Embed Size (px)

Citation preview

Review of Price Control Arrangements

An ACCC Discussion Paper

June 2004

Contents

1. INTRODUCTION .........................................................................................................4

1.1 PURPOSE .........................................................................................................................4

2. TIMETABLE AND INQUIRY PROCESS .................................................................6

2.1 MAKING A SUBMISSION TO THE PUBLIC INQUIRY ........................................................6

3. TERMS OF REFERENCE...........................................................................................8

4. BACKGROUND..........................................................................................................10

4.1 EFFICIENCY OBJECTIVES.............................................................................................11 4.2 SOCIAL POLICY/EQUITY OBJECTIVES .........................................................................11 4.3 PREVIOUS REVIEW OF PRICE CONTROL ARRANGEMENTS.........................................11

ACCC RECOMMENDATIONS ..........................................................................................12 4.4 CURRENT PRICE CONTROL ARRANGEMENTS .............................................................13 4.5 OTHER ARRANGEMENTS WHICH MAY AFFECT TELSTRA’S RETAIL PRICING...........15

5. MATTERS SUBMISSIONS SHOULD ADDRESS..................................................17

5.1 CURRENT STATE OF COMPETITION IN MARKETS .......................................................17 5.2 IMPACT OF PRICE CONTROLS ON COMPETITION, AVAILABILITY, CHOICE, QUALITY, PRICE AND INVESTMENT ...........................................................................................................19

IMPACT ON COMPETITION ..............................................................................................19 IMPACT ON AVAILABILITY, CHOICE, QUALITY AND PRICE.............................................22 IMPACT ON ECONOMICALLY EFFICIENT INVESTMENT DECISIONS..................................23

5.3 DISTRIBUTIONAL IMPACTS ..........................................................................................25 IMPACT ON DIFFERENT TYPES OF HOUSEHOLD AND BUSINESS CONSUMERS .................25 IMPACT ON DIFFERENT GEOGRAPHIC AREAS .................................................................28 DATA REQUIREMENTS....................................................................................................29

5.4 NEW AND EMERGING TECHNOLOGIES ........................................................................29 IMPACT ON PRICE CONTROL ARRANGEMENTS ...............................................................30 IMPACT OF PRICE CONTROL ARRANGEMENTS................................................................31

5.5 PROTECTION OF DISADVANTAGED GROUPS ...............................................................32 5.6 OTHER RELATED CONSIDERATIONS............................................................................34

CARRY-OVER CREDITS...................................................................................................34 ASSESSING AND ENFORCING COMPLIANCE....................................................................35 DURATION......................................................................................................................36

6. SUMMARY OF QUESTIONS ...................................................................................37

APPENDIX 1 MINISTERIAL DIRECTION.....................................................................41

3

APPENDIX 2 EFFICIENCY CONCEPTS.........................................................................43

APPENDIX 3 TERMS OF REFERENCE FOR PREVIOUS REVIEW .........................45

APPENDIX 4 HISTORY OF THE PRICE CONTROL ARRANGEMENTS ................47

4

1. Introduction

The Minister for Communications, Information Technology and the Arts (the Minister) has directed the Australian Competition and Consumer Commission (the Commission) to hold a public inquiry about the nature of price arrangements, which the Commission administers, that should apply to Telstra after the current arrangements – Telstra Carrier Charges – Price Control Arrangements, Notifications and Disallowance Determination No.1 of 2002 (the Determination) – expire on 30 June 2005. The Commission must report to the Minister by 31 January 2005.

In conducting the public inquiry, the Commission is required to consider, among other things, what form any future price control arrangements should take, including their duration, means of implementation, whether any complementary arrangements are necessary and mechanisms for assessing/enforcing compliance.

Price control arrangements of the form spelt out in the Determination were first introduced in 1989. Since that time, Telstra (or its predecessors, Telecom and the Overseas Telecommunications Corporation) has been subject to price controls on a range of telephony services.1 Price controls are considered a key telecommunications consumer safeguard that aim to ensure that efficiency improvements are passed through to consumers in the form of lower prices for telecommunications services in markets where competition is not yet fully developed. They have also been used as a tool for achieving the government’s social policy/equity objectives.

Since their introduction, the government has commissioned periodic reviews of the price control arrangements. The most recent review concluded in 2001. These reviews have proven necessary as the telecommunications industry has gone through a number of changes since 1989. In particular, the telecommunications market has evolved from one that was supplied solely by two government-owned enterprises, to one that is now serviced by numerous carriers and carriage service providers (CSPs).

1.1 Purpose

Under Division 3 of Part 25 of the Telecommunications Act 1997 (the Telecommunications Act), the Commission may choose, after deciding to hold a public inquiry about a matter, to prepare a Discussion Paper. A Discussion Paper identifies those issues that the Commission considers relevant to the matter in question, and sets out background material and discussion of those issues.

1 A summary history of the price control arrangements that have applied to Telstra and its predecessors since 1989 is at Appendix 4.

5

The purpose of this Discussion Paper, therefore, is to:

identify the issues which, in the Commission’s opinion, are relevant to a public discussion regarding the nature of the current price control arrangements and those that should apply to Telstra from 1 July 2005 onwards; and

set out background material about, and discussion of, those issues which the Commission thinks should be considered in a public process and which the Commission seeks comment on from industry participants, interest groups (including end-users) and the public more generally.

Section Two outlines the timetable and process for the public inquiry.

Section Three sets out the terms of reference for the public inquiry.

Section Four provides background information on the price control and other regulatory arrangements that apply to Telstra.

Section Five sets out the matters that the Commission would like submissions to address.

Section Six lists the questions the Commission has raised in the Discussion Paper.

Appendix One contains a copy of the Ministerial Direction that was given to the Commission.

Appendix Two contains discussion of some relevant efficiency concepts.

Appendix Three sets out the terms of reference for the previous review of the price control arrangements.

Appendix Four contains a summary history of the price control arrangements that have applied to Telstra (and its predecessors) since 1989.

6

2. Timetable and inquiry process

Under Division 3 of Part 25 of the Telecommunications Act, the Commission must provide a reasonable opportunity for any member of the public to make a written submission to a public inquiry. In particular, sub-section 500(2) specifies that a period of at least 28 days must be provided for the public to make written submissions to the Commission. Accordingly, the Commission requests written submissions by 13 August 2004.

Section 501 of the Telecommunications Act specifies that the Commission may hold hearings for the purpose of a public inquiry in order to receive submissions, or to provide a forum for public discussion of relevant issues. The Commission proposes to undertake a two-week public consultation process, which may involve a series of public hearings around various parts of the country during August. The dates of the public consultation process will be announced after submissions on the Discussion Paper have been received.

The Commission expects that it will publish a Draft Report setting out its preliminary findings by the end of October 2004. The Commission will then provide an opportunity to comment on the Draft Report prior to finalising the report by 31 January 2005.

In summary, the timetable for this inquiry is:

Release of Discussion Paper End June 2004

Deadline for written submissions on Discussion Paper 13 August 2004

Two-week public consultation process Mid/End-August (dates to be announced)

Draft Report End October 2004

Deadline for written submission on Draft Report End November 2004

Final Report 31 January 2005

2.1 Making a submission to the public inquiry

The Commission encourages all industry participants, interest groups and the public more generally to consider the matters set out in this Discussion Paper, and to make submissions to the Commission to assist its review of the current, and possible future, price control arrangements to apply to Telstra.

