Embed Size (px)

Citation preview

Resourcesand Energy

QuarterlyJune quarter 2012

BREE 2012, Resources and Energy Quarterly, June Quarter 2012, BREE, Canberra, June 2012.

© Commonwealth of Australia 2012

This work is copyright, the copyright being owned by the Commonwealth of Australia. The Commonwealth of Australia has, however, decided that, consistent with the need for free and open re-use and adaptation, public sector information should be licensed by agencies under the Creative Commons BY standard as the default position. The material in this publication is available for use according to the Creative Commons BY licensing protocol whereby when a work is copied or redistributed, the Commonwealth of Australia (and any other nominated parties) must be credited and the source linked to by the user. It is recommended that users wishing to make copies from BREE publications contact the Chief Economist, Bureau of Resources and Energy Economics (BREE). This is especially important where a publication contains material in respect of which the copyright is held by a party other than the Commonwealth of Australia as the Creative Commons licence may not be acceptable to those copyright owners.

The Australian Government acting through BREE has exercised due care and skill in the preparation and compilation of the information and data set out in this publication. Notwithstanding, BREE, its employees and advisers disclaim all liability, including liability for negligence, for any loss, damage, injury, expense or cost incurred by any person as a result of accessing, using or relying upon any of the information or data set out in this publication to the maximum extent permitted by law.

ISSN 1839-499X (Print)

ISSN 1839-5007 (Online)

Vol. 1, no. 4

From 1 July 2011, responsibility for resources and energy data and research was transferred from ABARES to the Bureau of Resources and Energy Economics (BREE).

Postal address:

Bureau of Resources and Energy Economics

GPO Box 1564

Canberra ACT 2601 Australia

Phone: +61 2 6276 1000

Email: [email protected]

Web: www.bree.gov.au

ForewordResources and Energy Quarterly is an important publication of the Bureau of Resources and Energy Economics (BREE). This issue provides an overview of the global macroeconomic situation; the most up-to-date global production, exports and values of major resources energy commodities and forecasts for 2011–2012 and 2012–13; reviews of key topics and issues of relevance to the sector; and detailed statistical tables on world production, consumption, stocks and trade in key commodities. The statistical tables in this and subsequent issues of Resources and Energy Quarterly incorporate what were previously published every quarter in BREE’s Resources and Energy Statistics.

In the review section of Resources and Energy Quarterly there is a review of the on-going euro crisis; a review of an analysis of end use energy intensity of major household appliances; and an overview of the Australian coal industry.

BREE’s latest forecast for the value of Australian exports of resources and energy for 2011–12 is about A$193 billion or about an 8 per cent increase from 2010–11. The forecast for 2012–13 is for the export value of resources and energy to increase by about 8 per cent to around A$209 billion. Much of this rise in export values is because of large projected increases in the volume of bulk commodity exports.

Quentin Grafton

Executive Director/Chief Economist

Bureau of Resources and Energy Economics

3

ContentsForeword..................................................................................................................................3

Contents...................................................................................................................................4

Acronyms and abbreviations....................................................................................................5

Macroeconomic outlook update and energy and minerals overview.......................................6

Energy outlook........................................................................................................................15

Oil.......................................................................................................................................15

Gas......................................................................................................................................18

Thermal coal.......................................................................................................................19

Resources outlook...................................................................................................................22

Steel and steel-making raw materials.................................................................................22

Gold....................................................................................................................................29

Metals overview.................................................................................................................32

Copper................................................................................................................................34

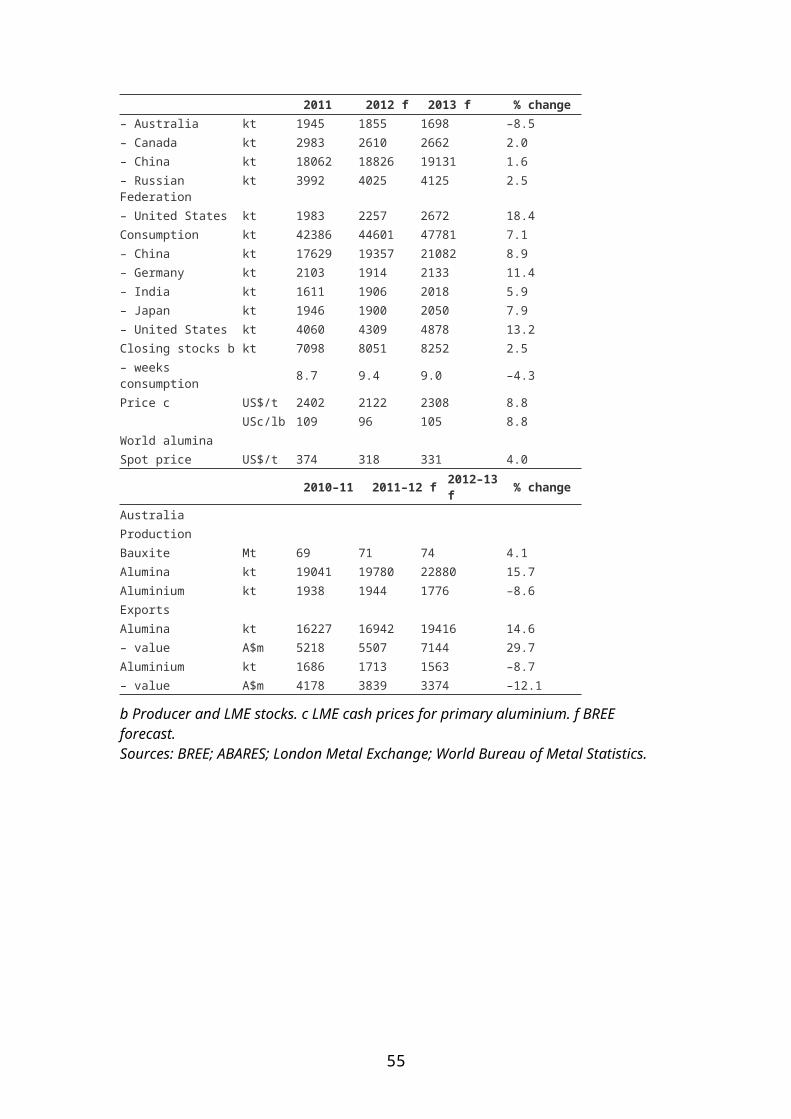

Aluminium..........................................................................................................................38

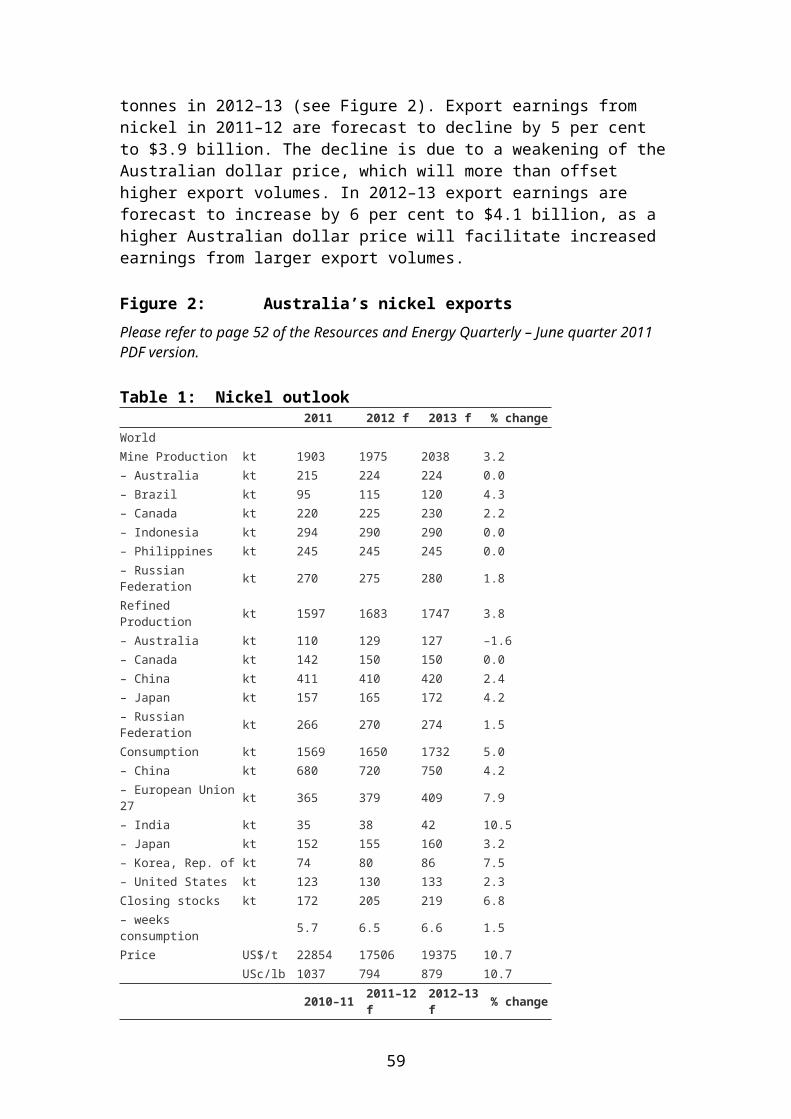

Nickel..................................................................................................................................42

Zinc.....................................................................................................................................46

Reviews...................................................................................................................................50

PIIGS, a Trojan horse and an optimal currency area...........................................................51

Energy intensity analysis of household appliances in Australia..........................................57

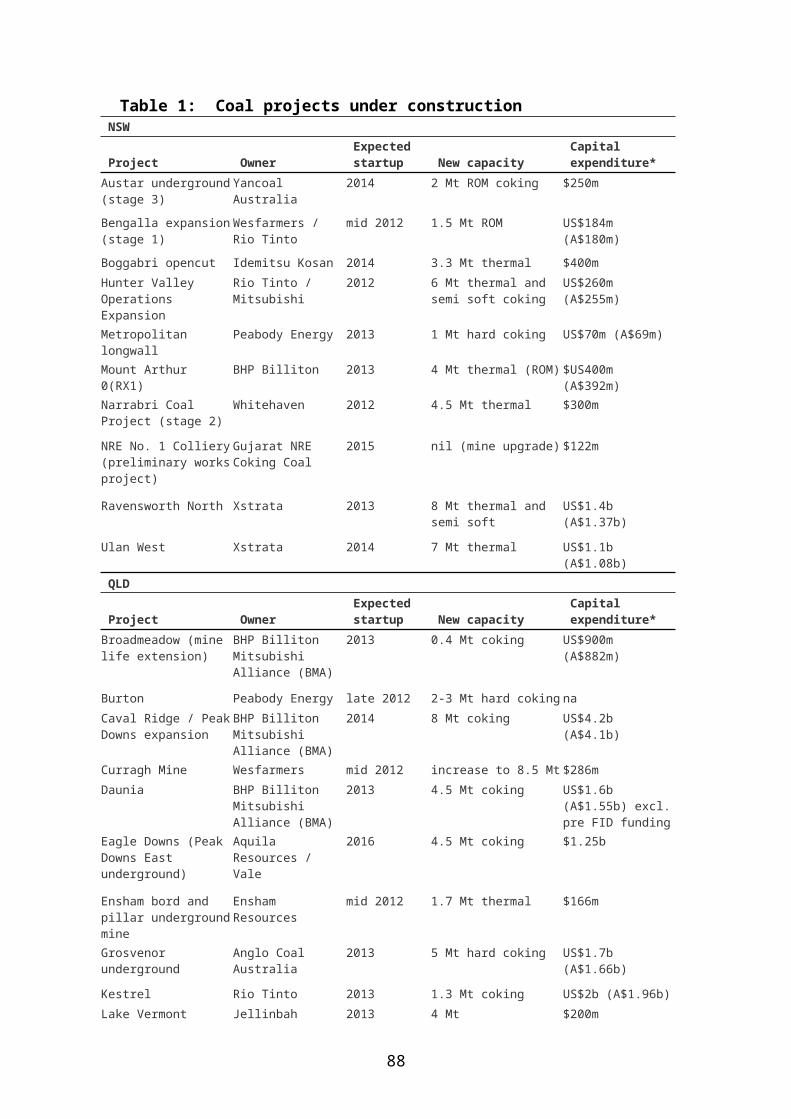

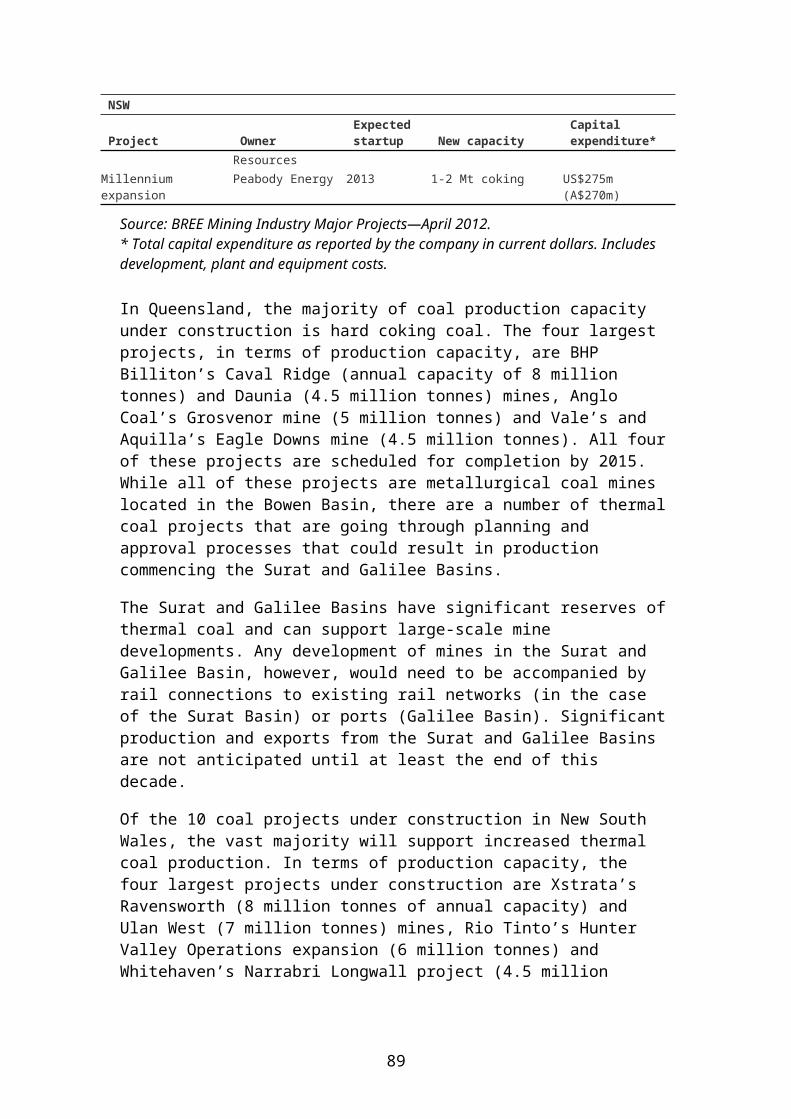

A short background of the Australian coal industry............................................................71

