Embed Size (px)

Citation preview

Industrial Logistic systems

RETAILERS - DRIVING VALUE FROM

THE SUPPLY CHAIN

Where are we and where are we heading?

Gary Benatar

Managing Director

Barclays Select Series 2015: Consumer Conference

Retailing

• Last stage in a channel of distribution from producer to

consumer

• Derived from the French word “retailler”, which means

“to cut up”.

Retailing is “exposing product to the sin of a customer purchase”

THE END RESULT

The Customer

Customer Focus

• Measuring REAL customer satisfaction

– Availability

– Range

– Price

Customer Focus - Availability

• Traditional methods

– DC or vendor to store service level: 98%

– Store out of stock ‘walks’: 97%

– Systemised lost sales calculation: 96.5%

• New Methods

– Online shop: 92%

– ‘Could you buy everything you wanted?’: 75%

Customer Focus - Range

• Old Method

– Store Size

– Managers Discretion

• New Method

– Store Size & Location

– Loyalty Card Data

– Customer Insight

Aligning suppliers to the customer

• Centralisation has meant that suppliers have been

disconnected from the consumer

Putting the customer at the centre of

everything

• For the supplier, need to align – Production, Purchasing, Replenishment, Sales

• For the retailer, need to align – Buying, Supply Chain, Store operations

• Traditional KPI’s can no longer be viewed in isolation e.g. – Production efficiency

– Transportation efficiency

– Sales

CONSUMER

• Consumerism

• Life-Style

• Urbanisation

• Age

• Mobility

Consumer

• Buy Local

• Life Style

• Working Woman

• Single

• Ageing Population

• Young

Consumer

More demanding

• FRESH

• HEALTH

• HYGIENE

• GREEN

Rights

• Right to safety

• Right to be informed

• Right to choose

• Right to be heard

• Right to redress

• Right to service

REAL NEEDS More demanding customers More educated and informed customers Higher expectations Ability to instantly price check More choices Other retail channels (e-Commerce) Move to convenience shopping More proliferation New product profile (e.g. cell) Pressure on margins Faster reaction – changes and expectations Better quality More fashion – less basics

Change

• Traditional focus of savings in Supply chain

• Supplier – DC – to Store – Technology

– Labour

– Transport

• Not customer focussed

• Don’t help with availability in store

Key focus should be to get product to customer

• We look at how we can improve on shelf availability and

service to the customer by being clever at the DC and supply end of the supply chain

• Differentiating the retailer from supplier to shelf

Retailer Focus

1. Margin

2. Buying power

3. Range control

4. Availability

5. Cost control

6. Find and eliminate

hidden inefficiencies

7. Store formats

8. Multiskilling

9. Entertainment

10. Consumer value

11. Market saturation and

stagnation

12. Competition

Supermarket Perspective

Ingredients Packaged Goods

FOOD Long Life Fresh (Food types)

(Food forms) Ambient Multiple Temp.

(Temperatures)

Health and Beauty Specialist Packaged

Regulated De-Regulated (Health Care)

Fashion Basic

Variety and

High quality DIY Finished Goods Materials

Specialist Comprehensive Services

Activity and Cost Drivers

1. Consumer

2. Product Supply

3. Technology

4. Regulations

5. Competition / Internationalisation

6. Promotions

7. Others

Technology

Computing

• Information

• More market research

• Collaboration

• Ownership of stock

• Service levels

• Traceability

• Simplification

• Click and Mortar

GM Food

• Wider range

• Confusion

Environmental

• Waste control

• Recycle

• GREEN

Supplier Relationships

• Who owns the customer ?

• Collaboration

• Co-ordinated promotions

• Retailer brand dominant

• Contractual relationships

Service level agreements

LOGISTICS CHALLENGES

Complex

Environments

Risk and Security

SKU Explosion

Quality

Emphasis

Green Issues

Energy Issues

Strategic Alliances

Outsourcing Selective

Automation

Technology

New Technologies

(ERP, WMS, LES,

RFID, voice)

Global

Competition

Global standards

Shrinking Labour Supply

Productivity

Quality

Flow Thru strategies

Lean Distribution

Cross Dock

People Management Innovation

Labour Relations

Logistics

Regulatory Issues

(EU, HAZMAT, HACCP)

INNOVATION IN DC DESIGN, LOGISTICS AND SUPPLY CHAIN

STRATEGIES –

RESULTING IN GREATER IN-STORE EFFICIENCY AND COST

SAVINGS

BETTER SERVICE TO CUSTOMERS

RETAIL IS PROBABLY THE MOST DIFFICULT

SUPPLY CHAIN AND LOGISTICS PROCESS:

