Embed Size (px)

Citation preview

GENERATIONAL IMPACT ON SPENDING

Across the Ages: Spotlight on Modern Retail

RETAIL INSIGHT

Made possible by generous support from:

Why Read this Report? While many factors go into consumer buying decisions, the ultimate buying choice is often based on factors that go beyond price, usefulness, and positioning of the item in a store or on a website. Research trends suggest that the generation a consumer was born into, which defines their attitudes and experiences, plays a role in their buying behavior.

Though individuals have distinct characteristics, researchers are continuing to identify common behaviors and attitudes within generational groups.

Thanks to a generous contribution from KPMG LLP, the NRF Foundation has created this report using consumer research by Prosper Insight and Analytics. All data found in this report, and more, can be found in the Retail Insight Center: research.nrffoundation.com

These findings provide valuable insights for retailers and marketers seeking to understand – and capitalize on – customer behavior.

1

GEN

ERATIO

NS

GEN

ERATIO

NS

GEN

ERATIO

NS

GEN

ERATIO

NS

the 80 million people born between 1981 and 1995, often are considered ambitious, optimistic, eager to learn, informal, entrepreneurial—and impatient. Growing up with computers, cell phones, and the internet, they expect technology to meet their needs, and to do so right away. For the purposes of this report, we’ll be looking only at Adult Millennials, who are at least 18 years old.

1“Meet the Generations,” University of Missouri Extension, http://extension.missouri.edu/extcouncil/documents/ecyl/Meet-the-generations.pdf, accessed November 15, 2013.2 Prosper’s Monthly Consumer Survey is conducted online, via email among more than 5,000 respondents. The survey is balanced to the U.S. Census to make it representative of adults 18+ in the U.S.3Prosper’s Media Behaviors & Influence Study is conducted online, via email among nearly 20,000 respondents. The survey is collected one time per year and is balanced to the U.S. Census to make it representative of adults 18+ in the U.S.

I AM

I AM

I AM

I AM

The Silent Generation,also known as “Traditionalists,” encompasses the 50 million people born roughly between the mid-1920s and 1945. Having lived through the Great Depression and World War II, they’re a hearty and loyal lot with traditional ethics and an eye toward quality in all things. But as they continue to age, this generation increasingly seeks value and comfort. Despite being quite vocal as the originators of the Civil Rights Movement, they take their name from the fact that they’re perceived as quiet, hardworking types who overcome obstacles to get the job done.

I AM

I AM

I AM

I AM

Baby Boomers,generally defined as those born between 1946 and 1964, were the ones who came up with the term “workaholic.” These 76 million folks, who are soon to be entering, or already in retirement, grew up in an age that challenged conventions and put a man on the moon—but also saw the assassinations of key political leaders and lost trust in government thanks to events like Watergate and the Vietnam War. They’ve used their sheer size over the years to promote individualism and social causes. They seek relationships, loyalty, and trust.

the 50 million people following in the footsteps of the massive generation before, includes those born between 1965 and 1980. Members of this generation have learned to fend for themselves, and as the first “latchkey” kids, they value flexibility, freedom, self-reliance, emotional security, and open communication.

I AM

I AM

I AM

I AM

Generation X,

Millennials,

I AM

I AM

I AM

I AM

Against this generational backdrop, the results of recent studies gain context and color. The NRF Foundation has gathered data from Prosper Insights & Analytics’ Monthly Consumer Surveys2 in addition to their Media Behaviors & Influence™ Study that specifically looks into the behaviors and preferences among consumers.3

Before we can dive into examining how these groups of Americans make purchase decisions and spend their money, it’s important to understand how the generations are defined. The University of Missouri Extension offers the following breakdown:1

Who are they?

2

The two golden questions among retailers are

There is no one answer to these questions, however, it can often come down to the consumer’s mindset, which is shaped by when they were born.

For example, when consumers were asked whether they believed in “living for today” in terms of spending, more than one out of every two Millennials (53%) agreed. Conversely, only 22.5% of Silents felt the same, placing value in planning and preparing for tomorrow. Even when this eldest generation was young, living through the Great Depression and World War II meant more emphasis on service and duty rather than frivolity, and “waste not, want not” has continued to sum up their spending philosophies.4

As consumers age, value and comfort become increasingly more important, and the want-it-now-buy-it-now “live for today” shopping philosophy becomes less common. For older consumers to commit to a purchase, they are more likely to need valid reasoning rather than simply desire or emotional impulse.

