Embed Size (px)

Citation preview

Reward in 2011Keeping pace with changes in the economic climate

2

ContentsAbout the Reward in 2011 research 1

Summary 2

Key findings 4

Research findings in detail 5

Business performance 5Upturn 6Salary forecasts 6Salary freezes 7How base pay is managed in organisations 10Short term incentives and other reward arrangements 12Staffing levels and recruitment 14

Sector analysis 15

Public and not for profit (PNFP) sector 15Retail 19Financial services 20Fast Moving Consumer Goods (FMCG) 21Oil and Gas 22Chemicals 23Industrial brands / Manufacturing 24

Key priorities and challenges 26

Conclusions and recommendations 30

1

About the Reward in 2011 researchThe Hay Group Reward Information Services “Reward in 2011” report has been compiled based upon a survey conducted in December 2010 designed to understand the challenges facing HR professionals in 2011.

The report follows on from the “Reward in 2010” research conducted by Hay Group in late 2009. The “Reward in 2011” report analyses the responses of organisations and reward professionals to the changing economic outlook and considers the impact of the government fiscal measures and recent spending review on the reward market in the next 12 months.

This report analyses information provided by 211 organisations who participated in our online survey (165 organisations from the private sector and 46 from the public sector). Typical respondents in Reward in 2011 included HR and reward professionals from medium to large size organisations across all major industries, representing over one million UK employees.

Thank you to all of you that took the time to complete this survey and we hope you find the report findings valuable and interesting.

The report includes:

� Business performance and outlook

� Salary changes

� Short term incentives and other reward arrangements

� Staffing levels and recruitment

� Key priorities and challenges

� Sector analyses

If you would like to discuss any aspect of this research, and/or would like further advice on any reward related issues, please contact us:

E: [email protected]: 020 7856 7200

2

SummaryRelative Growth

This research clearly demonstrates that the reward landscape in the UK in 2011 is set to become increasingly diverse with marked differences in expected pay increases between the public and private sectors.

Salary forecasts overall are improving for the second year- across all sectors the median forecast for base salary growth in 2011 is 2.5 per cent which is up by 0.5 per cent from our previous study in November 2009. However it is the marked difference between the medians for the public sector (0.4 per cent according to respondents) and the private sector (3 per cent according to respondents) that are most telling. Within the public sector employers have been forced to react to the cutbacks announced in the Comprehensive Spending Review (CSR) and this has inevitably had an impact on pay levels which is often the biggest single cost faced by organisations in this sector. In the private sector, however, the outlook is more positive with many organisations reporting improvements in the trading environment allowing them to ease some of the controls that had to be imposed on reward budgets in recent years in response to the global economic downturn.

Across all sectors we can see that in 2011 the proportion of organisations imposing salary freezes is set to decrease from 31 per cent last year to 18 per cent. When questioned specifically on the topic of likely pay freezes in 2011, 56 per cent of public sector respondents indicated that they are planning a pay freeze, compared to only 7 per cent of private sector respondents.

All of these planned changes to base salaries need to be understood in the context of inflation and with the Consumer Prices Index (CPI) currently at 3.7 per cent, real terms base pay levels for the majority of employees are set to decline with those in the public sector feeling the pinch especially.

As organisations look to maximise the return on investment of their reward budgets we can see that there is an increased focus on variable pay with the majority of organisations with short-term incentive schemes expecting to pay out bonuses on, or above, target in 2011. Variable pay and bonus schemes are also the area of reward that most organisations plan to review in 2011 as more organisations move toward pay for performance.

In contrast with the “Reward in 2010” research, these findings appear to show that reward professionals have a more optimistic view of the year ahead. Indeed, 70 per cent of private sector respondents are expecting business performance to be on or above targeted levels for 2010. Nevertheless, the picture looks rather less positive for the public sector going into 2011 and this is reflected in the confidence levels of reward professionals in this market.

Within the public sector further cost savings are likely to be made in the form of redundancies with the majority of organisations predicting reductions to staffing levels whereas those in private sector organisations expect to maintain or increase employee numbers.

The proportion of organisations imposing salary freezes is set to decrease from 31 per cent last year to 18 per cent.

3

“If cost of living continues to rise (eg. Fuel bills, VAT etc) then we may see an increase in discontentment from our currently stable employee base, if our pay budget cannot keep pace.”

FMCG respondent

In light of these findings it is unsurprising that the key challenges facing reward professionals in 2011 are talent management and employee engagement. With uncertainty over job losses and a reduction in employees’ pay in real terms, organisations - particularly in the public sector - will need to look at innovative ways of retaining key talent and maintaining employees’ morale.

These could involve improved communication to employees about the value of their total reward package, especially around benefits - the value of which can be frequently overlooked by employees. Additionally, the research suggests that organisations will be increasingly looking to target their limited reward budgets toward high performers through the increased use of performance related pay.

Overview 2011

Confidence continues to return to private sector organisations. The majority of those surveyed suggested that they either have already or will experience an upturn in 2011. Many challenges remain in the private sector, and this is certainly going to be the case for the public sector in the coming year and beyond.

Despite the optimistic outlook from private sector organisations for 2011, cost control is still at the forefront of Reward Professionals’ minds and the impact that may bring on employee engagement. One respondent summarises in their key challenges for 2011:

“Lack of budget for investment in reward adjustments...balancing requests for pay increases against budget constraints...delivering strategy with little resource.”

HR professionals are acutely aware of the external environment in which they operate and the pressures that brings: “Balancing pay budgets against the back drop of economic uncertainty. If cost of living continues to rise (eg. Fuel bills, VAT etc) then we may see an increase in discontentment from our currently stable employee base, if our pay budget cannot keep pace” FMCG respondent.

A direct consequence of the recession in reward terms is a general move in the market towards pay for performance. The clear advantages to this approach are efficiency savings, appropriate recognition and ultimately the retention of key performers. The research suggests that the majority of organisations are planning to continue focusing on variable pay and other reward arrangements such as pensions in order to achieve the outcomes they require. Although those outcomes may be markedly different in the public sector where the impact of the austerity measures will be keenly felt and the need to retain employee engagement as well as manage talent will be to the fore.

4

Key findings

Business Performance

� 70 per cent of private sector respondents are expecting business performance to be on or above targeted levels in 2010 (up by 13 points compared to November 09).

� There has been an overall increase in the proportion of respondents who expect business results to be above targeted levels.

� 61 per cent of respondents have experienced an upturn from the recession in the last twelve months.

Salary changes

� UK organisations are predicting median salary forecasts to be 2.5 per cent (3 per cent excluding salary freezes) for 2011, compared to a median forecast of 2 per cent last year.

� Public and not for profit sectors are showing the lowest salary forecasts at 0.4 per cent.

� 82 per cent of organisations have indicated that they will be increasing salaries in 2011, 93 per cent for private sector and 39 per cent for public sector.

� 78 per cent of private sector respondents are planning to lift their salary freeze within the next 12 months.

� Only 15 per cent of public sector organisations that have had a pay freeze in place will lift the freeze in the coming twelve months.

Short term incentives and other reward arrangements

� 73 per cent of respondents are anticipating that their 2011 short term incentive payments will be either on or above target (up by 23 points compared to Nov 09).

� Variable payments and pensions are the two main areas where organisations expect change over the course of the next year, with over 40 per cent stating they are planning to make changes in either one / both of these areas.