– Low margin business – inefficiency evident on bottom line

and price to customer

– Highly competitive

– Frequency of demand and replenishment

– Total variability – customer demand is unpredictable –

difficult to plan

– Seasonality - peak to average (especially in southern

hemisphere – Christmas, summer holiday, back to

school & end of yr bonus)

– Promotions

History direct store delivery by suppliers vs centralisation

SUPPLY CHAINS CAN’T

RUN IN SILOS

To effectively manage supply chain:

– Service levels or availability

– Quality

– Cost

SUPPLY CHAIN OF FUTURE

• Efficiency

• Speed

• Responsiveness

• Cost effective

• Quality operations

• Customer service

Does not change!!!! • More focussed

• More visible

• More measured

THE MEANS – LEAN THINKING

Adding Value Reducing Waste Managing Change

TYPICAL COSTS THROUGH

THE SUPPLY CHAIN

MANUFACTURE DISTRIBUTION RETAILER CUSTOMER

PROCESS

RAW

MATERIALS

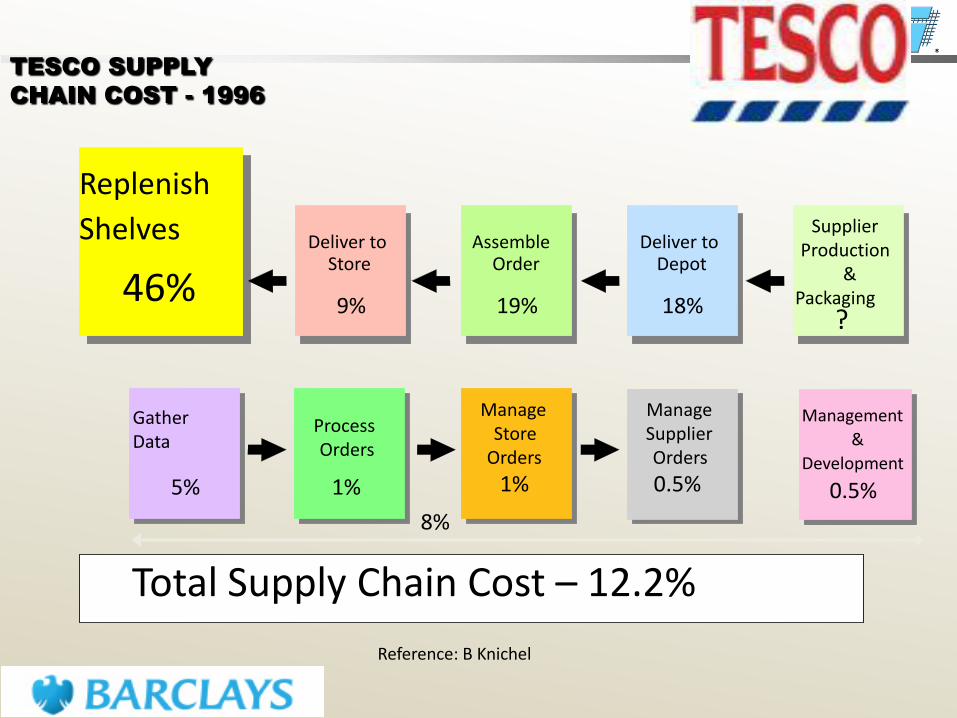

Total Supply Chain Cost – 12.2%

TESCO SUPPLY

CHAIN COST - 1996

Deliver to Store

Assemble Order

Supplier Production

& Packaging

?

Process Orders

Deliver to Depot 46%

Replenish

Shelves

Management

&

Development

Gather Data

Manage Store

Orders

Manage Supplier Orders

9% 19% 18%

5%

1%

1%

0.5%

0.5%

8%

Reference: B Knichel

Merchandise Units (MU’s) –Fast movers:

• Flow through at DC • Direct to shelf presented to customer as is • No pallets allowed in stores

Background To On Shelf Availability

• The success of the supply chain

is seen at the shelf. The interface

to the customer:

– Product availability

– Range

– Quality

– Cost of supply chain

• On Shelf Availability

– 1% out of stock = 4% lost sales (international studies)

– 33% chance of lost customer for an

out of stock (international studies)

Reducing Waste

• Errors

• Overproduction

• Waiting for People, Equipment or Materials

• Unnecessary Transport of goods

• Unnecessary movement of people

• Excess stock

• Poor process design

• Inappropriate Range

EVERYONE’S TALKING ABOUT GREEN

BUILDING

Less water

Smaller carbon footprints

More sunlight

Less waste

Less electricity

Environmentally friendly materials

What about inside the building?

