Embed Size (px)

Citation preview

“Research and Implementation: Lessons

from the Original Demonstration”

February 11, 2004

Teleconference

Agenda

Overview of Cash & Counseling Program

Presentation of Evaluation Results University of Maryland Baltimore County Qualitative Study Mathematica Results Question and Answer session

Review of Implementation Lessons Question and answer session

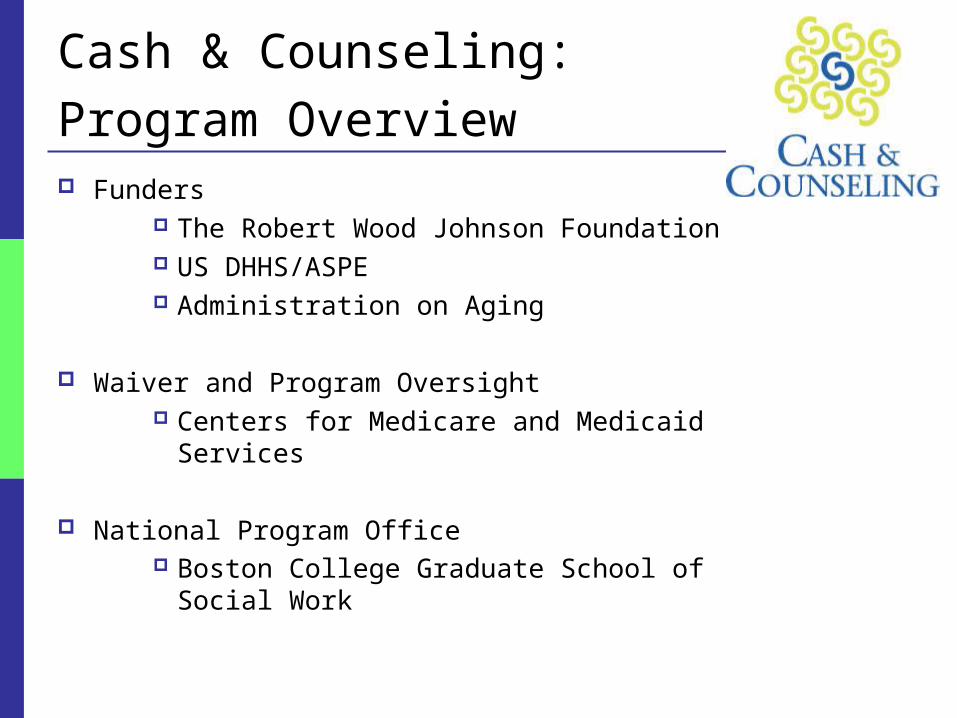

Cash & Counseling: Program Overview Funders

The Robert Wood Johnson Foundation US DHHS/ASPE Administration on Aging

Waiver and Program Oversight Centers for Medicare and Medicaid Services

National Program Office Boston College Graduate School of Social Work

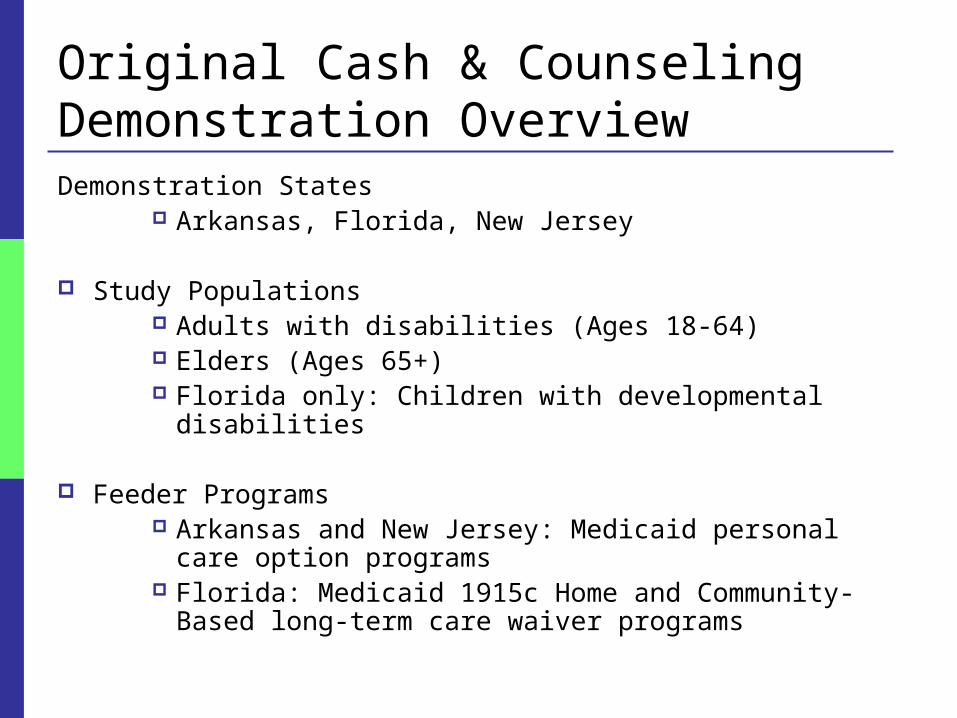

Original Cash & Counseling Demonstration OverviewDemonstration States

Arkansas, Florida, New Jersey

Study Populations Adults with disabilities (Ages 18-64) Elders (Ages 65+) Florida only: Children with developmental disabilities

Feeder Programs Arkansas and New Jersey: Medicaid personal care option programs Florida: Medicaid 1915c Home and Community-Based long-term

care waiver programs

Essential Elements of Cash & Counseling

Person-centered planning for personal assistance services

Consumer-directed individualized budgets

Client supports including financial management and counseling services (supports brokerage)

