cents on the dollar. Many lenders also said they have started or are considering asset, REO and loan sales. "We're definitely seeing the bid-ask spread between buyer and seller narrow, and in many cases reach equilibrium. That alignment should be the impetus many lenders need to bring large and small balance loans and REO to market," added Wes Boatwright, managing director of Jones Lang LaSalle's real estate investment banking team.

Advertisement

THE WATCH LIST NEWSLETTER 7

Simon Makes $10 Bil. Offer To Acquire General Growth Properties By: Sasha M. Pardy

The country's largest retail property owner has made a bold move to acquire its largest single competitor, General Growth Properties (GGP). On the morning of Feb. 16, 2009, Simon Property Group (NYSE:SPG) announced that it has offered to acquire GGP for $10 billion in a fully financed transaction that would include $9 billion in cash. Under terms of the offer, GGP shareholders would receive $6 per share in cash, plus a $3 per share distribution from GGP for the company's master planned community division. Simon's offer includes the pay off of $7 billion in claims owed to GGP's creditors, bond and note holders. GGP shareholders and creditors would be given the option to either receive the payouts or convert it to Simon common stock. Simon said the transaction would be financed through Simon's cash on hand, its existing credit facilities and equity co-investments from strategic institutional investors. The REIT believes it could complete due diligence within 30 days, but the deal would also be subject to customary bankruptcy court and creditor approvals. "Our offer provides much-needed certainty to conclude General Growth's protracted reorganization process," said Simon's chairman and CEO, David Simon. "We are confident it is far superior to any other third-party proposal or stand-alone plan that could be completed." General Growth issued a public response to Simon's offer late on Feb. 16, saying "we appreciate your interest and we recognize the potential value that Simon could bring as an option for the company to emerge from Chapter 11," wrote CEO Adam Metz. However, GGP is not about to take Simon's offer as it stands now. "We have concluded, based on discussions with other interested parties, that [Simon's offer] is not sufficient to preempt the process we are undertaking to explore all avenues to emerge from Chapter 11," Metz wrote. GGP has invited Simon to participate in the company's process, including providing access to needed information so that Simon "may evaluate [it's] indication of interest in the context of other strategic options." According to the Wall Street Journal, General Growth has also been negotiating with Brookfield Asset Management. In December, news surfaced that Brookfield had purchased close to $1 billion of General Growth's unsecured debt, which means it has a say in any restructuring of GGP's $7 billion in unsecured debt. In the latest reports, Brookfield may offer to provide General Growth with billions of dollars in capital to facilitate its emergence from bankruptcy, which could end up with GGP becoming an independent company with Brookfield as a major shareholder. "Full cash payment to all unsecured creditors and the substantial recovery for equity holders that Simon has proposed would be a great result," said Michael Stamer, counsel for the Official Committee of General Growth's Unsecured Creditors. "We fully support and encourage prompt engagement by the company with Simon." Simon said that it announced the $10 billion offer publicly because it did not hear back from GGP since it made the proposal to the retail property owner more than one week earlier. Substantive rumors that Simon intended to make a bid for General Growth first surfaced in November 2009. In its proposal letter to GGP, Simon said that it believes GGP's current trading value already includes a "takeover premium" and added that its "high percentage of insider ownership and the fact that the stock trades in an over-the-counter securities market, reflects a price that cannot be realized in a standalone reorganization." Simon also said it believes that GGP's reorganization plan has a "highly uncertain outcome" that could only be achieved over a lengthy amount of time at "considerable additional expense" and may result in "significant dilution of the current equity holders." The latest update on General Growth's reorganization came on Jan. 25th. The mall landlord said that 180 of its subsidiary debtors owning 96 properties had emerged from bankruptcy and it hired UBS Bank to assist in

THE WATCH LIST NEWSLETTER 8

evaluating potential financial transactions for its emergence from Chapter 11. At the time, GGP expected restructuring of 16 remaining loans totaling $2.1 billion to be complete "in the next few weeks." Indianapolis-based Simon currently owns, or has an interest in, 382 properties totaling 261 million square feet in North America, Europe and Asia. As of Feb. 3, Chicago-based General Growth's retail portfolio consisted of 200 regional shopping malls in 43 states totaling 200 million square feet. A merger of the two mall owners would further solidify Simon's ranking as the country's largest retail property owner and dwarf others in the industry. The next-closest would be Developers Diversified, which currently owns 665 retail properties in 44 states, Brazil, Canada and Puerto Rico, totaling more than 147 million square feet. Most of DDR's properties are not malls, however. The next-largest mall owner would be CBL & Associates -- its portfolio includes 163 properties, including 88 regional malls, in 27 states and totaling 87.8 million square feet. Lazard Ltd., J.P. Morgan and Morgan Stanley are acting as financial advisors to Simon; while the Wachtell, Lipton, Rosen & Katz firm is serving as legal advisor. Simon cited its "unmatched track record of completing large and successful acquisitions" as a testament to its ability to be able to complete this $10 billion acquisition successfully. This spring, Simon expects to close on its $2.325 billion acquisition of the Lightstone Group's Prime Outlets business (for more on that, follow this link). Simon is already the largest outlet shopping center owner in the country -- its Chelsea Premium Outlet Division operates 41 outlet centers in the U.S. and overseas. The acquisition of Prime Outlets would add 22 more outlet centers to its portfolio. Simon acquired Chelsea in late 2004 in a $4.6 billion deal. On April 3, 2007, Simon, with partner Farallon Capital, closed on its $8 billion acquisition of The Mills Corporation, taking on 20 regional malls and 17 lifestyle centers totaling 45 million square feet. Simon beat out Brookfield Asset Management in its bid to acquire the near-bankrupt Mills. Several assets in the Mills' portfolio were underperforming and Simon continues to work on adding value to many of them.

