Embed Size (px)

Citation preview

PUBLIC

Retail Banking Solutions

Merchant Instruction Manual

Your complete reference to program features and operating guidelines.

PUBLIC - 2

TABLE OF CONTENTS

1.0 COMPLIANCE WITH LEGISLATION .............................................. 7

1.1 Anti-Money Laundering ...................................................................................................... 7

1.2 Anti-Bribery & Corruption ................................................................................................... 8

2.0 CONTACT DETAILS .................................................................... 11

2.1 Merchant Contact Information ......................................................................................... 11

2.2 Customer Contact Information ......................................................................................... 11

3.0 INTRODUCTION TO HSBC ........................................................ 12

3.1 HSBC Bank Overview ........................................................................................................ 12

3.1.1 An introduction to HSBC - The world's local bank .............................................................. 12

3.1.2 HSBC Bank in Australia ....................................................................................................... 12

3.2 HSBC Product Overview .................................................................................................... 13

3.2.1 Introduction to HSBC flexible payment options .................................................................. 13

3.2.2 Products .............................................................................................................................. 13

3.3 HSBC VISA Classic Credit Card - Overview .......................................................................... 14

3.3.1 HSBC VISA Classic Credit Card – at a glance ....................................................................... 15

3.4 HSBC Promotional Terms .................................................................................................. 16

3.4.1 Interest free with payments (IF): HSBC Visa Classic Credit Card ......................................... 16

3.4.2 Interest free payment deferred (PD): HSBC Visa Classic Credit Card .................................. 16

3.4.3 Hybrid promotions: Interest Free & Payment Deferred Combinations ............................... 16

3.5 HSBC Visa Classic Credit Card – Product Information ......................................................... 17

3.5.1 Interest rate ........................................................................................................................ 17

3.5.2 Statements .......................................................................................................................... 17

3.5.3 Repayments ........................................................................................................................ 17

3.5.4 Easy Payment Options ........................................................................................................ 17

3.5.5 Card and PIN ....................................................................................................................... 18

3.5.6 Multiple promotions and transactions ............................................................................... 18

3.5.7 Card Activation ................................................................................................................... 18

3.5.8 Standard Visa purchases..................................................................................................... 18

3.5.9 Credit Limit Increase for Existing Cardholders .................................................................... 18

4.0 HSBC CONNECTED ................................................................... 19

4.1 Features and Functionality ............................................................................................... 19

4.2 Access .............................................................................................................................. 19

PUBLIC - 3

4.3 Software & Hardware Requirements................................................................................. 19

5.0 HSBC CONNECTED – MERCHANT INFORMATION ...................... 20

5.1 User Access Information ................................................................................................... 20

5.2 Merchant Passwords / Login Details ................................................................................. 21

5.2.1 Passwords ........................................................................................................................... 21

5.3 Tips for using HSBC Connected .......................................................................................... 22

6.0 HOW TO LOG INTO HSBC CONNECTED ..................................... 23

6.1 Logging in to Connected ................................................................................................... 23

6.2 Logging off ....................................................................................................................... 24

7.0 HSBC CONNECTED SUMMARY SCREENS ................................... 25

7.1 Application Manager ........................................................................................................ 25

7.1.1 Search for an Existing Instore Application or Add On ......................................................... 25

7.1.2 Retrieve an Application ....................................................................................................... 26

7.2 Application Summary ....................................................................................................... 27

8.0 APPLY FOR HSBC VISA CARD VIA HSBC CONNECTED................. 28

8.1 HSBC ID Requirements ...................................................................................................... 28

8.2 Card Pre - Application ....................................................................................................... 29

8.2.1 Eligibility & Privacy ............................................................................................................. 29

8.2.2 HSBC Pre-Application Checklist ........................................................................................... 30

8.2.3 Purchase Details ................................................................................................................. 31

8.3 Application Details ........................................................................................................... 32

8.3.1 Customer Details ................................................................................................................. 32

8.3.2 Address & Phone Number Details ....................................................................................... 33

8.3.3 Employment Details ............................................................................................................ 33

8.3.4 Financial Details .................................................................................................................. 35

8.3.5 Review and Submit ............................................................................................................. 37

8.4 Overview of HSBC VISA Classic Credit Card Application Process ......................................... 39

9.0 APPLICATION DECISIONS ......................................................... 40

9.1 Approved Decision ........................................................................................................... 40

9.2 Pending Decision .............................................................................................................. 41

9.2.1 Pending ID ........................................................................................................................... 41

9.2.2 Pending Other ..................................................................................................................... 42

9.3 Declined Decision ............................................................................................................. 42

PUBLIC - 4

9.4 Summary of Documentation required for a New Application ............................................. 43

10.0 PROCESSING AN ADD ON VIA HSBC CONNECTED ...................... 44

10.1 HSBC Credit Card Present.................................................................................................. 44

10.2 HSBC Credit Card NOT Present .......................................................................................... 46

10.3 Overview of HSBC VISA Classic Credit Card Add On Process ............................................... 49

11.0 SPLIT TRSANSACTIONS ............................................................ 50

11.1 How to Process a Split Transaction .................................................................................... 50

12.0 CREDIT (REFUND) TRANSACTIONS ........................................... 52

12.1 Overview of Credit Transaction Process............................................................................ 54

54

13.0 SETTLEMENT ........................................................................... 55

13.1 User Access Levels ............................................................................................................ 55

13.2 How to Process a Settlement ............................................................................................ 55

13.3 Overview of Settlement Process ...................................................................................... 57

14.0 OTHER HSBC CONNECTED FEATURES ....................................... 58

14.1 News & Bulletins .............................................................................................................. 59

15.0 MERCHANT ADMINISTRATION FUNCTIONS ............................. 60

15.1 Settlement Access ........................................................................................................... 60

15.2 Add User .......................................................................................................................... 61

15.3 Manage Existing User ....................................................................................................... 62

15.3.1 Modify an existing user: ..................................................................................................... 62

15.3.2 Reset Password .................................................................................................................. 63

15.3.3 Delete User ........................................................................................................................ 63

15.4 Training Mode.................................................................................................................... 64

16.0 HSBC ShopSmart ..................................................................... 65

16.1 New Application .............................................................................................................. 65

16.2 Add On ............................................................................................................................ 66

16.3 Merchant Information ..................................................................................................... 66

16.4 Customer Information ..................................................................................................... 66

16.5 System Support ............................................................................................................... 67

16.6 Connected and Settlement .............................................................................................. 67

16.7 Technical Requirements ................................................................................................... 67

PUBLIC - 5

17.0 Manual Application Form ........................................................ 69

17.1 When to use the Manual Application Form ....................................................................... 69

17.2 Operating Process for Manual Application Form .............................................................. 708

17.3 Location of the Manual Application Form…………………………………………………………………………68

18.0 FREQUENTLY ASKED QUESITIONS ............................................ 69

18.1 Merchant Questons .......................................................................................................... 69

18.2 Customer Questions ......................................................................................................... 71

19.0 ADMINISTRATION ................................................................... 72

19.1 Staff Training .................................................................................................................... 72

19.2 HSBC Advertising Guidelines ............................................................................................. 72

20.0 DEALING WITH HSBC AND THE CUSTOMERS .......................... 742

20.1 Dealing with the customer .............................................................................................. 742

20.2 Dealing with HSBC .......................................................................................................... 752

20.3 Escalation Process regarding feedback on HSBC…………………………………………………………………72 20.4 Escalation Process for a Suspicious Transaction………………………………………………………………...73

21.0 STATIONARY / POINT OF SALE ............................................... 744

21.1 Stationary / Point of Sale Ordering…………………………………………………………………………………….74 21.2 Delivery Schedule / Time Frames……………………………………………………………………………………….75

PUBLIC - 6

HSBC MERCHANT INSTRUCTION MANUAL

The HSBC Retail Banking Solutions Merchant Instruction Manual is provided by HSBC Bank Australia Limited ABN 48 006 434 162 as the provider of HSBC Consumer Finance. This is the Merchant Instruction Manual referred to in HSBC's Merchant Agreement. Each participating merchant must have a current Merchant Agreement with HSBC Bank Australia Limited (HSBC), enabling them to offer a finance facility to the general public. The agreement between HSBC and the participating merchant also details the merchant’s obligations under which finance is to be offered to customers, commencing on the date the Merchant Agreement is executed by HSBC. This manual is for use by HSBC’s accredited merchants when processing finance transactions using HSBC Retail Banking Solutions. It details the processes and procedures that must be followed by merchants and their staff. If you have any questions about the Merchant Instruction Manual or the Retail Banking Solutions program, please call HSBC on 1300 300 883. Copyright by HSBC: 2015

PUBLIC - 7

1.0 COMPLIANCE WITH LEGISLATION When dealing with this finance program the Merchant must:

• Comply with all applicable laws, including those relating to trade practices and fair trading, privacy, and consumer credit:

When dealing with customers personal information under this finance program the Merchant must comply with the following:

• The Merchant must not disclose any personal information (being a fact or opinion about an identifiable individual) collected or accessed in connection with an application or transaction to any person.

• The Merchant must not make records, or allow records to be made, of any personal

information. • The Merchant must use their best endeavours to ensure that all personal information is

kept under their control and secure from theft, loss, damage and unauthorised access, use and disclosure.

• The Merchant must not use any such personal information, except in accordance with these Operating Procedures.

• If the customer cannot understand the terms and conditions of applying for a HSBC account because the customer does not read English language, then the merchant should use the services of a professional interpreter service.

1.1 Anti-Money Laundering Anti-Money Laundering (“AML”) is a criminal or attempted criminal act to conceal or disguise the identity of illegally obtained proceeds, so that they appear to have originated from legitimate sources. This also extends to terrorist financing and/or proliferation financing. All HSBC employees and agents are expected to comply with applicable AML laws and regulations. All HSBC employees and agents shall be vigilant and must not allow HSBC to be used as a conduit for Money Laundering, Terrorist financing activities, tax evasion or other criminal activity (financial crime).

PUBLIC - 8

To assist HSBC in meeting its obligations under Anti-Money Laundering (AML) and Counter Terrorism Financing (CTF) Legislation. We require you as an Agent of HSBC to complete the following:

a) You must carefully examine the customers ID to ensure that it has not been tampered with or altered in anyway.

b) The primary photo ID must be current and the application must follow the same name and spelling as the primary ID provided by the customer. You must visually confirm that the applicant is the same as the photograph on the primary ID. Any doubts, you should not proceed and refer the application to HSBC's Retail Support Services.

c) You must be careful when entering the Customer name by ensuring the spelling is accurate and the name exactly matches their primary photo ID provided.

d) You must report anything you feel is suspicious to HSBC's Retail Support Services immediately upon becoming aware and wait for instructions from HSBC on next steps.

1.2 Anti-Bribery & Corruption

1.2.1 [Merchant] shall comply with, and shall ensure that its personnel, affiliates, associated

persons, agents, sub-contractors and any other third parties who may be used for or in relation to the provision of the Services are aware of and comply with, both the letter and spirit of applicable anti-corruption laws such that they will not take any actions or make any omissions which would cause either HSBC and/or any HSBC Group Member or [Supplier] to be in violation of applicable anti-corruption laws.