Quality assurance and improvement systems

Basic Model for Cash & Counseling

Step 1: Consumers receive traditional assessment and care plan

Step 2: A dollar value is assigned to that care plan

Step 3: Consumers receive enough information to make unbiased personal choice between managing individualized budget or receiving traditional agency-delivered services

Basic Model for Cash & Counseling

Step 4: Cash allowance group provided with financial management and counseling services (supports brokerage)

Step 5: Consumer and counselor develop cash plan to meet consumer’s personal assistance needs

Basic Model for Cash & Counseling

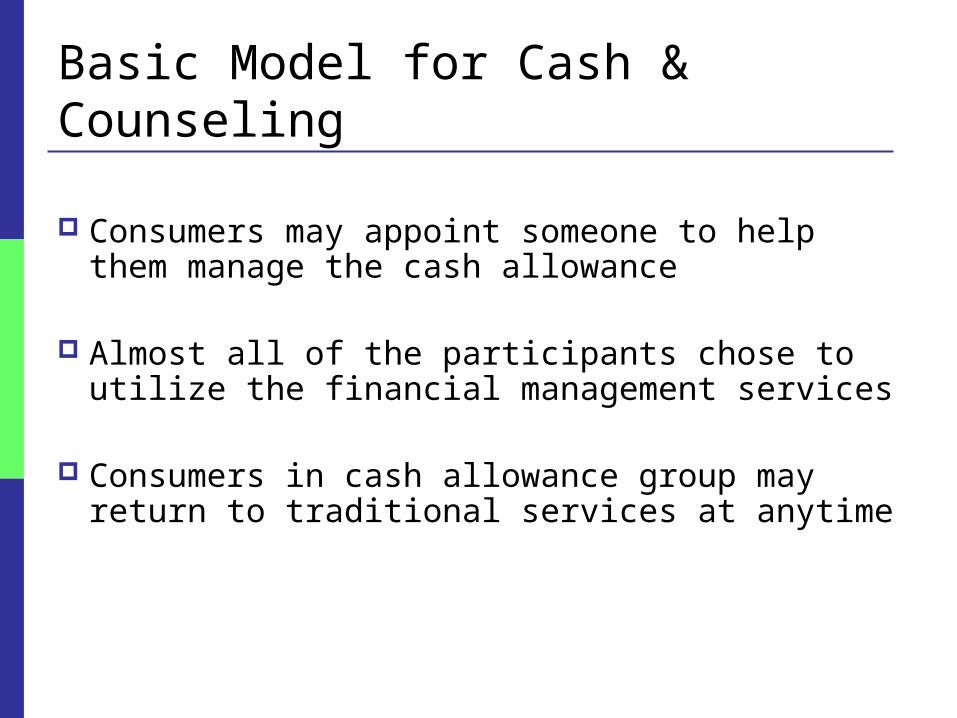

Consumers may appoint someone to help them manage the cash allowance

Almost all of the participants chose to utilize the financial management services

Consumers in cash allowance group may return to traditional services at anytime

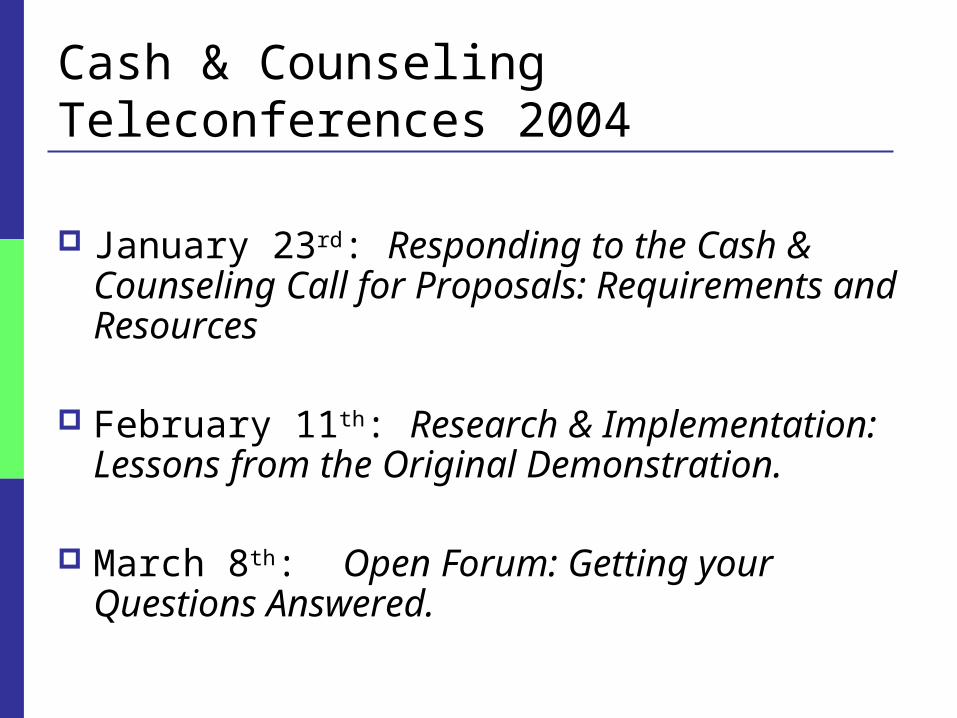

Cash & Counseling Teleconferences 2004

January 23rd: Responding to the Cash & Counseling Call for Proposals: Requirements and Resources

February 11th: Research & Implementation: Lessons from the Original Demonstration.

March 8th: Open Forum: Getting your Questions Answered.

