Embed Size (px)

Citation preview

Retailer Panel: The Cost of Growing Your BusinessModerator: Henry Armour, Ph. D., President and CEO | NACSPanelists:Ari Haseotes, CEO | Cumberland FarmsGlenn Plumby, Senior Vice President and COO | Speedway SuperAmerica LLCSonja Hubbard, Principal | Yates Group; former CEO | E-Z MART, Inc.

Corporate Overview

Introduction to Cumberland Farms

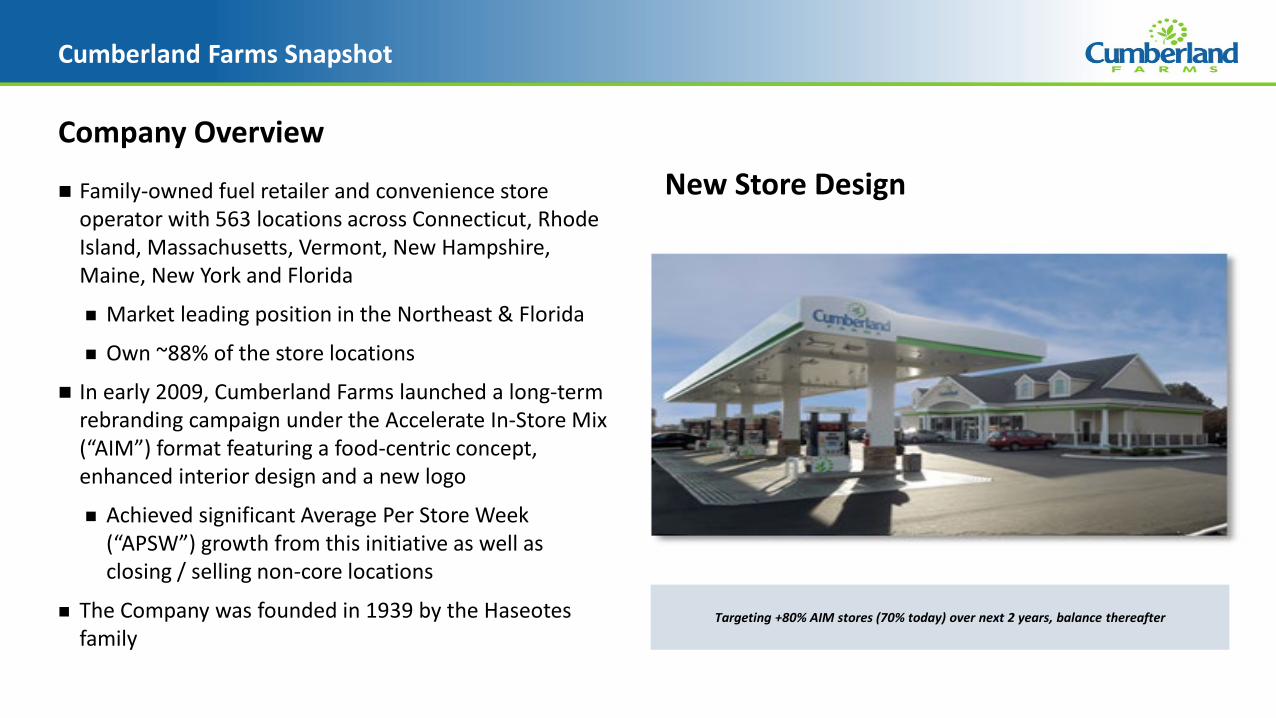

Cumberland Farms Snapshot

Company Overview

Family-owned fuel retailer and convenience store operator with 563 locations across Connecticut, Rhode Island, Massachusetts, Vermont, New Hampshire, Maine, New York and Florida

Market leading position in the Northeast & Florida

Own ~88% of the store locations

In early 2009, Cumberland Farms launched a long-term rebranding campaign under the Accelerate In-Store Mix (“AIM”) format featuring a food-centric concept, enhanced interior design and a new logo

Achieved significant Average Per Store Week (“APSW”) growth from this initiative as well as closing / selling non-core locations

