Embed Size (px)

Citation preview

VTB BANK

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR’S REPORT

FOR THE YEAR ENDED 31 DECEMBER 2020

VTB BANK CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR’S REPORT

2

CONTENTS

INDEPENDENT AUDITOR’S REPORT ............................................................................................................... 3

CONSOLIDATED INCOME STATEMENT ................................................................................................................ 12CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME ......................................................................... 13CONSOLIDATED STATEMENT OF FINANCIAL POSITION ................................................................................... 14CONSOLIDATED STATEMENT OF CASH FLOWS ................................................................................................ 15CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY .................................................... 17

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1. Principal Activities ................................................................................................................................................................ 18 2. Basis of Preparation ............................................................................................................................................................ 18

DELVING INTO NUMBERS

3. Analysis by Segment .................................................. 204-17. Notes to Income Statements ...................................... 2818-38. Notes to Statements of Financial Position .................. 35

RISK

39. Significant Accounting Estimates and Judgments ...... 6540. Operating Environment of the Group .......................... 6741. Financial Risk Management ....................................... 6842. Fair Value Measurement ............................................ 8743. Capital Management and Capital Adequacy ............ 102

GROUP STRUCTURE

44. Composition of the Group ......................................... 10445. Changes in Group structure ....................................... 10546. Investments in Associates and Joint Ventures .......... 10647. Non-controlling Interest............................................. 10948. Interests in Structured Entities .................................. 110

OFF BALANCE-SHEET ITEMS

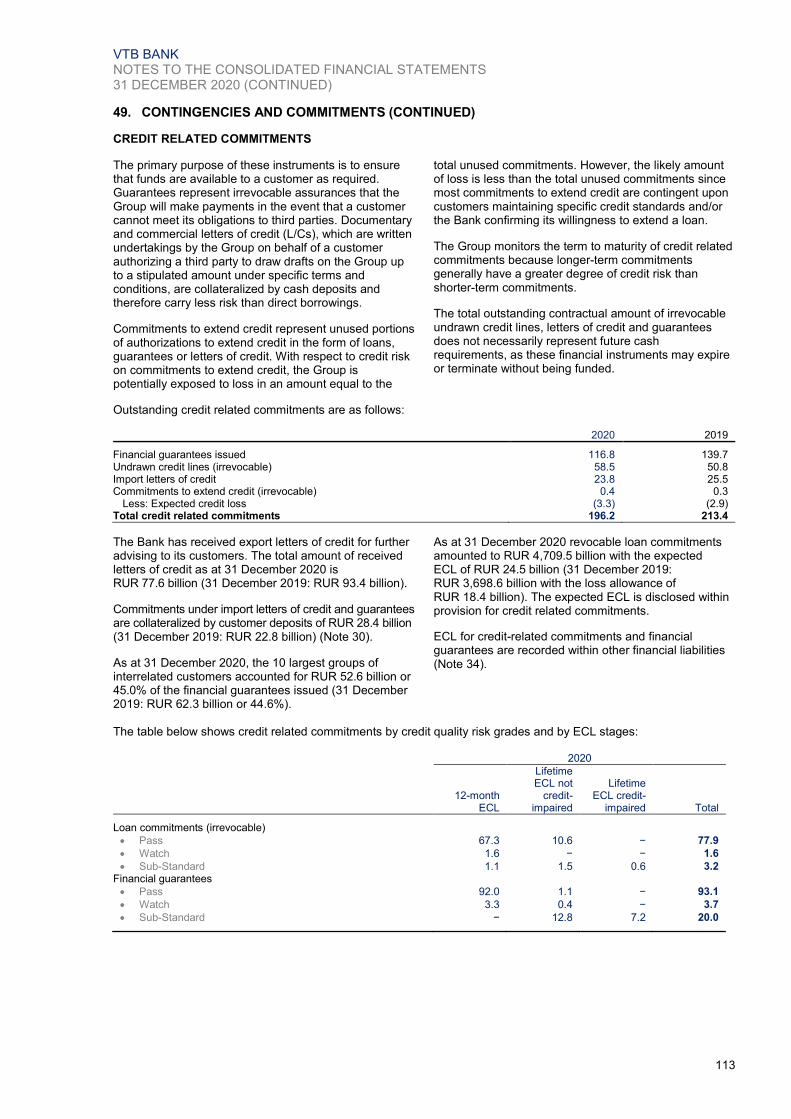

49. Contingencies and Commitments............................. 11250. Subsequent Events .................................................. 115

OTHER INFORMATION

51. Related Party Transactions ................................................................................................................................................ 11752. Offsetting of Financial Instruments ..................................................................................................................................... 11953. Share-Based Payments ..................................................................................................................................................... 12054. Basic and Diluted Earnings per Share ............................................................................................................................... 12155. Transfers of Financial Assets and Assets Held or Pledged as Collateral ............................................................................ 12156. Summary of Principal Accounting Policies ......................................................................................................................... 12357. New and Revised Standards ............................................................................................................................................. 13858. New Accounting Pronouncements ..................................................................................................................................... 13959. Changes in Presentation and Correction ........................................................................................................................... 139

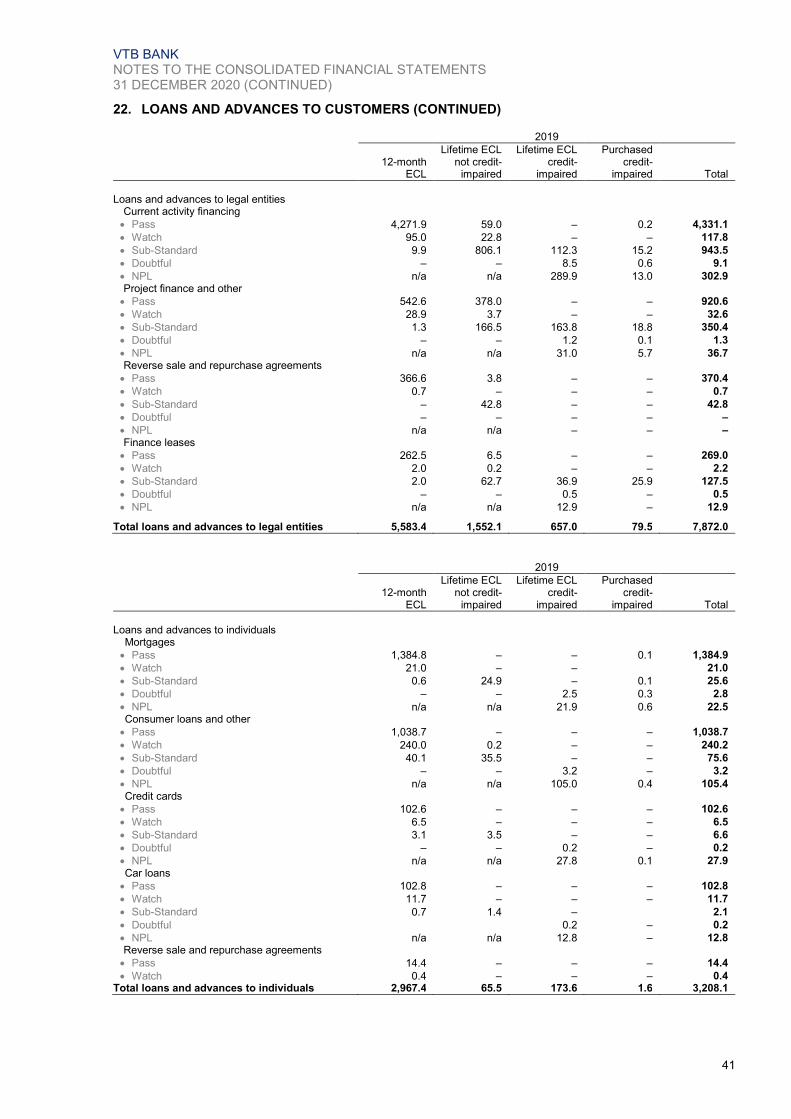

3 A member firm of Ernst & Young Global Limited

ErnstС&СYoungСLLC SadovnicheskayaСNab.тС77тСbld.С1 MoscowтС115035тСRussia Tel: с7Со495)С705С9700 с7Со495)С755С9700 Fax: с7Со495)С755С9701 www.ey.com/ru

С«Э Сэ С » иятС115035тС С

ич яС .тС77тС .С1 .: +7 (495) 705 9700

+7 (495) 755 9700 Ф : +7 (495) 755 9701

К : 59002827 Г : 1027739707203

И : 7709383532

Independent auditor’s report To the Shareholders and Supervisory Council of VTB Bank (public joint-stock company) Report on the audit of the consolidated financial statements

Opinion

We have audited the consolidated financial statements of VTB Bank (public joint-stock company) оhereinafterтСtheС“Bank”)СandСitsСsubsidiariesСоhereinafterтСtheС“Group”)тСwhichСcompriseСtheСconsolidated income statement and consolidated statement of comprehensive income for the year ended 31 December 2020, the consolidated statement of financial position as of 31 December 2020тСtheСconsolidatedСstatementsСofСcashСflowsСandСchangesСinСshareholders’Сequity for the year ended 31 December 2020, and notes to the consolidated financial statements, including a summary of significant accounting policies. In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Group as of 31 December 2020 and its consolidated financial performance and consolidated cash flows for the year then ended in accordance with International Financial Reporting Standards (IFRSs). Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (ISAs). Our responsibilities under those standards are further described in the Auditor’s responsibilities for the audit of the consolidated financial statements section of our report. We are independent ofСtheСGroupСinСaccordanceСwithСtheСInternationalСEthicsСStandardsСBoardСforСAccountants’ (IESBA) International Code of Ethics for Professional Accountants (including International Independence Standards) (IESBA Code) together with the ethical requirements that are relevant to our audit of the consolidated financial statements in the Russian Federation, and we have fulfilled our other ethical responsibilities in accordance with these requirements and the IESBA Code. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion. Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements of the current period. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. For each matter below, our description of how our audit addressed the matter is provided in that context.

4 A member firm of Ernst & Young Global Limited

We have fulfilled the responsibilities described in the Auditor’s responsibilities for the audit of the consolidated financial statements section of our report, including in relation to these matters. Accordingly, our audit included the performance of procedures designed to respond to our assessment of the risks of material misstatement of the consolidated financial statements. The results of our audit procedures, including the procedures performed to address the matters below, provide the basis for our audit opinion on the accompanying consolidated financial statements. Key audit matter How our audit addressed the key audit matter

Expected credit losses for loans and advances to customers and provision for credit related

commitments

Given the significance of the expected credit losses for loans and advances to customers and provision for creditСrelatedСcommitmentsСtoСtheСGroup’sСfinancial position, the complexity and judgements related to the estimation of expected credit losses under IFRS 9 Financial Instruments о“IFRSС9”)тСweСconsidered this area as a key audit matter.

Assessment on an individual and a portfolio basis of whether a significant increase in credit risk has occurred since initial recognition, as well as calculationСofСexpectedСcreditСlossesСо“ECL”)тСrequire judgement. Determination of whether an increase in credit risk has occurred is based on relative change in credit ratings, days past due and other objective and subjective factors. Selection of thresholds used to conclude that the increase in credit risk is significant, such as the extent of the downgrade in a credit rating, is also judgemental.

