Embed Size (px)

Citation preview

Returning Preparers

TAX SEASON 2018

Welcome and Introductions

Thank you for volunteering Mechanics—Restrooms, breaks Ask questions at any time Overview of training materials

Training Materials IRS Training Packet 4480

Test Pub 6744 Pub 4012 Pub 5157A

Practice Problems & Review Questions Digital Copies available at

http://www.empirejustice.org/cash/cash-training-center/ IRS/CASH Forms

Agenda

• Last Year Metrics • CASH Overview

– CASH Site and Hours

• Tax Preparer Requirements • Tax Preparer Process • Fed Tax Topics

– Questions on Basic Concepts – Advanced Income Topics

• Fed Adjustments • Fed Deductions • Fed Credits • NYS Return • Finishing the Return • Practice Lab Instructions • IRS Test Certification Instructions

Metrics

TOTAL CLIENTS 8051 HEALTH CARE COVERAGE

Type Number Perc Full Year Coverage 7184 89.23% Shared Resp Payment 309 3.84% Exemption 538 6.68% Prem Tax Credit 25 0.31%

Other Forms Education Credit 472 5.86% Schedule A - Itemized 317 3.94% Schedule B – Interest/Div 48 0.60% Schedule C – Self-emp 279 3.47% Schedule D – Stock 276 3.43% Schedule E – Rentals or K-1 31 0.39%

Metrics-EIC

FILING STATUS

FILING STATUS Number % of total # EIC % EIC Amount EIC Ave

Head of Household 1998 24.82% 1731 86.64%

4,817,083.00

2,782.83

Married Filing Jointly 719 8.93% 377 52.43%

966,503.00

2,563.67

Married Filing Seperate 190 2.36% 0.00%

Qualifying Widow(er) 3 0.04% 3 100.00%

7,161.00

2,387.00

Single 5141 63.86% 1259 24.49%

470,025.00

373.33

TOTAL CLIENTS 8051 3370 41.86%

6,260,772.00 1,857.80

Refunds/Bal Due

Refunds/Bal Due

Filing Status # Refund Amt Refund Ave Refund # Bal Due Sum Bal Due Ave Bal Due

Head of Household 1,927 8,288,121

4,301.05 62 67,844

1,094.26

Married Filing Jointly 640 2,045,290

3,195.77 60 62,310

1,038.50

Married Filing Seperate 122 90,336

740.46 63 57,450

911.90

Qualifying Widow(er) 3 7,987

2,662.33

Single 4,386 3,562,478

812.24 656 540,772

824.35

Totals 7,078 13,994,212

1,977.14 841 728,376

866.08

CASH OVERVIEW

• New Look for this year – We will work together at 1 site

– For Tax Preparers – will look a bit different • In-Person Tax Prep

– Set up in sections of 8 so that staff and QR are more accessible

• Drop off Tax Prep – Separate area for Drop-off – Working with community groups and local employers to increase

drop-off.

– Will be offering more information at site so can use in-person to do more complicated returns.

– Staff – seasonal staff will perform in rotating roles, and headquarters staff will be on hand to supervise.

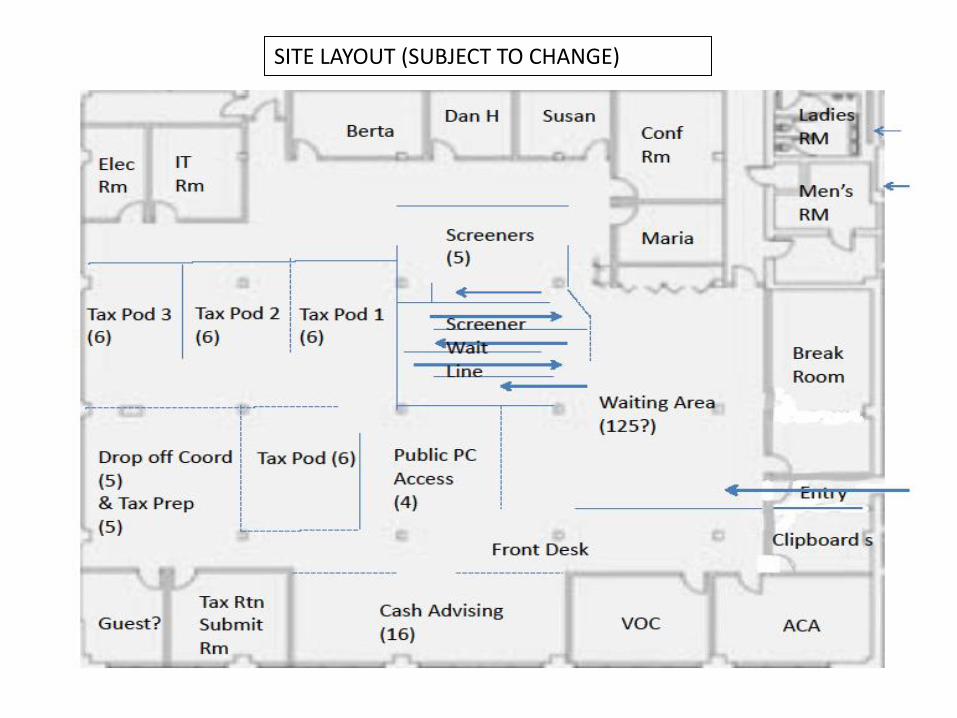

SITE LAYOUT (SUBJECT TO CHANGE)

Staff Roles

• Screener – new role in coordination with Control Desk (formerly Front Desk) – Will see each client as they come in to determine if they have all documents

needed. – Will make determination as to clients over limit – Will direct clients to self-help computer to get needed documents

• Banking – Go-to person to set up bank accounts • Tech-ops – Available to assistance with printers, computers, etc • Director or Designee – Available to handle site issues as needed • Quality Review – Will work with groups of volunteers to help with

questions and preform final QR on returns. • Transmissions/Rejects – will be responsible for transmitting returns and

working with rejects • Vol Manager – work with volunteer co-ordination • Admin Assistant – order supplies for site and break room

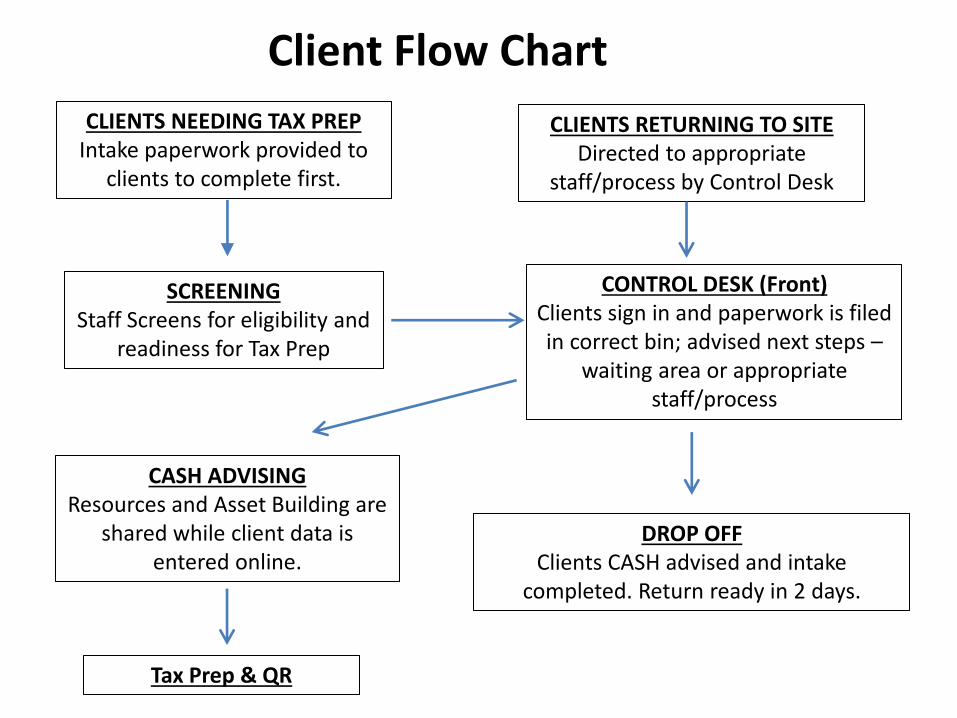

CLIENTS NEEDING TAX PREP Intake paperwork provided to

clients to complete first.

SCREENING Staff Screens for eligibility and

readiness for Tax Prep

CONTROL DESK (Front) Clients sign in and paperwork is filed in correct bin; advised next steps –

waiting area or appropriate staff/process

DROP OFF Clients CASH advised and intake

completed. Return ready in 2 days.

CASH ADVISING Resources and Asset Building are

shared while client data is entered online.

Tax Prep & QR

CLIENTS RETURNING TO SITE Directed to appropriate

staff/process by Control Desk

Client Flow Chart

TAX PREPARER PROCESS

• Tax Preparer Process – Traditional Process

– Drop off model

• VITA Scope of Service – IF NOT SURE--ASK SITE STAFF

• Forms used by C.A.S.H. – IRS INTAKE SHEET

– CASH INTAKE SHEET

– OTHER CASH FORMS • Disclosure Forms

• Envelope Cover and QR Sheet

TAX PREPARER REQUIREMENTS

• Complete Training – In person

– On-line using link and learn

– Combination

• Pass IRS Certification Test before volunteering

• Must work at least 1 shift between Jan 24-27 – “Soft Opening” Will give new preparers

opportunity to work with experienced preparers

• Work a minimum of 1 shift each week.