1.2.2 [Merchant] confirms that in connection with any transactions undertaken for and on

behalf of HSBC and/or any HSBC Group Member that it has not and undertakes that it shall not: (i) make any payments (including facilitation payments) or transfers of value, offers or promises; or (ii) give any financial or other advantage, make any requests, agreements to receive or accepting any financial or other advantage; in each case either directly or indirectly which has the purpose or effect of, or would mean acceptance of or acquiescence in, either directly or indirectly, public or commercial bribery, other unlawful or improper means of obtaining or retaining business or commercial advantage or the improper performance of any function or activity.

1.2.3 [Merchant] confirms, in relation to the provision of services to HSBC and/or any HSBC

Group Member, and the activities to be carried out under this Agreement, that its officers, directors and employees are subject to policies and procedures which are designed to prevent the occurrence of bribery and corrupt conduct, and undertakes that it shall procure compliance with such policies and procedures by its officers, directors, employees and (where permitted under this Agreement) sub-contractors.

1.2.4 [Merchant] shall not be relieved of any obligation or liability under this clause by reason

of any permitted sub-contracting any of its obligations under this Agreement pursuant to clause []. Notwithstanding the generality of the foregoing [Merchant] shall ensure that:

PUBLIC - 9

1.2.4.1 each such sub-contractor has adequate anti-bribery and corruption policies and procedures in place; and

1.2.4.2 the agreement between [Merchant] and the sub-contractor contains adequate anti-

bribery and corruption provisions, at least equivalent in effect to this clause [1].

1.2.5 [Merchant] warrants and represents that it is not currently under actual or, to [Merchant]’s knowledge, threatened investigation or inquiry, or being audited by any governmental authority in relation to any offence or alleged offence involving fraud, corruption or dishonesty, and that neither [Supplier], nor any of its current owners, directors, officers, employees, sub-contractors or agents has been convicted of or pleaded guilty to an offense involving fraud, corruption, or dishonesty, and that neither it nor any such individual has been listed by any government agency or non-governmental organisation as debarred, suspended, proposed for suspension or debarment, or otherwise ineligible for procurement programs.

1.2.6 [Merchant] warrants and represents that neither it nor its affiliates, or its or their

respective directors, officers, agents, employees or sub-contractors are individuals or entities are the target of economic and financial sanctions measures imposed by the United Nations, the European Union, the United Kingdom, the United States or any relevant and applicable jurisdiction (“Restricted Persons”). [Supplier] shall not directly or indirectly deal with Restricted Persons in connection with its dealings with HSBC and/or any HSBC Group Member.

1.2.7 [Merchant], its respective affiliates, associated persons, agents, sub-contractors or any

other third parties who may be used for the provision of services to HSBC shall disburse funds related to transactions involving HSBC and/or an HSBC Group only pursuant to a duly authorized written contract. No undisclosed or unrecorded fund(s) or asset(s) shall be established or maintained by [Supplier] or any affiliate, associated person, agent, sub-contractor or any other third party who may be used for the provision of services to HSBC and/or any HSBC Group Member.

1.2.8 [Merchant] shall document completely and accurately all transactions related to the Services and this Agreement in its books and records. All expenses related to transactions involving HSBC and/or an HSBC Group Member shall be supported by complete and accurate documentation, including without limitation invoices, receipts, proof of delivery and contracts. Such documentation shall be maintained throughout the duration of this Agreement and for a period of six (6) years after its expiry or termination, and shall be made available to HSBC upon reasonable notice for review.

1.2.9 [Merchant] shall promptly report to HSBC any breach or suspected breach of these

obligations and all requests or demands for any undue financial or other advantage of any kind received by it in connection with the performance of this Agreement.

1.2.10 In the event that HSBC has reason to believe that a breach of this clause [1] has occurred or may occur, HSBC may withhold without penalty or liability any payments otherwise due and payable under this Agreement until it receives confirmation to its satisfaction that no breach has occurred or will occur.

PUBLIC - 10

1.2.11 [Merchant] shall fully and effectively indemnify and keep indemnified HSBC from and

against, and agrees to pay on demand, any and all losses incurred by or awarded against HSBC as a result of any breach of the obligations referenced in this clause [1]. Without prejudice to the foregoing or to any other rights or remedies of HSBC, in the event of any breach of these obligations [Merchant] undertakes promptly to remedy the breach (or the circumstances giving rise to the breach) without charge.

1.2.12 [Merchant] acknowledges that HSBC may terminate this Agreement immediately in the

event that HSBC has a reasonable belief that a breach of this clause [1], or of any similar or equivalent provisions in any other agreement between [Merchant] and HSBC and/or an HSBC Group Member, has occurred or may occur.

PUBLIC - 11

2.0 CONTACT DETAILS

2.1 Merchant Contact Information

Enquiry Contact Details

Operating Hours*

AEST

HSBC Retail Support Enquiries relating to:

• New or existing applications

• Add On's • Credit Limit increases

Ph : 1300 300 883 Fax: 02 9255 2542

Mon-Wed, Fri: 8.30am - 9pm

Thurs: 8:30am - 10pm

Sat & Sun: 9:00am - 6pm

Merchant Settlement Enquiry

Stationery / Point of Sale

www.staplesadvantage.com.au

2.2 Customer Contact Information

Enquiry Contact Details

Operating Hours*

AEST

Visa Credit Card Customer Enquiries

132 152

24 hours, 7 days a week

Lost and stolen cards

1800 029 951 (Toll Free)

24 hours, 7 days a week

Credit Cards Online

www.hsbc.com.au

24 hours, 7 days a week

Payments by Mail

HSBC Credit Cards PO BOX 347

Artarmon, NSW, 1570

* Operating hours are Subject to change during daylight saving periods & public holidays

PUBLIC - 12

3.0 INTRODUCTION TO HSBC This Merchant Instruction Manual (MIM) is the "Merchant Instruction Manual" referred to in your Merchant Agreement with HSBC Bank Australia Limited. The MIM is an important document, which forms part of your Merchant Agreement. The MIM is to be used by Merchants whenever dealing with a HSBC VISA Card, and includes important information about: • Advertising and promoting cards • Application and transaction authorisation process; and • Training staff to enable them to comply with these procedures. All Merchants must comply with the procedures outlined in this document. In this document, references to “Merchants” include both Merchants and Merchant’s staff (unless otherwise stated).

3.1 HSBC Bank Overview

3.1.1 An introduction to HSBC - The world's local bank

Headquartered in London, HSBC is one of the largest banking and financial services organisations in the world. HSBC’s international network operates in 74 countries and territories in Europe, Asia-Pacific, the Middle East, North America and Latin America. HSBC provides a comprehensive range of financial services to more than 52 million customers through four customer groups and global businesses: Personal Financial Services (including consumer finance); Commercial Banking; Global Banking and Markets; and Private Banking.

3.1.2 HSBC Bank in Australia

In Australia, the HSBC Group offers an extensive range of financial services through a network of branches and offices nationally. These services include personal and commercial financial services, trade finance, non-advisory stockbroking, treasury and financial markets, financial planning and securities custody. When combined with the extensive resources of the HSBC Group, this enables us to offer our customers financial solutions that meet their personal lifestyle and aspirations.

PUBLIC - 13

3.2 HSBC Product Overview

3.2.1 Introduction to HSBC flexible payment options

This section of the Merchant Instruction Manual has information on HSBC's Retail Banking Solutions products, merchant contracts and promotional terms.

3.2.2 Products HSBC’s products offer Retail Banking Solutions customers flexible payment options. The products include:

HSBC’s Visa Classic Credit Card Other credit products that HSBC may develop and offer from time to time.

Note: These products are available to eligible customers who are permanent residents of Australia. HSBC reserves the right to change any features of any product, including our right to discontinue offering a particular product.

PUBLIC - 14

3.3 HSBC VISA Classic Credit Card - Overview HSBC’s Visa Classic Credit Card combines Point of Sale finance, with the convenience of a credit card. Customers apply for the card in-store or online and once approved can purchase immediately on:

• Interest Free, with minimum monthly repayments • Interest Free Payment Deferred

The Interest Free Type and length is offered at Point Of Sale at merchant discretion. In addition, customers can use their existing card for subsequent interest-free or payment deferred promotional purchases (see the Add-on Process for more details). This also applies for customers who have any HSBC Credit Cards issued in Australia. HSBC's Visa Classic Credit Card can also be used for everyday purchases, with up to 55 days interest free. The customer is able to spend up to their customer's assigned credit limit. Customers receive a monthly statement as they would for any other credit card, the minimum monthly payment required is 3% of the outstanding balance or $20, whichever is greater (if not a deferred Interest free payment promotion period). With the HSBC Visa Classic Credit Card, the minimum amount of a promotional transaction is $500 and the maximum limit is $50,000. This is subject to approved credit limits. Annual percentage rates (interest rates) are disclosed in the Credit Contract. They are also available from HSBC Retail Support or hsbc.com.au. The features of the HSBC Visa Classic Card include:

Visa worldwide acceptance – at over 22 million outlets and 800,000 ATMs Up to 55 days interest free on everyday purchases Apply & submit application in-store & get a response within 1 hour No application fee Competitive interest rates on balance transfers Access to interest free and deferred payment promotions at participating retailers

PUBLIC - 15

3.3.1 HSBC VISA Classic Credit Card – at a glance

Features HSBC

Visa Classic Credit Card

In-store application ✔

Extended Interest-free options available at participating retailers

✔

Deferred payment options available at participating retailers

✔

Monthly statements ✔

Up to 55 days interest-free on everyday purchases

✔

Card access ✔

Additional promotional purchases on the same account

✔

A low annual card fee ✔

Direct Debit payments ✔

No early repayment penalties ✔

PUBLIC - 16

3.4 HSBC Promotional Terms

There are three types of promotional terms available to HSBC's merchants.

3.4.1 Interest free with payments (IF): HSBC Visa Classic Credit Card a. The customer is required to make minimum monthly principal-reducing payments of 3% of

the outstanding interest-free balance (rounded down to the nearest dollar) or $20, whichever is greater.

b. A payment is required for each month of the term, with no interest charged during the interest-free months.

c. If the customer chooses not to pay out the total amount at the end of the promotional interest-free period, the prevailing cash advance annual percentage rate (APR) applies to the outstanding amount from the day after the promotion period expires.

d. The customer can make additional payments or payments greater than the requested 3% monthly minimum during the interest free period without any penalties.

Note: If the customer makes only the minimum monthly payments during the interest free period, there will be an amount due at the end of the promotional period. If this amount is not paid off by the last day of the promotional period, it will attract interest at the prevailing cash advance APR.

3.4.2 Interest free payment deferred (PD): HSBC Visa Classic Credit Card a. This is also known as “Buy Now, Pay Later”. b. The customer is not required to make repayments for the payment deferred term on the

promotional purchase and is charged no interest during those months. c. If the customer chooses not to pay out the total amount at the end of the promotional

period, the prevailing cash advance annual percentage rate (APR) applies to the outstanding amount from the day after the promotion period expires.

d. The customer can make additional repayments during the Interest Free Payment Deferred period without any penalties

3.4.3 Hybrid promotions: Interest Free & Payment Deferred Combinations A Hybrid promotion is where there is an Interest Free period and an Interest Free Payment Deferred period for the one promotion. Example 24MIF/12PD. a. The interest free period is longer than the payment deferred period, e.g. 24 months

interest free, of which 12 months are payment deferred. b. At the end of the 12 month payment deferred period, minimum monthly payments (3% or

$20, whichever is greater) are required for the remaining 12 months of the interest free period.

c. The total length of the interest free period is 24 months. The prevailing cash advance annual percentage rate (APR) applies to any outstanding amount from the day after the interest-free promotion period expires.

