Embed Size (px)

Citation preview

McKinsey Global InstituteSustainability and Resource Productivity Practice

Overview of conclusions February 15th, 2011

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Resource Revolution: Meeting the world’s energy, materials, food and water needs

McKinsey & Company 1|

Contents

▪ Overview

▪ Key exhibits

McKinsey & Company 2|

Key messages (1/2)

During the 20th century, real resource prices fell by almost half, despite a 20-fold expansion in global GDP.

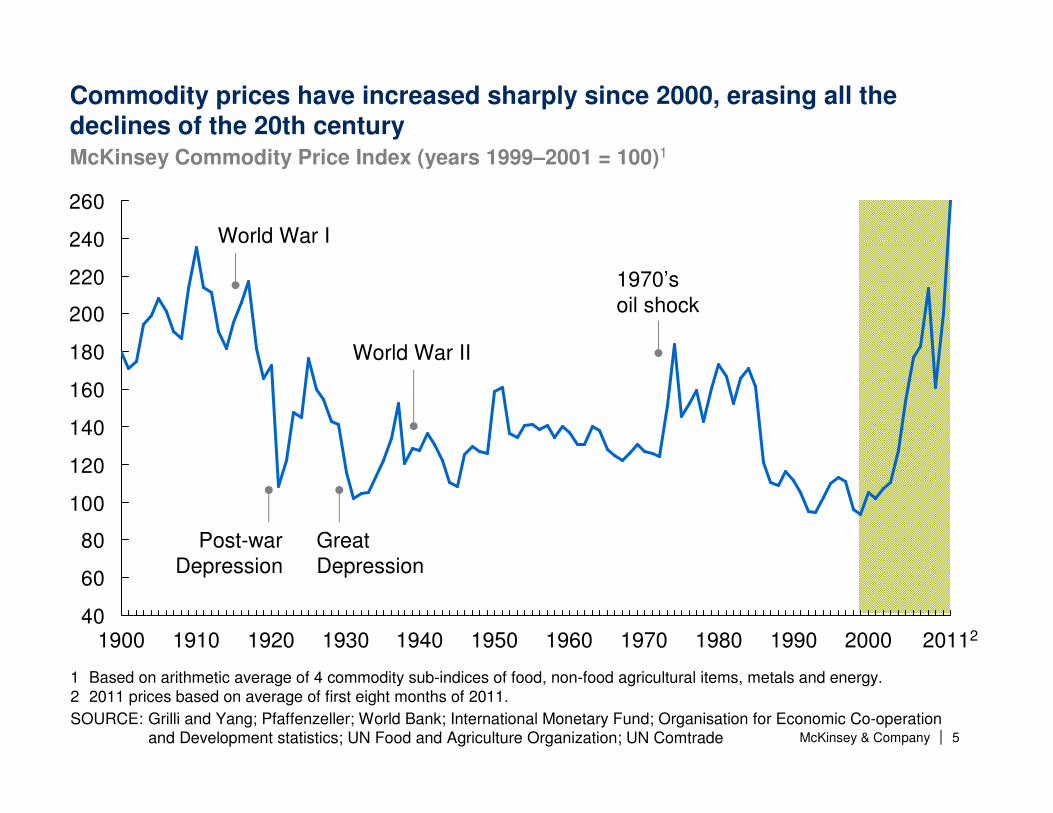

The last decade has undone the effects of the previous 100-year decline in resource prices. With the exception of energy in the 1970s, resource price volatility is at an all-time high.