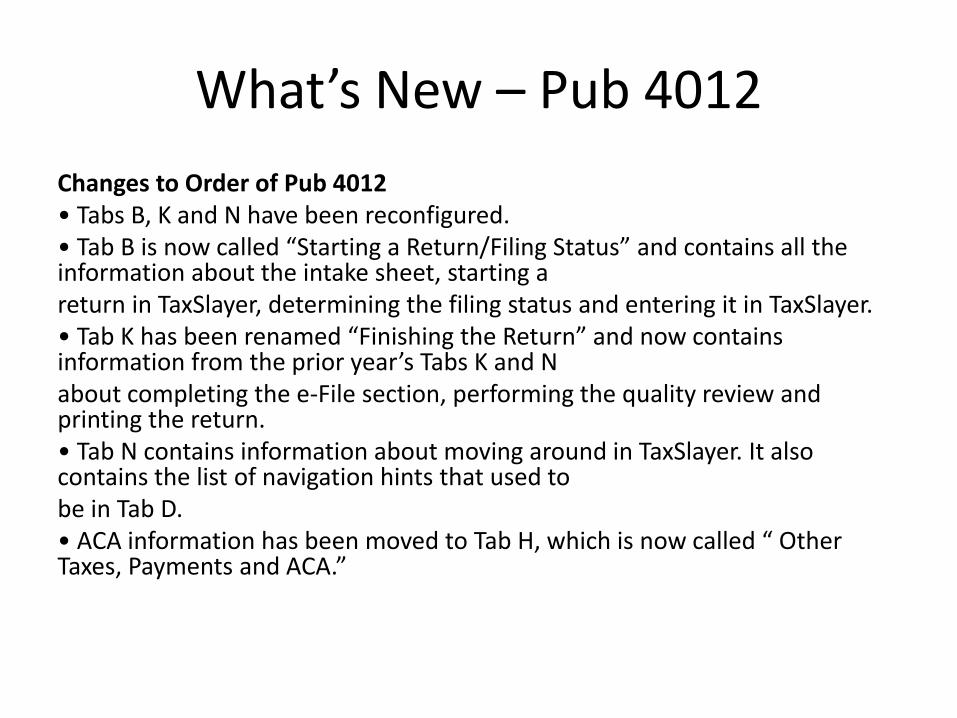

What’s New – Pub 4012

Changes to Order of Pub 4012 • Tabs B, K and N have been reconfigured. • Tab B is now called “Starting a Return/Filing Status” and contains all the information about the intake sheet, starting a return in TaxSlayer, determining the filing status and entering it in TaxSlayer. • Tab K has been renamed “Finishing the Return” and now contains information from the prior year’s Tabs K and N about completing the e-File section, performing the quality review and printing the return. • Tab N contains information about moving around in TaxSlayer. It also contains the list of navigation hints that used to be in Tab D. • ACA information has been moved to Tab H, which is now called “ Other Taxes, Payments and ACA.”

What’s New Taxes

• Expired Provisions

– Provisions are due to expire 12/31/16 BUT will they?

• Exclusion from Gross Income of qualified principal residence

• PMI deductible on schedule A

• Deduction for Qualified Tuition and Fees

What’s New

• Standard Mileage Rate – For 2017, the following rates are in effect:

• 53.5 cents per mile for business miles driven

• 17 cents per mile driven for medical or moving purposes

• 14 cents per mile driven in service of charitable organizations (no change)

• Itemized Deductions – Medical –

• The 7.5% threshold for taxpayers who have attained the age of 65 has expired.

• All taxpayers are now subject to a 10% AGI threshold.

4012 Reference Manual Training Based on Info in this Manual

• Tab A: Who Must File • Tab B: Starting a Return and Filing Status • Tab C: Exemptions/Dependency • Tab D: Income • Tab E: Adjustments • Tab F: Deductions • Tab G: Nonrefundable Credits • Tab H: Other Taxes, Payments and ACA • Tab I: Earned Income Credit • Tab J: Education Benefits

Federal Tax Topics

• Review “Basic” Tax Concepts

• Any Questions? • Filing Basics ( WHO MUST FILE)

• Filing Status

• Exemptions/Dependency

• Basic Income

• There is also more review information available on the CASH Web Site

Advanced Income

• Self -Employment Income/Expenses

• Pension Income With Taxable Amount Not Determined

• Stock Sales

• Credit Card Debt Forgiven

• Mortgage Loan Modification – PUB 4681

Self – Employment Income/Expenses

• Guidelines

– Cannot show a loss

– Cannot have expenses over 10,000

– Cannot have employees

– No Inventory

– No Home office deduction

Self – Employment Income

• Make sure to include both income form

– 1099-Misc

– Cash Income

• If Client gives you 1099-Misc – ASK if they have any cash income.

• Client should have records of Cash Income

• Directions for input into TaxSlayer starts at D-13 in Pub 4012.

Self – Employment Expenses

Type Deductible Expenses Non-Deductible Expenses

Advertising (Line 8)

Any materials for marketing your business (e.g. flyers, signage, ads, branded promo items, events or trade shows) and the cost of developing those (e.g. agency or designer costs).

Office holiday parties, gifts (e.g. books) that aren’t branded (use “Other Expenses”)

Business Insurance (Line 15)

Insurance intended to protect your business (e.g. fire, theft, flood, property, malpractice, errors and omission, general liability, malpractice, workers’ compensation).

Health insurance, auto insurance (use “Car Expenses” or Add Mileage), disability insurance

Car Expenses (Line 9) Use Standard Mileage rate – Reminder – only from 1st job to 2nd job, not to or from home.

Expenses (other than Parking/Tolls) if you use the standard mileage rate

Self Employed - expenses

Type Deductible Expenses Non-Deductible Expenses

Meals / Entertainment (Line 24b)

Meals or entertainment that you had with a client and during which you engaged in business discussions, or those incurred while traveling on an out-of-town business trip.

Meals for yourself (e.g. on lunch breaks); dues for athletic clubs

Office Expenses (Line 18)

Office expenses (e.g. cleaning services for office, general office maintenance) that don’t have a separate category.

Home office costs (use “Home Office”), rent (use “Rent”), utilities

Supplies (Line 22)

Any supplies that you use and replace (e.g. cleaning supplies if you clean homes, office supplies like pens or printer ink, hot/cold bags if you do delivery).

Office decorations and some other office expenses (use “Office Expenses”)

Travel (Line 24a)

Travel costs related to business trips (e.g. lodging, airfare or rental cars, local transportation). The travel must be overnight, away from your residence and primarily for business.

Personal costs while traveling (e.g. dinner with a friend), meals while traveling (use “Meals”)

Other Expenses (Line 27a)

Any other business expenses that are ordinary and necessary (e.g. education to improve skills for your job, banking fees, association dues, business gifts, industry magazines).

Expenses with their own separate categories, expenses that aren’t ordinary and necessary

Review Questions for Self-Emp.

1. (T/F) Total expenses may not exceed $10,000 for VITA volunteers to use Schedule C or C-EZ.

2. (T/F) If a taxpayer files a Schedule C or C-EZ and his/her net income is more than $400 he/she must pay Social Security Tax on the amount of net income.

3. (T/F) Most expenses can be entered directly on Schedule C or C-EZ.

4. (T/F) Taxes are paid only on the profit of a small business. 5. (T/F) CASH clients may not be aware that they should

declare babysitting or hairdressing money as a small business.

6. What benefits does the client receive from declaring self-employment income?

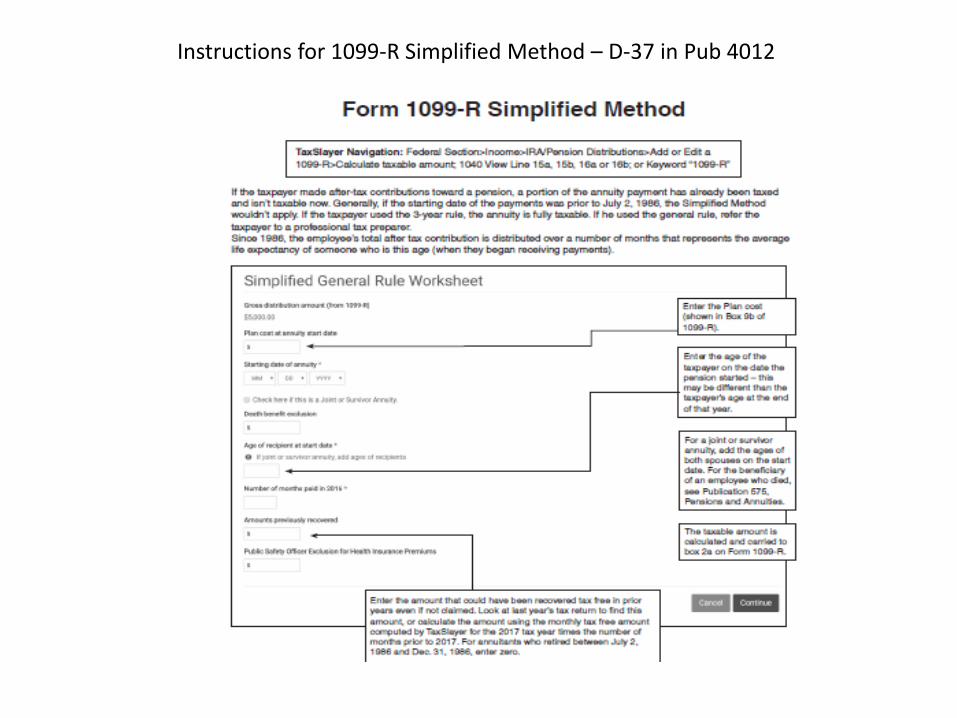

Pension Income With Taxable Amount Not Determined

Only applicable IF Box 2a is blank and an amount in Box 9b

Instructions for 1099-R Simplified Method – D-37 in Pub 4012

No Simplified Method Needed Different Amounts in Box 1 and 2a. Just enter both amounts.

Stock Sales (Capital Gains and Losses)

• See Pub 4012 – D-20 for directions on how to enter in TaxSlayer • Need 1099B (Brokers Statement) to enter

– Short-Term Capital Gains and Losses—Assets Held One Year or Less – Long-Term Capital Gains and Losses—Assets Held More Than One Year

• Transactions divided into four categories: – Short term transactions with basis reported to the IRS - categorized as

“Box A.” – Short term transactions with basis not reported to the IRS -

categorized as “Box B.” – Long term transactions with basis reported to the IRS - categorized as

“Box D.” – Long term transactions with basis not reported to the IRS - categorized

as “Box E.”

