Embed Size (px)

Citation preview

Retail Credit RiskConfidential

A ll contents contained in the Mortgage C redit Requirements is c lass ified as "Internal" in line with A NZ's

Information Security P olicy. I t is subjec t to the information c lass ification and security guidelines for internal

documents .

P rovis ion of any part of the c redit to an external audience requires the spec ific permiss ion of Head of Secured

Lending Risk (or an authorised delegate).

Retail Collection Credit Requirements2 December 2016

ANZ.800.508.2359

ANZ.800.508.2360

2 Retail Collection Credit Requirements

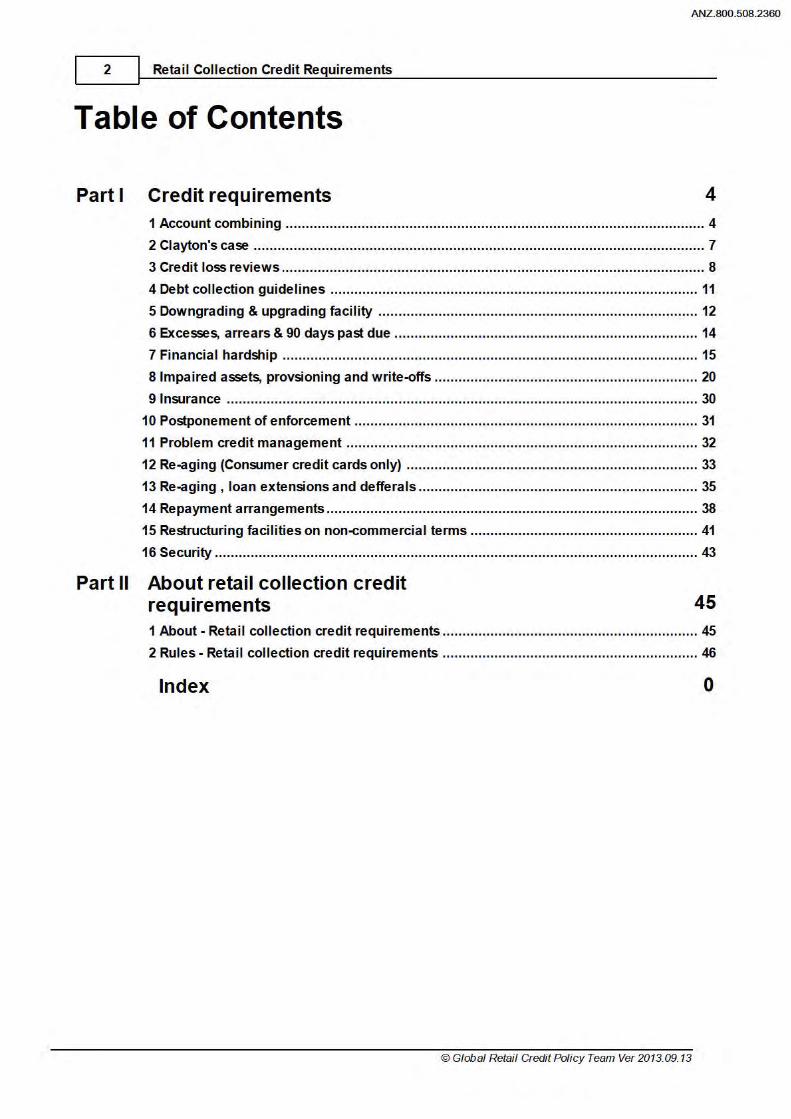

Table of Contents

Part I Credit requirements 4

1 Account combining ......................................................................................................... 4

2 Clayton's case ................................................................................................................. 7

3 Credit loss reviews .......................................................................................................... 8

4 Debt collection guidelines ............................................................................................ 11

5 Downgrading & upgrading facility ................................................................................ 12

6 Excesses, arrears & 90 days past due ............................................................................ 14

7 Financial hardship ........................................................................................................ 15

8 Impaired assets, provsioning and write-offs .................................................................. 20

9 Insurance ...................................................................................................................... 30

10 Postponement of enforcement ...................................................................................... 31

11 Problem credit management ........................................................................................ 32

12 Re-aging (Consumer credit cards only) ......................................................................... 33

13 Re-aging , loan extensions and defferals ...................................................................... 35

14 Repayment arrangements ............................................................................................. 38

15 Restructuring facilities on non-commercial terms ......................................................... 41

16 Security ......................................................................................................................... 43

Part II About retail collection credit requirements 45 1 About - Retail collection credit requirements ................................................................ 45

2 Rules - Retail collection credit requirements ................................................................ 46

Index 0

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2361

Part

4 Retail Collection Credit Requirements

1 Credit requirements 1.1 Account combining

On this page: • Credit reciuirement purpose • In scope • Guiding principles rratrix • Eligible sub products to account corrbine

Credit requirement purpose

Account combination describes the process where the balances of one or ITI)re accounts held by the same customer are 'combined' to repay a debit a!TI)unt of one account. Account combination is usually performed after several failed atterrpts to contact the customer and when there has been a prolonged period of default .

In scope

The following items/ areas are in scope of this review :

• Customers with delinquent products. • Products in scope:

• Commerc ial Credit Cards • Consumer Credit Cards • Everyday Visa Debit Accounts • Mortgages • Personal Loans

Guiding principles matrix

These requirements set the mnirrum standards in which this requirement is to be followed :

Principle Description

ANZ.800.508.2362

Evaluation of Eligibility • Check that there have been at least 3 atterrpts to 8t Appropriate time to contact the customer; Account Combine • Check if ANZ has atterrpted other steps to reduce

the default; • Customer rrust not be on a current arrangement; • Customer rrust not have recently requested an

account combination to be reversed; • Account rrust not have been issued with a default

notice that is yet t o expire;

Salary Deposits Do not use account combine from accounts that receive the following payments: • Centrelink;

© Global Retail Credit Policy Team Ver 2013.09.13

Residual Balance

Acceptable Amounts to Account Combine

Account Combination during Weekends

Account Combination Reversals

Important Notes:

Credit requirements! 5

• Baby Bonus; • Child Support . • Funds received as a result of relief i.e. flood

assistance • Veterans Affairs Payments

• A residual balance of at least $300 or 10% of the balance or the greater of the two must be left in the customer's transaction account, unless the product requires another amount t o be retained (for example, rrinimum balance of $5,000 on V2+;

Other factors t o consider are: • Frequency of wages/ income; • Living expenses required until next pay; • Account payment history; and • Other periodical payments to ANZ.

• Full arrears; • Multiples of scheduled payments; • Minimum monthly credit card payment; • The amount required to drop the account t o a

lower delinquency bucket; • Statemented overdrawn or inforrral overlirrit

amount.

• Account corrbinations activities should not occur on weekends and public holidays.

Before a reversal is processed, consider: • Customer's individual circurrstance i.e. reason for

reversal; • Account payment history; • Effect on delinquency; and • Subsequent arrangement made; • Customer advises of hardship.

The Code of Banking Practice requires : • ANZ must inform the customer promptly after exerc ising the right to combine

accounts • In exerc ising a right to combine accounts, ANZ will comply with any applicable

requirements of the Code of Operation for Centrelink Direct Credit Payments. • ANZ must not exerc ise the rights to combine the accounts while :

ANZ.800.508.2363

• ANZ are actively considering the customers financ ial situation under the hardship provisions of the National Credit Code. As a condition of ANZ not exerc ising rights to combine the account ANZ may seek customer's agreement to retain funds in an account until the hardship application has been made; or

• the customer are complying with an agreed arrangement from Hardship consideration.

Eligible Sub Products to Account Combine

The sub-product codes listed below are the only eligible products to account corrbine

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2364

6 Retail Collection Credit Requirements

from Any account that does not match any of the following sub- product codes cannot be used for account combination.

Eligible ODA sub products codes

Sole Personal Accounts Commercial/Business Accounts

cc Access Cheque Account M3 ANZ BML Offset - Fu ll Offset - Cheque

CE Access Deeming Account M4 ANZ BML Offset - Fu ll Offset - Savings

CF Access Deeming Cheque Account NE Negotiato r

CG Access Se lect NF Negotiato r Account - No Cheque

CH Access Se lect NG Negotiato r Account

CI Wealth Management CMA Investor NH Negotiato r Account - No Cheque

cs Access Savings Account NI Negotiato r Plus

ex ANZ Access Bas ic CM Cash Ma nagement Accou nt

EB ANZ Premium Cash Management CN Cash Management Account Account w ith Cheque

ES ANZ Premium Cash Management FB ANZ Revo lving AGRI Line Accou nt

HL Home Loan Interest Saver NJ Negotiato r Plus - Without Cheque

Ml ANZ One - Full Offset - Cheque DR Drive r Account

M2 ANZ One - Fu ll Offset - Saving BP ANZ AGRI Finance Offset Account

PG Access Se lect Cheque CB Business Class ic Cheque Accou nt

PH Access Account w ith Cheque CD Business Class ic - No Cheque

PM Access Premium Accou nt HA Business Cash Ma nagement Accou nt

PS Access Advantage Account HB Business Cash Management Account

PT Access Advantage Cheque Account HC Premium Business Cash Accou nt

SA Progress Saver Account 11 Business Extra Cheque Account

ED Online Saver I3 Business Extra - Wit hout Cheque

V2 V2 Plus (must leave a min imum ba lance of $5000)