Statistical tables......................................................................................................................77

4

Acronyms and abbreviationsABARES Australian Bureau of Agricultural and Resource Economics and Science

ABS Australian Bureau of Statistics

BREE Bureau of Resources and Energy Economics

FOB free on board

GDP gross domestic product

IEA International Energy Agency

IMF International Monetary Fund

LME London Metal Exchange

LNG liquefied natural gas

mb/d millions of barrels per day

MBtu million British thermal units

Mt million tonnes

OECD Organisation for Economic Co-operation and Development

OPEC Organisation of the Petroleum Exporting Countries

PPP purchasing-power parity

RBA Reserve Bank of Australia

TWI trade-weighted index

UNCTAD United Nations Conference on Trade and Development

WTI West Texas Intermediate

5

Macroeconomic outlook update and energy and minerals overviewNhu Che, Quentin Grafton and Pam Pham

Growth continues, but remains fragile with elevated downside risks

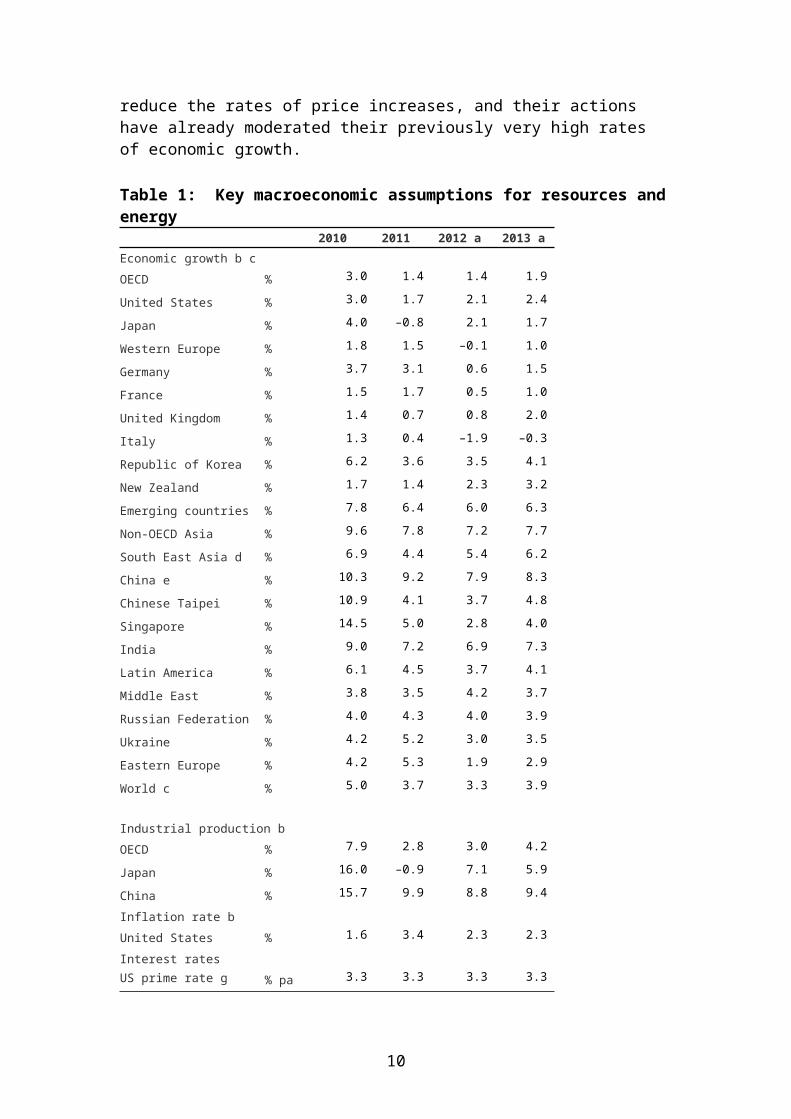

The global economy is projected to grow slowly in 2012 relative to 2011, and will remain fragile and subject to substantial downside risks. The updated World Economic Outlook (WEO) released by the International Monetary Fund (IMF) in April 2012 projects improved economic activity in the US during the second half of 2012, and a more expansionary policies in the euro area in response to the deepening economic crisis in the euro zone. In general, weak recovery is expected in key advanced economies, but economic activity is expected to remain robust in most emerging and developing economies. The ongoing political and economic crisis in Greece, and recent data that indicate a lower than expected rate of growth in China, are key concerns for the short-term outlook.

Global growth is projected to drop from about 3.7 per cent in 2011 to about 3.25 per cent in 2012 due to a slowdown caused by deteriorating sovereign and banking sector developments in the euro zone attributable to the current Greek economic crisis. The IMF (the April WEO) predicts a gradual renewal of economic activity and a return to about 4 per cent global economic growth in 2013.

Economic conditions in Europe remain problematic. Some progress has been made in addressing fiscal imbalances and implementing structural reforms, but much work remains to be done. The IMF (the April WEO) records that the balance of risks to Europe’s near-term growth prospects remains on the downside. Despite the progress in strengthening crisis management in recent months, a renewed escalation of the euro crisis and the Greek economic crisis remains a possibility as long as the underlying issues are not resolved (see Review article on the euro crisis). The euro zone is still projected to drop into a mild recession in 2012 as a result of the Greek sovereign debt crisis and a general loss of confidence, the effects of bank deleveraging on the real economy, and the impact of fiscal consolidation in response to market pressures. Added to this, lower than expected economic growth in China may have a negative impact on a number of advanced economies, including Australia.

Real GDP growth in the emerging and developing economies is projected to slow from 6.4 per cent in 2011 to 6.0 per cent in 2012, but then to reaccelerate to 6.3 per cent in 2013. The euro zone may face a further crisis, recession, and possible contagion. The spill-over from the euro zone crisis could also severely affect the rest of Europe. Other European economies would likely experience further financial volatility, although no major impact on activity is expected unless the euro zone crisis intensifies further. Downside risks may be accelerated if there were to be a disruption in global bond and currency markets that would be exacerbated by high

6

budget deficits and debt in Japan and the US, and could result in rapidly slowing activity in some emerging economies.

In the 17 June Greek election the New Democracy party, under the leadership of Antonis Samaras, won the highest number of votes and it has formed a coalition government. The election outcome has been viewed favourably by market commentators because the New Democracy Party is broadly in favour of the Greek bail-out and maintaining Greece within the euro zone.

Economic growth was robust in most of Asia and Latin America in 2011, but is expected to moderate in 2012 before regaining strength in 2013. Unlike some advanced economies concerned with lagging growth, the immediate concern for some of these emerging economies is their rising inflation.

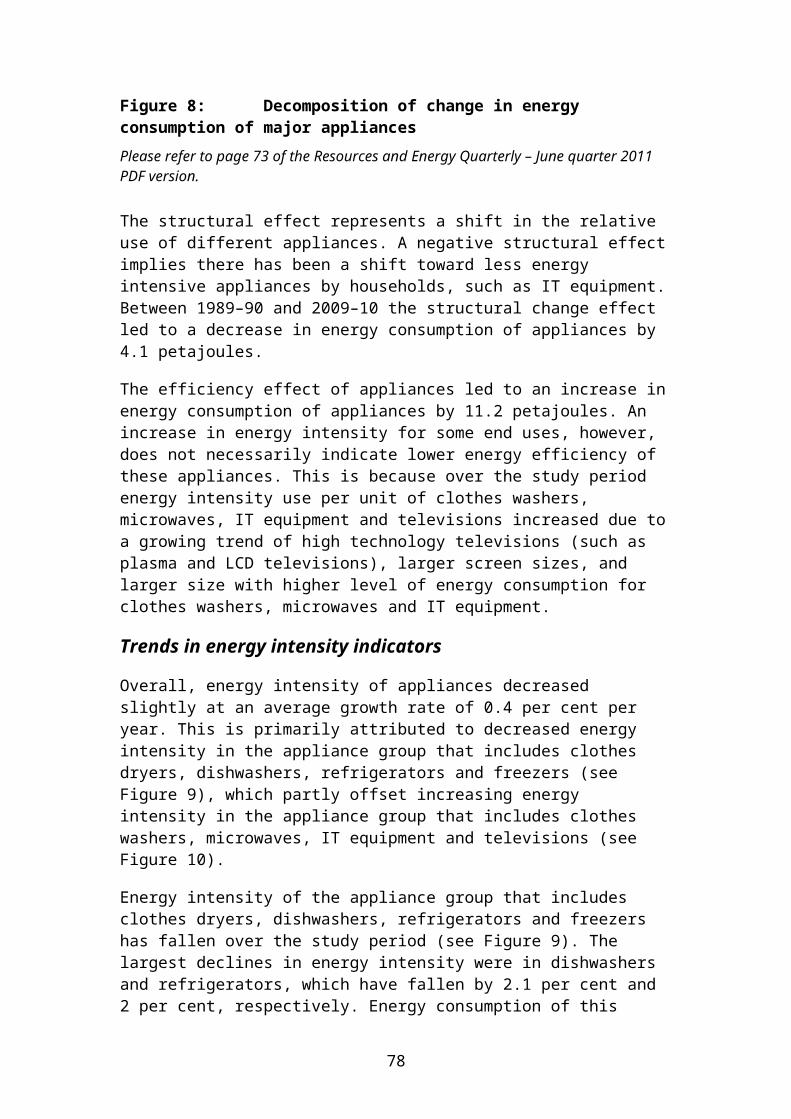

In Asia, recent data are broadly consistent with the modest slowdown that some authorities in the region have been trying to achieve in order to contain inflationary pressures. India and China, in particular, are trying to reduce the rates of price increases, and their actions have already moderated their previously very high rates of economic growth.

Table 1: Key macroeconomic assumptions for resources and energy2010 2011 2012 a 2013 a

Economic growth b c OECD % 3.0 1.4 1.4 1.9

United States % 3.0 1.7 2.1 2.4

Japan % 4.0 –0.8 2.1 1.7

Western Europe % 1.8 1.5 –0.1 1.0

Germany % 3.7 3.1 0.6 1.5

France % 1.5 1.7 0.5 1.0

United Kingdom % 1.4 0.7 0.8 2.0

Italy % 1.3 0.4 –1.9 –0.3

Republic of Korea % 6.2 3.6 3.5 4.1

New Zealand % 1.7 1.4 2.3 3.2

Emerging countries % 7.8 6.4 6.0 6.3

Non-OECD Asia % 9.6 7.8 7.2 7.7

South East Asia d % 6.9 4.4 5.4 6.2

China e % 10.3 9.2 7.9 8.3

Chinese Taipei % 10.9 4.1 3.7 4.8

Singapore % 14.5 5.0 2.8 4.0

India % 9.0 7.2 6.9 7.3

Latin America % 6.1 4.5 3.7 4.1

Middle East % 3.8 3.5 4.2 3.7

Russian Federation % 4.0 4.3 4.0 3.9

Ukraine % 4.2 5.2 3.0 3.5

Eastern Europe % 4.2 5.3 1.9 2.9

World c % 5.0 3.7 3.3 3.9

7

2010 2011 2012 a 2013 a

Industrial production bOECD % 7.9 2.8 3.0 4.2

Japan % 16.0 –0.9 7.1 5.9

China % 15.7 9.9 8.8 9.4

Inflation rate bUnited States % 1.6 3.4 2.3 2.3

Interest ratesUS prime rate g % pa 3.3 3.3 3.3 3.3

a BREE assumption. b Change from previous period. c Weighted using 2012 purchasing power parity (PPP) valuation of country gross domestic product by the IMF. d Indonesia, Malaysia, the Philippines, Thailand and Vietnam. e Excludes Hong Kong. g Commercial bank lending rates to prime borrowers in the US.Sources: BREE; ABS; IMF; OECD; RBA.

Economic prospects in Australia’s major mining export markets

Non-OECD economies

China’s rapid economic growth provides a substantial impact on the demand for energy and mining products imported from Australia. Although economic growth has moderated since mid-2011, consumption and investment are expected to remain robust. Growth has slowed to a more sustainable pace in China largely as a result of the effect of tighter domestic policies, which have helped to ease inflationary pressures. Chinese economic growth is projected to be around 8 per cent in 2012 and 2013. Commodity imports and consumption of more cyclical commodities—especially base metals, but also crude oil—have increased at a robust pace, in part due to continued solid domestic investment growth.

The Chinese economy continues to record strong growth, although this is projected to moderate in 2012. In part, this expected easing in economic growth is due to domestic economic policies to combat inflation, including the continuing unwinding of the 2008–09 fiscal stimulus, tighter monetary policy, and measures to contain price increases in its property market. Additionally, spill-over from problems in the broader global economy and some high internal risks facing the Chinese economy pose risks to its targeted level of economic growth. Based on purchasing power parity terms (PPP), China’s gross domestic product (GDP) is assumed to grow at 7.9 per cent in 2012. This is 0.3 percentage points lower than that assumed by BREE in March 2012. An annual rate of economic growth of 8.3 per cent is assumed for 2013.

Despite a slight moderation in its economic growth, Chinese domestic demand remains strong. Retail sales continue to expand and passenger vehicle sales are just below their late 2010 peak level. Although there has been relatively weaker export demand, manufacturing investment continues to grow. As a result, over the outlook period China is expected to continue its major role as a growth engine for the world economy.

8

Figure 1: Economic growth in Australia’s major resource and energy export markets

Please refer to page 9 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

The April WEO by the IMF discusses whether China will unexpectedly enter another period of ‘destocking’. The recent increase in cancelled warrants relative to total stocks in London Metal Exchange warehouses, which is a leading indicator of declining metal inventory buffers in the near term, is consistent with an expectation of robust growth in the demand for base metals over the near term in China.

Economic growth in India has moderated due to policies intended to combat rising inflationary pressures. Economic growth is projected to be 6.9 per cent in 2012, 0.1 percentage points lower than assumed by BREE in March 2012. The slowing in growth follows a significant tightening in monetary policy. Given a slight decrease in industrial production over the past quarter, industrial production in 2012 is projected to grow at around 5.9 per cent. This is below its early 2011 peak and 0.1 percentage points lower than expected by BREE in March 2012. In addition to the effect of tighter monetary policy, industrial production has also been affected by problems at a number of coal mines that have disrupted the fuel supply for coal-fired power stations.

Due to robust investment, near-term growth in ASEAN countries (including Indonesia, Malaysia, Philippines, Thailand, and Vietnam) is assumed to be around 5.4 per cent in 2012. This investment should offset a possible slowdown in export momentum.