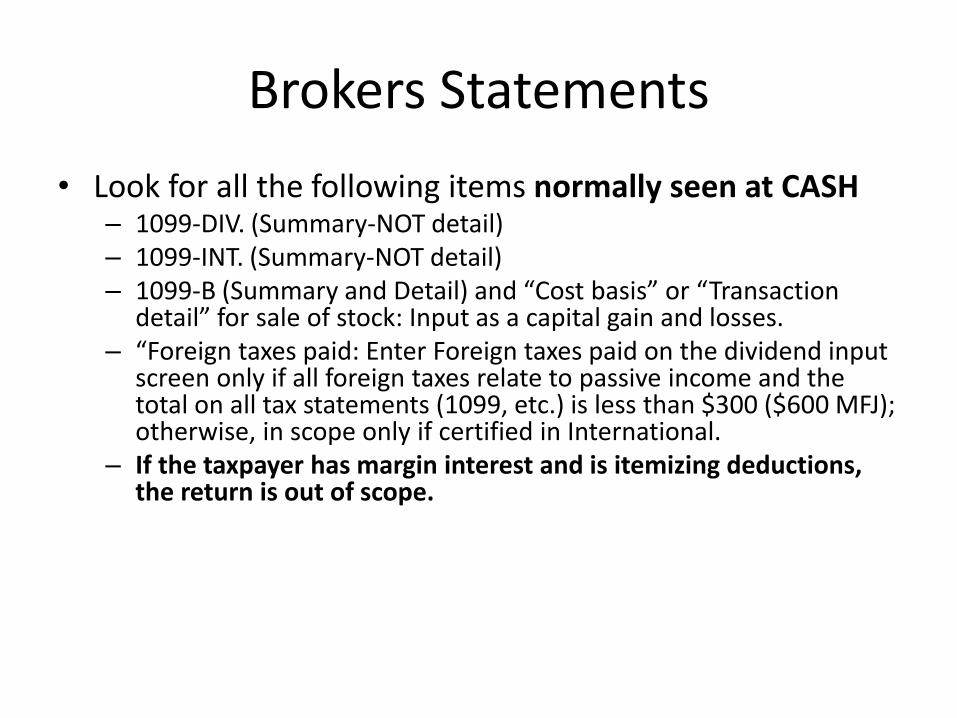

Brokers Statements

• Look for all the following items normally seen at CASH – 1099-DIV. (Summary-NOT detail) – 1099-INT. (Summary-NOT detail) – 1099-B (Summary and Detail) and “Cost basis” or “Transaction

detail” for sale of stock: Input as a capital gain and losses. – “Foreign taxes paid: Enter Foreign taxes paid on the dividend input

screen only if all foreign taxes relate to passive income and the total on all tax statements (1099, etc.) is less than $300 ($600 MFJ); otherwise, in scope only if certified in International.

– If the taxpayer has margin interest and is itemizing deductions, the return is out of scope.

Brokerage Statement

1099 – DIV

1099 – INT

Brokerage Statement Stock Sales

Short Term

Long Term

Capital Loss Carryover

• Very Rare at Site – need to know for certification Test

• Has to have information from previous tax year

• Enter in Schedule D Menu

Credit Card Debt Forgiven

• Anything but Credit Card Debt is OUT OF Scope for CASH/VITA.

• Contact Site Staff if question about what can be used.

• Client will have form 1099-C if over $600 but as with other income, must report any debt forgiven. – ALWAYS ask

• Enter in TaxSlayer under Income>Other Income>Cancellation of Debt Form 1099-C

Form 1099-C – Credit Card

1099-C – Qualified Principal Residence Indebtedness

• This is rarely seen at CASH

• This provision was expired and has not yet been extended.

• Refer to pages Ext-1 to Ext-6 in Pub 4012 for more information.

• Contact SITE STAFF if this needs to be done at site.

Adjustments/Deductions/Credits

Use this section for 13614-C to review what adjustments/deductions/credits will benefit clients

Itemized Deductions

Adjustment to income

Adjustment to income

Adjustment to income

Common Adjustments to Income

• Reduces Gross Income – Educator expenses

• Limit to $250 • Must be an educator in K-12

– Health savings account deduction • HAVE TO HAVE HSA Certification.

– NOT CERTIFIED—CALL QR STAFF ASSIGNED TO YOUR AREA

• Money that client or designee put in HSA. • NOT money put in by Employer (Code W on W-2 Form)

– IRA deduction – Not Normally Seen at CASH • Money put into IRA by client. NOT money from Employer Sponsored program

– Penalty on early withdrawal of savings • Seen on Clients Bank Int. Form • Should automatically flow to adjustments

– Student loan interest deduction • Limit to $2,500 • Form 1098-E

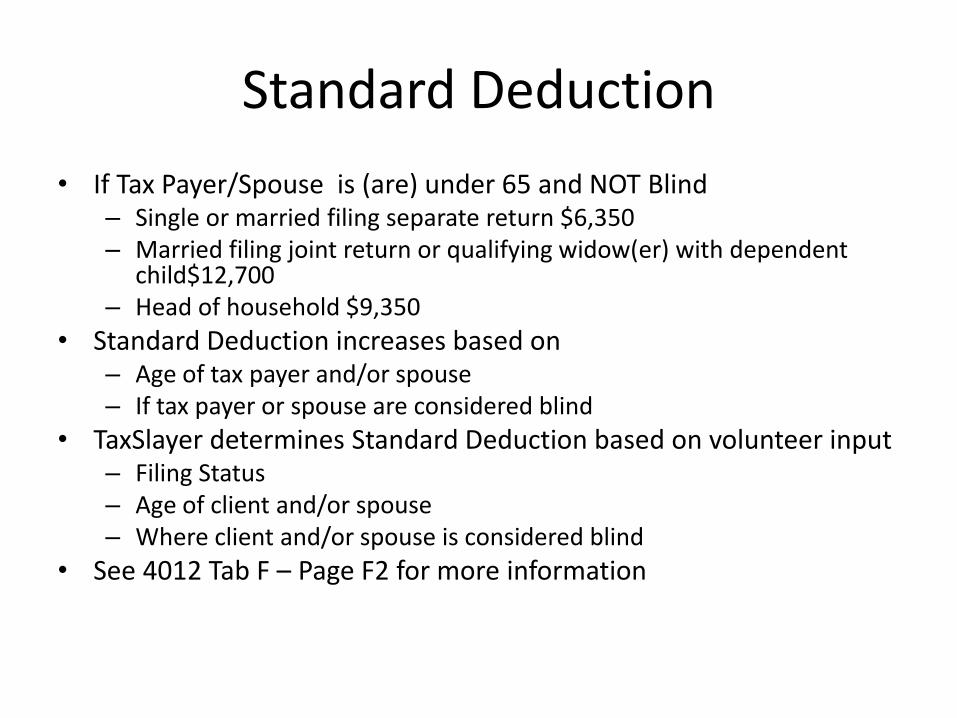

Standard Deduction

• If Tax Payer/Spouse is (are) under 65 and NOT Blind – Single or married filing separate return $6,350 – Married filing joint return or qualifying widow(er) with dependent

child$12,700 – Head of household $9,350

• Standard Deduction increases based on – Age of tax payer and/or spouse – If tax payer or spouse are considered blind

• TaxSlayer determines Standard Deduction based on volunteer input – Filing Status – Age of client and/or spouse – Where client and/or spouse is considered blind

• See 4012 Tab F – Page F2 for more information

Itemized Deductions

• Only useful to itemize when more than Standard Deduction

• 317 (3.94%) of our clients did itemized deductions

• Here is a look at the most common itemized deductions seen at CASH

Itemized Deductions

• Medical and Dental Expenses – can deduct only the part of your medical and dental

expenses that exceeds 10% of the amount on Form 1040, line 38.

– Can deduct • Medical Miles if not reimbursed • Co-Pays • Prescription Drugs • Out of Pocket Health Ins Premiums

– CANNOT Deduct • Over the Counter Drugs • Ins Premiums that are paid with before tax dollars through

employer • Gym Memberships

Itemized Deductions

• Taxes you paid

– NYS can deduct State Income Tax

– In RARE cases more advantageous to deduct Sales Tax

– Property Tax on 1st and 2nd home

– NOT Personal Property Tax in NYS

• Mortgage Interest

– Interest on main and 2nd home

– Also can deduct PMI

– CANNOT Deduct Property Ins

Itemized Deductions

• Charitable Contributions – Cash – no limit

• Can’t deduct Political Contributions • Can’t deduct gifts to friends

– Non-Cash • VITA Program has a limit of <$500 for non-Cash donations. • If over that limit, out of scope

• Unreimbursed Employee Expenses – Subject to >2% Income limit

• Gambling losses to the extent of Gambling Winnings

Credits

• Credits are determined by information given by client.

• Always be very careful about entering information as this can impact client refund

• Important to enter all income first as this what determines amount of most credits.

Credits – Non-Refundable Can only be used to the extent Taxes are owed – any excess will not be used and CANNOT be carried over

•

500

Amounts in these boxes can only add up to Tax

Child and Dependant Care Credit

• Available if you paid expenses for the care of a qualifying individual to enable you (and your spouse, if filing a joint return) to work or actively look for work.

• You may not take this credit if your filing status is married filing separately.

• The amount of the credit is a percentage of the amount of work-related expenses you paid to a care provider for the care of a qualifying individual. The percentage depends on your adjusted gross income.

• A qualifying individual for the child and dependent care credit is:

– Your dependent qualifying child who is under age 13 when the care is provided • Most normal for CASH clients

– Your spouse who is physically or mentally incapable of self-care and lived with you for more than half of the year, or

– An individual who is physically or mentally incapable of self-care, lived with you for more than half of the year, and either: (i) is your dependent; or (ii) could have been your dependent except that he or she has gross income that equals or exceeds the exemption amount, or files a joint return, or you (or your spouse, if filing jointly) could have been claimed as a dependent on another taxpayer's 2016 return.

Retirement Savings Contributions

• Look for Code D or Code E in Box 12 of W-2 – voluntary contribution or deferral to an IRA or other

qualified plan for 2017?