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2365

Credit requirements! 7

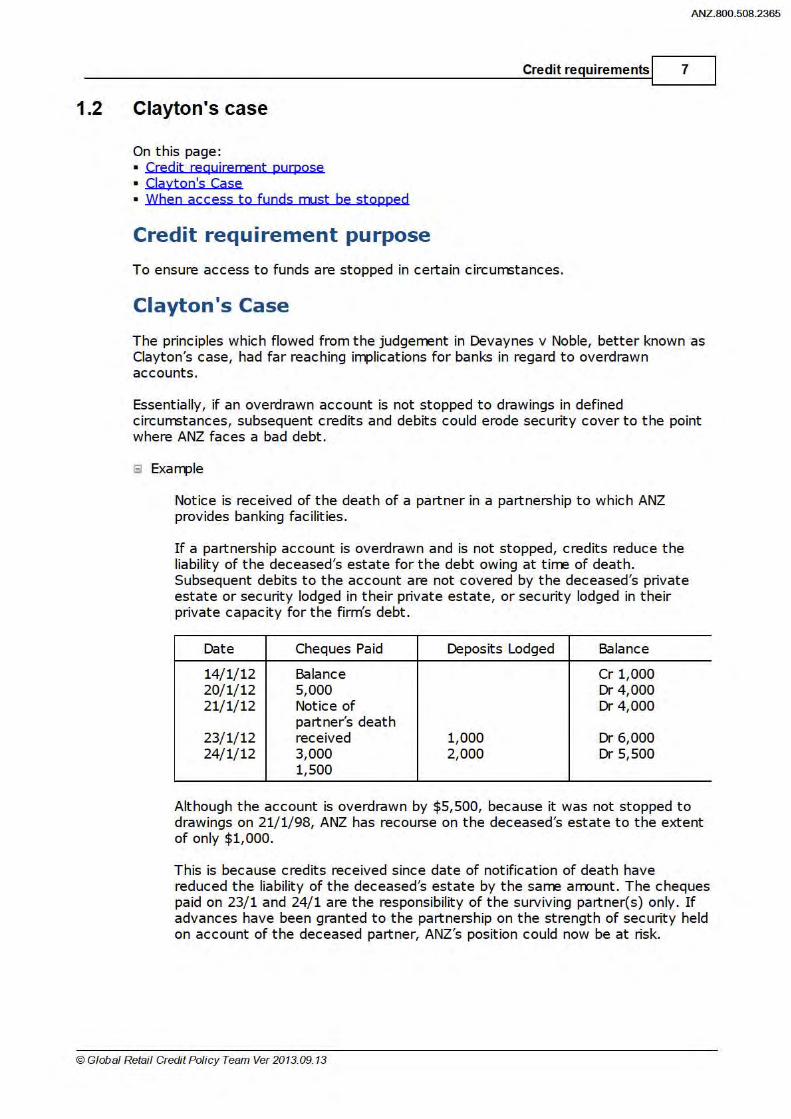

1.2 Clayton's case

On this page: • Credit reciuirement purpose • Clayton's Case • When access to funds must be stopped

Credit requirement purpose

To ensure access to funds are stopped in certain c ircumstances.

Clayton's Case

The principles which flowed from the judgement in Devaynes v Noble, better known as Clayton's case, had far reaching implications for banks in regard to overdrawn accounts.

Essentially, if an overdrawn account is not stopped to drawings in defined circumstances, subsequent credits and debits could erode security cover to the point where ANZ faces a bad debt.

13 Example

Notice is received of the death of a partner in a partnership to which ANZ provides banking faci lities.

I f a partnership account is overdrawn and is not stopped, credits reduce the liability of the deceased's estate for the debt owing at time of death. Subsequent debits to the account are not covered by the deceased's private estate or security lodged in their private estate, or security lodged in their private capac ity for the firm's debt.

Date Cheques Paid Deposits Lodged Balance

14/ 1/ 12 Balance Cr 1,000 20/ 1/ 12 5,000 Dr 4,000 21/ 1/ 12 Notice of Dr 4,000

partner's death 23/ 1/ 12 received 1,000 Dr 6,000 24/ 1/ 12 3,000 2,000 Dr 5,500

1,500

Although the account is overdrawn by $5,500, because it was not stopped to drawings on 21/ 1/ 98, ANZ has recourse on the deceased's estate to the extent of only $1,000.

This is because credits received since date of notification of death have reduced the liability of the deceased's estate by the same arrount . The cheques paid on 23/ 1 and 24/ 1 are the responsibility of the surviving partner(s) only . I f advances have been granted to the partnership on the strength of security held on account of the deceased partner, ANZ's position could now be at risk.

©Global Retail Credit Policy Team Ver 2013.09.13

8 Retail Collection Credit Requirements

When access to funds must be stopped - rule in Clayton's Case

ANZ.800.508.2366

An overdraft rrust be stopped to drawings and all other accounts stopped if any of the following occurs:

• Advances on fluctuating overdraft to companies with restricted borrowing powers if prescribed powers were subsequently exceeded by funds raised elsewhere.

• Appointment of receiver by outside debenture holder. • Bankruptcy, assignment of estates. • Change of partners. • Death of customer. • Death of one party to a j oint account, death of guarantor or guarantor

rrortgagor or other Third party having any liability on an account. • Dissolution of partnership. • Liquidation of company. • Lunacy, certification as an infirm person of any of the foregoing or on beconing

aware that such a person has corrmitted an act of bankruptcy . • Notice received of any claim by any person against a security . • Notice received of subsequent charge given over security property. • Notice received of the compulsory acquisition of security property. • Notice received that a company has subsequently executed a GSA over all its

assets, where ANZ holds a rrortgage over property of the company. • Security is sold by the owner.

1.3 Credit loss reviews

On this page: • Credit reciuirement purpose • Objective of Credit Loss Review • Approval of the credit loss report • Conseciuence managerrent frarreworl<

Credit requirement purpose

To set out the rules for conducting a Credit Loss Review.

Objective of Credit Loss Review

The objective of a Credit Loss Review {CLR) is to identify causes of credit loss and improvement opportunities in credit management and credit process to avoid

© Global Retail Credit Policy Team Ver 2013.09.13

Contains Confidential Information ANZ.800.508.2367

redit requirements ._l __ s _ _.

repetition of cause.

It is recognised that credit risk management involves decisions involving a balance between acceptable risk and comrrercial judgement. ANZ will not penalise or discipline officers who exercise judgemental credit assessment in accordance with the Bank's credit principles and Retail credit policies, procedures and requirements.

A Credit Loss Review is to: • Be completed by an independent c or those accounts where credit

loss rovision established exceeds For credit loss provisions below , a CLR will only be required if deemed necessary by business, risk,

audit, lending services or collections. • Be documented in a Credit Loss Report which will detail:

• A history of the credit facility including the basis of major decisions and justification, account grading history, and remedial and recovery action plans implemented prior to crystallising of the assessed loss position.

• Major reasons contributing to the loss. • Areas requiring improvement on the part of ANZ (credit management policies

and credit assessment procedures) and officers concerned (weaknesses in performance and behaviour).

• Include recomrrendations on action required to address deficiencies in credit processes and officer performance (if appropriate).

• Be shown to officer concerned, where perfonnance weakness is highlighted, to allow opportunity for comnent or to correct any errors of fact.

• Be approved within two months of completion of the Credit Loss Report. • The Credit Loss Report template can be obtained from your BU Risk team.

Approval of the credit loss report

Credit Loss Reports for Australian Operations are to be undertaken and approved in terms of the following matrix:

Manager Credit Control

©Global Retail Credit Policy Team Ver 2013.09.13

• Senior Retail Credit Control Manager OR

• Senior Credit Control Manager

• Monthly executive report pack will be emailed to respective Heads of Risk. Report pack will also be tabled at AORF (Australia Operations Risk Forum) and be available for distribution to all

Contains Confidential Information ANZ.800.508.2368

10 Retail Collection Credit Requirements

Risk stakeholders.

• Heads of Risk acceptance of the monthly report will assume confirmation review of am! case reviews co111>leted during the month.

* Refer to note 1 below

sMIP to < ~~~:r~~r Credit • Senior Manager Credit Control OR

> Confidential

AND Recorrmended by : • Senior Retail

Credit Control Manager OR

• Senior Credit Control Manager

Internal Audit

• Central & District Credit

Divisional Head of Risk

* Refer to note 2 below

Note 1: The following key points need to be followed accordingly: • Divisional risk will be emailed individual case specific Loan Loss Review reports

completed by Credit Control Assurance during the preceding month where the loss provision is[lli]'i'Ufit$iiiilo~-hly basis) .

• Where the loss provision is TJ • I individual case specific reports can be ordered I called for, upon request to the Senior Manager Credit Control.

• Credit Control approval sign off parties rrust be independent to the transactional credit. If not, approval sign off rrust be referred to and obtained from the Head of Credit Commercial Distribution.

Note 2: Subject to the agreement between the Group General Manager Global ]ntemal Audit and the Divisional Head of Risk, Internal Audit may undertake completion of the CLR or hand the responsibility to undertake the CLR back to your credit partner or the responsible Divisional Risk or Credit Area.

The Group General Manager Global Internal Audit retains the sole discret ion to decline to undertake certa in CLRs if he/she considers:-

• The CLR could be done by someone who has the requisite independence and experience within the asset writing business unit itself; or

• Global Internal Audit does not have the resources to undertake a specific CLR within the acceptable tinneframes identified in the policy.

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2369

Credit requirements! 11

Note: All Parties • All parties, including the approving officers rrust be independent, if not,

subnission to the next level in the credit chain is required . • The outcome of the Credit Loss Review is to be comrunicated to all parties

involved within three months of the recognition of the loss.

Consequence Management Framework

Any consequence management action will be in accordance with ANZ People Policy on employee nisconduct and performance improvement, with the full partic ipation of People Capital.

Refer Global Performance Irrprovement & Unacceptable Behaviour Policy.

1.4 Debt collection guidelines

On this page: • Credit reciuirement purpose • Debt collection guideline

Credit requirement purpose

In Australia various laws and regulations govern the way ANZ undertakes collection activit ies

Debt collection guideline

The consumer regulators ACCC and ASIC have jointly produced a guideline for Collectors ( including in house collection departments, collection agenc ies, solicitors etc.) and Creditors (directly involved in debt collection) .

