Embed Size (px)

Citation preview

Repot No. 7196-SD

BangladeshAn Agenda for Tax Reform(in Three Volumes) Volume 1: Executive Summary and OverviewDecember 15, 1989

Public Economics DivisionCountry Economics Departnent

Policy, Planning and Research

FOR OFFICIAL USE ONLY

Docuen"t of the World Bank

This document has a restricted distribution and may be used by recipientsonly In the performance of their official duties. Its contents may not otherwisebe disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

BANGLADESS

CURRENCY EOUIVALEINTS

The estimated value of the Bangladesh Taka (Tk) is fixed inrelation -.o a basket of reference currencies, vith the U.S. Dollarserving as the intervention currency.

1989

US$1 - Tk 33Tk 1 - US$ 0.030

Weights and Measures

1 Crore - 10 million

FISCJL Y1uAR

July I -- June 30

FOR OMCIAL USE ONLY

BANBLADESH: AN AGENDA FOR TAX REFORM

VOLUME I

Table of Contents

Page No.

EXECUTIVE SUMMARY ................................................... i

CHAPTER 1: OVERVIEW .................................................1

I: INTRODUCTION .. 1

II: THE TAX STRUCTURE AND ITS CONSEQUENCES. 4

III: AN AGENDA FOR REFORM .14

IV: CONSUMPTION-BASED TAXATION .15

The Role of Import Taxes .18

A. Protection .18B. Revenue .19

V: RAISING REVENUE .20

1. Excise Taxation .202. Public Sector Pricing .213. Administration .22

VI: INCOME TAXATION .. 23

1. Personal Income Tax .232. Company Income Tax .25

This report is based on the findings of a mission that visited Bangladesh

in December 1986. It was led by Pradeep Mitra and consisted of EhtishamAhmad (Consultant), Henrik Dahl, Vijai Gupta (Consultant), Chad Leechor,Jonathan Skinner (Consultant), and Nicholas Stern (Consultant, IMF).Subsequent inputs were provided by Chand Tikku (Consultant). Valuableassistance was a]Jo provided by Jaber Ehdaie and Syed Nizamuddin.Earlier drafts of the report were discussed with the Government ofBangladesh in January 1988, August 1988 and September 1989. The missiongratefully acknowledges the cooperation received from all concernedagencies of the Government of Bangladesh and, especially, from officialsof the National Board of Revenue and the Planning Commission.

i ~~~~~~~~- i -

This document has a restricted distribution and may be used by recipients only in the performanceof their ofilcial duties. Its contents may not otherwise be disclosed without World Bank authorizat;on.

BANGLADESH: AN AGENDA FOR TAX REFORM

VOLUME I

Table gf ContentsPage No.

VII: TAX ADMINISTRATION ........................ 27

The Administration of Indirect Taxes .28

1. Existing Organization .28Auxiliary Organizations .29Field Level Organizations .29

2. Recommendations .29

A. The National Board of Revenue .30B. Auxiliary Organizations .30C. Field-Level Organizations .32

:.- 3. Personnel Implications .324. Miscellaneous .33

The Administration of Direct Taxes . .33

1. Existing Organizations .33

Auxiliary Organizations .33Field Level Executive Organizations .34Field Level Appellate Organizations .34

2. Recommendations .34

The National Board of Revenue .35

B. Auxiliary Organizations .. 36

C. Field Level Executive Organizations .36

i. Senior Commissioners .36ii. Commissioners .37iii. Assessing Officers .37

D. Field Level Appellate Organizations .38

3. Personnel Implications .384. Revenue Implications .395. Miscellaneous .39

- ii- I

BANGLADESH: AN AGENDA FOR TAX REFORK

VOLUME I

Tabl of Contents

Page No.

VIII: AGRICULTURAL TAXATION .................................... 40

1. The Land Development Tax .............................. 402. The Non-Judicial Stamp Tax ............................ 413. Tax Burden on Agriculture ............................. 414. Raising Direct Taxes on Agriculture ................... 42

A. The Short-Term .................................... 42B. The Medium-to-Long Term ........................... 42C. Revenue-Sharing ................................... 43

1x: REVENUE ESTIMATES ................ 43

- iii -

BANGLADESH: AN AGENDA FOR TAX REFORM

VOLUME I

List of TablesPage No.

Table 1.1: Selected Features of the Bangladesh Tax System(Percentage) .......... 2

Table 1.2: Tax Structure in Selected Countries Average 1980/85(Percentage) ........... 3

Table 1.3: Revenue Receipts Under M'ajor Heading 1984/85 - 1988/89 . 5

Table 1.4: Economic Classification of Tax Revenue 1984/85 - 1988/89... 6

Table 1.5: Direct and Indirect Taxes by Source 1984/85 - 1988/89. 7

Table 1.6: Decomposition of Tax Revenues (As a Percentage ofTotal Tax Revenue) .12

Table 1.7: Tax Elasticities (E) and Buoyancies (B) .13

Table 1.8: Estimated Revenue Impact of Tax Reform Proposals(Billions of Taka, Current Prices) .44

- iv -

EECUTIVE SMMARY

Introduction

i. This report lays out a medium-to-long term agenda for reformitlgthe tax system in Bangladesh into an elastic, efficient and equitableinstrument of domestic resource mobilization. In focussing on structuralreform, the report adopts an explicitly developmental perspective. Such astance is justified by the need to raise public expenditure on a long-termbasis in a number of major sectors of the economy. It is recognizedhowever that the pressing nature of shorter-term expenditure imperatives,together with a share of external financing in the Annual DevelopmentProgram ranging between 80 to 90 percent, call for additional revenue to beraised during the transition towards an improved tax structure. For thatreason, the report also proposes a set of revenue-enhancing measures that,however, have effects on efficiency and equity tbat are consistent with thespirit of developmentally-oriented tax reform.

The Existing System

ii. The tax system was characterized in 1987/88 by (a) a tax effort of7.9 percent of GDP, (b) a ratio of direct tax to total tax revenue of 21.8percent and (c) a ratio of domestically based indirect tax revenue to totalindirect tax revenue of 35.2 percent. All three figures are low ininternational comparative perspective. The reasons are, respectively, (a)the low per capita income ($160) and degree of urbanization (13 percent),together with significant weaknesses in tax compliance and taxadministration, (b) the virtual exclusion of agriculture (or 47 percent ofGDP) from direct taxation, pervasive exemptions from personal incometaxation and the widespread use of holidays from company income taxation,and (c) the narrow base of the urban formal industrial sector (60 percentof urban value added).

iii. The economic consequences of the tax structure are as follows.First, the tax system is inelastic: a Tk 1 increase in gross domesticproduct generates a Tk 0.71 increase in tax revenue. This, inter alia,requires discretionary revenue-raising measures in every annual budgetamounting, in recent years, to 0.7 percent of GDP, a process that canintroduce considerable uncertainty into production and investmentdecisions. Second, the structure of taxation (a) discriminates againstexports and (b) undermines efficiency in production and investment. Thefirst is due to an effective rate of import taxation (39 percent) that,even without taking account of quantitative restrictions, is substantiallyhigher than that applying to domestic production (8 percent). The secondis caused by taxation of raw materials and capital goods: those twocategories account for over 80 percent of import tax revenue and, in asmuch as gas and petroleum products have numerous intermediate uses, for alarge proportion of excises on domestic production as well. The widespreadtaxation of intermediate goods offers signals to exporters that are notconsistent with comparative advantage, distorts production choices fordomestic producers and confounds policy intentions by causing higher orlower taxation of certain sectors than an examination of tax rates on their

- li -

final outputs alone would suggest. Third, the system is perceived as beinginequitable. This is due to (a) numerous exemptions that erode the base ofpersonal income taxation, losing in the process an amount nearly 3qual tothe total revenue currently raised by the tax, (b) virtual exclusion ofagricultural income from direct taxation that primarily benefits wealthierlandowners and (c) pervasive use of tax holidays for companies.

R21omme£datign

iv. The characteristics described above define a natural medium-termstrategy for reforming the tax system. Such reform must be directedtowards (1) securing a steady increase in the tax revenue-to-GDP ratio; (2)providing appropriate incentives for savings, investment, exports andefficient production; (3) ensuring some progressivity in incidence and (4)strengthening and building on existing administrative capacity. Thoseobjectives can ultimately be achieved by (1) a broad-based taxation ofconsumption rather than imports; (2) a shift in the pattern of taxation (a)in the case of commodity taxation away from inputs and towards outputs soas to minimize distortions in production choices, and (b) in the case ofdirect taxation towards encouragement of saving and investment; (3)eliminating incentive and equity-reducing provisions in personal incometaxation and (4) strengthening the National Board of Revenue (NBR), itsauxiliary organizations and field-level units. The policy changes requiredto further those objectives are addressed under six broad areas: (1)indirect tax policy, (2) personal income tax policy, (3) company income taxpolicy, (4) indirect tax administration, (5) direct tax administration, and(6) land taxation.