Although the Commission has developed a list of questions in this Discussion Paper to assist those parties which intend to make a submission, this list should in no way restrict submitters that wish to comment on other issues/matters.

7

To foster an informed and robust consultative process, the Commission proposes to treat all submissions as non-confidential, unless the submission contains information of a confidential nature and the author requests that the submission, or parts thereof, be kept confidential. Non-confidential written submissions given to the Commission will be made available to interested parties upon request.

Submissions can be addressed to:

Mr Sean Riordan Acting Director Telecommunications Regulatory Australian Competition and Consumer Commission GPO Box 520J Melbourne VIC 3001 Facsimile: (03) 9663 3699

In addition to a hard copy, those making submissions are requested, if they are able, to provide an electronic copy to [email protected].

Enquiries can be made to Sean Riordan on (03) 9290 1889.

8

3. Terms of reference

Under sub-section 496(1) of the Telecommunications Act, the Minister has the power to direct the Commission to hold a public inquiry about a matter concerning carriage services, content services or the telecommunications industry.

Under Part 9 of the Telecommunications (Consumer Protection and Service Standards) Act 1999, the Minister may specify that certain carrier charges should be subject to price control arrangements. In particular, section 154(1) specifies that the Minister may determine (in writing) that specified carrier charges may be subject to price control arrangements. Further, section 155(1) specifies that where charges are subject to price control arrangements, the Minister may determine (in writing) the price-cap arrangements and other price control arrangements to be applied in relation to the specific charges, and the principles which Telstra must comply with when making alterations to the charges. Telstra must comply with any such determination.

On 23 April 2004, the Minister directed the Commission to hold a public inquiry about the nature of price control arrangements that should apply to Telstra after the expiry of the current price control arrangements on 30 June 2005. A copy of this Direction is at Appendix 1.

In this Direction, the Minister requires the Commission to consider, among other things:

the appropriate form of future price control arrangements, including the composition of baskets and the level of price caps;

the duration of any such arrangements;

the means of implementation of any such arrangements;

whether any complementary arrangements are required to work in conjunction with the future price controls and, if so, their nature; and

mechanisms for assessing and enforcing compliance.

In addition, the Commission was directed to have regard to the following matters when holding the public inquiry:

the current state of competition in each of the markets that the Commission considers relevant;

the impact of the current price control arrangements, and possible future price control arrangements, on:

- competition and the future development of competition, having regard in particular to the telecommunications anti-competitive conduct regime under Parts XIB and XIC of the Trade Practices Act 1974;

9

- the availability, choice, quality and prices of services to consumers and any other impacts on consumers; and

- the telecommunications industry, including on economically efficient investment decisions;

the distribution of the short-term and long-term community and economic benefits and costs, including the impacts on different types of households and business consumers and geographic areas, from the current price control arrangements and, possible future price control arrangements, in particular, relating to any re-balancing of line rental and call charges;

the implications of new and emerging technologies on price control arrangements and of price control arrangements on new and emerging technologies; and

the appropriateness of the current price control arrangements, and possible future price control arrangements, for the protection of potentially disadvantaged residential and business customers in both metropolitan and rural areas.

10

4. Background

Price control arrangements, particularly those of the ‘CPI − X’ variety, have been aimed at promoting efficient pricing outcomes in telecommunications markets as well as achieving certain social policy/equity objectives. The underlying principle of CPI − X price controls is that prices should be able to move to reflect changes in underlying unit costs. In the current context, ‘CPI’ represents the change in the consumer price index while ‘X’ is a measure of firm or service-specific productivity growth, which is broadly, the difference between the growth of output and the growth of inputs used.

CPI − X price controls are designed to:

limit the ability of Telstra to set prices above costs;

provide an incentive to seek cost efficiencies in order to meet its price control obligations; and

allow Telstra to ‘rebalance’ its prices for greater efficiency.

Consider first the problem of a supplier being able to set prices above costs. Under normal circumstances, a supplier that has market power may have an incentive to price above-cost to extract as many rents as possible from a given market. Such profit maximising behaviour may be inefficient from a social welfare perspective as it could lead to higher prices for end-users and lower levels of output being consumed. CPI − X price controls can help prevent these efficiency losses by limiting the extent to which a firm with market power can price above-cost.

A second problem is that a supplier with market power may have less of an incentive to pursue cost efficiencies compared to firms operating in a highly competitive market. CPI − X per cent price controls aim to provide an incentive to achieve cost efficiencies in order to meet, and perhaps even exceed, those required by regulation.

A third justification for having CPI − X price controls on baskets of telecommunications services is that they give firms the freedom to structure their prices in a way that efficiently recovers ‘common’ costs of production. That is, the production of a series of telecommunications services often involves a number of common costs – or costs that cannot be attributed to a particular service and therefore can be allocated (using different methodologies) in some way across all services.

The stated objectives of the current price control arrangements are to:

(a) promote efficiency in markets not yet effectively competitive and pass on the benefits to consumers;

(b) protect low-income consumers from any adverse effects of line rental increases;

(c) ensure rural and remote customers share in benefits from greater competition;

11

(d) allow Telstra to gradually rebalance line rentals; and

(e) meet other equity objectives.2

These objectives are consistent with those that apply to the regulation of telecommunications more generally, the principle objective of which is the promotion of the long-term interests of end-users (the LTIE).3

This section provides some background on the nature of these efficiency and social policy/equity objectives. It then outlines the Commission’s recommendations flowing from its previous review of the price control arrangements and summarises the current price control arrangements that apply to Telstra.

4.1 Efficiency objectives

In the past, the Commission has outlined three major types of efficiency that it believes are relevant to the pricing of telecommunications services. These are referred to as productive, allocative and dynamic efficiency. A brief description of each type of efficiency is provided in Appendix 2, along with an indication of how it may be relevant to determining price control arrangements.

4.2 Social policy/equity objectives

A second major objective of the price control arrangements has been the achievement of certain social policy/equity objectives. In this regard, the government has been keen to ensure that consumers from different geographic areas and with different income levels are able to have access to affordable telecommunications services and share in the benefits arising from more competitive markets. The Commission notes that an issue for consideration during this public inquiry is whether there are alternative ways of structuring price controls in order to achieve given social policy objectives. This matter will be discussed further in sections 5.3 and 5.5.

4.3 Previous review of price control arrangements

In August 2000, the Commission was directed by the Minister to undertake a review of the Telstra price controls which the Commission administers. A copy of the Ministerial terms of reference for this review is at Appendix 3.

This terms of reference required the Commission to hold a public inquiry into whether there was a need for price control arrangements on Telstra to continue after the expiry of the Minister’s existing determination, the Carrier Charges – Price Control Arrangements, Notifications and Disallowance Determination No. 1 of 2000, on 30 June 2001.

2 DCITA, Telstra Carrier Charges – Price Control Arrangements…− Regulation Impact Statement, p. 4. 3 See section 3 of the Telecommunications Act 1997 for a complete list of these objectives.

12

They also specified that should the Commission consider there was still a need for price control arrangements after this time, that the public inquiry determine what form they should take, including the duration, means of implementation and mechanisms for their review.

