Embed Size (px)

Citation preview

Review of mobile wholesale voice call terminationmarkets

EU Market Review

15 May 2003

2

Contents

Summary 4

Chapter 1 Introduction 7

Chapter 2 The services considered in this review 12

Chapter 3 Definition of the relevant market 15

Chapter 4 Assessment of significant market power 42

Chapter 5 Detrimental effects arising from SMP in the

termination market 51

Chapter 6 Regulatory option appraisal and proposed remedies 59

Chapter 7 Proposed charge controls 97

Chapter 8 Consultation details 114

Annex A Notifications of proposals and proposedsignificant market power conditions of entitlement 116

Annex B Assessment of market power 169

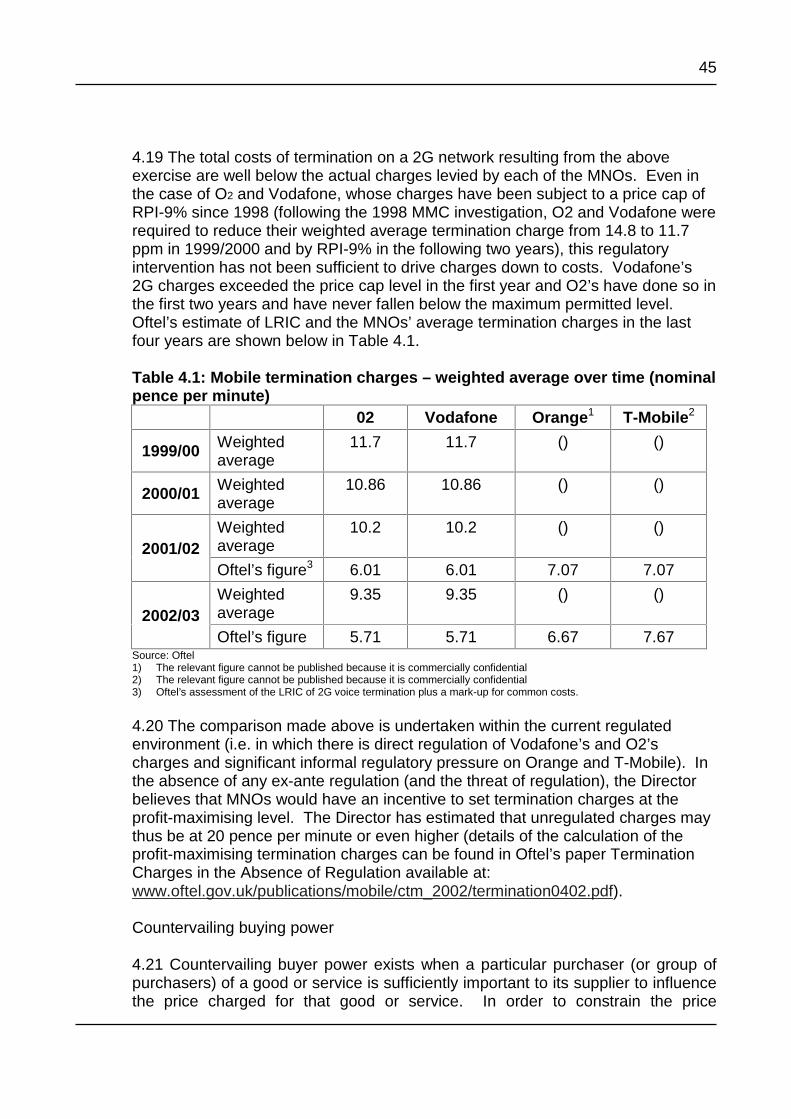

Annex C Alternative solutions 176

Annex D Cost of Capital 189

Annex E Explanation of LRIC and LRIC+ target charge 199

Annex F Evaluation of surcharge for the network externality 209

3

Annex G Fair target charge and the level of charge control 218

Annex H Charge cap mechanism 222

Annex I Treatment of ported numbers 227

Annex J List of questions for consultation 231

Annex K Glossary 233

4

Summary

A new regulatory regime

S.1 A new regulatory framework for electronic communications networks andservices will enter into force in the UK on 25 July 2003. The basis for the newregulatory framework is five new EU Communications Directives that are designedto create harmonised regulation across Europe and aimed at reducing entrybarriers and fostering prospects for effective competition to the benefit ofconsumers.

S.2 The new Directives require National Regulatory Authorities (NRAs), such asOftel, to carry out reviews of competition in communications markets, to ensurethat regulation remains appropriate in the light of changing market conditions.

Markets considered in this review

S.3 The markets considered in this review are those in which services are soldand purchased by communications providers in order to complete end-to-endcalls. The public electronic communications network (PECN) provider needs topurchase services to complete end-to-end calls when calls leave its network andare then terminated on another PECN provider’s network. These are calltermination services. This particular review considers wholesale voice callsterminated on individual mobile networks. However, through its roamingagreement, 3 provides 2G termination services to its subscribers via anotheroperator’s network. Therefore, in respect of 3, this review also considerswholesale 2G voice call termination provided to the subscribers of 3. Marketdefinition is discussed in detail in Chapter 3. This product market definition isbroadly consistent with the European Commission's Recommendation.

S.4 Definition of the retail market and assessment of retail market power are notincluded because they are not directly relevant to this review. Interactions with,and effects of regulation of wholesale termination on the retail market are,however, considered as part of this review.

Initial conclusions on Significant Market Power

S.5 The Director General of Telecommunications (the 'Director') has consideredwhether significant market power (SMP) is held by any communications providersin the relevant markets, taking into account the European Commission’sGuidelines on market analysis and the assessment of significant market powerand Oftel’s SMP Guidelines (available at:www.oftel.gov.uk/publications/about_oftel/2002/smpg0802).

S.6 As a result of this, the Director’s initial view is that each mobile networkoperator ("MNO") in the UK has significant market power in a separate market forvoice call termination on its network, and in the case of 3 wholesale 2G voice call

5

termination provided to its subscribers, and can be expected to have market powerfor at least the next three years. The key factors informing this initial view are:

• the existence of the calling party pays ("CPP") arrangements and mobile users’low sensitivity to the price of incoming calls;

• each MNO has a 100% share of the relevant market and is thus a monopolist;• the purchasers of mobile termination lack sufficient countervailing buyer power

to constrain charges to the competitive level; and• termination charges on 2G networks having been persistently and significantly

above costs, which demonstrates the ability and incentive of MNOs to setprices above the competitive level.

Regulatory remedies

S.7 The Director considers it appropriate to propose a number of remedies on allMNOs terminating voice calls from fixed or mobile calls on their network.

S.8 In summary the Director’s proposals are:

S.9 In respect of Vodafone, O2, T-mobile and Orange for their 2G call terminationservices, to require that they:

a) provide network access for the purposes of 2G call termination;b) not unduly discriminate in the provision of such access;c) publish a Reference Offer;d) give prior notification of price changes; ande) reduce termination charges in line with proposed charge controls.

S.10 In respect of Inquam, to require that it publish prices and give priornotification of price changes.

S.11 In respect of 3, and the 2G voice call termination services that it re-sells, arequirement that it sets charges on the basis of forward-looking long runincremental costs of providing that service.

S.12 The Director also proposes that there should be no ex-ante regulation of 3Gvoice call termination services.

S.13 In respect of the charge control proposed by the Director, 2G voicetermination provided by Vodafone, O2, Orange and T-Mobile should be subject toan RPI-X charge control, to last until 2006 (details of the proposed control can befound in Chapter 7 and Annex G). This should not be unfamiliar to any networkproviders as it broadly follows proposals already set out by the Director in hisstatement Review of the charge controls on calls to mobiles in September 2001. Italso follows the findings and recommendations of the Competition Commission,Report on references under section 13 of the Telecommunications Act 1984 on the

6

charges made by Vodafone, O2, Orange and T-Mobile for terminating calls fromfixed and mobile networks, of January 2003.

S.14 The Director believes that his proposals are consistent with the newregulatory framework and are a proportionate response to all MNOs’ SMP in theprovision of wholesale mobile voice call termination.