PUBLIC - 17

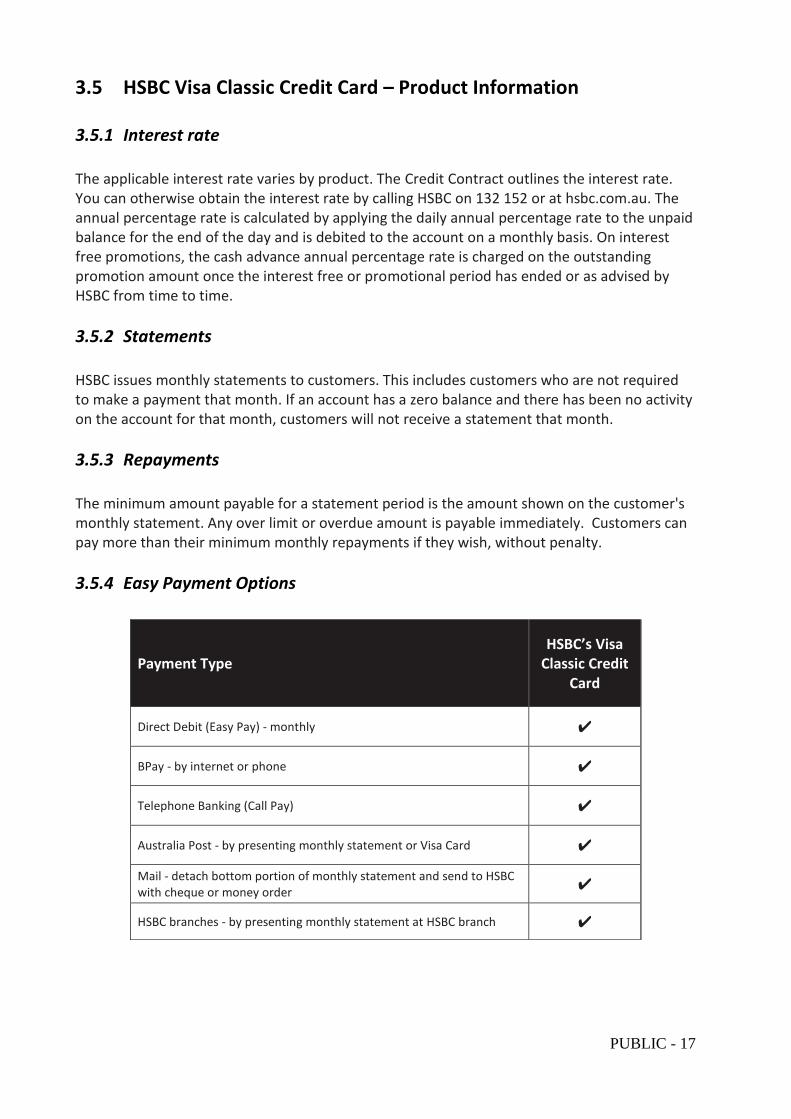

3.5 HSBC Visa Classic Credit Card – Product Information

3.5.1 Interest rate The applicable interest rate varies by product. The Credit Contract outlines the interest rate. You can otherwise obtain the interest rate by calling HSBC on 132 152 or at hsbc.com.au. The annual percentage rate is calculated by applying the daily annual percentage rate to the unpaid balance for the end of the day and is debited to the account on a monthly basis. On interest free promotions, the cash advance annual percentage rate is charged on the outstanding promotion amount once the interest free or promotional period has ended or as advised by HSBC from time to time.

3.5.2 Statements HSBC issues monthly statements to customers. This includes customers who are not required to make a payment that month. If an account has a zero balance and there has been no activity on the account for that month, customers will not receive a statement that month.

3.5.3 Repayments The minimum amount payable for a statement period is the amount shown on the customer's monthly statement. Any over limit or overdue amount is payable immediately. Customers can pay more than their minimum monthly repayments if they wish, without penalty.

3.5.4 Easy Payment Options

Payment Type HSBC’s Visa

Classic Credit Card

Direct Debit (Easy Pay) - monthly ✔

BPay - by internet or phone ✔

Telephone Banking (Call Pay) ✔

Australia Post - by presenting monthly statement or Visa Card ✔

Mail - detach bottom portion of monthly statement and send to HSBC with cheque or money order

✔

HSBC branches - by presenting monthly statement at HSBC branch ✔

PUBLIC - 18

Note: Payment options are shown on customers' monthly statement. Merchants cannot accept HSBC account payments in store.

3.5.5 Card and PIN

HSBC's Visa Credit Card customers are issued with a card and PIN once their application is approved.

3.5.6 Multiple promotions and transactions

Customers can access multiple special promotions and conduct standard transactions on their HSBC account, up to their available credit limit.

3.5.7 Card Activation

For security purposes, customers need to activate HSBC's Visa credit cards once they have received them. Instructions for doing this are sent with the cards.

3.5.8 Standard Visa purchases

The HSBC Visa Classic Credit Card has up to 55 days interest-free on non-promotional transactions. The customer is required to make monthly repayments of 3% of the total closing account balance or $20, whichever is greater.

3.5.9 Credit Limit Increase for Existing Cardholders Customers may request a credit limit increase by calling 132 152. The HSBC operator will have the customer complete a Credit Limit Increase Form and submit it to HSBC. Applications for credit limit increases are subject to HSBC's normal lending criteria. The process for requesting this is detailed in Credit Limit Increase section of this document.

PUBLIC - 19

4.0 HSBC CONNECTED

4.1 Features and Functionality HSBC's Connected is an internet-based finance application system that allows you to submit online applications for HSBC's Retail Banking Solutions products in real time. You can then monitor the status of the applications throughout the decision process and manage the finalising and settlement of interest free promotional purchases. HSBC Connected also offers you the ability to process and manage Add On transactions for existing HSBC credit card customers.

Note: The use of the HSBC Connected system is subject to the terms and conditions set out in the Merchant Agreement (i.e. your contract with HSBC).

4.2 Access HSBC's Connected is available on the World Wide Web at

https://connected.hsbc.com.au/multiapp It is a secure website with statutory banking security encryption. To access HSBC Connected, merchants will need to be set up with a username and password. Please contact your HSBC Business Development Manager for further information.

4.3 Software & Hardware Requirements In order to use HSBC Connected effectively you will need a PC with either:

• An internet connection (Connected performs best on a broadband connection) • Windows 2000 or Windows XP • Internet Explorer 8+ or Google Chrome • Adobe Reader 10.0 or higher • A compatible printer

PUBLIC - 20

5.0 HSBC CONNECTED – MERCHANT INFORMATION

5.1 User Access Information

HSBC Connected has different access levels for different Users:

Store Staff What you can access:

• Input application • Input Add-On Sales Voucher • Change or delete Sales Voucher details prior to settlement • Input and Process Credit (Refund) transactions • Retrieve instore and apply from home applications • Change your own password for login

Merchant Administrator What you can access:

• Input application • Input Add-On Sales Voucher • Change & Delete Sales Voucher details prior to settlement • Retrieve instore and apply from home applications • Create and maintain store users • Settle Sales Vouchers • Input and Process Credit (Refund) transactions

Group Administrator What you can access:

• Application Manager for all stores within the group • Change Sales Voucher details prior to settlement • Retrieve instore and apply from home applications • Settle Sales Vouchers • Input and Process Credit (Refund) transactions

PUBLIC - 21

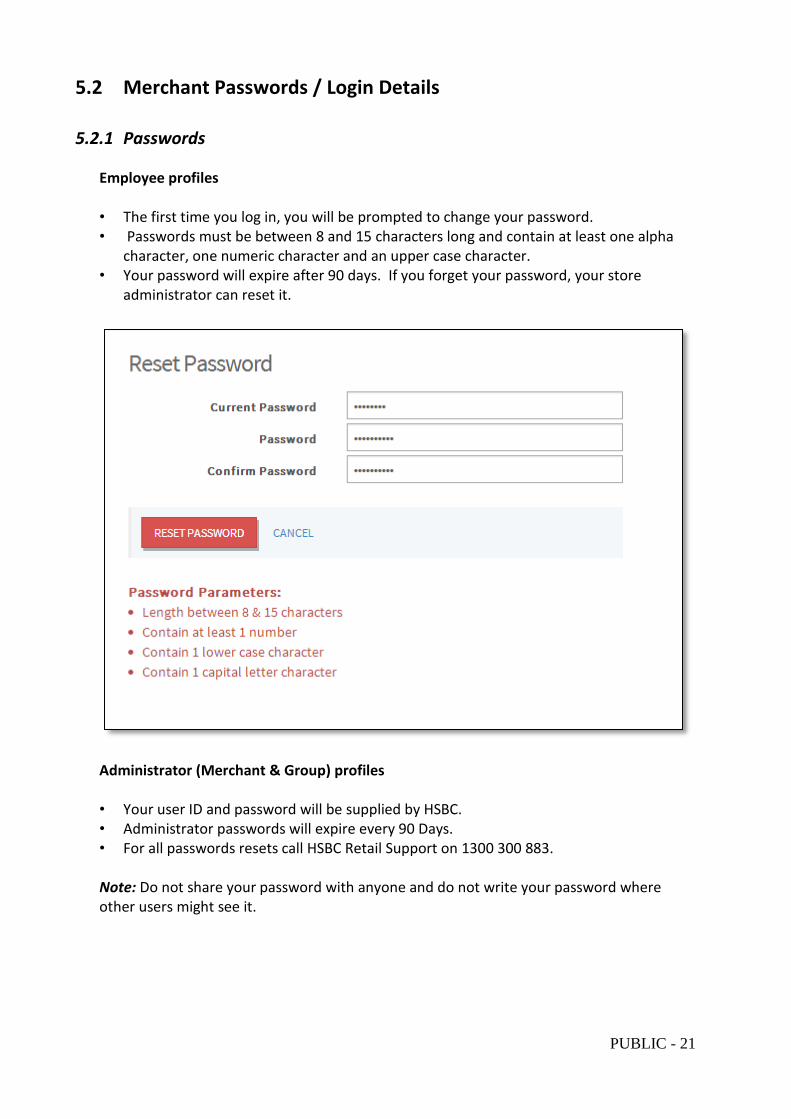

5.2 Merchant Passwords / Login Details

5.2.1 Passwords

Employee profiles • The first time you log in, you will be prompted to change your password. • Passwords must be between 8 and 15 characters long and contain at least one alpha

character, one numeric character and an upper case character. • Your password will expire after 90 days. If you forget your password, your store

administrator can reset it.

Administrator (Merchant & Group) profiles • Your user ID and password will be supplied by HSBC. • Administrator passwords will expire every 90 Days. • For all passwords resets call HSBC Retail Support on 1300 300 883. Note: Do not share your password with anyone and do not write your password where other users might see it.

