Embed Size (px)

DESCRIPTION

Risk Changes Following Ex-Dates of Stock Splits. Shen-Syan Chen National Taiwan University Robin K. Chou National Central University Wan-Chen Lee Ching Yun University. Introduction. Ex-dates for a stock split Changes in the number of shares outstanding and in the level of stock price - PowerPoint PPT Presentation

Citation preview

1

Risk Changes FollowingEx-Dates of Stock Splits

Shen-Syan ChenNational Taiwan University

Robin K. ChouNational Central University

Wan-Chen LeeChing Yun University

2

Introduction Ex-dates for a stock split

Changes in the number of shares outstanding and in the level of stock price

Should not affect the distribution of stock returns

But, shifts in the riskiness of the stocks have been found Stock return volatilities tend to increase s

ignificantly following split ex-dates

3

Introduction Increase in volatility after split ex-date

s Ohlson and Penman (1985), Lamoureux a

nd Poon (1987), Dubofsky (1991), … There have not been explanations for

the increase in volatility Microstructure biases do not explain the i

ncrease Desai et al. (1998) and Koski (1998)

4

Motivation Analyze the changes in the riskiness of

stocks following splits Focus on the long-term influence of st

ock splits on return volatility Up to five years subsequent to ex-dates Previous studies examine shifts in stock r

eturn volatility for a short period, usually less than one year following the splits

5

Motivation Focus on changes in the

components of equity risk Identify the sources of changes in

post-split stock return volatility

6

Hypothesis Equity risk contains systematic and

unsystematic risks

Hypothesis 1. There is an increase in equity betas after stock splits

Hypothesis 2. There is an increase in the residual variance after stock splits

7

Hypothesis By Hamada (1972)

Hypothesis 3. Any increase in post-split equity betas is due to an increase in asset betas

Hypothesis 4. Any increase in post-split equity beta is due to an increase in financial leverage

8

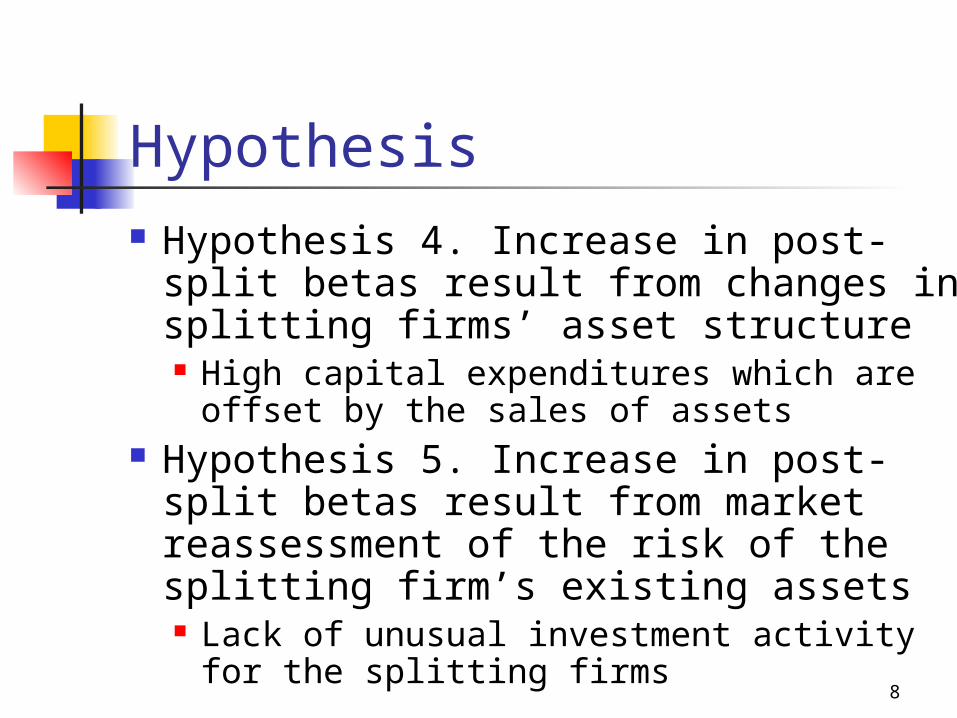

Hypothesis Hypothesis 4. Increase in post-split

betas result from changes in splitting firms’ asset structure High capital expenditures which are offset

by the sales of assets Hypothesis 5. Increase in post-split

betas result from market reassessment of the risk of the splitting firm’s existing assets Lack of unusual investment activity for

the splitting firms

9

Data Sample of stock splits

All splits from NYSE, AMEX and Nasdaq during 1981-1998

Excludes regulated utilities and financial institutions

The splits must have a split factor of at least 25%

No cash dividends or other stock distribution of 25% or more within 5 years after the split