Indirect Tax Administration

V. On indireet taxation, the report recommends (a) introductionwithin three years of a manufacturing-cum-import stage value added tax(VAT) applying at a single rate to the organized sector of the economy andreplacing existing excise taxes on domestic production, sales taxes onimports, and customs duties on a range of imported items for which there isno domestic production and which are therefore primarily revenue-raising;(b) supplementary levies on imports and domestic production of selectedluxuries; (c) zero rating of exports; and (d) customs duties that, thoughcontributing to revenue, are primarily protective in intent and are notcreditable under the VAT.

vi. These recommendations seek to move the point of taxation closer tofinal consumption, and, thereby, inasmuch as consumption is closely relatedto income, to enhance the elasticity of the tax system. The replacement ofinput-based taxation by output-based taxation will also reduce thedistortions in production and exportation that are characteri.-tic of thepresent system. While the initial scope of the VAT will coincide withthose of the indirect taxes that it replaces, the incentives for those notinitially registered under it to do so in order to claim tax credits oninputs, together with the gradual widening of the industrial base, willensure that the elasticity-enhancing and distortion-reducing effects of taxreform are continuing rather than ence-and-for-all .n nature. Therestriction of the VAT in the first instance to the manufacturing-cum-import stage and the choice of a single rate are dictated by administrativeconsiderations. However, the use of supplementary excises on selected

- iii -

luxuries and the fact that the poorest families depend mainly onnonmarketed food are expected to provide a moderate degree of progressionin the tax system. Finally, in sectors vhere protection is deemedappropriate as part of IDA's continuing dialogue with the government on theindustrial sector, and where the administrative resources to provideindustrial assistance directly to producers are lacking, it is recomendedthat protective customs duties be used and that these not be creditableunder the VAT.

Personal ncome Tax Policy

vii. On personal income taxation, the report recommends (a) inclusionof employment-related allowances in the tax base; (b) introduction of aconventional exemption limit; (c) introduction of a withholding tax on andelimin&tion of special exemptions for interest and dividends; (d)tightening of the scope of tax-deductible investment allowances in approvedassets; and (e) inclusion of realized capital gains in the tax base. Thesechanges could be introduced rapidly.

viii. These recommendations, which need to be viewed as an integratedpolicy package, would do away with the numerous exemptions that currentlyerode the base of the personal income tax, improve equity and strengthentax compliance. The inclusion of employment-related allowances wouldeliminate a major loophole under the present system. Moreover, thereplacement of the existing "filing threshold" by a conventional exemptionlimit would avoid undue hardship to those who would begin to pay taxes as aresult of the inclusion of employment-related allowances.1 Thewithholding tax on interest and dividends, together with a tightening ofthe scope of deductible investment rllowances, would eliminate a subsidythat accrues almost exclusively to the highest income groups and impairsthe equity of the system. FurtVaermore, it would do so while preservingincentives to save in approved assets and laying the foundation for aparticularly elastic source of revenue. The policy package would virtuallydouble the revenue contribution of the personal income tax system, with theextra revenue being raised in a markedly progressive way.

Comoanv Income Tax Policy

ix. On company income taxation, the report recommends that a study becommissioned as a matter of priority to ascertain the extent to whichindustrialization and regional development can be attributed to theextraordinarily generous tax incentives currently available and to set themagainst the considerable revenue losses and possibilities of abuse to whichtax holidays give rise. The findings would allow an informed judgment asto how the revenue costs of investment incentives may be lowered withoutprejudice to industrialization. In the meantime, it would be entirelyinappropriate to reduce the burden of company taxation any further.

1/ The filing threshold signals the existence of a tax liability which isthen computed on the basis of entire income rather than its excess overthe threshold. In contrast, an exemption limit defines taxable incomeas the excess over the exemption limit.

* iv

x. Should the proposed study on tax incentives and industrializationfind that a narrowing of the presently generous scope of tax holidays iswarranted, the company tax system should place greater reliance on theexisting instrument of accelerated depreciation allowances, combining itwith the phasing out of tax-deductibility of interest payments on loans.Such a system would raise significant amounts of revenue in a way thatpreserves efficiency in production and investment dects:.ons, i.e., withoutallowing the tax system to distort the choice of invesLment projects ordiscriminate between debt and equity finance.

Tax Administration

xi. The examination of tax administration in this report is designed(a) to strengthen its functioning in order to cope adequately withcompliance-reducing activities; and (b) to reform it in line with suggestedchanges in tax policy. The recommendations in every area build on existingadministrative structures and require a combination of strengthening ofexisting units with reorganization into new units at all levels. Thefollowing discussion recommends an integrated package of organizationalchanges at the apex of the administrative structure, for its auxiliaryorganizations, and field level units. A number of additional "stand alone"recommendations are presented as well. An appropriate timeframe, rangingfrom one to three years, is suggested in the report for each of thefollowing proposals.

xii. The National Board of Revenue (NBR) should (a) appoint four moremembers, two for indirect taxes: one in charge of taxation policy, planningand research and the other responsible for administration; and two fordirect taxes: one in charge of investigation, self-assessment, policy andresearch and the other responsible for administration, with a concomitantrearrangement of the responsibilities of the existing members; (b)reorganize and strengthen the Directorate of Research and Statistics; and(c) redistribute and streamline work within sections of the NBR.

xiii. Indirect Taxes. Turning to auxiliary organizations, it isrecommended that the existing Directorate of Inspection, Training andDrawback be divided, based on functions to be performed, into threeDirectorates of (a) Training, (b) Inspection, Organization and Methods,Audits, Manual and Publications and (c) Drawbacks, Manufacturer-in-Bond andRebates and each of them placed under a Director at the level of Collector.Recommendations are also made on the internal organization of the aboveDirectorates. Specific measures are proposed for a considerablestrengthening of the Directorate of Customs Intelligence and Investigationas well as the Office of the Controller of Customs Valuation. To helpdevelop a coordinated perspective on intelligence and investigative work,it is recommended that the above two organizations, together with theOffice of the Controller of Narcotics and Liquor, be brought under aDirectorate-General of Revenue Intelligence, Investigations and Operations,Valuation (Customs and Excise), Narcotics and Liquor.

- V .

xiv. Specific organizational reforms are proposed for each of the fieldlevel organizations. It is also recommended that the existing executivecollectorates concentrate on revenue collection by transferring allpreventive and intelligence work to three separate field-levelCollectorates of Customs (Preventive and Intelligence) set up for thispurpose.

xv. It is also recommended that (a) revenue accounting be done throughbanks rather than treasuries of the government; (b) computerization beintroduced in a phased manner in the executive field-level collectoratesand the Directorate of Research and Statistics; and (c) the HarmonizedSystem of Nomenclature be adopted for customs and excise tariffs.

xvi. Direct Taxes. With respect to auxiliary organizations it isrecommended that the existing Directorate of Inspection and Training bebifurcated into two separate Directorates, one for inspection and anotherfor training. A separate Directorate (Survey) should be created, withresponsibility for collecting information for cross-checking andinstituting follow-up action, for tax withholding and for taxpayereducation, printing and publication. The existing Directorate ofComplaints (Investigation) should be responsible for dealing with taxevasion petitions and be staffed by officers from the direct and indirecttax administration, thereby promoting coordinaticn between the two wings ofthe administration.

xvii. Specific organizational reforms are proposed for the field levelareaaxizations, both executive and appellate. The office of the SeniorCommissioner (Search, Seizure and Survey) should be abolished. It isrecommended that the area of self-assessment be enlarged and that aproportion of the larger tax returns be subject to detailed scrutiny to becompleted after a survey. Suggestions are made for improving the terms andconditions of employment in the Appellate Tribunal.

xviii. It is also recommended that (a) the vast majority of companies andprofessionals be required to submit tgx audit reports in a form to beprescribed by the income tax rules; (b) the "income year" be made uniform;(c) provisions for reopening completed assessments be liberalized; (d)interest and penalties be automatically levied, not only for late filing ofreturns but also on incomes brought to tax on assessment; (e) greater usebe made of presumptive taxation of "hard-to-tax" groups; (f) avoidablepaperwork be eliminated through reforms in the areas of crediting advancetax payments, issuance of assessment orders and the Jurisdiction of taxrecovery officers; and (g) computerization be introduced in a phased mannerinto the direct t2x administration.

xix. While implementation of the above measures to strengthen the; administration of all taxes will have salutary conseque:ces for revenue and

efficiency, their attractiveness would be further enhaaced if they did notinvolve significant new expenditures for the government. To that end, thereport suggests ways in which part of the new staff required in units whoserole is to be strengthened could come from a reorganization and merger ofexisting units and, where appropriate, from changes in existing personnelpolicies as well.

-vi -

hndsaxaton

xx. The analysis of agricultural taxation shows that (1) the directtax burden on agriculture is less than 0.5 percent of annual land income,(2) the indirect tax burden on rural and urban sectors is broadlycomparable, (3) there is no implicit taxation of agriculture viaprocurement price policy, domestic pricing below international prices orunfavorable terms of trade movements between agriculture and industry, and(4) agric-lture is taxed lightly both on historical grounds and relative toa number of other conditions. Furthermore, the fact that wealthierlandowners are suggested lightly compared to urban-based income taxpayersintensifies the presumption that the system creates serious rural-urbaninequities. While improvements in tax administration could yield someextra revenue from the land development tax (LDT) in the short run, theonly feasible way in particular of implementing a progressive LDT is tocontinue to improve and update the Record of Rights (ROR), a process thatis under way. Since this is costly, the GOB should study the extent towhich the land tax administration could use the information made availableby the new RORs to implement a progressive LDT without a significantreduction in compliance.