Consultation

S.15 The Director is seeking comments on his proposals by 24 July 2003. Oncehe has considered all responses, the Director intends to publish his finalproposals. Comments should be sent to Lawrence Knight, Oftel, 50 Ludgate Hill,London EC4M 7JJ or sent to [email protected]

S.16 The formal draft notification of the proposed market definition, SMPdesignation and specific conditions can be found in Annex A.

7

Chapter 1

Introduction

A new regulatory regime

1.1 A new regulatory framework for electronic communications networks andservices will enter into force in the UK on 25 July 2003. The basis for the newregulatory framework is five new EU Communications Directives ("the Directives")as follows:

• the Framework Directive (Directive 2002/21/EC);• the Access Directive (Directive 2002/19/EC);• the Authorisation Directive (Directive 2002/20/EC);• the Universal Service Directive (Directive 2002/22/EC); and• the Privacy Directive (Directive 2002/58/EC).

1.2 The new regulatory framework is designed to create harmonised regulationacross Europe and aimed at reducing entry barriers and fostering prospects foreffective competition to the benefit of consumers.

1.3 The Framework Directive provides the overall structure for the new regulatoryregime and sets out fundamental rules and objectives which read across all thenew directives. Article 8 of the Framework Directive sets out three key policyobjectives which have been taken into account as relevant in the preparation ofthis consultation document, namely promotion of competition, development of theinternal market and the promotion of the interests of the citizens of the EuropeanUnion. The Authorisation Directive establishes a new system whereby any personwill be generally authorised to provide communications services and/or networkswithout prior approval. The general authorisation replaces the existing licensingregime. The Universal Service Directive defines a basic set of services that mustbe provided to end-users. The Access and Interconnection Directive sets out theterms on which providers may access each others’ networks and services with aview to providing publicly available electronic communications services. Thesefour Directives must be implemented in the UK in other EU Member States on 25July 2003. The fifth Directive on Privacy establishes users’ rights with regard tothe privacy of their communications. This Directive was adopted slightly later thanthe other four Directives and has an implementation date of 31 October 2003.

Implementation

Communications Bill

1.4 In the UK, it is intended to implement the four main Directives through a newCommunications Act. The Communications Bill was introduced into the House ofCommons on 19 November 2002 and is available atwww.communicationsbill.gov.uk. The latest version of the Communications Bill is

8

that which completed its passage through the House of Commons on 4 March2003 and was introduced into the House of Lords on the following day. It can befound at that website. References to the Communications Bill in this document arereferences to that version of the Bill. The Bill may continue to be subject to changeas it proceeds through Parliament.

1.5 It is intended that the Communications Bill will receive royal assent by 25 July2003. However, in the event that the Communications Bill does not receive royalassent by 25 July 2003, the Government has acknowledged that implementationwill need to occur by Statutory Instruments made under the EuropeanCommunities Act 1972 for an interim period until the Bill enters into force. Further,if the Communications Bill does receive royal assent by 25 July 2003, it isexpected that OFCOM will not be ready by the summer to assume all of its dutiesforeseen by the Communications Bill. Should that be the case, theCommunications Bill makes specific provision to enable Ofcom’s functions to becarried out by the Director for a transitional period. For these reasons, thisdocument refers to the Director rather than Ofcom.

EC Directives

1.6 Article 16 of the Framework Directive provides that analysis of the relevantmarkets for the purpose of the new regime should be carried out as soon aspossible after the adoption of the European Commission’s Recommendation onmarkets ("the EU Recommendation"). The EU Recommendation was adopted on11 February 2003. This market review is the preparatory work required as to theanalysis of markets required by the new regime. In the UK, the ElectronicCommunications (Market Analysis) Regulations 2003 (SI 2003/330) (“theRegulations”) confirm the Director’s ability to carry out this preparatory work.Pursuant to the Regulations, Oftel is consulting on the market identification,designation of SMP (or not) and the SMP conditions proposed.

1.7 Oftel currently regulates the industry through conditions attached to licences.The existing licensing regime must end on 24 July 2003. Oftel is currentlyconsulting on a set of draft General Conditions for those obligations which willapply from 25 July 2003 to all persons providing electronic communicationsnetworks or services. However, new specific obligations arising from SMP canonly be imposed after 24 July where National Regulatory Authorities (NRAs) haveidentified operators as having significant market power in discrete marketsfollowing a market review. Before completing such reviews and imposing suchobligations, NRAs are required to conduct national consultations (under Art. 6 ofthe Framework Directive) and to notify the EC and other NRAs (under Art 7)allowing a minimum of a month for any representations. Certain access relatedconditions set under clause 42(5) of the Bill are also subject to this consultationprocess.

1.8 Oftel had planned to complete the market reviews in summer 2003, includingthe required notifications to be in a position to implement the full new regulatoryregime including all the specific conditions after 25 July 2003. However, at the

9

CoCom meeting of 9 April 2003, the EC advised, contrary to earlier indications,that NRAs could not make notifications of the outcome of market analyses to themor other NRAs before 25 July 2003.

1.9 Oftel has now considered the implications of the EC’s views. It means thatspecific obligations (particularly those arising from market analyses or in the formof certain types of Access Related conditions) cannot be imposed until thenotification period has expired, ie not before the end of August at the earliest. Inorder to avoid a regulatory lacuna, this means that existing conditions in theseareas will need to be carried over post July 2003 until this notification process iscomplete. The carry-over of such conditions in these circumstances is compatiblewith the EC Directives and provision for this purpose is included in Schedule 18 ofthe Communications Bill (amendments to which were tabled on 30 April 2003 inthe House of Lords to make such provision).

1.10 Oftel has set up a project to identify and advise operators of conditions andlinked decisions such as determinations, consents etc, which need to be continueduntil the market analyses and necessary consultations are complete. Furtherinformation on the procedure to be put in place will be advised to the industry indue course. Any queries should be addressed to the project manager, PeterDavies ([email protected]).

1.11 As a result of the EC’s revised view on the timing of notifications, Oftel nowproposes to make its first formal notifications under Arts. 6 and 7 of the FrameworkDirective after 25 July 2003 and then allowing a period of a month for response.Taking into account the time for Oftel to consider the representations made andprepare a final statement, the earliest Oftel expects to introduce new obligationsarising from the market reviews will be September 2003. However the EC can, inlimited circumstances, require a further two months to respond. If they invoke sucha requirement for a particular review, then the completion of that review will befurther delayed accordingly.

Market reviews

1.12 The new Directives include the requirement that national regulatoryauthorities (NRAs), such as Oftel, should carry out reviews of competition incommunications markets, to ensure that regulation remains proportionate in thelight of changing market conditions. Oftel already carries out market reviews aspart of its long term strategy, focusing on effective competition as the best meansto deliver a good deal for consumers.

1.13 As discussed above, Oftel is now conducting a series of market reviewsunder the Regulations. The timing of this review is subject to the issues set out inparagraphs 1.4 – 1.11 above.

1.14 Each market review has three stages:

10

• definition of the relevant market or markets;• assessment of competition in each market, in particular whether any

companies have Significant Market Power (SMP) in a given market; and• assessment of the options for regulation and proposal of appropriate

regulatory obligations where there has been a finding of SMP.

1.15 More detailed requirements and guidance concerning the conduct of marketreviews are provided in the Directives, the Communications Bill, the Regulations,and in additional documents issued by the European Commission and Oftel. Asrequired by the new regime, Oftel will take the utmost account of the two EuropeanCommission documents discussed in paragraphs 1.11 and 1.12 of this marketreview.

Recommendation on relevant product and service markets

1.16 The EU Recommendation has identified a set of product and service marketswithin the electronic communications sector, which are to be reviewed by NRAs.The EU Recommendation seeks to promote harmonisation across the EuropeanCommunity by ensuring that the same product and service markets are subject toa market analysis in all Member States. However, NRAs are able to regulatemarkets that differ from those identified in the EU Recommendation where this isjustified by national circumstances and where the Commission does not raise anyobjections. Accordingly, NRAs are to define relevant markets appropriate tonational circumstances, taking the utmost account of the product markets listed inthe EU Recommendation.