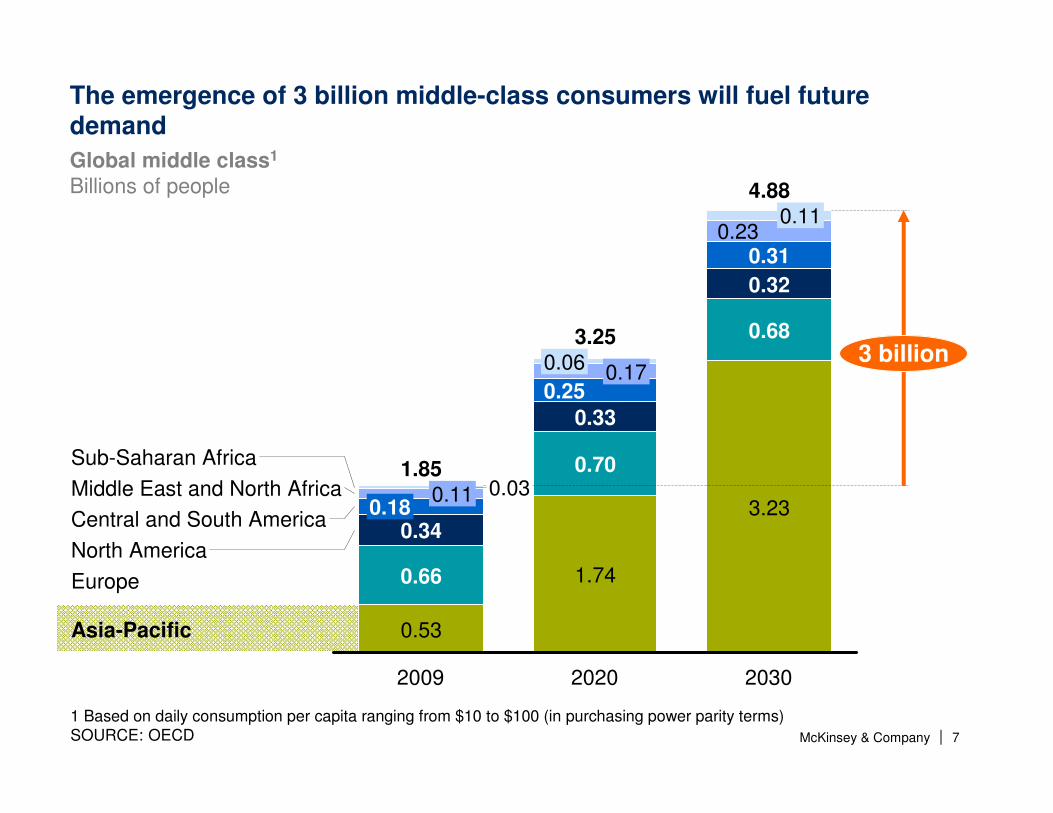

This is likely (but not certain) to continue over the next 20 years as 3 billion new middle class consumers are added to the global economy (especially in China and India), with demand for key resources increasing by up to 80%.

Resource productivity – both on the demand and supply-side - has the potential to address up to 30% of 2030 total resource demand.

Our estimates suggest that, excluding environmental externalities, the resource productivity prize could be worth $2.9 trillion per annum by 2030. Including these externalities and adjusting for subsidies, the prize would be worth $3.7 trillion per annum.

Just 15 types of opportunity, from improving the energy efficiency of buildings to moving to more efficient irrigation, represent roughly 75 percent of this prize.

While some supply expansion, especially for energy and steel, would still be necessary in a more resource productive economy, the strain on supply chains and environmental resources would be reduced.

McKinsey & Company 3|

Key messages (2/2)

Addressing climate change and ensuring universal energy access would require further action – requiring an additional ~$400b of annual investment over the next 20 years.

Tackling this resource agenda must start with new institutional mindsets and mechanisms that can develop more coordinated approaches to the challenge of resources.

In addition, there are 3 critical priorities for policymakers1.Unleash the power of the market by strengthening market signals, including removing the $1.1 trillion of resources subsidies and supporting stability in long-term prices2.This must be supported by addressing (non-price) market failures, including property rights, agency issues, access to capital and innovation3.Create long-term resilience by building awareness of risks and appropriate safety nets, strengthening and deepening innovation systems, and addressing consumer mindsets

For the private sector, 9 resource-related trends will shape competitive dynamics across a range of sectors. Successful firmsmust place resource issues at the heart of their business strategy, including mitigating resource risk in operations through building knowledge of relevant risks and capturing available efficiency opportunities, and aggressively going after new growth opportunities.

McKinsey & Company 4|

Contents

▪ Overview

▪ Key exhibits

McKinsey & Company 5|

Commodity prices have increased sharply since 2000, erasing all the declines of the 20th century

40

60

80

100

120

140

160

180

200

220

240

260

1970 201122000199019801960195019401930192019101900

World War I

Post-warDepression

Great Depression

World War II

1970’soil shock

McKinsey Commodity Price Index (years 1999–2001 = 100)1

1 Based on arithmetic average of 4 commodity sub-indices of food, non-food agricultural items, metals and energy. 2 2011 prices based on average of first eight months of 2011.

SOURCE: Grilli and Yang; Pfaffenzeller; World Bank; International Monetary Fund; Organisation for Economic Co-operation and Development statistics; UN Food and Agriculture Organization; UN Comtrade

McKinsey & Company 6|

Resource price volatility is at an all-time high, with the exception of energy in the 1970s Annual price volatility1

%

32

6

21

93

13171110

25

7

28

102120

89151514

87

26

131110917

11202424

15

201189 99796959493929191909

Energy

Food

Metals

Agricultural materials

39

14

38

56

471513

212220

SOURCE: Grilli and Yang; Pfaffenzeller; World Bank; International Monetary Fund; Organisation for Economic Co-operation and Development statistics; UN Food and Agriculture Organization; UN Comtrade

1 Calculated as the standard deviation of the commodity subindex divided by the average of the subindex over the time frame.

McKinsey & Company 7|

The emergence of 3 billion middle-class consumers will fuel future demand

Global middle class1

Billions of people

Middle East and North Africa

Sub-Saharan Africa

2030

3.23Central and South America

4.88

3 billion

Asia-Pacific

North America

Europe

0.68

0.32

0.310.23

0.11

2020

3.25

1.74

0.70

0.33

0.250.170.06

2009

1.85

0.53

0.66

0.340.18

0.11 0.03

1 Based on daily consumption per capita ranging from $10 to $100 (in purchasing power parity terms)SOURCE: OECD

McKinsey & Company 8|

0

50

100

150

200

250

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 45,000

Per capita GDPReal 2005 $PPP per person

Per capita energy consumption, 1970–2008, projected to 2030 for India and ChinaMillion British thermal units per person

Many countries have shown that as incomes rise, demand for resource increases—and a similar curve is likely in China and India

SOURCE: IEA; Global Insight; McKinsey analysis

ENERGY EXAMPLE

2030 projected

2030 projected

India

China

South Korea Japan

Germany

France

United Kingdom

United States

Australia

Historical range for energy consumption evolution

Historic (1970-2008)