Staffing levels and recruitment

� For 2011, half of respondents are aiming to maintain or increase current staffing levels whereas the other half is planning to decrease the number of staff.

� Talent management and the retention of high performers remains a concern for reward professionals.

Key priorities and challenges

� Respondents identified employee engagement and talent management as burning priorities to reward professionals in 2011

� Key challenges for 2011 are keeping pace with changes in the economic climate, the issue of ‘real pay’, managing talent and employee engagement.

Research findings in detail

Business performance

70 per cent of private sector respondents are expecting business performance to be on or above targeted levels in 2010. This is made up of 47 per cent who expect performance to be on target and the remaining 23 per cent who expect business results to be above target. There has been an increase in the proportion of respondents who expect results to be above targeted levels (up by 11 percentage points from November 09 and up by 21 percentage points from April 09).

Whilst the majority of private sector organisations are forecasting business results to be above targeted levels, there has also been a significant decrease in the number of organisations who expect business results to be below target (down by 13 per cent from November 09 as shown in graph below).

Unlike in 2009, it seems that more organisations have emerged from the recession; however, 30 per cent of private sector respondents are still feeling the impact of the downturn in their business performance forecast. The most prominent sector in this regard was retail, accounting for 36 per cent of those predicting business performance to be below target. Responses were from a mix of high street retailers and supermarkets.

On target

Above target

Below target

30%

47%

23%

On-target performance 2010

Our business performance will be:

On-target performance 2011

43% 45%

12%

On target performance - ‘Reward in 2010’ On target performance - ‘Reward in 2011’

5

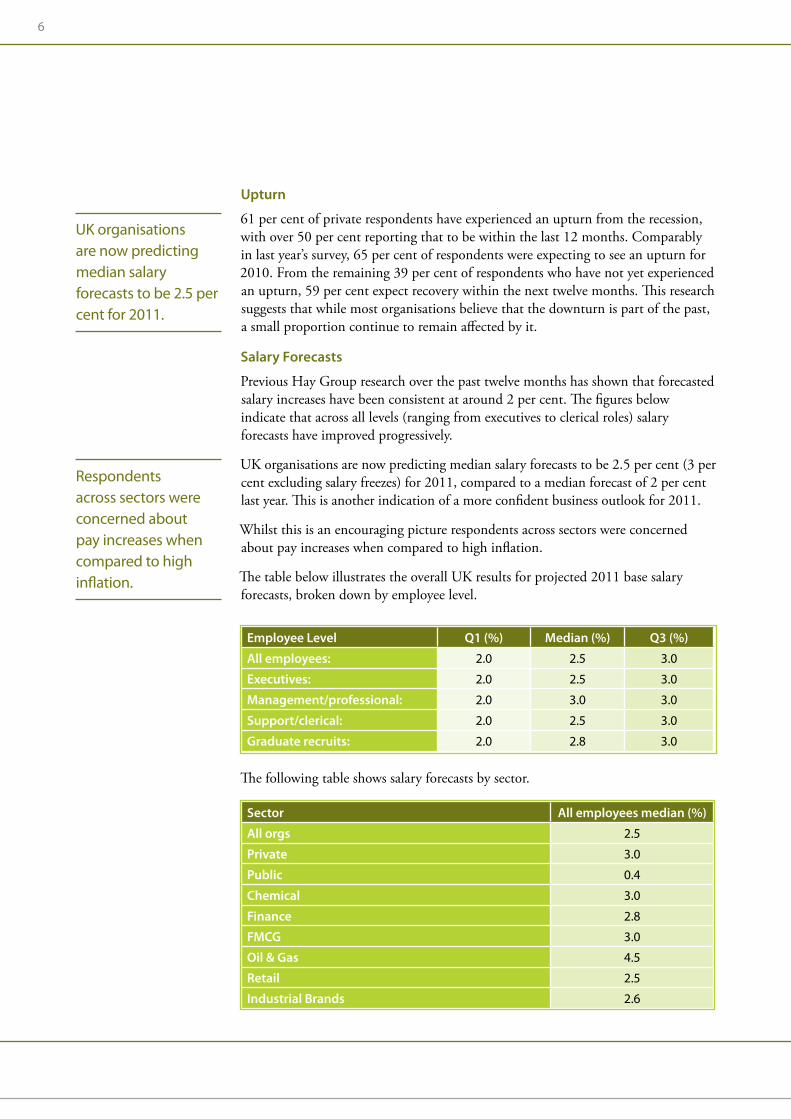

Respondents across sectors were concerned about pay increases when compared to high inflation.

Sector All employees median (%)

All orgs 2.5

Private 3.0

Public 0.4

Chemical 3.0

Finance 2.8

FMCG 3.0

Oil & Gas 4.5

Retail 2.5

Industrial Brands 2.6

Employee Level Q1 (%) Median (%) Q3 (%)

All employees: 2.0 2.5 3.0

Executives: 2.0 2.5 3.0

Management/professional: 2.0 3.0 3.0

Support/clerical: 2.0 2.5 3.0

Graduate recruits: 2.0 2.8 3.0

The following table shows salary forecasts by sector.

6

Upturn

61 per cent of private respondents have experienced an upturn from the recession, with over 50 per cent reporting that to be within the last 12 months. Comparably in last year’s survey, 65 per cent of respondents were expecting to see an upturn for 2010. From the remaining 39 per cent of respondents who have not yet experienced an upturn, 59 per cent expect recovery within the next twelve months. This research suggests that while most organisations believe that the downturn is part of the past, a small proportion continue to remain affected by it.

Salary Forecasts

Previous Hay Group research over the past twelve months has shown that forecasted salary increases have been consistent at around 2 per cent. The figures below indicate that across all levels (ranging from executives to clerical roles) salary forecasts have improved progressively.

UK organisations are now predicting median salary forecasts to be 2.5 per cent (3 per cent excluding salary freezes) for 2011, compared to a median forecast of 2 per cent last year. This is another indication of a more confident business outlook for 2011.

Whilst this is an encouraging picture respondents across sectors were concerned about pay increases when compared to high inflation.

The table below illustrates the overall UK results for projected 2011 base salary forecasts, broken down by employee level.

UK organisations are now predicting median salary forecasts to be 2.5 per cent for 2011.

When looking at the sector breakdown of salary forecasts for 2011, the largest forecast is seen in the Oil and Gas sector with median forecasts of 4.5 per cent (up by 1.5 percentage point from November 09 forecasts). This forecast suggests that the Oil and Gas industry is returning to pre-recession salary forecasts.

In addition, the confidence in the financial services sector is shown by a strong salary forecast at 2.8 per cent compared to last year when forecast was at 1 per cent. Industrial brands and manufacturing forecast suggests conservative growth, up by 0.6 per cent point compared to last year’s forecast. As anticipated, public and not for profit sectors are showing the lowest salary forecasts at 0.4 per cent due to the government pay deal freeze.

Salary Freezes

31 per cent of all respondents indicated that a salary freeze has been implemented within the last year. This is a 9 per cent decrease when compared to the “Reward in 2010” survey. Salary freezes in the private sector are on the decline

Beneath the headline figures, the private and public sector show stark contrast. 26 per cent of private sector respondents have had a pay freeze in 2010 compared to 50 per cent of public sector organisations.

78 per cent of organisations decided not to shield any professional categories from the freeze and chose to implement an all employee freeze rather than breaking down freezes into hierarchical level. This pattern is consistent across all sectors including the public sector.

