Embed Size (px)

Citation preview

1

Revised Tennessee Captive Insurance Act:

A New Beginning

Self-Insurance Institute of America, Inc.32nd Annual National Educational Conference & Expo

October 1-3, 2012 Indianapolis, IN

Kevin M. DohertyPresident

The Revised Tennessee Captive Insurance Act (H.B. 2007/S.B. 1540, the “Revised Act”) passed unanimously in both houses of Tennessee General Assembly on May 21, 2011Governor Haslam signed the Revised Act into law on June 10, 2011The Revised Act is Codified in T.C.A. Sections 56-13-101 et seq.

2

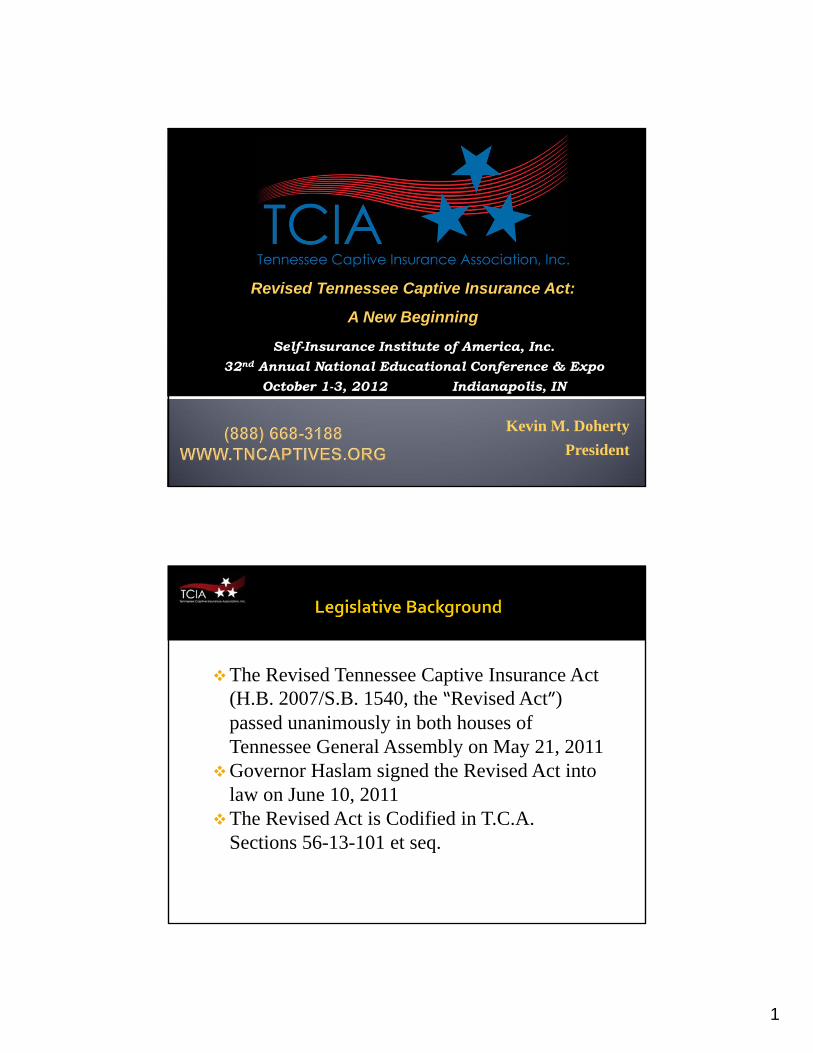

Pure captive insurance company - any company that insures risks of its parent, affiliated companies, or controlled unaffiliated business;Association captive insurance company - any company that insures risks of the member organizations of an association, affiliated companies, or the association itself;

“Industrial Insured Captive Insurance Company” - any company that insures the industrial insureds that comprise its industrial insured group, affiliated companies, and controlled unaffiliated business;

“Industrial insured” means an insured:

(A) Who procures insurance by using a full-time employee acting as an insurance manager or buyer;

(B) Whose aggregate annual premiums for insurance on all risks total at least $25,000; and

(C) Who has at least twenty-five (25) full-time employees.