Significant Market Power Guidelines

1.17 The European Commission has also issued guidelines on market analysisand the assessment of SMP (“the SMP Guidelines”). Oftel has produced additionalguidelines on the criteria to assess effective competition, which can be found athttp://www.oftel.gov.uk/publications/about_oftel/2002/smpg0802.htm. Thesesupplement the SMP Guidelines and replace Oftel’s effective competitionguidelines issued in August 2000.

Regulatory option appraisal

1.18 When considering the appropriate level of regulation if a finding of SMP isfound, Oftel will also give consideration to its regulatory option appraisal guidelinespublished in June 2002. These can be found at:http://www.oftel.gov.uk/publications/about_oftel/2002/roa0602.htm.

1.19 As explained in paragraph 1.14, there are three distinct stages to thisconsultation document. First, in chapter 3, Oftel defines the relevant market(s)considered in this review. Secondly, in chapter 4, Oftel assesses whether anynetwork provider has SMP in the relevant market or markets. As a result of Oftel’s

11

conclusions in chapter 4, chapters 5, 6 and 7 consider regulatory options andremedies for the Mobile Network Operators (MNOs).

Notification

1.20 Annex A contains the formal notification of the proposals made by theDirector as a result of the review, including the market(s) defined, the designationof SMP and the conditions proposed as a result of the market analysis. Thisimplements the provisions of Regulation 5 and 6 of the Regulations.

1.21 This document, including the formal notification in Annex A, has been madeaccessible to the European Commission and to the regulatory authorities in otherMember States in accordance with the scheme of the Directives.

12

Chapter 2

Services considered in this review

Details of services

2.1 In order for a customer of one public electronic communications network(PECN) to be able to speak with the customer of another such communicationsnetwork, the providers of these networks need to connect with each other.Network access services (which in this context refer to mobile voice calltermination) are those services that PECN providers need to purchase from eachother in order to enable the caller to speak with the intended recipient of the call onanother provider’s network. These services are referred to as wholesale servicesas they are sold and purchased by network providers rather than retail customers.Retail customers purchase retail services and these may involve use of a numberof wholesale services and one or more network.

2.2 If wholesale mobile voice call termination services were not readily available,retail customers could only communicate with retail customers connected to thesame network (known as 'on-net' calling). This would distort competition throughreduction in consumer choice and welfare. In order to maximise welfare, networkproviders need to purchase voice call termination from other network providers sothat their customers can contact the customers of the other network provider.

2.3 In the case of wholesale mobile voice call termination, this concerns callsbetween different mobile networks ('off-net' calls) and calls from a fixed network toa mobile network ('fixed-to-mobile' calls). When a call is made to a mobile phone,whether from a fixed line or from a mobile on another network, the call passesfrom the originating operator (A) to the terminating operator (B). The terminatingoperator charges a fee for connecting the call to its customer – the terminationcharge. This charge is paid by the originating operator and passed on to the callerin the retail price they pay for their call.

2.4 This consultation is only considering wholesale mobile voice call termination.The following mobile services are being covered in separate Oftel market reviews,following the EU Recommendation placing them in separate markets:

Fixed ormobile operator

(A)

Mobile operator‘(B)

Interconnection

13

• access to mobile networks, enabling the provision of retail voice services /calls made by retail customers from mobiles; and

• the wholesale service of international roaming, provided by UK mobilenetworks to foreign mobile networks, so that foreign mobile customers canuse their mobiles whilst in the UK.

Existing regulation

Charge Controls

2.5 Following an investigation by the Monopolies and Mergers Commission (nowrenamed the Competition Commission - ’the CC’) in 1998, which concluded thatthe termination charges of Vodafone and Cellnet (since renamed O2) were toohigh in relation to cost and against the public interest, controls were imposed onthe termination charges of Vodafone and O2. Their termination charges wereimmediately brought down to a ceiling of 11.7 pence per minute, which was thenreduced by RPI-9% in the each of the subsequent two years until March 2002.

2.6 In 2000/2001, Oftel undertook a review of the controls on Vodafone and O2and the level of competition in mobile voice call termination in general. At the endof that review, Oftel proposed that the termination charges of all four mobileoperators – Vodafone, O2, Orange and T-Mobile (or One 2 One as it was thenknown) – be reduced by RPI-12% each year for four years until March 2006. Themobile operators rejected the proposed licence modifications to bring into forcethese controls. As the Director still believed that controls were necessary toprotect consumers, in January 2002 he asked the Competition Commission toinvestigate whether, in the absence of controls, the termination charges of the fourmobile operators would be against the public interest and, if so, whether this couldbe remedied by way of a modification to their licences.

2.7 In February 2002, the Director, with their agreement, modified the licences ofVodafone and O2 so that the existing controls of RPI-9% on their terminationcharges were ‘rolled over’ for one year to March 2003, in order to protectconsumers pending the outcome of the CC investigation.

2.8 In its December 2002 report (Reports on references under section 13 of theTelecommunications Act 1984 on the charges made by Vodafone, O2, Orangeand T-Mobile for terminating calls from fixed and mobile networks), the CCconcluded that:

• the termination charges of the four mobile operators operate against thepublic interest;

• current termination charges are 30-40% above a fair charge;• consumers pay too much for calls from fixed lines to mobiles and from one

mobile network to another;• the high cost of termination deters people from calling mobiles; and

14

• those who make more calls to mobiles, either from a fixed line or anothernetwork, unfairly subsidise other mobile owners who mainly receive calls ormake on-net calls.

2.9 The December 2002 CC report recommended that:• each MNO should reduce the level of the total termination charge by 15 per

cent in real terms before 25 July this year;• O2’s and Vodafone’s charges should be subject to further reductions of

RPI-15% between 25 July 2003 and 31 March 2004 and for each of the twosubsequent financial years to March 2006; and

• Orange’s and T-Mobile’s charges should be reduced by RPI-14% between25 July 2003 and 31 March 2004 and in each of these subsequent two timeperiods.

2.10 The CC’s report is in line with the Director's conclusions in his statement ofSeptember 2001. The Director has accepted the CC’s recommendation of a one-off cut of 15% in real terms by July. Formal licence modifications to the MNO’slicences were put out to public consultation on 28 February 2003 (available at:www.oftel.gov.uk/publications/licensing/2003/fixmob_voda0203and www.oftel.gov.uk/publications/licensing/2003/fixmob_orangetmob03). Thosemodifications were made by the Director on 4 April 2003. Arrangements for anycontrol of termination charges after July 2003 are considered in this market reviewundertaken by Oftel under the requirements of the new European Directives.

Significant Market Power

2.11 Vodafone and O2 have been are at present designated as having significantmarket power (SMP) under the EC Interconnection Directive (Directive 97/33/EC).As a consequence of that designation, Vodafone and O2 are required to enter intointerconnection agreements with other Schedule 2 operators, not to discriminateunduly in the terms of interconnection offered to other networks, to provide theDirector with price notifications 24 hours in advance of them taking effect and toforward copies of all interconnect agreements

15

Chapter 3

Market definition

Mobile voice call termination

3.1 There are two aspects to the definition of a relevant market: the relevantproducts to be included in the same market and the geographic extent of themarket. Oftel’s approach to market definition follows that used by UK competitionauthorities and is in line with those used by European and US competitionauthorities. Market boundaries are determined by identifying constraints on theprice-setting behaviour of firms. There are two main competitive constraints toconsider: how far it is possible for customers to substitute other services for thosein question (demand-side substitution); and how far suppliers could switch, orincrease, production to supply the relevant products or services (supply-sidesubstitution) following a price increase.

3.2 The concept of the ‘hypothetical monopolist test’ is a tool used to help identifydemand-side and supply-side substitutes. A product is considered to constitute aseparate market if a hypothetical monopoly supplier could impose a small butsignificant, non-transitory price increase (SSNIP) above the competitive levelwithout losing sales to such a degree as to make this unprofitable. If such a pricerise would be unprofitable, because consumers would switch to other products, orbecause suppliers of other products would begin to compete with the monopolist,then the market definition should be expanded to include the substitute products.However, the relevant market is not necessarily the smallest that it is possible todefine using the hypothetical monopolist test. It may be appropriate to includeproducts (or areas) over which there are common pricing constraints such thatthey should be included within the same relevant market even if demand andsupply-side substitution are not present.