The Company was founded in 1939 by the Haseotes family

New Store Design

Targeting +80% AIM stores (70% today) over next 2 years, balance thereafter

Established Brand with a Long Operating History

Ari Haseotestakes over

responsibilities of retail division

2008 2017AIM next

generation launch

Early 1980’sLaunched coffee

offering

1939Founded by Vasilios

and Aphrodite Haseotes in

Cumberland, RI

2009Began investing in AIM concept stores to better serve customers

Mid 1950’sBegan selling and

producing ice cream and dairy products

1986Acquired

Northeast and Mid-Atlantic

marketing assets of Gulf Oil

1976Private label

beverage and bakery commissary

Enhanced breakfast offering as a part of

the AIM initiative

Late 2000’s

~2012Introduced pizza

offering as a part of the AIM initiative

Late 1990’sExpanded hot and

cold beverage offering

Exercised its option to acquire all outstanding

shares ofGulf Oil LP

2005

Product introductions

1971Opened first

fuel station inPutnam, CT

2015Sold Gulf and

Assured Dealer businesses

to ArcLight Capital Partners

2014Opened the

Culinary Center at its Distribution

Facility in Westborough, MA

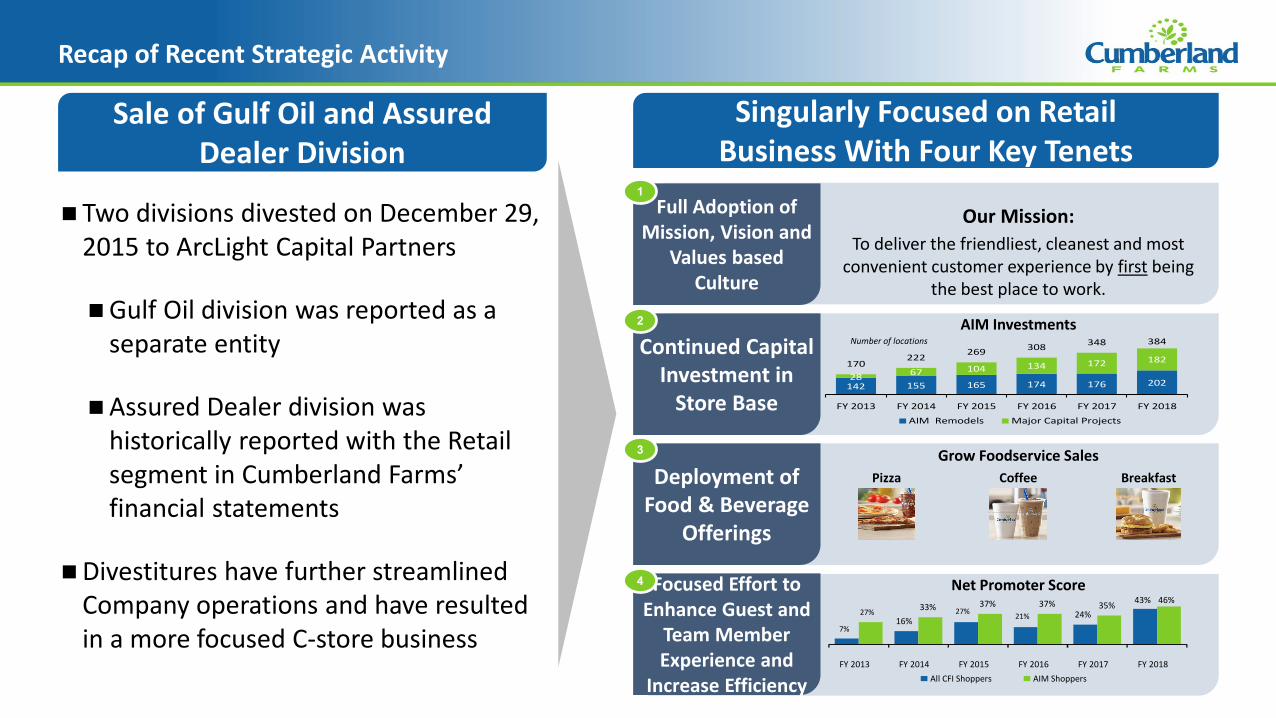

Recap of Recent Strategic Activity

Sale of Gulf Oil and Assured Dealer Division

Singularly Focused on Retail Business With Four Key Tenets

Two divisions divested on December 29, 2015 to ArcLight Capital Partners

Gulf Oil division was reported as a separate entity

Assured Dealer division was historically reported with the Retail segment in Cumberland Farms’ financial statements

Divestitures have further streamlined Company operations and have resulted in a more focused C-store business

Full Adoption of Mission, Vision and

Values based Culture

Continued Capital Investment in

Store Base

Deployment of Food & Beverage

Offerings

Focused Effort to Enhance Guest and

Team Member Experience and

Increase Efficiency

1

2

3

4

Our Mission: To deliver the friendliest, cleanest and most

convenient customer experience by first being the best place to work.