The calculation of ECL involves estimation techniques that use significant unobservable inputs and factors, such as internal credit ratings, complex statistical modelling and expert judgement. These techniques are used to determine probability of default, projected exposure at default and loss arising at default, based on available historical data and external information, which is adjusted for forward looking information, including forecast of macroeconomic variables.

The calculation of expected credit losses for significant credit-impaired financial assets on an individual basis requires analysis of financial and non-financial information and extensive use of assumptions. Assessment of estimated future cash flows is based on significant unobservable inputs, such as current and projected financial performance of the borrower, collateral value, and estimation of probabilities of possible outcomes. The use of different modelling techniques, assumptions and forecasts could produce significantly different estimates of the allowance for expected credit losses.

We focused our audit on the following:

• evaluating credit risk models and assumptions used to estimate key provisioning parameters, and determine expected credit losses on a portfolio basis;

• assessingСmanagement’sСjudgementСinСrelation to the identification of significant increases in credit risk on an individual and portfolio basis based on quantitative and qualitative criteria;

• testing estimated future cash flows, including collateral-sourced cash flows, in relation to significant credit-impaired loans and advances to customers and credit related commitments;

• assessing management’sСjudgementСinСrelationСto the evaluation of the effect of current economic situation related to COVID-19 pandemic on ECL calculation.

Our audit procedures included evaluation of expected credit loss methodology developed by the Group in accordance with the requirements of IFRS 9 to calculate the expected credit losses for loans and advances to customers and provision for credit related commitments.

We assessed the reasonableness of the credit risk factors and thresholds selected by the management to determine whether significant increase in credit risk has occurred on individual and portfolio basis. We evaluated consistency of application of the criteria selected by the management as of the reporting date. We analysed the information about the transfer of certain borrowers, most influenced by the COVID-19СpandemicтСfromС“12-monthСECL”СtoС“LifetimeСECLСnotСcredit-impaired”.

5 A member firm of Ernst & Young Global Limited

Key audit matter How our audit addressed the key audit matter

During 2020 in the current economic conditions, connected with COVID-19 pandemic and its influence on global and Russian economy, the Group reassessed the macroeconomic variables incused for ECL calculation; increased weighted estimates of credit losses for certain industries for the purpose of assessment on portfolio basis; transferredСcertainСborrowersСfromС“12-monthСECL” toС“LifetimeСECLСnotСcredit-impaired”;СdowngradedСcredit ratings for certain major borrowers assessed on an individual basis.

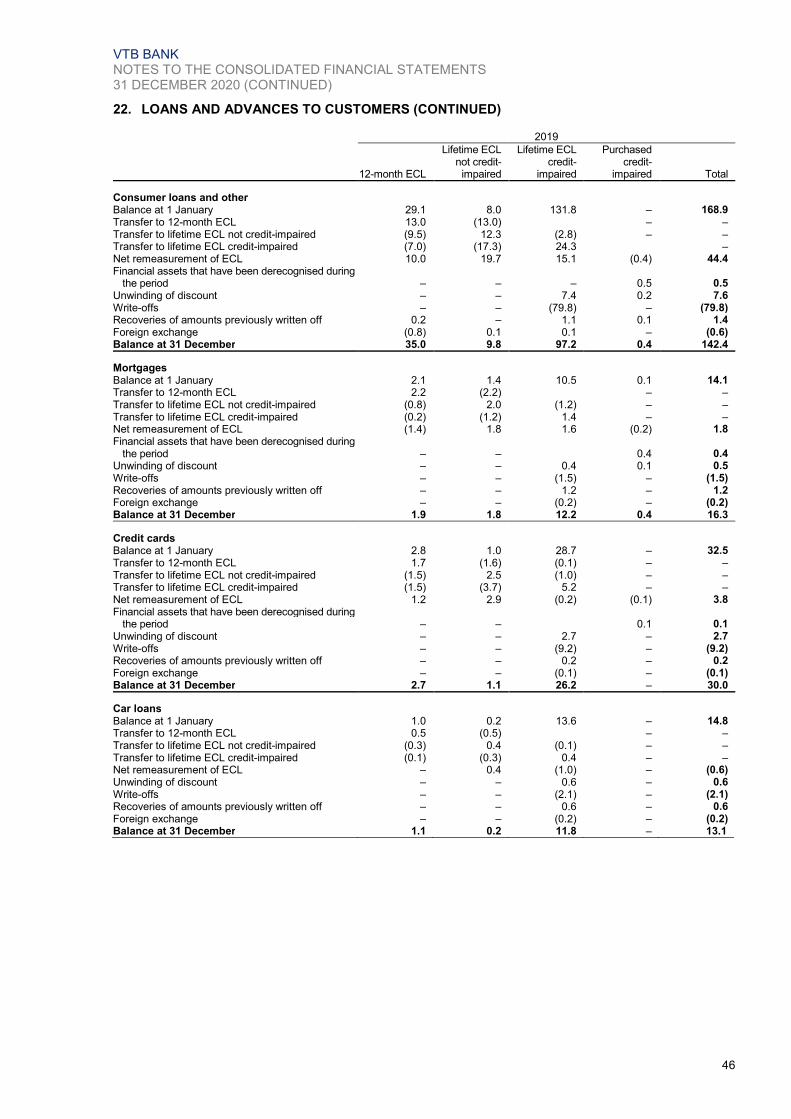

Information on the allowance for expected credit losses on loans and advances to customers and provision for credit related commitments is included in Note 22, Loans and advances to customers, Note 41, Financial risk management, and Note 49, Contingencies and commitments, to the consolidated financial statements.

To test allowance calculated on a portfolio basis, we evaluated underlying statistical models, key inputs and assumptions used and assessed incorporation of forward-looking information in the calculation of expected credit losses. For significant credit exposures, we evaluated, on a sample basis, internal credit ratings, credit risk factors and staging. We focused on the analysis ofСtheСGroup’sСapproach to assessment of the macroeconomic variables, including the effect of COVID-19 pandemic, on the forecasted economic information. We have also considered the results of retrospective testing of the IFRS 9 models performed by the Group.

For a sample of significant credit-impaired corporate exposures, we, together with our valuation specialists, challenged assumptions on estimated future cash flows, including value of collateral and probabilities of expected outcomes. We focused on the calculation of ECL for those borrowers that were most affected by current economic deterioration caused by COVID-19 pandemic.

We also assessed the disclosures in the consolidatedСfinancialСstatementsСaboutСtheСGroup’sСallowance for expected credit losses on loans and advances to customers and provision for credit related commitments.

Valuation of land, premises, investment property and property intended for sale in the ordinary course

of business

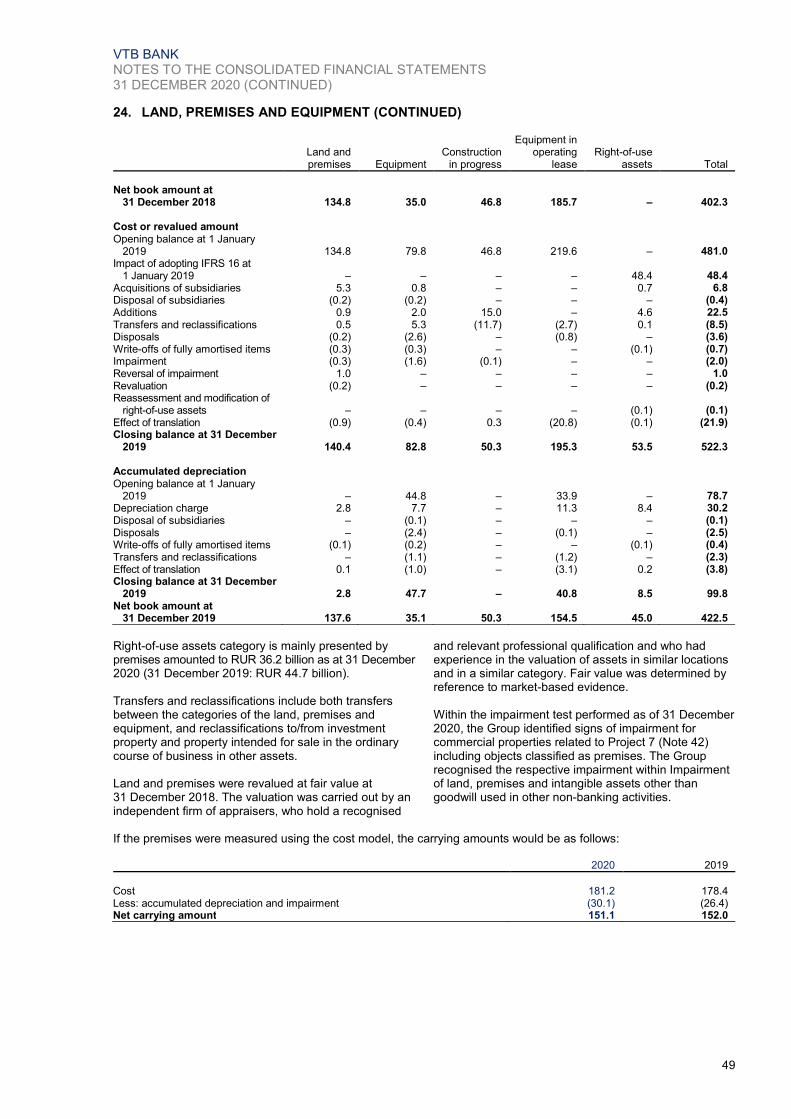

TheСGroup’sСaggregateСcarryingСvalueСofСlandтСpremises, investment property and property intended for sale in the ordinary course of business was RUR 261.5 billion at 31 December 2020. The Group determines the value of these assets with the assistance of independent or internal valuation specialists. The valuation models prepared by these specialists contain unobservable inputs and assumptions. Changes in these inputs and assumptions may have a significant impact on the valuation. The significance and subjectivity of these valuations make them a key audit matter.

In 2020 due to the deterioration of current economic situation, caused by COVID-19 pandemic, and the subsequent decline in business activity and purchasingСpowerСofСtheСGroup’sСcounterpartiesтСthe Group impaired certain items of land, premises, investment property and property intended for sale in the ordinary course of business. The amount of impairment recognised in 2020 comprised RUR 113.6 billion.

Our audit procedures included an assessment, on a sample basis, of the valuation methods and models as well as the sources of significant assumptions. We also tested the determination of the net realizable value of a sample of individually significant properties intended for sale in the ordinary course of business. We focused on the management’sСjudgementsСrelated to the effect of deterioration of current economic situation on the valuation of these assets.

Where management involved a valuation specialist, we assessed their qualification and objectivity. For a sample of individually significant properties, we involved our valuation specialists to assist us in assessing the reasonableness of the methodology andСassumptions.СWeСalsoСassessedСtheСGroup’sСdisclosures in relation to the valuation of land, premises and investment property.

6 A member firm of Ernst & Young Global Limited

Key audit matter How our audit addressed the key audit matter

Information on the valuation of land, premises, investment property and property intended for sale in the ordinary course of business is included in Note 24, Land, premises and equipment, Note 25, Investment property, Note 27, Other assets, and Note 42, Fair value measurement, to the consolidated financial statements.

Valuation of financial instruments not quoted in active market

Financial instruments not quoted in an active market (instruments in Level 2 and Level 3 of the fair value hierarchy) represent a significant part of theСGroup’sСinvestmentsСinСsecuritiesСandСderivatives, due from other banks and loans and advances to customers at fair value through profit or loss.

