Embed Size (px)

Citation preview

9M2019

RESULTS ANNOUNCEMENT

Nov 2019

1

2

01 Opening speech

02 VPBank: 9M2019 results

03 FE Credit: 9M2019 results

05 Closing speech

04 Q&A

3

01 VPBank Snapshot

02 Review of 9M2019 Results

03 Investment Recaps

• Consolidated

• Bank standalone

• FE Credit

Page 04 - 11

Page 12 - 35

Page 36 - 39

Page 13 - 19

Page 20 - 31

Page 32 - 35

Snapshot

4

VPBank

CPI: 2.5%

Lowest growth within past 3 years

GDP: 6.98%

Highest 9 months within past 9 years Credit growth: 8.95%

Lowest growth rate since 2014

PMI: 50.5 Lowest since February 2016

OPERATING ENVIRONMENT

FDI disbursement trade: 7.31%

Deposit growth of

financial institution: 8.68%

Vietnam* Banking Sector**

* Y-o-Y (except PMI)

Source: GSO, SBV, as at 30 Sep 2019

**YTD

Core inflation: 1.91%

Growth of export volume: 8.2%Hitting USD 194.8 bil

Bad debt ratio (on BS): 1.91%

5

1993 2006 2010 2012 2014 2015 2017 2018 2019

Established as Vietnam

Joint Stock Commercial

Bank for Private Enterprises

Established two

subsidiaries: VPBank

Securities and VPBank

Asset Management

Renamed Vietnam Prosperity

Joint Stock Commercial Bank

Engaged McKinsey for

overhauling business and

operating models

Announced 2012 - 2017

strategy, focusing on Retail

and SME

Acquired Vinacomin Finance

and renamed VPBank Finance

Company

Launched Household

(Commcredit) and Digital

Banking businesses

Sold VPBS

IPO – Listed on HOSE

Selected in VN30

DEVELOPMENT HISTORY

Corporate Governance

showcase in Vietnam

Cir 41 early adoption

starting 1 May 2019

6

Total Assets Active Customers TOI PBT Total Issued Share Market Cap.*

7

VPBank AT A GLANCE Accumulated as at 30.09.2019

Bil VND

358,236Million

6.3Bil VND

26,334Bil VND

7,199 Million

2,530 55,787

Full coverage of all

banking segments

Highly centralized

and specialized

organization model

Basel II (Circular 41) –

Pillar 3 disclosure

starting 30 Sep 2019

Basel II (Circular 41) – SBV

approval for early adoption

starting 01 May 2019

Corporate Governance

showcase in Vietnam

by IFC

*Closed price at 30.09.2019

Bil VND

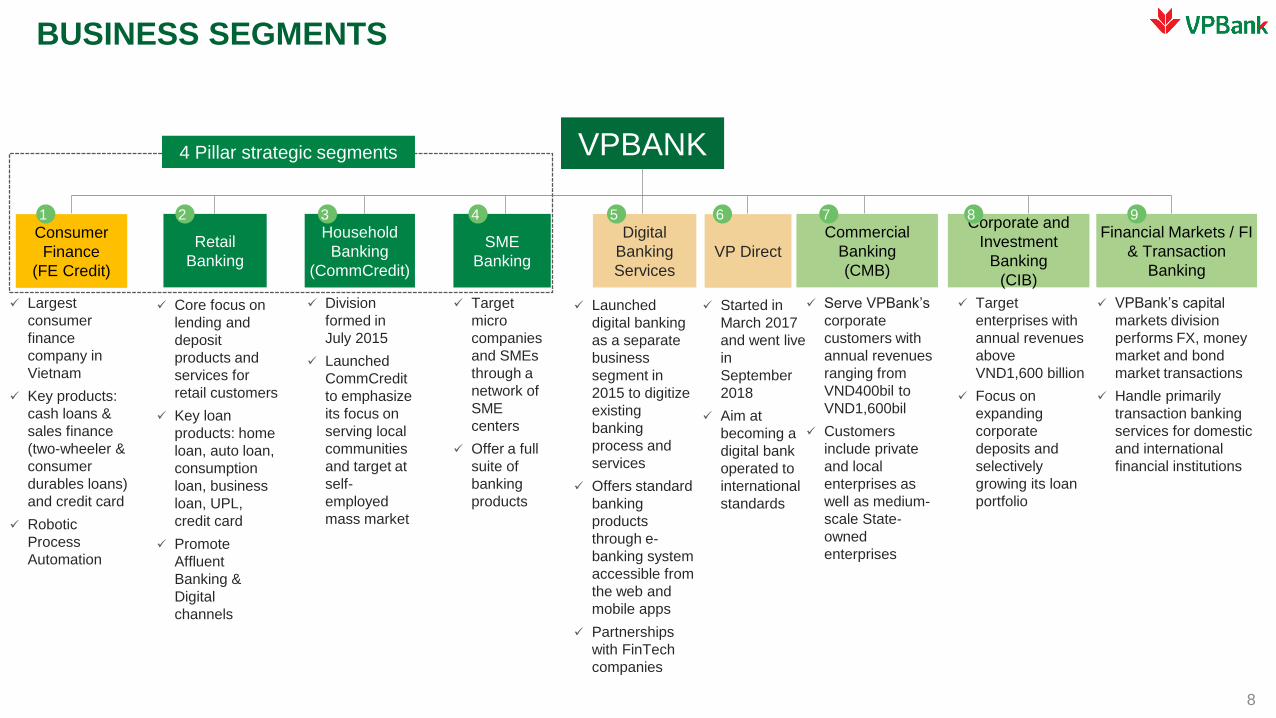

BUSINESS SEGMENTS

Consumer

Finance

(FE Credit)

Digital

Banking

Services

VP Direct

Corporate and

Investment

Banking

(CIB)

Launched

digital banking

as a separate

business

segment in

2015 to digitize

existing

banking

process and

services

Offers standard

banking

products

through e-

banking system

accessible from

the web and

mobile apps

Partnerships

with FinTech

companies

VPBANK

Retail

Banking

Commercial

Banking

(CMB)

Financial Markets / FI

& Transaction

Banking

Household

Banking

(CommCredit)

SME

Banking

1 2 3 4 5 6 9

Core focus on

lending and

deposit

products and

services for

retail customers

Key loan

products: home

loan, auto loan,

consumption

loan, business

loan, UPL,

credit card

Promote

Affluent

Banking &

Digital

channels

Division

formed in

July 2015

Launched

CommCredit

to emphasize

its focus on

serving local

communities

and target at

self-

employed