PUBLIC - 22

5.3 Tips for using HSBC Connected

Navigation • To navigate around the Connected screen, use the Tab key. To go back one field, use

Shift + Tab. • You can also use the mouse to click into a field. • When you finish entering the information into a page, click the button to continue and

check to see if any fields on the screen have been highlighted in Red. This is a prompt to tell you that information needs to be entered or corrected.

• To exit a screen, click the Application Manager button or the navigation button to the section you would like to go.

• Do not use your internet browser's Back and Forward buttons in a Connected session unless instructed, as these functions are not supported and will cause your session to lock up.

• To move from screen to screen, use the Save & Continue button or Back button on the Connected page.

• Do not bookmark any of the Connected pages except for the login screen. You will not be able to use any of the functions on a bookmarked page.

Timeout

• When you are logged into Connected the system will timeout after 10 minutes if it is not used, to protect the privacy of the applicant's details.

• Applications will be saved provided you have completed Step 1 of the applicant. Privacy

• To protect your customers' privacy, never leave information displayed on the screen.

• Always clear or minimise the screen if you leave your PC.

PUBLIC - 23

6.0 HOW TO LOG INTO HSBC CONNECTED

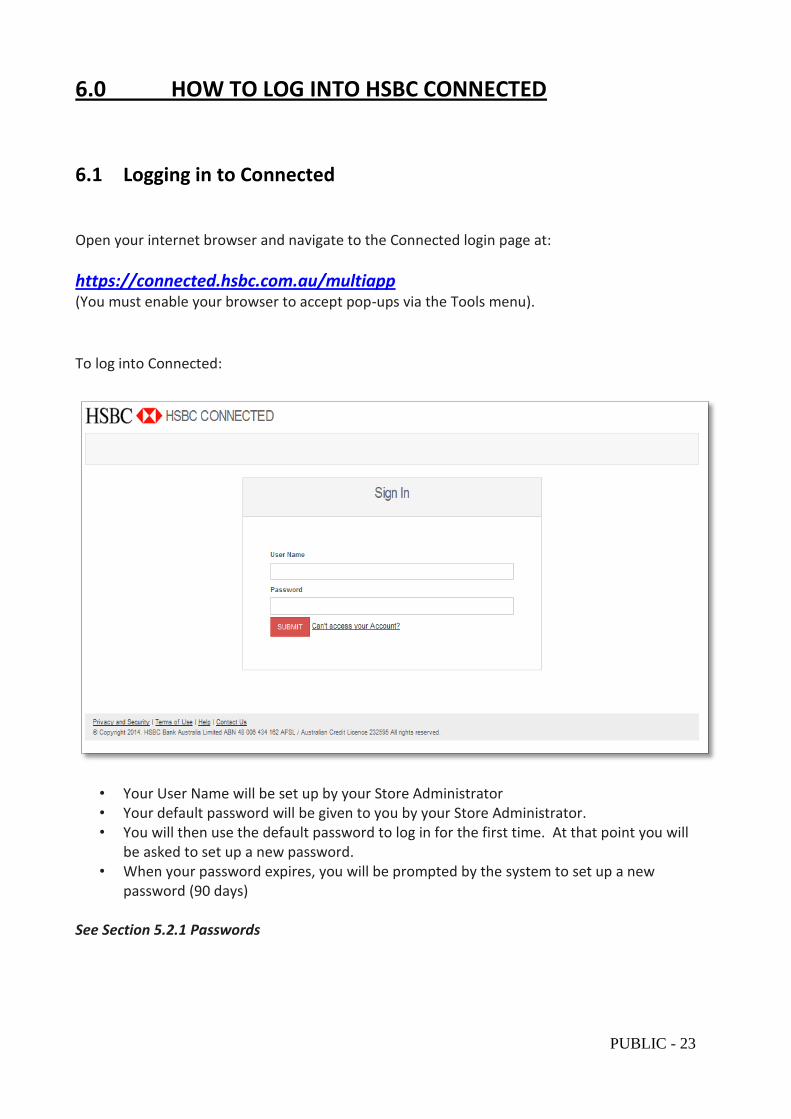

6.1 Logging in to Connected Open your internet browser and navigate to the Connected login page at:

https://connected.hsbc.com.au/multiapp (You must enable your browser to accept pop-ups via the Tools menu).

To log into Connected:

• Your User Name will be set up by your Store Administrator • Your default password will be given to you by your Store Administrator. • You will then use the default password to log in for the first time. At that point you will

be asked to set up a new password. • When your password expires, you will be prompted by the system to set up a new

password (90 days) See Section 5.2.1 Passwords

PUBLIC - 24

When you successfully log into the system you will see the News & Bulletins screen.

6.2 Logging off

Once you have finished using Connected you should log off. To do this,

1. Click Logout

2. Close the browser window.

PUBLIC - 25

7.0 HSBC CONNECTED SUMMARY SCREENS

7.1 Application Manager The function of the Application Manager is to give a merchant access to all New Applications

and Add-Ons that have been processed instore, as well as applications that a customer has

input from home.

7.1.1 Search for an Existing Instore Application or Add On

• If an application is Pending Other and was done less than 3 days ago, you will click on the number in that category.

• This will then open up and give you a results page with the applications listed.

• You then click on the Application ID Number and this will take you to the Application Summary Page.

• You can also search the results page using any of the above fields

• Type in the details and the application will be found.

A

C

B

B

C

A

PUBLIC - 26

7.1.2 Retrieve an Application The Retrieve an Application function can be used to:

Retrieve an application done instore that you cannot find in the Application

Manager.

Retrieve an Incomplete / Pending Application

Retrieve an application that was done via the Apply from Home link (SWIFT) by a

customer. The customer would have applied from home and has come instore to

complete the application process and make a purchase.

OPTION 1

• For customers that have applied from home via SWIFT

• You will need the Application Reference Number and Customer Date of Birth

OPTION 2

• For customers that have applied from home via SWIFT

• If the customer does not have their Application reference Number, input the Mother’s

Maiden Name, Email Address and Date of Birth (as input in application)

NOTE: With both options, the merchant staff member must always sight the customer

photo ID and verify that the customer is the applicant and it matches to the application

details. Merchant staff will be required to acknowledge this by checking the box on this

screen.

PUBLIC - 27

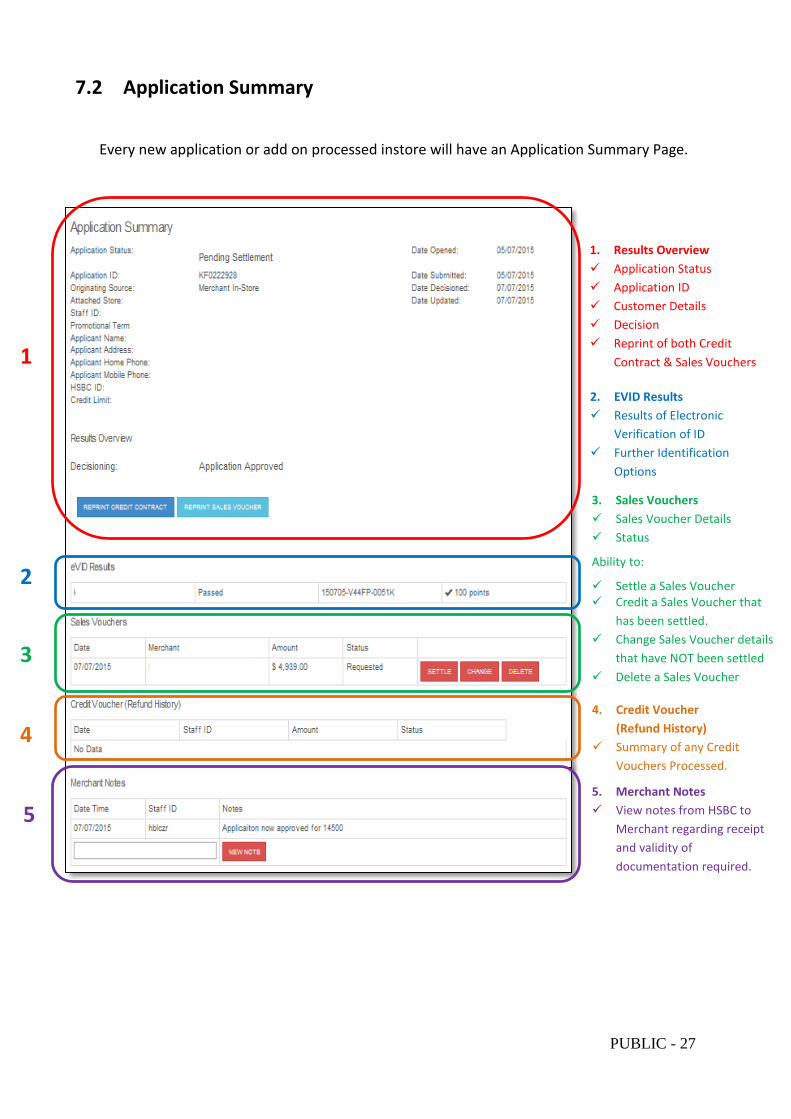

7.2 Application Summary

Every new application or add on processed instore will have an Application Summary Page.

1. Results Overview

Application Status

Application ID

Customer Details

Decision

Reprint of both Credit Contract & Sales Vouchers

5

1

2

3

4

1. Results Overview

Application Status

Application ID

Customer Details

Decision

Reprint of both Credit

Contract & Sales Vouchers

2. EVID Results

Results of Electronic

Verification of ID

Further Identification

Options

3. Sales Vouchers

Sales Voucher Details

Status

Ability to:

Settle a Sales Voucher Credit a Sales Voucher that

has been settled.

Change Sales Voucher details

that have NOT been settled

Delete a Sales Voucher

5. Merchant Notes

View notes from HSBC to

Merchant regarding receipt

and validity of

documentation required.

4. Credit Voucher

(Refund History)

Summary of any Credit

Vouchers Processed.

PUBLIC - 28

8.0 APPLY FOR HSBC VISA CARD VIA HSBC CONNECTED

8.1 HSBC ID Requirements

To apply, a customer must supply 1 Photo Identification document.

This ID can be either:

Current Australian Driver’s License with photo

Valid Australian Passport

Valid International Passport

The Merchant staff member will require to sight the ID and to input the ID details into the HSBC

Connected application.

Note:

• Documents must be sighted and must be original

• Photo ID must be current and must contain a photo

• All Drivers License must be laminated

Different Driver's Licenses from different states or territories will require different information for verification. The Connected system will advise what information is needed after you nominate where the Driver's License has been issued.