Responding to the Cash & Counseling Call for Proposals

Intent to Apply Deadline: February 13, 2004, 3pm EST

available at www.cashandcounseling.org

Full Proposal Deadline: March 31, 2004submit to [email protected]

Research and Implementation:

Lessons from the Original Cash & Counseling

Demonstration

Cash & Counseling Qualitative Study

Purpose of Qualitative Study Provide detailed information and stories about the

experience of Cash & Counseling consumers in each state

Four questions were addressed:Has the program made a difference in participants’

lives?How does participation in the program compare to

previous arrangements?How are services provided?How does the program work?

Methodology Focused on care units: Consumer/family member(s),

primary paid worker, and counselor

Samples included consumers of different ages, races, sexes, monthly cash benefits amounts, and types of workers (i.e. family vs. non-family)

Interviewers conducted hour long, face-to-face, tape-recorded interviews in the consumer’s home

Emerging Themes Stories were created from transcripts and

incorporated the perspective of all care unit members

Many themes were identified including: Choice is important to consumers Consumers valued the flexibility of the program Consumers found creative ways to use their monthly

allowance to meet their needs Consumers experienced improved quality of life and

satisfaction with their care

In Their Own Words: Consumers

*Mrs. Margaret Taylor, 64 years old, describing her non-family personal care worker

“She’s a beautiful person. She’s helpful and she’s just like an older daughter and she cooks and cleans and

does the laundry and puts things away…She just takes care. I don’t have to worry about her and

whatever I ask her and whatever I need, I ask her to do, and she does it and things I don’t even ask her to

do, she does.”*Names are changed to protect consumer confidentiality

In Their Own Words: Consumers

*Mr. Gilberto Santiago, 26 years old, describing how his life has changed since his father became his

primary paid caregiver

“You can trust him [father] more. You know that you will be taken care of better…As a young person, you

like to look good…your dad knows about that, he knows how your jeans fit…He [father] puts your hat on the way you want…[health aides] don’t take care

of you the same way your father does.”

*Names have been changed to protect consumer confidentiality

For More Information

Arkansas report is final and available on the web site; New Jersey report is in process of final revisions; Florida final report will be available in Fall 2004

Completed reports available at www.cashandcounseling.org

Effects on Consumers’ Service Use and

Well-Being: Findings from Arkansas

Leslie FosterStacy Dale

Randall BrownBarbara PhillipsJennifer Schore

Barbara Lepidus Carlson

Research and Implementation: Lessons from the Cash & Counseling Demonstration

Teleconference; February 11, 2004

Intended Effects of IndependentChoices

Medicaid beneficiaries with disabilities direct their own personal care services

Change amounts, timing, and types of services

Satisfaction and well-being improve- Without detriment to health and safety

Methods

Randomly assigned applicants after baseline

Interviewed treatment and control group members 9 months later

Compared regression-adjusted outcomes for the two groups

Arkansas Survey Sample Ages 18-64 Age 65+ Sample Size

Treatment group 243 642 Control group

230

624

Total

473

1,266

Source: Survey conducted 9 months after enrollment.

Ages 18-64 Age 65+ Sample Size

Treatment group 243 642 Control group

230

624

Total

473

1,266

Source: Survey conducted 9 months after enrollment.

Ages 18-64 Age 65+ Treatment group

243

642

Control group

230

624

Total

473

1,266

Source: Survey conducted 9 months after enrollment.

Received Paid Assistance in Past Two Weeks

80

95

68

95

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

Ages 18-64Ages 18-64 Age 65+Age 65+

*** ***TT

CC

TT

CC

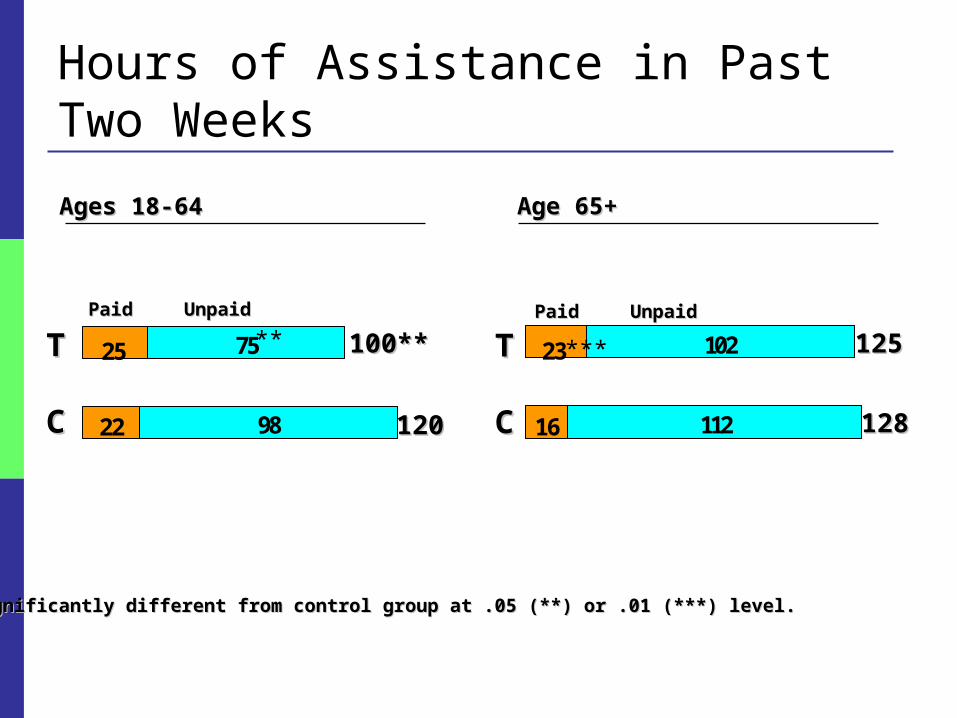

Hours of Assistance in Past Two Weeks

16 112

23 102

22 98

25 75

****,,***Significantly different from control group at .05 (**) or .01 (***) level.***Significantly different from control group at .05 (**) or .01 (***) level.