• Current thinking and research into environmentally friendly and green buildings focuses on the building shell

• Warehouses and Distribution Centres – normal to design for:

– Functional / Operational life – 5 to 10 years

– Infrastructure life – 10 to 20 years

• A once-off benefit in the building process

• The inside of the building – the operational and systems processes present a number of possibilities to be greener and more sustainable

THIS STILL DOESN’T MAKE GREEN BUILDING A BAD IDEA

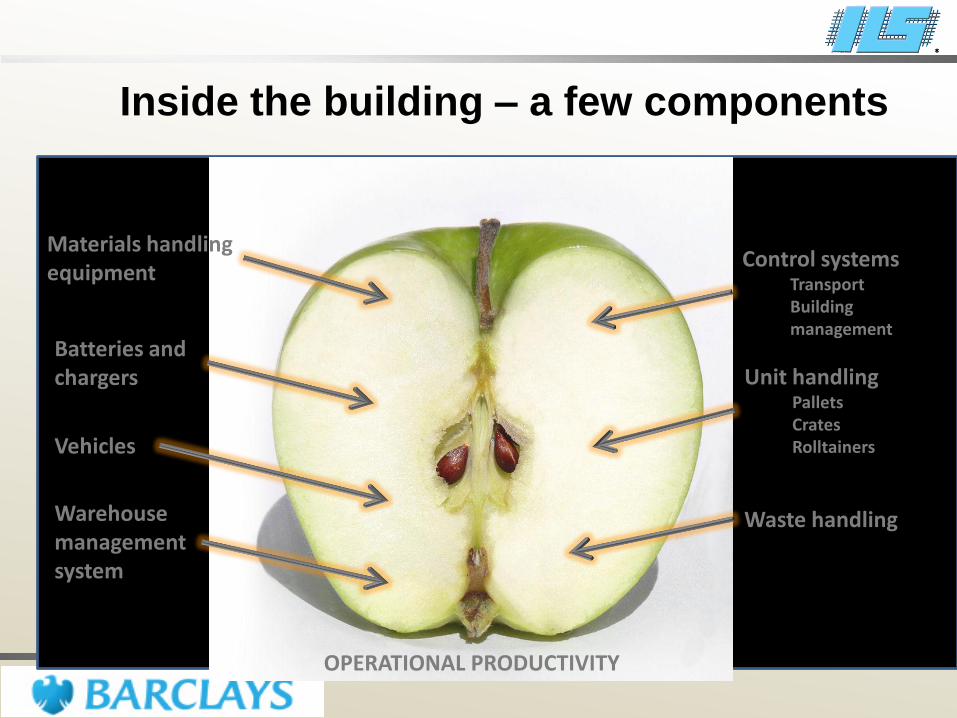

Inside the building – a few components

Materials handling equipment

Batteries and chargers

Vehicles

Control systems Transport Building management

Unit handling Pallets Crates Rolltainers

Warehouse management system

Waste handling

OPERATIONAL PRODUCTIVITY

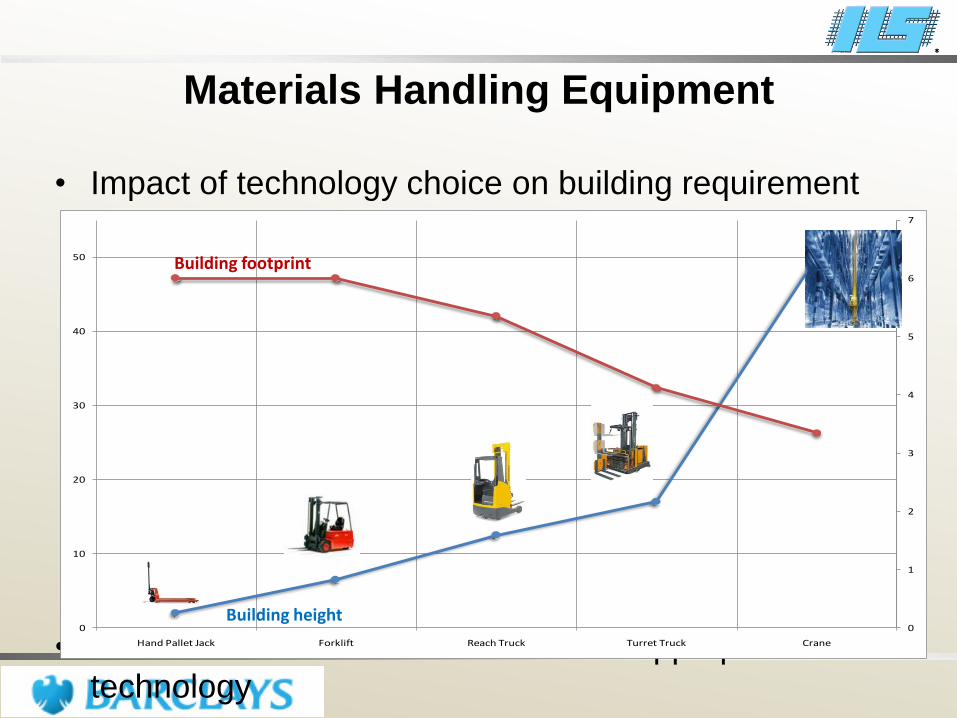

• Impact of technology choice on building requirement

• Choice is based on APPLICATION – appropriate

technology

0

1

2

3

4

5

6

7

0

10

20

30

40

50

Hand Pallet Jack Forklift Reach Truck Turret Truck Crane

Materials Handling Equipment

Building footprint

Building height

Batteries and Chargers

• Number of choices available for batteries and chargers

• Batteries

– Conventional flooded

– Low water use

– Sealed batteries

• Chargers

– Thyristor

– High Frequency

– High speed

Batteries and Chargers

• Battery management systems

– Battery rotation

– Fault finding

– Longer life

– Overall smaller fleet needed

– Controlled power use – peak demand

• Random rotation of batteries can achieve between 10

and 30% energy saving

Warehouse management systems

• The common beliefs...

– An ERP is a WMS

– An inventory management system can be a WMS

– A WMS is expensive and costly to maintain

• These beliefs remove all the functionality of a WMS that

directly improves productivity and therefore is more green

– RF technology – picking, putaway, replenishment (real-

time)

– Labour management

– Interleaving, etc., etc., etc.

Warehouse management systems

• A few examples of WMS functionality that drives

productivity up, throughput up and costs down

• Product slotting

– Logically layout of products in facility to maximise pick

productivity

– Pickers not driving all around the facility – shortest routes

Warehouse management systems