PUBLIC - 29

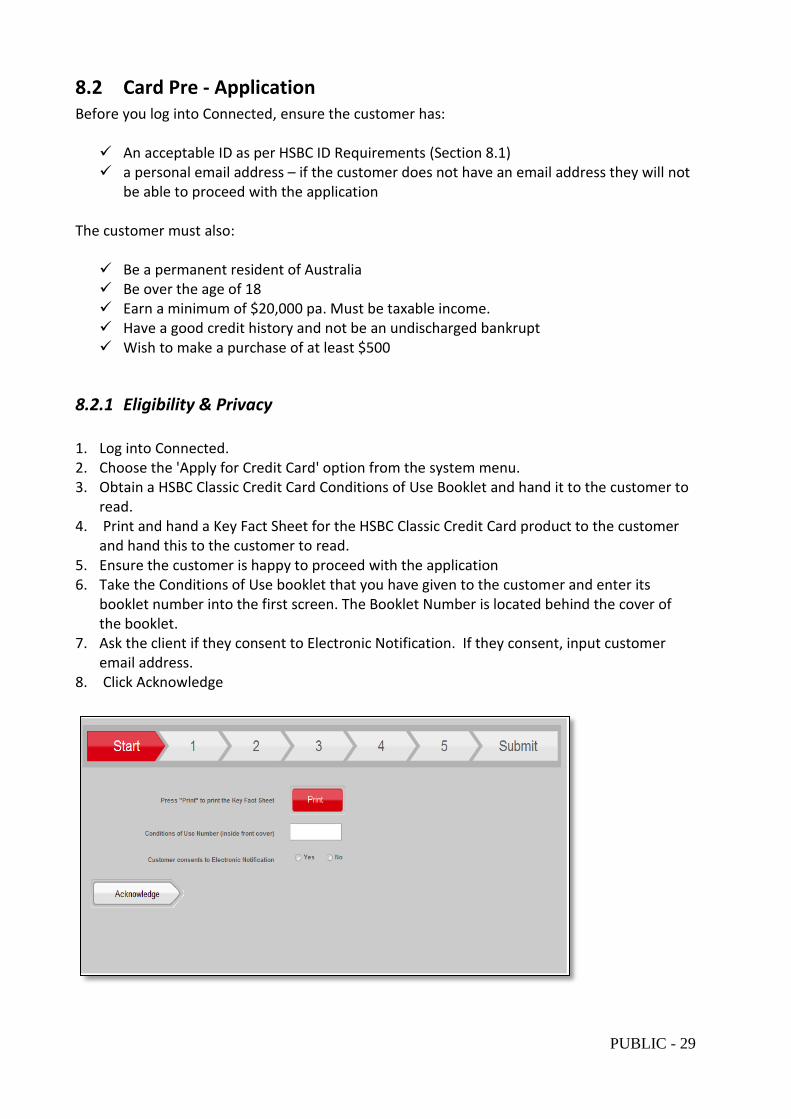

8.2 Card Pre - Application Before you log into Connected, ensure the customer has:

An acceptable ID as per HSBC ID Requirements (Section 8.1) a personal email address – if the customer does not have an email address they will not

be able to proceed with the application The customer must also:

Be a permanent resident of Australia Be over the age of 18 Earn a minimum of $20,000 pa. Must be taxable income. Have a good credit history and not be an undischarged bankrupt Wish to make a purchase of at least $500

8.2.1 Eligibility & Privacy 1. Log into Connected. 2. Choose the 'Apply for Credit Card' option from the system menu. 3. Obtain a HSBC Classic Credit Card Conditions of Use Booklet and hand it to the customer to

read. 4. Print and hand a Key Fact Sheet for the HSBC Classic Credit Card product to the customer

and hand this to the customer to read. 5. Ensure the customer is happy to proceed with the application 6. Take the Conditions of Use booklet that you have given to the customer and enter its

booklet number into the first screen. The Booklet Number is located behind the cover of the booklet.

7. Ask the client if they consent to Electronic Notification. If they consent, input customer email address.

8. Click Acknowledge

PUBLIC - 30

8.2.2 HSBC Pre-Application Checklist 1. Read the pre-application checklist to the customer. They must answer YES or NO to the

questions 2. Click Next. Note: There are validations throughout Connected. This is to ensure that the correct details are input and minimise errors thus ensure speedy processing for both the Customer and the Merchant.

PUBLIC - 31

8.2.3 Purchase Details The ID of the merchant staff member that is logged into Connected will be pre-filled. If this is not the ID of the sales staff entering the applicant details please log out of the system and enter Connected with the log in details of the merchant staff member entering the information. 1. Select the Finance Term from the drop down box the applicant will receive on the

promotional purchase if approved. Please note all available finance terms will be available in the drop down box. If the desired term is not available please contact your BDM.

2. Enter a brief description (type of item) being purchased. 3. Enter the total amount of the items being purchased.

Please note this is not the only section where the amount to be financed will be nominated. You will get an opportunity on approval to finalise the finance amount and change the finance term if necessary.

4. If the applicant is a merchant staff member, please nominate here and enter the applicants

staff ID.

PUBLIC - 32

8.3 Application Details Enter the application information. (Remember to fill in as many fields as possible. The Connected system will prompt you if a field is mandatory). Once you have completed Step 1 of the application, the Connected system will allocate an application ID to the application. This ID can be used to retrieve the application at any time should your internet connection fail during the application process or the application needs to be stopped for any reason. The ID is shown at the bottom of the page from Step 2 onwards.

8.3.1 Customer Details

An applicant will need to nominate an email address to apply for finance. We are unable to assist an applicant that is unable to provide an email address. In some fields, such as Nationality, you can type the first letter of the applicant's answer to jump to that section of the list. For example, you can press the “a” key to go to the first nationality starting with A, which is Australia. To scroll through all the options that start with A, keep pressing the “a” key. Connected will display or hide some fields on the application form depending on the data you enter. For example, if you select “yes” option under the “Are you an HSBC customer?” field, another field will appear. Please enter the applicant's HSBC account number there if they can supply it, however this field is not mandatory.

PUBLIC - 33

8.3.2 Address & Phone Number Details

Connected has Geo Coding technology that will try and identify the address you are entering and give you options to select. Just start typing the address within the address field in Connected and select the correct address when it is displayed. If the system cannot identify the address you wish to enter you can manually enter the entire address.

Note: The Home Phone field is for a landline number only. Do not enter a mobile number into this field as it may cause delays in processing the application. If the customer does not have a landline number as a home number, enter the customer's mobile number into the Mobile Phone field and leave the Home Phone field blank.

8.3.3 Employment Details

Depending on the employment status selected, the system will open and hide fields accordingly. If you select Home Duties, unemployed, full time education or retired in the ‘Current Employment status’, you will not need to complete the following fields: Job Title, Time with employer, Employers Name, Employer Phone and the entire ‘Employee Address’ section. If the applicant is self-employed or a contractor, additional fields will be provided for you to fill in. If the applicant is not self-employed but is contracting through an agency or via a fixed term contract directly with an employer, enter the agency or employer's details here.

PUBLIC - 34

PUBLIC - 35

8.3.4 Financial Details Ensure the applicant understands that this application should be made in the name of the

person who will be benefiting from the loan and who will therefore be responsible for it.

Therefore the application can only be submitted in one name and will be assessed on one

income.

When entering income details, please select the frequency, either Weekly, Fortnightly,

Monthly or Annually.

A. Income details for the applicant's main employment B. This includes a second job and any rental / investment income. Do not include the spouse or partner's income here. C. Enter spouse/partners Total Net Income

Note: Please ensure that the applicant will be able to provide proof of the income that is input

into the application (both Primary and Any Other Income) if requested by HSBC.

PUBLIC - 36

D. Show the minimum payment required: • Mortgage – minimum amount the bank requires • Rent - show the total rent payments if the applicant's name is on the lease • Rent/Board - show the applicant's share of the rent or board if the applicant's name is

not on the lease or if they are boarding.

E. This includes all loans and hire purchases for which the applicant is the primary or joint account holder. This does not include Credit Card repayments. F. Show all other living expenses that are not already listed.

G. Only show the credit / store cards for which the applicant is the primary or joint account holder, not a supplementary account holder.

• If a value > 0 is entered into the ‘Total Number of cards held’ field, then the fields ‘Total credit cards balance owing’ and ‘Total credit limits’ pop up and are mandatory fields.

PUBLIC - 37

8.3.5 Review and Submit Ask the applicant to check the information on the Review and Submit screen. (This is the last chance to change anything before the application is submitted). To change details, click Edit. You will be taken back to the applicable page on the application form so that you can amend the information there. When the information is correct, click Save and Review. The application will be returned to the Review and Submit page.

PUBLIC - 38

When the information is correct, answer the Credit Limit Increase and Over limit Consent questions and confirm the applicant has read and understood the Terms and Conditions of the product. Click Submit. The application will be submitted for assessment.

PUBLIC - 39

8.4 Overview of HSBC VISA Classic Credit Card Application Process

(HSBC Connected)

PUBLIC - 40

9.0 APPLICATION DECISIONS

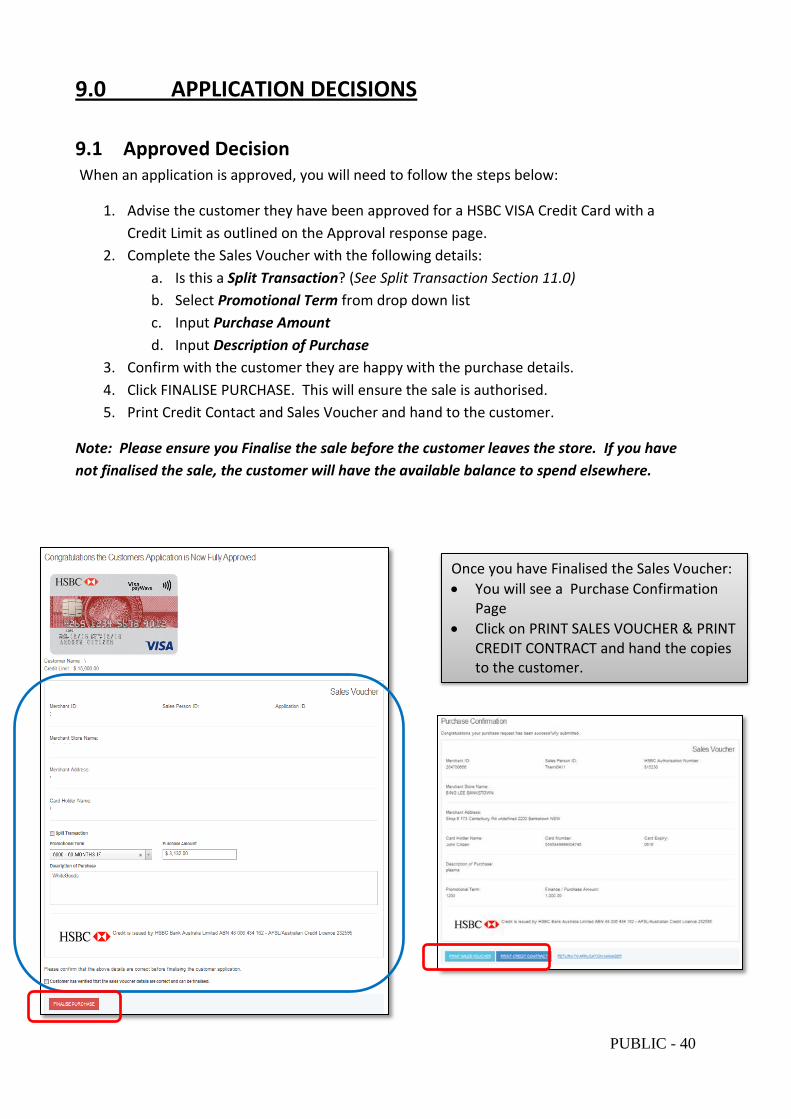

9.1 Approved Decision When an application is approved, you will need to follow the steps below:

1. Advise the customer they have been approved for a HSBC VISA Credit Card with a

Credit Limit as outlined on the Approval response page.