ACCC recommendations On 14 February 2001, the Commission provided the Minister with its Final Report. This report contained a series of recommendations on what form it considered future price control arrangements should take.4 These recommendations included: Of the services that were subject to retail price control arrangements in the existing

price control determination (line rental, local calls, national long distance, international long distance, fixed-to-mobile (FTM), connections, mobile phone services and leased line services), price control arrangements should be retained on all of these services except mobile phone and leased line services;

Those services that should remain subject to retail price control arrangements should be subject to a broad CPI – X per cent price cap. Under this form of price control, Telstra would be required to reduce the ‘weighted-average’ price of the price controlled services by CPI – X per cent each year;

The level of X for the broad basket of services should be in the order of 5 per cent per annum, and should apply for a period of three years;

All other existing sub-caps in the existing price control arrangements (other than the 22 cent sub-cap on local calls) and the local call parity requirement (which required the average price of local calls in non-metropolitan areas to be reduced by roughly the same amount as the average price in metropolitan areas in any given period) should be removed;

There should be an adjustment period over which rebalancing of line rental should be allowed to occur. The Commission recommended that this period not exceed 5 years;

The revenue weights used to determine whether Telstra had complied with its price control arrangements should be based on past year revenue levels;

Targeting of low-income groups should be based on measures of income rather than usage levels for telecommunications services; and

Targeted assistance or other equity measures recommended in the report should be funded from government or industry-based sources.

4 ACCC, Review of Price Control Arrangements, February 2001, can be viewed at: http://www.accc.gov.au/content/item.phtml?itemId=341837&nodeId=file3fadbdda9deb4&fn=Final%20report_Review%20price%20control_Feb01.pdf

13

The Commission also advised that the under-recovered amount of one three-year period of price control arrangements should not be ‘carried over’ (i.e. carried forward) to the next three-year period of price control arrangements.

The rationale for the Commission’s recommendations on line rental charges was that the price of residential line rental was only around 55 per cent of the full cost of provision for residential consumers. Hence, the immediate removal of all price controls on line rental could potentially see Telstra almost double the price of line rental for residential consumers. The Commission was concerned that this might have some severe and potentially unwanted distributional consequences.

It was also considered that the full benefits the Commission’s recommendations could only be achieved if they were applied in concert. Following receipt of the Final Report, the Minister rolled over the existing price control Determination for a further year, and the Department of Communications, Information and Technology and the Arts (DCITA) conducted a subsequent public consultation process with interested parties to ascertain further views on the Commission’s recommendations. The price control arrangements introduced by the Government and applying to Telstra for the period 1 July 2002 to 30 June 2005 are set out in the Minister’s current Determination. A copy of the current price control arrangements can be located at http://scaleplus.law.gov.au/html/instruments/0/97/0/2003091601.htm

4.4 Current price control arrangements

The central framework of the current price control arrangements comprises price caps that apply to three separate baskets of services as outlined below.

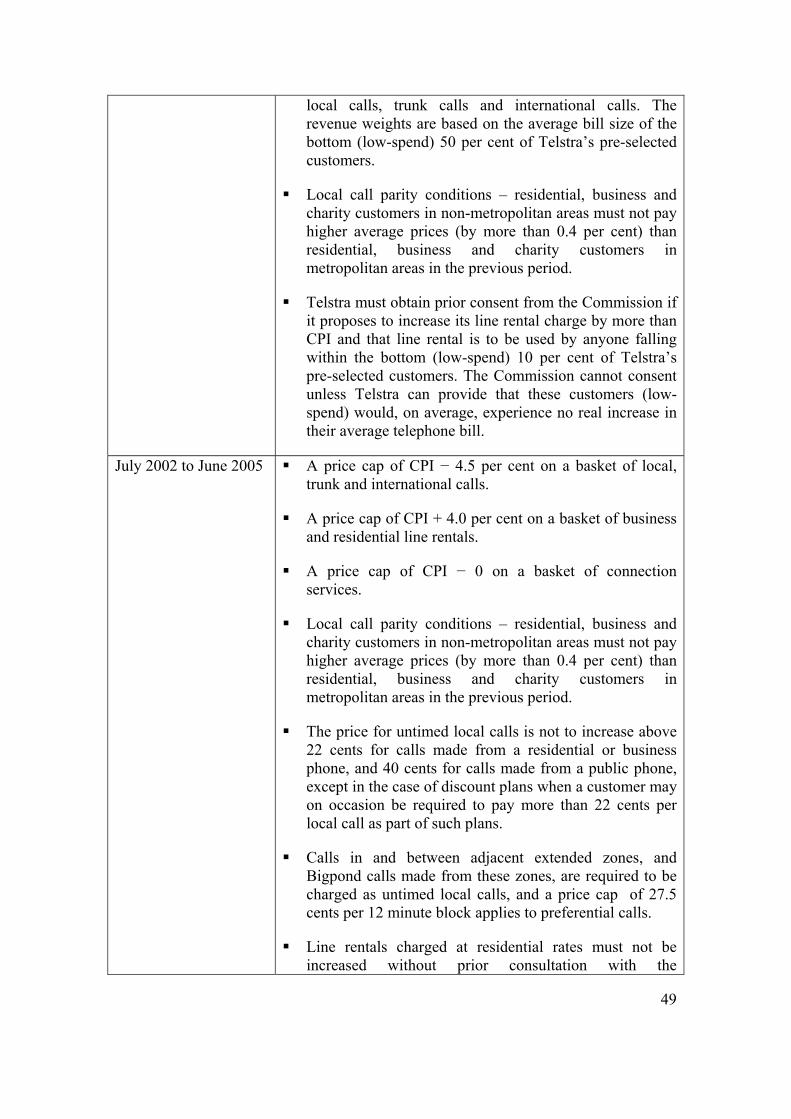

1) A price cap of CPI − 4.5 per cent on a basket of local, trunk (which includes national long distance and FTM services) and international calls. This means that Telstra is entitled to change the individual prices of these services as long as the aggregate price of all the services in the basket declines by 4.5 per cent annually in real terms (i.e. net of inflation).

2) A price cap of CPI + 4.0 per cent on a basket of business and residential line rentals. This means that any increase in average line rental charges in excess of CPI must be limited to 4.0 per cent annually in real terms.

3) A price cap of CPI − 0 on a basket of connection services. This means that the overall revenue-weighted price for these services must not rise in real terms in any given year.

The Determination provides that each price cap is an independent price cap and is not subject to any overall price cap. That is, price movements for each basket do not need to fit within a weighted average price movement for all services.

14

The Determination also provides for a number of other price controls that apply to a range of services.

The revenue-weighted average untimed local call price for residential and charity customers in non-metropolitan Australia in a given financial year is not to exceed the revenue-weighted average untimed local call price for residential and charity customers in metropolitan Australia in the previous financial year by more than 0.4 per cent.

The revenue-weighted average untimed local call price for business customers in non-metropolitan Australia in a given financial year is not to exceed the revenue-weighted average untimed local call price for business customers in metropolitan Australia in the previous financial year by more than 0.4 per cent.

The price for untimed local calls is not to increase above 22 cents for calls made from a residential or business phone, and 40 cents for calls made from a public phone, except in the case of discount plans when a customer may on occasion be required to pay more than 22 cents per local call as part of such plans.

Calls in and between adjacent extended zones, and Bigpond calls made from these zones, are required to be charged as untimed local calls, and a price cap of 27.5 cents per 12 minute block applies to preferential calls.

Line rentals charged at residential rates must not be increased without prior consultation with the Commission and it being satisfied that Telstra has complied with clause 22 of the Carrier License Conditions (Telstra Corporation Limited) Declaration 1997 to have in place a low-income package. This Declaration includes a requirement that Telstra consult with the Low-Income Measures Assessment Committee (LIMAC) if it makes changes to the low-income package.5 This is discussed further in section 4.5 below.