3.3 As set out in Chapter 2, the service considered in this review is wholesalemobile voice call termination. Call termination is the service necessary for anetwork operator to connect a caller with the intended recipient of the call on adifferent network. As discussed in Chapter 2, if call termination was not availablea network operator could only terminate calls to other customers on its network.This service is referred to as wholesale because it is sold and purchased bynetwork operators rather than retail customers.

3.4 This review only looks at voice call termination on public mobile networks (henceprivate mobile networks are excluded). Fixed voice call termination is dealt with in aseparate review, Review of fixed geographic call termination markets - 17 March 2003,(available at: www.oftel.gov.uk/publications/eu_directives/2003/eu_geo_term/index).Data termination is not considered. The analysis, hence, only covers GSM, 3G andTetra networks, but does not cover public wireless local access networks (WLANs)which are devoted to data transmission. SMS termination is also excluded.

16

Calling party pays

3.5 Before considering the market definition, it is important to consider the “callingparty pays” (‘CPP’) arrangement adopted in the UK telephony market because ithas a notable impact on the boundaries of this market. Under the CPParrangement, the calling party (and not the called party) pays the total price of aretail call. This means that the voice call termination charge is included in theoriginating network provider’s (either fixed or mobile) cost base and is reflected inthe retail price it sets for calls originating on its network. CPP, thus, leads to adisconnection between the person paying for the calls and so, indirectly, for thetermination charge (i.e. the calling party) and the person who makes the choice ofthe terminating network and could thereby influence the level of the terminationcharge (i.e. the called party).

3.6 The overall effect of this arrangement in the retail market (i.e. the market forcalls to mobiles) is that, while MNOs have an incentive to keep the price of thoseservices required and paid for by the subscriber at a level to attract and retaincustomers, they have less incentive to keep the price of calls to mobiles low. Thisis because those calling a mobile subscriber cannot take their business elsewhereif dissatisfied, as they have no alternatives to terminating the calls on the networkto which the called party subscribes.

3.7 In the wholesale market, the effect of the CPP arrangement is similar. For callsfrom fixed-to-mobiles, it means that the operators running fixed public electroniccommunications networks (fixed PECNs) pay the MNOs to terminate calls on theMNOs’ networks. The MNO has little incentive to keep voice call terminationcharges low, because the fixed PECN providers will pay a high charge as theyhave a commercial interest in ensuring that all calls made by their subscribers areterminated. For off-net mobile-to-mobile calls (i.e. from one MNO’s network toanother), the MNOs pay each other for termination of calls. Again, there is littleincentive to keep termination charges low, not least since cutting them would ineffect give the MNO’s competitors an advantage in the retail market by reducingtheir costs. Hence, CPP means that an MNO is likely to be able to raise voice calltermination charges above the competitive level without suffering sufficientadverse effects to make the rise unprofitable.

3.8 Overall, the Director considers that the CPP arrangement provides the MNOswith the freedom and the incentives to set their voice call termination chargesabove the competitive level.

Product market definition

3.9 As discussed above, the relevant product market is arrived at by starting fromthe smallest potential definition. In this case, the smallest possible marketdefinition is wholesale voice call termination to a specific mobile subscriber (ornumber), as a call to another individual it is unlikely to be a sufficiently goodsubstitute for a call to a specific recipient.

17

3.10 The following sections scrutinise that definition using the ‘hypotheticalmonopolist test’ to see whether it should be expanded to include other productseither because of demand-side substitution, supply-side substitution or theexistence of common pricing constraints.

Demand-side substitution

3.11 To assess whether there are any demand-side substitutes that should beincluded in the relevant market, it is necessary to examine the effect on customers’behaviour of an increase in termination charges by the hypothetical monopolistand whether such behaviour could make the rise unprofitable.

Retail demand-side substitution

3.12 The Director considers that an increase in termination charges is likely to leadto a rise in retail call prices. Termination charges form the largest part of themarginal cost incurred by a fixed PECN provider when providing fixed-to-mobilecalls. BT’s retail prices for calls to mobile are the sum of the charge it pays to theterminating MNO and BT’s regulated retention rate (discussed in Oftel’s Review ofthe fixed narrowband wholesale exchange line, call origination, conveyance andtransit markets, consultation – published on 17 March 2003). Therefore, BTtransfers any increase in the costs of providing calls to mobiles via its retail prices.Fixed PECN providers other than BT do not have market power in the retailmarket; it can thus be expected that they would follow BT’s behaviour. As forMNOs, Oftel considers that none of them has SMP in the retail market (discussedin Oftel’s Review of competition: mobile access and call origination – April 2003).Hence, when faced with an increase in the marginal cost of providing off-net calls,it is likely that MNOs will pass at least some of this cost into their off-net retailprices.

3.13 It is, therefore, relevant to consider how retail customers (the calling and thecalled parties) would respond to a price increase in calls to mobiles engendered bya rise in voice call termination charges and whether their reaction could be asource of competitive pressure on termination charges.

Behaviour of the calling party in response to an increase in the price of callsto mobiles

3.14 If callers reacted to an increase in the retail price for calling mobiles byemploying others means of communication to reach mobile subscribers, this formof substitution could act as a competitive constraint on voice call terminationcharges, although whether it would act as constraint depends on the amount ofsubstitution that takes place. It would affect the MNOs’ behaviour only if it wasenough to make the increase in the wholesale charges unprofitable. However, forcallers to react to an increase in the price of calls to mobiles, it is the Director’sview that three conditions need to be satisfied:

18

• callers must be sufficiently aware that they are calling a mobile and that theyare calling a specific network;

• callers must be sufficiently aware of the price of calling that particular network;and

• callers must be sensitive to changes in the prices of calling the network theywant to reach, i.e. an increase in the termination charge above the competitivelevel must cause consumers to adapt their behaviour to find an alternativesatisfactory way of contacting the person they want to call.

Awareness of calling a mobile and awareness of calling a specific mobile network

3.15 The lack of consumer awareness over the identification of mobile numbersappears to be fairly high. An Oftel residential consumer survey from August 2002(Consumers’ use of fixed telecoms services – published 24 October 2002) showsthat only 46% of all residential fixed consumers are “usually” aware of calling amobile phone (there has been little change in this figure over the previous 18months). This figure is higher (52%) among consumers who own a mobile phone,but is only 32% among consumers from households who do not have mobiles(Consumers’ use of mobile telephony - published 27 January 2003). These figureshave not changed much in the last two years, even though mobile penetration hasincreased.

3.16 In compiling the CC December 2002 report, the CC collected evidence onconsumer awareness of the identity of the particular mobile network they arecalling. The CC’s own market research (paragraph 2.136 in the December 2002report) indicated that on average only 28% mobile users knew whether they werecalling a mobile phone on the same network as themselves. The results of asurvey carried out by NOP for O2, which are quoted in the CC December 2002report (paragraph 2.136 in the December 2002 report ), found that 57% of fixedphone users who also owned a mobile claimed to know the mobile network theywere calling when using their fixed line, whereas only about 30% of fixed userswithout a mobile were aware of it. When NOP put the same question to mobile-only customers, a similar level of awareness was claimed as that of the owners ofboth fixed and mobile phones.

3.17 Hence, callers appear to the Director to have limited knowledge of specificnetworks they are connecting to when making a call to a mobile.

Awareness of relative and actual prices

3.18 Despite the high penetration of mobiles, there is still evidence of lowconsumer awareness of the costs of calling mobile numbers (in general and oneach specific networks). An Oftel qualitative study of telephone users’ behaviour(Oftel Price of Calls to Mobiles Qualitative Research Findings - published March2001) shows that most fixed line users do not generally check their phone bills;and, thus, that most were unable to quantify the costs of calling either a fixed or amobile number. Specific differences in the prices of calling different mobile

19

networks from a fixed line were also unknown and respondents assumed that theywould be essentially similar. A more recent Oftel residential consumer survey(Consumers’ use of fixed telecoms services – published 24 October 2002) showsthat just 17% know approximately how much it costs to call a mobile from theirfixed phone.