2. Complete the Sales Voucher with the following details:

a. Is this a Split Transaction? (See Split Transaction Section 11.0)

b. Select Promotional Term from drop down list

c. Input Purchase Amount

d. Input Description of Purchase

3. Confirm with the customer they are happy with the purchase details.

4. Click FINALISE PURCHASE. This will ensure the sale is authorised.

5. Print Credit Contact and Sales Voucher and hand to the customer.

Note: Please ensure you Finalise the sale before the customer leaves the store. If you have

not finalised the sale, the customer will have the available balance to spend elsewhere.

Once you have Finalised the Sales Voucher:

You will see a Purchase Confirmation Page

Click on PRINT SALES VOUCHER & PRINT CREDIT CONTRACT and hand the copies to the customer.

PUBLIC - 41

9.2 Pending Decision

9.2.1 Pending ID

If the Application response is Pending ID, you will need to follow the steps below:

1. Click on the Manual Check & Update button

2. Complete the additional forms of ID required and click on SUBMIT 100PT ID

Note: A list of acceptable ID documents are listed in the drop down box. These are the ONLY

ID’s that can be used.

PUBLIC - 42

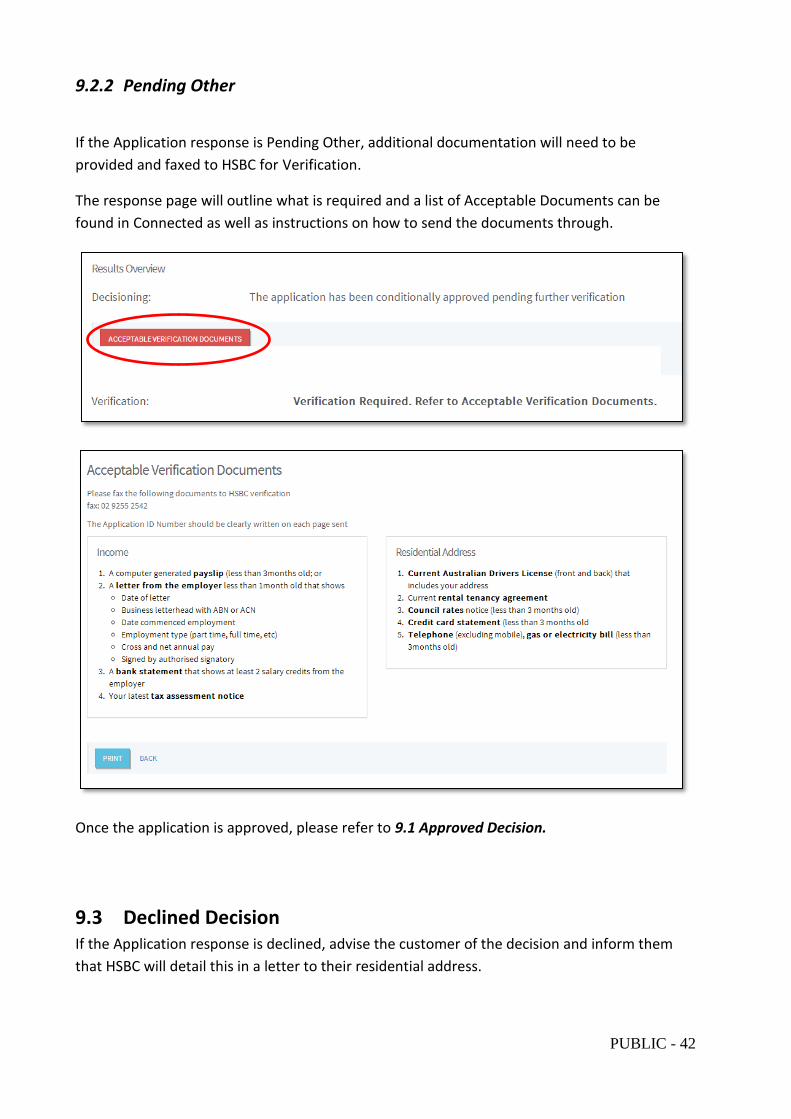

9.2.2 Pending Other

If the Application response is Pending Other, additional documentation will need to be

provided and faxed to HSBC for Verification.

The response page will outline what is required and a list of Acceptable Documents can be

found in Connected as well as instructions on how to send the documents through.

Once the application is approved, please refer to 9.1 Approved Decision.

9.3 Declined Decision If the Application response is declined, advise the customer of the decision and inform them

that HSBC will detail this in a letter to their residential address.

PUBLIC - 43

9.4 Summary of Documentation required for a New Application

The Connected system is designed to reduce the amount of documentation required to finalise

an application and settle a transaction.

However, it is very important that a client receives the appropriate documentation to ensure

they are fully aware of the Terms & Conditions of the product they are applying for.

Please ensure the applicant receives the following documentation at the nominated stages of

the application process.

Conditions of Use Booklet – this is handed to the customer prior to beginning the

application. They must be given the opportunity to read this and agree to proceed with

the application. Eligibility & Privacy section 8.2.1.

Key Fact Sheet – this is printed and handed to the customer to read as part of Eligibility

& Privacy section 8.2.1.

Credit Contract & Sales Voucher – once the applicant is approved and the purchase has

been finalised, print a copy of the Credit Contact and Sales Voucher and hand to the

customer. Approved Section 9.1

PUBLIC - 44

10.0 PROCESSING AN ADD ON VIA HSBC CONNECTED

An Add On is a promotional purchase for a customer who already has a HSBC Credit Card.

Since the customer already has an account with us they do not need to complete another

application. This promotional purchase will be an ‘add on’ to their account.

Note: The Credit Card must be and Australian issued HSBC Credit Card.

10.1 HSBC Credit Card Present

If a customer wishes to make an interest free purchase and they have their card present

instore, you will need to follow the steps below:

1. Ask the customer for the HSBC VISA Card and 1 form of Photo ID to verify.

Use the Photo ID to confirm the picture on the ID match to the person instore making the

purchase and the name of the ID is the same as the HSBC VISA Card.

2. Log in to Connected 3. Click on ‘Apply for an Add On’ 4. Click YES “Does the customer have their HSBC Card present?

5. Click NEXT

6. Complete the following fields:

a. Card Holder name (as it appears on the card)

b. Card Number

c. Expiry Date

d. Split Transaction

e. Promotional Term

f. Purchase Amount

g. Description of Purchase

h. Tick whether the customer consents to Electronic Notification

PUBLIC - 45

7. Click NEXT

8. If the transaction is approved, the Sales Voucher page will appear and you will need to click on ‘Print Sales Voucher’.

9. Once the Sales Voucher has been printed hand to the customer.

10. If the Add On is declined a message will appear on the screen. Advise the customer to

ring HSBC on the number provided on the screen for further information

PUBLIC - 46

10.2 HSBC Credit Card NOT Present

If a customer wishes to make an interest free purchase and they DO NOT have their card

present instore, you will need to follow the steps below:

4. Ask the customer for 1 form of Photo ID

5. Log in to Connected

6. Click on ‘Apply for an Add On’

7. Click NO “Does the customer have their HSBC Card present?

8. You will then be required to call HSBC on 1300 300 883. The customer will need to

speak with HSBC to obtain their card details.

9. Once HSBC has spoken to the customer and the required verification checks have been

successful, the HSBC Operator will give the customer their:

a. Card Number

b. Expiry Date

10. Click ‘OK’ once the customer is off the phone

PUBLIC - 47

11. You will then be required to complete the Photo ID section:

a. Photo ID type

b. Full Name as it appears on the document

c. Document Number Expiry Date

d. Does the customer consent to Electronic Notification – YES or NO

e. Tick to confirm you have verified the customer’s identity and that the photo

matches to the person that is instore.

f. Click NEXT

9. You will now need to complete the following fields:

a. Card Holder name (as it appears on the card)

b. Card Number

c. Expiry Date

d. Split Transaction

e. Promotional Term

f. Purchase Amount

g. Description of Purchase

h. Tick whether the customer consents to Electronic Notification

i. Click NEXT

PUBLIC - 48

10. If the transaction is approved, the Sales Voucher page will appear and you will need to

click on ‘Print Sales Voucher’.

11. Once the Sales Voucher has been printed hand to the customer.

12. If the Add On is declined a message will appear on the screen. Advise the customer to

ring HSBC on the number provided on the screen for further information

PUBLIC - 49

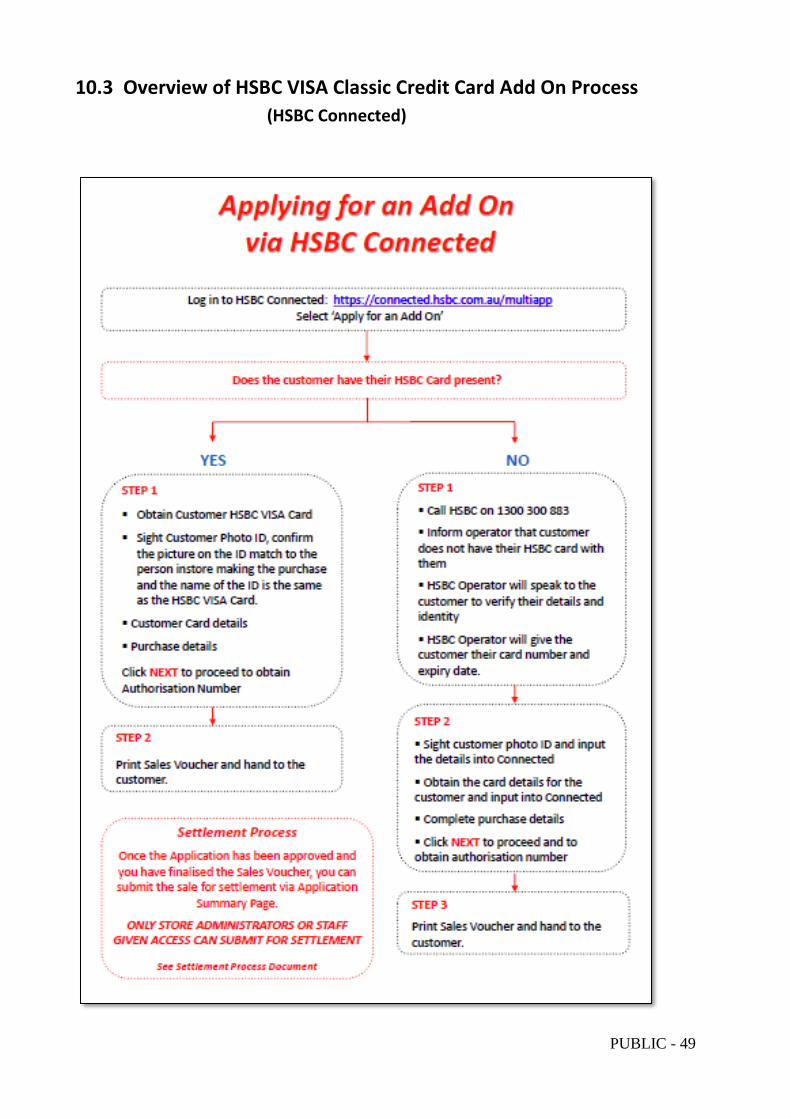

10.3 Overview of HSBC VISA Classic Credit Card Add On Process

(HSBC Connected)

PUBLIC - 50

11.0 SPLIT TRSANSACTIONS

HSBC Connected gives merchants the ability to split a finance transaction into 2 purchases.