10

Data Matched samples (Lewis et. al

(2002)) Matched by industry (two-digit SIC),

asset size (25% to 200% of the splitter), and normalized operating income (OIBD/Asset)

The comparison firm does not have any stock distribution of 25% or more within 5 years before and after the sample firm’s ex-date

11

Methodology Focus on the long-term influence of th

e splits on return volatility Calculate risk measures for both sam

ple firms and matched firms, then compare To control for the industry effect

T-statistics and Wilcoxon signed rank statistics are calculated for testing differences in mean and median, respectively

12

Empirical Results Changes in total equity risk (Table 2)

Splitting firms in general have lower total equity risk than the control firms

Relative to non-splitting firms, splitting firms experience a significant increase in total equity risk in the first year after splits

The increases in total equity variances in the first year appear to be transitory

13

Empirical Results Changes in systematic risk (Table 3)

Splitting firms have higher systematic risk than the control firms, in contrast to the total equity risk results

Significant increase in systematic risk for splitting firms, relative to non-splitting firms in year +1

Consistent with Hypothesis 1 But, this increase also seems to be

temporary (see results from year +2 to +5)

14

Empirical Results Changes in unsystematic risk (Table 4)

Splitting firms have lower unsystematic risk than the control firms

Significant increase in unsystematic risk for splitting firms, relative to non-splitting firms in year +1

Consistent with hypothesis 2 But, this increase seems to be temporary

(see results from year +2 to +5)

15

Empirical Results Changes in asset risk (a component

of the systematic risk) (Table 5) Splitting firms generally have higher

asset risk than control firms Asset risk for splitting firms only

increase in year +1, so it appears to be transitory

The post-split increases in equity betas are due to increases in splitting firms’ asset betas

Consistent with Hypothesis 3

16

Empirical Results Changes in financial risk (a

component of the systematic risk) (Table 6) Splitting firms have lower financial risk

than control firms The debt ratios of splitting firms do not

increase after splits, relative to non-splitting firms

The post-split increase in equity betas are not due to increases in the splitting firms’ financial leverage

Inconsistent with Hypothesis 4

17

Empirical Results Why does asset risk change? (Table 7 & 8)

Changes in asset structure or market reassessment of the risk of existing assets?

A temporary increase in capital outlays for the splitting firms in year +1 is identified in Table 7

From Table 8, there is no significant change in net capital outlays for the splitting firms

These imply that splitting firms are engaged in a replacement of assets in year +1

Consistent with Hypothesis 5, rather than Hypothesis 6

18

Empirical Results Why stock return volatility increase

temporarily after stock splits? Asset restructuring in year +1 increases

asset risk Asset risk in turn increases equity risk Equity risk increases result in stock return

volatility increases This study shed new light on the

source of changes in post-split volatility

19

Robustness Checks Stock splits lead to a significant chang

e in the trading activity of splitters This may affect the estimates of systemat

ic risk (Scholes and Williams (1977)) Apply the AC method by Dimson (1979) to

re-estimate equity betas and asset betas Empirical results in the paper remain unc

hanged (Table 9 and Table 10)

20

Robustness Checks Daily data may be prone to bid-ask bo

unces and price discreteness errors Use of weekly data can correct for this pr

oblem (Koski (1998)) We use weekly data to re-estimate equity

risk, systematic risk, unsystematic risk, and asset risk

Empirical results in the paper remain unchanged (Table 11)

21

Conclusions This study focus on the long-term

influence of stock splits on return volatility Splitting firms experience a significant

increase in total equity variance in year +1

But the increase is temporary A result that has not been found before

22

Conclusions Identify sources of the changes in

stock volatility subsequent to stock splits The increase in stock volatility after

stock splits is ultimately driven by the asset restructuring by the splitting firms

Asset restructuring induces increases in asset risk (business risk), systematic risk, and eventually total equity risk

Residual return variance also contribute Financial risk does not change