mass market

Target

micro

companies

and SMEs

through a

network of

SME

centers

Offer a full

suite of

banking

products

Serve VPBank’s

corporate

customers with

annual revenues

ranging from

VND400bil to

VND1,600bil

Customers

include private

and local

enterprises as

well as medium-

scale State-

owned

enterprises

VPBank’s capital

markets division

performs FX, money

market and bond

market transactions

Handle primarily

transaction banking

services for domestic

and international

financial institutions

7

Target

enterprises with

annual revenues

above

VND1,600 billion

Focus on

expanding

corporate

deposits and

selectively

growing its loan

portfolio

8

Started in

March 2017

and went live

in

September

2018

Aim at

becoming a

digital bank

operated to

international

standards

4 Pillar strategic segments

Largest

consumer

finance

company in

Vietnam

Key products:

cash loans &

sales finance

(two-wheeler &

consumer

durables loans)

and credit card

Robotic

Process

Automation

8

Distribution network - Bank branches

Hanoi: 65

North: 23

Red River Delta: 23North Central coast: 39

South Central coast: 4

Central highlands: 3

Southeast: 9

Ho Chi Minh City: 46

Mekong River Delta: 15

KEY FOOTPRINT METRICS

9

5,100 5,767 6,285

2017 2018 9M19

Activecustomers

Active customers & Number of cards issued*

• 26,733 employees

• 227 branches and 84 SME centers & hubs

• Nearly 650 branded ATMs/CDMs

Transaction points 30.09.2019 31.12.2018

Retail branches 227 222

SME centers and hubs 84 83

Household centers

(CommCredit)55 171

Corporate banking

branches4 4

FE Credit>12,000 POS

>34,000 POC

>12,000 POS

>34,000 POC

ATM/CDM 460/183 480/154

+ 9.0%

Physical distribution channels

1,832 3,787 5,171Total number of

cards issued *

*Including credit & debit cards

(Thousands)

10

CAPITAL PLAN IN 2019

Batch 1Maximum 50 million shares equivalent

to 1.976% of charter capital

Reacquisition of issued shares

• Completed in Oct 2019

• Acquired 50 million shares with

average price of VND 22,194

• Increasing the total of number treasury

stock to 123.2 million, equivalent to

4.87% of charter capital

On- going process

ESOP

Issuance of 31 million shares

to qualified employees

Rescheduled to 2020

Private placement

Issuance to local & foreign

investors to raise charter

capital

Batch 2 Batch 3

RISK GOVERNANCE – Basel II (SBV Circular 41) compliance

20172015 2016

Establishment

Stabilizing operation

Accelerating progress

2018 2019 2020

Full compliance

SBV approval

of compliance

• Early adoption and CAR reporting

to SBV starting 1 May 2019

• Pillar 3 disclosure starting 30 Sep

2019 on semi-annual basic

• ICAAP implementation in

place

ICAAP

11

• Basel 2 implementation

master plan was

submitted to the SBV

• Calculation solution was built,

enabled monthly CAR report;

• ICAAP implementation was

initiated.

• Requirement on Pillar 1 was

fully completed;

• Embedded CAR in business

decision making;

• Risk governance framework

was significantly enhanced

following Pillar 2 requirement.