Ages 18-64Ages 18-64 Age 65+Age 65+

***TT

CC

TT

CC

** 100**100**

120120

125125

128128

PaidPaid UnpaidUnpaid PaidPaid UnpaidUnpaid

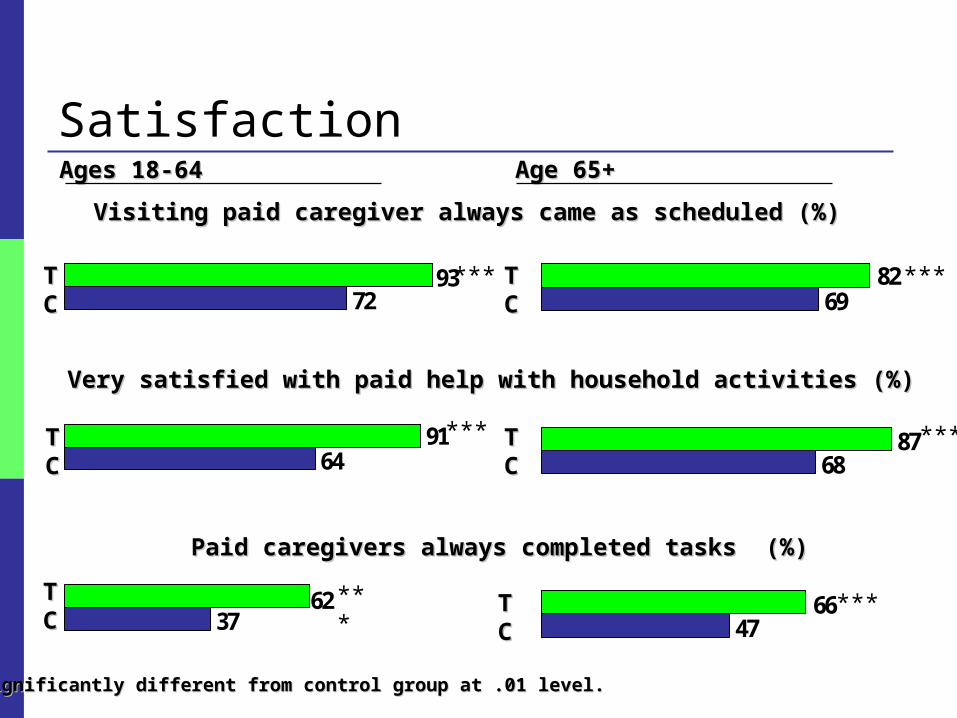

Satisfaction

37

64

72

62

91

93

47

68

69

87

66

82

Visiting paid caregiver always came as scheduled (%)Visiting paid caregiver always came as scheduled (%)

Very satisfied with paid help with household activities (%)Very satisfied with paid help with household activities (%)

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

Ages 18-64Ages 18-64 Age 65+Age 65+

***

***

***

***

TTCC

TTCC

TTCC

TTCC

*** ***

Paid caregivers always completed tasks (%)Paid caregivers always completed tasks (%)

TTCC

TTCC

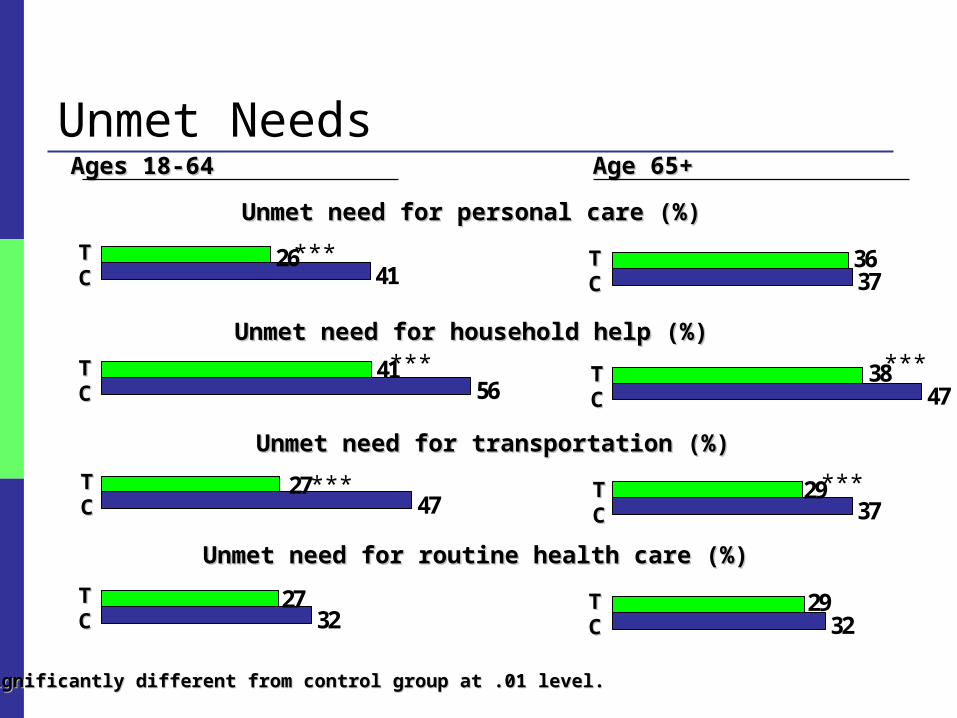

Unmet Needs

32

47

41

56

26

27

27

41

32

37

47

37

29

36

29

38

Unmet need for personal care (%)Unmet need for personal care (%)