Telstra must notify the Minister in advance if it intends to alter charges for directory assistance services, with the Minister able to disallow the proposed changes if they are considered not to be in the public interest.

Telstra must offer a line rental service to schools at a price at or below the standard line rental offered to residential customers.

Telstra is required to report to the Commission in relation to its compliance with the price control arrangements, before the end of three months after the end of the financial year in which a price-cap applies.

5 The LIMAC comprises representatives of welfare organisations agreed to by the Minister and it responsible for reporting annually to the Minister on the effectiveness of the low-income package and its marketing by Telstra; and assessing proposed changes to the package or Telstra’s marketing plan for the package.

15

4.5 Other arrangements which may affect Telstra’s retail pricing

As previously noted, the Commission has been directed to hold a public inquiry about the nature of price control arrangements that should apply to Telstra. Accordingly, the Commission interprets this as a direction to assess/review the current price controls with a view to determining the nature/form of future price control arrangements that should apply to Telstra from 1 July 2005 onwards.

Notwithstanding this, the Commission notes that in addition to price control arrangements, Telstra is subject to a number of other regulatory arrangements which affect the price it can charge in certain telecommunications markets. A summary of these other arrangement is provided below.

As noted in section 4.4 above, the current price control arrangements require that line rentals charged at residential rates must not be increased without prior consultation with the Commission and it being satisfied that Telstra has complied with clause 22 of the Carrier License Conditions (Telstra Corporation Limited) Declaration 1997.6 It is important to note, however, that this Declaration is a separate legislative instrument from the price control arrangements, and is administered by the Australian Communications Authority (ACA). In effect, this means that the Commission has a strictly limited role in ensuring that Telstra complies with the low-income measures outlined above.7

Telstra is also subject to a telecommunications-specific regulatory regime, under Parts XIB and XIC of the Trade Practices Act 1974 (the Act) which are administered by the Commission.

Part XIB of the Act prohibits a carrier or CSP from engaging in anti-competitive conduct – a prohibition known as the competition rule.

Part XIC of the Act, aims to promote competition in telecommunications markets by establishing the rights of third parties to gain access to certain (declared) services provided by Telstra’s infrastructure which are needed by such parties in order for them to provide telecommunications services. Under this provision, the Commission may be required to arbitrate disputes concerning the terms and conditions (including price) of access. 8 There is a question of how any access price determination by the Commission 6 Clause 22 was introduced as an amendment to the Carrier License Conditions (Telstra Corporation Limited) Declaration 1997 in 2002 to coincide with the introduction of the current price control arrangements that apply to Telstra. 7 Sub-clause 22(1) of this Declaration provided that by 1 July 2001 Telstra was required to offer, or have a plan for offering, products and arrangements to low-income customers that has been endorsed by low-income consumer advocacy groups and notified in writing to the ACA. Moreover, sub-clause 22(4) provides that Telstra must maintain and adequately resource LIMAC which was to comprise representatives of such organisations as approved by the Minister in writing from time to time. 8 In its Access Pricing Principles Telecommunications – a guide (1997) the Commission indicates that the prices of services declared under Part XIC that are necessary for competition in telecommunications markets should, in the usual case, be cost-based. The Commission went on to note that, in the usual case, cost-based pricing of access services in telecommunications will encourage efficient entry into telecommunications markets and economically efficient investment in telecommunications infrastructure.

16

relating to Telstra’s declared access (or wholesale) services might interact with the retail price controls that are the subject of this review. This issue will be explored in more detail in section 5.2.

Under Division 2 of Part 2 of the Telecommunications (Consumer Protection and Service Standards) Act 1999, Telstra is subject to a Universal Service Obligation (USO). The main requirement of the USO is that standard telephone services, payphones and prescribed carriage services are reasonably available to all people in Australia on an equitable basis. There is also an obligation relating to access to digital data services. At present, Telstra is the universal service provider (USP). To the extent that this might generate losses for Telstra because the provision of services to customers in certain parts of Australia generates revenues below the cost of supply, the Universal Service regime allows for the losses to be shared amongst all carriers in proportion to their aggregate telecommunications revenue. Hence, Telstra is able to recover some of its losses from the USO from other carriers in the telecommunications industry.

Amendments to the Telecommunications (Customer Protection and Service Standards) Act 1999 opened Universal Service Provision to competitive tendering where successful tenderers become the Universal Service Provider in specified zones. The contestability arrangements commenced on 1 July 2001, although the Commission understands that no alternative suppliers have sought to tender to provide USO services in these areas.

The USO arrangements have recently been reviewed by DCITA, and its findings were released on 17 June 2004. DCITA has recommended, among other things, that Telstra should fund all costs associated with fulfilling the historic telephony USO.9

9 DCITA’s findings can be viewed at http://www.dcita.gov.au/Article/0,,0_1-2_1-3_143-4_119242,00.html

17

5. Matters submissions should address

In order to help facilitate the public inquiry process, the Commission has identified a series of issues that it considers pertinent to addressing the terms of reference outlined in section 3. These issues are divided up in accordance with the matters the Commission has been directed to have regard to, as well as a section on the other issues which the Commission considers important.

A complete list of all the questions raised in this section is provided in section 6.

5.1 Current state of competition in markets

Assessing the extent of competition in the markets within which telecommunications services are supplied is a key consideration in determining the possible future price control arrangements that should apply to Telstra.

To the extent that price controls are considered necessary in markets where market discipline does not constrain Telstra’s market power, it follows that where it operates in an effectively competitive market there is no need on efficiency grounds to maintain price controls.10 Moreover, where the nature and/or extent of competition has changed in a particular telecommunications market, there may be a case for removing the price control constraints which currently exist, changing the nature/structure of price controls that already apply to a service or re-introducing price controls on a particular retail service – depending on the most recent competition assessment.

In the Commission’s 2001 review of the price control arrangements it concluded that retail price controls should be retained on line rental, local call, national long distance, FTM, international long distance and connection services. In reaching this view, the Commission noted that competition had not yet developed fully in the markets in which local calls, line rentals and connection services were supplied, and that it was not convinced that competitive forces were sufficiently strong enough to achieve effectively competitive pricing outcomes in the markets in which national long distance, international long distance and FTM services were supplied. On the other hand, the Commission considered that the market for the supply of mobile services had become sufficiently competitive such that it should be removed from the price control arrangements. Further, it considered that leased line services did not really fit within the objectives of the price control arrangements and their ongoing inclusion created administrative difficulties.

Subsequent analysis by Commission in its Emerging market structures in the communications sector report (June 2003) supported the view that Telstra’s vertical and horizontal integration, and the market power that this provides it with, suggests that there is not yet effective competition in a range of telecommunications markets –

10 However, this would still leave a possible distributional justification for maintaining price controls (discussed in sections 5.3 and 5.5), albeit one which may involve some trade-off with efficiency goals.

18

including those that are currently subject to retail price control arrangements.11 Similar conclusions have been reached by the Commission in more recent analysis.

The Commission’s Telecommunications competitive safeguards for the 2002-03 financial year report (June 2004)12 noted that although a limited degree of competition has emerged in the market within which local telecommunications services (i.e. local call and line rental services) are provided, Telstra remains dominant in most areas due to its ownership of the only ubiquitous fixed-line local access network in Australia – the customer access network (CAN). Similarly, in relation to national long distance and international call services, the Commission noted that despite some encouraging signs of competition, Telstra still retains a commanding presence in these markets since most of its competitors continue to rely on access to its CAN network if they want to supply these services.