AIM Investments

142 155 165 174 176 20228 67 104 134 172 182170

222 269 308 348 384

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

AIM Remodels Major Capital Projects

Grow Foodservice Sales

Net Promoter Score

Pizza Coffee Breakfast

Number of locations

7% 16%

27% 21% 24% 43%

27% 33% 37% 37% 35% 46%

FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018All CFI Shoppers AIM Shoppers

Leading C-Store Retailer in the Northeast and Florida

Company-operated convenience store network

Revenue from motor fuel sales, food sales, convenience merchandise and service sales

As of December 31, 2018, operated 563 stores

Approximately 88% owned stores

Many new AIM stores anticipated to be over 5,000 sq. ft., although now studying a more compact model

Up to 20 fueling positions for new AIM stores

560,000 sq. ft. owned manufacturing and distribution facility in Westborough, MA services all Northeast stores

FLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFLFL

CTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTCTRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRIRI

MAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMAMA

NJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJNJPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPAPA

NYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNYNY

NHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNHNH

VTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVTVT

MEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEMEME

Northeast

Florida

Northeast Stores:

515

Florida Stores:

48

Total Stores: 563

Second highest brand equity according to the Nielsen’s 2017 Store Choice Driver Report

Leading Position and Scale in Attractive Markets

CFI convenience stores and fuel stations are generally situated on well-traveled thoroughfares or other easily accessible sites in the Northeast and Florida

Population density, employment and personal income data are very favorable in the Northeast as compared to other regions of the U.S. (1)

Northeast has second fewest number of convenience stores per capita in the U.S. (1)

Lack of developable land combined with the regulatory and permitting considerations for fuel stations limit the threat of competition from new entrants

3.57

4.37 4.63

5.71

0.00

1.00

2.00

3.00

4.00

5.00

6.00

West Northeast Midwest South

U.S. Average

U.S. Convenience Stores per Capita (1)

Stores per 10,000 People

____________________(1) Population from 2016 U.S. Census (as of July 1, 2017), Number of stores from NACS 2016 SOI Report.(2) NACS Report as of December 31, 2016.(3) Represents store count as of December 31, 2017.(4) Market efficiency defined as gas gallon market share divided by gas outlet share.