• AGI $31,000 or less ($46,500 if head of household, $62,000 if married filing jointly)

• Born before January 2, 2000

• Cannot be claimed as a dependent on someone else’s tax return for 2017

• Not a full-time student2 during 2017

Credits – Refundable

• Additional refund above amount of tax owed • Most common

– Child Tax Credit – If not used as non-refundable • Only available for dependents under 17

– American Opportunity • Up to 1,500 is non-refundable • Up to 1,000 is refundable

– Net Premium Tax Credit • Excess amount owed client from ACA subsidy

– Earned Income Tax Credit • Most Important for CASH clients

Review Questions for Deductions/Credits 1. (T/F)Alimony paid to a former spouse can be treated as an adjustment on the payer’s tax return. Follow-

up question: What is the requirement for the receiver?

2. What does the IRS allow on Form 1040 to “soften” the impact of the self-employment tax calculated on Schedule SE?

3. (T/F) Most student loan interest is considered an adjustment for calculating AGI.

4. Martha is married but filing separately. Her husband has taken the standard deduction on his tax return. Martha has calculated a total of $17,500 in itemized deductions. What is the amount of deduction she can claim on her tax return?

5. (T/F) Medicare premiums are deductible regardless of whether a tax payer uses standard or itemized deductions.

6. (T/F) Either state income tax or state & local sales tax may be claimed as a deduction on Schedule A.

7. (T/F) TaxSlayer automatically calculates the standard deduction.

8. (T/F) A child must be under the age of 13 to be a qualifying child for the Child and Dependent Care Credit unless totally and permanently disabled.

9. (T/F) A child must be a dependent of the taxpayer to be a qualifying child for the Child and Dependent Care Credit.

10. (T/F) For the Child and Dependent Care Credit, on a joint return both taxpayers must be working, actively seeking a job or in school.

11. If a tax payer wishes to claim the Child and Dependent Care Expenses Credit, what information concerning the child care provider must be provided? (See Form 2441.)

12. (T/F) A qualifying child for the Child Tax Credit must be under the age of 17 at the end of the tax year.

13. Distinguish between “refundable” and “non-refundable” credits. Give an example of a “non-refundable” credit and the name of the most common and most beneficial “refundable” credit for lower income tax payers.

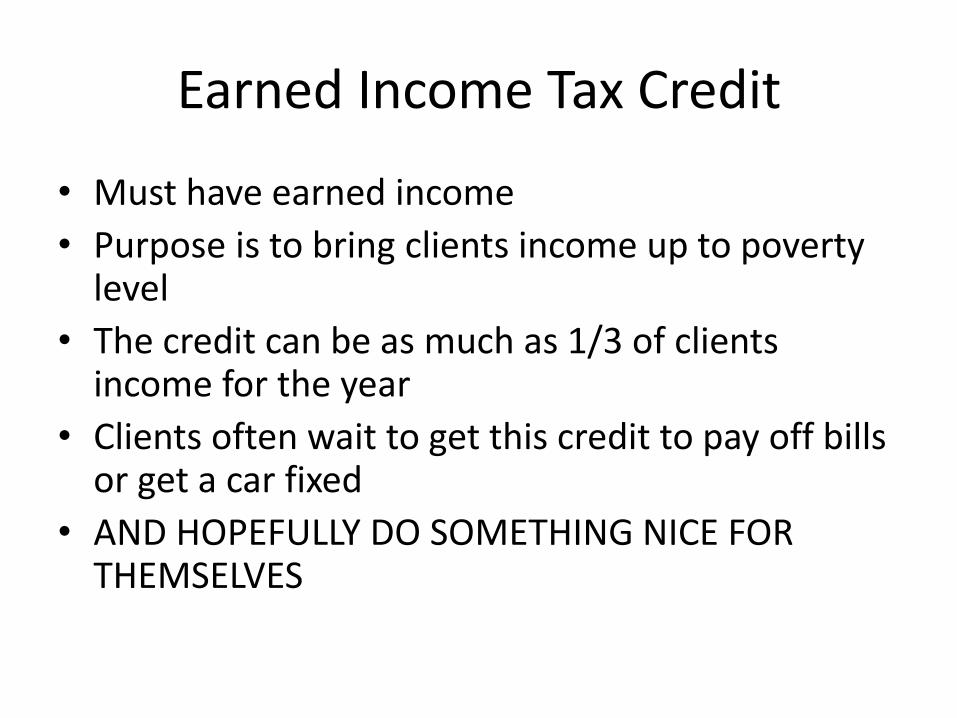

Earned Income Tax Credit

• Must have earned income

• Purpose is to bring clients income up to poverty level

• The credit can be as much as 1/3 of clients income for the year

• Clients often wait to get this credit to pay off bills or get a car fixed

• AND HOPEFULLY DO SOMETHING NICE FOR THEMSELVES

Earned Income Tax Credit-Rules

Earned Income Tax Credit-Limits

Maximum Credit Amounts The maximum amount of credit for Tax Year 2017 is: $6,318 with three or more qualifying children $5,616 with two qualifying children $3,400 with one qualifying child $510 with no qualifying children

EITC Review Questions

1. (T/F) taxpayer under age 25 with no qualifying children may still qualify for a small EITC.

2. (T/F) A taxpayer must have earned income to be eligible for EITC. 3. (T/F) Unemployment compensation is an example of earned income. 4. (T/F) A taxpayer with $4,000 interest on a savings account is NOT eligible for

EITC. 5. (T/F) Persons filing with the married filing separately status is eligible for EITC. 6. (T/F) A child must be the taxpayer’s dependent to be a qualifying child for EITC. 7. (T/F) A full time student age 25 would be a qualifying child for EITC. 8. (T/F) A qualifying child for EITC must have lived in the taxpayer’s home for more

than 6 months during the year, but temporary absences such as vacations and school are considered time living with the taxpayer.

9. (T/F) We must know if the taxpayer’s EITC was disallowed the previous year. 10. (T/F) When a child is claimed as a qualifying child for EIC by two tax payers, if one

is a parent, he/she is allowed to claim the child for the credit. 11. (T/F) If the parent has an ITIN, but the children have Social Security numbers,

EITC is allowed

Education Benefits

• Tuition and Fees Deduction

– Very RARE for CASH Clients

• American Opportunity Credit

• Life Time Learning Credit

• CANNOT CLAIM EDUCATION CREDIT IF FILING STATUS IS MARRIED FILING SEPARATELY

Education Credits

Determining Qualified Expenses

• Clients normally bring in form 1098-T

– Can be used to determine if

• student is more than ½ time

• not a graduate student

• CASH asks clients to get Student Account Record so Qualified expenses can be determined

• Screeners can sometimes determine if eligible for credit without Student Account Record

• Different expenses qualify for different credits

1098-T Example These numbers don’t tell “whole story”

Needs to be checked to eligible for American Opportunity Credit

If checked, Lifetime Learning Credit and NOT Eligible for NYS Tuition Credit

X

American Opportunity-what qualifies

What fees are required by college? What does student have to pay to take classes. Bought course related books from on-line bookseller for $500

Lifetime Learning – what qualifies

Not checked so eligible for Life Time Learning if meets other criteria

Still eligible for NYS Tuition if NOT graduate student even though not more that ½ time student

Lifetime Learning-what qualifies?

What if doesn’t have college record? What fees are required by college? What does student have to pay to take classes. Bought course related books from on-line bookseller for $500 What if employer reimburses for part of tuition?

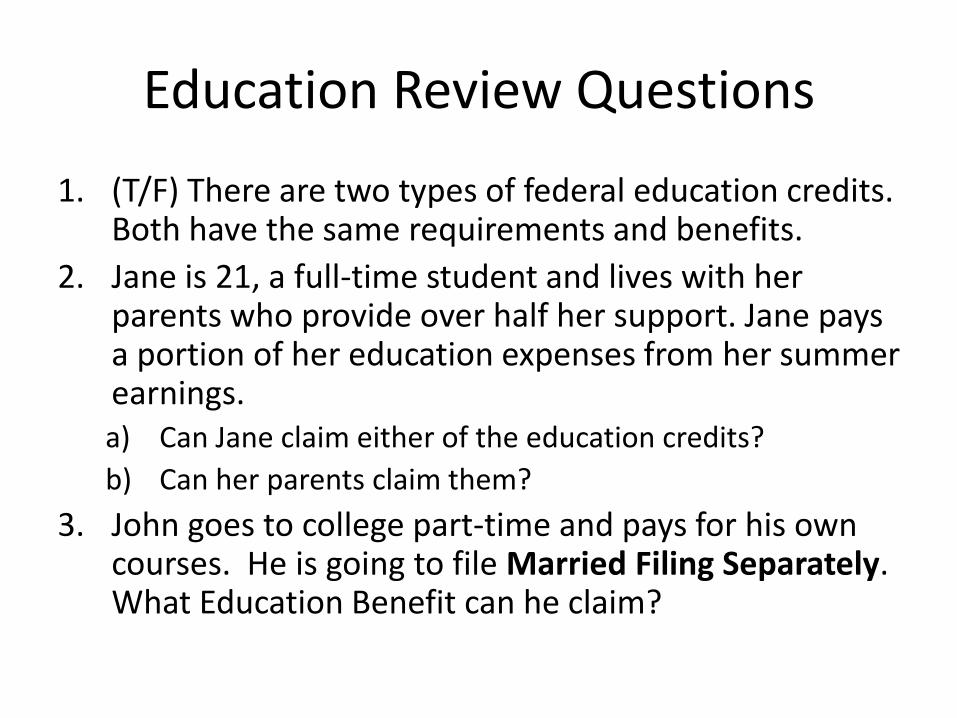

Education Review Questions

1. (T/F) There are two types of federal education credits. Both have the same requirements and benefits.

2. Jane is 21, a full-time student and lives with her parents who provide over half her support. Jane pays a portion of her education expenses from her summer earnings. a) Can Jane claim either of the education credits?

b) Can her parents claim them?

3. John goes to college part-time and pays for his own courses. He is going to file Married Filing Separately. What Education Benefit can he claim?