In March 2004, the Commission released its draft decision that the declaration of the GSM mobile termination service should be extended and that the price of the mobile termination service should be gradually decreased towards a conservative benchmarked target of 12 cents per minute over a staged adjustment period commencing on 1 July 2004 and concluding on 1 January 2007.13 In its draft decision, the Commission expressed a view that while the retail mobile services market is exhibiting more encouraging market outcomes than the markets for fixed-line telecommunications services, it is not considered fully competitive. Further, the draft decision re-affirmed the Commission’s view that the markets within which FTM services are provided are still not effectively competitive.

The Commission’s analysis about the state of competition in these markets may have an important bearing on the appropriate price control arrangements that should apply to Telstra for these services in the future.

One issue raised by submitters during the mobile review is whether FTM services need to be subject to a specific sub-cap – as opposed to just being included in a broad basket of call services – to ensure that reduced input costs are fully passed on to consumers. While the Commission’s draft decision did not favour a specific sub-cap on FTM prices, it did observe that the current retail price controls have exerted a weaker constraint on Telstra’s FTM pricing than under the previous regime, and this has coincided with FTM prices ceasing to decrease.

The Commission is seeking comment on the following issues in relation to the current state of competition in telecommunications markets.

11 A copy of the ACCC’s Emerging market structures in the communications sector (June 2003) report can be viewed at: http://www.accc.gov.au/content/index.phtml/itemId/337611. 12 This report was tabled in the House of Representatives on 17 June 2004. A copy of this report can be viewed at http://www.accc.gov.au/content/index.phtml/itemId/269251/fromItemId/3881. 13 The Commission’s Mobile Terminating Access Service – Draft decision on whether the Commission should extend, vary or revoke its existing determination of the mobile terminating access service (March -2004) is at http://www.accc.gov.au/content/index.phtml/itemId/333898/fromItemId/356715.

19

Questions to assist those preparing submissions:

Are any of the current price controlled markets now sufficiently competitive to warrant the removal of price controls on the relevant telecommunications service?

Having regard to the level of competition, are there any telecommunications services that should be subject to price controls that are not within the scope of the current arrangements?

Should mobile services remain outside the retail price controls?

Do FTM services need to be subject to their own specific price cap?

5.2 Impact of price controls on competition, availability, choice, quality, price and investment

In considering the impact of the current, and possible future, price control arrangements the Commission has been directed to have regard to the following factors:

competition and the future development of competition, having regard in particular to the telecommunications anti-competitive conduct regime and telecommunications access regime under Parts XIB and XIC of the Act;

the availability, choice, quality and prices of services to consumers and any other impacts on consumers; and

the telecommunications industry, including on economically efficient investment decisions.

Each of these factors is considered in turn below.

Impact on competition The extent to which current, and possible future, price control arrangements (both by themselves and through their interaction with other regulatory measures such as Parts XIB and XIC of the Act) impact on the development of competition is an important issue for consideration.

The two main ways that competition can develop in telecommunications markets is through facilities-based and access or service-based entry. Facilities-based competitors offer services by connecting users to their own network. For example, Telstra, SingTel Optus, Vodafone and Hutchison are facilities-based competitors in the mobile telecommunications market. In contrast, access/service-based competitors provide services to consumers by purchasing services from a facilities-based supplier, and in some cases, combine this with their own network elements. For example, a number of telecommunications carriers/CSPs purchase a domestic PSTN origination/termination

20

service from Telstra and use it to provide a range of fixed-line voice services to end-users.14

Price control arrangements may have an important impact on the extent and type of competition that develops in telecommunications markets, and therefore, on the operation on Parts XIB and XIC of the Act.

For example, new facilities-based entrants are attracted to a market by the prospect of financial return that is commensurate with the risks involved in their investment. Below-cost pricing for some services brought about by price controls may discourage entry in some markets unless an entrant expects to be able to recover projected losses from above-cost pricing from other services or areas. It is likely this may have been the impact of the long-standing constraint on the price of local calls – of which the current 22 cap on local call prices from a residential/business line is the latest manifestation. Similar issues may also arise from the 40 cent cap on local calls made from a public payphone. Following a recent ACA review which recommended to the Government that the Commission examine this issue, the Commission would welcome specific comments on the operation of this cap.

The current state of facilities-based competition in market within which local telecommunications services (line rentals and local calls) are provided may reflect the respective price-cost disparities discussed above. For example, the Commission has noted that a degree of facilities-based competition has emerged in the above-cost regions such as the CBDs of the major capital cities15, yet there is considerably less facilities-based competition in below-cost regions such as some metropolitan and many rural and regional areas. The impact of price controls on efficient investment incentives is discussed further in Impact on economically efficient investment decisions and in section 5.3.

Similarly, price control arrangements may also impact on the development of access/service-based competition in particular markets. Importantly, the likely impact will depend on their interaction with the access regime administered by the Commission under Part XIC.

For example, access-seekers’ can compete with Telstra in providing local call services to end-users by purchasing a declared local carriage service (LCS) from Telstra. The Commission currently adopts a ‘retail − minus’ methodology to determine an average

14 In cases where an access seeker does not use any of its own network components in supplying a service but instead completely utilises a facilities-based competitor’s network, is variously known as wholesale or resale competition. For example, some carriage service providers that supply a resale local call service do this by purchasing a complete LCS service from Telstra, but typically provide their own billing and customer support services. 15 Indeed, evidence of competing networks capable of providing voice, data and in some cases Pay-TV services in CBD areas, combined with the increased availability of alternative facilities and lower level regulated access services such as the ULLS and local PSTN originating and terminating services, led the Commission to remove access regulation of Telstra’s Local Carriage Service for CBD areas from July 2003.

21

access price (retail price of local call minus retail costs) in the event of an access dispute or when assessing an LCS undertaking.16

Under a retail-minus approach, the existence of a 22 cent price cap on local calls is unlikely to, per se, impact on the extent of wholesale competition in the market for local call services. That is because, even in the absence of such a cap, the calculated retail – minus charges will continue to allow access-seekers to earn a profit through the retail provision of these services, as long as they incur retail costs equal to or lower than Telstra.

On the other hand, if the Commission had adopted a cost-based approach to regulating LCS charges (i.e. such as TSLRIC or Total Service Long-Run Incremental Cost), there is potential that the price cap described above could impact on the extent/development of access/service-based competition. That is, if the calculated average TSLRIC charge was greater than the calculated average retail − minus charge, access-based competition particularly in low-yield/high-cost areas (i.e. rural and regional) may decline as the margins of access-seekers are squeezed due to the retail price cap of 22 cents. Alternatively, access/service-based competition in high-yield/low-cost areas may become more pervasive.

It was for this reason that the Commission adopted a retail-minus approach for this service in 2000. To the extent, however, that the TSLRIC-based charge (plus retail costs) becomes lower than the retail price, the justification for a retail-minus approach is reduced and the significance of the retail price cap on local calls for local service competition is much lessened.17

In a practical sense, there are difficulties associated with determining the extent to which price control arrangements, and their interaction with Parts XIB and XIC of the Act, affect competition in telecommunications markets. The discussion above suggests that price-cost disparities may be an important determinant of the extent and mixture of competition that develops in certain telecommunications markets, although the impact of this in relation to local calls may decline as network costs continue to fall.