CFI’s Leading Position in Northeast Markets

Market Share by Store Count

(3) (4)(2)Market CFI Market MarketState Sites Sites Share Efficiency

RI 509 45 8.8% 1.42

MA 3,392 205 6.0% 1.62

NH 900 46 5.1% 1.09

ME 1,028 43 4.2% 1.38

CT 1,695 71 4.2% 1.73

VT 592 19 3.2% 1.12

NY 8,570 77 0.9% 1.21

Northeast 16,686 506 3.0%

FL 9,930 51 0.5% 0.98

Total 26,616 557 2.1%

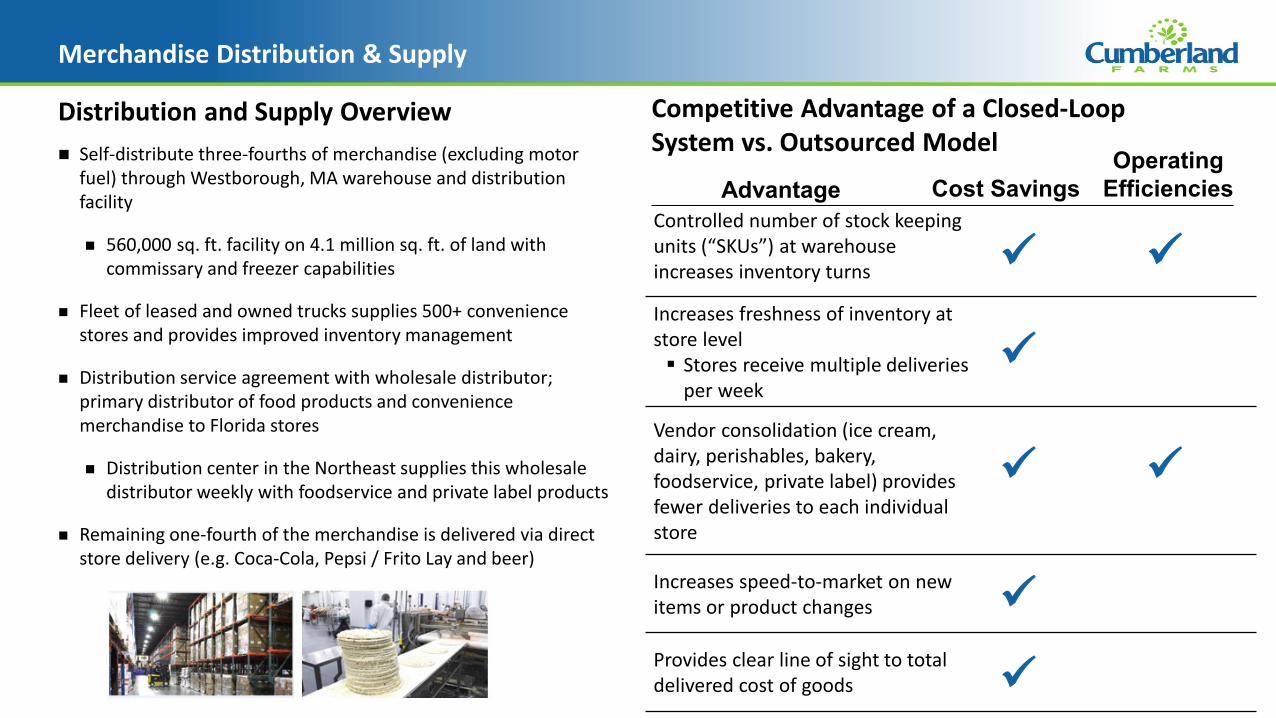

Merchandise Distribution & Supply

Competitive Advantage of a Closed-Loop System vs. Outsourced Model

Distribution and Supply Overview

Controlled number of stock keeping units (“SKUs”) at warehouse increases inventory turns

Increases freshness of inventory at store level Stores receive multiple deliveries

per week

Vendor consolidation (ice cream, dairy, perishables, bakery, foodservice, private label) provides fewer deliveries to each individual store

Increases speed-to-market on new items or product changes

Provides clear line of sight to total delivered cost of goods

Self-distribute three-fourths of merchandise (excluding motor fuel) through Westborough, MA warehouse and distribution facility

560,000 sq. ft. facility on 4.1 million sq. ft. of land with commissary and freezer capabilities

Fleet of leased and owned trucks supplies 500+ convenience stores and provides improved inventory management

Distribution service agreement with wholesale distributor; primary distributor of food products and convenience merchandise to Florida stores

Distribution center in the Northeast supplies this wholesale distributor weekly with foodservice and private label products

Remaining one-fourth of the merchandise is delivered via direct store delivery (e.g. Coca-Cola, Pepsi / Frito Lay and beer)