Consumers with a “Live for Today” Spending Philosophy

4 Prosper Insights Monthly Consumer Survey, December 2013

Millennials: 1981–1995

Gen X:1965–1980

Boomers:1946–1964

Silent: Before 1945

Agre

e

Agre

e

Agre

e

Agre

e53%

38%25%

23%

What brings consumers into a store or onto a website?

What Gets Consumers to Buy?

1) What is going to motivate them to buy?

2)

3

Millennials: 1981–1995

Gen X:1965–1980

Boomers:1946–1964

Silent: Before 1945

Agre

e

Agre

e

Agre

e

Agre

e

53%

38%25%

23%

This spending philosophy translates to specific attitudes on what consumers want to buy and how they want to buy it. Each product category comes with its own set of characteristics of weighted importance across the generations; but let’s focus specifically on how consumers are shopping for clothing.

Time has proven that Gen Xers are a relatively skeptical group—and their self-reliant attitudes and mistrust of traditional conventions has made them a hard sell for marketers. Along with generally rejecting the rules, they’re not typically following trends, either. Less than one in four Gen Xers (23.1%) consider the newest trends and styles personally important. A focus on traditional, conservative looks will be appealing to the largest share of those in this generation.

While the “lowest price” strategy works for some retailers, it turns out, not all consumers are turned on by low prices—at least when it comes to clothing. Though roughly three out of five consumers say they usually buy clothing when it’s on sale, there are some consumers across the age groups who don’t need a discount. More than one out of five Millennials (22%), about one in six Gen Xers (15.9%), and nearly as many Silents (14.4%) do not think a sale is important when they are shopping for clothing.

Boomers are the most likely to be bargain hunting; nearly three in 10 (28.9%) Boomers say they only buy clothing when it’s on sale, a larger share than any other group.5

What is Most Important?

5 Prosper Insights Monthly Consumer Survey, December 2013 4

Making the Purchase DecisionWhat’s going to make a consumer hit the “Buy Now” button or stand in line at a register? Among all age groups, two factors have solid influence on motivating people to buy: the advice of others and the research performed before a purchase is made.

Of all consumers, more than 80% at least occasionally seek advice before a purchase, regardless of whether the purchase is online or offline,6 and 86.1% at least occasionally research items online before buying in a store.7

6Prosper Insights Media Behaviors & Influence Study, 2012. 7Prosper Insights Monthly Consumer Survey, December 2013. Only top responses shown among those who regularly or occasionally research items online before buying in a store.

46%

Millennials 1981–1995 Gen X 1965–1980 Boomers 1946–1964 Silents Before 1946

58%

Electronics Apparel Shoes Appliances

37%

29%

57%

31%

28%

23%

34%

18%

26%

20%

15%

29%

22%

17%

Products Researched Online Before Buying in Stores

[ ]

5

Asking for Advice

Even in the digital age, face-to-face communication is still the go-to method for finding advice on a product before making a purchase.

Millennials are most likely to ask advice through a text (42%)—and the least likely of all other age groups to ask someone product questions in an email (20.9%). But marketers still trying to reach this age group via email shouldn’t give up yet; it’s just essential that those emails are optimized for mobile and contain personalized content.8 Millennials are the most likely to depend on blogs (22.3%) and responses from friends on Facebook (32.2%) when seeking advice on a purchase.

Gen Xers are more than comfortable on the computer and the most likely group to be asking advice through email. This generation is also social media savvy; they’re nearly just as likely as Millennials to be seeking purchase advice through Pinterest, branded Facebook pages, and LinkedIn.

Boomers and Silents, while just about as likely to be looking for advice before making a purchase as their younger counterparts, are much less likely to be seeking purchase input through nontraditional channels. These consumers are likely to be looking to the people they know for advice — through phone calls from home, emails, and face-to-face communication.

For someone to receive input, of course, someone else must be willing to give it, and all age groups stand ready to oblige. Close to 90% give advice about purchases at least occasionally (with the Silents less likely than others at 84.7%). Millennials and GenXers are most likely to write product reviews—even though only just over 10% will.9

Despite the low percentage of product review writers, the content is highly valuable to shoppers. Regardless of their age, among those who seek advice, more than a third read reviews before a purchase.