COMMENTARY FROM EXECUTIVES AND ANALYSTS

Jeffrey Spector, REIT research analyst for Bank of America - Merrill Lynch, said in a note that Simon's current offer would approximate an 8.% capitalization rate and also said that the $3 per share Simon offered to pay for General Growth's Master Planned Community assets implied a 40% cut to book value. Spector said he wouldn't be surprised if another bid surfaces for GGP; but he also expects that Simon would not hesitate to counter. "Given SPG's existing infrastructure advantages and their likely desire to prevent another player from entering the US mall space, we believe SPG may be less price-sensitive than other bidding peers." According to Spector, Simon currently has a 15% share of all malls in this country, while GGP has a 14% share -- put them together and the result would have Simon owning 30% of all U.S. malls. Further, Spector said he believes the combined company would own almost half of the nation's Class A malls. "The increased scale would provide SPG with more negotiating power with tenants, as well as greater control, and the ability to optimize mall positioning in key markets, where the portfolios overlap." Greg Maloney, president and CEO of Jones Lang LaSalle Retail shared with CoStar his opinion on what a Simon acquisition of GGP could mean for the retail real estate industry, as well as retailers. Above all, Maloney debunks several analysts' comments that Simon's would-be ownership of one-third of the nation's malls would adversely impact retailers or result in Simon exercising increased negotiating power or control over tenants. "When you're as large as Simon is now…what's another 200 malls? I don't think Simon would turn all the malls into boilerplate 'Simon' malls," said Maloney. Simon would still abide by the basic principles of retail real estate, said Maloney, "They still would have to provide a center where consumers and retailers can thrive." Regarding the impact on retailers, Maloney said "It goes both ways," explaining that in general, large retailers would remain on a level negotiation playing field with Simon, as a retailer with 200 stores in Simon's portfolio

THE WATCH LIST NEWSLETTER 9

means just as much to Simon as it does to the retailer. Plus retailers are much more savvy today than they were years ago, said Maloney, "they understand that in order to go into any location, regardless of the landlord, it has to make financial sense above all else." What will really be interesting if this acquisition were to occur, said Maloney, is how Simon will handle overlaps of malls in certain markets. "I think there's going to be a lot of overlaps, which could be a positive for the industry if it generates some sales of shopping centers, which would hopefully get contagious," said Maloney. "There are a lot of people sitting on the sidelines with cash that are waiting for things to get better. A lot of product potentially coming on the market is probably the most intriguing thing about this deal to me," he added. Maloney speculates that in markets where Simon has two Class A malls that overlap, it would likely keep both; but in markets where a B mall overlaps with an A, the B mall would most likely get sold. Does Maloney think a counter-bidder could win out over Simon? "There are probably groups out there trying to put together a better offer. But I am sure Simon has a plan and they're going to argue they could out-lease anyone," said Maloney. Additionally, he reminded us of Simon's efforts to buy out Taubman a while back and said the fight was interesting, but in the end, Simon didn't win. In Simon's initial statement, the REIT said "equity co-investments from strategic institutional investors" are involved in its offer, however, Rich Moore, an analyst at RBC Capital Markets said in a note that those investors may have more involvement in the deal than Simon inferred. "We spoke with Simon management regarding the transaction. Simon plans to do a joint venture with institutional investor partners. We would expect something in the range of a 50/50 venture," said Moore in a note. Moore said that while alternative bids are likely to emerge in this process, the likelihood of a competitor being able to outbid Simon is low, so he doesn't expect those proposals to be meaningful. In a phone interview with CoStar, Moore referenced Brookfield's attempt to buy the Mills in 2004 and said that it would likely make play against Simon this time around as well. "Simon did not get involved in the Mills transaction until the end; but once they did, no one else did. No one can run these malls as well as Simon. In the end, when David Simon wants it, you have to figure he can bid high enough to buy it. Simon has put together a pretty complete package and I think it's a very fair price," said Moore. He expects GGP and Brookfield to try to work together in an alternative transaction. "In the end, it's hard to believe that would be as attractive as Simon with its amazing balance sheet," said Moore. "We have long felt Simon would be the eventual acquirer of GGP given the synergies of adding class A malls to an already high quality mall portfolio," said Moore. If Simon does end up the ultimate owner of GGP malls, Moore commented, "For the mall business, it would be a huge sea change for retail. Simon would control about one-third of the malls and most would be high quality. Retailers would be forced to deal with Simon at a greater degree, so there would be much more leverage." "Simon is a leader in the mall business," Green Street analyst Jim Sullivan said in an interview with the Wall Street Journal. "Buying General Growth in one bite would take them from leader to dominant player. That's the legacy that I think is attracting [David Simon's] interest." Green Street estimates that of the 307 U.S. malls rated as Class A (sales per square foot of $400+), Simon owns 71 and GGP owns 77, which would have the resulting company owning nearly half of the country's top malls. Sullivan also expects that Simon would likely shed many of the lower quality GGP assets post-merge.