By splitting the transaction, you have the ability to settle each purchase at different times. This

means payment by HSBC will be made at the time of each settlement.

When you would do this:

When goods are being delivered at different times.

Where the purchase is made up of goods where a payment is made to a manufacturer

directly, in addition to a merchant.

Note: The Interest Free period will begin at different times for each purchase. The dates are

based on the date which the purchase is settled.

11.1 How to Process a Split Transaction

To split a transaction for either a new application or add on please follow the below steps:

1. On the Sales Voucher, tick the Split Transaction box

2. Select the promotional term. Only one term is available for both transactions.

3. For both Purchases:

a. Input Purchase amount (minimum $500)

b. Select Merchant Number from drop down list

c. Input Description of Purchase

4. Click NEXT

New Application Add On

PUBLIC - 51

5. If the transaction is approved, the Sales Voucher page will appear and you will need to

click on ‘Print Sales Voucher’ (2 sales vouchers will be printed).

6. Once the Sales Vouchers have been printed, hand to the customer.

7. If the Add On is declined a message will appear on the screen. Advise the customer to

ring HSBC on the number provided on the screen for further information

PUBLIC - 52

12.0 CREDIT (REFUND) TRANSACTIONS

HSBC Connected gives merchants the ability to Credit a Sales Voucher once it has been

submitted for settlement.

To process a Credit, follow the below steps:

1. Log into Application Manager and retrieve an application or add on

You will be able to credit any sales that have been settled from the Application Results

Page.

The CREDIT button will be visible once a Sales Voucher has been settled.

2. Once you have clicked on CREDIT button the below Credit Voucher will appear

Complete the Credit Details and click on SUBMIT to process the Credit Voucher

Ensure the credit amount DOES NOT exceed the original purchase amount of that sales

voucher

PUBLIC - 53

3. Once you have clicked on SUBMIT you will receive a Credit Confirmation.

4. Print the Credit Voucher and hand to the customer.

5. The Credit will be listed in the Credit Voucher (Refund History) overnight.

PUBLIC - 54

12.1 Overview of Credit Transaction Process

PUBLIC - 55

13.0 SETTLEMENT A transaction must be settled in order for the merchant to receive payment from HSBC and the customer to be billed for the transaction. Settlement mostly occurs once the customer has received their goods or as pre-arranged with the customer.

13.1 User Access Levels Not all Users will have the ability to ‘Settle’ a transaction once the goods have been delivered to the customer. The Store Administrator will have the access to settle all transactions. Otherwise, if required, the Store Manager or Store Administrator will make the decision of who will be entrusted with this responsibility. For those staff members that will be authorising settlement please select 'Yes' to Settlement Authority when adding a User (Section 15.2) You are able to remove or add this authority to any User by following the Modify User Steps (Section 15.3.1)

13.2 How to Process a Settlement

1. Log into Connected

2. Click on Application Manager

Any New Card Application and Add On Pending Settlements will be listed

PUBLIC - 56

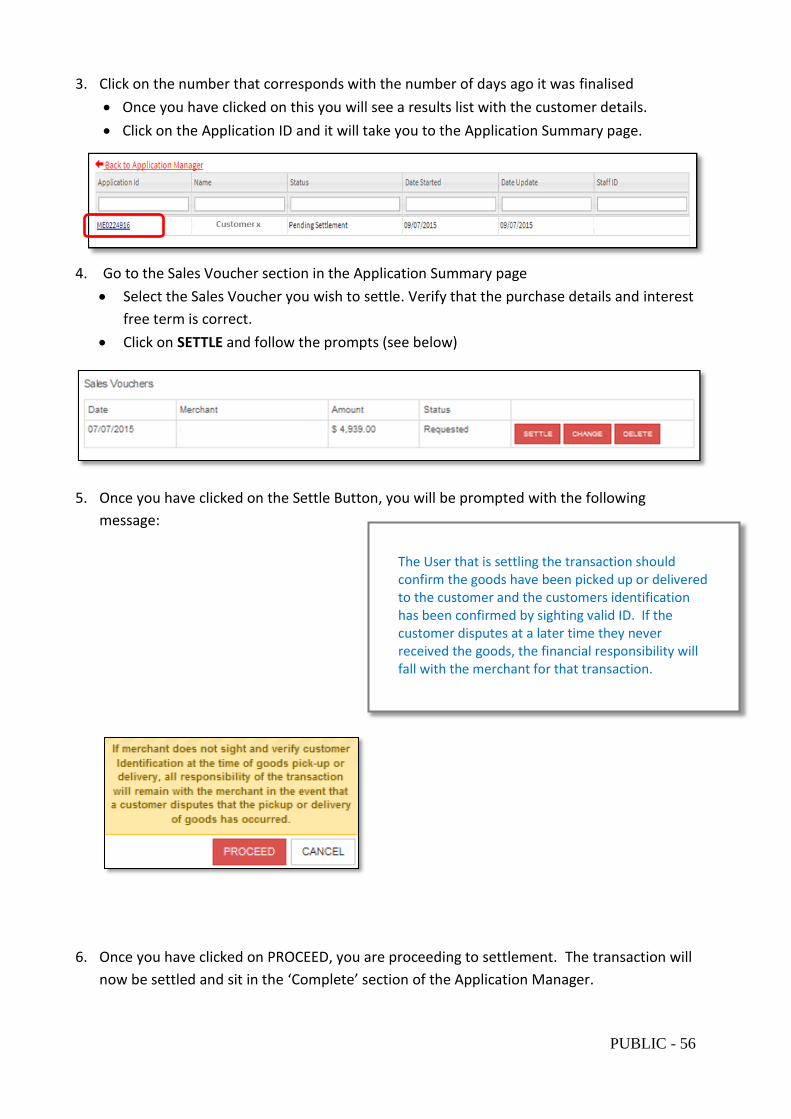

3. Click on the number that corresponds with the number of days ago it was finalised

Once you have clicked on this you will see a results list with the customer details.

Click on the Application ID and it will take you to the Application Summary page.

4. Go to the Sales Voucher section in the Application Summary page

Select the Sales Voucher you wish to settle. Verify that the purchase details and interest

free term is correct.

Click on SETTLE and follow the prompts (see below)

5. Once you have clicked on the Settle Button, you will be prompted with the following

message:

6. Once you have clicked on PROCEED, you are proceeding to settlement. The transaction will

now be settled and sit in the ‘Complete’ section of the Application Manager.

The User that is settling the transaction should confirm the goods have been picked up or delivered to the customer and the customers identification has been confirmed by sighting valid ID. If the customer disputes at a later time they never received the goods, the financial responsibility will fall with the merchant for that transaction.

PUBLIC - 57

7. Settlement Confirmation Page is generated.

13.3 Overview of Settlement Process

PUBLIC - 58

14.0 OTHER HSBC CONNECTED FEATURES

PUBLIC - 59

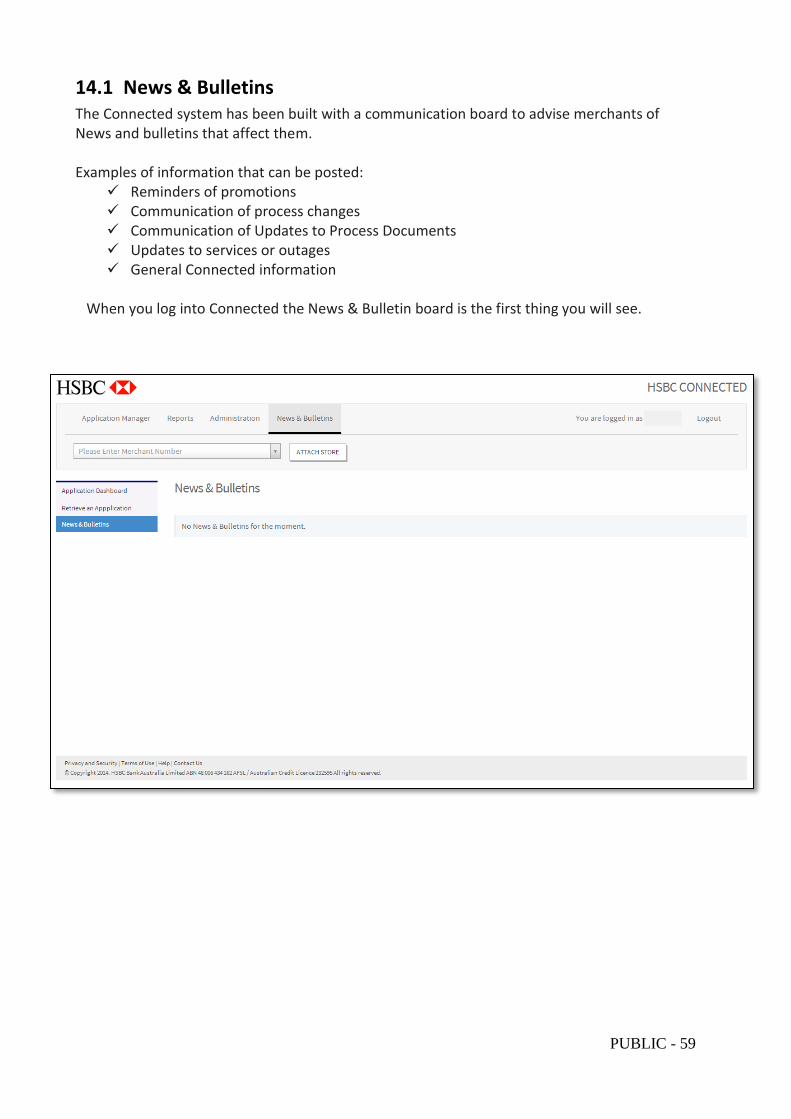

14.1 News & Bulletins The Connected system has been built with a communication board to advise merchants of News and bulletins that affect them. Examples of information that can be posted:

Reminders of promotions Communication of process changes Communication of Updates to Process Documents Updates to services or outages General Connected information

When you log into Connected the News & Bulletin board is the first thing you will see.

PUBLIC - 60

15.0 MERCHANT ADMINISTRATION FUNCTIONS A Merchant Administrator has the following access assigned to them:

• Input application • Input Add-On Sales Voucher • Change or Delete Sales Voucher details prior to settlement • Settle Sales Vouchers • Input and Process Credit (Refund) transactions • Retrieve instore and apply from home applications • Create and maintain store users

To Access the Administration functions, click on the ‘Administration’ link:

15.1 Settlement Access A transaction must be settled in order for the merchant to receive payment from HSBC and the customer to be billed for the transaction. A Merchant Administrator will have access to settle all transactions that have been processed instore, that is, both New Applications and Add Ons. See Section 13.0 Settlement for process outlines.

PUBLIC - 61

15.2 Add User

To create new users please follow below steps:

1. Click on ‘Add User’ 2. Complete the User Details Section A

Username: Must be a minimum of 5 characters and must contain both letters and numbers. NO special characters or spaces.