3

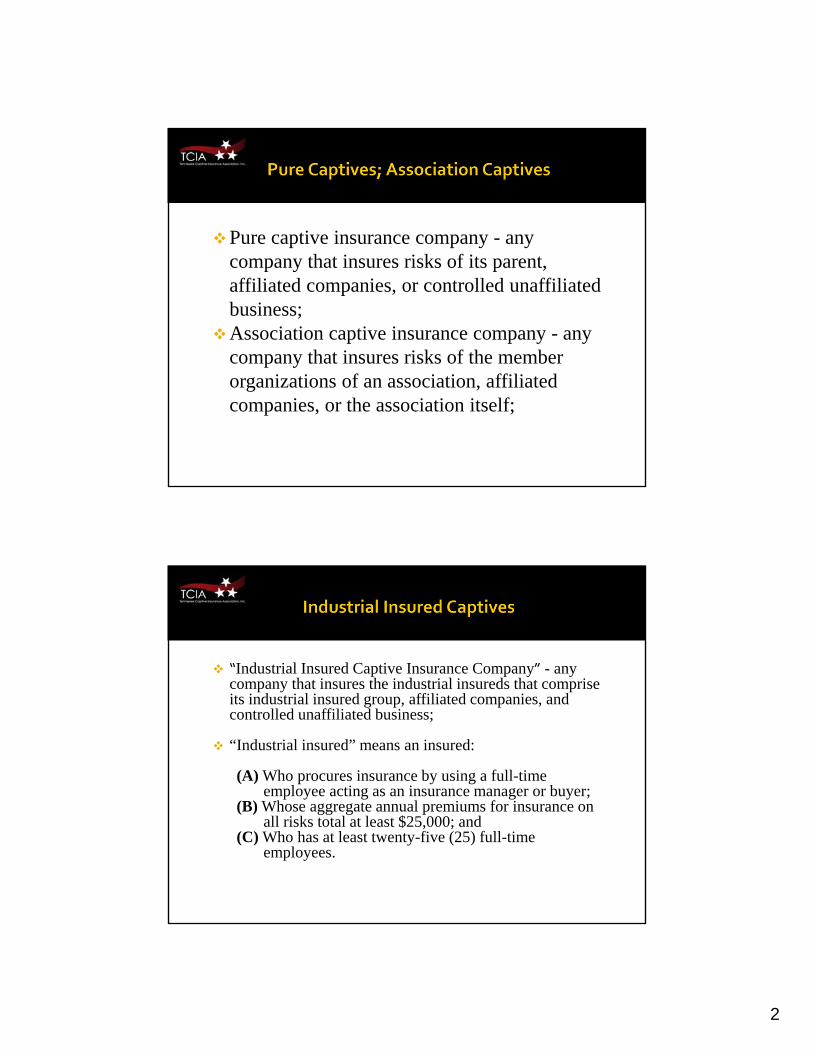

“Protected cell captive insurance company” means any captive:

(A) In which the minimum capital and surplus are provided by one (1) or more protected cell companies;

(B) That is formed or licensed under this chapter;(C) That insures the risks of separate participants through

participant contracts; and(D) That funds its liability to each participant through one

(1) or more protected cells and segregates the assets of each protected cell from the assets of other protected cells and from the assets of the protected cell captive insurance company's general account.

“Incorporated cell captive insurance company” means a protected cell captive insurance company that is established as a corporation or other legal entity separate from its incorporated cells that are also organized as separate legal entities.Can also utilize Series LLC law here in place of a corporation.

4

“Branch captive insurance company” means any alien captive insurance company licensed by the Commissioner to transact insurance in this state through a business unit with a principal place of business in this state. A branch captive insurance company is a pure captive insurance company with respect to operations in this state, unless otherwise permitted by the Commissioner.Branch captives are permitted for ERISA/employee benefits, as well as any other insurance or reinsurance permitted under this chapter.

“SPFC” or “special purpose financial captive” means a captive created for the limited purpose of entering into SPFC contracts and insurance securitization transactions. The creation of SPFCs is intended to achieve greater efficiencies in structuring and executing insurance securitizations, to diversify and broaden sources of capital for insurers, to facilitate access for many insurers to insurance securitization and capital markets financing technology, and to further the economic development and expand the interest of this state through its captive insurance program.

5

“SPFC contract” means a contract between the SPFC and the counterparty pursuant to which the SPFC agrees to provide insurance or reinsurance protection to the counterparty for risks associated with the counterparty's insurance or reinsurance business;SPFCs may provide insurance or reinsurance to a “counterparty” (which may be unaffiliated), including with respect to securitization transactions, subject to the discretion of the Commissioner.

Risk Retention Group - means a captive insurance company organized under the laws of this state pursuant to the Liability Risk Retention Act of 1986, as amended, compiled in 15 U.S.C. § 3901 et seq., as a stock or mutual corporation, a reciprocal or other limited liability entity. Risk retention groups formed under this chapter are subject to all applicable insurance laws, including but not limited to, any applicable provisions in chapters 1, 2, 5, 6, 11, and 45 of this title.