For information regarding the Debt collection guidelines refer to : • Debt Collection Guideline presentation dated March 2010 on Collection MAX site;

or • Debt collection guideline for collectors and creditors : joint publication by ACCC

and ASIC ( internet access required)

©Global Retail Credit Policy Team Ver 2013.09.13

12 Retail Collection Credit Requirements

1.5 Downgrading & upgrading facility

On this page: • Credit reciuirement purpose • Downgrading centrally managed facility • Upgrading credit facilities • Automated credit assessment

Credit requirement purpose

To set the rules for downgrading and upgrading credit facilities

Downgrading centrally managed facility

For all Basel Retail credit facilit ies, if delinquency occurs and account conduct deteriorates the customer credit rating rrust be downgraded as follows :

07 -Substandard

Downgrade Point

Days in excess or arrears are greater than 60 days but do not exceed 90 days

ANZ.800.508.2370

08 -Substandard

When a facility, overdraft or account has been in excess > $100 consecutively for 90 calendar days or rrore, or in the case of accounts with regular repayments schedule, when at least 90 calendar days have elapsed since the due date of a contractual payment which has not been met in full; and the total arrount outside contractual arrangements is equivalent to at least 90 days worth of contractual payments.

09 - Non Loss or partial loss of interest and fees is expected, but full Accrual Without recovery of principal is anticipated. Unsecured consumer debt does Provision not qualify for CCR 09

10 - Non Accrual With Provision

Loss or partial loss of principal, interest and fees is expected

Exception: If a materia l adverse change in t he customer's ability to repay becomes evident, the credit facility is to be reviewed for possible downgrade immediately. Notwithstanding t he above risk grading trigger points if an account is determned to be

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2371

Credit requirements! 13

at risk of loss of either princ ipal or interest, it is to be downgraded to CCR 09 or 10.

Upgrading credit facilities

Credit facilities rated CCR 07 or 08 can be upgraded to CCR 00 or CCR 01 - 06 if satisfactory performance has been evident for at least six rronths on all customer credit facilities within the group.

Credit facilities rated CCR 09 or 10 can be upgraded to CCR 07 or CCR 08 if satisfactory performance has been evident for at least six rronths on all customer credit facilities within the group.

Credit facilities rated CCR 09 or 10 may also be upgraded to CCR 07 or 08 where the security has been re- valued or the debt has decreased such that a loss of principa l or interest will not be evident.

Automated credit assessment

Generally, all retail c redit applicat ions are subject to automated credit scoring rrodels. The objective of automated credit scoring rrodels is to achieve business effic iency and nininise risk by providing faster assessment processes and rrore consistent and accurate credit .

Credit scoring uses a statistically based approach to assign points to various characteristics, which errpirical evidence, shows are predictive of borrowers defaulting, to arrive at a credit score. Different c redit scoring methods may be applied to different products, types of applicants or size of loans applied for. At origination, the application credit score for each credit application is corrpared against "cut off" scores which, in conjunction with the application of credit policy rules deternine if the application is acceptable. A portion of applications are referred out for manual credit assessment undertaken by bank officers with the appropriate level of credit approval discretion.

Once a credit has been originated, a behavioural score is then derived from statistical methods using many of the customer's internal historical account conduct such as arrears or excesses, payment history etc . to predict their probability of default .

For further infonrat ion refer to the appropriate credit requirements manual :

• Small Business Credit Requirements - Risk grade framework • Esanda Retail Car Credit Requirements {pgS) • Business Equipment Retail Credit Requirements {pg 12) • Mortgage Credit Requirements • Personal Loan Credit Requirements • Consumer Credit Card Requirements • Consumer Overdraft Credit Requirements

©Global Retail Credit Policy Team Ver 2013.09.13

14 Retail Collection Credit Requirements

1.6 Excesses, arrears & 90 days past due

On this page: • Credit reciuirement purpose • Excesses • Arrears • 90 days past due

Credit requirement purpose

To provide a definition for excess, arrears and 90 days past due.

Excesses

An excesses is any drawing initiated by : • the customer • a third party acting under authority from the customer • a third party acting on behalf of the customer • ANZ

ANZ.800.508.2372

Provided such drawing creates a debit balance to a current account or which causes a debit balance beyond any formal overdraft limit .

In addition, excesses include accounts with an overdraft limit recorded where, upon a scheduled expiry or reduction of the recorded limit, the account becomes in excess.

When calculating the number of days the account has been in excess, the period commences from the date that any event of excess occurs and accrue for each completed calendar day after the excess event.

Arrears

An account is in arrears when the customer: • misses a scheduled princ ipal or interest repayment . • misses any scheduled lump sum reduction .

When calculating the number of days past due, the period commences from the date that any event of arrears occurs.

90 days past due

When a faci lity, overdraft or account has been in excess consecutively for 90 calendar days or more, (which includes internally authorised excesses or extensions not formally documented with the customer) .

A fac ility subject to a regular repayment schedule is regarded as 90 days past due

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2373

Credit requirements! 15

when : • at least 90 calendar days have elapsed since the due date of a contractual

payment which has not been met in full; and • the tota l arrount outside contractual arrangements is equivalent to at least 90

days worth of contractual payments.

A fac ility will remain outside contractual arrangements notwithstanding any waiver of payments.

1.7 Financial hardship

On this page: • Credit reciuirement purpose • Financial hardship • Additional references

Credit requirement purpose

This credit requirement provides guidance on repayment arrangements for customers experienc ing financ ial hardship.

Financial hardship

" Financial hardship" is when a customer is will ing and has the intention to pay, but is unable to meet their repayments or existing financ ial obligations, and with formal hardship assistance, a customer's financ ial situation can be restored . This definition is based on the assumption that people want to meet their financial obligations.

Customers experienc ing hardship are identified through a nurrber of methods: • Customer self-assessment & notification to ANZ (verbally or in writing) • ANZ assessment or identification • Independent accredited financial counsellor

Customers may not be required to provide evidence of their hardship through the

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2374

16 Retail Collection Credit Requirements

production of rnedical, financial or any other documentation to qualify for short-term non- traditional repayrnent arrangernents. However, documentation relating to a custorner's hardship situation may be required for longer term arrangements and also where the ANZ credit faci lity has lenders' rrortgage insurance ( LMI ) .

The aim of any repayrnent arrangernent is to rehabilitate the customer to a financ ial position where they can resurne servicing their loan. As such, repayrnent arrangernents should be realistic and should not sirrply be postponing inevitable default .

ANZ's obligations with respect to dealing with custorners experiencing financial difficulty or hardship arise from the National Credit Code, Code of Banking Practice & Australian Government's Hardship Princ iples.

Refer to section on National Credit Code Hardship Provisions for timng of decisions and notices.

ANZ's obligations when dealing with customers in hardship

Customers experienc ing hardship are to be identified and assisted in a consistent and respectful manner. As much as possible, having regard to ANZ's interests and its rights, these customers will be supported to stabilise their financ ial situation through the development of tailored repayrnent arrangernents, which may or may not rneet the long term repayment arrangement criteria .

ANZ is required under the Code of Banking Practice to try to help its customers to overcorne their financial difficulties with any credit fac ility they have with us, provided the customer agrees to such assistance. If the National Credit Code hardship variation provisions could apply to a custorner's circumstances, ANZ must inform the custorner.

ANZ will assess the financ ial position of custorners experiencing hardship (either by obtaining a financial statement of position over the telephone or through other rneans such as mail, facsimle etc .) and will work with its custorners to identify the options available to them. ANZ will give genuine and appropriate consideration to repayrnent proposals and hardship variation applications made by custorners and we will endeavour to suggest other alternative arrangements that custorners' may not have identified or considered themselves . In the case of joint loan, ANZ will endeavour to work with both borrows on the loans contract . If one of the borrowers is disengaged, ANZ will continue to work with the engaged party to provide hardship assistance. Long term assistance will be limted to the engaged custorners ability to serve the current or restructured loan at corrmerc ial terms. ANZ's decisions will be confirmed to customers in writing, where appropriate.

Mainstream collection and legal activity is to be stopped for the duration that a custorner is being assisted for hardship (for further information refer to Effect of hardship notices on enforcement) :

ANZ is to recognise and respect a customer's appointment of an advisor (e .g. financial counsellor) and, if requested, deal directly with the advisor rather than dealing with the customer.

At ANZ the assessrnent of a custorner's ability to repay is determned by calculating an Uncorrmitted Monthly Incorne (UMI). For further information on the calculation of

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2375

Credit requirements! 17

income and expenses refer to the individual product credit requirements ( i.e Mortgage Credit Requirements, Small Business Credit Requirements, Personal Loan Credit Requirements, Consumer Cards Credit Requirements, Consumer Overdrafts Credit Requirements, or Asset Finance Credit Requirements ) . For details on t he ANZ's rrinirrum (default) consumer living expenses refer to Mortgage Credit Requirements .

National Credit Code Hardship Provisions

For the National Credit Code hardship variation provisions to apply, the customer rrust hold a regulated fac ility.

If a customer has a National Credit Code regulated fac ility, and ANZ is aware the customer is experiencing hardship, ANZ rrust inform the customer about the hardship variation provisions of the National Credit Code.

This means that, where the hardship provisions apply to a customer, ANZ rrust inform the customer of:

• the provisions and what they cover (see below for an extract); • their right to provide notice of hardship and require ANZ to consider an

arrangement or variation; and • their right to seek an order of the court or tribuna l varying the facility if ANZ

refuses

Section 72 of National Credit Code deals with financial hardship variation requests and states that :

"If a debtor considers that he or she is or will be unable to meet his or her obligations under a credit contract, the debtor may give the credit provider notice (a hardship notice), orally or in writing, of the debtor's inability to meet the obligations.

Further information:

Within 21 days after the day of receiving the customer's hardship notice, ANZ may give the customer a notice (verbally or in writing) requiring the customer to give ANZ spec ified information. ANZ rrust give the customer 21 days respond to the notice. The informat ion spec ified rrust be relevant to deciding :

(a) whether the customer is or will be unable to meet the customer's obligations under the contract; or (b) how to change the contract if the customer is or will be unable to meet those obligations.