Multifamily REIT CEOs Upbeat on Apartment Prospects Despite Bleak Fundamentals

By: Randyl Drummer Even as apartment rents continue to erode, vacancies remain at historic highs and prospects for recovery unlikely until next year, executives for the nation's largest publicly traded apartment companies sounded a note of optimism during the latest round of earnings conference calls, believing that the worst of the pain has already passed.

THE WATCH LIST NEWSLETTER 10

Most predicted slow and steady, if unspectacular, improvement in fundamentals over the course of 2010, though the path to recovery will be bumpy. "Management teams are sporting a new cloak of optimism, although it is heavily footnoted," said Citi REIT analyst Michael Bilerman in a research note. Some companies, such as AvalonBay Communities and Equity Residential based their optimism on capital raising, acquisition, development and other growth plans. Others, such as Camden Property Trust are holding back, shelving their 2010 development plans while deleveraging and charging off losses and impairments to their land and portfolios. Most companies said they are trying to boost occupancy by lowering rents, trading lower net operating income (NOI) in hopes of holding the line on vacancies during the current wave of job losses that has thinned the ranks of renters, especially among "echo boomers" in their 20s and 30s who are opting to double up with roommates or live with their parents. Just as their office and retail counterparts are doing, apartment companies are giving renters the upper hand. Meanwhile, the long-expected flood of distressed property sales hasn't yet materialized, with deals held back by limited financing availability and low interest rates that have mostly allowed borrowers to continue to service their loan debt, even though many of those loans are under water. For now, apartment executives are hanging their hopes on the unprecedented slowdown in housing construction, and the sheer numbers of the echo-boom generation, second in size only to the baby boomers, which they say point to strong expected rent growth starting in 2011, according to Marcus & Millichap's 2010 National Apartment Report. "It is simply a matter of time before an expanding economy releases this powerfully favorable demographic into the renter pool," said Marcus & Millichap President Harvey E. Green and Managing Director Hessam Nadji, authors of the report.

ACQUISITIONS: BACK ON THE RADAR SCREEN FOR SOME

After dropping about 70% from the peak, confidence and investment activity began to stir modestly in the second half of 2009 and into 2010. Private local buyers account for most of the activity, but REITs and institutions that have built-up capital are expected to continue targeting large properties in major markets this year. The largest apartment REIT, Equity Residential, has been first out of the gate. EQR earlier this month acquired two luxury apartment complexes in Manhattan from Macklowe Properties, River Tower and 777 Sixth Street, and signed a contract for a third, the Longacre House, for more than 900 units in deals totaling $475 million. EQR, headed by billionaire Sam Zell, also in the fourth quarter closed its purchase of Metropolitan at Pentagon Row, a 326-unit apartment complex in Arlington, VA, from joint venture partners Cornerstone Real Estate Advisers and Kettler for $100 million, according to CoStar information. The company has also acquired two other high-rises in Arlington and mid-rises in Seattle and Del Mar, CA, according to EQR President and CEO David Neithercut. "This is all good news for the apartment business," Neithercut told investors earlier this month. "I'm not suggesting that we're experiencing any kind of sharp inflection here. I would rather say we think we are at the beginning of a period of slowly, and I do mean slowly, improving fundamentals. But … if you add job growth to that picture, we believe that will quickly turn into one of the best operating periods in our history." The cautious return of large investors may signal a shift in strategies from wait-and-see to bargain-hunting. Some believe values have dropped sufficiently to encourage investors to resume acquisitions in stronger metros and submarkets rather than risk missed opportunities by attempting to time the absolute bottom of the market. "Visions of quality assets coming to market at fire-sale prices will continue to fade, and buyers and sellers will move closer to redefining fair value based on true assessments of quality and risk," Green and Nadji said in their report. "More distress is sure to come to market, but the quality will be highly mixed as lenders avert further losses by avoiding foreclosure on performing assets and those with reasonable prospects for stabilization."

THE WATCH LIST NEWSLETTER 11

REITs aren't the only buyers gearing up for future investments. Private local investors who liquidated their holdings at a tidy profit in the mid-2000s are coming back as buyers, Marcus & Millichap said. In what may be "the clearest signal yet that prices have adjusted to levels that can be sustained," such smaller investors recently have accounted for 82% of the dollar value in the current acquisitions pool, compared with 37% at the peak four years ago.