! Short-Term Revenue Enhancement

xxi. A number of the changes in the tax system recommended above wouldhave an immediate and positive impact on revenue. However, in as much asthis is not true of every recommended change, the report also proposesmeanures that can raise revenue in the short term without moving the taxsystem in directions contrary to the spirit of medium-to-long term reform.These include (a) specific proposals on a broad range of excises that haverevenue-raising potential with acceptable distributional consequences; (b)gre:-ter use of regulatory duties to mop up large scarci*y premia arising inthe market; and (c) review of high import duty rates to ascertain if lowerrates, by reducing evasion, could add to revenue as well as protection fordomestic industry.

OVEVIEW

1.1 The Third Five Year Plan stipulates a series of targets fordomestic resource mobilization over thz period 1984/85 to 1989/90. Theseare: (1) a more than 25 percent incwrease in the tax-to-GDP ratio; (2) a 5percent rise in the share of direct taxes in tax revenue; and (3) amovement away from trade-based taxes towards domestic sources of indirecttaxation, the share of the latter in total indirect taxation to rise by 18percent over the Plan period.

1.2 The rationale for the direction of change implied by those targetsis not hard to find. First, the need to raise public expenditure in anumber of major sectors of the economy on a long term basis, expectedimprovements in the pace of project implementation and a share of foreignfinancing in the Annual Development Program of between 80 and 90 percentcall for policies to raise the revenue-to-GDP ratio.1 Second, a rise inthe share of direct, or income taxation, has the potential for enhancingprogressivity of incidence thereby reducing perceptions of inequity in thetax system. Third, reduced dependence on trade-, and principally, import-based taxes would have the desirable effect of streamlining protection,thereby stimulating exports and efficient import substitution and reducingthe extent to which trade and industrial policies are hostage to revenueimperatives.

1.3 Some historical and comparative perspective on these figures isprovided by Tables 1.1 and 1.2 respectively. They show that a tax revenue-to-GDP ratio of under 8 percent ranks Bangladesh among the lowest of thelow-income countries and, furthermore, that there appears. to be nonoticeable trend in the behavior of the tax-to-GDP ratio since 1979/80.Indeed, the contribution of foreign grants and loans to resourceavailability exceeds that of tax revenue.2 Second, although the share ofdirect taxes in total tax revenue has increased since 1980/81, it issignificantly below that for other low-income countries in South Asia andsub-Saharan Africa. Third, the share of domestic indirect taxes in totalindirect tax revenue is among the lowest by international standards and hasexhibited no secular rise over the period as a whola. Thus, it is clearthat attaining the Third Five Year Plan targets will require a verysubstantial public domestic resource mobilization effort.

l/ The scope, adequacy and appropriateness of public expenditure is thesubject of a concurrent study.

2/ Thus, official development assistance in 1983/84 was 8.7 percent ofGNP.

- 2 -

Table 1.1: Selected Features of the Bangladesh Tax System(Percentage)

Domestically Based IndirectTax/GDP Direct Tax Revenue to Tax Revenue to Total

Year Ratio Total Tax Revenue Indirect Tax Revenue

1972/73 4.2 15.8 37.01973/74 4.4 14.5 31.51974/75 4.1 17.9 34.51975/76 6.8 18.5 30.71976/77 7.4 20.2 33.51977/78 6.9 18.5 28.71978/79 7.1 17.5 25.31979/80 7.4 17.3 23.61980/81 7.8 17.7 25.81981/82 7.5 20.4 28.81982/83 7.4 21.3 29.61983/84 6.8 19.9 31.51984/85 7.1 19.8 30.91985/86 7.2 21.2 30.91986/87 7.4 21.7 31.31987/88 7.9 21.8 35.21988/89* 7.9 20.8 37.5

Source: Bangladesh Fiscal Statistics, General Economics Division,Planning Comission, 1986. A/ Statistical Yearbook ofBangladesh 1984-85, Bangladesh Bureau of Statistics.

A/ Subsequent references to this source are abbreviated to"Bangladesh Fiscal Statistics."

*Provisional estimates.

-3-

Table 1.2: Tax Structure in Selected CountriesAverage 1980-85(Percentage)

DomesticallyDirect Tax Based Tax

S GNP Per Revenue To Revenue toCapita Tax/GDP Total Tax Indirect Tax(1984) Ratio Revenue Revenue

Bangladesh 130 7.3 20.1 29.3Malawi A/ 180 14.8 38.0 42.8India 260 16.2 30.1 44.6Ghana A/ 350 4.9 33.1 N.A.Pakistan 380 10.7 23.0 40.0Indonesia 540 20.1 80.2 / 66.9Thailand 860 13.1 22.1 66.8Philippines 660 10.8 24.8 60.7Malaysia 1980 22.8 44.9 b/ 38.3Korea £/ 2110 16.1 26.2 75.5

LDCs (82 countries) 4/ 1043.9 17.5 29.3

- Sub-Saharan Africa 4/ 579.1 17.6 30.3- Asia 4/ 864.4 14.9 30.3

- South Asia 4/ 183.3 12.4 13.0- East Asia d/ 1343.8 16.8 43.3

- Europe & Middle East 4/ 1537.0 19.7 30.2- Latin America d/ 1532.7 17.9 26.1

IndustrializedCountries /.S/ 10,105.1 29.7 34.2

a/ Data for 1982.

/ Including oil revenues. If these are excluded, the share of directtaxes in total tax revenue falls to 37.3%.

c/ Average 1980-1984 for Korea.

/ Data for 1979-1981.

p/ Excludes Japan and New Zealand.

Sources: Bangladesh Fiscal Statistics; Bangladesh Bureau of Statistics;Government Finance Statistics. (IMF) various issues andCountry Economic Memoranda, World Bank; V. Tanzi:"Quantitative Characteristics of the Tax Systems of DevelopingCountries", in Newbery, D. and N. Stern (eds.) Th hoyoTaxation for Develooinz- Countries (Oxford University Press forthe World Bank, 1987) and World Development Relpor, 1986.

- 4 -

1.4 The low tax-revenue-to-GDP ratio can in part be explained by percapita income and degree of urbanization both of which in the case ofBangladesh, are lower than that of comparator countries.3 This is becausethe growth of GDP augments the capacity to tax at the same time asurbanization generates a higher demand for public services that arefinanced via taxation. The low share of direct taxes may be attributed tothe virtual exclusion of agriculture, which accounts for 48 percent of GDP,from the purview of personal income taxation and the widespread use ofholidays from company income taxation. The comparatively limited role ofdomestic sources of taxation in indirect tax revenue is partly accountedfor by the narrow base of the formal industrial sector.

II. THE TAX STRUCTURE AND ITS CONSEOUENCES

1.5 Tables 1.3-1.5 report the breakdown of receipts from 1984/85 to1988/89. Taxes on imports account for over 50 percent of total taxrevenue. They comprise a number of elements: customs duties, which arelevied on c. and f. value, sales taxes, which are collected exclusively onimports and are assessed on customs duty-paid value, development surcharge,license fees and regulatory duty. While the breakdown among consumergoods, raw materials and capital goods in dutiable imports in 1985/86 wasin the proportions 19 percent: 57 percent: 24 percent, the correspondingdecomposition in customs duty and sales tax (CDST) collections was 20percent: 57 percent: 23 percent. This yields an average effective rate ofCDST on dutiable imports of 39 percent. Export duties are negligible,being levied currently on wet blue leather and raise somewhat over 1percent of revenue from taxes on international trade.

1.6 Over 97 percent of domestic indirect taxation comes Arom excisetaxes which are levied ex facto on domestic production and also on someservices. The domestic sales tax, which also used to apply at themanufacturing stage, was amalgamated with the excise tax to form a singletax at the ex-factory level. Given the heavy reliance on trade taxes,there has been an attempt to raise additional revenue from the domesticsector in recent years: in recent years, excises have accounted for 23percent of revenue. However, the base of domestic indirect taxation isconstrained by the narrowness of the formal sector industrial base. Two-thirds of excise tax revenue is accounted for by three categories of goods,viz., tobacco, gas and POL (petroleum, oil and lubricants) products. Theaverage rate of excise taxation, defined as the ratio of collections to thegross value of excisable production, is around 8 percent.

1.7 The remaining 3 percent of revenue from taxes on domesticproduction comes from domestic services: advertisement tax, electricityduty and motor vehicle tax.