OECD economies

Economic growth in OECD economies is assumed to be 1.4 per cent in 2012. The annual growth rate in Japan is assumed to be 2.1 per cent, 0.4 percentage points lower than assumed in March 2012 by BREE. The pace of growth in the 17 countries in the euro zone slowed in 2011, and is expected to deteriorate further in 2012. An expected slow-down in growth in the core northern euro zone economies, such as Germany, is likely to make economic conditions in the southern economies more difficult in 2012.

The German economy was the most robust economy in Western Europe in 2011, with strong export-led growth of 3.1 per cent. According to the April WEO projection, growth will slow in terms of industrial production and economic growth in 2012. Nevertheless, in the first quarter of 2012 the German economy actually grew more than expected due to exports to emerging markets which offset waning euro-area demand. With the euro region’s debt crisis ravaging economies from Greece to Spain, German companies have shifted focus to emerging markets. Car makers and their suppliers are benefitting from demand in faster-growing markets such as China, while falling unemployment and rising wages are stimulating spending at home.

9

The US economy improved throughout 2011 and continues to expand at a moderate rate in 2012. US economic activity gained strength through the year, with the quarterly growth rate rising each quarter. Growth in the US was determined primarily by domestic factors in 2011, and is estimated to grow at a rate of 2.1 per cent in 2012 and 2.4 per cent in 2013.

The US unemployment rate has declined in the past year and there are tentative signs of improvement in housing construction activity. Economic growth is expected to be supported by increases in consumption and business investment, with forward-looking indicators of economic activity improving. Assumed very low nominal interest rates over the next two years are expected to provide support to investment. Risks to the outlook include fiscal uncertainty, rapid fiscal consolidation from start of 2013, weakness in the housing market, and a potential financial spill-over from Europe.

The Republic of Korea’s economy is expected to grow at around 3.5 per cent in 2012, 0.9 percentage points lower than assumed in March 2012 by BREE. The Republic of Korea’s economic growth slowed recently due to lower exports caused by Europe’s debt crisis and the region’s economic downturn. Exports contracted 4.7 percent on-year in April, primarily as a result of decreases in shipments to the EU and Japan. The Republic of Korea’s economy, which heavily depends on overseas demand, has begun to show signs of the effects of weaker exports. Output in the mining and manufacturing sectors fell slightly in the first quarter of 2012.

Australia’s economic prospects

Real GDP in Australia, based on a PPP valuation of GDP, is assumed to grow at an annual rate of 2.9 per cent in 2011–12, 0.9 percentage points lower than expected in March 2012 by BREE. The decrease in anticipated economic growth in 2011–12 is primarily a result of lower than expected economic growth in the last quarter of 2011. The Reserve Bank of Australia cites the key factors contributing to lower annual growth are weaker export growth, including a decreasing trend in price within several economic sectors (such as mining); the appreciation of the exchange rate; and lower-than-anticipated growth in the global economy. Additionally, public spending was less than expected, private demand grew roughly as anticipated, dwelling investment was slightly weaker, and business investment slightly stronger.

The Australian economy is assumed to rebound in 2012–13 and grow at around 3.8 cent. The growth in the Australian economy is expected to be supported by mining-related activities, including high levels of mining investment. Significant expansions of iron ore and coal production capacity are underway, and are expected to contribute to solid growth in resource export volumes over the foreseeable future.

Overall, Australian domestic demand continues to grow at a robust pace, although the high level of the exchange rate and rapid growth in mining investment is offset by weak building activity and fiscal consolidation. Export growth is assumed to be at an above-trend pace, due to large volume increases.

10

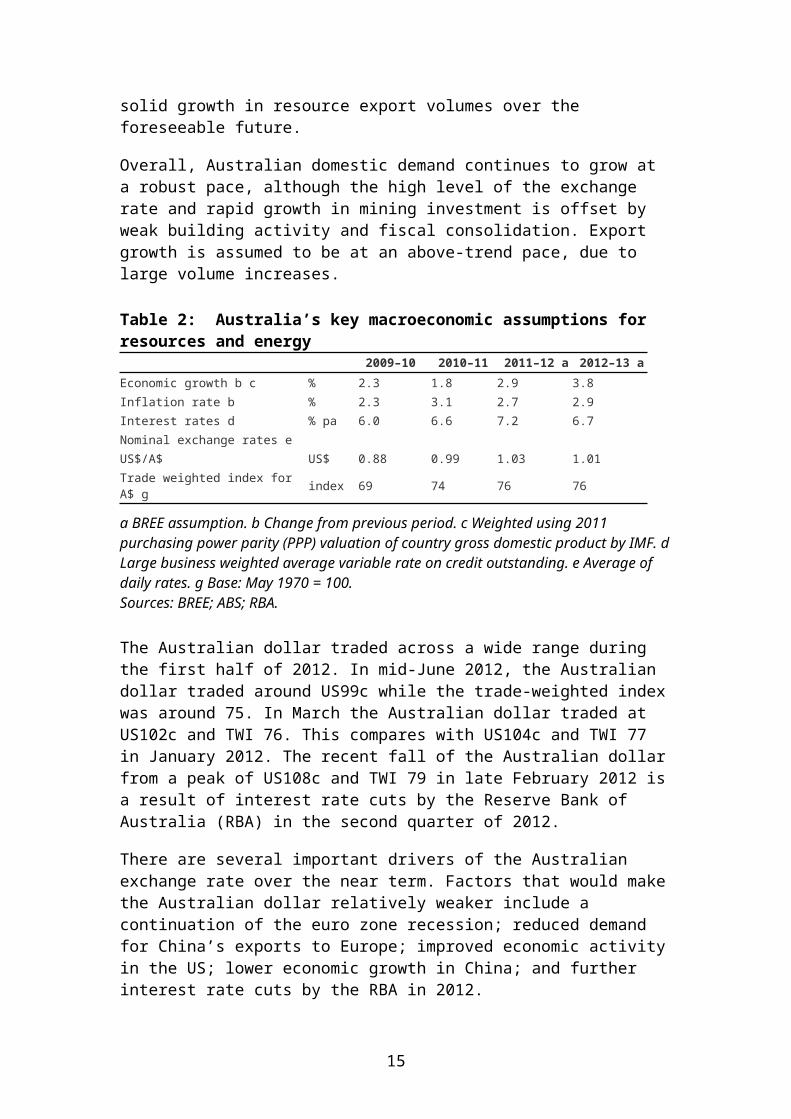

Table 2: Australia’s key macroeconomic assumptions for resources and energy

2009–10 2010–11 2011–12 a 2012–13 aEconomic growth b c % 2.3 1.8 2.9 3.8Inflation rate b % 2.3 3.1 2.7 2.9Interest rates d % pa 6.0 6.6 7.2 6.7Nominal exchange rates eUS$/A$ US$ 0.88 0.99 1.03 1.01Trade weighted index for A$ g index 69 74 76 76

a BREE assumption. b Change from previous period. c Weighted using 2011 purchasing power parity (PPP) valuation of country gross domestic product by IMF. d Large business weighted average variable rate on credit outstanding. e Average of daily rates. g Base: May 1970 = 100.Sources: BREE; ABS; RBA.

The Australian dollar traded across a wide range during the first half of 2012. In mid-June 2012, the Australian dollar traded around US99c while the trade-weighted index was around 75. In March the Australian dollar traded at US102c and TWI 76. This compares with US104c and TWI 77 in January 2012. The recent fall of the Australian dollar from a peak of US108c and TWI 79 in late February 2012 is a result of interest rate cuts by the Reserve Bank of Australia (RBA) in the second quarter of 2012.

There are several important drivers of the Australian exchange rate over the near term. Factors that would make the Australian dollar relatively weaker include a continuation of the euro zone recession; reduced demand for China’s exports to Europe; improved economic activity in the US; lower economic growth in China; and further interest rate cuts by the RBA in 2012.

Australian resources and energy commodities production and exports

In 2010–11, the gross value added produced from mining activities decreased by 2 per cent to $100.7 billion (in 2011–12 dollars) compared with 2009–10. By contrast, total employment in the mining sector increased by 19 per cent to total 205 300 people. Most of this increase is attributable to employment in the metal ore industry and the coal industry.

The Australian mine production index is forecast to increase by 6 per cent in 2012–13, relative to 2011–12, primarily due to a 7 per cent increase in the output of energy commodities, particularly uranium and black coal. Another contributing factor to this growth will be a forecast of 5 per cent increase in the production of metals and other minerals, underpinned by rising copper and gold production. Projected year-on-year volume increases in terms of Australia’s bulk commodities (iron ore, metallurgical and thermal coal, and LNG) in 2012-13 are expected to be in excess of 10 per cent.

11

Figure 2: Australian mine production index

Please refer to page 12 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

In 2012–13, the total export earnings for energy and mineral commodities are forecast to increase by 8 per cent to $209.5 billion supported by increases in the export values for both energy and mineral commodities (see Figure 3). Energy commodity export earnings in 2012–13 are anticipated to grow by 7 per cent to $82.3 billion as a result of strong increases in export earnings from thermal coal (up 7 per cent to $18.6 billion), LNG (up 29 per cent to $16.0 billion) and uranium (up 9 per cent to $800 million).

Figure 3: Australian energy and minerals export earnings

Please refer to page 13 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Mineral commodity export earnings in 2012–13 are forecast to increase by 10 per cent to $127.1 billion as a result of increases in the export values of alumina (up 30 per cent to $7.1 billion), gold (up 27 per cent to $19.7 billion), iron ore (up 7 per cent to $67 billion) and copper (up 7 per cent to $9 billion). Partially offsetting the increased export earnings for mineral commodities will be lower forecast export earnings for aluminium (down 12 per cent to $3.4 billion) and metallurgical coal (down 2 per cent to $29.7 billion).

Overall, the outlook for Australian resources and energy commodities production and exports in 2012–13 remains robust (see Table 3). The major indicators for Australia’s resources and energy commodity sector are presented in Table 4. Detailed forecast and projection for major energy and minerals commodities are outlined in the following Resources Outlook and Energy Outlook sections.

Table 3: Australia’s resources and energy commodity exports, by selected

commodities

Volume Value2010–11 2011–12 f growth % 2010–11 2011–12 f growth %

Alumina kt 16942 19416 14.6 $m 5507 7144 29.7

Aluminium kt 1713 1563 –8.8 $m 3839 3374 –12.1

Copper kt 884 974 10.2 $m 8418 9043 7.4

Gold t 331 361 9.1 $m 15558 19722 26.8

Iron ore Mt 463 510 10.2 $m 62788 66936 6.6

Nickel kt 240 258 7.5 $m 3902 4138 6.0

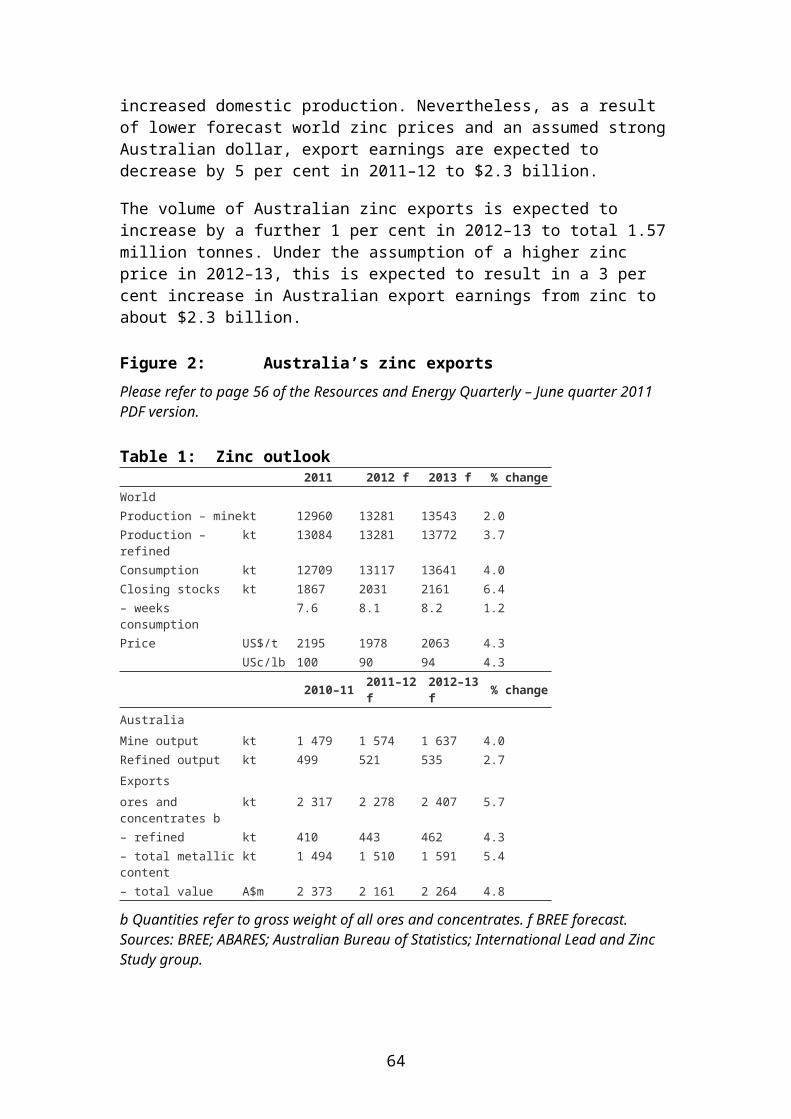

Zinc kt 1555 1571 1.0 $m 2263 2331 3.0

LNG Mt 19 23 21.1 $m 12392 16037 29.4

Metallurgical coal Mt 142 161 13.4 $m 30310 29682 –2.1

Thermal coal Mt 159 179 12.6 $m 17358 18590 7.1

Oil ML 19167 19389 1.2 $m 13012 13319 2.4

12

Volume Value2010–11 2011–12 f growth % 2010–11 2011–12 f growth %

Uranium t 7217 7860 8.9 $m 732 799 9.2

f BREE forecast.Sources: BREE; ABS.