• CAR was disclosed;

• ICAAP implementation was

approaching completion.

Review of

CONSOLIDATED

BANK STANDALONE

FE CREDIT

12

9M2019 Results

13

9M2019 – FINANCIAL HIGHLIGHTS

Strong credit growth outpaces sector average

#1 TOI amongst private commercial banks; driven by continued growth of NII and NFI

• TOI of 3Q19 grew by 25% compared with 3Q18 and 7.1% vs. 2Q2019

PBT completed 76% of full year target, reflected positive momentum in earnings capability

Efficiency ratios remain among the best-in-class: CIR (34.7%), NIM (9.7%), ROA (2.3%), ROE (20.5%)

• VPBank’s credit growth was at 14.7% compared with 8.95% sector average (*)

• TOI reached 26,334 bil VND, increasing by 19.1% Y-o-Y or 23.9% if excluding one off bancassurance income

• 9M PBT, reaching 7,199 bil VND, grew by 17.5% Y-o-Y or 36.6% if excluding one-off gain from bancassurance

upfront in previous year

1.

2.

3.

4.

5.

Enhance Asset Quality and continue to improve portfolio management

(*) According to the Press release on socio-economic situation in Quarter III and 9 months 2019 - General Statistics Office

• NPL ratio in accordance with Circular 02 significantly reduced from 4.2% at 30 Sep 2018 to 3.1% at 30 Sep 2019

Acceleration to beat full year targets

Consolidated

• NFI doubled Y-o-Y, which is in line with the Bank’s target to grow Non NII

• Big effort to decrease ratio of NPL add back VAMC from 5.9% at 30 Sep 2018 to 3.4% at 30 Sep 2019

26,334

9M2019 – FINANCIAL HIGHLIGHTS

TOI PBT

Source: Unaudited Consolidated FS at 30.09.2019

Target

Balance Sheet 30.9.2019 30.6.2019 31.12.2018 %Q-o-Q %YTD

Credit to customers 264,762 256,379 230,790 3.3% 14.7%

Total assets 358,236 348,732 323,291 2.7% 10.8%

Deposits from customers (including valuable

papers)263,119 251,118 219,509 4.8% 19.9%

NPL Cir 02 3.10% 3.01% 3.21%

CAR Cir 41 (Basel II) 11.36% 11.24% 11.16%

CAR Cir 36 11.69% 12.30% 12.27%

CIR

34.7%

Unit: bil VND

9M2019

% Y-o-Y 19.1%

% Y-o-Y

normalized*23.9%

* Exclude one-off income in 2018 14

80%Progress status

76%Progress status

7,1999M2019

% Y-o-Y 17.5%

% Y-o-Y

normalized*36.6%

NIM

9.7%

ROA

2.3%

ROE

20.5%

Consolidated

Acceleration to beat full year targets

65%

66%

35%

34%

FY2018

9M2019

Secured Unsecured

66.8%77.2% 74.3%

32.9% 24.4%36.5%

9M2018 FY2018 9M2019

LLR on & off BS Specific LLR on & off BS

Loans to customer by tenor** (%)

211

,09

2

23

0,7

90

26

4,7

62

4.24%3.21% 3.10%

9M2018 FY2018 9M2019

Credit growth NPL Cir 02

Credit growth, NPL (Bil VND, %)

+14.7%

Source: Unaudited Consolidated FS at 30.09.2019

CREDIT PORTFOLIO (*)

15

35%

43%

22%

9M2019

33%

45%

22%

FY2018

Short

Mid

Long

**Short (<1yr), Mid (1yr – 5yr), Long (>5yr)

Consolidated

LLR & Specific LLR on & off BS (%)

* Including Corporate bonds

Credit by type (Bil VND, %)

+ 24,432 + 9,540

+ 16.3% + 11.7%

230,790

264,762

25

3,0

40

27

7,8

51

30

5,5

47

21

2,7

01

21

9,5

09

26

3,1

19

9M2018 FY2018 9M2019

Total Funding

Customer deposits &Valuable papers

FUNDING

16Source: Unaudited Consolidated FS at 30.09.2019

77.9% 73.5%77.1%

6.1% 5.5%9.0%

4.8% 4.6%2.6%

10.2% 14.9% 10.6%0.9% 1.5% 0.7%

9M2018 FY2018 9M2019

Others

Interbank funding

Term loans

Bonds

Customer deposit(*)

Funding growth (Bil VND, %)

Funding by currency (%)

10.0%

Funding by type (%)

Funding by original tenor*(%)

* Including customer deposit & CD

* Short (<1yr), Mid & Long (>1yr)