Projected

McKinsey & Company 9|SOURCE: McKinsey analysis

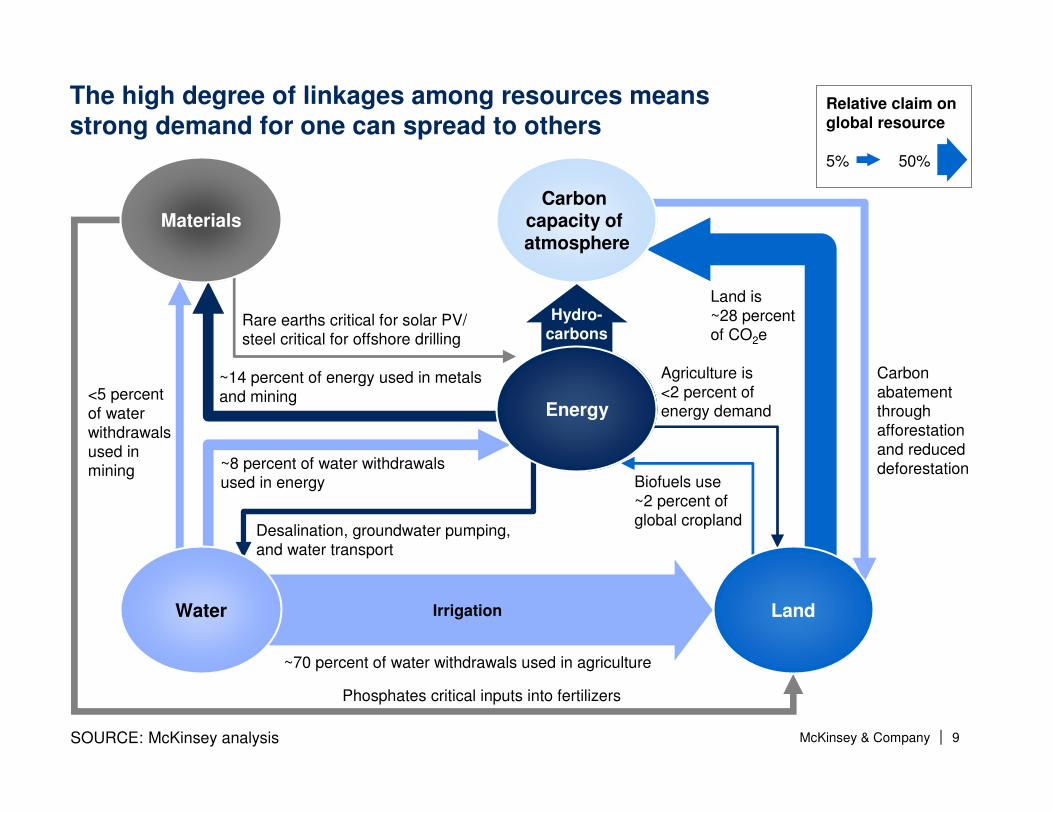

The high degree of linkages among resources means strong demand for one can spread to others

Irrigation

Desalination, groundwater pumping, and water transport

Biofuels use ~2 percent of global cropland

Land is ~28 percent of CO2e

Carbon abatement throughafforestation and reduced deforestation

~70 percent of water withdrawals used in agriculture

~8 percent of water withdrawals used in energy

~14 percent of energy used in metals and mining

Rare earths critical for solar PV/ steel critical for offshore drilling

Agriculture is<2 percent of energy demand

<5 percent of water withdrawals used in mining

Hydro-carbons

Relative claim on global resource

5% 50%

Phosphates critical inputs into fertilizers

Energy

Water

Carbon capacity of atmosphere

Land

Materials

McKinsey & Company 10|

IMF estimates that a 10 percent increase in the price of crude reduces global GDP by 0.2%-0.3% in one year

World Bank estimates that recent food price increases drove 44 million people into poverty

At least 8 countries commit 5 percent or more of their GDP to energy subsidies. In 2005, government subsidies were estimated to account for 14 percent of India’s GDP

These resource trends pose several risks to global growth and welfare

Just four countries—Iran, Iraq, Saudi Arabia, and Venezuela—hold almost 50 percent of known oil reserves

A recent study by the Economics of Climate Adaptation Working Group suggests that some regions are at risk of losing up to 12 percent of their annual GDP by 2030 as a result of existing climate patterns

McKinsey & Company 11|

In our productivity response case, there are opportunities that could meet 13 to 29 percent of resources demand

1 Productivity improvements include supply-side measures, such as enhanced oil recovery that lower effective remaining demand.

2 Supply-side levers such as improving recovery rates and the conversion rate in mining and coke do not save steel and are not reflected in this exhibit. We have included effective steel savings from higher scrap recycling.