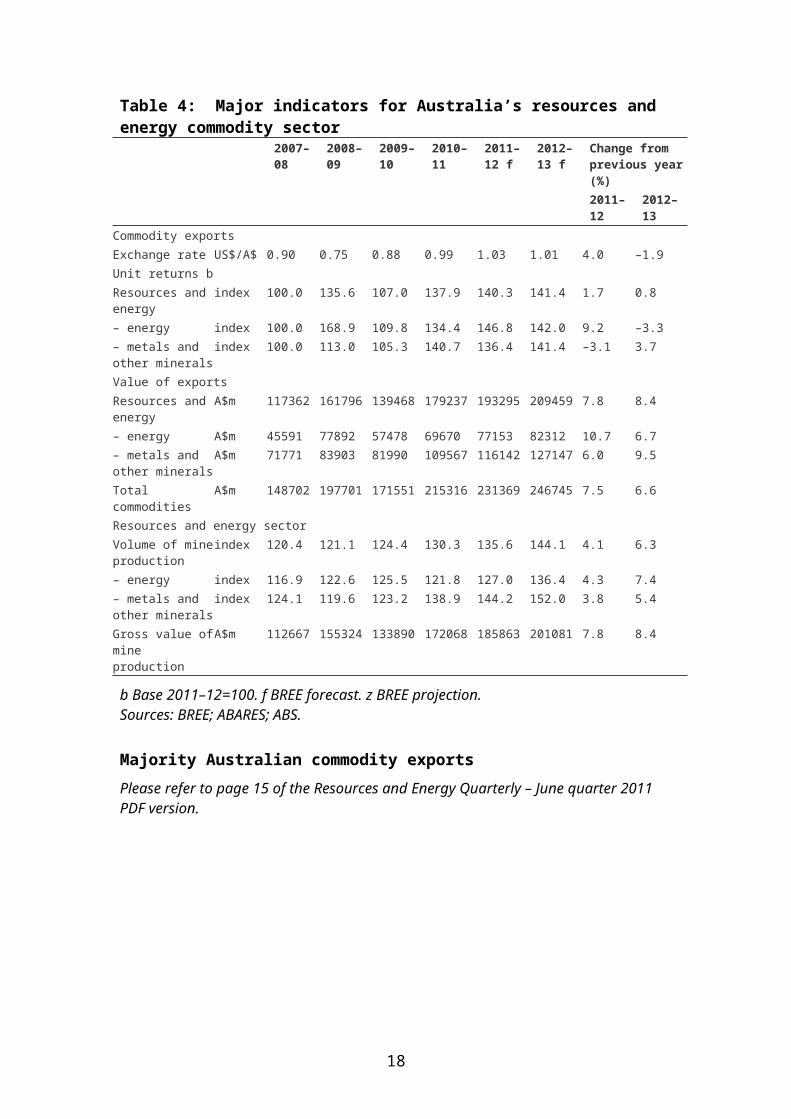

Table 4: Major indicators for Australia’s resources and energy commodity sector

2007–08

2008–09

2009–10

2010–11

2011–12 f

2012–13 f

Change from previous year (%)2011–12

2012–13

Commodity exports Exchange rate US$/A$ 0.90 0.75 0.88 0.99 1.03 1.01 4.0 –1.9Unit returns b Resources and energy

index 100.0 135.6 107.0 137.9 140.3 141.4 1.7 0.8

– energy index 100.0 168.9 109.8 134.4 146.8 142.0 9.2 –3.3– metals and other minerals

index 100.0 113.0 105.3 140.7 136.4 141.4 –3.1 3.7

Value of exportsResources and energy

A$m 117362 161796 139468 179237 193295 209459 7.8 8.4

– energy A$m 45591 77892 57478 69670 77153 82312 10.7 6.7– metals and other minerals

A$m 71771 83903 81990 109567 116142 127147 6.0 9.5

Total commodities A$m 148702 197701 171551 215316 231369 246745 7.5 6.6Resources and energy sectorVolume of mine production

index 120.4 121.1 124.4 130.3 135.6 144.1 4.1 6.3

– energy index 116.9 122.6 125.5 121.8 127.0 136.4 4.3 7.4– metals and other minerals

index 124.1 119.6 123.2 138.9 144.2 152.0 3.8 5.4

Gross value of mine production

A$m 112667 155324 133890 172068 185863 201081 7.8 8.4

b Base 2011–12=100. f BREE forecast. z BREE projection.Sources: BREE; ABARES; ABS.

Majority Australian commodity exports

Please refer to page 15 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

13

Energy outlook

Oil

Nina Hitchins

Oil prices higher over the short term

Crude oil prices eased in April and May 2012, and the Brent-WTI differential narrowed. In May the WTI price averaged US$95 a barrel and the Brent price averaged US$110, around 7 per cent lower than the average for the March quarter 2012 (see Figure 1). Lower prices reflected perceived easing of tensions in the Middle East, European sovereign debt concerns, slowing economic growth in China, and increasing OECD stocks.

The WTI price is forecast to average US$96 a barrel in 2012 and US$102 a barrel in 2013. The Brent price is forecast to average US$111 a barrel in 2012 and US$113 a barrel in 2013. Increasing oil consumption and persistently low OPEC spare capacity will underpin increases in oil prices.

OPEC spare capacity has continued to fall since the December quarter 2011. In May 2012, it averaged 3.1 million barrels a day, or around 8 per cent of OPEC production. Lower OPEC spare capacity reflected an incremental increase of OPEC crude production of 1 million barrels a day, relative to the end of 2011. Increased production offset expansions in capacity, particularly in Libya. OPEC spare capacity is expected to remain low for the remainder of 2012 and 2013, as a result of increasing OPEC production. Low OPEC spare capacity is expected to support higher prices.

There are several risks to the oil price forecast throughout 2012 and 2013. Deteriorating market sentiment with regard to the euro zone, and weaker than assumed economic growth in China could reduce world oil consumption and put downward pressure on prices. Alternatively, escalating tensions in the Middle East including those between the international community and Iran could reduce apparent availability of supply and support higher than forecast prices.

Figure 1: WTI and Brent oil prices

Please refer to page 17 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

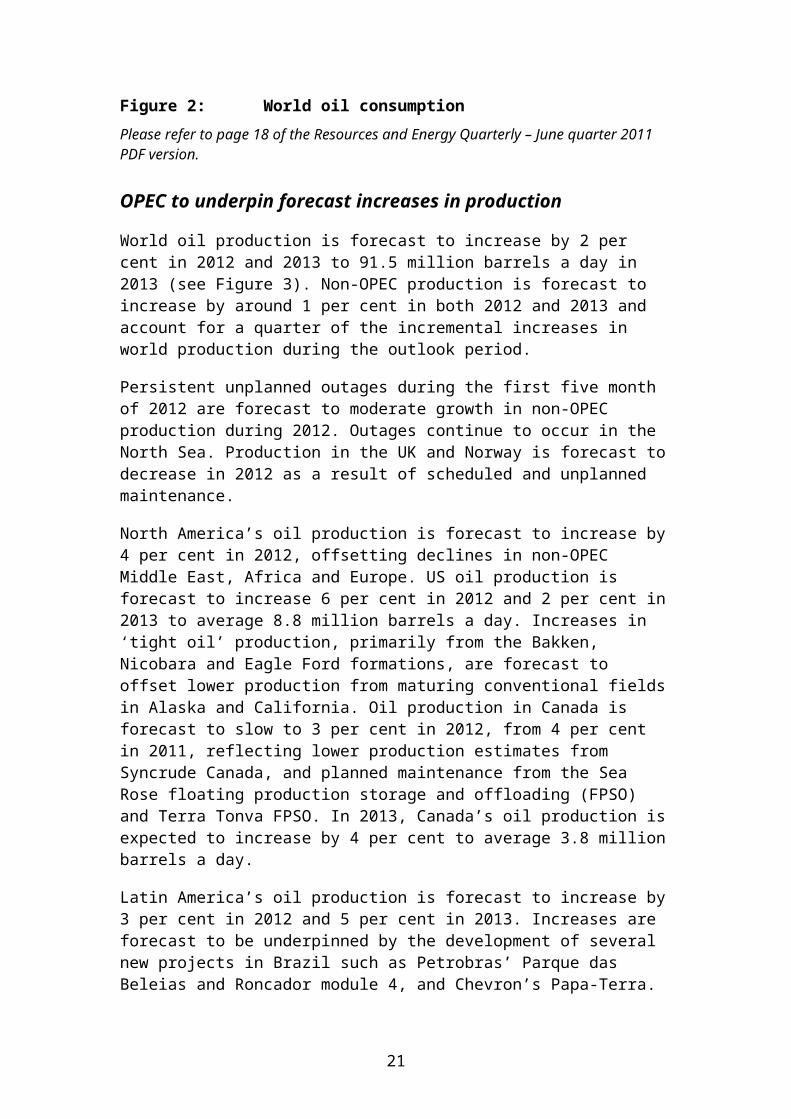

Growth in world consumption forecast to accelerate in 2013

World oil consumption is forecast to increase by 1 per cent in 2012 to 90.1 million barrels a day. In 2013, economic activity is assumed to pick-up and world oil consumption is forecast to increase by 1.5 per cent to 91.5 million barrels a day (see

14

Figure 2). Increases in non-OECD consumption are expected to offset moderate falls in OECD consumption.

Consumption in the OECD is forecast to fall 0.8 per cent in 2012 to 45.3 million barrels a day. Lower consumption in North America and Europe is forecast to offset increases in the OECD Pacific (Japan, the Republic of Korea and Australasia). Increases in OECD Pacific oil consumption are forecast to be supported by oil-fired electricity generation in Japan. Oil-fired electricity generation will be relied on to bridge the gap as a result of the temporary shutdown of Japan’s nuclear industry. In 2013, OECD oil consumption is forecast to remain relatively unchanged. Structural declines in the oil use intensity of OECD economies are forecast to be offset by stronger economic growth.

Consumption in non-OECD economies is forecast to increase by 3 per cent in both 2012 and 2013 to average 46.3 million barrels a day in 2013. A third of non-OECD growth is forecast to be attributable to China. Assumed weaker economic growth during 2012 will underpin lower growth in China’s oil consumption, which is forecast to slow to 4 per cent, down from 5 per cent in 2011. In 2013, China’s oil consumption growth is forecast to rebound to 5 per cent and average 10.4 million barrels a day.

Figure 2: World oil consumption

Please refer to page 18 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

OPEC to underpin forecast increases in production

World oil production is forecast to increase by 2 per cent in 2012 and 2013 to 91.5 million barrels a day in 2013 (see Figure 3). Non-OPEC production is forecast to increase by around 1 per cent in both 2012 and 2013 and account for a quarter of the incremental increases in world production during the outlook period.

Persistent unplanned outages during the first five month of 2012 are forecast to moderate growth in non-OPEC production during 2012. Outages continue to occur in the North Sea. Production in the UK and Norway is forecast to decrease in 2012 as a result of scheduled and unplanned maintenance.

North America’s oil production is forecast to increase by 4 per cent in 2012, offsetting declines in non-OPEC Middle East, Africa and Europe. US oil production is forecast to increase 6 per cent in 2012 and 2 per cent in 2013 to average 8.8 million barrels a day. Increases in ‘tight oil’ production, primarily from the Bakken, Nicobara and Eagle Ford formations, are forecast to offset lower production from maturing conventional fields in Alaska and California. Oil production in Canada is forecast to slow to 3 per cent in 2012, from 4 per cent in 2011, reflecting lower production estimates from Syncrude Canada, and planned maintenance from the Sea Rose floating production storage and offloading (FPSO) and Terra Tonva FPSO. In 2013,

15

Canada’s oil production is expected to increase by 4 per cent to average 3.8 million barrels a day.

Latin America’s oil production is forecast to increase by 3 per cent in 2012 and 5 per cent in 2013. Increases are forecast to be underpinned by the development of several new projects in Brazil such as Petrobras’ Parque das Beleias and Roncador module 4, and Chevron’s Papa-Terra.

OPEC oil production is forecast to increase by 3 per cent in 2012 and 2013 to average 37.9 million barrels a day in 2013. Increases in OPEC production are forecast to be underpinned by growth in the production of natural gas liquids, while OPEC crude oil production is forecast to increase by 2 per cent a year.

Figure 3: World oil supply

Please refer to page 19 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Australia’s production and exports

Australia’s production of crude oil and condensate is forecast to contract by 8 per cent in 2011–12, relative to 2010–11, to total 22.8 gigaliters. Lower production reflects planned maintenance on the North West Shelf for a redevelopment project, multiple unplanned shut-ins throughout the Carnarvon basin during cyclone season, and declines from maturing fields. Output from the Kitan project in the Bonaparte Basin, which commenced in October 2011, is expected to partially offset these declines. In 2012–13, Australia’s crude oil and condensate production is forecast to increase by 1 per cent as a result of the commencement of crude production from the Montara/Skua project and condensate from the Kipper gas project.

Australia’s exports of crude oil and condensate are forecast to follow a similar profile to production. Exports are forecast to contact by 2 per cent in 2011–12, and increase by 1 per cent in 2012–13 to total 19.4 gigalitres. The value of Australian oil exports is forecast to increase to $13.3 billion in 2012–13, reflecting forecast higher oil prices (see Figure 4).

Figure 4: Australia’s crude oil and condensate exports

Please refer to page 20 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

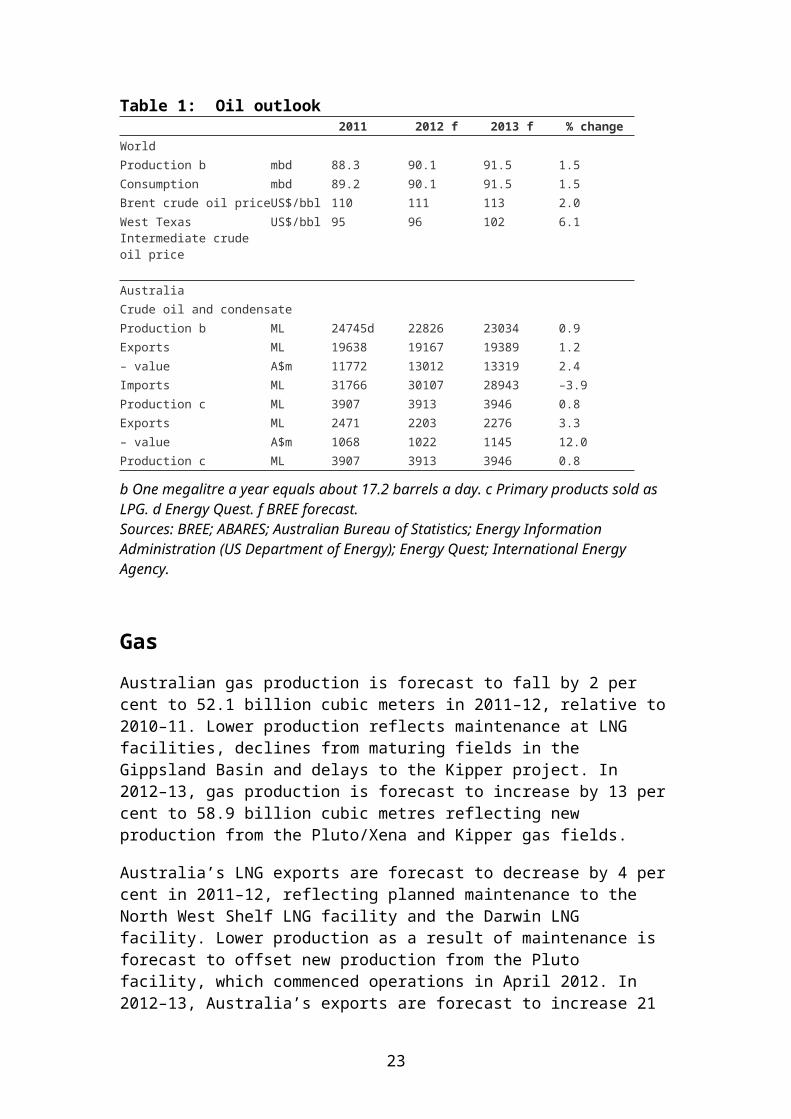

Table 1: Oil outlook2011 2012 f 2013 f % change

WorldProduction b mbd 88.3 90.1 91.5 1.5Consumption mbd 89.2 90.1 91.5 1.5Brent crude oil price US$/bbl 110 111 113 2.0West Texas Intermediate crude oil price

US$/bbl 95 96 102 6.1

16

2011 2012 f 2013 f % changeAustraliaCrude oil and condensateProduction b ML 24745d 22826 23034 0.9Exports ML 19638 19167 19389 1.2– value A$m 11772 13012 13319 2.4Imports ML 31766 30107 28943 –3.9Production c ML 3907 3913 3946 0.8Exports ML 2471 2203 2276 3.3– value A$m 1068 1022 1145 12.0Production c ML 3907 3913 3946 0.8

b One megalitre a year equals about 17.2 barrels a day. c Primary products sold as LPG. d Energy Quest. f BREE forecast.Sources: BREE; ABARES; Australian Bureau of Statistics; Energy Information Administration (US Department of Energy); Energy Quest; International Energy Agency.