3.19 As part of their 2002 investigation on calls to mobile, the CC also assessedhow knowledgeable mobile owners and fixed-line users are about the actual costsof calling mobiles and the relative costs of different call types. The CC's surveyonly covered awareness of the price of a fixed-to-mobile call because the largenumber of different tariffs available would have made it difficult to elicit reliableresponses about mobile-to-mobile prices. The main result was that only 21% ofcustomers had an approximate idea of the true cost of such a call. Evidencecollected by the CC (paragraph 2.136 to 2.141 in the December 2002 CC report)also suggests that a large number of callers to mobiles have little knowledge eitherof the actual or relative levels of prices for calling each mobile network.

3.20 An NOP survey, conducted on behalf of O2 and referred to in the December2002 report (paragraph 2.137 to 2.141 in the CC report ), tested consumers’knowledge of relative prices. This revealed that about 48% of respondentsthought that fixed-to-mobile calls were a lot more expensive than fixed-to-fixedcalls (findings which correspond to actual price relationships) and 36% said thatoff-net calls were a lot more expensive than fixed-to-fixed calls (which alsocorresponds to the actual position). Given that the difference between fixed-to-fixed and fixed-to-mobile is actually smaller than the difference between fixed-to-fixed and off-net prices, the fact that fewer respondents thought that off-net callswere a lot more expensive tends to confirm the finding that there is a lack ofwidespread awareness of the relative prices of different types of call. This surveyalso found that 50% of the consumers appear to be aware that on-net prices arelower than off-net prices and that the price of fixed-to-mobile calls varied by time ofday. In addition, 44% knew that the price of calling mobiles from fixed lines variedby the network being called.

3.21 The Director believes that even though there is some consumer awareness ofrelative prices for different types of calls, knowledge of actual prices is low, inparticular of the price of calling a specific network. The Director also notes thatmobile number portability makes it more difficult for called parties to know/identifywhich network they are calling (and thus what is the relevant price), unless theyare calling a person with whom they are in a repeated calling relationship.

Consumers’ sensitivity to changes in the prices of calling a specific network -adapting behaviour

3.22 Even if awareness of prices was high, competitive pressure will only beexerted if consumers are willing to adapt their behaviour through substitution, sothat MNOs lose profits on mobile termination if they attempt to raise terminationcharges.

20

3.23 The Director has considered a range of different possible types ofsubstitution:

• mobile to fixed calls as a substitute for off-net calls;• mobile-to-mobile calls as a substitute for fixed-to-mobile calls;• on-net mobile-to-mobile calls as a substitute for off-net calls;• SMS as a substitute for mobile-to-mobile calls;• unified messaging and message clips’;• voice over Internet Protocol calls; and• call-back arrangement.

3.24 However, as explained below, the Director considers that none of the aboveis likely to have a constraining effect on voice call termination charges.

Mobile to fixed calls as a substitute for off-net calls

3.25 Following an increase in termination charges and, thus, in the cost of callinganother mobile, the calling party may switch to calling the intended party on a fixednumber. However, it is unlikely that a call to a fixed line can represent asatisfactory substitute for calling someone on a mobile network in a sufficientnumber of instances to act as a constraint on the charges for mobile voice calltermination. In particular, a call to a fixed line is not a viable alternative if thecalled party does is on the move, since immediacy of contact is an importantfeature of calls to mobiles.

Mobile to mobile calls as a substitute for fixed-to-mobile calls

3.26 After an increase in termination charges and, thus, in the cost of callinganother mobile, the calling party may keep calling the desired party’s mobilenumber, but from a mobile phone rather than from a fixed one. The ability of thisform of substitution to constrain voice call termination charges depends on itseffect on the profits from termination services for the network operator. The priceof on-net calls does not include the termination charge and the service is designedto attract subscribers who care about inbound call prices (so that if they can be onsame network as their callers). Hence, on-net call retail prices are generally set atlow levels and generate lower revenues for the MNOs. In contrast, off-net calls aresubject to the same termination charge as calls from fixed lines. Hence,substitution may act as a constraint only if callers were to switch from fixed-to-mobile calls to on-net calls.

3.27 In the Director’s view, for on-net calls to be a viable alternative to fixed-to-mobile calls:• the caller must know the mobile network (s)he is calling; and• the caller must be on the same network as the call recipient.

3.28 It is not clear if this happens sufficiently in practice for it to act as a constraint(the only evidence available suggests that 13% of consumers with both fixed and

21

mobile phones use their mobile to make ‘on-net’ calls because it is cheaper). Asdiscussed above, awareness of the specific network called is limited (around 60%among mobile users). In addition mobile subscribers are split between four mainoperators, hence, the probability of the caller being able to reach the desired callrecipient with an on-net call is substantially less than 100%. The probability that acall remains on-net will reflect the market share of the mobile operator in theoutgoing retail market, currently between 24% and 27% on the basis of totalsubscribers. However this probability is likely to be higher, because there isevidence that some customers with repeated calling patterns tend to congregateon the same network (see section on closed user groups). On this basis, theavailability of on-net calls as a substitute for calls from fixed phones to mobiles islimited.

3.29 However, if a caller knows that (s)he makes calls to one network more oftenthan to the others, this could influence the choice of network so as to benefit fromthe lower prices charged for on-net calls. In that case, calling mobile-to-mobile on-net might be an effective substitute for a call from a fixed phone. However, thissubstitution is unlikely to constrain termination charges because MNOs designtariffs so as to separate the more price sensitive subscribers from the others (e.g.by attracting them with low on-net prices). They can, thus, put up terminationcharges for the less price sensitive subscribers. This issue is examined more indetail under the heading ‘Closed user groups’.

On-net mobile to mobile calls as a substitute for off-net calls

3.30 Termination charges for off-net calls could be constrained by substitution toon-net calls. This requires the calling party to be on the same network as thecalled party or to use more than one network to originate their calls (by havingmultiple SIM cards).

3.31 The use of multiple SIM cards appears unlikely because the process ofswitching cards (to make different calls) is laborious and time-consuming. Inaddition, MNOs often lock handsets to the SIM that is originally sold with thehandset so that it can only be used on their network. Those factors, and limitedconsumer awareness of the higher cost of off-net, (an Oftel survey, Consumers’use of mobile telephony – February 2001, found that 37% of users thought that off-net calls were ‘a lot more’ expensive, 29% thinking that they were ‘a little more’expensive and 30% considering they were ‘roughly’ the same), means that it maybe some considerable time before multiple SIM devices generate any significantcompetitive pressure on voice call termination charges. Oftel has found(Consumers' use of mobile telephony – November 2001) that, at present, while63% of mobile users were aware that it was possible to use different SIM cards tolog onto another network, only 6% of these (4% of total mobile users) usedmultiple SIM cards. Further details on multiple SIM cards can be found in Annex Calternative solutions.

3.32 A constraint may, nevertheless, be posed by groups of mobile owners whoare willing to switch networks to be on the same network and thus pay on-net

22

prices to call each other (for more details on these groups see the section onclosed user groups below). If enough subscribers switch MNOs to be on the samenetwork - the one with the lowest on-net charges - MNOs may not just loserevenues from off-net calls, but may even lose subscribers.

3.33 However, the Director considers that substitution of calls by on-net calls couldreduce, rather than increase, the constraint on the general level of voice calltermination charges. That is because MNOs, by offering lower on-net call prices,can segment the market by type of customer and separate the more price-sensitive customers from the others who are less price-sensitive. They can thenset high termination charges for others (i.e. off-net termination charges). Thus, theDirector is of the view that the nature and extent of this type of call substitution isnot sufficient to act as a competitive constraint on termination charges.

SMS as a substitute for mobile to mobile calls

3.34 Short message services (SMS) enable parties to exchange text messagesbetween mobile phones. SMS cannot act as a constraint on voice call terminationcharges, because SMS termination is offered by the same MNO which providesvoice termination. Thus, the MNO could set charges for SMS termination in sucha way as to avoid any competitive pressure on its charges for voice termination.

3.35 In addition, SMS can only be relatively short because the number ofcharacters allowed in a text message is limited to 160 characters. Furthermore,SMS are not real time because, unlike mobile voice calls, SMS are transferredbetween networks on a store and forward basis, rather than on a ‘real time’ basis.Therefore, SMS do not afford the opportunity for immediate conversation andinteraction offered by voice calls.