SOURCE: McKinsey analysis

512655

143492

1,9952,290

2951,270

6,3505,000–5,2001,150–1,3504,500

1,210–1,320

Remaining 2030 demand

Productivity improvements

435–500

2030 base-casedemand

1,710–1,755

2010 demand

1,535

-22%

-13%

-18 to -21%

-25 to -29%

WaterCubic kilometers

LandMillion cropland hectares

Primary energy1

QBTU

Steel2

Million tonnessteel equivalent

“PRODUCTIVITY RESPONSE” CASE

McKinsey & Company 12|

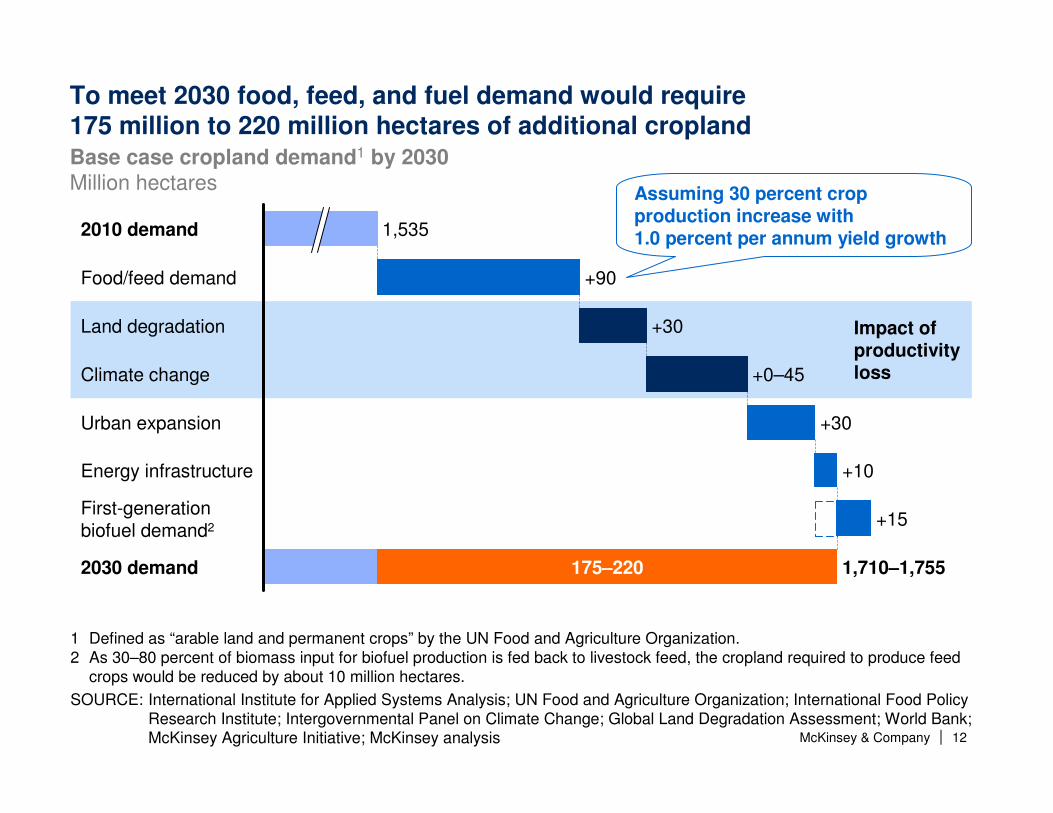

To meet 2030 food, feed, and fuel demand would require 175 million to 220 million hectares of additional croplandBase case cropland demand1 by 2030Million hectares

2030 demand 1,710–1,755175–220

First-generationbiofuel demand2 +15

Energy infrastructure +10

Urban expansion +30

Climate change +0–45

Land degradation +30

Food/feed demand +90

2010 demand 1,535

Impact of productivity loss

1 Defined as “arable land and permanent crops” by the UN Food and Agriculture Organization. 2 As 30–80 percent of biomass input for biofuel production is fed back to livestock feed, the cropland required to produce feed

crops would be reduced by about 10 million hectares.

SOURCE: International Institute for Applied Systems Analysis; UN Food and Agriculture Organization; International Food Policy Research Institute; Intergovernmental Panel on Climate Change; Global Land Degradation Assessment; World Bank; McKinsey Agriculture Initiative; McKinsey analysis

Assuming 30 percent crop production increase with 1.0 percent per annum yield growth

McKinsey & Company 13|

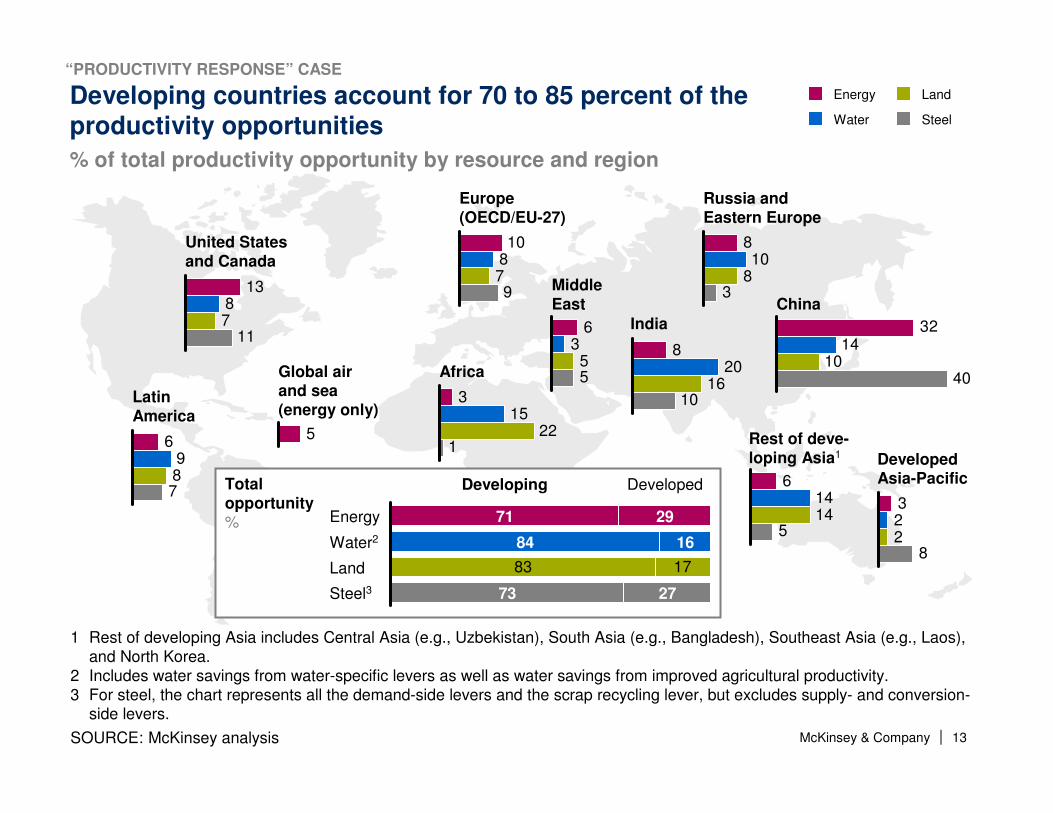

Developing countries account for 70 to 85 percent of the productivity opportunities