When looking forward, 82 per cent of organisations have indicated that they will be increasing salaries in 2011, whilst only 18 per cent are freezing

7

For the minority who have implemented freezes at different levels, the main reasons were employee engagement and staff retention particularly from private sector respondents. From a public sector perspective, no freeze has been implemented for teachers as the government deal exempted them from the pay deal cut.

When looking forward, 82 per cent of organisations have indicated that they will be increasing salaries in 2011, whilst only 18 per cent are freezing.

However, once again scratching beneath the surface shows some marked disparities between the public and private sectors. When asked if their organisation intends to increase salaries in 2011, 93 per cent of respondents in the private sector indicated that they would, whereas in the public sector only 39 per cent of respondents plan increases.

Of those organisations that indicated a salary freeze had been implemented in 2010, 56 per cent plan to lift the freeze within the next twelve months, with 30 per cent indicating that it would take longer than this period.

Public sector salary changes 2011

Freezing salaries

Increasing salaries

Decreasing salaries56%

39%

Private sector salary changes 2011

7% 5%

93%

All organisations – Lifting pay freeze

Don’t know

In the next 3 months

In the next 6 months

In the next year

Not within the next year

30%

14%

15%

19%

22%

8

Public sector – Lifting pay freeze

Don’t know

In the next 3 months

In the next 6 months

In the next year

Not within the next year

66%

19%

10%

5%

0%

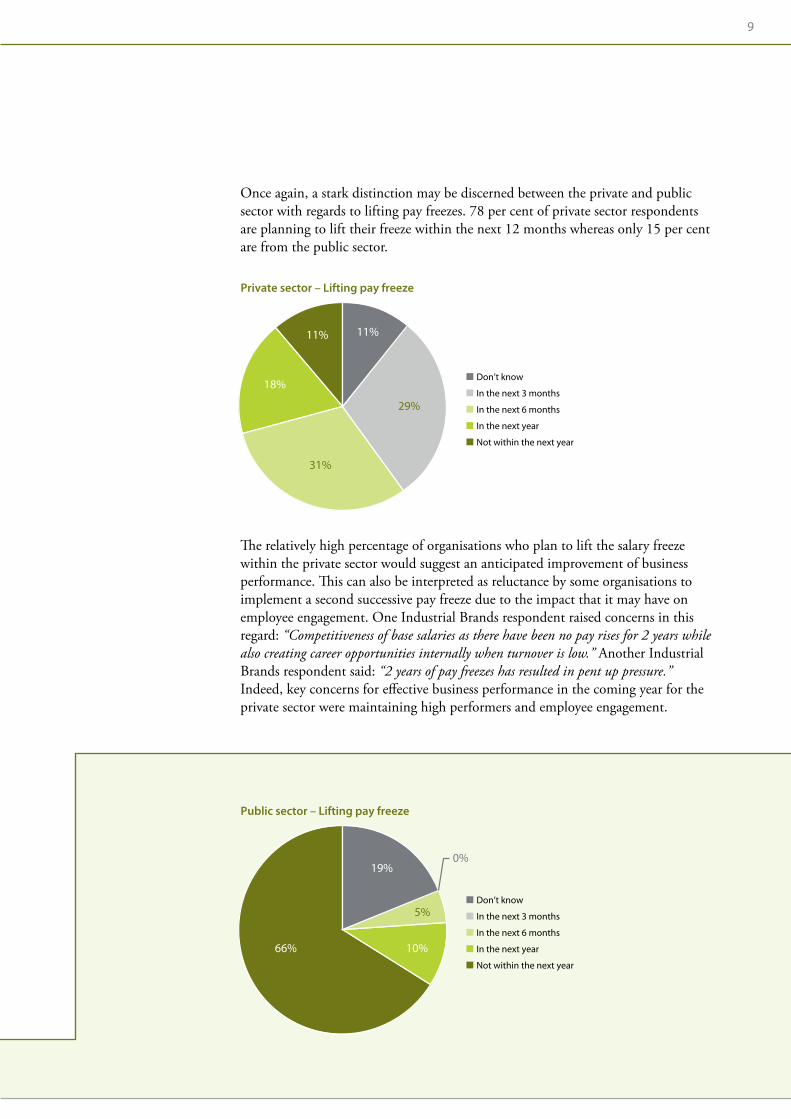

Once again, a stark distinction may be discerned between the private and public sector with regards to lifting pay freezes. 78 per cent of private sector respondents are planning to lift their freeze within the next 12 months whereas only 15 per cent are from the public sector.

The relatively high percentage of organisations who plan to lift the salary freeze within the private sector would suggest an anticipated improvement of business performance. This can also be interpreted as reluctance by some organisations to implement a second successive pay freeze due to the impact that it may have on employee engagement. One Industrial Brands respondent raised concerns in this regard: “Competitiveness of base salaries as there have been no pay rises for 2 years while also creating career opportunities internally when turnover is low.” Another Industrial Brands respondent said: “2 years of pay freezes has resulted in pent up pressure.” Indeed, key concerns for effective business performance in the coming year for the private sector were maintaining high performers and employee engagement.

Private sector – Lifting pay freeze

Don’t know

In the next 3 months

In the next 6 months

In the next year

Not within the next year

11% 11%

18%

29%

31%

9

66 per cent of public sector reward professionals do not expect the salary freezes to be lifted within the next year. This uncertainty is prevalent within the sector as a whole and is clearly linked to the current austerity measures. Interestingly, many of the concerns held by reward professionals in the public sector are similar to those in the private sector, for example, the impact on effective business performance following the spending review and the need to retain key talent and wider employee engagement. Reward professionals are consequently wary of implementing successive pay freezes with regards to the impact on employment engagement.