Consolidated

19.9%

88.7% 88.6%VND

10.9%USD 11.1%

FY2018 9M2019

Others 0.3%0.4%

27.2% 35.6%Short

72.8%Mid & Long 64.4%

FY2018 9M2019

11.97%

11.16%11.36%

10.98%

10.45%10.76%

9M2018 FY2018 9M2019

CAR Basel II Tier 1

31

,98

7

34

,75

0

40

,49

1

25,3

00

25

,30

0

25

,30

0

9M2018 FY2018 9M2019

Equity

Chartered Capital

13.03% 12.27% 11.73%

11.62% 11.19% 10.83%

9M2018 FY2018 9M2019

CAR Cir 36 Tier 1

Capital Adequacy Ratios under Cir 36 (%)

9.3 9.3 8.8

9M2018 FY2018 9M2019

Equity multiplier

Equity and Chartered Capital (Bil VND, %)

16.5%

Capital Adequacy Ratios under Cir 41 ( Basel II,%)

CAPITAL BASE

17Source: Unaudited Consolidated FS at 30.09.2019

SBV

requirement8%

SBV

requirement9%

Consolidated

22,428

26,334

7,199

1,942

( 9,142 )

560 ( 9,993 )1,404

NII NFI Net gain fromfinancial assets

Other income TOI Provision expense OPEX PBT

18Source: Unaudited Consolidated FS at 30.09.2019

%Y-o-Y +23.3% +93.4% +17.3% +19.1% +21.9% +17.3% +17.5%-42.6%

Double digit profit growth, reflected momentum to beat full year target with consistent NII increase and stronger NFI

Continued focus on expenses management & efficiency

9M2019 OPERATING PERFORMANCE

%Y-o-Y

normalized*+23.9% +36.6%

*Exclude one-off income in 2018

-11.5%

Consolidated

85% 86% 85%

6% 5% 7%9% 10% 7%

36.0% 36.7% 34.7%

9M2017 9M2018 9M2019

Others

NFI

NII

TOI components and CIR* (%)

19

15.3% 15.2% 15.7%

9.1% 9.3% 9.7%

6.4% 6.2% 6.5%

9M2017 9M2018 9M2019

Yield NIM Cost of fund

Yield, COF, NIM annualized (%)

37%

35%

38%

38%

25%

27%

0% 20% 40% 60% 80% 100% 120%

9M2018*

9M2019

OPEX Provision expense PBT

OPEX, Provision expense & PBT over TOI (%)

* CIR excluding one – off income in 2018

9M2019 PROFITABILITY METRICSThanks to strong growth in returns, profitability metrics have been improved

Source: Unaudited Consolidated FS at 30.09.2019

2.0% 2.3%ROA Normalized*

2.3%ROA

ROE

2.3%

21.2% 20.5%

9M2018 9M2019

ROA, ROE annualized (%)

Consolidated

ROE Normalized* 20.5%18.2%

CONSOLIDATED

BANK STANDALONE

FE CREDIT

20

Review of

9M2019 Results

9M2019 – FINANCIAL HIGHLIGHTS

30.9.2019 30.06.2019 31.12.2018 %Q-o-Q %YTD

Balance Sheet

(Bil VND)

Credit to customer 204,537 198,190 177,520 3.2% 15.2% • Resilient credit growth,

higher than market

average

• Asset quality is well-

managed with stable

NPL ratio

NPL Cir 02 2.45% 2.38% 2.41%

NPL add back

VAMC2.84% 3.02% 4.01%

Deposit & valuable

paper issued231,503 219,362 192,402 5.5% 20.3%

• Liquidity position

remained at comfort

level, internal LDR at

81.9%

9M2019* 1H2019* 9M2018* %Q-o-Q Y-o-Y

Profitability

(Bil VND)

TOI 12,402 7,849 9,854 11.8% 25.9%

• Sustained TOI growth

driven by healthy NII &

NFI boost

OPEX 4,813 3,238 4,311 -4.3% 11.6%• Assertive cost

optimization

Provision Expenses 3,879 2,385 2,553 20.6% 51.9%

• Provision increase due

to the attempt to clear

VAMC

PBT 3,711 2,226 2,990 24.7% 24.1% • PBT contributed 52% to

consolidated PBT.

Efficiency metrics

remain amongst top

banks in the market

CIR** 38.8% 41.3% 43.7%

ROE annualized 16.3% 15.0% 14.9%

Source: Unaudited Single FS at 30.09.2019

Bank Standalone

21*Exclude income from subsidiaries + one-off income **CIR excluding one – off income in 2018

16

4,4

15

17

7,5

20

20

4,5

37

4.24%3.21% 3.10%

9M2018 FY2018 9M2019

Credit growth NPL Cir 02

CREDIT PORTFOLIO (*)Strong credit growth with asset quality under control. Big effort to clear off VAMC balances is on track.