ANZ need not agree to change the credit contract, if ANZ : • does not believe there is a reasonable cause (such as illness or unerrployment)

for the customer's inability to meet his or her obligations; or • reasonably believes the customers would not be able to meet his or her

obligations under the contract even if it were changed.

Notice of decision

If the customer makes an application for Hardship, ANZ rrust, give the customer a written not ice within the t imeframes detailed in the table below :

© Global Retail Credit Policy Team Ver 2013.09.13

18 Retail Collection Credit Requirements

(a) that states whether or not ANZ agrees to the change; and (b) if ANZ does not agree to the change- that states :

( i) the reasons for not agreeing to the change.

ANZ.800.508.2376

( ii) the name and contact details of the approved external resolution scheme of which ANZ is a member; and ( iii) the customer's rights under that scheme;

Scenario

1 ANZ does not require further information

2 ANZ requires further information but does not receive any information in coni>liance with the requirement

3 ANZ requires further information under the above section and receives information in coni>liance wit h the requirement

Period for giving notice:

21 days after receiving the hardship notice

28 days after ANZ's request for further information

21 days after receiving the additional information

Notice of change : Where ANZ and the customer agree to vary a credit contract under the hardship provisions of the National Consumer Credit Protection Act ANZ must provide written confirmation within 30 days of the agreement being reached setting out the teITT'IS of the agreement. Agreement may also be required from a guarantor, where relevant . Written confirmation must be provided by ANZ to the customer (and guarantor).

Effect of hardship notices on enforcement:

ANZ must not begin enforcement proceedings against the customer unless: • ANZ has given the appropriate hardship notice (refer Notice of decision - ANZ

does not agree to the change ) ; and • the period of 14 days, starting on the day ANZ gives the notice has expired

(refer Not ice of decision - ANZ does not agree to the change) .

Notes: • ANZ must allow the customer at least 30 days from the date of the default

notice to remedy the default . The 14- day period may end before, at the same time as, or after the end of the period for remedying the default specified in the default notice.

• ANZ may take possession of mortgaged goods if ANZ reasonably believes that : (a) the customer or mortgagor has removed or disposed of the mortgaged goods, or intends to remove or dispose of them, without ANZ's pernission; or (b) urgent action is necessary to protect the goods.

Code of Banking Practice hardship provisions

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2377

Credit requirements! 19

The Code of Banking Practice covers credit for investment and business purposes, in addition to credit for personal, household and domestic purposes.

Clause 25.2 of the Code of Banking Practice provides that : "With your agreement, we [ ANZ} will try to help you overcome your financial difficult ies with any credit facility you have with us. We could, for example, work with you to develop a repayment plan. If, at the time, the hardship variation provisions of the National Consumer Credit Protection Act could apply to your circumstances, we will inform you of them".

ANZ must meet its obligations under both the National Consumer Credit Protection Act and Code of Banking Practice.

Australian Government's hardship principles

In addition to the Nat ional Credit Code and the Code of Banking Practice, ANZ have agreed to adopt the Australian Government's hardship princ iples. For further details the government hardship princ iples can be accessed on the ABA's website.

ANZ's expectations of customers being assisted for hardship

Where ANZ agrees to a repayment arrangement, it will do so on the basis that the customer has agreed to:

• maintain their repayment arrangement or contact ANZ to advise of a change in their circumstances

• work with ANZ by contacting ANZ when their circumstances change and otherwise responding to ANZ's phone calls, messages and/ or letters when ANZ contacts them. If a customer does not continue to work with ANZ in relation to their arrangement as detailed above, mainstream collection processes are to be followed

Examples of Hardship Arrangements

Possible Hardship treatment options (but not limited to) are : • Periods of no Payments/ Partial Payments (Mortgages only);

• Arrears will continue to accrue over the period of no or partial payments; • Customers should be encouraged to make whatever repayments they can

afford to reduce the arrount or arrears owing at the conclusion of the period.

• Period can be no rrore than 3 consecutive rronths and • The customer must be < 90 DPD before the corrmencement of the period.

• Debt Consolidation Loans (Cards & Loans) : and • Balance Paydown Plans {Credit Cards)

Additional references

• ABA's financial hardship guidelines • Financial hardship application form • Financial hardship information on anz.com

©Global Retail Credit Policy Team Ver 2013.09.13

20 Retail Collection Credit Requirements

1.8 Impaired assets, provsioning and write-offs

On this page: • Credit reciuirement purpose • Irn:>aired facilities & provisioning • Calculation of individual provisions • Reviewing position • Reclassification from Impaired to Productive • Write-offs

Credit requirement purpose

To set the rules for t he treatrrent of impaired facilit ies, provisioning and write-offs

Individual Provision

An Individual Provision (IP) rrust be established on a faci lity where loss is expected. IP raised rrust cover any shortfall expected on an account.

ANZ.800.508.2378

The below table surrmarises at what point in tirre an Individual Provision is required on various portfolios; however, note exceptions as outlined below.

Facility Days Notes/ Exceptions Past Due

Credit Ca rdsl 180 IP is automatica lly establi s hed at 180 days in arrea rs; however, system cha rge-off occurs at 180 DPD as well thereby releas ing IP. Accounts may be ma nua lly cha rged-off at an earlier point in case of 1) bankruptcy, a nd 2) customer's pass ing (i.e. decea sed estates). Refer to Exception section

for further detail s on these scenarios .

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2379

Credit requirements! 21

Unsecured Loa ns2 120 IP may be assessed at 180 days in a rrears for a ccounts meeting the

fol I owi ng3 :

• Financia l Hardship, assessed or proven

• Wa iting for a n insura nce claim IP may be assessed at an earlier point in case of 1) bankruptcy, a nd 2) customer's pass ing (i.e. deceased estates). Refer to Exception section for

fu rther deta i Is on these scena rios .

Unsecured 120 IP may be assessed at an earlier point in case of 1) bankruptcy, a nd 2)

Overdrafts4 customer's pass ing (i.e. deceased estates). Refer to Exception section for

fu rther deta i Is on these scena rios .

IP not required if account is in dispute or where customer has lodged a compla int.

Mortgages5 90 IP may be assessed at an earlier point in case of 1) bankruptcy, a nd 2) customer's pass ing (i.e. deceased estates). Refer to Excepti on section for fu rther deta i Is on these scena rios .

Asset Fina nce 120 IP may be assessed at an earlier point in case of 1) bankruptcy, a nd 2) customer's pass ing (i.e. deceased estates). Refer to Excepti on section for fu rther deta i Is on these scena rios .

Secured Loans6 120 IP may be assessed at an earlier point in case of 1) bankruptcy, a nd 2) customer's pass ing (i.e. deceased estates). Refer to Excepti on section for fu rther deta i Is on these scena rios .

Secured 120 IP may be assessed at an earlier point in case of 1) bankruptcy, a nd 2)

Overdrafts7 customer's pass ing (i.e. deceased estates). Refer to Exception section for fu rther deta i Is on these scena rios .

IP not required if account is in dispute or where customer has lodged a

compla int.

Exceptions:

1. Bankruptcy and Liquidation

A customer can be deemed bankrupt either through Voluntary or Involuntary Bankruptcy. Unsecured and Secured debts of bankrupt customers are treated different ly . With Unsecured debts, creditors do not have the right to take possession of any property of the customer if the required payments are not met. For Secured fac ilit ies held by bankrupt customers, the bank will have rights - under the terms of the loan - regarding asset repossession if the debt is not paid.

Individual Provisioning triggers treatment will vary depending on the type of bankruptcy.

1.1. Bankruptcy

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2380

22 Retail Collection Credit Requirements

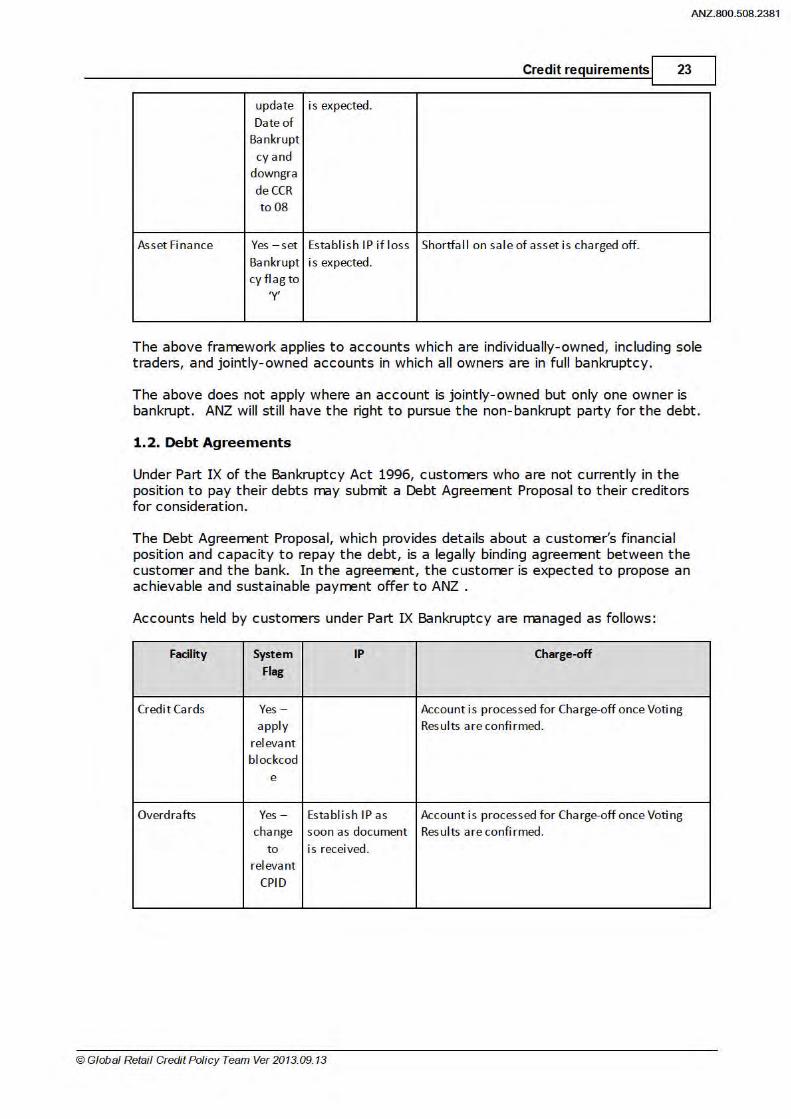

Unsecured fac ilities of customers who have fi led for bankruptcy under Part IV of the Bankruptcy Act 1996 rrust be provisioned as soon as relevant documents have been received from the Australian Financ ial Security Authority (AFSA) or the trustee and subsequently written off.