6

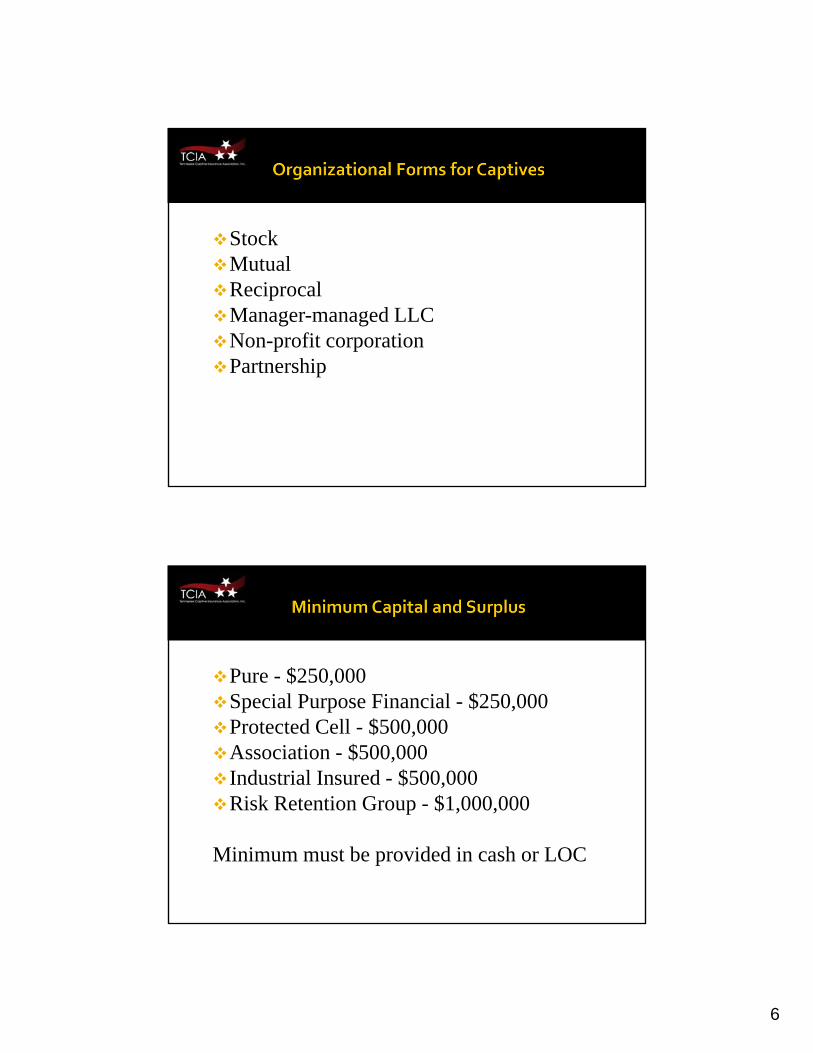

StockMutualReciprocalManager-managed LLCNon-profit corporationPartnership

Pure - $250,000Special Purpose Financial - $250,000Protected Cell - $500,000Association - $500,000Industrial Insured - $500,000Risk Retention Group - $1,000,000