NEW DEVELOPMENT ON HOLD

The majority of apartment companies have chosen to either cancel or scale back their 2010 development plans, according to a survey of company earnings statements and conference calls. Developers delivered just 94,000 units in 2009, according to Marcus & Millichap, a number expected to drop even lower this year, a level expected to be the lowest level since 1995. New construction starts have fallen to a 15-year low, with new development constituting just 0.5% of existing inventory. Fitch Ratings recently maintained a stable outlook for multifamily REITs in 2010 due to this limited supply, along with continued access to low-cost financing from government-sponsored entities Fannie Mae and Freddie Mac. The construction pause, along with a population surge among renters forming new households over the next three years, is expected to drive down vacancies and offer the opportunity to raise rents. With these numbers in mind, AvalonBay, unlike some of its rivals, said it remains committed to delivering new product. "Given greater visibility now for both the economy and capital markets and our positive outlook regarding the fundamentals in late 2011 and 2012, we will be increasing our acquisition, free development and development volumes this year to position us for the projected improvement in fundamentals," said AVB Chairman and CEO Bryce Blair. "We do intend to start some new developments in 2010 although the amount should be modest by historical standards upon the order of $400 million," added President Tim Naughton. "Most of the activity is likely to occur in the northeastern suburban markets where market conditions are more stable and wood frame communities offer better projected returns. In addition we are beginning to look at new land opportunities as some land owners and lenders are starting to consider disposing of their holdings and many of our competitors remain on the sidelines." The prospects for a recovery come as apartment vacancies hit a 30-year high in the fourth quarter, and rents fell 3% last year as landlords scrambled to retain existing tenants and attract new ones. Rising unemployment contributed to a more than 3% decline in asking rents in 2009, while effective rents fell nearly 6% and concessions rose. Landlords quickly cut rent in the first half of 2009 and concessions have become commonplace in formerly torrid housing markets, such as Fort Lauderdale, Las Vegas, Miami, Orlando, Phoenix, the Inland Empire, Sacramento and Tampa-St. Petersburg possibly reflecting increased competition from the single-family and condo "shadow" market.

GSES TO THE RESCUE

At the end of last year, 4.9% of CMBS were delinquent, a five-fold increase over the year before, Moody's Investors Service said last month. The Moody's "delinquency tracker" found that more than 8% of the bonds for apartment loans and more than 9% of bonds for hotel mortgages were delinquent. In another black-eye for the industry, multifamily is at the center of one of the biggest commercial real estate deals to come undone so far, the default on the debt used to finance the $5.4 billion purchase in 2006 of the massive Peter Cooper and Stuyvesant Town apartment community in Manhattan. The 11,000-unit property is now valued at less than half its purchase price. However, agency funding has likely helped stave off even higher multifamily delinquency rates. Fannie Mae and Freddie Mac dominated multifamily financing last year. Financing 81% of all multifamily activity based on Freddie Mac's accounting for a combined $36.4 billion. See related story in Watch List: "Fannie, Freddie Grabbing Ever-Higher Share of Multifamily Debt Financings"

THE WATCH LIST NEWSLETTER 12

The agencies' commercial loans have been among the best performing assets in their portfolios, and GSEs should remain the primary sources of financing for apartment investors, according to Marcus & Millichap. Beyond that, the lending climate for apartments will remain constrained and underwriting standards will be conservative in 2010: investors should expect loan to values to stay within the 55-75% range, M&M said.

Lennar Acquires $3 Billion Distressed Loan Portfolio By: Mark Heschmeyer Lennar Corp. in Miami, FL, closed on the purchase of two structured loans transactions with the FDIC. The transactions represent the purchase of two portfolios of loans with a combined unpaid balance of $3.05 billion. Lennar acquired indirectly 40% managing member interests in the limited liability companies created to hold the loans for $243 million (net of working capital and transaction costs), including up to $5 million to be contributed by its subsidiary Rialto Capital Advisors. The FDIC is retaining the remaining 60% equity interest and is providing $627 million of non-recourse financing at 0% interest for seven years. The transactions include 5,500 distressed residential and commercial real estate loans from 22 failed bank receiverships. Rialto Capital is a real estate investment management company focused on distressed real estate asset investment, management and workouts. Rialto will conduct the day-to-day management and workout of the portfolios. "Acquiring and working out distressed real estate loans was a large and extremely profitable part of our business during the last major real estate down cycle in the early 1990s," said Stuart Miller, president and CEO of Lennar. "We take great pride in understanding market cycles and identifying the opportune point of entry. As we have noted on our quarterly conference calls, we have been carefully preparing to invest in this space for the last two years. Our strong cash position and proven track record in this area enables us to capitalize on this market cycle and create long-term value for our shareholders. We expect these transactions will be accretive to 2010 earnings."