8“Think You Know Mobile Millennials? Think Again, Campaigner,” Campaigner.com survey, http://media.marketwire.com/attachments/201309/190290_Millennials-Infographic-FINAL_FINAL_092713.pdf, accessed November 15, 2013. 9Prosper Insights Media Behaviors and Influence Study, 2012

Across the board, of those who seek advice before buying, roughly eight in 10 do so in person. However, generational differences become apparent with other forms of communication:

[ ]

6

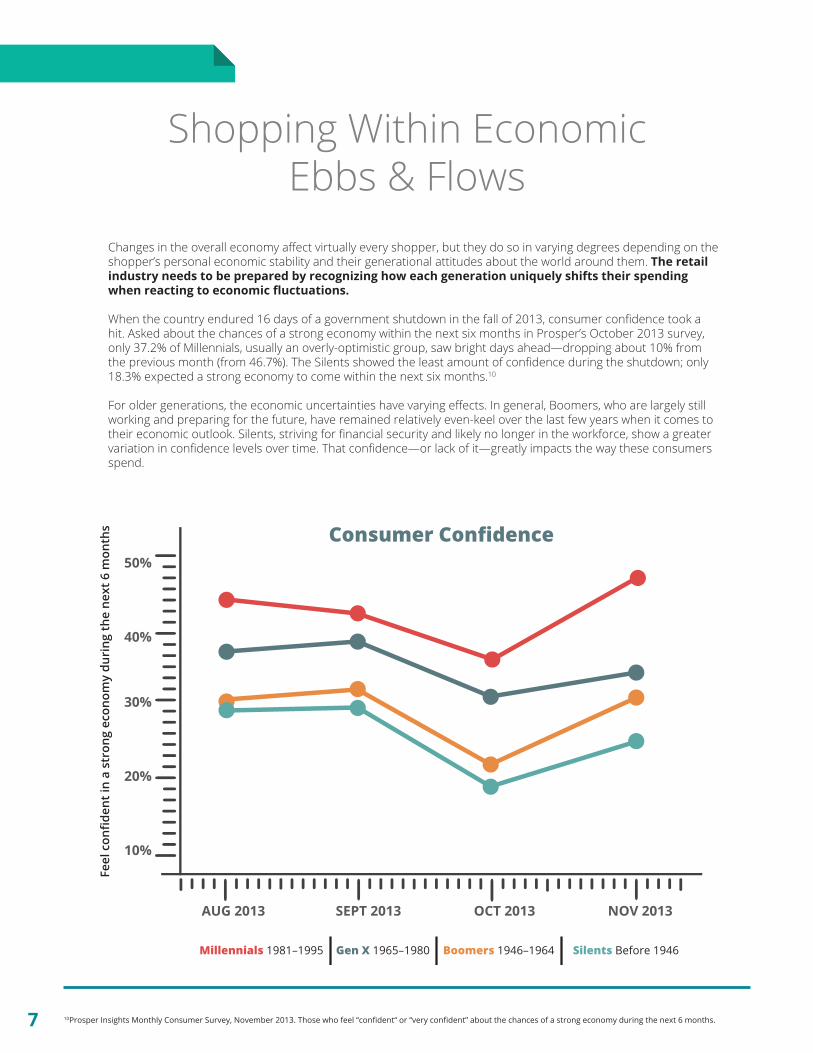

Changes in the overall economy affect virtually every shopper, but they do so in varying degrees depending on the shopper’s personal economic stability and their generational attitudes about the world around them. The retail industry needs to be prepared by recognizing how each generation uniquely shifts their spending when reacting to economic fluctuations.

When the country endured 16 days of a government shutdown in the fall of 2013, consumer confidence took a hit. Asked about the chances of a strong economy within the next six months in Prosper’s October 2013 survey, only 37.2% of Millennials, usually an overly-optimistic group, saw bright days ahead—dropping about 10% from the previous month (from 46.7%). The Silents showed the least amount of confidence during the shutdown; only 18.3% expected a strong economy to come within the next six months.10

For older generations, the economic uncertainties have varying effects. In general, Boomers, who are largely still working and preparing for the future, have remained relatively even-keel over the last few years when it comes to their economic outlook. Silents, striving for financial security and likely no longer in the workforce, show a greater variation in confidence levels over time. That confidence—or lack of it—greatly impacts the way these consumers spend.

Shopping Within EconomicEbbs & Flows

10Prosper Insights Monthly Consumer Survey, November 2013. Those who feel “confident“ or “very confident” about the chances of a strong economy during the next 6 months.