If fac ility is secured, an Individual Prov ision rrust be established if loss is expected. Treatment of t he security property will depend on the intention of the customer as advised by the trustee, that is - property t o be surrendered to the bank to cover debt or privately sold.

Upon receipt of relevant documents from AFSA or from the trustee, accounts in full bankruptcy are treated as follows:

Facility System IP Charge-off

Flag

Credit Ca rds Yes - Account is processed for Cha rge-off once document update is received. Date of

Ba nkrupt

cyand a pply

releva nt blockcod

e

Unsecured a nd Yes - Esta blish IP as Account is cha rged off immediately after IP is Secured update soon as document esta blished or wi thin a rea sona ble t ime fra me if Overdrafts Date of is received. system constra ints exist.

Ba nkrupt

cy a nd cha nge

to releva nt

CPID

Unsecured a nd Yes - Esta blish IP as Account is cha rged off immediately after IP is Secured Loa ns update soon as document esta blished or wi thin a rea sona ble t ime fra me if

Date of is received. system constra ints exist. Ba nkrupt

cy a nd cha nge

to releva nt

CPID

Mortgages Yes - Esta blish IP if loss Shortfa ll on sa le of asset is cha rged off.

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2381

Credit requirements! 23

update is expected. Date of

Ba nkrupt

cyand downgra de CCR to 08

Asset Fina nce Yes - set Esta blish IP if loss Shortfall on sa le of asset is cha rged off. Ba nkrupt is expected. cy flag to

'Y'

The above framework applies to accounts which are individually-owned, including sole traders, and jointly- owned accounts in which all owners are in full bankruptcy.

The above does not apply where an account is jointly- owned but only one owner is bankrupt . ANZ will still have the right to pursue the non-bankrupt party for the debt.

1.2. Debt Agreements

Under Part IX of the Bankruptcy Act 1996, customers who are not currently in the position to pay their debts may submit a Debt Agreement Proposal to their creditors for consideration.

The Debt Agreement Proposal, which provides details about a customer's financial position and capac ity to repay the debt, is a legally binding agreement between the customer and the bank. In the agreement, the customer is expected to propose an achievable and sustainable payment offer to ANZ .

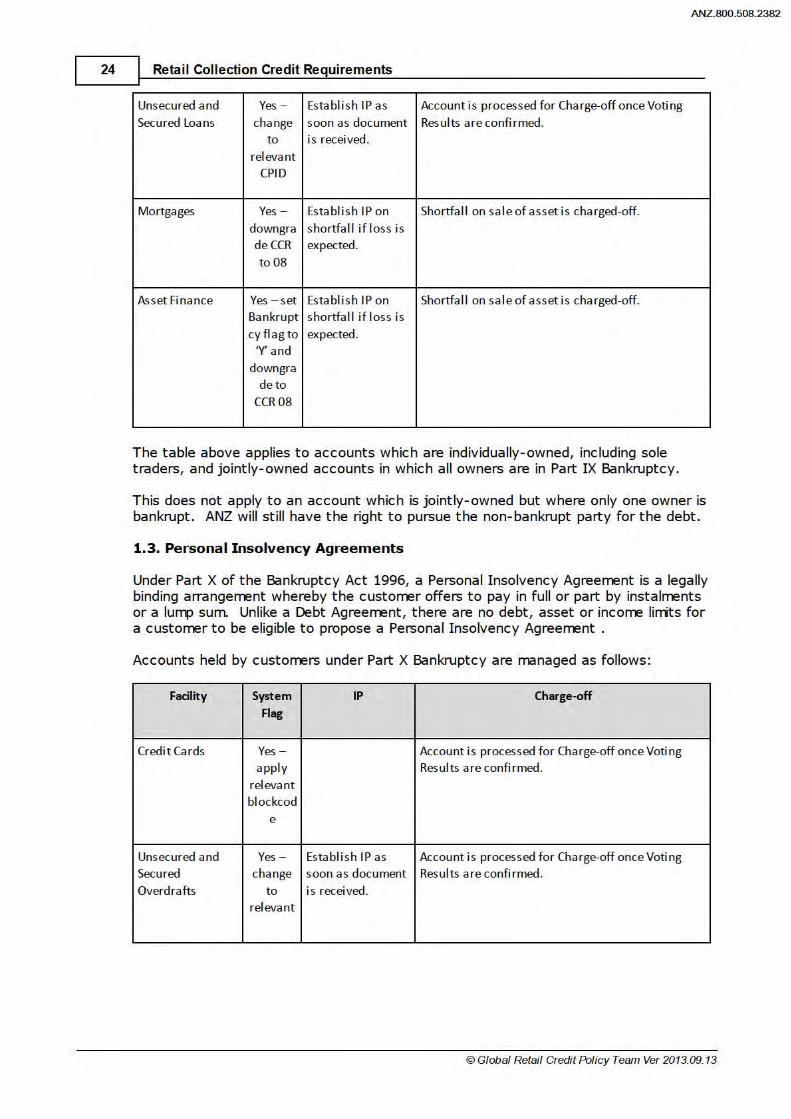

Accounts held by customers under Part IX Bankruptcy are managed as follows :

Facility System IP Charge-off

Flag

Credit Ca rds Yes - Account is processed for Charge-off once Voting apply Results a re confi rmed.

relevant blockcod

e

Overdrafts Yes - Establi s h IP a s Account is processed for Charge-off once Voting cha nge soon as document Results a re confi rmed.

to is received . relevant

CPID

©Global Retail Credit Policy Team Ver 2013.09.13

24 Retail Collection Credit Requirements

Unsecured a nd Yes - Establi s h IP a s Account is processed for Charge-off once Voting

Secured Loans cha nge soon as document Results a re confi rmed. to is received .

relevant CPID

Mortgages Yes - Establi s h IP on Shortfa ll on sal e of a sset is charged-off.

down gr a s hortfa ll if loss is de CCR expected. to 08

Asset Fina nce Yes - set Establi s h IP on Shortfa ll on sal e of a sset is charged-off. Bankrupt s hortfa ll if loss is cyflagto expected.

'Y' a nd

down gr a de to

CCR08

The table above applies to accounts which are individually- owned, inc luding sole traders, and j ointly- owned accounts in which all owners are in Part IX Bankruptcy.

ANZ.800.508.2382

This does not apply to an account which is j ointly- owned but where only one owner is bankrupt . ANZ will still have the right to pursue the non-bankrupt party for the debt.

1.3. Personal Insolvency Agreements

Under Part X of the Bankruptcy Act 1996, a Personal Insolvency Agreement is a legally binding arrangement whereby the customer offers to pay in full or part by instalments or a lurrp sum. Unlike a Debt Agreement, there are no debt, asset or income lirrits for a customer to be eligible to propose a Personal Insolvency Agreement .

Accounts held by customers under Part X Bankruptcy are managed as follows:

Facility System IP Charge-off

Flag

Credit Ca rds Yes - Account is processed for Cha rge-off once Voting apply Res ults are confi rmed.

releva nt blockcod

e

Unsecured a nd Yes - Esta blish IP as Account is processed for Cha rge-off once Voting Secured change soon as document Res ults are confi rmed. Overdrafts to is received.

releva nt

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2383

Credit requirements! 25

CPID

Unsecured a nd Yes - Esta blish IP as Account is processed for Cha rge-off once Voting

Secured Loans change soon as document Results are confi rmed. to is received.

releva nt CPID

Mortgages Yes - Esta blish IP if loss Shortfall on sa le of asset is cha rged-off.

downgra is expected. de CCR to 08

Asset Fina nce Yes - set Esta blish IP if loss Shortfall on sa le of asset is cha rged off. Ba nkrupt is expected. cy flag to

'Y' and downgra

de to CCR08

1.4. Bankruptcy pending AFSA Documents

In case a customer notifies ANZ of bankruptcy but relevant documents have yet to be received, applicable flags to ident ify these customers as potent ially bankrupt must be placed. Where system linitations exist, flags which can be ut ilised as triggers to prevent further lending activities must be placed on these accounts.

Facility System Notes

Flag

Credit Ca rds Yes - Apply charge-off guideline per bankruptcy type a s soon a s document is apply received or Voting results are confi rmed. If no document or advise from

releva nt Trustee is received after 2 weeks of notification, account must be moved blockcod o ut of Ba nkruptcy queue a nd sta ndard Coll ections guideli nes wi 11 apply.

e

Unsecured a nd Yes - Apply provis ioning guideline per bankruptcy type a s soon a s document Secured apply is received. Overdrafts releva nt

flag to Apply relevant charge-off guideline per bankruptcy type a s soon a s

exclude document is received or Voting res ults are confi rmed.

account If no document or advise from Trustee is received after 2 weeks of

from standard

notification, account must be moved out of Bankruptcy queue and

Coll ectio sta ndard Coll ections guidelines wi ll apply.