3.36 Evidence collected by Oftel on mobile users’ behaviour supports the aboveconclusion that SMS are unlikely to be good substitutes for voice calls. Qualitativeevidence (Oftel Price of Calls to Mobiles Qualitative Research Findings - March2001) shows that text messaging is regarded, especially by the young (who sendthe highest proportion of messages), as an activity separate from voice calls andthat SMS are largely additional to voice calls to mobile phones, rather than asubstitute. Further, a more recent Oftel survey (Consumers’ use of mobiletelephony - 27 January 2003) found that 30% of mobile users never use an SMSinstead of a mobile voice call, 20% rarely do so, 14% do so sometimes and 36%do so frequently.

Unified messaging services and ‘message clips’ as a substitute for mobile tomobile calls

3.37 Unified messaging services and ‘message clips’ (short voice or videomessage sent over the IP network) could also develop as a potential substitute forvoice calls. However, these technologies are not developed enough to bedeployed and it is difficult to assess when they will become commerciallyavailable. Moreover, the Director is of the view that, as with SMS, these services,

23

once available, are more unlikely to put any competitive pressure on voice calltermination charges, as the same MNO sets the termination charge for all theseservices.

Voice over Internet Protocol (VOIP) calls as a substitute for calls to mobiles

3.38 Voice calls to mobile phones could also potentially be delivered as VOIP callsusing general packet radio system (GPRS). GPRS is the enhancement to GSMthat allows a mobile subscriber to transmit and receive data in a packet mode.Packet mode data has the advantage that the resources of the network are onlyused when data is transmitted or received. This important enhancement allowsMNOs to charge users for the amount of data they send or receive, as opposed tothe length of time they are connected; hence it is ideal for services such as webbrowsing and connecting to the Internet. When a mobile subscriber is connectedto the Internet (is “on-line”) they could be contacted by another person, who is also"on-line", through a VOIP call. An example is the service provided by MicrosoftMessenger, which allows two parties who are on-line to set up a VOIP call bylogging on to a dedicated website (for example, an individual can go to the websitethat offers the VOIP service and check if the person they want to call is on-line. Ifthey are on-line, the server sends an alert saying that an incoming call is beingmade, they can then decide whether to take the incoming call).

3.39 VOIP calls could represent an effective substitute if the price for standardvoice calls to mobile were to rise (due to an increase in termination charges).This is due to the fact that the payment arrangement is different because on-linemobile users pay for the data they send or receive (at a per bit rate). Therefore inthe example given above, the individual making the on-line call only pays to be on-line (this does not include a mobile termination charge) and the target of the call (ifthey answer the call) similarly only pays to be connected to the website/server.Thus, in a VOIP call both the called and the calling parties pay forreceiving/making it. Such a partial Receiving Party Pays (RPP) arrangementchanges the incentives on the called party and is likely to affect their behaviour,although it is unclear in what specific manner. For example, it is possible that thecalled party does not accept VOIP calls because they would have to in part pay forthem, thus forcing the calling party to reach them via a standard voice call to theirmobile. In this case, VOIP calls would not impose competitive pressure on thelevel of the termination charges.

3.40 The constraining effect of VOIP calls may also be undermined by the MNOs'behaviour. The reason for that is that it is the MNO to which the called partysubscribes that sets both the voice termination charges and the price for theInternet connection. That MNO also determines the quality of service (i.e. datadelay and bit errors). Hence, it could adjust the GPRS quality parameters suchthat it was still acceptable for web browsing and e-mail, but not for voice calls.

3.41 A further reason why VOIP is at present unlikely to be an effective substitutefor standard voice calls to mobiles is that the called party must be on-line to be

24

contactable. Furthermore, the mobile handset must be GPRS-enabled and havethe hardware and software necessary to convert speech into data.

3.42 In conclusion, the Director considers that at present it unlikely that theavailability of VOIP calls could put competitive pressure on the level of mobilevoice call termination.

Call-back

3.43 Call-back refers to a situation where the direction of a call is ‘reversed’ andthe calling party is called back by the called party, either in an ad hoc manner orthrough a commercial scheme. Call-back could render an increase in terminationcharges unprofitable only if the profitability of outgoing calls is lower than that ofincoming calls, and call-back is carried out in sufficient volume.

3.44The Director has no evidence of any commercial operators currently offeringcall-back on calls to mobiles within the UK and found no evidence that the practiceof ad-hoc call-back is having a constraining effect on voice call terminationcharges.

3.45 It is possible that MNOs could introduce a call-back service to offer analternative to callers to their subscribers. The Director believes that this form ofcall-back could not be relied upon in the immediate future to act as a viableconstraint on mobile voice termination charges. This is partly because MNOs haveno incentive to introduce a service of a price and a quality such that it could act asan effective substitute for their own monopoly service. More details on theDirector’s view on this form of call-back are contained in Annex C on alternativesolutions.

3.46 Consequently, the Director is of the view that currently no competitivepressure on termination charges is exerted by or is likely to come from this source.

Initial conclusions on the behaviour of callers in response to an increase inthe price for calls to mobiles

3.47 On the basis of the evidence and the arguments discussed above, theDirector considers that the behaviour of callers in response to a rise in terminationcharges and, thus, in the price of calls to mobiles, is unlikely to render thisincrease unprofitable. Consumers’ low awareness of the prices of calls to mobilenetworks, the limited availability of effective substitutes and the use by the MNOsof on-net prices to separate the most price sensitive consumers suggests thatcallers are unlikely to react to a price increase. The Director has thereforereached the initial conclusion that no constraint on the level of mobile voice calltermination charges is currently likely to arise from the behaviour of callers tomobiles.

25

Behaviour of the called party in response to an increase in the price of callsto mobiles

Choice of network

3.48 There would be constraints on termination charges if mobile subscriberschose their network on the basis of the prices of incoming calls and, thus, switchednetwork as a result of an increase in these prices. However, as mentioned above,the CPP arrangement implies that the calling party, and not the called party, paysthe total price of a retail call. Therefore, the called party, who makes the choice ofthe terminating network, is not affected by the level of the prices of calls to her/him(and thus by the level of mobile termination charge of her/his network).

3.49 However, it is still possible that mobile subscribers could react to a rise in thetermination charges of the MNO they subscribe to by switching to a network withlower termination charges, if they expected that the higher price of calling themwould have an impact on their callers. For this to be true, it is the Director’s viewthat a number of conditions would have to be met:• mobile subscribers would have to value incoming calls to such an extent that a

change in the price of these calls could make them change network;• callers to mobiles should be sensitive to the price of outgoing calls;• callers to mobile should be aware of the mobile network they are calling and of

the price of calling it; and• mobile subscribers should be aware that callers to mobile are sensitive to and

have knowledge of the prices of outgoing calls.

3.50 The Director considers that only if all four of the above conditions have beenmet, would mobile subscribers consider that the level of the termination charges oftheir network affects the cost for others to call them, thereby influencing thenumber of calls they would receive. This could then act as a competitive constrainton mobile termination charges, since an MNO that increased its charges wouldsuffer a loss of users on its network.

3.51 However, the evidence collected by the Director leads to two mainconclusions:• that consumer awareness of the price of calls to mobile phones is low

especially in respect of the price of calls to each specific network; and• that the price of incoming calls is not considered by consumers to be an

important factor in their choice of a mobile network and other factors are moreinfluential.

3.52 In Oftel’s consumer survey from August 2002 (Consumers’ use of mobiletelephony - published 24 October 2002), just 46% of consumers said they “usuallyknew” they were calling a mobile phone from their fixed phone at home. AQualitative research carried out in March 2001, showed that few people had anyreal idea of the cost of calling mobiles, but it was perceived as ‘expensive’.

26

3.53 Evidence collected by the CC (paragraph 2.136 to 2.141 in the CC December2002 report) suggests that the majority of callers did not know the identity of theparticular mobile network they were calling and that a large number of callers hadlittle knowledge either of actual prices or the relative levels of charges for callingeach network. The CC concluded that these findings overall “reveal a degree ofawareness on the part of consumers which is insufficient to enable them to makean appreciable impact on prices or to drive termination charges down tocompetitive levels” (paragraph 2.141 in the CC report).