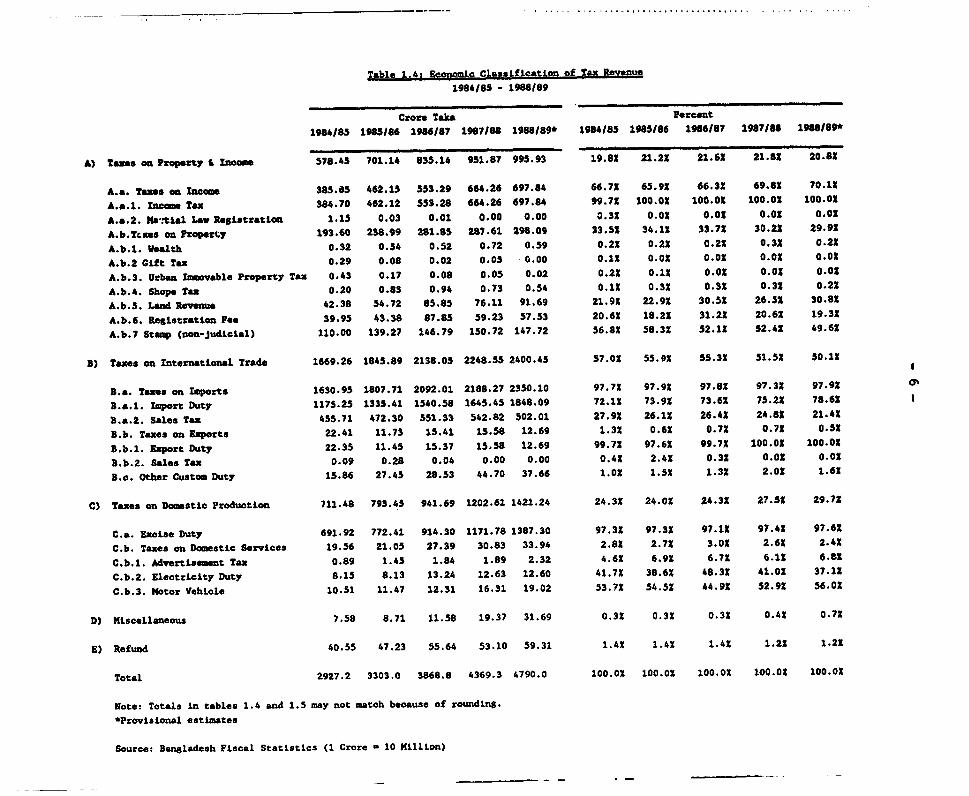

1.8 Direct taxation accounts for one-fifth of tax revenue. Withinthis category, income taxes are the most important, as Table 1.4 makesclear. Revenue arising from the taxation of personal and company incomeaccounts for 15 percent of total tax revenue or about 1.2 percent of GDP;roughly one-quarter of this can be attributed to the personal income

3/ The extent of urbanization in various comparator countries is reportedin Table 5.1 of this report.

Table 1.3t Revenue Receints Under Maitor Heading

1984185 - 1988189

Crore Taka Percent

1984185 1985186 1980187 1987188 1988189* 1984185 1985186 1986187 1987188 1988169'

A) Tex Receipts 2927.2 3303.0 3868.9 4371.0 4790.0 82.81 80.0X 52.62 63.21 84.9S

Custol 1183.1 1339.2 1541.9 1654.4 1844.9 40.4A 40.51 39.91 37.82 38.5X

Exciae 691.9 772.4 914.3 1171.8 1387.3 23.01 23.41 23.6X 26.81 29.0X

Sales 445.6 460.5 538.5 542.8 502.0 15.21 13.9X 13.91 12.42 10.51

Incolae 385.9 462.2 553.3 664.3 697.8 13.21 14.01 14.3A 15.2X 14.62

Land Revenue 42.4 54.7 65.7 76.1 91.7 1.41 1.71 1.72 1.7X 1.92

Staup(Non-Judicial) 110.0 139.3 146.8 150.7 147.7 3.8X 4.21 3.81 3.4Z 3.12

Registration 40.0 43.4 67.9 59.2 57.5 1.4X 1.31 1.81 1.45 1.2X

Motor VehIcle 10.5 11.5 12.3 16.3 19.0 0.41 0.31 0.31 0.4X 0.4X

Other 17.9 19.9 28.2 35.4 42.1 0.61 0.61 0.1 0.8X 0.91

B) lion-Tax ReceLpts 609.2 826.5 814.1 880.3 852.8 17.2X 20.01 17.41 16.81 15.11

Stem (Judielal) 4.2 7.2 9.0 12.3 15.8 0.71 0.91 1.1! 1.4X 1.91

Forest 45.6 60.6 52.4 57.7 51.2 7.5 7.3X 6.41 0.61 6.01

Post Offlce -17.6 -14.5 -24.1 -24.0 -15.5 -2.91 -1.8X -3.0X -2.7X -1.81

Telegraph * Telephone(Net) 27.5 84.6 62.3 96.7 122.0 4.51 10.21 7.71 11.02 14.3X

Reilvay(llet) -35.8 -116.0 -136.7 -153.1 -123.1 -6.4X -14.01 -16.68 -17.41 -14.41

Interest 124.3 230.9 191.6 227.0 107.7 20.41 27.91 23.5X 25.81 12.62

Nationalised Industries & Corp. 67.4 76.7 88.2 56.9 57.6 ll.1X 9.31 10.82 6.51 6.81

Nationalized Financial Institutions 213.0 268.3 257.3 121.1 136.6 35.0X 32.51 31.6Z 13.8X 16.02

Other 183.5 228.7 314.1 485.7 500.5 30.11 27.72 38.61 55.21 58.7X

Total(A-B) 3536.4 4129.5 4682.9 5251.3 5642.8 100.0 100.01 100.01 100.O 100.0

Source: Bangladesh Fiscal Statistics (1 Crore 1 l0 Million)

*Provisional estimate

_ _,. .......... ................... .....

Table 1.4t Econnmic Classification of Tax Revenue

1984185 - 1988189

Crore Taka parcont1984183 1985186 1986187 1987/88 1988189* 1984185 198U186 1986/87 198718U 198U189*

A) Taxs on Property lncote 578.45 701.14 835.14 951.87 995.93 19.82 21.21 21.62 21.82 20.81

A.&. Taxes on Income 385.85 462.15 553.29 664.26 697.84 66.7X 65.9X 66.3Z 69.82 70.12A.*.1. Incoae Tax 384.70 462.12 553.28 664.26 697.84 99.72 100.02 100.0 100.02 100.02A.a.2. Kax tiel Law Registration 1.15 0.03 0.01 0.00 0.00 0.32 0.02 0.02 0.0 0.02A.b.Tcses on ?:operty 193.60 238.99 281.B5 287.61 298.09 33.51 34.12 33.72 30.22 29.92A.b.l. Wealth 0.32 0.54 0.52 0.72 0.59 0.2% 0.22 0.22 0.3X 0.22A.b.2 Glft Tax 0.29 0.08 0.02 0.05 0.00 0.12 O.O 0.02 O.O 0.02A.b.3. Urban Immovable Property Tax 0.43 0.17 0.08 0.05 0.02 0.22 O.12 0.02 0.0 0.02A.b.4. Shope Tax 0.20 0.83 0.94 0.73 0.54 0.12 0.32 0.32 0.32 0.22A.b.5. Land Revenue 42.38 54.72 85.85 76.11 91.69 21.92 22.92 30.51 26.52 30.82A.b.6. Registration Fee 39.95 43.38 87.85 59.23 57.53 20.62 18.22 31.22 20.62 19.32A.b.7 Stamp (mon-judicial) 110.00 139.27 146.79 150.72 147.72 56.8X 58.32 52.1X 52.42 49.62

B) Taxes on International Trade 1669.26 1845.89 2138.05 2248.55 2400.45 57.02 55.92 55.3X 51.52 50.12

B.a. Taxes on Imports 1630.95 1807.71 2092.01 2188.27 2350.10 97.72 97.9X 97.82 97.32 97.92B.a.l. Import Duty 1175.25 1335.41 1540.58 1645.45 1848.09 72.12 73.92 73.62 75.22 78.62B.*.2. Sales Tax 455.71 472.30 551.33 542.82 502.01 27.9X 26.12 26.42 24.82 21.42B.b. Taxes on Exports 22.41 11.73 15.41 15.58 12.69 1.32 0.62 0.72 0.72 0.52B.b.l. Export Duty 22.35 11.45 15.37 15.58 12.69 99.72 97.62 99.72 100.O 100.02B.b.2. Sales Tax 0.09 0.28 0.04 0.00 0.00 0.42 2.42 0.32 0.02 O.OXB.c. Other Custom Duty 15.86 27.45 28.53 44.70 37.66 1.02 1.5X 1.32 2.02 1.62

C) Taxes on Domestic Production 711.48 793.45 941.69 1202.61 1421.24 24.3X 24.02 24.32 27.52 29.72

C.&. Excise Duty 691.92 772.41 914.30 1171.78 1387.30 97.32 97.32 97.13 97.42 97.62C.b. Taxes on Domestic Services 19.56 21.05 27.39 30.83 33.94 2.82 2.72 3.0X 2.62 2.4XC.b.2. Advertisement Tax 0.89 1.45 1.84 1.89 2.32 4.6X 6.92 6.72 6.12 6.82C.b.2. Electricity Duty 8.15 8.13 13.24 12.63 12.60 42.72 38.62 48.31 41.02 37.12C.b.3. Motor Vehicle 10.51 11.47 12.31 16.31 19.02 53.72 54.52 44.92 52.92 56.02