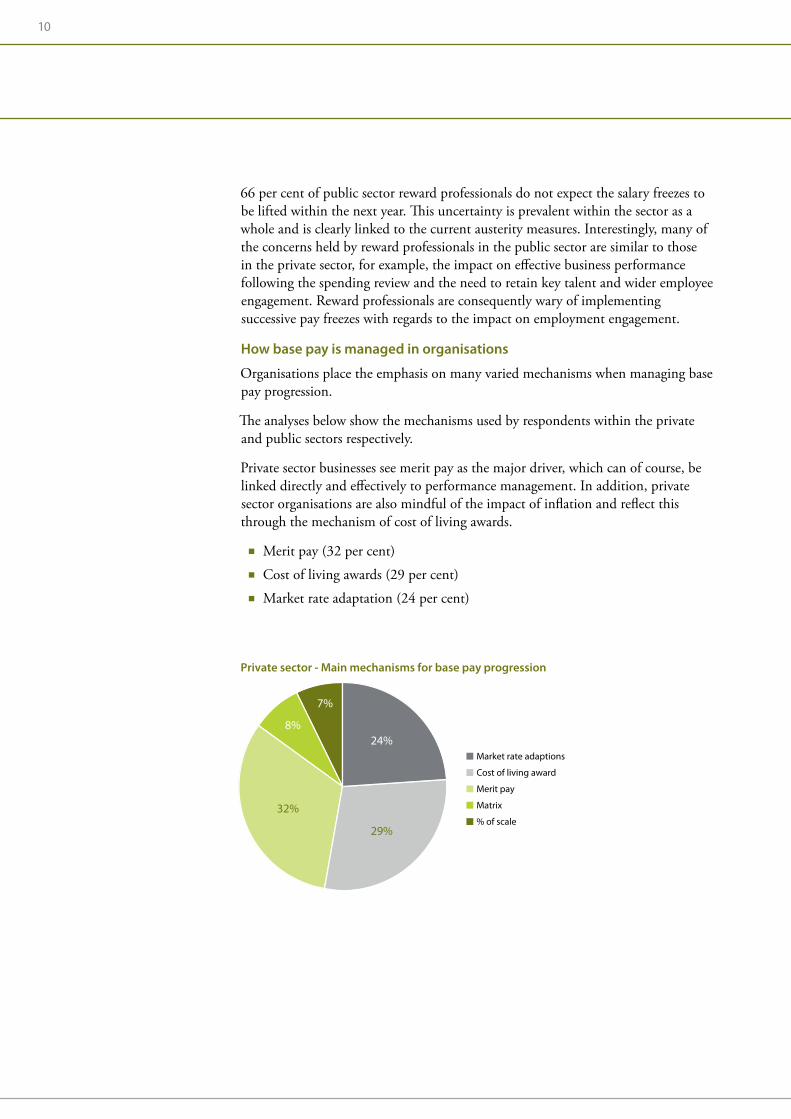

How base pay is managed in organisations

Organisations place the emphasis on many varied mechanisms when managing base pay progression.

The analyses below show the mechanisms used by respondents within the private and public sectors respectively.

Private sector businesses see merit pay as the major driver, which can of course, be linked directly and effectively to performance management. In addition, private sector organisations are also mindful of the impact of inflation and reflect this through the mechanism of cost of living awards.

� Merit pay (32 per cent)

� Cost of living awards (29 per cent)

� Market rate adaptation (24 per cent)

Private sector - Main mechanisms for base pay progression

Market rate adaptions

Cost of living award

Merit pay

Matrix

% of scale

7%

24%8%

29%

32%

10

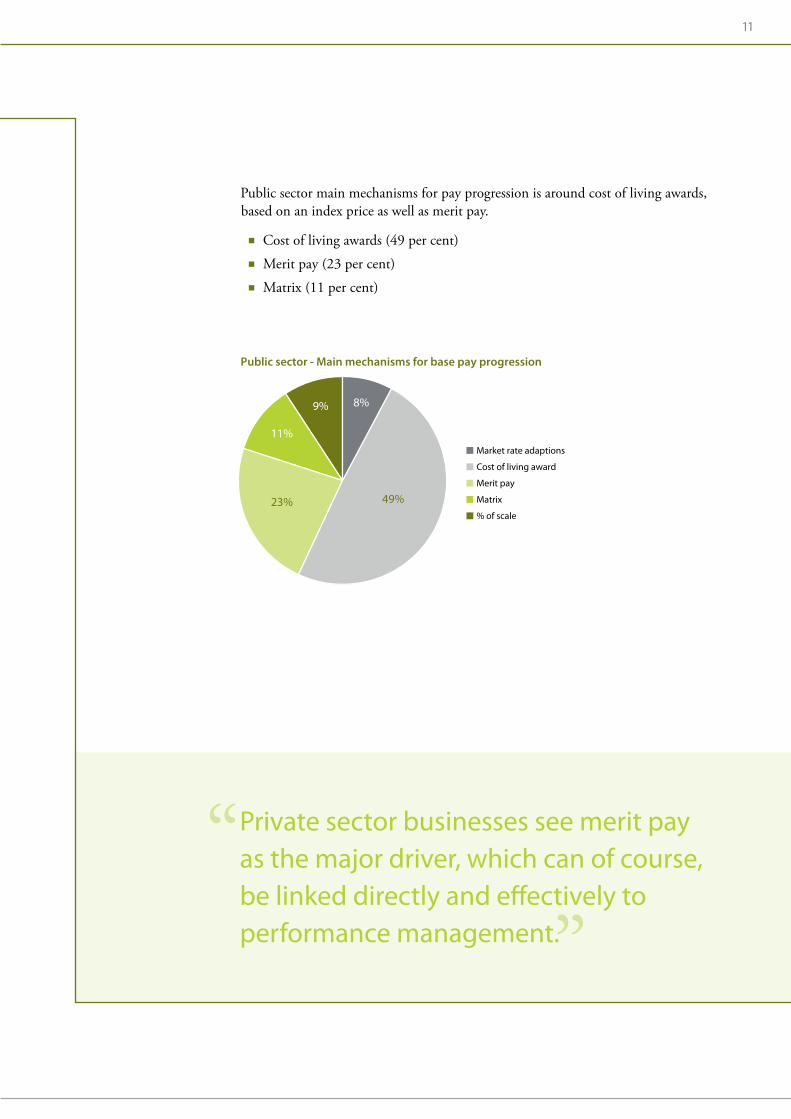

Public sector main mechanisms for pay progression is around cost of living awards, based on an index price as well as merit pay.

� Cost of living awards (49 per cent)

� Merit pay (23 per cent)

� Matrix (11 per cent)

Public sector - Main mechanisms for base pay progression

Market rate adaptions

Cost of living award

Merit pay

Matrix

% of scale

9% 8%

11%

49%23%

Private sector businesses see merit pay as the major driver, which can of course, be linked directly and effectively to performance management.

11

Short term incentives and other reward arrangements

Bonus Arrangements

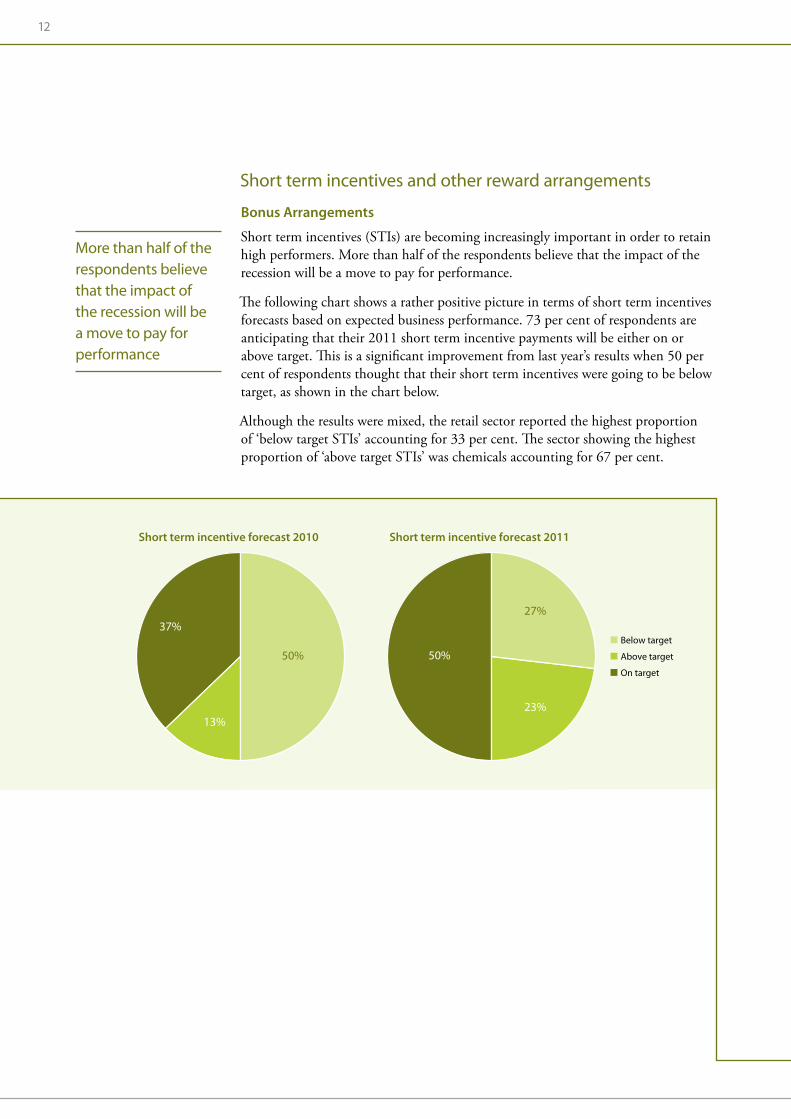

Short term incentives (STIs) are becoming increasingly important in order to retain high performers. More than half of the respondents believe that the impact of the recession will be a move to pay for performance.