Minimum must be provided in cash or LOC

7

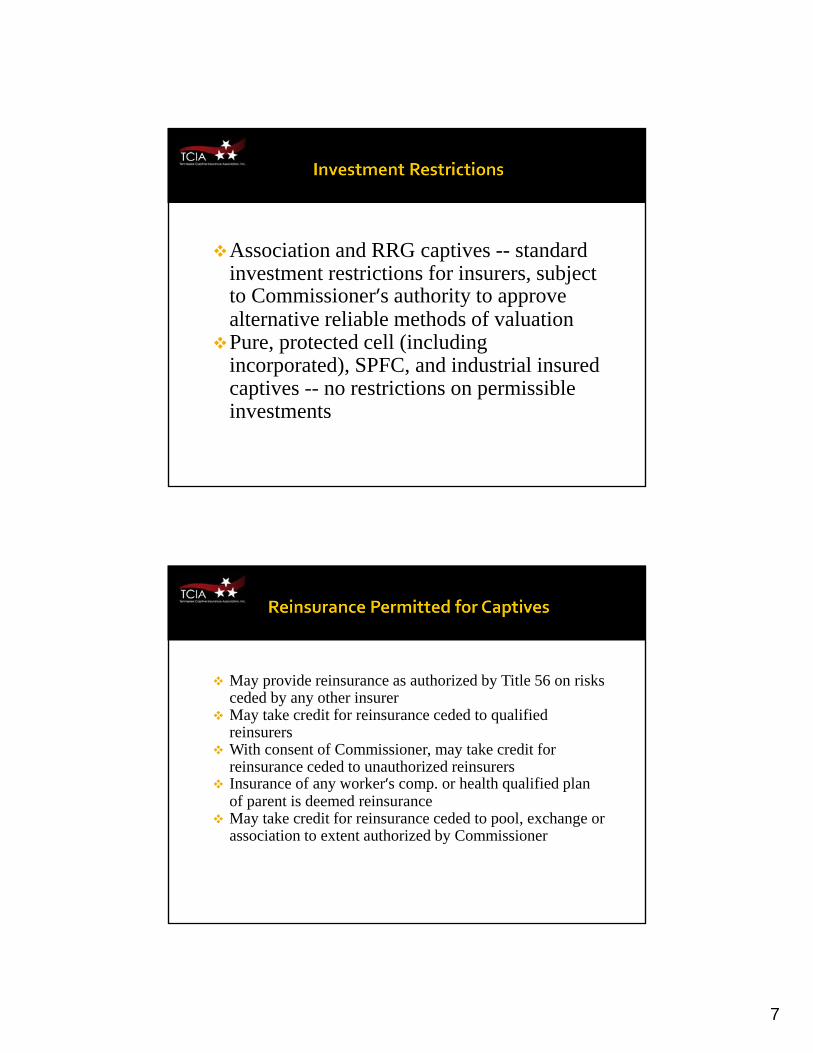

Association and RRG captives -- standard investment restrictions for insurers, subject to Commissioner’s authority to approve alternative reliable methods of valuationPure, protected cell (including incorporated), SPFC, and industrial insured captives -- no restrictions on permissible investments

May provide reinsurance as authorized by Title 56 on risks ceded by any other insurerMay take credit for reinsurance ceded to qualified reinsurersWith consent of Commissioner, may take credit for reinsurance ceded to unauthorized reinsurersInsurance of any worker’s comp. or health qualified plan of parent is deemed reinsuranceMay take credit for reinsurance ceded to pool, exchange or association to extent authorized by Commissioner