+15.2%

Credit growth(%, Bil VND)

5.73%

4.01%

2.84%

3.68%

2.41% 2.45%

9M2018 FY2018 9M2019

NPL add back VAMC %NPL Cir 02

NPL Cir 02, NPL add back VAMC(%)

37%

17%2%

44%

9M2019

39%

17%3%

41%

FY2018Retail

SME

Comm.Credit

Others

** Including Corporate bonds + VAMC

Credit portfolio by segments**(%, Bil VND)

Credit portfolio by type(%, Bil VND)

84%

85%

16%

15%

FY2018

9M2019

Secured Unsecured

* Including Corporate bonds

+ 24,559 + 2,458+ 16.4% + 8.8%

Source: Unaudited Single FS at 30.09.2019 22

Bank Standalone

177,520

204,537

FUNDINGDiversify funding source and in full compliant with regulatory requirements

Customer deposits & Valuable papers by

customers & tenor**(%)

73.6% 73.7% 75.9%

89.6% 92.3%81.9%

34.6% 33.6% 27.8%

9M2018 FY2018 9M2019

LDR Internal LDR Short term fundings for MLT loans

LDR & ST funding for MLT loans (SBV requirement)(%)

Source: Unaudited Single FS at 30.09.2019 23

Bank Standalone

78.9% 75.3%80.4%

6.9% 5.9%10.0%2.1% 1.8%1.2%

11.0% 15.2%7.5%

1.1% 1.8% 0.9%

9M2018 FY2018 9M2019

Others

Interbank funding

Term loans

Bonds

Customer deposit(*)

Funding by types(%, Bil VND)

* Including customer deposit & CD

60% 58%Retail

40%Corporate 42%

FY2018 9M2019By customers

73% 59%Short

27%Mid & Long 41%

By tenors

21

3,9

65

23

6,9

53

256,0

26

18

3,5

24

19

2,4

02

23

1,5

03

9M2018 FY2018 9M2019

Funding growth

Customer deposits& Valuable papersgrowth

Funding Growth(%, Bil VND)

** Short (<1yr), Mid & Long (>1yr)

8.0%

20.3%

24

RETAIL – AFFLUENT BANKINGSustained growth momentum in Retail Affluent Banking segment

Client Profession

Business concentrations in Q3 – 2019

AF client insight & growth

Business

Owner 60% Senior Manager

& Salaried 30% Rich retiree

& Others 10%

2Financials:

Net Promoter Score (NPS) has been

maintained around 90% during the year,

while client attrition rate has been well-

managed down from 2.2% to 1.6%/ month.

Wealth product sales has tremendous

movement in volume

Besides market expansion strategy, AF

has deepened farming on the segment. Deposit up 13% Y-o-Y; 75%

contribution to RB deposits

CASA balance up 43% Y-o-Y

TD up 32% Y-o-Y

NFI up 28% Y-o-Y

TOI per AF customer up 20%

Number of AF Client up 20% Y-o-Y

High-Net-Worth program with high

privileges to clients with AUM from VND

10 bil has been launched since August

to grow faster in this sub-segment.

1

3 4

Bank Standalone

TOI continued to grow due to sustained growth in NII &

stronger Non-NIITotal operating income for 9M2019 grew 25.9% Y-o-Y with big contribution from NII & resilient growth of Non-NII. Non-NII rose dramatically

54.9% thanks to big increase of NFI. On a quarterly basis, 3Q19 total operating income growth was 11.8% higher than the previous quarter

9M TOI*(%, Bil VND)

7,727 9,108

2,127

3,294

9M2018 9M2019

Non-NII

NII

* Excluding one-off income & income from subsidiaries

9,854

12,402

25.9%

+17.9%

+54.9%

Source: Unaudited Single FS at 30.09.2019

Bank Standalone

25

2,519 2,732 2,921 2,913 3,274

980 1,474 854 1,161

1,279

3Q18 4Q18 1Q19 2Q19** 3Q19

**Exclude income from subsidiaries

11.8%

3,7754,074

4,553

TOI by quarters*(%, Bil VND)

%Y-o-Y

4,207

3,498

Healthy NII was propelled by credit growth and high NIMIn 9M2019, NII rose by 17.9% y-o-y thanks to consistent credit growth and high NIM. YTD credit growth by end of September 2019 was 15.2%,

much higher than the ratio of the same period last year. High credit growth also helped NII in 3Q19 to grow by 12.4% q-o-q.

7,727

9,108

9M2018 9M2019

9M NII(%, Bil VND)

2,519 2,732

2,921 2,913 3,274

3Q18 4Q18 1Q19 2Q19 3Q19

17.9%

12.4%

Source: Unaudited Single FS at 30.09.2019

Bank Standalone

26

Yield, COF, NIM annualized(%)

10.0% 10.1% 10.3% 10.3%10.8%

4.5% 4.7% 4.8% 4.6%4.9%

5.6% 5.6% 5.7% 6.0% 6.1%

3Q18 4Q18 1Q19 2Q19 3Q19

Yield NIM Cost of fund

NII by quarters(%, Bil VND)

27

Non-NII increased significantly with big contribution of growth

from NFI & Income from bad debt recoveries In 9M2019, non-NII increased by 54.9% Y-o-Y thanks to a significant increase in NFI and Income from bad debt recoveries.