Unmet need for household help (%)Unmet need for household help (%)

Unmet need for transportation (%)Unmet need for transportation (%)

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

Ages 18-64Ages 18-64 Age 65+Age 65+

***

***

***

***

TTCC

TTCC

TTCC

TTCC

TTCC

TTCC

Unmet need for routine health care (%)Unmet need for routine health care (%)

***TTCC

TTCC

Adverse Events and Health Problems

4.0

13

29

6

1.3

28

1.91.4

7

19

8

19

Fell (%)Fell (%)

Saw doctor for a cut, burn, or scald (%)Saw doctor for a cut, burn, or scald (%)

**,,**Significantly different from control group at .10 (*) or .05 (**) level.**Significantly different from control group at .10 (*) or .05 (**) level.

Ages 18-64Ages 18-64 Age 65+Age 65+

*

TTCC

TTCC

TTCC

TTCC

**

Bed sores developed or worsened (%)Bed sores developed or worsened (%)

TTCC

TTCC

Satisfaction with Overall Care and Life

23

42

43

71

37

54

56

68

Very satisfied with overall care arrangements (%)Very satisfied with overall care arrangements (%)

****,,***Significantly different from control group at .05 (**) or .01 (***) level.***Significantly different from control group at .05 (**) or .01 (***) level.

Ages 18-64Ages 18-64 Age 65+Age 65+

***TT

CC

***

***

***

Very satisfied with way spending life (%)Very satisfied with way spending life (%)

TT

CC

TT

CC

TT

CC

The Experiences of Informal Caregivers and Hired Workers Under IndependentChoices

Stacy Dale

Leslie Foster

Randy Brown

Barbara Phillips

Barbara Carlson

Research and Implementation: Lessons from the Cash & Counseling Demonstration

Teleconference

February 11, 2004

Why Study Caregivers and Workers?

Informal caregivers Provide more in-home personal care than paid sources

Help Medicaid beneficiaries avoid nursing homes

Hired Workers

Must have positive experiences for consumer-direction to be sustainable

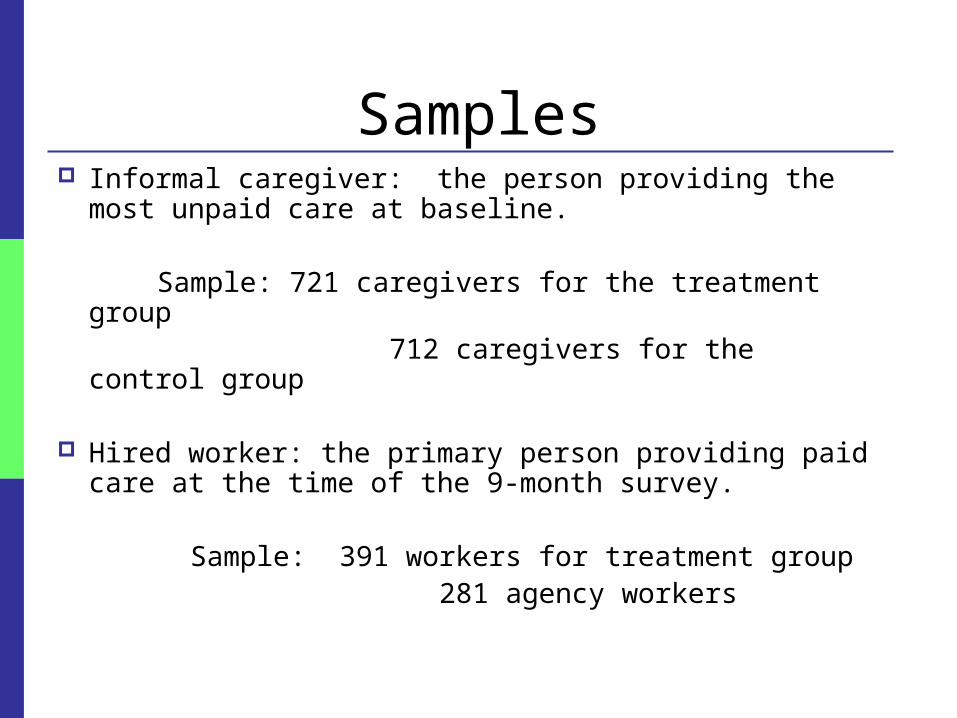

Samples Informal caregiver: the person providing the most unpaid

care at baseline. Sample: 721 caregivers for the treatment group 712 caregivers for the control group

Hired worker: the primary person providing paid care at the time of the 9-month survey.

Sample: 391 workers for treatment group 281 agency workers

Outcome MeasuresCompared survey responses (10 months post-baseline) of

treatment group caregivers to control group caregivers for these measures:

Amount of assistance

Satisfaction with care arrangements

Emotional, financial, physical well-being

Satisfaction with life

Informal Caregiver Characteristics

86% Female

93% Related to consumer

62% Lived with consumer

56% of treatment group caregivers became paid worker

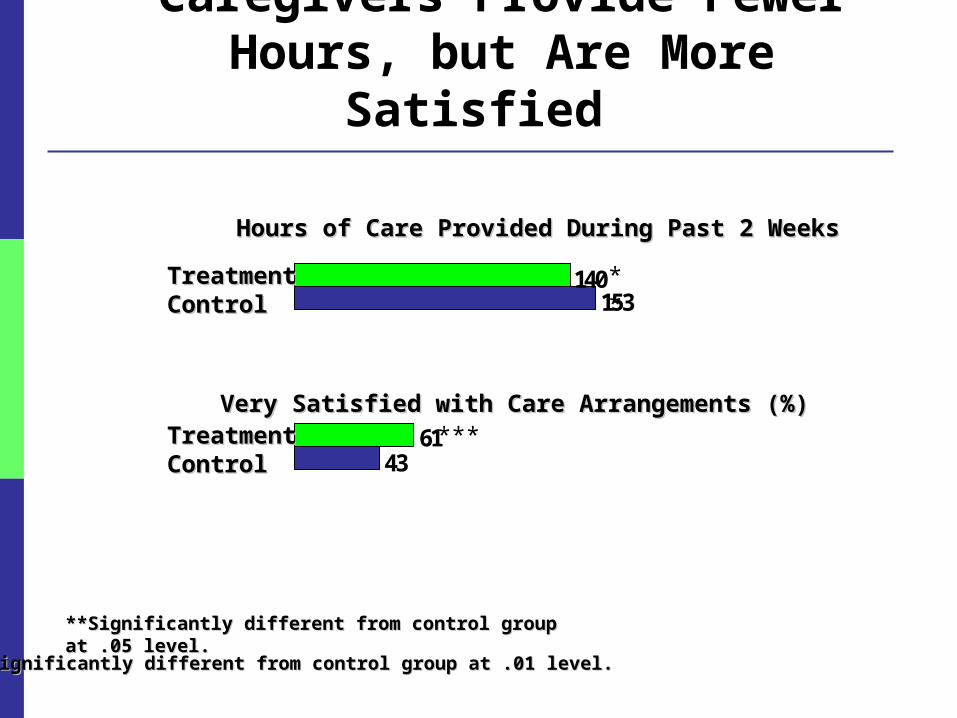

Caregivers Provide Fewer Hours, but Are More Satisfied

**Significantly different from control group at .05 level.**Significantly different from control group at .05 level.

43

153140

61

Hours of Care Provided During Past 2 WeeksHours of Care Provided During Past 2 Weeks

Very Satisfied with Care Arrangements (%)Very Satisfied with Care Arrangements (%)

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

**

***

TreatmentTreatmentControlControl

TreatmentTreatmentControlControl

Caregiver Well-Being

32

34

36

23

27

22

Report caregiving causes great financial strain (%)Report caregiving causes great financial strain (%)

Report caregiving causes great emotional strain (%)Report caregiving causes great emotional strain (%)

Report caregiving causes great physical strain (%)Report caregiving causes great physical strain (%)

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

***

***TreatmentTreatmentControlControl

TreatmentTreatmentControlControl

TreatmentTreatmentControlControl

***

Caregiver Health and Life Satisfaction

**Significantly different from control group at .05 level.**Significantly different from control group at .05 level.

39

47

51

36

Current Health is Fair or Poor Relative to PeersCurrent Health is Fair or Poor Relative to Peers

Very Satisfied with Life (%)Very Satisfied with Life (%)

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

**

***

TreatmentTreatmentControlControl

TreatmentTreatmentControlControl

Policy Concerns for Hired WorkersWithout agency support

Will workers be under-compensated or mistreated?

Will workers receive adequate training?

Will workers feel emotionally and physically strained?

What pattern of care will workers provide?

Findings for Hired WorkersHired workers Were mostly relatives (78%) and friends (16%) Received pay similar to that of agency workers: $6

per hour for about 12 hours a week Provided an average of 26 hours of unpaid care per

week Helped with wide range of tasks

Most Concerns about Workers Didn’t Materialize Many lacked formal training, but:

Most felt well-prepared No greater physical problems for workers or consumers

Had low compensation and fringes, but: Most were very satisfied with pay and conditions

Felt more emotional strain and wanted more respect but: Difference confined to hired relatives