The fair value of these instruments is determined by internally developed valuation models that may use complex assumptions and unobservable inputs. The significance and subjectivity of these valuations make them a key audit matter.

Information on the valuation of financial instruments not quoted in an active market is included in Note 42, Fair value measurement, to the consolidated financial statements.

Our audit procedures included an assessment, on a sample basis, of internally developed models and the sources of significant assumptions used in determining fair value. For a sample of individually significant instruments, we inspected, with assistance of our valuation specialists, the models and assumptions used, and/or performed an independent valuation assessment using alternative valuation methods and assumptions. We also assessedСtheСGroup’sСdisclosuresСinСrelationСtoСtheСvaluation of such financial instruments, including disclosures regarding significant Level 3 inputs used and sensitivity of the value to changes in these inputs.

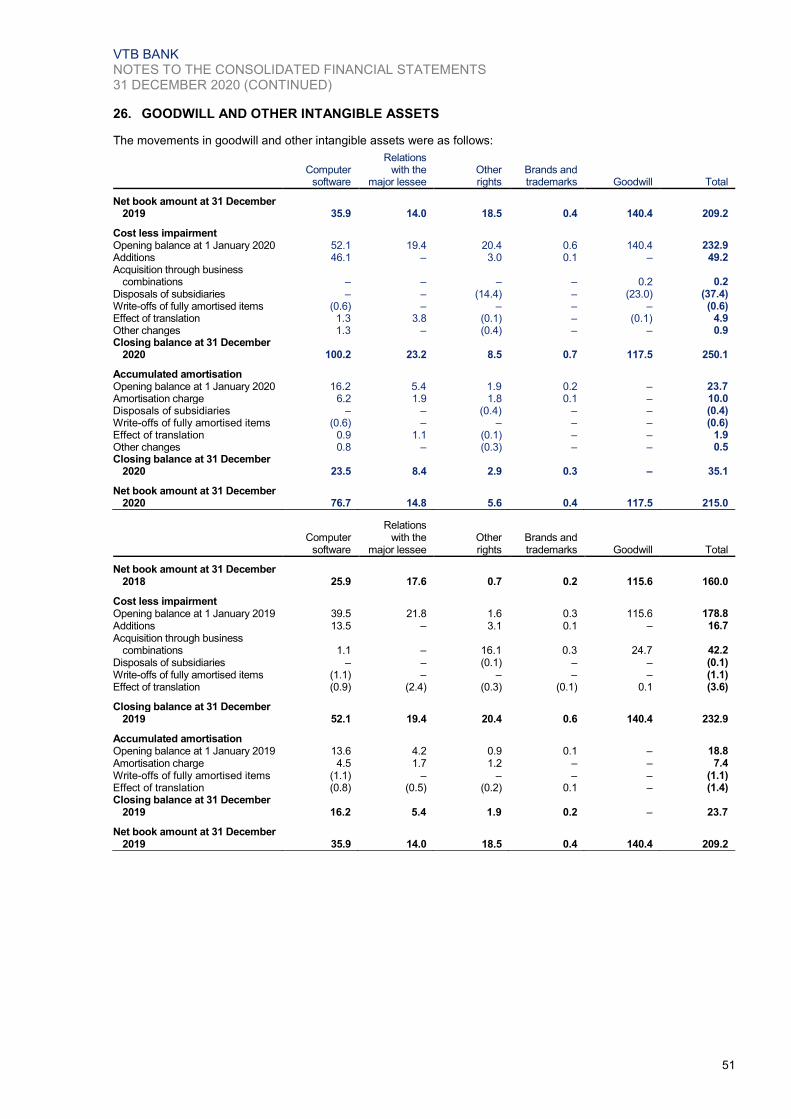

Goodwill impairment

Impairment of goodwill is a key audit matter due to both the significance of its carrying value and the judgement inherent in the impairment testing. Management has to use significant unobservable inputs and make assumptions in their goodwill impairment analysis to develop cash flow forecasts, and to determine appropriate growth rates and discount rates.

The use of different modelling techniques and assumptions could have significant impact on the outcome of the impairment testing.

Current economic deterioration, connected with COVID-19 pandemic, influenced the factors and assumptions used for cash flow forecasts.

Information on goodwill is included in Note 26, Goodwill and other intangible assets, to the consolidated financial statements.

We assessed, with the assistance of our business valuation specialists, management’sСgoodwillСimpairment analysis, including calculations of carrying values and recoverable amounts of cash-generating units. We evaluated forecasted cash flows, discount rates and long-term growth rates, by comparing them with the historical operating performance, business plans, market indicators and other available evidence. We focused on the analysis of assumptions updated for the current economic situations, which were used as a basis for cash flow forecasts. We assessed the disclosure prepared by the Group in relation to the results of testing.

7 A member firm of Ernst & Young Global Limited

Other information included in VTB Annual Report 2020

Other information consists of the information included in the VTB Annual Report 2020 оhereinafterтСtheС“AnnualСReport”)СotherСthanСtheСconsolidatedСfinancialСstatementsСandСourСauditor’sСreportСthereon.СManagementСisСresponsibleСforСtheСotherСinformation.СThe Annual Report is expected to be made available to us after the date of this auditor’sСreport.С Our opinion on the consolidated financial statements does not cover the other information and we will not express any form of assurance conclusion thereon. In connection with our audit of the consolidated financial statements, our responsibility is to read the other information identified above when it becomes available and, in doing so, consider whether the other information is materially inconsistent with the consolidated financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. Responsibilities of management and the Audit Committee for the consolidated financial

statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with IFRSs, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. In preparing the consolidated financial statements, management is responsible for assessing the Group’sСabilityСtoСcontinueСasСaСgoingСconcernтСdisclosingтСasСapplicableтСmattersСrelatedСtoСgoingСconcern and using the going concern basis of accounting unless management either intends to liquidate the Group or to cease operations, or has no realistic alternative but to do so. TheСAuditСCommitteeСisСresponsibleСforСoverseeingСtheСGroup’sСfinancialСreportingСprocess.

Auditor’s responsibilities for the audit of the consolidated financial statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and toСissueСanСauditor’sСreportСthatСincludes our opinion. Reasonable assurance is a high level of assurance but is not a guarantee that an audit conducted in accordance with ISAs will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

8 A member firm of Ernst & Young Global Limited

As part of an audit in accordance with ISAs, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

► Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

► Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressingСanСopinionСonСtheСeffectivenessСofСtheСGroup’sСinternalСcontrol.

► Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

► ConcludeСonСtheСappropriatenessСofСmanagement’sСuseСofСtheСgoingСconcernСbasisСofСaccounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditionsСthatСmayСcastСsignificantСdoubtСonСtheСGroup’sСabilityСto continue as a going concern. If we conclude that a material uncertainty exists, we are requiredСtoСdrawСattentionСinСourСauditor’sСreportСtoСtheСrelatedСdisclosuresСinСtheСconsolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor’sСreport.СHoweverтСfutureСeventsСorСconditionsСmayСcauseСtheСGroupСtoСceaseСtoСcontinue as a going concern.

► Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

► Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with the Audit Committee regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit. We also provide the Audit Committee with a statement that we have complied with relevant ethical requirements regarding independence and communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, actions taken to eliminate threats or safeguards applied.

9 A member firm of Ernst & Young Global Limited

From the matters communicated with the Audit Committee, we determine those matters that were of most significance in the audit of the consolidated financial statements of the current period and are thereforeСtheСkeyСauditСmatters.СWeСdescribeСtheseСmattersСinСourСauditor’sСreportСunless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication. Report in accordance with the requirements of Article 42 of the Federal Law of the Russian

Federation No. 395-1 Concerning Banks and Banking Activities of 2 December 1990

Management of the Bank is responsible for the compliance of the Banking group, where the Bank isСtheСparentСcreditСinstitutionСоhereinafterтСtheС“BankingСgroup”)СwithСtheСmandatoryСprudentialСratiosСestablishedСbyСtheСCentralСBankСofСtheСRussianСFederationСоhereinafterтСtheС“BankСofСRussia”) and for the conformity of internal control and organization of the risk management systems of the Banking group with the requirements set forth by the Bank of Russia in respect of such systems. In accordance with the requirements of Article 42 of the Federal Law of the Russian Federation No. 395-1 Concerning Banks and Banking Activities of 2 December 1990 (hereinafter, the “FederalСLaw”)тСduringСtheСauditСofСtheСGroup’sСconsolidatedСfinancialСstatementsСforСtheСyearСended 31 December 2020, we determined:

1) Whether the Banking group complied as of 1 January 2021 with the obligatory ratios established by the Bank of Russia;

2) Whether internal control and organization of the risk management systems of the Banking group conformed to the requirements set forth by the Bank of Russia for such systems in respect of the following:

• subordination of the risk management departments;

• theСexistenceСofСmethodologiesтСapprovedСbyСtheСBank’sСrespectiveСauthorizedСbodiesтСfor detecting and managing risks that are significant to the Bank and for performing stress-testing; the existence of a reporting system at the Bank pertaining to its significant risks and capital;

• consistency in applying and assessing the effectiveness of methodologies for managing risks that are significant to the Bank;

• oversight performed by the Supervisory Council and executive management of the BankСinСrespectСofСtheСBank’sСcomplianceСwithСriskСlimitsСandСcapitalСadequacyСrequirementsСsetСforthСinСtheСBank’sСinternalСdocumentsтСandСeffectivenessСandСconsistencyСofСtheСapplicationСofСtheСBank’sСriskСmanagementСprocedures.

This work included procedures selected based on our judgment, such as inquiries, analysis, reading of documents, comparison of the requirements, procedures and methodologies approved by the Bank with the requirements set forth by the Bank of Russia, and the recalculation, comparison and reconciliation of numerical values and other information. The findings from our work are provided below.

10 A member firm of Ernst & Young Global Limited

Compliance by the Banking group with the obligatory ratios established by the Bank of

Russia

We found that the values of the obligatory ratios of the Banking group as of 1 January 2021 were within the limits established by the Bank of Russia. We have not performed any procedures in respect of accounting data of the Banking group, except for those procedures we considered necessary to express our opinion on the fair presentation of the Group’sСconsolidatedСfinancialСstatements.С Conformity of internal control and organization of the risk management systems of the

Banking group with the requirements set forth by the Bank of Russia in respect of such

systems

• We found that, in accordance with the legal acts and recommendations issued by the Bank

of Russia, as of 31 December 2020 the Bank’s internal audit division was subordinated and accountableСtoСtheСSupervisoryСCouncilтСandСtheСBank’sСriskСmanagement departments were not subordinated or accountable to the departments that take the relevant risks.

• WeСfoundСthatСtheСBank’sСinternalСdocumentsСeffectiveСasСof 31 December 2020 that establish the methodologies for detecting and managing credit, market, operational, and liquidity risks that are significant to the Banking group and stress-testing have been approvedСbyСtheСBank’sСauthorizedСbodiesСinСaccordanceСwithСtheСlegalСactsСandСrecommendations issued by the Bank of Russia. We also found that, as of 31 December 2020, the Bank had a reporting system pertaining to credit, market, operational and liquidity risks that were significant to the Banking group and pertaining to its capital.