Advantage Cost SavingsOperating

Efficiencies

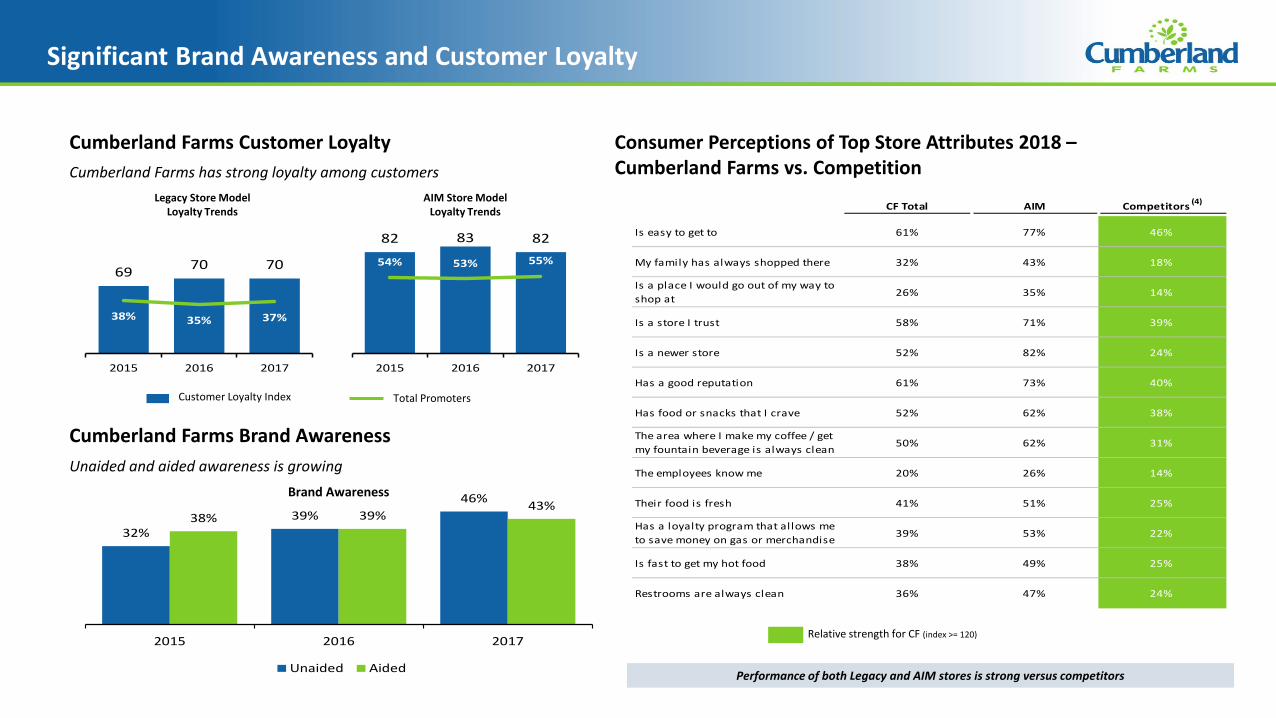

Significant Brand Awareness and Customer Loyalty

CF Total AIM Competitors (4)

Is easy to get to 61% 77% 46%

My family has always shopped there 32% 43% 18%

Is a place I would go out of my way to shop at 26% 35% 14%

Is a store I trust 58% 71% 39%

Is a newer store 52% 82% 24%

Has a good reputation 61% 73% 40%

Has food or snacks that I crave 52% 62% 38%

The area where I make my coffee / get my fountain beverage is always clean 50% 62% 31%

The employees know me 20% 26% 14%

Their food is fresh 41% 51% 25%

Has a loyalty program that allows me to save money on gas or merchandise 39% 53% 22%

Is fast to get my hot food 38% 49% 25%

Restrooms are always clean 36% 47% 24%

Consumer Perceptions of Top Store Attributes 2018 –Cumberland Farms vs. Competition

Performance of both Legacy and AIM stores is strong versus competitors

Relative strength for CF (index >= 120)

32%39%

46%38% 39%

43%

2015 2016 2017

Unaided Aided

Cumberland Farms Customer Loyalty

Cumberland Farms Brand Awareness

Cumberland Farms has strong loyalty among customers

Unaided and aided awareness is growing

82 83 82

54% 53% 55%

2015 2016 2017

69 70 70

38% 35% 37%

2015 2016 2017

Brand Awareness

Legacy Store Model Loyalty Trends

AIM Store Model Loyalty Trends

Total PromotersCustomer Loyalty Index

Multi-Pronged Growth Strategy

Growth Strategy Shifting merchandise mix towards higher-margin, differentiated items (e.g., private label and foodservice items such as coffee, frozen and fountain drinks, pizza, fresh sandwiches and bakery)

Focusing intensively upon brand development, consumer research and understanding and product innovation

Investing in technologies to drive efficiency and allow for more rapid, profitable and accurate decision making (i.e. fuel pricing software to optimize gross profit / volume dynamic and a supply chain management system)

Investing in technologies to drive customer loyalty and drive down credit card processing fees (i.e. SmartPay)

Utilizing AIM Concept stores to grow sales (APSW) and increase store productivity