Program Costs in Arkansas and Policy Implications

Randall Brown

Stacy Dale

Leslie Foster

Barbara Phillips

Jennifer Schore

Research and Implementation:Lessons from the Cash & Counseling Demonstration

Teleconference February 11, 2004

Expected Effects on Costs

Program required to be “budget neutral” per month of service

Waiver service costs could increase

Other Medicaid/Medicare costs may be affected

Medicaid cost pressures limit states’ options

Methods and Data Compare actual to expected costs for personal care services

Compare treatment and control groups on service use and costs

Data: Individual care plans

Medicaid claims

Medicare claims

Two-year follow-up data for 1312 first-year enrollees

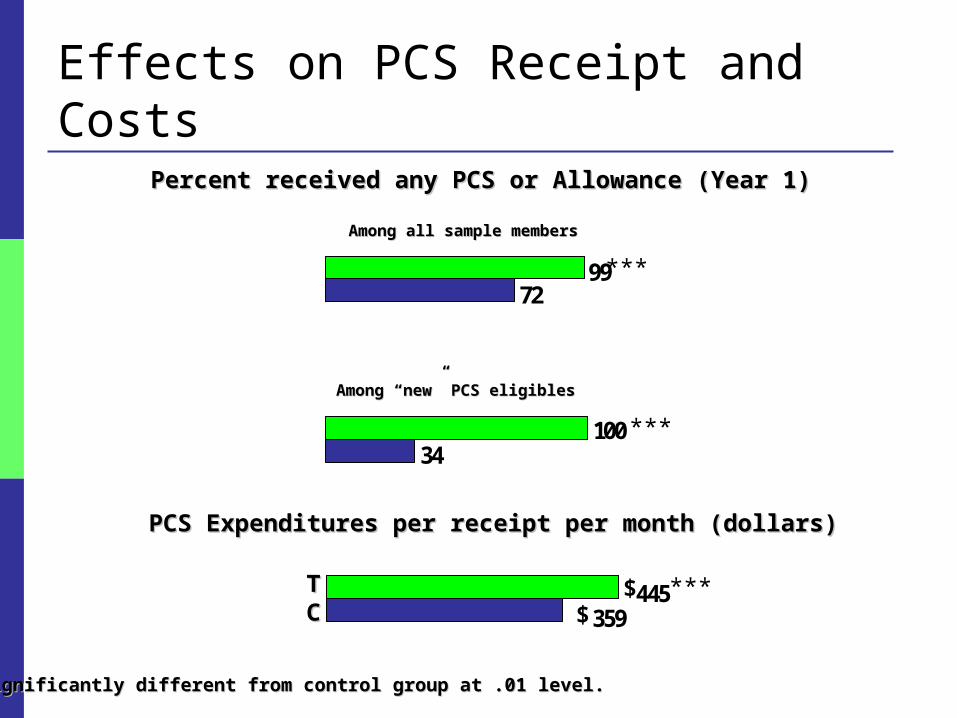

Effects on PCS Receipt and Costs

359445

PCS Expenditures per receipt per month (dollars)PCS Expenditures per receipt per month (dollars)

***Significantly different from control group at .01 level.***Significantly different from control group at .01 level.

***TTCC $

$

34

72

100

99

Percent received any PCS or Allowance (Year 1)Percent received any PCS or Allowance (Year 1)

***

***

Among all sample membersAmong all sample members

Among “new” PCS eligiblesAmong “new” PCS eligibles

Actual/Expected PCS in Month 12

0.70

0.82

1.07

0.99

(Mean actual cost) / (mean expected cost)(Mean actual cost) / (mean expected cost)

****,,***Significantly different from control group at .05 (**) or .01 (***) level.***Significantly different from control group at .05 (**) or .01 (***) level.

***TT

CC

***TT

CC

Note: Includes only those receiving an allowance for the treatment group, and only those receiving PC services for the control group.

(Hours received or cashed out) / (care plan hours)(Hours received or cashed out) / (care plan hours)

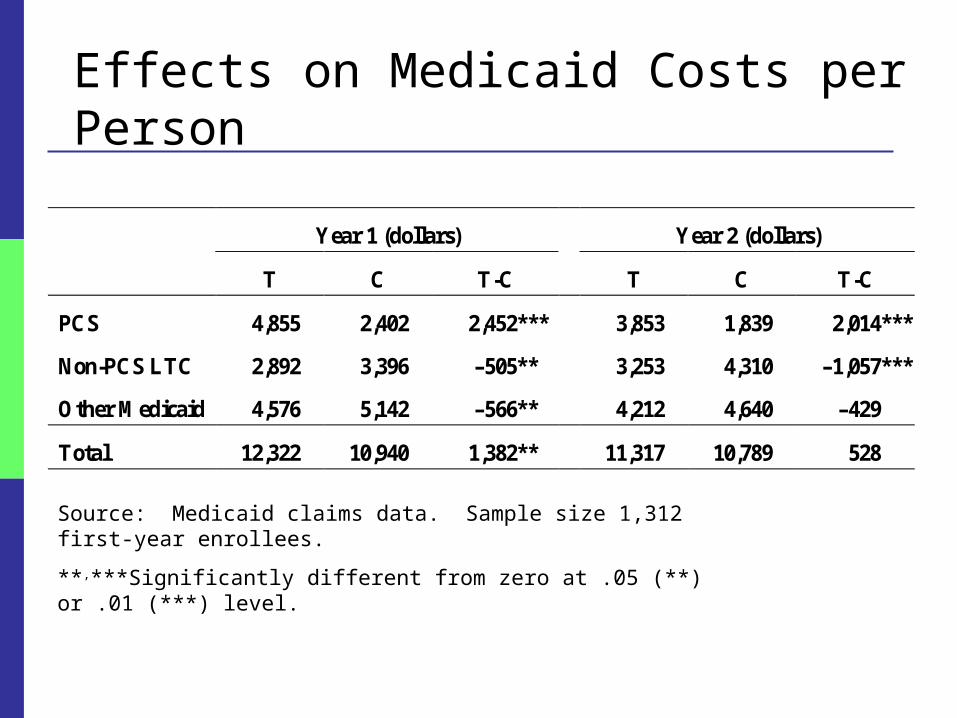

Effects on Medicaid Costs per Person

Year 1 (dollars) Year 2 (dollars)

T C T-C T C T-C

PCS 4,855 2,402 2,452*** 3,853 1,839 2,014***

Non-PCS LTC 2,892 3,396 –505** 3,253 4,310 –1,057***

Other Medicaid 4,576 5,142 –566** 4,212 4,640 –429

Total 12,322 10,940 1,382** 11,317 10,789 528

Source: Medicaid claims data. Sample size 1,312 first-year enrollees.

**,***Significantly different from zero at .05 (**) or .01 (***) level.

Sources of Reduction in Medicaid Costs

Year 1 (dollars) Year 2 (dollars)

T C T-C T C T-C

Nursing home 460 696 –235 1,149 1,749 –601**

Home health 336 479 –142 217 373 –156**

ElderChoices 1,752 1,961 –209** 1,384 1,586 –202

Alternatives 343 261 82 503 602 –99

All non-PCS LTC 2,892 3,396 –505 3,253 4,310 –1,057***

Source: Medicaid claims data. Sample size 1,312 first-year enrollees.