• We found that the frequency and consistency of reports prepared byСtheСBank’sСriskСmanagement departments and internal audit division during the year ended 31 December 2020 with regard to the management of credit, market, operational and liquidity risks of theСBankingСgroupСcompliedСwithСtheСBank’sСinternalСdocumentsтСand that those reports includedСobservationsСmadeСbyСtheСBank’sСriskСmanagementСdepartmentsСandСinternalСauditСdivision in respect of the effectiveness of relevant risk management methodologies.

• We found that, as of 31 December 2020, the authority of the Supervisory Council and executive management bodies of the Bank included control over compliance of the Banking group with internally established risk limits and capital adequacy requirements. For the purpose of control over the effectiveness and consistency of the risk management procedures applied by the Banking group during the year ended 31 December 2020, the Supervisory Council and executive management bodies of the Bank regularly reviewed the reportsСpreparedСbyСtheСBank’sСriskСmanagementСdepartments and internal audit division.

VTB BANK CONSOLIDATED INCOME STATEMENT FOR THE YEAR ENDED 31 DECEMBER (IN BILLIONS OF RUSSIAN ROUBLES)

The notes № 1-59 form an integral part of these consolidated financial statements. 12

Note 2020 2019 Change

Interest income calculated using the effective interest method 4 974.3 1,039.8 -6.3% Other interest income 4 81.5 67.2 21.3% Interest expense 4 (501.6) (636.5) -21.2% Payments to deposit insurance system 4 (22.5) (29.9) -24.7% Net interest income 4 531.7 440.6 20.7%

Provision charge for credit losses on debt financial assets 21, 22, 23 (227.0) (92.2) 146.2% Net interest income after provision for credit losses 304.7 348.4 -12.5%

Net fee and commission income 5, 59 136.8 121.6 12.5%

(Losses net of gains) / gains net of losses arising from sale and

revaluation of loans at fair value through profit or loss (3.1) 3.3 -193.9% Gains net of losses arising from other financial instruments at fair value

through profit or loss 6 32.8 63.1 -48.0% Gains net of losses arising from sale of financial assets at fair value

through other comprehensive income 7 0.8 1.0 -20.0% Gains net of losses / (losses net of gains) arising from foreign currencies

and precious metals 8, 59 18.9 (35.5) 153.2% Gains net of losses arising from disposal of financial assets at amortised

cost 1.4 9.1 -84.6% Other gains net of losses on financial instruments at amortised cost 0.7 0.2 250.0% Share in profit of associates and joint ventures 17.3 11.1 55.9% Impairment of investments in associates 46 (12.8) – n/a Gains from disposal of subsidiaries and associates 28, 45, 46 6.1 7.5 -18.7% Losses net of gains arising from extinguishment of liabilities (0.2) – n/a Provision charge for credit losses on credit related commitments and

other financial assets 27, 49 (19.9) (7.8) 155.1% Provision charge for legal claims and other commitments 49 (2.9) (3.3) -12.1% Excess of fair value of acquired net assets over cost – 5.6 -100.0% Other operating income 9 9.2 7.5 22.7% Non-interest gains 48.3 61.8 -21.8%

Revenue and other gains from operating lease of equipment 10 30.3 30.5 -0.7% Expenses related to equipment leased out 10 (17.3) (15.1) 14.6% Revenues less expenses from operating leasing 10 13.0 15.4 -15.6%

Net insurance premiums earned from non-state pension fund activity 13 14.1 40.8 -65.4% Net insurance claims incurred, movement in liabilities to policyholders

and acquisition costs on non-state pension fund activity 14 (30.0) (60.5) -50.4% Revenues less expenses from non-state pension fund activity (15.9) (19.7) -19.3%

Revenue and other gains from other non-banking activities 11 102.6 96.9 5.9% Cost of sales and other expenses from other non-banking activities 12, 59 (92.7) (87.0) 6.6% Expenses from write-down of property held for sale in the ordinary

course of business 59 (9.6) (6.2) 54.8% Impairment of land, premises and intangible assets other than goodwill

used in non-banking activities 24, 26 (17.0) (1.1) 1,445.5% Net loss from change in fair value of investment property recognised on

revaluation or disposal 25, 42 (87.0) (0.9) 9,566.7% Revenues less expenses from other non-banking activities (103.7) 1.7 -6,200.0%

(Impairment)/reversal of impairment of land, premises and intangible

assets other than goodwill 24, 26 (0.2) 0.1 -300.0% Other operating expense 15, 59 (23.4) (22.2) 5.4% Staff costs and administrative expenses 16 (269.9) (254.2) 6.2% Non-interest expenses (293.5) (276.3) 6.2%

Profit before tax 89.7 252.9 -64.5% Income tax expense 17 (14.4) (51.7) -72.1% Net profit 75.3 201.2 -62.6%

Net profit/(loss) attributable to: Shareholders of the parent 80.6 202.0 -60.1% Non-controlling interests (5.3) (0.8) 562.5%

Basic and diluted earnings per share (expressed in Russian roubles per share) 54 0.00503 0.01453 -65.4%

VTB BANK CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE YEAR ENDED 31 DECEMBER (IN BILLIONS OF RUSSIAN ROUBLES)

The notes № 1-59 form an integral part of these consolidated financial statements. 13

2020 2019

Net profit 75.3 201.2

Other comprehensive income/(loss): Other comprehensive income/(loss) to be reclassified to profit or loss in

subsequent periods: Net change in fair value of debt financial assets at fair value through other comprehensive

income, net of tax 8.6 7.4 Reclassification of gains to income statement on sale of debt financial assets at fair value

through other comprehensive income, net of tax (0.7) (0.7) Cash flow hedges, net of tax – 0.1 Share of other comprehensive income/(loss) of associates and joint ventures 4.3 (2.0) Effect of translation, net of tax 27.9 (21.2) Total other comprehensive income/(loss) to be reclassified to profit or loss in

subsequent periods 40.1 (16.3)

Other comprehensive income/(loss) not to be reclassified to profit or loss in

subsequent periods: Net change in fair value of equity financial assets at fair value through other

comprehensive income, net of tax 0.6 2.0 Actuarial losses net of gains arising from difference between pension plan assets and

obligations – (0.1) Land and premises revaluation, net of tax 0.1 (0.3) Total other comprehensive income not to be reclassified to profit or loss in

subsequent periods 0.7 1.6

Other comprehensive income/(loss), net of tax 40.8 (14.7)

Total comprehensive income 116.1 186.5 Total comprehensive income/(loss) attributable to: Shareholders of the parent 120.8 186.2 Non-controlling interests (4.7) 0.3

VTB BANK CONSOLIDATED STATEMENT OF CASH FLOWS FOR THE YEAR ENDED 31 DECEMBER (IN BILLIONS OF RUSSIAN ROUBLES)

The notes № 1-59 form an integral part of these consolidated financial statements. 15

Note 2020 2019

Cash flows from/(used in) operating activities Interest received 1,001.4 1,081.2 Interest paid (516.1) (649.7) Payments to deposit insurance system (24.6) (28.2) Gains on operations with trading financial assets 20.2 65.1 Gains/(losses)/gains incurred on dealing in foreign currency 59 6.7 (106.4) Fees and commissions received 59 191.4 169.9 Fees and commissions paid 59 (58.3) (55.2) Other operating income received 11.1 6.6 Other operating expenses paid 59 (22.1) (12.1) Revenue received from operating lease of equipment 19.0 28.4 Expenses paid related to equipment leased out (2.1) (4.8) Net insurance premiums received from non-state pension fund activity 14.0 40.7 Net insurance claims paid on non-state pension fund activity (2.9) (3.4) Revenue received from non-banking activities 78.7 101.1 Expenses paid related to non-banking activities (57.0) (87.7) Staff costs, administrative expenses paid (229.1) (227.3) Income tax paid (46.8) (53.4) Cash flows from operating activities before changes in operating assets and

liabilities 383.5 264.8

Net decrease/(increase) in operating assets Net increase in mandatory cash balances with central banks (9.8) (15.7) Net decrease/(increase) in correspondent accounts in precious metals 13.1 (2.9) Net increase in trading financial assets (126.0) (147.9) Net (increase)/decrease in due from other banks (204.6) 53.2 Net increase in loans and advances to customers (1,102.5) (319.5) Net increase in other assets (61.2) (129.4) Net (decrease)/increase in operating liabilities Net decrease in due to other banks (184.5) (200.2) Net increase in customer deposits 1,145.1 845.5 Net (decrease)/increase in debt securities issued other than bonds issued (20.3) 3.8 Net increase in other liabilities 8.4 17.8 Net cash (used in)/from operating activities (158.8) 369.5

Cash flows from/(used in) investing activities Dividends and other distributions received 10.8 10.7 Proceeds from redemption and sale of investment financial assets 214.3 341.4 Purchase of investment financial assets (827.1) (257.5) Purchase of subsidiaries, net of cash 0.3 (32.1) Disposal of subsidiaries, net of cash disposed 45 0.4 3.7 Acquisition and other contributions of shares in associates and joint ventures 46 (73.1) (39.1) Proceeds from sale of shares in associates and other distributions 80.1 0.3 Purchase of land, premises and equipment (64.3) (17.4) Proceeds from sale of land, premises and equipment 2.3 1.1 Purchase or construction of investment property (2.8) (6.6) Proceeds from sale of investment property 19.2 12.2 Purchase of intangible assets (47.6) (14.7) Proceeds from sale of intangible assets 0.2 0.1 Net cash (used in)/from investing activities (687.3) 2.1

VTB BANK CONSOLIDATED STATEMENT OF CASH FLOWS (CONTINUED) FOR THE YEAR ENDED 31 DECEMBER (IN BILLIONS OF RUSSIAN ROUBLES)

The notes № 1-59 form an integral part of these consolidated financial statements. 16

Note 2020 2019

Cash flows from/(used in) financing activities Dividends paid 38 (26.7) (31.1) Proceeds, net of repayment, from short-term local bonds issued – (13.6) Proceeds from local bonds issued 108.3 125.9 Repayment of local bonds (158.5) (16.3) Buy-back of local bonds (2.5) (12.0) Proceeds from sale of previously bought-back local bonds 0.1 0.6 Repayment of Eurobonds (66.2) – Buy-back of Eurobonds (5.6) (6.7) Proceeds from sale of previously bought-back Eurobonds 5.8 6.0 Repayment of syndicated loans (1.4) (1.6) Proceeds from other borrowings and funds from local central banks 1,773.2 402.6 Repayment of other borrowings and funds from local central banks (1,122.8) (394.0) Repayments of lease liabilities (6.3) (10.6) Proceeds from subordinated debt 74.6 20.0 Repayment of subordinated debt (3.0) (0.5) Purchase of shares in subsidiaries from non-controlling interests (0.7) (6.6) Cash received from sale of treasury shares 0.7 2.9 Cash paid for treasury shares (0.5) (2.4) Buy-back of perpetual loan participation notes (0.5) (10.6) Proceeds from sale of previously bought-back perpetual loan participation notes – 10.7 Amounts paid on perpetual loan participation notes 38 (15.4) (13.8) Net cash from financing activities 552.6 48.9

Effect of exchange rate changes on cash and cash equivalents 196.5 (24.0) Effect of change in impairment loss allowance 0.2 (0.2) Net (decrease)/increase in cash and cash equivalents (96.8) 396.3

At the beginning of year 18 1,325.6 929.3 At the end of year 18 1,228.8 1,325.6

Non-cash changes in liabilities arising from financial activities 2020 2019

Foreign currency translation Eurobonds 21.6 (6.4) Syndicated loans 1.6 3.0 Subordinated debt 22.2 14.6