The following chart shows a rather positive picture in terms of short term incentives forecasts based on expected business performance. 73 per cent of respondents are anticipating that their 2011 short term incentive payments will be either on or above target. This is a significant improvement from last year’s results when 50 per cent of respondents thought that their short term incentives were going to be below target, as shown in the chart below.

Although the results were mixed, the retail sector reported the highest proportion of ‘below target STIs’ accounting for 33 per cent. The sector showing the highest proportion of ‘above target STIs’ was chemicals accounting for 67 per cent.

More than half of the respondents believe that the impact of the recession will be a move to pay for performance

Below target

Above target

On target

50%

27%

23%

Short term incentive forecast 2010 Short term incentive forecast 2011

50%

37%

13%

12

Reward arrangements

71 per cent of respondents are planning to make changes to reward arrangements in the next year.

A number of respondents identified the delicate balance of maintaining benefits as on of the biggest barriers they face in controlling costs:

“Multiply legacy benefit plans increase costs but also make controlling costs more difficult.” Business Services organisation

and

“Third party cost increasing and company under pressure to retain benefits.” Financial Services organisation

The following table shows in which areas of the reward mix, companies are planning to focus on in the coming year.

This table highlights that organisations are planning to focus on variable pay and bonuses as well as pensions and retirement benefits. Bonuses and pensions are one of the most prominent compensation elements and allow a degree of flexibility with regards to managing costs. The cost of legacy defined benefit pension schemes were mentioned by numerous respondents across sectors. Indeed, the main drivers behind these changes are cost savings, efficiencies and business imperatives for both public and private sector.

“Tailoring our benefits to meet expectations as the company continues to work out of recession.”

A challenge listed by an Industrial Brands respondent.

Reward Arrangements % respondents

Variable pay / bonuses 23

Pensions / retirement benefits 18

Other benefits 13

Base pay 12

Company cars 9

Terms of employment 8

Health 7

Overtime 5

Allowances (e.g. short pay / call out / guaranteed payments)

5

13

Staffing levels and recruitment

When asked to look back to 2010, 50 per cent of organisations said they increased and/or maintained staffing levels regardless of the private / public sector remit. This is on a par with last year’s results. Organisations in Inner London as well as Scotland appear to have increased their staff levels, whereas other regions generally decreased their staffing levels. The decrease of staffing levels was mainly implemented through restructuring and redundancy programmes.

When asked about their expectations on staffing levels for 2011, clear sector differences may be noticed. An encouraging picture can be seen from the private sector, where 75 per cent of respondents are projecting to maintain or increase their workforce. In contrast, 72 per cent of respondents of public sector organisations are forecasting a reduction in their staffing levels. Organisations that are planning to change staffing levels identified a number of approaches including; restructuring, natural attrition and redundancy.

Organisations that have recently engaged in recruitment appear to indicate that the number of applicants in the market is higher than last year. Although organisations are receiving a higher volume and quality of applicants, only 18 per cent say that candidates are more flexible in their negotiations. This would suggest that the top talent retain a critical edge on recruiters at the moment, despite the current environment.

Finally, reward professionals appear to be concerned by skill shortages in the coming years. Technical, specialist and engineering skills are specific concerns within the private sector. In the public sector skill shortages will be an issue and respondents identified commissioning, professional and social worker positions as those most likely to be affected.

14

Although organisations are receiving a higher volume and quality of applicants, only 18 per cent suggest that candidates are more flexible in their negotiations. This would suggest that the top talent retain a critical edge on recruiters at the moment, despite the current environment.

Sector Analyses For sectors with ten or more respondents we carried out a separate sector analysis, the results of which are outlined below:

Public and not for profit (PNFP)

It is now widely acknowledged that the public sector is facing up to the most challenging budget cuts it has seen for a generation. As the Coalition Government seek to reduce the levels of public debt, some Local Authorities are seeing cuts of nearly 9 per cent in this year alone while central government spending on police forces in England and Wales will be reduced by 20 per cent in real terms over four years.

With pay and reward forming between 60 and 80 per cent of an organisation’s total costs, the Government has called for restraint at all levels. Feedback from our PNFP respondents points to an acceptance that reform is needed and highlights the desire to introduce some new and innovative practices. However, this comes alongside concerns about the rigidity of existing processes and the effect that these changes will have on recruitment, retention, motivation and engagement.

Concerns about the outcomes of the Comprehensive Spending Review (CSR) can be clearly observed in the results. Nearly half of our PNFP respondents cited these outcomes as the biggest threat to their organisation’s business performance or service delivery in the coming year and 77 per cent believe it has directly affected their organisational priorities for the year ahead.

The threat of compulsory redundancies following the CSR continues to effect motivation and engagement across the board. 91 per cent of organisations surveyed suggested they have already turned to or are planning to turn to restructuring, redundancy, recruitment freezes or a review of terms and conditions within the next 12 months and beyond.

Ensuring staff are engaged when their expectations of the ‘safety’ of the organisations benefits are reviewed. Key challenge identified by a public sector organisation.