Questions to assist those preparing submissions:

What impact, if any, do the current price control arrangements have on the development of facilities-based competition in telecommunications markets?

What impact, if any, do the current price control arrangements have on the operation, and development, of access-based competition in telecommunications markets?

16 When the LCS was declared in 1999, the Commission indicated that it would likely adopt a retail-minus methodology to determine an access price in the event of an access dispute or when assessing a LCS undertaking. The Commission confirmed this approach in October 2003. 17 See Final determination for model price terms and conditions for PSTN, ULLS and LCS, ACCC October 2003, chapter 12. This notes that continuing reductions in fixed network costs will mean that local call costs will fall progressively over the next few years to be below retail charges. This would signal a need for the ACCC to re-think its current retial-minus approach to LCS.

22

Are there any other important ways in which the current price controls affect competition in telecommunications markets?

What impact do price controls have on the operation of Parts XIB and XIC of the Act which are administered by the Commission?

How important are the price control arrangements to the development of competition in markets other than those directly regulated by the retail price control arrangements?

Impact on availability, choice, quality and price The Commission has been directed to consider the impact of the current and possible future price control arrangements, on the availability, choice, quality and price of services to consumers.

Price control arrangements can have a direct impact on the retail price of particular telecommunications services. For example, the current price control arrangements make provision for ‘rebalancing’ of line rental and call prices with a CPI + 4 per cent price cap on line rental and a separate CPI − 4.5 per cent price cap on a basket of call services.18

The previous price control arrangements provided for a general CPI − 5.5 per cent basket that encapsulated call, line rental and connection services along with ‘sub-caps’ on some individual services.

Prior to the implementation of the current arrangements, the Commission recommended that a CPI − X per cent price cap be retained on all services subject to price controls. The Commission reached this view, largely, because this would have given Telstra the freedom to rebalance line rental and call prices while ensuring overall cost reductions for consumers in line with aggregate total factor productivity improvements resulted in overall cost reductions for consumers. That is, a CPI − X per cent price cap on all services subject to price controls would have given Telstra the freedom to raise line rental prices within the broad basket towards cost, so long as it also reduced the price of call services by a sufficiently large amount such that the weighted average price of all services fell by X per cent in real terms each year. 19

18 Traditionally, Telstra has been limited in the extent to which it can increase the price of line rental services such that they have been priced below their long-run incremental cost of production. The shortfall in revenue Telstra suffers as a result of these constraints has traditionally been made up by pricing call services in excess of their long-run incremental costs of production. The resultant disassociation of prices and costs for both line rentals and call services does, however, generate allocative inefficiencies and a consequent reduction in the welfare of the community as a whole. Further, it may have the effect of dampening investment in network infrastructure, as the price of lines is unable to recover their cost of production. 19 The ACCC’s Final Report on the appropriate form of the previous price control arrangements recommended that that weighted average price of line rentals and call services should come down by 5 per cent per annum in real terms each year.

23

The extent to which the current arrangements compensate consumers adequately for increased line rental charges depends crucially on the level of the specified ‘X’ for the calls basket. The Commission notes that had an overall price cap of around CPI − 5 per cent applied under the current arrangements, this would have required greater reductions in call prices than required by the current CPI − 4.5 per cent price cap for call services.

This suggests that the current price control arrangements are not compensating consumers for increasing line rental charges to the same extent as previous price control arrangements where an overall cap existed. It may also suggest that consumers are not receiving the full benefits of total factor productivity improvements that are being achieved by Telstra over the course of the current price control arrangements.

Perhaps less obvious than the effect on price, price control arrangements can also have an impact on the quality of telecommunications services – particularly those subject to price controls. For example, the current arrangements allow Telstra to claim price control credits for quality improvements to the line rental service. That is, the price that Telstra has actually charged for a service may be deemed to have decreased where there has been an improvement in the quality of the service.

There is also a possibility that the current, or possible future, price control arrangements affect the availability and choice of telecommunications services. For example, price control arrangements which require that Telstra price-below cost in certain markets may discourage efficient facilities-based entry in these markets, thus reducing the potential for alternate suppliers to offer telecommunications services to end-users in the future.

Questions to assist those making submissions:

Should price caps apply to individual or baskets of services? How should any baskets be constructed?

Should there be a broad price cap on all telecommunications services that are subject to price controls? If so, what level should the CPI − X cap be set at?

Are the current price control measures that allow Telstra to claim price control credits for quality improvements to its line rental service an effective means to promote high quality telecommunications services? If not, by what alternative means should quality objectives be achieved?

What affect do the current price control arrangements have on the availability and/or choice of telecommunications services?

Impact on economically efficient investment decisions As noted earlier, maintaining a structure of retail prices that differ from the costs of provision can adversely affect the manner in which both facilities and access-based competition develops in telecommunications markets, and the type and level of investment in these markets.

24

There are potentially a number of tensions between the deployment of facilities-based entry, investment and retail price controls. Where retail price controls result in a uniform price across different markets – such as the current requirement that local call prices not exceed 22/40 cents – the current retail price controls result in higher margins for facilities-based competitors on customers that are less costly to service. The margins are lower (and even negative) for those that are more costly to service. The differences in these margins can have a number of adverse consequences on the development of facilities-based competition and investment.

First, facilities-based entry may be artificially restricted. Although facilities-based entry will be attractive where the costs of servicing customers are low it will be less attractive in other areas and for other customers. The increase in customer choice and the range of services available to consumers that facilities-based competition can stimulate will be restricted to certain areas, and within those areas, only to certain customers.

Second, in the areas where facilities-based entry does occur, there is the potential for inefficient investment. Some of the existing price controls restrict the manner in which Telstra can respond to facilities-based competition. For example, the current price controls require that revenue-weighted average untimed local call prices for non-metropolitan customers in a given year must not exceed the revenue-weighted average untimed local call price for metropolitan customers in the previous year by more than 0.4 per cent (the “local call pricing parity”). To the extent that entry occurs in metropolitan areas, the requirement to pass price declines to users in other areas may prevent Telstra from competing on price in metropolitan areas. The entrant may, as a result, gain market share even though Telstra has lower costs of serving those customers.

Retail price controls that allow greater alignment with costs may overcome the potential for these tensions to occur.

Similar tensions may also arise between the development of access-based entry, investment and the retail price controls, when a cost-based access approach is coupled with an average retail price approach that abstracts from such cost differences. Under a cost-based access regime, the current retail price controls will similarly result in higher margins when providing local services to high-volume customers and customers that are less costly to service. The margins will be lower (and even negative) for low volume users and users that are more costly to service. The differences in margins can have the same adverse consequences for the development of access-based entry as described above for facilities-based entry.

Important to considering the above tensions is to recognise that role cost-based access pricing has on encouraging efficient ‘build/buy’ decisions between facilities-based and access-based entry. Facilities-based entry requires significantly greater investment. In particular, it usually requires duplicating the local loop (or elements of it) rather than seeking access to it. For this decision to be efficient, the provider making the decision should, among other factors, weigh-up the cost of duplicating the local loop compared to the cost of the current provider allowing access to the local loop. If the price of

25

access to the local loop is not cost-based (for example it is above the cost of access to the local loop), there is a risk that the entrant may inefficiently decide to duplicate the loop. Similarly, if its below-cost, this could encourage inefficient access-based entry.