Other non-cash changes Local bonds (3.0) 11.4 Eurobonds 5.1 12.9 Syndicated loans – (2.1) Funds from local central banks 1.8 9.2 Subordinated debt (0.1) (3.7)

VTB BANK CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY FOR THE YEAR ENDED 31 DECEMBER (IN BILLIONS OF RUSSIAN ROUBLES)

The notes № 1-59 form an integral part of these consolidated financial statements. 17

Attributable to shareholders of the parent

Share capital

Share premium

Perpetual loan

participation notes

(Note 36)

Treasury shares and

bought back perpetual

loan participation

loan notes

Other reserves

(Note 37) Retained earnings Total

Non-controlling

interests (Note 47)

Total equity

Balance at 1 January 2019 659.5 433.8 156.3 (1.0) 82.4 190.3 1,521.3 (5.0) 1,516.3

Net result from treasury shares

transactions – – – 0.5 – (0.1) 0.4 – 0.4 Net result from bought back

perpetual loan participation notes transactions – – – 0.1 – – 0.1 – 0.1

Profit/(loss) for the period – – – – – 202.0 202.0 (0.8) 201.2 Other comprehensive (loss)/income – – – – (15.7) (0.1) (15.8) 1.1 (14.7) Total comprehensive

income/(loss) for the period – – – – (15.7) 201.9 186.2 0.3 186.5

Transfer of premises revaluation

reserve upon disposal or depreciation – – – – (0.3) 0.3 – – –

Reclassification of net change in fair value of equity instruments upon derecognition – – – – (0.3) 0.3 – – –

Share-based payments – – – – – (0.5) (0.5) – (0.5) Acquisition of subsidiaries – – – – – 0.6 0.6 5.1 5.7 Acquisition of non-controlling

interests – – – – – 3.0 3.0 (5.4) (2.4) Amounts paid on perpetual loan

participation notes – – – – – (13.8) (13.8) – (13.8) Foreign exchange translation of

perpetual loan participation notes – – (17.0) – – 17.0 – – – Tax effect recognised on perpetual

loan participation notes – – – – – (3.4) (3.4) – (3.4)

Dividends declared and other distributions to shareholders – – – – – (33.5) (33.5) (2.1) (35.6)

Balance at 31 December 2019 659.5 433.8 139.3 (0.4) 66.1 362.1 1,660.4 (7.1) 1,653.3

Net result from treasury shares

transactions – – – 0.2 – – 0.2 – 0.2 Net result from bought back

perpetual loan participation notes transactions – – – (0.5) – – (0.5) – (0.5)

Profit/(loss) for the period – – – – – 80.6 80.6 (5.3) 75.3 Other comprehensive income – – – – 39.9 0.3 40.2 0.6 40.8 Total comprehensive

income/(loss) for the period – – – – 39.9 80.9 120.8 (4.7) 116.1

Transfer of premises revaluation

reserve upon disposal or depreciation – – – – 5.3 (5.3) – – –

Reclassification of net change in fair value of equity instruments upon derecognition – – – – 0.8 (0.8) – – –

Share-based payments (Note 53) – – – – – (0.1) (0.1) – (0.1) Acquisition of non-controlling

interests – – – – – (14.7) (14.7) 14.0 (0.7) Amounts paid on perpetual loan

participation notes (Notes 38) – – – – – (15.4) (15.4) – (15.4) Foreign exchange translation of

perpetual loan participation notes – – 27.3 – – (27.3) – – – Tax effect recognised on perpetual

loan participation notes – – – – – 5.5 5.5 – 5.5 Dividends declared and other

distributions to shareholders (Notes 38) – – – – – (24.5) (24.5) (2.2) (26.7)

Other changes – – – – – (9.1) (9.1) – (9.1)

Balance at 31 December 2020 659.5 433.8 166.6 (0.7) 112.1 351.3 1,722.6 – 1,722.6

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020

18

1. PRINCIPAL ACTIVITIES VTB Bank and its subsidiaries (the “Group”) comprise Russian and foreign commercial banks, insurance, leasing and other entities controlled by the Group. VTB Bank, formerly known as Vneshtorgbank (the “Bank”, or “VTB”), was formed as Russia’s foreign trade bank under the laws of the Russian Federation on 17 October 1990. In 1998, following several reorganisations, VTB was reorganised into an open joint stock company. In October 2006 the Group started re-branding to change its name from Vneshtorgbank to VTB. In March 2007, the Bank for Foreign Trade was renamed into “VTB Bank” (Open Joint-Stock Company). In June 2015 “VTB Bank” (open joint-stock company) was renamed into VTB Bank (Public Joint-Stock Company) in accordance with the legislative requirements. On 2 January 1991, VTB received a general banking license (number 1000) from the Central Bank of the Russian Federation (CBR). In addition, VTB holds licenses required for trading and holding securities and engaging in other securities-related activities, including acting as a broker, a dealer and a custodian, and providing asset management and special depositary services. VTB and other Russian banks within the Group are regulated and supervised by the CBR. Foreign banks within the Group operate under the bank regulatory regimes of their respective countries. On 29 December 2004, the Bank became a member of the obligatory deposit insurance system provided by the State Corporation “Deposit Insurance Agency” (DIA). The Group subsidiary banks in Russia: “BM-Bank”, JSC, “Vozrozhdenie Bank”, PJSC, “Sarovbusinessbank”, PJSC and “Zapsibcombank”, PJSC are also members of the obligatory deposit insurance system provided by DIA. The State deposit insurance scheme implies that DIA guarantees repayment of individual deposits up to the

maximum total guaranteed amount of RUR 1.4 million with a 100% compensation of deposited amount from 29 December 2014. Starting 2019, the same guaranties are implied to deposits of legal entities referred to ‘small entities’ as it stated in legislation of the RF. In 2020, VTB re-registered its legal address to 11a Degtyarnyy Pereulok, Saint-Petersburg 191144, Russian Federation. VTB’s Head Office is located in Moscow. The Group operates in the corporate and investment banking, retail banking, real estate and other sectors. Corporate and investment banking include deposit taking and commercial lending, support of clients’ export/import transactions, foreign exchange, securities trading and trading in derivative financial instruments. The Group’s operations are conducted in both Russian and international markets. The Group conducts its banking business in Russia through VTB as a parent and several subsidiary banks. The Group operates outside Russia through subsidiary banks, located in Germany, the UK, Armenia, Belarus, Kazakhstan, Azerbaijan, Georgia and Angola; through representative offices located in Italy and China; through VTB branches in China and India, a branch of “VTB Bank (Europe)” in Austria and a branch of “VTB Capital”, Plc in Singapore. The Group investment banking division also engages in securities dealing and financial advisory in Hong Kong and investment banking operations in Bulgaria. VTB’s majority shareholder is the Russian Federation, acting through the Federal Property Agency, which holds 60.9% of VTB’s issued and outstanding ordinary shares as at 31 December 2020 (31 December 2019: 60.9%). Unless otherwise noted herein, all amounts are expressed in billions of Russian roubles rounded off to one decimal.

2. BASIS OF PREPARATION These consolidated financial statements (“financial statements”) have been prepared in accordance with International Financial Reporting Standards (“IFRS”). The Bank and its subsidiaries and associates maintain their accounting records in accordance with regulations applicable in their country of registration. These financial statements are based on those accounting books and records, as adjusted and reclassified to comply with IFRS.

These financial statements have been prepared under the historical cost convention, as modified by the initial recognition of trading financial instruments based on fair value, by the revaluation of land, premises and investment properties, investment securities at fair value through profit and loss and through other comprehensive income.

The summary of principal accounting policies applied in the preparation of these financial statements is set out below in Note 56. These policies have been consistently applied to all the periods presented, unless otherwise stated. These financial statements are presented in Russian roubles (RUR), the national currency of the Russian Federation, where the Bank is domiciled. Unless otherwise noted herein, all amounts are expressed in billions of Russian roubles rounded off to one decimal. Due to rounding, numbers presented throughout this document may not sum precisely to the totals provided and percentages may not precisely reflect the absolute figures.

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

19

DELVING INTO NUMBERS

3. ANALYSIS BY SEGMENT ............................. 20

4. INTEREST INCOME AND EXPENSE ............. 28

5. NET FEE AND COMMISSION INCOME ........ 28

6. GAINS NET OF LOSSES ARISING FROM OTHER FINANCIAL INSTRUMENTS AT FAIR VALUE THROUGH PROFIT OR LOSS ............29

7. GAINS NET OF LOSSES ARISING FROM SALE OF FINANCIAL ASSETS AT FAIR VALUE THROUGH OTHER COMPREHENSIVE INCOME ......................... 29

8. GAINS NET OF LOSSES / (LOSSES NET OF GAINS) ARISING FROM FOREIGN CURRENCIES AND PRECIOUS METALS .... 29

9. OTHER OPERATING INCOME...................... 29

10. REVENUES LESS EXPENSES FROM OPERATING LEASING .................................. 30

11. REVENUES AND OTHER GAINS FROM OTHER NON-BANKING ACTIVITIES ............ 30

12. COST OF SALES AND OTHER EXPENSES FROM OTHER NON-BANKING ACTIVITIES ...30

13. NET INSURANCE PREMIUMS EARNED FROM NON-STATE PENSION FUND ACTIVITY ....................................................... 30

14. NET INSURANCE CLAIMS INCURRED, MOVEMENT IN LIABILITIES TO POLICYHOLDERS AND ACQUISITION COSTS ON NON-STATE PENSION FUND ACTIVITY ....................................................... 31