% of total productivity opportunity by resource and region

1387

11

Energy

SteelWater

Land

820

1610

3214

1040

315

221

SOURCE: McKinsey analysis

1 Rest of developing Asia includes Central Asia (e.g., Uzbekistan), South Asia (e.g., Bangladesh), Southeast Asia (e.g., Laos), and North Korea.

2 Includes water savings from water-specific levers as well as water savings from improved agricultural productivity.3 For steel, the chart represents all the demand-side levers and the scrap recycling lever, but excludes supply- and conversion-

side levers.

322

8

61414

5

63

55

10879

810

83

6987

5

United States and Canada

India

China

Africa

Developed Asia-Pacific

Rest of deve-loping Asia1

Middle East

Europe (OECD/EU-27)

Russia and Eastern Europe

Latin America

Global air and sea (energy only)

83 17

73

DevelopedDeveloping

27

Land

Water2

Energy 71

84

29

16

Steel3

Total opportunity%

“PRODUCTIVITY RESPONSE” CASE

McKinsey & Company 14|

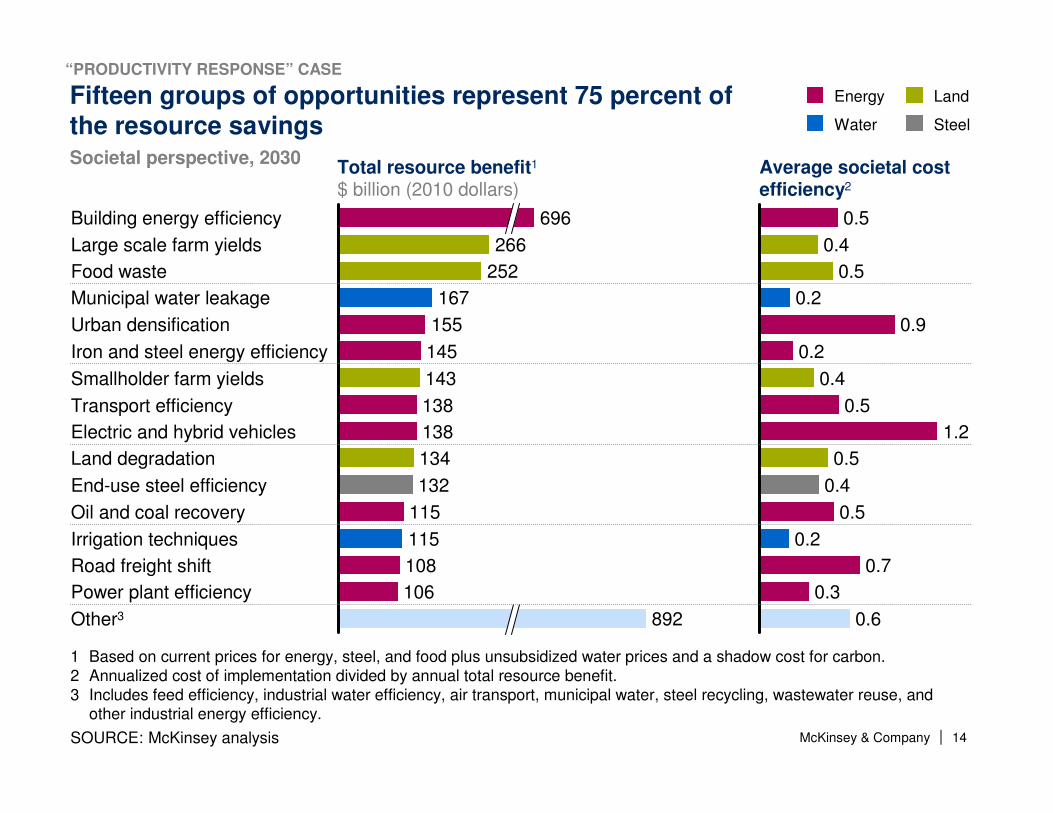

Fifteen groups of opportunities represent 75 percent ofthe resource savings

Electric and hybrid vehicles 138

134Land degradation

143Smallholder farm yields

138Transport efficiency

155Urban densification

145Iron and steel energy efficiency

252Food waste

167Municipal water leakage

696Building energy efficiency

266Large scale farm yields

Other3 892

Power plant efficiency 106

Road freight shift 108

Irrigation techniques 115

Oil and coal recovery 115

End-use steel efficiency 132

Total resource benefit1

$ billion (2010 dollars)Average societal cost efficiency2

0.6

0.3

0.7

0.2

0.5

0.4

0.5

1.2

0.5

0.4

0.2

0.9

0.2

0.5

0.4

0.5

Energy

Water

Land

Steel

1 Based on current prices for energy, steel, and food plus unsubsidized water prices and a shadow cost for carbon.2 Annualized cost of implementation divided by annual total resource benefit.3 Includes feed efficiency, industrial water efficiency, air transport, municipal water, steel recycling, wastewater reuse, and

other industrial energy efficiency.