**,***Significantly different from zero at .05 (**) or .01 (***) level.

Policy Implications Program worked from consumer viewpoint - Interested elders can direct their services

- Caregivers benefit too

Costs and access are interrelated

Lower long-term care costs offset higher PCS costs

Agencies might be motivated to compete

Early Florida results suggest generalizability

LESSONS from the IMPLEMENTATION of

CASH and COUNSELING

ARKANSAS, FLORIDA,

and NEW JERSEY

Outreach and Enrollment

Role of traditional agencies

Their cooperation is needed

Assigning them responsibility for outreach and enrollment can create problems

Building caseload quickly may require hiring dedicated staff

Outreach and Enrollment Direct outreach

To eligible beneficiaries and perhaps to their families Letters from the governor Targeting eliminates inquiries from ineligibles

Community education Useful for outreach if can be targeted Can help to generate support among community

providers

Outreach and Enrollment

Home visits to interested beneficiaries Necessary to explain the allowance program Involving family and friends reduces the number of visits

needed Avoid presence of aides from traditional agencies

Materials Must be easy to understand Need a variety of media—written, oral, and video In languages of eligible populations

Outreach and Enrollment

Formal screening process for appropriateness? May not be legally defensible Inconsistent with the philosophy of consumer direction

Allowing all interested to enroll Proved workable But can be costly due to early dropout

Representatives

Representatives assist the consumer with the allowance Naming representatives

Most representatives are related to the consumer• Required for children; many adult consumers will name them

Shared decision making typical Almost all representatives served the consumer well Special monitoring when the representative is also a worker

Counseling and the Spending Plan

Counselor concerns about liability for consumer outcomes

Initial spending plan Development can be time-consuming Consumer need for help not indicative of inappropriateness Advance preparation can minimize counselor home visits to develop

the plan

Plans must be revised as consumer needs and plans change

Techniques available to reduce need for revision

Use of the Allowance and Workers Hiring workers

Nearly all consumers use their allowance to hire workers

Most workers are relatives or acquaintances of the consumer Access to care can be improved by tapping this “labor

supply”

Consumers without a relative or acquaintance to hire often have difficulty hiring a worker Methods to assist them include training and worker

registries

Use of the Allowance and Workers Terminating workers

Consumers usually handle worker termination gently Some will need the assistance of counselors

Consumers take advantage of the flexibility of the allowance Purchase the service that is needed rather than the covered service

Fiscal Services

Nearly all consumers want payroll and check writing services Provided these are offered at little direct expense to them

Procedures needed for minimizing overpayment and recouping if necessary Payments may be deposited for which consumers have become

ineligible Consumers may overspend the allowance due to administrative error

Fiscal Services

Fiscal agents typically strapped when case loads are small May need assistance with cash flow until reach “break-even”

caseload Break-even caseload may vary from 200 to 1,000 consumers,

depending on the structure of payment

Need clear delineation of counselor and fiscal agent duties

Fiscal Services

Consumer financial statements Consumers need financial statement to monitor their

accounts Statements should be timely and easy to understand Should clearly list the amount and payee

Preventing Exploitation of Consumer Consumer exploitation was extremely rare A few questionable cases identified by counselor at

initial home visit Referred to protective services or back to traditional

program Periodic visits and telephone calls prevent

exploitation as consumers’ situations change Information and impressions from calls can signal need for

discretionary visit Telephone calls most useful when both consumer and

representative are contacted

Preventing Abuse of the Allowance Abuse of the allowance almost non-existent Critical to preventing abuse of the allowance are:

1. Review of initial and revised spending plans to ensure only permissible goods and services are included

2. Review time sheets and check requests before payment to ensure consistency with the spending plan

Given these 2 reviews, reviews of receipts not critical for prevention of abuse of funds held by fiscal agent

Structure and Procedures Having traditional agencies provide counseling

can create problems Traditional systems that offer a choice of counselors can be

responsive to consumer demand Support among traditional staff can improve if they

observe the value of an allowance program

Full-time counselors most efficient Workable to have sufficient caseload to occupy a

substantial portion of counselor’s time

Structure and Procedures Giving counselors authority to approve goods and

services on a pre-approved list: Reduces expense of review of spending plans State audit to ensure counselors follow approval procedures

Counseling tasks have many fiscal elements An efficient approach is to combine counseling and fiscal

services in the same organization and Make counselors responsible for some fiscal tasks

Steps from Enrollment to Receipt of Allowance (1-5)1. Consumer reviews rules and considers whether to name

representative and what to include in spending plan

2. Counselor visits the consumer to re-explain program and answer questions

3. Consumer and counselor prepare and sign a formal spending plan

4. Worker employment papers are completed and sent to fiscal agent for review

5. Counselor submits plan to program office for approval

Steps from Enrollment to Receipt of Allowance (6-10)6. Consumer, counselor, fiscal agent, and perhaps program

office resolve any errors in plan

7. Fiscal agent initiates consumer account from approved plan

8. Any errors in the employment papers are resolved by counselor, worker and fiscal agent

9. Traditional agency is notified of the date on which to terminate service

10. State Medicaid system is notified to initiate allowance

Reducing Time to the Allowance Some program structures and procedures are

more effective than others in reducing time to allowance

Procedures can be streamlined Programs should monitor elapsed time to

allowance Intervene if long lags observed

Program Costs

Avoid assigning responsibility for assessment and care planning to an advocate for the consumer

Cashing out care plans at a discount may be necessary to constrain costs

Overall costs could increase if the availability of an allowance increases demand

Costs and access are interrelated. Lower long-term care costs offset higher PCS costs.

Contact Information & Deadlines All inquiries about the program, selection criteria or

application process should be directed to Kristin Simone, Deputy Program Director, either via email at [email protected] or by calling 617.552.0620

Intent-to-Apply form due: February 13, 2004, 3p.m. EST

Full Proposal due: March 31, 2004 Intent-to-Apply form and application guidelines can

be found on www.cashandcounseling.org