Walgreens Acquiring Duane Reade for $1.075 Bil. By: Sasha M. Pardy In a move rivaling its top competitor's 2008 acquisition of Longs Drugs, Walgreens is acquiring New York-based drugstore chain Duane Reade from its private equity owners, Oak Hill Capital Partners, for $1.075 billion, which includes assumption of debt. If the transaction closes as expected by the end of August, Walgreens will own Duane Reade's 257 New York City area stores, its corporate office and its two distribution centers. "Duane Reade is a compelling strategic acquisition that will immediately provide Walgreens with a leading position in the largest drugstore market in the U.S.," said Walgreens president and CEO Greg Wasson. Walgreens currently operates 7,162 drugstores in all 50 states, the District of Columbia and Puerto Rico. This acquisition would increase the chain's size to 7,419 stores and further solidify its position as the nation's largest drugstore chain. CVS currently operates 7,025 stores in 44 states. According to Walgreens, Duane Reade generated $1.8 billion in net sales during 2009 and has the "highest sales per square foot in the retail drugstore industry nationwide." However, Duane Reade has been operating at a net loss for quite some time, to the extent that many industry observers predicted it would file bankruptcy due in 2009. Walgreens said it would "benefit" from the company's existing net operating losses because it could add value over time. Over the past two years, Duane Reade has made improvement efforts at several stores including store re-designs, on premise clinics, store-within-a-store beauty boutiques, and the launch of new private brand products. With Duane Reade's 50-year history in the New York City metro area, Walgreens plans to maintain the retailers' banner on the acquired stores. However, as Walgreens already operates 70 stores in the New York City market, a certain number of stores will be consolidated and closed over the course of time. Likewise, Walgreens plans to eventually consolidate Duane Reade's corporate office and other core functions into its own system.

THE WATCH LIST NEWSLETTER 13

Peter J. Solomon Co. acted as financial advisor to Walgreens in the transaction, and the law firm of Wachtell, Lipton, Rosen & Katz served as legal counsel for Walgreens. Goldman Sachs & Co. acted as lead financial advisor, and Bank of America Merrill Lynch acted as co-financial advisor to Oak Hill Capital Partners and Duane Reade. The law firm of Paul, Weiss, Rifkind, Wharton & Garrison LLP served as legal counsel to Duane Reade and its shareholders, including Oak Hill Capital Partners.

Getting Schooled By: Mark Heschmeyer Inland Public Properties Development Inc. (IPPD), a wholly owned subsidiary of Inland American Real Estate Trust Inc., entered into a sale-leaseback transaction with Imagine Schools Inc., a leading charter school operator. IPPD, on behalf of Inland American, purchased seven charter schools, in Arizona, Colorado, Florida, Maryland and Washington, DC, for $61 million. Imagine will lease back the schools for 20 years on a triple-net master lease. Charter schools are similar to traditional public schools since they are funded by the state, do not charge tuition or fees to attend, and their enrollment is open to the public. Imagine operates 71 public charter school campuses in 11 states and the District of Columbia. "This transaction demonstrates our commitment to social infrastructure assets, which are stable, income producing properties supported by state and federal funding programs," said Lori Foust, CFO of Inland American Business Manager & Advisor Inc. "These charter schools are strong additions to Inland American's diverse portfolio."

Brookfield Fund Picks Up Nearly 3 Mil-SF Portfolio From JPMorgan By: Randyl Drummer A group of funds sponsored by Brookfield Asset Management has acquired a 16-property, 2.9-million-square-foot office portfolio from JPMorgan Chase. Brookfield has now acquired more than 100 properties totaling about 12 million square feet over the last four years. "We think it represents one of the very few if not only transactions of scale that's taken place in the last 18 to 24 months that wasn't precipitated by a distressed situation on the part of an owner or lender," Steven H. Ganeless, senior vice president of Brookfield Real Estate Opportunity Fund, told CoStar. Ganeless did not disclose the value of the transaction, but Dow Jones News Service pegged the price at about $200 million. JPMorgan Chase is leasing back 60% of the space in the portfolio on a long-term basis as part of the deal. The bank was represented in the transaction by Houlihan Lokey and by J.P. Morgan Real Estate Advisors Inc. David Arthur, the Brookfield fund's president and managing partner, said the new owner has "opportunity to add significant value" to the portfolio, which includes four properties in Dallas, Tampa, FL, and Columbus, OH, that are 100% net-leased to JPMorgan Chase. The other properties are throughout the country and include an 800,000-square foot office tower in Houston and a 650,000-square foot office campus/data center site in Whippany, NJ. Brookfield describes the Houston and New Jersey properties in particular as "meaningful" value-add opportunities. The Brookfield REOF invests and manages two funds with $1.8 billion of assets totaling about 16 million square feet of commercial office, industrial and multifamily properties. Brookfield Asset Management Inc. has more than $90 billion of assets under management in property, renewable power and infrastructure.