15

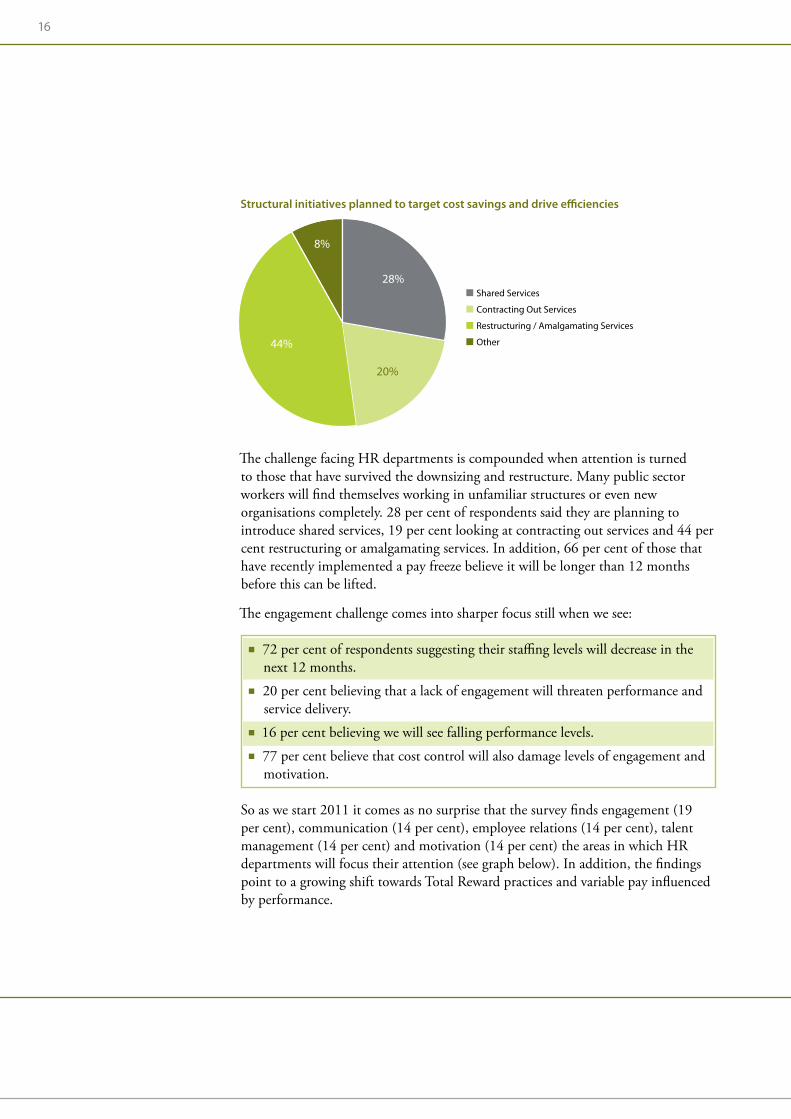

The challenge facing HR departments is compounded when attention is turned to those that have survived the downsizing and restructure. Many public sector workers will find themselves working in unfamiliar structures or even new organisations completely. 28 per cent of respondents said they are planning to introduce shared services, 19 per cent looking at contracting out services and 44 per cent restructuring or amalgamating services. In addition, 66 per cent of those that have recently implemented a pay freeze believe it will be longer than 12 months before this can be lifted.

The engagement challenge comes into sharper focus still when we see:

� 72 per cent of respondents suggesting their staffing levels will decrease in the next 12 months.

� 20 per cent believing that a lack of engagement will threaten performance and service delivery.

� 16 per cent believing we will see falling performance levels.

� 77 per cent believe that cost control will also damage levels of engagement and motivation.

So as we start 2011 it comes as no surprise that the survey finds engagement (19 per cent), communication (14 per cent), employee relations (14 per cent), talent management (14 per cent) and motivation (14 per cent) the areas in which HR departments will focus their attention (see graph below). In addition, the findings point to a growing shift towards Total Reward practices and variable pay influenced by performance.

Structural initiatives planned to target cost savings and drive e�ciencies

Shared Services

Contracting Out Services

Restructuring / Amalgamating Services

Other

8%

20%

28%

44%

16

Currently only 23 per cent of PNFP respondents cite ‘Merit Pay’ as a base for pay progression compared to 32 per cent in the private sector. However, in the next 12 months the area of variable pay / bonuses and terms of employment were the two main areas of change cited. The drivers for these changes were recorded as the need for cost savings, finding efficiencies and a move towards more greatly rewarding higher performers and away from the use of rigid increments based on scale.

The need to better acknowledge and reward high performers in the public sector is clearly a key focus in these challenging times. 69 per cent believe that cost control will damage their ability to retain high performers and several respondents cited a need to emphasise intangible rewards, provide career pathways, invest in training and development and provide opportunities for talented people to keep them engaged and committed.

Public Sector HR focus in 2011

Recognition

Talent management

Motivation

Retention

Employee Engagement

Communication

Reward

Employee Relations

14% 8%

10%

14%

19% 7%

14%

14%

Designing a reward strategy that will continue to reward, recruit and retain high performers whilst cutting costs and finding efficiency savings. Key challenge identified by a public sector organisation.

17

Areas for reward changes in the next 12 months

Base pay

Variable pay / bonuses

Terms of employment

Pensions / retirement bene�ts

Company cars

Health

Other bene�ts

Allowances

Overtime

11% 14%

11%

13%

13%

15%

15%

5%3%

It is clear that the public sector landscape will be a challenging one for the foreseeable future. However, this research highlights a growing appetite to move away from some of the traditional structures and be more flexible in the approach to pay and reward. Reward is clearly a fundamental ingredient in the talent, performance and engagement mix. A move towards flexible working, voluntary benefits, recognition and merit pay should serve to increase levels of engagement and performance, whilst assisting with the drive to contain costs and respond to the challenges of the spending review.

18

Retail

The retail sector is often seen as a barometer for the UK economy. If this is so, the outlook for 2011 is relatively optimistic but there are some significant concerns. The impact from the government’s comprehensive spending review (CSR) and recent VAT increases and therefore consumer confidence remains unclear.

When looking at the retail sector there is a clear divide between the fortunes of the major supermarkets (which generally performed well) and the high street retailers (which saw a much greater impact on sales over the period of the recession.)

64 per cent of respondents said their business performance would be on or above target for 2010, while 36 per cent said it would be below target. However, 75 per cent of organisations in the sector foresee an upturn in business performance within the next 6 to 12 months. All respondent organisations plan to increase salaries in 2011, with a median forecast increase of 2.5 per cent.

According to the respondents of our survey, the main threats to their business performance in 2011 will be the fallout from the government’s comprehensive spending review and ensuring that they maintain high performance in an uncertain environment. Reward and communication will be two major areas of focus for HR in 2011. One supermarket said a key challenge for next 12 months would be:

“managing and communicating reward in an uncertain climate.” While a high street retailer cited ‘managing employee expectations’ as one of the biggest barriers they face when controlling costs of their existing reward programmes. Communicating the value of an employees total remuneration can help promote the value of all elements of their package and thereby help maintain engagement and performance.

Within the retail sector, 66 per cent of organisations are planning to change their reward arrangements in the next 12 months. As a result of the recession many have indicated a move towards pay for performance in the way they manage pay. The pay budget is one of the major costs for retailers (an average of 15 per cent+ as a proportion of their annual turnover) - managing this cost effectively is therefore always high on the agenda.

19

Financial services

It doesn’t seem so long ago that many financial service organisations were on the brink in the midst of the global banking crisis and economic downturn. Our research shows that 2010 was a turning point: 90 per cent of organisations experienced an upturn in business performance in 2010. Over three quarters of respondents report business performance to be on or above target in 2010. All respondents will be increasing base salaries in 2011, the salary forecast is 2.8 per cent, slightly above the general all organisations forecast of 2.5 per cent. Although 2010 was a good year for the sector, with a positive forward looking view, there are some key challenges that will need to be addressed.

Retaining high performers and impact of new legislation were identified by respondents as the main threats to effective business performance / service delivery in 2011.

Now that the Committee of the European Banking Supervisors (CEBS) has published the final guidelines on implementation of the Capital Requirements Directive on remuneration regulations, organisations will need to tackle a number of topics. The first challenge for organisations in the sector will be to understand and determine how the remuneration regulations apply to their organisation, the second challenge will be the implementation of the regulations.

Some of the key areas that will need to be tackled by organisations will be rethinking their incentive and payout design and identifying appropriate pay mixes for different categories of staff.

20

FMCG

The FMCG sector has been resilient during the recession with people continuing to spend money on products such as food and drink. 82 per cent of respondents reported business performance as on or above target in 2010. On the back of this performance, the sector outlook for 2011 is optimistic.

Organisations in this sector were able to adapt their reward strategies relatively quickly in response to the change in economic climate. One consequence of the downturn was the opportunity it gave to reward functions in the sector to re-assess their cost base and to make informed decisions to ensure that they were not severely affected by the global recession. Now the upturn is within touching distance, 100 per cent of our surveyed organisations plan to increase salaries in the next 12 months, with a median salary forecast of 3 per cent.