In assessing the impact of the current, and possible future, price control arrangements on economically efficient investment decisions, a number of issues seem relevant.

Questions to assist those preparing submissions:

What impact, if any, do the current price control arrangements have on economically efficient investment in telecommunications markets?

What role, if any, do the restrictions on line rental charges have on investment in telecommunications markets? Has this changed over the course of the price control arrangements as line rental and call charges have been rebalanced?

Are there any other important ways in which the current price controls impact on economically investment in the telecommunications market?

Are there competition and investment efficiency grounds for removing or increasing the 40 cent cap on local calls made from a public payphone?

5.3 Distributional impacts

The Direction requires the Commission to have regard to the distribution of the short-term and long-term community and economic benefits and costs from the current or any future price control arrangements. In considering these distributional affects, the Commission has been directed to consider the impacts on different types of households, business consumers and geographic areas, with particular regard for the affects of any rebalancing of line rental and call charges.

The need to consider these distributional impacts arises because the price control arrangements have traditionally been used as a tool for achieving some of the government’s social policy/equity objectives. Hence, if price control arrangements are to continue to be used with these objectives in mind, the distributional impact of any changes to the current arrangements is an important consideration.

Accordingly, the Commission seeks comment from interested parties on the likely distributional impacts of any changes to the price control arrangements they might consider under sections 5.1 and 5.2 above. To assist parties in this regard, the remainder of this section addresses the types of issues parties should consider when making submissions.

Impact on different types of household and business consumers In the short-term, the major beneficiaries of any changes to the price control arrangements will be those household and business consumers who purchase relatively more of those services which become cheaper as a result of any changes to the price control arrangements.

26

For instance, the current CPI + 4 per cent price cap has provided Telstra with an incentive to rebalance its line rental and call prices applies to both business and residential line rentals. This means, for example, that over the period to which the current price controls apply (2002-05) Telstra has the ability to increase residential line rental charges above this cap if it maintains changes in business line rental charges below the capped amount.

One important implication of the inclusion of business and residential line rentals in the same basket is that the burden of increased line rental charges since the current price control arrangements were introduced is likely to have fallen on residential customers. This is largely because, prior to the commencement of these arrangements, the price of line rental for business customers was already much closer to efficient/underlying cost compared to the price of line rental for residential customers.20

As evidence of this, the Commission notes that Telstra’s residential line rental charges have increased significantly from 1 July 2002 to the present time, with charges under its HomeLine Complete plan increasing 23.1 per cent, to $26.95 and charges under its HomeLine Plus plan increasing 20.28 per cent, to $29.95. In contrast, Telstra’s business line rental charges increased by substantially less over this period, with charges under its BusinessLine Complete Plus plan increasing 2.9 per cent, to $34.95 and charges under its BusinessLine Plus plan increasing 2.5 per cent, to $40.95.

One advantage of a broad cap on all services subject to price control arrangements is that it would have required greater call charge reductions given the CPI + 4 per cent cap on line rentals.

In any case, a preliminary estimate based on a modelling exercise by the Commission suggests that Telstra’s average cost of providing a line is approximately $33 per month (including GST). Given that Telstra’s business rental is in the $34.95 to $40.95 range (i.e. above average costs) this would tend to suggest that Telstra’s latest increases in its residential line rental charges is getting very close to what is necessary to achieve cost recovery. Moreover, this would tend to suggest that rebalancing may not be a significant component of any future price control arrangements, as it was previously.

While both residential and to a lesser extent business customers have likely been worse off as a result of line rental increases, this has been at least somewhat offset by lower prices for a combined basket of local call, long distance and international call services. The Commission’s 2002-03 Price Control Report indicates that the weighted average price of the basket of call services (local, trunk and international calls) decreased by 1.3 per cent. This comprised a 1.2 per cent increase in the weighted average price of local calls which was more than offset by decreases in the weighted average price of trunk (−2.4 per cent) and international (−2.6 per cent) calls.21

20 The ACCC’s 2000 Discussion Paper indicated that the price of line rental for business customers was then $330 per annum (GST inclusive) compared to an average price for residential customers of $182.80 per annum (GST inclusive). 21 ACCC Report to the Minister for Communications, Information Technology and the Arts, Telstra’s compliance with the price control arrangements: 2002-03, May 2004, p. 10.

27

Indeed, there may be some threshold number of calls beyond which certain consumers would be better off under the current price control arrangements, as the increases in line rentals will be more than offset by the decrease in the price of call services This depends, however, on the extent to which call price reductions have been tempered or offset by carry-over credits from previous price control arrangements. Nonetheless, it suggests that any benefits arising from the current price control arrangements are more likely to be felt by households and businesses that purchase a relatively large number of trunk and international calls per line from Telstra.

Any future increases in ‘X’ in the CPI − X per cent price cap on a basket of call services will have greater benefit for those households and businesses that consume more of the services to which the price control applies. Hence, for any change in the price control arrangements, the distribution of benefits and cost will vary across different types of household and business consumers.

In the longer-term, the benefits and costs of alternative price control arrangements are most likely to be influenced by the degree to which these alternatives affect the development of competition and future investment patterns. To the extent that alternative price control arrangements lead to greater competition and more efficient investment in particular telecommunications markets, households and businesses which consume more of the services from these markets will benefit most.

Questions to assist those preparing submissions:

Which types of households and businesses benefit from the current price control arrangements, including the ability of Telstra to rebalance line rental charges with charges for other telecommunications services? Which type of households and businesses are disadvantaged?

What changes to the arrangements should be considered in order to promote the long-term interests of residential and business end-users respectively?

Which type of households and businesses will benefit as a result of changes interested parties suggest to the price control arrangements? Which type of households and businesses will be disadvantaged?

Which type of households and businesses would likely benefit from an increase in the “X” in the CPI − X price cap on a basket of call services? Which type of households and businesses would be disadvantaged?

In the long-term, what would be the distribution of benefits and costs across different types of business and household consumers if the current price control arrangements are retained?

In the long-term, what will be the distribution of benefits and costs of any suggested changes to the price control arrangements across different types of business and household consumers?

28

Impact on different geographic areas With regard to different geographic areas, the major beneficiaries of any changes in the price control arrangements will be those households and businesses that are situated in areas where the price of the services decrease as a result of any changes.

Hence, for example, removal of the current local call pricing parity and the cap on local call prices would most likely benefit metropolitan consumers at the expense of non-metropolitan consumers. That is, to some extent, the existing measures ensure that price reductions in geographic areas with greater competition (i.e. metropolitan areas) flow on to customers in areas where competition may not yet have developed (i.e. non-metropolitan areas such as rural and regional parts of Australia).

Under the current arrangements, Telstra must more closely align its prices for local calls in metropolitan and non-metropolitan areas respectively. This means that Telstra is less able to set different prices in different geographic regions based on underlying cost. There is however, a one-year lag which allows discrimination in current year pricing. Removal of these measures could potentially lead to Telstra reducing its prices for local calls to cost in metropolitan areas, whilst maintaining or increasing the price of local calls to cost in non-metropolitan areas. In this event, metropolitan consumers would likely benefit at the expense of non-metropolitan consumers.

The geographic distributional impact of current price controls that have allowed Telstra to raise the price of line rental towards cost depends on how rental has changed for different customers by geographic location. The Commission notes that differences in line rental have not bee introduced by different geographic areas. However, if rural areas tend to have lower incomes on average than metropolitan areas, the impact of increases will be greater.