D) Miscellaneous 7.58 8.71 11.58 19.37 31.69 0.32 0.3X 0.32 0.42 0.72

E) Refund 40.55 47.23 55.64 53.10 59.31 1.42 1.42 1.4 1.22 1.22

Total 2927.2 3303.0 3868.8 4369.3 4790.0 100.02 100.02 100.OX 100.0X 100.02

Note: Totals in tables 1.4 and 1.5 may not match because of rounding.*Provisional estimates

Source: Bangladesh Fiscal Statistics (1 Crore - 10 MiliLon)

- 7 -

Table 1.5: Direct and Indiract Taxes by Source1984/85-1988/89

Crore Taka

1984/85 1985/86 1986/87 1987/88 1988/89*

A. Indirect Taxes 2347.77 2601.85 3031.22 3419.20 3794.18

A.1. Customs 1183.10 1339.17 Ib41.88 1654.41 1844.88A.2. Central Excise 675.30 756.03 856.51 1154.62 1364.57A.3. Liquor and

Narcotics 16.62 16.38 17.79 17.15 22.76A.4. Sales 445.61 460.49 538.52 542.82 502.01A.5. Motor Vehicle 10.51 11.47 12.31 16.31 19.02A.6. Travel 7.33 8.56 8.92 16.95 20.50A.7. Electricity 8.16 8.13 13.24 12.63 12.60A.8. Advertisement 0.89 1.44 1.84 1.89 2.32A.9. Turnover 0.25 0.18 0.21 0.26 0.07A.10. Other 2.16 5.45

3. Direct Taxes 579.87 701.22 835.15 951.87 995.93

B.1. Income andCorporation 385.70 462.12 553.28 664.26 697.84

B.2. ML Regulation 1.15 0.03 0.01 0.00 0.00B.3. Land Revenue 42.38 54.72 65.65 76.11 91.69B.4. Stamp (Non-

Judicial) 110.00 139.27 146.79 150.72 147.72B.5. Registration 39.95 43.38 67.85 59.23 57.53B.6. Urban Immovable

Property 0.43 0.25 0.08 0.05 0.02B.7. Wealth 0.32 0.54 0.52 0.72 0.59B.8. Gift 0.29 0.08 0.02 0.05 0.00B.9. House Rent 0.00 0.00 0.00 0.00 0.00B.10. Betterment and

Shop 0.23 0.83 0.95 0.73 0.54

Total (A+B) 2927.64 3303.07 3866.37 4371.07 4790.11

Source: Bangladesh Fiscal Statistics1 Crore - 10 milllon

Note: Totals in Tables 1.4 and 1.5 may not match because of rounding.

* Provisional Estimates.

-8-

tax. Other direct taxes of significance are the non-judicial stamp tax andthe land development tax.

1.9 Flgures 1.1 to 1.3 and Table 1.6 show the breakdown of tax revenuein India and Pakistan in relation to Bangladesh. The greater dependence ontrade taxes in Bangladesh is clear. Since indirect taxation accounts forthe bulk of revenue, the larger relative role of agriculture and thevirtual exemption of agricultural income from taxation in all threecountries do not entirely explain the comparatively low tax revenue inBangladesh. More relevant is the make-up of consumption and the coverageof the indirect tax net. In comparing systems which depend largely onindirect taxation, a lower level of revenue is to be expected in an economywhere a higher proportion of consumption is in kind or on tax-exempt goods.Thus the higher levels of tax revenue in India than Pakistan, and Pakistanthan Bangladesh, may be in large part due to the broader coverage acrossgoods in India and a stronger administration.

1.10 While economic structure imposes certain constraints on taxation,there is considerable room for designing tax policy in ways that can betterserve the objectives of economic development. This is best appreciated byexamining the economic consequences of the tax structure in Bangladesh.

1.11 First, it may be observed that increases in tax revenue do notkeep pace with increases in GDP. Table 1.7 presents elasticities forvarious taxes. The period 1979/80 to 1984/85 is characterized by a highlyinelastic overall tax system. This is readily explained by the observationthat in Bangladesh the elasticity of a tax is inversely related to itsimportance in tax revenue; it is the highest for the income tax (1.11) andlowest for import duties (0.56) and the sales tax (0.55), the latter beinglevied on imports as well. This implies that maintaining even a constanttax revenue-to-GDP ratio requires discretionary changes in rates from year-to-year, a process which can introduce considerable uncertainty intoproduction and investment decisions. The buoyancy figures in Table 1.6incorporate the effects of discretionary changes.

1.12 Second, the overwhelming reliance on import taxation, which islevied at an average effective rate of 39 percent, compared to domesticindirect taxation which has an average effective rate of roughly 8 percent,implies that the system discriminates against exports and in favor ofimport-substitution. While there are certain sectors, identified andanalyzed in IDA's Industrial Sector Credit proposals,4 for which protectionis appropriate and warranted, postwar experience in developing countriessuggests that a generalized anti-export bias is inimical to the developmentof an efficient industrial sector capable of responding flexibly to achanging external environment.

1.13 Third, the fact that 81 percent of dutiable imports are rawmaterials and capital goods and that the effective rates of import duty onthose categories are 40 percent and 38 percent respectively, imply thatindustries using them are heavily taxed via the taxation of inputs. Thisis particularly serious for those export-oriented industries such as lightengineering goods where Bangladesh has a comparative advantage; their

4/ (World Bank Report No. P-4558-BD,May 18. 1987.)

BangladeshR.v.nu. Pr olb

44..

41% 4 < __t ~

c 4|| -

2"

2ft~~~~~~~~~wo

LI Customs + Sales O xcls- a hncmo-

C~~~~~~~~~

IndiaRvonue Profie

3 3hs

31%

29%aZC2"

* 227X S

2 ft

245

225621%

1756

"S

135

80/81 81/82 82/81 83/84 64/85 85/86

Yeara Custacos + Sales o Eacbis a knconm.

Pa;kistanAeetnu. Pofli.

45b

-

°-m - -

2 I _W-

202

1 . . ........

80/81 81182 82/83 63/84 64(8S

Vara Cu8tons t 0+ Excie A hncm

- 12 -

ITable .. 6: Decomposition of Tax Revenues(As a Percentage of Total Tax Revenue)

Bangladesh India Pakistan

Customs RgUtY

1980/81 42.1% 14.2% 18.0%1981/82 39.9% 14.3% 19.4%1982/83 42.1% 13.8% 17.9%1983/84 39.4% 13.1% 14.9%1984/85 40.4% 12.5% 15.8%1985/86 40.5% 12.9%

Salgs -Tax

1980/81 12.4% 17.2% 36.8%1981/82 13.2% 17.8% 35.0%1982/83 14.6% 18.8% 43.4%1983/84 14.8% 17.7% 43.2%1984/85 15.2% 19.7% 43.1%1985/86 13.9% 21.7%

Excise Tax

1980/81 20.9% 32.8% 34.0%1981/82 23.5% 30.7% 27.4%1982/83 22.2% 29.6% 26.9%1983/84 25.2% 32.4% 27.0%1984/85 23.6% 31.1% 25.4%1985/86 23.4% 30.2%

Income Tax

1980/81 19.1% 20.3% 7.4%1981/82 17.8% 21.0% 7.6%1982/83 14.6% 20.8% 7.1%1983/84 14.3% 20.6% 7.9%1984/85 13.2% 20.5% 7.8%1985/86 14.0% 19.9%

Sources: World Bank; Government of India, Economic Surveys; and FinanceDivision, Government of Pakistan.

-13 -

Table 1.7: Tax Elasticities (E) and Buoyancies (B)

PeriodTax Base 72/3-84/5 72/3-79/80 75/6-84/5 79/80-84/5

E B E B E B E B

All Taxes GDP atmarket prices 1.04 1.22 1.27 1.43 0.91 1.10 0.71 0.99

Import Dutiable valueDuties of imports 0.81 0.89 0.93 0.94 0.72 0.84 0.55 0.71

Sales Tax Duty-paid valueof imports 0.93 0.91 0.16 1.15 0.83 0.81 0.56 0.54

Excise GDP at marketDuties pries 0.86 1.23 0.91 1.12 0.76 1.18 0.83 1.34

Income Tax Non-agriculturalGDP 0.92 1.04 1.16 1.22 0.75 0.90 1.11 1.24

Source: Bangladesh Fiscal Statistics, 1972-73 to 1985-86. The buoyancyestimates are obtained by regressing the logarithm of the revenue onthe logarithm of the base. The elasticity estimates follow the sameprocedure but adjust revenue for "discretionary" measures.

- 14 -

competitiveness is seriously affected by duties and quantitativerestrictions on imports of basic inputs such as steel.

1.14 Fourth, the widespread taxation of intermediate goods via importduties and excise taxes leads to a total tax element in final price which,for certain sectors, is entirely due to the cascading effect of taxation oninputs used by them. Thls dLstorts productlon choices for domesticproducers, offers signals to exporters that ar- not consistent withcomparative advantage and confounds policy intentions by causing higher orlower taxation of certain sectors than an examinatlon of effective taxrates on their final outputs alone would suggest.

1.15 Fifth, a large number of exemptions erodes the base of thepersonal income tax which, among all existing tax instruments inBangladesh, is potentially the most capable of introducing progressivity inincidence. A notable example is provided by exclusion of housing,transportation and entertainment allowances from taxation. It is alsoparticularly true of the double exemption implicit in (1) deductibility ofupto one-third of income if allocated to a wide category of "approved"investments, followed by (2) untaxability of the capital income resultingfrom those investments. These features of -:he tax system weakenperceptions of equity that are important for its functioning.