Gas

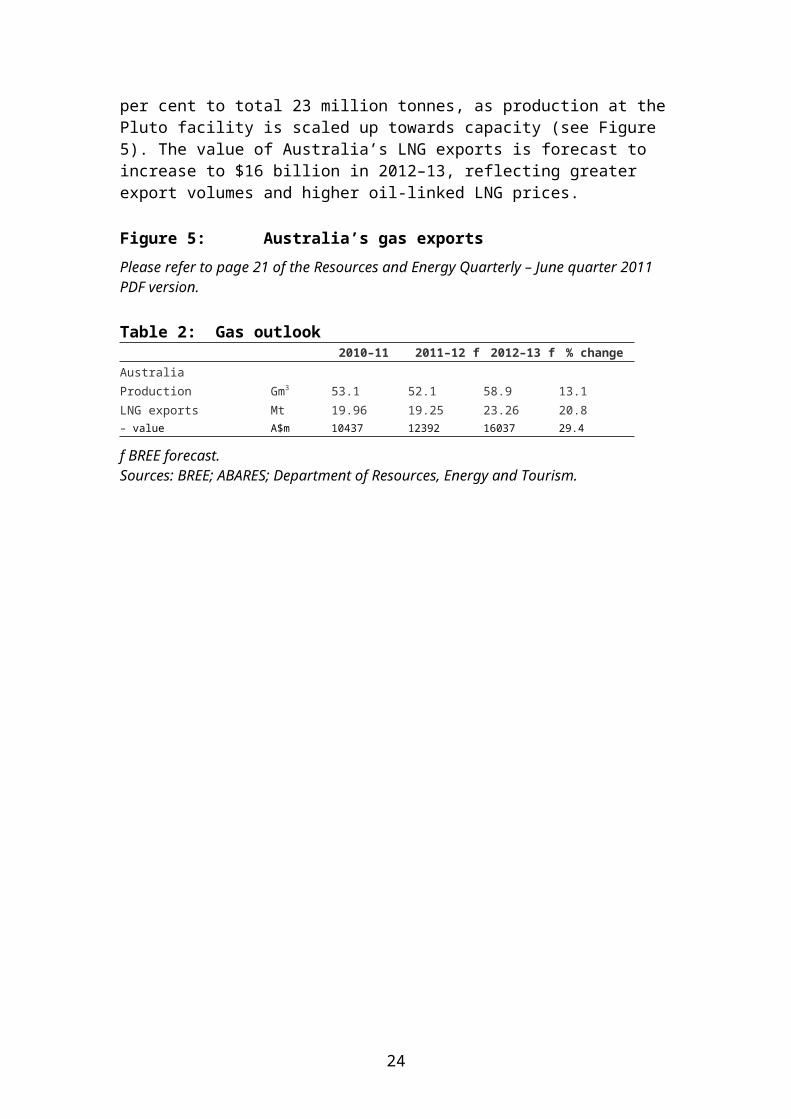

Australian gas production is forecast to fall by 2 per cent to 52.1 billion cubic meters in 2011–12, relative to 2010–11. Lower production reflects maintenance at LNG facilities, declines from maturing fields in the Gippsland Basin and delays to the Kipper project. In 2012–13, gas production is forecast to increase by 13 per cent to 58.9 billion cubic metres reflecting new production from the Pluto/Xena and Kipper gas fields.

Australia’s LNG exports are forecast to decrease by 4 per cent in 2011–12, reflecting planned maintenance to the North West Shelf LNG facility and the Darwin LNG facility. Lower production as a result of maintenance is forecast to offset new production from the Pluto facility, which commenced operations in April 2012. In 2012–13, Australia’s exports are forecast to increase 21 per cent to total 23 million tonnes, as production at the Pluto facility is scaled up towards capacity (see Figure 5). The value of Australia’s LNG exports is forecast to increase to $16 billion in 2012–13, reflecting greater export volumes and higher oil-linked LNG prices.

Figure 5: Australia’s gas exports

Please refer to page 21 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Table 2: Gas outlook2010–11 2011–12 f 2012–13 f % change

AustraliaProduction Gm3

53.1 52.1 58.9 13.1LNG exports Mt 19.96 19.25 23.26 20.8– value A$m 10437 12392 16037 29.4

f BREE forecast.Sources: BREE; ABARES; Department of Resources, Energy and Tourism.

17

Thermal coal

Tom Shael

Prices

Thermal coal contract prices were settled in early June at around US$115 a tonne for Japanese Financial Year (JFY) 2012 with several Japanese power utilities (see Figure 1). This price represents a decrease of about 12 per cent from the JFY 2011 price. In line with lower expected economic growth in China, India and the European Union (EU), thermal coal spot prices are around a US$30 a tonne discount from the JFY 2012 contract price.

Figure 1: JFY thermal coal prices

Please refer to page 22 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

World trade

The world thermal coal seaborne trade in 2012 is forecast to increase by around 4 per cent, relative to 2011, to total 871 million tonnes. The global seaborne trade in 2013 is forecast to increase by a further 5 per cent, relative to 2012, to total 919 million tonnes.

Imports

Growth in imports in 2012 and 2013 will primarily be supported by increased demand from Asia. Higher electricity demand associated with robust economic growth in emerging economies is expected to be a key driver of demand. India is forecast to contribute the most to this growth, growing by 14 per cent in 2012, relative to 2011, and by a further 17 per cent in 2013 to total 104 million tonnes. China is forecast to increase its seaborne imports by 6 million tonnes in both 2012 and 2013 to total 145 and 151 million tonnes, respectively.

In 2012, imports into the EU are forecast to fall by 1 million tonnes to 160 million tonnes. This expected decline is a result of assumed weak economic growth and lower electricity demand stemming from the euro zone crisis. In 2013 an assumed increase in economic growth in Europe will contribute to a 3 million tonnes increase in import demand into the EU from 2012 levels.

Japan’s imports of thermal coal are forecast to increase slightly in 2012 to total 128 million tonnes in response to the temporary shutdown of its nuclear electricity generation capacity. Japan’s imports in 2013 are forecast to increase by a further 1 million tonnes, to 129 million tonnes.

18

Exports

Higher import demand across 2012 and 2013 is forecast to be supplied with higher exports from Australia, Indonesia and Colombia. In 2012, Australia’s exports are forecast to increase by 11 per cent to 164 million tonnes. This represents a volume increase in Australia of 16 million tonnes that will be underpinned higher production rates from existing mines and recently commissioned operations. Increased volumes are forecast from: Xstrata’s Mangoola mine (annual capacity of 8 million tonnes), stage 1 of Yancoal’s Moolarben mine (8 million tonnes) and Peabody Energy’s expansion of its Wilpinjong operation (additional annual capacity of 2–3 million tonnes). In 2013, Australia’s exports are forecast to increase by a further 17 per cent to total 192 million tonnes. This large increase will be supported by production from soon-to-be-commissioned mines that include the Hunter Valley Operations Expansion (6 million tonnes) and Narrabri Coal Project stage 2 expansion (4.5 million tonnes).

In 2012, Indonesia’s exports are forecast to increase by 2 per cent to total 308 million tonnes, before increasing by a further 4 per cent in 2013 to 319 million tonnes. This growth is expected to be supported by increased production from PT Bumi’s, PT Adaro Energy’s and PT Indika Energy’s coal mines along with output expansions from mines located in the East Kalimantan region.

Exports from Colombia are forecast to remain relatively unchanged in 2012, before increasing by 6 million tonnes to total 82 million tonnes in 2013. Colombia’s higher thermal coal exports in 2013 should be supported by expansions to capacity at mines in the La Guajira and César regions.

In 2012, exports from the US are forecast to increase by 16 per cent, relative to 2011, to total 36 million tonnes. The sharp upturn is expected to be a response to low domestic demand arising from the cheap and plentiful supply of natural gas. Domestic production of thermal coal in the second half of 2012, however, is expected to decline sharply as producers respond to falling domestic demand and lower export prices. Despite the fall in production, exports should be robust as producers sell their stocks before placing mines on care and maintenance. Exports in 2013 are forecast to fall relative to 2012 levels to total 31 million tonnes.

Australia

In 2011–12, Australia’s thermal coal production is forecast to increase by 8 per cent, relative to 2010–11, to total 223 million tonnes. Production in 2012–13 is forecast to increase by a further 9 per cent, to 244 million tonnes.

In line with higher production, exports of thermal coal in 2011–12 and 2012–13 are forecast to be 159 million tonnes and 179 million tonnes, respectively. The growth in export volumes will be supported by increased port capacity associated with the start-up of the Port Waratah Coal Services’ Kooragang Island Coal Terminal expansion (11 million tonnes a year), the X50 expansion at Abbot Point (25 million

19

tonnes a year) and higher throughput at the Newcastle Coal Infrastructure Group’s Coal Terminal.

In 2011–12 the value of Australia’s thermal coal exports is forecast to increase by 24 per cent, relative to 2010–11, to total $17.4 billion primarily as a result of higher export volumes. In 2012–13, forecast higher export volumes will outweigh lower contract prices for JFY 2012 that should result in export earnings increasing to $18.6 billion.

Figure 2: Australia’s thermal coal exports

Please refer to page 24 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Table 1: Thermal coal outlook2011 2012 f 2013 f % change

WorldThermal coal Contract prices b US$/t 130 115 100 –13.0Coal trade Mt 837 871 919 5.4ImportsAsia Mt 569 599 632 5.4– China Mt 139 145 151 4.1– Chinese Taipei Mt 67 68 69 1.8– India Mt 78 89 104 16.9– Japan Mt 125 128 129 0.4– Korea, Rep. of Mt 97 99 102 3.0– Malaysia Mt 20 21 22 3.9– other Asia Mt 43 49 55 12.4Europe Mt 204 205 210 2.4– European Union 27 c Mt 161 160 163 1.6– other Europe Mt 43 45 48 5.5Other Mt 64 67 77 14.3ExportsAustralia Mt 148 164 192 18.5China Mt 13 12 12 2.5Colombia Mt 75 76 82 7.8Indonesia Mt 302 308 319 3.6Russian Federation Mt 97 99 99 0.6South Africa Mt 66 69 72 3.7United States Mt 31 36 31 –13.9Other Mt 105 108 111 2.3

2010–11 2011–12 f 2012–13 f % changeAustraliaProduction Mt 206.1s 223.4 244.3 13.8Exports Mt 143.3 159.0 179.3 19.6– value A$m 13956 17358 18590 13.8

b Japanese Fiscal Year, starting April 1, fob Australia basis, BREE Australia–Japan average contract price assessment. For steaming coal with a calorific value of 6700 kcal/kg (gross air dried. c Regarded as 27 countries for all years. f BREE forecast. s BREE estimate.Sources: BREE; ABARES; International Energy Agency; Coal Services Pty Ltd; Queensland Department of Mines and Energy.

20

Resources outlook

Steel and steel-making raw materials

Rubhen Jeya

Contract prices

In the first quarter of 2012, iron ore spot prices averaged around US$135 a tonne for 62 per cent iron ore content free on board (FOB) Australia, an increase of 4 per cent from the previous quarter. The increase in spot prices was largely due to the effect of weather-related supply disruptions in Western Australia and Brazil, and restocking in China. In the June quarter 2012, spot prices have averaged around US$135 a tonne, but prices in the second half of the June quarter have fallen. For 2012 as a whole, contract prices are forecast to average around US$136 a tonne (see Figure 1). In 2013, contract prices are assumed to moderate to average around US$131 a tonne. The forecast decrease in prices is a result of projected increased supply from Australia and Brazil, and a moderation of growth in import demand.

The June quarter 2012 contract prices for high-quality hard coking coal settled at around US$210 a tonne. This represents an 11 per cent decline from the March quarter contract price primarily due to weaker import demand. The September quarter contract prices are expected to settle higher at around US$225 a tonne partly as a result of reduced production associated with industrial action at BHP Billiton-Mitsubishi Alliance (BMA) mines in Queensland. For 2012 as a whole, contract prices for high-quality hard coking coal are forecast to average around US$221 a tonne. Hard coking coal contract prices are projected to moderate through 2013, underpinned by supply increases from Australia, Canada, Mongolia and Mozambique.