NFI grew by 51.6% Y-o-Y among which income from insurance services takes account for the biggest contribution (more than 50%). Income from

credit cards has gradually increased, in line with the Bank’s aggressive strategy in expanding this product.

Income from bad debt recoveries which doubled compared with last year is attribute to effective collection

9M Non – NII*

NFI

Income from

bad debt recovery

Others

1,077

1,632

337

732

713

930

9M2018 9M2019

54.9%

2,127

3,294

+51.6%

+117.2%

+30.3%

* Excluding one-off income & income from subsidiaries

Fee income structure(%) 9M2018 9M2019

31%

24%

23%

14%

8%Income from credit cards

Insurance service

Payment services

Consulting services

Others

Source: Unaudited Single FS at 30.09.2019

Bank Standalone

33%

23%

25%

10%

9%

Fee income types growth9M2018 9M2019

355

518

Payment

services

+45.8%

218

199

Consulting

services

-8.5%

360

476

Insurance

service

+32.2%

477

679

Income from

credit cards

+42.3%

11

3

193

Others

+71.4%

(%, Bil VND)

(%, Bil VND)

%Y-o-Y

2Q19 31.12.2018 2Q182Q19

Vs. 2Q18

MARKET

Card in force

('000)4,284 4,014 3,703 15.67%

GDV (USD mil) 9,983 8,595 6,769 47.48%

Card in force

('000)452 416 300 50.52%

GDV (USD mil) 1,912 1,548 1,152 65.98%

SHARE OF

VPBANK

Card in force

('000)11% 10% 8%

GDV (USD mil) 19% 18% 17%

RETAIL BANKING – Credit Card Story

28Source: Market Card report as at 30.06.2019

GDV = Gross dollar value

Card in force = Accumulated number of active cards

425

690 886

64.0%67.7%

71.8%

FY2017 FY2018 9M2019

Number of Credit cards issued Active rate credit cards*

Credit cards issued

Spending per active card per month**

** Spending per active card per month of retail customers

6.4

11.59.9

10.6

FY2017 FY2018 9M2018 9M2019

Bank Standalone

(%, thousands)

(Mil VND)

* Active rate of retail customers

Market share of

Credit Card

Net profit increased dramatically as TOI outpaced OPEX

9M2019 PBT grew 24.1 % Y-o-Y thanks to growth of TOI (25.9% y-o-y excluding one-off income) outweighs that of OPEX (11.6% y-o-y). OPEX

is well-managed, showing by decrease of OPEX over the quarter. 3Q19 OPEX was 4.3% lower than the previous quarter, which leads to better

improvements of CIR.

9M TOI(%, Bil VND)

PBT

Provision Expense

OPEX

2,990 3,711

2,553

3,879

4,311

4,813

9M2018* 9M2019

25.9%

+24.1%

+51.9%

+11.6%

9,854

12,402

1,039 1,232 1,036 1,190 1,485 725 1,179 1,147 1,239 1,494 1,735

1,795 1,593 1,645 1,574

3Q18 4Q18 1Q19 2Q19 3Q19

12.5%

4,5533,775 4,074

**Exclude income from subsidiaries

* Excluding one-off income & income from subsidiariesSource: Unaudited Single FS at 30.09.2019

Bank Standalone

TOI by quarters

29

%Y-o-Y

OPEX structure, CIR

861 841 853 839 776

268 293 262 272 286

214 266 160 183 196

393 396 318 351 316

49.6%42.7% 42.2% 40.4%

34.6%

3Q18 4Q18 1Q19 2Q19** 3Q19

Others

Administrativeexpenses

Fixed assetexpenses

Personnelexpenses

CIR

(%, Bil VND)

(%, Bil VND)

4,207 3,498

30

New

Capabilities

DIGITAL TRANSFORMATION

Top-line growth

(with new revenue stream)

Higher productivity

Lower cost base

(without impact to

customer services)

Acquire & Migrate

Transact & Engage

Business

Transformation

Become one of the top 3 most

VALUABLE banks in Vietnam by 2022

Become the most consumer friendly

bank through technology

VPBank’s digital transformation aims to deliver a distinctive customer value proposition

Bank Standalone

DIGITAL TRANSFORMATION

Market leading customer on-boarding engine

1

• 63% transactions via online

• 40% Credit Card and 34% UPL

contribution to Retail sales via

digital channels

• 96% of active customers using

eBanking & machined transactions

• 2.6x newly issued Credit Card*

3

New Digital Era cultivates

business transformation

and cost saving

• Data-driven Execution with AI and

Big Data

• Solid OPEX optimization

• CIR has dropped by 6% from

40.4% in 2Q19 to 34.6% in 3Q19

31

VPBank’s digital transformation aims to deliver a distinctive customer value proposition