Aggressively managing general & administrative expenses to enhance productivity and streamline business model

Investing in Team Members – recruiting, compensation / benefits, talent development and engagement

Enhance Sales and Profitability of Existing Stores

Remodeling Existing Locations & Building New Locations in AIM Format

Manage Expenses & Improve Cost Structure

The case for organic growth

It’s all about strategic alignment and, in Cumberland’s case, pursuit of a dual advantage

Differentiation achieved through marketing capabilities and brand recognition

Low Cost & Differentiation achieved through unique regional capabilities

Low Cost & Differentiation through continued growth in our core markets

Low Cost & Differentiation through uniformity in physical assets

Differentiation through superior quality, reliability, loyalty

Strategic Activity/Decision/Insight Aligned with Strategic Position…

Our corporate culture is the critical part of our brand/corporate strategy – how can we ensure continuity of this through acquisition of other cultures?

Store attributes (size, layout, parking/pump configuration) are integral to the brand experience

There is significant headroom in the markets in which we operate today

Our self-distribution model further reinforces our approach to regional scale

Focus on regional density – especially given the nature of the products we sell. “Having enough stores in the market to give our guests the opportunity to be loyal”

The case for organic growth

Some other (more practical) reasons

•We have seen results – our NTI AIM format has been successful and we have reliably achieved/exceeded our financial projections

•Acquiring quality assets that satisfy our store attribute requirements is very difficult and costly (what is the implied multiple assuming we’ve got to invest significantly to convert to our brand?) There can be risk here as well.

The case against organic growth

There are risks…

•A bird in the hand…

and increasing costs…

• While data suggest “headroom”, entitlement process is becoming increasingly challenging