Figure 1: Raw material contract prices, FOB Australia

Please refer to page 26 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Steel

World steel consumption

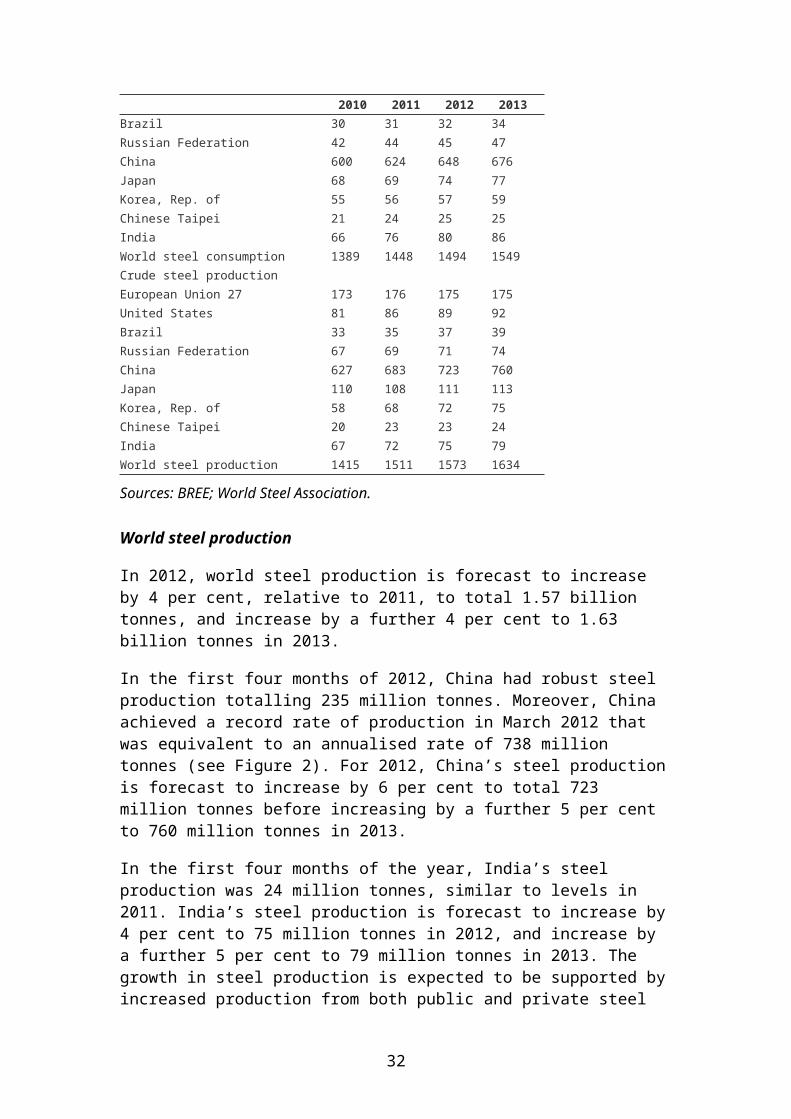

In 2012, world steel consumption is forecast to increase by 3 per cent, relative to 2011, to 1.5 billion tonnes, supported by demand from the construction of infrastructure projects in a number of developing economies. Despite robust growth in steel consumption, relative to 2011, the rate of growth is forecast to slow, in line with assumed weaker economic growth across the OECD and China. In 2013, world steel consumption is forecast to increase by about 4 per cent, relative to 2012, to total 1.55 billion tonnes (see Table 1).

21

In China, strong growth in steel consumption has been supported by the construction of public infrastructure and manufacturing of consumer durables. In 2012 and 2013, China’s steel consumption is forecast to increase by 4 per cent each year, to total 648 million tonnes and 676 million tonnes, respectively. Downward revisions have been made to China’s steel consumption growth from the March 2012 Resource and Energy Quarterly due to a reduction in assumed domestic economic growth.

In India, steel demand for infrastructure construction and higher consumption of consumer durables is expected to underpin a 7 per cent increase in steel consumption in 2013. In the European Union (EU), steel consumption is forecast to remain largely unchanged in 2012 and 2013 due to an assumed contraction in economic growth over the period.

Table 1: World steel consumption and production (Mt)2010 2011 2012 2013

Crude steel consumptionEuropean Union 27 160 162 162 162United States 90 94 95 97Brazil 30 31 32 34Russian Federation 42 44 45 47China 600 624 648 676Japan 68 69 74 77Korea, Rep. of 55 56 57 59Chinese Taipei 21 24 25 25India 66 76 80 86World steel consumption 1389 1448 1494 1549Crude steel productionEuropean Union 27 173 176 175 175United States 81 86 89 92Brazil 33 35 37 39Russian Federation 67 69 71 74China 627 683 723 760Japan 110 108 111 113Korea, Rep. of 58 68 72 75Chinese Taipei 20 23 23 24India 67 72 75 79World steel production 1415 1511 1573 1634

Sources: BREE; World Steel Association.

World steel production

In 2012, world steel production is forecast to increase by 4 per cent, relative to 2011, to total 1.57 billion tonnes, and increase by a further 4 per cent to 1.63 billion tonnes in 2013.

In the first four months of 2012, China had robust steel production totalling 235 million tonnes. Moreover, China achieved a record rate of production in March 2012 that was equivalent to an annualised rate of 738 million tonnes (see Figure 2). For 2012, China’s steel production is forecast to increase by 6 per cent to total 723

22

million tonnes before increasing by a further 5 per cent to 760 million tonnes in 2013.

In the first four months of the year, India’s steel production was 24 million tonnes, similar to levels in 2011. India’s steel production is forecast to increase by 4 per cent to 75 million tonnes in 2012, and increase by a further 5 per cent to 79 million tonnes in 2013. The growth in steel production is expected to be supported by increased production from both public and private steel producers. In the EU, steel production in 2012 and in 2013 is forecast to remain largely unchanged, relative to 2011, at around 175 million tonnes. This is due to the steel industry operating well below capacity.

Figure 2: Monthly world steel production

Please refer to page 28 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

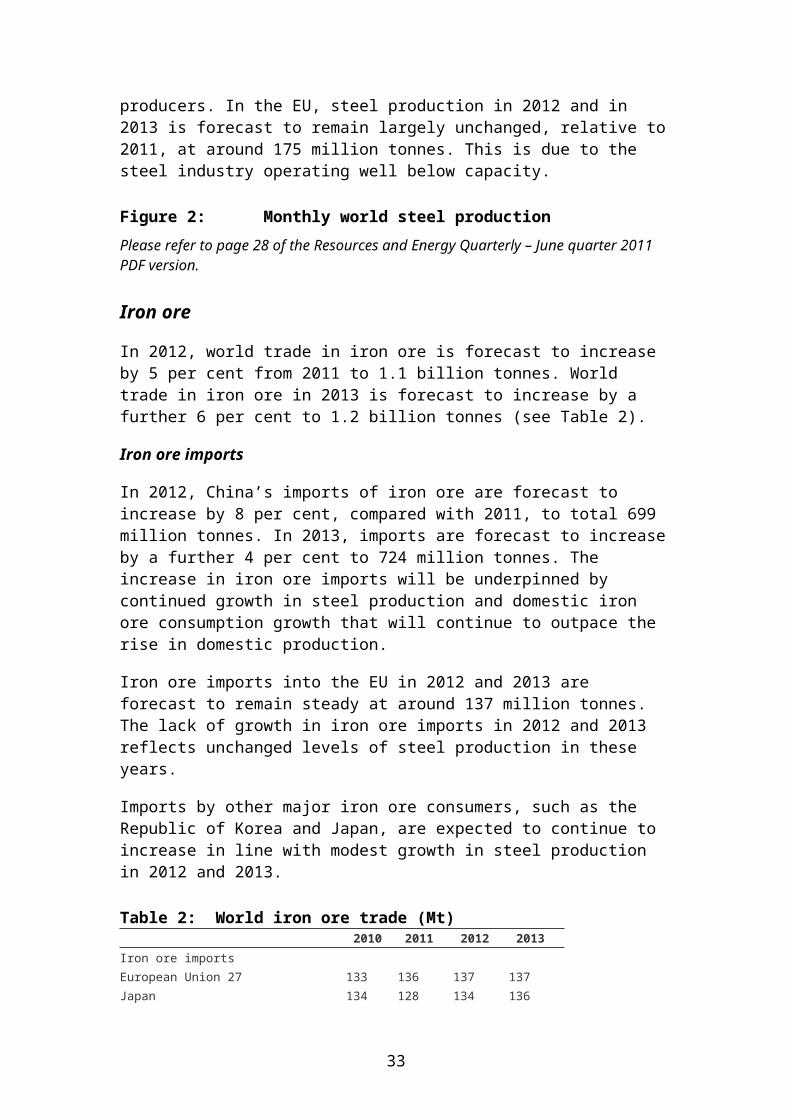

Iron ore

In 2012, world trade in iron ore is forecast to increase by 5 per cent from 2011 to 1.1 billion tonnes. World trade in iron ore in 2013 is forecast to increase by a further 6 per cent to 1.2 billion tonnes (see Table 2).

Iron ore imports

In 2012, China’s imports of iron ore are forecast to increase by 8 per cent, compared with 2011, to total 699 million tonnes. In 2013, imports are forecast to increase by a further 4 per cent to 724 million tonnes. The increase in iron ore imports will be underpinned by continued growth in steel production and domestic iron ore consumption growth that will continue to outpace the rise in domestic production.

Iron ore imports into the EU in 2012 and 2013 are forecast to remain steady at around 137 million tonnes. The lack of growth in iron ore imports in 2012 and 2013 reflects unchanged levels of steel production in these years.

Imports by other major iron ore consumers, such as the Republic of Korea and Japan, are expected to continue to increase in line with modest growth in steel production in 2012 and 2013.

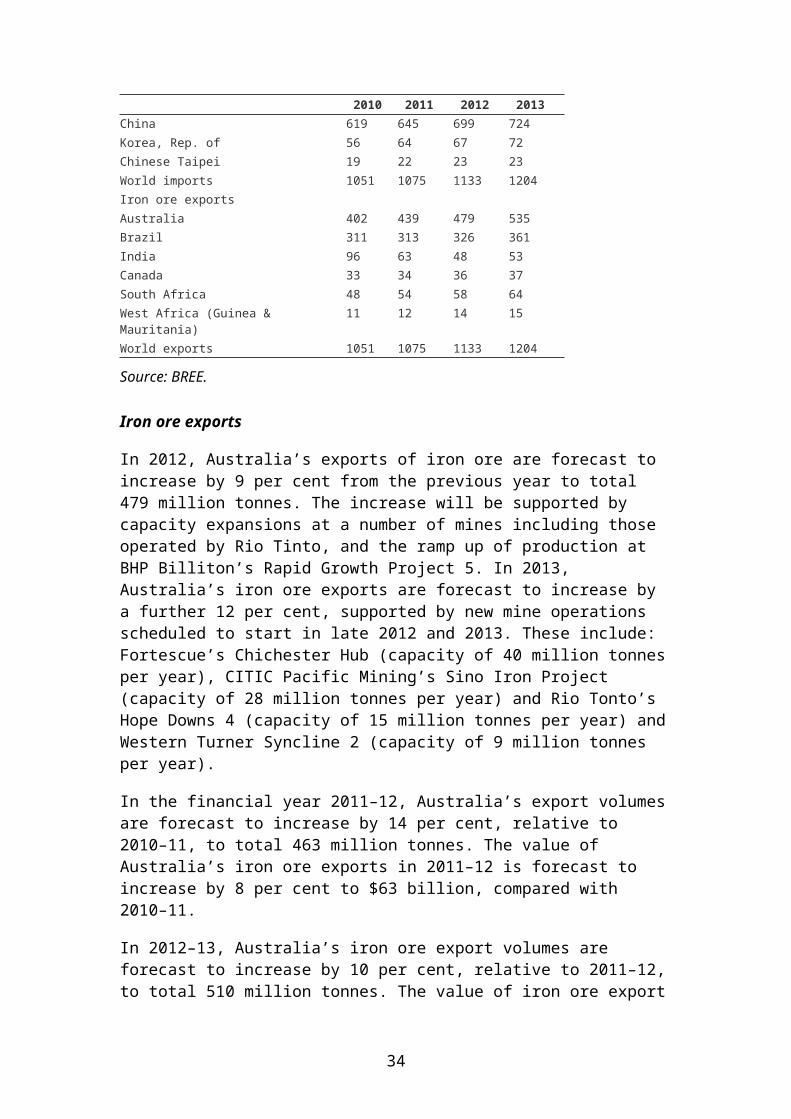

Table 2: World iron ore trade (Mt)2010 2011 2012 2013

Iron ore importsEuropean Union 27 133 136 137 137Japan 134 128 134 136China 619 645 699 724Korea, Rep. of 56 64 67 72Chinese Taipei 19 22 23 23World imports 1051 1075 1133 1204Iron ore exports

23

2010 2011 2012 2013Australia 402 439 479 535Brazil 311 313 326 361India 96 63 48 53Canada 33 34 36 37South Africa 48 54 58 64West Africa (Guinea & Mauritania) 11 12 14 15World exports 1051 1075 1133 1204

Source: BREE.

Iron ore exports

In 2012, Australia’s exports of iron ore are forecast to increase by 9 per cent from the previous year to total 479 million tonnes. The increase will be supported by capacity expansions at a number of mines including those operated by Rio Tinto, and the ramp up of production at BHP Billiton’s Rapid Growth Project 5. In 2013, Australia’s iron ore exports are forecast to increase by a further 12 per cent, supported by new mine operations scheduled to start in late 2012 and 2013. These include: Fortescue’s Chichester Hub (capacity of 40 million tonnes per year), CITIC Pacific Mining’s Sino Iron Project (capacity of 28 million tonnes per year) and Rio Tonto’s Hope Downs 4 (capacity of 15 million tonnes per year) and Western Turner Syncline 2 (capacity of 9 million tonnes per year).

In the financial year 2011–12, Australia’s export volumes are forecast to increase by 14 per cent, relative to 2010–11, to total 463 million tonnes. The value of Australia’s iron ore exports in 2011–12 is forecast to increase by 8 per cent to $63 billion, compared with 2010–11.

In 2012–13, Australia’s iron ore export volumes are forecast to increase by 10 per cent, relative to 2011–12, to total 510 million tonnes. The value of iron ore export values in 2013–13 is forecast to increase by 7 per cent to $67 billion (see Figure 3). This value is largely attributable to an increase in export volumes that will outweigh a slight decline in prices from the previous corresponding period.

In 2012, Brazil’s iron ore exports are forecast to increase by 4 per cent, relative to 2011, to total 326 million tonnes. Brazil’s exports in 2013 are forecast to increase by 11 per cent year on year to total 361 million tonnes. The slower growth in 2012, relative to 2013 is largely attributable to weather related production losses in the first quarter of 2012. The increase in exports in 2013 is largely a result of the increase in production at a number of mines in the south-eastern Systems and at Carajas where production is expected to ramp up from recent expansions and also from increased production at existing mines as these return to normal levels of production. A large proportion of these exports are expected to be sourced from expansions to Vale’s operations.