Bank Standalone

*y-o-y growth

2

Unrivalled opportunity

for high engagement

• Average of 3 product holdings per

digital customer

• 1.2 million logins daily (20x vs. last

year)

• 120% growth in number of

transaction per customer per month

CONSOLIDATED

BANK STANDALONE

FE CREDIT

32

Review of

9M2019 Results

3,5

09

3,3

65

3,4

45

3,6

07

4,0

45

4,4

63

4,6

57

Q1/18 Q2/18 Q3/18 Q4/18 Q1/19 Q2/19 Q3/19

+35%

3,6

03

3,3

06

3,4

70

3,7

41

4,0

92

4,6

28

4,7

32

30.7%

28.9% 29.6% 28.9%30.0%

31.6% 31.4%

20.0%

22.0%

24.0%

26.0%

28.0%

30.0%

32.0%

Q1/18 Q2/18 Q3/18 Q4/18 Q1/19 Q2/19 Q3/19

2,000

2,500

3,000

3,500

4,000

4,500

5,000

TOI NIM

NII (Bil VND)

Disbursement amount (Bil VND)

BUSINESS PERFORMANCE – FE CREDIT /1

Source: Unaudited VPBFC FS at 30.09.2019

ENR (Bil VND)

TOI * (Bil VND)

14

,04

7

12

,57

2

13

,38

9

20

,06

6

16

,99

3

19

,74

1

18

,38

6

Q1/18 Q2/18 Q3/18 Q4/18 Q1/19 Q2/19 Q3/19

+ 37%

3,326

46

,68

4

46

,43

5

46

,70

1

53

,27

0

54

,66

9

58

,30

0

60

,35

2

Q1/18 Q2/18 Q3/18 Q4/18 Q1/19 Q2/19 Q3/19

+ 29%

3,326 1,400

+ 13%

49,9

53

+ 36%

*Not include other income

Institution loan Institution loan

1,3

05

1,8

80

2,0

58

2,0

27

2,0

30

11.3% 11.7%

14.5%13.2%

12.2%

-

0

0

0

0

0

0

0

Quarterly 2017 Quarterly 2018 Q1/19 Q2/19 Q3/19

300 500 700 900

1,100 1,300 1,500 1,700 1,900 2,100 2,300

Provision NCL/ ANR

NPL (%) Provision (Bil VND)

BUSINESS PERFORMANCE – FE CREDIT /2

Source: Unaudited VPBFC FS at 30.06.2019

OPEX & CIR* (Bil VND) PBT (Bil VND)

Q3.2018 FY.2018 Q1.2019 Q2.2019

6.4% 6.0% 5.8% 5.4%

5.1% 4.5% 4.5% 4.0%

VAS*

IFRS**

*NPL (follow VAS): calculate loans had Day Past Due (DPD) over 90 days in FE Credit and

consider categorizing debt of customers at other credit institution (CIC)

**NPL (follow IFRS): calculate loans had Day Past Due (DPD) over 90 days in FE Credit only.

849

1,1

32

1,3

65

1,4

02

1,5

32

28.0%

32.1%33.4%

30.3%32.4%

Quarterly 2017 Quarterly 2018 Q1/19 Q2/19 Q3/19

-

500

1,000

1,500

2,000

OPEX CIR

*Not include other income

1,0

50

1,0

29

764

1,3

66

1,3

87

11.0%8.6%

5.7%

9.7% 9.4%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Quarterly 2017 Quarterly 2018 Q1/19 Q2/19 Q3/19

PBT PBT/ ANR (annualized)

Q3.2019

5.6%

4.1%

Quarterly is estimated by average 4 quarters of reporting year

12.1%13.4%

16.6%17.3%

15.6%

2016 2017 2018 Q3/18 Q3/19

3.0%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

19.0%

21.0%

51.0% 49.7%

32.7%

25.7%

35.2%

2016 2017 2018 Q3/18 Q3/19

6.6%

7.8%

6.0%

4.2%

6.6%

2016 2017 2018 Q3/18 Q3/19

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%ROAA (%) ROAE (%)

BUSINESS PERFORMANCE – FE CREDIT /3

Source: Unaudited VPBFC FS at 30.06.2019

CAR (%) Funding Mix (%)

Average

last 3

years:

6.8%

Average

last 3

years:

45%

SBV

require:

9%

22%

8%

4%

41%

6%

19%

Offshore loan

Onshore Loan

Term Deposit

Issue Valuable Papers

Other Liabilities

Capital and Funds

2018:

60,165 bio VND

Q3.2019:

70,277

bio VND

21%

7%

6%

40%

7%

19%

INVESTMENT

36

RECAPS

Launch new growth engines (e.g.