Store Map

• Arkansas• Louisiana• Oklahoma • Texas

We’ve only just begun

Opportunity Awaits…

E-Z Mart Circa 1970

Jim Yates, NACS Chairman 1992-1993

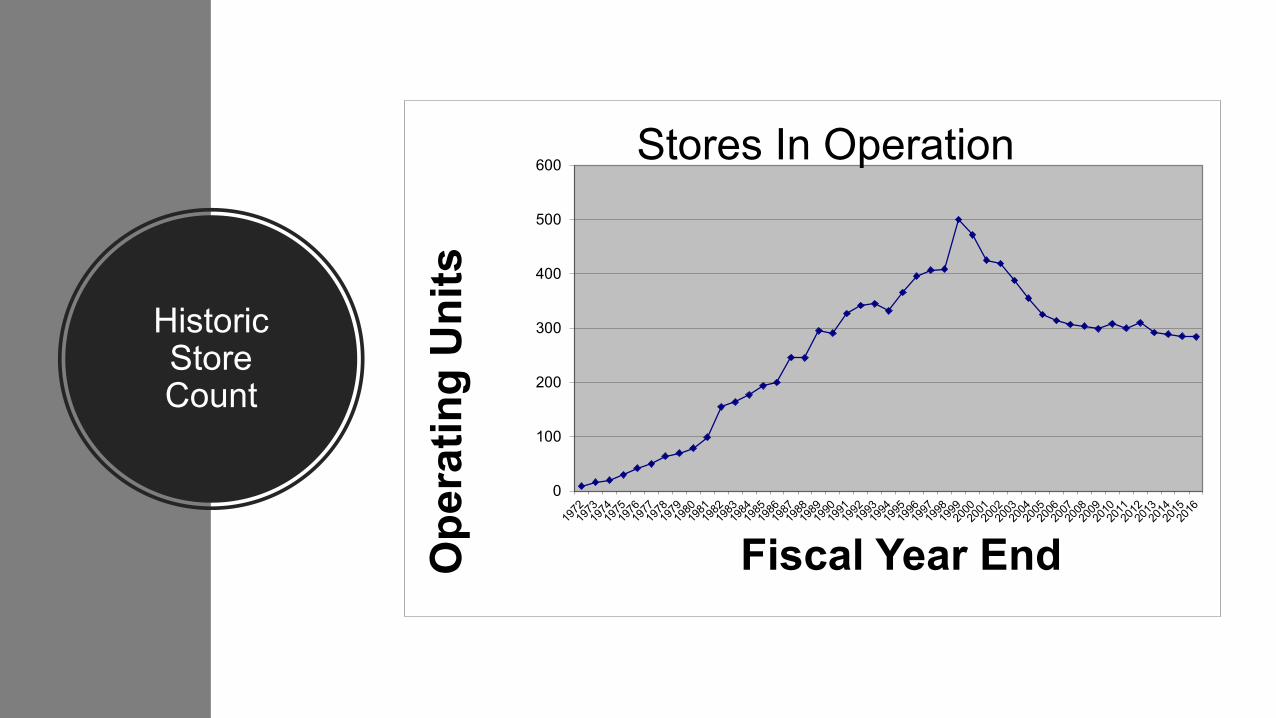

Historic Store Count

0

100

200

300

400

500

600

Ope

ratin

g U

nits

Fiscal Year End

Stores In Operation

Charles Darwin

• “It is not the strongest of the species that survives…nor the most intelligent that survives. It is the one most adaptable to change”.

Circa 1980-2000’s

Circa 2000--2017

Right Sizing By Store Improvement

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

-

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

-

200,000.00

400,000.00

600,000.00

800,000.00

1,000,000.00

1,200,000.00

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Per Store Average Sales & EBITDA Analysis

Series1 Series2 Series3

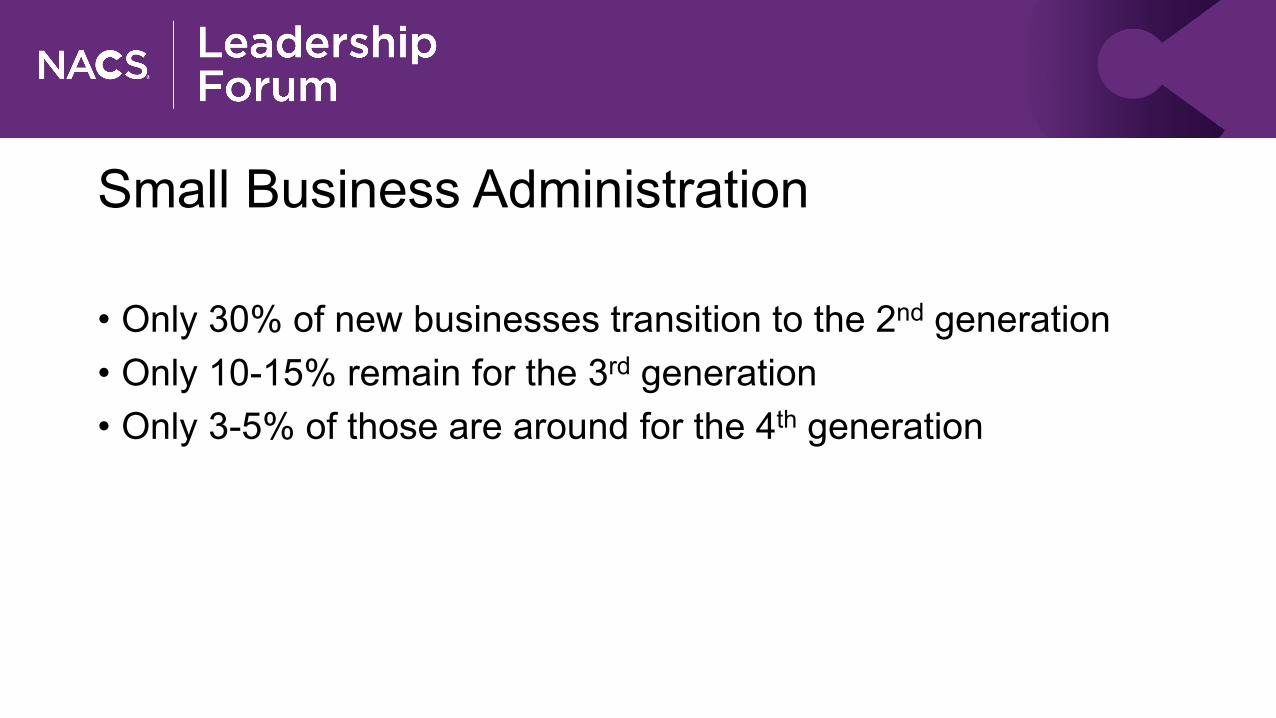

Small Business Administration

• Only 30% of new businesses transition to the 2nd generation• Only 10-15% remain for the 3rd generation • Only 3-5% of those are around for the 4th generation

Leadership Transition Types

Strategic leadership development is wisely accomplished by identifying future needs, personal goal-setting to recognize potential, professional development and mentoring to sustain.