Figure 3: Australia’s iron ore exports

Please refer to page 30 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

24

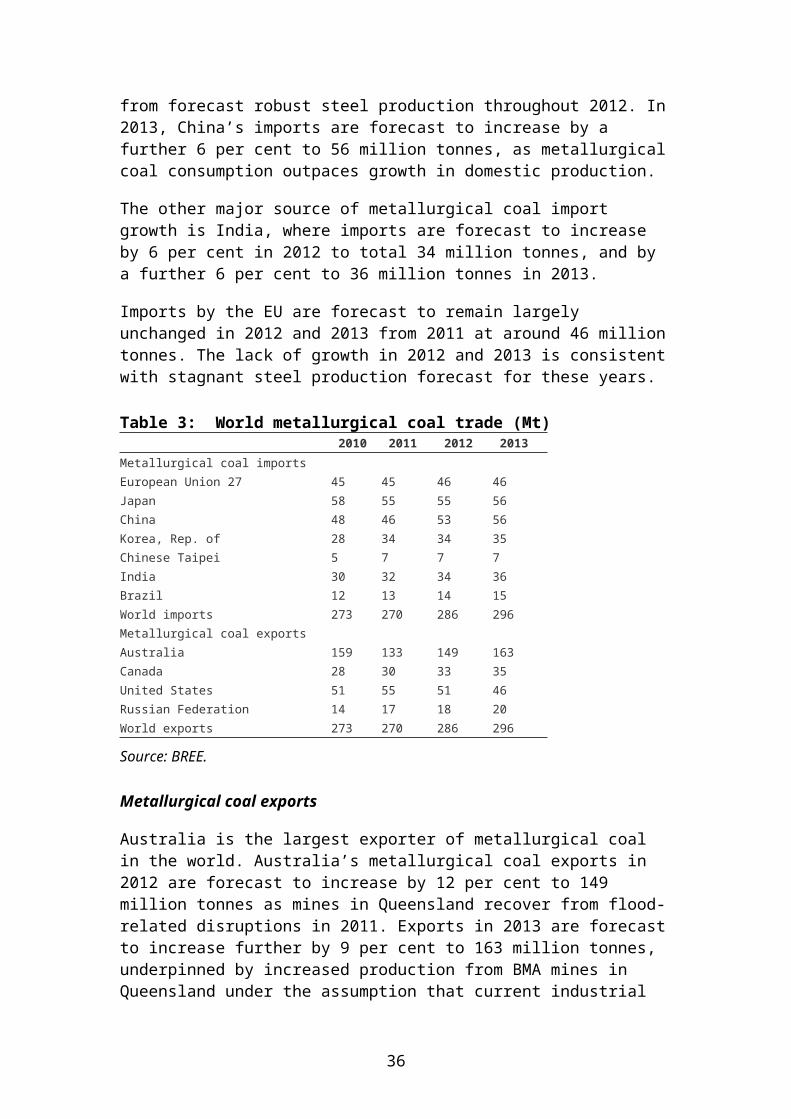

Metallurgical coal

In 2012, global trade in metallurgical coal is forecast to increase by 6 per cent to 286 million tonnes. World metallurgical trade is forecast to increase by a further 3 per cent to 296 million tonnes in 2013 supported by import growth in China and India (see Table 3).

Metallurgical coal imports

In the first three months of 2012, China increased its imports of metallurgical coal by around 17 per cent from the previous quarter. The higher volumes were sourced from increased exports from Australia and Mongolia. For 2012 as a whole, China’s metallurgical coal imports are forecast to increase by 15 per cent to 53 million tonnes, partly as a result of restocking at steel mills, but also from forecast robust steel production throughout 2012. In 2013, China’s imports are forecast to increase by a further 6 per cent to 56 million tonnes, as metallurgical coal consumption outpaces growth in domestic production.

The other major source of metallurgical coal import growth is India, where imports are forecast to increase by 6 per cent in 2012 to total 34 million tonnes, and by a further 6 per cent to 36 million tonnes in 2013.

Imports by the EU are forecast to remain largely unchanged in 2012 and 2013 from 2011 at around 46 million tonnes. The lack of growth in 2012 and 2013 is consistent with stagnant steel production forecast for these years.

Table 3: World metallurgical coal trade (Mt)2010 2011 2012 2013

Metallurgical coal importsEuropean Union 27 45 45 46 46Japan 58 55 55 56China 48 46 53 56Korea, Rep. of 28 34 34 35Chinese Taipei 5 7 7 7India 30 32 34 36Brazil 12 13 14 15World imports 273 270 286 296Metallurgical coal exportsAustralia 159 133 149 163Canada 28 30 33 35United States 51 55 51 46Russian Federation 14 17 18 20World exports 273 270 286 296

Source: BREE.

Metallurgical coal exports

Australia is the largest exporter of metallurgical coal in the world. Australia’s metallurgical coal exports in 2012 are forecast to increase by 12 per cent to 149

25

million tonnes as mines in Queensland recover from flood-related disruptions in 2011. Exports in 2013 are forecast to increase further by 9 per cent to 163 million tonnes, underpinned by increased production from BMA mines in Queensland under the assumption that current industrial disputes conclude shortly. There is also expected to be increased production from a number of mines that are scheduled to start up in 2013, such as Peabody Energy’s Burton mine and at Anglo Coal’s Grosvenor underground mines.

In 2012, US metallurgical coal exports are forecast to decrease by 7 per cent relative to 2011 to total 51 million tonnes. Exports are forecast to decline by a further 11 per cent in 2013 to total 46 million tonnes. The decline in US metallurgical coal exports is partly a result of a decline in import demand in Europe and from the idling of a number of coal mines.

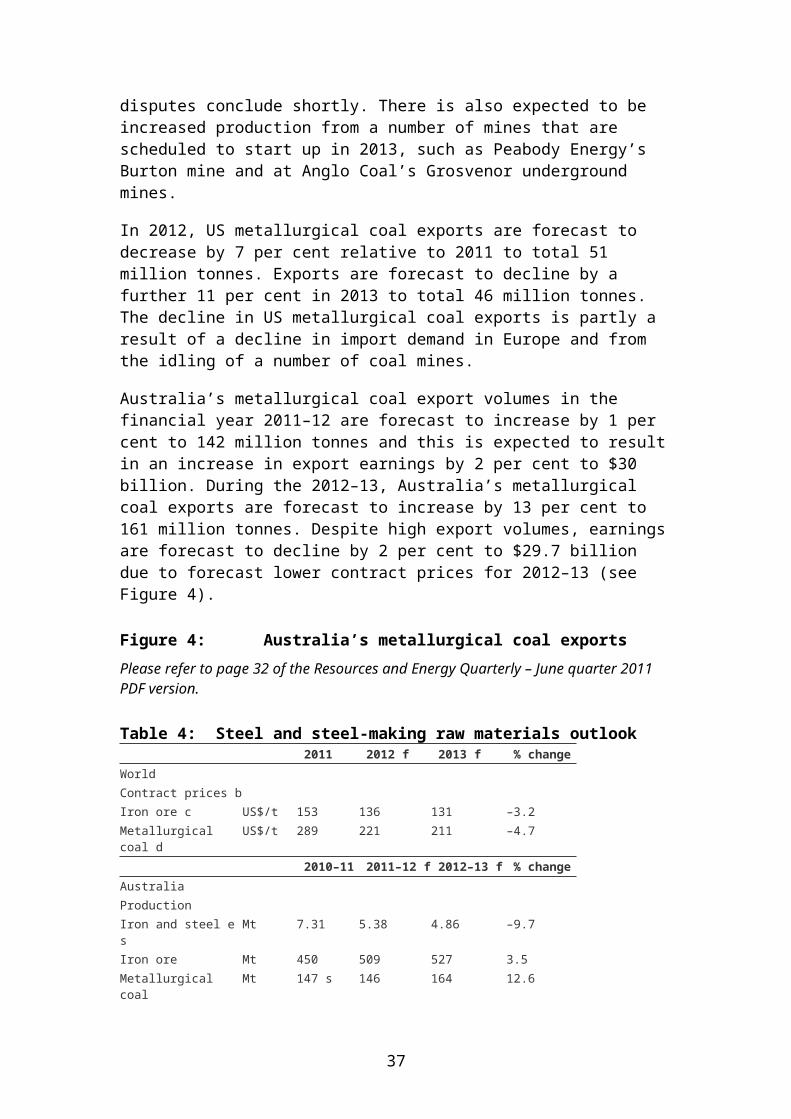

Australia’s metallurgical coal export volumes in the financial year 2011–12 are forecast to increase by 1 per cent to 142 million tonnes and this is expected to result in an increase in export earnings by 2 per cent to $30 billion. During the 2012–13, Australia’s metallurgical coal exports are forecast to increase by 13 per cent to 161 million tonnes. Despite high export volumes, earnings are forecast to decline by 2 per cent to $29.7 billion due to forecast lower contract prices for 2012–13 (see Figure 4).

Figure 4: Australia’s metallurgical coal exports

Please refer to page 32 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Table 4: Steel and steel-making raw materials outlook2011 2012 f 2013 f % change

WorldContract prices bIron ore c US$/t 153 136 131 –3.2Metallurgical coal d US$/t 289 221 211 –4.7

2010–11 2011–12 f 2012–13 f % changeAustraliaProductionIron and steel e s Mt 7.31 5.38 4.86 –9.7Iron ore Mt 450 509 527 3.5Metallurgical coal Mt 147 s 146 164 12.6ExportsIron and steel e s Mt 1.78 1.19 1.02 –14.3– value A$m 1 303 983 789 –19.7Iron ore Mt 407 463 510 10.3– value A$m 58387 62788 66936 6.6Metallurgical coal Mt 140 142 161 13.4– value A$m 29793 30310 29682 –2.1

b fob Australian basis, BREE Australia–Japan average contract price assessment. c Fines contract, 62% iron content basis. d High–quality hard coking coal. For example, Goonyella export coal. e Includes all steel items in ABS, Australian Harmonized Export Commodity Classification, chapter 72, ‘Iron and steel’, excluding ferrous waste and scrap and ferroalloys.

26

f BREE forecast. s BREE estimate.Sources: BREE; ABARES; International Iron and Steel Institute; Coal Services Australia; Queensland Coal Board; United Nations Conference on Trade and Development.

27

Gold

Adam Bialowas

Prices

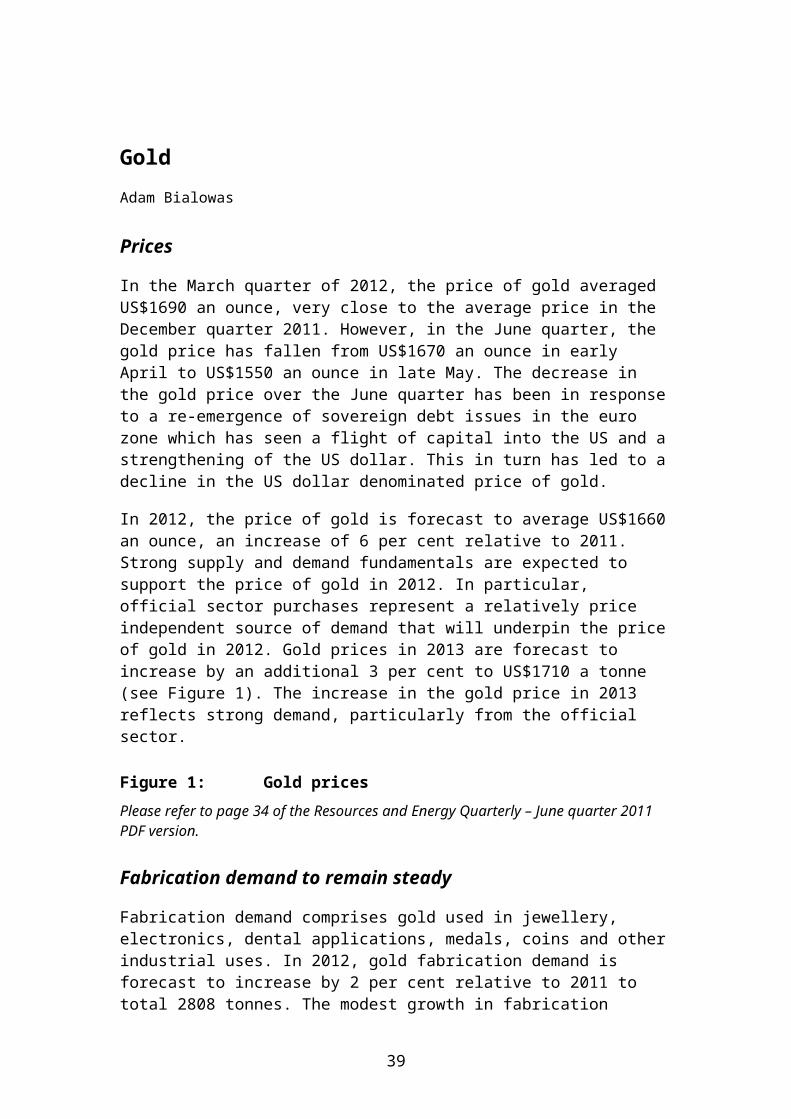

In the March quarter of 2012, the price of gold averaged US$1690 an ounce, very close to the average price in the December quarter 2011. However, in the June quarter, the gold price has fallen from US$1670 an ounce in early April to US$1550 an ounce in late May. The decrease in the gold price over the June quarter has been in response to a re-emergence of sovereign debt issues in the euro zone which has seen a flight of capital into the US and a strengthening of the US dollar. This in turn has led to a decline in the US dollar denominated price of gold.

In 2012, the price of gold is forecast to average US$1660 an ounce, an increase of 6 per cent relative to 2011. Strong supply and demand fundamentals are expected to support the price of gold in 2012. In particular, official sector purchases represent a relatively price independent source of demand that will underpin the price of gold in 2012. Gold prices in 2013 are forecast to increase by an additional 3 per cent to US$1710 a tonne (see Figure 1). The increase in the gold price in 2013 reflects strong demand, particularly from the official sector.

Figure 1: Gold prices

Please refer to page 34 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Fabrication demand to remain steady

Fabrication demand comprises gold used in jewellery, electronics, dental applications, medals, coins and other industrial uses. In 2012, gold fabrication demand is forecast to increase by 2 per cent relative to 2011 to total 2808 tonnes. The modest growth in fabrication demand reflects high gold prices that are expected to dampen consumption growth in many markets. This increase is driven largely by China, where income growth has fuelled significant demand for gold jewellery. In 2013, reflecting expectations of a more stable gold price, fabrication demand for gold is expected to increase by 2 per cent to 2856 tonnes.

Official sector purchases to continue

In 2012, official sector purchases of gold are expected to remain robust at 425 tonnes, similar to levels in 2011. The levels of official sector purchases are due to the exposure of many central banks to foreign exchange risks. The recent variability of the US dollar relative to some national currencies and concerns over the euro has led to increased interest in gold as a means of diversifying central bank asset holdings. In

28

2013 the official sector is expected to remain a net purchaser of gold at a level of 400 tonnes, as uncertainty remains in financial and asset markets.

Supply to increase modestly

World gold mine production in 2012 is forecast to increase by 3 per cent, relative to 2011, to 2907 tonnes. Production is expected to increase in Canada as a result of new developments such as New Gold’s New Afton project and AuRico’s Young-Davidson operation. Gold production in Turkey is also expected to increase due to the start up of Eldorado Gold’s Efemçukuru and Alacer Gold’s copper operations.

Global gold mine production is forecast to increase in 2013 by a further 2 per cent to 2977 tonnes. Strong growth is expected to come from the Russian Federation as a result of Polyus Gold’s Verninskoye and Natalka operations. Latin America will become an increasingly important gold producing region with new mines starting up such as Newgold’s Cerro Negro operation in Argentina and Barrick’s Pueblo Viejo mine in the Dominican Republic.