15. OTHER OPERATING EXPENSE .................. 31

16. STAFF COSTS AND ADMINISTRATIVE EXPENSES .................................................... 31

17. INCOME TAX ................................................. 32

18. CASH AND SHORT-TERM FUNDS ............... 35

19. TRADING FINANCIAL ASSETS ..................... 35

20. DERIVATIVE FINANCIAL INSTRUMENTS .... 36

21. DUE FROM OTHER BANKS .......................... 36

22. LOANS AND ADVANCES TO CUSTOMERS .. 38

23. INVESTMENT FINANCIAL ASSETS .............. 47

24. LAND, PREMISES AND EQUIPMENT ........... 48

25. INVESTMENT PROPERTY ............................ 50

26. GOODWILL AND OTHER INTANGIBLE ASSETS ......................................................... 51

27. OTHER ASSETS ............................................ 56

28. DISPOSAL GROUPS AND NON-CURRENT ASSETS HELD FOR SALE ............................ 57

29. DUE TO OTHER BANKS ............................... 58

30. CUSTOMER DEPOSITS ................................ 58

31. OTHER BORROWED FUNDS ...................... 59

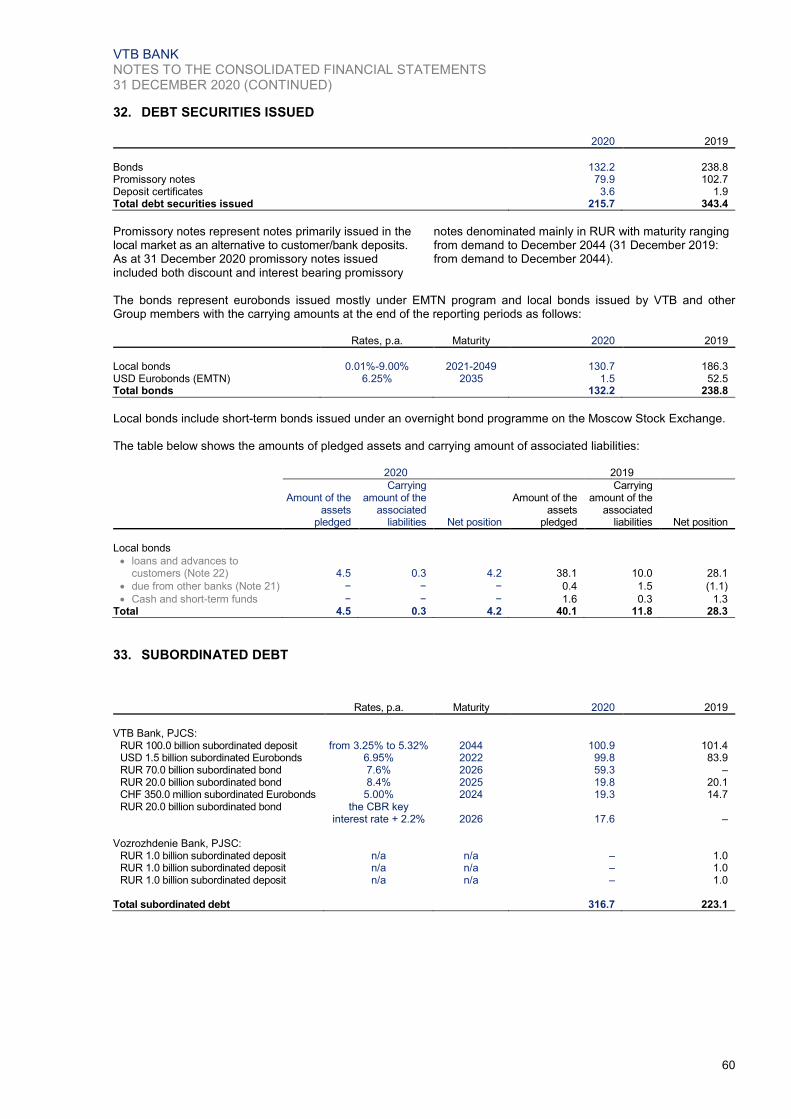

32. DEBT SECURITIES ISSUED ......................... 60

33. SUBORDINATED DEBT ............................... 60

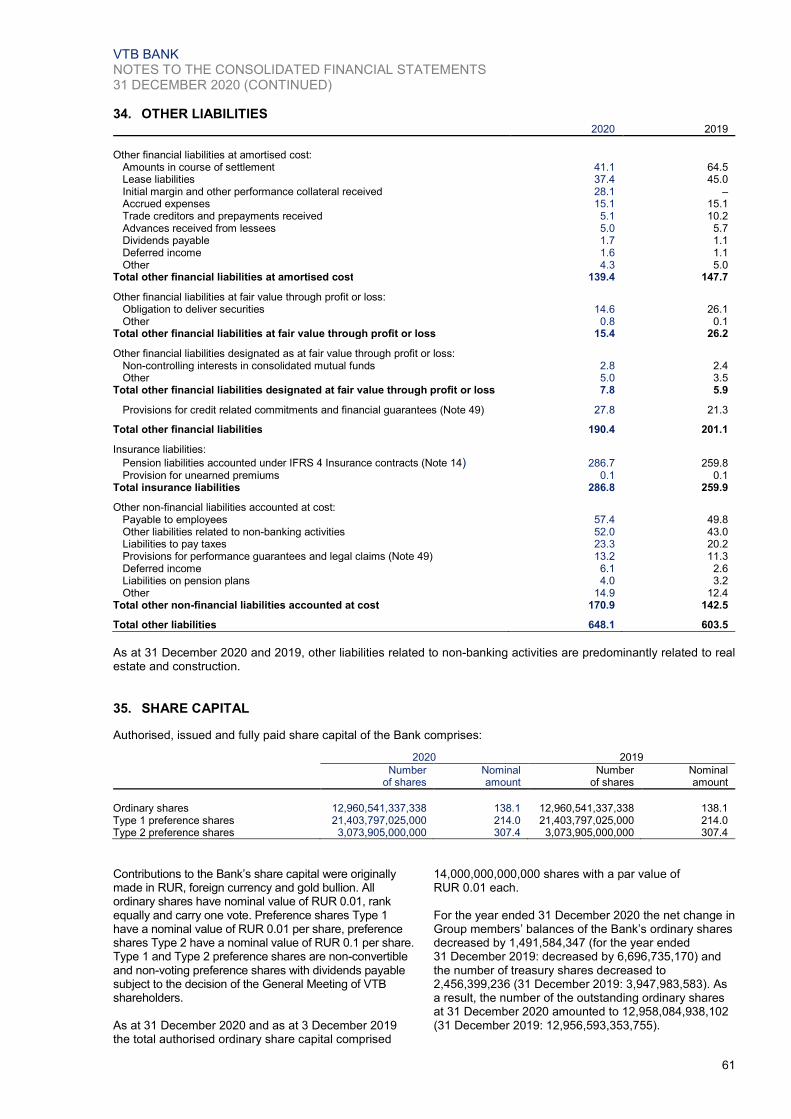

34. OTHER LIABILITIES ...................................... 61

35. SHARE CAPITAL ........................................... 61

36. PERPETUAL LOAN PARTICIPATION NOTES ........................................................... 62

37. OTHER RESERVES ...................................... 62

38. DIVIDENDS AND AMOUNTS PAID UNDER PERPETUAL LOAN PARTICIPATION NOTES ........................................................... 62

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

20

3. ANALYSIS BY SEGMENT In accordance with IFRS 8, Operating Segments, the Group has defined five reportable segments.

Corporate-Investment banking (CIB)

Medium and Small banking (MSB)

Retail business (RB)

Treasury

Other business The Group has also separately disclosed Corporate Centre. The Group also disclosed a new acquisition – non distributed item as a separate reportable segment that presents data of subsidiary banks for the quarter when these subsidiary banks were acquired. Following the further integration of activities of the subsidiary into the Group’s global business lines the data for the subsidiary are presented within reportable segments listed above. In 2019 included in the new acquisitions-non distributed reportable segment are the financial results of “Sarovbusinessbank”, PJSC and “Zapsibcombank”, PJSC for the 1st quarter of 2019. Their financial results for the 2nd, 3rd and 4th quarters of 2019 have been reallocated to respective reportable segments following completion of internal procedures. The composition of reportable segments is approved by resolutions of VTB Group’s Management Committee (Chief Decision Makers), the body that on a regular basis assesses performance of reportable segments and allocates resources to them. (a) Factors that management used in order to

identify the reportable segments

The Group’s segments are strategic business lines that are managed separately, focus on different clients and have product specialisation. The majority of the Group’s activities and resources are allocated and managed, and their performance is assessed via the respective segment information. (b) Segments’ business activities

The CIB, MSB and RB segments are global business lines that focus on servicing different customer segments. The Treasury and Other Business segments, as well as Corporate Centre do not constitute separate global business lines. The criteria used to identify client segments for each global business line are set by the Group Management Committee. They include principles for allocating customers between large, medium and small business customer segments.

CIB and MSB

CIB global business line encompasses operations with corporate customers that are 'large business' customers and banking financial institutions, as well as operations on the securities market, excluding operations with securities for liquidity management purposes. In addition, CIB global business line makes direct equity investments, becoming a partner in socially significant infrastructure projects and companies in various industries. CIB’s global business line offers partnership experience, infrastructure and financial resources of VTB Group, which allows them to increase their operational efficiency and investment appeal as part of a long-term strategy. Starting from reporting date 2020, a separate disclosure has been prepared highlighting the result of

these operations. MSB global business line encompasses operations with corporate customers of “medium business” and “small business” categories. Reportable segment comprises:

operations with prevailing market risk including loans with exposure to market risks;

corporate finance operations;

asset management, brokerage services and financial consulting;

operations with precious metals;

profit-taking operations on the financial and currency markets, including interbank market;

other products and services with prevailing market risk;

operations with prevailing credit risk and interest rate risk, such as lending to corporate customers (large and medium businesses segments), including overdrafts on customers’ current accounts;

trade and export financing;

operations with corporate customers: current and settlement accounts and term deposits;

documentary operations, including letters of credit and guarantees;

depositary operations;

fee-based services of all kinds not related to operations on the financial markets and currency valuables: settlement and cash services, collection, storage box, remote banking services, payment processing centre service.

Also includes term funding from certain clients (including promissory notes issued), based on the decision of VTB Group’s Management Committee.

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

21

3. ANALYSIS BY SEGMENT (CONTINUED) (b) Segments’ business activities (continued) Retail business

RB global business line encompasses operations with individuals and specific operations with corporate customers.

The retail business comprises operations with individuals and also internet and mobile POS-acquiring operations with major retail chains, operations of individuals with plastic cards, payroll related services, payment processing centre service, all types of insurance products and services, non-government pension funds.

Treasury

The Treasury comprises:

operations to manage liquidity (including those with securities portfolios maintained for liquidity management purposes);

operations on financial and interbank markets as a part of management of payment and currency positions, as well as interest rate risk management;

cash flow management within the Head office or subsidiary and between VTB Group members;

debt financing operations;

reallocation of resources between segments both within the Head office or subsidiary and between VTB Group members.

The net financial results of the Treasury reportable segment are allocated to other reportable segments in accordance with established methodology. Corporate Centre

The Corporate Centre represents unallocated staff and administrative expenses related to VTB Group’s management, as well as expenses on strategic programmes connected with VTB Group’s brand development and positioning on the local and international markets, etc. It may also include other items resulting from intersegment reallocations as determined by VTB Group’s Management Committee. Corporate Center also includes investments in associates not allocated to reportable segments and operations of companies in non-banking digital business. Starting from reporting date 2020, a separate disclosure has been prepared to disclose investments in operations of companies in non-banking digital business.

Other business

The other business includes two lines of business: Construction and development and Other. The Construction and development business line is non-banking operations undertaken by Group members operating in the construction and development industry. The Other activities represent non-banking business, including assets, which were transferred to the Group as a result of debt settlement. Starting from reporting date 2020, a separate disclosure has been prepared highlighting the result of these operations (c) Managing operating segments’ profit or loss,

assets or liabilities

The performance of a segment and its profit or loss are measured in accordance with IFRS, as adjusted by intersegment reallocations and decisions of VTB Group’s Management Committee regarding the allocation of operations between segments. The Head office and the Group members prepare segment reporting using unified rules. Intersegment transactions within a single entity of the Group are settled using the internal transfer prices, which are designed to reflect the cost of resources. Transfer prices are set and reviewed on a regular basis in each of the Group’s entities. VTB Group’s Management Committee evaluates segments’ performance based on their net profit after tax, as well as other qualitative and quantitative information. Intersegment transactions are predominantly conducted in the normal course of business. As at 31 December 2020, the Group’s reportable segments and their compositions remained as disclosed in the consolidated financial statements as at 31 December 2019.