SOURCE: McKinsey analysis

Societal perspective, 2030

“PRODUCTIVITY RESPONSE” CASE

McKinsey & Company 15|

Annual resource benefit$ billion, 2030

We have developed an integrated resource cost curve to compare productivity levers across resources

1.0

Lever width quantifies annual resource savings calculated as the resource volume saved (e.g., barrels of oil) times today’s price (e.g., $100/barrel of oil)

Lever height quantifies the cost efficiency of investment (i.e., the cost of implementation divided by the resource benefit)

Productivity opportunities with returns higher than the assumed hurdle rate

Productivity opportunities with returns lower than the assumed hurdle rate

Cost efficiency$ cost of implementation per $ resource benefit

SOURCE: McKinsey analysis

“PRODUCTIVITY RESPONSE” CASE

McKinsey & Company 16|

5

3

1

-1

-3

4,0003,5003,0002,5002,0001,5001,0005000

7

7

5

3

1

-1

-3

4,0003,5003,0002,5002,0001,5001,0000 500

Resource productivity opportunities could create societal benefits of up to $3.7 trillion, with 90 percent of opportunities above the hurdle rate

Steel

Land

Water

Energy

1 Based on current prices for energy, steel, and food, less energy taxes, plus subsidies, and a shadow cost for carbon (at $30 per tonne of carbon dioxide equivalent).

SOURCE: McKinsey analysis

2030

Societal perspective▪Societal prices1

▪Discount rate 4%

+800 billion

Cost efficiency of investment

Total annual resource benefit, $ billion

70% of productivity opportunities above

hurdle rate

90% of productivity opportunities above

hurdle rate

Investor perspective▪Current

prices▪Discount

rate 10%

“PRODUCTIVITY RESPONSE” CASE

McKinsey & Company 17|

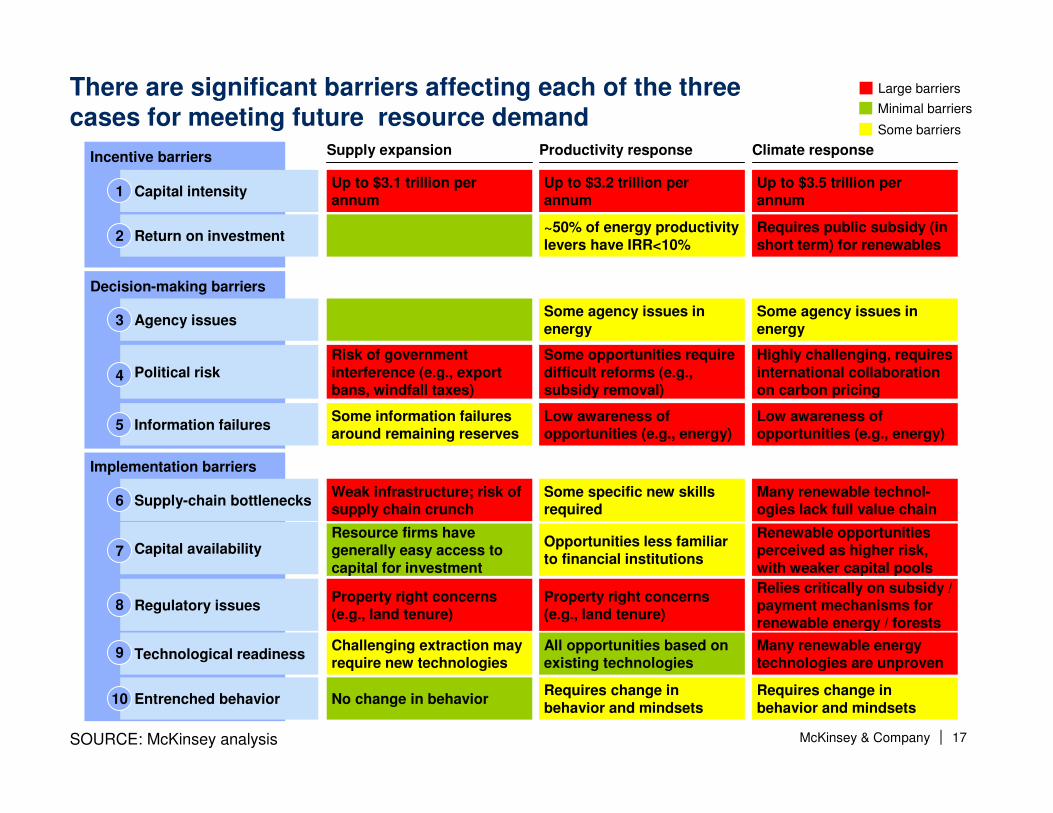

There are significant barriers affecting each of the three cases for meeting future resource demand

SOURCE: McKinsey analysis

Minimal barriers

Some barriers

Large barriers

Incentive barriersIncentive barriers

Decision-making barriers

Supply expansion

Up to $3.1 trillion per annum

Capital intensity1

Agency issues3

Risk of government interference (e.g., export bans, windfall taxes)

Political risk4

Some information failures around remaining reserves

Information failures5

Return on investment2

Productivity response

Up to $3.2 trillion per annum

Some agency issues in energy

Some opportunities require difficult reforms (e.g., subsidy removal)