AUG 2013 SEPT 2013 OCT 2013 NOV 2013

50%

40%

30%

20%

10%

Millennials 1981–1995 Gen X 1965–1980 Boomers 1946–1964 Silents Before 1946

Consumer Confidence

Feel

con

fiden

t in

a st

rong

eco

nom

y du

ring

the

next

6 m

onth

s

7

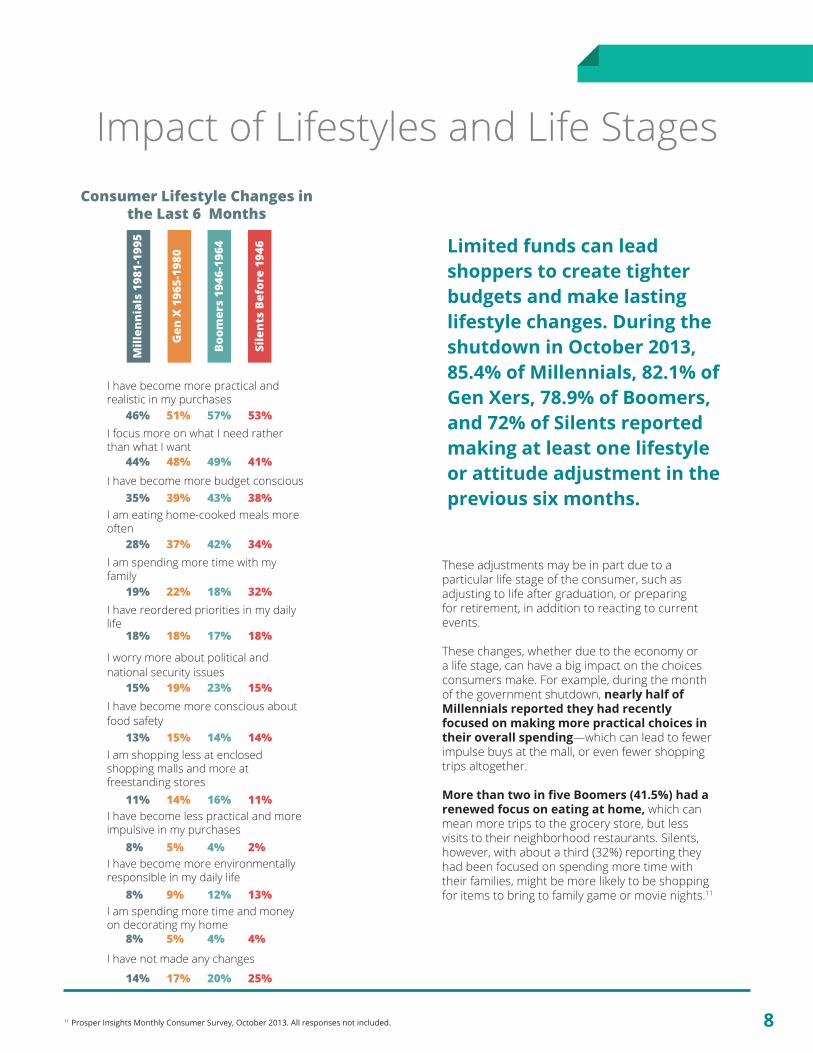

Impact of Lifestyles and Life Stages

These adjustments may be in part due to a particular life stage of the consumer, such as adjusting to life after graduation, or preparing for retirement, in addition to reacting to current events.

These changes, whether due to the economy or a life stage, can have a big impact on the choices consumers make. For example, during the month of the government shutdown, nearly half of Millennials reported they had recently focused on making more practical choices in their overall spending—which can lead to fewer impulse buys at the mall, or even fewer shopping trips altogether.

More than two in five Boomers (41.5%) had a renewed focus on eating at home, which can mean more trips to the grocery store, but less visits to their neighborhood restaurants. Silents, however, with about a third (32%) reporting they had been focused on spending more time with their families, might be more likely to be shopping for items to bring to family game or movie nights.11