THE WATCH LIST NEWSLETTER 14

Real Money: Capital Raisings, Property Financings Annaly Capital Management Inc. priced its public offering of $500 million in aggregate principal amount of its 4% convertible senior notes due 2015. Annaly granted the underwriter of the notes a thirty-day option to purchase up to an additional $75 million aggregate principal amount of the notes solely to cover over-allotments. The net proceeds to Annaly will be $484.8 million, which it expects to use to purchase mortgage-backed securities for its investment portfolio and for general corporate purposes. Pacific Office Properties Trust Inc. commenced a public offering of $400 million of its senior common stock. The senior common stock, priced at $10 per share, offers a cumulative dividend of 7.25%, declared daily and paid monthly, plus the potential for dividend increases that are triggered by increases in the Pacific Office listed common stock dividend. The company intends to use substantially all of the net proceeds from the offering to acquire and operate "value added" office properties in the western United States. Piedmont Office Realty Trust Inc. priced its public offering of 12 million shares of its Class A common stock at $14.50 per share. The underwriters have a 30-day option to purchase up to an additional 1.8 million shares. Gross proceeds would total about $200 million, which Piedmont intends to use for general corporate and working capital purposes, including capital expenditures related to renewal of leases and re-letting of space, the acquisition and development of (and/or investment in) office properties or, if market conditions warrant, repayment of debt or repurchase of outstanding shares of our common stock. Terreno Realty Corp. priced its initial public offering of 8.75 million shares of common stock at $20 per share. Concurrent with the closing of the offering, the company was to complete a private placement of an aggregate of 350,000 shares of common stock, at a price of $20 per share, to W. Blake Baird, the company's chairman and CEO, and Michael A. Coke, the company's president and CFO. The gross proceeds are expected to be $182 million and will be used to invest in industrial properties. Post Properties Inc. filed a prospectus supplement under which it may sell up to 4 million shares of its common stock from time to time. The company intends to use the proceeds from any sales for general corporate purposes. Keystone Property Group completed a $53.5 million refinancing for Keystone Summit Corporate Park in the Cranberry submarket in North Pittsburgh, PA. The loan is the first in the country to be originated and closed under the second generation of Commercial Mortgage-Backed Securities (CMBS) financing for a multi-borrower securitization. With this refinancing, Keystone was also able to cash out two-thirds of its equity. HFF arranged the following transactions.

• A $48 million construction loan for Canarsie Plaza, a 256,783-square-foot neighborhood shopping center under construction in Brooklyn, NY, working on behalf of a joint venture between Acadia Strategic Opportunity Fund II LLC and P/A Associates. The loan was secured through M&T Bank and Capital One Bank.

• A $45 million first mortgage loan secured by a 155,896-square-foot office building in Brookline Village in Brookline, MA, working on behalf of ND/CR 10 Brookline LLC, Loan proceeds were used to retire the existing debt on the property. The loan can be increased to fund the potential expansion of the building to accommodate its existing tenants. ND/CR 10 Brookline LLC is controlled by National Development and Charles River Realty Investors. The group purchased the property in early 2009.

• A $14 million financing for Pavilions Centre, a 200,000-square-foot grocery-anchored shopping center in Federal Way, WA, working on behalf of Kimco Realty Corp. HFF secured a non-recourse fixed-rate loan through a life insurance company.

• A $10.75 million refinancing for Gateway Tower, a 20-story, Class A office tower in St. Louis, MO, working on behalf of Sovereign Partners LLC. HFF secured the five-year, fixed-rate loan through Ladder Capital Finance. This financing retires a maturing CMBS loan that was originated by Bank of America in 2005.

• A $6 million in financing for three ground leases totaling 255 acres in California, Indiana and Pennsylvania working on behalf of an affiliate of The LCP Group LP. HFF placed the 38-month, fixed-rate permanent loan with a Texas-based life insurance company. The three parcels of land are improved with warehouse and distribution facilities leased to an international food company.

THE WATCH LIST NEWSLETTER 15

• A $3.335 million refinancing for Silver Oaks Apartments, a 57-unit multi-housing community in El Cajon, CA, working on behalf of a Linda Vista, CA-based private investor. HFF secured a 10-year, 5.90% fixed-rate Fannie Mae loan through Centerline Capital Group.

Berkadia Commercial Mortgage LLC originated two permanent, fixed-rate loans totaling $24,095,200 for multifamily properties in McHenry, IL. The 35-year, fully amortizing loans each had an interest rate of 4.63%. Westside Crest Apartments was financed for $7,135,200, and Fawn Ridge Apartments was financed for $16,960,000. The loans were originated the loans through the company's FHA/HUD program. The borrowers— first-time FHA/HUD borrowers—were Westside Crest LP and Fawn Ridge Apartments LP. Arbor Commercial Funding LLC funded the following deals.

• A $15,742,500 loan under the Fannie Mae DUS product line for the 216-unit complex known as Stone Ridge Apartments in Fayetteville, NC. The 10-year loan amortizes on a 30-year schedule and carries a note rate of 5.74%. Carolina Mortgage Co. secured the financing.

• A $14.5 million loan under the Fannie Mae DUS product line for the 204-unit complex known as Overlook at Golden Hills Apartments in Lexington, SC. The 10-year loan amortizes on a 30-year schedule and carries a note rate of 5.82%.

• A $6,846,790 loan under the Fannie Mae DUS product line for the 176-unit complex known as Carlisle on the Creek in Dallas, TX. The 7-year loan amortizes on a 30-year schedule and carries a note rate of 5.55%.

• Two loans totaling $6,104,300 under the Fannie Mae DUS product line. These loans include: Crescent Cove I in Evans, CO – a 96-unit complex in the amount of $4,229,300 funded under the Fannie Mae DUS product line. The 10-year loan amortizes on a 30-year schedule and carries a note rate of 5.75%. The second loan was for Amberwood Apartments II & III in Norfolk, NE – a 56-unit complex in the amount of $1,875,000 funded under the Fannie Mae DUS Small Loan product line. The 10-year loan amortizes on a 30-year schedule and carries a note rate of 5.89%.