8

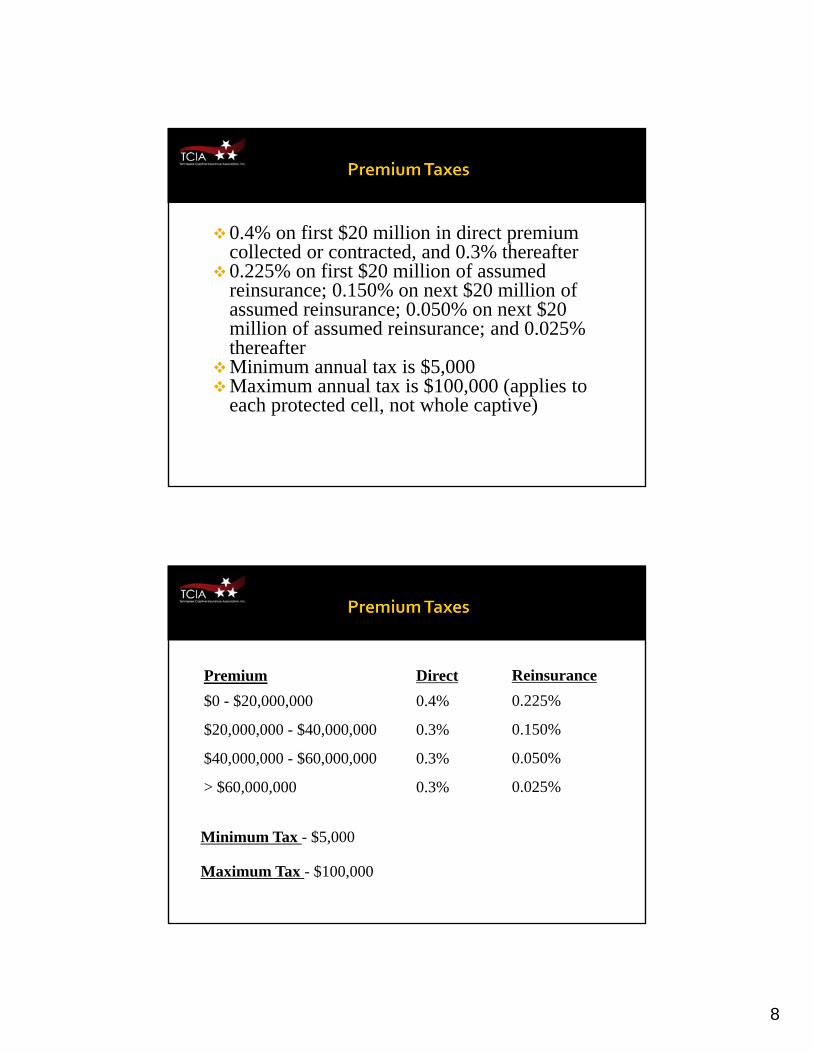

0.4% on first $20 million in direct premium collected or contracted, and 0.3% thereafter0.225% on first $20 million of assumed reinsurance; 0.150% on next $20 million of assumed reinsurance; 0.050% on next $20 million of assumed reinsurance; and 0.025% thereafterMinimum annual tax is $5,000Maximum annual tax is $100,000 (applies to each protected cell, not whole captive)

Premium$0 - $20,000,000

$20,000,000 - $40,000,000

$40,000,000 - $60,000,000

> $60,000,000

Direct0.4%

0.3%

0.3%

0.3%

Reinsurance0.225%

0.150%

0.050%

0.025%

Minimum Tax - $5,000

Maximum Tax - $100,000

9

Insurance treatment under federal tax law permits deferred taxation through deduction of premium payments and losses as well as loss reserves (including incurred but not reported losses – IBNR).Insurance treatment under federal tax law requires risk shifting and risk distribution.Can accomplish risk shifting and risk distribution through either a brother/sister arrangement or by insuring sufficient third party business.

Self-Insurance Institute of America, Inc.

32nd Annual National Educational Conference & ExpoOctober 1-3, 2012Indianapolis, IN

Tennessee Department of Commerce & Insurance

Captive Insurance Department

10

Agenda

A. Commerce & Insurance

B. Regulatory Team

C. Captive Assessment

D. Application

E. Forms

F. Q & A

Commerce & InsuranceTennessee is the second oldest US captive domicile having first passed a captive law in 1978.

Tennessee’s new captive law, contained in the Revised Tennessee Captive Insurance Act, became effective on September 1, 2011.

Changes in the new Act put Tennessee on the leading edge of captive regulations in the United States.

11

Commerce & InsuranceThe Law permits the formation of:

Traditional single parent captives (Pure)Group captivesIndustrial insured captivesRisk retention groupsProtected cell companiesBranch captives, andSpecial purpose financial captives

Regulatory Team

Julie Mix McPeak - Insurance Commissioner

Larry Knight - Assistant Commissioner

Michael A. Corbett - Director – Captive Insurance

Robert J. Ribe - Examinations Director

Tony Greer – Chief Counsel for Insurance

Andrew P. Rhea - Assistant General Counsel

12

FocusTwo primary objectives:

Monitoring the solvency and standards of captive insurance companies.

Ensuring regulation does not hinder the fair operation of the market.

Captive Assessment

The process:Select an authorized captive mangerEngage a qualified law firmArrange a meeting with the Commerce and Insurance Captive Director and staff.

13

Application Process

Two-track process:1. Prepare documents necessary for

incorporation. 2. Prepare documents necessary for

application to the Department.

Steam boat whistle.mp3

Application Process

Sample of additional information required:

Detailed plan of operationSubmit a description of coverage, limits & ratesAdequacy of loss prevention programsFeasibility studyStrength of managementBiographical affidavits

14

Application Process

Minimum Capital & Surplus Deposited with Commerce & Insurance:

Pure - $250,000

Special Purpose Financial - $250,000

Association - $500,000

Industrial - $500,000

Protected Cell - $500,000

RRG - $1,000,000

Application (continued)

Other requirements: The captive manager, CPA and actuary must be approved

by the captive department.

The Department may perform an organizational exam

shortly after issuing the Certificate of Authority.

Application fee - $675

Feasibility Study Review Pass thru: Est. $3,000 - $4,000

No annual license fee

15

Local Representation Requirements

Annual Directors meeting in Tennessee

Principal place of business in Tennessee

One board member must be a Tennessee

resident

Forms & Information

Forms & information available online (www.tn.gov/commerce/insurance/captive)

Application form

Biographical affidavit

Approval forms for managers, actuaries & CPA firms

List of currently approved managers, actuaries & CPAs

Index format for captive application

Letter of credit form

Helpful links

16

Comments, Questions & Suggestions

State of TennesseeDepartment of Commerce & Insurance

Captive Insurance Department

Working to create a world class captive insurance domicile in Tennessee

(888) 668-3188www.tncaptives.org