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

22

3. ANALYSIS BY SEGMENT (CONTINUED)

CIB MSB RB Treasury Corporate

centre Other

business New acquisitions –

non distributed Inter-segment eliminations Total

2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019

Revenues from: External customers 681.9 726.3 148.3 156.7 551.3 572.9 53.5 60.0 1.3 0.5 64.1 53.8 – 4.5 – – 1,500.4 1,574.7 Other segments 179.1 243.6 90.6 102.6 257.7 281.1 724.2 821.7 0.5 – 9.5 6.7 – 0.3 (1,261.6) (1,456.0) – – Total revenues 861.0 969.9 238.9 259.3 809.0 854.0 777.7 881.7 1.8 0.5 73.6 60.5 – 4.8 (1,261.6) (1,456.0) 1,500.4 1,574.7 Segment income and expense: Interest income 665.2 754.4 200.7 223.1 657.3 681.2 767.0 878.0 0.4 0.1 4.4 4.5 – 3.9 (1,239.2) (1,438.2) 1,055.8 1,107.0 Interest expense (502.3) (630.4) (135.9) (162.0) (436.6) (478.5) (640.6) (775.9) (0.1) (0.2) (25.2) (25.8) – (1.9) 1,239.1 1,438.2 (501.6) (636.5) Payments to deposit insurance

system (0.5) (0.3) (2.6) (3.2) (19.1) (26.1) (0.3) (0.1) – – – – – (0.2) – – (22.5) (29.9) Treasury result allocation 22.0 9.2 14.9 7.4 34.2 18.0 (115.6) (41.8) 35.8 (1.5) 8.7 8.7 – – – – – – Net interest income/(expense) 184.4 132.9 77.1 65.3 235.8 194.6 10.5 60.2 36.1 (1.6) (12.1) (12.6) – 1.8 (0.1) – 531.7 440.6 (Provision charge) / reversal of

provision for credit losses on debt financial assets (69.6) (33.1) (26.2) (14.6) (83.6) (48.8) (0.2) 0.8 (47.4) 4.3 – 0.2 – (1.0) – – (227.0) (92.2)

Net interest income/(expense) after provision charge for credit losses 114.8 99.8 50.9 50.7 152.2 145.8 10.3 61.0 (11.3) 2.7 (12.1) (12.4) – 0.8 (0.1) – 304.7 348.4

Net fee and commission income 33.7 32.8 31.2 30.3 66.0 55.4 5.0 1.9 – – 0.8 0.7 – 0.7 0.1 (0.2) 136.8 121.6 Other gains net of losses/(losses net

of gains) arising from financial instruments and foreign currencies 60.4 80.9 1.0 0.8 3.7 17.4 (16.3) (61.7) (0.6) – 3.0 3.8 – – 0.1 – 51.3 41.2

Share in profit/(loss) of associates and joint ventures 9.1 3.6 0.2 0.3 8.0 6.3 0.2 0.6 0.1 0.2 (0.3) 0.1 – – – – 17.3 11.1

Profit/(losses) from disposal of subsidiaries and associates 5.9 1.1 – – – – – 0.1 – – 0.2 6.3 – – – – 6.1 7.5

(Provision charge) / reversal of provision for credit losses on credit related commitments and other financial assets (16.1) (4.6) (5.9) (1.5) 0.1 (0.2) – – (0.8) (4.3) (0.1) (0.5) – – – – (22.8) (11.1)

Other operating (expense)/income 23.4 31.4 2.2 1.5 (34.7) (41.7) 0.8 (1.9) (0.8) (0.8) (118.4) (2.4) – 5.5 (6.3) (3.2) (133.8) (11.6) Net operating income/(expense) 231.2 245.0 79.6 82.1 195.3 183.0 – – (13.4) (2.2) (126.9) (4.4) – 7.0 (6.2) (3.4) 359.6 507.1 Staff costs and administrative

expenses (76.9) (71.7) (44.4) (38.9) (109.4) (103.2) – – (32.4) (32.3) (13.0) (10.2) – (1.3) 6.2 3.4 (269.9) (254.2) Profit/(loss) before tax 154.3 173.3 35.2 43.2 85.9 79.8 – – (45.8) (34.5) (139.9) (14.6) – 5.7 – – 89.7 252.9 Income tax (expense)/benefit (33.3) (37.9) (6.8) (8.7) (15.9) (14.8) – – 9.8 7.2 31.8 2.6 – (0.1) – – (14.4) (51.7) Net profit/(loss) 121.0 135.4 28.4 34.5 70.0 65.0 – – (36.0) (27.3) (108.1) (12.0) – 5.6 – – 75.3 201.2

Capital expenditure 9.8 3.7 14.8 3.7 57.5 19.1 – – 6.5 1.0 20.1 7.1 – – – – 108.7 34.6 Depreciation 18.9 17.2 3.9 2.9 13.5 13.3 – – 1.1 0.5 5.9 3.6 – 0.1 (0.1) (0.3) 43.2 37.3

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

23

3. ANALYSIS BY SEGMENT (CONTINUED)

CIB MSB RB Treasury Corporate

centre Other

business New acquisitions –

non distributed Inter-segment eliminations Total

2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019

Net profit/(loss) 121.0 135.4 28.4 34.5 70.0 65.0 – – (36.0) (27.3) (108.1) (12.0) – 5.6 – – 75.3 201.2

Net result on financial assets

at fair value through other comprehensive income, net of tax 1.8 2.1 – – 4.1 0.9 2.4 5.8 – – 0.2 – – 0.1 – (0.2) 8.5 8.7

Cash flow hedges, net of tax 0.4 0.1 – – – – – – – – (0.4) – – – – – – 0.1 Share of other comprehensive loss

of associates and joint ventures – 0.1 – – 0.1 0.1 4.2 (2.2) – – – – – – – – 4.3 (2.0) Effect of translation, net of tax – – – – – – 27.3 (21.1) 0.6 – – – – – – – 27.9 (21.1) Actuarial (losses net of gains) /

gains net of losses / arising from difference between pension plan assets and obligations – (0.1) – – – – – – – – – – – – – – – (0.1)

Land and premises revaluation, net of tax 0.3 – – – – – – – – – (0.2) (0.3) – – – – 0.1 (0.3)

Total other comprehensive (loss)/income before treasury result allocation 2.5 2.2 – – 4.2 1.0 33.9 (17.5) 0.6 – (0.4) (0.3) – 0.1 – (0.2) 40.8 (14.7)

Treasury result allocation 1.5 0.8 1.4 0.6 2.7 1.5 (33.9) 17.5 28.3 (20.4) – – – – – – – – Total other comprehensive

(loss)/income 4.0 3.0 1.4 0.6 6.9 2.5 – – 28.9 (20.4) (0.4) (0.3) – 0.1 – (0.2) 40.8 (14.7)

Total comprehensive income/(loss) 125.0 138.4 29.8 35.1 76.9 67.5 – – (7.1) (47.7) (108.5) (12.3) – 5.7 – (0.2) 116.1 186.5

As at 31 December 2020 and for the year then ended provision for credit losses on debt financial assets and provision charge for credit losses on debt financial assets amounted to RUR 898.7 billion and RUR 227.0 billion, respectively (31 December 2019: RUR 688.1 billion and RUR 92.2 billion, respectively); provision and provision charge for credit losses on off-balance sheet commitments and other financial assets amounted to RUR 44.3 billion and RUR 22.8 billion, respectively (31 December 2019: RUR 36.0 billion and RUR 11.1 billion, respectively).

Included in these balance sheet amounts is the amount of RUR 112.2 billion (31 December 2019: RUR 93.1 billion), which represents the provision for credit losses on debt financial instruments and off-balance sheet items related to the Group’s exposure to certain groups of borrowers that in the Group’s management view are subject to industry and other portfolio specific risks. Group’s exposures to these groups of borrowers are predominantly residing in the Corporate and Investment Banking segment.

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

24

3. ANALYSIS BY SEGMENT (CONTINUED)

CIB MSB RB Treasury Corporate

centre Other

business Inter-segment eliminations Total

2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019

Cash and short-term funds 76.1 28.5 12.4 – 198.3 113.4 942.7 1,193.0 – – – 0.1 – – 1,229.5 1,335.0 Mandatory cash balances with central banks – – – – – – 137.2 127.2 – – – – – – 137.2 127.2 Due from other banks 441.6 275.0 0.1 – 3.9 16.7 392.3 318.3 – 0.1 – – – – 837.9 610.1 Loans and advances to customers 7,014.2 5,951.2 1,428.3 1,340.3 3,586.2 3,157.8 295.4 329.6 (65.4) (17.9) 5.7 13.1 – – 12,264.4 10,774.1 Other financial instruments 792.1 452.8 0.8 0.4 281.4 223.9 749.9 265.1 0.4 0.3 8.9 18.2 – – 1,833.5 960.7 Investments in associates and joint ventures 198.0 141.9 0.9 0.8 97.5 86.1 5.1 4.2 20.1 17.5 5.3 14.4 – – 326.9 264.9 Other assets items 780.5 676.1 118.4 94.1 265.7 241.9 7.1 9.7 37.0 22.7 304.1 399.6 – – 1,512.8 1,444.1

Net amount of intersegment settlements – – 441.1 383.0 1,613.8 1,952.1 884.5 559.7 85.2 15.7 – – (3,024.6) (2,910.5) – – Segment assets 9,302.5 7,525.5 2,002.0 1,818.6 6,046.8 5,791.9 3,414.2 2,806.8 77.3 38.4 324.0 445.4 (3,024.6) (2,910.5) 18,142.2 15,516.1

Due to other banks 458.9 149.6 0.1 0.3 0.9 0.5 633.1 1,026.8 – – – – – – 1,093.0 1,177.2 Customer deposits 4,857.8 3,740.9 1,804.0 1,624.5 5,161.7 4,921.8 1,006.1 685.7 – – 1.4 1.3 – – 12,831.0 10,974.2 Other borrowed funds 181.1 142.3 2.3 0.8 3.3 2.3 866.5 203.5 – – – – – – 1,053.2 348.9 Debt securities issued 24.7 34.4 18.4 22.5 139.7 194.6 32.9 91.9 – – – – – – 215.7 343.4 Subordinated debt – – – – – – 316.7 223.1 – – – – – – 316.7 223.1 Other liabilities items 389.8 327.1 33.4 23.8 354.2 330.3 32.3 31.8 59.8 22.4 40.5 60.6 – – 910.0 796.0 Net amount of intersegment settlements 2,686.4 2,507.9 – – – – – – – – 338.2 402.6 (3,024.6) (2,910.5) – – Segment liabilities 8,598.7 6,902.2 1,858.2 1,671.9 5,659.8 5,449.5 2,887.6 2,262.8 59.8 22.4 380.1 464.5 (3,024.6) (2,910.5) 16,419.6 13,862.8