One of the biggest challenges that respondents say they will be facing during 2011 is the battle to retain key talent. As the marketplace becomes more buoyant, employees will ask themselves whether their current organisation is treating them fairly.

In order to meet this challenge 72 per cent of respondents plan to change their reward arrangements in the next 12 months. The focus will be on variable pay, with a majority citing a move to implementing pay for performance as the main change. FMCG companies are willing to pay their employees well, but only on the basis of strong individual and business performance.

100 per cent of our surveyed organisations plan to increase salaries in the next 12 months, with a median salary forecast of 3 per cent.

21

Oil and Gas

The median projected base salary increase for 2011 within the oil and gas sector is 4.5 per cent, 2 per cent higher than the overall average. This demonstrates that the oil and gas sector reward market has picked up again following the global economic crisis of recent years.

In the coming 12 months, the HR focus for the oil and gas sector will be towards talent management and reward. Almost all companies are concerned about the ongoing shortage of skilled employees for engineering, technical and upstream roles. To combat this, many organisations in the sector are concentrating on creating cost effective, robust pay structures and realigning their reward packages to make them attractive to potential employees.

27 per cent of organisations are also planning to change their pension arrangements; this is most probably around closing final salary schemes. It’s a sure sign that the defined benefit pension scheme is finally coming to an end when cash rich sectors like oil and gas are looking to close them.

Stable oil prices over the last year have helped organisations in the sector record increased profits on last year and this is reflected in the fact that 75 per cent of organisations will be paying out annual bonuses at or above target levels.

Possible legislation changes following on from the Deepwater Horizon drilling rig catastrophe could affect organisations in the next 12 months and beyond. In the US currently no new offshore oil and gas exploration licences are being granted and in Europe the EU has announced plans to introduce tougher controls.

22

Chemicals

The affect of the downturn on the chemicals sector was severe, a drop in demand for chemical supplies in industries such as construction and automotive impacted on revenue. During the worst of the downturn there were a lot of plant closures, redundancies and running down of inventories as part of necessary cost cutting programmes. However the outlook for 2011 is much brighter and the chemicals sector appears to have turned a corner. The hit was shorter and less severe than expected - chemicals organisations are starting to recover.

The projected base salary forecast within the sector is 3 per cent, which is higher than the all industries forecast (2.5 per cent). Over 80 per cent of respondents think business performance will be at or above target for 2010 and over 60 per cent have experienced an upturn in the last 12 months. This combined with organisation’s cost cutting measures during the recession has meant they are once again in a position to offer base pay increases and bonuses. 78 per cent of organisations in the chemicals sector foresee that 2011 short term incentive (bonus) payments for 2010 employee performance will be on or above target.

For the chemicals sector, the HR focus for the coming years will be on talent management, employee engagement and reward. When asked about key challenges for the next 12 months, one respondent summed up the problems affecting the sector well: “Reducing fear and disquiet. Keeping key middle managers engaged and committed whilst making changes they feel will threaten them. Ensuring the changes don’t drive wrong behaviour and are implemented fairly by all.” Respondents were concerned with a shortage of supply in the skill sets of engineering, technical and specialist roles. An ageing workforce compounds this and makes talent management a key priority.

The majority of organisations in the chemicals sector are planning to review their pay and reward structures in the next 12 months, with most companies focusing largely on variable pay and bonuses.

23

A more positive outlook also surrounds short term incentives, with 90 per cent of respondents reporting bonuses will be paid on or above target.

24

Industrial Brands / Manufacturing

The survey participants indicate the outlook for the industrial brands sector is significantly brighter for 2011 than last year. 86 per cent report business performance as on or above target in 2010 and 78 per cent say their organisation has experienced an upturn in the last year. When asked the same questions in last years survey the results were much more downbeat with 69 per cent reporting that business performance would be below target and 40 per cent saying it could take up to 18 months for an upturn to come.

A number of organisations reported recruitment freezes, site closures redundancy and restructuring over the past 12 months however when asked about 2011 this reduces dramatically with many looking to increase staffing levels.

32 per cent respondents reported pay freezes in 2010 showing they have been less prevalent than last years figure of 39 per cent. All participant organisations will be increasing pay in 2011 with a median of 2.6 per cent. A more positive outlook also surrounds short term incentives, with 90 per cent of respondents reporting bonuses will be paid on or above target. While the recession hit the industrial sector hard an upturn in fortunes for this sector has been felt more quickly than expected and a significant improvement in outlook can be seen in the results of this survey.

The Industrial Brands sector has been benefitting from wider economic recovery and a weaker pound has increased demand for UK exports in the manufacturing sector. The seasonally adjusted Markit/CIPS UK Manufacturing Purchasing Managers Index (PMI) reached a score of 58 in November 2010, which was its highest level for 16 years (a score greater than 50 reflects new business growth). While this indicates renewed confidence and demand in the market place, Reward specialists are still expected to continue with an agenda heavily influenced by controlling costs.

Over 40 per cent of respondents agreed that the biggest impact of the recession was over for their organisation. However 80 per cent feel there is pressure to seek efficiencies from reward to contribute to the cost agenda due to wider economic uncertainty. The recession has led to organisations changing the way they manage reward with 69 per cent moving towards managing pay for performance. The main area identified for change was variable pay. In terms of structural initiatives, 62 per cent are planning to target cost savings or drive efficiencies with a move to shared services.

Reward, talent management and employee engagement will be key areas of focus for HR in the next couple of years. As one respondent encapsulates in their answer to their key challenge in the next 12 months: “Ensuring we are competitive in the market place for attracting and retaining employees in key roles.” While another identifies an additional aspect as a key challenge: “The effects of high inflation on our workforce and the resulting expectations on pay increases.”

An increase in demand for skill sets in engineering, technical and IT has been experienced and 68 per cent believe this will be a key area of concern for coming years. Engineering is a skill set identified across different sectors as a function where HR is worried about a future supply of talent.

As the industrial brands sector moves from coping with a recession, it will need to ensure that key talent is motivated, engaged and appropriately rewarded while managing the outcomes from external economic pressures.

25

Key priorities and challenges

HR priorities

The main HR priorities facing reward professionals for 2010, 2011 & 2012 are:

Out of the eight key priorities provided to respondents, reward professionals identified employee engagement and talent management as the most significant to them. Communication, reward (notably variable payments and pensions as discussed previously) and employee relations were all among the priorities for reward professionals in the coming year.

Retention and motivation features less prominently among the responses, although as identified in other sections, retention of high performers is a key concern for most organisations.

The main HR priorities facing reward professionals for 2010, 2011 and 2012 are

20%

15%

10%

5%

0%

HR Focus

2010 2011 2012

Recognition Talent management

Motivation Retention Employee Engagement

Communi-cation

Reward Employee Relations

The main HR priorities facing reward professionals for 2010, 2011 and 2012 are

20%

15%

10%

5%

0%

HR Focus

2010 2011 2012

Recognition Talent management

Motivation Retention Employee Engagement

Communi-cation

Reward Employee Relations

26

Key challenges

Many of the challenges that private sector organisations have faced in recent years endure and are now very much on the agenda of public sector organisations.

Attracting, retaining and motivating employees remain central priorities for organisations in all sectors. However the improving market conditions in the private sector are not alone, a cause for total optimism. Organisations still have to face the challenges of increasing inflation, the impact of public sector job cuts on the economy and uncertainty over the future of interest rates.