• A few examples of WMS functionality that drives

productivity up, throughput up and costs down

• Interleaving

– Reach Trucks operating put-away and let-downs

simultaneously

– 50% increase in Reach Truck productivity

• Voice picking

– Paperless picking

• RF loading

– Paperless invoicing and dispatching

Optimising supply chain processes

• HOW DC process can influence store

– Delivering store friendly replenishment

• Warehouse is laid out in same sequence as store

• Cage/Pallet is picked in reverse sequence to how

shelves will be filled

• Like products are all delivered together

• Minimises travel time on shop floor for both people and

product

What to measure?

• Service to customer

• Cost

• Service from supplier

• Quality, integrity

• Value

• Sustainability

How do you measure?

• Total supply chain

• Components of the chain

• Benchmark

• Balanced scorecard

• Cost / efficiency

• Ability to support business

Example – Cellphone company VS Retailer

Update on retail challenges

• Trends and benchmarks

• Local challenges

• Local status, trends and challenges

– Centralisation

– Last 50 m

– International players - Globalisation

– Consumer Protection

– Carbon Footprint – sustainability

– Transport, congestion and legislation

– Fuel costs

Social networks and new media challenges

• Who uses MSN or Instant messenger for

communication

• Who uses Skype, Viber

• VOIP

• Who is on

– My Space

– MXIT

– Mig33?

WHAT DOES THIS MEAN?

• The rules are changing

• The way people communicate

CHANGES EXPECTAIONS

– Speed

– Response

– Instant expectation

• Customers are different

• Deal in different ways

• Can we communicate?

THE END

Real Customer Focus begins at the top. It can only happen with visible, passionate, relentless, commitment by all

IS THIS THE END

OR THE BEGINNING OF THE

END

"Only when the last tree is cut

only when the last river is polluted

only when the last fish is caught

only then, will they realize that you cannot

eat money”

Cree-Indian, Proverb

![China Syndrome: Supply crisis for Aussie retailers/media/Ferrier/Files/Documents... · China Syndrome: Supply crisis for Aussie retailers Perlstein said. “[It is] the inflationary](https://img.dokumen.tips/doc/110x75/5aaccfdf7f8b9aa9488d7862/china-syndrome-supply-crisis-for-aussie-retailers-mediaferrierfilesdocumentschina.jpg)