In assessing Telstra’s PSTN Undertaking in 2000, the Commission estimated that the cost of line rental varied across different geographic regions. In particular, the Commission found that the annual average cost of lines for 2000-01 was $156 in CBD areas, $348 in metropolitan areas, $310 in provincial areas and $473 in rural/remote areas.22 Hence, if Telstra is aligning its line rental charges with cost, those in rural/remote areas are likely to be incurring a substantial increase in the price of their line rental, relative to provincial, metropolitan and CBD customers. On the other hand, those in CBD areas (and especially those that are in business) are likely to be less affected by such realignment to cost and indeed would be expected to benefit from such changes.

In the longer run, there is a possibility that those in high-cost areas may find some benefit from the removal of price controls on local calls and line rentals. That is, if removal of these price controls makes facilities-based competition more attractive for potential investors, this could lead to a greater level of choice of services and price competition being provided in high-cost areas.

22 ACCC, A report on the assessment of Telstra’s undertaking for the Domestic PSTN Originating and Terminating Access services, July 2000, p. 65.

29

Questions to assist those preparing submissions:

Which geographic areas currently benefit from the current price control arrangements? Which geographic areas are disadvantaged by the current price control arrangements?

What changes to the arrangements should be considered in order to promote the long-term interests of metropolitan and non-metropolitan end-users respectively?

Which geographic areas will benefit as a result of changes interested parties suggest to the price control arrangements? Which geographic areas will likely be disadvantaged?

In the long-term, what will be the distribution of benefits and costs across different geographic areas if the current price control arrangements are retained and extended?

In the long-term, what will be the distribution of benefits and costs of any suggested change to the price control arrangements across different geographic areas?

Data requirements In many cases, estimating the distributional impact of a given price control change will require data on the distribution of calling patterns across different households, businesses, and geographic regions. Whilst the Commission recognises that attaining such data is probably not feasible for the majority of interested parties making submissions in this review, any modeling of the distributional impacts of proposed price control changes would be of particular value to the Commission.

5.4 New and emerging technologies

As the Commission noted in its Emerging market structures report, since the opening up of the Australian telecommunications market to full competition in July 1997, the industry has seen the emergence of many new competitors, technologies and modes of service delivery.23 Moreover, the increasing substitutability of platforms to deliver a wide range of telecommunications and other services, such as multi-media and broadcasting services – commonly referred to as ‘convergence’ – is likely to have important implications for the future regulation of the telecommunications industry, including the form/type/structure of price controls that should apply to Telstra.

The Direction requires the Commission to have regard to the implications of new and emerging technologies on price control arrangements, and conversely, of price control arrangements on new and emerging technologies.

Each of these issues is discussed in turn below.

23 ACCC, Emerging market structures in the communications sector, June 2003, p. 31

30

Impact on price control arrangements New and emerging technologies may have two quite distinct impacts on the future price controls that should apply to Telstra. First, the emergence of new technologies may require that the scope of retail price controls be extended to include new and emerging services where Telstra is a dominant supplier at the wholesale and/or retail level. Second, the emergence of new technologies, particularly those using new packet-based data modes to deliver voice, data, text and video services, could potentially remove the need for price controls on certain existing telecommunications services if, for example, it results in a reassessment of the traditional market boundaries that apply to those services because of greater competition by new services.

A relevant example of this may be the emergence of voice-over Internet Protocol (VoIP) technology. VoIP refers to the practice of providing a voice service using internet protocol technology24 instead of using the standard circuit-switched based PSTN network. Although the emergence of VoIP technology has been relatively slow to date and is still to overcome some technical difficulties, many industry analysts believe that it could become a substitute technology for traditional fixed-line telephony services that are currently supplied over Telstra’s PSTN network.

Another example of an emerging service which may impact on competition for traditional voice services over this period is the use of fixed and portable/nomadic wireless technologies to provide both voice and broadband services at a comparable standard to that offered by PSTN voice and basic DSL broadband technologies. Such networks are currently being progressively deployed in parts of Australia and avoid the need to use Telstra’s local loop network to connect customers or the substantial costs associated with re-cabling homes and businesses. As with VoIP technologies, the competitive impact of new wireless platforms over the next three years is still unclear.

The extent to which VoIP technology and new wireless platforms becomes a credible substitute for fixed-line voice services is likely to have important implications for the future price controls that should apply to Telstra. For example, if the market for VoIP services is effectively competitive and serves as a competitive constraint on Telstra’s supply of local, trunk and international call services, there may be a case for removing price controls on these services. A key consideration in this regard is the competitive impact of such technologies over the course of the next price cap period. Equally, the impact of the price controls themselves on incentives towards competitive supply of such technologies and services over this period is also pertinent and is discussed in the next section below.

In assessing the impact of the current, and any alternative future, price control arrangements on new and emerging technologies, a number of issues seem relevant.

24 The use of IP technology means that voice services are effectively transmitted through the use specified packet-based switching or switchless modes and can involve carriage either over the public internet – which can include gateway access to the PSTN – or in a more closed form of ‘peer-to-peer’ services which is only assessable by those who subscribe to the service.

31

Questions to assist those preparing submissions:

Are there currently any telecommunications services delivered by Telstra via means of a new or emerging technology that should be subject to retail price controls?

What is the potential for new and emerging technologies to increase the need for price controls on particular telecommunications services?

Are there currently any new or emerging technologies that reduce the need for retail price controls on certain telecommunications services?

Impact of price control arrangements Price control arrangements themselves may have an important impact on the development of new and emerging technologies. This includes technologies developed by Telstra, and technologies developed by its competitors.

Telstra’s incentive to invest in new and emerging technologies might be influenced by the extent to which the price control arrangements allow it to price above-cost or below-cost. For example, if the structure of price control arrangements allows Telstra to price above-cost in certain markets, it may be argued that it has less of an incentive to invest in new technologies/means of service delivery while it is earning in excess of ‘normal’ profits. On the other hand, if the structure of price control arrangements forces Telstra to price at, or even below, cost in certain markets, it may be argued that Telstra’s incentive to invest and innovate is greater as it may encourage it to invest in new technologies that allow it to provide these services at a lower cost.

From another perspective, retail price controls which allow Telstra to price above-cost in certain markets may actually encourage it to invest in new and innovative technologies. That is, if price controls allow Telstra to earn in excess of ‘normal’ profits in certain markets it may be inclined to use these profits to invest in new and emerging technologies for the provision of future services. By this same reasoning, price controls that force Telstra to price below-cost may stifle investment in new and emerging technologies.

The extent to which Telstra’s competitors have an incentive to invest in new and emerging technologies may also be influenced by retail price control arrangements. For example, price control arrangements that result in Telstra pricing below-cost in particular markets may discourage efficient entry via the development of a new technology/means of service delivery, if that entrant is unable to compete with Telstra’s below-cost retail price. Alternatively, price control arrangements that allow Telstra to price above-cost in certain markets might actually encourage the inefficient development of new technologies if an entrant’s costs are higher than Telstra’s, yet it still is able to enter the market and earn a profit due to the above-cost retail price .

In assessing the extent to the current, and any alternative future, price control arrangements impact on the development of new and emerging technologies a number of issues seem relevant.

32

Questions to assist those preparing submissions:

Do the current price control arrangements have any effect on the emergence of new technologies in telecommunications markets? If so, which technologies in particular and what it’s the likely affect?