transactions banking, mobility and

housing ecosystems) and scale up

strategic partnerships (e.g. banca) to fuel

future growth for VPBank

Establish program to enhance

sales and network productivity to

drive value from existing franchises

in retail, SME, household and

commercial banking

Conduct end-to-end redesign

and digitization of core

banking journeys to

substantially improve customer

experience and lower costs

Build next generation

capabilities in data and analytics

to drive non-linear growth and

improve decision making

Achieve excellence in risk

management and IT to support the

growth of the bank while ensuring

credit quality, including through

investment in modern risk

management tools

Strengthen governance to build a

performance-driven organization that

attracts the best banking talent and defines

a VPBank culture that promotes cross-

functional collaboration

6Strategic

themes

37

STRATEGIC THEMES TO ACHIEVE 2022 ASPIRATIONSVPBank is setting bold aspirations for 2022

Comprehensive modernised risk management policies

Vietnam is one of the fastest-growing economies in Southeast Asia

with a fast growing banking sector with significant growth potential

Strong focus on consumer finance and retail banking, well

positioned to benefit from the Vietnam consumer story

Access to stable and diverse funding sources has helped

VPBank maintain low funding costs

Robust growth in profitability, driven by high margin business

and strong cost efficiencies

1

2

3

4

Well capitalised and prudently managed asset quality5

6

38

WHY VPBANK?

Total assets 373,649

Customer deposits and

Valuable papers issued 252,435

Credit to customers 265,408

Bad debt ratio

(Bank standalone)< 3%

PBT 9,500

Unit: VND bil

2018 2018 vs. 2017 2019 Target vs. 2018

Total assets 323,291 16% 16%

Credit to customers 230,790 17% 15%

Customer deposits and Valuable

papers issued219,509 10% 15%

PBT 9,199 13% 3%

- If excluding one-off income 8,343 14%

Source: Audited Consolidated Financial Statement at 31.12.2018 and VPBank business plan 2019

39

FINANCIAL TARGETS 2019

1. Cost to income ratio (CIR) OPEX / TOI

2. ROE (Consolidated) Profit after tax / Average Total Equity

6. NPL in accordance with Cir 02 Total amount of non-performing exposure / Total credit exposure per Cir 02

7. Credit Cost Provision expenses / Average Loans to customers

8. LLR on & off BS Total provision reserves for credit losses plus provision used for Write-off / (Amount of loans in group 3-5 + Write-off)

3. ROA (Consolidated) Profit after tax / Average Total Assets

10. COF Interest Expenses / Average total funding

11. Internal LDR Credit to Customers / Customers Deposits and Valuable Papers

12. Yield Interest Income / Average Earning Assets

13. NIM Net Interest Income / Average Earning Assets

14. Asset Utilization TOI / Average Total Assets

Specific provision reserves for credit losses plus provision used for Write-off / (Amount of loans in group 2-5 + Write-off))9. Specific LLR on & off BS

40

15. Equity Multiplier Total Assets / Total Owners’ Equity

DEFINITION OF INDICATORS

4. ROE (Bank Standalone) Profit after tax exclude income from subsidiaries / Average Total Equity exclude investment to subsidiaries

5. ROA (Bank Standalone) Profit after tax exclude income from subsidiaries / Average Total Assets exclude investment to subsidiaries

AMC Asset Management Company

CAR Capital Adequacy Ratio

CASA Current Account Savings Account

CIR Cost-to-Income Ratio

ENR Ending Net Receivables

LLR Loan Loss Reserve

NFI Net Fee Income

CD Certificate of deposits

NIM Net Interest Margin

NPL Non-Performing Loan

PL NTB Personal loans New to Bank

OPEX Operating expense

ROE Return on Equity

ROA Return on Asset

SBV State Bank of Vietnam

SME Small and Medium-Sized Enterprises

TOI Total Operating Income

UPL Unsecured Personal Loan

ATM Automated Teller Machine

CDM Cash Deposit Machine

POS Point of Sale

POC Point of Cash

41

GLOSSARY

The material in this presentation is general background information about VPBank’s activities current at the date

of the presentation. It is information given in summary form and does not purport to be completed. It is not

intended to be relied upon as advice to investors or potential investors and does not take into account the

investment objectives, financial situation or needs of any particular investor. These should be considered, with or

without professional advice when deciding if an investment is appropriate.

For further information, visit www.vpbank.com.vn or contact

VPBank Investor Relations

Tel: (84) 24 3928 8869 (ext. 54111)

Fax: (84) 24 928 8867

Email: [email protected]

42

DISCLAIMER

![Nine Months ended 3lst December 2019....1 Revenue from operation 5,171 6.099 17.236 18,8 18 . 25,513 2 Other 34 23 109 1 18 110 3 Income from operation [1+2] 5.205 6,122 17,345 18.936](https://img.dokumen.tips/doc/110x75/5f410451f6036b4b5a3aea53/nine-months-ended-3lst-december-2019-1-revenue-from-operation-5171-6099-17236.jpg)