Unexpected departure requires immediate action to manage risk to trust, focus and even continued operations. A bridge plan is necessary if a permanent plan isn’t immediately evident.

Planned departure is the best case scenario as it affords lead time to create and implement a successful transition and organizational stability.

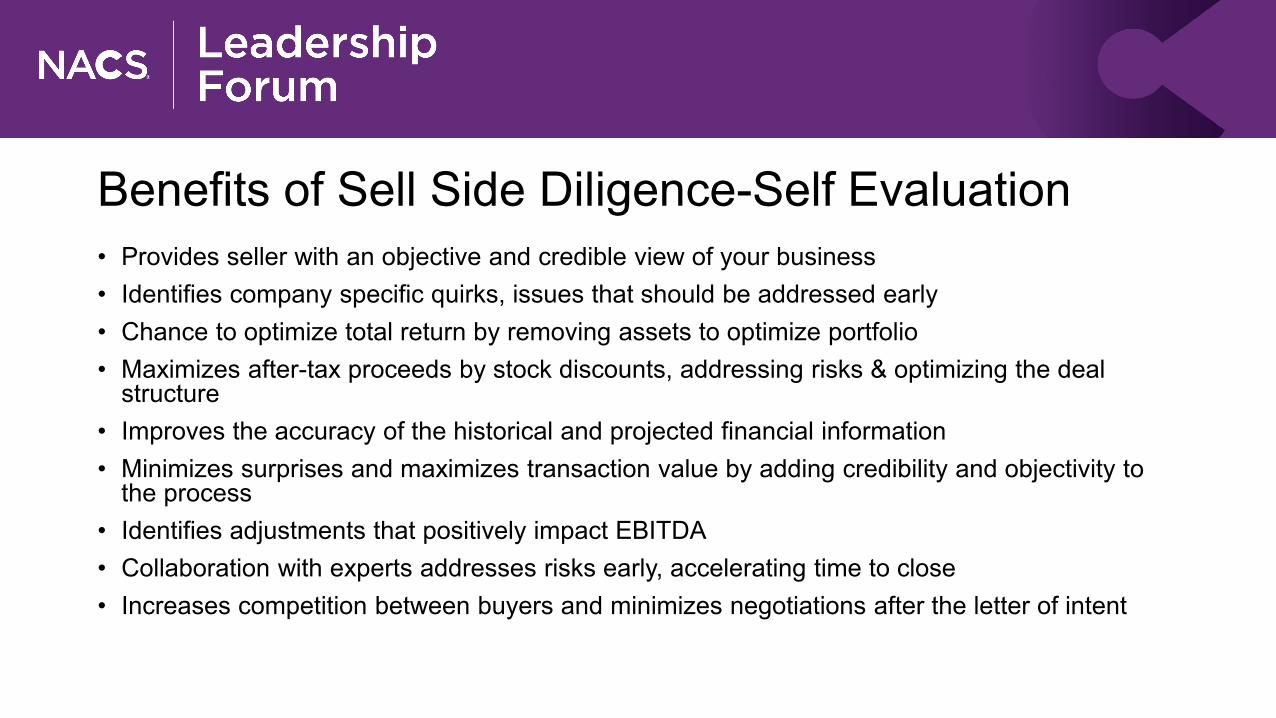

Benefits of Sell Side Diligence-Self Evaluation• Provides seller with an objective and credible view of your business• Identifies company specific quirks, issues that should be addressed early• Chance to optimize total return by removing assets to optimize portfolio• Maximizes after-tax proceeds by stock discounts, addressing risks & optimizing the deal

structure• Improves the accuracy of the historical and projected financial information• Minimizes surprises and maximizes transaction value by adding credibility and objectivity to

the process• Identifies adjustments that positively impact EBITDA• Collaboration with experts addresses risks early, accelerating time to close• Increases competition between buyers and minimizes negotiations after the letter of intent

Retirement Sucks!