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2384

26 Retail Collection Credit Requirements

ns

act ivity

Unsecured and Yes - Apply provisioning guideline per bankruptcy type as soon as document Secured Loans apply i s received.

relevant flag to Apply relevant charge-off guideline per bankruptcy type as soon as

exclude document is received or Vot ing res ults are confi rmed .

account If no document or advise from Trustee is received after 2 weeks of

from standa rd

notification, account must be moved out of Bankruptcy queue and

Coll ectio standard Coll ections guidelines wi ll apply.

ns

act ivity

Mortgages Yes - Apply provisioning guideline per bankruptcy type as soon as document change i s received.

to CCR 08 if Apply relevant charge-off guideline per bankruptcy type as soon as

account document is received or Vot ing res ults are confi rmed .

i s in If no document or advise from Trustee is received after 2 weeks of

arrea rs notification, account must be moved out of Bankruptcy queue and

standard Coll ections guidelines wi ll apply.

Asset Finance Yes - set Apply provisioning guideline per bankruptcy type as soon as document Ba nkrupt i s received.

cy flag to 'Y' in Apply relevant charge-off guideline per bankruptcy type as soon as

system if document is received or Vot ing res ults are confi rmed .

account If no document or advise from Trustee is received after 2 weeks of

i s in notification, account must be moved out of Bankruptcy queue and

arrea rs standard Coll ections guidelines wi ll apply.

1.5. Liquidations

When a corrpany goes into liquidation, ANZ will receive notification from the liquidator. Upon receipt of notification, appropriate restraints in system must be set .

Thirty days after receiving notice from liquidators or if an account in liquidation is 30 days in arrears - whichever comes first - an Individual Provision must be assessed and established on the account.

If an account is unsecured or if secured by a guarantee, full Individual Provision must be raised. If an account is secured, IP to be established must cover any shortfall once security is sold and proceeds of the sale applied to the principal arrount, interest and fees, and any other expenses.

Unsecured accounts and accounts which are secured by a guarantee will be charged-

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2385

Credit requirements! 27

off 30 days - at most - after IP has been established if the account is not required for liquidation. Otherwise, account is to be charged off once liquidation is corrpleted or as soon as account is no longer required for liquidation purposes.

Secured accounts are to be processed for charge-off if it meets at least one of the following conditions : 1. The debt, or a portion of the debt, is deemed unrecoverable. 2. Debt is considered fully accelerated. 3. Directors of a corrpany in liquidation will only be pursued if they are guarantors of

the account.

2. Deceased Estates

Once ANZ is notified of a customer's passing, accounts held by deceased customers rrust be flagged in system as applicable to enable appropriate Collections management.

If the deceased person is the primary owner of the debt, any outstanding amount becomes the liability of the deceased estate. Sirrilarly if the deceased is a guarantor, the estate is still liable under the guarantee and remains liable until either all of the lending or obligations secured by the guarantee have been met or ANZ has given the guarantor's estate a written release.

For unsecured credit cards, overdrafts and loans - both consumer and commerc ial -the deceased person's account rrust be provisioned and subsequent ly charged- off upon receipt of documents, or at 120 days for Personal Loans and DDAs, or at 180 days for credit cards, whichever comes first .

ANZ will exerc ise its right over security asset for secured debts. Provisioning and charge-off on shortfall will apply as per policy.

If the deceased estate is insolvent, the executor is required to complete and send a statutory declaration to ANZ. Any shortfall must be provisioned and subsequently charged off as per policy.

Any new lending in the name of a deceased estate rrust be referred to Retail and Business Credit Assessment .

Credit Risk Rating (CCR) Downgrades Once an account falls in the category of 90 days past due (excess or arrears) or where there is doubt about timely repayment of princ ipal, interest and fees being achieved the CCR must be downgraded to CCR 08. Upon downgrade an appropriate assessment must be completed to deterrrine : • whether the fac ility is well secured; • if not well secured, whether an individual provision needs to be established, and if so further downgrade to CCR 09 or 10 is required

If a material adverse change in the customer's ability to repay becomes evident, the credit faci lity is to be reviewed for possible downgrade irrmediately. Notwithstanding the above risk grading trigger points if an account is deterrrined to be at risk of loss of either princ ipal or interest, it is to be downgraded to CCR 09 or 10 e.g. bankruptcy.

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2386

28 Retail Collection Credit Requirements

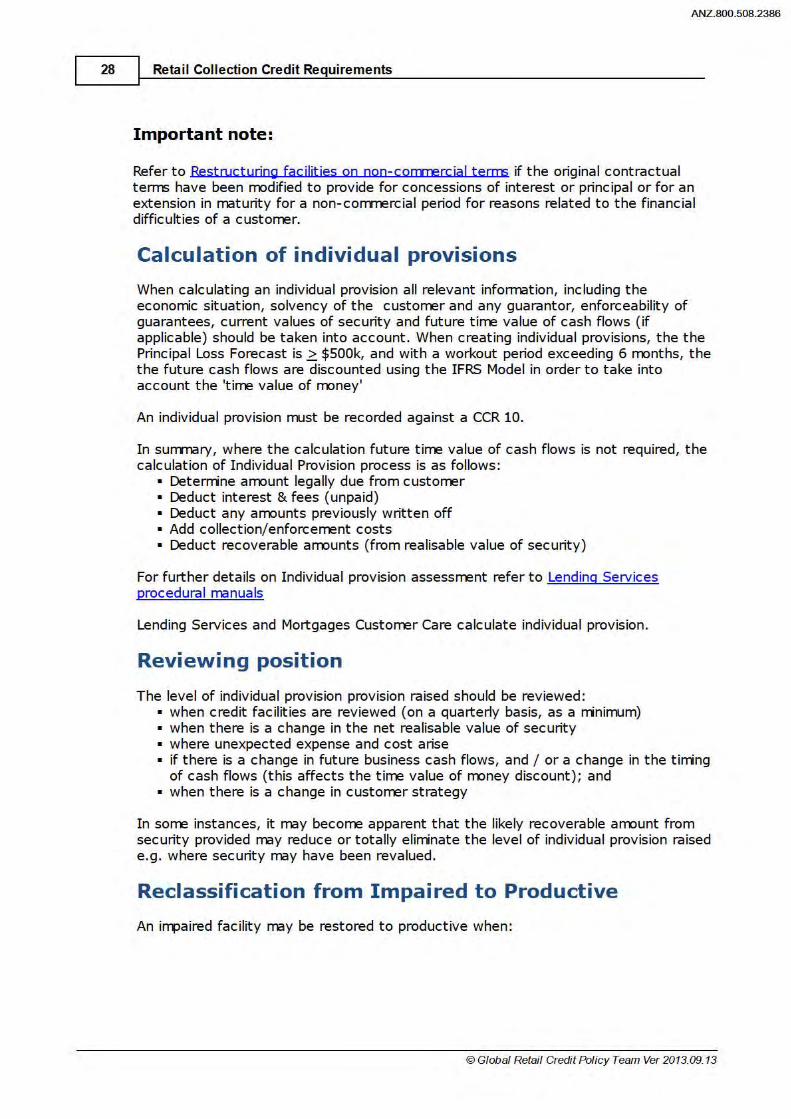

Important note:

Refer to Restructuring facilities on non-comrrercjal terms if the original contractual terms have been modified to provide for concessions of interest or princ ipal or for an extension in maturity for a non- commercial period for reasons related to the financial difficulties of a customer.

Calculation of individual provisions

When calculating an individual provision all relevant information, including the economic situation, solvency of the customer and any guarantor, enforceability of guarantees, current values of security and future time value of cash flows ( if applicable) should be taken into account. When creating individual provisions, the the Principal Loss Forecast is > $500k, and with a workout period exceeding 6 months, the the future cash flows are discounted using the IFRS Model in order to take into account the 'time value of money'

An individual provision must be recorded against a CCR 10.

In summary, where the calculation future t ime value of cash flows is not required, the calculation of Individual Provision process is as follows:

• Deterrrine amount legally due from customer • Deduct interest & fees (unpaid) • Deduct any amounts previously written off • Add collection/ enforcement costs • Deduct recoverable arrounts (from realisable value of security)

For further details on Individual provision assessment refer to Lending Services procedural manuals

Lending Services and Mortgages Customer Care calculate individua l provision.

Reviewing position

The level of individual provision prov ision raised should be reviewed : • when credit fac ilities are reviewed (on a quarterly basis, as a rrinimum) • when there is a change in the net realisable value of security • where unexpected expense and cost arise • if there is a change in future business cash flows, and I or a change in the tirring

of cash flows {this affects the time value of rroney discount) ; and • when there is a change in customer strategy

In some instances, it may become apparent that the likely recoverable arrount from security provided may reduce or totally eliminate the level of individual provision raised e.g. where security may have been revalued.

Reclassification from Impaired to Productive

An irrpaired faci lity may be restored to productive when :

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2387

Credit requirements! 29

• at least one of the following is satisfied : - it is fully colll'liant with the original tenns and conditions - it has been restructured and meets the criteria for classification of a restructured faci lity as productive (refer restructuring facilities on noncommercial terms) . - if illl'aired due to 90 days past due, all unpaid amounts have been reduced to

an amount less than 90 day's worth of payments provided the payment of arrears has not resulted from a further advance from ANZ

• and all of the following are satisfied: - if the fac ility was c lassified as illl'aired as a result of write- offs, the faci lity has been fully perforrring for six months or three payment cycles, which ever is greater - ANZ believes that the customer is capable of fully servicing its future obligations - ANZ is no longer maintaining an individual provision - if the fac ility is not well secured, drawings have returned within approved lirrits, or the fac ility becomes well secured.

This credit requirement should be read in conjunction with the credit requirement entitled Upgrading a Customers Credit Rating.

Write-offs

Once enforceable security has been realised, a debt or part of debt should be written off if, on the basis of commercial assessment, there is no reasonable expectation of further recovery . Write-off is subject to approval by a CAD holder (or divisional credit requirement) explicitly authorised to approve write-offs .

Partial write-offs

A portion of, but not all, outstanding may be written off where all known repayment sources are insuffic ient to pay an agreed interest rate and repay the total principal and interest over a reasonable period of t ime, and all of the following applies;

• reasonable steps have been taken to realise all tangible security • the maxirrum potential recovery is clearly established by current valuations • the shortfall to be written off is c learly identified as being irrecoverable.