Low awareness of opportunities (e.g., energy)

~50% of energy productivity levers have IRR<10%

Climate response

Up to $3.5 trillion per annum

Some agency issues in energy

Highly challenging, requires international collaboration on carbon pricing

Low awareness of opportunities (e.g., energy)

Requires public subsidy (in short term) for renewables

Weak infrastructure; risk of supply chain crunch

Resource firms have generally easy access to capital for investment

Property right concerns (e.g., land tenure)

Challenging extraction may require new technologies

Some specific new skills required

Opportunities less familiar to financial institutions

Property right concerns (e.g., land tenure)

All opportunities based on existing technologies

Requires change in behavior and mindsets

Many renewable technol-ogies lack full value chain

Renewable opportunities perceived as higher risk, with weaker capital pools

Relies critically on subsidy / payment mechanisms for renewable energy / forests

Many renewable energy technologies are unproven

Requires change in behavior and mindsets

No change in behavior

Implementation barriers

Supply-chain bottlenecks6

Capital availability7

Regulatory issues8

Technological readiness9

Entrenched behavior10

McKinsey & Company 18|

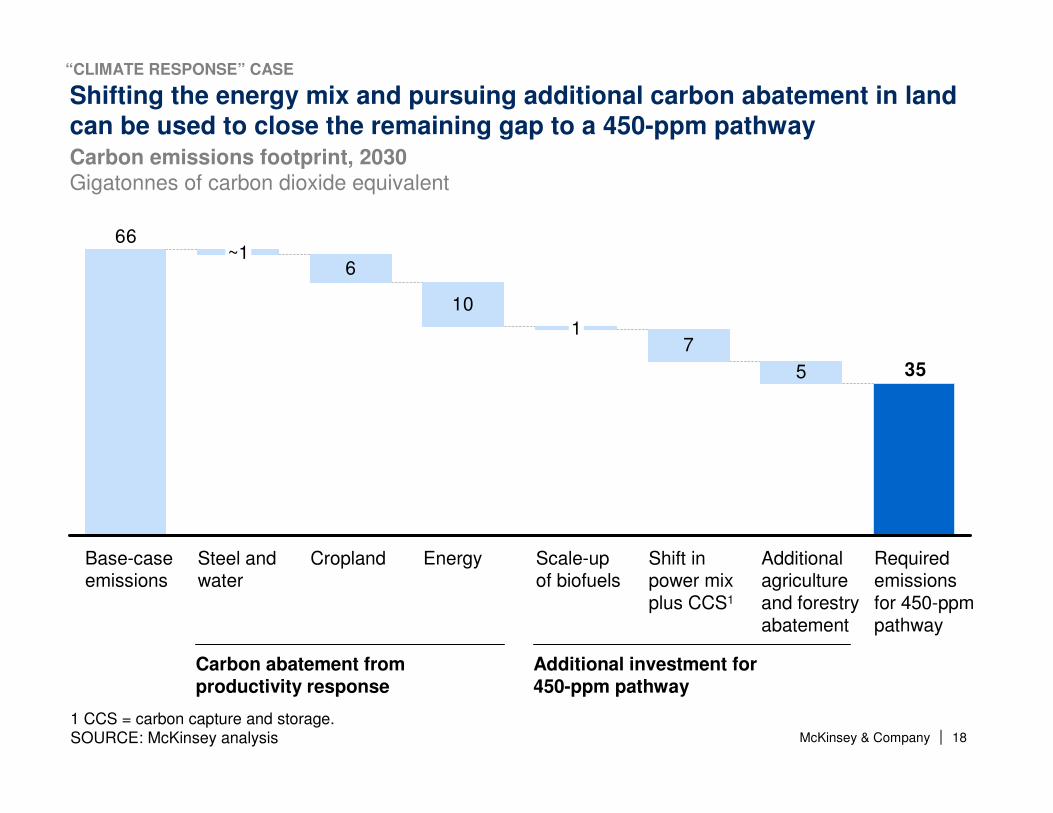

Additional investment for 450-ppm pathway

1 CCS = carbon capture and storage.SOURCE: McKinsey analysis

Shifting the energy mix and pursuing additional carbon abatement in land can be used to close the remaining gap to a 450-ppm pathway

6

10

7

5

66

35

Required emissions for 450-ppmpathway

Additional agriculture and forestry abatement

Shift in power mix plus CCS1

Scale-up of biofuels

1

Energy

~1

CroplandSteel and water

Base-case emissions

Carbon abatement from productivity response

Carbon emissions footprint, 2030Gigatonnes of carbon dioxide equivalent

“CLIMATE RESPONSE” CASE

McKinsey & Company 19|

Climateresponse

1,990–

2,140

Productivityresponse

1,690–

1,730

Supplyexpansion

1,400–

1,440

1,000

Capital investment could increase significantly under all three cases

SOURCE: McKinsey analysis

Average annual capital expenditure requirement, 2010–301

$ billion (2010 dollars)

1 Does not include capital expenditure for base-case productivity improvements; includes impact of capital price spikes due to supply constraints.

2030 cases

2010 capital expenditure

Energy SteelWater Land

445–

475

445–

475

500–

550

350

425–

515

425–

515

555–

675

270

375–

445

365–

435

345–

405

310

2,800–3,070

2,925–3,155

1,930

3,235–3,575

Total

ADDRESS NON-PRICE MARKET FAILURES

McKinsey & Company 20|

Power mix shifts significantly in a climate response case

Share of global power production%; terawatt hours

Climate response

Supply expansion/ productivity response1

1 Same power mix assumed in both the supply expansion and productivity response cases. End demand varies between the two cases—the first number shown on the 100% line refers to supply expansion; the second number to productivity response.