Complete remaining User Details

Section B

Roles: - Store Staff will not have settlement access - Settlement Staff will have settlement access

Input Store Merchant Number

Training Mode: - We recommend that you select YES in training mode when you set up a new employee. This allows the employee to practice entering applications without submitting them. See section 15.4. For employees already trained select NO.

3. Click on SAVE

4. A User ID and Password is then generated for the new user. Please ensure you give this information to the new user as they are required in order to log in.

A

B

PUBLIC - 62

15.3 Manage Existing User

It is important that you check things like the spelling of names before you create the user ID.

Occasionally, however, you might need to change the details and/or access level of a user. You

may also have been asked to reset the password for one of the employees in your store.

15.3.1 Modify an existing user: 1. Click on the Administration link.

2. Click on the ‘Manage Existing User’ link

3. You can search for the User you wish to manage using the user’s Last name or Username.

You can also just select the User from the list by clicking on the link.

4. Click the ‘Edit’ button and make the changes that you need to. Once all changes are made

click ‘Save’.

PUBLIC - 63

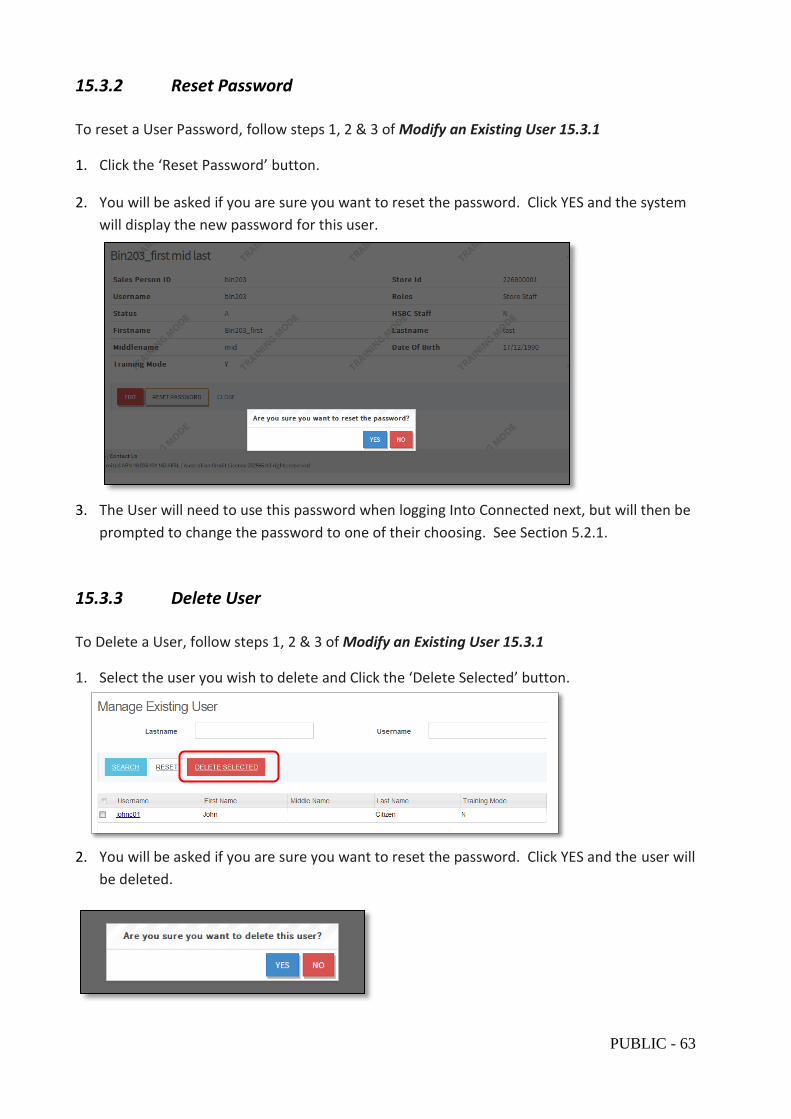

15.3.2 Reset Password To reset a User Password, follow steps 1, 2 & 3 of Modify an Existing User 15.3.1

1. Click the ‘Reset Password’ button.

2. You will be asked if you are sure you want to reset the password. Click YES and the system

will display the new password for this user.

3. The User will need to use this password when logging Into Connected next, but will then be

prompted to change the password to one of their choosing. See Section 5.2.1.

15.3.3 Delete User To Delete a User, follow steps 1, 2 & 3 of Modify an Existing User 15.3.1

1. Select the user you wish to delete and Click the ‘Delete Selected’ button.

2. You will be asked if you are sure you want to reset the password. Click YES and the user will

be deleted.

PUBLIC - 64

15.4 Training Mode Training Mode is available to all staff and can be set up for training by a Store Administrator. Training mode means that the team member can practice navigating through Connected and entering applications without interacting with the live system. Once the new user is confident that they can use Connected effectively, you can move them out of training mode When you create a user ID for a new employee it is a good idea to move them into training mode. To place a user into training mode, select 'Yes' when setting up a new user. To take a User off Training Mode (so they can use the live version of Connected) follow the steps to 'Modify a User' 15.3.1 and change your selection from 'Yes' to 'No'.

PUBLIC - 65

16.0 HSBC ShopSmart Welcome to the ShopSmart Payment Option from HSBC that will allow our customers to make Interest Free purchases through your online shopping cart. This overview is to be used with the suggested ShopSmart Flow – Merchant document and is designed to introduce you to the Operating Flow, Technical Integration Requirements and Customer Experience. The ShopSmart payment option is designed to offer all your online shopping customers the opportunity to make interest free purchases through your shopping cart. To do this we must classify shoppers into two categories:

• Non HSBC Customers will use the New App - Shop Cart flows

• Existing HSBC Credit Card Customers will use the Add On - Shop Cart flow

16.1 New Application

Non HSBC Customers will need to go through the HSBC Credit Card application process. Once Approved the customer will qualify for Interest Free purchases. The Application process will follow the existing SWIFT application process with one additional step. Once Approved the customer will need to view and acknowledge the Credit Contract and Product Schedule online to be able to load an Interest Free transaction straight away. HSBC will validate this when confirming the purchase. There are three ways a new HSBC customer can load an Interest Free transaction onto their account once Approved;

1) They can use their approved application number and DOB in the merchant shopping cart to load ONE Interest Free transaction. The only additional restriction to a normal Credit Card transaction is that the goods must be delivered to the same address the applicant has entered as their residential address on their credit card application. A merchant can choose to manually check the delivery address is the same as the residential address on file using Connected, or send HSBC the delivery address nominated to be validated. HSBC will validate this address when confirming the purchase.

2) The customer can visit one of the merchant’s stores. The merchant staff member will be able to locate the approved application through HSBC Connected system. They can print the Contract in store and follow their in store process outlined previously in this document.

3) The customer can wait 5 - 10 working days for their credit card to arrive in the mail. Once received and activated the customer can use the Add On function explained below to finalise their Interest Free purchase.

PUBLIC - 66

Please Note: It is expected that if asked by HSBC, the merchant will be able to verify what address goods were delivered. If the merchant takes on the responsibility of manually checking the delivery address is the same as the residential address in Connected, and fails to deliver goods to the address in Connected, HSBC has the right to recoup transaction funds from the merchant if the transaction is found to be fraudulent.

16.2 Add On

Existing HSBC Customers will be able to load Interest Free purchases on their HSBC Credit Cards by supplying the same account information as a normal online credit card purchase. By supplying their Card Number, Name on the Card, card CVV number and Expiry Date, HSBC can validate a transaction. The transaction will be subject to the same validations as a normal credit card transaction as well as the Interest Free characteristics.

16.3 Merchant Information

When merchants send HSBC transaction information to be validated, they will also accompany that data with information relating to the merchant. This includes:

• A User ID and Password provided to the merchant by HSBC to verify merchant

identification.

• The Interest Free term that must be loaded and current for the merchant.

• Group and/or Store ID that must match the Group and/or store the application has

originated from when using Approved Application number to load ONE transaction.

16.4 Customer Information

As per the In Store finance option, HSBC requires the customer to receive a Sales Voucher with certain information regarding the approved Interest Free transaction. The merchant is responsible for generating a Sales Voucher for the customer to print with the following information displayed:

• Transaction Date

• HSBC Authorisation Number

• Financed Amount

• Interest Free Term

PUBLIC - 67

• Card Number (first 12 digits must be truncated)

16.5 System Support

In the event there is a System failure the merchant can log the issue with HSBC by calling their HSBC Account Manager. HSBC can then investigate the cause and advise when resolved. Please Note: HSBC has scheduled system maintenance each night from Monday to Friday from 10pm - 2am EST. Both the New App and Add On functions will be down during this time.

16.6 Connected and Settlement

The HSBC ShopSmart facility will be linked to our HSBC Connected system. This will allow merchants a one central system to manage their Interest Free transactions. A customer will have two options to receive their goods. They can have the goods delivered to a nominated address or choose to go to a merchant store to pick up the goods. Delivery: If a customer wishes to have their goods delivered, the approved transaction will show in an 'Online Merchant Store' sign in within the Connected system. The merchant can then change, settle and credit transactions as they do today. Pick Up: If a customer nominates a merchant store they would like to visit to collect their goods, the approved Interest Free transaction will appear in that stores application manager in Connected. The store staff can follow the in store process to change, settle, or credit the transaction when the customer has collected their goods.

16.7 Technical Requirements

Technical requirements and specification documents can be provided on request. Please contact your Account Manager to organise these document and to have any of your questions answered.

PUBLIC - 68

17.0 Manual Application Form

17.1 When to Use the Manual Application Form

The Manual Application Form is only to be used by merchant in the following circumstances: o HSBC Connected system is down o Store is busy and unable to process application due to resource constraints

17.2 Operating Process for Manual Application Form

The below steps are to be used when using the Manual Application Form:

COU Booklet must be provided to the customer

KFS Sheet must be provided to the customer

COU Booklet number must be recorded on the application form

Customer completes application form

Merchant staff check form to ensure all fields are completed

Merchant staff enter application into HSBC Connected using the recorded COU booklet number and submit for decision

Decision: o Approved – Merchant contacts the customer to arrange for them to return to

store. Once the customer returns to the store, the Merchant will provide the customer a copy of the contract, schedule and sales voucher. The customer can then collect their goods.

o Conditionally Approved – Merchant contacts customer and informs them of the required documentation. The customer can either upload the documents via ‘image & attach’ at home or return to the store with the documents for the Merchant to send to HSBC

o Decline – Merchant contacts the customer and informs them of Decline decision.

Application must be destroyed to mitigate data loss.

17.3 Location of the Manual Application Form

A copy of the Manual Application Form can be found on the HSBC Merchant Services Page.

PUBLIC - 69

18.0 FREQUENTLY ASKED QUESTIONS

18.1 Merchant Questions Q: What is the minimum amount that we can offer a customer who wants to use finance?

A: For HSBC's Visa, the minimum purchase amount is $500 and the minimum limit approved is $1,000. Q: What is the maximum amount a customer can apply for?

A: HSBC's Visa Classic Credit Card has a maximum limit of $50,000. HSBC assesses each application and approves a credit limit based on the applicant's individual circumstances. Q: Does an existing HSBC Credit Card customer have to complete an application form again when they want to buy something else on a promotional term (e.g. 12 months interest free)?