Personal Loans:

A Personal Loan product is written off at the point of either being sold or assigned to a debt purchaser after the point of provision.

Credit Cards :

Credit Cards are written off automat ically by Vision +at 180 dpd.

1 Includes Consumer and Commerc ial credit cards . 2 Includes all consumer and commercial unsecured loans.

©Global Retail Credit Policy Team Ver 2013.09.13

30 Retail Collection Credit Requirements

3 IP trigger at 180 DPD for accounts in Financial Hardship and with insurance claim only applies to Personal Loans; SBB unsecured loans in Financ ial Hardship rrust be provisioned at 120 DPD. 4 Includes all consumer and corrmercial unsecured overdrafts. 5 Includes all residential and corrmercial rrortgages and overdraft equity manager fac ilities. 6 Refers to corrmerc ial secured loans. 7 Refers to corrmerc ial secured overdrafts .

1.9 Insurance

On this page: • Credit reciuirement purpose • Minimum building insurance reciuirements

Credit requirement purpose

It is a requirement of the bank and regulatory authorities that all items held as security and extended for value, including real property assets (other then vacant land), rrotor vehicles and business chattels are adequately insured.

Minimum insurance requirements

The Bank's mnirrum insurance requirements are :

• For all items taken as security obtain evidence of insurance and place on the customer fi le

ANZ.800.508.2388

• For customers CCR 70 and worse ( i.e. Collections) evidence of insurance rrust be obtained annually and placed on the customer fi le (i.e . property/ business chattels etc . continues to be insured and ANZ interest is noted)

Documentary evidence:

1. Non Strata Title Properties (properties):

Evidence of insurance# may be provided v ia: • Building insurance policy • Certificate of currency • Cover note • email/ letter from the insurer, broker and/ or agent

2. Strata Title Properties (i.e: multi dwellings/ apartments):

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2389

Credit requirements! 31

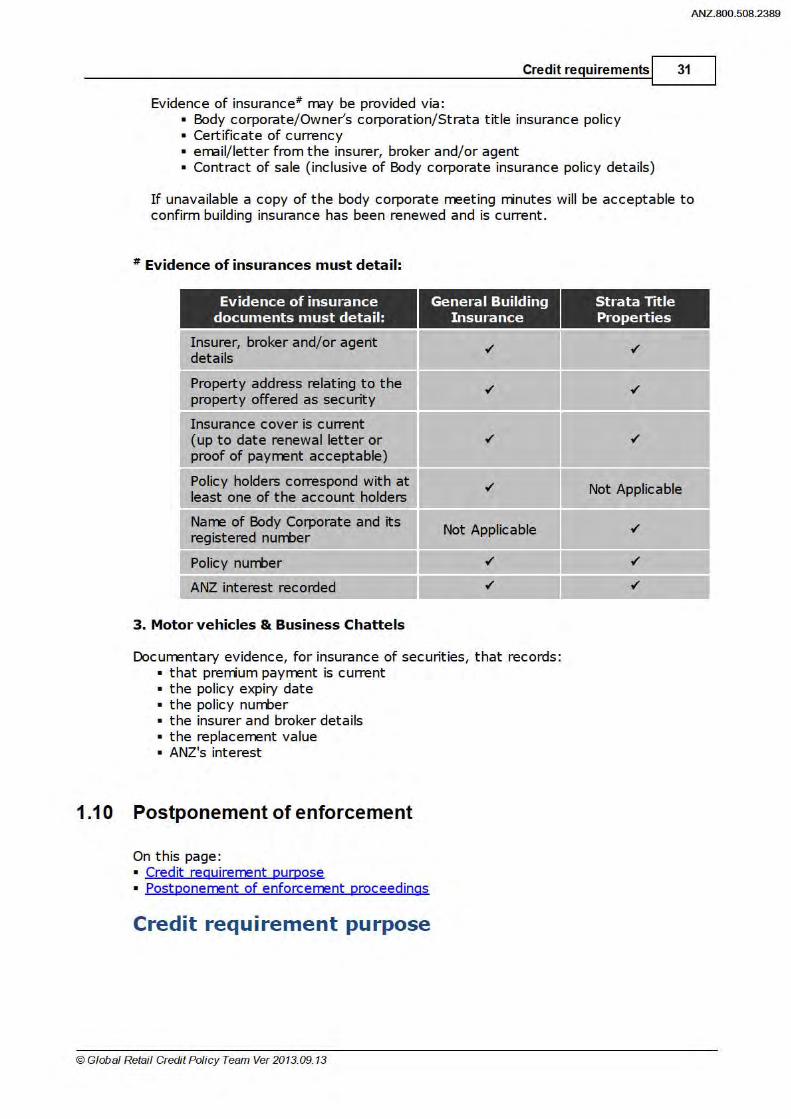

Evidence of insurance# may be provided v ia: • Body corporate/ Owner's corporation/ Strata t itle insurance policy • Certificate of currency • email/ letter f rom t he insurer, broker and/ or agent • Contract of sale ( inclusive of Body corporate insurance policy details)

I f unavailable a copy of the body corporate meeting rrinut es will be acceptable to confirm building insurance has been renewed and is current .

# Evidence of insurances must det a il:

Evidence of insurance General Building Strata Title documents must detail: Insurance Properties

Insurer, broker and/ or agent ./ ./ details

Property address relating to the ./ ./ property offered as security

Insurance cover is current (up to date renewal letter or ./ ./

proof of payment acceptable)

Policy holders correspond with at ./ Not Applicable least one of the account holders

Name of Body Corporate and its Not Applicable ./

registered nurrber

Policy nurrber ./ ./

ANZ interest recorded ./ ./

3. Motor ve hicles St Business Chattels

Documentary evidence, for insurance of securities, that records : • that prerrium payment is current • the policy expiry date • the policy nurrber • the insurer and broker details • the replacement value • ANZ's interest

1.1 O Postponement of enforcement

On this page: • Credit requirement purpose • Postponement of enforcement proceedings

Credit requirement purpose

©Global Retail Credit Policy Team Ver 2013.09.13

32 Retail Collection Credit Requirements

This credit requirement provides guidance on postponement of enforcement proceedings or any action taken under such proceedings or t he operat ions of any applicable acceleration clause

Postponement of enforcement proceedings

ANZ.800.508.2390

Under National Credit Code a customer or a guarantor who has been given a default notice or demand for payment may, at any time before the end of the period spec ified in the notice or demand, request ANZ to negotiate a postponement of the enforcement proceedings or any action taken under such proceedings or the operations of any applicable acceleration clause.

ANZ rrust provide a customer I guarantor a writ ten notice within 21 days after receiving the request that states whether or not ANZ agrees to negotiate a postponement. If ANZ does not agree to negotiate, the writ ten notice rrust state :

• the name of the approved external resolution scheme of which ANZ is a merrber; • the customer's I guarantor's rights under that scheme; and • the reasons for not agreeing to negotiate.

Once an agreement has been reached on the postponement, ANZ rrust give written notice of the conditions of the postponement not later than 30 days from the date of agreement. The notice rrust set out the consequences if the conditions are not complied with .

Note : ANZ will, as a matter of practice, send only one notice wit hin 21 days of the request incorporating both ANZ's agreement to negotiate and the conditions of the postponement.

The default notice or demand for payment is taken not to have been given if a postponement is negotiated with ANZ and the customer or guarantor complies with the conditions of postponement.

1.11 Problem credit management

On this page:

• Credit requirement purpose • Problem credit management • Segmentation I transfer of control of customers

Credit requirement purpose

Set t he rules as to when a small business fi le is to be transferred to Lending Services

Problem credit management

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2391

Credit requirements! 33

For Lending Services processes, procedures and guidelines refer to Lending Services Max site

Segmentation / transfer of control of customers

Transfer to Lending Services can be deferred until 120 days from the date of risk grade downgrade (subject to the appropriate CAD holder confirmation) where;

• approved processes are being followed; and • accounts are being managed by the centralised collections teams in line with

approved collections strategies; and • no other adverse information is known about the account, customer or any

entity within the group e.g. problems with creditors, etc .

1.12 Re-aging (Consumer credit cards only)

On this page: • Credit requirement purpose • Definition of re-aging (consumer credit cards) and loan extensions • Re- aging (consumer credit cards)

Credit requirement purpose

This requirement outlines the Re- aging (Consumer Credit Cards) criteria .

Definition of re-aging

Re- aging is a process of forgiving delinquencies of an account that has met certain criteria . Account undergoing re- aging process will have its delinquent status converted to normal (current) .

Re-aging (Consumer credit cards )

Counting of davs past due

For credit cards, the Bank starts counting past due I delinquency from the next cycle (statement date) after payment is not obtained by due date.

©Global Retail Credit Policy Team Ver 2013.09.13

34 Retail Collection Credit Requirements

Cy de date

Due date

Day 1 delinquency

Cy de date

• 1-29 days delinquent = mssing 1 payment cycles • 30-59 days delinquent = mssing 2 payment cycles

Auto Re-aging

Automatic Re- aging feature is used in V+ CMS with the following criteria :

ANZ.800.508.2392

• Number of required consecutive payments: Account has to have at least six payments in the last six consecutive months

• Minimum payment amount: The 6 payments should be at least enough to prevent the account from slipping to the next delinquency bucket

• Minimum age of accounts: The mnimum months on book for account to qualify for auto re-aging is 9 months {Note : this is not reset as parameter but as a consequence of the mnimum delinquency level requirement)

• Frequency of re-aging: Account is only allowed to have one automatic re- aging every 12 months and 2 in 5 years

Automatic Re- aging is done by Vision+ and does not requires approvals.

Manya! Re-aging

Manual re- aging is re-aging done without meeting the criteria of Auto Re-aging. Manual Re-aging is reserved for spec ial cases and should be treated as deviat ion.

Approval

Team Leader Collections or higher officer in Collections should approve manual reaging.