Whilst the “Reward in 2011” survey shows some encouraging results within the private sector, it is still worth noting that 32 per cent of private sector organisations agree that the biggest impact of the recession is not over against more than half of public sector respondents.

Below are some of the key challenges that respondents have identified as high on their reward agendas.

“Real” pay

At the time of publishing UK CPI (Consumer Price Index) stands at 3.7 per cent. Therefore the improving salary forecasts in the private sector remain insufficient to counter the effect of inflation. The truth of pay decreases in real terms in the private sector pale in comparison to the impact of public sector forecasts and the widening gap between inflation and salary movements.

Individuals will begin to feel the full impact of rising inflation during 2011 and when the increase in the standard rate of VAT from 17.5 per cent to 20 per cent in January 2011 is added into the equation the value of pay increases of less than 3 per cent and in some cases less than 0.5 per cent will quickly diminish. The true impact of this on employees is still uncertain however it is inevitable that there will be pressure on employers to increase salary budgets or risk losing key talent or failing to recruit effectively. However, with only gentle improvements in business performance and a conservative view on UK GDP growth this will provide a conundrum for organisations and force some difficult choices.

27

Keeping pace

Remaining competitive and meeting more challenging objectives in the context of and improving business performance outlook will test organisations right across UK industry during 2011.

“Balancing pay budgets against the back drop of economic uncertainty. If cost of living continues to rise (e.g. Fuel Bills, VAT, etc) then we may see an increase in discontentment from our currently stable employee base, if our pay budget cannot keep pace.” FMCG organisation.

A staggering 91 per cent of public sector respondents to this research indicated that they are considering restructuring, redundancies, recruitment freezes or a review of terms in the coming twelve months. These are clearly turbulent times in the public sector and the challenge for reward professionals in this market is to remain competitive with considerably fewer levers available to them to tackle employee engagement.

Managing Talent

Talent management is not a new concern for organisations, however it was brought into sharper focus for private sector organisations during the downturn. As budgets were cut and concerns over competitiveness in the marketplace grew, so the clamour to retain key talent and high performers intensified. This report identifies an improving picture in terms of business performance in the private sector into 2011 which goes hand in hand with the 0.5 per cent increase in salary forecasts. However, this is unlikely to make a marked difference to employee opinions and the challenge remains to recognise and effectively remunerate high performers, and many organisation will still see this as a priority.

“Ensuring we are competitive in the market place for attracting and retaining employees in key roles” Business services organisation.

The polarising effect of the recent Comprehensive Spending Review and government austerity measures between the private and public sectors is strongly reflected in this report and will bring specific challenges to the public sector. The now sizable gap in predicted salary forecasts between the private and public sectors may create a landscape of competition for talent from within the public sector that may prove difficult for that sector to withstand. Changing terms of employment, restructuring and contracting out of services within the public sector are reason enough for individuals to be unsettled, however when these factors are coupled with the prospect of salary forecasts of 0.4 per cent then the potential for a “brain drain” from public sector to the private sector is very real.

“Retention, and the ability to provide a talent management program with lack of funds”. Business services organisation.

28

Employee engagement

Organisations remain limited in the scope available to try to balance the cost agenda with the talent agenda. Managing employee expectations appears to be a critical issue within all sectors, as reward professionals need to provide an “offer that is competitive and motivational, whilst controlling costs”. FMCG organisation.

The pressure felt in recent years to seek efficiencies from reward and to ensure that this key element of organisational cost is firmly under control will remain, and will be most notably felt within the public sector. These are necessary measures but they do not come without consequences. For instance, 61 per cent of public sector and 52 per cent of private sector respondents are concerned that cost control will damage the organisation’s ability to retain high performers. Cost controls also raise concerns of the damage on employee engagement and the retention of key skills.

HR and Reward functions have adapted to changing circumstances in many ways during the economic downturn, but a pattern of note is the trend towards increasing the importance and value of variable pay and pay for performance. This pattern is supported by the evidence in this report (23 per cent of organisations intend to make changes to their variable pay arrangements). This is likely to be an area of attention, interest and challenge particularly for the public sector as they look to find ways to motivate, engage and reward without some of the traditional mechanisms at their disposal.

29

Conclusions and recommendationsThere is a growing optimism among reward professionals, with many anticipating a positive outlook for 2011. Pay freezes are less evident, short term incentive payouts are increasing in line with improved business performance and there is confidence that many of the challenges of 2009 and 2010 have been tackled effectively.

Improving business performance, gentle economic upturn and salary forecasts all provide encouraging metrics particularly for private sector organisations however the picture in the public sector is markedly different. Hay Group’s “Reward in 2010” report identified clear sector polarisation in terms of impact of the recession and it is clear from “Reward in 2011” that the importance of market sector is still great, however the dichotomy is now between the public and private sectors and less within the sectors within private industry.

Indeed, these are still difficult times for HR and reward professionals in all sectors despite some of the “green shoots” mentioned above. Government spending cuts will inevitably create challenges for all sectors over time, however it will be in the public sector where the challenge is greatest in 2011. Reward professionals in the public sector will need to do more with less this year, however there is a lot that can be learned from the experiences and the innovative approaches adopted by reward professionals in the private sector during the downturn.

In the current market conditions, wherever possible, organisations need to be actively considering and acting on the following:

� Communication: In an environment where the real value of pay increases to employees is in question it now more important than ever that individuals understand the full value of the reward package that they receive. Variable payments, pensions and healthcare amongst others are all elements of the reward package that may assist in tackling issues around employee engagement and talent management if communicated effectively.

� Innovation: The number of levers available to reward professionals remains limited so the emphasis must be on bringing fresh thinking to what it is organisations are seeking to reward. The value of intangible rewards, for example, the climate and culture of an organisation or the autonomy that individuals experience can be highly valued and should not be ignored when communicating to employees.

� Prioritisation: Reviewing existing reward strategy to ensure that the organisation’s priorities and policies are aligned is very important. This will necessarily take reward professionals back to “first principles” and will identify areas for efficiency saving and/or optimisation which will once again ensure that the, still limited, salary budgets are allocated most effectively.

30

Africa Cape Town Johannesburg Pretoria

Asia Bangkok BeijingHong KongJakarta Kuala LumpurMumbaiNew Delhi SeoulShanghaiShenzhenSingaporeTokyo

Europe Athens BarcelonaBerlin BilbaoBirminghamBratislavaBristolBrusselsBucharestBudapest DublinFrankfurtGlasgow

HelsinkiIstanbulKievLilleLisbonLondon MadridManchesterMilanMoscowOsloParisPrague RomeStockholm StrasbourgViennaVilniusWarsaw ZeistZurich

Middle EastDubaiTel Aviv

North America AtlantaBoston CalgaryCharlotteChicagoDallas

EdmontonHalifaxKansas CityLos AngelesMexico CityMontrealNew York MetroOttawaPhiladelphiaReginaSan FranciscoSan Jose (CR)TorontoVancouverWashington DC Metro

Pacific AucklandBrisbaneCanberraMelbournePerthSydneyWellington

South America BogotaBuenos AiresCaracasLimaSantiagoSao Paulo

Hay Group is a global consulting firm that works with leaders to transform strategy into reality. We develop talent, organise people to be more effective, and motivate them to perform at their best. With 86 offices in 47 countries, we have helped thousands of clients, including private, public and not-for-profit organisations representing every major business category. We focus on change in order to help people and organisations realize their potential.