• A $1.26 million loan under the Fannie Mae DUS Small Loan product line for the 22-unit complex known as Carriage Hills Apartments in New Haven, CT. The 10-year loan amortizes on a 30-year schedule and carries a note rate of 6.02%.

Colliers Spectrum Cauble closed a $15 million loan through a correspondent life insurer on an industrial portfolio owned by a joint venture between Seefried Properties and FRAPAG America. The funding was secured through life insurer UNUM to provide permanent financing on three distribution buildings totaling 551,631 square feet.

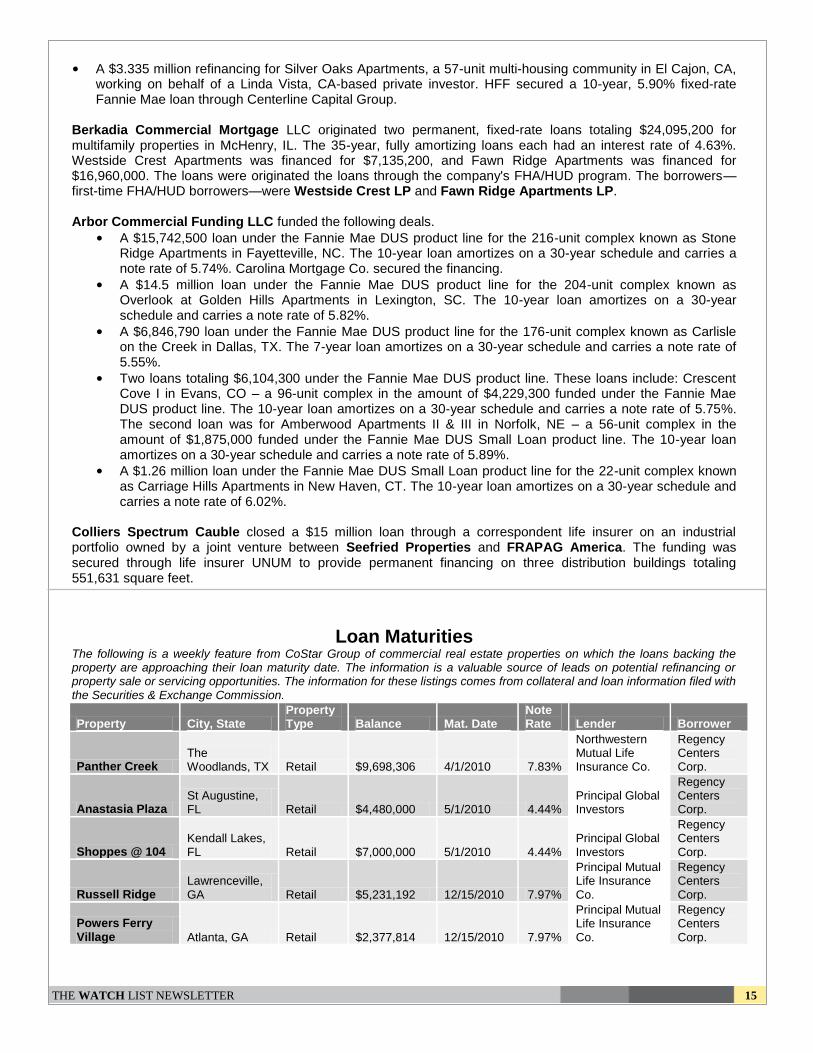

Loan Maturities The following is a weekly feature from CoStar Group of commercial real estate properties on which the loans backing the property are approaching their loan maturity date. The information is a valuable source of leads on potential refinancing or property sale or servicing opportunities. The information for these listings comes from collateral and loan information filed with the Securities & Exchange Commission.

Property City, State Property Type Balance Mat. Date

Note Rate Lender Borrower

Panther Creek The Woodlands, TX Retail $9,698,306 4/1/2010 7.83%

Northwestern Mutual Life Insurance Co.

Regency Centers Corp.

Anastasia Plaza St Augustine, FL Retail $4,480,000 5/1/2010 4.44%

Principal Global Investors

Regency Centers Corp.

Shoppes @ 104 Kendall Lakes, FL Retail $7,000,000 5/1/2010 4.44%

Principal Global Investors

Regency Centers Corp.

Russell Ridge Lawrenceville, GA Retail $5,231,192 12/15/2010 7.97%

Principal Mutual Life Insurance Co.

Regency Centers Corp.

Powers Ferry Village Atlanta, GA Retail $2,377,814 12/15/2010 7.97%

Principal Mutual Life Insurance Co.

Regency Centers Corp.

THE WATCH LIST NEWSLETTER 16

Property City, State Property Type Balance Mat. Date

Note Rate Lender Borrower

Market at Opitz Crossing

Woodbridge, VA Retail $11,517,074 3/1/2011 7.30%

Wachovia Securities

Regency Centers Corp.