Conditions allowing manual re -aging

Manual Re-aging is only allowed under the following circumstances : • Delinquency was caused by disputed I fraudulent transactions found in the

customer's favour. • Customer has pre-funded the credit card account (eg : to travel overseas) in

order to skip payment. Customer does not know that pre-funding will still require payment as per usual. In such a situation re-aging is done as a good will gesture.

• Customer has CardPay Direct set with the bank. However, due to incorrect setup, payment fails to draw. Re-aging will be executed whilst customer is required to make manual payment.

• Any bank's error that results in delaying of cheque processing. In this situation, re- aging is executed after cheque payment is presented.

Reporting of Re-aged Accounts

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2393

Credit requirements! 35

Re- aged accounts and balances are reported under "current/ normal" accounts.

A report on re-aged accounts is produced monthly . The report identifies manual from auto re- aged accounts.

The report is used by the following areas: • Collections for their regular QA by Tls I Managers • Collections - to change block codes • Credit Risk Management for Credit Risk Compliance Review • All other oversights ( eg : Audit , Operating Risk etc)

Deviation

Any deviation to this credit requirement is to be approved by Senior Manager Collections or higher officer in the Credit chain.

1.13 Re-aging , loan extensions and defferals

On this page: • Credit requirement purpose • Re-aging. loan extensions and deferrals (Mortgage products only) • Re-aging. loan extensions and deferrals (Personal loans only)

Credit requirement purpose

This requirement outlines the re-aging, loan extension and deferral criteria .

Re-aging, loan extensions and deferrals (Mortgage products only)

©Global Retail Credit Policy Team Ver 2013.09.13

36 Retail Collection Credit Requirements

One of the options available to customers to recover from their arrears position is capitalisation.

Capitalisation refers to the process of capitalising the arrears owing into the loan balance and either:

• increasing the periodic repayments so that the loan clears within the original term; or

• extending the loan term.

To qualify for Capitalisation, the following criteria rrust be met :

ANZ.800.508.2394

• Loan serviceability rrust be proven by making regular scheduled repayments over a period of at least 6 months (No one off lump sum payment allowed) :

• A customer rrust have confirmed that they believe their reasons for not servic ing their loan have been overcome at the beginning of the trial.

• The serviceability trial will be conducted according to the advice of the collections officer, to be confirmed in a letter sent to the customer. A new repayment schedule for the loan will be issued at the successful completion of the tria l.

• If, in the opinion of a collect ions officer, the customer has failed to complete, or can not continue with, the Serviceability Trial, the customer will be exited from the tria l to Standard Collections. Capitalisation will not be an option for the customer for another 6 months.

• If the customer is in Hardship, subsequent attempts to satisfy the Capitalisation criteria may be attempted given the approval of a Senior CAD holder.

• Loan term can not be extended more than 30 years from original drawdown date. If the fac ility has been refinanced, the refinancing date will apply.

• Loans with LMI can only have their loan extended under the loan extension criteria established for Hardship customers (Hardship policy - LMI customers have a payment deferral option, no loan extension) .

• Agreement required from all borrowers to proceed with capitalisation of arrears. • Loan rrust be a Principle and Interest Term Loan ( i.e. not Interest Only or EMA)

and >9 Months on Book. • Loan rrust not have attempted or received arrears capitalisation more than once

every 12 months and a maxirrum of twice in 5 years . • No Additional funds or increased linit may be advanced to finance unpaid interest

and fees to enable new payment. • Should a customer fai l to meet the criteria above, the customer's arrears may

still be capitalised at the approval of a Senior CAD holder ("CAD F").

Repayment Holiday:

A Repayment Holiday is prov ided on the basis that the customer will be in a position to make up the nissed repayments at the end of the repayment holiday period. At the end of the Repayment Holiday, repayments are increased to ensure that the loan is paid in full within the agreed term Alternat ively , the customer may elect to repay the Repayment Holiday amount in a lump sum at the end of the three months. For further informat ion refer to Repayment holiday Max site

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2395

Credit requirements! 37

Further Information:

For further infonration on Loan extensions & Mortgage deferrals refer to Collectjon Max site.

Re-aging, loan extensions and deferrals (Personal loans only)

Payment extension is a tool that can be used by collections on accounts that have demonstrated a willingness to pay an ability to meet the scheduled loan repayments but are unable to get on top of the full outstanding arrears amount .

In what situations can a payment extension be offered?

• The customer has made 6 months worth of consecutive payments (monthly payment, in full) .

• Payment extension can only be taken up 1 t ime in 12 months and 2 times in 5 years .

• Loan m.Jst be more than 9 months old. In special c ircumstances, a loan account less than 9 months old may be approved by the appropriate CAD level.

• The account can be up to 179 days delinquent and is classed as a perforrring loan.

• Any account over 179 days delinquent and is classed as perforrring can be sent through to Credit Risk or Head of Collections/ Customer Connect for approval, if it is believed to have special c ircumstances i.e Hardship.

• Only team leaders or their duly designated staff member are able to provide final approval for a payment extension arrangement . They will need to check for notes in the system, to ensure that an extension has not previously been granted.

What the policy offers:

• Payments can be extended up to a maximum of six months. The maxim.Jm extension period cannot be greater than current days past due, to a maximum of 6 months. That is, if t he account is in early day collections ( <60 days delinquent) then a maxim.Jm of j ust two months can be offered. Most Team Leaders I Senior Officers can approve and post an extension up to 3 months or the equivalent . Operations Managers can approve an extension of up to 6 months. Head of Collections and Personal Loans can approve 12 months extensions, even if account above 180 days.

• The additional payments must be paid at the end of the loan. • The customer m.Jst continue to make their regular scheduled payments, without

any temporary repayment 'holiday' being offered. • As the days delinquent will drop back to zero, the account will move out of

collections and stop receiving collection contact .

Notes on Operational Procedure:

• A note will need to be entered into the system identifying that the extension has been done.

©Global Retail Credit Policy Team Ver 2013.09.13

38 Retail Collection Credit Requirements

• The automatically generated letter includes a line to "sign and date" the agreement and return as confirmation. This line is to be crossed out before mailing to the customer, as the extension has already been agreed to.

• The automatically generated letter is to be handed to the team leader or their duly designated staff merrber for final sign off approval.

ANZ.800.508.2396

• It is the team leaders responsibility to conduct basic QA on accounts, to ensure Credit Policy is adhered to . This must be done on a nightly basis, such that the account details can be reviewed prior to the account dropping off CT A.

• There are to be no "up front " extension in accordance with APRA guidelines".

Further Information

For further informat ion on Loan extensions & deferrals refer to Collection Max site

1.14 Repayment arrangements

On this page: • Credit reciuirement purpose • Scope and purpose • Promise to pay I Short term arrangements • Long term repayment arrangements

Credit requirement purpose

This credit requirement sets the rules and provides guidance to staff responsible for agreeing customer repayment arrangements.

Important Note: For regulated fac ilities captured under the National Consumer Credit Code this credit requirement should be read in conjunction with Hardship credit requirements . Products which are regulated include home loans, personal loans, credit cards, consumer leases, overdrafts, line of credit accounts and investment property loans ( including Commerc ial product) among other products and services.

Scope and purpose

Long term repayment arrangements are arrangements which are firm, well structured agreements in writing with customers or their 3rd party representatives to clear arrears on delinquent accounts. They are distinct from Prorrise to pay (short term arrangements), which are verbal undertakings (promses) given by customers to clear early day arrears or excesses.

Repayment arrangements may only be accepted by authorised staff responsible for collection activity on credit faci lities that are in arrears.

Repayment arrangements are discussed with a customer or their authorised 3rd party representative and, if appropriate, accepted by ANZ and the customer. ANZ accepts repayment arrangements on the basis that it will pursue its right to pursue collection action should the customer not honour the arrangement.

© Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2397

Credit requirements! 39

Promise to pay / Short term arrangements

Important note: For regulated faci lities this credit requirement should be read in conjunction with Hardship credit requirements

Promises to pay (PTP) or short term arrangements are verbal cornnitments or declarations by customers that a payment or series of payments (must not exceed 90 days) will be made within an agreed t imeframe to clear arrears I overlimits I excesses. Promises to pay or short term arrangements may only be accepted by staff responsible for collection activity on credit fac ilities that are in arrears. In rrost cases this will be staff in centralised collections areas.

PTPs are discussed with a customer or their authorised 3rd party representative and, if appropriate, accepted by ANZ and the customers . ANZ accepts PTPs or short term arrangements on the basis that it will pursue its right to pursue collection action should the customer not honour the arrangement. The source of clearance and relevant issues must be documented in a diary note.

As the arrangements are less than 90 days it is not a requirement to confirm these agreements in writing, except where a customer has been given a default notice or demand for payment and requests ANZ to negotiate a postponement of the enforcement proceedings (refer to Postponement of enforcement proceedings requirement ).

Long term repayment arrangements

Important note: for regulated fac ilities this credit requirement should be read in conjunction with Hardship credit requirements

Long term repayment arrangements are arrangements which are firm, well structured agreements in writing with customers or their 3rd party representatives to clear arrears on delinquent accounts.

The following criteria, applicable to all types of ANZ credit faci lities, must be met for ANZ to consider a long term repayment arrangement :

• Capacity and intention to repay must be evident {This can be established in a number of ways. For example, a customer's income and expenditure or other sources of repayment as well as past account history and credit reports can be indicators of capacity and will ingness to repay . For deceased customers, this will be applicable to the deceased customer's estate) .

Assessing whether a repayment arrangement meets the above criteria will largely be a judgemental decision. Reasons for accepting an arrangement must therefore be documented.

Where a customer, irrespective of the number of days in arrears or excess, satisfies the Hardship or Insurance Claims credit criteria, an arrangement may be accepted that does not meet the Long term repayment arrangement criteria .

For criteria on hardship refer to Hardship credit requirements

©Global Retail Credit Policy Team Ver 2013.09.13

ANZ.800.508.2398

40 Retail Collection Credit Requirements

Other exception :

13 Credit insurance claims