3.54 The introduction of mobile number portability has further complicated mattersby rendering it extremely difficult for callers to find out which network they arecalling (and thus what is the relevant cost), unless they have a repeated callingrelationship with the person they are calling.

3.55 Oftel survey data on residential mobile owners suggests that the choice ofwhich mobile network to subscribe to is mostly driven by the cost to subscribers(and not to those who call them) of being part of a network. A consumer surveyfrom August 2002 (Consumers’ use of mobile telephony - published 24 October2002) revealed that:• 18% of mobile customers found out how much it would cost others to call their

mobile before choosing their network (up from 15% in February 2002; and• 8% of customers considered the cost of other people calling them as a major

factor in their choice of the mobile network (it was 9% in February 2002.

3.56 For the majority of residential customers (59%), outgoing call costs were themost significant reasons for choosing a network, compared with coverage andreception (21%) (Consumers’ use of mobile telephony - February 2002).

3.57 Business users – in particular small and medium sized enterprises (‘SMEs’) -appear to be more concerned than residential users about the cost of calling theirmobiles. This might be because their business depends on calls from clients, orbecause a significant part of their own phone bill is from their employees callingmobile phones. Oftel’s research (Consumers’ use of mobile telephony - 24October 2002) shows that 27% of SMEs consider the cheapest network to callwhen choosing a mobile network (up from 19% a year before). Similar toresidential consumers, SMEs revealed that other factors, such as coverage andcustomer service, were however of greater importance to them than the cost ofincoming calls when choosing the mobile network. SMEs are a small proportion oftotal business mobile ownership.

3.58 The British Market Research Bureau (BMRB) survey commissioned by theCC also found that the cost of incoming calls was not an important factor forconsumers when choosing their mobile network. It ranked 10th out of the 14factors suggested, the most important being ‘the price you pay to call others’. Inaddition, 61% of mobile users expressed more concern about the cost to them ofcalling others than the cost to others of reaching them. Only 9% were moreconcerned about the cost to others (paragraph 2.133 to 2.135 in the CC report).

27

3.59 These findings are consistent with those of the surveys of residentialcustomers commissioned by two of the MNOs. O2’s NOP survey found that fornearly 75% of respondents the cost to other people of calling them on their mobilephone was an unimportant factor when they decided which mobile network to join.Fewer than 20% said that it was important. A high proportion (85%) of bothcategories were unable to say why they took the view they did (paragraph 2.133 to2.135 in the CC report). The NOP survey commissioned by Vodafone showedthat the price of outgoing calls was much more important to mobile users than thecosts that others incurred to reach them (paragraph 2.133 to 2.135 in the CCreport.).

3.60 The Director considers that the available evidence supports the conclusionthat an insufficient number of consumers consider the prices of incoming callswhen choosing their network for it to provide a competitive constraint on the priceof calls to mobiles (see also section on closed user groups below).

Closed user groups

3.61 The existence of ‘closed user groups’ (i.e. groups of people whose memberscare about the cost to the other members of calling their mobile number), couldmitigate the effect of the CPP arrangement and act as a constraint on voice calltermination charges. However, for this constraint to be effective, these groupsshould be numerous and not isolated through targeted tariffs that bypasstermination.

3.62 As discussed above, the evidence available shows that few groups of peopleare sensitive to the cost of incoming calls, and even those that are sensitiveconsider the cost of outgoing calls to be far more relevant. The NOP survey,conducted for Vodafone and whose results are in contained in the CC’s December2002 report (paragraph 2.116 in the CC report ), reveals that 19% of mobile usersare on the same network as members of their family because it reduced callingcosts. Another NOP survey commissioned by O2, and reported in the CC report(paragraph 2.116 in the CC report ), also found that for around one-third ofrespondents the network used by people with whom they are likely to becommunicating is an important factor when deciding which network to join.However, it also found that for over half of respondents it was unimportant and ahigh percentage of these groups could not say why this factor was, or was not,important to them.

3.63 The BMRB survey commissioned by the CC (paragraph 2.116 in the CCreport ) confirms these findings. It found that 81% of consumers had neverchosen, or even changed, mobile network in order to be on the same network asthe people to whom they often spoke, while 15% had chosen their network on thisbasis and 4% had changed it for this purpose.

3.64 The Director considers that this evidence further reinforces his initialconclusion that most residential consumers are not affected in their choice of

28

mobile network by the cost to others of calling their mobile number. Only a smallminority of residential mobile users are interested in keeping the cost of callcharges among their circle of family and friends low.

3.65 Business users seem to be more concerned about the cost of calling theirmobiles both for their employees and their customers. Oftel’s August 2002 surveyof SMEs (Business use of mobile telephony - published 24 October 2002) showsthat a fifth of the SMEs with mobile phones had taken steps to reduce the cost tocall their own mobile phones (ranging from 19% of small businesses up to 38% ofmedium businesses), such as using mobile-to-mobile adaptations or private wireservices (see below).

3.66 In addition, the survey reports that 70% of SMEs with mobile phones usesome method to reduce the cost of customers to call their mobile phones. Toachieve that, 27% claimed to have chosen the cheapest network to call whenselecting a mobile network (up from 19% a year ago). However, the survey showsthat the most popular measure to keep cost down is keeping the call to the mobileshort (47%).

3.67 Overall, SMEs seem to be more concerned than residential consumers aboutthe costs of calling their mobiles and a significant proportion appeared to beadapting their behaviour to try to minimise this cost. However, SMEs are a smallproportion of total business mobile ownership and do not provide a completepicture of business users’ behaviour. In addition, those firms also stated that thecost of outgoing calls and the coverage were their most important concerns whenchoosing the network to which their employees subscribe. So even for thesecustomers, features other than the price of incoming calls have more influence ontheir choice of the network.

3.68 In addition, the effect of closed user groups in constraining voice calltermination charges is lessened by the ability of the MNOs to separate thesecustomers from others through special self-selecting arrangements that by-passhigh termination charges (e.g. on-net calls or private wire services). In this way,those customers who are most concerned about the price of calling mobiles andwho are most able to bring pressure to bear on the MNOs are prevented fromplacing any pressure on termination charges. The MNOs are then able to imposehigh termination charges on the less price-sensitive users.

Private wire services and mobile-to-mobile adaptations

3.69 As mentioned above, closed user groups do not generate sufficientcompetitive pressure to constrain the level of termination charges because theMNOs can separate them from less sensitive customers by offering specialarrangements that bypass termination. By separating out the more price-sensitivecustomers, the MNOs face less competitive pressure in setting charges for theother customers. Private wire services and mobile-to-mobile adaptations areexamples of such arrangements that segment the market in this way.

29

3.70 Private wire services are provided as leased lines that connect a corporateprivate exchange to a mobile network. They allow corporate customers to makeand receive calls to and from mobile phones without paying the retail price forfixed-to-mobile calls. Under private wire arrangements, the price for calls fromfixed-to-mobiles is lower than the price paid by the generality of fixed linecustomers. For SMEs that try to reduce the costs of calls to their own mobiles,private wire services are a relatively popular solution (Oftel’s Business use ofmobile telephony - published 24 October 2002 noted that 7% of small businessesand 21% of medium businesses used private wire services in this way).

3.71 Mobile-to-mobile adaptations consist of devices which give callers a radio linkfrom their private exchanges to allow fixed-to-mobile calls to be converted to on-net mobile-to-mobile calls. Using this facility, calls can be made from the fixedphones in the office to the company’s mobiles but are carried and charged in thesame way as calls from mobiles. This allows the subscriber to take advantage oflower prices for on-net calls rather than paying the standard price for calls fromfixed-to-mobiles.

3.72 Private wire services and mobile-to-mobile adaptations are likely to beintroduced only where the savings from lower prices for call to mobiles outweighthe costs of installing them. This, in turn, is likely to occur only where a sufficientproportion of the fixed line phone calls of the customer is directed to a singlemobile network. Thus, they are unlikely to be an effective substitute to standardfixed-to-mobile calls for residential consumers. However, as mentioned above, themain reason why their presence is unlikely to constrain termination charges forfixed-to-mobile calls generally is that they constitute a targeted tariff aimed atseparating out the most price-sensitive customers. They do not impose acompetitive constraint on the prices which operators can charge for calls to lessprice sensitive customers.