Reduced availability to see scrap supply decline

In 2012 the supply of scrap is forecast to decrease by 7 per cent to 1550 tonnes. The fall in scrap supply reflects consumers’ willingness to hold gold in the absence of better alternative investments. It also reflects the decreased availability of scrap as stock levels have been run down significantly over the past four years following successive increases in gold prices. Similarly, despite a forecast price increase in 2013, the quantity of gold sourced from scrap is expected to decline by a further 6 per cent to 1450 tonnes.

Australia’s gold production to increase strongly

Australia’s gold mine production in 2011–12 is forecast to decrease by 1 per cent relative to 2010–11 to total 261 tonnes. The decrease in production is due to a number of mines taking advantage of high gold prices to target lower ore grades that would otherwise have been uneconomic to extract.

Australia’s gold mine production in 2012–13 is expected to increase by 8 per cent relative to 2010–11 to total 283 tonnes. The largest contribution to this increase is expected to come from Newcrest’s Cadia East operation with an increase in capacity of 8 tonnes a year. Other mines starting up in 2012–13 include Millennium Minerals’ Nullagine and Crocodile Gold’s Cosmo Deeps.

Australia’s gold exports consist of refined gold from domestic mine production and imports of gold dore (impure gold) and scrap gold, which are shipped to Australia and then refined into gold bullion and re–exported. In 2011–12, the volume of Australia’s gold exports is forecast to increase by 10 per cent, relative to 2010–11, to total 331 tonnes. The increase in exports is expected to be supported by a forecast increased availability of scrap and gold dore from international sources as a result of

29

continued high prices for gold. Accordingly, the value of Australia’s gold exports is forecast to rise by 20 per cent in 2011–12 to $15.6 billion (see Figure 2).

In 2012–13, increases in exports of both domestically produced gold and re-exported scrap are forecast to result in export volumes rising by 9 per cent to 361 tonnes. The value of Australia’s gold exports is forecast to increase by 27 per cent to $19.7 billion. This reflects a combination of high gold prices and increased export volumes.

Figure 2: Australia’s gold exports

Please refer to page 36 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Table 1: Gold outlook2011 2012 f 2013 f % change

WorldFabrication consumption t 2759 2808 2856 1.7Mine production t 2818 2907 2977 2.4– China t 371 380 390 2.6– Australia t 259 272 297 9.2– United States t 233 240 247 2.9– Russian Federation t 212 217 222 2.3– South Africa t 198 195 190 –2.6Scrap sales t 1661 1550 1450 –6.5Net stock sales t (1720) (1633) (1551) –5.0– official sector t 455 425 400 –5.9– private sector t (1271) (1214) (1161) –4.0– producer hedging t 6 (10) (10) 0.0Price b US$/oz 1569 1663 1713 3.0

2010–11 2011–12 f 2012–13 f % changeAustraliaMine production t 265 261 283 8.4Exports t 301 331 361 9.1– value A$m 13016 15558 19722 26.8Price A$/oz 1389 1624 1698 4.5

b London Bullion Market Association AM price. f BREE forecast.Note: Net purchasing and dehedging shown in brackets.Sources: BREE; ABARES; Gold Fields Mineral Services; Australian Bureau of Statistics; London Bullion Market Association.

30

Metals overview

Adam Bialowas

Metals consumption

In the March quarter 2012, global consumption of aluminium, copper and nickel increased across most large consuming regions. The increase in consumption was largely underpinned increasing consumption in China and the US. Europe's consumption of metals in the first quarter of 2012 was generally lower, relative to the corresponding period in 2011 (see Figure 1).

While China's economic growth slowed in the first quarter of 2012, relative to the corresponding quarter in 2011, it remained robust and supportive of increased metals consumption. Also supporting China's metal consumption was the restocking of depleted inventories. The growth in US metals consumption was underpinned by improvements in economic activity and industrial production. Importantly for the US economy, housing construction has started to pick up which is a large consumer of copper and aluminium. In Europe, weak economic growth across the region has resulted in lower consumption of most metals in the March quarter of 2012, with the exception of nickel.

Figure 1: March quarter consumption of base metals, 2011 vs 2012

Please refer to page 37 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

In the June quarter 2012, uncertainty over the economic outlook is expected to result in weaker metals consumption growth in China and the US and the continued contraction of consumption in Europe. The uncertainty over potential impacts from Europe's sovereign debt crisis has resulted in lower consumer and business confidence. Many European economies are now in recession, which is expected to result in lower demand for metal-intensive products. In China, reduced economic activity in one of its major trading partners, Europe, is expected to result in a slowing in manufacturing activity. This in turn will lead to a slowing of economic growth and manufacturing activity resulting in a slowing of demand for metals. These developments have been reflected in price movements over the past quarter (see Figure 2). All metals prices have fallen over the course of the quarter with the largest decreases being for copper (16 per cent) and nickel (13 per cent).

Figure 2: Index of daily base metal prices

Please refer to page 38 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

31

Over the second half of 2012 and in 2013, metals consumption growth is expected to be subdued relative to growth rates in 2011 and 2010. Consumption growth in 2013 may start to increase associated with assumed stronger economic growth, particularly in Europe. In China the implementation of a stimulus package would be supportive of increased metals consumption. In the US, low energy prices, particularly for coal and gas, could be supportive of increased manufacturing activity, which in turn would support metals demand.

Metals prices

In 2012, most metals prices are forecast to decrease relative to 2011, before increasing modestly in 2013. The extent to which metals prices fall in 2012, relative to 2011 is linked to two factors. Firstly, metals price decreases will reflect market expectations for future consumption. If the economic conditions around the world worsen, metals prices would likely continue to fall.

Related to the economic outlook are movements of the US dollar. Economic uncertainty could lead to a flight of capital to US dollar denominated safe haven or quality investments. This would result in an appreciation of the value of the US dollar against other currencies, which in turn would reduce the purchasing power of non US denominated currencies place further downward pressures on commodity prices.

The second factor is the extent which metals production costs have increased over the past decade, which could limit price decreases. Capital and operating costs have been impacted by increases in the costs of plant and machinery, labour and other inputs. Additionally, high prices for many base metals in the preceding few years provided incentives for producers to mine progressively lower grade ores and/or deposits that are technically more difficult to mine. If prices continue to fall, the higher extraction and refining costs will cause a number of mines will become unprofitable and will be shut down. This in turn will lead to a reduction in supply which will provide some support for commodity prices.

In 2013, prices for most metals are forecast to increase as economic growth and consumption increase and under the assumption that the uncertainty that currently surrounds the economic outlook starts to ease (see Figure 3).

Figure 3: Index of quarterly base metal prices

Please refer to page 39 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

32

Copper

Adam Bialowas

Prices to decline in 2012 and 2013

In the March quarter of 2012 the price of copper averaged $US8300 a tonne. This represented an 11 per cent increase compared to the December quarter 2011 but a 14 per cent fall when compared to the March quarter 2011.

In the June quarter 2012 the copper price declined from US$8580 a tonne in early April to US$7520 a tonne in late-May. For 2012 as a whole, copper prices are forecast to average $US7860 a tonne, a decrease of 11 per cent relative to 2011 (see Figure 1). The decrease in prices over the June quarter and compared with 2011 is due to weaker market sentiment towards the outlook for global copper consumption. The weakening of market sentiment has occurred because of recent weaker Chinese economic data and uncertainty over the outlook for a number of large European economies.

Copper prices in 2013 are forecast to decrease by a further 3 per cent to $US7608 a tonne. Growth in world refined copper production is expected to outpace growth in consumption in 2013, placing downward pressure on prices.

Figure 1: Copper prices and stocks

Please refer to page 40 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Consumption to increase steadily

World consumption of refined copper in 2012 is forecast to increase by 4 per cent, relative to 2011, to total 20.3 million tonnes. A large proportion of this increase is expected to occur in China where copper consumption is forecast to increase by 8 per cent in 2012, to 8.5 million tonnes. Other countries where copper consumption is forecast to grow include: the US (up 4 per cent to 1.8 million tonnes), the Republic of Korea (up 6 per cent to 792 000 tonnes) and Brazil (up 4 per cent to 439 000 tonnes). By contrast, many OECD countries such as Germany and Italy are expected to register stagnant or decreases in consumption in 2012.

In 2013 world refined copper consumption is forecast to increase by a further 5 per cent, to 21.4 million tonnes. The strongest growth in consumption is forecast to occur in China (up 8 per cent to 9.2 million tonnes), supported by growth in other non-OECD economies such as Brazil (up 8 per cent to 475 000 tonnes), the Russian Federation (up 4 per cent to 720 000 tonnes) and India (up 5 per cent to 438 000 tonnes).

33

Mine production to grow strongly in 2013

In 2012 world copper production is forecast to increase by 2 per cent relative to 2011 to 16.5 million tonnes. The increase in copper production assumes an easing of industrial and labour disputes in Latin America and Indonesia which adversely impacted copper production in 2011. Africa’s copper production in 2012 is also forecast to increase, relative to 2011, underpinned by new operations such as First Quantum Minerals’ Kansanshi operation (annual capacity of 400 000 tonnes) and a continued ramp up to full production at Vedanta Resource’s Konkola operation (200 000 tonnes), both of which are located in Zambia.

World copper mine production in 2013 is expected to increase a further 9 per cent to 18 million tonnes, with growth occurring in Chile (up 4 per cent to 6 million tonnes) and Peru (up 7 per cent to 1.5 million tonnes). In Chile, Antofagasta’s Esperanza mine (annual capacity of 210 000 tonnes) is continuing to ramp up towards full production while in Peru Chinalco’s Tormocho mine (200 000 tonnes) is expected to commence production in 2013. Australia’s copper production in 2013 is forecast to increase by 16 per cent to 1.2 million tonnes supported by an expansion of the Cadia East mine and the start up of the Nullagine and DeGrussa mines.

Refined production to follow growth in mine production

In 2012 world refined production is forecast to increase by only 2 per cent to 20.2 million tonnes. Increases in world refined copper production are expected to continue to be constrained by a shortage of concentrates, rather than a lack of refining capacity. Growth is expected to come from Africa, particularly the Democratic Republic of Congo and Zambia, both of which have new mines which employ the solvent-extraction electro-winning (SX-EW) mining technique. China is forecast to remain the world’s largest producer of refined copper, increasing production by 8 per cent to 5.6 million tonnes. In 2013, as a result of improved concentrate availability, refined copper production is expected to grow by 6 per cent to 21.5 million tonnes. Increased production is expected to occur mainly in China and Africa.

Australia’s copper production and exports to increase

In 2011–12, Australia’s copper mine production is forecast to increase by 2 per cent, relative to 2010–11, to 971 000 tonnes. Increased production will be supported by the start up of Hillgrove Resources’ Kanmantoo mine (annual capacity of 20 000 tonnes) and Kimberley Metals’ Mineral Hill operation (10 000 tonnes). These new operations will more than offset the effects of the closure of Kagara Mining’s operation (annual capacity of 20 000 tonnes) in early 2012.

Australian copper mine production in 2012–13 is forecast to increase by 15 per cent to 1.1 million tonnes. A large proportion of this increase is expected to come from production at Newcrest’s expanded Cadia East operation (additional annual capacity of 80 000 tonnes) as well as the start up of Sandfire Resources’ DeGrussa operation (annual capacity of 70 000 tonnes). Assuming no unplanned refinery outages,

34

Australia’s refined copper production in 2012–13 is expected to increase 4 per cent to relative to 2011-12 to 504 000 tonnes.

Consistent with increased mine production, the metallic content of Australia’s copper exports is forecast to increase by 4 per cent in 2011–12 to 880 000 tonnes. The increase is expected to just offset a decline in the Australian dollar denominated price of copper, with the value of Australian copper exports remaining relatively unchanged at $8.4 billion (see Figure 2).

In 2012–13 exports of Australian copper, in metallic content terms, are forecast to increase by a further 10 per cent to 966 000 tonnes. The increase is expected to more than offset a decline in the Australian dollar denominated price of copper, resulting in a 7 per cent increase in the value of Australian copper exports to $9 billion.

Figure 2: Australia’s copper exports

Please refer to page 42 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Table 1: Copper outlook2011 2012 f 2013 f % change

World Mine production kt 16242 16533 18039 9.1– Chile kt 5263 5752 5959 3.6– China kt 1267 1356 1463 7.9– Peru kt 1235 1396 1496 7.2– United States kt 1138 1239 1369 10.5– Australia kt 959 1017 1184 16.4– Zambia kt 784 847 1010 19.2Refined production kt 19791 20249 21490 6.1Consumption kt 19472 20294 21366 5.3– China kt 7915 8540 9249 8.3– United States kt 1756 1824 1884 3.3– Germany kt 1251 1255 1260 0.4– Japan kt 1007 1000 1000 0.0– Korea, Rep. of kt 747 792 822 3.8– Russian Federation kt 676 692 720 4.0Closing stocks kt 985 940 1064 13.2– weeks consumption 2.6 2.4 2.6 8.3Price US$/t 8852 7860 7608 –3.2

USc/lb 401.5 365.5 345.1 –3.22010–11 2011–12 f 2012–13 f % change

Australia Mine output kt 952 971 1113 14.6Refined output kt 485 484 504 4.1Exports – ores and concentrates b

kt 1750 1832 2227 21.6

– refined kt 375 386 365 –5.4– total value A$m 8422 8418 9043 7.4

35

b Quantities refer to gross weight of all ores and concentrates. f BREE forecast.Sources: BREE; ABARES; Australian Bureau of Statistics; International Copper Study Group; World Bureau of Metal Statistics.

36

Aluminium

George Stanwix

Aluminium prices to recover

Falling world aluminium demand growth has largely contributed to the downward movement in aluminium prices in the first half of 2012. Aluminium prices averaged around US$2100 a tonne in the first half of 2012, a 17 per cent decrease on the corresponding period in 2011. For 2012 as a whole, aluminium prices are forecast to decline by 12 per cent relative to 2011, to average around US$2100 a tonne. Further price declines are expected to be limited by production curtailments and rising input costs in key producing regions. Aluminium stocks in 2012 are forecast to increase by 13 per cent, compared with 2011, to reach around 8.1 million tonnes, or 9.4 weeks of consumption (see Figure 1).

In 2013, aluminium prices are forecast to increase, by 9 per cent, relative to 2012, to average around US$2300 a tonne, underpinned by stronger aluminium consumption. The growth in aluminium demand is expected to be faster than the increase in production and is expected to result in a decrease in stocks to 8.3 million tonnes at the end of 2013, or around 9 weeks of consumption.

Figure 1: Aluminium prices and stocks

Please refer to page 44 of the Resources and Energy Quarterly – June quarter 2011 PDF version.

Aluminium consumption growth to strengthen in 2013