Affordable Care Act HEALTH CARE COVERAGE

Type Number Perc

Full Year Coverage 7184 89.23%

Shared Resp. Payment 309 3.84%

Exemption 538 6.68%

Prem Tax Credit 25 0.31%

Client completes, Reviewed by Screener/TP

Completed and reviewed by Screener /TP/QR

Most CASH clients had coverage all year

Minimum Essential Coverage - MEC • Employer-sponsored coverage:

– Group health insurance coverage for employees under— – COBRA coverage, – Retiree coverage, or

• Individual health coverage: – Health insurance purchased directly from an ins. company – Health insurance you purchase through the Marketplace – Health insurance provided through a student health plan – Catastrophic coverage

• Coverage under government-sponsored programs: – Medicare Part A coverage, – Medicare Advantage plans, – Most Medicaid coverage, – Children’s Health Insurance Program (CHIP) coverage, – Most types of TRICARE coverage, – Comprehensive health care programs offered by the Department of Veterans Affairs, – Refugee Medical Assistance, or – Coverage through a Basic Health Program (BHP) standard health plan.

Exemptions – most common

• Income below the filing threshold — – Gross income or your household income was less than

your applicable minimum threshold for filing a tax return.(automatically generated by TaxSlayer)

• Short coverage gap — – Went without coverage for less than 3 consecutive

months during the year. • There is a look-back rule for gaps of coverage at the start of

the year.

• Coverage Not Affordable – If you think this is the case-ask for help from Site Staff

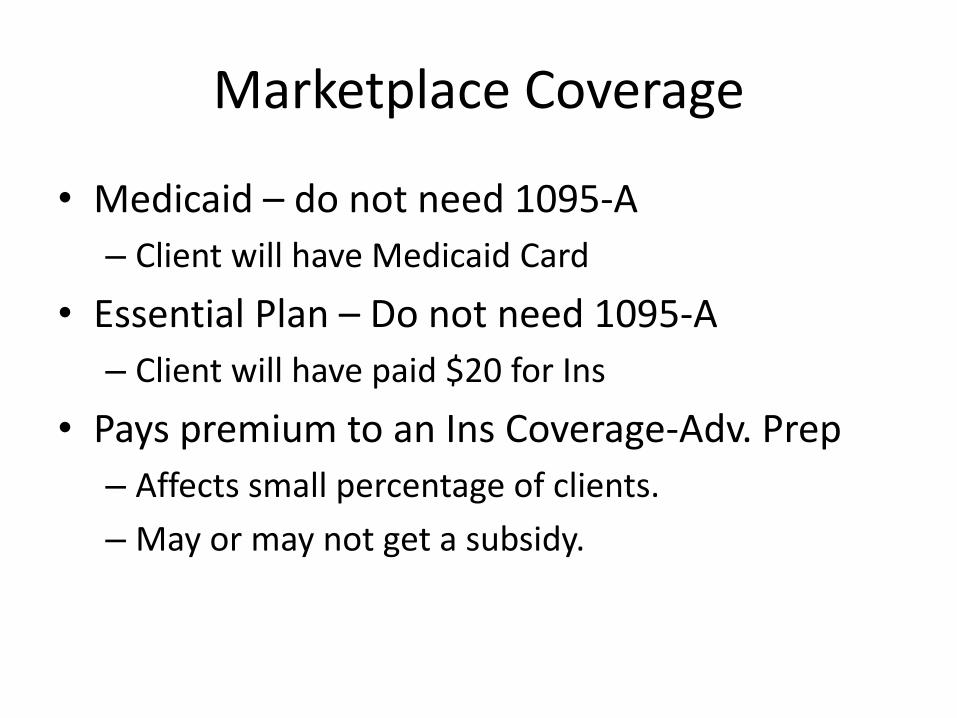

Marketplace Coverage

• Medicaid – do not need 1095-A

– Client will have Medicaid Card

• Essential Plan – Do not need 1095-A

– Client will have paid $20 for Ins

• Pays premium to an Ins Coverage-Adv. Prep

– Affects small percentage of clients.

– May or may not get a subsidy.

Eligibility for Premium Tax Credit

• To receive a premium tax credit, a person must: • Enroll in a Marketplace plan • Have income between 100 and 400 percent of the federal poverty line (FPL)

– Individual: $11,770 - $47,080 Family of four: $24,250 - $97,000

Exception for people with income below 100% FPL can claim PTC if they received APTC under the belief that they would be income-eligible for the credit. • Have an eligible filing status

– PTC cannot be claimed by a person who is Married Filing Separately

• *Exceptions for abused or abandoned spouses – PTC cannot be claimed on a dependent return (whoever claims an individual’s personal

exemption can claim their PTC)

• Not eligible for (or enrolled in) other minimum essential coverage (MEC) – Not eligible for Medicare or most Medicaid/CHIP or affordable employer- sponsored coverage

(regardless of whether the person is actually enrolled)

• *Many exceptions allow a person who received APTC to claim the credit despite eligibility for other coverage

Form 1095-A

This includes the

actual premium

paid plus the

APTC

This is the

benchmark plan

that helps establish

the PTC amount. . It

may be incorrect if:

(1) no APTC was paid, or

(2) a change in

circumstance was not

reported.

Advance payment of PTC

Use Annual Amounts ONLY if client had coverage all year for same amounts

ACA Review Questions 1. Joe is 20 and works to help put himself through college. He is totally supported

by his parents. They claim him as a dependent covered him on their Health Ins all 12 months.

a) Does Joe have Minimum Essential Coverage (MEC)? b) Who has to account for Joe’s health insurance coverage on their tax return?

2. Joe started his job June 1st and was not eligible for Ins. through his employer until Jan 1 of the next year. He was covered under Medicaid until May 31.

a) Can he go to the Marketplace to get insurance? b) What does Joe need to be careful about when getting insurance through the Marketplace? c) If Joe underestimates his income for the year will Joe have a “repayment?” d) If he overestimates his income, what happens on Joe’s tax return? e) What form will Joe need to show the tax preparer? f) Can Joe’s taxes be prepared without this form? Why or why not?

3. Hank has retiree health coverage from his old employer. His wife, Sara is in good health and has a dental policy only. Do both Hank and Sara have MEC?

4. Johnny was covered by Medicaid until February 23 of last year when he got a job. His employer-sponsored health coverage started after his probationary period ended on May 23

a) Does Johnny have full-year coverage? b) Will Johnny be liable for a shared responsibility payment?

1. If yes, for what months? 2. If no, why not?

First Time Home Buyers Credit

• If the taxpayer received the 2008 First Time Homebuyers Credit – Up to $7,500 loan that has to be paid back in 15 years – Form 5405 will be required to determine how much of

the credit must be repaid.

• Form 5405 – Part II if home has not been sold – This is the norm for CASH clients

• Have to know how much has been repaid. – Should be on client’s last year return. If not, client will

need to come back.

• If form not filled out,

Ready To Complete NYS Return

• CASH volunteers are ONLY certified to complete NYS returns. • Clients with out of state income are OUT OF SCOPE for CASH program

• Unless that State does not have Income Tax: Example – Florida • They will be given information on how to complete returns using Free Tax

Programs

Why CASH only does returns with NYS Income

• 4 Tax Situations that might be seen at CASH – Need only Federal Return – OK for CASH

• Income from a state that does not have Income tax – Examples: Alaska, Florida, Nevada, S. Dakota, Washington, Texas, Wyoming, New

Hampshire, Tennesee

– Part Year New York / Part Year other state – Not OK for CASH • Lived in NY, worked in NY, Lived in Other State, Worked in other State

– CASH will not start the return, even the Federal Return » To complete the “other state” the client will have to have the Fed and PY NY return

done again. » To correctly complete PY NY requires a different NYS Form and correct allocation of

income between the 2 state

– Live in NY, work in another state – Not OK for CASH • CASH will not complete the Fed return or resident NY return as there are

implications for Tax Credits from the state where work was done

– Work in NY, live in another state – Not OK for CASH • CASH will not complete the Fed or non-resident NY return due to tax credit

implications depending on State where client lived

Most information “flows” from Fed Input

NYS RETURNS

Name, Address, Filing Status, County and School District Dependent Information

Fed Income and Adjustments Flow to NYS

Make sure to verify information flowed correctly

NYS Additions to Fed Income

Drop down from Taxslayer W-2 Input

This should flow to NYS automatically if the input on the W-2 is correct. ALWAYS CHECK TO MAKE SURE

NYS Subtractions to Fed Income

Taxable Refunds (Line 25) Taxable Amount of Social Security(Line 27) Are AUTOMATICALLY SUBTRACTED

Pensions of NYS and Local Governments (Line 26) Pension and Annuity Income Exclusion (Line 29) HAVE TO BE MANUALLY INPUT

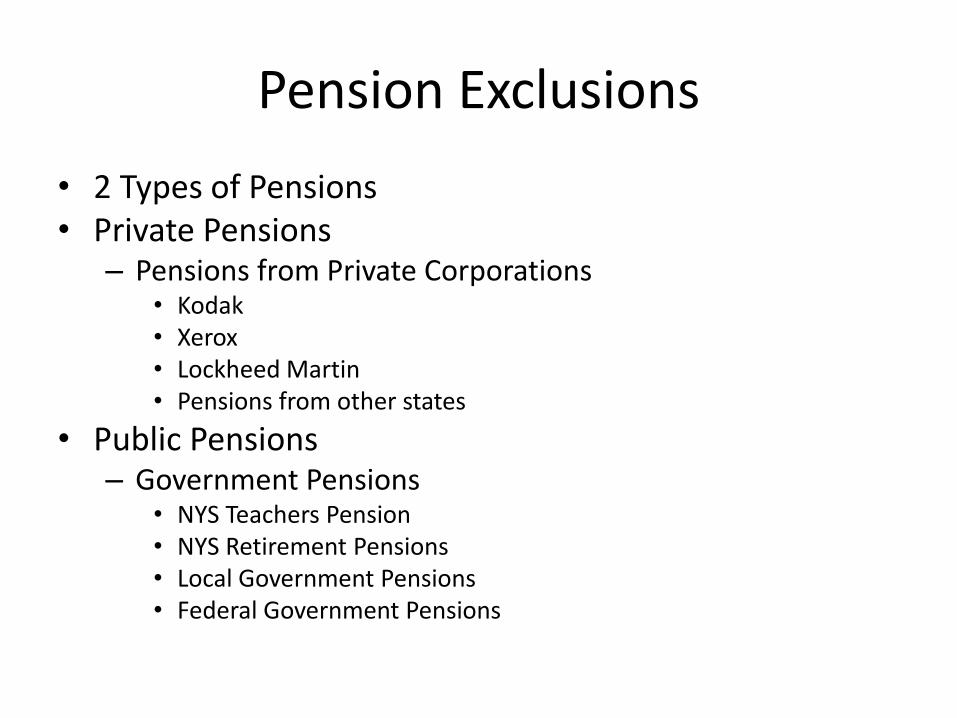

Pension Exclusions

• 2 Types of Pensions • Private Pensions

– Pensions from Private Corporations • Kodak • Xerox • Lockheed Martin • Pensions from other states