1.16 Sixth, the use of a filing threshold, currently set at Tk 36,000that signals tax liability on AU personal income as opposed simply to theexcess over the threshold, as would be the case under a conventionalexemption limit of the kind used in most countries, has a negative impacton tax compliance and, to some extent, on incentives for a significantnumber of taxpayers.

1.17 Seventh, the pervasive use of tax holidays as the predominantfiscal incentive to companies results in significant revenue losses vis-a-vis other systems which can provide comparable and, in some respects,superior investment incentives. When taken in conjunction with thegenerous treatment awarded by the personal income tax to the instrumentsusea to finance these investments, those incentives turn out to beextremely generous by international standards.

1.18 Finally, the virtual exclusion of increasingly concentratedagricultural wealth from direct taxation creates a widespread impressionthat the existing tax system is subversive of rural-urban equity,especially with respect to better-off rural housenolds.

III. AN AGENDA FOREFOM

1.19 The characteristics described above define a natural medium-termstrategy for reforming the tax system. Such reform must be directedtowards (1) securing a steady 'ncrease in the tax revenue-to-GDP ratio; (2)providing appropriate incentives for savings, investment, exports andefficient production; (3) ensuring some progressivity in incidence and (4)strengthening and building on existing acwinistrative capacity. Thoseubjectives can ultimately be achieved by (1) a broad-based taxation ofconsumption rather than imports; (2) a shift in the pattern of taxation (a)in tile case of commodity taxation away from inputs and towards outputs soaa tO minimize distortions in production choices, and (b) in the case ofdirect taxation towards encouragement of saving and investment; (3)

- 15 -

eliminatLag incentive and equity-reducing provisions in personal incometaxation and (4) strengthening the National Board of Revenue (NBR), itsauxiliary organizations and fiold-level units.

1.20 This report accordingly recommends changes in the tax system so asto make it more capable of furthering those objectives. In doing so, itpays close attention to what is feasible ln one of the world's lowestincome countries with seml-porous borders, weak administrative capacity andlimited tax compliance. These characteristics are manifested in smugglingand excise tax evasion, a tax administration (especially customs) lackingin resources relative to the demands placed on it and widespread publicperceptions of capricLousness in the Lncidence of the tax system. This hasthree implications. F'rst, any proposal on tax and tariff policy mustimplicitly take into account its effects or t.e* relative ease of smugglingand other compliance-reduclng actLvities. rhis places a premium onsimplicity and enforceability in the light of tax policies in neighboringcountries. Second, changes in tax policy Pad administration must bedirected towards removing exemptions and iapil-it subsidies that accrue towealthler individuals so as not to exacerbate perceptions of inequity.Third, the thrust of a reform program must be to balance the need to buildon existing administrative instruments with the requirement thatidentlfiable iLprovements be introduced within a medlum-to-long termmonitorable timetable.

1.21 The above discussion makes clear that thls report is concernedprimarily with recommending policy changes that will lay the foundationsfor an elastic, efficient and equitable tax system over a medium-to-longterm horlzon in Bangladesh. It will be seen that a number of the suggestedchanges have an immediate and positive impact on revenue. However, in asmuch as this is not true of every recommended change, and given thepressing nature of revenue needs, the report also proposes measures thatcan raise revenue urgently without moving the tax system in directionscontrary to the spirit of medium-to-long term tax reform.

IV. CONSUKPTION-BASED TAXATION

1.22 The taxation of consumption can be achieved either by a sales taxor a value-added tax at the retail level. Such broad based taxation at theretail level is not in prospect in Bangladesh in the near future. This isdue to the small size of retail outlets selling to consumers, the generallylow standards of bookkeeping in such establishments and the limited reachof the tax administration. Accordingly, the mission's princlpalrecommendation on indirect taxation is that the GOB take a series of stepswith a view to phasing in a rudimentary value-added tax (VAT) at themanufacturing-cum-import stage over a three-year period. The rudimentarynature of the VAT derives from the fact that it would, at the time ofintroduction, apply only to the "organized" sector of the economy, viz,international trade, the public sector and those industries whereadministrative capacity permlts effective imposition and collection oftaxes on output. This would build on existing duty drawback and excise taxrelief procedures, a number of which already possess the characteristics ofan embryonic VAT at the manufacturing-cum-import stage. Thus the mission'sproposals balance the need to acquire administrative experience with such

- 16 -

instruments against that of moving towards taxing consumption within atimeframe that is broadly consistent with that for the ongoing reform oftariffs and quantitative restrictions. Experience in other countries notcharacterized by strong tax administration suggests that a three-yearhorizon for the introduction of a rudimentary VAT is feasible forgovernments committed to tax reform.

1.23 Chapter 2 records the widespread use of the value-added cax.Nearly sixty countries, forty developing countries among them, use someform of VAT. Turning to low- and lower-middle-income countries, sometwenty countries in sub-Saharan Africa, as well as Indonesia, use taxeswith VAT-like characteristics that do not extend completely through theretail sector. Comparative experience suggests that the rudimentary VATrecommended for Bangladesh be of the csmatimj.ton type, be based on thedestination principle and be implemented in its crediting form. Theseterms, which are explained below, shape the nature of the steps that mustbe taken to reform the indirect tax structure. Taxation of value-addedimplies that a manufacturer subtracts from the tax due on output the taxespayable on purchases of all raw materials and capital goods; a consumption-type tax ensures that taxes paid on capital goods as well as raw materialsare deductible from taxes due on output. The destination principle isdesigned to tax all value-added, at home or abroad, of goods that have astheir final destination consumers in Bangladesh: this translates into thetaxation of imports but no taxation of exports. The crediting methodrequires a firm to subtract the tax already paid on its purchase invoicesfrom tax liability on its output and to forward the difference to theexchequer. 5

1.24 It will be recognized that a VAT at the manufacturing-cum-importstage applying to the organized sector alone does not tax finalconsumption. Thus, sectors not registered for tax purposes, viz., smallscale and unorganized manufacturing, much of wholesale and retail trade andagriculture will be taxed on their inputs, a feature that usuallyencourages registration by progressively more taxpayers under the VAT, thusadding to revenue growth. Hence the rudimentary VAT and concomitantchanges in administration discussed in subsequent chapters of the reportare to be seen as intermediate steps towards the evolution of a retail-based tax system.

1.25 Existing instruments on which the reform of indirect taxation mustbuild are as follows. To help offset the discrimination against exports,GOB provides for a variety of bonded warehouses and duty drawbackprocedures which allow exporters duty-free access to imported inputs.Exporters also enjoy excise tax relief on inputs via "in bond' facilities.These may be seen as attempts to implement a "destination principle" VAT inthe export sector with non-taxation of exports taking the form of "zerorating", i.e., refund of input taxes to a sector enjoying a zero taxliability on its output. In this area, the mission's proposals provide forstrengthening and extension of such procedures.

5/ To the extent that manufacturers will buy part of their inputs fromwholesalers and retailers not registered with the authorites,consideration should be given to "deemed-to-have-paid" provisions, asoutlined in Appendix 2.3.

- 17 -

1.26 Comparable provisions are much less developed for domesticproducers. There are some examples of CDST refund on inputs entering into(4..*-3tic production for narrowly specified activities but, as far as themission in aware, no examples of excise tax relief in such cases.Accordingly, the mission has proposed that such provisions be developed andextended to cover excisable goods in establishments registered with the taxauthorities. Furthermore, all existing instruments involve either "inbond" facilities or refunds. This is virtually inevitable with zero-ratedactivities such as exports unless exporting firms have tax liability ondomestic sales that are large enough to offset duty drawbacks. The missionsuggests that import duty and excise tax relief applying to domesticproduction use crediting methods.

1.27 It is further suggested that the steps taken to help phase in theproposed VAT include the adoption of the Harmonized System of Nomenclature(HSN). This can make the coverage of the excise tariff more comprehensiveand allow it to be matched readily with the customs tariff. Theintroduction and implementation of the HSN will permit a removal ofexemptions and hence a smoother transition to a mcnufacturer-cum-importstage VAT.

1.28 The NBR should also institute programs to (1) educate thetaxpaying public about the provisions of the crediting/drawback procedures;(2) move towards appropriate legislation necessary for the VAT; (3) trainstaff to administer the new tax and (4) strengthen the machinery requiredfor its auditing, collection and enforcement.

1.29 As a result of a recommended series of steps carried out over athree-year period, Bangladesh should replace the existing system of salestaxes on import, customs duties on a range of imported items for whichthere is no domestic production and which are therefore primarily revenue-raising and excise taxes levied on the organized sector by a rudimentaryVAT at the manufacturing-cum-import stage applying to that sector of theeconomy. It is proposed that the VAT apply at a common rate and besupplemented by a set of excises on domestically produced and importedluxuries and other items the consumption of which the government might wishto discourage. Customs duties that are primarily protective in intentwould continue for sectors where protection is deemed appropriate and noother instrument for extending such protection is available; this theme iselaborated below in paragraph 1.35.6 To fulfill that purpose, customsduties would not be creditable under the VAT. The system would "zero rate"exports and exempt all other sectors such as agriculture, small scale andunorganized manufacturing and much of wholesale and retail trade. Thisimplies that, while exporters would not be taxed on their inputs, theexempted sectors mentioned above would continue to pay taxes on theirinputs. Experience suggests that such a rate structure could provide amoderate degree of progression in the tax system, a feature that would beenhanced by the dependence of the poorest families on nonmarketed food.