2 RE = Renewables. Other RE include dedicated biomass, geothermal, and marine.

SOURCE: McKinsey analysis

2

3

2030 4332,582/26,617

210

11

12 4150

1

2

14 5 1 3

202027,519/24,593

42 21

3

9

2

72030

2020 24,59312 16 925 27

26,61713

06

6 17151121 1

Coal

CCS

Nuclear HydroWind

Solar Other RE2

Gas Oil

Current state 5 171322

022 02010 40 21,022

100% =

“CLIMATE RESPONSE” CASE

McKinsey & Company 21|

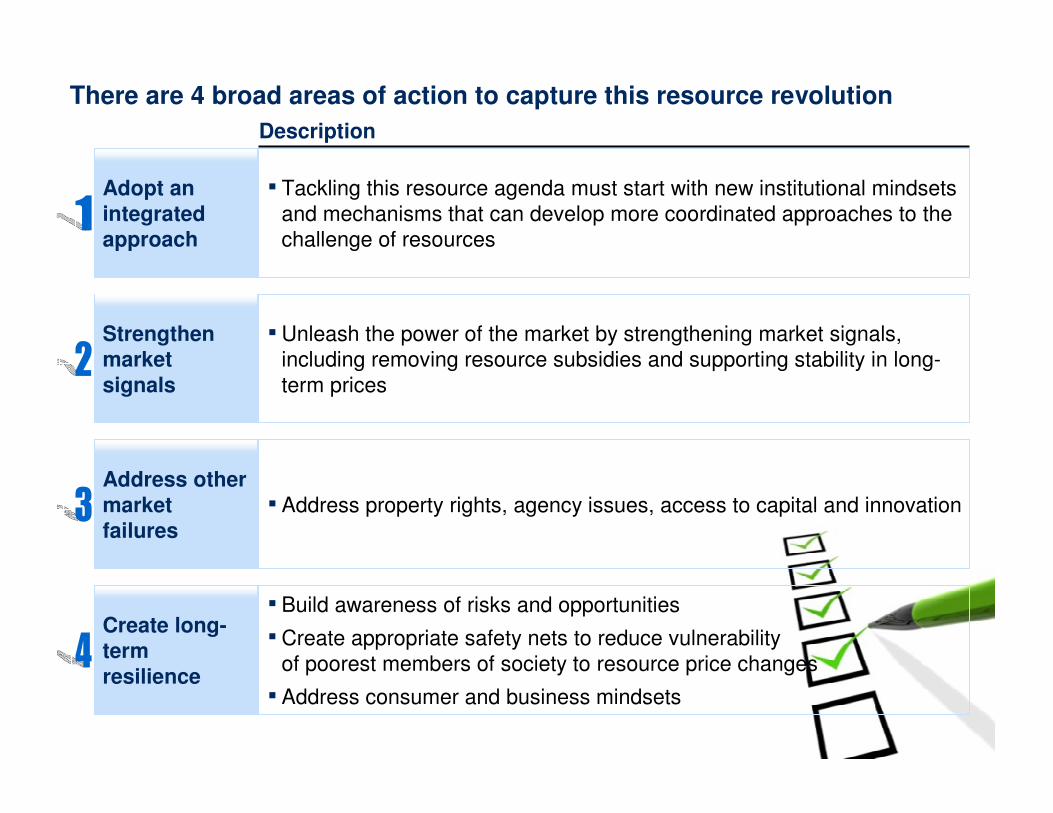

Create long-term resilience

▪ Build awareness of risks and opportunities

▪Create appropriate safety nets to reduce vulnerability of poorest members of society to resource price changes

▪ Address consumer and business mindsets

There are 4 broad areas of action to capture this resource revolution

Description

Adopt an integrated approach

▪ Tackling this resource agenda must start with new institutional mindsets and mechanisms that can develop more coordinated approaches to the challenge of resources

Strengthen market signals

▪Unleash the power of the market by strengthening market signals,including removing resource subsidies and supporting stability in long-term prices

Address other market failures

▪ Address property rights, agency issues, access to capital and innovation

McKinsey & Company 22|

Disruptive trends in three broad categories could shape private-sector competitive dynamics and value creation

Disruptive force

Industry

Illustrative facts

1 CPG = consumer packaged goods.SOURCE: McKinsey analysis

High

Medium

Low

Impact on sector

CPG1 MiningOil and gas

Resource cost-related forces

Regulation-related forces

Resource-related techno-logical forces

Rising volatility and correlation

Rising environmental costs

Rising geopolitical concerns

Public policy push to realize true cost of resources

The new social contract for access to resources

Supply-chain efficiency opportunities

Impact of technology on competitive advantage

More expensive resource input costs

The average cost per oil well doubled from 2000 to 2010

Potential impact on yields of greater than 10 percent in next 20 years

Annual volatility across resources is at its highest level of the past 100 years

>80 percent of available arable land is in countries with infrastructure or political issues

Current subsidies for agriculture, energy, and water total up to $1.1 trillion per year

Maintaining social license to operate is a top-four issue for metals/mining executives

CPG players can reduce energy consumption by 20 to 50 percent on average

Learning curves for renewable power sources range from 10 to 20 percent

Demand for resource-efficient products

Half of shoppers consider green attributes in their purchasing decisions