Specially Serviced Loan Volumes Quadruple U.S. CMBS loans are transferring to special servicing in larger batches and with increasing speed, according to Fitch Ratings in its weekly U.S. CMBS newsletter. Last month saw 248 loans totaling $4.27 billion move into special servicing. This figure is more than four times the balance that transferred in January of last year. The size of specially serviced loans has increased 2.4 times from 2009 to $17.2 million, with five loans greater than $100 million. "More loans will approach final maturity without available extensions or a refinancing commitment," said Mary MacNeill, Fitch managing director. "Available liquidity remains limited, which is making refinancing large loans more difficult even when they are performing." The distribution of property types in special servicing are as follows. Retail Total in special servicing: 842 loans ($15 billion); Rated universe: 12,837 loans ($127.3 billion). Hotel Total in special servicing: 275 loans ($11 billion); Rated universe: 2,131 loans ($49.3 billion). Multifamily Total in special servicing: 872 loans ($9.8 billion); Rated universe: 9,320 loans ($62.2 billion). Office Total in special servicing: 509 loans ($7.5 billion); Rated universe: 6,559 loans ($141.5 billion).

Watch List The following is a weekly feature from CoStar Group of properties that may potentially be affected by worsening financial conditions, borrower issues, deteriorating property conditions, or lease rollovers, tenant issues or vacancies. The information is a valuable source of leads on potential refinancing or property sale or servicing opportunities. The information for these listings comes from collateral and loan information filed as part of the loans inclusions in a commercial mortgage backed securities offering.

Property Address Property Type, Size

CMBS; Master Servicer; Special Servicer Comment

The Berkshires at Brookfield

782 E. Butler Road, Mauldin, SC

Multifamily, 702

BACM 2005-1; Bank of America; J.E. Robert Companies

Transferred to special servicing for maturity default on 1/10/10.

Berkshire Mall 655 Berkshire Road, Lanesborough, MA

Retail, 651,386

COMM 2005-FL10; Midland Loan Services; CT Investment Management The loan is scheduled to mature 03/09/2010.

THE WATCH LIST NEWSLETTER 17

Property Address Property Type, Size

CMBS; Master Servicer; Special Servicer Comment

Inn at Laguna Beach

211 N Coast Highway, Laguna Beach, CA Hotel, 70

COMM 2006-C7; Midland; CWCapital

Transferred to special servicing for imminent default. 2009 NCF DSCR was 0.95 with occupancy of 77%.

Penn Center East

100-700 Penn Center Blvd., Pittsburgh, PA

Office, 963,308

GSMC 2007-GG10; Wachovia; CWCapital Asset Management

Loan transferred to special servicing 2/2/10 for imminent default. File being reviewed to determine workout strategy going forward.

Centennial I & II

1949 & 2121 S. State St., Tacoma, WA

Office, 239,475

JPMC 2007-C1; Berkadia; Midland Loan Services

Transferred to special servicing for technical default/borrower bankruptcy.

321 Ellis Street 321 Ellis St., New Britain, CT

Industrial, 650,000

JPMC 2007-FL1; Berkadia; Berkadia

Transferred to special servicing for imminent default; last loan payment date was 11/9/09

Sofitel Minneapolis

5601 W. 78th St., Minneapolis, MN Hotel, 282

JPMC 2007-FL1; Wachovia; Berkadia

Transferred to special servicing for imminent default; last loan payment was 12/1/09.

Cerritos Corporate Tower

18000 Studebaker Road, Cerritos, CA

Office, 187,106

MLCFC 2007-5; Keybank; CWCapital Asset Management

Transferred to special servicing for imminent default. There has been an increase in vacancy over the last year, with little leasing activity.

Somerset Apartments

42211 Stonewood Road, Temecula, CA

Multifamily, 318

MLCFC 2007-5; KeyBank; CWCapital Asset Management

Transferred to special servicing for monetary default; last loan payment was 10/1/09.

Crowne Plaza-Addison

14315 Midway, Addison, TX Hotel, 429

MS 2007-IQ16; Berkadia; Centerline Capital Group

Transferred to special servicing for imminent default. The borrower submitted a letter to servicers on 12/2/09 indicating that the property is experiencing financial difficulties and projects a negative cash flow of $4.9 million between 2010 and 2015.

Rexcorp Princeton Office Portfolio

1 University Square Drive, 100, 104 & 115 Campus Drive, Princeton, NJ

Office, 444,774

UBS 2007-FL1; Berkadia; Berkadia

Transferred to special servicing for imminent default. The combined DSCR and occupancy for the six months ended 06/30/09 was 1.02x and 42%, respectively. The loan was scheduled to mature on 02/09/10.

KEY BENEFITS OF ADVERTISING IN THE WATCH LIST

• Visibility —The pdf Watch List Newsletter itself is downloaded by thousands of individuals weekly. And the stories in the newsletter are read about 75,000 times a month on average.

• Eye-Catching — In the pdf newsletter you get a half-page, four-color horizontal ad on a page with news. Your ad; your design; your message. The ad can be linked to individual email addresses and/or any web page of your choice.

• Easy — Submit a jpeg / gif image of your ad that is approximately. 2200 pixels wide x 1500 pixels high.

• Value-Added Editorial Content — As an advertiser you get exclusive access to a variety of data and research material used in compiling the newsletter. For example, spreadsheets showing amounts of commercial nonperforming loans and foreclosed assets for 8,108 federally insured lenders and a list of more than 765 funds that have raised more than $55 billion for real estate acquisitions.

• Email me at [email protected]