• Public Pensions – Government Pensions

• NYS Teachers Pension • NYS Retirement Pensions • Local Government Pensions • Federal Government Pensions

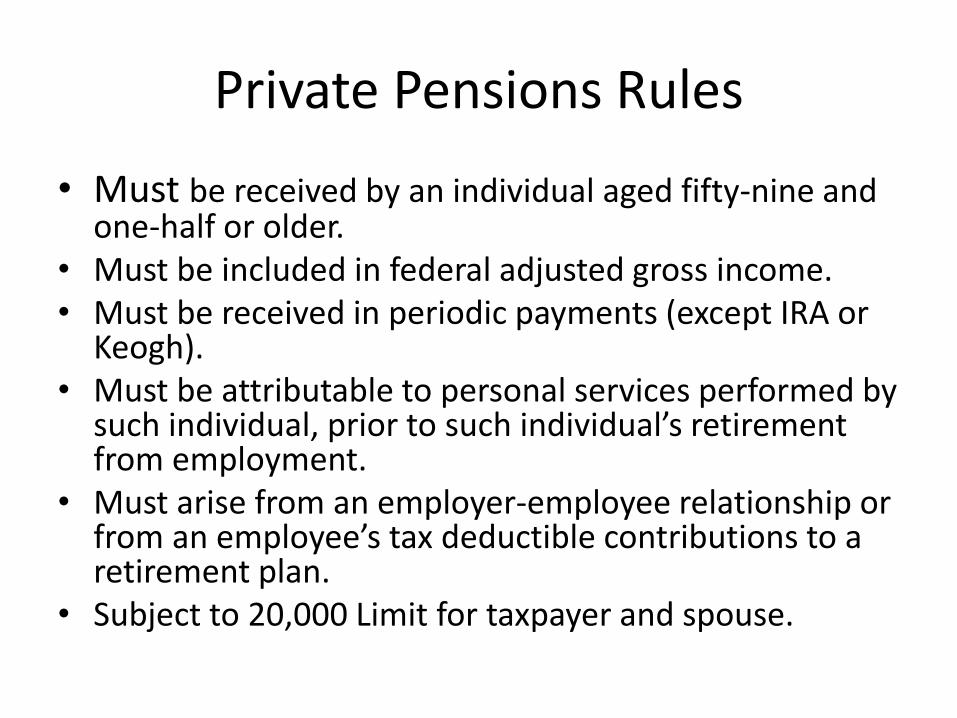

Private Pensions Rules

• Must be received by an individual aged fifty-nine and one-half or older.

• Must be included in federal adjusted gross income. • Must be received in periodic payments (except IRA or

Keogh). • Must be attributable to personal services performed by

such individual, prior to such individual’s retirement from employment.

• Must arise from an employer-employee relationship or from an employee’s tax deductible contributions to a retirement plan.

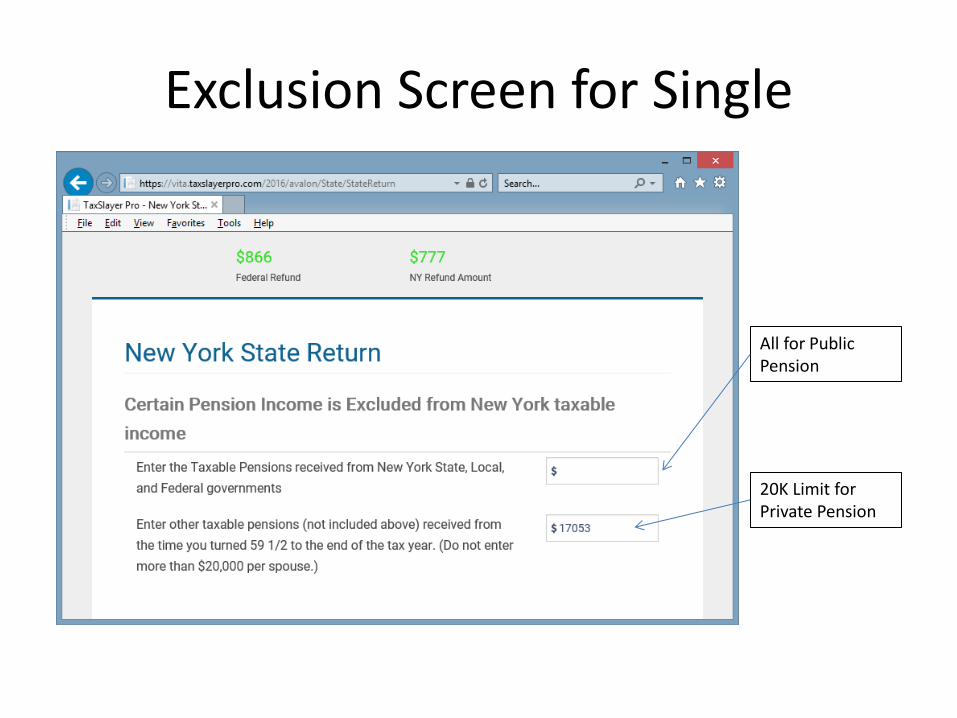

• Subject to 20,000 Limit for taxpayer and spouse.

Public Pensions Rules

• Pension income is not taxable in New York if it is paid by:

– New York State or local government

– Federal government, including Social Security benefits and certain railroad retirement benefits

Exclusion Screen for Single

All for Public Pension

20K Limit for Private Pension

Exclusion Screen for MFJ

All for Public Pension for each spouse

20K Limit per person: If one spouse has 22 K and the other spouse has 18K Exemptions would be 20,000 and 18,000

NYS CREDITS All NYS Credits are refundable so even if not eligible for Fed Credit, make sure to input information to get NYS credit

Credits that will be generated from Fed Input Empire Child Credit Child and Dependent Care Credit NYS Earned Income Credit

UNIQUE NYS CREDITS

• DO NOT Flow from Fed Return so are “Most Missed” Items when QR is done.

– IT-214 – Real Estate (Renters) Credit

– IT-209 – Non-Custodial Parent EIC

– IT-272 – NYS Tuition Credit

– IT-245 – Vol Fire/EMS Credit

IT-214 – Real Property Tax Credit • Conditions to claim Real Property Tax Credit

– Your household gross income was $18,000 or less.

• Includes Taxable Income

– Flows from Fed Return

• Non-taxable income

– SSI, non-taxable Social Security

– You occupied the same New York residence for six months or more.

– You were a New York State resident for all of 2016.

– You could not be claimed as a dependent on another taxpayer’s federal income tax return.

– Your residence was not completely exempted from real property taxes.

• Homeowners

– The current market value of all real property you owned was $85,000 or less.

– You or your spouse paid real property taxes.

– Any rent you received for nonresidential use of your residence was 20% or less of the total rent you received.

• Renters

– You or a member of your household paid rent for your residence.

– The average monthly rent you and other members of your household paid was $450 or less, not counting charges for heat, gas, electricity, furnishings, or board.

IT-209 – Non-Custodial Parent EIC

• Claim the noncustodial EIC only if you meet all of the following conditions for the tax year. – be a full-year New York State resident, – be at least 18 years of age, – be a parent of a minor child (or children) with whom you do not

reside, – have an order in effect for at least one-half of the tax year

requiring you to make child support payments payable through a New York State Support Collection Unit (SCU)

– have paid an amount in child support at least equal to the amount of current child support you were required to pay by all court orders.

• Have Birthdate and SS Number of Qualifying Child • Credit is usually 20% of Federal EIC

IT-272 – NYS Tuition Credit

• If Fed return has Education Credits, make sure to review if client is eligible for NYS Tuition Credit

• To qualify for the college tuition credit or itemized deduction, – Tax Payer/ spouse, or dependent(s) must be an

undergraduate student enrolled at or attending an institution of higher education and have

– paid qualified college tuition expenses

• Only expenses for undergraduate enrollment or attendance qualify.

IT-245 – Vol Fire/EMS Credit

• Credit is seen very rarely – for awareness only

• The volunteer firefighters’ and ambulance workers’ credit is available to full-year New York State residents who are active volunteer firefighters or volunteer ambulance workers for the entire tax year for which the credit is claimed.

• The Credit cannot be claimed if the Taxpayer received a real property tax exemption that relates to your volunteer service.

NYS Review Questions

1. (T/F) A taxpayer must identify the school district in which he/she resides.

2. (T/F) Only homeowners are entitled to the NYS IT-214 credit. 3. (T/F) NYS personal exemptions are the same as IRS code. 4. (T/F) NYS Child and Dependent Care (form IT 216) is a refundable

credit. 5. (T/F) IT-214 filers must have total household income $18,000 or

less. Social Security, SSI, and child support must be included in that amount.

6. (T/F) NYS College Tuition Credit is refundable and available only for undergraduate study.

7. Which credits are available to people with no taxable income? How can you e-file for them?

Tax Preparer Process

• Look at process for preparing a return

Steps To Complete Tax Return • Go to Front Desk and get the next return that is ready to

be prepared that is within your certification.

• Call client from Front Desk Area.

• Greet client and take them back to your desk

Be sure and look at all circled items. Must have HSA certification to do HSA.