11 Prosper Insights Monthly Consumer Survey, October 2013. All responses not included.

46% 51% 57% 53%

44% 48% 49% 41%

35% 39% 43% 38%

28% 37% 42% 34%

19% 22% 18% 32%

18% 18% 17% 18%

15% 19% 23% 15%

13% 15% 14% 14%

11% 14% 16% 11%

8% 5% 4% 2%

8% 9% 12% 13%

8% 5% 4% 4%

14% 17% 20% 25%

Mill

enni

als

1981

-199

5

Gen

X 1

965-

1980

Boom

ers

1946

-196

4

Sile

nts

Befo

re 1

946

I have become more practical and realistic in my purchases

I focus more on what I need rather than what I want

I have become more budget conscious

I am eating home-cooked meals more often

I am spending more time with my family

I have reordered priorities in my daily life

I worry more about political and national security issues

I have become more conscious about food safety

I am shopping less at enclosed shopping malls and more at freestanding stores

I have become less practical and more impulsive in my purchases

I have become more environmentally responsible in my daily life

I am spending more time and money on decorating my home

I have not made any changes

Consumer Lifestyle Changes in the Last 6 Months

Limited funds can lead shoppers to create tighter budgets and make lasting lifestyle changes. During the shutdown in October 2013, 85.4% of Millennials, 82.1% of Gen Xers, 78.9% of Boomers, and 72% of Silents reported making at least one lifestyle or attitude adjustment in the previous six months.

8

As retailers have shifted their focus towards online and digital, they’ve added a number of services and features to attract, engage, and maintain customers. When comparing across age groups, some tactics work, while others fall flat.

Low prices are important across all age groups, however, from 2009 to today, price has significantly more impact on the Boomer generation (75.3% consider low prices “very important” when shopping online). The economic recession has been particularly challenging on Boomer retirement plans and careers, and this has had a lasting influence on how they shop online.

While six in 10 Millennials (59.6%) consider free shipping of high importance, it’s those in the Silent generation that most value this service (69.8% consider it very important). The eldest group also highly values flexible return policies, with 60.1% rating it as “very important.”

Live customer service remains important for consumers shopping online; it is significantly important for at least a third of consumers across all age groups. As of December 2013, nearly two in five (38.5%) consumers considered live customer service when shopping online to be very important, compared to 40.8% who felt this way in December 2008. Even among the Millennials, who typically steer towards more automated shopping experiences, this feature is important for online shopping (32.5%).

The options to pick up or return an item bought online to a store, rather than mail it back, is a service we’ve seen added across multiple retail channels and continues to be a convenience that’s valued across the generations. About two in five consumers from any age group consider this service to be “very valuable”.12

How Online Services Motivate Shoppers

12Prosper Insights Monthly Consumer Survey, December 2013

LOW PRICES

FREE SHIPPING

LIVE CUSTOMER SERVICE

PICKUP/RETURNTO STORE

9

For as different as the generations are, in attitudes, their current life stage and past experiences, some things hold constant: value is still value; not everyone follows the trends; and customers will seek services and products that meet their needs. Customers of all ages will openly speak about the things they like—and the things they don’t, although the channels they use to communicate may vary and evolve.

Some ingrained preferences that differentiate consumer generations may hold constant throughout a consumer’s life. For example, Millennials may be the biggest spendthrift generation we’ll see. This group is considered the most likely to spend freely—no doubt influenced by the ever-evolving customer-centric shopping model, which makes nearly everything available at their fingertips.

And some preferences and shopping trends are shaped by the life stage of the consumer. For example, someone entering retirement may place more value on low prices, facing a fixed income in the years to come. Middle-aged consumers, who are likely to be supporting a home, are likely to be on the lookout for deals and discounts on everyday items in order to keep their budgets intact.

As the online shopping experience continues to evolve and expand—expected to reach $370 billion in sales by 201713 — the consumer shopping experience is changing across all generations and generations to come. For brick-and-mortar retailers to remain competitive in the omnichannel market, it’s essential for stores to provide an extra level of value that a consumer may not find online, tailored to their preferences—such as personalized customer service or a unique experience with the products, in order to get them out of the house. Likewise, retailers with online storefronts will need to adjust their features and services to attract and keep customers.

13Forrester Research Online Retail Forecast, 2012

GENERATIONAL IMPACT ON SPENDING

Across the Ages:

GENERATIONSGENERATIONSGENERATIONSGENERATIONS

Summing it Up

10

Discover more research in the Retail Insight Center research.nrffoundation.com

Spotlight on Modern Retail

RETAIL INSIGHT

The Retail Insight Center is made possible by:

![BY VANAIR Installation Instructions - R44Installation Instructions - R44 INSTALLATION BearPaw Installation Reference Documentation: [1] Robinson R44 - Maintenance Manual & Instruction](https://img.dokumen.tips/doc/110x75/611c1e10c6d43953dc4a519f/by-vanair-installation-instructions-installation-instructions-r44-installation.jpg)