Net (loss)/profit after tax by segment Segment assets Segment liabilities

1 1 1 1 1 1 1 1 1 1 1

2 2 2 2 2 2 2 2 2 2 2

3 3 3 3 3 3 3 3 3 3 3

4 4 4 4 4 4 4 4 4 4 4

5 5 5 5 5 5 5 5 5 5 5

6 6 6 6 6 6 6 6 6 6 6

7 7 7 7 7 7 7 7 7 7 7

8 8 8 8 8 8 8 8 8 8 8

9 9 9 9 9 9 9 9 9 9 9

10 10 10 10 10 10 10 10 10 10 10

11 11 11 11 11 11 11 11 11 11 11

12 12 12 12 12 12 12 12 12 12 12

13 13 13 13 13 13 13 13 13 13 13

14 14 14 14 14 14 14 14 14 14 14

15 15 15 15 15 15 15 15 15 15 15

16 16 16 16 16 16 16 16 16 16 16

17 17 17 17 17 17 17 17 17 17 17

18 18 18 18 18 18 18 18 18 18 18

19 19 19 19 19 19 19 19 19 19 19

20 20 20 20 20 20 20 20 20 20 20

21 21 21 21 21 21 21 21 21 21 21

22 22 22 22 22 22 22 22 22 22 22

23 23 23 23 23 23 23 23 23 23 23

24 24 24 24 24 24 24 24 24 24 24

25 25 25 25 25 25 25 25 25 25 25

26 26 26 26 26 26 26 26 26 26 26

27 27 27 27 27 27 27 27 27 27 27

28 28 28 28 28 28 28 28 28 28 28

29 29 29 29 29 29 29 29 29 29 29

30 30 30 30 30 30 30 30 30 30 30

31 31 31 31 31 31 31 31 31 31 31

32 32 32 32 32 32 32 32 32 32 32

33 33 33 33 33 33 33 33 33 33 33

33 33 33 33 33 33 33 33 33 33 33

135.434.5

65.0 -27.3-12.0 5.6

-

201.2

2019

RBSMBCIB Corporate

centerNew

acquisitionsInter-segment

eliminations

TotalOther

business

121.028.4

70.0 -36.0

-108.1

- - 75.3

2020

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

51%

9%

24%

14%2%

31 Dec 2020

CIB

SMB

RB

Treasury

Other

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

1 1 1 1 1 1 1

36%

11%

34%

18%

1%

31 Dec 2020

CIB

SMB

RB

Treasury

Other

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

25

3. ANALYSIS BY SEGMENT (CONTINUED)

Operations of reportable segments related to long term investments of CIB, non-bank digital assets and other business transferred to the Group under debt settlement are presented below:

CIB without long term Investments

Long term Investments Total CIB

Corporate centre without non-bank

digital assets Non-bank digital

assets Total Corporate

centre

Other business without assets credit

workout Assets credit workout Total

Other business

2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019

Revenues from: External customers 618.0 653.7 63.9 72.6 681.9 726.3 0.4 0.2 0.9 0.3 1.3 0.5 – – 64.1 53.8 64.1 53.8 Other segments 178.9 243.0 0.2 0.6 179.1 243.6 0.1 – 0.4 – 0.5 – – – 9.5 6.7 9.5 6.7 Total revenues 796.9 896.7 64.1 73.2 861.0 969.9 0.5 0.2 1.3 0.3 1.8 0.5 – – 73.6 60.5 73.6 60.5 Segment income and expense: Interest income 656.2 748.3 9.0 6.1 665.2 754.4 – 0.1 0.4 – 0.4 0.1 – – 4.4 4.5 4.4 4.5 Interest expense (482.8) (610.6) (19.5) (19.8) (502.3) (630.4) (0.1) (0.2) – – (0.1) (0.2) – – (25.2) (25.8) (25.2) (25.8) Payments to deposit insurance

system (0.5) (0.3)

– – (0.5) (0.3) – – – – – – – – – – – – Treasury result allocation 19.3 8.9 2.7 0.3 22.0 9.2 35.8 (1.5) – – 35.8 (1.5) – – 8.7 8.7 8.7 8.7

Net interest income/(expense) 192.2 146.3 (7.8) (13.4) 184.4 132.9 35.7 (1.6) 0.4 – 36.1 (1.6) – – (12.1) (12.6) (12.1) (12.6) (Provision charge) / reversal of

provision for credit losses on debt financial assets (69.5) (33.1) (0.1) – (69.6) (33.1) (47.4) 4.3 – – (47.4) 4.3 – – – 0.2 – 0.2

Net interest income/(expense) after provision charge for credit losses 122.7 113.2 (7.9) (13.4) 114.8 99.8 (11.7) 2.7 0.4 – (11.3) 2.7 – – (12.1) (12.4) (12.1) (12.4)

Net fee and commission income 33.7 32.6 – 0.2 33.7 32.8 – – – – – – – – 0.8 0.7 0.8 0.7 Other gains net of losses/(losses net

of gains) arising from financial instruments and foreign currencies 55.2 64.3 5.2 16.6 60.4 80.9 (0.6) – – – (0.6) – – – 3.0 3.8 3.0 3.8

Share in profit/(loss) of associates and joint ventures 0.1 0.3 9.0 3.3 9.1 3.6 0.2 0.2 (0.1) – 0.1 0.2 – – (0.3) 0.1 (0.3) 0.1

Profit/(losses) from disposal of subsidiaries and associates 1.9 – 4.0 1.1

5.9 1.1 – – – – – – – – 0.2 6.3 0.2 6.3

(Provision charge) / reversal of provision for credit losses on credit related commitments and other financial assets (16.1) (4.6) – – (16.1) (4.6) (0.8) (4.3) – – (0.8) (4.3) – – (0.1) (0.5) (0.1) (0.5)

Other operating (expense)/income 12.9 22.8 10.5 8.6 23.4 31.4 0.3 (0.3) (1.1) (0.5) (0.8) (0.8) – – (118.4) (2.4) (118.4) (2.4) Net operating income/(expense) 210.4 228.6 20.8 16.4 231.2 245.0 (12.6) (1.7) (0.8) (0.5) (13.4) (2.2) – – (126.9) (4.4) (126.9) (4.4) Staff costs and administrative

expenses (76.6) (71.5) (0.3) (0.2) (76.9) (71.7) (32.4) (32.3) – – (32.4) (32.3) (10.4) (8.1) (2.6) (2.1) (13.0) (10.2) Profit/(loss) before tax 133.8 157.1 20.5 16.2 154.3 173.3 (45.0) (34.0) (0.8) (0.5) (45.8) (34.5) (10.4) (8.1) (129.5) (6.5) (139.9) (14.6) Income tax (expense)/benefit (31.2) (36.8) (2.1) (1.1) (33.3) (37.9) 9.7 7.1 0.1 0.1 9.8 7.2 2.1 1.6 29.7 1.0 31.8 2.6 Net profit/(loss) 102.6 120.3 18.4 15.1 121.0 135.4 (35.3) (26.9) (0.7) (0.4) (36.0) (27.3) (8.3) (6.5) (99.8) (5.5) (108.1) (12.0)

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

26

3. ANALYSIS BY SEGMENT (CONTINUED)

CIB without long term Investments

Long term Investments Total CIB

Corporate centre without non-bank

digital assets Non-bank digital

assets Total Corporate

centre

Other business without assets credit

workout Assets credit workout Total

Other business

2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019

Net profit/(loss) 102.6 120.3 18.4 15.1 121.0 135.4 (35.3) (26.9) (0.7) (0.4) (36.0) (27.3) (8.3) (6.5) (99.8) (5.5) (108.1) (12.0)

Net result on financial assets at fair

value through other comprehensive income, net of tax 1.8 2.6 – (0.5) 1.8 2.1 – – – – – – – – 0.2 – 0.2 –

Cash flow hedges, net of tax 0.4 0.1 – – 0.4 0.1 – – – – – – – – (0.4) – (0.4) – Share of other comprehensive loss

of associates and joint ventures – 0.1 – – – 0.1 – – – – – – – – – – – – Effect of translation, net of tax – – – – – – 0.6 – – – 0.6 – – – – – – – Actuarial (losses net of gains) /

gains net of losses / arising from difference between pension plan assets and obligations – (0.1) – – – (0.1) – – – – – – – – – – – –

Land and premises revaluation, net of tax 0.3 – – – 0.3 – – – – – – – – – (0.2) (0.3) (0.2) (0.3)

Total other comprehensive (loss)/income before treasury result allocation 2.5 2.7 – (0.5) 2.5 2.2 0.6 – – – 0.6 – – – (0.4) (0.3) (0.4) (0.3)

Treasury result allocation 1.5 0.8 – – 1.5 0.8 28.3 (20.4) – – 28.3 (20.4) – – – – – – Total other comprehensive

(loss)/income 4.0 3.5 – (0.5) 4.0 3.0 28.9 (20.4) – – 28.9 (20.4) – – (0.4) (0.3) (0.4) (0.3)

Total comprehensive income/(loss) 106.6 123.8 18.4 14.6 125.0 138.4 (6.4) (47.3) (0.7) (0.4) (7.1) (47.7) (8.3) (6.5) (100.2) (5.8) (108.5) (12.3)

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

27

3. ANALYSIS BY SEGMENT (CONTINUED)

CIB without long term

Investments Long term

Investments Total CIB

Corporate centre without non-bank

digital assets Non-bank digital

assets Total Corporate

centre

Other business without assets credit

workout Assets credit workout

Total Other business

2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019 2020 2019

Cash and short-term funds 76.0 28.3 0.1 0.2 76.1 28.5 – – – – – – – – – 0.1 – 0.1 Mandatory cash balances with

central banks – – – – – – – – – – – – – – – – – – Due from other banks 441.6 275.0 – – 441.6 275.0 – – – 0.1 – 0.1 – – – – – – Loans and advances to customers 6,962.4 5,915.4 51.8 35.8 7,014.2 5,951.2 (65.4) (17.9) – – (65.4) (17.9) – – 5.7 13.1 5.7 13.1 Other financial instruments 752.0 442.0 40.1 10.8 792.1 452.8 0.4 0.3 – – 0.4 0.3 – – 8.9 18.2 8.9 18.2 Investments in associates and joint

ventures – – 198.0 141.9 198.0 141.9 19.4 16.9 0.7 0.6 20.1 17.5 – – 5.3 14.4 5.3 14.4 Other assets items 768.3 535.9 12.2 140.2 780.5 676.1 34.4 21.4 2.6 1.3 37.0 22.7 82.7 59.1 221.4 340.5 304.1 399.6 Net amount of intersegment

settlements – – – – – – 49.8 14.4 35.4 1.3 85.2 15.7 – – – – – – Segment assets 9,000.3 7,196.6 302.2 328.9 9,302.5 7,525.5 38.6 35.1 38.7 3.3 77.3 38.4 82.7 59.1 241.3 386.3 324.0 445.4

Due to other banks 458.9 149.6 – – 458.9 149.6 – – – – – – – – – – – – Customer deposits 4,827.4 3,740.9 30.4 – 4,857.8 3,740.9 – – – – – – – – 1.4 1.3 1.4 1.3 Other borrowed funds 181.1 142.3 – – 181.1 142.3 – – – – – – – – – – – – Debt securities issued 24.7 34.4 – – 24.7 34.4 – – – – – – – – – – – – Subordinated debt – – – – – – – – – – – – – – – – – – Other liabilities items 373.2 311.2 16.6 15.9 389.8 327.1 24.6 22.1 35.2 0.3 59.8 22.4 – – 40.5 60.6 40.5 60.6 Net amount of intersegment

settlements 2,417.4 2,193.0 269.0 314.9 2,686.4 2,507.9 – – – – – – 78.0 55.2 260.2 347.4 338.2 402.6 Segment liabilities 8,282.7 6,571.4 316.0 330.8 8,598.7 6,902.2 24.6 22.1 35.2 0.3 59.8 22.4 78.0 55.2 302.1 409.3 380.1 464.5

VTB BANK NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2020 (CONTINUED)

28

3. ANALYSIS BY SEGMENT (CONTINUED) Geographical segment information based on geographical location of entities within the Group: 2020 2019