This would signify that client is here only for renters credit BUT always double check documents to verify

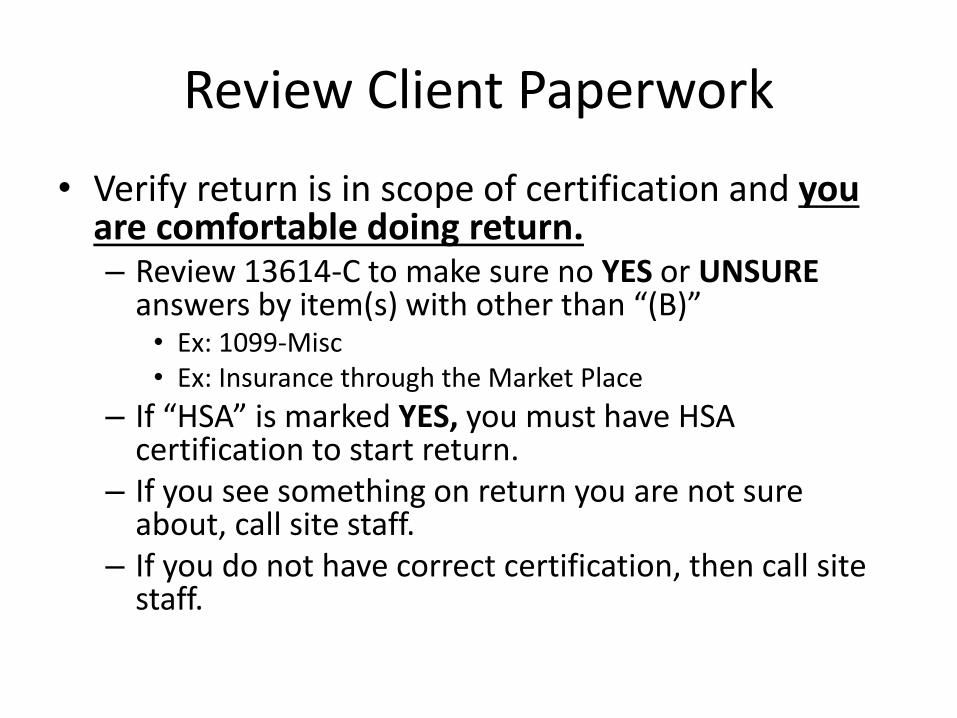

Review Client Paperwork

• Verify return is in scope of certification and you are comfortable doing return. – Review 13614-C to make sure no YES or UNSURE

answers by item(s) with other than “(B)” • Ex: 1099-Misc • Ex: Insurance through the Market Place

– If “HSA” is marked YES, you must have HSA certification to start return.

– If you see something on return you are not sure about, call site staff.

– If you do not have correct certification, then call site staff.

Before Entering Information

• Use IRS and CASH intake sheets and client information to:

– Verify ID and Social Security numbers for everyone on return

– Determine filing status

– Verify dependent information –

• make sure to complete the shaded area on the intake sheet

– Review income documents with client and verify information is complete

– Review expenses, adjustments

• Pay special attention to Education expenses – must have student account record

– Review Health Insurance Information

• Make sure to complete shaded area on the intake sheet

– Review information on CASH Intake sheet

– Direct Deposit information

• Should have blank check or bank document to verify

– If any information missing, call site staff and DO NOT start return.

Start Tax Return in TaxSlayer

– Organize all paperwork by IRS intake sheet sections – Input all information according to topics on menu bar

using • Social Security Number • Basic Information

– Taxpayer information

• Dependent Information

– Using “Enter Myself” option • Income always first • Adjustments are under “Deductions” menu • Credits are under “Deductions” menu • Identity Theft Pin is under “Misc. Forms” menu

– Make sure to enter Health Insurance information from “tree” on left side.

Finishing the Return

• Now that all the input is done, next step is to “Finish the Return”

Finishing the Return

• When Fed and State input is complete • Review input one last time to double check input • Continue to E-File Section – 7 Sections

– Return Type – Tax Preparation and E-File Information – State Return(s) – Taxpayer Bank Account Information – Third Party Designee Info – Questions – State ID (Optional)

Return Type- Fed Refund

Check if NOT filing Fed Return

Check based on Client Input ALWAYS encourage Direct Deposit

Refund - State

Banking Information

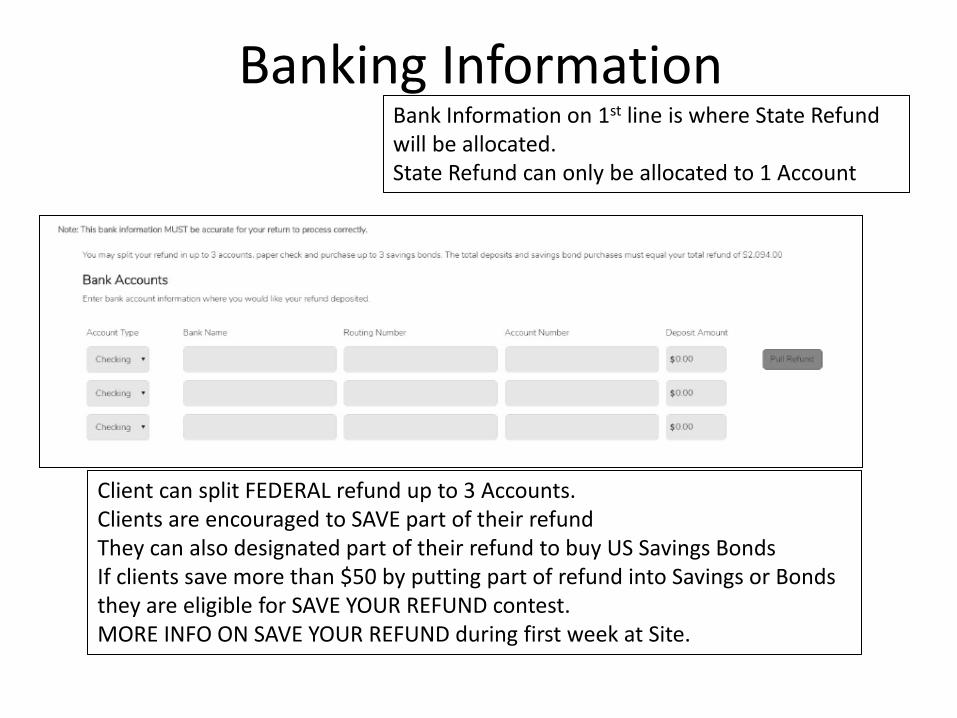

Client can split FEDERAL refund up to 3 Accounts. Clients are encouraged to SAVE part of their refund They can also designated part of their refund to buy US Savings Bonds If clients save more than $50 by putting part of refund into Savings or Bonds they are eligible for SAVE YOUR REFUND contest. MORE INFO ON SAVE YOUR REFUND during first week at Site.

Bank Information on 1st line is where State Refund will be allocated. State Refund can only be allocated to 1 Account

Third Party Designee Info

This section is not completed at CASH Vita Sites

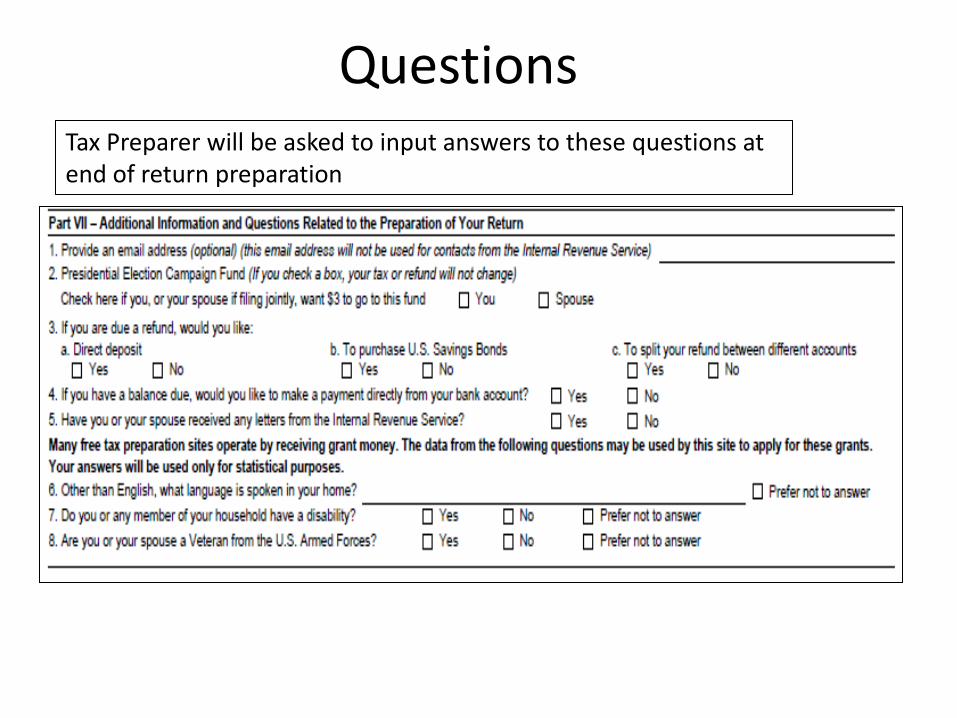

Questions Tax Preparer will be asked to input answers to these questions at end of return preparation

State ID

This information is normally taken of NYS drivers License

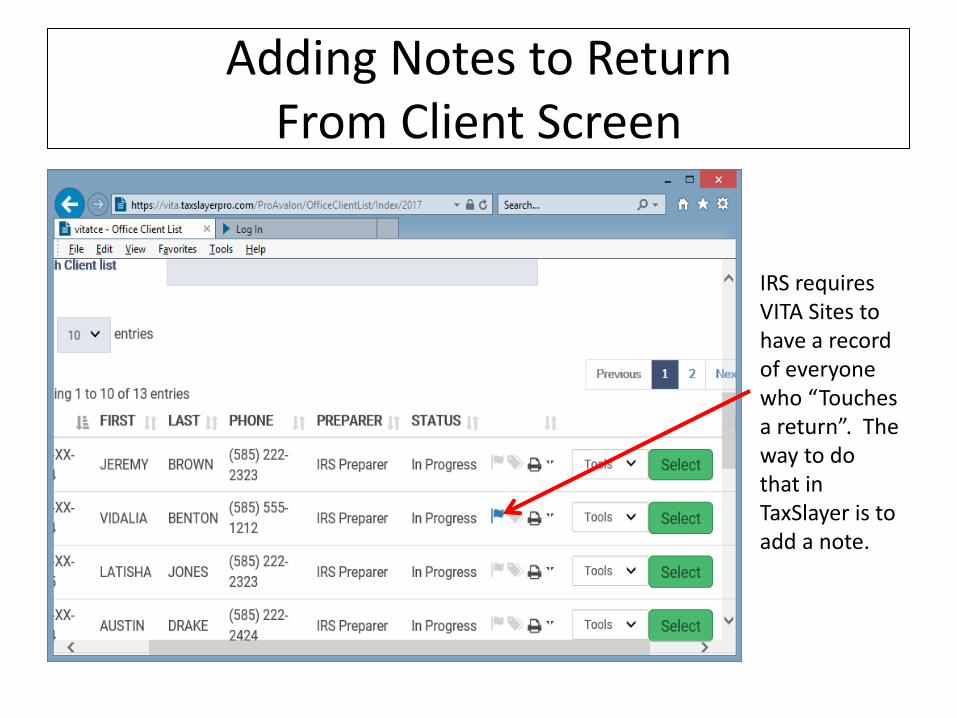

Adding Notes to Return From Client Screen

IRS requires VITA Sites to have a record of everyone who “Touches a return”. The way to do that in TaxSlayer is to add a note.