1.30 In suary, the reformed system of indirect taxation on importswould be characterized by (i) a value added tax at a standard rate, (ii)supplementary excises on imports of selected luxuries and (iii) primarily

6/ It is recognized that these would make a positive contribution torevenue as well.

- 18 -

protective customs duties in certain sectors. Correspondingly, fordomestic production, there would be (1) value added tax at a standard rate,and (ii) supplementary excises on domestic production of the same luxuries.As mentioned before, luxury excises on domestic production and importswould be matched for tax purposes. The rate of VAT would be set so as toraise as much revenue as the duties and taxes initially replaced by it.International experience, presented in Chapter 2, suggests that the growthof indirect tax revenue has kept pace with that of GDP in countries thathave introduced a value added tax.

1.31 Chapter 2 of the report therefore highlights two sets of themes.First, a VAT is desirable on the grounds that it moves the focus oftaxation towards consumption and away from intermediate goods with theirattendant deleterious effects on efficient production and exports.Notwithstanding its desirability however, a VAT at the retail level cannotbe implemented in the near future. This leads to the second theme, viz.,that the COB needs to follow a series of policies in the immediate future,that can build on existing instruments and eventually phase in amanufacturer-cum-import stage VAT applying to the organized sector over athree-year period. A widening of the tax base should occur through (i)progressive implementation of the HSN and concomitant removal ofexemptions; (ii) general strengthening of customs and excise administrationalong lines detailed in Chapter 3; and (iii) the process of

j industrialization over time. In turn, deepening coverage of the tax systemto the retail level could be introduced on an experimental basis for a fewitems such as selected POL products that are sold in retail establishmentsover a certain size. However, it is recognized that any significantprogress at that level must await the emergence of retail outlets that arelarge enough to make registration for tax purposes cost-effective for theauthorities.

The Role of Import Taxes

1.32 The above proposals, which are consistent with GOB's avowedobjective of reducing reliance on CDSTs in indirect tax revenue, would alsohave two significant implications. First, by assigning a primarilyprotective role to customs duties, they would have the effect of reducingthe very substantial protection afforded to a broad range of import-substituting industries under the present system. Second, the loss ofrevenue implied by progressive extension of duty drawback and creditingfacilities would have to be offset by increases in excise tax rates onfinal goods. Both protection and revenue dimensions of the proposals aretherefore examined below.

A. Protectin

1.33 The GOB, in line with the objectives of the New Industrial Policyof 1982, has decided to reduce and streamline protection afforded todomestic industry. To that end, it has decided as part of the IDA-supported Industrial Sector Credit to reduce the number of CDST slabs aswell as the rates, to phase out items from the negative and restrictedlists of imports subject to quantitative restrictions (QRs) and toimplement substantial tariff reform in the textiles and steel andengineering sectors which together account for roughly 30 percent of value-added in manufacturing.7 A number of the reductions in the textiles andsteel tariffs simply recognize what is already the case, viz., that

7/ World Bank, 2p. cit.

- 19 -

compliance-reducing measures in a country with semi-porous borders andlimited administrative capacity make high statutory rates irrelevant. Tothat extent, a closer alignment of statutory with effective rates, byencouraging imports through official channels will increase revenue andincrease protection to activities such as cotton weaving which have beenadversely affected by smuggled fabrics. Nevertheless, in as much as 81percent of imports are raw materials and capital goods which have aneffective CDST rate of 39 percent the broad intent of the proposals, viz.,to reduce and streamline protection, removes a major obstacle to a movetowards consumption based taxation.

1.34 In contrast with excise taxation, the mission has not, with theexceptions noted in paragraph 1.37 below, developed any specific proposalswith respect to tariff rates. This is because any increase in those rateswould go against the objectives of the New Industrial Policy as well asthat of ultimately reducing reliance on import taxation. On the otherhand, further reductions must be tailored to the circumstances ofindividual manufacturing sectors -- a task already being pursued as part ofIDA's continuing dialogue on the industrial sector with GOB.

1.35 Protective customs duties on imports, by not being part of theVAT, would provide an (implicit) subsidy to domestic producers of suchgoods. Furthermore, since customs duties raise the user prices of thegoods on which they are levied, the implicit subsidy in question would befinanced by taxing its users. The rationale for such subsidies is providedby the argument that they are required to make certain import-substitutingsectors of the economy ultimately competitive with foreign producers. Asmentioned above, IDA, in its dialogue with GOB on industrial policy, isattempting to identify sectors where such arguments are persuasive andwhere subsidization through tariff protection should therefore be extendedon a time bound basis. Efficiency would require making such subsidiesexplicit rather than implicit, as is the case with protective customsduties. It is recognized however that administrative capacity and otherdifficulties constrain the extension of explicit subsidies in all but a fewsectors such as steel where the dominance of a large public sector plant(e.g., Chittagong Steel Mills) makes it easier to protect via explicitsubsidies. This implies that customs duties not creditable under the VATwill be required for purposes of protection. It may also be noted thatcustoms duties, in contrast with explicit subsidies, are a source ofrevenue, a consideration that will howvever, assume progressively lessimportance with the growth of domestic production, the revenue elasticityof a VAT and the mission's proposals for raising additional revenue in theshort run presented in Section V below. The proposed separation of customsduties intc those that are primarily revenue-raising and the next and theinclusion of the revenue-raising component into the VAT would however, havethe advantage of weakening the links between industrial policy, of whichproection is an element, and thus allow discussions on promoting efficientindustrialization to be conducted more independently of overall revenueconcerns.

B. IRevnue

1.36 The framework developed in Chapter 4 suggests that tariff reformin the textiles, steel and engineering sectors would lose no more than 1.5percent of annual tax revenue. As against that, the removal of items from

- 20 -

the negative and restricted lists and their free importation subject tosuitably chosen customs duties could generate substantial amounts ofrevenue to the government without significant increases in import volumes.This would reoove the subsidies enjoyed by industrial importers of rawmaterials on the restricted list or the premium enjoyed by commercialimporters. The extent to which this could be absorbed by profit margins asopposed to being passed on to consumers in the form of higher prices willdepend on the structure of the particular industry affected by thesemeasures. While the average scarcity premLum enjoyed by such items hasbeen calculated by an existing study to be 35 percent, the variance forindividual items is large. Revenue estimates would require knowledge ofwhat proportion of imports are allowable under quantitative restrictions aswell as the structure of affected industries. Chapter 3 recommends thatthe reorganized Directorate of Research and Statistics in the NationalBoard of Revenue as well the new office of the Controller of Customs andExcise Valuation be entrusted with collecting such information on scarcitypremia. This will serve as a valuable input into the setting ofappropriate customs duty schedules, and hence, on estimates of resultingrevenue gains.

1.37 The mission has two proposals to make in this area. First, it isrecommended that whenever large scarcity premia arise in the market --examples in FY87 included corrugated iron sheets and second hand clothing-- that the government use the existing instrument of regulatory dutiesmore extensively to transfer to the government the profits otherwisoaccruing to those who acquire the goods at prices lower than those rulingon the market. Second, it is suggested that combined CDST rates on itemsin excess of 75 percent be reviewed by government to ascertain if lowerrates, by reducing evasion, could raise more revenue as well as provideprotection to domestlc industry.

1.38 The above arguments suggest that the revenue constraints on awell-designed package of tariff rationalization may be less important thanis believed to be the case. However, since tariff reform is a continuingprocess which, in the interests of efficiency and export development shouldcover the entire industrial sector, it is necessary to discover domestic-based alternative sources of revenue. Furthermore, as suggested inparagraph 1.35, protection, where deemed appropriate, should be financed bygeneral sources of revenue whenever feasible. Finally, the progressivestrengthening and extension of duty drawback, "in bond' and creditingprocedures recommended by the mlssion will involve losses of revenue:indeed, it is essential to a final goods-based indirect tax system thatsuch losses be adjusted via upward revisions in excise tax rates on finalgoods. For these reasons, the next section outlines a number of proposalsthat could raise significant amounts of revenue within the context of theexisting tax structure.

V. FAISING REVINUK

1. Ezcise TaxatLon

1.39 The mission has examined measures that (1) raise significantamounts of revenue within the existing system; (2) keep exclse rates below25 percent wherever possible so as not to affect the cost structure of

- 21 -

domestically produced internationally traded goods too adversely; (3) focuson final goods as far as possible; (4) do not interfere with progressivityof incidence and (5) concentrate on goods where the administrativesituation is in hand. These proposals could be implemented as soon as theauthorities wanted to do so for revenue-raising purposes.