Multiple SIM cards

3.73 If mobile users could receive their incoming calls on mobile networks otherthan the one to which they subscribe for making outbound calls, this could putsome pressure on mobile voice termination charges. For that form of substitutionto take place, the called party must be able to switch their handset betweendifferent networks. This is possible through the use of multiple SIM cards.

3.74 A subscriber can have a mobile phone with an internal dual SIM cardholderthat allows him to switch from one network to another by turning the phone on andoff. There are already devices available in the UK market which allow customersto use different SIM cards in the same handset and, thus, switch betweennetworks (Oftel is aware of the existence of SIM holders that can hold up to fourSIMs). However, to place some pressure on the MNO with high terminationcharges the subscriber should be, by default, on the network with cheap voice calltermination charges and only switch to the other network to make cheap outboundcalls. This is laborious and time-consuming (because to switch networks is anoperation that requires time). In addition, it relies on the called party having the

30

incentive to change network every time (s)he needs to make a call and to switchback again at the end of the call, so that the next inbound call will use the networkwith lower termination charges. It is doubtful that such an incentive currentlyexists given the CPP arrangement and customer behaviour under thatarrangement. Hence, it is more likely that subscribers currently exploit the dualSIM card opportunity purely to take advantage of differences in the prices ofoutgoing calls.

3.75 An automatic mechanism to re-route calls can also be considered. In thatcase, a mechanism would be implemented that instructs the called party’s mobilephone to switch network automatically when a call is arriving. No such mechanismcurrently exists and, in the Director’s view, it is unlikely to develop in theforeseeable future, due to significant technological difficulties and to the lack ofincentives on the part of the called party to make use of a facility that reduces thecost of incoming calls. In addition, a further hurdle is posed by the need for MNOsto allow access to their handsets/SIM cards to install the necessary software (aswell as allowing any necessary signalling to pass across the mobile network tocontrol network selection) since the MNOs have little incentive to give this co-operation.

3.76 The main limitation of these two scenarios is that they rely on the called partyhaving an interest in reducing the cost to other persons of calling his/her mobile(as for example (s)he needs to acquire a multiple SIM handset). At present, thisincentive is absent (see above paragraph 3.7); though this could change overtime,as discussed in Annex C.

Call- divert

3.77 To have calls automatically forwarded, mobile users could subscribe to apersonal numbering service (PNS) which allows them to give out a single numberand have all their calls directed to any number they specify (e.g. their fixed line).Calls to PNS are more expensive than calls to mobile numbers because:• to divert calls an additional leg is added to their route (Calls to a personal

number go to the PNS provider first, which then forwards it to the appropriateterminating network). PNS providers have to ensure that they can cover thecost of terminating calls to any number specified by the subscriber (i.e. also tomobile numbers); and

• PNS providers need to keep a database of the numbers to which it mustforward the calls.

3.78 Calls to PNS can be either CPP or RPP, but in either case their higher priceimplies that it seems unlikely that they could represent effective substitutes to callsto mobile phones for called and calling parties. This service may, thus, beattractive only for those subscribers who are sensitive to the price for others to callthem on their mobile. However, the MNOs will typically have already separatedthese subscribers from the generality of subscribers by offering them speciallytargeted tariffs.

31

3.79 An alternative to PNS is for the called party to use a single terminal that isboth a cordless phone and a GSM phone. This allows subscribers to make andreceive calls using their "fixed line" (via the cordless element of the phone), whenwithin the range of the cordless base station and the GSM element, when outsideof it. Thus, while the called party is within the range of the cordless base station,there is a substitute for the termination service.

3.80 However, the cost of such dual phones is currently high and, since the rangeof the cordless base station is limited, the savings that accrue to the called party(from lower outgoing charges) are small. It is the calling party who derives most ofthe benefits from the use of these phones, but, as discussed above, due to CPP,most mobile subscribers would not factor into their decision any saving apart fromtheir own (see section on closed user groups for consideration of the minority ofmobile subscribers that do consider the cost to others). Hence, these phones arenot widely used. The situation may, however, become different if over time there isa change in the incentives on the called party change.

3.82 Therefore, for the reasons set out above the Director believes that automaticcall forwarding services do not currently generate significant pressure on the levelof mobile voice termination charges.

Initial conclusions on the behaviour of called party in response to anincrease in the price for calls to mobiles

3.83 On the basis of the evidence and the arguments discussed above, theDirector considers that the behaviour of mobile subscribers in response to a rise intermination charges above the competitive level and, thus, in the price of calls totheir mobiles is unlikely to render this increase unprofitable. The majority ofsubscribers are unlikely to react to a price increase and the presence of someusers who choose their mobile network also on the basis of the cost of incomingcalls is not sufficient to constrain voice call termination charges (because of theability of the MNOs to separate these customers from the other through specialself-selecting arrangements). Hence, at present, no significant constraints on theMNOs’ ability to set termination charges above the competitive level appear toarise from the behaviour of the called party.

Initial conclusions on retail demand-side substitution

3.84 In conclusion, the Director considers that there are no effective retaildemand-side substitutes that could constrain mobile termination charges to thecompetitive level.

Wholesale demand-side substitution

3.85 Substitution of wholesale voice call termination on an MNO’s network withwholesale voice call termination on a different MNO’s network cannot provide anydirect constraint on termination charges, since an operator wishing to offer calls to

32

a customer of a specific MNO must purchase termination from that MNO or it willnot be able to terminate the calls (on this issue see also the section on multipleSIM above).

Initial conclusions on demand-side substitution

3.86 For the reasons listed above, the Director considers that at present, there areno effective demand-side substitutes for voice call termination to specificsubscribers of a particular MNO. However, before reaching an initial conclusion onthe appropriate market definition, it is necessary to examine if there is anypotential for supply-side substitution or if products (or areas) over which there arecommon pricing constraints should be included within the market definition.

Supply-side substitution

3.87 Supply-side substitution occurs when, in response to a rise in the price of aproduct, suppliers of other products switch into supplying the product whose pricehas risen and render the price increase unprofitable for the firm whichimplemented it. This entry has to be fast enough (i.e. happen within one year) andat sufficiently low cost, otherwise it would be classified as new entry and its impactcould be considered as part of the SMP assessment rather than in the marketdefinition.

Retail supply-side substitution

3.88 For retail supply-side substitution to impose a constraint on the level ofmobile voice termination charges, there would have to be operators which do notcurrently provide calls to mobiles that can switch into such provision and thusundermine a price set above the competitive level. In order to have such an effect,the new provider(s) would have to be able to provide a service which did not relyon the provision of termination from the MNO to which the called party subscribes.At present, the Director cannot identify any such provider that would not dependon the MNO to which the called party subscribes to terminate the calls.

Wholesale supply-side substitution

3.89 For supply-side substitution to be an effective constraint on mobile voicetermination charges, there have to be other firms who could switch into theprovision of wholesale voice call termination to a specific subscriber of an MNO’snetwork with relative ease in response to an increase in termination charges.

MNOs other than the one to which the called party subscribes

3.90 Supply-side substitution in the wholesale market for mobile voice terminationcould come most easily from other MNOs, which have the necessary networkinfrastructure and expertise to terminate mobile calls. However, having a mobilenetwork is not sufficient for an MNO to be able to terminate calls to a subscriber ofa rival network. For this to happen, the mobile phone should automatically move

33

from its home network, on to that of the alternative MNO on which the call wouldthen be terminated.

3.91 It is possible for GSM handsets to operate on more than one network. Thiswas an original design requirement of GSM, and is relied upon for internationalroaming. However, it is not currently possible for the originating network of a callto a mobile to select which MNO terminates a mobile call.

3.92 Hence, it is the Director’s view that at present the lack of access tohandsets/SIM details and the technical difficulties in taking control of the handsetconstitute an effective barrier to an MNO providing voice termination tosubscribers of another MNO.

Local Area Networks over short-range radio technologies or Wireless Local AreaNetworks