Adding notes to return From inside return

Click on client name at top. Pick Notes

Add initials for Screened, TP and place for QR when complete

Return Notes – what next

• If the return has to be opened to – To add banking information

– To mark complete after drop-off pick-up

– To correct the return, such as after a reject

– For any other reason

• Make sure to update the Notes section by adding a new note so the “trail” of what was done to a return can be followed.

• This is important to answer client questions after return has been accepted.

Quality Review

• Call Quality Review

– When Fed and State Return are complete

– When all the questions on Finishing return are done

– When State ID has been input

– When QR Cover sheet has been filled out

QR Process Make sure Information is on cover sheet

LEGIBLE HANDWRITING IS APPRECIATED

To help us learn more about how our clients save, record this information about refunds

QR Process

• Quality Review Staff or Volunteer will review return • Will once again review IRS and CASH Intake Sheets • Will verify Spelling of names, SS numbers, Birthdates • Will verify all input into return

– Verify refund/balance due – Will re-check bank information

• Will review for missed items – If Pension, was exclusion correctly subtracted – If college student was IT-272 correctly filled out – If eligible for Real Property Credit was IT-214 filled out

• When complete, Quality Review will set return for e-file and print return

Reviewing return with client

• AFTER return passes Quality Review and it is printed

• Tax Preparer reviews return with client verifying one more time

– Spelling of names, SS #’s, Birthdates

• Explain what makes up refunds

– Credits, etc

• Explain why Balance Due

LAST STEP

• After client indicates understanding of return they sign IRS and NYS E-file forms

IRS E-File Form 8879

Signing this form is the same as signing the 1040 Form. The client is signing that the information they have provided is “TRUE, CORRECT, and COMPLETE. MAKE SURE THEY UNDERSTAND THAT WHEN SIGNING

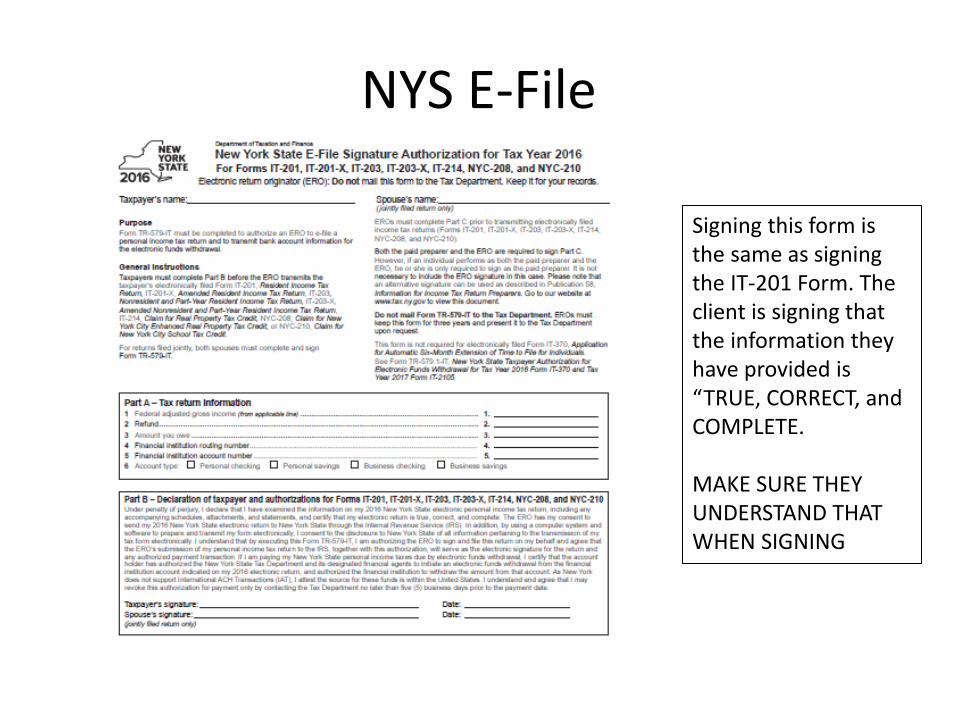

NYS E-File

Signing this form is the same as signing the IT-201 Form. The client is signing that the information they have provided is “TRUE, CORRECT, and COMPLETE. MAKE SURE THEY UNDERSTAND THAT WHEN SIGNING

Return is complete

• Give client copy of return

– How to put return together will be reviewed at Site

– To Keep in CASH envelope

• One Copy of Income Documents

• IRS Intake Sheet

• CASH Intake Sheet

• Any other information deemed pertinent

– File envelopes ready for Transmit in designated area

– If Return CANNOT be completed, contact QR Staff or Volunteer for direction what to do.

Return Finished !!

Take a break Get a Snack

Go to Control Desk Area when ready to start a new return

When to call Site Staff

• MFJ When Spouse Owes To IRS/State – Fed – Injured Spouse

– State – Non-Obligated Spouse

• When someone does not have full year health coverage and you are not sure about exemption.

• When you see a form you don’t recognize

• When return is a paper return

• When you have any other questions

Questions?

Next Steps

A look at TaxSlayer Practice Lab IRS Test

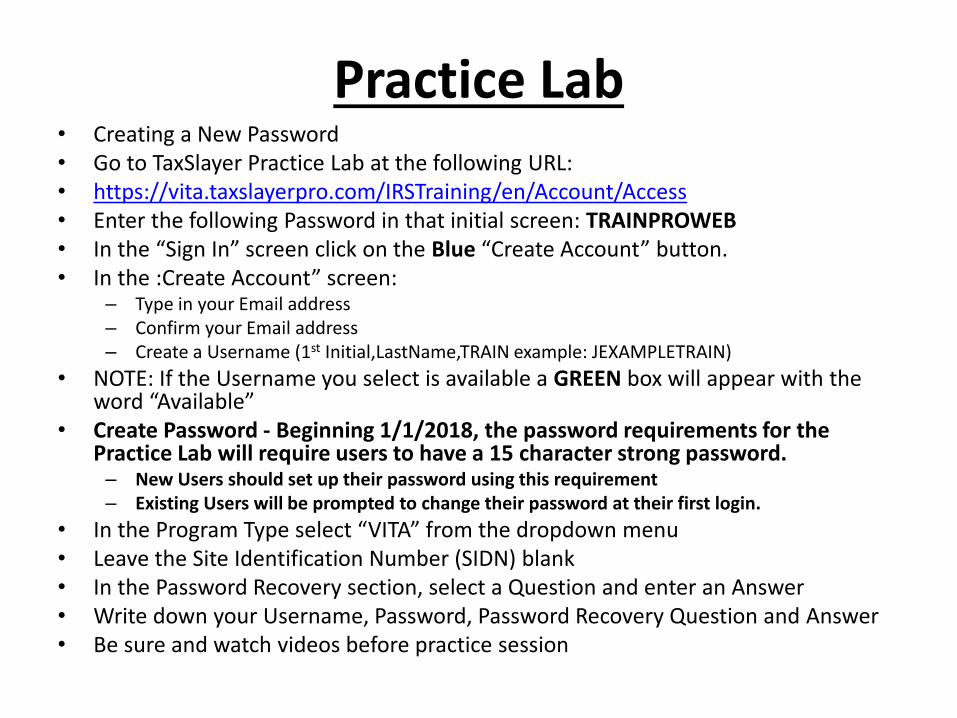

Practice Lab • Creating a New Password • Go to TaxSlayer Practice Lab at the following URL: • https://vita.taxslayerpro.com/IRSTraining/en/Account/Access • Enter the following Password in that initial screen: TRAINPROWEB • In the “Sign In” screen click on the Blue “Create Account” button. • In the :Create Account” screen:

– Type in your Email address – Confirm your Email address – Create a Username (1st Initial,LastName,TRAIN example: JEXAMPLETRAIN)

• NOTE: If the Username you select is available a GREEN box will appear with the word “Available”

• Create Password - Beginning 1/1/2018, the password requirements for the Practice Lab will require users to have a 15 character strong password. – New Users should set up their password using this requirement – Existing Users will be prompted to change their password at their first login.

• In the Program Type select “VITA” from the dropdown menu • Leave the Site Identification Number (SIDN) blank • In the Password Recovery section, select a Question and enter an Answer • Write down your Username, Password, Password Recovery Question and Answer • Be sure and watch videos before practice session

VOLUNTEER WEBSITES

• C.A.S.H. Training Page – digital training materials and training schedules – Includes Instructions on how to recover a password

– http://www.empirejustice.org/cash/cash-training-center

• Volunteer Hub – Sign-up for training/volunteer shifts – http://cash.volunteerhub.com/ (UNDER CONSTRUCTION)

– More information will be coming in early January

• TaxSlayer Practice Lab – site to do watch instruction videos, complete practice returns and returns for test. – https://vita.taxslayerpro.com/IRSTraining/

• IRS Test Site – site to put in test answers – www.linklearncertification.com/d/

The Test

• Test is in Pub 6744 – 3 parts to test for Tax Preparers

• Volunteer Standards Of Conduct

• Intake/Interview

• Certification Test

• Answer questions in test book for both – TEST And Retest

• Input Answers on IRS Certification Web Site – https://www.linklearncertification.com/d/

• Hints for Test on last page of Agenda