1.40 The specific packages are described and analyzed in Chapter 2.Package I raises statutory excise rates on a variety of presently excisableitems to around 10 to 15 percent, with the tax on luxury items beingincoeased above the 20 percent range. A second variant of the packageomits the 10 percent tax on tea to examine the distributional consequencesof such a measure. Package 2 includes a tax on edible oils of 15 percentand increases the excise on woollen items (from 5 percent to 15 percent),and mild steel goods and ceramics (from 5 percent and 10 percentrespectively to 20 percent). Again, since the tax on edible oils may beregressive, the estimation of the effects of Package 2 is repeated withoutthe excise tax on edible oil. Package 3 considers the effects of a 20percent uniform tax on all items included in Packages 1 and 2. Allpackages include an excise tax on cigarettes at 230 percent of the ex-factory value.

1.41 The framework used to evaluate those proposals, which is fullydescribed in Chapter 4, traces their impact on (1) prices paid by and realincomes of 10 socio-economic groups8 as a result of excise taxation; (2)income accruing to those groups as a result of changes in factorremuneration generated by such taxation; and (3) revenue raised by thegovernment taking into account the induced effects on CDST revenue viachanges in export competitiveness and import demands. The first twoprovide measures of tax incidence acting via the expenditure and incomesides respectively; the last calculates the net revenue accruing to thegovernment. The analysis of Chapter 2 suggests that these measures couldraise additional net revenue ranging from Tk 1234 million at 1984/85 pricesfor Package 1 to Tk 2625 million at 1984/85 prices for Package 3 and do sowith immediate effect. Turning to incidence, they do not accentuateinequality and have a roughly proportional impact across household groupsin both rural and urban areas. However, the quantitative framework used isdeliberately set up in a way that generates conservative estimates ofrevenue and biases incidence outcomes in the direction of regressivity.Hence, the actual pattern of consumption and tax rate changes can beexpected to bear somewhat less heavily on the poor than the rich.

2. Public Sector Pricing

1.42 An increase in the price of a publicly supplied good is like anincrease in indirect taxation: it will generally increase public revenueand increase prices to the private sector. A complete study of publicrevenues should therefore include an analysis of public sector prices andapply the same principles as used above in the analysis of indirecttaxation. Thus, in line with VAT-type arguments, it is desirable that

8/ The socio-economic groups distinguished by the analysis are: landlessrural, small farmers, medium farmers (tenants), medium farmers(owners), large farmers, largest farmers, rural informal sector, ruralformal sector, urban informal sector and urban formal sector.

- 22 -

prices of publicly produced goods and services to intermediate users, viz.,electricity for industrial uses be guided by social opportunity costs andthat prices to final consumers, viz., electriclty for final salesincorporate a premium over social opportunity costs to reflect the sector'scontribution to domestic resource mobilization. In the case ofnonrenewable resources, the calculation of marginal costs should reflectthe relevant depletion profiles and eventual costs of substitutes.

1.43 The mission did not have the resources to undertake a systematicapplication of the above principles to a wide range of sectors taking intoaccount the need to raise public revenue. However, there are a number ofsectors where the consequences of raising administered prices to marginalcosts of supply have been examined. The IDA Energy Sector Credit missionshave calculated that such price increases in power could yield additionalrevenue increases of the order of Tk 1100 million in FY88 to Tk 11 billionin FY92. The corresponding figures for the gas sector range from anadditional Tk 1700 million in FY88 to Tk 22 billion in FY92. To the extentthat these increases are over and above those assumed in the AnnualDevelopment Program (ADP), their retention by the companies to self-financespecified proportions of their investment program would lead to acorresponding saving in the ADP budget. If, on the other hand, the extrarevenue flows directly to the government, there is an increase in revenue.In either event, it must be noted that these proposals contribute towardsreducing the budget deficit.9

1.44 The Country Economic Memorandum 1987 explored the revenue anddistributional impact of moving current prices to efficiency prices acrossa whole range of sectors. It is estimated that this would yield revenueequivalent to an additional 2 percent of GDP by FY90 with acceptabledistributional consequences.10

3. AjhminLstrgtLon

1.45 The mission has identified several weaknesses in theadministration of taxes in Bangladesh. Chapters 3 and 7 are devoted to adetailed examination of these matters; an outline of the principalrecommendations is provided later in this chapter. Those proposals havethe potential for additional revenue that would justify the costs ofimplementing them.

1.46 This review of excise tax reform, existing estimates of publicsector pricing reform and proposals on replacement of QRs by CDSTs suggeststhat there is enough potential in the economy for replacing tariffs byalternative sources of revenue and hence for moving towards a system whichencourages industrial efficiency and export production, avoids taxation ofinputs and provides for greater elasticity in the response of tax revenueto GDP.

9/ Cf. Bangladesh: Energy Sector Credit, Development Credit Agreement(Yellow Cover; World Bank, July 29, 1987).

10/ Cf. Bangladesh: Promoting Higher Growth and Human Development (WorldBank Report No. 6616-BD. March 10, 1987). The sectors examined werefoodgrains, fertilizer, irrigation, natural gas, power, petroleum,transport, education, health and post offices.

- 23 -

VI. INCOME TAX&TION

1.47 Direct taxation raises less than one-fifth of tax revenue. Withinthis category, income taxes are the most important. Revenue arising fromthe taxation of personal and company income accounts for 15 percent oftotal tax revenue or about 1.2 percent of GDP. The share of the personalincome tax in income tax revenue is roughly one-quarter, the latterimplying that this revenue source accounts for around 0.3 percent of GDP.

1. Personal Income Tax

1.48 The personal income tax combines global income from earned andunearned sources and applies to, it a graduated rate structure. If globalincome exceeds a filing threshold of Tk 36,000, the individual is liablefor taxes, which are calculated as follows. First, the graduated tax ratesare applied to income. The current rate structure has 5 relatively widebrackets, starting at 10 percent for the first Tk 55,000 of taxable incomeand each spanning Tk 55,000 of taxable income to 50 percent for incomeexceeding Tk 220,000. It may be noted that the filing threshold simplysignals the existence of a tax liability which is then computed on thebasis of global income rather than its excess over the filing threshold.11Second, one-third of income in excess of the filing threshold iscalculated. The amount of tax due is the lower of the two figures.

1.49 The basic rules set out above are substantially modified by avariety of exemptions, four of which are cited here.

1 2 First, globalincome for tax purposes excludes certain allowances, such as those forhousing, transport and entertainment, where each type of allowance issubject to a ceiling. Second, upto one-third of global income may bededucted from the tax base, provided the amount is invested in a broadrange of approved assets. Third, interest income upto Tk 15,000 and mostdividend income are exempt from global income for tax purposes.

13 Fourth,capital gains are separated from other sources of income before they aretaxed and are not taxed at all if they are reinvested in approved assets.

1.50 The tax provisions described above imply that a salary earner witha basic salary of Tk 36 000, a (tax-deductible) housing-cum-transportationallowance of Tk 24,000,4 ;and a consequent gross income of Tk 60,000 - afigure almost 2h times average family income, has no income tax liability.For gross income between Tk 60,000 and Tk 83,000, the tax is computedaccording to the one-third rule, or the second method outlined in paragraph1.48. This results in a marginal tax rate of 22.2 percent rather than 10perrent (the lowest slab in the graduated rate structure).

15 Grossincomes between Tk 83,000 and Tk 292,000 attract tax liability according to

11/ For this reason, the mission has chosen to use the term "filingthreshold" rather than a more conventional "exemption limit."

12/ The complete list is presented in Chapter 5.

13/ All interest income has been subject to a Jamuna bridge surcharge at 4percent since October 1985; a flood relief levy at 4 percent applicableto interest and dividends for the period upto June 30, 1988, was addedin September 1987.

14/ This comprises a housing allowance of Tk 18,000 (50 percent of basicsalary) and a transportation allowance of Tk 6,000.

- 24 -

the graduated rate structure. Incomes exceeding Tk 292,000 are, onceagain, subject to the one-third rule.

1.51 The mission is of the view that the combination of a highexemption level, relatively low marginal tax rates and generous specialincentives make the personal income tax system far more generous than thatof other countries in the region. The picture of tax liability constructedabove does not, however, take into account the fact that individuals with acombination of salary and capital income can reduce their tax liabilitiesfurther. Of particular concern is the revenue loss that occurs becausetaxpayers can lower their liability first by the deduction allowed forapproved investments, and subsequeotly by paying no taxes on capital incomeaccruing from those investments.16 This is confirmed by inspection of asample of returns supplied by the NBR which show a pattern in which littleinvestment income is reported, and yet investment deductions areextensively used. This "double allowance" seriously impairs the equity ofthe income tax system, since capital income is more important for wealthiertaxpayers. Subsidizing a source of income which accrues almost exclusivelyto the highest income groups sharply reduces the progressivity of the tax.Furthermore, wealthier taxpayers can more fully utilize this doubleallowance, since the exemption limit for allowable investments, defined asa fixed proportion of income, is greater for higher income groups.

1.52 The mission's recommendations on reform of personal income taxpolicy are governed by the need to broaden the base of the tax in order toraise revenue, improve equity and remove anomalies that can adverselyaffect incentives and tax compliance. The proposals presented below aremutually reinforcing and therefore need to be viewed as a policy package.These changes could be introduced soon and would serve to enhance the roleof personal income taxation in the tax system.